UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q/A

(Amendment No. 1)

(Mark One)

☒QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES

EXCHANGE ACT OF 1934

For the quarterly period ended June 30, 2021

or

☐TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES

EXCHANGE ACT OF 1934

For the transition period from to

Commission File Number: 001-39292

Butterfly Network, Inc.

(Exact name of registrant as specified in its charter)

| | |

Delaware | | 84-4618156 |

(State or other jurisdiction of incorporation or organization) | | (IRS Employer Identification No.) |

| | |

530 Old Whitfield Street Guilford, Connecticut | | 06437 |

(Address of principal executive offices) | | (Zip Code) |

(203) 689-5650

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| | | | |

Title of each class | | Trading Symbol(s) | | Name of each exchange on which registered |

Class A common stock, $0.0001 Par Value Per Share | | BFLY | | The New York Stock Exchange |

Warrants to purchase one share of Class A common stock, each at an exercise price of $11.50 per share | | BFLY WS | | The New York Stock Exchange |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| | ||||

Large accelerated filer | ◻ | Accelerated filer | ◻ | | |

| | | | | |

Non-accelerated filer | ☒ | Smaller reporting company | ☒ | Emerging growth company | ☒ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

As of August 1, 2021, the registrant had 167,526,111 shares of Class A common stock outstanding and 26,426,937 shares of Class B common stock outstanding.

EXPLANATORY NOTE

Butterfly Network, Inc. (the “Company”) has determined that an administrative error occurred in connection with the filing of its Quarterly Report on Form 10-Q for the three months ended June 30, 2021 that was filed with the Securities and Exchange Commission (the “SEC”) on August 9, 2021 (the “Original Report”). While the Original Report was reviewed and approved by the appropriate officers of the Company prior to its filing with the SEC, the Company did not obtain manual or electronic signatures from the Company’s officers whose conformed signatures were set forth in the Original Report, as required by Rule 12b-11 and Rule 302(b) of Regulation S-T under the Securities Exchange Act of 1934, as amended (the “Signature Authorization Rules”). This Amendment No. 1 on Form 10-Q/A (the “Amendment No. 1”) to the Original Report is being filed in order to reflect that the Company has obtained the required signatures to this Amendment No. 1 from its officers, as required by the Signature Authorization Rules.

Except as described above, this Amendment No. 1 does not modify or update disclosure in, or exhibits to, the Original Report. Furthermore, this Amendment No. 1 does not change any previously reported financial results, nor does it reflect events occurring after the date of the Original Report. Information not affected by this Amendment No. 1 remains unchanged and reflects the disclosures made at the time the Original Report was made.

i

TABLE OF CONTENTS

|

| |

| Page |

|---|---|---|---|---|

| | | | |

| | | 3 | |

| | | | |

| | 4 | ||

| | | | |

| | 4 | ||

| | | | |

| | Condensed Consolidated Balance Sheets as of June 30, 2021 and December 31, 2020 (Unaudited) | | 4 |

| | | | |

| | | 5 | |

| | | | |

| | | 6 | |

| | | | |

| | | 7 | |

| | | | |

| | Notes to Condensed Consolidated Financial Statements (Unaudited) | | 8 |

| | | | |

| Management’s Discussion and Analysis of Financial Condition and Results of Operations | | 26 | |

| | | | |

| | 38 | ||

| | | | |

| | 39 | ||

| | | | |

| | 38 | ||

| | | | |

| | 40 | ||

| | | | |

| | 40 | ||

| | | | |

| | 41 | ||

| | | | |

| | 41 | ||

| | | | |

| | 41 | ||

| | | | |

| | 41 | ||

| | | | |

| | 41 | ||

| | | | |

| | | 44 | |

| | | | |

In this Quarterly Report on Form 10-Q, the terms “we,” “us,” “our,” the “Company” and “Butterfly” mean Butterfly Network, Inc. (formerly Longview Acquisition Corp.) and our subsidiaries. On February 12, 2021 (the “Closing Date”), Longview Acquisition Corp., a Delaware corporation (“Longview” and after the Business Combination described herein, the “Company”), consummated a business combination (the “Business Combination”) pursuant to the terms of the Business Combination Agreement, dated as of November 19, 2020 (the “Business Combination Agreement”), by and among Longview, Clay Merger Sub, Inc., a Delaware corporation (“Merger Sub”), and Butterfly Network, Inc., a Delaware corporation (“Legacy Butterfly”). Immediately upon the consummation of the Business Combination and the other transactions contemplated by the Business Combination Agreement (collectively, the “Transactions”, and such completion, the “Closing”), Merger Sub merged with and into Legacy Butterfly, with Legacy Butterfly surviving the Business Combination as a wholly-owned subsidiary of Longview (the “Merger”). In connection with the Transactions, Longview changed its name to “Butterfly Network, Inc.” and Legacy Butterfly changed its name to “BFLY Operations, Inc.”

ii

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This Quarterly Report on Form 10-Q includes forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), that relate to future events or our future financial performance regarding, among other things, the plans, strategies and prospects, both business and financial, of the Company. These statements are based on the beliefs and assumptions of the Company’s management team. Although the Company believes that its plans, intentions and expectations reflected in or suggested by these forward-looking statements are reasonable, the Company cannot assure you that it will achieve or realize these plans, intentions or expectations. Forward-looking statements are inherently subject to risks, uncertainties and assumptions. Generally, statements that are not historical facts, including statements concerning possible or assumed future actions, business strategies, events or results of operations, are forward-looking statements. These statements may be preceded by, followed by or include the words “believes,” “estimates,” “expects,” “projects,” “forecasts,” “may,” “will,” “should,” “seeks,” “plans,” “scheduled,” “anticipates” or “intends” or similar expressions. The forward-looking statements are based on projections prepared by, and are the responsibility of, the Company’s management. Forward-looking statements contained in this Quarterly Report on Form 10-Q include, but are not limited to, statements about:

| ● | our rapid growth may not be sustainable and depends on our ability to attract and retain customers; |

| ● | our business could be harmed if we fail to manage our growth effectively; |

| ● | the ability to recognize the anticipated benefits of the Business Combination, which may be affected by, among other things, competition and our ability to grow and manage growth profitably and retain our key employees; |

| ● | our projections are subject to risks, assumptions, estimates and uncertainties; |

| ● | our business is subject to a variety of U.S. and foreign laws, which are subject to change and could adversely affect our business; |

| ● | the success, cost and timing of our product development activities; |

| ● | the potential attributes and benefits of our products and services; |

| ● | our ability to obtain and maintain regulatory approval for our products, and any related restrictions and limitations of any authorized product; |

| ● | our ability to identify, in-license or acquire additional technology; |

| ● | our ability to maintain our existing license, manufacturing and supply agreements; |

| ● | our ability to compete with other companies currently marketing or engaged in the development of ultrasound imaging devices, many of which have greater financial and marketing resources than us; |

| ● | the size and growth potential of the markets for our products and services, and the ability of each to serve those markets, either alone or in partnership with others; |

| ● | the pricing of our products and services and reimbursement for medical procedures conducted using our products and services; |

| ● | changes in applicable laws or regulations; |

| ● | our ability to remediate the material weakness in our internal controls over financial reporting; |

| ● | our estimates regarding expenses, revenue, capital requirements and needs for additional financing; |

| ● | our ability to raise financing in the future; |

| ● | our financial performance; |

| ● | failure to protect or enforce our intellectual property rights could harm our business, results of operations and financial condition; |

| ● | the ability to maintain the listing of our Class A common stock on the New York Stock Exchange; |

| ● | economic downturns and political and market conditions beyond our control could adversely affect our business, financial condition and results of operations; and |

| ● | the impact of the COVID-19 pandemic on our business. |

These and other risks and uncertainties are described in greater detail under the caption “Risk Factors” in Item 1A of Part I of our Annual Report on Form 10-K for the fiscal year ended December 31, 2020, as amended, in Item 1A of Part II of this quarterly report, and in other filings that we make with the Securities and Exchange Commission, or SEC. The risks described under the heading “Risk Factors” are not exhaustive. New risk factors emerge from time to time, and it is not possible to predict all such risk factors, nor can the Company assess the impact of all such risk factors on its business or the extent to which any factor or combination of factors may cause actual results to differ materially from those contained in any forward-looking statements. Forward-looking statements are not guarantees of performance. You should not put undue reliance on these statements, which speak only as of the date hereof. All forward-looking statements attributable to the Company or persons acting on its behalf are expressly qualified in their entirety by the foregoing cautionary statements. The Company undertakes no obligations to update or revise publicly any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law.

3

PART I — FINANCIAL INFORMATION

Item 1. Financial Statements

BUTTERFLY NETWORK, INC.

