UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2024

Commission file number 001-38661

Elanco Animal Health Incorporated

(Exact name of Registrant as specified in its charter) | | | | | | | | |

| INDIANA | | 82-5497352 |

| (State or other jurisdiction of | | (I.R.S. Employer |

| incorporation or organization) | | Identification No.) |

2500 INNOVATION WAY, GREENFIELD, INDIANA 46140

(Address and zip code of principal executive offices)

Registrant’s telephone number, including area code (877) 352-6261

Securities registered pursuant to Section 12(b) of the Act: | | | | | | | | | | | | | | |

| Title of each class | | Trading Symbol(s) | | Name of each exchange on which registered |

| Common Stock, no par value | | ELAN | | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act:

None.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of a “large accelerated filer,” “accelerated filer,” “smaller reporting company” and "emerging growth company" in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | | | | | | | | | | | | | |

| Large accelerated filer | ☒ | | | | | Accelerated filer | ☐ |

| Non-accelerated filer | ☐ | | | Smaller reporting company | ☐ |

| | | | | | Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act).

Yes ☐ No ☒

Aggregate market value of the common equity held by non-affiliates computed by reference to the price at which the common equity was last sold as of June 30, 2024, the last business day of the Registrant’s most recently completed second fiscal quarter, was approximately $7.1 billion. The registrant has no non-voting common stock.

The number of shares of common stock outstanding as of February 20, 2025 was 494,613,940.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant's definitive proxy materials for its 2025 Annual Meeting of Shareholders are incorporated by reference into Part III hereof.

ELANCO ANIMAL HEALTH INCORPORATED

FORM 10-K

FOR THE YEAR ENDED DECEMBER 31, 2024

TABLE OF CONTENTS | | | | | | | | | | | | | | |

| | | | |

| | | | |

| Item 1. | | | | |

| Item 1A. | | | | |

| Item 1B. | | | | |

| Item 1C. | | | | |

| Item 2. | | | | |

| Item 3. | | | | |

| Item 4. | | | | |

| | | |

|

| | | | |

| Item 5. | | | | |

| Item 6. | | | | |

| Item 7. | | | | |

| Item 7A. | | | | |

| Item 8. | | | | |

| Item 9. | | | | |

| Item 9A. | | | | |

| Item 9B. | | | | |

| Item 9C. | | | | |

| | | | |

| | | | |

| Item 10. | | | | |

| Item 11. | | | | |

| Item 12. | | | | |

| Item 13. | | | | |

| Item 14. | | | | |

| | | | |

| | | |

|

| Item 15. | | | | |

| Item 16. | | | | |

| | | | |

| | | | |

FORWARD-LOOKING STATEMENTS AND RISK FACTOR SUMMARY

This Annual Report on Form 10-K (Form 10-K) includes forward-looking statements within the meaning of the federal securities laws. These forward-looking statements include, without limitation, statements concerning the impact on Elanco Animal Health Incorporated and its subsidiaries (collectively, Elanco, the Company, we, us or our) caused by the integration of business acquisitions, expected synergies and cost savings, product launches, global macroeconomic conditions, expectations relating to liquidity and sources of capital, our expected compliance with debt covenants, cost savings, expenses and reserves relating to restructuring actions, our industry and our operations, performance and financial condition, and including, in particular, statements relating to our business, growth strategies, distribution strategies, product development efforts and future expenses.

Forward-looking statements are based on our current expectations and assumptions regarding our business, the economy and other future conditions. Because forward-looking statements relate to the future, by their nature, they are subject to inherent uncertainties, risks and changes in circumstances that are difficult to predict. As a result, our actual results may differ materially from those contemplated by the forward-looking statements. Important risk factors that could cause actual results to differ materially from those in the forward-looking statements include regional, national or global political, economic, business, competitive, market and regulatory conditions, including but not limited to the following:

•operating in a highly competitive industry;

•the success of our research and development (R&D), regulatory approval and licensing efforts;

•the impact of disruptive innovations and advances in veterinary medical practices, animal health technologies and alternatives to animal-derived protein;

•competition from generic products that may be viewed as more cost-effective;

•changes in regulatory restrictions on the use of antibiotics in farm animals;

•an outbreak of infectious disease carried by farm animals;

•risks related to the evaluation of animals;

•consolidation of our customers and distributors;

•the impact of increased or decreased sales into our distribution channels resulting in fluctuations in our revenues;

•our dependence on the success of our top products;

•our ability to complete acquisitions and divestitures and to successfully integrate the businesses we acquire;

•our ability to implement our business strategies or achieve targeted cost efficiencies and gross margin improvements;

•manufacturing problems and capacity imbalances, including at our contract manufacturers;

•fluctuations in inventory levels in our distribution channels;

•risks related to the use of artificial intelligence (AI) in our business;

•our dependence on sophisticated information technology systems and infrastructure, including the use of third-party, cloud-based technologies, and the impact of outages or breaches of the information technology systems and infrastructure we rely on;

•the impact of weather conditions, including those related to climate change, and the availability of natural resources;

•demand, supply and operational challenges associated with the effects of a human disease outbreak, epidemic, pandemic or other widespread public health concern;

•the loss of key personnel or highly skilled employees;

•adverse effects of labor disputes, strikes and/or work stoppages;

•the effect of our substantial indebtedness on our business, including restrictions in our debt agreements that limit our operating flexibility and changes in our credit ratings that lead to higher borrowing expenses and restrict access to credit;

•changes in interest rates that adversely affect our earnings and cash flows;

•risks related to the write-down of goodwill or identifiable intangible assets;

•the lack of availability or significant increases in the cost of raw materials;

•risks related to foreign and domestic economic, political, legal and business environments;

•risks related to foreign currency exchange rate fluctuations;

•risks related to underfunded pension plan liabilities;

•our current plan not to pay dividends and restrictions on our ability to pay dividends;

•the potential impact that actions by activist shareholders could have on the pursuit of our business strategies;

•risks related to tax expense or exposures;

•actions by regulatory bodies, including as a result of their interpretation of studies on product safety;

•the possible slowing or cessation of acceptance and/or adoption of our farm animal sustainability initiatives;

•the impact of increased regulation or decreased governmental financial support related to the raising, processing or consumption of farm animals;

•risks related to tariffs, trade protection measures or other modifications of foreign trade policy;

•the impact of litigation, regulatory investigations and other legal matters, including the risk to our reputation and the risk that our insurance policies may be insufficient to protect us from the impact of such matters;

•challenges to our intellectual property rights or our alleged violation of rights of others;

•misuse, off-label or counterfeiting use of our products;

•unanticipated safety, quality or efficacy concerns and the impact of identified concerns associated with our products;

•insufficient insurance coverage against hazards and claims;

•compliance with privacy laws and security of information;

•risks related to environmental, health and safety laws and regulations; and

•inability to achieve goals or meet expectations of stakeholders with respect to environmental, social and governance matters.

See "Item 1A. Risk Factors" in Part I of this Form 10-K for a further description of these and other factors. Although we have attempted to identify important risk factors, there may be other risk factors not presently known to us or that we presently believe are not material that could cause actual results and developments to differ materially from those made in or suggested by the forward-looking statements contained in this Form 10-K. If any of these risks materialize, or if any of the above assumptions underlying forward-looking statements prove incorrect, actual results and developments may differ materially from those made in or suggested by the forward-looking statements contained in this Form 10-K. We caution you against relying on any forward-looking statements, which should also be read in conjunction with the other cautionary statements that are included elsewhere in this Form 10-K. Any forward-looking statement made by us in this Form 10-K speaks only as of the date hereof. Factors or events that could cause our actual results to differ may emerge from time to time, and it is not possible for us to predict all of them. We undertake no obligation to publicly update or to revise any forward-looking statement, whether as a result of new information, future developments or otherwise, except as may be required by law.

