UNITED STATES SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| | For the fiscal year ended: December 31, 2007 |

| OR | |

| | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| o | For the transition period from __________ to __________ |

Commission File Number 0-11244

| GERMAN AMERICAN BANCORP, INC. |

| (Exact name of registrant as specified in its charter) |

| INDIANA | | 35-1547518 |

| (State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

| 711 Main Street, Box 810, Jasper, Indiana | | 47546 |

| (Address of Principal Executive Offices) | | (Zip Code) |

Registrant’s telephone number, including area code: (812) 482-1314

Securities registered pursuant to Section 12 (b) of the Act

| Title of Each Class | | Name of each exchange on which registered |

| Common Shares, No Par Value | | |

| Preferred Stock Purchase Rights | | The NASDAQ Stock Market LLC |

Securities registered pursuant to Section 12(g) of the Act: None

| Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. | o Yes | x No |

| | | |

| Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. | o Yes | x No |

| | | |

| Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. | x Yes | o No |

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K: o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer or a non-accelerated filer, or a smaller reporting company:

Large accelerated filer o Accelerated filer x Non-accelerated filer o Smaller reporting company o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). o Yes x No

The aggregate market value of the registrant’s common shares held by non-affiliates of the registrant, computed by reference to the price at which the common shares were last sold, as of June 30, 2007 (the last business day of the registrant’s most recently completed second fiscal quarter) was approximately $142,378,000. This calculation does not reflect a determination that persons are affiliates for any other purposes.

As of March 1, 2008, there were outstanding 11,029,484 common shares, no par value, of the registrant.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Proxy Statement of German American Bancorp, Inc., for the Annual Meeting of its Shareholders to be held April 24, 2008, to the extent stated herein, are incorporated by reference into Part III.

GERMAN AMERICAN BANCORP, INC.

ANNUAL REPORT ON FORM 10-K

For Fiscal Year Ended December 31, 2007

Table of Contents

PART I | | |

| Item 1. | Business | 3-6 |

| Item 1A. | Risk Factors | 6-8 |

| Item 1B. | Unresolved Staff Comments | 8 |

| Item 2. | Properties | 8 |

| Item 3. | Legal Proceedings | 8 |

| Item 4. | Submission of Matters to a Vote of Security Holders | 8 |

| | | |

PART II | | |

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 9-10 |

| Item 6. | Selected Financial Data | 11 |

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 12-28 |

| Item 7A. | Quantitative and Qualitative Disclosures About Market Risk | 29 |

| Item 8. | Financial Statements and Supplementary Data | 30-64 |

| Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 65 |

| Item 9A. | Controls and Procedures | 65 |

| Item 9B. | Other Information | 65 |

| | | |

PART III | | |

| Item 10. | Directors and Executive Officers of the Registrant | 66 |

| Item 11. | Executive Compensation | 66 |

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | |

| Item 13. | Certain Relationships and Related Transactions | 67 |

| Item 14. | Principal Accountant Fees and Services | 67 |

| | | |

PART IV | | |

| Item 15. | Exhibits and Financial Statement Schedules | 68 |

| | | |

| SIGNATURES | 69 |

| | |

| INDEX OF EXHIBITS | 70-72 |

Information included in or incorporated by reference in this Annual Report on Form 10-K, our other filings with the Securities and Exchange Commission and our press releases or other public statements, contain or may contain “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Please refer to a discussion of our forward- looking statements and associated risks in Item 1, “Business – Forward-Looking Statements and Associated Risks” and our discussion of risk factors in Item 1A, “Risk Factors” in this Annual Report on Form 10-K.

PART I

Item 1. Business.

General.

German American Bancorp, Inc. is a financial services holding company based in Jasper, Indiana. The Company’s Common Stock is traded on NASDAQ’s Global Select Market under the symbol GABC. The principal subsidiary of German American Bancorp, Inc., is its banking subsidiary, German American Bancorp which operates through six community banking affiliates with 28 retail banking offices in the ten contiguous Southern Indiana counties of Daviess, Dubois, Gibson, Knox, Lawrence, Martin, Monroe, Perry, Pike, and Spencer. German American Bancorp, Inc., also owns a trust, brokerage, and financial planning subsidiary, which operates from the banking offices of the bank subsidiary and a full line property and casualty insurance agency with six insurance agency offices throughout its market area.

Throughout this report, when we use the term “Company”, we will usually be referring to the business and affairs (financial and otherwise) of the Company and its consolidated subsidiaries as a whole. Occasionally, we will refer to the term “parent company” or “holding company” when we mean to refer to only German American Bancorp, Inc.

The Company’s lines of business include retail and commercial banking, mortgage banking, comprehensive financial planning, full service brokerage and trust administration, and a full range of personal and corporate insurance products. Financial and other information by segment is included in Note 16 – Segment Information of the Notes to the Consolidated Financial Statements included in Item 8 of this Report and is incorporated into this Item 1 by reference. Substantially all of the Company’s revenues are derived from customers located in, and substantially all of its assets are located in, the United States.

Subsidiaries.

The Company’s principal operating subsidiaries are described in the following table:

1) Name | | 2) Type of Business | | 3) Principal Office Location |

| German American Bancorp | | Commercial Bank | | Jasper, IN |

| German American Insurance, Inc. | | Multi-Line Insurance Agency | | Jasper, IN |

| German American Financial Advisors & Trust Company | | Trust, Brokerage, Financial Planning | | Jasper, IN |

Two of these subsidiaries (German American Bancorp and German American Insurance, Inc.) do business in the various communities served by the Company under distinctive trade names that relate to the names under which the Company (or a predecessor) has done banking or insurance business with the public in those communities in prior years.

Competition.

The industries in which the Company operates are highly competitive. The Company’s subsidiary bank competes for commercial and retail banking business within its core banking segment not only with financial institutions that have offices in the same counties but also with financial institutions that compete from other locations in Southern Indiana and elsewhere. The Company’s subsidiaries compete with commercial banks, savings and loan associations, savings banks, credit unions, production credit associations, federal land banks, finance companies, credit card companies, personal loan companies, investment brokerage firms, insurance agencies, insurance companies, lease finance companies, money market funds, mortgage companies, and other non-depository financial intermediaries. Many of these banks and other organizations have substantially greater resources than the Company.

Employees.

At March 1, 2008 the Company and its subsidiaries employed approximately 365 full-time equivalent employees. There are no collective bargaining agreements, and employee relations are considered to be good.

Effectiveness Plan.

Management of the Company embarked during the last half of 2007 upon a formal study of the operating effectiveness and efficiency of its financial services operations. This effectiveness study has resulted in the preparation by management of an action plan (“Effectiveness Plan”), which has been approved in principle by the Company’s Board of Directors. This Effectiveness Plan identifies certain tactical steps (including steps that are designed to enhance non-interest income and to reduce non-interest expense) that the Company’s Board of Directors believes must be taken if the Company is to achieve its goal of achieving financial performance that would fall within the top 25% of publicly-traded Midwest banking companies of similar size or larger.

For purposes of measuring its progress toward achieving top-quartile financial performance, the Company’s Board of Directors has established a peer group of larger bank holding companies in the Midwest. The members of this peer group are subject to change from time to time, and were most recently publicly identified (as the group was constituted in 2006 for purposes of 2006 executive compensation) by the Company’s proxy statement for its 2007 annual meeting. The Company intends to identify the members of this peer group (as it was constituted in 2007 for purposes of 2007 executive compensation) in its proxy statement for its 2008 annual meeting.

Full implementation of the plan initiatives is scheduled to be completed by the end of 2008. While the Company expects that it will begin to achieve during 2008 some of the benefits from the operating and other efficiencies that the Company hopes to achieve as a result of the implementation of the Plan, the Company also expects that its implementation of certain plan initiatives will result in certain non-routine charges to non-interest expense during 2008. Accordingly, the Company anticipates that 2009 will be the earliest fiscal year in which the intended benefits of the Plan might be realized by the Company.

Regulation and Supervision.

