|

|

| |

| UNITED STATES SECURITIES AND EXCHANGE COMMISSION |

| Washington, D.C. 20549 |

| FORM 10-K |

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) |

| OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

| |

| For the fiscal year ended June 30, 2016 | Commission file number 1-5128 |

|

| |

| MEREDITH CORPORATION |

| (Exact name of registrant as specified in its charter) |

| | |

| Iowa | 42-0410230 |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

| | |

| 1716 Locust Street, Des Moines, Iowa | 50309-3023 |

| (Address of principal executive offices) | (ZIP Code) |

| | |

Registrant's telephone number, including area code: (515) 284-3000 |

|

| | | | |

| Securities registered pursuant to Section 12(b) of the Act: |

| | Title of each class | | Name of each exchange on which registered | |

| | Common Stock, par value $1 | | New York Stock Exchange | |

|

| | | | | | | | |

| Securities registered pursuant to Section 12(g) of the Act: |

| | | | Title of class | | | |

| Class B Common Stock, par value $1 |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer," and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer x Accelerated filer o Non-accelerated filer o Smaller reporting company o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

The registrant estimates that the aggregate market value of voting and non-voting common equity held by non-affiliates of the registrant at December 31, 2015, was $1,557,000,000 based upon the closing price on the New York Stock Exchange at that date.

|

| | |

| Shares of stock outstanding at July 31, 2016 |

| Common shares | 39,286,518 |

|

| Class B shares | 5,283,303 |

|

| Total common and Class B shares | 44,569,821 |

|

|

| | | | |

| DOCUMENT INCORPORATED BY REFERENCE |

Certain portions of the Registrant's Proxy Statement for the Annual Meeting of Shareholders to be held on November 9, 2016, are incorporated by reference in Part III to the extent described therein. |

| | | | | |

| | | TABLE OF CONTENTS | | |

| | | | Page | |

| | | Part I | | |

| | | Business | | |

| | | Description of Business | | |

| | | Local Media | | |

| | | National Media | | |

| | | Executive Officers of the Company | | |

| | | Employees | | |

| | | Other | | |

| | | Available Information | | |

| | | Forward Looking Statements | | |

| | | Risk Factors | | |

| | | Unresolved Staff Comments | | |

| | | Properties | | |

| | | Legal Proceedings | | |

| | | Mine Safety Disclosures | | |

| | | | | |

| | | Part II | | |

| | | Market for Registrant's Common Equity, Related Shareholder | | |

| Matters, and Issuer Purchases of Equity Securities | | |

| | | Selected Financial Data | | |

| | | Management's Discussion and Analysis of Financial | | |

| Condition and Results of Operations | | |

| | | Quantitative and Qualitative Disclosures About Market Risk | | |

| | | Financial Statements and Supplementary Data | | |

| | | Changes in and Disagreements with Accountants on | | |

| Accounting and Financial Disclosure | | |

| | | Controls and Procedures | | |

| | | Other Information | | |

| | | | | |

| | | Part III | | |

| | | Directors, Executive Officers, and Corporate Governance | | |

| | | Executive Compensation | | |

| | | Security Ownership of Certain Beneficial Owners and | | |

| Management and Related Stockholder Matters | | |

| | | Certain Relationships and Related Transactions and | | |

| Director Independence | | |

| | | Principal Accounting Fees and Services | | |

| | | | | |

| | | Part IV | | |

| | | Exhibits, Financial Statement Schedules | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | | |

Meredith Corporation and its consolidated subsidiaries are referred to in this Annual Report on Form 10-K (Form 10-K) as Meredith, the Company, we, our, and us. |

ITEM 1. BUSINESS

GENERAL

Meredith Corporation has been committed to service journalism for nearly 115 years. Meredith began in 1902 as an agricultural publisher. In 1924, the Company published the first issue of Better Homes and Gardens. The Company entered the television broadcasting business in 1948. Today, Meredith uses multiple media outlets—including broadcast television, print, digital, mobile, and video—to provide consumers with content they desire and to deliver the messages of our advertising and marketing partners. The Company is incorporated under the laws of the State of Iowa. Our common stock is listed on the New York Stock Exchange under the ticker symbol MDP.

The Company operates two business segments: local media and national media. Our local media segment consists of 16 owned television stations and one operated television station located across the United States (U.S.) concentrated in fast growing markets with related digital and mobile media assets. The owned television stations consist of seven CBS affiliates, five FOX affiliates, two MyNetworkTV affiliates, one NBC affiliate, one ABC affiliate, and one independent station. Local media's digital presence includes 13 websites, 13 mobile-optimized websites, and nearly 40 applications (apps) focused on news, sports, and weather-related information.

Our national media segment includes leading national consumer media brands delivered via multiple media platforms including print magazines and digital and mobile media, brand licensing activities, database-related activities, and business-to-business marketing products and services. It focuses on the food, home, parenthood, and health markets and is a leading publisher of magazines serving women. In fiscal 2016, we published in print more than 20 subscription magazines, including Better Homes and Gardens, Parents, Family Circle, Allrecipes, Rachael Ray Every Day, Martha Stewart Living, Shape, and FamilyFun, and nearly 140 special interest publications. Twenty of our brands are also available as digital editions on one or more of the six major digital newsstands and on major tablet devices. The national media segment's extensive digital media presence consists of nearly 50 websites, more than 30 mobile-optimized websites, and nearly 15 apps. Of those websites and apps, the Allrecipes brand accounts for 19 web and mobile sites serving 23 countries in 12 languages, and 2 mobile apps across multiple countries and platforms. The national media segment also includes digital and customer relationship marketing, which provides specialized marketing products and services to some of America's leading companies; a large consumer database; brand licensing activities; and other related operations.

Financial information about industry segments can be found in Item 7-Management's Discussion and Analysis of Financial Condition and Results of Operations and in Item 8-Financial Statements and Supplementary Data under Note 15.

The Company's largest revenue source is advertising. National and local economic conditions affect the magnitude of our advertising revenues. Both local media and national media revenues and operating results can be affected by changes in the demand for advertising and consumer demand for our products. Television advertising is seasonal and cyclical to some extent, traditionally generating higher revenues in the second and fourth fiscal quarters and during key political contests and major sporting events. Magazine circulation revenues are generally affected by national and regional economic conditions and competition from other forms of media.

BUSINESS DEVELOPMENTS

In September 2015, the Company entered into a merger agreement with Media General, Inc. (Media General). In January 2016, this agreement was terminated.

In December 2015, Meredith entered into a new 10-year contract with Sequential Brands Group, Inc. to license the Martha Stewart media properties. This agreement replaced the October 2014 agreement with Martha Stewart Living Omnimedia (which was acquired by Sequential Brands Group, Inc. in 2015). Under the new agreement, Meredith assumed the cross-platform editorial responsibilities for the Martha Stewart media properties. Martha Stewart Living is published 10 times annually with a rate base of 2.1 million. Martha Stewart Weddings, a quarterly publication, is the #1-selling bridal magazine on newsstands.

Allrecipes magazine's rate base was increased to 1.25 million with the September/October 2015 issue and then to 1.3 million with the February/March 2016 issue. This latest increase represented a 160 percent increase in rate base since the magazine's launch in 2013.

In January 2016, Meredith announced an analytical alliance with Nielsen to measure the total Return on Advertising Spend for native digital advertising campaigns on Allrecipes.com and other Meredith digital properties. This measurement capability combines Meredith Shopper Marketing's ability to deliver and measure offers at the store level with Nielsen's Similarities Market Test service, which works to determine the extent in-market activities are driving sales. These insights and analytics allow marketers to better navigate the digital space to understand promotions that lead to purchases.

