As filed with the Securities and Exchange Commission on May 14, 2024

Registration No. 333-

Republic of the Marshall Islands (State or other jurisdiction of incorporation or organization) | | | 4412 (Primary Standard Industrial Classification Code Number) | | | N/A (I.R.S. Employer Identification No.) |

Filana R. Silberberg, Esq. Will Vogel, Esq. Watson Farley & Williams LLP 250 West 55th Street, 31st Floor New York, New York 10019 +1 (212) 922-2200 (telephone number) | | | Barry Grossman, Esq. Sarah Williams, Esq. Matthew Bernstein, Esq. Ellenoff Grossman & Schole LLP 1345 Avenue of the Americas, 11th Floor New York, United States 10105 +1 (212) 370-1300 (telephone number) |

| | | Emerging growth company ☒ |

| | | Per Share | | | Total | |

Initial public offering price | | | $ | | | $ |

Underwriting discounts and commissions(1) | | | $ | | | $ |

Proceeds to the Company, before expenses | | | $ | | | $ |

| (1) | The underwriter shall receive an underwriting discount of up to 6.9% per share for sales to investors in this offering. We have agreed that Maxim Group LLC will also receive a warrant to purchase a number of common shares that is equal to up to 6.9% of the aggregate number of common shares sold in this offering (up to 86,250 common shares, or up to 99,188 common shares if the underwriter exercises the over-allotment option in full), at an exercise price per share equal to 110% of the offering price, subject to certain anti-dilution adjustments (the “Representative’s Warrant”). The Representative’s Warrant will be non-exercisable for six (6) months from the date of effectiveness of the registration statement of which this prospectus forms a part and will expire three (3) years after such date. The Representative’s Warrant and the common shares issuable upon exercise of the Representative’s Warrant are also being registered under the registration statement of which this prospectus forms a part. We have also agreed to reimburse the underwriters for certain expenses. We refer you to the section entitled “Underwriting” of this prospectus for additional information regarding total compensation and other items of value payable to the underwriters. |

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | |

| • | The cyclicality and volatility of charter hire rates for dry bulk vessels. |

| • | Our dependence on an index-linked charter and the potential adverse effects of any future decrease in spot freight charter rates or indexes. |

| • | Over-supply of dry bulk vessel capacity, which may depress charter rates and vessel values. |

| • | The continuing decline in worldwide economic conditions. |

| • | Outbreaks of epidemic and pandemic diseases, including COVID-19, and any relevant governmental responses thereto. |

| • | Terrorist attacks and international hostilities. |

| • | Risks associated with operating ocean-going vessels. |

| • | Rising fuel prices. |

| • | Inflation. |

| • | Our revenues are subject to seasonal fluctuations. |

| • | The imposition of climate change and greenhouse gas restrictions. |

| • | Pending and future tax law changes. |

| • | Increased scrutiny of environmental, social and governance. |

| • | Restrictions or sanctions imposed by the United States, the European Union or other governments. |

| • | Regulation and liability under environmental laws and safety requirements. |

| • | Regulations relating to ballast water discharge. |

| • | Increased inspection procedures, tighter import and export controls and new security regulations. |

| • | Acts of piracy on ocean-going vessels. |

| • | Operational risks relating to the operation of dry bulk vessels. |

| • | Any failure of our vessels fail to maintain their class certification or fail any annual survey, intermediate survey, or special survey, or any scheduled class survey taking longer or being more expensive than anticipated. |

| • | Failure of industry groups to renew industry-wide collective bargaining agreements may disrupt our operations. |

| • | The arrest or attachment of our vessels by maritime claimants. |

| • | Government requisition of our vessels during a period of war or emergency. |

| • | Limited operating history |

| • | The market value of our vessels may decrease, which could limit the amount of funds that we can borrow, or trigger breaches of certain financial covenants under future loan agreements and other financing arrangements we may enter into, and we may incur an impairment or, if we sell vessels following a decline in their market value, a loss. |

| • | Limitations in the availability or operation of our vessel. |

| • | Inability to obtain financing for our vessels or to pursue other business opportunities. |

| • | Delays in the delivery of any vessels we may acquire, or the delivery of such vessels with significant defects. |

| • | The incurrence of substantial debt levels. |

| • | Restrictive covenants in future loan agreements and other financing arrangements that we may enter into, including the potential presence of cross-default provisions thereunder. |

| • | Inability to manage our growth properly and expand our market share. |

| • | Vessel ageing, and purchasing and operating secondhand vessels. |

| • | Any failure of our current or future counterparties to meet their obligations. |

| • | Rising crew costs. |

| • | Difficulty in improving our operating and financial systems and in securing suitable employees and crew for our vessels as we expand our business. |

| • | Inability to attract and retain key management personnel and other employees. |

| • | Damage of our vessels and unexpected repair costs. |

| • | Credit risk in connection with maintaining cash with a limited number of financial institutions. |

| • | Our dependence on the ability of our subsidiaries to distribute funds to us in order to satisfy our financial obligations or to pay dividends. |

| • | Inability to compete for charters with new entrants or established companies with greater resources. |

| • | The lack of fleet diversification. |

| • | Potential litigation. |

| • | Inherent operational risks in the shipping industry that may not be adequately covered by our insurances and becoming retrospectively subject to calls or premiums in amounts based not only on our own claim records, but also on the claim records of all other members of protection and indemnity associations. |

| • | Failure to comply with the U.S. Foreign Corrupt Practices Act of 1977, the UK Bribery Act or other similar laws. |

| • | The implications of being classified as a passive foreign investment company. |

| • | The implications of having to pay tax on U.S. source income. |

| • | The implications of being a “foreign private issuer”. |

| • | The implications of being entitled to exemption from certain Nasdaq corporate governance standards. |

| • | The implications of conducting business in China. |

| • | Changing laws and evolving reporting requirements. |

| • | Cyber-attacks. |

| • | The smuggling of drugs or other contraband onto our vessels. |

| • | The unpredictability of potential bankruptcy proceedings due to the international nature of our operations. |

| • | The implications of being incorporated in the Republic of the Marshall Islands. |

| • | The implications of our operations becoming subject to economic substance requirements. |

| • | The implications of certain forum selection provisions included in our amended and restated articles of incorporation. |

| • | The possibility of the enforceability of certain forum selection provisions included in our amended and restated articles of incorporation being challenged. |

| • | The inability of investors to serve process on or enforce U.S. judgments against us. |

| • | The implications of being an “emerging growth company”. |

| • | The implications of being a company publicly listed in the United States. |

| • | Our dependence on Pavimar to manage our business. |

| • | Pavimar is a privately held company and there is little or no publicly available information about it. |

| • | Management fees are payable to Pavimar regardless of our profitability or whether our vessels are employed. |

| • | Conflicts of interest of our Chairwoman and Chief Executive Officer and Pavimar. |

| • | The lack of and existing market for our common shares and the potential fluctuation of our share price. |

| • | Dilution as a result of any reliance on equity issuances, which will not require shareholder approval, to fund our growth. |

| • | Future issuance of common shares may trigger anti-dilution provisions in our Series A Preferred Shares. |

| • | Fluctuations in the market price of our common shares and the lack of a guaranteed continuing public market for resales. |

| • | Share price volatility as a result of a possible “short squeeze” due to a sudden increase in demand of our common shares that largely exceeds supply. |

| • | Share price volatility, including any share-run up, unrelated to our actual or expected operating performance, financial condition or prospects. |

| • | Risks related to any inability to pay dividends and the discretion of our Board of Directors to declare and pay dividends. |

| • | Our Chairwoman and Chief Executive Officer beneficially owns 100% of our Series B Preferred Shares and has control over us. |

| • | We expect to be a “controlled company” under Nasdaq corporate governance rules and we may be exempt from certain corporate governance requirements that could adversely affect our public shareholders. |

| • | Anti-takeover provisions in our amended and restated articles of incorporation and amended and restated bylaws. |

| • | The issuance of preferred shares. |

| • | A failure to meet the continued listing requirements of Nasdaq, resulting in a delisting of our common shares. |

| • | exemption from the auditor attestation requirement in the assessment of the emerging growth company’s internal controls over financial reporting under Section 404(b) of the Sarbanes-Oxley Act of 2002, or Sarbanes-Oxley; |

| • | exemption from new or revised financial accounting standards applicable to public companies until such standards are also applicable to private companies; and |

| • | exemption from compliance with any new requirements adopted by the Public Company Accounting Oversight Board, or the PCAOB, requiring mandatory audit firm rotation or a supplement to the auditor’s report in which the auditor would be required to provide additional information about the audit and financial statements. |

| • | decrease in available financing for vessels; |

| • | no active secondhand market for the sale of vessels; |

| • | decrease in demand for dry bulk vessels and limited employment opportunities; |

| • | charterers seeking to renegotiate the rates for existing time charters; |

| • | loan covenant defaults in the shipping industry; and |

| • | declaration of bankruptcy by some operators, charterers and vessel owners. |

