UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

| | | | | |

| ☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 28, 2024

or

| | | | | |

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to .

Commission File Number 1-5480

Textron Inc.

(Exact name of registrant as specified in its charter)

| | | | | | | | |

| Delaware | | 05-0315468 |

| (State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

| 40 Westminster Street, Providence, RI | | 02903 |

| (Address of principal executive offices) | | (Zip code) |

Registrant’s Telephone Number, Including Area Code: (401) 421-2800

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | |

| Title of Each Class | Trading Symbol(s) | Name of Each Exchange on Which Registered |

| Common Stock — par value $0.125 | TXT | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

______________________________________________

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. xYes ¨ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act . ¨ Yes x No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x Yes ¨ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). x Yes ¨No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act (Check one):

| | | | | | | | | | | | | | | | | |

| Large accelerated filer | x | | | Accelerated filer | ☐ |

| Non-accelerated filer | ☐ | Smaller reporting company | ☐ | Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ◻

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒ Yes ¨ No

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant's executive officers during the relevant recovery period pursuant to §240.10D-1(b) ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). ☐ Yes ☒ No

The aggregate market value of the registrant’s Common Stock held by non-affiliates at June 29, 2024 was approximately $16.0 billion based on the New York Stock Exchange closing price for such shares on that date. The registrant has no non-voting common equity.

At February 1, 2025, 182,572,762 shares of Common Stock were outstanding.

| | |

| Documents Incorporated by Reference |

Part III of this Report incorporates information from certain portions of the registrant’s Definitive Proxy Statement for its Annual Meeting of Shareholders to be held on April 23, 2025.

Textron Inc.

Index to Annual Report on Form 10-K

For the Fiscal Year Ended December 28, 2024

PART I

Item 1. Business

Textron Inc. is a multi-industry company that leverages its global network of aircraft, defense, industrial and finance businesses to provide customers with innovative products and services around the world. References to “Textron Inc.,” the “Company,” “we,” “our” and “us” in this Annual Report on Form 10-K, unless otherwise indicated, refer to Textron Inc. and its consolidated subsidiaries.

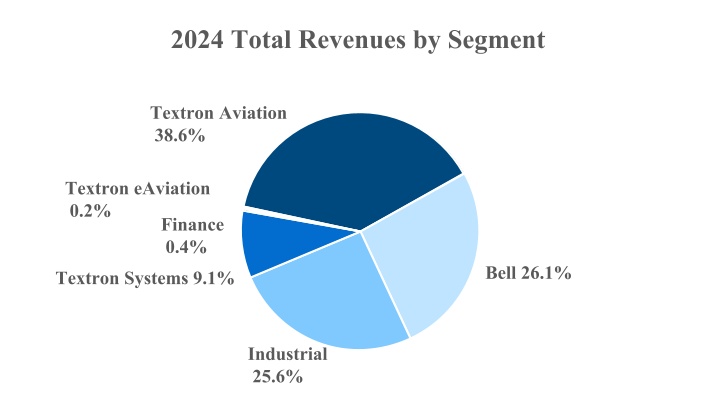

We conduct our business through six operating segments: Textron Aviation, Bell, Textron Systems, Industrial and Textron eAviation, which represent our manufacturing businesses, and Finance, which represents our captive finance business. Our segments include numerous separately incorporated subsidiaries. Total revenues for 2024 were $13.7 billion and are presented below by segment and customer type.

The following description of our business and operating segments should be read in conjunction with Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

Textron Aviation Segment

Textron Aviation is a leader in general aviation. Textron Aviation manufactures, sells and services Cessna and Beechcraft aircraft, and services the Hawker brand of business jets. The segment has two principal product lines: aircraft and aftermarket parts and services. Aircraft includes sales of business jets, turboprop aircraft, military trainer and defense aircraft and piston engine aircraft. Aftermarket parts and services includes commercial parts sales and maintenance, inspection and repair services, and advanced flight training devices.

Textron Aviation's business jets include the Cessna Citation M2 Gen2, Citation CJ3+, Citation CJ4 Gen2, Citation XLS Gen2, Citation Latitude and the Citation Longitude. In October 2024, Textron Aviation introduced its next generation of light jets, the Citation M2 Gen3, CJ3 Gen3 and CJ4 Gen3, which will include the revolutionary Garmin Emergency Autoland technology. Currently under development, the CJ3 Gen2 is expected to enter into service in 2025, the CJ4 Gen3 is expected to enter into service in 2026, and the M2 Gen3 and CJ3 Gen3 are expected to enter into service in 2027. In addition, Textron Aviation is developing the Citation Ascend, a high-performance midsize business jet, which is continuing to progress through the Federal Aviation Administration's (FAA) certification process and is expected to enter into service in 2025.

Textron Aviation’s turboprop aircraft include the Beechcraft King Air 260, King Air 360ER and King Air 360, and the Cessna Caravan, Grand Caravan EX and SkyCourier. The Beechcraft Denali, a high-performance single engine turboprop aircraft under development, continues toward FAA certification. The Denali will be powered by an engine expected to be up to 20% more efficient than similarly sized engines.

Textron Aviation’s military trainer and defense aircraft include the Beechcraft T-6 trainer, which has been used to train pilots from more than 40 countries, and the AT-6 light attack military aircraft. Textron Aviation’s piston engine aircraft include the Cessna Skyhawk, Skylane, Turbo Skylane, Turbo Stationair HD and the Beechcraft Baron G58 and Bonanza G36.

Textron Aviation markets its products worldwide through its own sales force, as well as through a network of authorized independent sales representatives. With a product lineup ranging from introductory training aircraft through super mid-size business jets, Textron Aviation’s diverse customer base includes fractional aircraft businesses, charter and fleet operators, corporate aviation, individual buyers, training schools, airlines, and special mission, military and government operators.

In support of its family of aircraft, Textron Aviation operates a global network of more than 20 service centers. In addition, more than 300 authorized independent service centers are located throughout the world. Textron Aviation-owned service centers provide customers with 24-hour service and maintenance. Textron Aviation also provides its customers with around-the-clock parts support and offers a mobile support program with over 80 mobile service units.

Bell Segment

Bell is a leading supplier of military and commercial helicopters, tiltrotor aircraft, and related spare parts and services in the world. Tiltrotor aircraft are designed to provide the benefits of both helicopters and fixed-wing aircraft.

Bell supplies advanced military helicopters and provides parts and support services to the U.S. Government and to military customers outside the United States. Bell’s primary U.S. Government programs are for the development of a next generation tiltrotor aircraft for the U.S. Army’s Future Long Range Assault Aircraft (FLRAA) program and the production and support of the V-22 tiltrotor aircraft and H-1 helicopters. Under the U.S. Government-sponsored foreign military sales program, Bell offers the V-22 tiltrotor aircraft and H-1 helicopter products for sale to other countries.

The FLRAA development contract was awarded to Bell in December 2022. In 2024, the U.S. Army announced approval of Milestone B for the FLRAA program, establishing FLRAA as a program of record and transitioning the program to the Engineering and Manufacturing Development phase. This phase includes continued digital modeling, detailed hardware and software design, and fabrication of hardware, as Bell proceeds to critical design review and the first prototype flight planned for 2026.