In January 2016, Meredith announced the launch of two brand licensing programs under the Shape and EatingWell brands. Meredith partnered with Apparel Bridge LLC to create SHAPE® Active, an activewear collection designed for women. The collection is available at selected digital and small specialty retailers, with additional retail partners expected. Under the EatingWell brand, Meredith entered into a multi-year licensing partnership with Bellisio Foods, Inc. to produce a line of healthy frozen food products that focus on single-serve meals, with expansions planned into other products. These products will debut in supermarkets and retail grocery stores nationwide in fall 2016.

The Company discontinued the use of the American Baby brand following its combination with Fit Pregnancy to create a new brand called Fit Pregnancy and Baby. The new magazine covers a range of topics important to new moms including beauty, nutrition, health, style, and infant development.

In May 2016, Meredith was named the second largest global licensor by License!Global magazine. Meredith moved to the second place ranking after its fourth year of being ranked.

In fiscal 2016, we successfully renewed agreements with cable systems, satellite, and telecommunications companies that covered approximately 40 percent of subscribers. Additionally, we successfully completed new network affiliation agreements with CBS in our Hartford, Springfield, and St. Louis markets.

DESCRIPTION OF BUSINESS

Local Media

Local media contributed 33 percent of Meredith's consolidated revenues in fiscal 2016. Information about the Company's television stations at June 30, 2016, follows:

|

| | | | | |

Station, Market | DMA National Rank 1 | Network Affiliation | Virtual Channel | Expiration Date of FCC License | Average Audience Share 2 |

| | | | | | |

| WGCL-TV | 9 | CBS | 46 | 4-1-2021 | 4.6 % |

| Atlanta, GA | | | | | |

| | | | | | |

| KPHO-TV | 12 | CBS | 5 | 10-1-2022 | 6.1 % |

| Phoenix, AZ | | | | | |

| | | | | | |

| KTVK | 12 | Independent | 3 | 10-1-2022 | 3.6 % |

| Phoenix, AZ | | | | | |

| | | | | | |

| KMOV | 21 | CBS | 4 | 2-1-2022 | 10.3 % |

| St. Louis, MO | | | | | |

| | | | | | |

| KPTV | 24 | FOX | 12 | 2-1-2023 | 5.2 % |

| Portland, OR | | | | | |

| | | | | | |

| KPDX | 24 | MyNetworkTV | 49 | 2-1-2023 | 2.4 % |

| Portland, OR | | | | | |

| | | | | | |

| WSMV-TV | 29 | NBC | 4 | 8-1-2021 | 8.0 % |

| Nashville, TN | | | | | |

| | | | | | |

| WFSB | 30 | CBS | 3 | 4-1-2023 | 11.5 % |

| Hartford, CT | | | | | |

| New Haven, CT | | | | | |

| | | | | | |

| KCTV | 33 | CBS | 5 | 2-1-2022 | 9.2 % |

| Kansas City, MO | | | | | |

| | | | | | |

| KSMO-TV | 33 | MyNetworkTV | 62 | 2-1-2022 | 0.9 % |

| Kansas City, MO | | | | | |

| | | | | | |

| WHNS | 37 | FOX | 21 | 12-1-2020 | 4.2 % |

| Greenville, SC | | | | | |

| Spartanburg, SC | | | | | |

| Asheville, NC | | | | | |

| Anderson, SC | | | | | |

| | | | | | |

| KVVU-TV | 40 | FOX | 5 | 10-1-2022 | 4.8 % |

| Las Vegas, NV | | | | | |

| | | | | | |

| WALA-TV | 58 | FOX | 10 | 4-1-2021 | 7.4 % |

| Mobile, AL | | | | | |

| Pensacola, FL | | | | | |

| | | | | | |

|

| | | | | |

Station, Market | DMA National Rank 1 | Network Affiliation | Virtual Channel | Expiration Date of FCC License | Average Audience Share 2 |

| | | | | | |

| WNEM-TV | 71 | CBS | 5 | 10-1-2021 | 14.3 % |

| Flint, MI | | | | | |

| Saginaw, MI | | | | | |

| Bay City, MI | | | | | |

| | | | | | |

| WGGB-TV | 116 | ABC | 40 | 4-1-2023 | 10.5 % |

| Springfield, MA | | FOX | 40.2 | | 3.2 % |

| Holyoke, MA | | | | | |

| | | | | | |

| WSHM-LD | 116 | CBS | 3 | 4-1-2023 | 7.3 % |

| Springfield, MA | | | | | |

| Holyoke, MA | | | | | |

| | | | | | |

| | | | | | |

1 Designated Market Area (DMA) is a registered trademark of, and is defined by, Nielsen Media Research. The national rank is from the 2015-2016 DMA ranking. |

| | | | | | |

2 Average audience share represents the estimated percentage of households using television tuned to the station in the DMA. The percentages shown reflect the average total day shares (6:00 a.m. to 2:00 a.m.) for the November 2015, February 2016, and May 2016 measurement periods. |

Operations

The principal sources of the local media segment's revenues are: 1) local non-political advertising focusing on the immediate geographic area of the stations; 2) national non-political advertising; 3) political advertising which is cyclical with peaks occurring in our odd fiscal years (e.g. fiscal 2015, fiscal 2017) and particularly in our second fiscal quarter of those years; 4) retransmission of our television signals by cable systems, satellite, and telecommunications companies; 5) digital advertising on the stations' web, mobile websites, and apps; and 6) station operation management fees.

The stations sell commercial time to both local/regional and national advertisers. Rates for spot advertising are influenced primarily by the market size, number of competitors including in-market broadcasters, audience share, and audience demographics. The larger a station's audience share in any particular daypart, the more leverage a station has in setting advertising rates. Generally, as supply and demand fluctuate in the market, so do a station's advertising rates. Most national advertising is sold by an independent representative firm. The sales staff at each station generates local/regional advertising revenues.

Typically 40 to 50 percent of a market's television advertising revenue is generated during local newscasts. Station personnel are continually working to grow their news ratings, which in turn will augment revenues. The Company broadcasts local newscasts in high definition in all of our markets.

Meredith's 16 national network affiliations at our television stations also influence advertising rates. Generally, a network affiliation agreement provides a station the exclusive right to broadcast network programming in its local service area. In return, the network has the right to sell most of the commercial advertising aired during network programs.

Our CBS affiliation agreements expire in August 2017 and June 2020. The MyNetworkTV affiliation agreements expire in September 2018. Our FOX affiliation in Springfield, Massachusetts is currently extended while under renewal negotiations; all other FOX affiliation agreements expire in December 2017. Our NBC affiliation agreement expires in December 2017 and our ABC affiliation agreement expires in December 2019. On top of increases in fiscal 2015, programming fees paid to CBS and FOX increased significantly in fiscal 2016. These payments are in essence a portion of the retransmission fees that Meredith receives from cable, satellite, and telecommunications service providers, which pay Meredith to carry our television programming in our markets.

These stations generally also pay networks for certain programming and services such as marquee sports (professional football, college basketball, and Olympics) and news services. The Company's FOX affiliates also pay the FOX network for additional advertising spots during prime-time programming. While Meredith's relations with the networks historically have been very good, the Company can make no assurances they will remain so over time.

Retransmission revenue is generated from cable, satellite, and telecommunications service providers who pay Meredith for access to our television station signals so that they may retransmit our signals and charge their subscribers for this programming. These fees increased in fiscal 2016 primarily due to renegotiations of expiring contracts and negotiated contract step-ups on existing contracts effective during the year.

The Federal Communications Commission (FCC) has permitted broadcast television station licensees to use their digital spectrum for a wide variety of services such as high-definition television programming, audio, data, mobile applications, and other types of communication, subject to the requirement that each broadcaster provide at least one free video channel equal in quality to the current technical standards. Several of our stations are broadcasting one or more additional programming streams on their digital channel. Examples include: three markets have MyNetworkTV, two of our markets air the LAFF network, eight of our markets carry COZI TV network, four broadcast Escape network, Springfield airs the FOX network, and two markets air local news and weather.

