UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

☑ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended March 31, 2020

or

☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission file number: 001-12537

NEXTGEN HEALTHCARE, INC.

(Exact name of registrant as specified in its charter)

| |

California (State or other jurisdiction of incorporation or organization) | 95-2888568 (IRS Employer Identification No.) |

18111 Von Karman Avenue, Suite 800, Irvine, California (Address of principal executive offices) | 92612 (Zip Code) |

(949) 255-2600

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Trading Symbol | Name of each exchange on which registered |

Common Stock, $0.01 Par Value | NXGN | NASDAQ Global Select Market |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☑ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☑

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☑ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit). Yes ☑ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company,” and "emerging growth company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer ☑ | | Accelerated filer ☐ | | Non-accelerated filer ☐ | | Smaller reporting company ☐ | | Emerging growth company ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☑

The aggregate market value of the voting stock held by non-affiliates of the Registrant as of September 30, 2019: $849,511,000 (based on the closing sales price of the Registrant’s common stock as reported on the NASDAQ Global Select Market on that date of $15.67 per share)*

The Registrant has no non-voting common equity.

The number of outstanding shares of the Registrant’s common stock as of May 26, 2020 was 66,105,068 shares.

* For purposes of this Annual Report on Form 10-K, in addition to those shareholders which fall within the definition of “affiliates” under Rule 405 of the Securities Act of 1933, as amended, holders of ten percent or more of the Registrant’s common stock are deemed to be affiliates for purposes of this Report.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant's definitive proxy statement related to the 2020 Annual Shareholders' Meeting to be filed with the Securities and Exchange Commission within 120 days of the registrant’s fiscal year ended March 31, 2020 are incorporated herein by reference in Part III of this Annual Report on Form 10-K where indicated.

NEXTGEN HEALTHCARE, INC.

TABLE OF CONTENTS

2020 ANNUAL REPORT ON FORM 10-K

Table of Contents

CAUTIONARY STATEMENT

This Annual Report on Form 10-K (this "Report") and certain information incorporated herein by reference contain forward-looking statements within the “safe harbor” provisions of the Private Securities Litigation Reform Act of 1995. All statements included or incorporated by reference in this Report, other than statements that are purely historical, are forward-looking statements. Words such as “anticipate,” “expect,” “intend,” “plan,” “believe,” “seek,” “estimate,” “will,” “should,” “would,” “could,” “may,” and similar expressions also identify forward-looking statements. These forward-looking statements include, without limitation, discussions of the impact of the COVID-19 pandemic and measures taken in response thereto, as well as our product development plans, business strategies, future operations, financial condition and prospects, developments in and the impacts of government regulation and legislation and market factors influencing our results. Our expectations, beliefs, objectives, intentions and strategies regarding our future results are not guarantees of future performance and are subject to risks and uncertainties, both foreseen and unforeseen, that could cause actual results to differ materially from results contemplated in our forward-looking statements. These risks and uncertainties include, but are not limited to, our ability to continue to develop new products and increase systems sales in markets characterized by rapid technological evolution, consolidation, and competition from larger, better-capitalized competitors. Many other economic, competitive, governmental and technological factors could affect our ability to achieve our goals, and interested persons are urged to review the risks factors discussed in “Item 1A. Risk Factors” of this Report, as well as in our other public disclosures and filings with the Securities and Exchange Commission (“SEC”). Because of these risk factors, as well as other variables affecting our financial condition and results of operations, past financial performance may not be a reliable indicator of future performance and historical trends should not be used to anticipate results or trends in future periods. We assume no obligation to update any forward-looking statements. You are cautioned not to place undue reliance on forward-looking statements, which speak only as of the date of the filing of this Report. Each of the terms “NextGen Healthcare,” “NextGen,” “we,” “us,” “our,” or the “Company” as used throughout this Report refers collectively to NextGen Healthcare, Inc. and its wholly-owned subsidiaries, unless otherwise indicated.

3

Table of Contents

PART I

ITEM 1. BUSINESS

Company Overview

NextGen Healthcare is a leading provider of software and services that empower ambulatory healthcare practices to manage the risk and complexity of delivering care in the rapidly evolving U.S. healthcare system. Our combination of technological breadth, depth and domain expertise makes us a preferred solution provider and trusted advisor for our clients. In addition to highly configurable core clinical and financial capabilities, our portfolio includes tightly integrated solutions that deliver on ambulatory healthcare imperatives including: population health, care management, patient outreach, telemedicine and nationwide clinical information exchange.

We serve clients across all 50 states. Our approximately 100,000 providers deliver care in nearly every medical specialty in a wide variety of practice models including accountable care organizations (“ACOs”), independent physician associations (“IPAs”), managed service organizations (“MSOs”), Veterans Service Organizations (“VSOs”), and Dental Service Organizations (“DSOs”). Our clients include some of the largest and most progressive multi-specialty groups in the country. With the recent addition of behavioral health to our strong medical and oral health capabilities, we continue to extend our share not only in Federally Qualified Health Centers (“FQHCs”), but also in the emerging integrated care market.

NextGen Healthcare has historically enhanced our offering through both organic and inorganic activities. In October 2015, we divested our former Hospital Solutions division to focus exclusively on the ambulatory marketplace. In January 2016, we acquired HealthFusion Holdings, Inc. and its cloud-based electronic health record and practice management solution. In April 2017, we acquired Entrada, Inc. and its cloud-based, mobile platform for clinical documentation and collaboration. In August 2017, we acquired EagleDream Health, Inc. and its cloud-based population health analytics solution. In January 2018, we acquired Inforth Technologies for its specialty-focused clinical content. In October 2019, we acquired Topaz Information Systems, LLC for its behavioral health solutions. In December 2019, we acquired Medfusion, Inc. for its Patient Experience Platform (i.e., patient portal, self-scheduling, and patient pay) capabilities and OTTO Health, LLC for its integrated virtual care solutions, notably telemedicine. The integration of these acquired technologies has made NextGen Healthcare’s solutions among the most comprehensive and powerful in the market.

Our company was incorporated in California in 1974. Previously named Quality Systems, Inc., we changed our corporate name to NextGen Healthcare, Inc. in September 2018. Our principal offices are located at 18111 Von Karman Ave., Suite 800, Irvine, California, 92612, and our principal website is www.nextgen.com. We operate on a fiscal year ending on March 31.

Industry Background, Regulatory Environment, and Market Opportunity

Over the last decade, the ambulatory healthcare market has experienced significant regulatory change, which has driven the need for improved technology to enable practice transformation. Recognizing it was imperative to digitize the American health system to stem the escalating cost of healthcare and improve the quality of care being delivered, Congress enacted the Health Information Technology for Economic and Clinical Health Act in 2009 (“HITECH Act”). The legislation stimulated healthcare organizations to not only adopt electronic health records, but to use them to collect discrete data that could be used to drive quality care. This standardization supported early pay-for-reporting and pay-for-performance programs.