Through its commercial business, Bell is a leading supplier of commercially certified helicopters and support to corporate, private, law enforcement, utility, public safety and emergency medical helicopter operators, and U.S. and foreign governments. Bell produces a variety of commercial aircraft types, including light single- and twin-engine helicopters and medium twin-engine helicopters, along with other related products. The commercial helicopters currently offered by Bell include the 429, 407GXi, 412EPX and 505 Jet Ranger X. Bell’s super medium commercial helicopter, the 525 Relentless, continues toward FAA certification.

For both its military programs and its commercial products, Bell provides post-sale support and service for an installed base of approximately 13,000 helicopters. Bell operates a global network of eight Company-operated service centers and four global parts distribution centers. In addition, approximately 85 independent service centers are located in about 35 countries. Collectively, these service sites offer a complete range of logistics support, including parts, support equipment, technical data, training devices, pilot and maintenance training, component repair and overhaul, engine repair and overhaul, aircraft modifications, aircraft customizing, accessory manufacturing, contractor maintenance, field service and product support engineering.

Textron Systems Segment

The businesses in our Textron Systems segment develop, manufacture and integrate a variety of products and services for U.S. and international military, government and commercial customers to support defense, homeland security, aerospace, infrastructure protection and other customer missions. Product and service offerings of this segment include electronic systems and solutions, advanced marine craft, piston aircraft engines, live military air-to-air and air-to-ship training, weapons and related components, unmanned aircraft systems and both manned and unmanned armored and specialty vehicles.

Notable products currently developed and produced by the Textron Systems segment include the Ship-to-Shore Connector, the U.S. Navy's next generation of Landing Craft Air Cushion vehicles; a family of test and simulation products; the Aerosonde Small Unmanned Aircraft System, a multi-mission capable unmanned aircraft system for commercial and military operations; and piston aircraft engines under the Lycoming brand. Notable service offerings of the segment include fee-for-service programs, using unmanned aircraft systems, and live military air-to-air and air-to-ship training and support services for U.S. Navy, Marine and Air Force personnel provided by Airborne Tactical Advantage Company.

Industrial Segment

Our Industrial segment designs and manufactures a variety of products within the Kautex and Textron Specialized Vehicles businesses.

Kautex is a leader in designing and manufacturing plastic fuel systems for automobiles and light trucks, including blow-molded solutions for conventional plastic fuel tanks and pressurized plastic fuel tanks for hybrid vehicle applications. Kautex also develops and manufactures clear-vision systems for automotive safety and advanced driver assistance systems (ADAS). Our cleaning systems are comprised of nozzles, reservoirs, inlets and pumps to support onboard cleaning for windscreens, headlamps and ADAS cameras and sensors. In addition, Kautex produces plastic tanks for selective catalytic reduction systems used to reduce emissions from diesel engines, and other fuel system components. Kautex also offers lightweight, composite Pentatonic battery systems, which include enclosures, underbody protection and thermal management systems, for use in electric vehicles, from hybrid to full battery-powered.

Kautex’s business model is focused on developing and maintaining long-term customer relationships with leading global original equipment manufacturers (OEMs). Kautex, which is headquartered in Bonn, Germany, operates over 30 plants in 13 countries in close proximity to its customers, along with 9 engineering/research and development locations around the world.

Our Textron Specialized Vehicles businesses manufacture and sell products under our E-Z-GO, Arctic Cat, TUG Technologies, Douglas Equipment, Premier, Safeaero, Ransomes, Jacobsen and Cushman brands. These businesses design, manufacture and sell golf cars; off-road utility vehicles; powersports products; light transportation vehicles; aviation ground support equipment; professional turf-maintenance equipment; and specialized turf-care vehicles. A significant portion of the products sold by these businesses are powered with lithium batteries, greatly reducing the products’ impact on the environment.

The diversified customer base for Textron Specialized Vehicles includes golf courses and resorts, government agencies and municipalities, consumers, outdoor enthusiasts, and commercial and industrial users such as factories, warehouses, airlines, planned communities, hunting preserves, educational and corporate campuses, sporting venues and landscaping professionals. Sales are made through a network of independent distributors and dealers worldwide and the Bass Pro Shops and Cabela's retail outlets, which sell our powersports products under the Tracker Off Road brand, as well as factory direct resources. In addition, we also manufacture powersports products for OEMs for resale to customers under the OEM’s branding.

Textron eAviation Segment

Our Textron eAviation segment is focused on research and development initiatives related to sustainable aviation solutions and includes Pipistrel, a manufacturer of light aircraft. Pipistrel offers a family of light aircraft and gliders with both electric and combustion engines, including the Velis Electro, which is the world’s first, and currently only, electric aircraft to receive full type certification from the European Union Aviation Safety Agency and from the UK Civil Aviation Authority. In 2024, the FAA granted a light-sport aircraft airworthiness exemption for the Pipistrel Velis Electro, allowing flight training in an electric aircraft within the United States.

The Textron eAviation segment is also developing both hybrid and electric propulsion aircraft, including Pipistrel's Nuuva V300, a long-range, large-capacity hybrid-electric vertical takeoff and landing aircraft, and an electric vertical takeoff and landing (eVTOL) aircraft. The Nuuva V300's first hover flight is expected in 2025 and initial testing on the Nexus, a full-scale technology demonstrator eVTOL, is expected to begin in 2025.

Finance Segment

Our Finance segment, or the Finance group, is a commercial finance business that consists of Textron Financial Corporation (TFC) and its consolidated subsidiaries. The Finance segment provides financing primarily to purchasers of new and pre-owned Textron Aviation aircraft and Bell helicopters. A substantial number of the originations in our finance receivable portfolio are cross-border transactions for aircraft sold outside of the U.S. In 2024 and 2023, our Finance group made payments of $109 million and $160 million, respectively, to finance the Manufacturing group's sale of Textron-manufactured products to third parties.

Backlog

Backlog represents amounts allocated to contracts that we expect to recognize as revenue in future periods when we perform under the contracts. Backlog excludes unexercised contract options and potential orders under ordering-type contracts, such as Indefinite Delivery, Indefinite Quantity contracts.

Our backlog at the end of 2024 and 2023 is summarized below:

| | | | | | | | |

| (In millions) | December 28,

2024 | December 30,

2023 |

| Textron Aviation | $ | 7,845 | | $ | 7,169 | |

| Bell | 7,469 | | 4,780 | |

| Textron Systems | 2,594 | | 1,950 | |

| Total backlog | $ | 17,908 | | $ | 13,899 | |

U.S. Government Contracts and Other Governmental Regulation

Our operations, products and services are subject to various government regulations, including regulations related to U.S. government business, international regulation of aviation products and services, and environmental regulations.