PART I

Overview

Elanco Animal Health Incorporated and its subsidiaries (collectively, Elanco, the Company, we, us, or our) is a global leader in animal health, dedicated to innovating and delivering products and services to prevent and treat disease in farm animals and pets. We partner with farmers, pet owners, veterinarians and society to create value and help our customers improve the health of animals in their care, while also making a meaningful impact on the communities we serve. Our diverse, durable product portfolio is sold in more than 90 countries and serves animals across many species, primarily: dogs and cats (collectively, pet health) and cattle, poultry, swine, sheep and, prior to the divestiture of our aqua business in July 2024, aqua (collectively, farm animal). With this ability to reach the world's animals, we are committed to fulfilling our customer promise: To be your advocate and continually earn your trust, improving the health of animals and creating value through innovative products, expertise and service. Through our customer promise and our commitment to excellence, we strive to advance the well-being of animals, people and the planet, enabling us to realize our vision of Food and Companionship Enriching Life.

With a heritage dating back to 1954, we were formerly a business unit of Eli Lilly and Company (Lilly), becoming an independently incorporated company on September 18, 2018. We finalized our separation from Lilly in March 2019. In August 2020 we acquired Bayer Animal Health, marking the largest acquisition in industry history. This acquisition enabled us to become a more diverse, durable and global company with greater reach and scale. This acquisition also helped us expand our portfolio, creating a better balance between our pet health and farm animal products and between the United States (U.S.) and international markets, while also expanding our omnichannel presence in both the veterinary clinic and in retail markets, including e-commerce.

We have continuously strengthened and expanded our three-pronged strategy: Innovation, Portfolio and Productivity, which remains our foundation for sustained growth and profitability. Over time, we expect to achieve revenue growth and improved profitability by delivering consistent, high-impact Innovation and prioritizing large market opportunities in major geographies. We consistently innovate to improve the health of animals and to benefit our customers. Our focused strategy prioritizes certain assets, including late-stage potential blockbusters, while maximizing life cycle management and refilling the early-stage pipeline to achieve a consistent flow of innovation. We also continue to optimize our diverse Portfolio to grow, leveraging our deep, established customer relationships and expanding product offerings. We will also continue to drive geographic and channel expansion, to reach more of the world's animals. Further, we continue to focus on our strategic Productivity initiatives to improve earnings and cash flows.

In addition, we continue to enhance our approach to sustainability and environmental, social and governance (ESG) principles, focusing on the four interconnected pillars below, which we refer to as Elanco's Healthy Purpose™, designed to create a meaningful impact today and for years to come:

Healthier Animals: We are helping pets and farm animals live healthy, high-quality lives by continuously expanding our portfolio and identifying new and innovative animal care products, practices and services to support animal health and well-being.

Healthier People: We help improve people's lives and livelihoods by promoting animal companionship and enabling healthier and more plentiful and environmentally friendly production of meat, milk, fish and eggs.

Healthier Planet: We are committed to minimizing our environmental footprint while leveraging product and service innovations to help our customers advance their own sustainability efforts.

Healthier Enterprise: We are committed to growing our business with integrity and excellence with respect to all stakeholders, fostering an inclusive, cause-driven culture where employees can make a difference – encouraging ownership, growth and well-being.

Commercial Operations

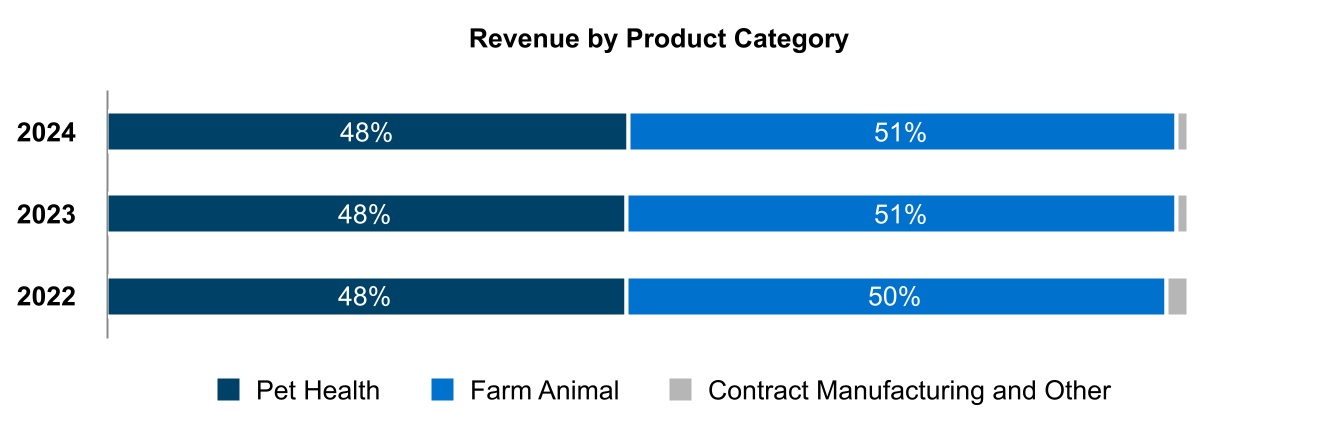

We operate our business as a single segment within the animal health industry, dedicated to fulfilling our vision of Food and Companionship Enriching Life. We advance this vision by offering a comprehensive portfolio of products in the pet health and farm animal product categories. Our reported revenue by product category was as follows:

Contract manufacturing and other represents revenue from arrangements in which we manufacture products on behalf of a third party and royalty revenue.

International Operations

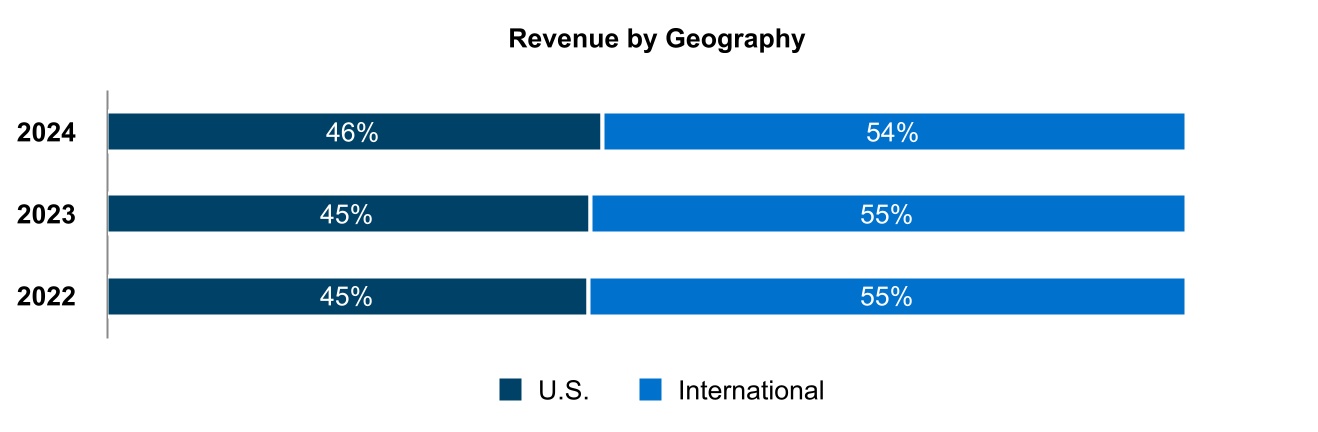

Our operations are conducted globally. The U.S. is our largest market, accounting for 46% of our total revenue in 2024. By total revenue, China, Brazil and the United Kingdom (U.K.) are our largest markets outside the U.S. Our reported revenue by geographic region was as follows:

Products

We have a diverse portfolio of products marketed under approximately 200 brands, including products for both pets and farm animals.

| | | | | |

| Pet Health: Our pet health products help pets live longer, healthier and more active lives. Our global pet health portfolio is focused on parasiticides, vaccines and therapeutics. We have one of the broadest parasiticide portfolios in the pet health market based on indications, species and formulations, with products that protect pets from fleas, ticks and internal parasites. Our Advantage Family of brands (Advantage™, K-9 Advantix™, Advocate™, AdTab™, among others) and Seresto™ products are over-the-counter treatments for the prevention and elimination of fleas and ticks and complement our prescription parasiticide products, which include our Credelio Family of brands (Credelio™, Credelio Cat™, Credelio Plus™), Interceptor Plus™, Drontal Family of brands (Doncit™, Drontal™, Drontal Plus™) and Trifexis™. Our vaccines portfolio provides differentiated prevention coverage for a number of important pet health risks and is available in the U.S. only. In therapeutics, we have a broad pain portfolio for dogs and cats across modes of action, indications and disease stages. Pet owners are increasingly treating osteoarthritis in their pets, and our Galliprant™ product offers a convenient at home solution for pet owners. Additionally, we have products that offer treatment for otitis (ear infections) and treatments for certain cardiovascular and dermatology indications. |

| | | | | |

| Farm Animal: Our farm animal products help farmers improve animal health and wellbeing and raise livestock more sustainably, delivering more food while using fewer resources and enhancing the integrity of the food supply. Our farm animal portfolio of products for cattle (beef and dairy), swine and poultry is primarily focused on: 1) efficiency and performance; 2) disease prevention and treatment; 3) food safety; and 4) sustainability. Our products include medicated feed additives, injectable antibiotics, vaccines, insecticides and enzymes, among others. Key farm animal products Rumensin™, Baytril™ and Experior® are used extensively in cattle, while our Maxiban™ and Monteban™ products are valuable offerings for the control and prevention of intestinal disease in poultry. |

In 2024, our top five selling products and/or product families were our Advantage Family (cats and dogs), Seresto (cats and dogs), Rumensin (cattle), Maxiban / Monteban (poultry) and our Credelio Family (cats and dogs). These products and product families combined to represent approximately 36% of our total revenue in 2024, with our largest product family, Advantage Family, representing approximately 10% of total revenue. Information regarding our principal products and product families, those that represented approximately 1% or more of our revenue in 2024, is as follows:

Pet Health Products

| | | | | | | | | | | | | | |

| | | | |

| Product | | Description | | Primary Species |

| | | | |

| Advantage Family | | Family of topical applications that provide broad-spectrum protection against and treatment of fleas, ticks, mosquitoes, lice and biting flies. Certain products within the Advantage Family also provide protection against heartworm, lungworm and other gastrointestinal worm infections, including roundworms, whipworms and hookworms. | | Cats, Dogs |

| | | | |

| Atopica™ | | Controls atopic dermatitis. | | Dogs |

| | | | |

| | | | |

| | | | |

| Credelio Family | | Family of oral products that kills adult fleas, treats flea infestations and treats and controls tick infestations. The introduction of Credelio Quattro™ in January 2025 adds a monthly chewable tablet for dogs that protects against fleas, ticks, heartworms, roundworms, hookworms and three different species of tapeworms. | | Cats, Dogs |

| Drontal Family | | Family of injectable and oral tablet dewormers indicated for the removal of tapeworms, hookworms, roundworms and whipworms. | | Cats, Dogs |

| Galliprant | | Controls pain and inflammation associated with osteoarthritis. | | Dogs |

| | | | |

| | | | |

| | | | |

| Interceptor Plus | | Prevents heartworm disease and helps treat and control roundworm, hookworm, whipworm and tapeworm infections. | | Dogs |

| Milbemax™ | | Treats and controls parasitic infections due to common intestinal worms. | | Cats, Dogs |

| Onsior™ | | Controls postoperative pain and inflammation associated with certain surgeries. | | Cats, Dogs |

| Seresto | | Flea and tick collar with a patented low dose, slow-release technology that kills and repels fleas and ticks which may transmit vector-borne diseases and kills lice for up to 8 months. | | Cats, Dogs |

| Trifexis | | Prevents heartworm disease, kills fleas, helps prevent flea infestations and also helps treat and control hookworms, roundworms and whipworms. | | Dogs |

TruCan™ (vaccines) | | Includes multiple products that collectively protect against distemper, adenovirus, parvovirus, corona, parainfluenza, leptospira canicola and other diseases. | | Dogs |

Farm Animal Products

| | | | | | | | | | | | | | |

| | | | |

| Product | | Description | | Primary Species |

AviPro™ (vaccines) | | Includes multiple products that collectively protect against Newcastle disease, infectious bronchitis, fowl cholera, paramyxovirus Type 3, Bursal Disease, other diseases and foodborne pathogens like Salmonella. | | Poultry |

| | | | |

| Baytril | | Injectable antibiotic active against bacterial respiratory disease pathogens. Baytril is a shared-class antibiotic. | | Cattle, Swine |

| Catosal™ | | Injectable for prevention or treatment of deficiencies of vitamin B12 and phosphorus. | | Cattle |

| | | | |

| | | | |

| Denagard™ | | Treats swine dysentery. Denagard is a shared-class antibiotic. | | Swine |

| Experior | | Reduces ammonia gas emissions from an animal or its waste. | | Cattle |

| | | | | | | | | | | | | | |

| | | | |

| Product | | Description | | Primary Species |

| Hemicell | | Enzyme supplement for poultry and swine feeds. | | Poultry, Swine |

| Maxiban / Monteban | | Prevents coccidiosis in broiler chickens. Maxiban and Monteban are animal-only antibiotics and ionophores. | | Poultry |

| | | | |

| Pulmotil™ | | Controls swine respiratory disease and bovine respiratory disease (BRD). Pulmotil is a shared-class antibiotic. | | Cattle, Swine |

| Rumensin | | Improves feed and milk production efficiency and increases rate of weight gain in cows. Also prevents and controls coccidiosis for cows, calves (excluding veal calves) and goats. Rumensin is an animal-only antibiotic and an ionophore. | | Cattle |

| Surmax™ | | Prevents necrotic enteritis in broiler chickens. Surmax is an animal-only antibiotic. | | Poultry |

| | | | |

| | | | |

| | | | |

A key element of our targeted value creation strategy is to drive revenue growth through portfolio development and product innovation. We continue to pursue the development of new chemical and biological molecules, as well as additional registrations and indications for current products. Our future growth depends on both our pipeline of new products, including new products we develop internally, develop with partners or that we are able to obtain through licenses or acquisitions, and the life cycle management of our existing products. We believe we are an industry leader in animal health R&D, with a track record of successful product innovation, business development and commercialization. New product development and regulatory highlights during 2024 included the following:

Bovaer: In May 2024, the U.S. Food and Drug Administration (FDA) completed its comprehensive, multi-year review of Bovaer® (3-NOP), a first-in-class methane-reducing feed ingredient for use in lactating dairy cattle. Producers began feeding the product to cattle in the U.S. during the third quarter of 2024.

Zenrelia: We received final FDA approval for Zenrelia®, a JAK inhibitor targeting control of pruritus and atopic dermatitis in dogs, in September 2024. We launched Zenrelia shortly after final approval, with the first sales occurring in late September. We have also received approval for Zenrelia in Brazil, Canada and Japan. Additional reviews are ongoing in other key markets, including Europe, U.K. and Australia.

