UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

________________________________________

FORM 10-K

|

| |

| ý | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended February 3, 2013

OR

|

| |

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File Number 1-8207

THE HOME DEPOT, INC.

(Exact name of registrant as specified in its charter)

DELAWARE

(State or other jurisdiction of incorporation or organization)

95-3261426

(I.R.S. Employer Identification No.)

2455 PACES FERRY ROAD, N.W., ATLANTA, GEORGIA 30339

(Address of principal executive offices) (Zip Code)

Registrant’s Telephone Number, Including Area Code: (770) 433-8211

SECURITIES REGISTERED PURSUANT TO SECTION 12(b) OF THE ACT:

|

| |

| TITLE OF EACH CLASS | NAME OF EACH EXCHANGE ON WHICH REGISTERED |

| Common Stock, $0.05 Par Value Per Share | New York Stock Exchange |

SECURITIES REGISTERED PURSUANT TO SECTION 12(g) OF THE ACT: None

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ý No ¨

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No ý

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No ¨

Indicate by check mark whether the Registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the Registrant was required to submit and post such files). Yes ý No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check one):

|

| | | |

Large accelerated filer ý | Accelerated filer o | Non-accelerated filer o (Do not check if a smaller reporting company) | Smaller reporting company o |

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No ý

The aggregate market value of the common stock of the Registrant held by non-affiliates of the Registrant on July 29, 2012 was $80.2 billion.

The number of shares outstanding of the Registrant’s common stock as of March 11, 2013 was 1,485,517,485 shares.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Registrant’s proxy statement for the 2013 Annual Meeting of Shareholders are incorporated by reference in Part III of this Form 10-K to the extent described herein.

THE HOME DEPOT, INC.

FISCAL YEAR 2012 FORM 10-K

TABLE OF CONTENTS

|

| | |

| | |

| | | |

| Item 1. | | |

| | | |

| Item 1A. | | |

| | | |

| Item 1B. | | |

| | | |

| Item 2. | | |

| | | |

| Item 3. | | |

| | | |

| Item 4. | | |

| | | |

| | |

| | | |

| Item 5. | | |

| | | |

| Item 6. | | |

| | | |

| Item 7. | | |

| | | |

| Item 7A. | | |

| | | |

| Item 8. | | |

| | | |

| Item 9. | | |

| | | |

| Item 9A. | | |

| | | |

| Item 9B. | | |

| | | |

| | |

| | | |

| Item 10. | | |

| | | |

| Item 11. | | |

| | | |

| Item 12. | | |

| | | |

| Item 13. | | |

| | | |

| Item 14. | | |

| | | |

| | |

| | | |

| Item 15. | | |

| | | |

| | | |

CAUTIONARY STATEMENT PURSUANT TO THE

PRIVATE SECURITIES LITIGATION REFORM ACT OF 1995

Certain statements regarding our future performance constitute "forward-looking statements" as defined in the Private Securities Litigation Reform Act of 1995. Forward-looking statements may relate to, among other things, the demand for our products and services, net sales growth, comparable store sales, state of the economy, state of the residential construction, housing and home improvement markets, state of the credit markets, including mortgages, home equity loans and consumer credit, inventory and in-stock positions, commodity price inflation and deflation, implementation of store and supply chain initiatives, continuation of share repurchase programs, net earnings performance, earnings per share, capital allocation and expenditures, liquidity, return on invested capital, management of relationships with our suppliers and vendors, stock-based compensation expense, the effect of accounting charges, the effect of adopting certain accounting standards, the ability to issue debt on terms and at rates acceptable to us, store openings and closures, expense leverage and financial outlook.

Forward-looking statements are based on currently available information and our current assumptions, expectations and projections about future events. You should not rely on our forward-looking statements. These statements are not guarantees of future performance and are subject to future events, risks and uncertainties – many of which are beyond our control or are currently unknown to us – as well as potentially inaccurate assumptions that could cause actual results to differ materially from our expectations and projections. These risks and uncertainties include, but are not limited to, those described in Item 1A, "Risk Factors," and elsewhere in this report.

Forward-looking statements speak only as of the date they are made, and we do not undertake to update these statements other than as required by law. You are advised, however, to review any further disclosures we make on related subjects in our periodic filings with the Securities and Exchange Commission ("SEC").

PART I

Item 1. Business.

Introduction

The Home Depot, Inc. is the world’s largest home improvement retailer based on Net Sales for the fiscal year ended February 3, 2013 ("fiscal 2012"). The Home Depot stores sell a wide assortment of building materials, home improvement products and lawn and garden products and provide a number of services. The Home Depot stores average approximately 104,000 square feet of enclosed space, with approximately 24,000 additional square feet of outside garden area. As of the end of fiscal 2012, we had 2,256 The Home Depot stores located throughout the United States including the Commonwealth of Puerto Rico and the territories of the U.S. Virgin Islands and Guam, Canada and Mexico. When we refer to "The Home Depot," the "Company," "we," "us" or "our" in this report, we are referring to The Home Depot, Inc. and its consolidated subsidiaries.

The Home Depot, Inc. is a Delaware corporation that was incorporated in 1978. Our Store Support Center (corporate office) is located at 2455 Paces Ferry Road, N.W., Atlanta, Georgia 30339. Our telephone number is (770) 433-8211.

We maintain an Internet website at www.homedepot.com. We make available on our website, free of charge, our Annual Reports to shareholders, Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, Proxy Statements and Forms 3, 4 and 5, and amendments to those reports, as soon as reasonably practicable after filing such documents with, or furnishing such documents to, the SEC.

We include our website addresses throughout this filing for reference only. The information contained on our websites is not incorporated by reference into this report.

For information on key financial highlights, including historical revenues, profits and total assets, see the "Five-Year Summary of Financial and Operating Results" on page F-1 of this report and Item 7, "Management's Discussion and Analysis of Financial Condition and Results of Operations."

Our Business

Operating Strategy

In fiscal 2012, we continued to execute on our strategy focused on the following key initiatives:

| |

| • | Customer Service. Our customer service initiative is anchored on the principles of creating an emotional connection with our customers, putting customers first, taking care of our associates and simplifying the business. We underscored the importance of this initiative in fiscal 2012 by retraining all U.S. store associates on our Customers FIRST program prior to the Spring selling season. During fiscal 2012, we continued to invest in information technology and made certain strategic acquisitions to serve our customers more effectively. Through these efforts, we have continually improved our customer satisfaction survey results. We also sought to maintain competitive wages and incentive opportunities to attract, retain and motivate our associates. |

| |

| • | Product Authority. Our product authority initiative is facilitated by our merchandising transformation and portfolio strategy, which is focused on delivering product innovation, assortment and value. In fiscal 2012, we introduced a wide range of innovative new products to our professional and do-it-yourself customers, while remaining focused on offering every day values in our stores. |

| |

| • | Disciplined Capital Allocation, Productivity and Efficiency. We have advanced this initiative through building best-in-class competitive advantages in information technology and supply chain. During fiscal 2012, we completed the mechanization of our Rapid Deployment Center ("RDC") network, and we continue to focus on operating and optimizing our supply chain network. We also advanced this initiative through our continued focus on disciplined capital allocation and expense control, which drove higher returns on invested capital and allowed us to return value to shareholders through share repurchases and dividends. |

| |

| • | Interconnected Retail. As customers increasingly expect to be able to buy how, when and where they want, we believe that providing a seamless shopping experience across multiple channels, with an expanded array of merchandise, will be a key enabler for future success. The interconnected retail initiative is woven throughout our business and connects our other three key initiatives. In fiscal 2012, we launched several projects to support this initiative, starting in the first quarter with the rollout of a significant upgrade to our website, which enhanced the layout, visual appearance and responsiveness of the site. We also began construction of a new distribution center to support direct-to-customer fulfillment, with a second distribution center also under development, and we added new customer call centers in Utah and Georgia. Lastly, we introduced new programs, such as Buy Online, Return In Store ("BORIS") and Buy Online, Ship to Store ("BOSS"), to expand upon Buy Online, Pick-Up In Store ("BOPIS"), which we introduced in fiscal 2011. |