The Company is subject to regulation and supervision by the Board of Governors of the Federal Reserve System (“FRB”) under the Bank Holding Company Act of 1956, as amended (“BHC Act”), and is required to file with the FRB annual reports and such additional information as the FRB may require. The FRB may also make examinations or inspections of the Company. Under FRB policy, the Company is expected to act as a source of financial strength to its bank subsidiary and to commit resources to support that subsidiary even in circumstances where the Company might not do so absent such an FRB policy.

The Company’s subsidiary bank is under the supervision of and subject to examination by the Indiana Department of Financial Institutions (“DFI”), and the Federal Deposit Insurance Corporation (“FDIC”). Regulation and examination by banking regulatory agencies are primarily for the benefit of depositors rather than shareholders.

With certain exceptions, the BHC Act prohibits a bank holding company from engaging in (or acquiring direct or indirect control of more than 5 percent of the voting shares of any company engaged in) nonbanking activities. One of the principal exceptions to this prohibition is for activities deemed by the FRB to be “closely related to banking.” Under current regulations, bank holding companies and their subsidiaries are permitted to engage in such banking-related business ventures as consumer finance; equipment leasing; credit life insurance; computer service bureau and software operations; mortgage banking; and securities brokerage.

Under the BHC Act, certain well-managed and well-capitalized bank holding companies may elect to be treated as a “financial holding company” and, as a result, be permitted to engage in a broader range of activities that are “financial in nature” and in activities that are determined to be incidental or complementary to activities that are financial in nature. These activities include underwriting, dealing in and making a market in securities; insurance underwriting and agency activities; and merchant banking. Banks may also engage through financial subsidiaries in certain of the activities permitted for financial holding companies, subject to certain conditions. The Company has not elected to become a financial holding company and its subsidiary bank has not elected to form financial subsidiaries.

The Company's bank subsidiary and that bank’s subsidiaries may generally engage in activities that are permissible activities for state chartered banks under Indiana banking law, without regard to the limitations that might apply to such activities under the BHC Act if the Company were to engage directly in such activities at the parent company level or through parent company subsidiaries that were not also bank subsidiaries.

Indiana law and the BHC Act restrict certain types of expansion by the Company and its bank subsidiary. The Company and its subsidiaries may be required to apply for prior approval from (or give prior notice and an opportunity for review to) the FRB, the DFI, and/or other bank regulatory or other regulatory agencies, as a condition to the acquisition or establishment of new offices, or the acquisition (by merger or consolidation, purchase or otherwise) of the stock, business or properties of other banks or other companies.

The earnings of commercial banks and their holding companies are affected not only by general economic conditions but also by the policies of various governmental regulatory authorities. In particular, the FRB regulates money and credit conditions and interest rates in order to influence general economic conditions, primarily through open-market operations in U.S. Government securities, varying the discount rate on bank borrowings, and setting reserve requirements against bank deposits. These policies have a significant influence on overall growth and distribution of bank loans, investments and deposits, and affect interest rates charged on loans and earned on investments or paid for time and savings deposits. FRB monetary policies have had a significant effect on the operating results of commercial banks in the past and this is expected to continue in the future. The general effect, if any, of such policies upon the future business and earnings of the Company cannot accurately be predicted.

The Company and its bank subsidiary are required by law to maintain minimum levels of capital. These required capital levels are expressed in terms of capital ratios, known as the leverage ratio and the capital to risk-based assets ratios. The Company and its bank subsidiary each exceeded the minimum required capital levels for each measure of capital adequacy as of December 31, 2007. See Note 9 to the Company's consolidated financial statements that are presented in Item 8 of this Report, which Note 9 is incorporated herein by reference.

Also, federal regulations define five categories of financial institutions for purposes of implementing prompt corrective action and supervisory enforcement requirements of the Federal Deposit Insurance Corporation Improvements Act of 1991. The category to which the most highly capitalized institutions are assigned is termed “well-capitalized.” Institutions falling into this category must have a total risk-based capital ratio (the ratio of total capital to risk-weighted assets) of at least 10%, a Tier 1 risk-based capital ratio (the ratio of Tier 1, or “core”, capital to risk-weighted assets) of at least 6%, a leverage ratio (the ratio of Tier 1 capital to total assets) of at least 5%, and must not be subject to any written agreement, order or directive from its regulator relative to meeting and maintaining a specific capital level. On December 31, 2007, the Company had a total risk-based capital ratio of 10.63%, a Tier 1 risk-based capital ratio of 8.69% (based on Tier 1 capital of $82,335,000 and total risk-weighted assets of $947,987,000), and a leverage ratio of 7.41%. The Company’s affiliate bank met all of the requirements of the “well-capitalized” category. In addition the Company meets the requirements of the FRB to be considered a “well-capitalized” bank holding company. Accordingly, the Company does not expect these regulations to significantly impact operations.

Our parent company is a corporation separate and distinct from its bank and other subsidiaries. Most of the parent company’s revenues historically have been comprised of dividends, fees, and interest paid to it by its bank subsidiary, and this is expected to continue in the future. This subsidiary is subject to statutory restrictions on its ability to pay dividends. The FRB possesses enforcement powers over bank holding companies and their non-bank subsidiaries that enable it to prevent or remedy actions that in its view may represent unsafe or unsound practices or violations of applicable statutes and regulations. Among these powers is the ability in appropriate cases to proscribe the payment of dividends by banks and bank holding companies. The FDIC and DFI possess similar enforcement powers over the bank subsidiary. The “prompt corrective action” provisions of federal banking law impose further restrictions on the payment of dividends by insured banks which fail to meet specified capital levels and, in some cases, their parent bank holding companies.

Internet Address; Internet Availability of SEC Reports.

The Company's Internet address is www.germanamericanbancorp.com.

Forward-Looking Statements and Associated Risks.

The Company from time to time in its oral and written communications makes statements relating to its expectations regarding the future. These types of statements are considered "forward-looking statements" within the meaning of the Private Securities Litigation Reform Act of 1995. Such forward-looking statements can include statements about the Company’s net interest income or net interest margin; adequacy of allowance for loan losses, and the quality of the Company’s loans, investment securities and other assets; simulations of changes in interest rates; litigation results; dividend policy; estimated cost savings, plans and objectives for future operations; and expectations about the Company’s financial and business performance and other business matters as well as economic and market conditions and trends. They often can be identified by the use of words like “expect,” “may,” “will,” “would,” “could,” “should,” “intend,” “project,” “estimate,” “believe” or “anticipate,” or similar expressions.

The Company may include forward-looking statements in filings with the SEC, such as this Form 10-K, in other written materials, and in oral statements made by senior management to analysts, investors, representatives of the media, and others. It is intended that these forward-looking statements speak only as of the date they are made, and the Company undertakes no obligation to update any forward-looking statement to reflect events or circumstances after the date on which the forward-looking statement is made.

The descriptions of the Company’s intent to take certain steps by the end of 2008 pursuant to its Effectiveness Plan described above in Item 1, “Business,” of this report, and of the Company’s anticipation that implementation of the plan may improve its financial performance toward top-quartile levels (as measured against a peer group of larger Midwest banking companies) within certain time periods, are "forward-looking statements" within the meaning of the Private Securities Litigation Reform Act of 1995. The Company’s financial performance in past periods, including its most recent fiscal year, has not been within the top quartile of this peer group. The Company cautions readers that they should not construe the above disclosure as constituting a projection by management that an improvement in the Company’s future performance or earnings, for the years 2008, 2009 or any interim or subsequent period, will in fact occur, regardless of the degree of success experienced in implementation of the Effectiveness Plan. Further, the peer group’s performance may improve in future periods, thus making achievement of this goal difficult even if the Company’s financial performance in fact improves in future periods when measured solely against the Company’s prior performance.

