As filed with the Securities and Exchange Commission on November 1, 2021.

Registration No. 333-257929

Utah | | | 6022 | | | 83-0356689 |

(State or other jurisdiction of incorporation or organization) | | | (Primary Standard Industrial Classification Code Number) | | | (I.R.S. Employer Identification Number) |

Peter G. Smith, Esq. Terrence Shen, Esq. Kramer Levin Naftalis & Frankel LLP 1177 Avenue of the Americas New York, NY 10036 (212) 715-9100 | | | Beth A. Whitaker, Esq. Heather Archer Eastep, Esq. Hunton Andrews Kurth LLP 1445 Ross Avenue, Suite 3700 Dallas, TX 75202 (214) 979-3000 |

Large accelerated filer | | | ☐ | | | Accelerated filer | | | ☐ |

Non-accelerated filer | | | ☒ | | | Smaller reporting company | | | ☒ |

| | | | | Emerging growth company | | | ☒ |

| | | Per Share | | | Total | |

Initial public offering price | | | $ | | | $ |

Underwriting discount(1) | | | $ | | | $ |

Proceeds to us (before expenses) | | | $ | | | $ |

| (1) | The underwriters will also be reimbursed for certain expenses incurred in this offering. See “Underwriting” for additional information. |

| | |  |

| • | permitted to present only two years of audited financial statements, in addition to any required interim financial statements, and only two years of related discussion in “Management’s Discussion and Analysis of Financial Condition and Results of Operations;” |

| • | exempt from the requirement to obtain an attestation from our auditors on management’s assessment of our internal control over financial reporting under the Sarbanes-Oxley Act of 2002, or the Sarbanes-Oxley Act; |

| • | permitted to choose not to comply with any new requirements adopted by the Public Company Accounting Oversight Board, or PCAOB, requiring mandatory audit firm rotation or a supplement to the auditor’s report providing additional information about the audit and our audited financial statements; |

| • | permitted to provide less extensive disclosure about our executive compensation arrangements; and |

| • | not required to hold non-binding shareholder advisory votes on executive compensation or golden parachute arrangements. |

| • | our strategic relationships with third party loan origination platforms, many of whom use technology to facilitate loan origination, that allow us to capture a high volume of diverse loan origination and loan performance data from the billions of dollars of loans that we have originated, sold or held in four main lending areas; |

| • | our FinView™ Analytics Platform (“FinView™”), including our enterprise data warehouse, which is a proprietary technology developed by us to enhance our ability to gather and interpret performance data for the loans originated by us and to help us identify attractive risk-adjusted market sectors; |

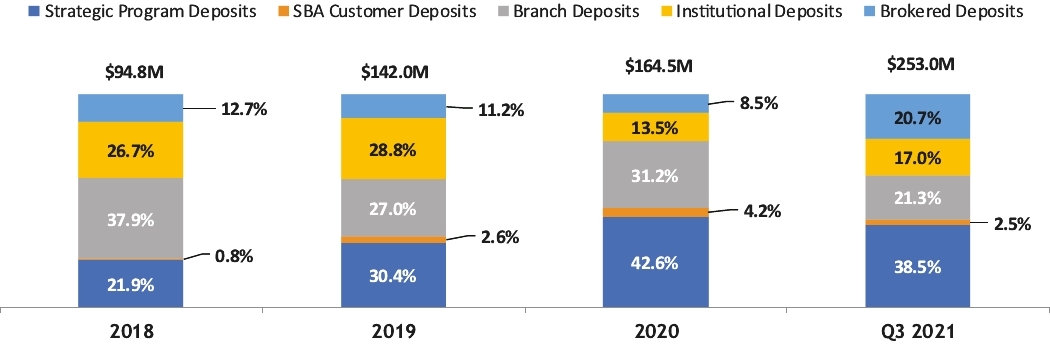

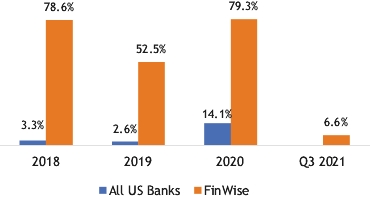

| • | our core deposits which, as of September 30, 2021 and December 31, 2020, constituted 79.3% and 91.5% of our funding sources, respectively (excluding the Paycheck Protection Program Liquidity Facility (the “PPPLF”)), and have been highly reliable and relatively low cost (our core deposits comprise the sum of demand deposits, negotiable order of withdrawal (“NOW”) accounts, money market deposit accounts (“MMDA”), savings accounts, and time deposits under $250,000 that are not brokered deposits); and |

| • | our seasoned management team, which has considerable banking experience, particularly in our core lines of business. |

| • | In SBA 7(a) lending, we lend to small business and professionals. Our credit risk management is augmented by the fact the loans are partially guaranteed by the SBA. We further mitigate our credit risk in this program by using data, such as the nature of the business, use of proceeds, length of time in business and management experience to help us target loans that we believe have lower credit risk. Our prudent underwriting, closing and servicing processes are essential to effective utilization of the SBA 7(a) program, as the SBA guaranty is conditioned upon proper underwriting, closing and servicing by the lender. |

| • | In our Strategic Program lending, we originate unsecured and secured consumer and business loans to borrowers with certain Bank-approved credit profiles. The credit profiles are based on specific predetermined underwriting criteria informed by our extensive data and analytics. While we sell the vast majority of loans in this lending program shortly after origination, the Bank may choose to retain a portion of the funded loans and/or receivables. Our credit risk is mitigated by focusing on amortizing loans, lending to borrowers with demonstrated ability to repay, and extending loans that are priced appropriately to the credit profile of the borrower (including credit history). Smaller loans are often unsecured and therefore rely more on predictive models that allow us to appropriately price credit based on probable losses. |

| • | SBA 7(a) Lending: Since 2014, we have utilized relationships with third parties (primarily BFG) to originate loans partially guaranteed by the SBA, to small businesses and professionals. We typically sell the SBA-guaranteed portion (generally 75% of the principal balance) of the loans we originate at a premium in the secondary market while retaining all servicing rights and the unguaranteed portion. We analyze public data provided by the SBA to target or avoid loans and industries with specific characteristics that may lead to unacceptable rates of future loan losses. We believe the experience of our management team, our ability to analyze loan performance data, our loan processing structure, our ability to leverage our referral relationship with BFG, careful underwriting, servicing and proactive collection policies have resulted in charge-off experience in our SBA portfolio that outperforms industry averages. Based on data sets for the SBA beginning January 1, 2014 through September 30, 2021, SBA 7(a) loans made by the Bank have a charge-off rate of 0.2% versus 0.9% for the entire SBA 7(a) lending industry on average. We believe, based on our current relatively low market penetration, the opportunity to continue to expand this business line is significant and that the SBA 7(a) product provides an entry point to broaden our banking relationship with these customers to potentially include deposits and POS financing opportunities. Loan terms generally range from 120 to 300 months and interest rates currently range from the prime rate plus 200 basis points to the prime rate plus 275 basis points, as adjusted quarterly. In 2020, we originated approximately $80.3 million in SBA 7(a) loans and held approximately $96.2 million of SBA 7(a) loans on our balance |

| • | Strategic Programs: Over the past five years, we have established Strategic Programs with various third-party consumer and commercial platforms that use technology to streamline the Bank’s origination of consumer and small commercial loans. We currently have 11 Strategic Program relationships. We are highly selective in establishing relationships with platforms for our Strategic Programs. We also place a high priority on regulatory compliance and have implemented comprehensive compliance management systems with an emphasis on oversight of platforms in our Strategic Program. Finally, we seek to establish relationships with Strategic Program platforms whose philosophy aligns with our goal of helping our customers move forward, and who augment our product offerings and enable us to realize operating efficiencies. We typically retain Strategic Program loans for a number of business days after we originate the loans, following which we may sell the loan receivables or whole loans to the Strategic Program platform or other investors. The terms of our Strategic Programs generally require each Strategic Program platform to establish a reserve deposit account with the Bank, intended to protect the Bank in the event a purchaser of loan receivables originated through our Strategic Programs cannot meet its contractual obligation to purchase. |

| • | Residential and Commercial Real Estate Lending. We operate a single branch location in Sandy, Utah. From this branch, we offer commercial and consumer banking services throughout the greater Salt Lake City, Utah MSA. These products are delivered using a high-touch service, relationship banking approach. The majority of the lending product consists of residential non-speculative construction loans which generate both non-interest income and interest income. Construction loan terms generally range from 9 to |

| • | Consumer Lending via our POS Lending Program: Since 2011, the Bank has offered collateralized and uncollateralized loans to finance the purchase of retail goods and services, such as pianos, spas, and home improvements. Loan applications are submitted at the point-of-sale through an online portal. Historically, all of the loans originated through our POS lending program have been held on our balance sheet. We currently manage the credit risk associated with these loans through a variety of processes, including targeting super prime (FICO score of 720 and higher), prime (FICO score of 660 through 719) and near-prime (FICO score of 640 through 659) borrowers, prudent underwriting, proper administration, careful servicing, proactive collection policies and comprehensive merchant due diligence. Loan terms are generally 60 months and interest rates currently range from 7.0% to 14.5%. We utilize a high degree of automation in this program and track loan applications, analyze credit and approve loans by deploying a combination of FinView™ and “off-the-shelf” technology solutions. The majority of the approximately $5.5 million and $4.7 million in consumer loans outstanding as of December 31, 2020 and September 30, 2021, respectively, that were not generated through our Strategic Programs were originated in connection with our POS lending program. In 2020, we originated approximately $2.8 million in POS loans and held approximately $4.4 million of POS loans on our balance sheet as of December 31, 2020. During the nine months ended September 30, 2021, we originated approximately $1.8 million in POS loans and held approximately $3.9 million of POS loans on our balance sheet as of September 30, 2021. We expect to expand this program via enhanced marketing efforts. |