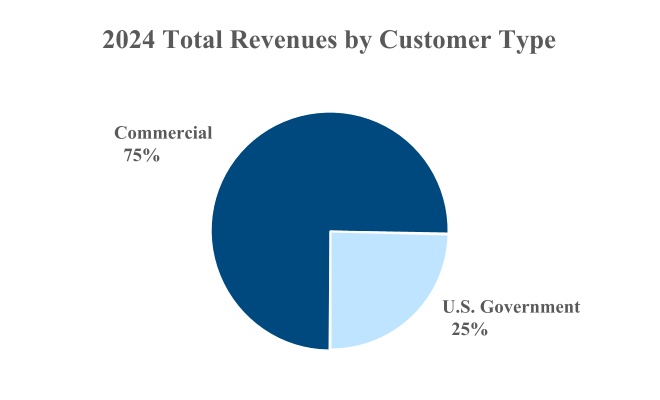

Contracts with the U.S. Government, including contracts under the U.S. Government-sponsored foreign military sales program, generated approximately 25% of our consolidated revenues in 2024, primarily in our Bell and Textron Systems segments. We must comply with and are affected by laws and regulations relating to the formation, administration and performance of U.S. Government contracts. These laws and regulations, among other things, require certification and disclosure of all cost and pricing

data in connection with contract negotiation; define allowable and unallowable costs and otherwise govern our right to reimbursement under certain cost-based U.S. Government contracts; and safeguard and restrict the use and dissemination of classified and covered defense information and the export of certain products and technical data. New laws, regulations or procurement requirements, or changes to current ones, can significantly increase our costs, reducing our profitability.

Our contracts with the U.S. Government generally may be terminated by the U.S. Government for convenience or if we default in whole or in part by failing to perform under the terms of the applicable contract. If the U.S. Government terminates a contract for convenience, we normally will be entitled to payment for the cost of contract work performed before the effective date of termination, including, if applicable, reasonable profit on such work, as well as reasonable termination costs. If, however, the U.S. Government terminates a contract for default, generally: (a) we will be paid the contract price for completed supplies delivered and accepted and services rendered, an agreed-upon amount for manufacturing materials delivered and accepted and for the protection and preservation of property, and an amount for partially completed products accepted by the U.S. Government; (b) the U.S. Government may not be liable for our costs with respect to unaccepted items and may be entitled to repayment of advance payments and progress payments related to the terminated portions of the contract; (c) the U.S. Government may not be liable for assets we own and utilize to provide services under the “fee-for-service” contracts; and (d) we may be liable for excess costs incurred by the U.S. Government in procuring undelivered items from another source. See the Aerospace and Defense Industry section in Item 1A. Risk Factors for additional information related to regulation of U.S. Government business.

Our commercial aircraft manufacturing businesses are regulated by the FAA in the U.S. and by similar aviation regulatory governing authorities internationally, including, the European Aviation Safety Agency. Maintenance facilities and aftermarket services must also comply with FAA and international regulations. These regulations address production and quality systems, airworthiness and installation approvals, repair procedures and continuing operational safety. For an aircraft to be manufactured and sold, the model must receive a type certificate from the appropriate aviation authority, and each aircraft must receive a certificate of airworthiness. Aircraft outfitting and completions also require approval by the appropriate aviation authority. See the Strategic Risks section in Item 1A. Risk Factors for additional information with respect to risks related to obtaining certification of new aircraft products.

Our operations are subject to numerous laws and regulations designed to protect the environment. For additional information regarding environmental matters, see Note 17 to the Consolidated Financial Statements in Item 8. Financial Statements and Supplementary Data, and the Business and Operational Risks and Risks Related to Regulatory, Legal and Other Matters sections in Item 1A. Risk Factors.

Based on current information and the applicable laws and regulations currently in effect, compliance with government regulations, including environmental regulations, has not had, and we do not expect it to have, a material effect on our capital expenditures, earnings or competitive position. However, laws and regulations may be changed or adopted that impose additional compliance requirements which could necessitate capital expenditures or otherwise increase our costs of doing business, reducing our profitability and negatively impacting our operating results.

Human Capital Resources

At December 28, 2024, we employed approximately 34,000 employees worldwide, with approximately 80% located in the U.S. and the remainder located outside of the U.S. Approximately 7,400, or 28%, of our U.S. employees, most of whom work for our Bell and Textron Aviation segments, are represented by unions under collective bargaining agreements, and certain of our non-U.S. employees are represented by organized works councils. From time to time, our collective bargaining agreements expire. Historically, we have been successful in negotiating renewals to expiring agreements without any material disruption of operating activities; however, on September 21, 2024, Textron Aviation’s largest union rejected a proposed new contract and initiated a strike. The strike impacted approximately 5,000 of Textron Aviation’s employees at its manufacturing, parts and distribution and service center facilities in Wichita, Kansas. On October 20, 2024, Textron Aviation and the union reached an agreement and a new five-year labor contract was ratified.

Our success is highly dependent upon our ability to hire, train and retain a workforce with the skills necessary for our businesses to develop and manufacture the products desired by our customers. We need highly skilled personnel in multiple areas including, among others, engineering, manufacturing, information technology, cybersecurity, flight operations, business development and strategy and management. In order to attract and retain highly skilled employees, we offer comprehensive compensation and benefit programs, career opportunities and an engaging, inclusive environment where employees are treated with dignity and respect.

Health and Safety

The health and safety of our employees, contractors and communities is a priority, and we strive to provide our employees with healthy working conditions and safe facilities. To maintain and enhance the safety of our employees, we promote a workplace safety culture of continuous improvement, shared responsibility, and individual accountability. We use an annual goal setting

process to drive injury rate improvements, and the injury rate reduction goal is a performance metric that is tracked and reported to senior leadership and the Audit Committee of the Board of Directors.

Talent and Career Development

Our talent development programs are designed to prepare our employees at all levels to take on new career and growth opportunities at Textron. Leadership, professional and functional training courses are tailored for employees at each stage of their careers and include a mix of enterprise-wide and business unit-specific programs. Textron University, an internal corporate function, provides (i) facilitated face-to-face professional and leadership development programs, (ii) web-based general and specialized functional and technical courses and (iii) an online portal to access advanced skills technical training, manage recertification of existing qualifications and other career planning tools and resources.

The current and future talent needs of each of our businesses are assessed annually through a formal talent review process which enables us to develop leadership succession plans and provide our employees with potential new career opportunities. In addition, leaders from functional areas within each business belong to enterprise-wide councils that conduct annual talent reviews. These processes enable us to fill talent needs by matching employees who are ready to assume significant leadership roles with opportunities that best fit their career path, which may be in other businesses within the enterprise.

We believe by employing highly talented employees who feel valued, respected and are able to contribute fully, we will improve performance, innovation, collaboration and talent retention, all of which contributes to stronger business results and reinforces our reputation as leaders in our industries and communities.

For discussion of certain risks relating to human capital management, see the Risks Related to Human Capital section in Item 1A. Risk Factors.

Patents and Trademarks

We own, or are licensed under, numerous patents throughout the world relating to products, services and methods of manufacturing. Patents developed while under contract with the U.S. Government may be subject to use by the U.S. Government. We also own or license active trademark registrations and pending trademark applications in the U.S. and in various foreign countries or regions, as well as trade names and service marks. While our intellectual property rights in the aggregate are important to the operation of our business, we do not believe that any existing patent, license, trademark or other intellectual property right is of such importance that its loss or termination would have a material adverse effect on our business taken as a whole.