In 2010, the Affordable Care Act (“ACA”) established the roadmap for shifting American healthcare from volume (fee-for-service) to a value-based care (“VBC”) system that rewards improved outcomes at lower costs (fee-for-value). This was followed by the Medicare Access and CHIP Reauthorization Act of 2015 (“MACRA”), bipartisan legislation that further changed the way Medicare rewards clinicians for value vs. volume. Initially focused on government-funded care, the domain of the Centers for Medicare & Medicaid Services (“CMS”), these programs are now firmly established on the commercial insurance side of the industry as well.

VBC created the need for a new category of healthcare information technology (“HIT”) tools that could be used to identify and treat groups of patients, or cohorts, based on risk. Population Health Management (“PHM”) tools support these needs by identifying patient risk, engaging patients, coordinating care, and determining when interventions are needed to improve clinical and financial outcomes. According to estimates from Frost & Sullivan in May 2020, the United States PHM market is expected to reach $9.4 billion in total revenue by 2022, representing a compound annual growth rate (“CAGR”) of 28% from 2017.

Importantly, the introduction of VBC programs was only an element of the broader approach to reducing healthcare expenditure. It was also accompanied by significant reductions in Medicare spending with a projected reduction of $253 billion in payments by 2029, as reported by RevCycle Intelligence in October 2019. The drive to reduce costs initially led to consolidation in the healthcare system that was followed by a significant shift of care from the inpatient to lower cost outpatient setting. Ambulatory surgery centers (ASCs) have become an essential component of comprehensive, low cost distributed care. According to an October 2019 report from ResearchandMarkets, ASCs continue to perform more than half of all U.S. outpatient surgical procedures and are expected to see greater volumes as the number of outpatient procedures increases by an estimated 15% by 2028. From 2015 to 2022, the proportion of outpatient cases performed in ASCs is expected to increase across most service lines with the largest jump (10%) to occur in spine procedures. Among other factors, consumerism is set to play a major role in driving ASC volume increases, as procedures performed in ASCs cost an average of 58% less than the

4

Table of Contents

same procedure in a hospital outpatient department. The need to sustain revenue has made it extremely important for practices to secure their patient market share, elevating patient loyalty to a significant determinant of provider success. In addition to being loyal, groups participating in value-based contracts realized that patients also needed to be engaged in their care and interested in improving their own health. The need to attract, retain and engage patients has made patient experience one of the most important aspects of evolving care delivery in the United States. Capturing patient market share and thriving in a market driven by VBC requires both an integrated platform and a full view of the patient population’s clinical and cost data, neither of which could be accomplished without new technologies to collect and analyze multi-sourced patient data. Effectively implemented, these new technologies allow organizations to enhance financial viability while exercising the freedom to join, affiliate, integrate or interoperate in ways that maximize strategic control.

Although the HITECH Act led to the successful adoption of electronic health records, many in the healthcare industry were dissatisfied with the level of exchange of health information between different providers and across different software platforms. With the passing of the MACRA law in 2015, the U.S. Congress declared it a national objective to achieve widespread exchange of health information through interoperable certified EHR technology. Then, in December 2016, the 21st Century Cures Act (“Cures Act”) was passed and signed into law. Among many other policies, the law includes numerous provisions intended to encourage nationwide interoperability.

In March 2020, the HHS Office of the National Coordinator for Health Information Technology (“ONC”) released a final regulation which implements the key interoperability provisions included in the Cures Act. The rule calls on developers of certified EHRs to adopt standardized application programming interfaces (“APIs”) and to meet a list of other new certification and maintenance of certification requirements in order to maintain approved federal government certification status.

The ONC rule also implements the information blocking provisions of the Cures Act, including identifying reasonable and necessary activities that do not constitute information blocking. Under the Cures Act, HHS has the regulatory authority to investigate and assess civil monetary penalties of up to $1,000,000 against certified health IT developers found to be in violation of “information blocking.”

The new regulations will require significant compliance efforts for healthcare providers, information networks, exchanges, and HIT companies. However, CURES also creates opportunities for improving care delivery and outcomes through increased data exchange between providers, and easier patient access to their own health information. Key to unlocking these benefits is the introduction of new Fast Healthcare Interoperability Resources (“FHIR”) standards. ONC’s goal is for certified HIT companies to adopt FHIR-based API standards. Meanwhile, CMS is requiring hospitals to provide electronic admission, discharge and transfer notification to other healthcare facilities, providers and designated care team members.

Through the expansion of our NextGen® Share interoperability services platform and API partner marketplace, we will address the increased demand for moving and sharing patient data from the EHR easily, quickly and securely. Interoperability improves patient experience and care coordination, enhances patient safety, and reduces costs. We are also expanding resources such as educational webinars, blogs and videos on interoperability to help educate and support healthcare providers.

In recent years, there has been incremental investment to improve the delivery of behavioral healthcare. One of the central drivers of this investment has been the opioid epidemic which claims more than 70,000 lives a year in the United States. The integrated care model previously prevalent mainly in FQHCs, a model which calls for integration of behavioral health and primary care in single care settings, has also gained momentum. Both behavioral health and the integrated care workflows require broad, purpose built, tailored HIT capabilities, many of which are supported by the NextGen platform.

In late 2019, the emergence of a novel coronavirus, or COVID-19, was reported and in January 2020, the World Health Organization (“WHO”), declared it a Public Health Emergency of International Concern. In March 2020, the WHO escalated COVID-19 as a pandemic. According to Johns Hopkins University, as of May 29, 2020, more than 5.9 million cases of COVID-19 have been reported in over 188 countries with more than 364,000 deaths. In addition to the socioeconomic disruption caused by the pandemic, both treatment and suppression measures stressed the very fabric of the U.S. healthcare system in some geographies, exacerbating some of the existing challenges with capacity, balance and reimbursement. Among the measures to slow the spread of the disease and flatten the curve in line with healthcare system capacity was social/physical distancing. The need to access care while still social distancing was addressed early on with the limited use of virtual visits and was energized when the federal government reduced regulatory barriers and addressed payment parity between virtual and in-person visits. With these tailwinds, telemedicine quickly became regarded as a safer way for patients and providers to engage each other while also relieving economic pressure on the medical practice. We believe that the uptake of telemedicine will transcend COVID-19 and that virtual visits will become a permanent and important change in the way care is delivered. Keeping patients out of the transit system, out of the waiting room and away from other sick patients is simply good medicine.

We also believe that ambulatory practices will emerge from the pandemic with a clearer appreciation of the importance of business continuity and will turn to NextGen more often for managed services. Consequently, we expect to see increased subscription of our revenue cycle management services, managed hosting, and our emerging capabilities for managed clinical and administrative services.

