UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

|

| |

| (Mark One) | |

| ý | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2013

OR

|

| |

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to .

Commission File Number 001-07845

LEGGETT & PLATT, INCORPORATED

(Exact name of registrant as specified in its charter)

|

| | |

| Missouri | | 44-0324630 |

(State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

No. 1 Leggett Road Carthage, Missouri | | 64836 |

| (Address of principal executive offices) | | (Zip code) |

Registrant’s telephone number, including area code: (417) 358-8131

SECURITIES REGISTERED PURSUANT TO SECTION 12(b) OF THE ACT:

|

| | |

| Title of Each Class | | Name of each exchange on which registered |

| Common Stock, $.01 par value | | New York Stock Exchange |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ý No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

| | | |

| Large accelerated filer | x | | Accelerated filer ¨ |

| Non-accelerated filer | ¨ | (Do not check if a smaller reporting company) | Smaller reporting company ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No ý

The aggregate market value of the voting stock held by non-affiliates of the registrant (based on the closing price of our common stock on the New York Stock Exchange) on June 28, 2013 was $4,242,267,870.

There were 138,895,256 shares of the registrant’s common stock outstanding as of February 14, 2014.

DOCUMENTS INCORPORATED BY REFERENCE

Part of Item 10, and all of Items 11, 12, 13 and 14 of Part III are incorporated by reference from the Company’s definitive Proxy Statement for the Annual Meeting of Shareholders to be held on May 7, 2014.

TABLE OF CONTENTS

LEGGETT & PLATT, INCORPORATED—FORM 10-K

FOR THE YEAR ENDED December 31, 2013

|

| | | |

| | Page Number |

| 1 |

|

| PART I |

| Item 1. | | 2 |

|

| | | |

| Item 1A. | | 17 |

|

| | | |

| Item 1B. | | 20 |

|

| | | |

| Item 2. | | 20 |

|

| | | |

| Item 3. | | 21 |

|

| | | |

| Item 4. | | 21 |

|

| | | |

| Supp. Item. | | 22 |

|

| PART II |

| Item 5. | | 24 |

|

| | | |

| Item 6. | | 26 |

|

| | | |

| Item 7. | | 27 |

|

| | | |

| Item 7A. | | 59 |

|

| | | |

| Item 8. | | 60 |

|

| | | |

| Item 9. | | 60 |

|

| | | |

| Item 9A. | | 60 |

|

| | | |

| Item 9B. | | 61 |

|

| PART III |

| Item 10. | | 62 |

|

| | | |

| Item 11. | | 65 |

|

| | | |

| Item 12. | | 65 |

|

| | | |

| Item 13. | | 65 |

|

| | | |

| Item 14. | | 65 |

|

| PART IV |

| Item 15. | | 66 |

|

| | |

| 119 |

|

| | |

| 121 |

|

Forward-Looking Statements

This Annual Report on Form 10-K and our other public disclosures, whether written or oral, may contain “forward-looking” statements including, but not limited to: projections of revenue, income, earnings, capital expenditures, dividends, capital structure, cash flows or other financial items; possible plans, goals, objectives, prospects, strategies or trends concerning future operations; statements concerning future economic performance, possible goodwill or other asset impairment; and the underlying assumptions relating to the forward-looking statements. These statements are identified either by the context in which they appear or by use of words such as “anticipate,” “believe,” “estimate,” “expect,” “intend,” “may,” “plan,” “project,” “should” or the like. All such forward-looking statements, whether written or oral, and whether made by us or on our behalf, are expressly qualified by the cautionary statements described in this provision.

Any forward-looking statement reflects only the beliefs of the Company or its management at the time the statement is made. Because all forward-looking statements deal with the future, they are subject to risks, uncertainties and developments which might cause actual events or results to differ materially from those envisioned or reflected in any forward-looking statement. Moreover, we do not have, and do not undertake, any duty to update or revise any forward-looking statement to reflect events or circumstances after the date on which the statement was made. For all of these reasons, forward-looking statements should not be relied upon as a prediction of actual future events, objectives, strategies, trends or results.

Readers should review Item 1A Risk Factors in this Form 10-K for a description of important factors that could cause actual events or results to differ materially from forward-looking statements. It is not possible to anticipate and list all risks, uncertainties and developments which may affect the future operations or performance of the Company, or which otherwise may cause actual events or results to differ materially from forward-looking statements. However, the known, material risks and uncertainties include the following:

| |

| • | factors that could affect the industries or markets in which we participate, such as growth rates and opportunities in those industries; |

| |

| • | adverse changes in inflation, currency, political risk, U.S. or foreign laws or regulations (including tax law changes), consumer sentiment, housing turnover, employment levels, interest rates, trends in capital spending and the like; |

| |

| • | factors that could impact raw materials and other costs, including the availability and pricing of steel scrap and rod and other raw materials, the availability of labor, wage rates and energy costs; |

| |

| • | our ability to pass along raw material cost increases through increased selling prices; |

| |

| • | price and product competition from foreign (particularly Asian and European) and domestic competitors; |

| |

| • | our ability to improve operations and realize cost savings (including our ability to fix under-performing operations and to generate future earnings from restructuring-related activities); |

| |

| • | our ability to maintain profit margins if our customers change the quantity and mix of our components in their finished goods; |

| |

| • | our ability to realize 25-35% contribution margin on incremental unit volume growth; |

| |

| • | our ability to achieve expected levels of cash flow; |

| |

| • | our ability to maintain and grow the profitability of acquired companies; |

| |

| • | our ability to maintain the proper functioning of our internal business processes and information systems and avoid modification or interruption of such systems, through cyber-security breaches or otherwise; |

| |

| • | a decline in the long-term outlook for any of our reporting units that could result in asset impairment; |

| |

| • | our ability to control expenses related to "conflict mineral" regulations and to effectively manage our supply chains to avoid loss of customers; |

| |

| • | decisions from the Department of Commerce and International Trade Commission regarding the extension of antidumping duties on imported mattress innersprings from China, South Africa and Vietnam; and |

| |

| • | litigation including product liability and warranty, taxation, environmental, intellectual property, antitrust, option backdating and workers’ compensation expense. |

PART I

Item 1. Business.

Summary

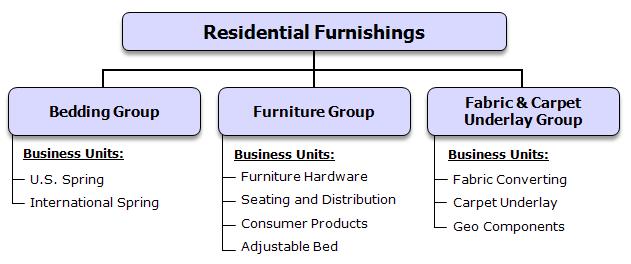

Leggett & Platt, Incorporated was founded as a partnership in Carthage, Missouri in 1883 and was incorporated in 1901. The Company, a pioneer of the steel coil bedspring, has become an international diversified manufacturer that conceives, designs and produces a wide range of engineered components and products found in many homes, offices, retail stores, automobiles and commercial aircraft. As discussed below, our operations are organized into 20 business units, which are divided into 10 groups under our four segments: Residential Furnishings; Commercial Fixturing & Components; Industrial Materials; and Specialized Products.

Overview of Our Segments

Residential Furnishings Segment

Our Residential Furnishings segment began in 1883 with the manufacture of steel coiled bedsprings. Today, we supply a variety of components used by bedding and upholstered furniture manufacturers in the assembly of their finished products. Our range of products offers our customers a single source for many of their component needs.

Efficient manufacturing methods, internal production of key raw materials and machinery, and numerous manufacturing and assembly locations allow us to supply many customers with components at a lower cost than they can produce themselves. In addition to cost savings, sourcing components from us allows our customers to focus on designing, merchandising and marketing their products.

Products

Products manufactured or distributed by our Residential Furnishings groups include:

Bedding Group

| |

| • | Innersprings (sets of steel coils, bound together, that form the core of a mattress) |

| |

| • | Wire forms for mattress foundations |

Furniture Group

| |

| • | Steel mechanisms and hardware (enabling furniture to recline, tilt, swivel, rock and elevate) for reclining chairs and sleeper sofas |

| |

| • | Springs and seat suspensions for chairs, sofas and love seats |

| |

| • | Steel tubular seat frames |

| |

| • | Bed frames, ornamental beds, and “top-of-bed” accessories |

Fabric & Carpet Underlay Group

| |

| • | Structural fabrics for mattresses, residential furniture and industrial uses |

| |

| • | Carpet underlay materials (bonded scrap foam, felt, rubber and prime foam) |

| |

| • | Geo components (synthetic fabrics and various other products used in ground stabilization, drainage protection, erosion and weed control, as well as silt fencing) |

Customers

| |

• | Manufacturers of finished bedding (mattresses and foundations) and upholstered furniture |

| |

• | Retailers and distributors of adjustable and ornamental beds, bed frames and carpet underlay |

| |

| • | Contractors, landscapers, road construction companies and government agencies using geo components |

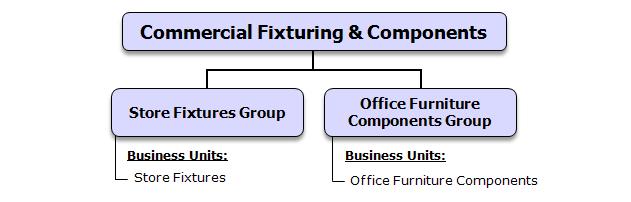

Commercial Fixturing & Components Segment

Our Store Fixtures group designs, produces, installs and manages our customers’ store fixtures projects. Our Office Furniture Components group designs, manufactures, and distributes a wide range of engineered components and products primarily for the office seating market.