Information about our Executive Officers

The following table sets forth certain information concerning our executive officers as of February 6, 2025.

| | | | | | | | |

| Name | Age | Current Position with Textron Inc. |

| Scott C. Donnelly | 63 | Chairman, President and Chief Executive Officer |

| Frank T. Connor | 65 | Executive Vice President and Chief Financial Officer |

| Julie G. Duffy | 59 | Executive Vice President and Chief Human Resources Officer |

| E. Robert Lupone | 65 | Executive Vice President, General Counsel, Secretary and Chief Compliance Officer |

Mr. Donnelly joined Textron in June 2008 as Executive Vice President and Chief Operating Officer and was promoted to President and Chief Operating Officer in January 2009. He was appointed to the Board of Directors in October 2009 and became Chief Executive Officer of Textron in December 2009. In July 2010, Mr. Donnelly was appointed Chairman of the Board of Directors effective September 1, 2010. Previously, Mr. Donnelly was the President and CEO of General Electric Company’s Aviation business unit, a position he had held since July 2005. GE’s Aviation business unit is a leading maker of commercial and military jet engines and components, as well as integrated digital, electric power and mechanical systems for aircraft. Prior to July 2005, Mr. Donnelly served as Senior Vice President of GE Global Research, one of the world’s largest and most diversified industrial research organizations with facilities in the U.S., India, China and Germany and held various other management positions since joining General Electric in 1989.

Mr. Connor joined Textron in August 2009 as Executive Vice President and Chief Financial Officer. Previously, Mr. Connor was head of Telecom Investment Banking at Goldman, Sachs & Co. from 2003 to 2008. Prior to that position, he served as Chief Operating Officer of Telecom, Technology and Media Investment Banking at Goldman, Sachs & Co. from 1998 to 2003. Mr. Connor joined the Corporate Finance Department of Goldman, Sachs & Co. in 1986 and became a Vice President in 1990 and a Managing Director in 1996.

On October 23, 2024, we announced that Mr. Connor will be retiring effective February 28, 2025. David Rosenberg, currently our Vice President – Investor Relations, has been appointed Executive Vice President and Chief Financial Officer to succeed Mr. Connor, effective March 1, 2025. Mr. Rosenberg, 48, has more than 24 years of experience in the aviation industry. Prior to his role as Vice President – Investor Relations, he served as Senior Vice President & Chief Financial Officer of Textron Aviation from 2018 through 2023, having previously held leadership positions in finance at Textron Aviation. Following Textron’s acquisition of Beechcraft in 2014, as Textron Aviation’s Vice President, Integration & Strategy, Mr. Rosenberg led the successful merger and integration of Beechcraft and Textron’s Cessna Aircraft business, which created today’s Textron Aviation segment. Prior to Textron’s acquisition of Beechcraft, Mr. Rosenberg held a series of leadership positions in financial planning, business management, strategic planning and operations with Beechcraft and its predecessor companies.

Ms. Duffy was named Executive Vice President, Human Resources in July 2017 and Executive Vice President and Chief Human Resources Officer in April 2022. Ms. Duffy joined Textron in 1997 as a member of the corporate legal team and has since held positions of increasing responsibility within the Company’s legal function, previously serving as Vice President and Deputy General Counsel – Litigation, a position she had held since 2011. In that role she was responsible for managing the corporate litigation staff with primary oversight of litigation throughout Textron. She has also played an active role in developing, implementing and standardizing human resources policies across the Company and served as the senior legal advisor on employment and benefits issues.

Mr. Lupone joined Textron in February 2012 as Executive Vice President, General Counsel, Secretary and Chief Compliance Officer. Previously, he was Senior Vice President and General Counsel of Siemens Corporation (U.S.) since 1999 and General Counsel of Siemens AG for the Americas since 2008. Prior to joining Siemens in 1992, Mr. Lupone was Vice President and General Counsel of Price Communications Corporation.

Available Information

We make available free of charge on our Internet Web site (www.textron.com) our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 as soon as reasonably practicable after we electronically file such material with, or furnish it to, the Securities and Exchange Commission.

Forward-Looking Information

Certain statements in this Annual Report on Form 10-K and other oral and written statements made by us from time to time are “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements, which may describe strategies, goals, outlook or other non-historical matters, or project revenues, income, returns or other financial measures, often include words such as “believe,” “expect,” “anticipate,” “intend,” “plan,” “estimate,” “guidance,” “project,” “target,” “potential,” “will,” “should,” “could,” “likely” or “may” and similar expressions intended to identify forward-looking statements. These statements are only predictions and involve known and unknown risks, uncertainties, and other factors that may cause our actual results to differ materially from those expressed or implied by such forward-looking statements. Given these uncertainties, you should not place undue reliance on these forward-looking statements. Forward-looking statements speak only as of the date on which they are made, and we undertake no obligation to update or revise any forward-looking statements. In addition to those factors described herein under “Risk Factors,” among the factors that could cause actual results to differ materially from past and projected future results are the following:

•Interruptions in the U.S. Government’s ability to fund its activities and/or pay its obligations;

•Changing priorities or reductions in the U.S. Government defense budget, including those related to military operations in foreign countries;

•Our ability to perform as anticipated and to control costs under contracts with the U.S. Government;

•The U.S. Government’s ability to unilaterally modify or terminate its contracts with us for the U.S. Government’s convenience or for our failure to perform, to change applicable procurement and accounting policies, or, under certain circumstances, to withhold payment or suspend or debar us as a contractor eligible to receive future contract awards;

•Changes in foreign military funding priorities or budget constraints and determinations, or changes in government regulations or policies on the export and import of military and commercial products;

•Volatility in the global economy or changes in worldwide political conditions that adversely impact demand for our products;

•Volatility in interest rates or foreign exchange rates and inflationary pressures;

•Risks related to our international business, including establishing and maintaining facilities in locations around the world and relying on joint venture partners, subcontractors, suppliers, representatives, consultants and other business partners in connection with international business, including in emerging market countries;

•Our Finance segment’s ability to maintain portfolio credit quality or to realize full value of receivables;

•Performance issues with key suppliers or subcontractors;

•Legislative or regulatory actions, both domestic and foreign, impacting our operations or demand for our products;

•Our ability to control costs and successfully implement various cost-reduction activities;

•The efficacy of research and development investments to develop new products or unanticipated expenses in connection with the launching of significant new products or programs;

•The timing of our new product launches or certifications of our new aircraft products;

•Our ability to keep pace with our competitors in the introduction of new products and upgrades with features and technologies desired by our customers;

•Pension plan assumptions and future contributions;

•Demand softness or volatility in the markets in which we do business;

•Cybersecurity threats, including the potential misappropriation of assets or sensitive information, corruption of data or operational disruption;

•Difficulty or unanticipated expenses in connection with integrating acquired businesses;

•The risk that acquisitions do not perform as planned, including, for example, the risk that acquired businesses will not achieve revenue and profit projections;

•The impact of changes in tax legislation;

•The risk of disruptions to our business and the business of our suppliers, customers and other business partners due to unexpected events, such as pandemics, natural disasters, acts of war, strikes, terrorism, social unrest or other societal, geopolitical or macroeconomic conditions;

•Risks related to changing U.S. and foreign trade policies, including increased trade restrictions or tariffs; and

•The ability of our businesses to hire, train and retain the highly skilled personnel necessary for our businesses to succeed.