5

Table of Contents

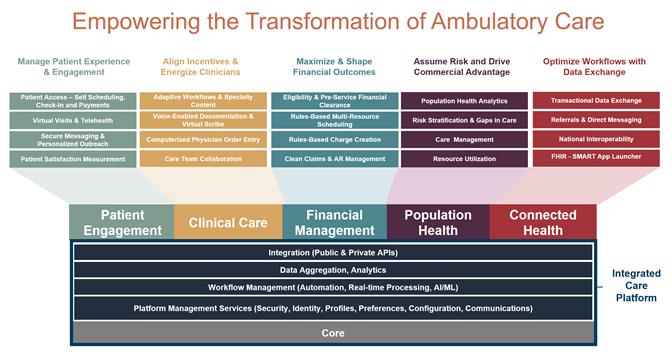

Based on these trends, successful clients must undertake the following imperatives:

| 1. | Manage patient experience and engagement |

| 2. | Align incentives and energize clinicians |

| 3. | Maximize and shape financial outcomes |

| 4. | Assume risk and drive commercial advantage |

| 5. | Optimize workflows with data exchange |

Our Strategy

We empower the accelerating transformation of ambulatory care by delivering solutions that enable groups to be successful under all models of care, including emerging value-based care in which providers assume risk while minimizing risk. We primarily serve groups that focus on delivering care in ambulatory settings, and do so across diverse practice sizes, specialties, and business constructs. In addition to traditional medical specialties, we participate actively with groups that deliver oral (dental) and behavioral healthcare, and with those that combine these in the emerging model for integrated care.

Our configurability enables groups to drive commercial advantage with creative workflows for patient access, patient-provider interactions, clinical workflows and care coordination. At the same time, our automation helps drive variability and cost out of the back office by accommodating exacting regulatory, billing and reporting requirements. We embrace both the art and science of delivering healthcare in the transforming U.S. healthcare system.

We believe that the ability to interoperate in a complex, heterogeneous healthcare ecosystem is one of the keys to providing great care and healthy financial outcomes. Because we interoperate with the major stakeholders across the U.S. healthcare system and power many of the nation’s Health Information Exchanges (“HIEs”), we help keep patient data more secure, promote continuity of care, lower the cost of care delivery and perhaps most importantly improve the patient experience.

We recognize that patient experience drives patient engagement and that engaged patients have better outcomes. Consequently, much of our activity over the last few years has been informed by the emergence of the patient as an active, involved consumer. Our solutions help our clients create a holistic, personalized care experience that drive loyalty and satisfaction.

We surround our technical solutions with implementation and optimization services and provide business process outsourcing with managed hosting and revenue cycle management services. With some of our most sophisticated clients, we have been asked to share the breadth of our experience as they shape their strategies. We believe that this sort of engagement, acting as a virtual extension of our clients’ leadership teams, is an important step along our journey to becoming a trusted advisor.

As one of the leading healthcare information technology players in the U.S. ambulatory marketplace, we plan to continue investing in our current capabilities as well as building and/or acquiring new capabilities as we guide our clients through the market’s transformation. We expect to continue to empower the transformation of care through the following strategic priorities:

| • | Be a learning organization and transform ahead of the industry |

| • | Be a trusted advisor for our customers and prospects |

| • | Deliver breadth, depth and configurability to enable our clients to effectively execute their strategies |

| • | Use automation to drive variability and cost from our clients’ operations |

| • | Drive real innovation in patient experience and patient-provider interactions |

| • | Help our clients be recognized as interoperability leaders in their regions and areas of specialty |

| • | Integrate new capabilities (whether organic or inorganic) more quickly and successfully than others. |

6

Table of Contents

Our Solutions

NextGen Healthcare’s software and services-based solutions are aligned with our clients’ strategic imperatives (refer to top row in the image below). The foundation for our integrated ambulatory care platform is a core of our industry-leading electronic health records (“EHR”) and practice management (“PM”) systems that support clinical and financial activities. These can be deployed on premise or in the cloud. Our primary cloud infrastructure provider is Amazon Web Services (“AWS”). We optimize the core with an automation and workflow layer that gives our clients control over how platform capabilities are implemented to drive their desired outcomes. The workflow layer includes mobile capabilities proven to reduce physician burden. Our cloud-based population health and analytics engine allows our clients to improve results in both fee-for-service and fee-for-value environments. In support of extensibility, we surround the core with open, web-based APIs to drive the secure exchange of health and patient data with connected health solutions. Finally, to ensure our clients get maximum value from our solutions, we have augmented our technology with key services aligned with their needs, helping to ensure they reach their organizational goals.

Patient Engagement Solutions boost loyalty and improve outcomes by engaging patients in their own care. Our Patient Experience Platform empowers patients to manage their own health through direct patient-provider messaging, online scheduling, automated reminders, easy payment options, and virtual visits. The ability of patients to handle their own scheduling and billing frees provider staff, restoring valuable time.

NextGen® Patient Portal – Drives patient engagement and satisfaction with easy, intuitive, 24/7 access to payments, scheduling, complete personal health information, and communication. It facilitates and simplifies comprehensive information exchange, offering anytime, anywhere access from PCs, tablets, and smart phones.

NextGen Self Scheduling™ A fully-integrated self-scheduling application that empowers patients to schedule the visit that works best for them with configurations that allow the practice to control virtually every facet of that interaction from visit-specific screening questions to provider-specific scheduling preferences.

NextGen® Patient Pay – Allows patients one integrated solution that delivers an integrated point of sale, credit card on file, automated payment collection, online and mobile compatible automated phone pay and kiosk payments.

NextGen Virtual Visits™ (formerly known as OTTO Health) - Delivers a tightly integrated, bi-directional telehealth experience that allows patients to have a virtual visit with their own provider’s care team. The solution allows for screen-sharing, document passing, in-visit chat, one-touch access to interpretive services, and a "no-login" experience for patients.

7

Table of Contents

Clinical Care Solutions improve the quality and efficiency of care delivery as well as the patient and provider experience. They significantly ease the administrative burden and enable the delivery of high quality, personalized care. Providers can automate patient intake, streamline clinical workflows, and leverage vendor-agnostic interoperability to achieve quality measures and qualify for incentives.

NextGen® Enterprise EHR – Our electronic health records solution stores and maintains clinical patient information and offers a workflow module, prescription management, automatic document and letter generation, patient education, referral tracking, interfaces to billing and lab systems, physician alerts and reminders, and reporting and data analysis tools.

NextGen® Mobile (formerly known as Entrada®) – Enables physicians and other caregivers to quickly and easily create relevant documentation within the EHR without sacrificing productivity. A true EHR mobile experience, the platform provides a fast, easy way for caregivers to view and share real-time clinical content and complete key tasks directly from their mobile device.

NextGen® Office (formerly known as Meditouch®) – A cloud-based EHR and PM solution for physicians and medical billing services designed to meet the specific needs of smaller practices. Received top score for Overall Satisfaction and Product Functionality in the 2019 KLAS Small Practice Ambulatory EMR/PM (10 or fewer physicians) Report.

Financial Management Solutions are comprised of software and key analytics that allow clients to drive healthy, predictable financial outcomes. More than just billing and collection services, financial management involves all functions that effectively capture revenue at the lowest cost, while providing an efficient experience for the patient. Financial management solutions help practices improve performance and correct operational inefficiencies, while enhancing the practice’s financial outcomes throughout the revenue cycle.