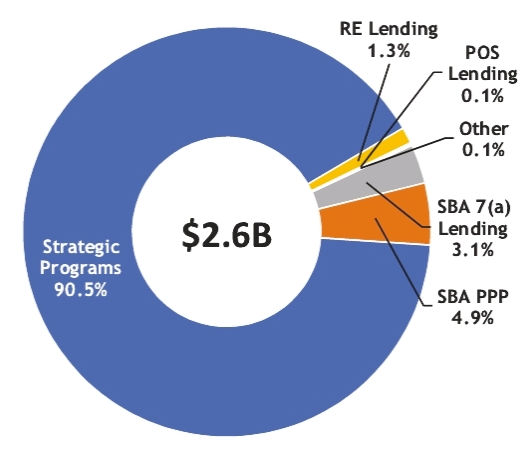

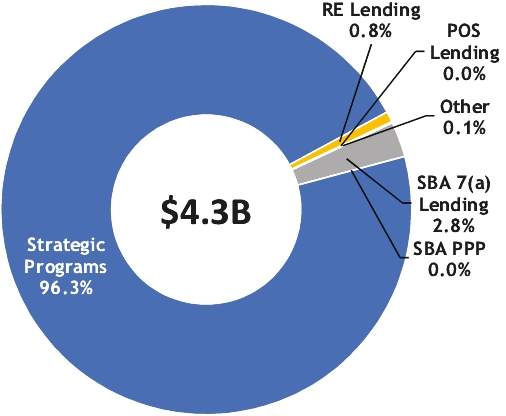

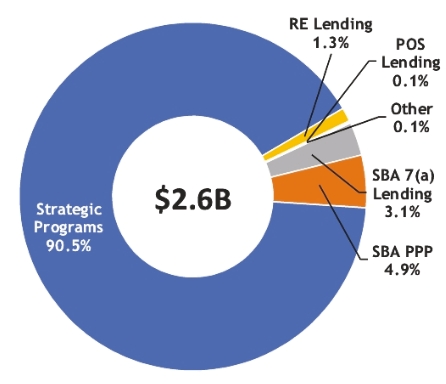

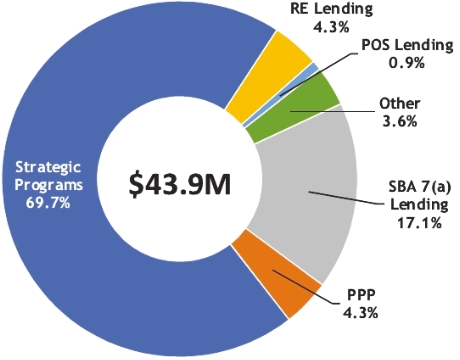

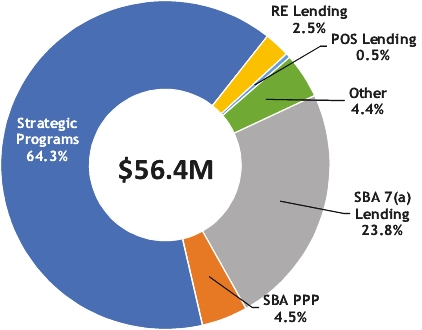

Year End 2020 Origination Volume | | | Loan Portfolio as of 12/31/20 |

| | |  |

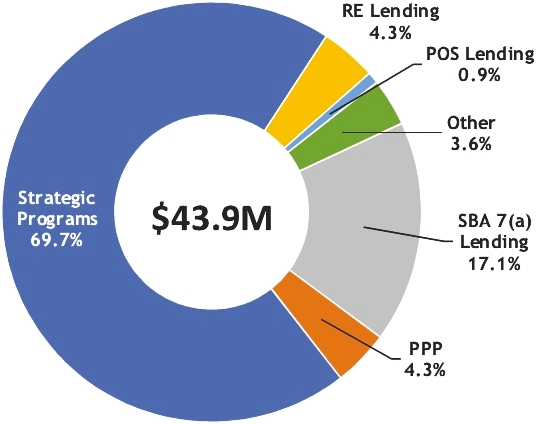

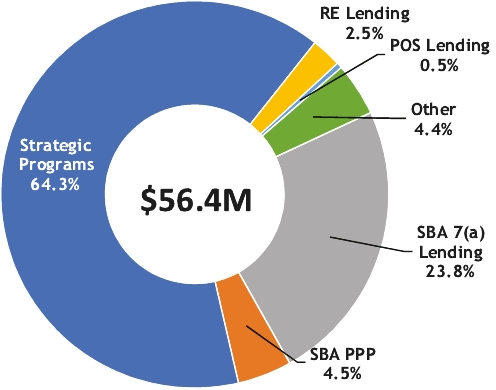

Year End 2020 Revenue by Business Line | |||

| |||

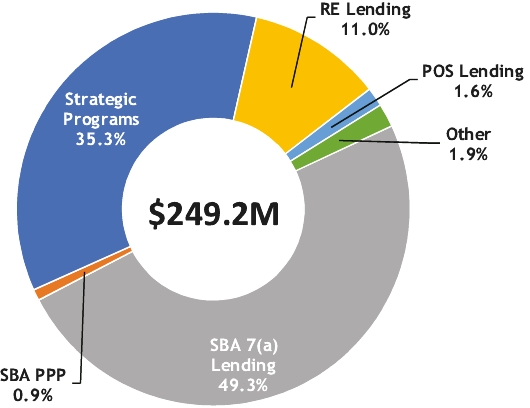

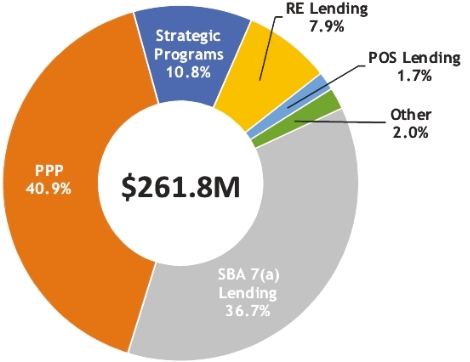

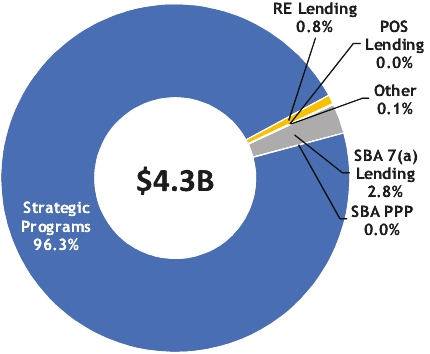

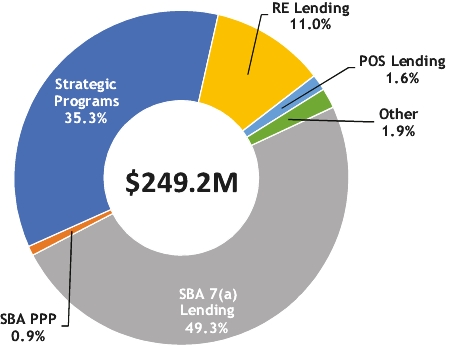

Q3 2021 Origination Volume | | | Loan Portfolio as of 09/30/21 |

| | |  |

Q3 2021 Revenue by Business Line | |||

| |||

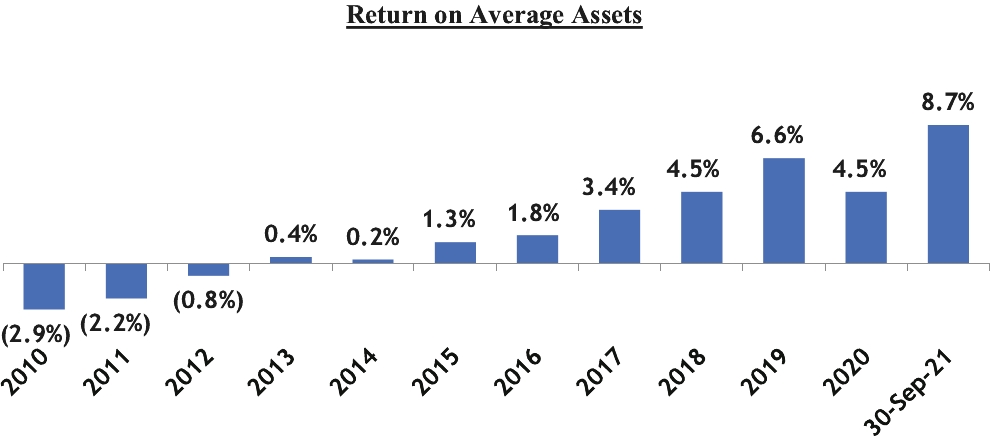

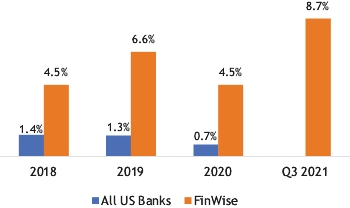

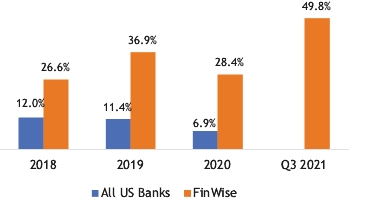

Return on Average Assets | | | Return on Average Equity |

| | |  |

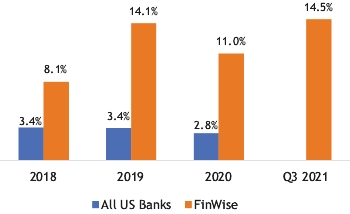

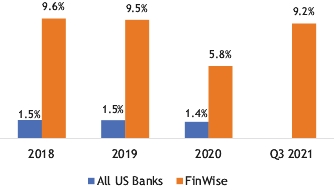

Net Interest Margin | | | Noninterest Income / Average Assets |

| | |  |

Efficiency Ratio | |||

| |||

NAICS Sub-Sector Code | | | Description | | | September 30, 2021 % of Total |

541 | | | Professional, Scientific and Technical Services | | | 15.9% |

454 | | | Non-Store Retailers (Electronic Shopping) | | | 15.6% |

423 | | | Merchant Wholesalers, Durable Goods | | | 8.5% |

621 | | | Ambulatory Health Care Services | | | 6.3% |

445 | | | Food and Beverage Stores (Grocery, Convenience) | | | 4.5% |

623 | | | Nursing and Residential Care Facilities | | | 4.4% |

448 | | | Clothing and Clothing Accessories Stores | | | 4.3% |

238 | | | Specialty Trade Contractors | | | 4.1% |

811 | | | Manufacturing Repair and Maintenance | | | 3.8% |

442 | | | Furniture and Home Furnishings Stores | | | 2.9% |

| | | All Other | | | 29.7% | |

Total | | | | | 100.0% |

| • | Strategic Programs: $100 billion in total available market based on industry data and estimates. Our estimation of the total available market for the Strategic Program business line is based on industry data for unsecured personal loans. We believe the total available market may be larger than this as the Bank offers Strategic Programs specific to POS lending and commercial lending which may not be accounted for in the above estimates. |

| • | SBA Lending $150 billion in total available market based on SBA agency reports. |

| • | POS Lending: $160 billion in total available market based on industry data and estimates. |

