UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-K |

☑ ANNUAL REPORT Pursuant to Section 13 or 15(d) |

OF the Securities Exchange Act of 1934 |

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended June 30, 2024 | Commission File Number 001-07233 |

STANDEX INTERNATIONAL CORPORATION |

(Exact name of registrant as specified in its Charter) |

Delaware | 31-0596149 |

(State of incorporation) | (I.R.S. Employer Identification No.) |

23 KEEWAYDIN DRIVE, Salem, New Hampshire | 03079 |

(Address of principal executive offices) | (Zip Code) |

(603) 893-9701 |

(Registrant’s telephone number, including area code) |

SECURITIES REGISTERED PURSUANT TO SECTION 12(b) OF THE SECURITIES EXCHANGE ACT OF 1934: |

Title of Each Class | Trading Symbol(s) | Name of Each Exchange on Which Registered |

Common Stock, Par Value $1.50 Per Share | SXI | New York Stock Exchange |

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein and will not be contained, to the best of Registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ☒ | Accelerated filer ☐ | Non-accelerated filer ☐ | Smaller Reporting Company ☐ |

| | | | Emerging growth company ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 USC. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. YES ☒ NO ☐

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). YES ☐ NO ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to § 240.10D-1(b). ☐

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the Registrant at the close of business on December 31, 2023 was approximately $1,855,686,511. Registrant’s closing price as reported on the New York Stock Exchange for December 31, 2023 was $158.38 per share.

The number of shares of Registrant's Common Stock outstanding on July 31, 2024 was 11,854,539.

Documents incorporated by reference

Portions of the Proxy Statement for the Registrant’s 2024 Annual Meeting of Stockholders (the “Proxy Statement”) are incorporated by reference into Part III of this report.

Forward Looking Statement

Statements contained in this Annual Report on Form 10-K that are not based on historical facts are “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements may be identified by the use of forward-looking terminology such as “should,” “could,” “may,” “will,” “expect,” “believe,” “estimate,” “anticipate,” “intend,” “continue,” or similar terms or variations of those terms or the negative of those terms. There are many factors that affect the Company’s business and the results of its operations and that may cause the actual results of operations in future periods to differ materially from those currently expected or anticipated. These factors include, but are not limited to: the impact of pandemics and other global crises or catastrophic events on employees, our supply chain, and the demand for our products and services around the world; materially adverse or unanticipated legal judgments, fines, penalties or settlements; conditions in the financial and banking markets, including fluctuations in exchange rates and the inability to repatriate foreign cash; domestic and international economic conditions, including the impact, length and degree of economic downturns on the customers and markets we serve and more specifically conditions in the automotive, construction, aerospace, defense, transportation, food service equipment, consumer appliance, energy, oil and gas and general industrial markets; lower-cost competition; the relative mix of products which impact margins and operating efficiencies in certain of our businesses; the impact of higher raw material and component costs, particularly steel, certain materials used in electronics parts, petroleum based products, and refrigeration components; the impact of higher transportation and logistics costs, especially with respect to transportation of goods from Asia; an inability to realize the expected cost savings from restructuring activities including effective completion of plant consolidations, cost reduction efforts including procurement savings and productivity enhancements, capital management improvements, strategic capital expenditures, and the implementation of lean enterprise manufacturing techniques; the potential for losses associated with the exit from or divestiture of businesses that are no longer strategic or no longer meet our growth and return expectations; the inability to achieve the savings expected from global sourcing of raw materials and diversification efforts in emerging markets; the impact on cost structure and on economic conditions as a result of actual and threatened increases in trade tariffs; the inability to attain expected benefits from acquisitions and the inability to effectively consummate and integrate such acquisitions and achieve synergies envisioned by the Company; market acceptance of our products; our ability to design, introduce and sell new products and related product components; the ability to redesign certain of our products to continue meeting evolving regulatory requirements; the impact of delays initiated by our customers; and our ability to increase manufacturing production to meet demand; the impact on our operations of any successful cybersecurity attacks; and potential changes to future pension funding requirements. In addition, any forward-looking statements represent management's estimates only as of the day made and should not be relied upon as representing management's estimates as of any subsequent date. While the Company may elect to update forward-looking statements at some point in the future, the Company and management specifically disclaim any obligation to do so, even if management's estimates change.

PART I

Item 1. Business

Standex International Corporation and subsidiaries ("we," "us," "our," the "Company" and "Standex" is a diversified industrial manufacturer with leading positions in a variety of products and services that are used in diverse commercial and industrial markets. Headquartered in Salem, New Hampshire, we have six operating segments aggregated into five reportable segments: Electronics, Engraving, Scientific, Engineering Technologies, and Specialty Solutions. Two operating segments are aggregated into Specialty Solutions. Our businesses work in close partnership with our customers to deliver custom solutions or engineered components that solve their unique and specific needs, an approach we call "Customer Intimacy."

Standex was incorporated in 1975 and is the successor of a corporation organized in 1955. We have paid dividends each quarter since Standex became a public corporation in November 1964. Overall management, strategic development and financial control are led by the executive staff at our corporate headquarters. Our growth strategy is focused on four key areas: (1) Increasing our presence in rapidly growing markets and applications (2) executing new product development in both core and adjacent market applications; (3) expanding geographically where meaningful business opportunities exist; and (4) undertaking strategically aligned acquisitions that strengthen and/or expand these core businesses. We direct our investments towards markets with long term, secular growth prospects such as renewable energy, electric vehicles, smart power grid, military and defense and life sciences.

Unless otherwise noted, references to years are to fiscal years. Currently our fiscal year end is June 30. Our fiscal year 2024 includes the twelve-month period from July 1, 2023 to June 30, 2024.

Our long-term business strategy is to create, improve, and enhance shareholder value by building more profitable, focused industrial platforms through our Standex Value Creation System. This methodology employs four components: Balanced Performance Plan, Growth Disciplines, Operational Excellence, and Talent Management and provides both a company-wide framework and tools used to achieve our goals. We intend to continue investing organically and inorganically in high margin and growth businesses using this balanced and proven approach.

It is our objective to grow larger and more profitable business units through both organic and inorganic initiatives. We have a particular focus on identifying and investing in opportunities that complement our products and will increase the overall scale, global presence and capabilities of our businesses. We continue to execute on acquisitions where strategically aligned with our businesses and where the opportunity meets our investment metrics. We have divested, and likely will continue to divest, businesses that we feel are not strategic or do not meet our growth and return expectations.

The Company’s strong historical cash flow has been a cornerstone for funding our capital allocation strategy. We use cash flow generated from operations to fund investments in capital assets to upgrade our facilities, improve productivity and lower costs, invest in the strategic growth programs described above, including organic and inorganic growth, and to return cash to our shareholders through payment of dividends and stock buybacks.

Please visit our website at www.standex.com to learn more about us or to review our most recent SEC filings. The information on our website is for informational purposes only and is not incorporated into this Annual Report on Form 10-K.

Description of Segments

Electronics

Our Electronics group is a global component and value-added solutions provider of both sensing and switching technologies as well as magnetic power conversion components and assemblies. Electronics competes on the basis of Customer Intimacy by designing, engineering, and manufacturing innovative solutions, components and assemblies to solve our customers’ application needs through our Partner/Solve/Deliver® approach. Our approach allows us to expand the business through organic growth with current customers as well as developing new products, driving geographic expansion, and pursuing inorganic growth through strategic acquisitions.