Products

Products manufactured or distributed by our Commercial Fixturing & Components groups include:

Store Fixtures Group

| |

| • | Custom-designed, full store fixture packages for retailers, including shelving, counters, showcases and garment racks |

| |

| • | Standardized shelving used by large retailers, grocery stores and discount chains |

Office Furniture Components Group

| |

| • | Bases, columns, back rests, casters and frames for office chairs, and control devices that allow office chairs to tilt, swivel and elevate |

| |

| • | Select lines of private label finished furniture |

Customers

Customers of the Commercial Fixturing & Components segment include:

| |

| • | Retail chains and specialty shops |

| |

| • | Office, institutional and commercial furniture manufacturers |

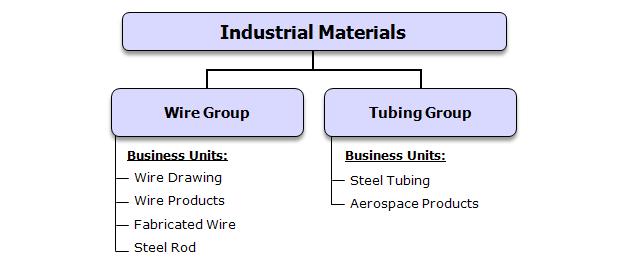

Industrial Materials Segment

We believe that the quality of our products and services, together with low cost, have made us the leading U.S. supplier of drawn steel wire. Our Wire group operates a steel rod mill with an annual output of approximately 500,000 tons, of which a substantial majority is used by our own wire mills. We have four wire mills that supply virtually all the wire consumed by our other domestic businesses. Our Steel Tubing business unit also supplies a portion of our internal needs for welded steel tubing. In addition to supporting our internal requirements, we supply many external customers with wire and steel tubing products.

In 2012, we completed the acquisition of Western Pneumatic Tube (Western). Western is a leading provider of integral components for critical aircraft systems, and formed the Aerospace Products business unit within the Tubing Group. Western specializes in fabricating thin-walled, large diameter, welded tubing and specialty formed products from titanium, nickel and other specialty materials for leading aerospace suppliers and OEMs. In 2013, we expanded our Aerospace Products business unit with the acquisition of two companies. The first was a UK-based business that extended our capability in aerospace tube fabrication. The second was a French-based company that

added small-diameter, high-pressure seamless tubing to our product portfolio. For further information about acquisitions, see Note R on page 109 of the Notes to Consolidated Financial Statements.

Products

Products manufactured or distributed by our Industrial Materials groups include:

Wire Group

| |

| • | Fabricated wire products |

Tubing Group

| |

| • | Fabricated tube components |

| |

| • | Titanium and nickel tubing for the aerospace industry |

Customers

We use about half of our wire output and roughly 15-20% of our steel tubing output to manufacture our own products. For example, we use our wire and steel tubing to make:

| |

| • | Bedding and furniture components |

| |

| • | Motion furniture mechanisms |

| |

| • | Commercial fixtures and shelving |

| |

| • | Automotive seat components |

The Industrial Materials segment also has a diverse group of external customers, including:

| |

| • | Bedding and furniture makers |

| |

| • | Automotive seating manufacturers |

| |

| • | Aerospace suppliers and OEMs |

| |

| • | Mechanical spring makers |

| |

| • | Waste recyclers and waste removal businesses |

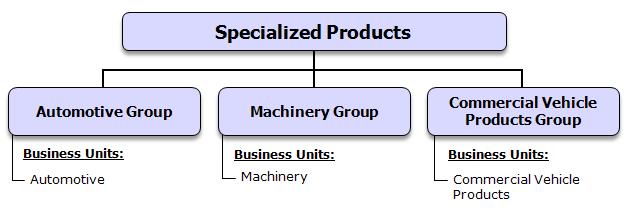

Specialized Products Segment

Our Specialized Products segment designs, produces and sells components for automotive seating, specialized machinery and equipment, and service van interiors. Our established design capability and focus on product development have made us a leader in innovation. We also benefit from our broad geographic presence and our internal production of key raw materials and components.

Products

Products manufactured or distributed by our Specialized Products groups include:

Automotive Group

| |

| • | Manual and power lumbar support and massage systems for automotive seating |

| |

| • | Automotive control cables |

| |

| • | Low voltage motors and motion assemblies |

| |

| • | Formed metal and wire components for seat frames |

Machinery Group

| |

| • | Full range of quilting machines for mattress covers |

| |

| • | Machines used to shape wire into various types of springs |

| |

| • | Industrial sewing/finishing machines |

Commercial Vehicle Products Group

| |

| • | Van interiors (the racks, shelving and cabinets installed in service vans) |

Customers

Our primary customers for the Specialized Products segment include:

| |

| • | Automobile seating manufacturers |

| |

| • | Telecommunication, cable, home service and delivery companies |

Strategic Direction

Key Financial Metric

Total Shareholder Return (TSR), relative to peer companies, is the key financial measure that we use to assess long-term performance. TSR = (Change in Stock Price + Dividends)/Beginning Stock Price). Our goal is to achieve TSR in the top 1/3 of the S&P 500 companies over rolling three-year periods through a balanced approach that employs all four TSR sources: revenue growth, margin expansion, dividends, and share repurchases. For the three-year measurement period that ended December 31, 2013 we generated TSR of 56% (16% per year on average), which placed us in the top one half of the S&P 500.

Our incentive programs reward return generation and profitable growth. Senior executives participate in a TSR-based incentive program (based on our performance compared to a group of approximately 320 peers). Business unit bonuses emphasize the achievement of higher returns on the assets under the unit’s direct control.

Returning Cash to Shareholders

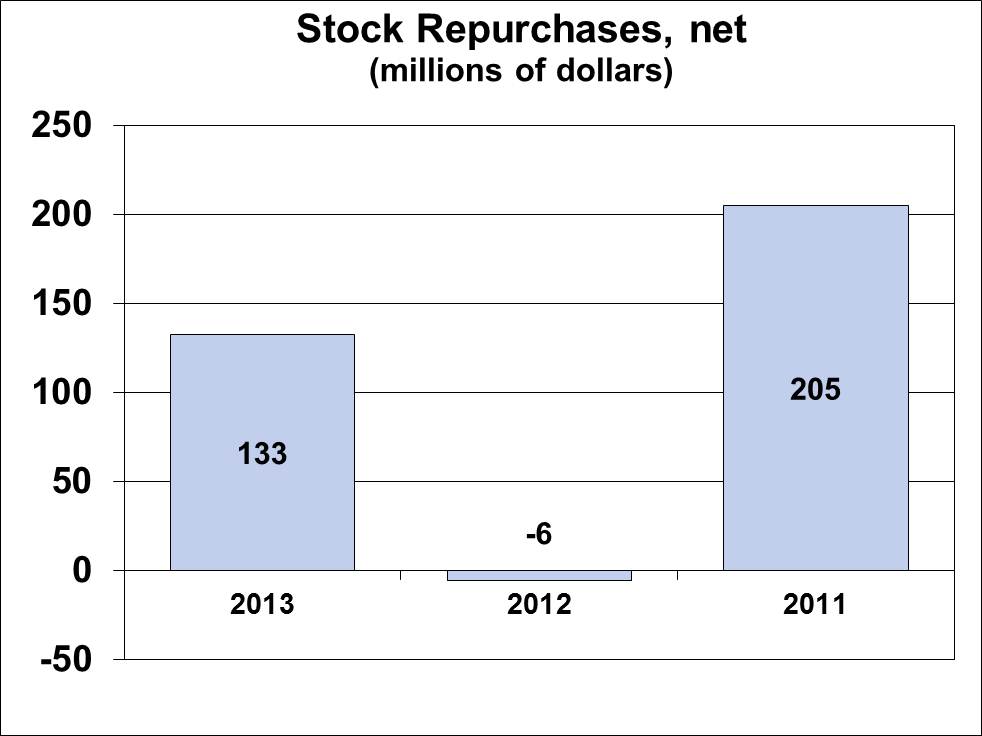

During the past three years, we generated $1.2 billion of operating cash, and we returned much of this cash to shareholders in the form of dividends and share repurchases. Dividends and share repurchases are expected to remain significant contributors to long-term TSR.