Customer Service

Our Customers. The Home Depot stores serve three primary customer groups, and we have different customer service approaches to meet their particular needs:

| |

| • | Do-It-Yourself ("D-I-Y") Customers. These customers are typically home owners who purchase products and complete their own projects and installations. Our associates assist these customers with specific product and installation questions both in our stores and through online resources and other media designed to provide product and project knowledge. We also offer a variety of clinics and workshops both to impart this knowledge and to build an emotional connection with our D-I-Y customers. |

| |

| • | Do-It-For-Me ("D-I-F-M") Customers. These customers are typically home owners who purchase materials themselves and hire third parties to complete the project or installation. Our stores offer a variety of installation services targeted at D-I-F-M customers who select and purchase products and installation of those products from us in the store. Our installation programs include products such as carpeting, flooring, cabinets, countertops and water heaters. In addition, we provide professional installation of a number of products sold through our in-home sales programs, such as roofing, siding, windows, furnaces and central air systems. |

| |

| • | Professional Customers. These customers are primarily professional remodelers, general contractors, repairmen, small business owners and tradesmen. We offer a variety of special programs to these customers, including delivery and will-call services, dedicated staff, expanded credit programs, designated parking spaces close to store entrances and bulk pricing programs for both online and in-store purchases. We recognize the unique service needs of the professional customer and use our expertise to facilitate their buying experience. |

In fiscal 2012, we undertook a number of projects and new developments to enhance our customers' shopping experiences. In addition to retraining our associates on the Customers FIRST program, we rolled out the "First Phone Junior" to all of our

stores. This version combines the communication features of a phone with the product and inventory lookup features of our First Phone, but without its complex business analytics and product ordering features. We can now spread the basic functionality and customer service benefits of the First Phone throughout the store at a lower cost. We also implemented a new "Store to Store" feature, which allows our associates to look up inventory in other stores, reserve the inventory and complete the sales transaction for the customer. We continued to take tasking out of the stores so that our associates can focus on assisting customers. To improve our labor efficiency, we have developed tools for automated, in-aisle inventory management to replace our former manual, paper-driven processes. As of the end of fiscal 2012, approximately 57% of our store labor hours were dedicated to customer-facing activity, with a goal of reaching 60% by the end of fiscal 2013.

In fiscal 2012, we continued to automate our special order and installation process to improve transparency and communication and to simplify the customer experience, and we launched MyInstall on our website, which allows our customers to schedule appointments and track their projects online. Our recent strategic acquisitions are also aimed at improving our customers' home improvement experiences. Red Beacon, acquired at the end of fiscal 2011, is a website that helps our D-I-F-M customers find professionals to help them complete home improvement projects. This acquisition enables us to deliver on consumer expectations by making it easier to get these projects done; it allows us to help our professional customers find jobs; and it builds relationships with our customers. We also acquired two companies that provided services to our customers – a flooring measurement company and a kitchen and bath refacing company. These acquisitions enable us to strengthen and unify our customers' home services experience under The Home Depot brand.

We help our professional, D-I-Y and D-I-F-M customers finance their projects by offering private label credit products in our stores through third-party credit providers. In fiscal 2012, our customers opened approximately 2.5 million new The Home Depot private label credit accounts, and at fiscal year end the total number of The Home Depot active account holders was approximately 10 million. Private label credit card sales accounted for approximately 22% of sales in fiscal 2012. In addition, to improve customer convenience at the register, we completed our rollout of PayPal® as an in-store payment option and, in certain stores, implemented a program for customers to receive an electronic copy of their receipt.

Our Associates. Our associates are key to our customer service initiative. We empower our associates to deliver excellent customer service through our Customers FIRST training program, and we have a number of Company-sponsored programs to recognize stores and individual associates for exceptional customer and community service. At the end of fiscal 2012, we employed approximately 340,000 associates, of whom approximately 21,000 were salaried, with the remainder compensated on an hourly or temporary basis. To attract and retain qualified personnel, we seek to maintain competitive salary and wage levels in each market we serve. We measure associate satisfaction regularly and maintain multiple means of ensuring effective communications with our associates. We believe that our employee relations are very good.

Product Authority

Our Products. Our product portfolio strategy is aimed at delivering innovation, assortment and value. A typical The Home Depot store stocks approximately 30,000 to 40,000 products during the year, including both national brand name and proprietary items. We also offer over 600,000 products through our Home Depot and Home Decorators Collection websites. To enhance our merchandising capabilities, we continued to make improvements to our information technology tools in fiscal 2012 to give our merchants and suppliers greater visibility into category and item performance and to continue to increase the localized assortment in our stores. We also acquired BlackLocus, Inc., a data analytics and pricing firm, which will bring additional tools and capabilities to support our merchandising team.

In fiscal 2012, we introduced a number of innovative and distinctive products to our customers at attractive values. Examples of these new products include the second generation of EcoSmart® LED light bulbs, including the only Daylight Downlight LED sold in retail; an improved version of Behr® Premium Ultra Interior Paint & Primer in One; appliances from Electrolux®, Whirlpool® and Frigidaire®; the second generation of Ryobi® lithium battery technology for power tools; a "click version" of tile with realistic wood looks from TrafficMaster® Allure™; and one inch cellular window blinds under our Home Decorators Collection brand.

During fiscal 2012, we offered a number of proprietary and exclusive brands across a wide range of departments, such as Husky® hand tools and tool storage, Defiant® door locks, Everbilt® hardware fasteners, Hampton Bay® lighting and fans, Vigoro® lawn care products, RIDGID® and Ryobi® power tools and Glacier Bay® bath fixtures. We also introduced the HDX brand in February 2012, with products in the tools and hardware, storage and cleaning categories. We will continue to assess strategic alliances and relationships with suppliers and opportunities to expand the range of products available under brand names that are exclusive to The Home Depot.

From our Store Support Center, we maintain a global sourcing program to obtain high-quality products directly from manufacturers around the world. Our merchant team identifies and purchases innovative products directly for our stores. Additionally, we have three sourcing offices located in the Chinese cities of Shanghai, Shenzhen and Dalian, as well as sourcing offices in Gurgaon, India; Rome, Italy; Monterrey, Mexico and Toronto, Canada.

Quality Assurance. We have both quality assurance and engineering resources that are dedicated to overseeing the quality of all of our products, whether they are directly imported, locally or globally sourced or proprietary branded products. Through these programs, we have established criteria for supplier and product performance that are designed to ensure that our products comply with applicable international, federal, state and local safety, quality and performance standards. We also have a Supplier Social and Environmental Responsibility Program designed to ensure that our suppliers adhere to the highest standards of social and environmental responsibility.

Energy Saving Products and Programs. As an industry leader, The Home Depot is committed to doing the right thing for our customers and the environment. By providing consumers a selection of environmentally preferred products that help them save money, energy and water, we are helping to ensure a more sustainable future. Through our Eco Options® Program introduced in 2007, we have created product categories that allow consumers to easily identify products that meet specifications for energy efficiency, water conservation, healthy home, clean air and sustainable forestry. As of the end of fiscal 2012, our Eco Options® Program has certified over 5,000 products. Through this program, we sell products such as ENERGY STAR® refrigerators, dishwashers, compact fluorescent light ("CFL") bulbs, EcoSmart® LED light bulbs, programmable thermostats, tankless "on demand" water heaters and other products, enabling our customers to save on their utility bills. LED light bulbs, which use approximately 85% less energy and last up to 20 years longer than traditional incandescent bulbs, continued to be one of our fastest growing categories for the year. We estimate that in fiscal 2012, sales of ENERGY STAR® qualified products helped consumers save over $700 million in annual utility costs. We also helped our customers save water through sales of WaterSense®-labeled bath faucets, showerheads, aerators and toilets. Through the sales of these products, we estimate that we have helped consumers save over 30 billion gallons of water and over $200 million in water bills.

In fiscal 2012, we made extensive updates to the Eco Options® page on our website to enable us to address growing customer demand for environmentally responsible and cost-saving products and projects. The newly enhanced site increases consumer awareness of the environmental impacts of various products, provides educational tips and identifies "green" projects. The site also helps consumers identify products included in the Eco Options® program, and it now includes a calculator to enable consumers to determine energy and water savings achievable by making small changes in their homes.