CONDENSED CONSOLIDATED BALANCE SHEETS

(In thousands, except share and per share amounts)

(Unaudited)

| | | | | | | |

|

| June 30, |

| December 31, | | ||

|

| 2021 |

| 2020 |

| ||

Assets | |

| | |

| | |

Current assets: | |

| | |

| | |

Cash and cash equivalents | | $ | 19,605 | | $ | 60,206 | |

Marketable securities | | | 489,890 | | | — | |

Accounts receivable, net | |

| 7,809 | |

| 5,752 | |

Inventories | |

| 46,947 | |

| 25,805 | |

Current portion of vendor advances | | | 17,115 | | | 2,571 | |

Prepaid expenses and other current assets | |

| 9,294 | |

| 2,998 | |

Total current assets | | $ | 590,660 | | $ | 97,332 | |

Property and equipment, net | | | 7,436 | | | 6,870 | |

Non-current portion of vendor advances | |

| 26,365 | |

| 37,390 | |

Other non-current assets | |

| 6,802 | |

| 5,599 | |

Total assets | | $ | 631,263 | | $ | 147,191 | |

Liabilities, convertible preferred stock and stockholders’ equity (deficit) | |

| | | | | |

Current liabilities: | |

|

| |

|

| |

Accounts payable | | $ | 5,264 | | $ | 16,400 | |

Deferred revenue, current | |

| 10,894 | |

| 8,443 | |

Accrued purchase commitments, current | |

| 22,890 | |

| 22,890 | |

Accrued expenses and other current liabilities | | | 19,327 | | | 21,962 | |

Total current liabilities | | $ | 58,375 | | $ | 69,695 | |

Deferred revenue, non-current | | | 4,840 | | | 2,790 | |

Convertible debt | | | — | | | 49,528 | |

Loan payable | | | — | | | 4,366 | |

Warrant liabilities | | | 99,754 | | | — | |

Accrued purchase commitments, non-current | | | 19,660 | | | 19,660 | |

Other non-current liabilities | | | 2,282 | | | 2,146 | |

Total liabilities | | $ | 184,911 | | $ | 148,185 | |

Commitments and contingencies (Note 16) | | | | | | | |

Convertible preferred stock: | | | | | | | |

Convertible preferred stock (Series A, B, C and D) $.0001 par value with an aggregate liquidation preference of $0 and $383,829 at June 30, 2021 and December 31, 2020, respectively; 0 and 107,197,118 shares authorized, issued and outstanding at June 30, 2021 and December 31, 2020, respectively | | | — | | | 360,937 | |

Stockholders’ equity (deficit): | | | | | | | |

Class A common stock $.0001 par value; 600,000,000 and 116,289,600 shares authorized at June 30, 2021 and December 31, 2020, respectively; 167,477,126 and 6,593,291 shares issued and outstanding at June 30, 2021 and December 31, 2020, respectively | | | 17 | | | 1 | |

Class B common stock $.0001 par value; 27,000,000 and 26,946,089 shares authorized at June 30, 2021 and December 31, 2020, respectively; 26,426,937 and 0 shares issued and outstanding at June 30, 2021 and December 31, 2020, respectively | | | 3 | | | — | |

Additional paid-in capital | | | 844,770 | | | 32,874 | |

Accumulated deficit | | | (398,438) | | | (394,806) | |

Total stockholders’ equity (deficit) | | $ | 446,352 | | $ | (361,931) | |

Total liabilities, convertible preferred stock and stockholders’ equity (deficit) | | $ | 631,263 | | $ | 147,191 | |

The accompanying notes are an integral part of these condensed consolidated financial statements.

4

BUTTERFLY NETWORK, INC.

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS AND COMPREHENSIVE LOSS

(In thousands, except share and per share amounts)

(Unaudited)

| | | | | | | | | | | | | |

| | Three months ended June 30, | | Six months ended June 30, | | ||||||||

|

| 2021 |

| 2020 |

| 2021 |

| 2020 | | ||||

Revenue: | | |

| | |

| | |

| | |

| |

Product | | $ | 13,012 | | $ | 9,990 | | $ | 22,608 | | $ | 17,199 | |

Subscription | |

| 3,501 | |

| 1,802 | |

| 6,350 | |

| 3,263 | |

Total revenue | | $ | 16,513 | | $ | 11,792 | | $ | 28,958 | | $ | 20,462 | |

Cost of revenue: | |

|

| |

|

| |

|

| |

|

| |

Product | | | 7,858 | | | 11,385 | | | 13,506 | | | 20,647 | |

Subscription | |

| 435 | |

| 242 | |

| 814 | |

| 486 | |

Total cost of revenue | | $ | 8,293 | | $ | 11,627 | | $ | 14,320 | | $ | 21,133 | |

Gross profit | | $ | 8,220 | | $ | 165 | | $ | 14,638 | | $ | (671) | |

Operating expenses: | | | | | | | | | | | | | |

Research and development | | $ | 17,088 | | $ | 11,940 | | | 32,804 | | | 24,456 | |

Sales and marketing | |

| 10,540 | |

| 5,955 | |

| 20,347 | |

| 11,870 | |

General and administrative | |

| 17,279 | |

| 5,341 | |

| 51,920 | |

| 10,583 | |

Total operating expenses | |

| 44,907 | |

| 23,236 | |

| 105,071 | |

| 46,909 | |

Loss from operations | | $ | (36,687) | | $ | (23,071) | | $ | (90,433) | | $ | (47,580) | |

Interest income | | $ | 607 | | $ | 23 | | | 846 | | | 222 | |

Interest expense | |

| (7) | |

| (113) | |

| (645) | |

| (118) | |

Change in fair value of warrant liabilities | | | 33,458 | | | — | | | 87,570 | | | — | |

Other income (expense), net | |

| (262) | |

| (70) | |

| (895) | |

| (99) | |

Loss before provision for income taxes | | $ | (2,891) | | $ | (23,231) | | $ | (3,557) | | $ | (47,575) | |

Provision for income taxes | |

| 51 | |

| 10 | |

| 75 | |

| 20 | |

Net loss and comprehensive loss | | $ | (2,942) | | $ | (23,241) | | $ | (3,632) | | $ | (47,595) | |

Net loss per common share attributable to Class A and B common stockholders, basic and diluted | | $ | (0.02) | | $ | (3.85) | | $ | (0.02) | | $ | (7.92) | |

Weighted-average shares used to compute net loss per share attributable to Class A and B common stockholders, basic and diluted | | | 192,180,141 | | | 6,034,191 | | | 149,286,700 | | | 6,006,711 | |

The accompanying notes are an integral part of these condensed consolidated financial statements.

5

BUTTERFLY NETWORK, INC.

CONDENSED CONSOLIDATED STATEMENTS OF CHANGES IN CONVERTIBLE PREFERRED STOCK AND STOCKHOLDERS’ EQUITY (DEFICIT)

(In thousands, except share amounts)

(Unaudited)

| | | | | | | | | | | | | | | | | | | | | | | | | |

Three months ended June 30, 2020 | |||||||||||||||||||||||||

|

| |

|

| |

|

| |

|

| |

| |

|

| |

|

| |

|

| |

|

| |

| | Convertible | | | Class A | | Class B | | | | | | | | | | |||||||||

| | Preferred | | | Common | | Common | | Additional | | | | | Total | |||||||||||

| | Stock | | | Stock | | Stock | | Paid-In | | Accumulated | | Stockholders’ | ||||||||||||

| | Shares | | Amount | | | Shares | | Amount | | Shares | | Amount | | Capital | | Deficit | | Equity (Deficit) | ||||||

March 31, 2020 | | 107,197,118 | | $ | 360,937 | | | 6,013,465 | | $ | 1 | | — | | $ | — | | $ | 22,633 | | $ | (256,415) | | $ | (233,781) |

Net loss | | — | | | — | | | — | | | — | | — | | | — | | | — | | | (23,241) | | | (23,241) |

Common stock issued upon exercise of stock options | | — | | | — | | | 32,393 | | | — | | — | | | — | | | 70 | | | — | | | 70 |

Stock-based compensation expense | | — | | | — | | | — | | | — | | — | | | — | | | 2,690 | | | — | | | 2,690 |