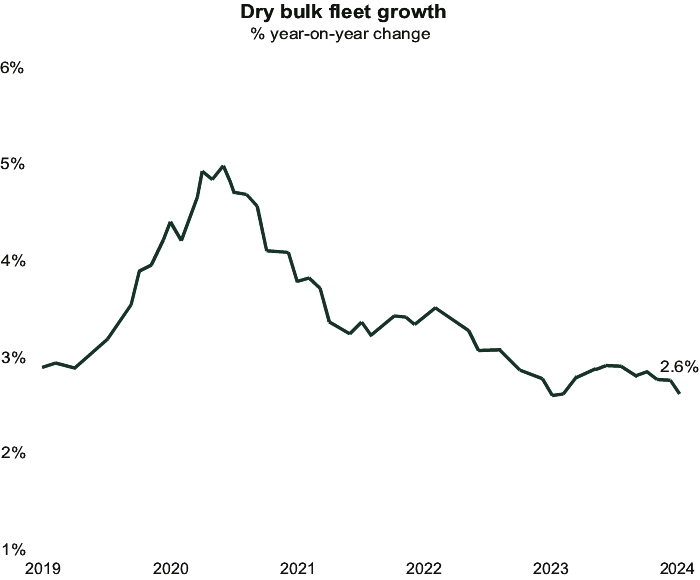

| • | the number of newbuilding orders and deliveries, including delays in vessel deliveries; |

| • | the number of shipyards and their ability to deliver vessels; |

| • | potential disruption, including supply chain disruptions, of shipping routes due to accidents or political events; |

| • | scrapping and recycling rate of older vessels; |

| • | vessel casualties; |

| • | the price of steel and vessel equipment; |

| • | product imbalances (affecting the level of trading activity) and developments in international trade; |

| • | the number of vessels that are out of service, namely those that are laid-up, drydocked, awaiting repairs or otherwise not available for hire; |

| • | vessels’ average speed; |

| • | technological advances in vessel design and capacity; |

| • | availability of financing for new vessels and shipping activity; |

| • | the imposition of sanctions; |

| • | changes in national or international regulations that may effectively cause reductions in the carrying capacity of vessels or early obsolescence of tonnage; |

| • | changes in environmental and other regulations that may limit the useful life of vessels; |

| • | port or canal congestion; and |

| • | changes in market conditions, including political and economic events, wars (including the ongoing conflict between Russia and Ukraine and between Israel and Hamas, or the Houthi crisis in the Red Sea), acts of terrorism, natural disasters (including diseases, epidemics and pandemics) and changes in interest rates or inflation rates. |

| • | crew strikes and/or boycotts; |

| • | acts of God; |

| • | the damage to or destruction of vessels ; |

| • | terrorism, piracy or other detentions; |

| • | environmental accidents; |

| • | cargo and property losses or damage; and |

| • | business interruptions caused by mechanical failure, grounding, fire, explosions and collisions, human error, war, terrorism, political action in various countries, labor strikes or adverse weather conditions and other circumstances or events. |

| • | Adoption of mandatory data collection system: At MEPC 70 in October 2016, a mandatory data collection system, or the IMO DCS, was adopted which requires vessels above 5,000 gross tons to report consumption data for fuel oil, hours under way and distance travelled. This DCS covers any maritime activity carried out by ships, including dredging, pipeline laying, ice-breaking, fish-catching and off-shore installations. The data is annually reported to the flag state which issues a statement of compliance to the relevant vessel. MEPC 79 adopted additional amendments to Annex VI to revise the DCS and reporting requirements in connection with the implementation of the Energy Efficiency Existing Ship Index, or EEXI, and carbon intensity indicator framework, which amendments will become effective on May 1, 2024. |

| • | Amendments to MAPROL Annex VI requiring ships to reduce their greenhouse gas emissions. Effective from January 1, 2023, the Revised Annex VI to the IMO International Convention for the Prevention of Pollution from Ships of 1973, as from time to time amended, generally referred to as MARPOL, includes carbon intensity measures, which cover certain requirements for vessels to calculate their EEXI following technical means to improve their energy efficiency and to establish their annual operational carbon intensity indicator and rating. |

| • | Net zero greenhouse emissions in the EU by 2050. In 2021, the EU adopted a European Climate Law (Regulation (EU) 2021/1119), establishing the aim of reaching net zero greenhouse gas emissions in the EU by 2050, with an intermediate target of reducing greenhouse gas emissions by at least 55% by 2030, compared to 1990 levels. In July 2021, the European Commission launched the “Fit for 55” to support the climate policy agenda. As of January 2019, large ships calling at EU ports have been required to collect and publish data on carbon dioxide emissions and other information. |

| • | Maritime ETS scheme became effective in January 2024. On January 1, 2024 the EU Emissions Trading Scheme, or the ETS, for ships sailing into and out of EU ports, came into effect, and the FuelEU Maritime Regulation is expected to come into effect on January 1, 2025. The ETS is to apply gradually over the period from 2024 to 2026. 40% of allowances would have to be surrendered in 2025 for the year 2024; 70% of allowances would have to be surrendered in 2026 for the year 2025; and 100% of allowances would have to be surrendered in 2027 for the year 2026. Compliance is to be on a companywide (rather than per ship) basis and “shipping company” is defined widely to capture both the ship owner and any contractually appointed commercial operator/ship manager/bareboat charterer who assumes responsibility for full compliance under the ETS and under the ISM Code. If the latter contractual arrangement is entered into this needs to be reflected in a certified mandate signed by both parties and presented to the administrator of the scheme. The cap under the ETS would be set by taking into account EU MRV system emissions data for the years 2018 and 2019, adjusted, from year 2021 and is to capture 100% of the emissions from intra-EU maritime voyages; 100% of emissions from ships at berth in EU ports and 50% of emissions from voyages which start or end at EU ports (but the other destination is outside the EU). Furthermore, the newly passed EU Emissions Trading Directive 2023/959/EC makes clear that all maritime allowances would be auctioned and there will be no free allocation. 78.4 million emissions allowances are to be allocated specifically to maritime. If we do not receive allowances from our charterers, we will be forced to purchase allowances from the market, which can be costly if our charterers do not compensate us for such cost, especially if other shipping companies are similarly looking to do the same. New systems, including personnel, data management systems, costs recovery mechanisms, revised service agreement terms and emissions reporting procedures will have to be put in place, at significant cost, to prepare for and manage the administrative aspect of ETS compliance. The cost of compliance, and of our future EU emissions and costs to purchase an allowance for emissions (if we must purchase in order to comply) are unknown and difficult to predict, and are based on a number of factors, including the size of our fleet, our trips within and to and from the EU, and the prevailing cost of allowances. |

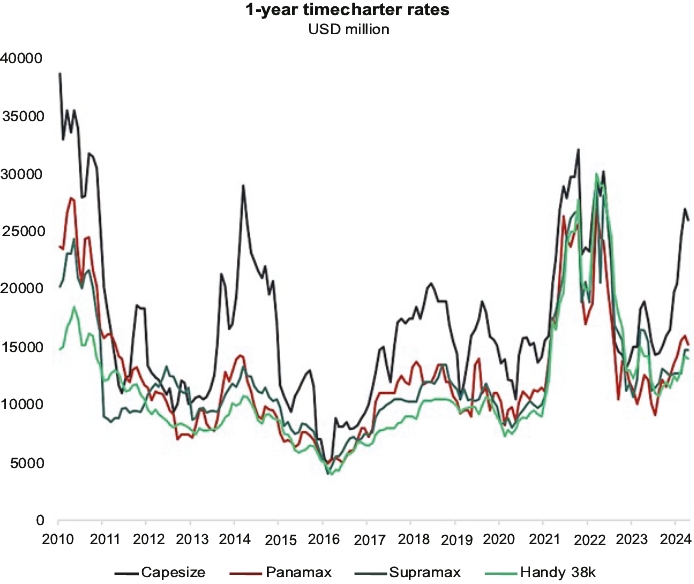

| • | general economic and market conditions affecting the shipping industry, including changes in global dry cargo commodity demand and supply; |

| • | prevailing levels of charter rates; |

| • | competition from other shipping companies; |

| • | sophistication and condition of the vessels; |

| • | advances in vessel efficiency and technology; |

| • | where the vessel was built, as-built specifications and subsequent modifications and improvements; |