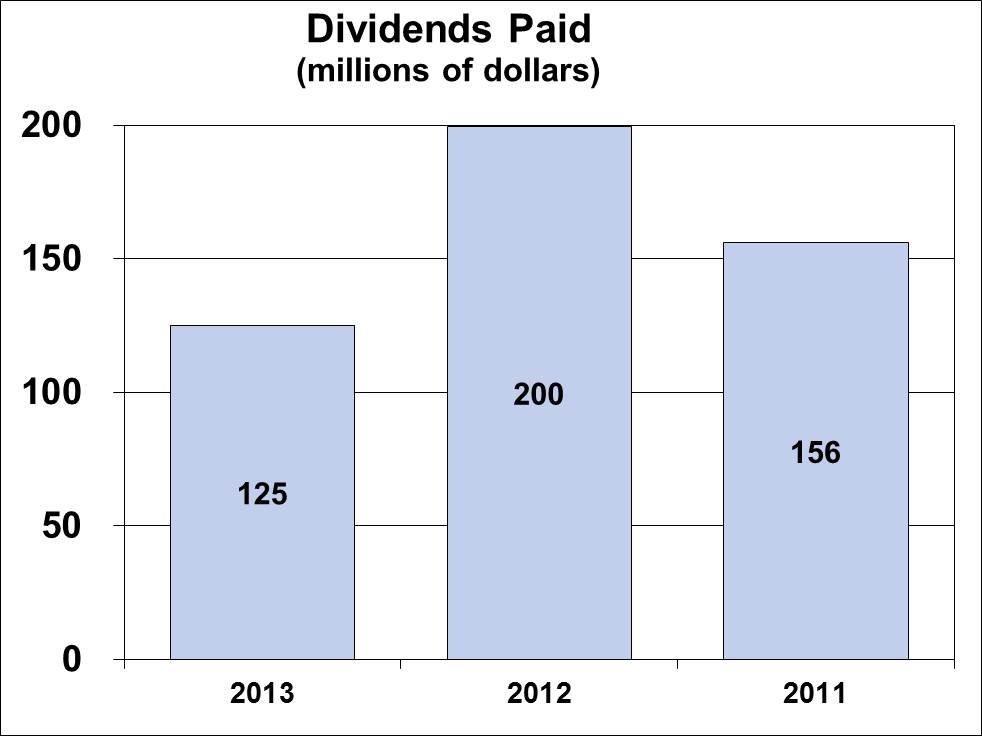

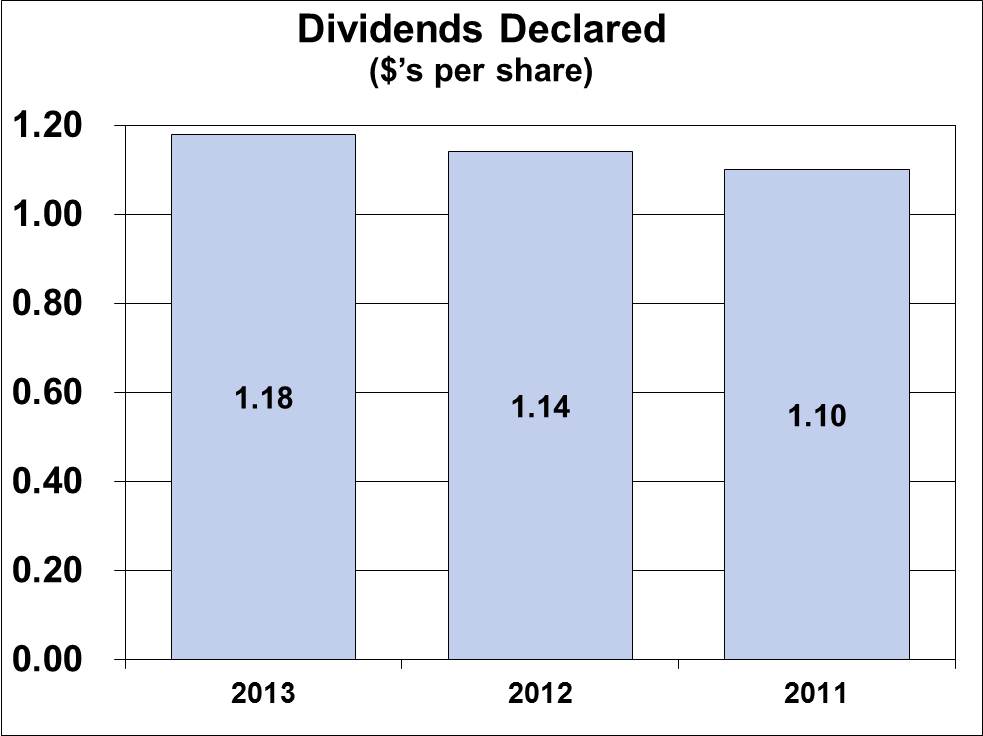

We currently pay a quarterly dividend of $.30 per share. Our dividend payout target is 50-60% of earnings; however we have been above that target in recent years. Our dividend payout ratio (dividends declared per share/earnings per share) was 106%, 67% and 88% in 2011, 2012 and 2013, respectively. As our markets recover, we expect to move into our target payout range. In the meantime, we expect to generate enough cash to continue to pay and modestly grow the dividend. The Company has consistently (for over 20 years) generated operating cash in excess of our annual requirement for capital expenditures and dividends.

We expect to use cash (after repayment of debt and funding capital expenditures, dividends, and growth opportunities) for share repurchases. During the past three years, we have repurchased 18 million shares of our stock (and issued 11 million shares through employee benefit plans), which reduced the net outstanding shares by approximately 5%. In 2013, we repurchased 6 million shares at an average per share price of $30.81 (and issued 3 million shares through employee benefit plans). In 2013, our shares outstanding was reduced by approximately 2% to 139.4 million at year-end.

Portfolio Management

We utilize a rigorous strategic planning process to help guide future decisions regarding business unit roles, capital allocation priorities, and new areas in which to grow. We review the portfolio classification of each unit on an annual basis to determine its appropriate role (Grow, Core, Fix, or Divest). This review includes criteria such as competitive position, market attractiveness, business unit size, and fit within our overall objectives, as well as financial indicators such as growth of EBIT (earnings before interest and taxes) and EBITDA (earnings before interest, taxes, depreciation and amortization), operating cash flows, and return on assets. Business units in the Grow category should provide avenues for profitable growth from competitively advantaged positions in attractive markets. Core business units are expected to enhance productivity, maintain market share, and generate cash flow from operations while using minimal capital. To remain in the portfolio, business units are expected to consistently generate after-tax returns in excess of our cost of capital. Business units that fail to consistently attain minimum return goals will be moved to the Fix or Divest categories.

Disciplined Growth

Long-term, we aim to achieve consistent, profitable growth of 4-5% annually. To attain this goal, we will need to supplement the approximate 2-3% growth that our markets typically produce (in normal economic times) with two additional areas of opportunity. First, we must enhance our success rate at developing and commercializing innovative new products within markets in which we already enjoy strong competitive positions. Second, we need to uncover new growth platforms: opportunities in markets new to us containing margins and growth higher than the Company's average, and in which we would possess a competitive advantage.

Our long-term, 4-5% annual growth objective envisions periodic acquisitions. We seek acquisitions within our Grow businesses, and look for opportunities to enter new, higher growth markets (carefully screened for sustainable competitive advantage). We expect all acquisitions to (a) have a clear strategic rationale, a sustainable competitive advantage, a strong fit with the Company, and be in an attractive and growing market; (b) create value by enhancing Total Shareholder Return; (c) for stand-alone companies: generally, revenue in excess of $50 million, strong management and future growth opportunity with a strong market position in a market growing faster than GDP; and (d) for add-on companies: generally, revenue in excess of $15 million, significant synergies, and a strategic fit with an existing business unit.

Acquisitions

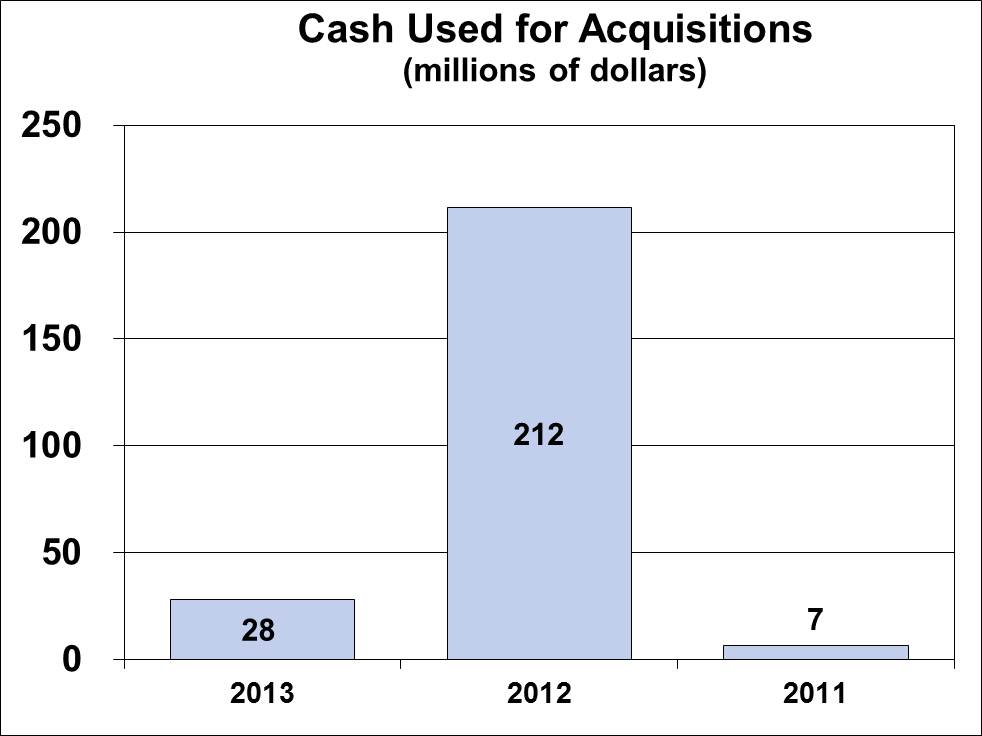

In 2013, we expanded our Aerospace Products business unit with the acquisition of two companies. The first was a UK-based business acquired in May that extended our capability in aerospace tube fabrication. The second was a French-based company acquired in July that added small-diameter, high-pressure seamless tubing to our product portfolio. With these acquisitions, our Aerospace Products business unit, which is part of the Industrial Materials segment, has an annual revenue run rate in excess of $120 million.

In 2012, we acquired for a cash purchase price of $188 million, Western Pneumatic Tube, which produces thin-walled, large diameter, welded tubing and specialty formed products for aerospace applications. Western fabricates products from specialty materials, such as titanium, nickel, stainless steel, and other high strength metals for use in aircraft systems, including fuel, hydraulic, pneumatic, environmental, life support, stability, and cooling systems. Western operates two facilities, one in Kirkland, Washington, and another in Poway, California, and is part of the Aerospace Products business unit.

We had no significant acquisitions in 2011.

For further information about acquisitions, see Note R on page 109 of the Notes to Consolidated Financial Statements.

Divestitures

There were no significant divestitures in 2011, 2012 or 2013.

For further information about divestitures and discontinued operations, see Note B on page 78 of the Notes to Consolidated Financial Statements.

Segment Financial Information

For information about sales to external customers, sales by product line, EBIT, and total assets of each of our segments, refer to Note F on page 84 of the Notes to Consolidated Financial Statements.

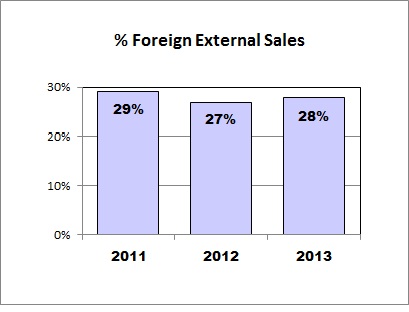

Foreign Operations

The percentages of our external sales related to products manufactured outside the United States for the previous three years are shown below.

Our international operations are principally located in China, Europe, Canada and Mexico. The products we make in these countries primarily consist of:

China

| |

| • | Innersprings for mattresses |

| |

| • | Recliner mechanisms and bases for upholstered furniture |

| |

| • | Formed wire for upholstered furniture |

| |

| • | Retail store fixtures and gondola shelving |

| |

| • | Office furniture components, including chair bases and casters |

| |

| • | Formed metal products, lumbar and seat suspension systems for automotive seating |

| |

| • | Cables and small electric motors used in lumbar systems for automotive seating |

| |

| • | Machinery and replacement parts for machines used in the bedding industry |

Europe

| |

| • | Innersprings for mattresses |

| |

| • | Seamless tubing and specialty formed products for aerospace applications |

| |

| • | Lumbar and seat suspension systems for automotive seating |

| |

| • | Machinery and equipment designed to manufacture innersprings for mattresses and other bedding-related components |

Canada

| |

| • | Fabricated wire for the furniture and automotive industries |

| |

| • | Chair bases, table bases and office chair controls |

| |

| • | Lumbar supports for automotive seats |

| |

| • | Wire and steel storage systems and racks for service vans and utility vehicles |

Mexico

| |

| • | Innersprings and fabricated wire for the bedding industry |

| |

| • | Retail point-of-purchase displays |

| |

| • | Automotive control cable systems and seating components |

| |

| • | Shafts for the appliance industry |

Our international expansion strategy is to locate our operations where we believe we would possess a competitive advantage and where demand for components is growing. Also, in instances where our customers move the production of their finished products overseas, we have located facilities nearby to supply them more efficiently.