In partnership with the U.S. Green Building Council, we launched a website in fiscal 2012 to help our customers easily identify products with potential Leadership in Energy and Environmental Design ("LEED") point values. At the end of fiscal 2012, we had approximately 3,500 "LEED for Homes" products sold in our stores and online. The website, found at www.leed.homedepot.com, is designed to simplify the complexities of building green and arm our customers with the tools needed to navigate the LEED for Homes programs by providing tips, informative videos and educational content.

We continue to offer our nationwide, in-store CFL bulb recycling program launched in 2008. This service is offered to customers free of charge and is available in all U.S. stores. We also maintain an in-store rechargeable battery recycling program. Launched in 2001 and currently done in partnership with Call2Recycle, this program is also available to customers free of charge in all stores throughout the U.S. Through these recycling programs, in fiscal 2012 we helped recycle over 600,000 pounds of CFL bulbs and over 852,000 pounds of rechargeable batteries collected from our customers. In fiscal 2012, we also recycled over 98,000 lead acid batteries collected from our customers under our lead acid battery exchange program, as well as approximately 173,000 tons of cardboard through a nationwide cardboard recycling program across our U.S. stores.

Net Sales of Major Product Groups. The following table shows the percentage of Net Sales of each major product group (and related services) for each of the last three fiscal years:

|

| | | | | | | | |

| Product Group | Percentage of Net Sales for Fiscal Year Ended |

February 3,

2013 | | January 29,

2012 | | January 30,

2011 |

| Plumbing, electrical and kitchen | 30.8 | % | | 30.5 | % | | 30.0 | % |

| Hardware and seasonal | 29.4 |

| | 29.5 |

| | 29.4 |

|

| Building materials, lumber and millwork | 20.6 |

| | 21.1 |

| | 21.7 |

|

| Paint and flooring | 19.2 |

| | 18.9 |

| | 18.9 |

|

| Total | 100.0 | % | | 100.0 | % | | 100.0 | % |

Net Sales outside the U.S. were $8.4 billion, $8.0 billion and $7.5 billion for fiscal 2012, 2011 and 2010, respectively. Long-lived assets outside the U.S. totaled $3.1 billion, $3.1 billion and $3.2 billion as of February 3, 2013, January 29, 2012 and January 30, 2011, respectively.

Seasonality. Our business is subject to seasonal influences. Generally, our highest volume of sales occurs in our second fiscal quarter, and the lowest volume occurs during our fourth fiscal quarter. Fiscal 2012 included 53 weeks, rather than 52 weeks. As a result, our fourth fiscal quarter in 2012 included an extra week, which increased sales for that quarter.

Competition. Our industry is highly competitive, with competition based primarily on customer service, price, store location and appearance, and quality, availability and assortment of merchandise. Although we are currently the world’s largest home improvement retailer, in each of the markets we serve there are a number of other home improvement stores, electrical, plumbing and building materials supply houses and lumber yards. With respect to some products and services, we also compete with specialty design stores, showrooms, discount stores, local, regional and national hardware stores, mail order firms, warehouse clubs, independent building supply stores and, to a lesser extent, other retailers, as well as with installers of home improvement products. In addition, we face growing competition from online and multichannel retailers.

Intellectual Property. Our business has one of the most recognized brands in North America. As a result, we believe that The Home Depot® trademark has significant value and is an important factor in the marketing of our products, e-commerce, stores and business. We have registered or applied for registration of trademarks, service marks, copyrights and internet domain names, both domestically and internationally, for use in our business. We also maintain patent portfolios relating to some of our products and services and seek to patent or otherwise protect innovations we incorporate into our products or business operations.

Disciplined Capital Allocation, Productivity and Efficiency

Logistics. Our supply chain operations are focused on creating a competitive advantage through ensuring product availability for our customers, effectively using our investment in inventory, and managing total supply chain costs. Our fiscal 2012 initiatives have been to further optimize and efficiently operate our network, build new logistics capabilities and improve our inventory management systems and processes.

Our distribution strategy is to provide the optimal flow path for a given product. RDCs play a key role in optimizing our network as they allow for aggregation of product needs for multiple stores to a single purchase order and then rapid allocation and deployment of inventory to individual stores upon arrival at the RDC. This results in a simplified ordering process and improved transportation and inventory management. To enhance our RDC network, we continued adding mechanization, and at the end of fiscal 2012, all 18 of our U.S. RDCs were mechanized. We also expanded our U.S. transload program for imported products to four facilities operated by third parties near ocean ports. Transload facilities allow us to improve our import logistics costs and inventory management by enabling imported product to flow through our RDC network.

Over the past several years, we have centralized our inventory planning and replenishment function and implemented new forecasting and replenishment technology. This has helped us to improve our in-stock rates and our inventory productivity at the same time. At the end of fiscal 2012, over 91% of our U.S. store products were ordered through central replenishment.

In addition to our 18 RDCs in the U.S., at the end of fiscal 2012, we operated 33 bulk distribution centers, which handle products distributed optimally on flat bed trucks, in the U.S. and Canada. We also operated 36 conventional distribution centers, which include stocking, direct fulfillment and specialty distribution centers, in the U.S., Canada and Mexico. We remain committed to leveraging our supply chain capabilities to fully utilize and optimize our improved logistics network.

Commitment to Environmentally Responsible Operations. The Home Depot is committed to conducting business in an environmentally responsible manner. This commitment impacts all areas of our business, including energy usage, supply chain, store construction and maintenance, and, as noted above under "Energy Saving Products and Programs," product selection and delivery of product knowledge to our customers.

In fiscal 2012, we continued to implement strict operational standards that establish energy efficient practices in all of our U.S. facilities. These include HVAC unit temperature regulation and adherence to strict lighting schedules, which are the largest sources of energy consumption in our stores, as well as use of energy management systems in each store to monitor energy efficiency. We estimate that by implementing and utilizing these energy saving programs, we have saved over 5.5 billion kilowatt hours (kWh) since 2004, and we are on track to meet our goal of a 20% reduction in kWh per square foot in our U.S. stores by 2015.

Through our supply chain efficiencies described above under "Logistics," we are targeting a 20% reduction in our domestic supply chain greenhouse gas emissions from 2008 to 2015, which would equate to annual fuel savings of approximately 25 million gallons. We also continued to monitor our "carbon footprint" from the operation of our stores as well as from our transportation and supply chain activities. Through our energy conservation and supply chain initiatives, we reduced our absolute carbon emissions by approximately 777,000 metric tons in 2011 compared to 2010.

With respect to construction of our stores, we partnered with the U.S. Green Building Council and have built seven LEED for New Construction certified or similarly certified stores. In 2012, we opened a new store in Lodi, California and used a grant from the U.S. Department of Energy to help design, monitor and verify the energy savings at that store. The building is designed to consume substantially less energy than the 2007 90.1 ASHRAE standards established by the American Society of Heating, Refrigerating and Air-Conditioning Engineers, an international society that sets forth HVAC and refrigeration standards to promote sustainability. We also implemented a rainwater reclamation pilot in 2010. As of the end of fiscal 2012, we have retrofitted 81 of our stores with reclamation tanks to collect rainwater and condensation from HVAC units and garden center roofs, which is in turn used to water plants in our outside garden centers. In September 2011, we opened a store in St. Croix in the U.S. Virgin Islands with both ground mount and roof mount solar panel systems, and we estimate the combined total annual energy production of these systems to be over 580 megawatt hours.

Our efforts have resulted in a number of environmental awards and recognitions. For example, in 2012, we were named "Retail Partner of the Year" by the ENERGY STAR® division of the U.S. Environmental Protection Agency (the "EPA") for our overall excellence in energy efficiency, and we received the EPA's WaterSense® "2012 Associate Education Excellence Award." We were also recognized as a "High Performer" by the Carbon Disclosure Project.