| • | lifetime maintenance record; |

| • | supply and demand for vessels; |

| • | types, sizes, and age of vessels; |

| • | number of upcoming newbuilding deliveries |

| • | the cost to order and construct a new vessel; |

| • | number of vessels scrapped or otherwise removed from the world fleet; |

| • | the scrap value of vessels; |

| • | changes in governmental, environmental and other regulations that may limit the useful life of vessels; |

| • | decreased costs and increases in use of other modes of transportation; |

| • | global economic or pandemic-related crises; |

| • | ability of willing buyers to access financing and capital; and |

| • | the cost of retrofitting or modifying existing ships to respond to technological advances in vessel design or equipment, changes in applicable governmental, environmental or other regulations or standards, or otherwise. |

| • | our ability to obtain additional financing, if necessary, for working capital, capital expenditures, acquisitions or other purposes may be impaired, or such financing may be unavailable on favorable terms, or at all; |

| • | we may need to use a substantial portion of our cash from operations to make principal and interest payments on our bank debt and financing liabilities, reducing the funds that would otherwise be available for operations, future business opportunities and any future dividends to our shareholders; |

| • | our debt level could make us more vulnerable to competitive pressures or a downturn in our business or the economy generally than our competitors with less debt; and |

| • | our debt level may limit our flexibility in responding to changing business and economic conditions. |

| • | generate excess cash flow so that we can invest without jeopardizing our ability to cover current and foreseeable working capital needs, including debt service obligations, if any; |

| • | finance our operations; |

| • | identify and acquire suitable vessels; |

| • | identify and consummate corporate acquisitions or joint ventures; |

| • | integrate any acquired businesses or vessels, including those operating in sectors in which we do not currently operate, successfully with our existing operations; |

| • | access qualified personnel and crew to manage and operate our growing business and fleet; and |

| • | expand our customer base, including in new sectors. |

| • | continue to operate our vessels and service our customers; |

| • | renew existing charters upon their expiration; |

| • | secure new charters; |

| • | obtain insurance on commercially acceptable terms; |

| • | maintain satisfactory relationships with our customers and suppliers; and |

| • | successfully execute our growth strategy. |

| • | our existing common shareholders’ proportionate ownership interest in us will decrease; |

| • | the amount of cash available for dividends payable per common share may decrease; |

| • | the relative voting strength of each previously outstanding common share may be diminished; and |

| • | the market price of our common shares may decline. |

| • | seasonal variations in our results of operations; |

| • | changes in market valuations of similar companies and stock market price and volume fluctuations generally; |

| • | changes in earnings estimates or the publication of research reports by analysts; |

| • | speculation in the press or investment community about our business or the shipping industry generally; |

| • | strategic actions by us or our competitors such as acquisitions or restructurings; |

| • | the potentially thin trading market for our common shares, which may render them illiquid; |

| • | regulatory developments; |

| • | additions or departures of key personnel; |

| • | general market conditions; |

| • | systemic risks; and |

| • | domestic and international economic, market and currency factors unrelated to our performance. |

| • | authorize our Board of Directors to issue “blank check” preferred stock without shareholder approval, including preferred shares with superior voting rights, such as the Series B Preferred Shares; |

| • | provide for a classified Board of Directors with staggered, three-year terms; |

| • | permit the removal of any director only for cause upon the affirmative vote of not less than two-thirds of the outstanding shares of our capital stock entitled to vote for such director; |

| • | prohibit shareholder action by written consent unless the written consent is signed by all shareholders entitled to vote on the action; |

| • | limit the persons who may call special meetings of shareholders; and |

| • | establish advance notice requirements for nominations for election to our Board of Directors or for proposing matters that can be acted on by shareholders at meetings of shareholders. |

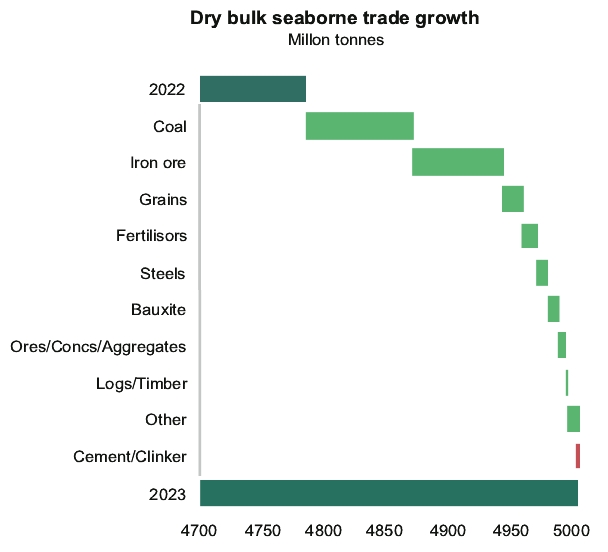

| • | changes in shipping industry trends, including charter rates, vessel values and factors affecting vessel supply and demand; |

| • | changes in seaborne and other transportation patterns; |

| • | changes in the supply of or demand for dry bulk commodities, including dry bulk commodities carried by sea, generally or in particular regions; |

| • | changes in the number of newbuildings under construction in the dry bulk shipping industry; |

| • | changes in the useful lives and the value of our vessels and the related impact on our compliance with loan covenants; |

| • | the aging of our fleet and increases in operating costs; |

| • | changes in our ability to complete future, pending or recent acquisitions or dispositions; |

| • | changes to our financial condition and liquidity, including our ability to pay amounts that we owe and obtain additional financing to fund capital expenditures, acquisitions and other general corporate activities; |

| • | risks related to our business strategy, areas of possible expansion or expected capital spending or operating expenses; |

| • | changes in our ability to leverage the relationships and reputation in the dry bulk shipping industry of Pavimar and Mrs. Panagiotidi, our Chairwoman and Chief Executive Officer; |

| • | changes in the availability of crew, number of off-hire days, classification survey requirements and insurance costs for the vessels in our fleet; |

| • | changes in our relationships with our contract counterparties, including the failure of any of our contract counterparties to comply with their agreements with us; |

| • | loss of our customers, charters or vessels; |

| • | damage to our vessels; |

| • | potential liability from future litigation and incidents involving our vessels; |

| • | our future operating or financial results; |

| • | acts of terrorism and other hostilities, pandemics or other calamities; |

| • | changes in global and regional economic and political conditions; |

| • | general domestic and international political conditions or events, including “trade wars” and sanctions and the ongoing wars between Russia and Ukraine and between Israel and Hamas; |

| • | changes in governmental rules and regulations or actions taken by regulatory authorities, particularly with respect to the dry bulk shipping industry; |

| • | our ability to continue as a going concern; and |

| • | other factors discussed in the “Risk Factors” section of this prospectus. |

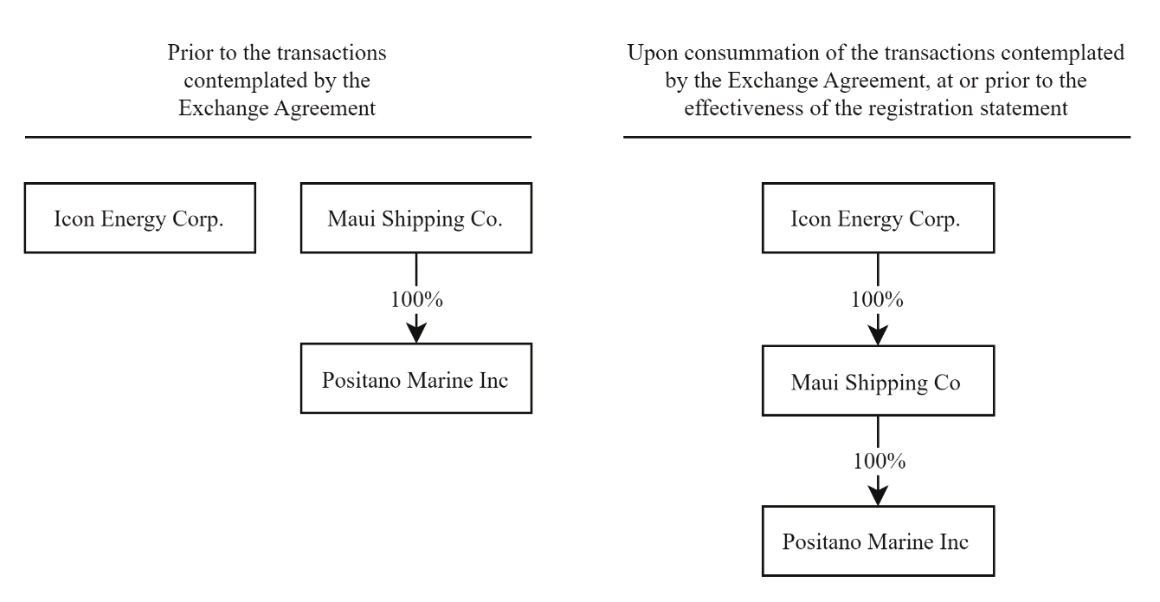

| • | on an actual basis as of December 31, 2023, giving effect to the exchange agreement to be executed at or prior to the effectiveness of the registration statement of which this prospectus forms a part; |