Our international operations face the risks associated with any operation in a foreign country. These risks include:

| |

| • | Foreign currency fluctuation |

| |

| • | Foreign legal systems that make it difficult to protect intellectual property and enforce contract rights |

| |

| • | Increased costs due to tariffs, customs and shipping rates |

| |

| • | Potential problems obtaining raw materials, and disruptions related to the availability of electricity and transportation during times of crisis or war |

| |

| • | Inconsistent interpretation and enforcement, at times, of foreign tax laws |

| |

| • | Political instability in certain countries |

Our Specialized Products segment, which derives roughly 76% of its trade sales from foreign operations, is particularly subject to the above risks. These and other foreign-related risks could result in cost increases, reduced profits, the inability to carry on our foreign operations and other adverse effects on our business.

Geographic Areas of Operation

We have manufacturing facilities in countries around the world, as shown below.

|

| | | | | | | |

| | | | | | | | |

| | Residential Furnishings | | Commercial Fixturing & Components | | Industrial Materials | | Specialized Products |

| North America | | | | | | | |

| Canada | n | | n | | | | n |

| Mexico | n | | | | n | | n |

| United States | n | | n | | n | | n |

| Europe | | | | | | | |

| Austria | | | | | | | n |

| Belgium | | | | | | | n |

| Croatia | n | | | | | | n |

| Denmark | n | | | | | | |

| France | | | | | n | | |

| Germany | | | | | | | n |

| Hungary | | | | | | | n |

| Italy | | | n | | | | n |

| Switzerland | | | | | | | n |

| United Kingdom | n | | | | n | | n |

| South America | | | | | | | |

| Brazil | n | | | | | | |

| Asia | | | | | | | |

| China | n | | n | | | | n |

| India | | | | | | | n |

| South Korea | | | | | | | n |

| Africa | | | | | | | |

| South Africa | n | | | | | | |

For further information concerning our external sales related to products manufactured outside the United States and our tangible long-lived assets outside the United States, refer to Note F on page 84 of the Notes to Consolidated Financial Statements.

Sales by Product Line

The following table shows our approximate percentage of external sales by classes of similar products for the last three years:

|

| | | | | | | | | | |

| Product Line | 2013 | | 2012 | | 2011 |

| Furniture Group | 18 | % | | 18 |

| % | | 18 |

| % |

| Bedding Group | 18 | | | 18 |

| | | 18 |

| |

| Fabric & Carpet Underlay Group | 16 | | | 15 |

| | | 15 |

| |

| Automotive Group | 13 | | | 13 |

| | | 12 |

| |

| Wire Group | 12 | | | 12 |

| | | 14 |

| |

| Store Fixtures Group | 7 | | | 8 |

| | | 9 |

| |

| Tubing Group | 5 | | | 4 |

| | | 2 |

| |

| Office Furniture Components Group | 5 | | | 5 |

| | | 5 |

| |

| Machinery Group | 3 | | | 3 |

| | | 3 |

| |

| Commercial Vehicle Products Group | 3 | | | 4 |

| | | 4 |

| |

Distribution of Products

In each of our segments, we sell and distribute our products primarily through our own personnel. However, many of our businesses have relationships and agreements with outside sales representatives and distributors. We do not believe any of these agreements or relationships would, if terminated, have a material adverse effect on the consolidated financial condition, operating cash flows or results of operations of the Company.

Raw Materials

The products we manufacture require a variety of raw materials. We believe that worldwide supply sources are readily available for all the raw materials we use. Among the most important are:

| |

| • | Various types of steel, including scrap, rod, wire, coil, sheet, stainless and angle iron |

| |

| • | Woven and non-woven fabrics |

| |

| • | Titanium and nickel-based alloys and other high strength metals |

We supply our own raw materials for many of the products we make. For example, we produce steel rod that we make into steel wire, which we then use to manufacture:

| |

| • | Innersprings and foundations for mattresses |

| |

| • | Springs and seat suspensions for chairs and sofas |

| |

| • | Automotive seating components |

We supply a substantial majority of our domestic steel rod requirements through our own rod mill. Our wire drawing mills supply nearly all of our U.S. requirements for steel wire. We also produce welded steel tubing, both for our own consumption and for sale to external customers.

Customer Concentration

We serve thousands of customers worldwide, sustaining many long-term business relationships. In 2013, our largest customer accounted for approximately 6% of our consolidated revenues. Our top 10 customers accounted for approximately 23% of these consolidated revenues. The loss of one or more of these customers could have a

material adverse effect on the Company, as a whole, or on the respective segment in which the customer’s sales are reported, including our Residential Furnishings, Commercial Fixturing & Components and Specialized Products segments.

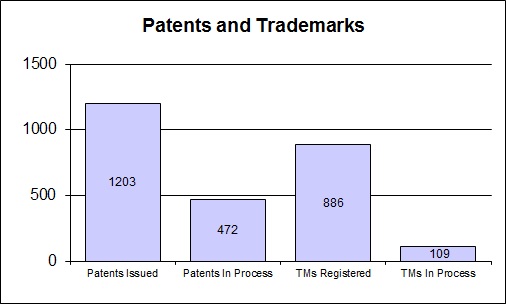

Patents and Trademarks

The chart below shows the approximate number of patents issued, patents in process, trademarks registered and trademarks in process held by our operations as of December 31, 2013. No single patent or group of patents, or trademark or group of trademarks, is material to our operations, as a whole. Most of our patents relate to products sold in the Specialized Products segment, while a substantial majority of our trademarks relate to products sold in the Residential Furnishings and Specialized Products segments.

Some of our most significant trademarks include:

| |

| • | Semi-Flex® (box spring components and foundations) |

| |

| • | Mira-Coil®, VertiCoil®, Lura-Flex®, Superlastic® and Comfort Core® (mattress innersprings) |

| |

| • | Active Support Technology® (mattress innersprings) |

| |

| • | Wall Hugger® (recliner chair mechanisms) |

| |

| • | Super Sagless® (motion and sofa sleeper mechanisms) |

| |

| • | No-Sag® (wire forms used in seating) |

| |

| • | Tack & Jump® and Pattern Link® (quilting machines) |

| |

| • | Hanes® (fiber materials) |

| |

| • | Schukra®, Pullmaflex® and Flex-O-Lator® (automotive seating products) |

| |

| • | Spuhl® (mattress innerspring manufacturing machines) |

| |

| • | Gribetz® and Porter® (quilting and sewing machines) |

| |

| • | Quietflex® and Masterack® (equipment and accessories for vans and trucks) |

Research and Development

We maintain research, development and testing centers in Carthage, Missouri and at many of our other facilities. We are unable to calculate precisely the cost of research and development because the personnel involved

in product and machinery development also spend portions of their time in other areas. However, we estimate the cost of research and development was $20 million in 2011, $22 million in 2012 and $24 million in 2013.

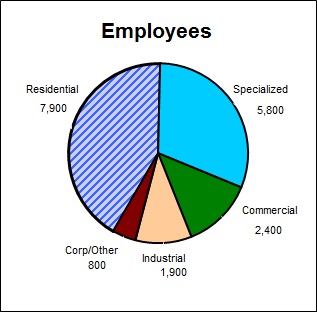

Employees

As of December 31, 2013, we had approximately 18,800 employees, of which roughly 13,200 were engaged in production. Of the 18,800, approximately 9,100 were international employees (5,200 in China). Roughly 14% of our employees are represented by labor unions that collectively bargain for work conditions, wages or other issues. We did not experience any material work stoppage related to contract negotiations with labor unions during 2013. Management is not aware of any circumstances likely to result in a material work stoppage related to contract negotiations with labor unions during 2014. The chart below shows the approximate number of employees by segment.

As of December 31, 2012, we had approximately 18,300 employees.

Competition

Many companies offer products that compete with those we manufacture and sell. The number of competing companies varies by product line, but many of the markets for our products are highly competitive. We tend to attract and retain customers through product quality, innovation, competitive pricing and customer service. Many of our competitors try to win business primarily on price but, depending upon the particular product, we experience competition based on quality, performance and availability as well. In general, our competitors tend to be smaller, private companies.

We believe we are the largest U.S. manufacturer, in terms of revenue, of the following:

| |

| • | Components for residential furniture and bedding |

| |

| • | Components for office furniture |

| |

| • | Automotive seat support and lumbar systems |

| |

| • | Bedding industry machinery for wire forming, sewing and quilting |

| |

| • | Thin-walled, titanium, nickel and other specialty tubing for the aerospace industry |

We continue to face pressure from foreign competitors as some of our customers source a portion of their components and finished products offshore. In addition to lower labor rates, foreign competitors benefit (at times) from lower raw material costs. They may also benefit from currency factors and more lenient regulatory climates. We typically remain price competitive, even versus many foreign manufacturers, as a result of our efficient operations, low labor content, vertical integration in steel and wire, logistics and distribution efficiencies, and large scale purchasing of raw materials and commodities. However, we have also reacted to foreign competition in certain cases, by selectively adjusting prices, and by developing new proprietary products that help our customers reduce total costs.

Premium non-innerspring mattresses (those that have either a foam or air core) experienced rapid growth in the U.S. bedding market in recent years. These products represent a relatively small portion of the bedding market in units (approximately 10%-12%), but comprise a larger portion of the market in dollars (approximately 25%-30%) due to their higher average selling prices. In 2013, non-innerspring mattress sales declined and the proportion of the total bedding market that they represent also decreased. Most traditional bedding manufacturers (who are our customers) now offer mattresses that combine an innerspring core with top layers comprised of specialty foam and gel. These hybrid products, which allow our customers to address a consumer preference for the feel of a specialty mattress and the characteristics of an innerspring, have been well received by consumers.