Asset Growth Rate (Over Prior Period) | | | Total Loan Originations ($000s) |

| | |  |

| • | Kent Landvatter. Mr. Landvatter joined the Company and the Bank in September 2010 as the President and Chief Executive Officer. Mr. Landvatter has over 40 years of financial services and banking experience, including experience with distressed banks and serving as the president of two de novo banks, Comenity Capital Bank and Goldman Sachs Bank, USA. |

| • | Javvis Jacobson. Mr. Jacobson joined the Company and the Bank in March 2015 as the Executive Vice President and Chief Financial Officer. Mr. Jacobson has over 20 years of financial services experience, including at Deloitte, where he served for several years managing audits of financial institutions. Mr. Jacobson also served for several years as the Chief Financial Officer of Beehive Credit Union with over $190 million in assets. |

| • | James Noone. Mr. Noone joined the Bank in February 2018 and was named Executive Vice President and Chief Credit Officer in June 2018. Mr. Noone has 20 years of financial services experience including commercial and investment banking as well as private equity. Prior to joining the Bank, Mr. Noone served as Executive Vice President of Prudent Lenders, an SBA service provider from 2012 to 2018. |

| • | Dawn Cannon. Ms. Cannon joined the Bank in March 2020 as the Senior Operating Officer and was named Executive Vice President and Chief Operating Officer in July 2020. Ms. Cannon has over 17 years of banking experience, including serving as the Executive Vice President of Operations of EnerBank, an industrial bank that focused on lending programs similar to our POS lending program, where she was instrumental in building it from 23 to 285 full time employees and from $10 million to $1.4 billion in total assets. |

| • | Michael O’Brien. Mr. O’Brien joined the Company and the Bank in September 2021 as Executive Vice President, Chief Compliance and Risk Officer and Corporate Counsel. Mr. O’Brien has over 20 years of legal, compliance and risk management experience in financial services. He practiced law in New York and Washington, D.C. with nationally recognized law firms prior to legal positions with E*TRADE Financial and Sallie Mae Bank. Mr. O’Brien also previously served as Chief Compliance Officer of EnerBank USA, a Utah industrial bank. He is currently licensed to practice law in Utah and Washington, D.C. |

| • | David Tilis. Mr. Tilis joined the Bank in March 2016 as a Vice President and Director of Specialty Lending and now serves as the Chief Strategy Officer and Senior Vice President. Mr. Tilis has over 15 years of financial services experience, including serving as a Vice President of Cross River Bank overseeing SBA lending and playing a significant role in strategic relationships. |

| • | the impact, duration and severity of the ongoing Covid-19 pandemic (including the emergence of any new variants thereof), the response of governmental authorities to the Covid-19 pandemic and our participation in Covid-19-related government programs such as the PPP administered by the SBA and created under the CARES Act; |

| • | cybersecurity breaches and system failures affecting FinView™; |

| • | operational and strategic risks, including the risk that we may not be able to implement our growth strategy and risks related to cybersecurity, our continued ability to establish relationships with Strategic Program service providers, and the possible loss of key members of our senior leadership team; |

| • | credit risks, including risks related to the significance of SBA 7(a), Strategic Programs and construction loans in our portfolio, our relationship with BFG, our ability to effectively manage our credit risk and the potential deterioration of the business and economic conditions in our markets; |

| • | liquidity and funding risks, including the risk that we will not be able to meet our obligations due to risks relating to our funding sources; |

| • | market and interest rate risks, including risks related to interest rate fluctuations and the monetary policies and regulations of the Board of Governors of the Federal Reserve System, or the Federal Reserve; |

| • | third-party risk, including risks that we may be unable to maintain or increase loan originations facilitated through our Strategic Programs; |

| • | reputational risks, including the risk that we may be subject to negative publicity about us or our industry, including the transparency, fairness, user experience, quality, and reliability of our lending products or distribution channels; |

| • | legislative, regulatory, legal, and reputational risks related to our Strategic Programs, including those relating to our small dollar lending program; |

| • | reversal of regulatory pronouncements that provided clarity for Strategic Programs on “true lender” rules; |

| • | legal, accounting and compliance risks, including risks related to the extensive state and federal regulation under which we operate and changes in such regulations; |

| • | changes in the regulatory oversight environment impacting our Strategic Programs or non-compliance of federal and state consumer protection laws by our Strategic Program service providers; and |

| • | offering and investment risks, including illiquidity and volatility in the trading of our common stock, limitations on our ability to pay dividends and the dilution that investors in this offering will experience. |

| • | assumes no exercise by the underwriters of their option to purchase up to an additional shares of common stock; |

| • | assumes that the shares of common stock sold in this offering are sold at $ per share, which is the midpoint of the price range set forth on the cover page of this prospectus; |

| • | excludes 881,988 shares of common stock issuable upon exercise of stock options outstanding as of September 30, 2021, at a weighted average exercise price of $4.30 per share (comprising 481,728 shares of fully vested common stock issuable upon exercise of stock options and 400,260 shares of unvested common stock issuable upon exercise of stock options); |

| • | does not attribute to any director, executive officer, employee, principal shareholder, business associate or other related person any purchases of shares of our common stock in this offering, including through the directed share program described in “Underwriting—Directed Share Program”; and |

| • | excludes 270,000 shares of common stock issuable upon exercise of fully vested warrants outstanding at a weighted average exercise price of $6.67 per share. |

Balance Sheet Data | | | As of and for the Nine Months Ended September 30, | | | As of and for the years ended December 31, | |||||||||

($ in thousands) | | | 2021 | | | 2020 | | | 2020 | | | 2019 | | | 2018 |

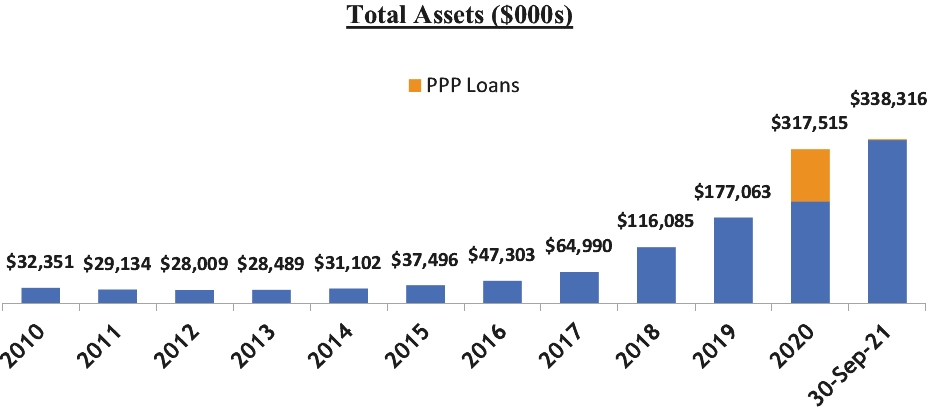

Total assets | | | $338,316 | | | $318,340 | | | $317,515 | | | $177,062 | | | $116,085 |

Cash and cash equivalents | | | 68,106 | | | 32,169 | | | 47,383 | | | 34,779 | | | 26,004 |

Investment securities held-to-maturity, at cost | | | 4,414 | | | 1,929 | | | 1,809 | | | 453 | | | 570 |

Loans receivable, net | | | 178,748 | | | 227,266 | | | 232,074 | | | 105,725 | | | 78,034 |

Strategic Program loans held-for-sale, at lower of cost or fair value | | | 62,702 | | | 45,035 | | | 20,948 | | | 25,109 | | | 6,956 |

SBA servicing asset | | | 4,368 | | | 2,419 | | | 2,415 | | | 2,034 | | | 1,581 |

Investment in Business Funding Group, at fair value | | | 5,241 | | | 3,785 | | | 3,770 | | | 3,459 | | | — |

Deposits | | | 253,036 | | | 184,623 | | | 164,476 | | | 142,021 | | | 94,824 |

PPP Liquidity Facility | | | 2,259 | | | 84,330 | | | 101,007 | | | — | | | — |

Total shareholders’ equity | | | 69,138 | | | 40,929 | | | 45,872 | | | 33,095 | | | 19,225 |

Tangible shareholders’ equity(1) | | | 69,138 | | | 40,929 | | | 45,872 | | | 33,095 | | | 19,225 |

| | | For the Nine Months Ended September 30, | | | For the Years Ended December 31, | ||||||||||

($ in thousands, except for per share data) | | | 2021 | | | 2020 | | | 2020 | | | 2019 | | | 2018 |

Income Statement Data | | | | | | | | | | | |||||

Interest income | | | $33,690 | | | $20,941 | | | $29,506 | | | $21,408 | | | $8,073 |

Interest expense | | | 984 | | | 1,352 | | | 1,756 | | | 1,462 | | | 846 |

Net interest income | | | 32,706 | | | 19,589 | | | 27,750 | | | 19,946 | | | 7,227 |

Provision for loan losses | | | 5,536 | | | 5,234 | | | 5,234 | | | 5,288 | | | 980 |

Net interest income after provision for loan losses | | | 27,170 | | | 14,355 | | | 22,516 | | | 14,658 | | | 6,247 |

Noninterest income: | | | | | | | | | | | |||||

Strategic Program fees | | | 11,877 | | | 6,878 | | | 9,591 | | | 8,866 | | | 5,026 |

Gain on sale of loans | | | 7,876 | | | 2,560 | | | 2,849 | | | 4,167 | | | 2,957 |

SBA loan servicing fees | | | 800 | | | 745 | | | 1,028 | | | 607 | | | 545 |

Other noninterest income | | | 2,162 | | | 758 | | | 905 | | | 223 | | | 128 |

Total noninterest income | | | 22,715 | | | 10,941 | | | 14,373 | | | 13,863 | | | 8,656 |

Noninterest expense | | | 21,140 | | | 16,092 | | | 21,749 | | | 15,685 | | | 9,538 |

Provision for income taxes | | | 7,273 | | | 2,622 | | | 3,942 | | | 3,177 | | | 1,333 |

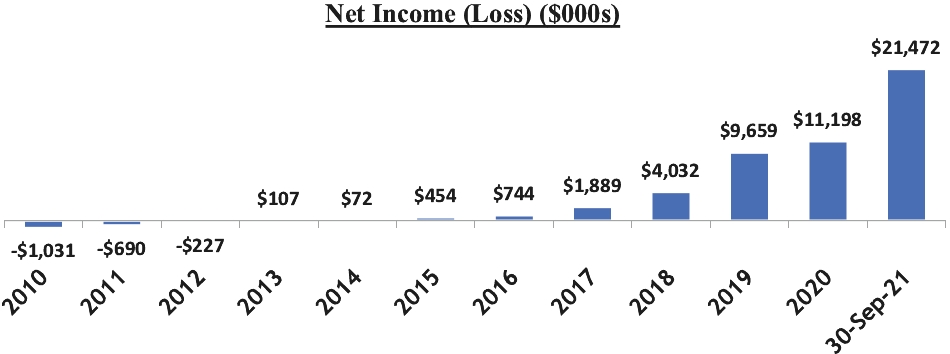

Net income | | | $21,472 | | | $6,582 | | | $11,198 | | | $9,659 | | | $4,032 |

| | | For the Nine Months Ended September 30, | | | For the Years Ended December 31, | ||||||||||

($ in thousands, except for per share data) | | | 2021 | | | 2020 | | | 2020 | | | 2019 | | | 2018 |

Per Share Data (Common Stock) | | | | | | | | | | | |||||

Earnings: | | | | | | | | | | | |||||

Basic | | | $2.47 | | | $0.76 | | | $1.29 | | | $1.37 | | | $0.65 |

Diluted(2) | | | $2.34 | | | $0.76 | | | $1.28 | | | $1.37 | | | $0.65 |

Book value(3) | | | $7.90 | | | $4.73 | | | $5.30 | | | $3.80 | | | $2.74 |

Tangible book value(1) | | | $7.90 | | | $4.73 | | | $5.30 | | | $3.80 | | | $2.74 |

| | | September 30, | | | December 31, | ||||||||||

Selected Performance Metrics | | | 2021 | | | 2020 | | | 2020 | | | 2019 | | | 2018 |