June 30, 2020 | | 107,197,118 | | $ | 360,937 | | | 6,045,858 | | $ | 1 | | — | | $ | — | | $ | 25,393 | | $ | (279,656) | | $ | (254,262) |

| | | | | | | | | | | | | | | | | | | | | | | | | |

Six months ended June 30, 2020 | |||||||||||||||||||||||||

|

| |

|

| |

|

| |

|

| |

| |

|

| |

|

| |

|

| |

|

| |

| | Convertible | | | Class A | | Class B | | | | | | | | | | |||||||||

| | Preferred | | | Common | | Common | | Additional | | | | | Total | |||||||||||

| | Stock | | | Stock | | Stock | | Paid-In | | Accumulated | | Stockholders’ | ||||||||||||

| | Shares | | Amount | | | Shares | | Amount | | Shares | | Amount | | Capital | | Deficit | | Equity (Deficit) | ||||||

December 31, 2019 | | 107,197,118 | | $ | 360,937 | | | 5,939,950 | | $ | 1 | | — | | $ | — | | $ | 19,782 | | $ | (232,061) | | $ | (212,278) |

Net loss | | — | | | — | | | — | | | — | | — | | | — | | | — | | | (47,595) | | | (47,595) |

Common stock issued upon exercise of stock options | | — | | | — | | | 105,908 | | | — | | — | | | — | | | 224 | | | — | | | 224 |

Stock-based compensation expense | | — | | | — | | | — | | | — | | — | | | — | | | 5,387 | | | — | | | 5,387 |

June 30, 2020 | | 107,197,118 | | $ | 360,937 | | | 6,045,858 | | $ | 1 | | — | | $ | — | | $ | 25,393 | | $ | (279,656) | | $ | (254,262) |

| | | | | | | | | | | | | | | | | | | | | | | | | |

Three months ended June 30, 2021 | |||||||||||||||||||||||||

|

| |

|

| |

|

| |

|

| |

| |

|

| |

|

| |

|

| |

|

| |

| | Convertible | | | Class A | | Class B | | | | | | | | | | |||||||||

| | Preferred | | | Common | | Common | | Additional | | | | | Total | |||||||||||

| | Stock | | | Stock | | Stock | | Paid-In | | Accumulated | | Stockholders’ | ||||||||||||

| | Shares | | Amount | | | Shares | | Amount | | Shares | | Amount | | Capital | | Deficit | | Equity (Deficit) | ||||||

March 31, 2021 | | — | | $ | — | | | 164,862,470 | | $ | 16 | | 26,426,937 | | $ | 3 | | $ | 831,640 | | $ | (395,496) | | $ | 436,163 |

Net loss | | — | | | — | | | — | | | — | | — | | | — | | | — | | | (2,942) | | | (2,942) |

Common stock issued upon exercise of stock options and warrants | | — | | | — | | | 2,147,422 | | | 1 | | — | | | — | | | 5,375 | | | — | | | 5,376 |

Common stock issued upon vesting of restricted stock units | | — | | | — | | | 467,234 | | | — | | — | | | — | | | — | | | — | | | — |

Stock-based compensation expense | | — | | | — | | | — | | | — | | — | | | — | | | 7,755 | | | — | | | 7,755 |

June 30, 2021 | | — | | $ | — | | | 167,477,126 | | $ | 17 | | 26,426,937 | | $ | 3 | | $ | 844,770 | | $ | (398,438) | | $ | 446,352 |

| | | | | | | | | | | | | | | | | | | | | | | | | |

Six months ended June 30, 2021 | |||||||||||||||||||||||||

| | | | | | | | | | | | | | | | | | | | | | | | | |

| | Convertible | | | Class A | | Class B | | | | | | | | | | |||||||||

| | Preferred | | | Common | | Common | | Additional | | | | | Total | |||||||||||

| | Stock | | | Stock | | Stock | | Paid-In | | Accumulated | | Stockholders’ | ||||||||||||

| | Shares | | Amount | | | Shares | | Amount | | Shares | | Amount | | Capital | | Deficit | | Equity (Deficit) | ||||||

December 31, 2020 | | 107,197,118 | | $ | 360,937 | | | 6,593,291 | | $ | 1 | | — | | $ | — | | $ | 32,874 | | $ | (394,806) | | $ | (361,931) |

Net loss | | — | | | — | | | — | | | — | | — | | | — | | | — | | | (3,632) | | | (3,632) |

Common stock issued upon exercise of stock options and warrants | | — | | | — | | | 5,302,472 | | | 1 | | — | | | — | | | 11,688 | | | — | | | 11,689 |

Common stock issued upon vesting of restricted stock units | | — | | | — | | | 467,234 | | | — | | — | | | — | | | — | | | — | | | — |

Conversion of convertible preferred stock | | (107,197,118) | | | (360,937) | | | 80,770,178 | | | 8 | | 26,426,937 | | | 3 | | | 360,926 | | | — | | | 360,937 |

Conversion of convertible debt | | — | | | — | | | 5,115,140 | | | 1 | | — | | | — | | | 49,916 | | | — | | | 49,917 |

Net equity infusion from the Business Combination | | — | | | — | | | 69,228,811 | | | 6 | | — | | | — | | | 361,281 | | | — | | | 361,287 |

Stock-based compensation expense | | — | | | — | | | — | | | — | | — | | | — | | | 28,085 | | | — | | | 28,085 |

June 30, 2021 | | — | | $ | — | | | 167,477,126 | | $ | 17 | | 26,426,937 | | $ | 3 | | $ | 844,770 | | $ | (398,438) | | $ | 446,352 |

The accompanying notes are an integral part of these condensed consolidated financial statements.

6

BUTTERFLY NETWORK, INC.

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(In thousands)

(Unaudited)

| | | | | | |

| | Six months ended June 30, | ||||

| | 2021 | | 2020 | ||

Cash flows from operating activities: | | | | | | |

Net loss |

| $ | (3,632) |

| $ | (47,595) |

Adjustments to reconcile net loss to net cash used in operating activities: | |

| | |

| |

Depreciation and amortization | |

| 915 | |

| 593 |

Non-cash interest expense on convertible debt | | | 389 | | | 113 |

Stock-based compensation expense | | | 28,035 | | | 5,345 |

Change in fair value of warrant liabilities | | | (87,570) | | | 0 |

Other | | | 498 | | | 1,000 |

Changes in operating assets and liabilities: | |

| | | | |

Accounts receivable | | | (1,979) | | | (3,198) |

Inventories | |

| (21,113) | |

| (2,994) |

Prepaid expenses and other assets | | | (6,352) | | | 535 |

Vendor advances | | | (3,519) | | | 2,281 |

Accounts payable | | | (11,088) | | | 1,630 |

Deferred revenue | | | 4,501 | | | 2,928 |

Accrued expenses and other liabilities | | | 986 | | | (44) |

Net cash used in operating activities | | $ | (99,929) | | $ | (39,406) |

| | | | | | |

Cash flows from investing activities: | |

|

| |

|

|

Purchases of marketable securities | | | (692,514) | | | 0 |

Sales of marketable securities | | | 202,000 | | | 0 |

Purchases of property and equipment | |

| (1,829) | |

| (1,908) |

Net cash used in investing activities | | $ | (492,343) | | $ | (1,908) |

| |

| | |

| |

Cash flows from financing activities: | |

| | |

| |

Proceeds from exercise of stock options and warrants | |

| 11,686 | |

| 224 |

Net proceeds from equity infusion from the Business Combination | | | 548,403 | | | 0 |

Proceeds from loan payable | |

| 0 | | | 4,366 |

Proceeds from issuance of convertible debt | |

| 0 | | | 20,150 |

Payment of loan payable | | | (4,366) | | | 0 |

Payments of debt issuance costs | | | (52) | | | 0 |

Net cash provided by financing activities | | $ | 555,671 | | $ | 24,740 |

Net (decrease) increase in cash, cash equivalents and restricted cash | | $ | (36,601) | | $ | (16,574) |

Cash, cash equivalents and restricted cash, beginning of period | | | 60,206 | | | 90,002 |

Cash, cash equivalents and restricted cash, end of period | | $ | 23,605 | | $ | 73,428 |

| | | | | | |

Reconciliation of cash, cash equivalents and restricted cash reported within the condensed consolidated balance sheets | | | | | | |

Cash and cash equivalents | | $ | 19,605 | | $ | 73,428 |

Restricted cash | | | 4,000 | | | 0 |

Total cash, cash equivalents and restricted cash shown in the statement of cash flows | | $ | 23,605 | | $ | 73,428 |

The accompanying notes are an integral part of these condensed consolidated financial statements.

7

BUTTERFLY NETWORK, INC.

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

Note 1. Organization and Description of Business

Butterfly Network, Inc., formerly known as Longview Acquisition Corp. (the “Company” or “Butterfly”) was incorporated in Delaware on February 4, 2020. The Company’s legal name became Butterfly Network, Inc. following the closing of the business combination discussed in Note 3 “Business Combination”. The prior period financial information represents the financial results and condition of BFLY Operations, Inc.