| • | on an as adjusted basis as of December 31, 2023, to give effect to the amount of $3,000 of additional paid-in-capital, which was paid out of the Company’s cash on hand, including cash generated from operations subsequent to December 31, 2023. As this return of additional paid-in capital was made after the date of the latest balance sheet presented but prior to the effectiveness of the registration statement of which this prospectus forms a part, it has been given retroactive effect in the accompanying consolidated balance sheet as of December 31, 2023; and |

| • | on an as further adjusted basis to reflect the sale by us of 1,250,000 common shares pursuant to this offering, assuming an initial public offering price of $5.00 per share, representing the midpoint of the range set forth on the cover page of this prospectus and assuming no exercise of the underwriters’ over-allotment option to purchase additional shares, and after deducting estimated underwriting discounts and commissions and estimated offering expenses (save for non-cash offering expenses and offering expenses already paid by us up to December 31, 2023), resulting in assumed net proceeds of $4.6 million. |

| | | As of December 31, 2023 | |||||||

(In Thousands of U.S. Dollars, except share data) | | | ACTUAL | | | AS ADJUSTED | | | AS FURTHER ADJUSTED |

Total Cash | | | $2,702 | | | $— | | | $4,629 |

Shareholders’ equity: | | | | | | | |||

Common shares—authorized 750,000,000 shares with a $0.001 par value, 200,000 shares issued and outstanding on actual (as adjusted 200,000 and as further adjusted 1,450,000) | | | — | | | — | | | 1 |

Series A Preferred Shares—authorized 1,500,000 shares with a $0.001 par value, 15,000 shares, actual, as adjusted and as further adjusted, issued and outstanding | | | — | | | — | | | — |

Series B Preferred Shares—authorized 1,500,000 shares with a $0.001 par value, 1,500,000 shares, actual, as adjusted and as further adjusted, issued and outstanding | | | 2 | | | 2 | | | 2 |

Series C Participating Preferred Shares—authorized 1,500,000 shares with a $0.001 par value, no shares, actual, as adjusted and as further adjusted, issued and outstanding | | | — | | | — | | | — |

Additional paid-in capital | | | [•] | | | [•] | | | [•] |

Retained earnings | | | [•] | | | [•] | | | [•] |

Total shareholders’ equity | | | $9,169 | | | $9,169 | | | $13,743 |

Total Capitalization | | | $9,169 | | | $9,169 | | | $13,743 |

| | | Post-Offering(1) | | | Full Exercise of Over-allotment Option(2) | |

Assumed initial public offering price per common share | | | $5.00 | | | $5.00 |

Net tangible book value per common share as of December 31, 2023(3) | | | $45.85 | | | $45.85 |

Decrease in pro forma as adjusted net tangible book value per common share attributable to purchasers of our common shares in this offering | | | $36.37 | | | $36.92 |

Pro forma as adjusted net tangible book value per common share after this offering | | | $9.48 | | | $8.93 |

Accretion per common share to purchasers of our common shares in this offering | | | $4.48 | | | $3.93 |

| (1) | Assumes net proceeds from the offering of 1,250,000 common shares, and assumes that the underwriters’ over-allotment option has not been exercised. |

| (2) | Assumes net proceeds from the offering of 1,437,500 common shares, and assumes that the underwriters’ over-allotment option has been exercised in full. |

| (3) | Giving effect to the exchange agreement to be executed at or prior to the effectiveness of the registration statement of which this prospectus forms a part. |

Over-allotment option not exercised (in thousands, except for number of shares, percentages and per share data) | | | Common shares purchased | | | Total consideration | | | Average price per common share | ||||||

| | | Number | | | Percent | | | Amount | | | Percent | | |||

Existing shareholders | | | 200,000(1) | | | 13.8% | | | $8,592(1) | | | 57.9% | | | $42.96 |

New investors | | | 1,250,000 | | | 86.2% | | | $6,250 | | | 42.1% | | | $5.00 |

Total | | | 1,450,000 | | | 100.0% | | | $14,842 | | | 100.0% | | | $10.24 |

| (1) | Giving effect to the exchange agreement to be executed at or prior to the effectiveness of the registration statement of which this prospectus forms a part. |

Over-allotment option exercised in full (in thousands, except for number of shares, percentages and per share data) | | | Common shares purchased | | | Total consideration | | | Average price per common share | ||||||

| | | Number | | | Percent | | | Amount | | | Percent | | |||

Existing shareholders | | | 200,000(1) | | | 12.2% | | | $8,592(1) | | | 54.4% | | | $42.96 |

New investors | | | 1,437,500 | | | 87.8% | | | $7,188 | | | 45.6% | | | $5.00 |

Total | | | 1,637,500 | | | 100.0% | | | $15,780 | | | 100.0% | | | $9.64 |

| (1) | Giving effect to the exchange agreement to be executed at or prior to the effectiveness of the registration statement of which this prospectus forms a part. |

| • | exemption from the auditor attestation requirement in the assessment of the emerging growth company’s internal controls over financial reporting under Section 404(b) of Sarbanes-Oxley; |

| • | exemption from new or revised financial accounting standards applicable to public companies until such standards are also applicable to private companies; and |

| • | exemption from compliance with any new requirements adopted by the PCAOB, requiring mandatory audit firm rotation or a supplement to the auditor’s report in which the auditor would be required to provide additional information about the audit and financial statements. |

| • | the number of vessels in our fleet; |

| • | our customer relationships; |

| • | our access to capital required to acquire additional vessels and implement our business strategy; |

| • | our ability to acquire and sell vessels at prices we deem satisfactory; and |

| • | our and our vessel manager’s ability to: |

| ○ | successfully utilize and employ our vessels at economically attractive rates; |

| ○ | effectively and efficiently manage our vessels and control vessel operating costs; and |

| ○ | ensure compliance with regulations, environmental, health and safety standards applicable to our business. |

(in thousands of U.S. dollars, except fleet data and daily results) | | | Year ended December 31, 2023 | | | Year ended December 31, 2022 |

Fleet data: | | | | | ||

Ownership Days | | | 365.0 | | | 365.0 |

Available Days | | | 365.0 | | | 365.0 |

Operating Days | | | 364.9 | | | 363.6 |

Vessel Utilization | | | 100.0% | | | 99.6% |

Average number of vessels | | | 1.0 | | | 1.0 |

| | | | | |||

Daily results: | | | | | ||

Daily TCE | | | $11,822 | | | $20,160 |

Daily OPEX | | | $5,151 | | | $4,893 |

(in thousands of U.S. dollars, except fleet data and daily results) | | | Year ended December 31, 2023 | | | Year ended December 31, 2022 |

TCE and Daily TCE: | | | | | ||

Revenue, net | | | $4,476 | | | $7,241 |

Less: Voyage expenses | | | (162) | | | (270) |

Plus: Other operating income | | | — | | | 359 |

TCE | | | $4,314 | | | $7,330 |

Operating Days | | | 364.9 | | | 363.6 |

Daily TCE | | | $11,822 | | | $20,160 |

| | | | | |||

Daily OPEX: | | | | | ||

Vessel operating expenses | | | $1,880 | | | $1,786 |

Ownership Days | | | 365.0 | | | 365.0 |

Daily OPEX | | | $5,151 | | | $4,893 |

| | | | | |||

EBITDA: | | | | | ||

Net income | | | $1,155 | | | $4,242 |

Plus: Depreciation expense | | | 680 | | | 680 |

Plus: Amortization of deferred drydocking costs | | | 357 | | | 360 |

Less: Interest income | | | (56) | | | (13) |

EBITDA | | | $2,136 | | | $5,269 |

(in thousands of U.S. dollars) | | | Year ended December 31, 2023 | | | Year ended December 31, 2022 |

Revenue, net | | | $4,476 | | | $7,241 |

Voyage expenses | | | (162) | | | (270) |

Vessel operating expenses | | | (1,880) | | | (1,786) |

Management fees | | | (274) | | | (274) |

General and administrative expenses | | | (18) | | | (12) |

Other operating income | | | — | | | 359 |

Depreciation expense | | | (680) | | | (680) |

Amortization of deferred drydocking costs | | | (357) | | | (360) |

Finance costs | | | (3) | | | (3) |

Interest income | | | 56 | | | 13 |

Other (costs)/income, net | | | (3) | | | 14 |

| | | $1,155 | | | $4,242 |

(in thousands of U.S. dollars) | | | Year ended December 31, 2023 | | | Year ended December 31, 2022 |