Readers are further cautioned that, by their nature, all forward-looking statements are based on assumptions and are subject to risks, uncertainties, and other factors. Among the assumptions that underlie the Company’s plan to improve its financial performance through the Effectiveness Plan are assumptions that (a) the Effectiveness Plan will be supported by officers, employees and customers of the Company and (b) the Company’s business and affairs, financial and otherwise, will not be adversely affected by unrelated trends, conditions, or events. Actual results may differ materially and adversely from the expectations of the Company that are expressed or implied by any forward-looking statement. The discussions in Item 1A, “Risk Factors,” and in Item 7 of this Form 10-K, “Management's Discussion and Analysis of Financial Condition and Results of Operations,” list some of the factors that could cause the Company's actual results to vary materially from those expressed or implied by any forward-looking statements. Other risks, uncertainties, and factors that could cause the Company’s actual results to vary materially from those expressed or implied by any forward-looking statement include the ability of the Company to affect the tactical steps contemplated by the action plan as currently planned by management without significant delay or unplanned expense; the unknown future direction of interest rates and the timing and magnitude of any changes in interest rates; the effects of changes in competitive conditions; of the possibility that the Company may acquire other businesses or intangible customer relationships of other companies and the costs of integrations of such acquired businesses and intangible customer relationships; the introduction, withdrawal, success, and timing of business initiatives and strategies; changes in customer borrowing, repayment, investment, and deposit practices; changes in fiscal, monetary, and tax policies; changes in financial and capital markets including those arising from the continuing uncertainties commonly associated with the mortgage-backed securities markets and the auction-rate securities markets, and those arising from uncertainties concerning the financial stability of bond insurers; the possibility of a recession or other adverse change in general economic conditions, either nationally or regionally, resulting in, among other things, credit quality deterioration; the impact, extent and timing of technological changes; capital management activities; actions of the Federal Reserve Board and legislative and regulatory actions and reforms; changes in accounting principles and interpretations; the inherent uncertainties involved in litigation and regulatory proceedings which could result in the Company’s incurring loss or damage regardless of the merits of the Company’s claims or defenses; and the continued availability of earnings and excess capital sufficient for the lawful and prudent declaration and payment of cash dividends. Investors should consider these risks, uncertainties, and other factors in addition to those mentioned by the Company in its other SEC filings from time to time when considering any forward-looking statement.

Item 1A. Risk Factors.

While we a have a history of profitability and operate in mature industries with capital that exceeds the requirements of bank regulatory agencies, an investment in our common stock (like an investment in the equity securities of any business enterprise) is subject to investment risks and uncertainties. The following describes some of the principal risks and uncertainties to which we and our assets and businesses are subject; other risks are briefly identified in our cautionary statement that is included “Forward-Looking Statements and Associated Risks” in Part I, Item 1, “Business.” Although we seek ways to manage these risks and uncertainties and to develop programs to control those that we can, we ultimately cannot predict the future. Future results may differ materially from past results, and from our expectations and plans.

If our actual loan losses exceed our estimates, our earnings and financial condition will be impacted.

A significant source of risk for any bank or other enterprise that lends money arises from the possibility that losses will be sustained because borrowers, guarantors and related parties may fail (because of financial difficulties or other reasons) to perform in accordance with the terms of their loan agreements. In our case, we originate many loans that are secured, but some loans are unsecured depending on the nature of the loan. With respect to secured loans, the collateral securing the repayment of these loans includes a wide variety of real and personal property that may be insufficient to cover the obligations owed under such loans. Collateral values may be adversely affected by changes in prevailing economic, environmental and other conditions, including declines in the value of real estate, changes in interest rates, changes in monetary and fiscal policies of the federal government, wide-spread disease, terrorist activity, environmental contamination, natural disasters, and other external events. We have adopted underwriting and credit monitoring procedures and policies, including the establishment and review of the allowance for loan losses and regular review of appraisals and borrower financial statements, that we believe are appropriate to mitigate the risk of loss by assessing the likelihood of nonperformance and the value of available collateral, monitoring loan performance and diversifying our credit portfolio. Such policies and procedures, however, may not prevent unexpected losses that could have a material adverse effect on our business, financial condition, results of operations or liquidity. For additional information regarding our asset quality, see Part II, Item 7 (“Management’s Discussion and Analysis of Financial Condition and Results of Operations.”)

We could be adversely affected by changes in interest rates.

Our earnings depend largely on the relationship between the yield on earning assets, primarily loans and investments, and the cost of funds, primarily deposits and borrowings. This relationship, known as the interest rate spread, is subject to fluctuation and is affected by economic and competitive factors which influence interest rates, the volume and mix of interest-earning assets and interest-bearing liabilities and the level of non-performing assets. Fluctuations in interest rates affect the demand of customers for our products and services. We are subject to interest rate risk to the degree that our interest-bearing liabilities reprice or mature more slowly or more rapidly or on a different basis than its interest-earning assets. Significant fluctuations in interest rates could have a material adverse effect on our business, financial condition, results of operations or liquidity. For additional information regarding interest rate risk, see Part II, Item 7A, (“Quantitative and Qualitative Disclosures About Market Risk.”)

Our success is tied to the economic vitality of our Southern Indiana markets.

We conduct business from offices that are exclusively located in ten contiguous counties of Southern Indiana, from which substantially our entire customer base is drawn. Because of the geographic concentration of our operations and customer base, our results depend largely upon economic conditions in this area. Deterioration in economic conditions in this area could adversely affect the quality of our loan portfolio and the demand for our products and services, and accordingly, could have a material adverse effect on our business, financial condition, results of operations or liquidity. See also Part I, Item 1, “Business — Competition.”

We face substantial competition.

The banking and financial services business in our markets is highly competitive. We compete with much larger regional, national, and international competitors. In addition, new banks could be organized in our market area which might bid aggressively for new business to capture market share in these markets. Developments increasing the nature or level of our competition, or decreasing the effectiveness by which we compete, could have a material adverse effect on our business, financial condition, results of operations or liquidity. See also “Competition,” and “Regulation and Supervision.”

Our business expansion and capital management strategies may be less successful than planned.

We from time to time consider opportunities to expand our business including strategies for launching new internal business initiatives and buying or investing in other businesses or business assets. Our earnings and financial condition could be adversely affected to the extent that the acquisitions or other business initiatives and strategies are not successful (or take longer than expected to achieve expected results) and such initiative or strategies could even result in losses. We also from time to time engage in activities (such as repurchasing and issuing our capital stock or other securities, and utilizing the borrowing capacity of our parent company to borrow funds from third party lenders on short and long term bases) in order to manage our capital structure and to finance acquisitions in a manner that we believe is most advantageous. These capital management activities and financing activities, however, also carry risks in the event that our business does not develop as expected or there are changes in the market for our common stock or in the capital and financial markets generally.

We operate in a highly regulated environment and changes in laws and regulations to which we are subject may adversely affect our results of operations.

The banking industry in which we operate is subject to extensive regulation and supervision under federal and state laws and regulations. The restrictions imposed by such laws and regulations limit the manner in which we conduct our business, undertake new investments and activities and obtain financing. These regulations are designed primarily for the protection of the deposit insurance funds and consumers and not to benefit our shareholders. Financial institution regulation has been the subject of significant legislation in recent years and may be the subject of further significant legislation, none of which is in our control. Significant new laws or changes in, or repeals of, existing laws (including changes in federal or state laws affecting corporate taxpayers generally or financial institutions specifically) could have a material adverse effect on our business, financial condition, results of operations or liquidity. Further, federal monetary policy, particularly as implemented through the Federal Reserve System, significantly affects credit conditions, and any unfavorable change in these conditions could have a material adverse effect on our business, financial condition, results of operations or liquidity. See also Part I, Item 1, “Business -- Supervision and Regulation of Banking Activities."

The manner in which we report our financial condition and results of operations may be affected by accounting changes.