Credelio Quattro: In October 2024, we received final approval from the FDA for Credelio Quattro, a monthly chewable tablet for dogs that protects against fleas, ticks, heartworms, roundworms, hookworms and three different species of tapeworms. Credelio Quattro was launched, with the first commercial sale occurring in January 2025.

Experior: In October 2024, we received multiple combination clearance approvals from the FDA for Experior to be used in combination with other farm animal products, allowing for broader use in heifers, which represent nearly 40% of the fed cattle population in the U.S.

Seasonality

While many of our products are sold consistently throughout the year, we do experience seasonality in our pet health business due to increased demand for certain parasiticide product offerings in the first half of the year. For example, in 2024 approximately 70% and 55% of total annual revenue generated by our higher-margin parasiticide products Seresto and Advantage Family, respectively, occurred during the first half of the year, which is reflective of the flea and tick season in the Northern Hemisphere.

Sales and Marketing

Through our global sales force of over 2,200 sales representatives, our veterinary consultants and our key distributors, we seek to build strong customer relationships and fulfill demand for our products. Our sales representatives visit our customers, including consultants, veterinarians, farm animal producers and resellers, to inform, promote and sell our products and to support customers. Our veterinary consultants are available to provide scientific consulting focused on disease management and herd management, training and education on diverse topics, including responsible product use, and generally have advanced degrees in veterinary medicine, veterinary nutrition or other agriculture-related fields. These direct relationships with customers allow us to better understand their needs and provide us access to customer decision makers. Additionally, our sales representatives and veterinary consultants focus on collaborating with our customers to educate and support them on topics such as local disease awareness and to help them adopt new and more sophisticated animal health solutions, which may include the use of our products. In addition, our sales and marketing organization provides enhanced value by supporting farm animal producers to maximize their yields and reduce their costs. Furthermore, our expertise and data analytics help our customers analyze large amounts of health and production data in order to improve production efficiency and business performance.

Customers

We primarily sell our pet health products to third-party distributors and retailers, as well as directly to veterinarians who typically then sell our products to pet owners. We primarily sell our farm animal products to third-party distributors and directly to a diverse set of farm animal producers, including beef, dairy, pork and poultry operations. Our omnichannel presence allows us to sell into both the veterinary clinic and retail markets, including e-commerce. Certain top selling pet health products, including the Advantage Family and Seresto, are offered through these channels. Our largest customer, an affiliate of Cencora, Inc., is a third-party veterinary distributor and represented approximately 11% of our total revenue in 2024. Our second largest customer, which is also a third-party distributor, represented approximately 6% of revenue in 2024, while no other customer represented greater than 5% of revenue during 2024.

Research and Development

Our R&D efforts focus on delivering consistent, high-impact innovation. Our R&D team is a project driven organization, with our R&D projects executed and led by highly experienced individuals with deep technical knowledge and substantial experience in discovery research, clinical sciences, technological development and regulatory expertise across our pet health and farm animal product categories. We believe this approach allows us to consistently progress our multi-year innovation projects toward regulatory approvals, while ensuring clear visibility to the innovation portfolio composition, value and progress. As of December 31, 2024, we employed over 1,000 employees in our global R&D and Regulatory Affairs organizations.

Our R&D organization utilizes a fully integrated global network of labs, service centers and development sites supported by a network of third-party partners. We also have a significant international regulatory operation that manages new product submissions and ensures ongoing compliance for our existing commercial portfolio. Our global R&D sites are comprised of the following:

| | | | | | | | | | | |

| R&D Centers of Excellence with a Global Scope | | Major Regional Centers for Key Markets |

| Kemps Creek, Australia | Speke, U.K. | | Sao Paulo, Brazil |

| Monheim, Germany | Fort Dodge, Iowa | | Shanghai, China |

| Bangalore, India | Greenfield, Indiana (R&D headquarters) | | |

| Basel, Switzerland | | | |

Our R&D efforts focus on products that prevent and treat disease, improve and extend quality of life, improve the type of care received by animals and reduce the environmental impact of raising livestock. We seek to concentrate our resources on projects that match our strategy and where we can leverage our broad technical and commercial capabilities. In addition to supporting our existing product portfolio, new product innovation is a core part of our business strategy. Our approach is a build, buy or partner strategy to develop compelling innovations that originate from our scientists and innovators, academia, agribusiness or external partners including human pharmaceutical, agriculture and biotechnology organizations. We focus our R&D investments on projects that target novel product introductions with new active ingredients, as well as products leveraging known active ingredients in new indications, presentations, combinations and species expansion.

Our R&D efforts are balanced across species, development phases and technology platforms. We apply large and small molecule approaches for both farm animals and pets. Additionally, we employ various delivery strategies for products, including in-feed, injectable, oral and topical formulations developed in conjunction with our manufacturing team to assure reliable and consistent production that leverages the capabilities within our internal and external manufacturing network.

Portfolio investment decisions and prioritization are influenced by the probability of technical success, economic value, time to market, portfolio fit and balance. R&D expenses totaled $344 million in 2024, $327 million in 2023 and $321 million in 2022.

Manufacturing and Supply Chain

We have a global manufacturing network of 17 sites comprised of the following:

| | | | | | | | | | | | | | |

| International | | | | U.S. |

| Barueri, Brazil | | Santa Clara, Mexico | | Clinton, Indiana |

| Chengdu, China | | Manukau, New Zealand(1) | | Terre Haute, Indiana |

| Wusi, China | | Banwol, South Korea | | Fort Dodge, Iowa |

| Huningue, France | | Chungli, Taiwan | | Elwood, Kansas |

| Cuxhaven, Germany | | Speke, United Kingdom(2) | | Kansas City, Kansas |

| Kiel, Germany | | | | Winslow, Maine |

(1)In October 2024, we entered into an agreement to sell our manufacturing facility in Manukau, New Zealand. This transaction is expected to close in the first half of 2025 pending regulatory approvals and subject to other closing conditions.

(2)In November 2024, we acquired the manufacturing facility and related assets in Speke, U.K. from a previous contract manufacturing partner. See Note 4. Acquisitions, Divestitures and Other Arrangements to the consolidated financial statements for further information.

Our products are manufactured both at the sites listed above that are operated by us and across a network of approximately 130 contract manufacturing organizations (CMOs). Our external manufacturing team centrally governs and provides oversight to our global CMO relationships. We select CMOs based on several factors, including: (1) their ability to reliably supply products or materials that meet our quality standards at an optimized cost; (2) their access to specialty products and technologies; (3) capacity; (4) financial analyses; and (5) local presence. Our external manufacturing team seeks to ensure that all CMOs we use adhere to our standards of manufacturing quality.

Pharmaceutical production processes are complex, highly regulated and can vary widely from product to product. Shifting or adding manufacturing capacity can be a lengthy process requiring significant capital expenditures, process modifications and regulatory approvals. We have in the past invested in, and will continue to invest in, improvements to our existing manufacturing facilities. For example, in 2024 we announced a planned $130 million expansion of our biologics manufacturing facility in Elwood, Kansas to enable further growth of our monoclonal antibody portfolio. We also intend to continue our efficiency improvement programs in our manufacturing and supply chain organization. Our strong quality control and quality assurance programs are managed and coordinated globally and are in place at all internal manufacturing sites and external manufacturing hubs. We also regularly inspect and audit our internal sites and CMO locations.