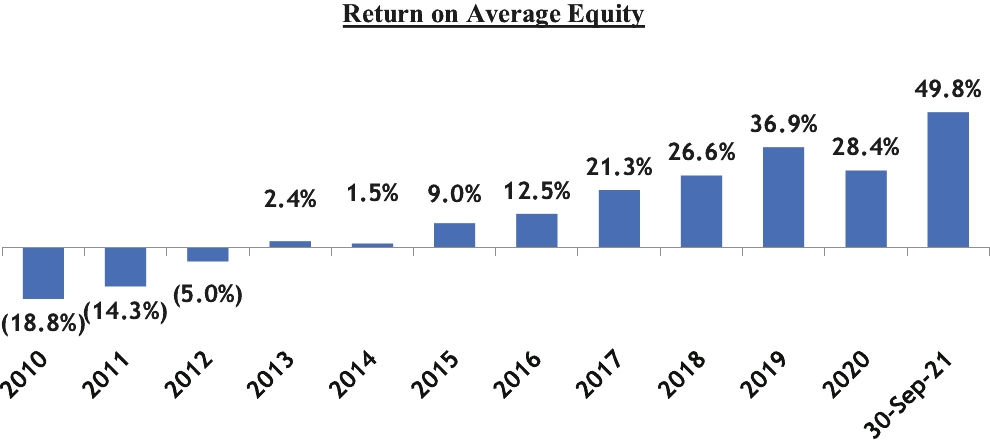

Return on average assets(4)(7) | | | 8.7% | | | 3.5% | | | 4.5% | | | 6.6% | | | 4.5% |

Return on average equity(4)(7) | | | 49.8% | | | 23.7% | | | 28.4% | | | 36.9% | | | 26.6% |

Average yield on loans(5) | | | 18.0% | | | 14.8% | | | 14.1% | | | 19.3% | | | 10.9% |

Average cost of deposits(5) | | | 1.2% | | | 2.0% | | | 1.9% | | | 2.0% | | | 1.6% |

Net interest margin(5) | | | 14.5% | | | 11.2% | | | 11.0% | | | 14.1% | | | 8.1% |

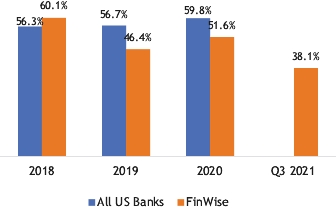

Efficiency ratio(1) | | | 38.1% | | | 52.7% | | | 51.6% | | | 46.4% | | | 60.1% |

Noninterest income to total revenue(6) | | | 41.0% | | | 35.8% | | | 34.1% | | | 41.0% | | | 54.5% |

Noninterest income to average assets(7) | | | 9.2% | | | 5.9% | | | 5.8% | | | 9.5% | | | 9.6% |

Average equity to average assets(7) | | | 17.5% | | | 14.9% | | | 16.0% | | | 17.8% | | | 16.7% |

Total shareholders’ equity to total assets | | | 20.4% | | | 12.9% | | | 14.4% | | | 18.7% | | | 16.6% |

Tangible shareholders’ equity to tangible assets(1) | | | 20.4% | | | 12.9% | | | 14.4% | | | 18.7% | | | 16.6% |

Employees at period end | | | 113 | | | 89 | | | 95 | | | 86 | | | 54 |

| | | As of and For the Nine Months Ended September 30, | | | As of and For the Years Ended December 31, | ||||||||||

($ in thousands) | | | 2021 | | | 2020 | | | 2020 | | | 2019 | | | 2018 |

Selected Loan Metrics | | | | | | | | | | | |||||

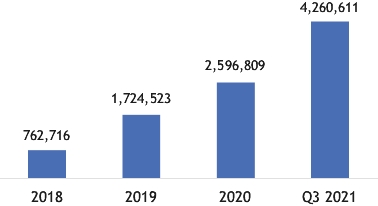

Number of loans originated | | | 877,328 | | | 410,318 | | | 749,746 | | | 522,981 | | | 145,839 |

Amount of loans originated | | | $4,260,611 | | | $1,745,882 | | | $2,596,809 | | | $1,724,523 | | | $762,716 |

Number of loans serviced | | | 1,422 | | | 2,158 | | | 2,045 | | | 1,482 | | | 1,252 |

| | | | | | | | | | | ||||||

Asset Quality Ratios | | | | | | | | | | | |||||

Nonperforming loans | | | $757 | | | $940 | | | $831 | | | $1,108 | | | $87 |

Nonperforming loans to total assets | | | 0.2% | | | 0.3% | | | 0.3% | | | 0.6% | | | 0.1% |

Net charge offs to average loans | | | 1.1% | | | 2.0% | | | 1.7% | | | 2.3% | | | 0.2% |

Allowance for loan losses to loans held for investment | | | 5.2% | | | 3.0% | | | 2.6% | | | 4.1% | | | 2.1% |

Allowance for loan losses to total loans | | | 3.9% | | | 2.5% | | | 2.4% | | | 3.3% | | | 2.0% |

Allowance for loan losses to total loans (less PPP loans)(1) | | | 3.9% | | | 4.5% | | | 4.0% | | | 3.3% | | | 2.0% |

Net charge-offs | | | $2,095 | | | $2,737 | | | $3,559 | | | $2,492 | | | $163 |

| | | September 30, | | | December 31, | ||||||||||

Capital Ratios8 | | | 2021 | | | 2020 | | | 2020 | | | 2019 | | | 2018 |

Leverage ratio (under CBLR) | | | 19.5% | | | 16.3% | | | 16.6% | | | — | | | — |

Tier 1 leverage ratio (Bank) | | | — | | | — | | | — | | | 16.2% | | | 15.7% |

Tier 1 risk-based capital ratio (Bank) | | | — | | | — | | | — | | | 19.3% | | | 19.4% |

Total risk-based capital ratio (Bank) | | | — | | | — | | | — | | | 20.5% | | | 20.6% |

Common equity Tier 1 (Bank) | | | — | | | — | | | — | | | 19.3% | | | 19.4% |

| (1) | These measures are not measures recognized under United States generally accepted accounting principles, or GAAP, and are therefore considered to be non-GAAP financial measures. See “GAAP Reconciliation and Management Explanation of Non-GAAP Financial Measures” for a reconciliation of these measures to their most comparable GAAP measures. Tangible shareholders’ equity is defined as total shareholders’ equity less goodwill and other intangible assets. The most directly comparable GAAP financial measure is total shareholder’s equity. We had no goodwill or other intangible assets as of any of the dates indicated. We have not considered loan servicing rights as an intangible asset for purposes of this calculation. As a result, tangible shareholders’ equity is the same as total shareholders’ equity as of each of the dates indicated. The efficiency ratio is defined as total noninterest expense divided by the sum of net interest income and noninterest |

| (2) | We calculated our diluted earnings per share for each year shown as our net income divided by the weighted average number of shares of our common stock outstanding during the relevant period adjusted for the dilutive effect of outstanding options to purchase shares of our common stock. See Note 16 to our audited consolidated financial statements appearing elsewhere in this prospectus for more information regarding the dilutive effect. We calculated earnings per share on a basic and diluted basis using the following outstanding share amounts: |

| | | For the Nine Months Ended September 30, | | | For the Years Ended December 31, | ||||||||||

Share data | | | 2021 | | | 2020 | | | 2020 | | | 2019 | | | 2018 |

Weighted average shares outstanding, basic | | | 8,177,575 | | | 8,021,902 | | | 8,025,390 | | | 7,038,896 | | | 6,208,840 |

Weighted average shares outstanding, diluted | | | 8,630,356 | | | 8,038,545 | | | 8,069,634 | | | 7,053,354 | | | 6,208,842 |

Shares outstanding at end of period | | | 8,746,110 | | | 8,660,334 | | | 8,660,334 | | | 8,709,756 | | | 7,013,202 |

| (3) | Book value per share equals our total shareholders’ equity as of the date presented divided by the number of shares of our common stock outstanding as of the date presented. The number of shares of our common stock outstanding as of September 30, 2021 and December 31, 2020, 2019 and 2018 has been presented in note (2) above. |

| (4) | We have calculated our return on average assets and return on average equity for a year by dividing our net income for that year by our average assets and average equity, as the case may be, for that year. |

| (5) | We calculate average yield on loans by dividing loan interest income by average loans. We calculate average cost of deposits by dividing deposit expense by average interest-earning deposits. We calculate our average loans and average interest-earning deposits for a year by dividing the sum of our total loans balance or interest-earning deposit balance, as the case may be, as of the close of business on each day in the relevant year and dividing by the number of days in the year. Net interest margin represents net interest income divided by average interest-earning assets. Loan fees are included in interest income on loans and represent approximately $3.2 million (including approximately $1.8 million in fees related to PPP loans) and $1.1 million (including approximately $0.5 million in fees related to PPP loans) for the nine months ended September 30, 2021 and 2020, and $1.4 million (including approximately $1.2 million in fees related to PPP loans), $0.9 million, and $0.6 million for the years ended December 31, 2020, December 31, 2019, and December 31, 2018, respectively. |

| (6) | We calculate the ratio of noninterest income to total revenue as noninterest income (excluding securities gains or losses) divided by the sum of net interest income plus noninterest income (excluding securities gains or losses). |

| (7) | We calculate our average assets and average equity for a year by dividing the sum of our total asset balance or total shareholder’s equity balance, as the case may be, as of the beginning of the relevant year and at the end of the relevant year, and dividing by two. We calculate our average assets and average equity for a given reporting period representing a less than annual period by dividing (a) the sum of our total asset balance or total shareholder’s equity balance, as the case may be, as of the close of business (i) at the beginning of the relevant reporting period and (ii) at the ending of the relevant reporting period, by (b) two. |

| (8) | Under the prompt corrective action rules, an institution is deemed “well capitalized” if its leverage ratio, Common Equity Tier 1 ratio, Tier 1 Capital ratio, and Total Capital ratio meet or exceed 5%, 6.5%, 8%, and 10%, respectively. On September 17, 2019, the federal banking agencies jointly finalized a rule intending to simplify the regulatory capital requirements described above for qualifying community banking organizations that opt into the Community Bank Leverage Ratio (“CBLR”) framework, as required by Section 201 of Economic Growth, the Regulatory Relief and Consumer Protection Act (the “Regulatory Relief Act”). The Bank has elected to opt into the Community Bank Leverage Ratio framework starting in 2020. Under these new capital requirements, as temporarily amended by the CARES Act, the Bank must maintain a leverage ratio greater than 8% for 2020 and 8.5% for 2021. See these changes more fully discussed under “Supervision and Regulation—The Regulatory Relief Act.” |

| • | “Tangible shareholders’ equity” is defined as total shareholders’ equity less goodwill and other intangible assets. The most directly comparable GAAP financial measure is total shareholder’s equity. We had no goodwill or other intangible assets as of any of the dates indicated. We have not considered loan servicing rights as an intangible asset for purposes of this calculation. As a result, tangible shareholders’ equity is the same as total shareholders’ equity as of each of the dates indicated. |

| • | “Tangible book value per share” is defined as book value per share less goodwill and other intangible assets, divided by the outstanding number of common shares at the end of each period. The most directly comparable GAAP financial measure is book value per share. We had no goodwill or other intangible assets as of any of the dates indicated. We have not considered loan servicing rights as an intangible asset for purposes of this calculation. As a result, tangible book value per share is the same as book value per share as of each of the dates indicated. |

| • | “Efficiency ratio” is defined as total noninterest expense divided by the sum of net interest income and noninterest income. We believe this measure is important as an indicator of productivity because it shows the amount of revenue generated for each dollar spent. |

| • | “Tangible shareholders’ equity to tangible assets” is defined as total shareholders’ equity less goodwill and other intangible assets, divided by total assets less goodwill and other intangible assets. The most directly comparable GAAP financial measure is total shareholders’ equity to total assets. We had no goodwill or other intangible assets as of any of the dates indicated. We have not considered loan servicing rights as an intangible asset for purposes of this calculation. As a result, tangible shareholders’ equity to tangible assets is the same as total shareholders’ equity to total assets as of each of the dates indicated. |

| • | “Allowance for loan losses to total loans (less PPP loans)” is defined as the allowance for loan losses divided by total loans minus PPP loans. The most directly comparable GAAP financial measure is allowance for loan losses to total loans. We believe this measure is important because the allowance for loan losses will not be utilized for PPP loans since they are 100% guaranteed by the SBA. We believe that the non-GAAP measure more accurately discloses the proportion of loans that might utilize the allowance for loan losses consistently with periods prior to the presence of PPP loans. |

| • | “Total nonperforming assets and troubled debt restructurings to total assets (less PPP loans)” is defined as the sum of nonperforming assets and troubled debt restructurings divided by total assets minus PPP loans. The most directly comparable GAAP financial measure is the sum of nonperforming assets and troubled debt restructurings to total assets. We believe this measure is important because we believe that PPP loans will not be included in nonperforming assets or troubled debt restructurings since PPP loans are 100% guaranteed by the SBA. We believe that the non-GAAP measure more accurately discloses the proportion of nonperforming assets and troubled debt restructurings to total assets consistently with periods prior to the presence of PPP loans. |

| | | Nine Months Ended September 30, | | | Year Ended December 31, | ||||||||||

($ in thousands) | | | 2021 | | | 2020 | | | 2020 | | | 2019 | | | 2018 |

Noninterest expense | | | $21,140 | | | $16,092 | | | $21,749 | | | $15,685 | | | $9,538 |