For the past five years, there have been antidumping duty orders on innerspring imports from China, South Africa and Vietnam, ranging from 116% to 234%. The orders remain in effect while the Department of Commerce (DOC) and the International Trade Commission (ITC) conduct separate reviews to determine whether to extend the duties through February 2019 (for China) and December 2018 (for South Africa and Vietnam). If it is determined that the revocation of the duties would likely lead to the continuation or recurrence of dumping of innersprings (determined by the DOC) and material injury to the U.S. innerspring industry (determined by the ITC), the duties will be extended. We believe that, without the extension, it is likely that dumping will recur and the U.S. innerspring industry will be materially injured. As a result, we are actively participating in the DOC and ITC reviews. We expect the DOC and ITC to issue their respective determinations in March 2014. If the duties are not extended, they will be retroactively revoked to February 2014 (for China) and December 2013 (for South Africa and Vietnam).

In addition, because of the documented evasion of antidumping orders by shipping of goods through third countries and falsely identifying the countries of origin, Leggett, along with several U.S. manufacturers have formed a coalition and are working with members of Congress, the DOC, and U.S. Customs and Border Protection to seek stronger enforcement of existing antidumping and/or countervailing duty orders.

Seasonality

As a diversified manufacturer, we generally have not experienced significant seasonality. The timing of acquisitions, dispositions, and economic factors in any year can distort the underlying seasonality in certain of our businesses. Historically, for the Company as a whole, the second and third quarters typically have proportionately greater sales, while the first and fourth quarters are generally lower.

| |

| • | Residential Furnishings: typically does not exhibit any significant seasonality, except for a reduction in fourth quarter sales. |

| |

| • | Commercial Fixturing & Components: generally has stronger third quarter sales of its store fixture products, with the fourth quarter significantly lower. This aligns with the retail industry’s normal construction cycle—the opening of new stores and completion of remodeling projects in advance of the holiday season. |

| |

| • | Industrial Materials: minimal variation in sales throughout the year. |

| |

| • | Specialized Products: relatively little quarter-to-quarter variation in sales, although the automotive business is typically somewhat heavier in the second and fourth quarters of the year and lower in the third quarter due to model changeovers and plant shutdowns in the automobile industry during the summer. |

Backlog

Our customer relationships and our manufacturing and inventory practices do not create a material amount of backlog orders for any of our segments. Production and inventory levels are geared primarily to the level of incoming orders and projected demand based on customer relationships.

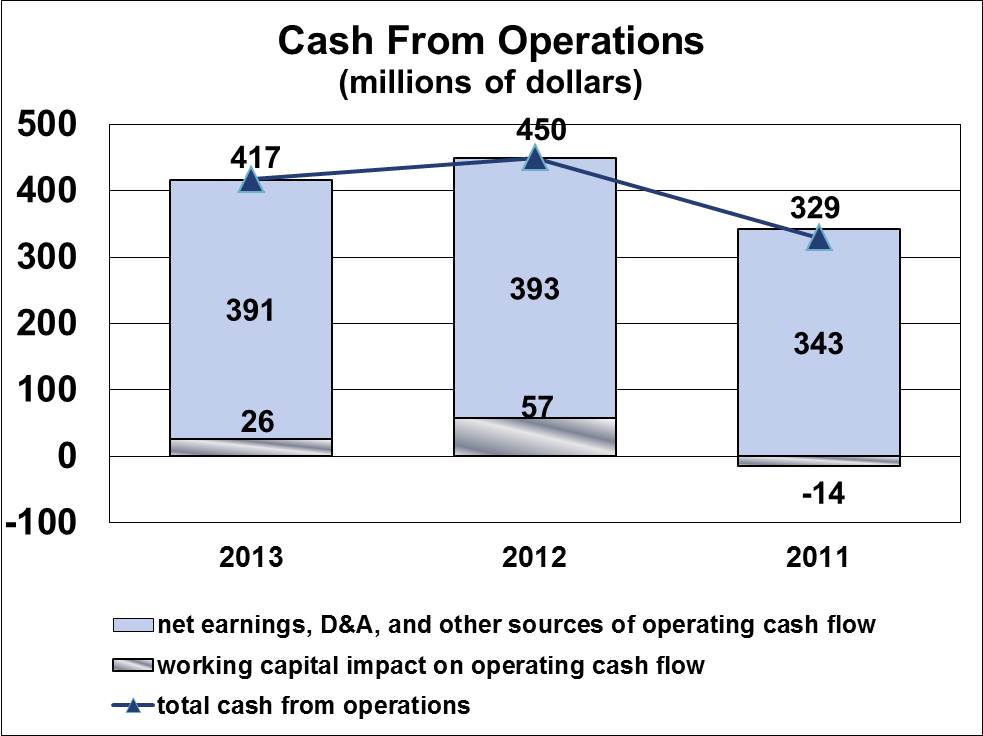

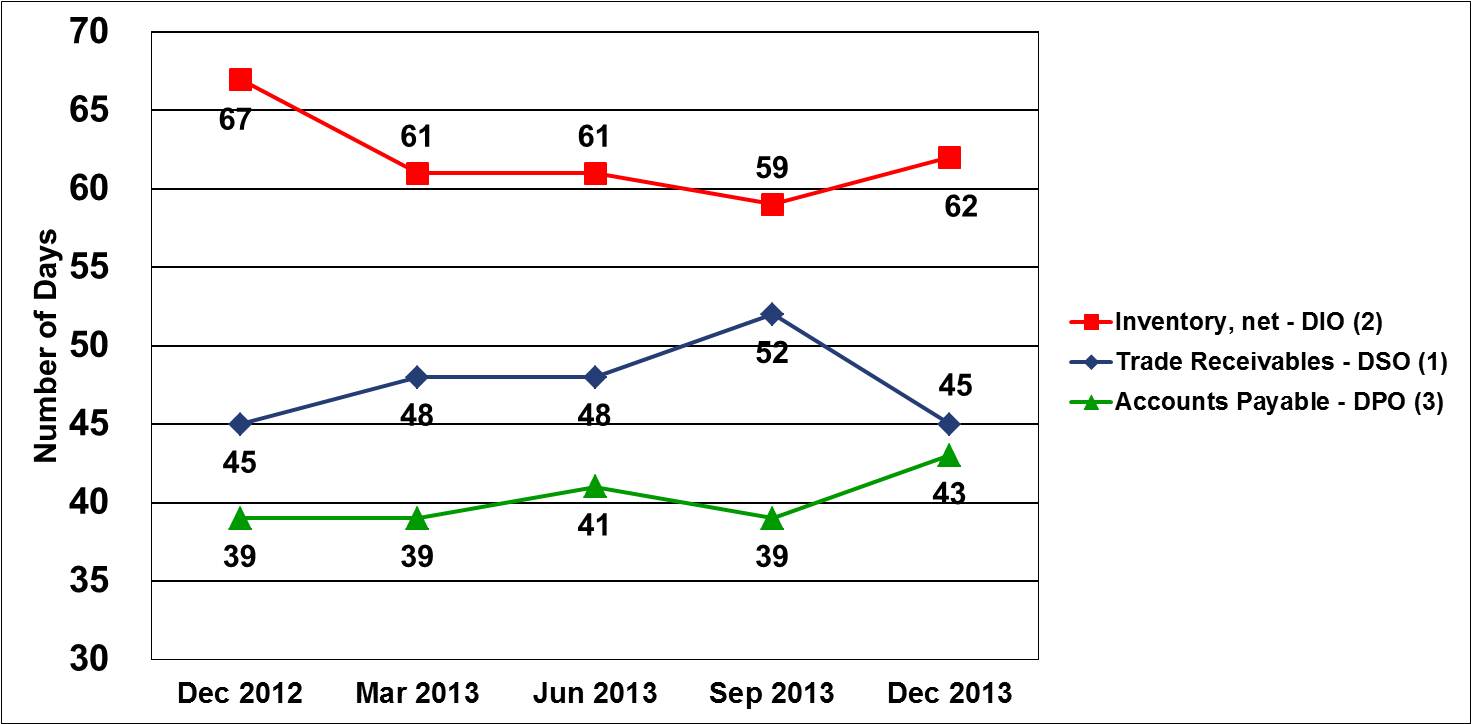

Working Capital Items

For information regarding working capital items, see the discussion of “Cash from Operations” in Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations on page 39.

Government Contracts

The Company does not have a material amount of sales derived from Government contracts subject to renegotiation of profits or termination at the election of any Government.

Environmental Regulation

Our operations are subject to federal, state, and local laws and regulations related to the protection of the environment. We have policies intended to ensure that our operations are conducted in compliance with applicable laws. While we cannot predict policy changes by various regulatory agencies, management expects that compliance with these laws and regulations will not have a material adverse effect on our competitive position, capital expenditures, financial condition, liquidity or results of operations.

Internet Access to Information

We routinely post information for investors to our website (www.leggett.com) under the Investor Relations section. Our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and all amendments to those reports are made available, free of charge, on our website as soon as reasonably practicable after electronically filed with, or furnished to, the SEC. In addition to these reports, the Company’s Financial Code of Ethics, Code of Business Conduct and Ethics, and Corporate Governance Guidelines, as well as charters for the Audit, Compensation, and Nominating & Corporate Governance Committees of our Board of Directors, can be found on our website under the Corporate Governance section. Information contained on our website does not constitute part of this Annual Report on Form 10-K.

Discontinued Operations

Some of our prior businesses are disclosed in our annual financial statements as discontinued operations since (i) the operations and cash flows of the businesses were clearly distinguished and have been or will be

eliminated from our ongoing operations; (ii) the businesses have either been disposed of or are classified as held for sale; and (iii) we will not have any significant continuing involvement in the operations of the businesses after the disposal transactions.

For information on discontinued operations, see Note B on page 78 of the Notes to Consolidated Financial Statements.

Item 1A. Risk Factors.

Investing in our securities involves risk. Set forth below and elsewhere in this report are risk factors that could cause actual results to differ materially from the results contemplated by the forward-looking statements contained in this report. We may amend or supplement these risk factors from time to time by other reports we file with the SEC.

We have exposure to economic and other factors that affect market demand for our products which may negatively impact our sales, operating cash flow and earnings.