To maintain supply of our products, we use a variety of techniques, including comprehensive quality and planning and inventory management systems. We generally seek to develop an appropriate inventory strategy to fill market demand until an alternative source of supply can be implemented, in the event a supplier becomes unable to provide the required materials or product. However, various developments have led, and in the future may lead, to interruption or shortages in supply until we establish new sources, implement alternative processes, bring new manufacturing facilities online or pause or discontinue product sales in one or more markets. For example, in September 2024 one of our contract manufacturing supply partners, TriRx Speke Ltd (TriRx Speke), entered into trading administration in the U.K. Although we minimized supply disruption through our acquisition of this site in November 2024, additional manufacturing or supply chain challenges could occur in the future.

Raw Materials

We purchase certain raw materials and active pharmaceutical ingredients (API) necessary for the commercial production of our products from a variety of third-party suppliers. Principal materials used in our manufacturing operations for key brands are typically available from more than one source; however, we may in some instances obtain certain raw or intermediate materials from only a single source. Our active ingredients for biologics are manufactured primarily in internal facilities, while chemically derived active ingredients are sourced from external partners.

Competition

We face intense competition globally. Competition may vary depending on the particular region, species, product category or individual product. We compete principally on the basis of product quality, price, cost-effectiveness, promotional effectiveness, new product development and product differentiation. Certain Elanco products, both existing and new, may compete with other branded or generic products already on the market or that are later developed by competitors. When competitors introduce new products with ease-of-use, therapeutic or cost advantages, our products may become subject to decreased sales and/or price reductions.

Our primary competitors include animal health medicines and vaccines companies such as Zoetis Inc., Boehringer Ingelheim Vetmedica, Inc., the animal health division of Boehringer Ingelheim GmbH, and Merck Animal Health, the animal health division of Merck & Co., Inc. We also compete with numerous other producers of animal health products throughout the world, including start-up companies working in the animal health area. In addition, we also face competition globally from manufacturers of generic drugs and producers of nutritional health products.

Intellectual Property

Our technology, brands and other intellectual property are important elements of our business. We rely on patent, trademark, copyright and trade secret laws, as well as regulatory exclusivity periods and non-disclosure agreements to protect our intellectual property rights. Our policy is to vigorously protect, enforce and defend our rights to our intellectual property.

Our product portfolio and certain product candidates enjoy the protection of approximately 6,700 patents and applications, filed in over 90 countries, with a concentration in our major markets as well as other markets with strong patent laws and protections. While many of the patents and patent applications in our portfolio are the result of our own work, others have been developed in collaboration with partners, acquired through business transactions

or licensed to us by third parties. A subset of our current products or product candidates are covered by patents and patent applications.

Patents for individual products expire at different times based on the date of the patent filing (or occasionally, the date of patent grant) and the legal term of patents in the countries where such patents are obtained. Some of our principal products, including certain products within our Advantage Family, Rumensin and Maxiban / Monteban do not have patent protection. Other products are protected by patents that expire over the next several years. Below is a summary of our recent and upcoming key patent expirations:

•Galliprant is protected by patents in the U.S., Europe, Canada, Japan and other key markets. While patents covering the active ingredient, grapiprant, expired in 2021 in all markets except Japan, patents covering the physical form of the active ingredient remain in force and will expire between 2026 and 2031, depending on jurisdiction. Patent coverage relating to methods of use and formulation will expire in 2035 in most jurisdictions.

•The Seresto formulation patent will expire in the U.S. in September 2027. In Europe, the formulation patents will expire in June 2025, but in some countries, including Spain, Italy and the U.K., supplementary protection certificates (SPCs) have been granted that expire in August 2026.

•Patent coverage for Milbemax/Interceptor chewable products expired in July 2024 in Europe and other key markets. Patent coverage for Interceptor Plus extends through October 2028 in the U.S.

•The U.S. patent for Experior's active ingredient, lubabegron, will expire in April 2025. Coverage for Experior methods of use will expire in 2037 in the U.S. and 2035 in other key markets.

Additionally, many of our vaccine products, including the TruCan family of vaccines, are based on proprietary or patented master seeds and formulations. We actively seek to protect our proprietary information, including our trade secrets and proprietary know-how, through a variety of means, including by seeking to require our employees, consultants, advisors and partners to enter into confidentiality agreements and other arrangements upon the commencement of their employment or engagement.

We seek to file and maintain trademarks around the world based on commercial activities in most regions where we have, or desire to have, a business presence for a particular product. We currently maintain more than 12,800 trademark applications and registrations in major regions, primarily identifying products dedicated to the care of livestock and pets.

Regulatory Matters

The sale of animal health products is governed by the laws and regulations specific to each country in which we sell our products. To maintain compliance with these regulatory requirements, we have established processes, systems and dedicated resources with end-to-end involvement from product concept to launch and maintenance in the market. Our regulatory function is Elanco's key interface with the relevant authorities and is responsible for applying for and obtaining the necessary registrations and post-approvals, extending them if appropriate (e.g., developing claims in additional species), updating (e.g., changes to shelf-life or manufacturing site) and ongoing monitoring of safety and efficacy through our global pharmacovigilance system. In this way, the regulatory function ensures registrations remain valid and our products can continue to be sold. To effectively do this, our regulatory function actively engages in dialogue with the relevant authorities regarding policies that relate to animal health products. In most of our markets, the relevant authority is separate from those governing human medicinal products.

United States

FDA. The regulatory body that is responsible for the regulation of animal health pharmaceuticals in the U.S. is the Center for Veterinary Medicine (CVM), a division of the FDA. All manufacturers of animal health pharmaceuticals must demonstrate their products to be safe, effective and produced by a consistent method of manufacture as defined under the Federal Food, Drug and Cosmetic Act (FFDCA). The FDA’s basis for approving a new animal drug application is documented in a Freedom of Information Summary. Post-approval monitoring of products is required by law, with reports being provided to the CVM’s Office of Surveillance and Compliance. Reports of product quality defects, adverse events or unexpected results are maintained and submitted in accordance with the law. Additionally, as part of the drug experience report, we are required to submit all new information pertaining to the safety or effectiveness of a product, regardless of the source.

U.S. Department of Agriculture (USDA). The regulatory body in the U.S. for veterinary biologicals is the USDA. The Center for Veterinary Biologics within the Animal and Plant Health Inspection Service in the USDA is responsible for the regulation of animal health biologicals, which includes but is not limited to vaccines, bacterins, allergens, certain antibodies, antitoxins, toxoids, immunostimulants, certain cytokines, antigenic or immunizing components of live microorganisms and diagnostic components of natural or synthetic origin, or that are derived from synthesizing or altering various substances or components of substances such as microorganisms, genes or genetic sequences, carbohydrates, proteins, antigens, allergens or antibodies. All manufacturers of animal health biologicals must show their products to be pure, safe, effective and produced by a consistent method of manufacture as defined under the

Virus Serum Toxin Act. Post-approval monitoring of products is also required. Reports of product quality defects, adverse events or unexpected results are maintained and submitted in accordance with the agency requirements.

Environmental Protection Agency (EPA). The main regulatory body in the U.S. for veterinary pesticides is the EPA. The EPA’s Office of Pesticide Programs is responsible for the regulation of most pesticide products applied to animals in accordance with a memorandum of understanding between the FDA and the EPA for products that are subject to regulation under both the FFDCA and the Federal Insecticide, Fungicide and Rodenticide Act (FIFRA). All manufacturers of animal health pesticides must show their products will not cause unreasonable adverse effects to humans or the environment as stated in the act. Within the U.S., individual state pesticide authorities must also approve pesticide products that have been approved by the EPA before distribution in that state. Post-approval monitoring of products is required, with reports provided to the EPA and some state regulatory agencies.