Item 1A. Risk Factors

Our business, financial condition and results of operations are subject to various risks, including those discussed below, which may affect the value of our securities. The risks discussed below are those that we believe currently are the most significant to our business.

Aerospace and Defense Industry Risks

Demand for our aircraft products is cyclical and lower demand adversely affects our financial results.

Demand for business jets, turbo props and commercial helicopters has been cyclical and difficult to forecast. From time to time, the demand for our aircraft products has been adversely impacted by unexpected events and may be impacted by such events in the future. Therefore, future demand for these products could be significantly and unexpectedly less than anticipated and/or less than previous period deliveries. Similarly, there is uncertainty as to when or whether our existing commercial backlog for aircraft products will convert to revenues as the conversion depends on production capacity, customer needs and credit availability, among other factors. Changes in economic conditions have in the past caused, and in the future may cause, customers to request that firm orders be rescheduled, deferred or cancelled. Reduced demand for our aircraft products or delays or cancellations of orders previously has had and, in the future, could have a material adverse effect on our cash flows, results of operations and financial condition.

We have customer concentration with the U.S. Government; reduction in U.S. Government defense spending can adversely affect our results of operations and financial condition.

During 2024, we derived approximately 25% of our revenues from sales to a variety of U.S. Government entities. Our revenues from the U.S. Government largely result from contracts awarded to us under various U.S. Government defense-related programs. Considerable uncertainty exists regarding how future budget and program decisions will develop. We cannot predict the impact on existing, follow-on or future programs from changes in the threat environment, defense spending levels, government priorities, political leadership, procurement practices, inflation and other macroeconomic trends, military strategy, or broader societal changes. Significant changes in national and international priorities for defense spending could affect the funding, or the timing of funding, of our programs, which could negatively impact our results of operations and financial condition.

The funding of U.S. Government defense programs is subject to congressional appropriation decisions and the U.S. Government budget process which includes enacting relevant legislation, such as appropriations bills and accords on the debt ceiling. Although multiple-year contracts may be planned in connection with major procurements, Congress generally appropriates funds on a fiscal year basis even though a program may continue for several years. Consequently, programs often are only partially funded initially, and additional funds are committed only as Congress makes further appropriations. Further uncertainty with respect to ongoing programs could also result in the event that the U.S. Government finances its operations through temporary funding measures such as “continuing resolutions” rather than full-year appropriations or if a government shutdown were to occur and were to continue for an extended period of time. If we incur costs in advance or in excess of funds committed on a contract, we are at risk for non-reimbursement of those costs until additional funds are appropriated. The reduction, termination or delay in the timing of funding for U.S. Government programs for which we currently provide or propose to provide products or services from time to time has resulted and, in the future, may result in a loss of anticipated revenues. A loss of such revenues could materially

and adversely impact our results of operations and financial condition. In addition, because our U.S. Government contracts generally require us to continue to perform even if the U.S. Government is unable to make timely payments, we may need to finance our continued performance for the impacted contracts from our other resources on an interim basis. An extended delay in the timely payment by the U.S. Government could have a material adverse effect on our liquidity.

U.S. Government contracts can be terminated at any time and may contain other unfavorable provisions.

The U.S. Government typically can terminate or modify any of its contracts with us either for its convenience or if we default by failing to perform under the terms of the applicable contract. In the event of termination for the U.S. Government’s convenience, contractors are generally protected by provisions covering reimbursement for costs incurred on the contracts and profit on those costs but not the anticipated profit that would have been earned had the contract been completed. A termination arising out of our default for failure to perform could expose us to liability, including but not limited to, all costs incurred under the contract plus potential liability for re-procurement costs in excess of the total original contract amount, less the value of work performed and accepted by the customer under the contract. Such an event could also have an adverse effect on our ability to compete for future contracts and orders. If any of our contracts are terminated by the U.S. Government whether for convenience or default, our backlog would be reduced by the expected value of the remaining work under such contracts. We also enter into “fee for service” contracts with the U.S. Government where we retain ownership of, and consequently the risk of loss on, aircraft and equipment supplied to perform under these contracts. Termination of these contracts could materially and adversely impact our results of operations. On contracts for which we are teamed with others and are not the prime contractor, the U.S. Government could terminate a prime contract under which we are a subcontractor, irrespective of the quality of our products and services as a subcontractor. In addition, in the event that the U.S. Government is unable to make timely payments, failure to continue contract performance places the contractor at risk of termination for default. Any such event could have a material adverse effect on our cash flows, results of operations and financial condition.

As a U.S. Government contractor, we are subject to procurement rules and regulations; our failure to comply with these rules and regulations could adversely affect our business.

We must comply with and are affected by laws and regulations relating to the formation, administration and performance of U.S. Government contracts. These laws and regulations, among other things, require certification and disclosure of all cost and pricing data in connection with contract negotiation, define allowable and unallowable costs and otherwise govern our right to reimbursement under certain cost-based U.S. Government contracts, and safeguard and restrict the use and dissemination of classified information, covered defense information, and the exportation of certain products and technical data. New laws, regulations or procurement requirements or changes to current ones (including, for example, regulations related to cybersecurity) can significantly increase our costs, reducing our profitability. Our failure to comply with procurement regulations and requirements could allow the U.S. Government to suspend or debar us from receiving new contracts for a period of time, reduce the value of existing contracts, issue modifications to a contract, withhold cash on contract payments, and control and potentially prohibit the export of our products, services and associated materials, any of which could negatively impact our results of operations, financial condition or liquidity. A number of our U.S. Government contracts contain provisions that require us to make disclosure to the Inspector General of the agency that is our customer if we have credible evidence that we have violated U.S. criminal laws involving fraud, conflict of interest, or bribery; the U.S. civil False Claims Act; or received a significant overpayment under a U.S. Government contract. Failure to properly and timely make disclosures under these provisions may result in a termination for default or cause, suspension and/or debarment, and potential fines.

As a U.S. Government contractor, our businesses and systems are subject to audit and review by the Defense Contract Audit Agency (DCAA) and the Defense Contract Management Agency (DCMA).

We operate in a highly regulated environment and are routinely audited and reviewed by the U.S. Government and its agencies such as the DCAA and DCMA. These agencies review our performance under contracts, our cost structure and our compliance with laws and regulations applicable to U.S. Government contractors. The systems that are subject to review include, but are not limited to, our accounting, estimating, material management and accounting, earned value management, purchasing and government property systems. If an audit uncovers improper or illegal activities, we may be subject to civil and criminal penalties and administrative sanctions that may include the termination of our contracts, forfeiture or reduction of profits, suspension or reduction of payments, fines, and, under certain circumstances, suspension or debarment from future contracts for a period of time. Whether or not illegal activities are alleged, the U.S. Government also has the ability to decrease or withhold certain payments when it deems systems subject to its review to be inadequate. These laws and regulations affect how we conduct business with our government customers and, in some instances, impose added costs on our business.

Our profitability and cash flow varies depending on the mix of our government contracts and our ability to control costs.