As a supplier of products to a variety of industries, we are adversely affected by general economic downturns. Our operating performance is heavily influenced by market demand for our components and products. Market demand for the majority of our products is most heavily influenced by consumer confidence. To a lesser extent, market demand is impacted by other broad economic factors, including disposable income levels, employment levels, housing turnover and interest rates. All of these factors influence consumer spending on durable goods, and drive demand for our components and products. Some of these factors also influence business spending on facilities and equipment, which impacts approximately one-third of our sales.

Demand weakness in our markets can lead to lower unit orders, sales and earnings in our businesses. Several factors, including a weak global economy, a depressed housing market, or low consumer confidence could contribute to conservative spending habits by consumers around the world. Short lead times in most of our markets allow for limited visibility into demand trends. Many consumers continue to postpone spending on larger ticket items such as bedding and furniture. If economic and market conditions deteriorate, we may experience material negative impacts on our business, financial condition, operating cash flows and results of operations.

Costs of raw materials could negatively affect our profit margins and earnings.

Raw material cost increases (and our ability to respond to cost increases through selling price increases) can significantly impact our earnings. We typically have short-term commitments from our suppliers; therefore, our raw material costs generally move with the market. When we experience significant increases in raw material costs, we typically implement price increases to recover the higher costs. Inability to recover cost increases (or a delay in the recovery time) can negatively impact our earnings. Conversely, if raw material costs decrease, we generally pass through reduced selling prices to our customers. Reduced selling prices combined with higher cost inventory can reduce our segment margins and earnings.

Steel is our principal raw material. The global steel markets are cyclical in nature and have been volatile in recent years. This volatility can result in large swings in pricing and margins from year to year. In late 2013, steel costs increased unexpectedly, and the timing of the increase (late in the year) resulted in a concentration of LIFO expense in the fourth quarter. We are implementing price increases in early 2014 to recover these higher costs. Our operations can also be impacted by changes in the cost of fabrics and foam scrap. We experienced significant fluctuations in the cost of these commodities in recent years.

As a producer of steel rod, we are also impacted by volatility in metal margins (the difference in the cost of steel scrap and the market price for steel rod). In the later half of 2013, metal margins within our rod production operation were compressed due to downward pressure on steel rod prices from Chinese imports. Also, if scrap costs

raise more rapidly than the price of steel rod, the metal margins will be compressed. In either instance, compressed metal margins could negatively impact our result of operations.

Higher raw material costs in recent years led some of our customers to modify their product designs, changing the quantity and mix of our components in their finished goods. In some cases, higher cost components were replaced with lower cost components. This primarily impacted our Residential Furnishings and Industrial Materials product mix and decreased profit margins. This trend could further negatively impact our results of operations.

Competition could adversely affect our market share, sales, profit margins and earnings.

We operate in markets that are highly competitive. We believe that most companies in our lines of business compete primarily on price, but, depending upon the particular product, we experience competition based on quality, performance and availability as well. We face ongoing pressure from foreign competitors as some of our customers source a portion of their components and finished products from Asia and Europe. In addition to lower labor rates, foreign competitors benefit (at times) from lower raw material costs. They may also benefit from currency factors and more lenient regulatory climates. If we are unable to purchase key raw materials, such as steel, at prices competitive with those of foreign suppliers, our ability to maintain market share and profit margins could be harmed by foreign competitors.

Premium non-innerspring mattresses (those that have either a foam or air core) have experienced rapid growth in the U.S. bedding market in recent years. While still a relatively small portion of the total market in units (approximately 10%-12%), these products represent a much larger portion of the total market in dollars (approximately 25%-30%) due to their higher average selling prices. If sales of foam or air core mattresses continue to grow appreciably, it could reduce our market share in the U.S. bedding market, and negatively impact our sales and earnings.

The revocation of duties on imports of innersprings from China, South Africa and Vietnam could reduce our market share, sales, profit margins and earnings.

For the past five years, there have been antidumping duty orders on innerspring imports from China, South Africa and Vietnam, ranging from 116% to 234%. The orders remain in effect while the Department of Commerce (DOC) and the International Trade Commission (ITC) conduct separate reviews to determine whether to extend the duties through early 2019 (for China) and late 2018 (for South Africa and Vietnam). If it is determined that the revocation of the duties would likely lead to the continuation or recurrence of dumping of innersprings (determined by the DOC) and material injury to the U.S. innerspring industry (determined by the ITC), the duties will be extended. We believe that, without the extension, it is likely that dumping will recur and the U.S. innerspring industry will be materially injured. As a result, we are actively participating in the DOC and ITC reviews. We expect the DOC and ITC to issue their respective determinations in March 2014. If the DOC and ITC revoke the duties it could reduce our share in the innersprings market, our sales, profit margins and earnings.

Our goodwill and other long-lived assets are subject to potential impairment which could negatively impact our earnings.

A significant portion of our assets consists of goodwill and other long-lived assets, the carrying value of which may be reduced if we determine that those assets are impaired. At December 31, 2013, goodwill and other intangible assets represented approximately $1.1 billion, or approximately 36% of our total assets. In addition, net property, plant and equipment and sundry assets totaled approximately $696 million, or approximately 22% of total assets. If actual results differ from the assumptions and estimates used in the goodwill and long-lived asset valuation calculations, we could incur impairment charges, which could negatively impact our earnings.

We review our ten reporting units for potential goodwill impairment in June as part of our annual goodwill impairment testing, and more often if an event or circumstance occurs making it likely that impairment exists. In addition, we test for the recoverability of long-lived assets at year end, and more often if an event or circumstance

indicates the carrying value may not be recoverable. We conduct impairment testing based on our current business strategy in light of present industry and economic conditions, as well as future expectations. The annual goodwill impairment review performed in June 2013 indicated no goodwill impairments, but fair market value for one of our ten reporting units (Store Fixtures) exceeded book value by approximately 18%. The goodwill associated with the Store Fixtures reporting unit was approximately $109 million at December 31, 2013. The unit is dependent upon capital spending by retailers on both new stores and remodeling of existing stores. Although 2012 performance was better than expected, 2013 fell short of expectations. The predictability of future results is less certain than that of our other reporting units due to the project nature of this business. If we are not able to achieve projected performance levels in Store Fixtures, future impairments could be possible, which would negatively impact our earnings.

We had been reviewing the Commercial Vehicle Products (CVP) group, which is part of the Specialized Products segment, as part of our ongoing strategic planning process with one possible strategic alternative being to divest all or part of the group. During this process, an unexpected decline in CVP group sales, earnings and operating cash flows occurred. Consequently, we received a lower than previously expected indication of value relating to the potential disposition of the business. As a result, we conducted an interim valuation of the CVP group goodwill and other long-lived assets and, in December, concluded that an impairment charge was required primarily relating to goodwill of the CVP group. We recorded a goodwill impairment charge of $63 million in the fourth quarter. A further decline in the CVP group business could result in future impairments which would negatively impact our earnings.

We are exposed to foreign currency risk which may negatively impact our competitiveness, profit margins and earnings.

We expect that international sales will continue to represent a significant percentage of our total sales, which exposes us to currency exchange rate fluctuations. In 2013, 28% of our sales were generated by international operations. The revenues and expenses of our foreign operations are generally denominated in local currencies; however, certain of our operations experience currency-related gains and losses where sales or purchases are denominated in currencies other than their local currency. Further, our competitive position may be affected by the relative strength of the currencies in countries where our products are sold. Foreign currency exchange risks inherent in doing business in foreign countries may have a material adverse effect on our future operations and financial results.

Technology failures or cyber security breaches could have a material adverse effect on our operations.

We rely on information systems to obtain, process, analyze and manage data, as well as to facilitate the manufacture and distribution of inventory to and from our facilities. We receive, process and ship orders, manage the billing of, and collections from, our customers, and manage the accounting for, and payment to, our vendors. Security breaches of this infrastructure can create system disruptions or unauthorized disclosure of confidential information. If this occurs, our operations could be disrupted, or we may suffer financial loss because of lost or misappropriated information. We cannot be certain that advances in criminal capabilities or new discoveries in the field of cryptography will not compromise our technology protecting information systems. If these systems are interrupted or damaged by these events or fail for any extended period of time, then our results of operations could be adversely affected.

We may not be able to realize deferred tax assets on our balance sheet depending upon the amount and source of future taxable income.

Our ability to realize deferred tax assets on our balance sheet is dependent upon the amount and source of future taxable income. Economic uncertainty or tax law changes could impact our underlying assumptions on which valuation reserves are established and negatively affect future period earnings and balance sheets.

We are exposed to legal contingencies related to various lawsuits and other claims that, if realized, could have a material negative impact on our earnings and cash flows.

We are a defendant in various legal proceedings, including antitrust lawsuits related to the alleged price fixing of prime foam and carpet underlay products, and other proceedings and claims. When it is probable, in management's judgment, that we may incur monetary damages or other costs resulting from these proceedings or other claims, and we can reasonably estimate the amounts, we record appropriate liabilities in the financial statements and make charges against earnings. If our assumptions or analysis regarding these contingencies is incorrect, we could incur damages which could have a material negative impact on our earnings and cash flows.

Item 1B. Unresolved Staff Comments.

None.

Item 2. Properties.

The Company’s corporate office is located in Carthage, Missouri. We currently have 131 manufacturing locations, of which 85 are located across the United States and 46 are located in 17 foreign countries. We also have various sales, warehouse and administrative facilities. However, our manufacturing plants are our most important properties.

Manufacturing Locations by Segment

|

| | | | | | | | | | |

| | | Company- Wide | | Subtotals by Segment |

| Manufacturing Locations | | Residential Furnishings | | Commercial Fixturing & Components | | Industrial Materials | | Specialized Products |

| United States | | 85 | | 50 | | 10 | | 12 | | 13 |

| Europe | | 17 | | 3 | | 1 | | 3 | | 10 |

| Asia | | 14 | | 4 | | 2 | | — | | 8 |

| Canada | | 8 | | 2 | | 2 | | — | | 4 |

| Mexico | | 5 | | 2 | | — | | 1 | | 2 |

| Other | | 2 | | 2 | | — | | — | | — |

| Total | | 131 | | 63 | | 15 | | 16 | | 37 |

__________________________________________________________

Manufacturing locations that we own produced approximately 70% of our sales in 2013. We also lease many of our manufacturing, warehouse and other facilities on terms that vary by lease (including purchase options, renewals and maintenance costs). For additional information regarding lease obligations, see Note K on page 92 of the Notes to Consolidated Financial Statements.