The costs of television programming are significant. In addition to network affiliation fees, there are two principal programming costs for Meredith: locally produced programming, including local news; and purchased syndicated programming. The Company continues to increase our locally produced news and entertainment programming to control content and costs and to attract advertisers. Syndicated programming costs are based largely on demand from stations in the market and can fluctuate significantly.

Competition

Meredith's television stations compete directly for advertising dollars and programming in their respective markets with other local television stations, radio stations, cable television providers, and digital websites and mobile sites. Other mass media providers such as newspapers and their websites are also competitors. Advertisers compare market share, audience demographics, and advertising rates, and take into account audience acceptance of a station's programming, whether local, network, or syndicated.

Regulation

The ownership, operation, and sale of broadcast television stations, including those licensed to the Company, are subject to the jurisdiction of the FCC, which engages in extensive regulation of the broadcasting industry under authority granted by the Communications Act of 1934, as amended (Communications Act), including authority to promulgate rules and regulations governing broadcasting. The Communications Act requires broadcasters to serve the public interest. Among other things, the FCC assigns frequency bands; determines stations' locations and operating parameters; issues, renews, revokes, and modifies station licenses; regulates and limits changes in ownership or control of station licenses; regulates equipment used by stations; regulates station employment practices; regulates certain program content, including commercial matters in children's programming; has the authority to impose penalties for violations of its rules or the Communications Act; and imposes annual fees on stations. Reference should be made to the Communications Act, as well as to the FCC's rules, public notices, and rulings for further information concerning the nature and extent of federal regulation of broadcast stations.

Broadcast licenses are granted for eight-year periods. The Communications Act directs the FCC to renew a broadcast license if the station has served the public interest and is in substantial compliance with the provisions of the Communications Act and FCC rules and policies. Management believes the Company is in substantial compliance with all applicable provisions of the Communications Act and FCC rules and policies and knows of no reason why Meredith's broadcast station licenses will not be renewed.

The FCC has, on occasion, changed the rules related to local ownership of media assets, including rules relating to the ownership of one or more television stations in a market. The FCC's media ownership rules are subject to

further review by the FCC, various court appeals, petitions for reconsideration before the FCC, and possible actions by Congress. We cannot predict the impact of any of these developments on our business.

The Communications Act and the FCC also regulate relationships between television broadcasters and cable, satellite, and telecommunications television providers. Under these provisions, most cable systems must devote a specified portion of their channel capacity to the carriage of the signals of local television stations that elect to exercise this right to mandatory carriage. Alternatively, television stations may elect to restrict cable systems from carrying their signals without their written permission, referred to as retransmission consent. Congress and the FCC have established and implemented generally similar market-specific requirements for mandatory carriage of local television stations by satellite television providers when those providers choose to provide a market's local television signals. These rules, including related rules on exclusivity, good faith bargaining, and "over-the-top" carriage are subject to further review by the FCC and possible actions by Congress. We cannot predict the impact of any of these developments on our business.

The FCC proposed a plan, called the National Broadband Plan, to increase the amount of spectrum available in the United States for wireless broadband use. In furtherance of the National Broadband Plan, Congress enacted, and the President signed into law, legislation authorizing the FCC to conduct a “reverse auction” for which television broadcast licensees could submit bids to receive compensation in return for relinquishing all or a portion of their rights in the television spectrum of their full service and/or Class A stations. Under the new law, the FCC may hold one reverse auction, and another auction for the newly freed spectrum. The FCC must complete both auctions by 2022. In May 2014, the FCC adopted a Report and Order setting forth the basic framework for the reverse auction and the subsequent repacking of broadcast television signals into a new television band plan. The reverse auction began on May 31, 2016. Further actions from the FCC are expected in the coming months.

Even if a television licensee does not participate in the reverse auction, the results of the auction could materially impact a station's operations. The FCC has the authority to force a television station to change channels and/or modify its coverage area to allow the FCC to rededicate certain channels within the television band for wireless broadband use. We cannot predict whether or how this action will affect the Company or our television stations.

In addition to the National Broadband Plan, Congress and the FCC have under consideration, and in the future may adopt, new laws, regulations, and policies regarding a wide variety of other matters that also could affect, directly or indirectly, the operation, ownership transferability, and profitability of the Company's broadcast stations and affect the ability of the Company to acquire additional stations. In addition to the matters noted above, these could include spectrum usage fees, regulation of political advertising rates, restrictions on the advertising of certain products (such as alcoholic beverages), program content restrictions, and ownership rule changes.

Other matters that could potentially affect the Company's broadcast properties include technological innovations and developments generally affecting competition in the mass communications industry for viewers or advertisers, such as home video recording devices and players, satellite radio and television services, cable television systems, newspapers, outdoor advertising, and internet-delivered video programming services.

The information provided in this section is not intended to be inclusive of all regulatory provisions currently in effect. Statutory provisions and FCC regulations are subject to change, and any such changes could affect future operations and profitability of the Company's local media segment. Management cannot predict what regulations or legislation may be adopted, nor can management estimate the effect any such changes would have on the Company's television broadcasting operations.

National Media

National media contributed 67 percent of Meredith's consolidated revenues in fiscal 2016. Better Homes and Gardens magazine, our flagship brand, continues to account for a significant percentage of revenues and operating profit of the national media segment and the Company.

Magazines

Information for our major subscription magazine titles as of June 30, 2016, follows:

|

| | | | | |

| Title | Description | Frequency per Year | Year-end Rate Base |

| 1 |

| | | | | |

| Better Homes and Gardens | Women's service | 12 | 7,600,000 |

| |

| Family Circle | Women's service | 12 | 4,000,000 |

| |

| Shape | Women's lifestyle | 10 | 2,500,000 |

| |

| Parents | Parenthood | 12 | 2,200,000 |

| |

| FamilyFun | Parenthood | 9 | 2,100,000 |

| |

| Martha Stewart Living | Women's service | 10 | 2,050,000 |

| |

| Fit Pregnancy and Baby | Parenthood | 11 | 2,000,000 |

| |

| Rachael Ray Every Day | Women's lifestyle and food | 10 | 1,700,000 |

| |

| Allrecipes | Food | 6 | 1,300,000 |

| |

| EatingWell | Women's lifestyle and food | 6 | 1,000,000 |

| |

| Midwest Living | Travel and lifestyle | 6 | 950,000 |

| |

| Ser Padres | Hispanic parenthood | 8 | 850,000 |

| |

| Traditional Home | Home decorating | 8 | 850,000 |

| |

| Siempre Mujer | Hispanic women's lifestyle | 6 | 550,000 |

| |

| Successful Farming | Farming business | 13 | 390,000 |

| |

| Wood | Woodworking | 7 | 380,000 |

| |

|

| | |

| 1 | | Rate base is the circulation guaranteed to advertisers. Actual circulation generally exceeds rate base and for most of the Company's titles is tracked by the Alliance for Audited Media, which issues periodic statements for audited magazines. |

In addition to these major magazine titles, we published nearly 140 special interest publications under approximately 90 titles in fiscal 2016, primarily under the Better Homes and Gardens brand. The titles are issued from one to six times annually and sold primarily on newsstands. A limited number of subscriptions are also sold to certain special interest publications. The following special interest titles were published quarterly or more frequently: American Patchwork & Quilting; Country Gardens; Diabetic Living; Do It Yourself; Eat This, Not That!; and Quilts & More.