European Union (EU)

The European Medicines Agency (EMA) is a centralized agency of the EU responsible for the scientific evaluation of many of the Veterinary Medicinal Products (VMP) developed by pharmaceutical companies for use in the EU. The agency has a veterinary review section distinct from the medical review section for human products. The Committee for Veterinary Medicinal Products (CVMP) is responsible for scientific review of the submissions for VMP, including immunological products. If the CVMP concludes that all requirements for quality, safety and efficacy are met and the product benefits outweigh the risks, it issues a positive opinion that is forwarded to the European Commission, which takes the final decision following the European comitology procedure. The centralized marketing authorization is valid in all of the EU and in Northern Ireland. All countries that are not part of the EU but belong to the European Economic Area (EEA), such as Norway, Iceland and Liechtenstein, have been part of the scientific assessment done by the CVMP. These countries issue a national marketing approval in accordance with the European Commission's decision.

If approval is sought for products that either cannot or do not need to follow the centralized procedure, approval can also be achieved by national approval in an EEA country agency. This national authorization can be mutually recognized by other EEA countries/EU member states (Mutual Recognition Procedure). In addition, national and mutual recognition can be done in a combined procedure (Decentralized Procedure).

A series of regulations, directives, guidelines, EU Pharmacopeia Monographs and other legislation provide the requirements for approval in the EU. In general, these requirements are similar to those in the U.S., requiring demonstrated evidence of purity, safety, efficacy and consistency of manufacturing processes.

The European Food Safety Authority (EFSA) is the agency of the EU that provides scientific advice and communicates with respect to existing and emerging risks associated with the food chain. Based on EFSA’s mandate, it evaluates applications for feed additives, including coccidiostats, enzymes and several nutritionals for animals.

The European Chemicals Agency (ECHA) is the agency of the EU for the safe use of chemicals. Based on the ECHA’s mandate, it conducts the evaluation of biocides for the EU.

We are also governed by each of the national regulatory bodies in the EU.

United Kingdom

The Veterinary Medicines Directorate (VMD) is the main regulatory body in the U.K. responsible for regulating and controlling veterinary pharmaceuticals. A trade agreement between the U.K. and the EU includes regulatory and customs cooperation mechanisms, as well as provisions supporting open and fair competition. The Northern Ireland protocol, which is part of the trade deal, requires that VMD follow EU rules in Northern Ireland. Laws applying to the rest of the U.K. remain largely aligned.

Brazil

The Ministry of Agriculture, Livestock Production and Supply (MAPA) is the regulatory body in Brazil that is responsible for the regulation and control of pharmaceuticals, biologicals and medicinal feed additives for animal use. MAPA’s regulatory activities are conducted through the Secretary of Agricultural Defense and its Livestock Products Inspection Department. In addition, regulatory activities are conducted at a local level through the Federal Agriculture Superintendence. These activities include the inspection and licensing of both manufacturing and commercial establishments for veterinary products, as well as the submission, review and approval of pharmaceuticals, biologicals and medicinal feed additives. MAPA is one of the most active regulatory agencies in Latin America, having permanent seats at several international animal health forums, such as Codex Alimentarius, World Organization for Animal Health and Committee of Veterinary Medicines for the Americas.

China

The Ministry of Agriculture and Rural Affairs (MARA) is the regulatory body that is responsible for the regulation and control of pharmaceuticals, biologicals, disinfectants, medicinal feed additives, pesticides and feed/feed additives for animal use. There are three organizations under the MARA that regulate animal health:

•The Institute of Veterinary Drug Control (IVDC) is responsible for the evaluation of new applications, renewals, variations, manufacturers, quality methods and tissue residue methods for pharmaceuticals, biologicals, disinfectants and medicinal feed additives.

•The feed/feed additive office is responsible for the registration and renewal of feed and feed additives.

•The pesticide bureau is responsible for the registration and renewal of pesticide products.

Rest of World

Country-specific regulatory laws typically have provisions that include requirements for certain labeling, safety, efficacy and manufacturers’ quality control procedures (to assure the consistency of the products), manufacturing site standards, as well as company records and reports. Many other countries’ regulatory agencies either refer to some or all of the requirements of the U.S. or EU and may have additional specific local requirements. Most authorities also consider the standards set by international animal health entities, including the World Organization for Animal Health (WOAH), Codex Alimentarius and the International Cooperation on Harmonization of Technical Requirements for Registration of Veterinary Medicinal Products (VICH).

Joint FAO/WHO Expert Committee on Food Additives. The Joint FAO/WHO Expert Committee on Food Additives is an international expert scientific committee that is administered jointly by the Food and Agriculture Organization of the United Nations (FAO) and the World Health Organization (WHO). It provides a risk assessment/safety evaluation of residues of veterinary drugs in animal products, exposure and residue definition and maximum residue limit proposals for veterinary drugs. Similarly, the Joint FAO/WHO Meeting on Pesticide Residues (JMPR) is an international expert scientific group administered jointly by the FAO and WHO. JMPR reviews residues and analytical aspects of the pesticides, estimates the maximum residue levels, reviews toxicological data and estimates acceptable daily intakes for humans of the pesticides under consideration. Elanco works with this committee to establish acceptably safe levels of residual substances in food-producing animals after treatment with veterinary drugs or pesticides. This in turn enables the calculation of appropriate withdrawal times for our products prior to an animal entering the food chain.

Advertising and Promotion Review. Promotion of animal health products is controlled by regulations in many countries. These rules generally restrict advertising and promotion to those claims and uses that have been reviewed and endorsed by the applicable agency. We conduct a review of promotion material for compliance with the local and regional requirements in the markets where we sell animal health products.

Import and Export of Products. The importation and exportation of animal health products is controlled by regulations in many countries. In some jurisdictions this may include obtaining separate permits or licenses by product or by company or filing notices with applicable regulatory agencies prior to import or export of product. We ensure compliance with local, regional and global regulations in the markets where we import/export our animal health products.

International Cooperation on Harmonization of Technical Requirements for Registration of Veterinary Medicinal Products. VICH is a trilateral (EU-Japan-U.S.) program launched in 1996 aimed at harmonizing technical requirements for veterinary product registration. Several other countries have obtained observer status, for example, Canada, New Zealand, Australia, South Africa and the U.K., or are linked to VICH on the basis of the VICH Outreach Forum, a VICH initiative with the main objective of providing a basis for wider international harmonization of technical requirements. In addition, the World Organization for Animal Health is an associate member of VICH.

Environmental, Health and Safety

In addition to the laws and regulations discussed above, we are also subject to various federal, state, local and foreign laws and regulations, both within and outside the U.S., relating to environmental, health and safety (EHS) and sustainability matters. These laws and regulations govern matters such as the emission and discharge of hazardous materials into the ground, air or water; the generation, use, storage, handling, treatment, packaging, transportation, exposure to and disposal of hazardous and biological materials, including recordkeeping, reporting and registration requirements; and the health and safety of our employees. Due to our operations, these laws and regulations also require us to obtain and comply with permits, registrations and other authorizations issued by governmental authorities. These authorities can modify or revoke our permits, registrations or other authorizations and can enforce compliance through fines and injunctions.

Certain environmental laws impose joint and several liability, without regard to fault, for clean-up costs related to the disposal or release of hazardous substances into the environment, including at third-party sites or offsite disposal locations, or at sites that are currently owned or operated (or were formerly owned or operated) where such a disposal or release occurred. Although our current reserves for environmental remediation obligations are not material, we could be subject to liability for the investigation and remediation of legacy environmental contamination caused by historical industrial activity at sites we own or on which we operate. We are also monitoring and investigating environmental contamination from past industrial activity at certain sites. In connection with past divestitures, we have undertaken certain indemnification obligations that may require us, in the future, to conduct or

finance environmental clean-ups at sites that we no longer own or operate. We have also entered into indemnification agreements in connection with certain of our past acquisitions, pursuant to which we are, or may be, indemnified for various environmental clean-ups. However, such indemnities are limited in both time and scope and may be further limited in the presence of new information or may not be available at all.