In the opinion of management, the Company’s owned and leased facilities are suitable and adequate for the manufacture, assembly and distribution of our products. Our properties are located to allow quick and efficient delivery of products and services to our diverse customer base. Our productive capacity, in general, continues to exceed current operating levels. With our current utilization levels, we should be able to increase unit sales by approximately $400 million (based on current sales mix) without the need for large capital investment.

Item 3. Legal Proceedings.

The information in Note T beginning on page 113 of the Notes to Consolidated Financial Statements is incorporated into this section by reference.

Environmental Matter Involving Potential Monetary Sanctions of $100,000 or More

On March 27, 2013, Region 5 of the U.S. Environmental Protection Agency issued a Notice of Violation("NOV") alleging that our subsidiary, Sterling Steel Company, violated the Clean Air Act and the Illinois State Implementation Plan currently in place. Sterling operates a steel rod mill in Sterling, Illinois. The NOV alleges that Sterling, since 2008, has exceeded the allowable annual particulate matter and manganese emission limits for its arc furnace. Sterling requested a conference with the EPA to discuss the alleged violations. The conference was held on May 20, 2013.

On July 23, 2013, the EPA issued a Finding of Violation alleging that Sterling violated the opacity limitations of its air permit and Federal and state regulations. A conference to discuss the Finding of Violation occurred in the third quarter.

Sterling intends to vigorously defend these matters in any enforcement action that may be pursued by the EPA. The EPA did not specify any amount of penalty or injunctive relief being sought in the NOV, Finding of Violation or in any conference. Any settlement or adverse finding could result in the payment by Sterling of fines, penalties, capital expenditures, or some combination thereof. Although the outcome of these matters cannot be predicted with certainty, we do not expect them, either individually or in the aggregate, to have a material adverse effect on our financial position, cash flows or results of operations.

Sunset Review Regarding Extension of Antidumping Duties on Innerspring Imports

For the past five years, there have been antidumping duty orders on innerspring imports from China, South Africa and Vietnam, ranging from 116% to 234%. The orders remain in effect while the U.S. Department of Commerce (DOC) and the International Trade Commission (ITC) each conduct separate reviews (one for each country) to determine whether to extend the duties through February 2019 (for China) and December 2018 (for South Africa and Vietnam). The DOC reviews (Case Nos. A-570-928; A-791-821; and A-552-803) and ITC reviews (Investigation Nos. 731-TA-1140; 731-TA-1141; and 731-TA-1142) were self-initiated on November 1, 2013. We filed three Statements of Intent to Participate in the DOC reviews on December 2, 2013 (one for each country). We also filed a Statement of Willingness to Participate in the ITC reviews on December 2, 2013 (one collective filing).

If it is determined that the revocation of the duties would likely lead to the continuation or recurrence of dumping of innersprings (determined by the DOC) and material injury to the U.S. innerspring industry (determined by the ITC), the duties will be extended. We have argued that, without the extension, it is likely that dumping will recur, the U.S. innerspring industry will be materially injured, and, as such, the duty orders should be extended. If the orders are revoked, the revocation would occur retroactively to February 19, 2014 (for China) and December 10, 2013 (for South Africa and Vietnam). We expect the DOC and ITC to issue their respective determinations in March 2014.

Item 4. Mine Safety Disclosures.

Not applicable.

Supplemental Item. Executive Officers of the Registrant.

The following information is included in accordance with the provisions of Part III, Item 10 of Form 10-K and Item 401(b) of Regulation S-K.

The table below sets forth the names, ages and positions of all executive officers of the Company. Executive officers are normally appointed annually by the Board of Directors.

|

| | | | |

| Name | | Age | | Position |

| David S. Haffner | | 61 | | Board Chair and Chief Executive Officer |

| Karl G. Glassman | | 55 | | President and Chief Operating Officer |

| Matthew C. Flanigan | | 52 | | Executive Vice President and Chief Financial Officer |

| Jack D. Crusa | | 59 | | Senior Vice President, Specialized Products |

| Perry E. Davis | | 54 | | Senior Vice President, Residential Furnishings |

| David M. DeSonier | | 55 | | Senior Vice President, Strategy & Investor Relations |

| Scott S. Douglas | | 54 | | Senior Vice President, General Counsel |

| Joseph D. Downes, Jr. | | 69 | | Senior Vice President, Industrial Materials |

| John G. Moore | | 53 | | Senior Vice President, Chief Legal & HR Officer and Secretary |

| Dennis S. Park | | 59 | | Senior Vice President, Commercial Fixturing & Components |

| William S. Weil | | 55 | | Vice President, Corporate Controller and Chief Accounting Officer |

______________________________

Subject to the employment and severance benefit agreements with Mr. Haffner, Mr. Glassman and Mr. Flanigan, listed as exhibits to this Report, the executive officers generally serve at the pleasure of the Board of Directors. Our employment agreement with Mr. Haffner provides that he may terminate the agreement if not nominated as a director and appointed to the Board's executive committee. Employment agreements with Mr. Glassman and Mr. Flanigan provide that they may terminate their agreements if not nominated as a director of the Company. In addition, each may terminate their respective agreement if not elected to their current executive officer position. See Exhibit Index on page 122 for reference to the agreements.

David S. Haffner was elected Board Chair of the Company in 2013 and continues to serve as Chief Executive Officer since his appointment in 2006. He previously served as President from 2002 to 2013, Chief Operating Officer from 1999 to 2006, and as Executive Vice President from 1995 to 2002. He has served the Company in various capacities since 1983.

Karl G. Glassman was appointed President of the Company in 2013 and has served as Chief Operating Officer since 2006. He previously served as Executive Vice President from 2002 to 2013, President of Residential Furnishings from 1999 to 2006, Senior Vice President from 1999 to 2002 and in various capacities since 1982.

Matthew C. Flanigan was appointed Executive Vice President of the Company in 2013 and has served as Chief Financial Officer since 2003. He previously served as Senior Vice President from 2005 to 2013, Vice President from 2003 to 2005, President of the Office Furniture Components Group from 1999 to 2003 and in various capacities since 1997.

Jack D. Crusa was appointed Senior Vice President in 1999 and President of Specialized Products in 2004. He previously served as President of Industrial Materials from 1999 to 2004, and President of the Automotive Group from 1996 to 1999. He has served the Company in various capacities since 1986.

Perry E. Davis was appointed Senior Vice President and President of Residential Furnishings in 2012. He previously served as Vice President of the Company, President—Bedding Group from 2006 to 2012, as Vice President of the Company, Executive VP of the Bedding Group and President—U.S. Spring beginning in 2005. He also served as Executive VP of the Bedding Group and President—U.S. Spring from 2004 to 2005, President—Central Division Bedding Group from 2000 to 2004, and in various capacities since 1981.

David M. DeSonier was appointed Senior Vice President—Strategy & Investor Relations in 2011. He previously served as Vice President—Strategy & Investor Relations from 2007 to 2011 and served as Vice President—Investor Relations and Assistant Treasurer from 2002 to 2007. He joined the Company as Vice President—Investor Relations in 2000.

Scott S. Douglas was appointed Senior Vice President—General Counsel in 2011. He previously served the Company as Vice President beginning in 2008, and General Counsel beginning in 2010. He also served as Vice President—Law and Deputy General Counsel from 2008 to 2010, Associate General Counsel—Mergers & Acquisitions from 2001 to 2007, and Assistant General Counsel from 1991 to 2001. He has served the Company in various legal capacities since 1987.

Joseph D. Downes, Jr. was appointed Senior Vice President of the Company in 2005 and President of the Industrial Materials Segment in 2004. He previously served the Company as President of the Wire Group from 1999 to 2004 and in various capacities since 1976.

John G. Moore was appointed Senior Vice President, Chief Legal and HR Officer and Secretary in 2011. He was appointed Secretary in 2010, Chief Legal and HR Officer in 2009 and Vice President—Corporate Affairs & Human Resources in 2008. He served as Vice President—Corporate Governance from 2006 to 2008, Vice President and Associate General Counsel from 2001 to 2006, and as Managing Counsel and Assistant General Counsel from 1998 to 2001. He has served the Company in various legal capacities since 1993.

Dennis S. Park was appointed Senior Vice President and President of Commercial Fixturing & Components in 2006. He previously served as Vice President and President of Home Furniture and Consumer Products from 2004 to 2006, and Vice President and President of Home Furniture Components from 1996 to 2004. He has served the Company in various capacities since 1977.

William S. Weil was appointed Chief Accounting Officer in 2004, Vice President in 2000 and Corporate Controller in 1991. He previously served the Company in various other accounting capacities since 1983.

PART II

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

Our common stock is traded on the New York Stock Exchange (symbol LEG). The table below highlights quarterly and annual stock market information for the last two years.

|

| | | | | | | | | | | | | | |

| | Price Range | | Volume of Shares Traded (in Millions) | | Dividend Declared |

| | High | | Low | |

| 2013 | | | | | | | |

| First Quarter | $ | 33.80 |

| | $ | 27.24 |

| | 74.0 |

| | $ | 0.29 |

|

| Second Quarter | 34.28 |

| | 29.59 |

| | 74.7 |

| | 0.29 |

|

| Third Quarter | 32.52 |

| | 28.59 |

| | 63.1 |

| | 0.30 |

|

| Fourth Quarter | 31.33 |

| | 28.00 |

| | 65.2 |

| | 0.30 |

|

| For the Year | $ | 34.28 |

| | $ | 27.24 |

| | 277.0 |

| | $ | 1.18 |

|

| 2012 | | | | | | | |

| First Quarter | $ | 23.73 |

| | $ | 21.26 |

| | 119.0 |

| | $ | 0.28 |

|

| Second Quarter | 23.98 |

| | 19.26 |

| | 129.9 |

| | 0.28 |

|

| Third Quarter | 25.24 |

| | 20.50 |

| | 107.9 |

| | 0.29 |

|

| Fourth Quarter | 27.89 |

| | 24.35 |

| | 84.8 |

| | 0.29 |

|

| For the Year | $ | 27.89 |

| | $ | 19.26 |

| | 441.6 |

| | $ | 1.14 |

|

______________________________

Price and volume data reflect composite transactions; price range reflects intra-day prices; data source is Bloomberg.