Components are manufactured in plants located in the U.S., Mexico, the U.K., Germany, Japan, China and India.

Markets and Applications

Our highly engineered products and vertically integrated manufacturing capabilities provide solutions to an array of markets and provide safe and efficient power transformation, current monitoring, and isolation, as well as switch, sensor and relay solutions to monitor systems for function and safety. The end-user of our engineered solution is typically an original equipment manufacturer (“OEM”) or industrial equipment manufacturer. End-user markets include, but are not limited to, appliances, electrification (electric vehicles, solar, smart-grid, alternative energy), security, military, medical, aerospace, test and measurement, power distribution, transportation, and general industrial applications.

Brands

Business unit names are Standex Electronics, Standex-Meder Electronics, Renco Electronics, Northlake Engineering, Agile Magnetics, Sensor Solutions, Standex Electronics Japan, Minntronix and Sanyu. Other associated brand names include the MEDER, KENT, and KOFU reed switch brands.

Products and Services

Our sensing products employ reed switch, Hall effect, inductive, conductive and other technologies. Sensing based solutions include reed relays, fluid level, proximity, motion, flow, HVAC condensate as well as custom electronic sensors containing our core technologies. The magnetics or power conversion products include custom wound transformers and inductors for low and high frequency applications, current sense technology, advanced planar transformer technology, value added assemblies, and mechanical packaging.

Customers

The business sells globally to a wide variety of mainly OEM customers focused in the end markets noted previously through a direct sales force, regional sales managers, field applications engineers, commissioned agents, representative groups, and distribution channels.

Engraving

Our Engraving group is a global creator and provider of custom textures and surface finishes on tooling that enhance the beauty and function of a wide range of consumer good and automotive products. We focus on continuing to meet the needs of a changing marketplace by offering experienced craftsmanship while investing in new technologies such as laser engraving and soft surface skin texturized tooling. Our growth strategy is to continue to develop and/or acquire technologies to enhance surface textures that also allow our customers to introduce more sustainable manufacturing processes and reduce their own energy consumption. We are one company operating in 18 countries using a consistent approach to guarantee harmony on global programs in service of our customers.

Markets and Applications

Standex Engraving Mold Tech has become the global leader in its industry by offering a full range of services to OEM’s, Tier 1 suppliers, mold makers and product designers. From start to finish, these services include the design of bespoke textures, the verification of the texture on a prototype, engraving a mold, enhancing and polishing it, and then offering on-site try-out support with ongoing tool maintenance and texture repair capabilities. In addition to these services, we also produce soft trim tooling such as in mold graining (IMG) and nickel shells.

Brands

In addition to the Mold Tech brand, Engraving companies and brands also include:

| | ● | Piazza Rosa and World Client Services (WCS), which both offer laser engraving and tool finishing in Europe and Mexico. |

| | ● | Tenibac-Graphion, which provides additional texturizing and prototyping capabilities in North America and China. |

| | ● | GS Engineering, which employs advanced processes and technology to rapidly produce molds for the creation of soft-touch surfaces. |

| | ● | Innovent, which is a specialized supplier of tools and machines used to produce diapers and products that contain absorbent materials between layers of non-woven fabric. |

Products and Services

Texturing is achieved with either a laser or a chemical etching technique.

| | ● | Laser Engraving offers superior features, such as multiple gloss levels, the elimination of paint and optimized scratch performance, and sharp definition for precise geometric patterns. |

| | ● | Chemical Engraving produces carefully designed textures and finishes without seams or distortion. Our Digital Transfer Technology offers an exclusive service which guarantees consistency, pattern integrity and texture harmony around the world. |

Architexture Design Studio uses proprietary technology called Model-Tech® which utilizes proven expertise to create and test custom textures. During the Model-Tech process, an original texture is first designed to offer beauty and function, which ultimately is used to create a large-format skin that can be wrapped on a model for testing.

Tooling Performance services include the enhancement, finishing and repair of a tool to improve its use during manufacturing.

| | ● | Tool Enhancement services increase the wear resistance of the mold. Processes include advanced tool finishing services, anti-scratch, laser hardening in localized areas, Tribocoat® and Release Coat. |

| | ● | Tool Finishing and Repair allows customers to achieve outstanding quality while saving valuable time. These services include laser micro-welding, polishing and lapping, laser cladding to accommodate engineering changes, mold assembly, tool management, maintenance, texture repair and on-site support. |

Soft Trim Tooling and nickel shell molds are used to produce soft surfaces that emulate the feel of natural materials. The IMG process we support consumes significantly less energy in our customers' operations than the traditional slush molding process.

Customers

The Engraving business has become the global leader providing these products and services by offering a full range of services to automotive OEM’s, product designers, Tier 1 suppliers, and toolmakers all around the world.

Scientific

Our Scientific business specializes in providing specialty temperature-controlled equipment for the medical, scientific, pharmaceutical, biotech, and industrial markets. We design and produce these products in Summerville, SC, ensuring high quality and reliability

We offer a range of products in our portfolio that control the temperatures of critical healthcare products, medications, vaccines, and laboratory samples. Our focus is on solving customer problems for these critical applications, delivering innovative products and solutions that meet stringent regulatory requirements and the unique needs of our customers.

Markets and Applications

The scientific and healthcare equipment that we design, assemble and manufacture is used in hospitals, pharmacies, clinical laboratories, reference laboratories, physicians’ offices, life science laboratories, government and academic facilities, and industrial testing laboratories. Our product offerings include:

| | ● | Laboratory and medical grade refrigerators, freezers and accessories, |

| | ● | Cryogenic storage tanks and accessories, |

| | ● | Blood bank refrigerators and plasma freezers, |

| | ● | Ultra low temperature freezers, and |

| | ● | Environmental stability chambers and incubators. |

Brands

Our products are sold under various brands including American BioTech Supply (ABS), Lab Research Products (LRP),Corepoint, Cryosafe and CryoGuard.

Products and Services

We manufacture and provide specialty-controlled temperature equipment purpose-built for the medical, scientific, pharmaceutical, biotech and industrial markets. Our comprehensive portfolio includes a range of innovative storage solutions for medications, vaccines, blood products, patient samples, biologics and laboratory samples.

Customers

Scientific products are sold to medical and laboratory distributors, healthcare facilities, research universities, pharmaceutical and biotech companies, pharmacies and industrial facilities.

Engineering Technologies

Our Engineering Technologies Group (ETG) is a provider of innovative, metal-formed solutions for OEM and Tier 1 manufacturers for use in their advanced engineering designs.

Our solutions seek to address unique customer design challenges such as reduction of input weight, material cost, part count, and complexity involving all formable materials with particular focus on large dimensions, large thickness or thin-wall construction, complex shapes and contours, and/or single-piece construction requirements. Engineering Technologies devises and manufactures these cost-effective components and assemblies by combining a portfolio of best-in-class forming technologies and technical experience, vertically integrated manufacturing processes, and group wide technical and design expertise.

We intend to grow sales and product offerings by investing in advancements in our current and new technologies and identifying new cutting-edge solutions for these capabilities in existing and adjacent markets via customer and research collaboration.