Magazine Advertising—Advertising revenues are generated primarily from sales to clients engaged in consumer marketing. Many of Meredith's larger magazines offer regional and demographic editions that contain similar editorial content but allow advertisers to customize messages to specific markets or audiences. The Company sells two primary types of magazine advertising: display and direct-response. Advertisements are either run-of-press (printed along with the editorial portions of the magazine) or inserts (preprinted pages). Most of the national media segment's advertising revenues are derived from run-of-press display advertising. Meredith also possesses strategic marketing capabilities, which provide clients and their agencies with access to all of Meredith’s media platforms and capabilities, including print, television, digital, video, mobile, consumer events, and custom marketing. Our team of creative and marketing experts delivers innovative solutions across multiple media channels that meet each client's unique advertising and promotional requirements.

Magazine Circulation—Subscriptions obtained through direct-mail solicitation, agencies, insert cards, the internet, and other means are Meredith's largest source of circulation revenues. Revenue per subscription and related expenses can vary significantly by source. Some subscription sources generate lower revenues than other sources, but have proportionately lower related costs. The majority of subscription magazines are also sold by single copy. Single copies sold on newsstands are distributed primarily through magazine wholesalers, who have the right to receive credit from the Company for magazines returned to them by retailers.

Digital and Mobile Media

We have 20 of our titles available as digital editions, with an audience of approximately 890,000. Digital subscriptions and single copy sales collectively represent 3 percent of our total rate base.

National media's nearly 50 websites and more than 30 mobile-optimized websites provide ideas and inspiration. These branded websites focus on the topics that women care about most—food, home, entertaining, and meeting the needs of moms—and on delivering powerful content geared toward lifestyle topics such as health, beauty, style, and wellness. Digital traffic across our various platforms averaged 71 million unique monthly visitors in fiscal 2016. Our brands have a strong social networking presence as well. In fiscal 2016, national media reached over 28 million Facebook fans, nearly 11 million Twitter followers, and 5 million Pinterest followers.

Other Sources of Revenues

Other revenues are derived from digital and customer relationship marketing, other custom publishing projects, brand licensing agreements, and ancillary products and services.

Meredith Xcelerated Marketing—Meredith Xcelerated Marketing (MXM) is a strategic and creative agency with digital expertise across all channels. MXM provides fully-integrated marketing solutions for some of the world's top brands, including Kraft, Lowe's, TGI Friday’s, and NBC Universal. MXM's revenue is independent of advertising and circulation, though sometimes its services are sold as part of larger programs that include advertising components.

Brand Licensing—Meredith owns a portfolio of valuable registered trademarks. Meredith brand licensing generates royalty revenue through multiple long term licensing agreements with retailers, manufacturers and service providers. Brand licensing extends the reach of Meredith brands into additional consumer channels in the U.S. and abroad.

In place for many years, Meredith has a direct-to-retail licensing agreement with Walmart for Better Homes and Gardens-branded products sold at Wal-Mart Stores, Inc. (Walmart) in the U.S., Walmart.com, and emerging in Mexico and China. We recently extended our licensing agreement with Walmart through 2019. Meredith also has a long-term agreement to license the Better Homes and Gardens brand to Realogy Corporation, which continues to build a residential real estate franchise system as Better Homes and Gardens Real Estate, LLC. The network now includes more than 300 offices and more than 10,000 agents across the U.S., Canada, and the Bahamas.

During fiscal 2016, Meredith announced two new licensing programs. The first is a line of healthy frozen food entrées by Bellisio Foods, Inc. sold under the EatingWell brand. The program will be available at retail in the second-half of calendar 2016, and therefore, did not contribute to fiscal 2016 results. The second new licensing program is a line of women's activewear clothing by Apparel Bridge sold under the Shape brand. It debuted digitally and at a small number of specialty retail stores in the weeks leading to the close of fiscal 2016, and therefore did not meaningfully contribute to fiscal 2016 results.

Meredith's national media brands are currently distributed in more than 80 countries, including a localized presence in more than 30 countries such as Australia, China, India, Mexico, Russia, and Turkey.

The Company continues to pursue activities that will serve consumers and advertisers while also extending and strengthening the reach and vitality of our brands.

Meredith has licensed exclusive global rights to publish and distribute books based on our consumer-leading brands, including the powerful Better Homes and Gardens imprint, to a book publisher. Meredith creates book content and retains all approval and content rights while the publisher is responsible for book layout and design, printing, sales and marketing, distribution, and inventory management. Meredith receives royalties based on net sales subject to a guaranteed minimum.

Production and Delivery

Paper, printing, and postage costs accounted for 25 percent of the national media segment's fiscal 2016 operating expenses.

Coated publication paper is the major raw material essential to the national media segment. We directly purchase all of the paper for our magazine production and custom publishing business. The Company has contractual agreements with major paper manufacturers to ensure adequate supplies for planned publishing requirements. The price of paper is driven by overall market conditions and is therefore difficult to predict. In fiscal 2016, average paper prices decreased 2 percent. They declined 3 percent in fiscal 2015 and 4 percent in fiscal 2014. Management anticipates paper prices will be stable during fiscal 2017 and that fiscal 2017 average paper prices will be relatively flat compared to fiscal 2016 given no significant shifts in the current supply and demand structure are anticipated.

Meredith has multi-year printing contracts with two major domestic printers for the printing of our magazines.

Postage is a significant expense of the national media segment. We continually seek the most economical and effective methods for mail delivery, including cost-saving strategies that leverage work-sharing opportunities offered within the postal rate structure. Periodical postage accounts for over 80 percent of Meredith's postage costs, while other mail items—direct mail, replies, and bills—account for nearly 20 percent. The Governors of the United States Postal Service (USPS) review prices for mailing services annually and adjust postage rates periodically. In general, postage rate changes are capped by law at the rate of inflation as measured by the Consumer Price Index (CPI). The most recent rate change was effective in April 2016, which was a rare reduction in postage. The change was not CPI driven, rather it rolled-back the temporary 4.3 percent exigent increase that was implemented in January 2014 to allow the USPS to recover losses associated with the recent recession. Prior to fiscal 2016, postage prices had risen in each of Meredith's last five fiscal years. While we expect postage prices to again increase in January 2017, due to a legislatively mandated calendar 2017 review by the Postal Regulatory Commission could potentially result in adjustments to the current rate setting regime. The impact of any such change would most likely be effective with the January 2018 increase.

Meredith continues to work independently and with others to encourage and help the USPS find and implement efficiencies to contain rate increases. We cannot, however, predict future changes in the postal rates or the impact they will have on our national media business.

Subscription fulfillment services for Meredith's national media segment are provided by third parties. National magazine newsstand distribution services are provided by third parties through multi-year agreements.

Competition

Publishing is a highly competitive business. The Company's magazines and related publishing products and services compete with other mass media, including the internet and many other leisure-time activities. Competition for advertising dollars is based primarily on advertising rates, circulation levels, reader demographics, advertiser results, and sales team effectiveness. Competition for readers is based principally on editorial content, marketing skills, price, and customer service. While competition is strong for established titles, gaining readership for newer magazines and specialty publications is especially competitive.

EXECUTIVE OFFICERS OF THE COMPANY

Executive officers are elected to one year terms each November. The current executive officers of the Company are:

Stephen M. Lacy—Chairman and Chief Executive Officer (August 10, 2016 - present) and a director of the Company since 2004. Formerly Chairman, President, and Chief Executive Officer (2010 - 2016). Age 62.

Thomas H. Harty—President and Chief Operating Officer (August 10, 2016 - Present). Formerly President, National Media Group (2010 - 2016). Age 53.

Paul A. Karpowicz—President, Local Media Group (2005 - present). Age 63.

Jonathan B. Werther—President, National Media Group (August 10, 2016 - present). Formerly EVP/President Meredith Digital (2013-2016) and Chief Strategy Officer (2012-2013). Prior to joining Meredith, Mr. Werther served as President of Simulmedia (2010-2012). Age 47.

Joseph H. Ceryanec—Vice President-Chief Financial Officer (2008 - present). Age 55.

John S. Zieser—Chief Development Officer/General Counsel and Secretary (2006 - present). Age 57.