Cash provided by operating activities | | | $2,505 | | | $3,989 |

Cash used in investing activities | | | (22) | | | (225) |

Cash used in financing activities | | | (3,332) | | | (2,638) |

Net (Decrease)/Increase in Cash and Cash Equivalents | | | $(849) | | | $1,126 |

Cash and Cash equivalents at the beginning of the period | | | 3,551 | | | 2,425 |

Cash and Cash equivalents at the end of the period | | | $2,702 | | | $3,551 |

Category | | | Carrying capacity |

Handysize/Handymax | | | 20,000-49,000 dwt |

Supramax/Ultramax | | | 50,000-66,000 dwt |

Panamax/Kamsarmax | | | 70,000-82,500 dwt |

Post Panamax/Mini Cape | | | 90,000-120,000 dwt |

Capesize/Newcastlemax | | | 120,000+ |

| (i) | injury to, destruction or loss of, or loss of use of, natural resources and related assessment costs; |

| (ii) | injury to, or economic losses resulting from, the destruction of real and personal property; |

| (iii) | loss of subsistence use of natural resources that are injured, destroyed or lost; |

| (iv) | net loss of taxes, royalties, rents, fees or net profit revenues resulting from injury, destruction or loss of real or personal property, or natural resources; |

| (v) | lost profits or impairment of earning capacity due to injury, destruction or loss of real or personal property or natural resources; and |

| (vi) | net cost of increased or additional public services necessitated by removal activities following a discharge of oil, such as protection from fire, safety or health hazards, and loss of subsistence use of natural resources. |

Name | | | Age | | | Position |

Ismini Panagiotidi | | | 41 | | | Chief Executive Officer, and Chairwoman of the Board (Class III Director) |

Dennis Psachos | | | 41 | | | Chief Financial Officer |

Spiros Vellas* | | | 43 | | | Class I Director |

Evangelos Macris* | | | 73 | | | Class II Director |

Kalliopi Kyriakakou** | | | 42 | | | Secretary |

| * | Mr. Spiros Vellas and Mr. Evangelos Macris have each agreed to serve on our Board of Directors effective immediately after the effectiveness of the registration statement of which this prospectus forms a part. |

| ** | Mrs. Kalliopi Kyriakakou has agreed to serve as our Secretary effective immediately after the effectiveness of the registration statement of which this prospectus forms a part. |

| | | Common Shares Beneficially Owned Prior to Offering | | | Common Shares to be Beneficially Owned After Offering | |||||||

Name | | | Number | | | Percentage | | | Number | | | Percentage(1) |

Atlantis Holding Corp. (Ismini Panagiotidi)(1) | | | 200,000(2) | | | 100% | | | 200,000 | | | 13.8% |

All other directors and executive officers individually | | | 0 | | | 0 | | | 0 | | | 0 |

| (1) | Upon completion of this offering, Mrs. Ismini Panagiotidi will hold 1,500,000 Series B Preferred Shares (representing all such Series B Preferred Shares outstanding), each Series B Preferred Share having the voting power of 1,000 common shares and which is subject to adjustment as described herein. The Series B Preferred Shares to be held by Mrs. Panagiotidi represent 99.90% of the aggregate voting power of our total issued and outstanding share capital. In addition, upon completion of this offering, Mrs. Panagiotidi will hold 15,000 Series A Preferred Shares (representing all such Series A Preferred Shares outstanding). The Series A Preferred Shares may be converted into common shares, at the applicable conversion price then in effect, at any time and from time to time commencing on the first business day following the one-year anniversary of the closing date of our initial public offering and until the day falling on the eight-year anniversary of the closing date of our initial public offering. Please see “Description of Capital Stock” for a description of the rights of the holder of our Series A Preferred Shares and Series B Preferred Shares relative to the rights of the holders of our common shares and other series of preferred stock. |

| (2) | Giving effect to the exchange agreement to be executed at or prior to the effectiveness of the registration statement of which this prospectus forms a part. |

| • | 750,000,000 common shares, par value $0.001 per share, of which 200,000 shares will be issued and outstanding at or prior to the effectiveness of the registration statement of which this prospectus forms a part; and |

| • | 250,000,000 preferred shares, par value $0.001 per share, out of which: |

| ○ | 1,500,000 Series A Preferred Shares have been designated, of which 15,000 will be issued and outstanding at or prior to the effectiveness of the registration statement of which this prospectus forms a part; |

| ○ | 1,500,000 Series B Preferred Shares have been designated, of which 1,500,000 will be issued and outstanding at or prior to the effectiveness of the registration statement of which this prospectus forms a part; and |

| ○ | 1,500,000 Series C Participating Preferred Shares have been designated, of which none will be issued and outstanding at or prior to the effectiveness of the registration statement of which this prospectus forms a part. |

| • | Ranking. The Series A Preferred Shares rank, with respect to dividend distributions and distributions upon our liquidation, dissolution or winding up of our affairs (whether voluntary or involuntary), sale of substantially all of our assets, property or business, or a change of control of us (each, a “Liquidation Event”), (i) senior to our common shares, our Series B Preferred Shares, our Series C Participating Preferred Shares and to any other class or series of our stock that may be established in the future that is not expressly stated to be on parity with or senior to the Series A Preferred Shares in the payment of dividends and the distribution of assets upon a Liquidation Event (together with our common shares, the “Junior Stock”), (ii) on parity with any class or series of capital stock that may be established in the future that is expressly stated to be on parity with the Series A Preferred Shares with respect to the payment of dividends and the distribution of assets upon a Liquidation Event, and (iii) junior to any class or series of capital stock that may be established in the future that is expressly stated to rank senior to the Series A Preferred Shares with respect to the payment of dividends and the distribution of assets upon a Liquidation Event, and to all existing and future indebtedness and other liabilities, including trade payable and other non-equity claims on us. |

| • | Conversion Rights. The holders of Series A Preferred Shares have the right, subject to certain conditions, at any time and from time to time commencing on the first business day following the one-year anniversary of the closing date of this offering and until the day falling on the eight-year anniversary of the closing date of this offering, to convert all or any portion of the Series A Preferred Shares held by such holder into our common shares at the conversion rate then in effect. Each Series A Preferred Share is convertible into the number of our common shares equal to the quotient of the aggregate stated amount of the Series A Preferred Shares converted plus any accrued and unpaid dividends divided by the lower of (i) 150% of the initial public offering price per common share in this offering (the “Pre-Determined Price”) and (ii) the volume weighted average price (VWAP) of our common shares over the five consecutive trading day period expiring on the trading day immediately prior to the date of delivery of written notice of the conversion. The Pre-Determined Price is also subject to appropriate adjustment for dilution, including but not limited to, certain issuances of additional common shares at a deemed price per share lower than the conversion price, certain dividends and distributions, stock combinations or splits, reclassifications or similar events affecting our common shares. The Series A Preferred Shares are otherwise not convertible into or exchangeable for property or shares of any other series or class of our capital stock. |

| • | Voting Rights. So long as any Series A Preferred Shares are outstanding, in addition to any other vote or consent of shareholders required by law or by our amended and restated articles of incorporation, the vote or consent of the holders of at least 66 2/3% of the Series A Preferred Shares at the time outstanding, voting together as a separate class, given in person or by proxy, either in writing without a meeting or by vote at any meeting called for the purpose, will be necessary for effecting or validating: (i) any amendment, alteration or repeal of any provision of our amended and restated articles of incorporation or amended and restated bylaws that would alter or change the voting powers, preferences or special rights of the holders of the Series A Preferred Shares so as to affect them adversely; (ii) the issuance of Dividend Parity Stock if the Accrued Dividends on all outstanding Series A Preferred Shares through and including the most recently completed Dividend Period have not been paid or declared and a sum sufficient for the payment thereof has been set aside for payment; (iii) any amendment or alteration of our amended and restated articles of incorporation to authorize or create, or increase the authorized amount of, any Senior Stock; or (iv) any consummation of (x) a binding share exchange or reclassification involving the Series A Preferred Shares, (y) a merger or consolidation of the Company with another entity (whether or not a corporation), or (z) a conversion, transfer, domestication or continuance of the Company into another entity or an entity |