Our segment is comprised of our Spincraft businesses with locations in Billerica, MA, New Berlin, WI, and Newcastle upon Tyne in the U.K.

Markets and Applications

Spincraft products serve applications within the space, aviation, defense, energy, medical, and general industrial markets.

| | ● | The space market we serve is comprised of components and assemblies for space launch vehicles, engines, crewed and uncrewed spacecraft and other space infrastructure. |

| | ● | The aviation market offerings include a large portfolio of components and assemblies for commercial and private aircraft engines, nacelles and fuel systems. |

| | ● | The defense market we serve covers a wide spectrum of applications including components for missiles, naval propulsion and structures, large dimension exhaust systems and military aircraft engine solutions. |

| | ● | Applications within the energy market include components and assemblies for new and MRO gas turbines, as well as solutions for oil & gas exploration operations. |

Brands

This group's brand name is Spincraft.

Products and Services

| | ● | Space: Fuel tanks and fuel tank domes, rocket engine components, crew vehicle and unmanned spacecraft structures and bulkheads |

| | ● | Aviation: Nacelle inlet lipskins & ducts, engine components and fuel tank elements |

| | ● | Defense: Missile nose cones & structures, naval propulsion components and structures, exhaust assemblies, and military aircraft engine & exhaust components |

| | ● | Energy: Power generation turbine & other assemblies, oil & gas exploration connection components |

Customers

Engineering Technologies components are sold directly to large space, aviation, defense, energy and medical companies, or suppliers to those companies.

Specialty Solutions

Specialty Solutions is comprised of two businesses: Federal Industries and Custom Hoists. These businesses differentiate themselves in their respective markets by collaborating with customers to develop and deliver custom solutions.

Federal Industries provides merchandising solutions to retail and food service customers whose revenue stream is enhanced through food presentation. Federal Industries focuses on the challenges of enabling retail and food service establishments to provide food and beverages that are fresh and appealing while at the same time providing for food safety, and energy efficiency. Our key differentiator is the ability to customize products to meet customers' needs within industry standard lead-times. This differentiator is used to target the convenience store, school cafeterias and quick-service restaurant segments.

Custom Hoists is a supplier of engineered hydraulic cylinders that meet customer specific requirements for demanding applications. Our engineering expertise coupled with broad manufacturing capabilities and responsiveness to customer needs drives our top line growth opportunities. We leverage our full line of products for the construction markets in dump truck and trailer applications and deep expertise in the refuse market to expand into new adjacent markets, targeting the most challenging custom applications. Flexible design capability, a global supply chain and speed to market enable us to be successful in growing our business. Our team is dedicated to superior customer service through our technical engineering support and on-time delivery.

Specialty Solutions products are designed and/or manufactured in Hayesville, OH; Belleville, WI; and Tianjin, China.

Markets and Applications

Federal Industries custom designs and manufactures refrigerated, heated and dry merchandising display cases for bakery, deli, confectionary and packaged food products utilized in restaurants, convenience stores, quick-service restaurants, supermarkets, drug stores and institutions such as hotels, hospitals, and school cafeterias.

Custom Hoist products are utilized by OEMs on vehicles such as dump trucks, dump trailers, bottom dumps, garbage trucks (both recycling and rear loader), container roll off vehicles, hook lift trucks, liquid waste handlers, vacuum trucks, compactors, balers, airport catering vehicles, container handling equipment for airlines, lift trucks, yard tractors, and underground mining vehicles.

Brands

Federal Industries products are sold under the Federal brand.

Custom Hoists products are sold under the Custom Hoist brand.

Products and Services

Federal Industries offers a selection of display cases, including innovative customization, for fresh food merchandising requirements.

Custom Hoists designs and manufactures single and double acting telescopic and piston rod hydraulic cylinders for original and aftermarket use in construction equipment, refuse, airline support, mining, oil and gas, and other material handling applications.

Customers

Specialty Solutions products are sold to OEMs, distributors, service organizations, aftermarket repair outlets, end-users, dealers, buying groups, consultants, government agencies and manufacturers.

The following provides a description of key areas impacting our Company.

Working Capital

Our primary source of working capital is the cash generated from continuing operations. No segments require any special working capital needs outside of the normal course of business.

Competition

Standex manufactures and markets products many of which have achieved a unique or leadership position in their market, however, we encounter competition in varying degrees in all product groups and for each product line. Competitors include domestic and foreign producers of the same and similar products. The principal methods of competition are industry and design expertise, product performance and technology, price, delivery schedule, quality of services, and other terms and conditions. Standex competes on the basis of Customer Intimacy in which our teams work as extensions of our customers organizations to apply our expertise and technology to address needs with customer solutions.

International Operations

International operations are conducted at 42 locations, including Europe, Canada, China, Japan, India, Southeast Asia, Korea and Mexico. See the Notes to Consolidated Financial Statements for international operations financial data. Our net sales from continuing international operations decreased slightly from 39% in fiscal year 2023 to 38% in fiscal year 2024. International operations are subject to certain inherent risks in connection with the conduct of business in foreign countries including, exchange controls, price controls, limitations on participation in local enterprises, nationalizations, expropriation and other governmental action, restrictions of repatriation of earnings, and changes in currency exchange rates.

Research and Development

We develop and design new products to meet customer needs in order to offer enhanced products or to provide customized solutions for customers. Developing new and improved products, broadening the application of established products, and continuing efforts to improve our methods, processes, and equipment continues to drive our success. Research and development costs are quantified in the Notes to Consolidated Financial Statements.

Environmental Matters

Based on our knowledge and current known facts, we believe that we are presently in substantial compliance with all existing applicable environmental laws and regulations and do not anticipate (i) any instances of non-compliance that will have a material effect on our future capital expenditures, earnings or competitive position or (ii) any material capital expenditures for environmental control facilities.

Financial Information about Geographic Areas

Information regarding revenues from external customers attributed to the United States, all foreign countries and any individual foreign country, if material, is contained in the Notes to Consolidated Financial Statements, “Revenue from Contracts with Customers.”

Human Capital Resources

Standex International understands that its rich history of success and future opportunities are directly linked to its dedicated, engaged, and diverse workforce. As of June 30, 2024, we employ approximately 3,700 employees of which approximately 1,100 are in the United States. About 200 of our U.S. employees are represented by unions. Our competitive wages and benefits align with those of other manufacturers in our geographic locations. We prioritize open, two-way communication and foster strong relationships with both our non-union employees and the various unions and works councils within our business segments. Regular training programs tailored to employees’ roles and optional development opportunities are available for those seeking personal and professional growth. Our global Standex Safety Council, which includes representatives from all Standex sites, meets regularly to enhance our safety culture and monitor our Total Recordable Incident Rate.

The Chief Human Resources Officer frequently collaborates with the Chief Executive Officer to align Human Capital strategies and initiatives with our business goals. We aim to provide a rewarding employee experience across the company by continuously reviewing our Human Capital Resources metrics, such as safety metrics, turnover rates, and culture survey responses. These reviews help us promote a safe, inclusive, and engaging work environment. Our LEAP performance management and development process emphasizes both manager engagement and employee ownership. We conduct regular employee engagement and satisfaction surveys, including our annual Culture Survey. Insights from these surveys drive senior management’s efforts to continually improve our company culture and operations.