EMPLOYEES

As of June 30, 2016, the Company had approximately 3,600 full-time and 130 part-time employees. Only a small percentage of our workforce is unionized. We consider relations with our employees to be good.

OTHER

Name recognition and the public image of the Company's trademarks (e.g., Better Homes and Gardens and Parents) and television station call letters are vital to the success of our ongoing operations and to the introduction of new businesses. The Company protects our brands by aggressively defending our trademarks and call letters.

The Company had no material expenses for research and development during the past three fiscal years. Revenues from individual customers and revenues, operating profits, and identifiable assets of foreign operations were not significant. Compliance with federal, state, and local provisions relating to the discharge of materials into the environment and to the protection of the environment had no material effect on capital expenditures, earnings, or the Company's competitive position.

AVAILABLE INFORMATION

The Company's corporate website is meredith.com. The content of our website is not incorporated by reference into this Form 10-K. Meredith makes available free of charge through our website our Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and amendments to those reports filed or furnished to the Securities and Exchange Commission (SEC) pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 as soon as reasonably practical after such documents are electronically filed with or furnished to the SEC. Meredith also makes available on our website our corporate governance information including charters of all of our Board Committees, our Corporate Governance Guidelines, our Code of Ethics, and our Bylaws. Copies of such documents are also available free of charge upon written request.

FORWARD LOOKING STATEMENTS

This Form 10-K, including the sections titled Item 1-Business, Item 1A-Risk Factors, and Item 7-Management's Discussion and Analysis of Financial Condition and Results of Operations, contains forward-looking statements that relate to future events or our future financial performance. We may also make written and oral forward-looking statements in our SEC filings and elsewhere. By their nature, forward-looking statements involve risks, trends, and uncertainties that could cause actual results to differ materially from those anticipated in any forward-looking statements. Such factors include, but are not limited to, those items described in Item 1A-Risk Factors below, those identified elsewhere in this document, and other risks and factors identified from time to time in our SEC filings. We have tried, where possible, to identify such statements by using words such as believe, expect, intend, estimate, may, anticipate, will, likely, project, plan, and similar expressions in connection with any discussion of future

operating or financial performance. Any forward-looking statements are and will be based upon our then-current expectations, estimates, and assumptions regarding future events and are applicable only as of the dates of such statements. Readers are cautioned not to place undue reliance on such forward-looking statements that are part of this filing; actual results may differ materially from those currently anticipated. The Company undertakes no obligation to update or revise any forward-looking statements, whether as a result of new information, future events, or otherwise.

ITEM 1A. RISK FACTORS

In addition to the other information contained or incorporated by reference into this Form 10-K, investors should consider carefully the following risk factors when investing in our securities. In addition to the risks described below, there may be additional risks that we have not yet perceived or that we currently believe are immaterial.

Advertising represents the largest portion of our revenues and advertising demand may fluctuate from period to period. In fiscal 2016, 55 percent of our revenues were derived from advertising. Advertising constitutes 71 percent of our local media revenues and 48 percent of our national media revenues. Demand for advertising is highly dependent upon the strength of the U.S. economy. During an economic downturn, demand for advertising may decrease. The growth in alternative forms of media, particularly electronic media including those based on the internet, has increased the competition for advertising dollars, which could in turn reduce expenditures for magazine and television advertising or suppress advertising rates.

Circulation revenues represent a significant portion of our revenues. Magazine circulation is another significant source of revenue, representing 20 percent of total revenues and 30 percent of national media revenues. Preserving the number of copies sold is critical for maintaining advertising sales. Magazines face increasing competition from alternative forms of media and entertainment. As a result, sales of magazines through subscriptions and at the newsstand could decline. As publishers compete for subscribers, subscription prices could decrease and marketing expenditures may increase.

Technology in the media industry continues to evolve rapidly. Advances in technology have led to an increasing number of alternative methods for the delivery of content and have driven consumer demand and expectations in unanticipated directions. If we are unable to exploit new and existing technologies to distinguish our products and services from those of our competitors or adapt to new distribution methods that provide optimal user experiences, our business, financial condition, and prospects may be adversely affected. Technology developments also pose other challenges that could adversely affect our revenues and competitive position. New delivery platforms may lead to pricing restrictions, the loss of distribution control, and the loss of a direct relationship with consumers. We may also be adversely affected if the use of technology developed to block the display of advertising on websites proliferates. In addition, technologies such as subscription streaming media services and mobile video are increasing competition for household audiences and advertisers. This competition may make it difficult for us to grow or maintain our broadcasting and print revenues, which we believe may challenge us to expand the contribution of our digital businesses.

Our websites and internal networks may be vulnerable to unauthorized persons accessing our systems, which could disrupt our operations. The Company uses computers in substantially all aspects of our business operations. Our website activities involve the storage and transmission of proprietary information, which we endeavor to protect from unauthorized access. However, it is possible that unauthorized persons may be able to circumvent our protections and misappropriate proprietary information or cause interruptions or malfunctions in our digital operations. We invest in security resources and technology to protect our data and business processes against risk of data security breaches and cyber-attack, but the techniques used to attempt attacks are constantly changing. A breach or successful attack could have a negative impact on our operations or business reputation.

Evolving privacy and information security laws and regulations may impair our ability to market to consumers. Meredith's consumer database includes first-party data that is used to market our products to our customers and is also rented to or used on behalf of marketing and advertising clients. As public awareness shifts to data gathering and usage, privacy rights, and data protection, new laws and regulations may be passed that would restrict or prevent us from utilizing this data. Such restrictions could reduce or eliminate this resource for generating revenue for the Company.

World events may result in unexpected adverse operating results for our local media segment. Our local media results could be affected adversely by world events such as wars, political unrest, acts of terrorism, and natural disasters. Such events can result in significant declines in advertising revenues as the stations will not broadcast or will limit broadcasting of commercials during times of crisis. In addition, our stations may have higher newsgathering costs related to coverage of the events.

Our local media operations are subject to FCC regulation. Our broadcasting stations operate under licenses granted by the FCC. The FCC regulates many aspects of television station operations including employment practices, political advertising, indecency and obscenity, programming, signal carriage, and various technical matters. Violations of these regulations could result in penalties and fines. Changes in these regulations could impact the results of our operations. The FCC also regulates the ownership of television stations. Changes in the ownership rules could adversely affect our ability to consummate future transactions. Details regarding regulation and its impact on our local media operations are provided in Item 1-Business beginning on page 5.

Loss of or changes in affiliation agreements could adversely affect operating results for our local media segment. Due to the quality of the programming provided by the networks, stations that are affiliated with a network generally have higher ratings than unaffiliated independent stations in the same market. As a result, it is important for stations to maintain their network affiliations. Most of our stations have network affiliation agreements. Seven are affiliated with CBS, five with FOX, two with MyNetworkTV, one with NBC, and one with ABC. These television networks produce and distribute programming in exchange for each of our stations' commitment to air the programming at specified times and for commercial announcement time during the programming. In most cases, we also make cash payments to the networks. These payments are in essence a portion of the retransmission fees that Meredith receives from cable, satellite, and telecommunications service providers, which pay Meredith to carry our television programming in our markets. The non-renewal or termination of any of our network affiliation agreements would prevent us from being able to carry programming of the affiliate network. This loss of programming would require us to obtain replacement programming, which may involve higher costs and/or which may not be as attractive to our audiences, resulting in reduced revenues. Furthermore, the non-renewal of any retransmission consent agreement with a major cable, satellite, or telecommunications service provider could adversely affect the economics of our relationship with the applicable network(s), advertising revenues, and our local brands. If renewed, our network affiliation agreements and our retransmission agreements may be renewed on terms that are less favorable to us. Our CBS affiliation agreements expire in August 2017 and June 2020. The MyNetworkTV affiliation agreements expire in September 2018. Our Fox affiliation in Springfield, Massachusetts is extended and being negotiated to be renewed currently, all other FOX affiliation agreements expire in December 2017. Our NBC affiliation agreement expires in December 2017 and our ABC affiliation agreement expires in December 2019.