Our financial condition and results of operations that are presented in the Consolidated Financial Statements, accompanying Notes to the Consolidated Financial Statements, and selected financial data appearing elsewhere within this report, are, to a large degree, dependent upon our accounting policies. The selection of and application of these policies involve estimates, judgments and uncertainties that are subject to change, and the effect of any change in estimates or judgments that might be caused by future developments or resolution of uncertainties could be materially adverse to our reported financial condition and results of operations. See the discussion of critical accounting policies and estimates that we have determined to be the most susceptible to change in the near term that is included in the section captioned “Critical Accounting Policies and Estimates” in Part II, Item 7 (“Management’s Discussion and Analysis of Financial Condition and Results of Operations”) for a complete discussion. In addition, authorities that prescribe accounting principles and standards for public companies from time to time change those principles or standards or adopt formal or informal interpretations of existing principles or standards, which changes or interpretations (to the extent applicable to us) could result in changes that would be materially adverse to our reported financial condition and results of operations.

Item 1B. Unresolved Staff Comments.

None.

Item 2. Properties.

The Company’s executive offices are located in the main office building of its bank subsidiary, German American Bancorp, at 711 Main Street, Jasper, Indiana. The main office building contains approximately 23,600 square feet of office space. The Company’s subsidiaries conduct their operations from 34 other locations in Southern Indiana.

Item 3. Legal Proceedings.

There are no material pending legal proceedings, other than routine litigation incidental to the business of the Company’s subsidiaries, to which the Company or any of its subsidiaries is a party or of which any of their property is the subject.

Item 4. Submission of Matters to a Vote of Security Holders.

There were no matters submitted during the fourth quarter of 2007 to a vote of security holders, by solicitation of proxies or otherwise.

PART II

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

Market and Dividend Information

German American Bancorp, Inc.’s stock is traded on NASDAQ’s Global Select Market under the symbol GABC. The quarterly high and low closing prices for the Company’s common stock as reported by NASDAQ and quarterly cash dividends declared and paid are set forth in the table below.

| | | 2007 | | 2006 | |

| | | | | | | Cash | | | | | | Cash | |

| | | High | | Low | | Dividend | | High | | Low | | Dividend | |

| | | | | | | | | | | | | | |

Fourth Quarter | | $ | 14.00 | | $ | 12.12 | | $ | 0.140 | | $ | 14.41 | | $ | 13.59 | | $ | 0.140 | |

Third Quarter | | $ | 14.09 | | $ | 11.91 | | $ | 0.140 | | $ | 14.39 | | $ | 12.89 | | $ | 0.140 | |

Second Quarter | | $ | 14.45 | | $ | 13.10 | | $ | 0.140 | | $ | 13.65 | | $ | 12.90 | | $ | 0.140 | |

First Quarter | | $ | 14.50 | | $ | 13.22 | | $ | 0.140 | | $ | 13.70 | | $ | 12.83 | | $ | 0.140 | |

| | | | | | | | | $ | 0.560 | | | | | | | | $ | 0.560 | |

The Common Stock was held of record by approximately 3,641 shareholders at March 1, 2008.

Cash dividends paid to the Company’s shareholders are primarily funded from dividends received by the parent company from its bank subsidiary. The declaration and payment of future dividends will depend upon the earnings and financial condition of the Company and its subsidiaries, general economic conditions, compliance with regulatory requirements affecting the ability of the bank subsidiary to declare dividends, and other factors.

Transfer Agent: | | Computershare | Shareholder | | Terri A. Eckerle |

| | | Priority Processing | Information and | | German American Bancorp, Inc |

| | | 250 Royall St | Corporate Office: | | P. O. Box 810 |

| | | Canton, MA 02021 | | | Jasper, Indiana 47547-0810 |

| | | Contact: Shareholder Relations | | | (812) 482-1314 |

| | | (800) 884-4225 | | | (800) 482-1314 |

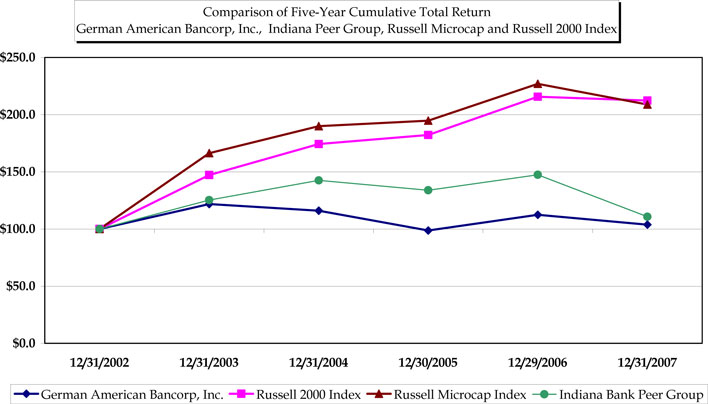

Stock Performance Graph

The following graph compares the Company’s five-year cumulative total returns with those of the Russell 2000 Stock Index, Russell Microcap Stock Index, and the Indiana Bank Peer Group. The Indiana Bank Peer Group (which is a custom peer group identified by Company management) includes all Indiana-based commercial bank holding companies (excluding companies owning thrift institutions that are not regulated as bank holding companies) that have been in existence as commercial bank holding companies throughout the five-year period ended December 2007, the stocks of which have been traded on an established securities market (NYSE, AMEX, NASDAQ) throughout that five-year period. The returns of each company in the Indiana Bank Peer Group have been weighted to reflect the company’s market capitalization. The Russell 2000® Stock Index, which is designed to measure the performance of the small-cap segment of the U.S. equity universe, is a subset of the Russell 3000® Index (which measures the performance of the largest 3000 U.S. companies) that includes approximately 2,000 of the smallest securities in that index based on a combination of their market cap and current index membership, and is annually reconstituted at the end of each June. The Company’s stock was included in the Russell 2000 through June 2005. The Russell Microcap® Stock Index is an index representing the smallest 1,000 securities in the small-cap Russell 2000 Index plus the next 1,000 securities, which is also annually reconstituted at the end of each June. The Company’s stock is currently included in the Russell Microcap Index.

| Return based on $100 invested on December 31, 2002 and the reinvestment of dividends |

Stock Repurchase Program Information

The following table sets forth information regarding the Company's purchases of its common shares during each of the three months ended December 31, 2007.

| | | Total | | | | | | Maximum Number | |

| | | Number | | | | Total Number of Shares | | (or Approximate Dollar | |

| | | Of Shares | | Average Price | | (or Units) Purchased as Part | | Value) of Shares (or Units) | |

| | | (or Units) | | Paid Per Share | | of Publicly Announced Plans | | that May Yet Be Purchased | |

Period | | Purchased | | (or Unit) | | or Programs | | Under the Plans or Programs (1) | |

| | | | | | | | | | |

| October 2007 | | | — | | | — | | | — | | | 272,789 | |

| November 2007 | | | — | | | — | | | — | | | 272,789 | |

| December 2007 | | | — | | | — | | | — | | | 272,789 | |

(1) On April 26, 2001, the Company announced that its Board of Directors had approved a stock repurchase program for up to 607,754 of its outstanding common shares, of which the Company had purchased 334,965 common shares through December 31, 2007 (both such numbers adjusted for subsequent stock dividends). The Board of Directors established no expiration date for this program. The Company purchased no shares under this program during the quarter ended December 31, 2007.

Item 6. Selected Financial Data.