In fiscal year 2025, we will implement a Human Capital Management System to further support our commitment to our workforce. This system will enhance our ability to manage and develop our talent, streamline operations enhance employee development and satisfaction ensuring that we continue to provide a rewarding and supportive environment for all employees.

Standex hosts an annual meeting event in the first quarter of the fiscal year with the extended global leadership team, representative of all our business segments and corporate functions, in which participants join together to align on business and culture goals, participate in leadership development training, share best practices and build unity across the company.

The Inclusion Advisory Council (IAC) serves as a collaborative platform for employee voices, informing and aligning the company’s commitment to inclusivity. The IAC provides operational input to the Executive Leadership Team in three key areas: setting global inclusivity and diversity goals, collaborating with Corporate Communications to highlight the IAC’s work, and championing the implementation of IAC initiatives. Additionally, we launched the Women and Leadership Employee Resource Group in fiscal year 2023, aiming to increase the representation of women at all levels, enhancing the company’s success through relationships and partnerships. Work continues to add additional ERGs in partnership with the IAC.

Executive Officers of Standex

The executive officers of the Company as of June 30, 2024 are as follows:

Name | Age | Principal Occupation During the Past Five Years |

| | | |

David Dunbar | 62 | President and Chief Executive Officer of the Company since January 2014. |

| | | |

Ademir Sarcevic | 49 | Vice President and Chief Financial Officer of the Company since September 2019. Various positions over the years at Pentair plc from 2012 to September 2019 with increasing responsibility ending as Senior Vice President and Chief Accounting Officer. |

| | | |

Alan J. Glass | 60 | Vice President, Chief Legal Officer and Secretary of the Company since April 2016. |

| | | |

| Annemarie Bell | 52 | Vice President, Chief Human Resources Officer since July 2021, Vice President of Human Resources from June 2019 to July 2021, Interim Vice President of Human Resources from October 2018 through June 2019; Vice President of Human Resources for four of Standex business units from October 2015 through October 2018. |

| | | |

| Max Arets | 51 | Vice President, Chief Information Officer since April 2024. Various positions of increasing responsibility in IT Audit, finance systems, project management and information systems and with Tyco International and Pentair from 2005 to March 2024 ending as Vice President, Digital Enterprise. |

| | | |

| Amy Gagnon | 45 | Vice President, Chief Accounting Officer of the Company since January 2024. Corporate Controller from September 2021 to January 2024 and Assistant Controller from March 2020 to September 2021. Assistant Controller at Vapotherm, Inc. from 2018 until joining the Company in March 2020. |

The executive officers are elected each year at the first meeting of the Board of Directors subsequent to the annual meeting of stockholders, to serve for one-year terms of office. There are no family relationships among any of the directors or executive officers of the Company.

Long-Lived Assets

Long-lived assets are described and discussed in the Notes to Consolidated Financial Statements under the caption “Long-Lived Assets.”

Available Information

Standex’s corporate headquarters are at 23 Keewaydin Drive, Salem, New Hampshire 03079, and our telephone number at that location is (603) 893-9701.

The U.S. Securities and Exchange Commission (the “SEC”) maintains an internet website at www.sec.gov that contains our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and proxy statements, and all amendments thereto. Standex’s internet website address is www.standex.com. Our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and proxy statements, and all amendments thereto, are available free of charge on our website as soon as reasonably practicable after such reports are electronically filed with or furnished to the SEC. In addition, our code of business conduct, our code of ethics for senior financial management, our corporate governance guidelines, and the charters of each of the committees of our Board of Directors (which are not deemed filed by this reference), are available on our website and are available in print to any Standex shareholder, without charge, upon request in writing to “Chief Legal Officer, Standex International Corporation, 23 Keewaydin Drive, Salem, New Hampshire, 03079.”

Item 1A. Risk Factors

An investment in the Company involves various risks, including those mentioned below and those that are discussed from time to time in our other periodic filings with the Securities and Exchange Commission. Investors should carefully consider these risks, along with the other information filed in this report, before making an investment decision regarding the Company. Any of these risks could have a material adverse effect on our financial condition, results of operations and/or value of an investment in the Company.

A pandemic or other global health crisis could adversely affect our revenues, operating results, cash flow and financial condition.

Our business and operations, and the operations of our suppliers, business partners and customers, were adversely affected by the Coronavirus (or COVID-19) pandemic which is impacted worldwide economic activity including in many countries or localities in which we operate, sell, or purchase goods and services. Any future pandemics or other global health crises could similarly have an adverse effect on our revenues, operating results, cash flow and financial condition. The ultimate extent to which any such circumstance impacts our business will depend on the severity, location and duration of the issue, the actions undertaken in response by local and world governments and health officials, and the success of medical efforts to address and mitigate the threat.

A deterioration in the domestic and international economic environment, whether by way of inflationary conditions or recessionary conditions, could adversely affect our operating results, cash flow and financial condition.

Recent inflationary conditions in the United States, Europe and other parts of the world have increased virtually all of our costs including our cost of materials, labor and transportation. We attempt to maintain our profit margins by anticipating such inflationary pressures and increasing our prices where possible in accordance with contractual requirements and competitive conditions. While we thus far have been largely successful in mitigating the impact of such inflationary conditions, we may be unable to continue to increase our own prices sufficiently to offset cost increases, and, to the extent that we are able to do so, we may not be able to maintain existing operating margins and profitability. Additionally, competitors operating in regions with less inflationary pressure may be able to compete more effectively which could further impact our ability to increases prices and/or result in lost sales.

Recessionary economic conditions, with or without a tightening of credit, could adversely impact major markets served by our businesses, including cyclical markets such as automotive, aviation, energy and power, heavy construction vehicle, general industrial, consumer appliances and food service. An economic recession could adversely affect our business by:

| | • | reducing demand for our products and services, particularly in markets where demand for our products and services is cyclical; |

| | • | causing delays or cancellations of orders for our products or services; |

| | • | reducing capital spending by our customers; |

| | • | increasing price competition in our markets; |

| | • | increasing difficulty in collecting accounts receivable; |

| | • | increasing the risk of excess or obsolete inventories; |

| | • | increasing the risk of impairment to long-lived assets due to reduced use of manufacturing facilities; |

| | • | increasing the risk of supply interruptions that would be disruptive to our manufacturing processes; and |

| | • | reducing the availability of credit and spending power for our customers. |

We rely on our credit facility to provide us with sufficient capital to operate our businesses and to fund acquisitions.

We rely on our revolving credit facility, in part along with operating cash flow, to provide us with sufficient capital to operate our businesses and to fund acquisitions. The availability of borrowings under our revolving credit facility is dependent upon our compliance with the covenants set forth in the facility, including the maintenance of certain financial ratios. Our ability to comply with these covenants is dependent upon our future performance, which is subject to economic conditions in our markets along with factors that are beyond our control. Violation of those covenants could result in our lenders restricting or terminating our borrowing ability under our credit facility, cause us to be liable for covenant waiver fees or other obligations, or trigger an event of default under the terms of our credit facility, which could result in acceleration of the debt under the facility and require prepayment of the debt before its due date. Even if new financing is available, in the event of a default under our current credit facility, the interest rate charged on any new borrowing could be substantially higher than under the current credit facility, thus adversely affecting our overall financial condition. If our lenders reduce or terminate our access to amounts under our credit facility, we may not have sufficient capital to fund our working capital needs and/or acquisitions or we may need to secure additional capital or financing to fund our working capital requirements or to repay outstanding debt under our credit facility or to fund acquisitions.