Client relationships are important to our brand licensing and consumer relationship marketing businesses. Our ability to maintain existing client relationships and generate new clients depends significantly on the quality of our products and services, our reputation, and the continuity of Company and client personnel. Dissatisfaction with our products and services, damage to our reputation, or changes in key personnel could result in a loss of business.

Paper and postage prices are difficult to predict and control. Paper and postage represent significant components of our total cost to produce, distribute, and market our printed products. In fiscal 2016, these expenses accounted for 18 percent of national media's operating costs. Paper is a commodity and its price can be subject to significant volatility. All of our paper supply contracts currently provide for price adjustments based on prevailing market prices; however, we historically have been able to realize favorable paper pricing through volume discounts.

The USPS distributes substantially all of our subscription magazines and many of our marketing materials. Postal rates are dependent on the operating efficiency of the USPS and on legislative mandates imposed upon the USPS. Although we work with others in the industry and through trade organizations to encourage the USPS to implement efficiencies that will minimize rate increases, we cannot predict with certainty the magnitude of future price changes for paper and postage. Further, we may not be able to pass such increases on to our customers.

Acquisitions pose inherent financial and other risks and challenges. As a part of our strategic plan, we have acquired businesses and we expect to continue acquiring businesses in the future. These acquisitions can involve a number of risks and challenges, any of which could cause significant operating inefficiencies and adversely affect our growth and profitability. Such risks and challenges include underperformance relative to our expectations and the price paid for the acquisition; unanticipated demands on our management and operational resources; difficulty in integrating personnel, operations, and systems; retention of customers of the combined businesses; assumption of contingent liabilities; and acquisition-related earnings charges. If our acquisitions are not successful, we may record impairment charges. Our ability to continue to make acquisitions will depend upon our success at identifying suitable targets, which requires substantial judgment in assessing their values, strengths, weaknesses, liabilities, and potential profitability, as well as the availability of suitable candidates at acceptable prices and whether restrictions are imposed by regulations. Moreover, competition for certain types of acquisitions is significant, particularly in the fields of broadcast stations and digital media. Even if successfully negotiated, closed, and integrated, certain acquisitions may not advance our business strategy and may fall short of expected return on investment targets.

Further impairment of goodwill and intangible assets is possible, depending upon future operating results and the value of the Company's stock. Although the Company wrote down its goodwill and intangible assets in the national media segment by $155.8 million in fiscal 2016, further impairment charges are possible. We test our goodwill and indefinite-lived intangible assets for impairment during the fourth quarter of every fiscal year and on an interim basis if indicators of impairment exist. Factors which influence the evaluation include, among many things, the Company's stock price and expected future operating results. If the carrying value of a reporting unit or an intangible asset is no longer deemed to be recoverable, a potentially material impairment charge could be incurred. At June 30, 2016, goodwill and intangible assets totaled $1.8 billion, or 68 percent of Meredith's total assets, with $1.0 billion in the national media segment and $0.8 billion in the local media segment. The review of goodwill is performed at the reporting unit level. The Company has three reporting units, local media, magazine brands, and MXM. As of May 31, 2016, the date that management last performed our annual review of impairment of goodwill and intangible assets, there were no qualitative factors that indicated that a quantitative impairment analysis was needed for the the local media reporting unit. The fair value of the magazine brands reporting unit exceeded its net assets by approximately 20 percent. In the fourth quarter of fiscal 2016, the Company determined that the MXM reporting unit was impaired. The resulting evaluation determined that the carrying value of MXM's goodwill exceeded its estimated fair value and an impairment charge of $116.9 million was recorded by the Company. Changes in key assumptions about the economy or business prospects used to estimate fair value or other changes in market conditions could result in additional impairment charges. Although these charges would be non-cash in nature and would not affect the Company's operations or cash flow, they would reduce stockholders' equity and reported results of operations in the period charged.

We have two classes of stock with different voting rights. We have two classes of stock: common stock and Class B stock. Holders of common stock are entitled to one vote per share and account for 43 percent of the voting power. Holders of Class B stock are entitled to ten votes per share and account for the remaining 57 percent of the voting power. There are restrictions on who can own Class B stock. The majority of Class B shares are held by members of Meredith's founding family. Control by a limited number of holders may make the Company a less attractive takeover target, which could adversely affect the market price of our common stock. This voting control also prevents other shareholders from exercising significant influence over certain of the Company's business decisions.

|

| | |

| | | |

The preceding risk factors should not be construed as a complete list of factors that may affect our future operations and financial results. |

| | | |

ITEM 1B. UNRESOLVED STAFF COMMENTS

None.

ITEM 2. PROPERTIES

Meredith is headquartered in Des Moines, IA. The Company owns buildings at 1716 and 1615 Locust Street and is the sole occupant of these buildings. The Company believes these facilities are adequate for their intended use.

The local media segment operates from facilities in the following locations: Atlanta, GA; Phoenix, AZ; St. Louis, MO; Beaverton, OR; Nashville, TN; Rocky Hill, CT; Fairway, KS; Greenville, SC; Henderson, NV; Mobile, AL; Saginaw, MI; and Springfield, MA. The Company believes these properties are adequate for their intended use. The property in St. Louis is leased, while the other properties are owned by the Company. Each of the broadcast stations also maintains one or more owned or leased transmitter sites.

The national media segment operates mainly from the Des Moines offices and from a leased facility in New York, NY. The New York facility is used primarily as advertising sales offices for all Meredith magazines and as headquarters for Family Circle, Shape, Parents, FamilyFun, Fit Pregnancy and Baby, Rachael Ray Every Day, and Siempre Mujer properties. Allrecipes operates out of leased space in Seattle, WA. We have also entered into leases for magazine editorial offices, MXM operations, and national media sales offices in the states of California, Colorado, Illinois, Michigan, Texas, Vermont, and Virginia. The Company believes these facilities are sufficient to meet our current and expected future requirements.

ITEM 3. LEGAL PROCEEDINGS

There are various legal proceedings pending against the Company arising from the ordinary course of business. In the opinion of management, liabilities, if any, arising from existing litigation and claims are not expected to have a material effect on the Company's earnings, financial position, or liquidity.

ITEM 4. MINE SAFETY DISCLOSURES

Not applicable.

ITEM 5. MARKET FOR REGISTRANT'S COMMON EQUITY, RELATED SHAREHOLDER MATTERS, AND ISSUER PURCHASES OF EQUITY SECURITIES

MARKET INFORMATION, DIVIDENDS, AND HOLDERS

The principal market for trading Meredith's common stock is the New York Stock Exchange (trading symbol MDP). There is no separate public trading market for Meredith's Class B stock, which is convertible share for share at any time into common stock. Holders of both classes of stock receive equal dividends per share.

The range of trading prices for the Company's common stock and the dividends per share paid during each quarter of the past two fiscal years are presented below.

|

| | | | | | | | | | | |

| | High |

| | Low |

| | Dividends |

|

| Fiscal 2016 | | | | | |

| First Quarter | $ | 53.11 |

| | $ | 39.40 |

| | $ | 0.4575 |

|

| Second Quarter | 47.70 |

| | 38.80 |

| | 0.4575 |

|

| Third Quarter | 48.00 |

| | 35.03 |

| | 0.4950 |

|

| Fourth Quarter | 52.49 |

| | 44.80 |

| | 0.4950 |

|

| | | | | | |

| | | | | | |

| | High |

| | Low |

| | Dividends |

|

| Fiscal 2015 | | | | | |

| First Quarter | $ | 50.24 |

| | $ | 42.69 |

| | $ | 0.4325 |

|

| Second Quarter | 55.75 |

| | 41.95 |

| | 0.4325 |

|

| Third Quarter | 57.22 |

| | 49.63 |

| | 0.4575 |

|

| Fourth Quarter | 55.56 |

| | 50.25 |

| | 0.4575 |

|

Meredith stock became publicly traded in 1946, and quarterly dividends have been paid continuously since 1947. Meredith has increased our dividend for 23 consecutive years. It is currently anticipated that comparable dividends will continue to be paid in the future.