We are strongly committed to maintaining a safe shopping and working environment for our customers and associates and protecting the environment of the communities in which we do business. Our Environmental, Health & Safety ("EH&S") function is dedicated to ensuring the health and safety of our customers and associates, with trained associates who evaluate, develop, implement and enforce policies, processes and programs on a Company-wide basis. Our EH&S policies are woven into our everyday operations and are part of The Home Depot culture. Some common program elements include: daily store inspection checklists (by department); routine follow-up audits from our store-based safety team members and regional, district and store operations field teams; equipment enhancements and preventative maintenance programs to promote physical safety; departmental merchandising safety standards; training and education programs for all associates, with varying degrees of training provided based on an associate's role and responsibilities; and awareness, communication and recognition programs designed to drive operational awareness and understanding of EH&S issues.

Interconnected Retail

Our interconnected retail initiative supports and connects our three other key initiatives. In fiscal 2012, we focused on leveraging technology to improve our customer's retail experience and provide better access to and information about our products. As described above, these efforts included information technology solutions that take tasks out of the store and free our associates to devote more time to customer-facing activities. They also included significant website enhancements that allow customers to more easily find and purchase an expanded array of products and provide them with flexibility and convenience for their purchases (for example, through our BOPIS, BORIS, BOSS and "Store to Store" programs). Through our website, which can be accessed through computers, tablets, smart phones and other mobile devices, customers can purchase products and track their installation projects through MyInstall and can connect with our associates and with one another to gain product and project knowledge in areas that are important to them. For example, in fiscal 2012, we updated the Eco Options® page on our website to provide more information for our environmentally-minded customers, and we had convenience in mind when we introduced a mobile application that allows our customers to select and purchase products quickly. Furthermore, to increase the productivity and efficiency of our associates, merchants and suppliers and ensure that

the right product is in the right place to meet our customers' needs, we continued to develop our distribution forecasting and replenishment system for enhanced inventory management.

Item 1A. Risk Factors.

The risks and uncertainties described below could materially and adversely affect our business, financial condition and results of operations and could cause actual results to differ materially from our expectations and projections. You should read these Risk Factors in conjunction with "Management’s Discussion and Analysis of Financial Condition and Results of Operations" in Item 7 and our Consolidated Financial Statements and related notes in Item 8. There also may be other factors that we cannot anticipate or that are not described in this report generally because we do not currently perceive them to be material. Those factors could cause results to differ materially from our expectations.

Sustained uncertainty regarding current economic conditions and other factors beyond our control could adversely affect demand for our products and services, our costs of doing business and our financial performance.

Our financial performance depends significantly on the stability of the housing, residential construction and home improvement markets, as well as general economic conditions, including changes in gross domestic product. Adverse conditions in or sustained uncertainty about these markets or the economy could adversely impact consumer confidence, causing our customers to delay purchasing or determine not to purchase home improvement products and services. Other factors – including high levels of unemployment and foreclosures, interest rate fluctuations, fuel and other energy costs, labor and healthcare costs, the availability of financing, the state of the credit markets, including mortgages, home equity loans and consumer credit, weather, natural disasters and other conditions beyond our control – could further adversely affect demand for our products and services, our costs of doing business and our financial performance.

Strong competition could adversely affect prices and demand for our products and services and could decrease our market share.

We operate in markets that are highly competitive. We compete principally based on customer service, price, store location and appearance, and quality, availability and assortment of merchandise. In each market we serve, there are a number of other home improvement stores, electrical, plumbing and building materials supply houses and lumber yards. With respect to some products and services, we also compete with specialty design stores, showrooms, discount stores, local, regional and national hardware stores, mail order firms, warehouse clubs, independent building supply stores and, to a lesser extent, other retailers, as well as with installers of home improvement products. In addition, we face growing competition from online and multichannel retailers as our customers increasingly use computers, tablets, smart phones and other mobile devices to shop online. Intense competitive pressures from one or more of our competitors or our inability to adapt effectively and quickly to a changing competitive landscape could affect our prices, our margins or demand for our products and services. If we are unable to timely and appropriately respond to these competitive pressures, including through maintenance of superior customer service and customer relationships, our market share and our financial performance could be adversely affected.

We may not timely identify or effectively respond to consumer needs, expectations or trends, which could adversely affect our relationship with customers, the demand for our products and services, and our market share.

It is difficult to successfully predict the products and services our customers will demand. The success of our business depends in part on our ability to identify and respond promptly to evolving trends in demographics, consumer preferences, expectations and needs, and unexpected weather conditions, while also managing inventory levels. Further, we have an aging store base that requires maintenance to deliver the shopping environment our customers desire. Failure to maintain attractive stores and to timely identify or effectively respond to changing consumer preferences, expectations and home improvement needs could adversely affect our relationship with customers, the demand for our products and services, and our market share.

Our success depends upon our ability to attract, train and retain highly qualified associates while also controlling our labor costs.

Our customers expect a high level of customer service and product knowledge from our associates. To meet the needs and expectations of our customers, we must attract, train and retain a large number of highly qualified associates while at the same time controlling labor costs. Our ability to control labor costs is subject to numerous external factors, including prevailing wage rates and health and other insurance costs, as well as the impact of legislation or regulations governing labor relations or healthcare benefits. In addition, we compete with other retail businesses for many of our associates in hourly positions, and we invest significant resources in training and motivating them to maintain a high level of job satisfaction. These positions have historically had high turnover rates, which can lead to increased training and retention costs. There is no assurance that we will be able to attract or retain highly qualified associates in the future.

We rely on third party suppliers. If we fail to identify and develop relationships with a sufficient number of qualified suppliers, or if our current suppliers experience financial difficulties, our ability to timely and efficiently access products that meet our high standards for quality could be adversely affected.

We buy our products from suppliers located throughout the world. Our ability to continue to identify and develop relationships with qualified suppliers who can satisfy our high standards for quality and our need to access products in a timely and efficient manner is a significant challenge. Our ability to access products also can be adversely affected by political instability, the financial instability of suppliers (particularly in light of continuing economic difficulties in various regions of the world), suppliers’ noncompliance with applicable laws, trade restrictions, tariffs, currency exchange rates, supply disruptions, shipping interruptions or costs, and other factors beyond our control.

If we are unable to effectively manage and expand our alliances and relationships with selected suppliers of brand name products, we may be unable to effectively execute our strategy to differentiate ourselves from our competitors.

As part of our focus on product differentiation, we have formed strategic alliances and exclusive relationships with selected suppliers to market products under a variety of well-recognized brand names. If we are unable to manage and expand these alliances and relationships or identify alternative sources for comparable products, we may not be able to effectively execute product differentiation.

If we do not maintain the security of customer, associate, supplier or company information, we could damage our reputation, incur substantial additional costs and become subject to litigation.

Our information systems are vulnerable to an increasing threat of continually evolving cybersecurity risks. Any significant compromise or breach of our data security could significantly damage our reputation, cause the disclosure of confidential customer, associate, supplier or company information, and result in significant costs, lost sales, fines and lawsuits. While we have implemented systems and processes to protect against unauthorized access to secured data and prevent data loss, there is no guarantee that these procedures are adequate to safeguard against all data security breaches. The regulatory environment related to information security, data collection and privacy is increasingly rigorous, with new and constantly changing requirements applicable to our business, and compliance with those requirements could result in additional costs.

A failure of a key information technology system or process could adversely affect our business.

We rely extensively on information technology systems, some of which are managed by third-party service providers, to analyze, process and manage transactions and data. We also rely heavily on the integrity of this data in managing our business. We or our service providers could experience errors, interruptions, delays or cessations of service in key portions of our information technology infrastructure, which could significantly disrupt our operations and be expensive, time consuming and resource-intensive to remedy.

Disruptions in our customer-facing technology systems could impair our interconnected retail strategy and give rise to negative customer experiences.

Through our information technology developments, we are able to provide an improved overall shopping environment and a multichannel experience that empowers our customers to shop and interact with us from computers, tablets, smart phones and other mobile communication devices. We use our website both as a sales channel for our products and also as a method of providing product, project and other relevant information to our customers to drive both in-store and online sales. We have multiple online communities and knowledge centers that allow us to inform, assist and interact with our customers. Multichannel retailing is continually evolving and expanding, and we must effectively respond to changing customer expectations and new developments. Disruptions, failures or other performance issues with these customer-facing technology systems could impair the benefits that they provide to our online and in-store business and negatively affect our relationship with our customers.

The implementation of our supply chain and technology initiatives could disrupt our operations in the near term, and these initiatives might not provide the anticipated benefits or might fail.