The Company is an innovative digital health business whose mission is to democratize healthcare by making medical imaging accessible to everyone around the world. Butterfly’s solution uses a unique combination of software and hardware technology to enable medical imaging to drive more clinical insight at patient point-of-care. The hardware platform works alongside cloud-based software that is intended to make the product easy to use, integrate with the clinical workflow and be accessible on a user’s smartphone, tablet, and/or healthcare enterprise systems.

The Company operates wholly-owned subsidiaries in Australia, Germany, the Netherlands, the United Kingdom and Taiwan.

Note 2. Summary of Significant Accounting Policies

Basis of Presentation and Principles of Consolidation

The accompanying condensed consolidated financial statements include the accounts of Butterfly Network, Inc. and its wholly-owned subsidiaries and have been prepared in accordance with accounting principles generally accepted in the United States of America (“U.S. GAAP”) and pursuant to the accounting disclosure rules and regulations of the Securities and Exchange Commission (the “SEC”) regarding interim financial reporting. Certain information and note disclosures normally included in the financial statements prepared in accordance with U.S. GAAP have been condensed or omitted pursuant to such rules and regulations. Therefore, these condensed consolidated financial statements should be read in conjunction with the consolidated financial statements and notes included in the Company’s audited consolidated financial statements as of and for the years ended December 31, 2020 and 2019. All intercompany balances and transactions are eliminated upon consolidation.

The condensed consolidated balance sheet as of December 31, 2020, included herein, was derived from the audited consolidated financial statements as of that date, but does not include all disclosures, including certain notes required by U.S. GAAP, required on an annual reporting basis. Certain prior period amounts have been reclassified to conform to the current period presentation.

In the opinion of management, the accompanying condensed consolidated financial statements reflect all normal recurring adjustments necessary to present fairly the financial position, results of operations, and cash flows for the interim periods. The results for the three and six months ended June 30, 2021 are not necessarily indicative of the results to be expected for any subsequent quarter, the year ending December 31, 2021, or any other period.

Except as described elsewhere in this Note 2 including under the heading “Recent Accounting Pronouncements Adopted” and Note 3 “Business Combination”, there have been no material changes to the Company’s significant accounting policies as described in the audited consolidated financial statements as of December 31, 2020 and 2019.

COVID-19 Outbreak

The COVID-19 pandemic that began in 2020 has created significant global economic uncertainty and has impacted the Company’s operating results, financial condition and cash flows. The full extent to which the COVID-19 pandemic will directly or indirectly impact the Company’s business, results of operations and financial condition will depend on future developments that are highly uncertain, including those that result from new information that may emerge concerning COVID-19, the actions taken to contain or treat COVID-19 and the economic impacts of COVID-19.

8

The estimates of the impact on the Company’s business may change based on new information that may emerge concerning COVID-19, the actions to contain it or treat its impact and the economic impact on local, regional, national and international markets. The Company has not incurred any significant impairment losses in the carrying values of its assets as a result of the COVID-19 pandemic and is not aware of any specific related event or circumstance that would require the Company to revise the estimates reflected in its condensed consolidated financial statements.

Although the Company has incurred recurring losses in each year since inception, the Company expects its cash and cash equivalents and marketable securities will be sufficient to fund operations for at least the next twelve months

Concentration of Credit Risk

Financial instruments that potentially subject the Company to concentration of credit risk consist principally of cash and cash equivalents, marketable securities and accounts receivable. At June 30, 2021, substantially all of the Company’s marketable securities were invested in mutual funds with one financial institution. At December 31, 2020, substantially all of the Company’s cash and cash equivalents were invested in money market accounts at one financial institution. The Company also maintains balances in various operating accounts above federally insured limits. The Company has not experienced significant losses on such accounts and does not believe it is exposed to any significant credit risk on cash and cash equivalents and marketable securities.

As of June 30, 2021 and December 31, 2020, 0 customer accounts for more than 10% of the Company’s accounts receivable. For the three and six months ended June 30, 2021 and 2020, 0 customer accounts for more than 10% of the total revenues.

Segment Information

The Company’s Chief Operating Decision Maker, its Chief Executive Officer (“CEO”), reviews the financial information presented on a consolidated basis for purposes of allocating resources and evaluating its financial performance. Accordingly, the Company has determined that it operates in a single reportable segment. Substantially all of the Company’s long-lived assets are located in the United States. Since the Company operates in 1 operating segment, all required financial segment information can be found in the condensed consolidated financial statements.

Use of Estimates

The Company makes estimates and assumptions about future events that affect the amounts reported in its condensed consolidated financial statements and accompanying notes. Future events and their effects cannot be determined with certainty. On an ongoing basis, management evaluates these estimates, judgments and assumptions.

The Company bases its estimates on historical and anticipated results and trends and on various other assumptions that the Company believes are reasonable under the circumstances, including assumptions as to future events. Changes in estimates are recorded in the period in which they become known. Actual results could differ from those estimates, and any such differences may be material to the Company’s condensed consolidated financial statements. Except with respect to estimates related to the warrant liabilities, there have been no material changes to the Company’s use of estimates as described in the audited consolidated financial statements as of December 31, 2020.

Investments in Marketable Securities

The Company’s investments in marketable securities are ownership interests in fixed income mutual funds. The equity securities are stated at fair value, as determined by quoted market prices. As the securities have readily determinable fair value, unrealized gains and losses are reported as other income (expense), net on the condensed consolidated statements of operations and comprehensive loss. Subsequent gains or losses realized upon redemption or sale of these securities are also recorded as other income (expense), net on the condensed consolidated statements of operations and comprehensive loss. The Company considers all of its investments in marketable securities as available for use in current operations and therefore classifies these securities within current assets on the condensed consolidated balance sheets. For the three and six months ended June 30, 2021, the Company recognized $0.2 million and $0.5 million, respectively, of unrealized losses that relate to equity securities still held as of June 30, 2021.

9

Restricted Cash

Restricted cash includes deposits in financial institutions used to secure a lease agreement. The Company classified the amounts within other non-current assets as the deposit is used to secure a long-term lease. The amount shown as restricted cash is included with cash and cash equivalents when reconciling the beginning-of-period and end-of-period total amounts shown in the condensed consolidated statement of cash flows.

Warrant Liability

The Company’s outstanding warrants include publicly-traded warrants (the “Public Warrants”) which were issued as one-third of a warrant per unit during the Company’s initial public offering on May 26, 2020 (the “IPO”) and warrants sold in a private placement to Longview’s sponsor (the “Private Warrants”). The Company evaluated its warrants under ASC 815-40, Derivatives and Hedging—Contracts in Entity’s Own Equity, and concluded that they do not meet the criteria to be classified in stockholders’ equity. Since the Public Warrants and Private Warrants meet the definition of a derivative under ASC 815, the Company recorded these warrants as long-term liabilities on the balance sheet at fair value upon the Closing of the Business Combination, with subsequent changes in their respective fair values recognized in the condensed consolidated statements of operations and comprehensive loss at each reporting date.

Recent Accounting Pronouncements Adopted

In August 2018, the Financial Accounting Standards Board (“FASB”) issued ASU 2018-15, Customer’s Accounting for Implementation Costs Incurred in a Cloud Computing Arrangement that Is a Service Contract (Topic 350-40), which aligns the requirements for capitalizing implementation costs incurred in a hosting arrangement that is a service contract with the requirements for capitalizing implementation costs incurred to develop or obtain internal-use software (and hosting arrangements that include an internal-use software license). As a result, eligible implementation costs incurred in a cloud computing arrangement that is a service contract are capitalized as prepaid expenses and other current assets on the balance sheet, recognized on a straight-line basis over its life in the statement of operations and comprehensive loss in the same line item as the fees for the associated arrangement, and the related activity is generally classified as an operating activity in the statement of cash flows. The Company prospectively adopted such guidance on January 1, 2021 and there was no material effect of adoption on the condensed consolidated financial statements as of and for the three and six months ended June 30, 2021.

Recent Accounting Pronouncements Issued but Not Yet Adopted

In February 2016, the FASB issued ASU 2016-02, Leases (Topic 842) which outlines a comprehensive lease accounting model and supersedes the prior lease guidance. The new guidance requires lessees to recognize almost all of their leases on the balance sheet by recording a lease liability and corresponding right-of-use assets. It also changes the definition of a lease and expands the disclosure requirements of lease arrangements. As per the latest ASU 2020-05 issued by the FASB, entities that have not yet issued or made available for issuance their financial statements as of June 3, 2020 can defer the new guidance for one year. For public entities, this guidance was effective for annual reporting periods beginning January 1, 2019, including interim periods within that annual reporting period. For other entities, this guidance is effective for the annual reporting period beginning January 1, 2022, and interim reporting periods within annual reporting periods beginning January 1, 2023. This will require application of the new accounting guidance at the beginning of the earliest comparative period presented in the year of adoption. The impact of the Company's adoption of Topic 842 to the consolidated financial statements will be to recognize the operating lease commitments as operating lease liabilities and right-of-use assets upon adoption, which will result in an increase in the assets and liabilities recorded on the balance sheet. The Company is continuing its assessment, which may identify additional impacts Topic 842 will have on the condensed consolidated financial statements and disclosures.