| • | Dividends. The holders of Series A Preferred Shares will be entitled to receive, out of funds legally available for the purpose, biannual dividends payable in either cash or, at the Company’s option, in Series A Preferred Shares (“PIK Shares”), or a combination thereof, on each June 30 and December 31 of each year (each such date being referred to herein as a “Dividend Payment Date”), commencing on the first Dividend Payment Date. Dividends will accumulate in each dividend period from and including the preceding Dividend Payment Date or the initial issue date, as the case may be, to but excluding the applicable Dividend Payment Date for such dividend period (each, a “Dividend Period”). If any Dividend Payment Date otherwise would fall on a day that NASDAQ is not open for trading and which is not a Saturday, a Sunday or other day on which banks in New York City are authorized or required by law to close (a “Business Day”), declared dividends will be paid on the immediately succeeding Business Day without the accumulation of additional dividends. Dividends on the Series A Preferred Shares will be payable based on a 360-day year consisting of twelve 30-day months and will accrue at a rate of 9.00% per annum (the “Dividend Rate”) on the stated amount per Series A Preferred Share and on any Accrued Dividends, from and including the original issue date (or, for any subsequently issued and newly outstanding Series A Preferred Shares, from the Dividend Payment Date immediately preceding the issuance date of such Series A Preferred Shares). |

| • | Maturity/Redemption. The Series A Preferred Shares are perpetual, non-redeemable and have no maturity date. |

| • | Liquidation, Dissolution or Winding Up. In the event of any liquidation, dissolution, winding up of the Company or other Liquidation Event, whether voluntary or involuntary, the Series A Preferred Shares shall have a liquidation preference of $1,000 per share (plus Accrued Dividends to the date fixed for payment of such amount (whether or not declared), and no more). A consolidation or merger of us with or into any other entity, individually or in a series of transactions, will not be deemed a liquidation, dissolution or winding up of our affairs for this purpose. In the event that our assets available for distribution to holders of the outstanding Series A Preferred Shares and all Liquidation Parity Stock are insufficient to permit payment of all required amounts, our assets then remaining will be distributed among the holders of Series A Preferred Shares, as applicable, ratably on the basis of their relative aggregate Liquidation |

| • | No Preemptive Rights; No Sinking Fund. The holders of Series A Preferred Shares do not have any preemptive rights. The Series A Preferred Shares will not be subject to any sinking fund or any other obligation of us for their repurchase or retirement. |

| • | Conversion Rights. The Series B Preferred Shares are not convertible into our common shares. |

| • | Voting Rights. Each Series B Preferred Share has the voting power of 1,000 common shares and counts for 1,000 votes for purposes of determining quorum at a meeting of shareholders, subject to adjustment to maintain a substantially identical voting interest in the Company following the (i) creation or issuance of a new series of shares of the Company carrying more than one vote per share to be issued to any person other than holders of the Series B Preferred Shares, except for the creation (but not the issuance) of Series C Participating Preferred Shares substantially in the form approved by the Board and included as an exhibit to this registration statement, without the prior affirmative vote of a majority of votes cast by the holders of the Series B Preferred Shares or (ii) issuance or approval of common shares pursuant to and in accordance with the Rights Agreement (as defined below). The holders of Series B Preferred Shares and the holders of our common shares shall vote together as one class on all matters submitted to a vote of our shareholders, except that the Series B Preferred Shares vote separately as a class on amendments to our amended and restated articles of incorporation that would materially alter or change the powers, preference or special rights of the Series B Preferred Shares. |

| • | Distributions. The Series B Preferred Shares have no dividend or distribution rights, other than upon our liquidation, dissolution or winding up, as described below. Also, if we declare or make any dividend or other distribution of voting securities of a subsidiary which we control to the holders of our common shares by way of a spin off or other similar transaction, then, in each such case, each holder of Series B Preferred Shares shall be entitled to receive preferred shares of the subsidiary whose voting securities are so distributed with at least substantially similar rights, preferences, privileges and voting powers, and limitations and restrictions as those of the Series B Preferred Shares. |

| • | Maturity/Redemption. The Series B Preferred Shares are perpetual, non-redeemable and have no maturity date. |

| • | Ranking, Liquidation, Dissolution or Winding Up. Upon any liquidation, dissolution or winding up of the Company, Series B Preferred Shares shall be entitled to receive a payment on the same terms as, and rank pari-passu with, the common shares with respect thereto, up to an amount equal to the par value of $0.001 per share Series B Preferred Share. Holders of shares of this Series will have no other rights to distributions upon any liquidation, dissolution or winding up of the Company. |

| • | No Preemptive Rights; No Sinking Fund. Holders of the Series B Preferred Shares do not have any preemptive rights. The Series B Preferred Shares will not be subject to any sinking fund or any other obligation of us for their repurchase or retirement. |

| • | not be redeemable; |

| • | entitle holders to dividend payments in an amount per share equal to the aggregate per share amount of all cash dividends, and the aggregate per share amount (payable in kind) of all non-cash dividends or other distributions other than a dividend payable in our common shares or a subdivision of our outstanding common shares (by reclassification or otherwise), declared on our common shares; and |

| • | entitle holders to one vote on all matters submitted to a vote of the shareholders of the Company. |

| • | prior to such time, our Board of Directors approved either the Business Combination or the transaction which resulted in the shareholder becoming an Interested Shareholder; |

| • | upon consummation of the transaction which resulted in the shareholder becoming an Interested Shareholder, the Interested Shareholder owned at least eighty-five percent (85%) of the outstanding common shares of the Company at the time the transaction commenced, excluding for purposes of determining the number of common shares outstanding those shares or equity interests owned (i) by persons who are directors and also officers and (ii) employee stock plans in which employee participants do not have the right to determine confidentially whether shares or equity interests held subject to the plan will be tendered in a tender or exchange offer; or |

| • | at or subsequent to such time, the Business Combination is approved by our Board and authorized at an annual or special meeting of shareholders, and not by written consent, by the affirmative vote of the holders of at least two-thirds of the Voting Power of the outstanding Voting Shares of the Company that are not owned by the Interested Shareholder; or (4) the stockholder was or became an Interested Stockholder prior to the consummation of the initial public offering of the Company’s common shares under the United States Securities Act of 1933, as amended. |

| • | A shareholder becomes an Interested Shareholder inadvertently and (i) as soon as practicable divests itself of ownership of sufficient shares or equity interests so that the shareholder ceases to be an Interested Shareholder; and (ii) would not,at any time within the three-year period immediately prior to a Business Combination between the Company and such shareholder, have been an Interested Shareholder but for the inadvertent acquisition of ownership; or |

| • | the Business Combination is proposed prior to the consummation or abandonment of and subsequent to the earlier of the public announcement or the notice required hereunder of a proposed transaction which (i) constitutes one of the transactions described in the following sentence; (ii) is with or by a person who either was not an Interested Shareholder during the previous three years or who became an Interested Shareholder with the approval of our Board; and (iii) is approved or not opposed by a majority of the members of our Board then in office (but not less than one) who were directors prior to any person becoming an Interested Shareholder during the previous three years or were recommended for election or elected to succeed such directors by a majority of such directors. The proposed transactions referred to in the preceding sentence are limited to: |

| ○ | a merger or consolidation of the Company (except for a merger in respect of which, pursuant to the BCA, no vote of the shareholders of the Company is required); |

| ○ | a sale, lease, exchange, mortgage, pledge, transfer or other disposition (in one transaction or a series of transactions), whether as part of a dissolution or otherwise, of assets of the Company or of any |

| ○ | a proposed tender or exchange offer for fifty percent (50%) or more of the outstanding common shares of the Company. |

| • | “Interested Shareholder” means any person (other than the Company and any direct or indirect majority-owned subsidiary of the Company) that (i) is the owner of 15% or more of the outstanding common shares of the Company, or (ii) is an affiliate or associate of the Company and was the owner of fifteen percent (15%) or more of the outstanding common shares of the Company at any time within the three-year period immediately prior to the date on which it is sought to be determined whether such person is an Interested Shareholder; and the affiliates and associates of such person; provided, however, that the term “Interested Shareholder” shall not include any person whose ownership of shares in excess of the fifteen percent (15%) limitation set forth herein is the result of action taken solely by the Company; provided that such person shall be an Interested Shareholder if thereafter such person acquires additional common shares of the Company, except as a result of further Company action not caused, directly or indirectly, by such person. For the purpose of determining whether a person is an Interested Shareholder, the common shares of the Company deemed to be outstanding shall include common shares deemed to be owned by the person, but shall not include any other unissued shares which may be issuable pursuant to any agreement, arrangement or understanding, or upon exercise of conversion rights, warrants or options, or otherwise. Notwithstanding the foregoing, none of Ismini Panagiotidi or her affiliates and associates shall be considered an Interested Shareholder; |

| • | “Voting Power” means, with respect to a class or series of capital stock or classes of capital stock, as the context may require, the aggregate number of votes that the holder(s) of such class or series of capital stock or classes of capital stock, or any relevant portion thereof, entitled to vote at a meeting of shareholders, as the context may require, have; and |