On July 31, 2016, there were approximately 1,020 holders of record of the Company's common stock and 550 holders of record of Class B stock.

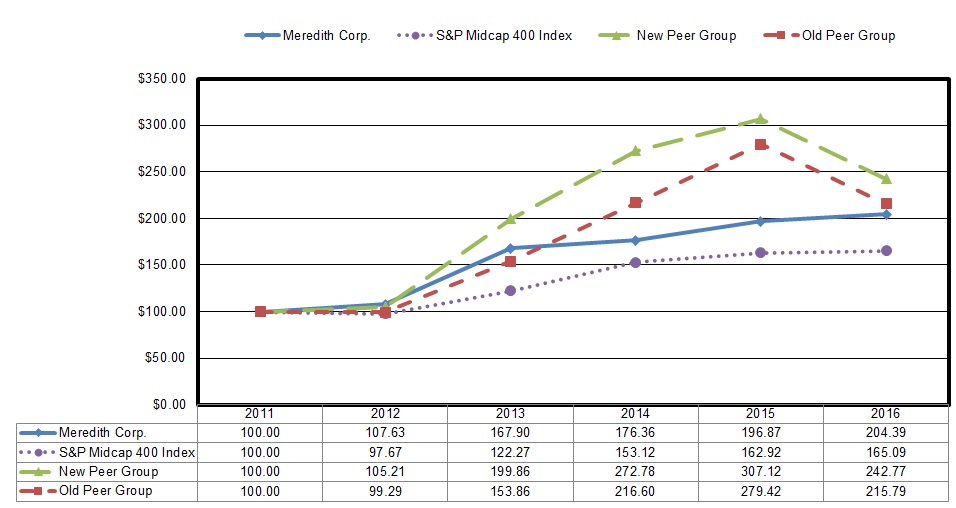

COMPARISON OF SHAREHOLDER RETURN

The following graph compares the performance of the Company's common stock during the period July 1, 2011, to June 30, 2016, with the Standard and Poor's (S&P) MidCap 400 Index and with a peer group of companies engaged in multimedia businesses primarily with publishing and/or television broadcasting in common with the Company.

The peer group was revised this fiscal year to include Nexstar Broadcasting Group, Inc. and Time Inc. (since June 9, 2014, the date its stock began trading) and to remove Graham Holding Company and Martha Stewart Living Omnimedia, Inc., which was acquired by Sequential Brands Group, Inc. effective December 4, 2015. Graham

Holding Company was removed from the peer group as it is no longer substantially in the same businesses as the Company. The graph includes both the revised peer group (New Peer Group) and the peer group used in the prior year (Old Peer Group).

The S&P MidCap 400 Index is comprised of 400 mid-sized U.S. companies with a market cap in the range of $1.4 billion to $5.9 billion in primarily the financial, information technology, industrial, and consumer discretionary industries weighted by market capitalization. The New Peer Group selected by the Company for comparison, which is also weighted by market capitalization, is comprised of Media General, Inc.; Nexstar Broadcasting Group, Inc., TEGNA Inc.; The E.W. Scripps Company, and Time Inc. The Old Peer Group, which is also weighted by market capitalization, is comprised of Graham Holding Company; Martha Stewart Living Omnimedia, Inc.; Media General, Inc.; TEGNA Inc.; and The E.W. Scripps Company.

The graph depicts the results for investing $100 in the Company's common stock, the S&P MidCap 400 Index, the New Peer Group, and the Old Peer Group at closing prices on June 30, 2011, assuming dividends were reinvested.

ISSUER PURCHASES OF EQUITY SECURITIES

The following table sets forth information with respect to the Company's repurchases of common stock during the quarter ended June 30, 2016.

|

| | | | | | | | | | | | | | | |

| Period | (a) Total number of shares purchased 1, 2 | (b) Average price paid per share | (c) Total number of shares purchased as part of publicly announced programs | (d) Approximate dollar value of shares that may yet be purchased under the programs |

| | | | | | | | | | (in thousands) |

April 1 to April 30, 2016 | 48,750 | | | $ | 49.80 |

| | | 6,635 | | | $ | 88,752 |

| |

May 1 to May 31, 2016 | 269,809 | | | 50.94 | | | 91,514 | | | 84,187 |

| |

June 1 to June 30, 2016 | 29,662 | | | 51.23 | | | 4,469 | | | 83,958 |

| |

| Total | 348,221 | | | 50.80 | | | 102,618 | | | | |

|

| |

1 | The number of shares purchased includes 5,192 shares in April 2016, 31,514 shares in May 2016, and 3,501 shares in June 2016 delivered or deemed to be delivered to us in satisfaction of tax withholding on option exercises and the vesting of restricted shares. These shares are included as part of our repurchase program and reduce the repurchase authority granted by our Board. The number of shares repurchased excludes shares we reacquired pursuant to forfeitures of restricted stock. |

2 | The number of shares purchased includes 42,115 shares in April 2016, 178,295 shares in May 2016, and 25,193 shares in June 2016 deemed to be delivered to us on tender of stock in payment for the exercise price of options. These shares do not reduce the repurchase authority granted by our Board. |

In May 2014, Meredith announced the Board of Directors had authorized the repurchase of up to $100.0 million in additional shares of the Company's stock through public and private transactions. The table above reflects the amounts that may be repurchased under this authorization.

For more information on the Company's share repurchase program, see Item 7-Management's Discussion and Analysis of Financial Condition and Results of Operations, under the heading "Share Repurchase Program" on page 34.

ITEM 6. SELECTED FINANCIAL DATA

Selected financial data for the fiscal years 2012 through 2016 are contained under the heading "Five-Year Financial History with Selected Financial Data" beginning on page 86 and are primarily derived from consolidated financial statements for those years. Information contained in that table is not necessarily indicative of results of operations in future years and should be read in conjunction with Item 7-Management's Discussion and Analysis of Financial Condition and Results of Operations and Item 8-Financial Statements and Supplementary Data of this Form 10-K.

ITEM 7. MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

Management's Discussion and Analysis of Financial Condition and Results of Operations (MD&A) consists of the following sections:

MD&A should be read in conjunction with the other sections of this Form 10-K, including Item 1-Business, Item 6-Selected Financial Data, and Item 8-Financial Statements and Supplementary Data. MD&A contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These statements are based upon our current expectations and could be affected by many risks, uncertainties, and changes in circumstances including the uncertainties and risk factors described throughout this filing, particularly in Item 1A-Risk Factors. Important factors that could cause actual results to differ materially from those described in forward-looking statements are set forth under the heading “Forward Looking Statements" in Item 1-Business.

EXECUTIVE OVERVIEW

Meredith has been committed to service journalism for nearly 115 years. Today, Meredith uses multiple distribution platforms – including broadcast television, print, digital, mobile, and video – to provide consumers with content they desire and to deliver the messages of its advertising and marketing partners.

Meredith operates two business segments. The local media segment includes 16 owned television stations and one managed station reaching 11 percent of U.S. households. Meredith’s portfolio is concentrated in large, fast-growing markets, with seven stations in the nation’s Top 25 markets—including Atlanta, Phoenix, St. Louis, and Portland—and 13 in Top 50 markets. Meredith’s stations produce more than 660 hours of local news and entertainment content each week, and operate leading local digital destinations.