In June 2016, the FASB issued ASU 2016-13, Financial Instruments — Credit Losses (Topic 326): Measurement of Credit Losses on Financial Instruments. ASU 2016-13 requires an entity to utilize a new impairment model known as the current expected credit loss (“CECL”) model to estimate its lifetime “expected credit loss” and record an allowance that, when deducted from the amortized cost basis of the financial asset, presents the net amount expected to be collected on the financial asset. The CECL model is expected to result in more timely recognition of credit losses. ASU 2016-13 also requires new disclosures for financial assets measured at amortized cost, loans, and available-for-sale debt securities. For

10

public entities, this guidance was effective for annual reporting periods beginning January 1, 2020, including interim periods within that annual reporting period. For other entities, this guidance is effective for the annual reporting period beginning January 1, 2023, including interim periods within that annual reporting period. The standard will apply as a cumulative-effect adjustment to retained earnings as of the beginning of the first reporting period in which the guidance is adopted. The Company is in the process of evaluating the impact the adoption of this pronouncement will have on the Company’s condensed consolidated financial statements and disclosures.

Note 3. Business Combination

On February 12, 2021 (the “Closing Date”), the Company consummated the previously announced business combination (the “Business Combination”) pursuant to the terms of the Business Combination Agreement, dated as of November 19, 2020 (the “Business Combination Agreement”), by and among Longview, Clay Merger Sub, Inc., a Delaware corporation incorporated on November 12, 2020 (“Merger Sub”), and Butterfly Network, Inc., a Delaware corporation (“Legacy Butterfly”).

Immediately upon the consummation of the Business Combination and the other transactions contemplated by the Business Combination Agreement (collectively, the “Transactions”, and such completion, the “Closing”), Merger Sub merged with and into Legacy Butterfly, with Legacy Butterfly surviving the Business Combination as a wholly-owned subsidiary of Longview (the “Merger”). In connection with the Transactions, Longview changed its name to “Butterfly Network, Inc.” and Legacy Butterfly changed its name to “BFLY Operations, Inc.”

The Merger is accounted for as a reverse recapitalization in accordance with U.S. GAAP primarily due to the fact that Legacy Butterfly stockholders continue to control the Company following the closing of the Business Combination. Under this method of accounting, Longview is treated as the “acquired” company for accounting purposes and the Business Combination is treated as the equivalent of Legacy Butterfly issuing stock for the net assets of Longview, accompanied by a recapitalization. The net assets of Longview will be stated at historical cost, with no goodwill or other intangible assets recorded. Reported shares and earnings per share available to holders of the Company’s capital stock and equity awards prior to the Business Combination have been retroactively restated reflecting the exchange ratio established pursuant to the Business Combination Agreement (1:1.0383).

Pursuant to the Merger, at the Effective Time of the Merger (the “Effective Time”):

| • | each share of Legacy Butterfly capital stock (other than the Legacy Butterfly Series A preferred stock) that was issued and outstanding immediately prior to the Effective Time was automatically canceled and converted into the right to receive 1.0383 shares of the Company’s Class A common stock, rounded down to the nearest whole number of shares; |

| • | each share of Legacy Butterfly Series A preferred stock that was issued and outstanding immediately prior to the Effective Time was automatically canceled and converted into the right to receive 1.0383 shares of the Company’s Class B common stock, rounded down to the nearest whole number of shares; |

| ||

| • | each option to purchase shares of Legacy Butterfly common stock, whether vested or unvested, that was outstanding and unexercised as of immediately prior to the Effective Time was assumed by the Company and became an option (vested or unvested, as applicable) to purchase a number of shares of the Company’s Class A common stock equal to the number of shares of Legacy Butterfly common stock subject to such option immediately prior to the Effective Time multiplied by 1.0383, rounded down to the nearest whole number of shares, at an exercise price per share equal to the exercise price per share of such option immediately prior to the Effective Time divided by 1.0383 and rounded up to the nearest whole cent;

|

11

| • | each Legacy Butterfly restricted stock unit outstanding immediately prior to the Effective Time was assumed by the Company and became a restricted stock unit with respect to a number of shares of the Company’s Class A common stock, rounded to the nearest whole share, equal to the number of shares of Legacy Butterfly common stock subject to such Legacy Butterfly restricted stock unit immediately prior to the Effective Time multiplied by 1.0383; and |

| • | the principal amount plus accrued but unpaid interest, if any, on the Legacy Butterfly convertible notes outstanding as of immediately prior to the Effective Time was automatically canceled and converted into the right to receive shares of the Company’s Class A common stock, with such shares of the Company’s Class A common stock calculated by dividing the outstanding principal plus accrued interest, if any, of each Legacy Butterfly convertible note by $10.00, rounded down to the nearest whole number of shares. |

In addition, on February 12, 2021, Longview filed the Second Amended and Restated Certificate of Incorporation (the “Restated Certificate”) with the Secretary of State of the State of Delaware, which became effective simultaneously with the Effective Time. As a consequence of filing the Restated Certificate, the Company adopted a dual class structure, comprised of the Company’s Class A common stock, which is entitled to 1 vote per share, and the Company’s Class B common stock, which is entitled to 20 votes per share. The Company’s Class B common stock is subject to a “sunset” provision if Jonathan M. Rothberg, Ph.D., the founder of Legacy Butterfly and Chairman of the Company (“Dr. Rothberg”), and other permitted holders of the Company’s Class B common stock collectively cease to beneficially own at least 20 percent (20%) of the number of shares of the Company’s Class B common stock (as such number of shares is equitably adjusted in respect of any reclassification, stock dividend, subdivision, combination or recapitalization of the Company’s Class B common stock) collectively held by Dr. Rothberg and permitted transferees of the Company’s Class B common stock as of the Effective Time.

In addition, concurrently with the execution of the Business Combination Agreement, on November 19, 2020, Longview entered into subscription agreements (the “Subscription Agreements”) with certain institutional investors (the “PIPE Investors”), pursuant to which the PIPE Investors purchased, immediately prior to the Closing, an aggregate of 17,500,000 shares of Longview Class A common stock at a purchase price of $10.00 per share (the “PIPE Financing”).

The total number of shares of the Company’s Class A common stock outstanding immediately following the Closing was approximately 164,862,470, comprising:

59 | ||

| • | 95,633,659 shares of the Company’s Class A common stock issued to Legacy Butterfly stockholders (other than certain holders of Legacy Butterfly Series A preferred stock) and holders of Legacy Butterfly convertible notes in the Merger; |

| • | 17,500,000 shares of the Company’s Class A common stock issued in connection with the Closing to the PIPE Investors pursuant to the PIPE Financing; |

| ||

| • | 10,350,000 shares of the Company’s Class A common stock issued to holders of shares of Longview Class B common stock outstanding at the Effective Time; and

|

| • | 41,378,811 shares of the Company’s Class A common stock held by holders of Longview Class A common stock outstanding at the Effective Time. |

The total number of shares of the Company’s Class B common stock issued at the Closing was approximately 26,426,937. Immediately following the Closing, Dr. Rothberg held approximately 76.2% of the combined voting power of the Company. Accordingly, Dr. Rothberg and his permitted transferees control the Company and the Company is a

12

controlled company within the meaning of the corporate governance standards of the New York Stock Exchange (the “NYSE”).

The most significant change in the post-combination Company’s reported financial position and results was an increase in cash of $589.5 million. The Company as the accounting acquirer incurred $11.4 million in transaction costs relating to the Business Combination, which has been offset against the gross proceeds recorded in additional paid-in capital in the condensed consolidated statements of changes in convertible preferred stock and stockholders’ equity (deficit). The Company on the date of Closing used proceeds of the Transactions to pay off $30.9 million, representing all significant liabilities of the acquiree excluding the warrant liability. As of the date of the Closing, the Company recorded net liabilities of $186.5 million with a corresponding offset to additional paid-in capital. The net liabilities include warrant liabilities of $187.3 million and other insignificant assets and liabilities. The Company received proceeds of $0.6 million related to other transactions that occurred at the same time as the Business Combination.