In addition to clean-up actions brought by federal, state, local and foreign governmental entities, private parties could raise personal injury or other claims against us due to the presence of, or exposure to, hazardous materials on, from or otherwise relating to such a property. We have made, and intend to continue to make, necessary expenditures for compliance with applicable EHS laws and regulations.

Human Capital

Employees. As of December 31, 2024, we employed approximately 9,000 full time employees and approximately 450 fixed-duration employees, which are individuals hired for a pre-defined length of time (typically one to four years). Approximately 30% of our global workforce is U.S.-based, while slightly more than 10% of our global employees are members of unions, works councils, trade associations or are otherwise subject to collective bargaining agreements, primarily in Germany and the U.S.

Our Culture. At Elanco, we are committed to fostering an inclusive culture where employees can make a difference, encouraging ownership, growth and well-being. We are committed to creating a culture built on the foundation of the three following values that guide our decisions and the four following behavioral pillars that guide our actions:

Values:

Integrity – Do the right thing in the right way.

Respect – Respect people, our customers and the animals in their care.

Excellence – Be accountable. Continuously improve. Deliver with discipline.

Behavioral Pillars:

Involve – We seek participation and input to gain commitment and passionate performance and create an engaged community. We act with humility as One Elanco, collaborating for the best outcomes for the entire company.

Deliver – We focus on the essential, build mastery and diligently deliver on our commitments to our colleagues, customers and shareholders.

Own – We are accountable and empowered. We ask questions and raise concerns. We are fully invested in Elanco's success.

Innovate – We bring an innovative mindset that drives continuous improvement of our processes, products and services.

At Elanco, this culture drives employee performance, and our employees are driven by these values and behavioral pillars. Leadership and employees are encouraged to evaluate performance with these values and behavioral pillars in mind.

Inclusion, Diversity, Equity and Accessibility (IDEA). Our comprehensive IDEA strategy includes talent acquisition efforts focused on attracting high-quality candidates from a variety of sources and learning, mentoring and development opportunities for all employees. We also support the continued needs of our workforce through the evolution of our benefits, including paid time off and parental leave.

Our Global IDEA Council is an employee-led and leadership-supported group that influences the strategic direction of IDEA efforts at Elanco and represents our sites and affiliates from around the world. Additionally, nine Elanco Employee Resources Groups (ERGs) are essential to delivering our promise to employees to foster an inclusive culture and are key to the success of our IDEA strategy. ERGs are unique communities of employees from historically under-recognized groups, and their allies, offering support and professional development opportunities. Any employee is eligible to join any ERG.

Total Rewards. We invest in our workforce by offering competitive salaries, incentives and benefits. Our pay-for-performance philosophy is designed to create ownership and to help ensure we attract and retain talent, as well as reward and recognize top-performing employees through merit increases and other rewards. We benchmark our total rewards annually to ensure our compensation and benefit programs remain competitive with our peers. Our benefits are one way we support our employees’ well-being and deliver on our employee promise.

Development. We offer employees opportunities to advance their careers at Elanco and are committed to equipping employees with relevant skills and development opportunities to help them thrive and meet the ever-changing needs of customers and stakeholders across our dynamic and growing industry.

Beyond professional growth and development, Elanco employees actively engage in initiatives aligned to Elanco's Healthy Purpose to advance the well-being of animals, people, the planet and our enterprise, enabling us to realize our vision of Food and Companionship Enriching Life.

Available Information

Our website address is www.elanco.com. On our website, specifically within the "Investor Relations" section, we make available, free of charge, our annual, quarterly and current reports, including amendments to such reports, as soon as reasonably practicable after we electronically file such material with, or furnish such material to, the U.S. Securities and Exchange Commission (the SEC). In addition, the SEC maintains an internet site that contains reports, proxy and information statements, and other information regarding issuers, including Elanco, that file electronically with the SEC at www.sec.gov.

Information relating to corporate governance at Elanco, including our Corporate Governance Guidelines, Code of Conduct, Financial Code of Ethics, Articles of Incorporation, Bylaws, Committee Charters; information concerning our executive officers and members of our Board of Directors; and ways to communicate are also available on our website, www.elanco.com. We will provide any of the foregoing information without charge upon written request to Elanco’s Corporate Secretary, Elanco, 2500 Innovation Way, Greenfield, Indiana 46140. Information relating to shareholder services is also available on our website.

Information contained on our website is not part of, or incorporated by reference, in this Form 10-K.

Our business, financial condition and results of operations are subject to various risks, including but not limited to the risks described below. If any of such risks actually materializes, our business, financial condition and results of operations could be materially adversely affected.

Risks Related to the Animal Health Industry

The animal health industry is highly competitive.

The animal health industry is highly competitive. Our competitors include standalone animal health businesses, the animal health businesses of large pharmaceutical companies, specialty animal health businesses and companies that mainly produce generic products. Several start-up companies also compete in the animal health industry. We believe many of our competitors are conducting R&D activities in areas served by our products and in areas in which we are developing products. We also face competition from producers of nutritional health products. These competitors may have access to greater financial, marketing, technical and other resources. As a result, they may be able to devote more resources to developing, manufacturing, marketing and selling their products, initiating or withstanding substantial price competition or more readily taking advantage of acquisitions or other opportunities. Further, consolidation in the animal health industry could result in existing competitors realizing additional efficiencies or improving portfolio bundling opportunities, thereby potentially increasing their market share and pricing power, which could lead to a decrease in our revenue and profitability. For example, many of our competitors have relationships with key distributors and, because of their size, an ability to offer attractive pricing incentives, which may negatively impact or hinder our relationships with these distributors. In addition to competition from established market participants, new entrants to the animal health industry could substantially reduce our market share, render our products obsolete or disrupt our business model.

Competitive pressures could arise from, among other things, differences in safety and efficacy product profiles, limited demand growth or a significant number of additional competitive products being introduced into a particular market, price reductions by competitors, the ability of competitors to capitalize on their economies of scale, the ability of competitors to produce or otherwise procure animal health products at lower costs than we can and the ability of competitors to access more or newer technology than we can. To the extent any of our competitors are more successful with respect to any key competitive factor, or we are forced to reduce, or are unable to raise, the price of any of our products in order to remain competitive, our business, financial condition and results of operations could be materially adversely affected.

Our R&D, acquisition and licensing efforts may fail to generate commercially successful new products or to expand the use of our existing products.

Our future success depends on both our existing product portfolio and our pipeline of new products, including new products that we develop internally or through joint ventures and products we obtain through licenses or acquisitions. We commit substantial effort, funds and other resources to R&D, primarily through our own dedicated resources but also through collaborations with third parties. We also have acquired or partnered with a number of smaller animal health businesses, and we intend to continue to do so in the future. There are significant risks and uncertainties involved with the execution of these partnerships, many of which are outside our control, including the inability to develop, license or otherwise acquire product candidates or products and insufficient access to capital to fund such investments. We also cannot predict whether any products, once launched, will be commercially successful or will achieve revenue that is consistent with our expectations.

The animal health industry is subject to regional and local trends and regulations and, as a result, products that are successful in some markets may not achieve similar success when introduced into other markets. Furthermore, the timing and cost of our R&D may increase, and our R&D may become less predictable as, among other things, regulations applicable to our industry make it more time-consuming and/or costly to research, develop and register products. If we are unable to generate commercially successful new products or expand the use of our existing products, our business, financial condition and results of operations could be materially adversely affected.