The following selected data should be read in conjunction with the consolidated financial statements and related notes that are included in Item 8 of this Report, and “Management's Discussion and Analysis of Financial Condition and Results of Operations,” which is included in Item 7 of this Report (dollars in thousands, except per share data).

| | | 2007 | | 2006 | | 2005 | | 2004 | | 2003 | |

Summary of Operations: | | | | | | | | | | | |

| Interest Income | | $ | 72,261 | | $ | 63,594 | | $ | 50,197 | | $ | 47,710 | | $ | 50,619 | |

| Interest Expense | | | 33,646 | | | 27,398 | | | 17,984 | | | 16,471 | | | 21,084 | |

| Net Interest Income | | | 38,615 | | | 36,196 | | | 32,213 | | | 31,239 | | | 29,535 | |

| Provision for Loan Losses | | | 3,591 | | | 925 | | | 1,903 | | | 2,015 | | | 811 | |

| Net Interest Income after Provision | | | | | | | | | | | | | | | | |

| For Loan Losses | | | 35,024 | | | 35,271 | | | 30,310 | | | 29,224 | | | 28,724 | |

| Non-interest Income | | | 15,704 | | | 15,993 | | | 14,502 | | | 9,620 | | | 12,934 | |

| Non-interest Expense | | | 37,221 | | | 37,059 | | | 31,756 | | | 30,609 | | | | (2) |

| Income before Income Taxes | | | 13,507 | | | 14,205 | | | 13,056 | | | 8,235 | | | 9,439 | |

| Income Tax Expense | | | 4,102 | | | 3,984 | | | 3,335 | | | 996 | | | 1,271 | |

| Net Income | | $ | 9,405 | | $ | 10,221 | | $ | 9,721 | | $ | 7,239 | | $ | 8,168 | |

| | | | | | | | | | | | | | | | | |

Year-end Balances: | | | | | | | | | | | | | | | | |

| Total Assets | | $ | 1,131,710 | | $ | 1,093,424 | | $ | 946,467 | | $ | 942,094 | | $ | 925,946 | |

| Total Loans, Net of Unearned Income | | | 867,721 | | | 796,259 | | | 651,956 | | | 629,793 | | | 611,866 | |

| Total Deposits | | | 877,421 | | | 867,618 | | | 746,821 | | | 750,383 | | | 717,133 | |

| Total Long-term Debt | | | 86,786 | | | 68,333 | | | 66,606 | | | 69,941 | | | | (2) |

| Total Shareholders’ Equity | | | 97,116 | | | 92,391 | | | 82,255 | | | 83,669 | | | 83,126 | |

| | | | | | | | | | | | | | | | | |

Average Balances: | | | | | | | | | | | | | | | | |

| Total Assets | | $ | 1,114,140 | | $ | 1,029,838 | | $ | 925,851 | | $ | 927,528 | | $ | 938,992 | |

| Total Loans, Net of Unearned Income | | | 840,849 | | | 715,260 | | | 634,526 | | | 622,240 | | | 618,340 | |

| Total Deposits | | | 889,736 | | | 814,440 | | | 730,220 | | | 731,467 | | | 711,310 | |

| Total Shareholders’ Equity | | | 93,677 | | | 88,451 | | | 84,479 | | | 82,558 | | | 87,703 | |

| | | | | | | | | | | | | | | | | |

Per Share Data (3): | | | | | | | | | | | | | | | | |

| Net Income | | $ | 0.85 | | $ | 0.93 | | $ | 0.89 | | $ | 0.66 | | $ | 0.73 | |

| Cash Dividends | | | 0.56 | | | 0.56 | | | 0.56 | | | 0.56 | | | 0.53 | |

| Book Value at Year-end | | | 8.81 | | | 8.39 | | | 7.73 | | | 7.68 | | | 7.60 | |

| | | | | | | | | | | | | | | | | |

Other Data at Year-end: | | | | | | | | | | | | | | | | |

| Number of Shareholders | | | 3,647 | | | 3,438 | | | 3,494 | | | 3,219 | | | 3,198 | |

| Number of Employees | | | 371 | | | 397 | | | 367 | | | 372 | | | 383 | |

Weighted Average Number of Shares (3) | | | 11,009,536 | | | 10,994,739 | | | 10,890,987 | | | 10,914,622 | | | 11,176,766 | |

| | | | | | | | | | | | | | | | | |

Selected Performance Ratios: | | | | | | | | | | | | | | | | |

| Return on Assets | | | 0.84 | % | | 0.99 | % | | 1.05 | % | | 0.78 | % | | 0.87 | % |

| Return on Equity | | | 10.04 | % | | 11.56 | % | | 11.51 | % | | 8.77 | % | | 9.31 | % |

| Equity to Assets | | | 8.58 | % | | 8.45 | % | | 8.69 | % | | 8.88 | % | | 8.98 | % |

| Dividend Payout | | | 65.65 | % | | 60.29 | % | | 62.83 | % | | 84.46 | % | | 73.26 | % |

| Net Charge-offs to Average Loans | | | 0.32 | % | | 0.50 | % | | 0.26 | % | | 0.24 | % | | 0.14 | % |

| Allowance for Loan Losses to Loans | | | 0.93 | % | | 0.90 | % | | 1.42 | % | | 1.40 | % | | 1.35 | % |

| Net Interest Margin | | | 3.83 | % | | 3.96 | % | | 3.92 | % | | 3.86 | % | | 3.61 | % |

(1) | In 2004, the Company recognized a $3.7 million non-cash pre-tax charge (which reduced Non-interest Income) for the other-than-temporary decline in value of its FHLMC and FNMA preferred stock portfolio. In 2006, the Company sold these same FHLMC and FNMA preferred stocks and recognized a pre-tax gain of $951. |

(2) | In 2003, the Company prepaid $40.0 million of FHLB borrowings within its mortgage banking segment. The prepayment fees associated with the extinguishment of these borrowings totaled $1.9 million. |

(3) | Share and Per Share Data excludes the dilutive effect of stock options. |

Year to year financial information comparability is affected by the purchase accounting treatment for mergers and acquisitions. See Note 18 to the Company’s consolidated financial statements included in Item 8 of this Report.

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

German American Bancorp, Inc. is a financial services holding company based in Jasper, Indiana. The Company’s Common Stock is traded on NASDAQ’s Global Select Market, under the symbol GABC. The principal subsidiary of German American Bancorp, Inc., is its banking subsidiary, German American Bancorp, which operates through six community banking affiliates with 28 retail banking offices in the ten contiguous Southern Indiana counties of Daviess, Dubois, Gibson, Knox, Lawrence, Martin, Monroe, Perry, Pike, and Spencer. German American Bancorp, Inc., also owns a trust, brokerage, and financial planning subsidiary, which operates from the banking offices of the bank subsidiary, and full line property and casualty insurance agency with six insurance agency offices throughout its market area.

Throughout this Management’s Discussion and Analysis, as elsewhere in this report, when we use the term “Company”, we will usually be referring to the business and affairs (financial and otherwise) of the Company and its subsidiaries and affiliates as a whole. Occasionally, we will refer to the term “parent company” or “holding company” when we mean to refer to only German American Bancorp, Inc.

The information in this Management’s Discussion and Analysis is presented as an analysis of the major components of the Company’s operations for the years 2005 through 2007 and its financial condition as of December 31, 2007 and 2006. This information should be read in conjunction with the accompanying consolidated financial statements and footnotes contained elsewhere in this report and with the description of business included in Item 1 of this Report (including the cautionary disclosure regarding “Forward Looking Statements and Associated Risks”). Financial and other information by segment is included in Note 16 to the Company’s consolidated financial statements included in Item 8 of this Report and is incorporated into this Item 7 by reference.

The statements of management's expectations and goals concerning the Company's future operations and performance that are set forth in the following Management Overview and in other sections of this Item 7 (including but not limited to statements regarding the Company’s Effectiveness Plan described in Item 1 of the report) are forward-looking statements, and readers are cautioned that these forward-looking statements are based on assumptions and are subject to risks, uncertainties, and other factors. Actual results may differ materially from the expectations of the Company that is expressed or implied by any forward-looking statement. This Item 7, as well as the discussions in Item 1 ("Business") entitled "Forward-Looking Statements and Associated Risks" and in Item 1A (“Risk Factors”) (which discussions are incorporated in this Item 7 by reference) list some of the factors that could cause the Company's actual results to vary materially from those expressed or implied by any such forward-looking statements.

MANAGEMENT OVERVIEW

The Company’s net income declined 8% in 2007 compared with 2006. The Company’s 2007 net income totaled $9,405,000, or $0.85 per share, compared with $10,221,000, or $0.93 per share, for 2006. The Company's results for 2007 have been adversely affected by higher levels of provisions for loan losses, as discussed below, attributable largely to the resolution of certain specific credits (discussed below) during 2007 and to additional provision necessary in connection with the growth in the Company's loans. Also contributing to the lower level of earnings was an other-than-temporary impairment charge on the Company’s equity securities portfolio during 2007 compounded by a gain the Company recognized on the sale of its agency-issued preferred stocks during 2006. Current year earnings were positively affected by increases within the Company’s net interest income and non-interest income, exclusive of securities gains and losses. The improvement in the level of net interest income was largely attributable to strong loan growth. Loans outstanding grew by $72.0 million or 9% during 2007 following an increase of $145.1 million or 22% during 2006. The Company experienced double digit percentage growth in trust and investment product fees, service charges on deposit accounts, and insurance revenues during 2007.