Note 4. Revenue Recognition

Disaggregation of Revenue

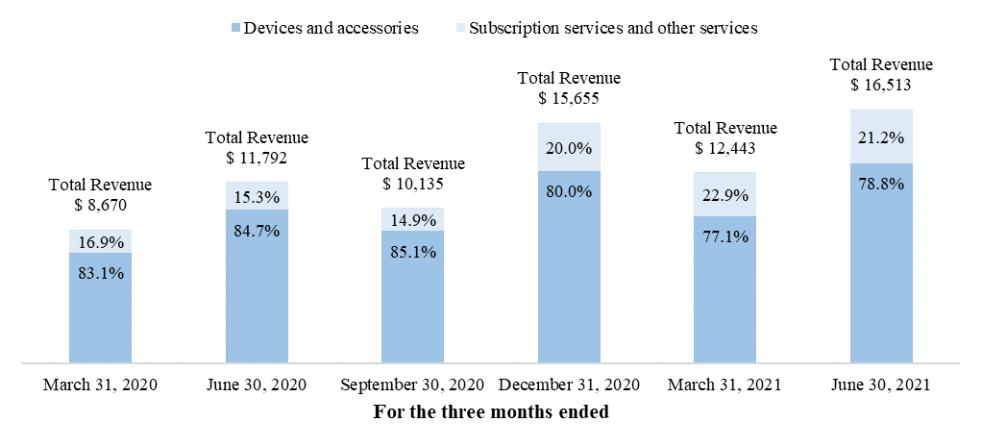

The Company disaggregates revenue from contracts with customers by product type and by geographical market. The Company believes that these categories aggregate the payor types by nature, amount, timing and uncertainty of their revenue streams. The following table summarizes the Company’s disaggregated revenues (in thousands) for the three and six months ended June 30, 2021 and 2020:

| | | | | | | | | | | | | | | |

| | Pattern of | | Three months ended June 30, | | Six months ended June 30, | | ||||||||

| | Recognition | | 2021 | | 2020 | | 2021 | | 2020 | | ||||

By Product Type: |

| |

|

| |

|

| |

|

| |

|

| |

|

Devices and accessories | | Point-in-time | | $ | 13,012 | | $ | 9,990 | | $ | 22,608 | | $ | 17,199 | |

Subscription services and other services | | Over time | | | 3,501 | | | 1,802 | | | 6,350 | | | 3,263 | |

Total revenue | | | | $ | 16,513 | | $ | 11,792 | | $ | 28,958 | | $ | 20,462 | |

By Geographical Market: | | | | | | | | | | | | | | | |

United States | | | | $ | 11,146 | | $ | 8,216 | | $ | 20,042 | | $ | 14,568 | |

International | | | | | 5,368 | | | 3,576 | | | 8,917 | | | 5,894 | |

Total revenue | | | | $ | 16,513 | | $ | 11,792 | | $ | 28,958 | | $ | 20,462 | |

Contract Balances

Contract balances represent amounts presented in the condensed consolidated balance sheets when either the Company has transferred goods or services to the customer, or the customer has paid consideration to the Company under the contract. These contract balances include trade accounts receivable and deferred revenue. Deferred revenue represents cash consideration received from customers for services that are transferred to the customer over the respective subscription period. The accounts receivable balances represent amounts billed to customers for goods and services where the Company has an unconditional right to payment of the amount billed.

The following table provides information about receivables and deferred revenue from contracts with customers (in thousands):

| | | | | | |

|

| June 30, |

| December 31, | ||

| | 2021 | | 2020 | ||

Accounts receivable, net | | $ | 7,809 | | $ | 5,752 |

Deferred revenue, current | |

| 10,894 | |

| 8,443 |

Deferred revenue, non-current | |

| 4,840 | |

| 2,790 |

The Company recognizes a receivable when it has an unconditional right to payment, and payment terms are typically 30 days for all product and service sales. The allowance for doubtful accounts was $0.4 million and $0.6 million as of June 30, 2021 and December 31, 2020, respectively.

13

The amount of revenue recognized during the three months ended June 30, 2021 and 2020 that was included in the deferred revenue balance at the beginning of the period was $3.6 million and $0.9 million, respectively. The amount of revenue recognized during the six months ended June 30, 2021 and 2020 that was included in the deferred revenue balance at the beginning of the period was $5.6 million and $1.9 million, respectively.

The Company incurs incremental costs of obtaining contracts and costs of fulfilling contracts with customers. The amount of costs capitalized during the three and six months ended June 30, 2021 and 2020 was not significant.

Transaction Price Allocated to Remaining Performance Obligations

On June 30, 2021, the Company had $20.6 million of remaining performance obligations. The Company expects to recognize 64% of its remaining performance obligations as revenue in the next twelve months, and an additional 36% thereafter.

Note 5. Fair Value of Financial Instruments

Fair value estimates of financial instruments are made at a specific point in time, based on relevant information about financial markets and specific financial instruments. As these estimates are subjective in nature, involving uncertainties and matters of significant judgment, they cannot be determined with precision. Changes in assumptions can significantly affect estimated fair value.

The Company measures fair value as the price that would be received to sell an asset or paid to transfer a liability (an exit price) in an orderly transaction between market participants at the reporting date. The Company utilizes a three-tier hierarchy, which prioritizes the inputs used in the valuation methodologies in measuring fair value:

| ● | Level 1 — Valuations based on quoted prices in active markets for identical assets or liabilities that an entity has the ability to access. |

| ● | Level 2 — Valuations based on quoted prices for similar assets or liabilities, quoted prices for identical assets or liabilities in markets that are not active, or other inputs that are observable or can be corroborated by observable data for substantially the full term of the assets or liabilities. |

| ● | Level 3 — Valuations based on inputs that are supported by little or no market activity and that are significant to the fair value of the assets or liabilities. The Company has no assets or liabilities valued with Level 3 inputs. |

The carrying value of cash and cash equivalents, accounts receivable, accounts payable and accrued liabilities approximates their fair values due to the short-term or on-demand nature of these instruments.

There were no transfers between fair value measurement levels during the periods ended June 30, 2021 and December 31, 2020.

The Company determined the fair value of its Public Warrants as Level 1 financial instruments, as they are traded in active markets. Because any transfer of Private Warrants from the initial holder of the Private Warrants would result in the Private Warrants having substantially the same terms as the Public Warrants, management determined that the fair value of each Private Warrant is the same as that of a Public Warrant. Accordingly, the Private Warrants are classified as Level 2 financial instruments.

14

The following table summarizes the Company’s assets and liabilities that are measured at fair value on a recurring basis, by level, within the fair value hierarchy (in thousands):

| | | | | | | | | | | | |

| | | | | Fair Value Measurement Level | |||||||

| | Total | | Level 1 | | Level 2 | | Level 3 | ||||

June 30, 2021: |

| |

|

| |

|

| |

|

| |

|

Marketable securities: |

| |

|

| | |

| |

|

| |

|

Mutual funds | | $ | 489,890 | | $ | 489,890 | | $ | — | | $ | — |

Total assets at fair value on a recurring basis | | $ | 489,890 | | $ | 489,890 | | $ | — | | $ | — |

| | | | | | | | | | | | |

Warrants: | | | | | | | | | | | | |

Public Warrants | | $ | 66,652 | | $ | 66,652 | | $ | — | | $ | — |

Private Warrants | | | 33,102 | | | — | | | 33,102 | | | — |

Total liabilities at fair value on a recurring basis | | $ | 99,754 | | $ | 66,652 | | $ | 33,102 | | $ | — |

The Company did not have any assets or liabilities similar to those above requiring fair value measurement at December 31, 2020.

Note 6. Inventories

A summary of inventories is as follows at June 30, 2021 and December 31, 2020 (in thousands):

| | | | | | |

|

| June 30, |

| December 31, | ||

|

| 2021 |

| 2020 | ||

Raw materials | | $ | 32,020 |

| | 7,688 |

Work-in-progress | |

| 776 |

| | 865 |

Finished goods | |

| 14,151 |

| | 17,252 |

Total inventories | | $ | 46,947 | | $ | 25,805 |

Work-in-progress represents inventory items in intermediate stages of production by third-party manufacturers. For the three and six months ended June 30, 2021, net realizable value inventory adjustments and excess and obsolete inventory charges were not significant and were recognized in product cost of revenues. For the three and six months ended June 30, 2020, net realizable value inventory adjustments and excess and obsolete inventory charges were $0.7 million and $0.7 million, respectively, and were recognized in product cost of revenues.