Our credit facility contains covenants that restrict our activities.

Our revolving credit facility contains covenants that restrict our activities, including our ability to:

| | • | incur additional indebtedness; |

| | • | make investments, including acquisitions; |

| | • | pay cash dividends to shareholders unless we are compliant with the financial covenants set forth in the credit facility; and |

Our global operations subject us to international business risks.

We operate in 42 locations outside of the United States in Europe, Canada, China, Japan, India, Singapore, Korea, Mexico, Turkey and Malaysia. If we are unable to successfully manage the risks inherent to the operation and expansion of our global businesses, those risks could have a material adverse effect on our results of operations, cash flow or financial condition. These international business risks include:

| | • | fluctuations in currency exchange rates; |

| | • | changes in government regulations; |

| | • | restrictions on repatriation of earnings; |

| | • | import and export controls; |

| | • | political, social and economic instability; |

| | • | potential adverse tax consequences; |

| | • | difficulties in staffing and managing multi-national operations; |

| | • | unexpected changes in zoning or other land-use requirements; |

| | • | difficulties in our ability to enforce legal rights and remedies; and |

| | • | changes in regulatory requirements. |

Failure to achieve expected savings and synergies could adversely impact our operating profits and cash flows.

We focus on improving profitability through LEAN enterprise, low-cost sourcing and manufacturing initiatives, improving working capital management, developing new and enhanced products, consolidating factories where appropriate, automating manufacturing processes, diversification efforts and completing acquisitions which deliver synergies to stimulate sales and growth. If we are unable to successfully execute these programs, such failure could adversely affect our operating profits and cash flows. In addition, actions we may take to consolidate manufacturing operations to achieve cost savings or adjust to market developments may result in restructuring charges that adversely affect our profits.

Violation of anti-bribery or similar laws by our employees, business partners or agents could result in fines, penalties, damage to our reputation or other adverse consequences.

We cannot assure that our internal controls, code of conduct and training of our employees will provide complete protection from reckless or criminal acts of our employees, business partners or agents that might violate United States or international laws relating to anti-bribery or similar topics. A violation of these laws could subject us to civil or criminal investigations that could result in substantial civil or criminal fines and penalties, and which could damage our reputation.

We face significant competition in our markets and, if we are not able to respond to competition in our markets, our net sales, profits and cash flows could decline.

Our businesses operate in highly competitive markets. To compete effectively, we must retain long standing relationships with significant customers, offer attractive pricing, maintain product quality, meet customer delivery requirements, develop enhancements to products that offer performance features that are superior to our competitors and which maintain our brand recognition, continue to automate our manufacturing capabilities, continue to grow our business by establishing relationships with new customers, diversify into emerging markets and penetrate new markets. In addition, many of our businesses experience sales churn as customers seek lower cost suppliers. We attempt to offset this churn through our continual pursuit of new business opportunities. However, if we are unable to compete effectively or succeed in our pursuit of new business opportunities, our net sales, profitability and cash flows could decline. Pricing pressures resulting from competition may adversely affect our net sales and profitability.

If we are unable to successfully introduce new products and product enhancements, our future growth could be impaired.

Our ability to develop new products and innovations to satisfy customer needs or demands in the markets we serve can affect our competitive position and often requires significant investment of resources. Difficulties or delays in research, development or production of new products and services or failure to gain market acceptance of new products and technologies may significantly reduce future net sales and adversely affect our competitive position.

Increased prices or significant shortages of the commodities that we use in our businesses could result in lower net sales, profits and cash flows.

We purchase large quantities of steel, aluminum, refrigeration components, freight services, and other metal commodities for the manufacture of our products. We also purchase significant quantities of relatively rare elements used in the manufacture of certain of our electronics products. Historically, prices for commodities and rare elements have fluctuated, and we are unable to enter into long-term contracts or other arrangements to hedge the risk of price increases in many of these commodities. Significant price increases for these commodities and rare elements could adversely affect our operating profits if we cannot timely mitigate the price increases by successfully sourcing lower cost commodities or rare elements or by passing the increased costs on to customers. Shortages or other disruptions in the supply of these commodities or rare elements could delay sales or increase costs.

Current and threatened tariffs on components and finished goods from China and other countries could result in lower net sales, profits and cash flows and could impair the value of our investments in our Chinese operations.

As part of our low-cost country sourcing strategy, we (i) maintain manufacturing facilities in China and (ii) import certain components and finished goods from our own facilities and third-party suppliers in China. Many of the components and finished goods we import from China are subject to tariffs enacted by the United States government. While we attempt to pass on these additional costs to our customers, competitive factors (including competitors who import from other countries not subject to such tariffs) may limit our ability to sustain price increases and, as a result, may adversely impact our net sales, profits and cash flows. The maintenance of such tariffs over the long-term also could impair the value of our investments in our Chinese operations. In addition, the imposition of tariffs may influence the sourcing habits of certain end users of our products and services which, in turn, could have a direct impact on the requirements of our direct customers for our products and services. Such an impact could adversely affect our net sales, profits and cash flows.

An inability to identify or complete future acquisitions could adversely affect our future growth.

As part of our growth strategy, we intend to pursue acquisitions that provide opportunities for profitable growth for our businesses and enable us to leverage our competitive strengths. While we continue to evaluate potential acquisitions, we may not be able to identify and successfully negotiate suitable acquisitions, obtain financing for future acquisitions on satisfactory terms, obtain regulatory approval for certain acquisitions or otherwise complete acquisitions in the future. An inability to identify or complete future acquisitions could limit our future growth.

We may experience difficulties in integrating acquisitions.

Integration of acquired companies involves several risks, including:

| | • | inability to operate acquired businesses profitably; |

| | • | failure to accomplish strategic objectives for those acquisitions; |

| | • | unanticipated costs relating to acquisitions or to the integration of the acquired businesses; |

| | • | difficulties in achieving planned cost savings synergies and growth opportunities; and |

| | • | possible future impairment charges for goodwill and non-amortizable intangible assets that are recorded as a function of acquisitions. |

Additionally, our level of indebtedness may increase in the future if we finance acquisitions with debt, which would cause us to incur additional interest expense and could increase our vulnerability to general adverse economic and industry conditions and limit our ability to service our debt or obtain additional financing. We cannot assure that future acquisitions will not have a material adverse effect on our financial condition, results of operations and cash flows.

Impairment charges could reduce our profitability.

We test goodwill and our other intangible assets with indefinite useful lives for impairment on an annual basis or on an interim basis if a potential impairment factor arises that indicates the fair value of the reporting unit may fall below its carrying value. Various uncertainties, including adverse conditions in the capital markets or changes in general economic conditions, could impact the future operating performance at one or more of our businesses which could significantly affect our valuations and could result in additional future impairments. The recognition of an impairment of a significant portion of goodwill would negatively affect our results of operations.

Materially adverse or unforeseen legal judgments, fines, penalties or settlements could have an adverse impact on our profits and cash flows.