We have made, and we plan to continue to make, significant investments in our supply chain and technology. These initiatives are designed to streamline our operations to allow our associates to continue to provide high quality service to our customers, while simplifying customer interaction and providing our customers with a more interconnected retail experience. The cost and potential problems and interruptions associated with the implementation of these initiatives, including those associated with managing third-party service providers and employing new web-based tools and services, could disrupt or reduce the efficiency of our operations in the near term. In addition, our improved supply chain and new or upgraded technology might not provide the anticipated benefits, it might take longer than expected to realize the anticipated benefits, or the initiatives might fail altogether.

Disruptions in our supply chain and other factors affecting the distribution of our merchandise could adversely impact our business.

A disruption within our logistics or supply chain network, including damage or destruction to our distribution centers, could adversely affect our ability to deliver inventory in a timely manner, which could impair our ability to meet customer demand for products and result in lost sales or damage to our reputation. Such a disruption could negatively impact our financial performance or financial condition.

If we are unable to manage effectively our installation service business, we could suffer lost sales and be subject to fines, lawsuits and damaged reputation.

We act as a general contractor to provide installation services to our D-I-F-M customers through third-party installers. As such, we are subject to regulatory requirements and risks applicable to general contractors, which include management of licensing, permitting and quality of our third-party installers. We have established processes and procedures that provide protections beyond those required by law to manage these requirements and ensure customer satisfaction with the services provided by our third-party installers. If we fail to manage these processes effectively or provide proper oversight of these services, we could suffer lost sales, fines and lawsuits, as well as damage to our reputation, which could adversely affect our business.

Our costs of doing business could increase as a result of changes in, increased enforcement of, or adoption of new federal, state or local laws and regulations.

We are subject to various federal, state and local laws and regulations that govern numerous aspects of our business. Recently, there have been a large number of legislative and regulatory initiatives and reforms, as well as increased enforcement of existing laws and regulations by federal, state and local agencies. Changes in, increased enforcement of, or adoption of new federal, state or local laws and regulations governing minimum wage or living wage requirements, other wage, labor or workplace regulations, the sale of some of our products, transportation, logistics, taxes, energy costs or environmental matters could increase our costs of doing business or impact our store operations. Healthcare reform under the Patient Protection and Affordable Care Act and the Health Care and Education Reconciliation Act of 2010 could adversely impact our labor costs and our ability to negotiate favorable terms under our benefit plans for our associates.

If we cannot successfully manage the unique challenges presented by international markets, we may not be successful in our international operations.

Our ability to successfully conduct retail operations in, and source from, international markets is affected by many of the same risks we face in our U.S. operations, as well as unique costs and difficulties of managing international operations. Our international operations, including any expansion in international markets, may be adversely affected by local laws and customs, U.S. laws applicable to foreign operations and other legal and regulatory constraints, as well as political and economic conditions. Risks inherent in international operations also include, among others, potential adverse tax consequences, greater difficulty in enforcing intellectual property rights, risks associated with the Foreign Corrupt Practices Act and local anti-bribery law compliance, challenges in our ability to identify and gain access to local suppliers and the impact of foreign currency exchange rates and fluctuations.

The inflation or deflation of commodity prices could affect our prices, demand for our products, our sales and our profit margins.

Prices of certain commodity products, including lumber and other raw materials, are historically volatile and are subject to fluctuations arising from changes in domestic and international supply and demand, labor costs, competition, market speculation, government regulations and periodic delays in delivery. Rapid and significant changes in commodity prices may affect the demand for our products, our sales and our profit margins.

Our ability to obtain additional financing on favorable terms, if needed, could be adversely affected by the volatility in the capital markets.

We obtain and manage liquidity from the positive cash flow we generate from our operating activities and our access to capital markets, including our commercial paper programs supported by a back-up credit facility with a consortium of banks. There is no assurance that our ability to obtain additional financing through the capital markets, if needed, will not be adversely impacted due to economic conditions. New or incremental tightening in the credit markets, low liquidity and volatility in the capital markets could result in diminished availability of credit, higher cost of borrowing and lack of confidence in the equity market, making it more difficult to obtain additional financing on terms that are favorable to us.

Changes in accounting standards and subjective assumptions, estimates and judgments by management related to complex accounting matters could significantly affect our financial results or financial condition.

Generally accepted accounting principles and related accounting pronouncements, implementation guidelines and interpretations with regard to a wide range of matters that are relevant to our business, such as revenue recognition, asset impairment, impairment of goodwill and other intangible assets, inventories, lease obligations, self-insurance, tax matters and litigation, are highly complex and involve many subjective assumptions, estimates and judgments. Changes in these rules or their interpretation or changes in underlying assumptions, estimates or judgments could significantly change our reported or expected financial performance or financial condition.

We are involved in a number of legal proceedings, and while we cannot predict the outcomes of those proceedings and other contingencies with certainty, some of these outcomes may adversely affect our operations or increase our costs.

We are involved in a number of legal proceedings, including government inquiries and investigations, and consumer, employment, tort and other litigation that arise from time to time in the ordinary course of business. Litigation is inherently unpredictable, and the outcome of some of these proceedings and other contingencies could require us to take or refrain from taking actions which could adversely affect our operations or could result in excessive verdicts. Additionally, defending against these lawsuits and proceedings may involve significant expense and diversion of management’s attention and resources from other matters.

Item 1B. Unresolved Staff Comments.

Not applicable.

Item 2. Properties.

The following tables show locations of the 1,976 The Home Depot stores located in the U.S. and its territories and the 280 The Home Depot stores outside the U.S. at the end of fiscal 2012:

|

| | | | | | |

| U.S. Locations | Number of Stores |

| | U.S. Locations | Number of Stores |

|

| Alabama | 28 |

| | Montana | 6 |

|

| Alaska | 7 |

| | Nebraska | 8 |

|

| Arizona | 56 |

| | Nevada | 21 |

|

| Arkansas | 14 |

| | New Hampshire | 20 |

|

| California | 232 |

| | New Jersey | 67 |

|

| Colorado | 46 |

| | New Mexico | 13 |

|

| Connecticut | 29 |

| | New York | 100 |

|

| Delaware | 9 |

| | North Carolina | 40 |

|

| District of Columbia | 1 |

| | North Dakota | 1 |

|

| Florida | 153 |

| | Ohio | 70 |

|

| Georgia | 90 |

| | Oklahoma | 16 |

|

| Guam | 1 |

| | Oregon | 27 |

|

| Hawaii | 7 |

| | Pennsylvania | 70 |

|

| Idaho | 11 |

| | Puerto Rico | 8 |

|

| Illinois | 76 |

| | Rhode Island | 8 |

|

| Indiana | 24 |

| | South Carolina | 25 |

|

| Iowa | 10 |

| | South Dakota | 1 |

|

| Kansas | 16 |

| | Tennessee | 39 |

|

| Kentucky | 14 |

| | Texas | 178 |

|

| Louisiana | 27 |

| | Utah | 22 |

|

| Maine | 11 |

| | Vermont | 3 |

|

| Maryland | 41 |

| | Virgin Islands | 2 |

|

| Massachusetts | 45 |

| | Virginia | 49 |

|

| Michigan | 70 |

| | Washington | 45 |

|

| Minnesota | 33 |

| | West Virginia | 6 |

|

| Mississippi | 14 |

| | Wisconsin | 27 |

|

| Missouri | 34 |

| | Wyoming | 5 |

|

| | | | Total U.S. | 1,976 |

|

|

| | | | | | |

| International Locations | Number of Stores | | International Locations | Number of Stores |

| Canada: | | | Mexico: | |

| Alberta | 27 |

| | Aguascalientes | 1 |

|

| British Columbia | 26 |

| | Baja California Norte | 5 |

|

| Manitoba | 6 |

| | Baja California Sur | 2 |

|

| New Brunswick | 3 |

| | Chiapas | 2 |

|

| Newfoundland | 1 |

| | Chihuahua | 5 |

|

| Nova Scotia | 4 |

| | Coahuila | 5 |

|

| Ontario | 86 |

| | Colima | 2 |

|

| Prince Edward Island | 1 |

| | Distrito Federal | 7 |

|

| Quebec | 22 |

| | Durango | 1 |

|

| Saskatchewan | 4 |

| | Guanajuato | 4 |

|

| Total Canada | 180 |

| | Guerrero | 1 |

|

| | | | Hidalgo | 1 |

|

| | | | Jalisco | 6 |

|

| | | | Michoacán | 2 |

|

| | | | Morelos | 2 |

|

| | | | Nuevo León | 10 |

|

| | | | Puebla | 4 |

|

| |

|

| | Queretaro | 3 |

|

| |

| | Quintana Roo | 1 |

|

| | | | San Luis Potosi | 1 |

|

| | | | Sinaloa | 3 |

|

| | | | Sonora | 4 |

|

| | | | State of Mexico | 14 |

|

| | | | Tabasco | 1 |

|

| | | | Tamaulipas | 5 |

|

| | | | Tlaxcala | 1 |

|

| | | | Veracruz | 6 |

|

| | | | Yucatan | 1 |

|

| | | | Total Mexico | 100 |

|

During fiscal 2012, we opened three new The Home Depot stores in the U.S., including one relocation. We also opened nine new stores in Mexico. We closed seven stores in China.