Note 7. Non-Current Assets

The Company’s property and equipment, net consists of the following at June 30, 2021 and December 31, 2020 (in thousands):

| | | | | | |

| | June 30, | | December 31, | ||

|

| 2021 |

| 2020 | ||

Property and equipment, historical cost | | $ | 11,754 | | $ | 10,268 |

Less: accumulated depreciation and amortization | |

| (4,318) | |

| (3,398) |

Property and equipment, net | | $ | 7,436 | | $ | 6,870 |

Other non-current assets consist of the following at June 30, 2021 and December 31, 2020 (in thousands):

| | | | | | |

|

| June 30, |

| December 31, | ||

|

| 2021 |

| 2020 | ||

Security deposits | | $ | 1,883 | | $ | 1,888 |

Restricted cash | | | 4,000 | | | — |

Deferred offering costs | |

| — | |

| 3,711 |

Other long-term assets | | | 919 | | | — |

Total other non-current assets | | $ | 6,802 | | $ | 5,599 |

15

Note 8. Accrued Expenses and Other Current Liabilities

Accrued expenses and other current liabilities consist of the following at June 30, 2021 and December 31, 2020 (in thousands):

| | | | | | |

|

| June 30, |

| December 31, | ||

|

| 2021 |

| 2020 | ||

Employee compensation | | $ | 8,177 | | $ | 5,968 |

Customer deposits | |

| 1,165 | |

| 1,177 |

Accrued warranty liability | |

| 370 | |

| 646 |

Non-income tax | |

| 3,560 | |

| 3,695 |

Professional fees | |

| 3,293 | |

| 5,432 |

Vendor settlements | | | — | | | 2,975 |

Other | |

| 2,762 | |

| 2,069 |

Total accrued expenses and other current liabilities | | $ | 19,327 | | $ | 21,962 |

Warranty expense activity for the three and six months ended June 30, 2021 and 2020 is as follows (in thousands):

| | | | | | | | | | | | | |

| | Three months ended June 30, | | Six months ended June 30, | | ||||||||

|

| 2021 |

| 2020 |

| 2021 |

| 2020 |

| ||||

Balance, beginning of period | | $ | 1,186 | | $ | 1,099 | | $ | 1,826 | | $ | 876 | |

Warranty provision charged to operations | |

| 167 | |

| 788 | |

| (225) | |

| 1,512 | |

Warranty claims | |

| (192) | |

| (363) | |

| (440) | |

| (864) | |

Balance, end of period | | $ | 1,161 | | $ | 1,524 | | $ | 1,161 | | $ | 1,524 | |

The Company classifies its accrued warranty liability based on the timing of expected warranty activity. The future costs of expected activity greater than one year is recorded within other non-current liabilities on the condensed consolidated balance sheet.

Note 9. Convertible Preferred Stock

The Company has issued 4 series of Convertible Preferred Stock, Series A through Series D. The following table summarizes the authorized, issued and outstanding Convertible Preferred Stock of the Company as of immediately prior to the Business Combination and December 31, 2020 (in thousands, except share and per share information):

| | | | | | | | | | | | | | | | | | | |

|

| |

| Issuance |

| Shares |

| Total |

| | |

| | |

| Initial | |||

| | | | Price | | Authorized, | | Proceeds or | | | | | Net | | Liquidation | ||||

| | Year of | | per | | Issued and | | Exchange | | Issuance | | Carrying | | Price per | |||||

Class | | Issuance | | share | | Outstanding | | Value | | Costs | | Value | | share | |||||

Series A |

| 2012 | | $ | 0.04 |

| 26,946,090 | | $ | 1,038 | | $ | 11 | | $ | 1,027 | | $ | 0.77 |

Series B |

| 2014 | |

| 0.77 |

| 25,957,500 | |

| 20,000 | |

| 99 | |

| 19,901 | |

| 0.77 |

Series C |

| 2014 – 2015 | |

| 3.21 |

| 29,018,455 | |

| 93,067 | |

| 246 | |

| 92,821 | |

| 3.21 |

Series D |

| 2018 | |

| 9.89 |

| 25,275,073 | |

| 250,000 | |

| 2,812 | |

| 247,188 | |

| 9.89 |

| | | | | |

| 107,197,118 | | | | | | | | | | | | |

Prior to the completion of the Business Combination there were no significant changes to the terms of the Convertible Preferred Stock. Upon the Closing of the Business Combination, the Convertible Preferred stock converted into the right to receive Class A and Class B common stock based on the Business Combination’s conversion ratio of 1.0383 of the Company’s shares for each Legacy Butterfly share. The Company recorded the conversion at the carrying value of the Convertible Preferred Stock at the time of Closing. There are 0 shares of Convertible Preferred Stock outstanding as of June 30, 2021.

Note 10. Equity Incentive Plans

The Company’s 2012 Employee, Director and Consultant Equity Incentive Plan (the “2012 Plan”) was adopted by its Board of Directors and stockholders in March 2012. The Butterfly Network, Inc. Amended and Restated 2020 Equity

16

Incentive Plan (the “2020 Plan”) was approved by the Board of Directors in the fourth quarter of 2020 and by the stockholders in the first quarter of 2021. Grants under the 2012 Plan and 2020 Plan are included in the tables below.

In connection with the Closing of the Business Combination, the Company adjusted the equity awards as described in Note 3 “Business Combination”. The adjustments to the awards did not result in incremental expense as the equitable adjustments were made pursuant to a preexisting, nondiscretionary anti-dilution provision in the 2012 Plan, and the fair-value, vesting conditions and classification of the awards are the same immediately before and after the modification.

Stock option activity

The following table summarizes the changes in the Company’s outstanding stock options for the six months ended June 30, 2021:

| | |

| | Number of |

| | Options |

Outstanding at December 31, 2020 |

| 26,708,329 |

Granted |

| 2,929,935 |

Exercised |

| (5,326,940) |

Forfeited |

| (6,960,118) |

Outstanding at June 30, 2021 |

| 17,351,206 |

Each award will vest based on continued service which is generally over 4 years. The grant date fair value of the award will be recognized as stock-based compensation expense over the requisite service period. The grant date fair value was determined using similar methods and assumptions as those previously disclosed by the Company.

On January 23, 2021, the former Chief Executive Officer and member of the Board of Directors resigned from his position as Chief Executive Officer. Pursuant to the separation agreement between the former Chief Executive Officer and the Company, the former officer received equity-based compensation. The equity compensation includes the acceleration of vesting of the officer’s service based options. The acceleration of 1.6 million options was pursuant to the original option award agreement. The Company recognized $2.6 million of expense related to the acceleration of this option award during the six months ended June 30, 2021. NaN expense related to the acceleration of this option award was recognized during the three months ended June 30, 2021.

Restricted stock unit (“RSU”) activity

The following table summarizes the changes in the Company’s outstanding restricted stock units for the six months ended June 30, 2021:

| | |

| | Number of |

| | RSUs |

Outstanding at December 31, 2020 |

| 1,894,897 |

Granted |

| 1,911,208 |

Vested |

| (467,234) |

Forfeited |

| — |

Outstanding at June 30, 2021 |

| 3,338,871 |

Included in the table above are service-based restricted stock units. During the six months ended June 30, 2021, the Company granted 0.9 million service-based awards. Each award will vest based on continued service which is generally over 4 years. The grant date fair value of the award will be recognized as stock-based compensation expense over the requisite service period. The fair value of restricted stock units was estimated on the date of grant based on the fair value of the Company’s Class A common stock.

Included in the table above are performance-based restricted stock units. In January 2021, the Company granted 1.0 million restricted stock units to certain employees. In 2020, the Company granted 1.9 million restricted stock units to certain employees and consultants, including a grant of 1.0 million restricted stock units to the Chairman of the Board and

17

significant shareholder of Butterfly. The awards are subject to certain service conditions and performance conditions. The service condition for these awards is satisfied by providing service to the Company based on the defined service period per the award agreement. The performance-based condition is satisfied upon the occurrence of a business combination event as defined in the award agreement. The achievement of the performance condition was deemed satisfied in the first quarter of 2021, as the completion of the Business Combination occurred.

The fair value of performance-based restricted stock units was estimated on the date of grant based on the fair value of the Company’s Class A common stock. For each award, the Company recognizes the expense over the requisite service period as defined in the award agreement. During the six months ended June 30, 2021, the Company recognized the full grant date fair value of the awards for the Chairman of the Board and one other consultant as service to the Company was no longer required since the Business Combination closed in the first quarter of 2021. NaN expense for these awards was recognized during the three months ended June 30, 2021. For the remaining awards, continued service is still required for the awards to continue to vest per the award agreements.