Net interest income | | | $32,706 | | | $19,589 | | | $27,750 | | | $19,946 | | | $7,227 |

Total noninterest income | | | $22,715 | | | $10,941 | | | $14,373 | | | $13,863 | | | $8,656 |

Adjusted operating revenue | | | $55,421 | | | $30,530 | | | $42,123 | | | $33,809 | | | $15,883 |

Efficiency ratio | | | 38.1% | | | 52.7% | | | 51.6% | | | 46.4% | | | 60.1% |

| | | As of September 30, | | | Year Ended December 31, | ||||||||||

($ in thousands) | | | 2021 | | | 2020 | | | 2020 | | | 2019 | | | 2018 |

Allowance for loan losses | | | $9,640 | | | $7,028 | | | $6,199 | | | $4,531 | | | $1,735 |

Total loans | | | $249,214 | | | $281,989 | | | $261,777 | | | $136,662 | | | $87,816 |

PPP loans | | | $2,303 | | | $126,625 | | | $107,145 | | | $0 | | | $0 |

Total loans less PPP loans | | | $246,911 | | | $155,364 | | | $154,632 | | | $136,662 | | | $87,816 |

Allowance for loan losses to total loans (less PPP loans) | | | 3.9% | | | 4.5% | | | 4.0% | | | 3.3% | | | 2.0% |

| | | As of September 30, | | | Year Ended December 31, | ||||||||||

($ in thousands) | | | 2021 | | | 2020 | | | 2020 | | | 2019 | | | 2018 |

Total nonperforming assets and troubled debt restructuring | | | $864 | | | $1,119 | | | $1,701 | | | $1,108 | | | $87 |

Total assets | | | $338,316 | | | $318,340 | | | $317,515 | | | $177,062 | | | $116,085 |

PPP loans | | | $2,303 | | | $126,625 | | | $107,145 | | | $0 | | | $0 |

Total assets less PPP loans | | | $336,013 | | | $191,715 | | | $210,370 | | | $177,062 | | | $116,085 |

Total nonperforming assets and troubled debt restructurings to total assets (less PPP loans) | | | 0.3% | | | 0.6% | | | 0.8% | | | 0.6% | | | 0.1% |

| • | demand for our products and services may decline, making it difficult to grow assets and income; |

| • | if the economy is unable to fully reopen, and high levels of unemployment continue for an extended period of time, loan delinquencies, requests for deferrals and modifications, problem assets, and foreclosures may increase, resulting in increased charges and reduced income; |

| • | collateral for loans, especially real estate, may decline in value, which could cause loan losses to increase; |

| • | our allowance for loan losses may have to be increased if borrowers experience financial difficulties beyond forbearance periods or if the federal government fails to guarantee or forgive our customers’ PPP loans, which will adversely affect our net income; |

| • | the net worth and liquidity of loan guarantors may decline, impairing their ability to honor commitments to us; |

| • | as the result of the decline in the Federal Reserve Board’s target federal funds rate to near 0%, the yield on our assets may continue to decline to a greater extent than the decline in our cost of interest-bearing liabilities, reducing our net interest margin and spread and reducing net income; |

| • | it may be challenging to grow our core business if the recovery from the economic impact caused by Covid-19 is slow or unpredictable; |

| • | our PPP loan customers may fail to qualify for PPP loan forgiveness, or we may experience other uncertainties or losses related to our PPP loans; |

| • | our cybersecurity risks are increased as the result of an increase in the number of employees working remotely; |

| • | we rely on third party vendors for certain services and the unavailability of a critical service due to the Covid-19 outbreak could have an adverse effect on us; and |

| • | FDIC premiums may increase if the agency experiences additional resolution costs. |

| • | possible constraints on liquidity and capital, due to supporting client activities or regulatory actions, |

| • | higher operating costs, increased cybersecurity risks and a potential loss of productivity while we work remotely, and |

| • | higher level of loan modifications and distressed credit management. |

| • | navigating complex and evolving regulatory and competitive environments; |

| • | increasing the number of borrowers and investors utilizing a marketplace; |

| • | verifying borrowers’ creditworthiness and ensuring accurately and appropriately priced loans; |

| • | the use of alternative credit models that pose regulatory uncertainties, or otherwise increase regulatory risk; |

| • | increasing the volume of loans facilitated through a marketplace and transaction fees received for matching borrowers and investors through a marketplace; |

| • | entering into new markets and introducing new loan products; |

| • | monitoring business activities to avoid being deemed an investment company or being required to register as a broker-dealer and the increased cost and regulation associated therewith; |

| • | continuing to revise proprietary credit decision-making and scoring models, particularly in the face of changing macro and economic conditions; |

| • | continuing to develop, maintain and scale a platform; |

| • | conduct debt collection and servicing activities in compliance with federal, state and municipal laws; |

| • | effectively training internal employees, third-party vendors and service providers in requirements imposed by federal, state and municipal laws and ensuring said employees, vendors and service providers comply with said laws; |

| • | effectively using limited personnel and technology resources; |

| • | effectively maintaining and scaling financial and risk management controls and procedures; |

| • | maintaining the security of the platform and the confidentiality of the information provided and utilized across the platform; and |

| • | attracting, integrating and retaining an appropriate number of qualified employees. |

| • | difficulty in estimating the value of any target company; |

| • | investing time and incurring expense associated with identifying and evaluating potential investments or acquisitions and negotiating potential transactions, resulting in our attention being diverted from the operation of our existing business; |

| • | the lack of history among our management team in working together on acquisitions and related integration activities; |

| • | obtaining necessary regulatory approvals, which we may have difficulty obtaining or be unable to obtain; |

| • | the time, expense and difficulty of integrating the operations and personnel of any combined businesses; |

| • | unexpected asset quality problems with acquired companies; |

| • | inaccurate estimates and judgments used to evaluate credit, operations, management and market risks with respect to any target institution or assets; |

| • | risks of impairment to goodwill or other-than-temporary impairment of investment securities; |

| • | potential exposure to unknown or contingent liabilities of banks and businesses we acquire; |

| • | an inability to realize expected synergies or returns on investment; |

| • | potential disruption of our ongoing banking business; |

| • | maintaining adequate regulatory capital; and |

| • | loss of key employees, key customers or key business counterparties following our investment or acquisition. |

| • | actual or anticipated fluctuations in our operating results, financial condition or asset quality; |

| • | changes in general economic or business conditions; |

| • | the effects of, and changes in, trade, monetary and fiscal policies, including the interest rate policies of the Federal Reserve; |

| • | publication of research reports about us, our competitors or the financial services industry generally, or changes in, or failure to meet, securities analysts’ estimates of our financial and operating performance, or lack of research reports by industry analysts or ceasing of coverage; |

| • | operating and stock price performance of companies that investors deem comparable to us; |

| • | additional or anticipated sales of our common stock or other securities by us or our existing shareholders; |

| • | additions or departures of key personnel; |

| • | perceptions in the marketplace regarding our competitors or us; |

| • | significant acquisitions or business combinations, strategic relationships, joint ventures or capital commitments by or involving our competitors or us; |

| • | other economic, competitive, governmental, regulatory or technological factors affecting our operations, pricing, products and services; and |

| • | other news, announcements or disclosures (whether by us or others) related to us, our competitors, our core markets or the financial services industry. |

| • | because the Company is a legal entity separate and distinct from the Bank and does not have any stand-alone operations, our ability to pay dividends depends on the ability of the Bank to pay dividends to us, and the FDIC, the UDFI and Utah state law may, under certain circumstances, restrict the payment of dividends to us from the Bank; |

| • | Federal Reserve policy requires bank holding companies to pay cash dividends on common shares only out of net income available over the past year and only if prospective earnings retention is consistent with the organization’s expected future needs and financial condition; and |

| • | our board of directors may determine that, even though funds are available for dividend payments, retaining the funds for internal uses, such as expansion of our operations, is necessary or appropriate in light of our business plan and objectives. |

| • | conditions relating to the Covid-19 pandemic, including the severity and duration of the associated economic slowdown either nationally or in our market areas, and the response of governmental authorities to the Covid-19 pandemic and our participation in Covid-19-related government programs such as the PPP; |

| • | system failure or cybersecurity breaches of our network security; |

| • | the success of the financial technology industry, the development and acceptance of which is subject to a high degree of uncertainty, as well as the continued evolution of the regulation of this industry; |

| • | our ability to keep pace with rapid technological changes in the industry or implement new technology effectively; |

| • | our reliance on third-party service providers for core systems support, informational website hosting, internet services, online account opening and other processing services; |

| • | general economic conditions, either nationally or in our market areas (including interest rate environment, government economic and monetary policies, the strength of global financial markets and inflation and deflation), that impact the financial services industry and/or our business; |

| • | increased competition in the financial services industry, particularly from regional and national institutions and other companies that offer banking services; |

| • | our ability to measure and manage our credit risk effectively and the potential deterioration of the business and economic conditions in our primary market areas; |

| • | the adequacy of our risk management framework; |

| • | the adequacy of our allowance for loan losses; |

| • | the financial soundness of other financial institutions; |

| • | new lines of business or new products and services; |

| • | changes in SBA rules, regulations and loan products, including specifically the Section 7(a) program, changes in SBA standard operating procedures or changes to the status of the Bank as an SBA Preferred Lender; |

| • | changes in the value of collateral securing our loans; |

| • | possible increases in our levels of nonperforming assets; |

| • | potential losses from loan defaults and nonperformance on loans; |

| • | our ability to protect our intellectual property and the risks we face with respect to claims and litigation initiated against us; |

| • | the inability of small- and medium-sized businesses to whom we lend to weather adverse business conditions and repay loans; |

| • | our ability to implement aspects of our growth strategy and to sustain our historic rate of growth; |

| • | our ability to continue to originate, sell and retain loans, including through our Strategic Programs; |