We are and may, from time to time, become a party to legal proceedings incidental to our businesses, including, but not limited to, alleged claims relating to product liability, environmental compliance, patent infringement, commercial disputes and employment and regulatory matters. In accordance with United States generally accepted accounting principles, we establish reserves based on our assessment of contingent liabilities. Subsequent developments in legal proceedings may affect our assessment and estimates of loss contingencies, recorded as reserves, which could require us to record additional reserves or make material payments which could adversely affect our profits and cash flows. Even the successful defense of legal proceedings may cause us to incur substantial legal costs and may divert management's time and resources away from our businesses.

The costs of complying with existing or future environmental regulations, and of correcting any violations of these regulations, could impact adversely our profitability.

We are subject to a variety of environmental laws relating to the storage, discharge, handling, emission, generation, use and disposal of chemicals, hazardous waste and other toxic and hazardous materials used to manufacture, or resulting from the process of manufacturing, our products and providing our services. We cannot predict the nature, scope or effect of regulatory requirements to which our operations might be subject or the manner in which existing or future laws will be administered or interpreted. We are also exposed to potential legacy environmental risks relating to businesses we no longer own or operate. Future regulations could be applied to materials, products or activities that have not been subject to regulation previously. The costs of complying with new or more stringent regulations, or with more vigorous enforcement of these or existing regulations, could be significant.

In addition, properly permitted waste disposal facilities used by us as a legal and legitimate repository for hazardous waste may in the future become mismanaged or abandoned without our knowledge or involvement. In such event, legacy landfill liability could attach to or be imposed upon us in proportion to the waste deposited at any disposal facility.

Environmental laws require us to maintain and comply with a number of permits, authorizations and approvals and to maintain and update training programs and safety data regarding materials used in our processes. Violations of these requirements could result in financial penalties and other enforcement actions. We could be required to halt one or more portions of our operations until a violation is cured. Although we attempt to operate in compliance with these environmental laws, we may not succeed in this effort at all times. The costs of curing violations or resolving enforcement actions that might be initiated by government authorities could be substantial.

The costs of complying with existing or future regulations applicable to our products, and of correcting any violations of such regulations, could adversely impact our profitability.

Certain of our products are subject to regulations promulgated by administrative agencies such as the Department of Energy, Occupational Health and Safety Administration and the Food and Drug Administration. Such regulations, among other matters, specify requirements regarding energy efficiency and product safety. Regulatory violations could result in financial penalties and other enforcement actions. We could be required to halt production of one or more products until a violation is cured. Although we attempt to produce our products in compliance with these requirements, the costs of curing violations or resolving enforcement actions that might be initiated by administrative agencies could be substantial.

Our results could be adversely affected by natural disasters, political crises, labor unrest or other catastrophic events.

Natural disasters, such as hurricanes, tornadoes, floods, earthquakes, and other adverse weather and climate conditions; political crises, such as terrorist attacks, war, labor unrest, and other political instability; or other catastrophic events, such as disasters occurring at our suppliers' manufacturing facilities, whether occurring in the United States or internationally, could disrupt our operations or the operations of one or more of our suppliers. Certain of our key manufacturing facilities are located in geographic areas with a higher than nominal risk of earthquake and flood (such as Japan) and hurricane (such as South Carolina). The effects of global warming have elevated the possibility of natural catastrophes which could impact these and other locations as well as the locations of certain of our customers and suppliers. Certain of our key facilities are in areas of higher than nominal political risk (such as China). The labor workforces in four of our U.S. facilities belong to unions and a strike, slowdown or other concerted effort could adversely impact production at the affected facility. To the extent any of these events occur, our operations and financial results could be adversely affected.

An expansion of the war in Ukraine could adversely affect our results of operations and financial condition.

To date, we have experienced minimal impacts on our businesses related to the ongoing war in Ukraine, beyond the general impact on global energy prices and other economic conditions. However, customer demand for our products and services as well as raw material and components from our suppliers may be impacted in the future if the war was to extend beyond Ukrainian borders, especially into Europe. Any of these impacts could have an adverse effect on our results of operations and financial condition.

We depend on our key personnel and the development of high potential employees; the loss of their services may adversely affect our business.

We believe that our success depends on our ability to hire new talent, develop existing talent and the continued employment of our senior management team and other key personnel. While we engage in ongoing succession planning, if one or more members of our senior management team or other key personnel were unable or unwilling to continue in their present positions, our business could be seriously harmed. In addition, if any of our key personnel joins a competitor or forms a competing company, some of our customers might choose to use the services of that competitor or those of a new company instead of our own. Other companies seeking to develop capabilities and products or services similar to ours may hire away some of our key personnel. If we are unable to maintain and develop our key personnel and attract new employees, the execution of our business strategy may be hindered and our growth limited.

Strategic divestitures and contingent liabilities from businesses that we sell could adversely affect our results of operations and financial condition.

From time to time, we have sold and may continue to sell business that we consider to be either underperforming or no longer part of our strategic vision. The sale of any such business could result in a financial loss and/or write-down of goodwill which could have a material adverse effect on our results for the financial reporting period during which such sale occurs. In addition, in connection with such divestitures, we have retained, and may in the future retain responsibility for some of the known and unknown contingent liabilities related to certain divestitures such as lawsuits, tax liabilities, product liability claims, and environmental matters.

The trading price of our common stock has been volatile, and investors in our common stock may experience substantial losses.

The trading price of our common stock has been volatile and may become volatile again in the future. The trading price of our common stock could decline or fluctuate in response to a variety of factors, including:

| | • | our failure to meet the performance estimates of securities analysts; |

| | • | changes in financial estimates of our net sales and operating results or buy/sell recommendations by securities analysts; |

| | • | fluctuations in our quarterly operating results; |

| | • | substantial sales of our common stock; |

| | • | changes in the amount or frequency of our payment of dividends or repurchases of our common stock; |

| | • | general stock market conditions; or |

| | • | other economic or external factors. |

Decreases in discount rates and actual rates of return could require an increase in future pension contributions to our pension plans which could limit our flexibility in managing our Company.

The discount rate and the expected rate of return on plan assets represent key assumptions inherent in our actuarially calculated pension plan obligations and pension plan expense. If discount rates and actual rates of return on invested plan assets were to decrease significantly, our pension plan obligations could increase materially. Although our pension plans have been frozen, the size of future required pension contributions could require us to dedicate a greater portion of our cash flow from operations to making contributions, which could negatively impact our financial flexibility.

Our business could be negatively impacted by cybersecurity threats, information systems and network interruptions, and other security threats or disruptions.

Our information technology networks and related systems are critical to the operation of our business and essential to our ability to successfully perform day-to-day operations. Cybersecurity threats are persistent, evolve quickly, and include, but are not limited to, computer viruses, ransomware, attempts to access information, denial of service and other electronic security breaches. These events could disrupt our operations or customers and other third-party IT systems in which we are involved and could negatively impact our reputation among our customers and the public which could have a negative impact on our financial conditions, results of operations, or liquidity.

We are subject to increasing regulation associated with data privacy and processing, the violation of which could result in significant penalties and harm our reputation.