NextGen® Enterprise PM – Our practice management offering is a seamlessly integrated, scalable, multi-module solution that includes a master patient index, enterprise-wide appointment scheduling with referral tracking, and clinical support. It was recognized as the #1 Practice Management Solution (11-75 Physicians) in 2019 and 2020 Best in KLAS Report.

NextGen® Electronic Healthcare Transactions – Automates the exchange of electronic data among providers, payers and patients. Included in this offering are insurance eligibility, authorizations, electronic claims, remittance, patient appointment reminders, and electronic statements.

Population Health Solutions enable our clients’ practices to focus their clinical workforce on the patients with the greatest need. We do this by providing a single source of truth by aggregating disparate data, including vendor-agnostic clinical data with paid claims data. Sophisticated analytics are applied to this data to generate insights that enable practices to improve the quality of care, identify high risk patients who require enriched services, and coordinate the care of patients with chronic conditions. Cost and utilization analytics allow practices to successfully participate in risk-bearing contracts by providing timely insights into areas of over-utilization, under-utilization and mis-utilization of healthcare resources.

NextGen® Population Health Analytics (formerly known as Eagle Dream Health) – Delivers robust capabilities for core population health insights using integrated clinical and claims data to support both broad and deep analysis for populations of interest (attribute visualization, risk stratification, gaps in care, etc.).

NextGen® Population Health Performance Management – Supports proactive value-based contract management including network management (leakage/keepage), network design (geospatial view of network), clinical variation analysis, and a wide range of resource utilization metrics.

NextGen® Population Health Patient Care Management – Enables scalable management of care and payment reform initiatives driven by collaborative care and workflow automation. Stratifies risk and prioritizes resources. The platform provides a dynamic patient specific care plan builder as well as a longitudinal care management record, and dedicated care management future reminder and tasking tools. A unique feature of our offering includes analytics driven patient outreach facilitating care coordinators’ ability to automate communications with patients based on quality initiatives and value-based contract commitments.

8

Table of Contents

Connected Health Solutions enable better care by ensuring the patient and provider are making decisions based on the patient’s full medical record. Interoperability is the ability of different information technology systems to communicate and exchange usable data. In healthcare, it enables caregivers to more effectively work together within and across organizational boundaries, and informed patients to be better equipped to collaborate on their own care. To provide the highest quality care at the lowest cost, organizations must capture and share information both within and across organizational boundaries outside their networks. In addition, interoperability must be frictionless and easy to implement or the opportunity to inform patient care will be missed. Our integrated, interoperable solutions and services enable providers to leverage their current technology for better outcomes and truly connected patient care.

NextGen® Connect Integration Engine – Enables patient data from disparate systems to be easily and securely shared, aggregated, and put to work, regardless of EHR, PM, or other HIT platform or location.

NextGen® Share – A broad and expanding suite of plug-and-play interoperability solutions which help NextGen® Enterprise EHR users safely and securely exchange clinical content with external providers and organizations. The platform includes support for secure direct messaging with more than 1.2 million providers and organizations, care quality integration to enable automated data exchange on behalf of nearly 240 million patients, and clinical data exchange interfaces with payers.

NextGen® Health Data Hub (HDH) – A fully redesigned data aggregation platform to meet the expanding market demand for robust data sharing, aggregation, and community access. HDH was built from the ground-up to provide comprehensive, continuous access to aggregated patient health data on a robust, reliable, platform that will enable system-wide connectivity, and support the growing enterprise data management needs for HIEs, hospitals and large ambulatory practices.

NextGen Healthcare provides real-world solutions to our clients to help them achieve their strategic objectives. Often, but not always, those software solutions are augmented with key services. Through these services we enable clients to perform better financially and focus on their primary mission of providing efficient and high-quality patient care. We believe COVID-19 will increase client appetite to outsource non-core services and that NextGen is well-positioned to be their partner in these areas.

Managed Services

NextGen® Managed Cloud Services – Our scalable, cloud hosting services reduce the burden of information technology expertise from our clients and speed implementations, simplify upgrades, cut technology costs significantly and provide 24/7 monitoring and support by a broad and constantly expanding team of technical experts

NextGen® Revenue Cycle Management Services (formerly known as NextGen® Financial Suite) – Includes billing and collections, electronic claims submission and denials management, electronic remittance and payment posting and accounts receivable follow-up. Our dedicated account management model helps make NextGen Healthcare a top-performing provider of RCMS as reported in the 2020 KLAS Ambulatory RCM Services Report.

Professional Services – Services include training, project management, functional and detailed specification preparation, configuration, testing, and installation services. Our consulting services, which include physician, professional, and technical consulting, assisting clients to optimize their staffing and software solutions, enhance financial and clinical outcomes, achieve regulatory requirements in the drive to value-based care, and meet the evolving requirements of healthcare reform.

Client Service and Support – Our technical services staff provides support for the dependable and timely resolution of technical inquiries from clients. Such inquiries are made via telephone, email and the internet. We offer several levels of support, with the most comprehensive service covering 24 hours a day, seven days a week.

Proprietary Rights

We rely on a combination of patents, copyrights, trademarks, service marks, trade secrets, and contractual restrictions to establish and protect proprietary rights in our products and services. To protect our proprietary rights, we enter into confidentiality agreements and invention assignment agreements with our employees with whom such controls are relevant. In addition, we include intellectual property protective provisions in our client contracts. However, because the software industry is characterized by rapid technological change, we believe such factors as the technological and creative skills of our personnel, new product developments, frequent product enhancements, name recognition, and reliable product maintenance are more important to establishing and maintaining a technology leadership position than the various legal protections of our technology.

We rely on software that we license from third parties for certain components of our products and services. These components enhance our products and services and help meet evolving client needs. The failure to license any necessary technology, or to maintain our existing licenses, could result in reduced functionality of or reduced demand for our products.

Although we believe our products and services, and other proprietary rights, do not infringe upon the proprietary rights of third parties, third parties may assert intellectual property infringement claims against us in the future. Any such claims may result in costly, time-consuming litigation and may require us to enter into royalty or cross-license arrangements.

9

Table of Contents

Competition

The markets for healthcare information systems and services are intensely competitive and highly fragmented. Our traditional full-suite competitors in the healthcare information systems and services market include: Allscripts Healthcare Solutions, Inc., athenahealth, Inc., Cerner Corporation, eClinicalWorks, Epic Systems Corporation, and Greenway Health, LLC. Emerging smaller competitors also bring competition in specific sectors of the market. Additionally, we face competition from services-only competitors like business process outsourcers, hosting providers and transcription companies.

The EHR, PM, interoperability, and connectivity markets, in particular, are subject to rapid changes in technology. We expect that competition in these market segments could increase as new competitors enter the market. We believe our principal competitive advantages are our ambulatory-only focus, our comprehensive and fully-integrated solution, and our deep domain expertise, which enables our subject matter experts to serve as trusted advisors to our clients.