Of our 2,256 stores operating at the end of fiscal 2012, approximately 90% were owned (including those owned subject to a ground lease) consisting of approximately 209.8 million square feet, and approximately 10% of such stores were leased consisting of approximately 24.7 million square feet.

Additionally, at the end of fiscal 2012, we had six Home Decorators Collection locations in Georgia, Illinois, Kansas, Missouri, New Jersey and Oklahoma, and one specialty paint and flooring location in Tianjin, China.

At the end of fiscal 2012, we operated 153 warehouses and distribution centers located in 35 states or provinces, consisting of approximately 37.2 million square feet, of which approximately 1.2 million is owned and approximately 36.0 million is leased.

Our executive, corporate staff, divisional staff and financial offices occupy approximately 2.2 million square feet of leased and owned space in Atlanta, Georgia. At the end of fiscal 2012 including the offices in Atlanta, we occupied an aggregate of approximately 3.5 million square feet, of which approximately 2.1 million square feet is owned and approximately 1.4 million square feet is leased, for store support centers and customer support centers.

Item 3. Legal Proceedings.

We are reporting the following proceedings to comply with SEC regulations, which require us to disclose certain information about proceedings arising under federal, state or local environmental provisions if we reasonably believe that such proceedings may result in monetary sanctions of $100,000 or more.

As previously reported, in September 2010, the Company was contacted by district attorneys in three counties in California within the South Coast Air Quality Management District (the "SCAQMD") and the City of Los Angeles regarding allegations that the Company sold products in those counties with VOC (volatile organic compound) levels in excess of amounts permitted by SCAQMD rules. In June 2011, two related complaints were filed in the Superior Court of California – County of Los Angeles against the Company. The first action was brought by the SCAQMD and alleges that the Company sold products with higher-than-permitted VOC levels. This action seeks $30 million in civil penalties and injunctive relief. The second action was brought by the Los Angeles City Attorney and the district attorneys of each of Orange, Riverside and San Bernardino counties and alleges that the Company engaged in unfair business practices and false advertising when selling these products. This action seeks unspecified civil penalties and injunctive relief. Both actions are scheduled to be tried together as a bench trial in May 2013. In March 2013, we tentatively reached a joint settlement agreement to resolve these actions for an aggregate of $6.9 million, plus $1.1 million in fees and costs. The settlement requires the approval of the trial court.

Item 4. Mine Safety Disclosures.

Not applicable.

PART II

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

Since April 19, 1984, our common stock has been listed on the New York Stock Exchange, trading under the symbol "HD." The Company paid its first cash dividend on June 22, 1987, and has paid cash dividends during each subsequent quarter. Future dividend payments will depend on the Company’s earnings, capital requirements, financial condition and other factors considered relevant by the Board of Directors.

The table below sets forth the high and low sales prices of our common stock on the New York Stock Exchange and the quarterly cash dividends declared per share of common stock for the periods indicated.

|

| | | | | | | | | | | |

| | Price Range | | Cash Dividends Declared |

| | High | | Low | |

| Fiscal Year 2012 | | | | | |

| First Quarter Ended April 29, 2012 | $ | 52.03 |

| | $ | 44.39 |

| | $ | 0.29 |

|

| Second Quarter Ended July 29, 2012 | $ | 53.71 |

| | $ | 47.02 |

| | $ | 0.29 |

|

| Third Quarter Ended October 28, 2012 | $ | 63.20 |

| | $ | 51.39 |

| | $ | 0.29 |

|

| Fourth Quarter Ended February 3, 2013 | $ | 67.82 |

| | $ | 60.65 |

| | $ | 0.39 |

|

| Fiscal Year 2011 | | | | | |

| First Quarter Ended May 1, 2011 | $ | 38.48 |

| | $ | 35.68 |

| | $ | 0.25 |

|

| Second Quarter Ended July 31, 2011 | $ | 37.46 |

| | $ | 33.47 |

| | $ | 0.25 |

|

| Third Quarter Ended October 30, 2011 | $ | 37.22 |

| | $ | 28.51 |

| | $ | 0.29 |

|

| Fourth Quarter Ended January 29, 2012 | $ | 45.41 |

| | $ | 35.54 |

| | $ | 0.29 |

|

As of March 11, 2013, there were approximately 146,000 shareholders of record of our common stock and approximately 1,066,000 additional "street name" holders whose shares are held of record by banks, brokers and other financial institutions.