Additionally, as part of our development strategy, we often hire clinical research organizations to perform preclinical testing and clinical trials for drug candidates. Clinical trials and procedures are inherently uncertain and there can be no assurance that these trials or procedures will be enrolled or completed in a timely or cost-effective manner or result in a commercially viable product or indication. Failure to achieve positive clinical trial and/or testing results could have a material adverse effect on our prospects. Furthermore, unfavorable or inconsistent clinical data from current or future clinical trials or procedures conducted by us, our competitors or third parties, or perceptions regarding this clinical data, could adversely affect our ability to obtain necessary approvals and the market’s view of our future prospects.

Lastly, new products may appear promising in development but fail to reach the market within the expected or optimal timeframe, or at all. We may be unable to predict with precision when, if or subject to what conditions any of

our products now under development will be approved and/or launched, or if approved, whether limitations to a product or the specific circumstances for which a product is approved, will match our expectations. For example, in the second quarter of 2024, the FDA determined that our Zenrelia product label would be required to include a boxed warning on safety. We believe the inclusion of this warning has slowed the product adoption curve, although the extent of any such effect cannot be definitely determined. In addition, product extensions or additional indications may not be approved. Developing and commercializing new products subjects us to inherent risks and uncertainties, including (i) delayed or denied regulatory approvals, (ii) delays or challenges with producing products in accordance with regulatory requirements, on a commercial scale and at a reasonable cost; (iii) failure to accurately predict the market for new products; and (iv) efficacy and safety concerns, any of which could lead to a slower or more limited commercial adoption of one of our products than initially estimated. In addition, a failure to continue to identify and develop products, both internally and through external sources, could impact our future success. Once necessary regulatory approvals are obtained, the commercial success of any new product depends upon, among other things, its acceptance by veterinarians and end customers, and on our ability to successfully manufacture, market and distribute products in sufficient quantities to meet demand. If we are unable to successfully bring a product to market, our business, financial condition and results of operations could be materially adversely affected.

Disruptive innovation and advances in veterinary medical practices, animal health technologies and alternatives to animal-derived protein could negatively affect the markets for our products.

The markets for our products are regularly impacted by the introduction and/or broad market acceptance of newly developed or alternative products that address the diseases and conditions for which we sell products. For example, the market for our pet health therapeutics has been particularly affected by innovation in new molecules and delivery formulations in recent years. Separately, there has been an increased focus in certain markets to seek replacements for animal-derived protein with alternative, plant-based or other natural or synthetic protein sources. Technological breakthroughs by others may render our products obsolete and reduce or eliminate the market for our products. Introduction or acceptance of competing animal health products and innovation or disruptive protein alternatives could materially adversely affect our business, financial condition and results of operations.

Generic products may be viewed as more cost-effective than our products.

In certain markets, we face competition from generic alternatives to our products. We depend on patents and related rights to enable our exclusive sale of certain products. Patents for individual products expire at different times based on a variety of factors, including the date of the patent filing (or sometimes the date of patent grant) and the legal term of patents in the jurisdictions where such patents are obtained. The extent of protection afforded by our patents varies from jurisdiction to jurisdiction and is limited by the scope of the claimed subject matter of our patents, the term of the patent and the availability and enforcement of legal remedies in the applicable jurisdiction. Some of our principal products, including certain products within our Advantage Family, Rumensin and Maxiban / Monteban do not have patent protection. Other products are protected by patents that expire over the next several years. As the patents for a brand name product expire, competitors may begin to introduce generic or other alternatives, and as a result, we may face competition from lower-priced alternatives to many of our products. For further information, see "Item 1. Business – Intellectual Property."

Generic competitors are becoming more aggressive in terms of launching products before patent rights expire, and, because of attractive pricing, sales of generic products are an increasing percentage of overall animal health sales in certain regions. If animal health customers increase their use of new or existing generic products, we may be forced to lower our prices and/or provide discounts or rebates in order to compete with generic products. In such event, our business, financial condition and results of operations could be materially adversely affected.

Regulatory restrictions and bans on the use of antibiotics and productivity products in farm animals, as well as changing market demand, may continue to negatively affect demand for certain of our farm animal products.

Our operational results have been, and may continue to be, affected by regulations and changing market demand. In certain markets, including the U.S., sales of certain of our farm animal products have been negatively affected by changes in consumer sentiment for proteins and dairy products produced without the use of antibiotics or other products intended to increase animal production. There are two classes of antibiotics used in animal health: shared-class, or medically important, antibiotics, which are used to treat, control and/or prevent infectious diseases caused by pathogens that occur in both humans and animals; and animal-only antibiotics, which are used to treat, control and/or prevent infectious diseases in animals, and in some instances, promote animal growth performance. Concerns that the use of antibiotics in farm animal production may lead to increased antibiotic resistance of human pathogens have resulted in regulation and changing market demand. For example, in 2022 the EU began restricting the use of preventative antibiotics to farm animals through feed. Similar bans and restrictions in other countries could result in a material adverse effect on our sales of antibiotic products.

In recent years, the percentage of our total revenue from sales of shared-class antibiotics has declined, driven primarily by changing regulations in many markets, as well as market demand and our tiered approach to antibiotic stewardship, which has included removing growth promotion from labels and requiring veterinary oversight in the U.S. and other markets. Globally, during 2024, our revenue from shared-class antibiotics decreased 8% in comparison to 2023 and represented 9% of total revenue, while our revenue from animal-only antibiotics increased 4% in comparison to 2023 and represented 15% of total revenue. In 2024, 89% of our revenue from animal-only antibiotics resulted from the sale of ionophores. Ionophores are a special class of animal-only antimicrobials, and because of their animal-only designation, mode of action and spectrum of activity, to date their use has not been materially impacted by regulations or changing market demand in many international markets.

The impact of changes in regulations and market preferences regarding the use of antibiotics and productivity products in farm animals could have a material adverse effect on our business, financial condition and results of operations. If there is an increased public perception that consumption of food derived from animals that utilize our products poses a risk to human health, there may be a further decline in the production of those food products and, in turn, demand for our products. In addition, antibiotic resistance concerns will likely result in additional restrictions or bans, expanded regulations or public pressure to further reduce the use of antibiotics in farm animals, increased demand for antibiotic-free protein or changes in the market acceptance or regulatory treatment of ionophores, any of which could materially adversely affect our business, financial condition and results of operations.

An outbreak of infectious disease carried by farm animals could negatively affect the demand for, and sale and production of, our farm animal products.

Sales of our farm animal products could be materially adversely affected by a general outbreak of infectious disease, or an outbreak of disease carried by farm animals, which could lead to the widespread death or precautionary destruction of farm animals as well as the reduced consumption and demand for animal-derived protein. In addition, outbreaks of disease carried by farm animals may reduce regional or global sales of particular animal-derived food products or result in reduced exports of such products, either due to heightened export restrictions or import prohibitions, which may reduce demand for our farm animal products due to reduced herd or flock sizes.

In recent years, outbreaks of various diseases, including African Swine Fever, avian influenza, foot-and-mouth disease, bovine spongiform encephalopathy (otherwise known as BSE or “mad cow” disease) and porcine epidemic diarrhea virus (otherwise known as PEDV) have negatively impacted sales of our animal health products. The discovery of additional cases of any of these, or other diseases, may result in additional restrictions on animal-derived protein, reduced herd or flock sizes or reduced demand for animal-derived protein, any of which may have a material adverse effect on our business, financial condition and results of operations. In addition, the outbreak of any highly contagious disease near our main production sites could require us to immediately halt production of our products at such sites or force us to incur substantial expenses in procuring raw materials or products elsewhere.

Our R&D relies on evaluations of animals, which may become subject to bans, additional restrictive regulations or increased attention from activism movements.