Privacy and Security

Our business operations involve hosting, storing, processing and transmitting confidential information including patient health information and payment card information. In addition to single-tenant environments, we operate unified, multi-tenant platforms that offer reliability, scalability, performance, security and privacy for our clients. Our infrastructure resides in several geographically diverse regions across the United States. We maintain a comprehensive security program designed to help safeguard the confidentiality, integrity and availability of our clients’ data, which includes both organizational and technical control measures and the security and privacy of our service offerings. We also have systems in place to monitor the safety of patient information as well as procedures designed to take immediate action.

We have the industry’s most well-known certifications for payment card and healthcare data. Including Payment Card Industry Data Security Standard (PCI-DSS) Level 1 Service Provider, Security Organization Control 2, or SOC 2 Type II, DirectTrust Health Information Service Provider (HISP), and HITRUST Common Security Framework (CSF). These certifications give our clients third-party assurance we are meeting or exceeding Health Insurance Portability and Accountability Act (HIPAA) guidelines. As a PCI-DSS Level 1 Service Provider, we are committed to upholding industry security standards to cardholder data. The Level 1 PCI compliance allows us to minimize clients’ PCI scope.

While we have implemented physical, technical, and administrative safeguards designed to help protect our systems, in the event of a system interruption, security incident, or breach, these safeguards may not prevent future cybersecurity incidents or breaches. We have a comprehensive and documented Information Security Management Program designed to secure the data within our infrastructure and provide appropriate reporting disclosure, and response. In addition, all of our associates are required to complete annual cybersecurity training, HIPAA training, and PCI DSS training. These training modules are reviewed annually to ensure compliance with the latest regulatory guidelines, laws, and industry best practices.

Managing Cybersecurity Risks

Our business operations involve hosting, storing, processing and transmitting confidential information including patient health information. We have implemented physical, technical, and administrative safeguards designed to help protect our systems, in the event of a system interruption, security incident, or breach. However, these safeguards may not prevent future cybersecurity incidents or breaches. We have a comprehensive and documented Information Security Management Program designed to secure the data within our infrastructure and provide appropriate reporting disclosure, and response. In addition, all of our associates are required to complete annual cybersecurity training, HIPAA training, and PCI DSS training. These training modules are reviewed annually to ensure compliance with the latest regulatory guidelines, laws, and industry best practices.

Research and Development

The healthcare information systems and services industry is characterized by rapid technological change, requiring us to engage in continuing investments in our research and development to update, enhance and improve our systems. This includes expansion of our software and service offerings that support pay-for-performance initiatives around accountable care organizations, bringing greater ease of use and intuitiveness to our software products, enhancing our managed cloud and hosting services to lower our clients' total cost of ownership, expanding our interoperability and enterprise analytics capabilities, and furthering development and enhancements of our portfolio of specialty-focused templates within our electronic health records software.

10

Table of Contents

Sales and Marketing

We sell and market our products primarily through a direct sales force and to a significantly lesser extent, through a reseller channel. NextGen Healthcare also provides solutions to networks of practices such as MSOs, IPAs, ACOs, ambulatory care centers (“ACCs”), and community health centers (“CHCs”). Our direct sales force is comprised of sales executives and account executives, who seek to understand the client strategy and identify the opportunities in their practice and build both a multistage roadmap to reach the desired end state. For large clients, we use both inside and outside sales where efforts are a mix of on-site as well as web based. For smaller clients, efforts are all inside sales via web and phone, all of whom deliver presentations to potential clients by demonstrating our systems and capabilities either on prospective client’s premises or through video meeting and web-based presentations. System demonstrations for mobile workflow and analytics solutions are more web-based as these offerings tend to be targeted to larger practices. Both the direct and reseller channel salesforces concentrate on multi-product/solution sales opportunities. Our sales and marketing employees identify prospective clients through a variety of means, including: a healthcare data and analytics platform, search engine optimization and value exchange content on nextgen.com; digital advertising; direct mail and email campaigns; referrals from existing clients and industry consultants; contacts at professional society meetings and trade shows; webinars; public relations and social media campaigns; and telemarketing. Resources have shifted more heavily to digital marketing as we meet potential clients where they are and how they shop for services. Additionally, we focus on thought leadership and content marketing to highlight our industry knowledge, expertise and the successes of our diverse client base. On the larger end of the range, our sales cycle can vary significantly and typically ranges from six to 18 months from initial contact to contract execution. Smaller practices on NextGen Office tend to have significantly shorter sales cycles ranging in weeks. Historically, software licenses are normally delivered to a client almost immediately upon receipt of an order and we normally receive up-front licensing fees. Implementation and training services are normally rendered based on a mutually agreed upon timetable. Moving forward, we expect more of our transactions to move to subscriptions. Clients have the option to purchase hosting and maintenance services which, are invoiced on a monthly, quarterly or annual basis. Subscriptions are delivered electronically after the agreement is signed. They generally include implementation and are typically billed monthly after implementation or based on volume or throughput. We continue to concentrate our direct sales and marketing efforts on the ambulatory market from large multi-specialty organizations to small-single specialty practices in high-opportunity specialty segments.

We have numerous clients and do not believe that the loss of any single client would adversely affect us. No client accounted for 10% or more of our net revenue during each of the years ended March 31, 2020, 2019 and 2018. In addition, software license sales to resellers represented less than 10% of total revenue for each of the years ended March 31, 2020, 2019 and 2018. Substantially all of our clients are located in the United States.

Employees

As of March 31, 2020, we had approximately 2,754 full-time employees, of which 758 were based in Bangalore, India and substantially all other employees were based in the United States. We believe that our future success depends in part upon recruiting and retaining qualified sales, marketing and technical talent as well as other employees. None of our employees are covered by a collective bargaining agreement or are represented by a labor union.

Available Information

Our principal website is www.nextgen.com. We make our periodic and current reports, together with amendments to these reports, filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended, available on our website, free of charge, as soon as reasonably practicable after such material is electronically filed with, or furnished to, the SEC. You may access such filings through our Investor Relations website at http://investor.nextgen.com. The SEC maintains an internet site at www.sec.gov that contains the reports, proxy statements and other information that we file electronically with the SEC. Our website and the information contained therein or connected thereto is not intended to be incorporated into this Report or any other report or information we file with the SEC. We also use the following social media channels as a means of disclosing information about the company, our platform, our planned financial and other announcements and attendance at upcoming investor and industry conferences:

| • | NextGen Healthcare Twitter Account (https://twitter.com/NextGen?s=20) |

| • | NextGen Healthcare Company Blog (https://www.nextgen.com/blog) |

| • | NextGen Healthcare Facebook Page (https://www.facebook.com/NextGenHealthcare) |

| • | NextGen Healthcare LinkedIn Page (https://www.linkedin.com/company/nextgenhealthcareinc/) |

| • | NextGen Healthcare Instagram Page (https://www.instagram.com/nextgenhealthcare/) |

| • | NextGen Healthcare YouTube Page (https://www.youtube.com/user/nghisinc) |

We encourage our investors and others to review the information we make public in these locations as such information could be deemed to be material information. Please note that this list may be updated from time to time.