The Company’s total stock-based compensation expense for all stock option and restricted stock unit awards for the periods presented was as follows (in thousands):

| | | | | | | | | | | | | |

| | Three months ended June 30, | | Six months ended June 30, | | ||||||||

|

| 2021 |

| 2020 |

| 2021 |

| 2020 |

| ||||

Cost of revenue – subscription | | $ | 1 | | $ | 5 | | $ | 3 | | $ | 10 | |

Research and development | |

| 1,562 | |

| 1,174 | |

| 2,953 | |

| 2,433 | |

Sales and marketing | | | 2,085 | | | 493 | | | 3,758 | | | 1,026 | |

General and administrative | | | 4,090 | | | 990 | | | 21,321 | | | 1,876 | |

Total stock-based compensation expense | | $ | 7,738 | | $ | 2,662 | | $ | 28,035 | | $ | 5,345 | |

Note 11. Net Loss Per Share

We compute net income per share of Class A and Class B common stock using the two-class method. Basic net loss per share is computed by dividing the net loss by the weighted-average number of shares of each class of the Company’s common stock outstanding during the period. Diluted net loss per share is computed by giving effect to all potential shares of the Company’s common stock, including those presented in the table below, to the extent dilutive. Basic and diluted net loss per share was the same for each period presented as the inclusion of all potential shares of the Company’s common stock outstanding would have been anti-dilutive. Since the Company was in a net loss position for all periods presented, the basic earnings per share (“EPS”) calculation excludes preferred stock as it does not participate in net losses of the Company.

As the Company uses the two-class method required for companies with multiple classes of common stock, the following table presents the calculation of basic and diluted net loss per share for each class of the Company’s common stock outstanding (in thousands, except share and per share amounts):

| | | | | | | | | | |

Three months ended June 30, 2021 | | | | | | | | | | |

| | | | | | | | Total | | |

|

| Class A |

| Class B |

| Common Stock | | |||

Numerator: | | |

| | |

|

| |

| |

Allocation of undistributed earnings | | $ | (2,537) | | $ | (405) | | $ | (2,942) | |

Numerator for basic and diluted EPS – loss available to common stockholders | | $ | (2,537) | | $ | (405) | | $ | (2,942) | |

Denominator: | |

|

| |

|

| |

|

| |

Weighted-average common shares outstanding | |

| 165,753,204 | |

| 26,426,937 | |

| 192,180,141 | |

Denominator for basic and diluted EPS – weighted-average common stock | |

| 165,753,204 | |

| 26,426,937 | |

| 192,180,141 | |

Basic and diluted loss per share | | $ | (0.02) | | $ | (0.02) | | $ | (0.02) | |

18

| | | | | | | | | | |

Three months ended June 30, 2020 | | | | | | | | | | |

| | | | | | | | Total | | |

|

| Class A |

| Class B |

| Common Stock | | |||

Numerator: | | |

| | |

|

| |

| |

Allocation of undistributed earnings | | $ | (23,241) | | $ | — | | $ | (23,241) | |

Numerator for basic and diluted EPS – loss available to common stockholders | | $ | (23,241) | | $ | — | | $ | (23,241) | |

Denominator: | |

|

| |

|

| |

|

| |

Weighted-average common shares outstanding | |

| 6,034,191 | |

| — | |

| 6,034,191 | |

Denominator for basic and diluted EPS – weighted-average common stock | |

| 6,034,191 | |

| — | |

| 6,034,191 | |

Basic and diluted loss per share | | $ | (3.85) | | $ | — | | $ | (3.85) | |

| | | | | | | | | | |

Six months ended June 30, 2021 | | | | | | | | | | |

| | | | | | | | Total | | |

|

| Class A |

| Class B |

| Common Stock | | |||

Numerator: | | |

| | |

|

| |

| |

Allocation of undistributed earnings | | $ | (3,138) | | $ | (494) | | $ | (3,632) | |

Numerator for basic and diluted EPS – loss available to common stockholders | | $ | (3,138) | | $ | (494) | | $ | (3,632) | |

Denominator: | |

|

| |

|

| |

|

| |

Weighted-average common shares outstanding | |

| 128,991,979 | |

| 20,294,721 | |

| 149,286,700 | |

Denominator for basic and diluted EPS – weighted-average common stock | |

| 128,991,979 | |

| 20,294,721 | |

| 149,286,700 | |

Basic and diluted loss per share | | $ | (0.02) | | $ | (0.02) | | $ | (0.02) | |

| | | | | | | | | | |

Six months ended June 30, 2020 | | | | | | | | | | |

| | | | | | | | Total | | |

|

| Class A |

| Class B |

| Common Stock | | |||

Numerator: | | |

| | |

|

| |

| |

Allocation of undistributed earnings | | $ | (47,595) | | $ | — | | $ | (47,595) | |

Numerator for basic and diluted EPS – loss available to common stockholders | | $ | (47,595) | | $ | — | | $ | (47,595) | |

Denominator: | |

|

| |

|

| |

|

| |

Weighted-average common shares outstanding | |

| 6,006,711 | |

| — | |

| 6,006,711 | |

Denominator for basic and diluted EPS – weighted-average common stock | |

| 6,006,711 | |

| — | |

| 6,006,711 | |

Basic and diluted loss per share | | $ | (7.92) | | $ | — | | $ | (7.92) | |

For the periods presented above, the net income per share amounts are the same for Class A and Class B common stock because the holders of each class are entitled to equal per share dividends or distributions in liquidation in accordance with the Certificate of Incorporation. The undistributed earnings for each year are allocated based on the contractual participation rights of the Class A and Class B common stock as if the earnings for the year had been distributed. As the liquidation and dividend rights are identical, the undistributed earnings are allocated on a proportionate basis.

19

For the periods presented, anti-dilutive common equivalent shares were as follows:

| | | | | |

| | June 30, | | ||

|

| 2021 |

| 2020 |

|

Outstanding options to purchase common stock | | 17,351,206 | | 26,738,214 | |

Outstanding restricted stock units | | 3,338,871 | | — | |

Outstanding warrants | | 20,653,028 | | — | |

Outstanding convertible preferred stock (Series A through D) | | — | | 107,197,118 | |

Total anti-dilutive common equivalent shares | | 41,343,105 | | 133,935,332 | |

Note 12. Related Party Transactions

Prior to the Closing of the Business Combination, there were no significant changes in the nature of the Company’s related party transactions since December 31, 2020. Pursuant to a First Addendum dated November 19, 2020 to the Amended and Restated Technology Services Agreement dated November 11, 2020 by and between the Company, 4Catalyzer Corporation (“4Catalyzer”), and other participant companies controlled by Dr. Rothberg (the “ARTSA”), Butterfly terminated its participation under the ARTSA immediately prior to the Effective Time of the Business Combination.

A summary of related-party transactions and balances with 4Catalyzer are as follows (in thousands):

| | | | | | | | | | | | |

| | Three months ended June 30, | | Six months ended June 30, | ||||||||

|

| 2021 |

| 2020 |

| 2021 |

| 2020 | ||||

Total incurred for operating expenses | | $ | 48 | | $ | 1,418 | | $ | 541 | | $ | 3,067 |

| | | | | | |

|

| June 30, | | December 31, | ||

| | 2021 |

| 2020 | ||

Due from related parties | | $ | 25 | | $ | 38 |

Due to related parties | |

| 13 | |

| 154 |

Note 13. Loan Payable

In May 2020, the Company received loan proceeds of $4.4 million under the Paycheck Protection Program (“PPP”). The Company used the loan proceeds for eligible purposes, including payroll, benefits, rent and utilities. The Company accounted for the loan as debt. Following the Closing of the Business Combination discussed in Note 3 “Business Combination”, the Company repaid the loan in full in February 2021. The Company recognized an insignificant amount of interest expense in the condensed consolidated statement of operations and comprehensive loss related to the loan.

Note 14. Convertible Debt

In the year ended December 31, 2020, the Company issued convertible debt for total gross proceeds of $50.0 million.

Pursuant to the terms of the debt, at the Effective Time of the Merger discussed in Note 3 “Business Combination”, the convertible debt was automatically cancelled and converted into the right to receive shares of the Company’s Class A common stock. The debt was converted with $49.9 million, the net carrying value of the debt as of the Closing of the Business Combination, in stockholders’ equity with a corresponding decrease to the convertible debt for the principal, accrued interest and unamortized debt issuance costs in the condensed consolidated statement of operations and comprehensive loss.

The Company recorded interest expense and amortization expense for the issuance costs of $0.6 million and $0.1 million for the six months ended June 30, 2021 and 2020, respectively. The Company recorded interest expense and amortization expense for the issuance costs of $0.0 million and $0.1 million for the three months ended June 30, 2021 and 2020, respectively.

20

Note 15. Warrants

Public Warrants