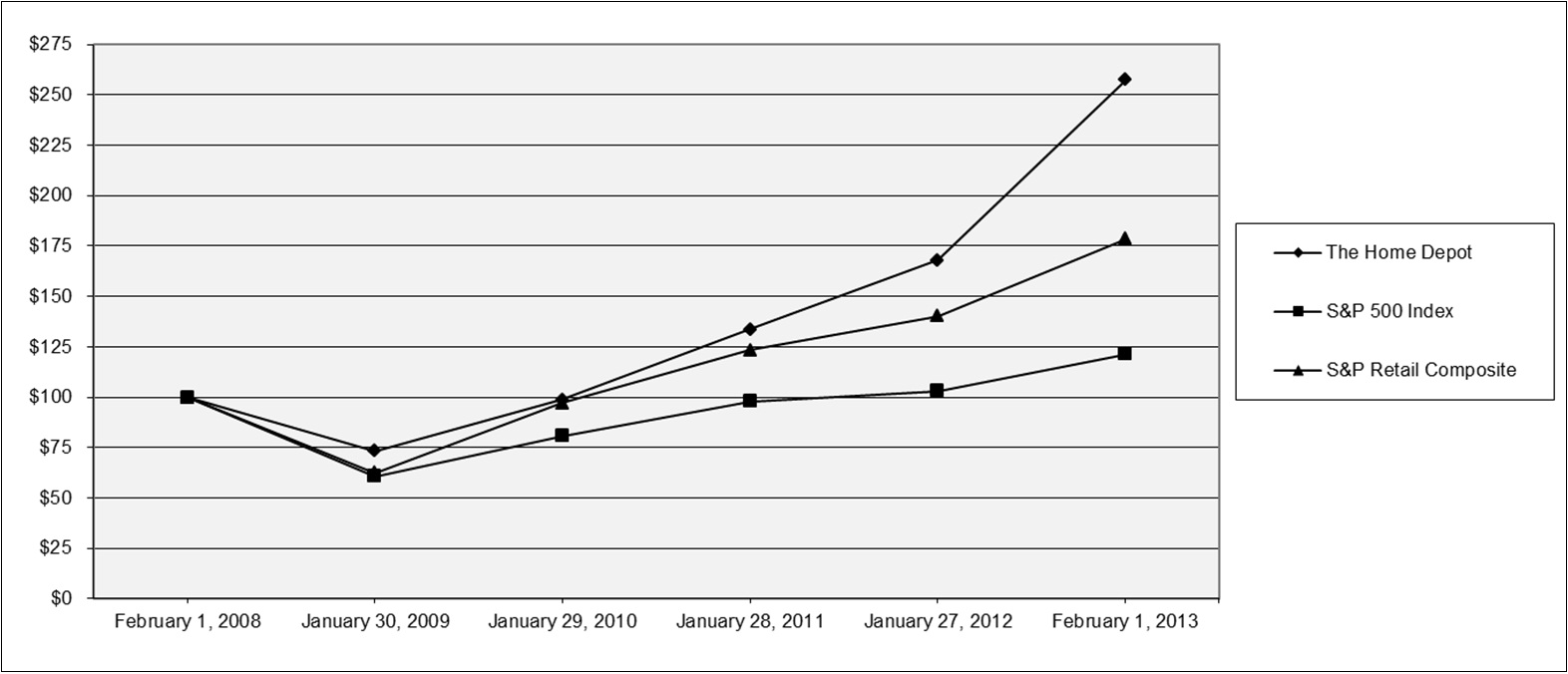

Stock Performance Graph

The graph and table below present the Company’s cumulative total shareholder returns relative to the performance of the Standard & Poor’s 500 Composite Stock Index and the Standard & Poor’s Retail Composite Index for the five-year period commencing February 1, 2008, the last trading day of fiscal 2007, and ending February 1, 2013, the last trading day of fiscal 2012. The graph assumes $100 invested at the closing price of the Company’s common stock on the New York Stock Exchange and each index on February 1, 2008 and assumes that all dividends were reinvested on the date paid. The points on the graph represent fiscal year-end amounts based on the last trading day in each fiscal year.

|

| | | | | | | | | | | | | | | | | | | | | | | |

| | February 1, 2008 | | January 30, 2009 | | January 29, 2010 | | January 28, 2011 | | January 27, 2012 | | February 1, 2013 |

| The Home Depot | $ | 100.00 |

| | $ | 73.23 |

| | $ | 98.87 |

| | $ | 133.58 |

| | $ | 168.08 |

| | $ | 257.62 |

|

| S&P 500 Index | $ | 100.00 |

| | $ | 60.63 |

| | $ | 80.72 |

| | $ | 97.88 |

| | $ | 103.10 |

| | $ | 121.25 |

|

| S&P Retail Composite Index | $ | 100.00 |

| | $ | 62.28 |

| | $ | 96.88 |

| | $ | 123.43 |

| | $ | 140.22 |

| | $ | 178.55 |

|

Issuer Purchases of Equity Securities

Since the inception of the Company's share repurchase program in fiscal 2002 through the end of fiscal 2012, the Company has repurchased shares of its common stock having a value of approximately $37.6 billion. The number and average price of shares purchased in each fiscal month of the fourth quarter of fiscal 2012 are set forth in the table below:

|

| | | | | | | | | | | | | |

| Period | Total Number of Shares Purchased(1) | | Average Price Paid Per Share(1) | | Total Number of Shares Purchased as Part of Publicly Announced Program(2) | | Dollar Value of Shares that May Yet Be Purchased Under the Program(2) |

| Oct. 29, 2012 – Nov. 25, 2012 | 784,340 |

| | $ | 63.56 |

| | 737,172 |

| | $ | 3,063,069,066 |

|

Nov. 26, 2012 – Dec. 23, 2012(3) | 5,254,485 |

| | $ | 62.49 |

| | 5,252,936 |

| | $ | 2,826,716,204 |

|

| Dec. 24, 2012 – Feb. 3, 2013 | 6,502,215 |

| | $ | 64.25 |

| | 6,485,514 |

| | $ | 2,410,014,073 |

|

—————

| |

| (1) | These amounts include repurchases pursuant to the Company’s 1997 and 2005 Omnibus Stock Incentive Plans (the "Plans"). Under the Plans, participants may surrender shares as payment of applicable tax withholding on the vesting of restricted stock and deferred share awards. Participants in the Plans may also exercise stock options by surrendering shares of common stock that the participants already own as payment of the exercise price. Shares so surrendered by participants in the Plans are repurchased pursuant to the terms of the Plans and applicable award agreement and not pursuant to publicly announced share repurchase programs. |

| |

| (2) | The Company’s common stock repurchase program was initially announced on July 15, 2002. As of the end of fiscal 2012, the Board had approved purchases up to $40.0 billion, of which $2.4 billion remained available at the end of fiscal 2012. In February 2013, our Board of Directors authorized a new $17.0 billion share repurchase program that replaces the previous authorization. |

| |

| (3) | In the third quarter of fiscal 2012, the Company paid $650 million under an Accelerated Share Repurchase ("ASR") agreement with a third-party financial institution and received an initial delivery of approximately 9 million shares. The transaction was completed in the fourth quarter of fiscal 2012, with the Company receiving approximately 2 million additional shares to settle the agreement. The Average Price Paid Per Share was calculated with reference to the average stock price of the Company's common stock over the term of the ASR agreement. |

In March 2013, the Company entered into an ASR agreement with a third-party financial institution to repurchase $1.5 billion of the Company’s common stock. See Note 6 to the Consolidated Financial Statements included in this report. Shares received in connection with the ASR agreement will be reflected in the share repurchase table in future quarters.

Sales of Unregistered Securities

During the fourth quarter of fiscal 2012, the Company issued 436 deferred stock units under The Home Depot, Inc. NonEmployee Directors’ Deferred Stock Compensation Plan pursuant to the exemption from registration provided by Section 4(a)(2) of the Securities Act of 1933, as amended (the "Securities Act"). The deferred stock units were credited to the accounts of those nonemployee directors who elected to receive board retainers in the form of deferred stock units instead of cash during the fourth quarter of fiscal 2012. The deferred stock units convert to shares of common stock on a one-for-one basis following a termination of service as described in this plan.

During the fourth quarter of fiscal 2012, the Company credited 24,961 deferred stock units to participant accounts under The Home Depot FutureBuilder Restoration Plan pursuant to an exemption from the registration requirements of the Securities Act for involuntary, non-contributory plans. The deferred stock units convert to shares of common stock on a one-for-one basis following a termination of service as described in this plan.

Item 6. Selected Financial Data.

The information required by this item is incorporated by reference to page F-1 of this report.

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

Executive Summary and Selected Consolidated Statements of Earnings Data

For the fiscal year ended February 3, 2013 ("fiscal 2012"), we reported Net Earnings of $4.5 billion and Diluted Earnings per Share of $3.00 compared to Net Earnings of $3.9 billion and Diluted Earnings per Share of $2.47 for the fiscal year ended January 29, 2012 ("fiscal 2011"). The results for fiscal 2012 included a total charge of $145 million, net of tax, related to the closing of our remaining seven big box stores in China ("China store closings") in fiscal 2012, which had a negative impact of $0.10 to Diluted Earnings per Share. Excluding the charges related to the China store closings, Net Earnings were $4.7 billion and Diluted Earnings per Share were $3.10 for fiscal 2012.

Net Sales increased 6.2% to $74.8 billion for fiscal 2012 from $70.4 billion for fiscal 2011. Our comparable store sales increased 4.6% in fiscal 2012, driven by a 2.9% increase in our comparable store average ticket and an increase in our comparable store customer transactions. Comparable store sales for our U.S. stores increased 4.9% in fiscal 2012.

Fiscal 2012 consisted of 53 weeks compared with 52 weeks for fiscal 2011. The 53rd week added approximately $1.2 billion in Net Sales and increased Diluted Earnings per Share by approximately $0.07 for fiscal 2012.

In fiscal 2012, we continued to focus on the following four key initiatives:

Customer Service – Our focus on customer service is anchored on the principles of creating an emotional connection with customers, putting customers first and simplifying the business. In fiscal 2012, we opened new customer call centers in Utah and Georgia to support our interconnected business. In addition, as a result of initiatives such as our new scheduling system for our associates and a centralized return to vendor process initiated in fiscal 2011, we now have approximately 57% of our store labor hours dedicated to customer-facing activity and expect to achieve our goal of 60% in fiscal 2013. Through these and other efforts, we continue to see our customer satisfaction survey scores improve.

Product Authority – Our focus on product authority is facilitated by our merchandising transformation and portfolio strategy, which is aimed at delivering product innovation, assortment and value. As part of this effort, we introduced innovative new products and great values for both our professional and D-I-Y customers in a variety of departments. Also in fiscal 2012, we expanded some of our appliance showrooms to include the Electrolux®, Whirlpool® and Frigidaire® brands. These brands were also added to our e-commerce platform in fiscal 2012.