Management also continues to focus on the control of the Company's operating expenses, and believes that the fact that operating expenses declined in the second half of 2007 and increased by less than one percent during 2007 compared to 2006 has contributed to an increase in the Company's overall operating efficiency. As discussed in Item 1 of this Report, “Business”, under “Effectiveness Plan” (which discussion is incorporated into this Management Overview by reference), the Company intends to take by the end of 2008 certain tactical steps (including steps that are designed to enhance non-interest income and to reduce non-interest expense) to improve its operating effectiveness and efficiency. Future results of operations may be impacted by non-routine charges to non-interest expense that may be recorded as a result of the implementation of the Effectiveness Plan during 2008, and by the expected longer-term benefits of the Effectiveness Plan that the Company anticipates realizing as early as 2009 in the areas of non-interest income and non-interest expense. Readers are cautioned to review the cautionary statements concerning the Effectiveness Plan that are included in the discussion entitled "Forward-Looking Statements and Associated Risks" that is included in Item 1 of this report and has already been incorporated into this Item 7 by reference.

MERGERS AND ACQUISITIONS

On October 1, 2005 PCB Holding Company (“PCB”) merged with and into the Company. PCB’s sole banking subsidiary, Peoples Community Bank, operated two banking offices in Tell City, Indiana. PCB’s assets and equity (unaudited) as of September 30, 2005 totaled $34.6 million and $4.8 million, respectively. Under the terms of the merger, the shareholders of PCB received an aggregate of 257,029 shares of common stock of the Company valued at approximately $3.5 million and approximately $3.2 million of cash, representing a total transaction value of $6.7 million. This merger was accounted for under the purchase method of accounting.

On January 1, 2006, Stone City Bancshares, Inc. (“Stone City”) merged with and into the Company, and as a result the Company acquired all of the stock of Stone City’s sole banking subsidiary, Stone City Bank of Bedford, Indiana, which operated two banking offices in Bedford, Indiana. Stone City’s assets and equity as of December 31, 2005 totaled $61.2 million and $5.4 million, respectively. Under the terms of the merger, the shareholders of Stone City received aggregate cash payments of approximately $6.4 million and 349,468 common shares of the Company valued during a pre-closing valuation period of approximately $4.6 million, representing a total transaction value of approximately $11.0 million. This merger was accounted for under the purchase method of accounting.

On October 1, 2006 the Company acquired substantially all of the assets, net of certain assumed liabilities of Keach and Grove Insurance, Inc. of Bedford, Indiana. The agency operations became a part of German American Insurance, Inc., the Company’s property and casualty insurance entity. The purchase price for this transaction was $2.26 million in cash. This merger was accounted for under the purchase method of accounting.

CRITICAL ACCOUNTING POLICIES AND ESTIMATESINTRODUCTION |

The financial condition and results of operations for German American Bancorp, Inc. presented in the Consolidated Financial Statements, accompanying Notes to the Consolidated Financial Statements, and selected financial data appearing elsewhere within this report, are, to a large degree, dependent upon the Company’s accounting policies. The selection of and application of these policies involve estimates, judgments and uncertainties that are subject to change. The critical accounting policies and estimates that the Company has determined to be the most susceptible to change in the near term relate to the determination of the allowance for loan losses, the valuation of securities available for sale, and the valuation allowance on deferred tax assets.

Allowance for Loan Losses

The Company maintains an allowance for loan losses to cover probable incurred credit losses at the balance sheet date. Loan losses are charged against the allowance when management believes the uncollectibility of a loan balance is confirmed. Subsequent recoveries, if any, are credited to the allowance. Allocations of the allowance may be made for specific loans, but the entire allowance is available for any loan that, in management’s judgment, should be charged-off. A provision for loan losses is charged to operations based on management's periodic evaluation of the necessary allowance balance. Evaluations are conducted at least quarterly and more often if deemed necessary. The ultimate recovery of all loans is susceptible to future market factors beyond the Company's control.

The Company has an established process to determine the adequacy of the allowance for loan losses. The determination of the allowance is inherently subjective, as it requires significant estimates, including the amounts and timing of expected future cash flows on impaired loans, estimated losses on other classified loans and pools of homogeneous loans, and consideration of past loan loss experience, the nature and volume of the portfolio, information about specific borrower situations and estimated collateral values, economic conditions, and other factors, all of which may be susceptible to significant change. The allowance consists of two components of allocations, specific and general. These two components represent the total allowance for loan losses deemed adequate to cover losses inherent in the loan portfolio.

Commercial and agricultural loans are subject to a standardized grading process administered by an internal loan review function. The need for specific reserves is considered for credits when graded substandard or special mention, or when: (a) the customer’s cash flow or net worth appears insufficient to repay the loan; (b) the loan has been criticized in a regulatory examination; (c) the loan is on non-accrual; or, (d) other reasons where the ultimate collectibility of the loan is in question, or the loan characteristics require special monitoring. Specific allowances are established in cases where management has identified significant conditions or circumstances related to an individual credit that we believe indicates the loan is impaired. Specific allocations on impaired loans are determined by comparing the loan balance to the present value of expected cash flows or expected collateral proceeds. Allocations are also applied to categories of loans not considered individually impaired but for which the rate of loss is expected to be greater than historical averages, including those graded substandard or special mention and non-performing consumer or residential real estate loans. Such allocations are based on past loss experience and information about specific borrower situations and estimated collateral values.

General allocations are made for other pools of loans, including non-classified loans, homogeneous portfolios of consumer and residential real estate loans, and loans within certain industry categories believed to present unique risk of loss. General allocations of the allowance are primarily made based on a five-year historical average for loan losses for these portfolios, judgmentally adjusted for economic factors and portfolio trends.

Due to the imprecise nature of estimating the allowance for loan losses, the Company’s allowance for loan losses includes a minor unallocated component. The unallocated component of the allowance for loan losses incorporates the Company’s judgmental determination of inherent losses that may not be fully reflected in other allocations, including factors such as economic uncertainties, lending staff quality, industry trends impacting specific portfolio segments, and broad portfolio quality trends. Therefore, the ratio of allocated to unallocated components within the total allowance may fluctuate from period to period.

Securities Valuation

Securities available-for-sale are carried at fair value, with unrealized holding gains and losses reported separately in accumulated other comprehensive income (loss), net of tax. The Company obtains market values from a third party on a monthly basis in order to adjust the securities to fair value. Equity securities that do not have readily determinable fair values are carried at cost. Additionally, all securities are required to be written down to fair value when a decline in fair value is other than temporary; therefore, future changes in the fair value of securities could have a significant impact on the Company’s operating results. In determining whether a market value decline is other than temporary, management considers the reason for the decline, the extent of the decline and the duration of the decline. As of December 31, 2007, gross unrealized losses on the securities available-for-sale portfolio totaled approximately $422,000.

Income Tax Expense

Income tax expense involves estimates related to the valuation allowance on deferred tax assets and loss contingencies related to exposure from tax examinations.

A valuation allowance reduces deferred tax assets to the amount management believes is more likely than not to be realized. In evaluating the realization of deferred tax assets, management considers the likelihood that sufficient taxable income of appropriate character will be generated within carryback and carryforward periods, including consideration of available tax planning strategies. As of December 31, 2007, the Company had a deferred tax asset of $649,000 which includes tax credit carryforwards of $403,000. Based on the long carryforward periods available, management has assessed it more likely than not that these credits will be realized and no valuation allowance has been established on this asset.