| • | the concentration of our lending and depositor relationships through Strategic Programs in the financial technology industry generally; |

| • | our ability to attract additional merchants and retain and grow our existing merchant relationships; |

| • | interest rate risk associated with our business, including sensitivity of our interest earning assets and interest bearing liabilities to interest rates, and the impact to our earnings from changes in interest rates; |

| • | the effectiveness of our internal control over financial reporting and our ability to remediate any future material weakness in our internal control over financial reporting; |

| • | potential exposure to fraud, negligence, computer theft and cyber-crime and other disruptions in our computer systems relating to our development and use of new technology platforms; |

| • | our dependence on our management team and changes in management composition; |

| • | the sufficiency of our capital, including sources of capital and the extent to which we may be required to raise additional capital to meet our goals; |

| • | compliance with laws and regulations, supervisory actions, the Dodd-Frank Act, the Regulatory Relief Act, capital requirements, the Bank Secrecy Act, anti-money laundering laws, predatory lending laws, and other statutes and regulations; |

| • | changes in the laws, rules, regulations, interpretations or policies relating to financial institutions, accounting, tax, trade, monetary and fiscal matters; |

| • | our ability to maintain a strong core deposit base or other low-cost funding sources; |

| • | results of examinations of us by our regulators, including the possibility that our regulators may, among other things, require us to increase our allowance for loan losses or to write-down assets; |

| • | our involvement from time to time in legal proceedings, examinations and remedial actions by regulators; |

| • | further government intervention in the U.S. financial system; |

| • | the ability of our Strategic Program service providers to comply with regulatory regimes, including laws and regulations applicable to consumer credit transactions, and our ability to adequately oversee and monitor our Strategic Program service providers; |

| • | our ability to maintain and grow our relationships with our Strategic Program service providers; |

| • | natural disasters and adverse weather, acts of terrorism, pandemics, an outbreak of hostilities or other international or domestic calamities, and other matters beyond our control; |

| • | compliance with requirements associated with being a public company; |

| • | level of coverage of our business by securities analysts; |

| • | the effective use of proceeds from this offering; |

| • | future equity and debt issuances; and |

| • | other factors that are discussed in the section entitled “Risk Factors,” beginning on page 26. |

| • | on an actual basis; and |

| • | on an as adjusted basis to give effect to the issuance and sale by us of shares of common stock in this offering and our receipt of the net proceeds therefrom (assuming the underwriters do not exercise their option to purchase additional shares) at an assumed initial public offering price of $ per share, which is the midpoint of the price range set forth on the cover page of this prospectus, after deducting underwriting discounts and estimated offering expenses payable by us. |

| | | September 30, 2021 | ||||

($ in thousands, except per share data) | | | Actual | | | As Adjusted(1) |

Cash and cash equivalents | | | $68,106 | | | $ |

PPP Liquidity Facility | | | 2,259 | | | |

| | | | | |||

Shareholders’ equity | | | | | ||

Preferred stock, $.001 par value, 4,000,000 authorized; no shares issued and outstanding as of September 30, 2021, actual and adjusted | | | — | | | — |

Common stock, $.001 par value, 40,000,000 shares authorized; 8,746,110 shares issued and outstanding as of September 30, 2021, actual and adjusted, respectively | | | 9 | | | |

Additional paid-in-capital | | | 18,647 | | | |

Retained earnings | | | 50,482 | | | |

Total shareholders’ equity | | | $69,138 | | | $ |

Total capitalization | | | $71,397 | | | $ |

| | | | | |||

Company capital ratios: | | | | | ||

Leverage ratio(2) | | | 19.5% | | | % |

Total equity to total assets | | | 20.4% | | | % |

Tangible shareholders’ equity to tangible assets(3) | | | 20.4% | | | % |

| | | | | |||

Per Share: | | | | | ||

Book value per share | | | $7.90 | | | $ |

Tangible book value per share(3) | | | $7.90 | | | $ |

| (1) | Each $1.00 increase (decrease) in the assumed initial public offering price of $ per share (the midpoint of the price range set forth on the cover page of this prospectus) would increase (decrease) our as adjusted total shareholders’ equity and total capitalization by approximately $ million, assuming no change to the number of shares of common stock being offered hereby as set forth on the cover page of this prospectus, and after deducting underwriting discounts and estimated offering expenses payable by us. The As Adjusted leverage ratio assumes all net proceeds from this offering will be contributed to the Bank as regulatory capital. Although we intend to contribute substantially all net proceeds from this offering to the Bank as regulatory capital, our management will retain broad discretion to allocate the net proceeds of this offering and may not in fact contribute substantially all net proceeds from this offering to the Bank as regulatory capital. |

| (2) | See discussion under “Supervision and Regulation—The Regulatory Relief Act” describing the regulatory capital framework applicable to the Bank. |

| (3) | These measures are not measures recognized under GAAP and are therefore considered to be non-GAAP financial measures. See “GAAP Reconciliation and Management Explanation of Non-GAAP Financial Measures” for a reconciliation of these measures to their most comparable GAAP measures. |

Assumed initial public offering price per share | | | $ |

Tangible book value per share of common stock at September 30, 2021 | | | $7.90 |

Increase in tangible book value per share of common stock attributable to this offering | | | $ |

As adjusted tangible book value per share of common stock after this offering | | | $ |

Dilution per share of common stock to new investors in this offering | | | $ |

| | | Shares Purchased | | | Total Consideration (Dollars in thousands) | | | Average Price | |||||||

| | | Number | | | Percent | | | Amount | | | Percent | | | Per Share | |

Shareholders as of September 30, 2021 | | | 8,746,110 | | | % | | | $ | | | % | | | $ |

New investors in this offering | | | | | % | | | | | % | | | $ | ||

Total | | | | | % | | | $ | | | % | | | $ | |

| • | our strategic relationships with third party loan origination platforms, many of whom use technology to facilitate loan origination, that allow us to capture a high volume of diverse loan origination and loan performance data from the billions of dollars of loans that we have originated, sold or held in four main lending areas; |

| • | our FinView™ Analytics Platform, including our enterprise data warehouse, which is a proprietary technology developed by us to enhance our ability to gather and interpret performance data for the loans originated by us and to help us identify attractive risk-adjusted market sectors; |

| • | our core deposits which, as of September 30, 2021 and December 31, 2020, constitute 79.3% and 91.5% of our funding sources (excluding the PPPLF), respectively and have been highly reliable and relatively low cost (our core deposits comprise the sum of demand deposits, NOW accounts, MMDA accounts, savings accounts, and time deposits under $250,000 that are not brokered deposits); and |

| • | our seasoned management team, which has considerable banking experience, particularly in our core lines of business. |

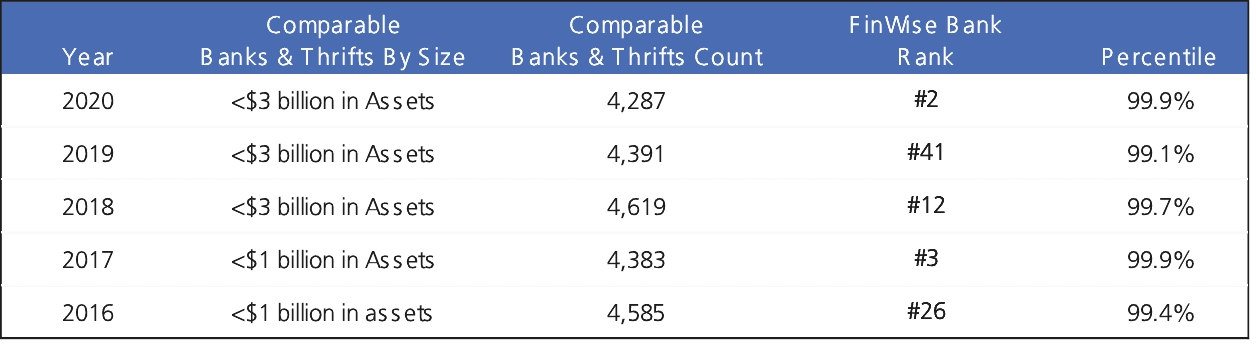

Year | | | Comparable Banks & Thrifts By Size | | | Comparable Banks & Thrifts Count | | | FinWise Bank Rank | | | Percentile |

2020 | | | <$3 billion in Assets | | | 4,287 | | | #2 | | | 99.9% |

2019 | | | <$3 billion in Assets | | | 4,391 | | | #41 | | | 99.1% |

2018 | | | <$3 billion in Assets | | | 4,619 | | | #12 | | | 99.7% |

2017 | | | <$1 billion in Assets | | | 4,383 | | | #3 | | | 99.9% |

2016 | | | <$1 billion in Assets | | | 4,585 | | | #26 | | | 99.4% |

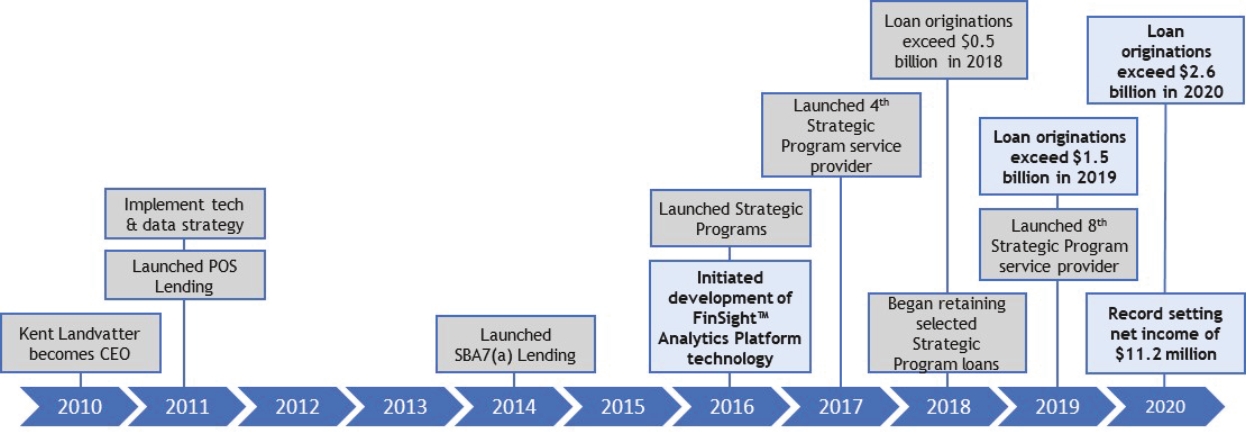

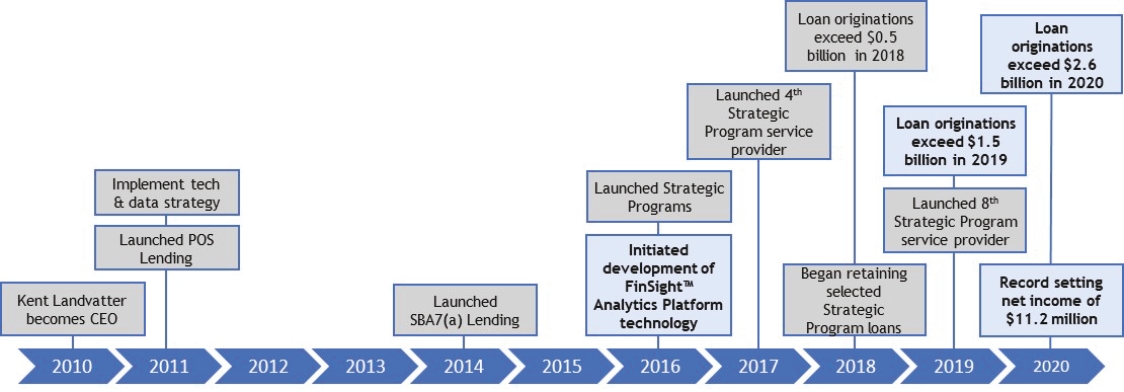

| - | 2011 |

| ○ | Raised approximately $0.3 million through the private placement of our common stock to position the Company for growth |