Under fixed-price contracts, generally we receive a fixed price irrespective of the actual costs we incur, and, consequently, we absorb any costs in excess of the fixed price. Changes in underlying assumptions, circumstances or estimates used in developing the pricing for such contracts can adversely affect our results of operations. Additionally, fixed-price contracts generally require progress payments rather than performance-based payments which can delay our ability to recover a significant amount of costs

incurred on a contract and thus affect the timing of our cash flows. Under fixed-price incentive contracts, we share with the U.S. Government cost underrun savings, which are derived from total cost being less than target costs; we also share in cost overruns, which occur when total costs exceed target costs up to a negotiated cost ceiling; however, we are solely responsible for costs above the ceiling. Under time and materials contracts, we are paid for labor at negotiated hourly billing rates and for certain expenses. Under cost-reimbursement contracts that are subject to a contract-ceiling amount, we are reimbursed for allowable costs and paid a fee, which may be fixed or performance-based; however, if our costs exceed the contract ceiling or are not allowable under the provisions of the contract or applicable regulations, we may not be able to obtain reimbursement for all such costs. Due to the nature of our work under government contracts, we sometimes experience unforeseen technological or schedule difficulties and cost overruns due to inflation, labor shortages, supply chain challenges, bid protests, and/or other factors. Under each type of contract, if we are unable to control costs or if our initial cost estimates are incorrect, our cash flows, results of operations and financial condition could be adversely affected. Cost overruns also may adversely affect our ability to sustain existing programs and obtain future contract awards.

The market for U.S. Government defense business is highly competitive, and the competitive bidding process increases pricing pressure and cost which may affect our ability to win new contracts for major government programs.

Our defense businesses operate in highly competitive markets in which they participate in rigorous, increasingly competitive bidding processes against other defense companies for U.S. government business. The U.S. Government relies upon competitive contract award types, including indefinite-delivery, indefinite-quantity, other transaction agreements and multi-award contracts, which often create increased pricing pressure and increase our cost by requiring that we submit multiple bids or share in costs. In addition, multi-award contracts increase our cost as they require that we make sustained efforts to compete for task orders and delivery orders under the contract. Further, the competitive bidding process is costly, in some instances requires significant research and development and/or engineering efforts to participate and demands employee and managerial time to prepare bids and proposals for contracts that may not be awarded to us or may be split among competitors.

Despite our best efforts, the U.S. Government customer sometimes chooses competitor's offerings over our offerings and there can be no assurance that our businesses will be selected for government programs with significant long-term revenues. Even if we are successful in obtaining an award, we have in the past and may in the future encounter bid protests from unsuccessful bidders on new program awards. Bid protests could result in significant expenses associated with justifying the selection or due to potential program delays and could result in contract modifications that alter schedule or scope or even cause the loss of the contract award. Even when a bid protest does not result in the loss of a contract award, the resolution could postpone commencement of contract activity, resulting in additional cost and delay in the recognition of revenue and profit. If we are unable to continue to compete successfully against our current or future competitors, do not win government programs with significant long-term revenues or do not prevail in bid protests, we may experience declines in future revenues and profitability, which could have a material adverse effect on our financial position, results of operations or cash flows.

Strategic Risks

Developing new products and technologies entails significant risks and uncertainties.

To continue to grow our revenues and segment profit, we must successfully develop new products and technologies or modify our existing products and technologies for our current and future markets. Our future performance depends, in part, on our ability to identify emerging technological trends and customer requirements and to develop and maintain competitive products and services. Delays or cost overruns in the development and acceptance of new products or certification of new aircraft and other products occur from time to time and could adversely affect our results of operations. These delays or cost overruns could be caused by unanticipated technological hurdles, production changes to meet customer demands, unanticipated difficulties in obtaining required regulatory certifications of new aircraft or other products, or failure on the part of our suppliers to deliver components as agreed. We also could be adversely affected if our research and development efforts are less successful than expected or if these efforts require significantly more funding to achieve our goals than anticipated. In particular, the success of Textron eAviation depends in large part, on our ability to develop and certify new electric and hybrid electric aircraft products in order to achieve our long-term strategy of offering a family of sustainable aircraft for urban air mobility, general aviation, cargo and special mission roles. In addition, new products and technologies could generate unanticipated safety or other concerns resulting in expanded product liability risks, potential product recalls and other regulatory issues that could have an adverse impact on us. Furthermore, because of the lengthy research and development cycle involved in bringing certain of our products to market, we cannot predict the economic conditions that will exist when any new product is complete, and the market for our product offerings does not always develop or continue to expand as we anticipate.

A reduction in capital spending in the aerospace or defense industries could have a significant effect on the demand for new products and technologies under development, which could have an adverse effect on our financial condition and results of operations. In addition, our investments in equipment or technology that we believe will enable us to obtain future contracts for our U.S. Government or other customers may not result in contracts or revenues sufficient to offset such investment. We cannot be sure that our competitors will not develop competing technologies which gain superior market acceptance compared to our

products. A significant failure in our new product development efforts, a substantial change to schedule, a material change in an anticipated market or the failure of our products or services to achieve customer acceptance relative to our competitors’ products or services, could have an adverse effect on our financial condition and results of operations.

We have made and may continue to make acquisitions that increase the risks of our business.

We enter into acquisitions with the intention of expanding our business and enhancing shareholder value. Acquisitions involve risks and uncertainties that, in some cases, have resulted, and, in the future, could result in our not achieving expected benefits. Such risks include difficulties in integrating newly acquired businesses and operations in an efficient and cost-effective manner; challenges in achieving expected strategic objectives, cost savings and other benefits; the risk that the acquired businesses’ markets do not evolve as anticipated and that the acquired businesses’ products and technologies do not prove to be those needed to be successful in those markets; the risk that our due diligence reviews of the acquired business do not identify or adequately assess all of the material issues which impact valuation of the business or result in costs or liabilities in excess of what we anticipated; the risk that we pay a purchase price that exceeds what the future results of operations would have merited; the risk that the acquired business may have significant internal control deficiencies or exposure to regulatory sanctions; and the potential loss of key customers, suppliers and employees of the acquired businesses.

Business and Operational Risks

Risks arising from uncertainty in global macroeconomic conditions may harm our business.

We are sensitive to global macroeconomic conditions. Negative macroeconomic factors may have an adverse effect on our business, results of operations and financial condition, as well as on our distributors, customers, subcontractors and suppliers, and on activity in many of the industries and markets we serve. We cannot predict changes in worldwide or regional economic or political conditions and government policies as such factors are highly volatile and beyond our control. If current macroeconomic pressures, including from inflation and labor and supply chain challenges, continue or if global macroeconomic conditions deteriorate and remain at depressed levels for extended periods, our business, results of operations and financial condition could be materially adversely affected. In addition, changes in laws or policies governing the terms of foreign trade, and in particular increased trade restrictions, tariffs or taxes on imports from countries where we manufacture or sell our products or from where we import products or raw materials (either directly or through our suppliers) could adversely impact our competitive position, business operations and financial results.

Our business could be negatively impacted by cybersecurity threats and other disruptions.