Meredith’s national media segment reaches more than 100 million unduplicated women, including nearly 75 percent of U.S. millennial women. Meredith is the leader in creating content across media platforms in key consumer interest areas such as food, home, parenting, and health through well-known brands such as Better Homes and Gardens, Allrecipes, Parents, and Shape. The national media segment features robust brand licensing activities, including more than 3,000 SKUs of branded products at 4,000 Walmart stores across the U.S. and at Walmart.com. Meredith Xcelerated Marketing is an award-winning, strategic, and creative agency that provides fully integrated marketing solutions for many of the world’s top brands.

Both segments operate primarily in the U.S. and compete against similar media and other types of media on both a local and national basis. In fiscal 2016, the national media segment accounted for 67 percent of the Company's $1.6 billion in revenues while local media segment revenues contributed 33 percent.

Meredith's balanced portfolio consistently generates substantial free cash flow, and the Company is committed to growing Total Shareholder Return through dividend payments, share repurchases, and strategic business investments. Fiscal 2016 was a year of strong growth in revenues and cash flow. We generated record revenues of $1.65 billion, a 3 percent increase over fiscal 2015.

Fiscal 2016 business highlights included:

| |

| • | Expanding audiences across media platforms and increased reach to millennial women: |

| |

| ◦ | Readership across our magazine portfolio grew to a record 127 million, according to the Spring 2016 GfK Mediamark Research & Intelligence Report. |

| |

| ◦ | Traffic to our digital sites increased to more than 80 million monthly unique visitors. |

| |

| ◦ | Our reach to U.S. millennial women grew by 9 percentage points to 72 percent of American female millennials. |

| |

| ◦ | Meredith’s multi-channel reach among American women hit an all-time high of 102 million. Additionally, Meredith’s database has grown to 125 million American consumers. |

| |

| ◦ | In our television portfolio, nine of our stations ranked No. 1 or No. 2 in late news, and eight stations ranked No. 1 or No. 2 in morning news, according to the May 2016 rating book data compiled by Nielsen. |

| |

| ◦ | These audience metrics are followed closely by our advertising clients, who use them to inform advertising rates and their return on advertising across our brands. |

| |

| • | Growing magazine, digital, and non-political television advertising revenue. National media's magazine advertising revenues grew in the low-single digits and digital advertising was up in the mid-teens. Local media's non-political advertising revenues also increased in the mid-single digits, including digital advertising, which was up in the low-teens. |

| |

| • | Increasing revenues from businesses not dependent on traditional advertising. Our brand licensing activities delivered record performance in fiscal 2016 and are now ranked No. 2 in the world, according to License!Global magazine. Additionally, local media delivered growth in retransmission consent fees and contribution by renewing retransmission consent agreements with pay television providers. |

| |

| • | Continuing strong execution of our Total Shareholder Return strategy. We grew our dividend for the 23rd-straight year, increasing it in February by 8 percent to $1.98 per share on an annualized basis. We’ve paid an annual dividend for 69 straight years, and it’s currently yielding approximately 4 percent. We also strengthened our balance sheet by paying down $100.0 million of debt. |

LOCAL MEDIA

Local media derives the majority of its revenues—71 percent in fiscal 2016—from the sale of advertising both over the air and on our stations' websites and apps. The remainder comes from television retransmission fees, station operation management fees, television production services, and other services.

The stations sell advertising to both local/regional and national accounts. Political advertising revenues are cyclical in that they are significantly greater during biennial election campaigns (which take place primarily in odd-numbered fiscal years) than at other times. We generate additional revenues from internet activities and programs focused on local interests such as community events and college and professional sports.

Changes in advertising revenues tend to correlate with changes in the level of economic activity in the U.S. and in the local markets in which we operate stations, and with the cyclical changes in political advertising discussed previously. Programming content, audience share, audience demographics, and the advertising rates charged relative to other available advertising opportunities also affect advertising revenues. On occasion, unusual events necessitate uninterrupted television coverage and will adversely affect spot advertising revenues.

Local media's major expense categories are employee compensation and programming fees paid to the networks. Employee compensation represented 42 percent of local media's operating expenses in fiscal 2016. Compensation expense is affected by salary and incentive levels, the number of employees, the costs of our various employee benefit plans, and other factors. Programming fees paid to the networks represented 20 percent of this segment's fiscal 2016 expenses. Sales and promotional activities, costs to produce local news programming, and general overhead costs for facilities and technical resources accounted for most of the remaining 38 percent of local media's fiscal 2016 operating expenses.

NATIONAL MEDIA

Advertising revenues made up 48 percent of fiscal 2016 national media revenues. These revenues were generated from the sale of advertising space in our magazines and on our websites to clients interested in promoting their brands, products, and services to consumers. Changes in advertising revenues tend to correlate with changes in the level of economic activity in the U.S. Indicators of economic activity include changes in the level of gross domestic product, consumer spending, housing starts, unemployment rates, auto sales, and interest rates. Circulation levels of Meredith's magazines, reader demographic data, and the advertising rates charged relative to other comparable available advertising opportunities also affect the level of advertising revenues.

Circulation revenues accounted for 30 percent of fiscal 2016 national media revenues. Circulation revenues result from the sale of magazines to consumers through subscriptions and by single copy sales on newsstands in print form, primarily at major retailers and grocery/drug stores, and in digital form on tablets and other media devices. In the short term, subscription revenues, which accounted for 86 percent of circulation revenues, are less susceptible to economic changes because subscriptions are generally sold for terms of one to three years. The same economic factors that affect advertising revenues also can influence consumers' response to subscription offers and result in lower revenues and/or higher costs to maintain subscriber levels over time. Subscription revenues per copy and related costs can also vary significantly by subscription source. Some subscription sources generate lower revenues than other sources, but have proportionately lower related costs. A key factor in our subscription success is our industry-leading database. It contains an abundance of attributes on 125 million individuals, which represents 80 percent of American homeowners and nearly 65 percent of millennial women. The size and depth of our database is a key to our circulation model and allows more precise consumer targeting. Newsstand revenues are more volatile than subscription revenues and can vary significantly month to month depending on economic and other factors.

The remaining 22 percent of national media revenues came from a variety of activities that included the sale of customer relationship marketing products and services as well as brand licensing, product sales, and other related activities. MXM offers integrated promotional, database management, relationship, and direct marketing capabilities for corporate customers, both in printed and digital forms. These other revenues are generally affected by changes in the level of economic activity in the U.S. including changes in the level of gross domestic product, consumer spending, unemployment rates, and interest rates.

National media's major expense categories are production and delivery of publications and promotional mailings and employee compensation costs. Paper, postage, and production charges represented 25 percent of the segment's operating expenses in fiscal 2016. The price of paper can vary significantly on the basis of worldwide demand and supply for paper in general and for specific types of paper used by Meredith. The printing of our publications is outsourced. We typically have multi-year contracts for the printing of our magazines, a practice which reduces price fluctuations over the contract term. Postal rates are dependent on the operating efficiency of the USPS and on legislative mandates imposed on the USPS. The USPS adjusted rates most recently in April 2016, which resulted in

a rare reduction in postage. This adjustment was the result of rolling-back the 4.3 percent exigent increase implemented in January 2014. We currently expect an inflationary rate increase in January 2017. Meredith works with others in the industry and through trade organizations to encourage the USPS to implement efficiencies and contain rate increases.

Employee compensation, which includes benefits expense, represented 23 percent of national media's operating expenses in fiscal 2016, and is affected by the same factors noted for local media. Impairment charges accounted for 14 percent of national media's fiscal 2016 expenses. The remaining 38 percent of fiscal 2016 national media expenses included costs for magazine newsstand distribution, advertising and promotional efforts, and overhead costs for facilities and technology services.

FISCAL 2016 FINANCIAL OVERVIEW

| |