| ○ | Enhanced Bank control environment by revising policies and procedures, establishing oversight committees, and developing a standardized process for the Bank to launch new programs |

| ○ | In August, the FDIC Cease and Desist Order was removed |

| ○ | Resumed lending in the local community after the capital raise and removal of FDIC Cease and Desist Order |

| ○ | Launched our POS lending program |

| ○ | Launched our commercial leasing program |

| ○ | Introduced our strategy for using technology and data as a competitive advantage |

| - | 2013 |

| ○ | Returned to profitability |

| - | 2014 |

| ○ | Raised approximately $0.2 million through the private placement of our common stock to fund Company growth |

| ○ | Launched our SBA 7(a) lending program and began receiving loan referrals from BFG, a nationally significant referral source of SBA loans and the Bank’s primary SBA referral source |

| - | 2015 |

| ○ | Mr. Javvis Jacobson joined the Company and the Bank as Executive Vice President and Chief Financial Officer to lead our financial and day-to-day operational matters |

| - | 2016 |

| ○ | Mr. David Tilis, Senior Vice President and Chief Strategy Officer, joined the Bank’s management team to lead the launch of our Strategic Programs |

| ○ | Managed one Strategic Program platform at year end as a result of launching one new third-party loan origination platform focused on unsecured, closed-end debt consolidation credit products |

| ○ | Launched the initial development of FinView™, including our initial development of our data warehouse, in conjunction with the start of our Strategic Programs |

| ○ | Raised approximately $0.7 million through the private placement of our common stock to support Company growth |

| ○ | Ranked #26 by S&P in top 100 best performing banks and thrifts under $1 billion in total assets |

| - | 2017 |

| ○ | Managed one Strategic Program platform at year end as a result of launching one new third party loan origination platform focused on unsecured, closed-end, debt consolidation credit products |

| ○ | Further developed FinView™ to include the use of the first Application Programming Interface (“API”) to connect with our Strategic Program service providers to facilitate credit decisioning and funding |

| ○ | Raised approximately $2.7 million through the private placement stock to support Company growth |

| ○ | Ranked #3 by S&P in top 100 best performing banks and thrifts under $1 billion in total assets |

| - | 2018 |

| ○ | Opened a loan production office in Rockville Centre, New York primarily to support our Strategic Programs and SBA 7(a) lending programs |

| ○ | Mr. James Noone joined the Bank as Executive Vice President and Chief Credit Officer and implemented comprehensive processes leading to a significant expansion of our SBA 7(a) lending program |

| ○ | Managed seven Strategic Program platforms at year end as a result of launching three new third-party loan origination platforms which were focused on unsecured, closed-end, consumer installment credit products |

| ○ | Commenced credit analyses that now form the basis of FinView™ and, as a result, we began retaining selected Strategic Program loans |

| ○ | Raised approximately $4.0 million through the private placement of our common stock to support Company growth |

| ○ | Ranked #12 by S&P in top 100 best performing banks and thrifts under $3 billion in total assets |

| - | 2019 |

| ○ | Managed eight Strategic Program platforms at year end as a result of launching one new third-party loan origination platform which was focused on unsecured, closed-end, consumer installment credit products |

| ○ | Continued the buildout of our credit analyses that now form the basis of FinView™ and, as a result, we began retaining additional Strategic Program loans |

| ○ | To further solidify our mutually beneficial relationship with BFG, the Company issued additional shares of its common stock, representing 10.9% of the Company’s outstanding common stock at the time of purchase, to certain members of BFG in exchange for certain of their interests in BFG, representing a 10.0% aggregate membership interest in BFG |

| ○ | Ranked #41 by S&P in top 100 best performing banks and thrifts under $3 billion in total assets |

| ○ | Ranked 9th largest SBA 7(a) originator in the state of New York |

| - | 2020 |

| ○ | Managed eight Strategic Program platforms at year end as a result of launching one new third-party loan origination platform which was focused on commercial working capital credit products and the closure, due to the Covid-19 pandemic, of one third-party loan origination platform launched in 2017 which was focused on commercial working capital credit products |

| ○ | Completed the buildout of our enterprise data warehouse which supports the compilation and storage of origination and servicing loan data for FinView™ |

| ○ | Began development of new API version 2.0 to optimize connection with our Strategic Program platforms to facilitate a more efficient onboarding experience for new Strategic Program launches and automation of certain regulatory compliance, enterprise risk management and testing programs oversight at the Bank |

| ○ | Issued warrants to acquire shares of Company common stock to certain members of BFG in exchange for a right of first refusal to acquire, and an option to purchase, any and all membership interests in BFG until January 1, 2028 |

| ○ | The Bank’s diversification strategy was tested by the Covid-19 pandemic. Our planned reduction in the at-risk loan portfolio during 2020 and our ability to generate income from multiple sources resulted in revenues and net income exceeding those generated in 2019 |

| ○ | Ms. Dawn Cannon joined the Bank’s management team as Executive Vice President and Chief Operating Officer to lead and expand our operational capabilities, including the growth of our POS lending programs as part of our long-term strategic plan |

| ○ | Ranked #2 by S&P in the top 100 best performing banks and thrifts under $3 billion in total assets |

| - | 2021 |

| ○ | Managed 11 Strategic Program platforms as of September 30, 2021 as a result of launching two new third-party platforms, one focused on unsecured student tuition credit products and one focused on unsecured, open-end, consumer credit products. |

| ○ | Loan originations exceeded $4.3 billion as of September 30, 2021. |

| ○ | Mr. Michael O’Brien joined the Company’s and the Bank’s management team as Executive Vice President, Chief Compliance and Risk Officer and Corporate Counsel to lead the newly combined Compliance and Risk Departments and to serve as our Corporate Counsel. |

| • | In SBA 7(a) lending, we lend to small business and professionals. Our credit risk management is augmented by the fact the loans are partially guaranteed by the SBA. We further mitigate our credit risk in this program by using data, such as the nature of the business, use of proceeds, length of time in business and management experience to help us target loans that we believe have lower credit risk. Our prudent underwriting, closing and servicing processes are essential to effective utilization of the SBA 7(a) program, as the SBA guaranty is conditioned upon proper underwriting, closing and servicing by the lender. |

| • | In our Strategic Program lending, we originate unsecured and secured consumer and business loans to borrowers with certain Bank-approved credit profiles. The credit profiles are based on specific predetermined underwriting criteria informed by our extensive data and analytics. While we sell the vast majority of loans in this lending program shortly after origination, the Bank may choose to retain a portion of the funded loans and/or receivables. Our credit risk is mitigated by focusing on amortizing loans, lending to borrowers with demonstrated ability to repay, and extending loans that are priced appropriately to the credit profile of the borrower (including credit history). Smaller loans are often unsecured and therefore rely more on predictive models that allow us to appropriately price credit based on probable losses. |

Return on Average Assets | | | Return on Average Equity |

| | | |

Net Interest Margin | | | Noninterest Income / Average Assets |

| | | |

NAICS Sub-Sector Code | | | Description | | | September 30, 2021 % of Total |

541 | | | Professional, Scientific and Technical Services | | | 15.9% |

454 | | | Non-Store Retailers (Electronic Shopping) | | | 15.6% |

423 | | | Merchant Wholesalers, Durable Goods | | | 8.5% |

621 | | | Ambulatory Health Care Services | | | 6.3% |

445 | | | Food and Beverage Stores (Grocery, Convenience) | | | 4.5% |

623 | | | Nursing and Residential Care Facilities | | | 4.4% |

448 | | | Clothing and Clothing Accessories Stores | | | 4.3% |

238 | | | Specialty Trade Contractors | | | 4.1% |

811 | | | Manufacturing Repair and Maintenance | | | 3.8% |

442 | | | Furniture and Home Furnishings Stores | | | 2.9% |

| | | All Other | | | 29.7% | |

Total | | | 100.0% | |||

| • | Strategic Programs: $100 billion in total available market based on industry data and estimates. Our estimation of the total available market for the Strategic Program business line is based on industry data for unsecured personal loans. We believe the total available market may be larger than this as the Bank offers Strategic Programs specific to POS lending and commercial lending which may not be accounted for in the above estimates. |

| • | SBA Lending $150 billion in total available market based on SBA agency reports. |

| • | POS Lending: $160 billion in total available market based on industry data and estimates. |

Asset Growth Rate (Over Prior Period) | | | Total Loan Originations ($000s) |

| | | |

| • | Kent Landvatter. Mr. Landvatter joined the Company and the Bank in September 2010 as the President and Chief Executive Officer. Mr. Landvatter has over 40 years of financial services and banking experience, including experience with distressed banks and serving as the president of two de novo banks, Comenity Capital Bank and Goldman Sachs Bank, USA. |

| • | Javvis Jacobson. Mr. Jacobson joined the Company and the Bank in March 2015 as the Executive Vice President and Chief Financial Officer. Mr. Jacobson has over 20 years of financial services experience, including at Deloitte, where he served for several years managing audits of financial institutions. Mr. Jacobson also served for several years as the Chief Financial Officer of Beehive Credit Union with over $190 million in assets. |

| • | James Noone. Mr. Noone joined the Bank in February 2018 and was named Executive Vice President and Chief Credit Officer in June 2018. Mr. Noone has 20 years of financial services experience including commercial and investment banking as well as private equity. Prior to joining the Bank, Mr. Noone served as Executive Vice President of Prudent Lenders, an SBA service provider from 2012 to 2018. |

| • | Dawn Cannon. Ms. Cannon joined the Bank in March 2020 as the Senior Operating Officer and was named Executive Vice President and Chief Operating Officer in July 2020. Ms. Cannon has over 17 years of banking experience, including serving as the Executive Vice President of Operations of EnerBank, an industrial bank that focused on lending programs similar to our POS lending program, where she was instrumental in building it from 23 to 285 full time employees and from $10 million to $1.4 billion in total assets. |

| • | Michael O’Brien. Mr. O’Brien joined the Company and the Bank in September 2021 as Executive Vice President, Chief Compliance and Risk Officer and Corporate Counsel. Mr. O’Brien has over 20 years of legal, compliance and risk management experience in the financial services industry. He practiced law in New York and Washington, D.C. with nationally recognized law firms prior to legal positions with E*TRADE Financial and Sallie Mae Bank. Mr. O’Brien also previously served as Chief Compliance Officer of EnerBank USA, a Utah industrial bank. He is currently licensed to practice law in Utah and Washington, D.C. |

| • | David Tilis. Mr. Tilis joined the Bank in March 2016 as a Vice President and Director of Specialty Lending and now serves as the Chief Strategy Officer and Senior Vice President. Mr. Tilis has over 15 years of financial services experience, including serving as a Vice President of Cross River Bank overseeing SBA lending and playing a significant role in strategic relationships. |