Our information technology (IT) and related systems are critical to the efficient operation of our business and essential to our ability to perform day to day processes. We routinely face persistent security threats, including threats to our IT infrastructure and unlawful attempts to gain access to our confidential, classified or otherwise proprietary information via phishing/malware campaigns and other cyberattack methods, as well as threats to the physical security of our facilities and employees. The threats we face vary from those common to most industries, to attacks by more advanced and persistent, highly organized adversaries, including nation state actors, which target us for the national security information in our possession, for our role in developing advanced technology systems or with the goal of committing fraudulent activity. Our customers, suppliers and subcontractors are likewise targeted, and attack methods continue to evolve. Some cyberattacks depend on human error or manipulation, including phishing attacks or schemes that use social engineering or artificial intelligence to gain access to systems or carry out disbursement of funds or other frauds. Developments in artificial intelligence and machine learning provide threat actors with the capability to use more sophisticated means to attack our systems and may exacerbate cybersecurity risk.

While we have experienced cybersecurity attacks, such attacks have not resulted in a material information security breach and we have not suffered any material losses relating to such attacks. Due to the evolving nature of security threats, the possibility of future material incidents cannot be completely mitigated, and we may not always be successful in timely detecting, reporting or responding to cyber incidents. Future attacks or breaches of data security, whether of our systems, the systems of our customers, suppliers, subcontractors or other business partners, or the systems of our service providers or other third parties who may have access to our data for business purposes, could disrupt our operations, cause the loss of business information or compromise confidential information, exposing us to liability or regulatory action. Such an incident also could require significant management attention and resources, increase costs that may not be covered by insurance, and result in reputational damage, potentially adversely affecting our competitiveness and our results of operations. Products and services that we provide to our customers may themselves be subject to cyberthreats which may not be detected or effectively mitigated, resulting in potential losses that could adversely affect us and our customers. In addition, our customers, including the U.S. Government, are increasingly requiring cybersecurity protections and mandating cybersecurity standards in our products, and we may incur additional costs to comply with such demands. For information on our cybersecurity governance, risk management and strategy, see Item 1C. Cybersecurity.

Challenges faced by our subcontractors or suppliers could materially and adversely affect our performance.

We rely on other companies to provide raw materials, major components and subsystems for our products. Subcontractors also perform services that we provide to our customers in certain circumstances. We depend on these suppliers and subcontractors to meet our contractual obligations to our customers and conduct our operations. Our ability to meet our obligations to our customers could be adversely affected if suppliers or subcontractors do not provide the agreed-upon supplies or perform the agreed-upon services in compliance with customer requirements and in a timely and cost-effective manner. Likewise, the quality of our products could be adversely impacted if companies to whom we delegate manufacture of major components or subsystems for our products, or from whom we acquire such items, do not provide components or subsystems which meet required specifications and perform to our and our customers’ expectations. Our businesses are experiencing and may continue to experience manufacturing inefficiencies and production delays as a result of shortages and delays of critical components for our products and other issues related to our direct or indirect suppliers. Suppliers may be unable to quickly recover from natural disasters, acts of war, and other events beyond their control and may be subject to additional risks such as material or labor shortages, inflationary conditions or other financial problems that limit their ability to conduct their operations, resulting in their inability to perform as anticipated. As a result, we have experienced, and may continue to experience, cost increases for certain materials and components which, along with increased energy and shipping costs and other inflationary pressures, have negatively impacted, and may continue to negatively impact, our profitability. The risk of these adverse effects would likely be greater in circumstances where we rely on only one or two subcontractors or suppliers for a particular raw material, product or service. In particular, in the aircraft industry, most vendor parts are certified by the regulatory agencies as part of the overall Type Certificate for the aircraft being produced by the manufacturer. If a vendor does not or cannot supply its parts, then the manufacturer’s production line may be stopped until the manufacturer can design, manufacture and certify a similar part itself or identify and certify another similar vendor’s part, resulting in significant delays in the completion of aircraft. Such events may adversely affect our financial results, damage our reputation and relationships with our customers, and result in regulatory actions and/or litigation.

We are subject to risks of doing business globally that could adversely impact our business.

During 2024, we derived approximately 29% of our revenues from international business, including U.S. exports. Conducting business internationally exposes us to additional risks than if we conducted our business solely within the U.S. We maintain manufacturing facilities, service centers, supply centers and other facilities worldwide, including in various emerging market countries. Risks related to international operations include import, export, economic sanctions and other trade restrictions; changing U.S. and foreign procurement policies and practices; changes in international trade policies, including higher tariffs on imported goods and materials and renegotiation of free trade agreements; potential retaliatory tariffs imposed by foreign countries against U.S. goods; impacts on our non-U.S. suppliers and customers due to acts of war or terrorism occurring internationally; restrictions on technology transfer; difficulties in protecting intellectual property; increasing complexity of employment and environmental, health and safety regulations; foreign investment laws; exchange controls; repatriation of earnings or cash settlement challenges; compliance with increasingly rigorous data privacy and protection laws; competition from foreign and multinational firms with home country advantages; economic and government instability; acts of industrial espionage, acts of war and terrorism and related safety concerns. The impact of any one or more of these or other factors could adversely affect our business, financial condition or operating results.

Additionally, some international government customers require contractors to agree to specific in-country purchases, technology transfers, manufacturing agreements or financial support arrangements, known as offsets, as a condition for a contract award. These contracts generally extend over several years and may include penalties if we fail to perform in accordance with the offset requirements which are often subjective. We also are exposed to risks associated with using foreign representatives and consultants for international sales and operations and teaming with international subcontractors and suppliers in connection with international programs. In many foreign countries, particularly in those with developing economies, it is common to engage in business practices that are prohibited by laws and regulations applicable to us, such as the Foreign Corrupt Practices Act. Although we maintain policies and procedures designed to facilitate compliance with these laws, a violation of such laws by any of our international representatives, consultants, joint ventures, business partners, subcontractors or suppliers, even if prohibited by our policies, could have an adverse effect on our business and reputation.

Natural disasters or other events outside of our control have disrupted and may in the future disrupt our operations, adversely affect our results of operations and financial condition, and may not be fully covered by insurance.

Natural disasters, including hurricanes, fires, tornados, floods and other forms of severe weather, the intensity and frequency of which are being exacerbated by climate change, along with other impacts of climate change, such as rising sea waters, as well as other events outside of our control including public health crises, pandemics, power outages and industrial accidents, have in the past and could in the future disrupt our operations and adversely affect our business. Any of these events could result in physical damage to and/or complete or partial closure of one or more of our facilities and temporary or long-term disruption of our operations or the operations of our suppliers by causing business interruptions or by impacting the availability and cost of materials needed for manufacturing or otherwise impacting our ability to deliver products and services to our customers. Existing insurance arrangements may not provide full protection for the costs that may arise from such events. The occurrence of any of

these events could materially increase our costs and expenses and have a material adverse effect on our business, financial condition and results of operations.

Financial Risks

If our Finance segment has difficulty collecting on its finance receivables, our financial performance could be adversely affected.

The financial performance of our Finance segment depends on the quality of loans, leases and other assets in its portfolio. Portfolio quality can be adversely affected by several factors, including finance receivable underwriting procedures, collateral value, geographic or industry concentrations, and the effect of general economic conditions. In addition, a substantial number of the originations in our finance receivable portfolio are cross-border transactions for aircraft sold outside of the U.S. Cross-border transactions present additional challenges and risks in the event of borrower default, which can result in difficulty or delay in collecting on the related finance receivables. If our Finance segment has difficulty successfully collecting on its finance receivable portfolio, our cash flow, results of operations and financial condition could be adversely affected.