11

Table of Contents

ITEM 1A. RISK FACTORS

You should carefully consider the risks described below, as well as the other cautionary statements and risks described elsewhere and the other information contained in this Report and in our other filings with the SEC, including subsequent Quarterly Reports on Form 10-Q and Current Reports on Form 8-K. We operate in a rapidly changing environment that involves a number of risks. The risks and uncertainties described below are not the only ones we face. Additional risks and uncertainties not presently known to us or that we currently deem immaterial may also affect our business operations. If any of these known or unknown risks actually occur, our business, financial condition or results of operations could be materially and adversely affected, in which case the trading price of our common stock may decline and you may lose all or part of your investment.

Risks Related to Our Business

The extent to which the COVID-19 pandemic and measures taken in response thereto could adversely affect our financial condition, future bookings, and results of operations will depend on future developments, which are highly uncertain and are difficult to predict. The COVID-19 global pandemic and efforts to control its spread have significantly curtailed the movement of people, goods and services in the United States and worldwide. The impact of the outbreak has been rapidly evolving in the United States and other countries, including India where we have significant operations, and has led to the implementation of various responses, including government-imposed quarantines, travel restrictions, business and school closures, government-imposed postponements of non-life threatening medical procedures, and other public health safety measures. We have modified our business practices accordingly (for example, restricting employee travel, moving the vast majority of our employees to remote working, cancelling and postponing meetings, events, and conferences, and so forth). There is no certainty that such measures will be sufficient to mitigate the risks posed by the virus, and our ability to perform critical functions could be harmed.

The magnitude and duration of the disruption and decline in business activity due to COVID-19 is uncertain. We may experience a negative financial impact due to a number of factors, including without limitation:

| • | A general decline in business activity including the impact of our clients’ office closures; |

| • | A disproportionate impact on the healthcare groups and other healthcare professionals with whom we contract; |

| • | Financial pressures on our clients, which may in turn result in their deferment of purchase decisions, or a delay in collections or non-payment; |

| • | Declines in new business bookings as our clients reduce or delay purchasing decisions; |

| • | Extensions of the length of sales and implementation cycles; |

| • | Disruptions to our supply chains and our third-party vendors, partners, and suppliers |

| • | Difficulty accessing the capital and credit markets on favorable terms, or at all, and a severe disruption and instability in the global financial markets, or deteriorations in credit and financing conditions which could affect our access to capital necessary to fund business operations and address maturing liabilities on a timely basis; |

| • | The potential negative impact on the health or productivity of employees, especially if a significant number of them are impacted; |

| • | Disruptions and expense due to employee terminations; |

| • | A deterioration in our ability to ensure business continuity during a disruption; |

| • | Social, economic, and labor instability in India where we have significant operations. |

The extent to which the COVID-19 pandemic will impact our financial condition and results of operations will depend on future developments, which are highly uncertain and difficult to predict, including but not limited to the duration and spread of the pandemic, its severity, the actions to contain the virus or treat its impact, its impact on our strategic investments, and how quickly and to which extent normal economic and operating conditions can resume. Even after the COVID-19 pandemic has subsided, we may experience material adverse impacts to our business as a result of the global or U.S. economic impact and any recession that has occurred or may occur in the future. There are no comparable recent events that provide guidance as to the effect the COVID-19 pandemic may have and, as a result, the ultimate impact of the pandemic on our operations and financial results is highly uncertain and subject to change.

Additionally, concerns over the economic impact of the COVID-19 pandemic have caused extreme volatility in financial and capital markets which has and may continue to adversely impact our stock price and may adversely impact our ability to access capital markets.

The rapid development and fluidity of the pandemic situation precludes any prediction as to the ultimate adverse impact of COVID-19. This uncertainty has and may continue to affect our results of operations, financial condition and cash flows.

12

Table of Contents

We face significant, evolving competition which, if we fail to properly address, could adversely affect our business, results of operations, financial condition and price of our stock. The markets for healthcare information systems are intensely competitive, and we face significant competition from a number of different sources. Several of our competitors have substantially greater name recognition and financial, technical, product development and marketing resources than we do. There has been significant merger and acquisition activity among a number of our competitors in recent years. Some of our larger competitors, who have greater scale than we do, have and may continue to become more active in our markets both through internal development and acquisitions. Transaction induced pressures, or other related factors may result in price erosion or other negative market dynamics that could adversely affect our business, results of operations, financial condition and price of our stock.

We compete in all of our markets with other major healthcare related companies, information management companies, systems integrators and other software developers. Competition in our markets occurs on the basis of several factors, including price, innovation, client service, product quality and reliability, scope of services, industry acceptance, and others. Competitive pressures and other factors, such as new product introductions by us or our competitors, may result in price or market share erosion that could adversely affect our business, results of operations and financial condition. Also, there can be no assurance that our applications will achieve broad market acceptance or will successfully compete with other available software products. If we fail to distinguish our offerings from other options available to healthcare providers, the demand for and market share of our offerings may decrease.

Saturation or consolidation in the healthcare industry could result in the loss of existing clients, a reduction in our potential client base and downward pressure on the prices for our products and services. As the healthcare information systems market evolves, saturation of this market with our products or our competitors' products could limit our revenues and opportunities for growth. There has also been increasing consolidation amongst healthcare industry participants in recent years, creating integrated healthcare delivery systems with greater market power. As provider networks and managed care organizations consolidate, the number of market participants decreases and competition to provide products and services like ours will become more intense. The importance of establishing relationships with key industry participants will become greater and our inability to make initial sales of our systems to, or maintain relationships with, newly formed groups and/or healthcare providers that are replacing or substantially modifying their healthcare information systems could adversely affect our business, results of operations and financial condition. These consolidated industry participants may also try to use their increased market power to negotiate price reductions for our products and services. If we were forced to reduce our prices, our business would become less profitable unless we were able to achieve corresponding reductions in our expenses.

Many of our competitors have greater resources than we do. In order to compete successfully, we must keep pace with our competitors in anticipating and responding to the rapid changes involving the industry in which we operate, or our business, results of operations and financial condition may be adversely affected. The software market generally is characterized by rapid technological change, changing client needs, frequent new product introductions and evolving industry standards. The introduction of products incorporating new technologies and the emergence of new industry standards could render our existing products obsolete and unmarketable. There can be no assurance that we will be successful in developing and marketing new products that respond to technological changes or evolving industry standards. New product development depends upon significant research and development expenditures which depend ultimately upon sales growth. Any material shortfall in revenue or research funding could impair our ability to respond to technological advances or opportunities in the marketplace and to remain competitive. If we are unable, for technological or other reasons, to develop and introduce new products in a timely manner in response to changing market conditions or client requirements, our business, results of operations and financial condition may be adversely affected.

In response to increasing market demand, we are currently developing new generations of targeted software products. There can be no assurance that we will successfully develop these new software products or that these products will operate successfully, or that any such development, even if successful, will be completed concurrently with or prior to introduction of competing products. Any such failure or delay could adversely affect our competitive position or could make our current products obsolete.