| • | “Voting Shares” means, with respect to any corporation, shares of any class or series of capital stock entitled to vote in connection with the election of directors and/or all other matters submitted to a vote and, with respect to any entity that is not a corporation, any equity interest entitled to vote in connection with the election of the directors or other governing body of such entity and/or all other matters submitted to a vote. |

| • | not be redeemable; |

| • | entitle holders to quarterly dividend payments in an amount per share equal to the aggregate per share amount of all cash dividends, and the aggregate per share amount (payable in kind) of all non-cash dividends or other distributions other than a dividend payable in common shares or a subdivision of our outstanding common shares (by reclassification or otherwise), declared on common shares since the immediately preceding quarterly dividend payment date; and |

| • | entitle holders to one vote on all matters submitted to a vote of the shareholders of the Company. |

| • | Flip In. If an Acquiring Person obtains beneficial ownership of 10% (15% in the case of a passive institutional investor) or more of our common shares, then each Right will entitle the holder thereof to purchase, for the Exercise Price, a number of common shares (or, in certain circumstances, cash, property or other securities of ours) having a then-current market value of twice the Exercise Price. However, the Rights are not exercisable following the occurrence of the foregoing event until such time as the Rights are no longer redeemable by us, as further described below. |

| • | Flip Over. If, after an Acquiring Person obtains 10% (15% in the case of a passive institutional investor) or more of our common shares, (i) the Company merges into another entity; (ii) an acquiring entity merges |

| • | Notional Shares. Shares held by affiliates and associates of an Acquiring Person, including certain entities in which the Acquiring Person beneficially owns a majority of the equity securities, and Notional Common Shares (as defined in the Rights Agreement) held by counterparties to a Derivatives Contract (as defined in the Rights Agreement) with an Acquiring Person, will be deemed to be beneficially owned by the Acquiring Person. |

| | Marshall Islands | | | Delaware | |

| | Shareholder Meetings | | |||

| | May be held at a time and place as designated in the bylaws. | | | May be held at such time or place as designated in the certificate of incorporation or the bylaws, or if not so designated, as determined by the board of directors. | |

| | Notice: | | | Notice: | |

| | Whenever shareholders are required to take any action at a meeting, written notice of the meeting shall be given which shall state the place, date and hour of the meeting and, unless it is an annual meeting, indicate that it is being issued by or at the direction of the person calling the meeting. Notice of a special meeting shall also state the purpose for which the meeting is called. | | | Whenever shareholders are required to take any action at a meeting, a written notice of the meeting shall be given which shall state the place, if any, date and hour of the meeting, and the means of remote communication, if any. | |

| | A copy of the notice of any meeting shall be given personally, sent by mail or by electronic mail not less than 15 nor more than 60 days before the meeting. | | | Written notice shall be given not less than 10 nor more than 60 days before the meeting. | |

| | Shareholders’ Written Consent | | |||

| | Unless otherwise provided in the articles of incorporation, any action required to be taken at a meeting of shareholders may be taken without a meeting, without prior notice and without a vote, if a consent in writing, setting forth the action so taken, is signed by all the shareholders entitled to vote with respect to the subject matter thereof, or if the articles of incorporation so provide, by the holders of outstanding shares having not less than the minimum number of votes that would be necessary to authorize or take such action at a meeting at which all shares entitled to vote thereon were present and voted. | | | Any action required to be taken at a meeting of shareholders may be taken without a meeting if a consent for such action is in writing and is signed by shareholders having not fewer than the minimum number of votes that would be necessary to authorize or take such action at a meeting at which all shares entitled to vote thereon were present and voted. | |

| | Merger or Consolidation | | |||

| | Any two or more domestic corporations may merge or consolidate into a single corporation if approved by the board of each constituent corporation and if authorized by a majority vote at a shareholder meeting of each such corporation by the holders of outstanding shares. | | | Any two or more corporations existing under the laws of the state may merge into a single corporation pursuant to a board resolution and upon the majority vote by shareholders of each constituent corporation at an annual or special meeting. | |

| | Marshall Islands | | | Delaware | |

| | Authorization by a majority vote of the holders of a class of shares may be required if such class is entitled to vote if a proposed amendment to the articles, undertaken in connection with such merger or consolidation, would increase or decrease the aggregate number of authorized shares of such class, increase or decrease the par value of the shares of such class, or alter or change the powers, preferences or special rights of the shares of such class so as to affect them adversely. | | | Authorization by a majority vote of the holders of a class of shares may be required if such class is entitled to vote if a proposed amendment to the articles, undertaken in connection with such merger or consolidation, would increase or decrease the aggregate number of authorized shares of such class, increase or decrease the par value of the shares of such class, or alter or change the powers, preferences, or special rights of the shares of such class so as to affect them adversely. However, unless expressly required by its certificate of incorporation, no vote of stockholders of a constituent corporation that has a class or series of stock that is listed on a national securities exchange or held of record by more than 2,000 holders immediately prior to the execution of the agreement of merger by such constituent corporation shall be necessary to authorize a merger that meets certain conditions. | |

| | Any sale, lease, exchange or other disposition of all or substantially all the assets of a corporation, if not made in the corporation’s usual or regular course of business, once approved by the board of directors (and notice of the meeting shall be given to each shareholder of record, whether or not entitled to vote), shall be authorized by the affirmative vote of two-thirds of the shares of those entitled to vote at a shareholder meeting, unless any class of shares is entitled to vote thereon as a class, in which event such authorization shall require the affirmative vote of the holders of a majority of the shares of each class of shares entitled to vote as a class thereon and of the total shares entitled to vote thereon. | | | Every corporation may at any meeting of the board sell, lease or exchange all or substantially all of its property and assets as its board deems expedient and for the best interests of the corporation when so authorized by a resolution adopted by the holders of a majority of the outstanding stock of the corporation entitled to vote. | |

| | Upon approval by the board, any domestic corporation owning at least 90% of the outstanding shares of each class of another domestic corporation may merge such other corporation into itself without the authorization of the shareholders of any such corporation. | | | Any corporation owning at least 90% of the outstanding shares of each class of another corporation may merge the other corporation into itself and assume all of its obligations without the vote or consent of shareholders; however, in case the parent corporation is not the surviving corporation, the proposed merger shall be approved by a majority of the outstanding stock of the parent corporation entitled to vote at a duly called shareholder meeting. | |

| | Directors | | |||

| | The number of directors may be fixed by the bylaws, by the shareholders, or by action of the board under the specific provisions of a bylaw. The number of board members may be changed by an amendment to the bylaws, by the shareholders, or by action of the board under the specific provisions of a bylaw. | | | The number of board members shall be fixed by, or in a manner provided by, the bylaws and amended by an amendment to the bylaws, unless the certificate of incorporation fixes the number of directors, in which case a change in the number shall be made only by an amendment to the certificate of incorporation. | |

| | Marshall Islands | | | Delaware | |

| | If the board is authorized to change the number of directors, it can only do so by a majority of the entire board and so long as no decrease in the number shall shorten the term of any incumbent director. | | | Shareholders entitled to vote upon amendments to the bylaws hold the power to adopt, amend or repeal bylaws in a stock corporation that has received any payment for its stock, unless such power is otherwise conferred upon the directors in the certificate of incorporation. An amendment to the certification of incorporation must be approved by the board and a majority of outstanding stock entitled to vote thereon. | |

| | Removal of Directors: | | | Removal of Directors: | |

| | Any or all of the directors may be removed for cause by vote of the shareholders. The articles of incorporation or the bylaws may provide for such removal by board action, except in the case of any director elected by cumulative voting, or by shareholders of any class or series when entitled by the provisions of the articles of incorporation. | | | Any or all of the directors may be removed, with or without cause, by the holders of a majority of the shares entitled to vote unless the certificate of incorporation otherwise provides. | |

| | If the articles of incorporation or bylaws provide any or all of the directors may be removed without cause by vote of the shareholders. | | | In the case of a classified board, shareholders may effect the removal of any or all directors only for cause unless the certificate of incorporation provides otherwise. | |