Tax related loss contingencies, including assessments arising from tax examinations and tax strategies, are recorded as liabilities when the likelihood of loss is probable and an amount or range of loss can be reasonably estimated. In considering the likelihood of loss, management considers the nature of the contingency, the progress of any examination or related protest or appeal, the views of legal counsel and other advisors, experience of the Company or other enterprises in similar matters, if any, and management’s intended response to any assessment.

Net income declined $816,000 or 8% to $9,405,000 or $0.85 per share in 2007 compared to $10,221,000 or $0.93 per share in 2006. The decline in earnings during 2007 was largely the result of a $2,666,000 increase in the provision for loan losses. Partially mitigating the increased provision was an increase in net interest income of $2,419,000. Non-interest income declined $289,000 or 2% during 2007 while non-interest expense increased by $162,000 or less than 1% during 2007.

Net income increased $500,000 or 5% to $10,221,000 or $0.93 per share in 2006 compared to $9,721,000 or $0.89 per share during 2005. The increase in net income during 2006 compared with 2005 was attributable principally to an increase in net interest income of $3,983,000, a reduction in provision for loan losses of $978,000, and a gain on the sale of the Company’s portfolio of agency preferred stock of $951,000, which were partially mitigated by an increase of $5,303,000 in non-interest expense. The increases in net interest income and non-interest expenses were largely attributable to acquisitions of PCB Holding Company and Stone City Bancshares, Inc., which are discussed in Note 18 to the consolidated financial statements included in Item 8 of this Report.

NET INTEREST INCOME

Net interest income is the Company’s single largest source of earnings, and represents the difference between interest and fees realized on earning assets, less interest paid on deposits and borrowed funds. Several factors contribute to the determination of net interest income and net interest margin, including the volume and mix of earning assets, interest rates, and income taxes. Many factors affecting net interest income are subject to control by management policies and actions. Factors beyond the control of management include the general level of credit and deposit demand, Federal Reserve Board monetary policy, and changes in tax laws.

Net interest income increased $2,419,000 or 7% (an increase of $1,953,000 or 5% on a tax-equivalent basis) for the year ended 2007 compared with 2006. The increase in net interest income was primarily attributable to an increased level of average earning assets for the year ended 2007 compared with 2006. The higher level of earning assets was primarily attributable to an increase in the average level of loans outstanding, and in particular a higher level of average commercial and agricultural loans. Average earning assets totaled $1.023 billion during 2007 compared with $941.6 million during 2006.

For 2007, the net interest margin decreased to 3.83% compared to 3.96% during 2006. Net interest margin is tax equivalent net interest income expressed as a percentage of average earning assets. The Company’s yield on earning assets totaled 7.12% compared with a cost of funds (expressed as a percentage of average earning assets) of 3.29% netting to a net interest margin of 3.83% for the year ended December 31, 2007. The Company’s yield on earning assets was 6.87% compared with a cost of funds of 2.91% netting to a net interest margin of 3.96% for the year ended December 31, 2006.

Net interest income increased $3,983,000 or 12% (an increase of $3,809,000 or 11% on a tax-equivalent basis) for the year ended 2006 compared with 2005. The increase in net interest income was primarily attributable to an increased level of average earning assets and an increased net interest margin for the year ended 2006 compared with 2005. The higher level of earning assets was primarily attributable to an increase in the average level of loans outstanding that resulted from new loan activity and from the previously discussed banking acquisitions completed effective October 1, 2005 and effective January 1, 2006. Average earning assets totaled $941.6 million during 2006 compared with $853.3 million during 2005.

For 2006, the net interest margin increased to 3.96% compared to 3.92% during 2005. The Company’s yield on earning assets totaled 6.87% compared with a cost of funds (expressed as a percentage of average earning assets) of 2.91% producing the net interest margin of 3.96% for the year ended December 31, 2006. The Company’s yield on earning assets was 6.03% compared with a cost of funds of 2.11% netting to a net interest margin of 3.92% for the year ended December 31, 2005.

The following table summarizes net interest income (on a tax-equivalent basis) for each of the past three years. For tax-equivalent adjustments, an effective tax rate of 34% was used for all years presented (1).

| | | Average Balance Sheet | | | | | | | |

| | | (Tax-equivalent basis / dollars in thousands) | | | | | | | |

| | | Twelve Months Ended | | Twelve Months Ended | | Twelve Months Ended | |

| | | December 31, 2007 | | December 31, 2006 | | December 31, 2005 | |

| | | Principal | | Income/ | | Yield / | | Principal | | Income/ | | Yield / | | Principal | | Income/ | | Yield / | |

| | | Balance | | Expense | | Rate | | Balance | | Expense | | Rate | | Balance | | Expense | | Rate | |

| | | | | | | | | | | | | | | | | | | | |

ASSETS | | | | | | | | | | | | | | | | | | | |

Federal Funds Sold and Other Short-term Investments | | $ | 9,626 | | $ | 478 | | | 4.96% | | $ | 10,971 | | $ | 545 | | | 4.97 | % | $ | 10,632 | | $ | 316 | | | 2.97 | % |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Securities: | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Taxable | | | 149,108 | | | 6,992 | | | 4.69% | | | 174,007 | | | 7,763 | | | 4.46 | % | | 161,499 | | | 5,954 | | | 3.69 | % |

| Non-taxable | | | 23,913 | | | 1,423 | | | 5.95% | | | 41,312 | | | 2,721 | | | 6.59 | % | | 46,666 | | | 3,297 | | | 7.07 | % |

Total Loans and Leases (2) | | | 840,849 | | | 63,958 | | | 7.61% | | | 715,260 | | | 53,621 | | | 7.50 | % | | 634,526 | | | 41,860 | | | 6.60 | % |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| TOTAL INTEREST EARNING ASSETS | | | 1,023,496 | | | 72,851 | | | 7.12% | | | 941,550 | | | 64,650 | | | 6.87 | % | | 853,323 | | | 51,427 | | | 6.03 | % |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Other Assets | | | 98,389 | | | | | | | | | 97,570 | | | | | | | | | 81,771 | | | | | | | |

| Less: Allowance for Loan Losses | | | (7,745 | ) | | | | | | | | (9,282 | ) | | | | | | | | (9,243 | ) | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| TOTAL ASSETS | | $ | 1,114,140 | | | | | | | | $ | 1,029,838 | | | | | | | | $ | 925,851 | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

LIABILITIES AND SHAREHOLDERS’ EQUITY | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Interest-Bearing Demand Deposits | | $ | 153,033 | | $ | 3,280 | | | 2.14% | | $ | 140,786 | | $ | 2,625 | | | 1.86 | % | $ | 137,318 | | $ | 1,436 | | | 1.05 | % |

| Savings Deposits | | | 177,001 | | | 4,858 | | | 2.74% | | | 174,095 | | | 4,263 | | | 2.45 | % | | 156,820 | | | 2,212 | | | 1.41 | % |

| Time Deposits | | | 425,878 | | | 19,151 | | | 4.50% | | | 369,800 | | | 14,441 | | | 3.91 | % | | 314,420 | | | 9,741 | | | 3.10 | % |

| FHLB Advances and Other Borrowings | | | 117,084 | | | 6,357 | | | 5.43% | | | 113,559 | | | 6,069 | | | 5.34 | % | | 98,932 | | | 4,595 | | | 4.64 | % |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| TOTAL INTEREST-BEARING LIABILITIES | | | 872,996 | | | 33,646 | | | 3.85% | | | 798,240 | | | 27,398 | | | 3.43 | % | | 707,490 | | | 17,984 | | | 2.54 | % |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Demand Deposit Accounts | | | 133,824 | | | | | | | | | 129,759 | | | | | | | | | 121,662 | | | | | | | |

| Other Liabilities | | | 13,643 | | | | | | | | | 13,388 | | | | | | | | | 12,220 | | | | | | | |

| TOTAL LIABILITIES | | | 1,020,463 | | | | | | | | | 941,387 | | | | | | | | | 841,372 | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Shareholders’ Equity | | | 93,677 | | | | | | | | | 88,451 | | | | | | | | | 84,479 | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| TOTAL LIABILITIES AND SHAREHOLDERS’ EQUITY | | $ | 1,114,140 | | | | | | | | $ | 1,029,838 | | | | | | | | $ | 925,851 | | | | | | | |

| NET INTEREST INCOME | | | | | $ | 39,205 | | | | | | | | $ | 37,252 | | | | | | | | $ | 33,443 | | | | |

| NET INTEREST MARGIN | | | | | | | | | 3.83% | | | | | | | | | 3.96 | % | | | | | | | | 3.92 | % |

(1) | | Effective tax rates were determined as though interest earned on the Company’s investments in municipal bonds and loans was fully taxable. |

| (2) | | Loans held-for-sale and non-accruing loans have been included in average loans. Interest income on loans includes loan fees of $806, $1,727, and $1,326 for 2007, 2006, and 2005, respectively. |

