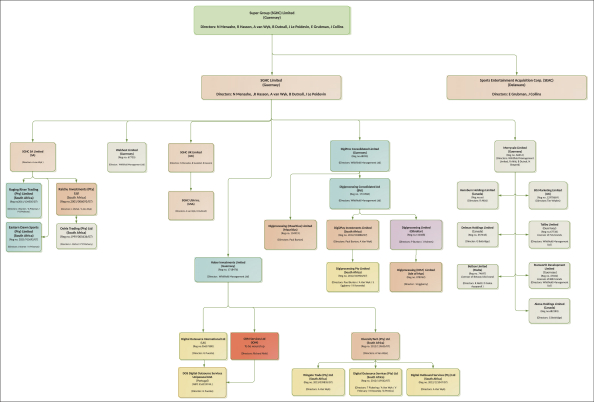

SPORTS ENTERTAINMENT ACQUISITION CORP.

NOTES TO FINANCIAL STATEMENTS

DECEMBER 31, 2020

(As Restated)

NOTE 1. DESCRIPTION OF ORGANIZATION AND BUSINESS OPERATIONS

Sports Entertainment Acquisition Corp. (the “Company”) was incorporated in Delaware on July 30, 2020. The Company was formed for the purpose of effecting a merger, capital stock exchange, asset acquisition, stock purchase, reorganization or similar business combination with one or more businesses (the “Business Combination”). The Company is not limited to a particular industry or sector for purposes of consummating a Business Combination. The Company is an early stage and emerging growth company and, as such, the Company is subject to all of the risks associated with early stage and emerging growth companies.

As of December 31, 2020, the Company had not commenced any operations. All activity for the period from July 30, 2020 (inception) through December 31, 2020 related to the Company’s formation and the initial public offering (“Initial Public Offering”), which is described below. The Company will not generate any operating revenues until after the completion of its initial Business Combination, at the earliest. The Company generates non-operating income in the form of interest income from the proceeds derived from the Initial Public Offering.

The registration statement for the Company’s Initial Public Offering was declared effective on October 1, 2020. On October 6, 2020 the Company consummated the Initial Public Offering of 40,000,000 units (the “Units” and, with respect to the shares of Class A common stock included in the Units sold, the “Public Shares”), at $10.00 per Unit, generating gross proceeds of $400,000,000 which is described in Note 4.

Simultaneously with the closing of the Initial Public Offering, the Company consummated the sale of an aggregate of 10,000,000 warrants (the “Private Placement Warrants”) at a price of $1.00 per Private Placement Warrant in private placements to Sports Entertainment Acquisition Holdings LLC (the “Sponsor”) and an affiliate of PJT Partners LP, generating gross proceeds of $10,000,000, which is described in Note 5.

On October 15, 2020, the Company issued an additional 5,000,000 Units issued for total gross proceeds of $50,000,000, in connection with the underwriters’ partial exercise of their over-allotment option. Simultaneously with the partial closing of their over-allotment option, the Company also consummated the sale of an additional 1,000,000 Private Placement Warrants at $1.00 per Private Placement Warrant, generating total proceeds of $1,000,000.

Transaction costs amounted to $25,318,504, consisting of $9,000,000 in cash underwriting fees, $15,750,000 of deferred underwriting fees and $568,504 of other offering costs.

Following the closing of the Initial Public Offering on October 6, 2020, and the partial exercise of the over-allotment option on October 15, 2020, an amount of $450,000,000 ($10.00 per Unit) from the net proceeds of the sale of the Units in the Initial Public Offering and the sale of the Private Placement Warrants was placed in a trust account (the “Trust Account”) located in the United States. The funds in the Trust Account are invested only in U.S. government securities, within the meaning set forth in Section 2(a)(16) of the Investment Company Act of 1940, as amended (the “Investment Company Act”), with a maturity of 185 days or less or in any open-ended investment company that holds itself out as a money market fund meeting certain conditions of Rule 2a-7 of the Investment Company Act, as determined by the Company, until the earlier of: (i) the completion of a Business Combination and (ii) the distribution of the funds held in the Trust Account, as described below.

Substantially all of the net proceeds of the Initial Public Offering and the sale of the Private Placement Warrants are intended to be applied generally toward consummating a Business Combination, and the Company’s management has broad discretion to identify targets for such a potential Business Combination and

F-7