| | Dissenters’ Rights of Appraisal | | |||

| | Shareholders have a right to dissent from any plan of merger, consolidation or sale of all or substantially all assets not made in the usual course of business, and receive payment of the fair value of their shares. However, the right of a dissenting shareholder under the BCA to receive payment of the appraised fair value of his or her shares shall not be available for the shares of any class or series of stock, which shares or depository receipts in respect thereof, at the record date fixed to determine the shareholders entitled to receive notice of and to vote at the meeting of the shareholders to act upon the agreement of merger or consolidation, were either (i) listed on a securities exchange or admitted for trading on an interdealer quotation system or (ii) held of record by more than 2,000 holders. The right of a dissenting shareholder to receive payment of the fair value of his or her shares shall not be available for any shares of stock of the constituent corporation surviving a merger if the merger did not require for its approval the vote of the shareholders of the surviving corporation. | | | Appraisal rights shall be available for the shares of any class or series of stock of a corporation in a merger or consolidation, subject to limited exceptions, such as a merger or consolidation of corporations listed on a national securities exchange in which listed stock is offered for consideration which is (i) listed on a national securities exchange or (ii) held of record by more than 2,000 holders. Notwithstanding those limited exceptions, appraisal rights will be available if shareholders are required by the terms of an agreement of merger or consolidation to accept certain forms of uncommon consideration. | |

| | Marshall Islands | | | Delaware | |

| | A holder of any adversely affected shares who does not vote on or consent in writing to an amendment to the articles of incorporation has the right to dissent and to receive payment for such shares if the amendment: • alters or abolishes any preferential right of any outstanding shares having preference; or • creates, alters, or abolishes any provision or right in respect to the redemption of any outstanding shares; or • alters or abolishes any preemptive right granted by law and not disseated by the articles of incorporation of such holder to acquire shares or other securities; or • excludes or limits the right of such holder to vote on any matter, except as such right may be limited by the voting rights given to new shares then being authorized of any existing or new class. | | | Shareholders do not have appraisal rights due to an amendment of the company’s certificate of incorporation unless provided for in such certificate. | |

| • | an individual citizen or resident of the United States; |

| • | a corporation (or other entity treated as a corporation for U.S. federal income tax purposes) that is created or organized (or treated as created or organized) in or under the laws of the United States, any state thereof or the District of Columbia; |

| • | an estate whose income is includible in gross income for U.S. federal income tax purposes regardless of its source; or |

| • | a trust if (i) a U.S. court can exercise primary supervision over the trust’s administration and one or more U.S. persons are authorized to control all substantial decisions of the trust, or (ii) it has a valid election in effect under applicable U.S. Treasury regulations to be treated as a U.S. person. |

| • | financial institutions or “financial services entities”; |

| • | broker-dealers; |

| • | taxpayers who have elected mark-to-market accounting for U.S. federal income tax purposes; |

| • | tax-exempt entities; |

| • | governments or agencies or instrumentalities thereof; |

| • | insurance companies; |

| • | regulated investment companies; |

| • | real estate investment trusts; |

| • | certain expatriates or former long-term residents of the United States; |

| • | persons that actually or constructively own 10% or more (by vote or value) of our shares; |

| • | persons that own shares through an “applicable partnership interest”; |

| • | persons required to recognize income for U.S. federal income tax purposes no later than when such income is reported on an “applicable financial statement”; |

| • | persons that hold our common shares as part of a straddle, constructive sale, hedging, conversion or other integrated transaction; or |

| • | persons whose functional currency is not the U.S. dollar. |

| • | more than 50% of the value of our stock is owned, directly or indirectly, by “qualified shareholders,” that are persons (i) who are “residents” of our country of organization or of another foreign country that grants an “equivalent exemption” to corporations organized in the United States, and (ii) we satisfy certain substantiation requirements, which we refer to as the “50% Ownership Test”; or |

| • | our stock is “primarily” and “regularly” traded on one or more established securities markets in our country of organization, in another country that grants an “equivalent exemption” to United States corporations, or in the United States, which we refer to as the “Publicly-Traded Test.” |

| • | we have, or are considered to have, a fixed place of business in the United States involved in the earning of shipping income; and |

| • | substantially all of our U.S. source gross shipping income is attributable to regularly scheduled transportation, such as the operation of a vessel that follows a published schedule with repeated sailings at regular intervals between the same points for voyages that begin or end in the United States, or, in the case of income from the leasing of a vessel, is attributable to a fixed place of business in the United States. |

| • | at least 75% of our gross income for such taxable year consists of passive income (e.g., dividends, interest, capital gains and rents derived other than in the active conduct of a rental business); or |

| • | at least 50% of the average value of the assets held by us during such taxable year produce, or is held for the production of, passive income. |

| • | the excess distribution or gain would be allocated ratably over the Non-Electing Holder’s aggregate holding period for our common shares; |

| • | the amount allocated to the current taxable year and any taxable year before we became a passive foreign investment company would be taxed as ordinary income; and |

| • | the amount allocated to each of the other taxable years would be subject to tax at the highest rate of tax in effect for the applicable class of taxpayer for that year, and an interest charge for the deemed deferral benefit would be imposed with respect to the resulting tax attributable to each such other taxable year. |

| • | fails to provide an accurate taxpayer identification number; |

| • | is notified by the IRS that backup withholding is required; or |

| • | fails in certain circumstances to comply with applicable certification requirements. |

| | | Number of Shares | |

Underwriter | | | |

Maxim Group LLC | | | 1,250,000 |

TOTAL | | | 1,250,000 |

| | | Per Common Share | | | Total Without Exercise of Over-Allotment Option | | | Total With Full Exercise of Over-Allotment Option | |

Initial public offering price | | | | | | | |||

Underwriting discounts and commissions(1) | | | | | | | |||

Proceeds, before expenses, to us | | | | | | |

| (1) | The underwriter shall receive an underwriting discount of between 6.4% and 6.9% per share for sales to investors in this offering. We have agreed that Maxim Group LLC will also receive a Representative’s Warrant to purchase a number of common shares that is equal to between 6.4% and 6.9% of the aggregate number of common shares sold in this offering (up to 86,250 common shares, or up to 99,188 common shares if the underwriter exercises the over-allotment option in full), at an exercise price per share equal to 110% of the offering price, subject to certain anti-dilution adjustments. The Representative’s Warrant will be non-exercisable for six months from the date of |

| • | Stabilizing transactions — The representative may make bids or purchases for the purpose of pegging, fixing or maintaining the price of the shares, so long as stabilizing bids do not exceed a specified maximum. |

| • | Over-allotments and syndicate covering transactions — The underwriters may sell more common shares in connection with this offering than the number of shares than they have committed to purchase. This |

| • | Penalty bids — If the representative purchases shares in the open market in a stabilizing transaction or syndicate covering transaction, it may reclaim a selling concession from the underwriters and selling group members who sold those shares as part of this offering. |

| • | Passive market making — Market makers in the shares who are underwriters or prospective underwriters may make bids for or purchases of shares, subject to limitations, until the time, if ever, at which a stabilizing bid is made. |

| • | the information set forth in this prospectus and otherwise available to the representative; |

| • | our prospects and the history and prospects for the industry in which we compete; |

| • | an assessment of our management; |

| • | our prospects for future earnings; |

| • | the general condition of the securities markets at the time of this offering; |

| • | the recent market prices of, and demand for, publicly traded common shares of generally comparable companies; and |

| • | other factors deemed relevant by the underwriters and us. |

SEC registration fee | | | $1,142 |

FINRA filing and other fees | | | $8,150 |

NASDAQ listing and other fees | | | $55,000 |

Legal fees and expenses | | | $715,000 |

Printing expenses | | | $35,000 |

Accounting fees and expenses | | | $220,000 |

Transfer agent fees and expenses | | | $5,250 |

Underwriter fees and accountable expenses | | | $80,000 |

Miscellaneous | | | $125,458 |

Total(1) | | | $1,245,000 |

| (1) | Including approximately $25,000 of expenses already paid by us up to December 31, 2023, and approximately $30,000 of non-cash charges. Excluding these items, the total expenses (other than underwriting discounts and commissions) deducted from the estimated net proceeds from this offering amount to $1,190,000. |

| | | Notes | | | December 31, 2023 | | | December 31, 2022 | |

Assets | | | | | | | |||

Current assets | | | | | | | |||

Cash and cash equivalents | | | 2 | | | $2,702 | | | $3,551 |

Trade receivables | | | 2 | | | — | | | 117 |

Due from manager | | | 3 | | | 207 | | | 168 |

Inventories | | | 2 | | | 57 | | | 134 |

Prepayments and advances | | | | | 43 | | | 44 | |

Other current assets | | | | | 13 | | | 25 | |

Total current assets | | | | | $3,022 | | | $4,039 | |

Non-current assets | | | | | | | |||

Vessel, net | | | 4 | | | 9,181 | | | 9,861 |

Advances for vessel improvements | | | 4 | | | 22 | | | — |

Deferred drydocking costs, net | | | 5 | | | 340 | | | 697 |

Deferred issuance costs | | | 2 | | | 317 | | | — |

Total non-current assets | | | | | $9,860 | | | $10,558 | |

Total assets | | | | | $12,882 | | | $14,597 | |

| | | | | | | ||||

Liabilities and shareholders’ equity | | | | | | | |||