Year End 2020 Origination Volume | | | Loan Portfolio as of 12/31/20 |

| | |  |

Q3 2021 Origination Volume | | | Loan Portfolio as of 09/30/21 |

| | |  |

Q3 2021 Revenue by Business Line | |||

| |||

| | | September 30, | | | December 31, | |||||||

| | | 2021 | | | 2020 | |||||||

| | | Total Loans | | | % of Loans in Category of total loans | | | Total Loans | | | % of Loans in Category of total loans | |

SBA | | | $125,192 | | | 50.2% | | | $203,317 | | | 77.7% |

Commercial, non-real estate | | | 3,955 | | | 1.6% | | | 4,020 | | | 1.5% |

Residential real estate | | | 25,105 | | | 10.1% | | | 17,740 | | | 6.8% |

Strategic Program loans | | | 87,876 | | | 35.3% | | | 28,265 | | | 10.8% |

Commercial real estate | | | 2,357 | | | 0.9% | | | 2,892 | | | 1.1% |

Consumer | | | 4,729 | | | 1.9% | | | 5,543 | | | 2.1% |

Total | | | $249,214 | | | 100.0% | | | $261,777 | | | 100.0% |

| • | understanding the customer’s financial condition and ability to repay the loan; |

| • | evaluating management performance and expertise and industry experience; |

| • | verifying that the primary and secondary sources of repayment are adequate in relation to the amount and structure of the loan; |

| • | observing appropriate loan-to-value guidelines for collateral secured loans; |

| • | maintaining our targeted levels of diversification for the loan portfolio, both as to type of borrower and type of collateral; and |

| • | ensuring that each loan is properly documented with perfected liens on collateral. |

| • | whether the applicant has any other loans(s) (including through the PPP, SBA EIDL, other stimulus financing) that have repayment or contingent repayment requirements which could impact cash flow; |

| • | for commercial applicants, whether the business revenue and staffing levels have been impacted by the Covid-19 pandemic and whether business has a contingency plan for revenues and operations for a minimum of the next 18 months; |

| • | for individual applicants, whether his or her source of income has been or may be impacted; |

| • | how governmental restrictions, including stay-at-home orders, social distancing, travel, traffic flow, and trade limitations have impacted applicant’s business operations or personal cash flow; |

| • | whether historical financial information can be reasonably relied upon based on current market conditions; and |

| • | the impact current market conditions have on collateral adequacy. |

| • | Ensure the Safety of Principal—Bank investments are generally limited to investment-grade instruments that fully comply with all applicable regulatory guidelines and limitations. Allowable non-investment-grade instruments must be approved by the board of directors. |

| • | Income Generation—The Bank’s investment portfolio is managed to maximize income on invested funds in a manner that is consistent with the Bank’s overall financial goals and risk considerations. |

| • | Provide Liquidity—The Bank’s investment portfolio is managed to remain sufficiently liquid to meet anticipated funding demands either through declines in deposits and/or increases in loan demand. |

| • | Mitigate Interest Rate Risk—Portfolio strategies are used to assist the Bank in managing its overall interest rate sensitivity position in accordance with goals and objectives approved by our board of directors. |

Location | | | Owned/ Leased | | | Lease Expiration | | | Type of Office |

Murray, Utah | | | Leased | | | November 1, 2021 | | | Corporate Headquarters |

Sandy, Utah | | | Leased | | | July 31, 2024 | | | Retail Bank Branch |

Rockville Centre, New York | | | Leased | | | December 31, 2022 | | | Loan Production Office |

| | | For Nine Months Ended September 30, | | | For the Years Ended December 31, | ||||||||||

($ in thousands) | | | 2021 | | | 2020 | | | 2020 | | | 2019 | | | 2018 |

Interest income | | | $33,690 | | | $20,941 | | | $29,506 | | | $21,408 | | | $8,073 |

Interest expense | | | (984) | | | (1,352) | | | (1,756) | | | (1,462) | | | (846) |

Provision for loan losses | | | (5,536) | | | (5,234) | | | (5,234) | | | (5,288) | | | (980) |

Non-interest income | | | 22,715 | | | 10,941 | | | 14,373 | | | 13,863 | | | 8,656 |

Non-interest expense | | | (21,140) | | | (16,092) | | | (21,749) | | | (15,685) | | | (9,538) |

Provision for income taxes | | | (7,273) | | | (2,622) | | | (3,942) | | | (3,177) | | | (1,333) |

Net income | | | 21,472 | | | 6,582 | | | 11,198 | | | 9,659 | | | 4,032 |

| | | Nine Months Ended September 30, | ||||||||||||||||

| | | 2021 | | | 2020 | |||||||||||||

($ in thousands) | | | Average Balance | | | Interest | | | Average Yield/Rate | | | Average Balance | | | Interest | | | Average Yield/Rate |

Interest earning assets: | | | | | | | | | | | | | ||||||

Interest-bearing deposits with the Federal Reserve, non | | |||||||||||||||||

U.S. central banks and other banks | | | $50,303 | | | $36 | | | 0.1% | | | $45,147 | | | $193 | | | 0.6% |

Investment securities | | | 1,687 | | | 19 | | | 1.5% | | | 1,533 | | | 25 | | | 2.2% |

Loans held for sale | | | 50,212 | | | 14,908 | | | 39.6% | | | 17,073 | | | 6,963 | | | 54.4% |

Loans held for investment | | | 198,767 | | | 18,727 | | | 12.6% | | | 169,092 | | | 13,760 | | | 10.8% |

Total interest earning assets | | | 300,968 | | | 33,690 | | | 14.9% | | | 232,845 | | | 20,941 | | | 12.0% |

Less: allowance for loan losses | | | (6,908) | | | | | | | (6,689) | | | | | ||||

Non-interest earning assets | | | 14,522 | | | | | | | 7,718 | | | | | ||||

Total assets | | | $308,582 | | | | | | | $233,874 | | | | | ||||

Interest bearing liabilities: | | | | | | | | | | | | | ||||||

Demand | | | $5,604 | | | $38 | | | 0.9% | | | $2,234 | | | $48 | | | 2.9% |

Savings | | | 8,006 | | | 9 | | | 0.2% | | | 6,053 | | | 11 | | | 0.2% |

Money market accounts | | | 19,641 | | | 55 | | | 0.4% | | | 15,893 | | | 84 | | | 0.7% |

Certificates of deposit | | | 61,587 | | | 757 | | | 1.6% | | | 60,617 | | | 1,109 | | | 2.4% |

Total deposits | | | 94,838 | | | 859 | | | 1.2% | | | 84,797 | | | 1,252 | | | 2.0% |

Other borrowings | | | 48,133 | | | 125 | | | 0.3% | | | 37,973 | | | 100 | | | 0.4% |

Total interest bearing liabilities | | | 142,971 | | | 984 | | | 0.9% | | | 122,770 | | | 1,352 | | | 1.5% |

Non-interest bearing deposits | | | 100,704 | | | | | | | 71,741 | | | | | ||||

Non-interest bearing liabilities | | | 9,732 | | | | | | | 3,448 | | | | | ||||

Shareholders’ equity | | | 55,175 | | | | | | | 35,915 | | | | | ||||

Total liabilities and shareholders’ equity | | | $308,582 | | | | | | | $233,874 | | | | | ||||

Net interest income and interest rate spread | | | | | $32,706 | | | 14.0% | | | | | $19,589 | | | 10.5% | ||

Net interest margin | | | | | | | 14.5% | | | | | | | 11.2% | ||||

Ratio of average interest-earning assets to average interest- bearing liabilities | | | | | | | 210.5% | | | | | | | 189.7% | ||||

| | | Years Ended December 31, | |||||||||||||||||||||||||

| | | 2020 | | | 2019 | | | 2018 | |||||||||||||||||||

($ in thousands) | | | Average Balance | | | Interest | | | Average Yield/Rate | | | Average Balance | | | Interest | | | Average Yield/Rate | | | Average Balance | | | Interest | | | Average Yield/Rate |

Interest earning assets: | | | | | | | | | | | | | | | | | | | |||||||||

Interest-bearing deposits with the Federal Reserve, non | | ||||||||||||||||||||||||||

U.S. central banks and other banks | | | $43,892 | | | $201 | | | 0.5% | | | $33,290 | | | $664 | | | 2.0% | | | $17,673 | | | $313 | | | 1.8% |

Investment securities | | | 1,622 | | | 34 | | | 2.1% | | | 516 | | | 16 | | | 3.0% | | | 493 | | | 10 | | | 2.0% |

Loans held for sale | | | 20,154 | | | 10,560 | | | 52.4% | | | 12,249 | | | 7,782 | | | 63.5% | | | 5,120 | | | 2,409 | | | 47.0% |

Loans held for investment | | | 187,314 | | | 18,711 | | | 10.0% | | | 94,954 | | | 12,946 | | | 13.6% | | | 65,785 | | | 5,341 | | | 8.1% |

Total interest earning assets | | | 252,982 | | | 29,506 | | | 11.7% | | | 141,009 | | | 21,408 | | | 15.2% | | | 89,071 | | | 8,073 | | | 9.1% |

Less: allowance for loan losses | | | (6,706) | | | | | | | (2,708) | | | | | | | (1,087) | | | | | ||||||

Non-interest earning assets | | | 8,130 | | | | | | | 4,005 | | | | | | | 2,086 | | | | | ||||||

Total assets | | | $254,406 | | | | | | | $142,306 | | | | | | | $90,070 | | | | | ||||||

Interest bearing liabilities: | | | | | | | | | | | | | | | | | | | |||||||||

Demand | | | $3,237 | | | $62 | | | 1.9% | | | $222 | | | $— | | | 0.1% | | | $276 | | | $— | | | 0.2% |

Savings | | | 6,234 | | | 16 | | | 0.2% | | | 4,762 | | | 12 | | | 0.2% | | | 4,292 | | | 11 | | | 0.2% |

Money market accounts | | | 16,327 | | | 104 | | | 0.6% | | | 14,973 | | | 109 | | | 0.7% | | | 10,951 | | | 76 | | | 0.7% |

Certificates of deposit | | | 57,496 | | | 1,401 | | | 2.4% | | | 52,691 | | | 1,341 | | | 2.5% | | | 36,424 | | | 759 | | | 2.1% |

Total deposits | | | 83,294 | | | 1,583 | | | 1.9% | | | 72,648 | | | 1,462 | | | 2.0% | | | 51,943 | | | 846 | | | 1.6% |

Other borrowings | | | 49,044 | | | 173 | | | 0.4% | | | — | | | — | | | 0.0% | | | — | | | — | | | 0.0% |

Total interest bearing liabilities | | | 132,338 | | | 1,756 | | | 1.3% | | | 72,648 | | | 1,462 | | | 2.0% | | | 51,943 | | | 846 | | | 1.6% |

Non-interest bearing deposits | | | 80,537 | | | | | | | 41,866 | | | | | | | 21,430 | | | | | ||||||

Non-interest bearing liabilities | | | 3,941 | | | | | | | 3,888 | | | | | | | 1,581 | | | | | ||||||

Shareholders’ equity | | | 37,590 | | | | | | | 23,904 | | | | | | | 15,116 | | | | | ||||||