Regulatory scrutiny of privacy, data protection, collection, use and sharing of data is increasing on a global basis. Like all global companies, we are subject to a number of laws, rules and directives (“privacy laws”) relating to the collection, use, retention, security, processing and transfer (“processing”) of personally identifiable information about our employees, customers and suppliers (“personal data”) in the countries where we operate. The most notable of these privacy laws is the EU’s General Data Protection Regulation (“GDPR”), which came into effect in 2018. GDPR extends the scope of the EU data protection law to all foreign companies processing data of EU residents and imposes a strict data protection compliance regime with severe penalties for non-compliance of up to the greater of 4% of worldwide turnover and €20 million. While we continue to strengthen our data privacy and protection policies and to train our personnel accordingly, a determination that there have been violations of GDPR or other privacy or data protection laws could expose us to significant damage awards, fines and other penalties that could, individually or in the aggregate, materially harm our results of operations and reputation.

Various restrictions in our charter documents, Delaware law and our credit agreement could prevent or delay a change in control that is not supported by our board of directors.

We are subject to several provisions in our charter documents, Delaware law and our credit facility that may discourage, delay or prevent a merger, acquisition or change of control that a stockholder may consider favorable. These anti-takeover provisions include:

| | • | maintaining a classified board and imposing advance notice procedures for nominations of candidates for election as directors and for stockholder proposals to be considered at stockholders' meetings; |

| | • | a provision in our certificate of incorporation that requires the approval of the holders of 80% of the outstanding shares of our common stock to adopt any agreement of merger, the sale of substantially all of the assets of the Company to a third party or the issuance or transfer by the Company of voting securities having a fair market value of $1 million or more to a third party, if in any such case such third party is the beneficial owner of 10% or more of the outstanding shares of our common stock, unless the transaction has been approved prior to its consummation by all of our directors; |

| | • | requiring the affirmative vote of the holders of at least 80% of the outstanding shares of our common stock for stockholders to amend our amended and restated by-laws; |

| | • | covenants in our credit facility restricting mergers, asset sales and similar transactions; and |

| | • | the Delaware anti-takeover statute contained in Section 203 of the Delaware General Corporation Law. |

Section 203 of the Delaware General Corporation Law prohibits a merger, consolidation, asset sale or other similar business combination between the Company and any stockholder of 15% or more of our voting stock for a period of three years after the stockholder acquires 15% or more of our voting stock, unless (1) the transaction is approved by our board of directors before the stockholder acquires 15% or more of our voting stock, (2) upon completing the transaction the stockholder owns at least 85% of our voting stock outstanding at the commencement of the transaction, or (3) the transaction is approved by our board of directors and the holders of 66 2/3% of our voting stock, excluding shares of our voting stock owned by the stockholder.

Item 1B. Unresolved Staff Comments

None.

Item 1C. Cybersecurity

Cybersecurity Risk Management and Strategy

Like other global companies, we face various cybersecurity threats that could have a material adverse effect on our business strategy, results of operations or financial condition. Cybersecurity, therefore, is an important element of our business and our overall enterprise risk management program, and while we have experienced a small number of cyber incidents over the last few years, none to date have been material or had a material adverse effect on our business or financial condition. To mitigate the risk, we have established a multilayered approach to assessing, identifying and managing material risks from cybersecurity threats, which includes the following:

| | ● | An annual cybersecurity risk assessment as part of our Enterprise Risk Management (ERM) program, which reviews and evaluates the potential impact and likelihood of various cyber risks and defines a framework for mitigating measures and residual risk. |

| | ● | A cybersecurity roadmap that is built from the risk assessment and feeds into our annual IT expenditure plan and which outlines the actions and investments we intend to take to enhance our cybersecurity posture and capabilities. |

| | ● | A continuous cybersecurity risk monitoring and response process, which involves daily review and real-time alerts of security incidents, a multi-disciplinary escalation and review process, and a reporting and filing protocol for material incidents within four business days of materiality determination. |

| | ● | A periodic cyber risk assessment conducted by independent experts, which provides an external validation and benchmarking of our cybersecurity practices and performance. |

As part of our cybersecurity program, we have and will continue to engage third parties, such as consultants, network security firms, auditors, and forensics providers, to assist us in assessing, managing, or investigating cyber risks or incidents. For example, we have engaged industry recognized third parties to monitor and conduct penetration and vulnerability testing on our networks and to assist us in the conduct of tabletop exercises.

In order to oversee and identify risks from cybersecurity threats associated with our use of third-party service providers, we perform third-party risk assessments designed to help protect against the misuse of IT by third parties and business partners and generally request that third-party service providers provide us information about their security policies and procedures.

Cybersecurity Governance and Oversight

We have a cybersecurity governance structure that involves the oversight and involvement of our board of directors and senior management.

Our board of directors, through its Audit Committee, maintains oversight of risks, including cybersecurity risks, and receives an update from the Director of IT Security and the Chief Information Officer (CIO) at each quarterly committee meeting. The Audit Committee also reports to the full board on cybersecurity matters as part of its regular report out after each meeting. The Audit Committee Chair is immediately informed of any breach that could be more than de minimis and is kept apprised of any resulting investigation and is briefed on the substance of any Form 8-K filing related to a material cybersecurity incident.

At the management level, oversight of our cybersecurity program rests with an internal committee comprised of the CIO, the Chief Legal Officer (CLO), and the Director of IT Security, who have in aggregate over 40 years of experience in assessing and managing cyber risks. The committee is responsible for overseeing the implementation and execution of our cybersecurity program and policies, and for engaging external experts as needed. The committee also reviews the log of security incidents as needed to validate that there are no materiality issues in the aggregate. The committee reports to the Audit Committee on a quarterly basis or more frequently as needed. We have an Incident Response Team comprised of IT, legal, and internal audit personnel that is activated with the help of other disciplines in the event of a perceived breach or security risk. The team is responsible for assessing the impact and materiality of the incident in accordance with a written Incidence Response Plan, determining the appropriate response and remediation actions, and communicating with internal and external stakeholders as needed.

In an effort to deter and detect cyber threats, we have a required cybersecurity training program that is provided to all new employees during on-boarding and semi-annually to employees with access to our IT resources, which aims to raise awareness and foster a culture of cybersecurity among our workforce. We also have an ongoing process of sending simulated phishing emails to employees. The results of these simulated attempts are monitored and reported to each employee’s manager. Training includes such cybersecurity topics as social engineering, phishing, password protection, confidential data protection, asset use and mobile security. The training also emphasizes the importance of reporting all incidents immediately.

Item 2. Properties

We operate a total of 62 facilities including manufacturing plants, service centers, and warehouses located throughout the United States, Europe, Canada, Southeast Asia, Korea, Japan, China, India, Brazil, and Mexico. The Company owns 20 of the facilities and the others are leased. For the year ended June 30, 2024, the approximate building space utilized by each segment is as follows:

| | | | | | | Area in Square Feet (in thousands) | |

Segment | | Number of Locations | | | Leased | | | Owned | | | Total | |

Asia Pacific | | | 10 | | | | 138 | | | | 177 | | | | 315 | |

EMEA(1) | | | 3 | | | | - | | | | 125 | | | | 125 | |

Other Americas | | | 1 | | | | - | | | | 56 | | | | 56 | |

United States | | | 7 | | | | 148 | | | | 74 | | | | 222 | |

Electronics | | | 21 | | | | 286 | | | | 432 | | | | 718 | |

| | | | | | | | | | | | | | | | | |

Asia Pacific | | | 11 | | | | 508 | | | | - | | | | 508 | |

EMEA(1) | | | 12 | | | | 176 | | | | 70 | | | | 246 | |

Other Americas | | | 3 | | | | 90 | | | | - | | | | 90 | |

United States | | | 6 | | | | 88 | | | | 79 | | | | 167 | |

Engraving | | | 32 | | | | 862 | | | | 149 | | | | 1,011 | |

| | | | | | | | | | | | | | | | | |

United States | | | 1 | | | | 164 | | | | - | | | | 164 | |

Scientific | | | 1 | | | | 164 | | | | - | | | | 164 | |

| | | | | | | | | | | | | | | | | |

EMEA(1) | | | 1 | | | | 83 | | | | - | | | | 83 | |

United States | | | 2 | | | | 107 | | | | 171 | | | | 278 | |

Engineering Technologies | | | 3 | | | | 190 | | | | 171 | | | | 361 | |

| | | | | | | | | | | | | | | | | |

Asia Pacific | | | 1 | | | | 76 | | | | - | | | | 76 | |

United States | | | 2 | | | | 33 | | | | 198 | | | | 231 | |

Specialty Solutions | | | 3 | | | | 109 | | | | 198 | | | | 307 | |

| | | | | | | | | | | | | | | | | |

United States | | | 2 | | | | 19 | | | | - | | | | 19 | |

Corporate & Other | | | 2 | | | | 19 | | | | - | | | | 19 | |

Total | | | 62 | | | | 1,630 | | | | 950 | | | | 2,580 | |

(1) EMEA consists of Europe, Middle East and S. Africa.

In general, the buildings are in sound operating condition and are considered to be adequate for their intended purposes and current uses.

We own substantially all of the machinery and equipment utilized in our businesses.

Item 3. Legal Proceedings

Discussion of legal matters is incorporated by reference to Part II, Item 8, Note 12, “CONTINGENCIES,” in the Notes to the Consolidated Financial Statements.

Item 4. Mine Safety Disclosures

Not Applicable

PART II

Item 5. Market for the Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

The principal market in which the Common Stock of Standex is traded is the New York Stock Exchange under the ticker symbol “SXI”. The approximate number of stockholders of record on July 31, 2024 was 1,092.

Additional information regarding our equity compensation plans is presented in the Notes to Consolidated Financial Statements under the caption “Stock-Based Compensation and Purchase Plans” and Item 12 “Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters.”

Issuer Purchases of Equity Securities (1) | | | | | | | | | | | | | | | | |

Quarter Ended June 30, 2024 | | | | | | | | | | | | | | | | |

Period | | (a) Total Number of Shares (or units) Purchased | | | (b) Average Price Paid per Share (or unit) | | | (c) Total Number of Shares (or units) Purchased as Part of Publicly Announced Plans or Programs | | | (d) Maximum Number (or Appropriate Dollar Value) of Shares (or units) that May Yet Be Purchased Under the Plans or Programs | |

April 1 - April 30, 2024 | | | 242 | | | $ | 173.11 | | | | 242 | | | $ | 33,301 | |

May 1 - May 31, 2024 | | | - | | | | - | | | | - | | | | 33,301 | |

June 1 - June 30, 2024 | | | - | | | | - | | | | - | | | | 33,301 | |

TOTAL | | | 242 | | | $ | 173.11 | | | | 242 | | | $ | 33,301 | |

(1) The Company has a Stock Buyback Program (the “Program”) which was originally announced on January 30, 1985 and most recently amended on April 28, 2022. Under the Program, the Company is authorized to repurchase up to an aggregate of $200 million of its shares. Under the program, purchases may be made from time to time on the open market, including through 10b5-1 trading plans, or through privately negotiated transactions, block transactions, or other techniques in accordance with prevailing market conditions and the requirements of the Securities and Exchange Commission. The Board’s authorization is open-ended and does not establish a timeframe for the purchases. The Company is not obligated to acquire a particular number of shares, and the program may be discontinued at any time at the Company’s discretion.

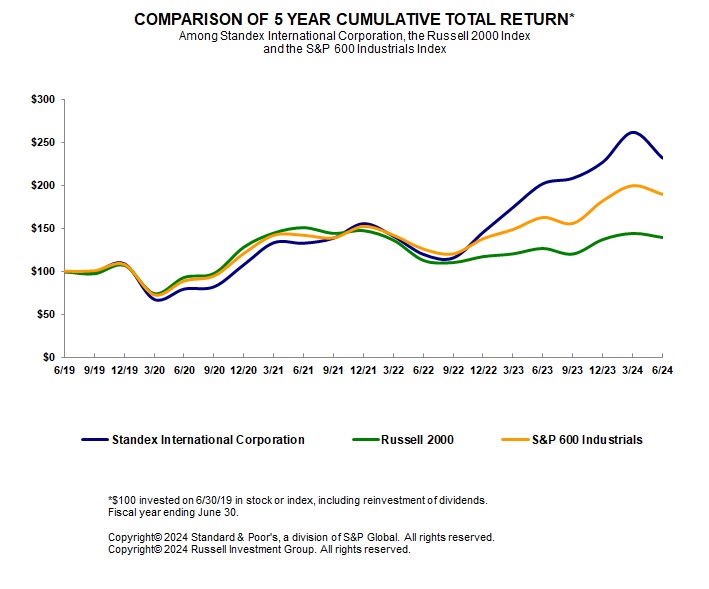

The graph below matches Standex International Corporation's cumulative 5-Year total shareholder return on common stock with the cumulative total returns of the Russell 2000 index and the S&P 600 Industrials index. The graph tracks the performance of a $100 investment in our common stock and in each index (with the reinvestment of all dividends) from 6/30/2019 to 6/30/2024.

Item 6. [Reserved]

Not Applicable

Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations

Overview

We are a diversified industrial manufacturer with leading positions in a variety of products and services that are used in diverse commercial and industrial markets. We have six operating segments that aggregate to five reportable segments. Please refer to Item 1. Business, above, for additional information regarding our segment structure and management strategy.

As part of our ongoing strategy:

| | o | On May 3, 2024, we acquired Sanyu Electric Pte Ltd, or SEPL, a privately held distributor of reed relays. Its results are reported in the Electronics segment. |

| | o | On February 19, 2024, we acquired, through our subsidiary Standex Electronics Japan Corporation, privately-held, Japanese-based Sanyu Switch Co., Ltd (Sanyu). Sanyu designs and manufactures reed relays, test sockets, testing systems for semiconductor and other electronics manufacturing, and other switching applications. Its results are reported in the Electronics segment. |

| | o | On July 31, 2023, we acquired Minntronix, a privately held company. Minntronix designs and manufactures customized as well as standard magnetics components and products including transformers, inductors, current sensors, coils, chokes, and filters. The products are used in applications across cable fiber, smart meters, industrial control and lighting, electric vehicles, and home security markets. Its results will be reported in the Electronics segment. |

| | o | In the third quarter of fiscal year 2023, we divested our Procon business for $75.0 million. This transaction reflects the continued simplification of our portfolio and enables greater focus on managing our larger platforms and pursuing growth opportunities. Proceeds will be deployed towards organic and inorganic initiatives and returning capital to shareholders. Its results are reported within our Specialty Solutions segment. In fiscal year 2023, we received $67.0 million cash consideration and recorded a pre-tax gain on the sale of $62.1 million in the Consolidated Financial Statements. Cash consideration received at closing excludes amounts held in escrow and was net of closing cash. |