We periodically need to obtain financing and such financing may not be available to us on satisfactory terms, if at all.

We periodically need to obtain financing in order to meet our debt obligations as they come due, to support our operations and/or to make acquisitions. Our access to the debt capital markets and the cost of borrowings are affected by a number of factors including market conditions and the strength of our credit ratings. If we cannot obtain adequate sources of credit on favorable terms, or at all, our business, operating results, and financial condition could be adversely affected.

Unanticipated changes in our tax rates or exposure to additional income tax liabilities could affect our profitability.

We are subject to income taxes in the U.S. and various non-U.S. jurisdictions, and our domestic and international tax liabilities are subject to the location of income among these different jurisdictions. Our effective tax rate could be adversely affected by changes in the mix of earnings in countries with differing statutory tax rates, changes in the valuation of deferred tax assets and liabilities, changes in the amount of earnings indefinitely reinvested offshore, changes to unrecognized tax benefits or changes in tax laws, which could affect our profitability. In particular, the carrying value of deferred tax assets is dependent on our ability to generate future taxable income, as well as changes to applicable statutory tax rates. In addition, the amount of income taxes we pay is subject to audits in various jurisdictions, and a material assessment by a tax authority could affect our profitability.

Risks Related to Regulatory, Legal and Other Matters

We are subject to increasing compliance risks that could adversely affect our operating results.

As a global business, we are subject to laws and regulations in the U.S. and other countries in which we operate. International sales and global operations require importing and exporting goods, software and technology, some of which have military applications subjecting them to more stringent import-export controls across international borders on a regular basis. For example, we sometimes initially must obtain licenses and authorizations from various U.S. Government agencies before we are permitted to sell certain of our aerospace and defense products outside the U.S., and we are not always successful in obtaining these licenses or authorizations in a timely manner. Both U.S. and foreign laws and regulations applicable to us have been increasing in scope and complexity. For example, both U.S. and foreign governments and government agencies regulate the aviation industry, and they have previously and may in the future impose new regulations for additional aircraft security or other requirements or restrictions. New or changing laws and regulations or related interpretation and policies could increase our costs of doing business, affect how we conduct our operations, adversely impact demand for our products, and/or limit our ability to sell our products and services. Compliance with laws and regulations of increasing scope and complexity is even more challenging in our business environment in which reducing our operating costs is often necessary to remain competitive. In addition, a violation of U.S. and/or foreign laws by one of our employees or business partners could subject us or our employees to civil or criminal penalties, including material monetary fines, or other adverse actions, such as denial of import or export privileges and/or debarment as a government contractor which could damage our reputation and have an adverse effect on our business.

Certain of our products are subject to laws regulating consumer products and could be subject to repurchase or recall as a result of safety issues.

As a distributor of consumer products in the U.S., certain of our products are subject to the Consumer Product Safety Act, which empowers the U.S. Consumer Product Safety Commission (CPSC) to exclude from the market products that are found to be unsafe or hazardous. Under certain circumstances, the CPSC has in the past and could require in the future us to repair, replace or refund the purchase price of one or more of our products, or potentially even discontinue entire product lines. We also may voluntarily take such action and, from time to time, have done so, but within strictures recommended by the CPSC. The CPSC also can impose fines or penalties on a manufacturer for non-compliance with its requirements. Furthermore, failure to timely notify the CPSC of a potential safety hazard can result in significant fines being assessed against us. Any repurchases or recalls of our products or an imposition of fines or penalties could be costly to us and could damage the reputation or the value of our brands. Additionally, laws regulating certain consumer products exist in some states, as well as in other countries in which we sell our products, and more restrictive laws and regulations could be adopted in the future.

Increased regulation and stakeholder expectations related to global climate change could negatively affect our operating results.

Increased worldwide public awareness and concern regarding global climate change has resulted and is likely to continue to result in more legislative and regulatory efforts, in the U.S., the European Union and in other jurisdictions in which we operate, in an effort to address the negative impacts of climate change. Recently enacted laws and regulations include, and future such laws and regulations may include, more prescriptive required reporting on environmental metrics, climate change related risks and associated financial and other impacts, as well as increased oversight of and reporting on our supply chain and other compliance requirements. We expect that compliance with such laws and regulations will require additional internal and external resources. Stricter limits on greenhouse gas emissions generated by our facilities or by our products that produce carbon emissions, carbon pricing mechanisms and/or energy taxes could also be imposed. Compliance with stricter limits may necessitate larger investment in product development and manufacturing equipment and/or facilities, as well as sourcing from new suppliers and/or higher costs from existing suppliers. These increased regulatory requirements are expected to increase our direct and indirect costs and could negatively impact our business, results of operations, financial condition and competitive position. Our failure to adequately comply with such laws and regulations could jeopardize our ability to receive contract awards from the U.S. government and other customers.

Moreover, our investors, customers, employees and other stakeholders increasingly expect us to reduce greenhouse gas emissions generated by our operations by implementing more efficient manufacturing technologies and increasing the amount of renewable energy used within our facilities. While we are engaged in efforts to transition to a lower carbon economy by reducing the emissions generated by our operations and increasing our use of renewable energy, these efforts take time and resources and may increase our energy acquisition and other costs and require capital investment. In addition, our stakeholders expect us to reduce greenhouse gas emissions from the use of our products, including by developing and incorporating sustainable technologies into our products. We expect that most of our businesses will require significant research and development investment to succeed in developing the new technologies and products that will enable us to significantly reduce such emissions from the use of our products and successfully compete in a lower carbon economy. We may not realize the anticipated benefits of our investments and actions for a variety of reasons, including technological challenges, evolving government and customer requirements and our ability to anticipate them and develop the desired technologies and products on a timely basis. Our competitors may develop these technologies and products before we do and they may be deemed by our customers to be superior to technologies and products we may develop, and they may otherwise gain industry acceptance in advance of, or instead of, our products. In addition, as we and our competitors develop increasingly sustainable technologies, demand for our existing offerings may decrease or become nonexistent.

We are subject to legal proceedings and other claims.

We are subject to legal proceedings and other claims arising out of the conduct of our business, including proceedings and claims relating to commercial and financial transactions; government contracts; alleged lack of compliance with applicable laws and regulations; disputes with suppliers, production partners or other third parties; product liability; patent and trademark infringement; employment disputes; and environmental, safety and health matters. Due to the nature of our manufacturing business, we are regularly subject to liability claims arising from accidents involving our products, including claims for serious personal injuries or death caused by weather or by pilot, driver or user error. In the case of litigation matters for which reserves have not been established because the loss is not deemed probable, it is reasonably possible that such claims could be decided against us and could require us to pay damages or make other expenditures in amounts that are not presently estimable. In addition, we cannot be certain that our reserves are adequate and that our insurance coverage will be sufficient to cover one or more substantial claims. Furthermore, we may not be able to obtain insurance coverage at acceptable levels and costs in the future. Litigation is inherently unpredictable, and we could incur judgments, receive adverse arbitration awards or enter into settlements for current or future claims that could adversely affect our results of operations in any particular period.

Intellectual property infringement claims of others and the inability to protect our intellectual property rights could harm our business and our customers.