Disciplined Capital Allocation, Productivity and Efficiency – Our approach to driving productivity and efficiency is advanced through continuous operational improvement, incremental supply chain benefits, disciplined capital allocation and expense control and building shareholder value through higher returns on invested capital and total value returned to shareholders in the form of dividends and share repurchases. In fiscal 2012, we completed the mechanization of all of our RDCs, which we expect to further improve the cost effectiveness of this platform. Our inventory turnover ratio was 4.5 times at the end of fiscal 2012 compared to 4.3 times at the end of fiscal 2011.

We repurchased a total of 74 million shares for $4.0 billion through ASR agreements and the open market during fiscal 2012. In addition, in February 2013, our Board of Directors authorized a new $17.0 billion share repurchase program that replaces the previous authorization, and announced a 34% increase in our quarterly cash dividend to $0.39 per share.

Interconnected Retail – Our focus on interconnected retail is based on building a competitive platform across all commerce channels. During fiscal 2012, we launched improvements to our website, including MyInstall, which is designed to improve transparency and communication in installation projects and to simplify the customer experience. We made several enhancements to our professional customer website, including adding an online bulk pricing program that mirrors our in-store bulk pricing program. We also introduced new programs, such as Buy Online, Return In Store ("BORIS") and Buy Online, Ship To Store ("BOSS") in fiscal 2012, to expand upon Buy Online, Pick-Up In Store ("BOPIS"), which we introduced in fiscal 2011.

In May 2012, we acquired MeasureComp L.L.C., a flooring measurement and quote building company. MeasureComp's business was largely dedicated to The Home Depot and by in-sourcing this service under Home Depot Measurement Services, we expect to build a seamless process for our flooring customers that is designed to provide a better experience for them and a better close rate for us.

In October 2012, we completed the acquisition of U.S. Home Systems, Inc. ("USHS"). USHS was an exclusive provider of kitchen and bath refacing products and services as well as closet and garage organizational systems to The Home Depot. This acquisition will allow us to create more effective interconnection between our stores and the USHS in-home selling platform under Home Depot Interiors, similar to what we have done with our roofing, siding and windows businesses.

We also completed the acquisition of BlackLocus, Inc. in December 2012. BlackLocus is a data analytics and pricing company, which will bring additional tools and capabilities to support our merchandising team.

We opened twelve new stores, including nine new stores in Mexico, two new stores in the U.S. and one relocation in the U.S., and closed seven stores in China in fiscal 2012, for a total store count of 2,256 at the end of fiscal 2012. As of the end of fiscal 2012, a total of 280 of our stores, or 12.4%, were located in Canada and Mexico.

We generated $7.0 billion of cash flow from operations in fiscal 2012. We used this cash flow to fund $4.0 billion of share repurchases, pay $1.7 billion of dividends and fund $1.3 billion in capital expenditures.

Our return on invested capital (computed on net operating profit after tax for the trailing twelve months and the average of beginning and ending long-term debt and equity) was 17.0% for fiscal 2012 compared to 14.9% for fiscal 2011.

We believe the selected sales data, the percentage relationship between Net Sales and major categories in the Consolidated Statements of Earnings and the percentage change in the dollar amounts of each of the items presented below are important in evaluating the performance of our business operations.

|

| | | | | | | | | | | | | | | | | |

| | % of Net Sales | | % Increase (Decrease) In Dollar Amounts |

| | Fiscal Year(1) |

| | 2012 | | 2011 | | 2010 | | 2012 vs. 2011 | | 2011 vs. 2010 |

| NET SALES | 100.0 | % | | 100.0 | % | | 100.0 | % | | 6.2 | % | | 3.5 | % |

| GROSS PROFIT | 34.6 |

| | 34.5 |

| | 34.3 |

| | 6.5 |

| | 4.1 |

|

| Operating Expenses: | | | | | | | | | |

| Selling, General and Administrative | 22.1 |

| | 22.8 |

| | 23.3 |

| | 3.0 |

| | 1.1 |

|

| Depreciation and Amortization | 2.1 |

| | 2.2 |

| | 2.4 |

| | (0.3 | ) | | (2.7 | ) |

| Total Operating Expenses | 24.2 |

| | 25.0 |

| | 25.7 |

| | 2.7 |

| | 0.8 |

|

| OPERATING INCOME | 10.4 |

| | 9.5 |

| | 8.6 |

| | 16.6 |

| | 14.1 |

|

| Interest and Other (Income) Expense: | | | | | | | | | |

| Interest and Investment Income | — |

| | — |

| | — |

| | N/M |

| | N/M |

|

| Interest Expense | 0.8 |

| | 0.9 |

| | 0.8 |

| | 4.3 |

| | 14.3 |

|

| Other | (0.1 | ) | | — |

| | 0.1 |

| | N/M |

| | (100.0 | ) |

| Interest and Other, net | 0.7 |

| | 0.8 |

| | 0.8 |

| | (8.1 | ) | | 4.8 |

|

EARNINGS BEFORE PROVISION FOR INCOME TAXES | 9.7 |

| | 8.6 |

| | 7.8 |

| | 19.0 |

| | 15.1 |

|

| Provision for Income Taxes | 3.6 |

| | 3.1 |

| | 2.8 |

| | 22.9 |

| | 12.9 |

|

| NET EARNINGS | 6.1 | % | | 5.5 | % | | 4.9 | % | | 16.8 | % | | 16.3 | % |

| SELECTED SALES DATA | | | | | | | | | |

Number of Customer Transactions (in millions)(2) | 1,364.0 |

| | 1,317.5 |

| | 1,305.7 |

| | 3.5 | % | | 0.9 | % |

Average Ticket(2) | $ | 54.89 |

| | $ | 53.28 |

| | $ | 51.93 |

| | 3.0 | % | | 2.6 | % |

Weighted Average Weekly Sales per Operating Store (in thousands) | $ | 627 |

| | $ | 601 |

| | $ | 581 |

| | 4.3 | % | | 3.4 | % |

Weighted Average Sales per Square Foot(2) | $ | 318.63 |

| | $ | 299.00 |

| | $ | 288.64 |

| | 6.6 | % | | 3.6 | % |

Comparable Store Sales Increase (%)(3) | 4.6 | % | | 3.4 | % | | 2.9 | % | | N/A |

| | N/A |

|

Note: Certain percentages may not sum to totals due to rounding.

—————

| |

| (1) | Fiscal years 2012, 2011 and 2010 refer to the fiscal years ended February 3, 2013, January 29, 2012 and January 30, 2011, respectively. Fiscal year 2012 includes 53 weeks; fiscal years 2011 and 2010 include 52 weeks. |

| |

| (2) | The 53rd week of fiscal 2012 increased customer transactions by approximately 21 million, positively impacted average ticket by approximately $0.06 and positively impacted weighted average sales per square foot by approximately $5.51. |

| |

| (3) | Includes Net Sales at locations open greater than 12 months, including relocated and remodeled stores and excluding closed stores. Retail stores become comparable on the Monday following their 365th day of operation. Comparable store sales is intended only as supplemental information and is not a substitute for Net Sales or Net Earnings presented in accordance with generally accepted accounting principles. Net Sales for the 53rd week of fiscal 2012 are not included in comparable store sales results for fiscal 2012. |

N/M – Not Meaningful

N/A – Not Applicable

Results of Operations

For an understanding of the significant factors that influenced our performance during the past three fiscal years, the following discussion should be read in conjunction with the Consolidated Financial Statements and the Notes to Consolidated Financial Statements presented in this report.

Fiscal 2012 Compared to Fiscal 2011

Net Sales

Fiscal 2012 consisted of 53 weeks compared to 52 weeks in fiscal 2011. Net Sales for fiscal 2012 increased 6.2% to $74.8 billion from $70.4 billion for fiscal 2011. The increase in Net Sales for fiscal 2012 reflects the impact of positive comparable store sales and $1.2 billion of Net Sales attributable to the additional week in fiscal 2012. Total comparable store sales increased 4.6% for fiscal 2012 compared to an increase of 3.4% for fiscal 2011.