Shareholders and Dividends

As of February 14, 2014, we had 9,196 shareholders of record.

We expect to continue to pay dividends on our common stock and we are targeting a dividend payout ratio (dividends declared per share/earnings per share) of 50-60%, though it has been and will likely be higher for the near term. Our dividend payout ratio was 106%, 67% and 88% in 2011, 2012 and 2013, respectively. See the discussion of the Company’s targeted dividend payout under “Pay Dividends” in Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations on page 43.

During 2012, the Company declared four quarterly dividends, but paid five of them, given its decision to accelerate the first quarter 2013 dividend payment into December 2012 in anticipation of individual tax rate increases. For 2013, the Company returned to its typical dividend practice and paid the fourth quarter dividend in 2014. The five dividend payments in 2012 utilized approximately $200 million of cash while the three payments in 2013 utilized roughly $125 million of cash.

Issuer Purchases of Equity Securities

The table below is a listing of our purchases of the Company’s common stock during each calendar month of the fourth quarter of 2013.

|

| | | | | | | | | | | | | |

| Period | | Total Number of Shares Purchased(1) | | Average Price Paid per Share | | Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs(2) | | Maximum Number of Shares that May Yet Be Purchased Under the Plans or Programs(2) |

| October 2013 | | 351,046 |

| | $ | 30.02 |

| | 351,046 |

| | 6,315,750 |

|

| November 2013 | | 770,797 |

| | $ | 29.59 |

| | 766,505 |

| | 5,549,245 |

|

| December 2013 | | 884,023 |

| | $ | 30.67 |

| | 883,332 |

| | 4,665,913 |

|

| Total | | 2,005,866 |

| | $ | 30.14 |

| | 2,000,883 |

| | |

______________________________

| |

| (1) | This number includes 4,983 shares which were not repurchased as part of a publicly announced plan or program, all of which were shares surrendered in transactions permitted under the Company’s benefit plans. It does not include shares withheld for taxes for option exercises and stock unit conversions. |

| |

| (2) | On August 4, 2004, the Board authorized management to repurchase up to 10 million shares each calendar year beginning January 1, 2005. This standing authorization was first reported in the quarterly report on Form 10-Q for the period ended June 30, 2004, filed August 5, 2004, and will remain in force until repealed by the Board of Directors. As such, effective January 1, 2014, the Company was authorized by the Board of Directors to repurchase up to 10 million shares in 2014. No specific repurchase schedule has been established. |

Item 6. Selected Financial Data.

|

| | | | | | | | | | | | | | | | | | | |

| (Unaudited) | 2013 1 | | 2012 2,3 | | 2011 2,4 | | 2010 2 | | 2009 2 |

| (Dollar amounts in millions, except per share data) | | | | | | | | | |

| Summary of Operations | | | | | | | | | |

| Net Sales from Continuing Operations | $ | 3,746 |

| | $ | 3,706 |

| | $ | 3,619 |

| | $ | 3,340 |

| | $ | 3,015 |

|

| Earnings from Continuing Operations | 193 |

| | 243 |

| | 174 |

| | 187 |

| | 119 |

|

| (Earnings) Attributable to Noncontrolling Interest, net of tax | (3 | ) | | (2 | ) | | (3 | ) | | (6 | ) | | (3 | ) |

| Earnings (loss) from Discontinued Operations, net of tax | 7 |

| | 7 |

| | (18 | ) | | (4 | ) | | (4 | ) |

| Net Earnings | 197 |

| | 248 |

| | 153 |

| | 177 |

| | 112 |

|

| Earnings per share from Continuing Operations | | | | | | | | | |

| Basic | 1.31 |

| | 1.67 |

| | 1.17 |

| | 1.20 |

| | .73 |

|

| Diluted | 1.29 |

| | 1.65 |

| | 1.16 |

| | 1.18 |

| | .73 |

|

| Earnings (Loss) per share from Discontinued Operations | | | | | | | | | |

| Basic | .05 |

| | .05 |

| | (.12 | ) | | (.03 | ) | | (.03 | ) |

| Diluted | .05 |

| | .05 |

| | (.12 | ) | | (.03 | ) | | (.03 | ) |

| Net Earnings (Loss) per share | | | | | | | | | |

| Basic | 1.36 |

| | 1.72 |

| | 1.05 |

| | 1.17 |

| | .70 |

|

| Diluted | 1.34 |

| | 1.70 |

| | 1.04 |

| | 1.15 |

| | .70 |

|

| Cash Dividends declared per share | 1.18 |

| | 1.14 |

| | 1.10 |

| | 1.06 |

| | 1.02 |

|

| Summary of Financial Position | | | | | | | | | |

| Total Assets | $ | 3,108 |

| | $ | 3,255 |

| | $ | 2,915 |

| | $ | 3,001 |

| | $ | 3,061 |

|

| Long-term Debt, including capital leases | $ | 688 |

| | $ | 854 |

| | $ | 833 |

| | $ | 762 |

| | $ | 789 |

|

______________________________

| |

1 | In the fourth quarter of 2013, we incurred $67 million of charges related to the Commercial Vehicle Products group ($63 million goodwill impairment charge and $4 million accelerated amortization of a customer-related intangible asset). In the third quarter of 2013, we recorded a $9 million bargain purchase gain related to an acquisition. |

| |

2 | Amounts for 2012 through 2009 were retrospectively adjusted to reflect the reclassification of certain businesses from continuing to discontinued operations in 2013. For information about discontinued operations, see Note B on page 78 of the Notes to Consolidated Financial Statements. |

| |

3 | Net earnings for 2012 include a $27 million net tax benefit primarily related to the release of valuation allowances on certain Canadian deferred tax assets, partially offset by deferred withholding taxes on earnings in China. |

| |

4 | The Company incurred asset impairment charges and restructuring-related charges totaling $44 million in 2011. Of these charges, $25 million were associated with continuing operations and $19 million were related to discontinued operations. |

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

2013 HIGHLIGHTS

Acquisitions contributed to modest sales growth in 2013. Same location sales (excluding acquisitions) were essentially flat, with slightly higher unit volume offset by lower trade sales from our rod mill. Sales growth continued in Automotive and Carpet Underlay but these gains were largely offset by declines in Store Fixtures, Commercial Vehicle Products (CVP), and Adjustable Bed.

As discussed throughout the year, we have been considering strategic alternatives for our CVP business. Late in 2013, it became apparent that current market values for certain CVP assets had fallen below recorded book values, and we recognized non-cash impairment and other charges related to the goodwill and other intangible assets of the business. Earnings in 2013 decreased (versus 2012) as result of these charges and the non-recurrence of a significant tax benefit from 2012.

We expanded our Aerospace Products business unit in 2013 with the acquisition of two companies. These new European-based operations added small diameter, high pressure seamless tubing to our product portfolio and extended our capability in aerospace tube fabrication.

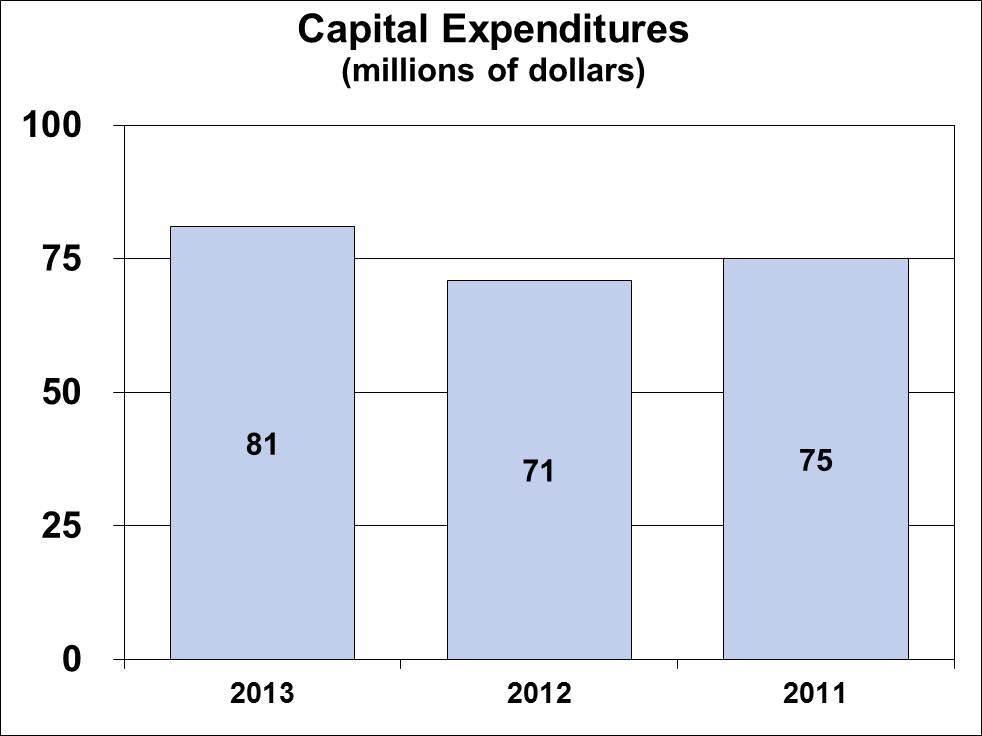

Operating cash for the full year was strong, helped in part by improvements in working capital levels. We again generated more than enough cash from operations to comfortably fund dividends and capital expenditures, something we've accomplished for over 20 years.

2013 marked the 42nd consecutive annual dividend increase for the company, with a compound annual growth rate of 13% over that time period. Only one other S&P 500 company can claim as high a rate of dividend growth for as many years.

Our financial profile remains strong. We ended 2013 with net debt to net capital below the conservative end of our long-standing targeted range. In April we repaid $200 million of notes that matured and ended the year with nearly all of our $600 million commercial paper program and revolver facility available.

We assess our overall performance by comparing our Total Shareholder Return (TSR) to that of peer companies on a rolling three-year basis. We target TSR in the top one-third of the S&P 500 over the long term. For the three years ended December 31, 2013, we generated TSR of 16% per year on average. That places us in the top half of the S&P 500, but shy of our top one-third goal.