13

Table of Contents

Uncertainty in global economic and political conditions may negatively impact our business, operating results or financial condition. Global economic and political uncertainty have caused in the past, and may cause in the future, unfavorable business conditions such as a general tightening in the credit markets, lower levels of liquidity, increases in the rates of default and bankruptcy and extreme volatility in credit, equity and fixed income markets. These macroeconomic conditions could negatively affect our business, operating results or financial condition in a number of ways. Instability can make it difficult for our clients, our vendors, and us to accurately forecast and plan future business activities and could cause constrained spending on our products and services, delays and a lengthening of our sales cycles and/or difficulty in collection of our accounts receivable. Current or potential clients may be unable to fund software purchases, which could cause them to delay, decrease or cancel purchases of our products and services or to not pay us or to delay paying us for previously purchased products and services. Our clients may cease business operations or conduct business on a greatly reduced basis. Bankruptcies or similar insolvency events affecting our clients may cause us to incur bad debt expense at levels higher than historically anticipated. Further, economic instability could limit our ability to access the capital markets at a time when we would like, or need, to raise capital, which could have an impact on our ability to react to changing business conditions or new opportunities. Finally, our investment portfolio is generally subject to general credit, liquidity, counterparty, market and interest rate risks that may be exacerbated by these global financial conditions. If the banking system or the fixed income, credit or equity markets deteriorate or remain volatile, our investment portfolio may be impacted and the values and liquidity of our investments could be adversely affected as well.

Our relationships with strategic partners may fail to benefit us as expected. We face risk and/or the possibility of claims from activities related to strategic partners, which could be expensive and time-consuming, divert personnel and other resources from our business and result in adverse publicity that could harm our business. We rely on third parties to provide services for our business. For example, we use national clearinghouses in the processing of some insurance claims and we outsource some of our hardware services and the printing and delivery of patient statements for our clients. These third parties could raise their prices and/or be acquired by our competitors, which could potentially create short and long-term disruptions to our business, negatively impacting our revenue, profit and/or stock price. We also have relationships with certain third parties where these third parties serve as sales channels through which we generate a portion of our revenue. Due to these third-party relationships, we could be subject to claims as a result of the activities, products, or services of these third-party service providers even though we were not directly involved in the circumstances leading to those claims. Even if these claims do not result in liability to us, defending and investigating these claims could be expensive and time-consuming, divert personnel and other resources from our business and result in adverse publicity that could harm our business. In addition, our strategic partners may compete with us in some or all of the markets in which we operate.

We have acquired companies, and may engage in future acquisitions, which may be expensive, time consuming, subject to inherent risks and from which we may not realize anticipated benefits. Historically, we have acquired numerous businesses, technologies, and products. We may acquire additional businesses, technologies and products if we determine that these additional businesses, technologies and products are likely to serve our strategic goals. Acquisitions have inherent risks, which may have a material adverse effect on our business, financial condition, operating results or prospects, including, but not limited to the following:

| • | failure to achieve projected synergies and performance targets; |

| • | potentially dilutive issuances of our securities, the incurrence of debt and contingent liabilities and amortization expenses related to intangible assets with indefinite useful lives, which could adversely affect our results of operations and financial condition; |

| • | using cash as acquisition currency may adversely affect interest or investment income, which may in turn adversely affect our earnings and /or earnings per share; |

| • | unanticipated expenses or difficulty in fully or effectively integrating or retaining the acquired technologies, software products, services, business practices, management teams or personnel, which would prevent us from realizing the intended benefits of the acquisition; |

| • | failure to maintain uniform standard controls, policies and procedures across acquired businesses; |

| • | difficulty in predicting and responding to issues related to product transition such as development, distribution and client support; |

| • | the possible adverse effect of such acquisitions on existing relationships with third party partners and suppliers of technologies and services; |

| • | the possibility that staff or clients of the acquired company might not accept new ownership and may transition to different technologies or attempt to renegotiate contract terms or relationships, including maintenance or support agreements; |

| • | the assumption of known and unknown liabilities; |

| • | the possibility of disputes over post-closing purchase price adjustments such as performance-based earnouts; |

14

Table of Contents

| • | the possibility that the due diligence process in any such acquisition may not completely identify material issues associated with product quality, product architecture, product development, intellectual property issues, regulatory risks, compliance risks, key personnel issues or legal and financial contingencies, including any deficiencies in internal controls and procedures and the costs associated with remedying such deficiencies; |

| • | difficulty in entering geographic and/or business markets in which we have no or limited prior experience; |

| • | difficulty in integrating acquired operations due to geographical distance and language and cultural differences; |

| • | diversion of management's attention from other business concerns; and |

| • | the possibility that acquired assets become impaired, or that acquired assets lead us to determine that existing assets become impaired, requiring us to take a charge to earnings which could be significant. |

A failure to successfully integrate acquired businesses or technology could, for any of these reasons, have an adverse effect on our financial condition and results of operations.

Our failure to manage growth could harm our business, results of operations and financial condition. We have in the past experienced periods of growth which have placed, and may continue to place, a significant strain on our non-cash resources. We have also expanded our overall software development, marketing, sales, client management and training capacity, and may do so in the future. In the event we are unable to identify, hire, train and retain qualified individuals in such capacities within a reasonable timeframe, such failure could have an adverse effect on the operation of our business. In addition, our ability to manage future increases, if any, in the scope of our operations or personnel will depend on significant expansion of our research and development, marketing and sales, management and administrative and financial capabilities. The failure of our management to effectively manage expansion in our business could have an adverse effect on our business, results of operations and financial condition.

We may experience reduced revenues and/or be forced to reduce our prices. We may be subject to pricing pressures with respect to our future sales arising from various sources, including amount other things, government action affecting reimbursement levels. Our clients and the other entities with which we have business relationships are affected by changes in statutes, regulations, and limitations on government spending for Medicare, Medicaid, and other programs. Recent government actions and future legislative and administrative changes could limit government spending for Medicare and Medicaid programs, limit payments to healthcare providers, increase emphasis on competition, impose price controls, initiate new and expanded value-based reimbursement programs and create other programs that potentially could have an adverse effect on our business. If we experience significant downward pricing pressure, our revenues may decline along with our ability to absorb overhead costs, which may leave our business less profitable.

Our operations are dependent upon attracting and retaining key personnel. If such personnel were to leave unexpectedly, we may not be able to execute our business plan. Our future performance depends in significant part upon the continued service of our key development and senior management personnel and successful recruitment of new talent. These personnel have specialized knowledge and skills with respect to our business and our industry. Because we have a relatively small number of employees when compared to other leading companies in our industry, our dependence on maintaining our relationships with key employees and successful recruiting is particularly significant.

The industry in which we operate is characterized by a high level of employee mobility and aggressive recruiting of skilled personnel. There can be no assurance that our current employees will continue to work for us. Loss of services of key employees could have an adverse effect on our business, results of operations and financial condition. Furthermore, we may need to grant additional equity incentives to key employees and provide other forms of incentive compensation to attract and retain such key personnel. Equity incentives may be dilutive to our per share financial performance. Failure to provide such types of incentive compensation could jeopardize our recruitment and retention capabilities.

We may be subject to harassment or discrimination claims and legal proceedings, and our inability or failure to respond to and effectively manage publicity related to such claims could adversely impact our business. Our Code of Business Conduct and Ethics and other employment policies prohibit harassment and discrimination in the workplace, in sexual or in any other form. We have ongoing programs for workplace training and compliance, and we investigate and take disciplinary action with respect to alleged violations. However, actions by our employees could violate those policies. With the increased use of social media platforms, including blogs, chat platforms, social media websites, and other forms of Internet-based communications that allow individuals access to a broad audience, there has been an increase in the speed and accessibility of information dissemination. The dissemination of information via social media, including information about alleged harassment, discrimination or other claims, could harm our business, brand, reputation, financial condition, and results of operations, regardless of the information's accuracy.

Our recent strategy shift and the resulting business reorganization plan we are implementing may be disruptive both internally and externally, and we may not fully realize the anticipated benefits. We recently embarked on a new strategic plan geared toward realigning our business structure and strategy to rapidly emerging changes in the healthcare industry. As this process continues, we anticipate that it will result in continued evaluation of our organizational structure in order to achieve greater efficiency, as well as investments in new market solutions and changes to our culture that we hope will drive revenue growth and provide increased value to stakeholders and shareholders. There can be no assurance that our current or future strategic realignment efforts will be successful. Our ability to achieve the anticipated benefits of our strategy shift is subject to

15

Table of Contents

estimates and assumptions, which may vary based on numerous factors and uncertainties, some of which are beyond our control. Reorganization programs entail a variety of known and unknown risks that may increase our costs or impair our ability to achieve operational efficiencies, such as distraction to management and employees, loss of workforce capabilities, loss of continuity, accounting charges for technology-related write-offs and workforce reduction costs, decreases in employee focus and morale, uncertainty and turbulence among our clients and vendors, higher than anticipated separation expenses, litigation, and the failure to meet financial and operational targets. If we are unable to effectively implement our strategic shift and realign our business to address the rapidly evolving market, we and our shareholders may not realize the anticipated financial, operational, and other benefits from these initiatives.

If we are unable to manage our growth in the new markets we may enter, our business and financial results could suffer. Our future financial results will depend in part on our ability to profitably manage our business in new markets that we may enter. We are engaging in the strategic identification of, and competition for, growth and expansion opportunities in new markets or offerings, including but not limited to the areas of interoperability, patient engagements, data analytics and population health. With several of our recent acquisitions, we have expanded into the market for cloud-based EHR products. It remains uncertain whether the market for cloud-based products will expand to the levels of demand and market acceptance we anticipate, and there can be no assurance that we will be able to successfully scale the acquired companies’ products to meet our clients’ expectations. In addition, as clients move from fee-for-service to fee-for-value reimbursement strategies in conjunction with the adoption of population health business models, we may not make appropriate and timely changes to our service offerings consistent with shifts in market demands and expectations. In order to successfully execute on our growth initiatives, we will need to, among other things, manage changing business conditions, anticipate and react to changes in the regulatory environment, and develop expertise in areas outside of our business's traditional core competencies. Difficulties in managing future growth in new markets could have a significant negative impact on our business, financial condition and results of operations.

We may not be successful in developing or launching our new software products and services, which could have a negative impact on our financial condition and results of operations. We invest significant resources in the research and development of new and enhanced software products and services. Over the last few years we have incurred, and will continue to incur, significant internal research and development expenses, a portion of which have been and may continue to be recorded as capitalized software costs. We cannot provide assurances that we will be successful in our efforts to plan, develop or sell new software products that meet client expectations, which could result in an impairment of the value of the related capitalized software costs, an adverse effect on our financial condition and operating results and a negative impact the future of our business. Additionally, we cannot be assured that we will continue to capitalize software development costs to the same extent as we have done to date, as the result of changes in development methodologies and other factors. To the extent that we capitalize a lower percentage of total software development costs, our earnings could be reduced.

We have substantial development and other operations in India, and we use offshore third-party partners located in India and other countries that subject us to regulatory, economic, social and political uncertainties in India and to laws applicable to U.S. companies operating overseas. We are subject to several risks associated with having a portion of our assets and operations located in India and by using third party service providers in India and other countries. Many U.S. companies have benefited from many policies of the Government of India and the Indian state governments in the states in which we operate, which are designed to promote foreign investment generally and the business process services industry in particular, including significant tax incentives, relaxation of regulatory restrictions, liberalized import and export duties and preferential rules on foreign investment and repatriation. There is no assurance that such policies will continue. Various factors, such as changes in the current Government of India, could trigger significant changes in India’s economic liberalization and deregulation policies and disrupt business and economic conditions in India generally and our business in particular. In addition, our financial performance and the market price of our common stock may be adversely affected by general economic conditions and economic and fiscal policy in India, including changes in exchange rates and controls, interest rates and taxation policies, as well as social stability and political, economic or diplomatic developments affecting India in the future. In particular, India has experienced significant economic growth over the last several years, but faces major challenges in sustaining that growth in the years ahead. These challenges include the need for substantial infrastructure development and improving access to healthcare and education. Our ability to recruit, train and retain qualified employees, develop and operate our captive facility could be adversely affected if India does not successfully meet these challenges. In addition, U.S. governing authorities may pressure us to perform work domestically rather than using offshore resources. Furthermore, local laws and customs in India may differ from those in the U.S. For example, it may be a local custom for businesses to engage in practices that are prohibited by our internal policies and procedures or U.S. laws and regulations applicable to us, such as the Foreign Corrupt Practices Act (“FCPA”). The FCPA generally prohibits U.S. companies from giving or offering money, gifts, or anything of value to a foreign official to obtain or retain business and requires businesses to make and keep accurate books and records and a system of internal accounting controls. We cannot guarantee that our employees, contractors, and agents will comply with all of our FCPA compliance policies and procedures. If we or our employees, contractors, or agents fail to comply with the requirements of the FCPA or similar legislation, government authorities in the U.S. and elsewhere could seek to impose civil or criminal fines and penalties which could have a material adverse effect on our business, operating results, and financial condition.

16

Table of Contents

We face the risks and uncertainties that are associated with litigation and investigations, which may adversely impact our marketing, distract management and have a negative impact upon our business, results of operations and financial condition. We face the risks associated with litigation and investigations concerning the operation of our business, including claims by clients regarding product and contract disputes, by other third parties asserting infringement of intellectual property rights, by current and former employees regarding certain employment matters, by certain shareholders, and by governmental and regulatory bodies for failures to comply with applicable laws. The uncertainty associated with substantial unresolved disputes may have an adverse effect on our business. In particular, such disputes could impair our relationships with existing clients and our ability to obtain new clients. Defending litigation and investigative matters may require substantial cost and may result in a diversion of management's time and attention away from business operations, which could have an adverse effect on our business, results of operations and financial condition.