The following table sets forth for the periods indicated a summary of the changes in interest income and interest expense resulting from changes in volume and changes in rates:

Net Interest Income – Rate/Volume Analysis:

(Tax-Equivalent basis, dollars in thousands)

| | | 2007 compared to 2006 | | 2006 compared to 2005 | |

| | | Increase / (Decrease) Due to (1) | | Increase / (Decrease) Due to (1) | |

| | | Volume | | Rate | | Net | | Volume | | Rate | | Net | |

| Interest Income: | | | | | | | | | | | | | |

| Federal Funds Sold and Other Short-term Investments | | $ | (67 | ) | $ | — | | $ | (67 | ) | $ | 10 | | $ | 219 | | $ | 229 | |

| Taxable Securities | | | (1,153 | ) | | 382 | | | (771 | ) | | 487 | | | 1,322 | | | 1,809 | |

| Non-taxable Securities | | | (1,056 | ) | | (242 | ) | | (1,298 | ) | | (362 | ) | | (214 | ) | | (576 | ) |

| Loans and Leases | | | 9,542 | | | 795 | | | 10,337 | | | 5,677 | | | 6,084 | | | 11,761 | |

| Total Interest Income | | | 7,266 | | | 935 | | | 8,201 | | | 5,812 | | | 7,411 | | | 13,223 | |

| | | | | | | | | | | | | | | | | | | | |

| Interest Expense: | | | | | | | | | | | | | | | | | | | |

| Savings and Interest-bearing Demand | | | 344 | | | 906 | | | 1,250 | | | 274 | | | 2,966 | | | 3,240 | |

| Time Deposits | | | 2,356 | | | 2,354 | | | 4,710 | | | 1,896 | | | 2,804 | | | 4,700 | |

| FHLB Advances and Other Borrowings | | | 190 | | | 98 | | | 288 | | | 730 | | | 744 | | | 1,474 | |

| Total Interest Expense | | | 2,890 | | | 3,358 | | | 6,248 | | | 2,900 | | | 6,514 | | | 9,414 | |

| | | | | | | | | | | | | | | | | | | | |

| Net Interest Income | | $ | 4,376 | | $ | (2,423 | | $ | 1,953 | | $ | 2,912 | | $ | 897 | | $ | 3,809 | |

| (1) | The change in interest due to both rate and volume has been allocated to volume and rate changes in proportion to the relationship of the absolute dollar amounts of the change in each. |

See the Company’s Average Balance Sheet and the discussions headed USES OF FUNDS, SOURCES OF FUNDS, and “RISK MANAGEMENT – Liquidity and Interest Rate Risk Management” for further information on the Company’s net interest income, net interest margin, and interest rate sensitivity position.

PROVISION FOR LOAN LOSSES

The Company provides for loan losses through regular provisions to the allowance for loan losses. The provision is affected by net charge-offs on loans and changes in specific and general allocations required on the allowance for loan losses. Provisions for loan losses totaled $3,591,000, $925,000, and $1,903,000 in 2007, 2006 and 2005, respectively.

The increased level of provision for loan losses during 2007 was largely attributable to a write-down of a single non-performing credit facility secured by two hotel properties at the time the properties were acquired by deed in lieu of foreclosure and moved into other real estate owned during the first quarter of 2007. During the first quarter of 2007, the write-down and additional provision for loan loss on this credit totaled $1,300,000 with an additional $160,000 in indirect provision charges recognized due to the impact of this write-down on the Company’s historical loss ratios and resulting required reserve levels. Also contributing to the elevated level of provision during 2007 was the Company’s loan growth.

Finally, another contributing factor to the elevated levels of provision during the year ended December 31, 2007 compared with 2006 was the finalization of settlement of a large non-performing credit in the second quarter of 2006. The Company recognized a charge-off of approximately $393,000 on this individual credit facility. The specific allocation as of year end 2005 was for considerably more than the level of charge-off allowing the Company to recover the balance of the specific allocation assigned to the credit during 2006, impacting the comparability of 2006 and 2007 provision for loan losses.

The Company’s provision for loan losses declined during 2006 in conjunction with a decline in the Company’s level of non-performing loans. The largest factor in the Company’s ability to recognize the reduced level of provision for loan losses was the finalization of settlement of a previously identified large nonperforming credit in the second quarter of 2006 that was previously discussed.

These provisions were made at a level deemed necessary by management to absorb estimated, probable incurred losses in the loan portfolio. A detailed evaluation of the adequacy of the allowance for loan losses is completed quarterly by management, the results of which are used to determine provisions for loan losses. Management estimates the allowance balance required using past loan loss experience, the nature and volume of the portfolio, information about specific borrower situations and estimated collateral values, economic conditions, and other factors. Refer also to the sections entitled CRITICAL ACCOUNTING POLICIES AND ESTIMATES and “RISK MANAGEMENT – Lending and Loan Administration” for further discussion of the provision and allowance for loan losses.

NON-INTEREST INCOME

During 2007, Non-interest Income declined $289,000 or 2% compared with 2006. The decline was primarily attributable to Net Gain / (Loss) on Securities largely offset by increases in Trust and Investment Product Fees, Service Charges on Deposit Accounts, and Insurance Revenues. During 2006, Non-interest Income totaled $15,993,000, an increase of 10% compared with 2005. The increase during 2006 was largely attributable to the gain on the sale of the Company’s FHLMC and FNMA preferred stock portfolio and an increase in revenues generated by the Company’s insurance operations.

| | | | | % Change From | |

Non-interest Income (dollars in thousands) | | Years Ended December 31, | | Prior Year | |

| | | 2007 | | 2006 | | 2005 | | 2007 | | 2006 | |

| Trust and Investment Product Fees | | $ | 2,590 | | $ | 2,210 | | $ | 2,081 | | | 17 | % | | 6 | % |

| Service Charges on Deposit Accounts | | | 4,361 | | | 3,901 | | | 3,723 | | | 12 | | | 5 | |

| Insurance Revenues | | | 5,794 | | | 5,094 | | | 4,703 | | | 14 | | | 8 | |

| Other Operating Income | | | 2,817 | | | 2,920 | | | 3,068 | | | (4 | ) | | (5 | ) |

| Subtotal | | | 15,562 | | | 14,125 | | | 13,575 | | | 10 | | | 4 | |

| Net Gains on Sales of Loans and Related Assets | | | 822 | | | 917 | | | 927 | | | (10 | ) | | (1 | ) |

| Net Gain / (Loss) on Securities | | | (680 | ) | | 951 | | | — | | | n/m | (1) | | n/m | (1) |

| TOTAL NON-INTEREST INCOME | | $ | 15,704 | | $ | 15,993 | | $ | 14,502 | | | (2 | ) | | 10 | |

(1) n/m = not meaningful

Trust and Investment Product Fees increased $380,000 or 17% during 2007 as compared to 2006. These increases were driven by increased levels of brokerage commission revenue. Service Charges on Deposit Accounts increased $460,000 or 12% during 2007 as compared to 2006. These increases were largely attributable to increased usage and fees associated with the Company’s overdraft protection service program.

Insurance Revenues increased $700,000 or 14% during 2007 as compared 2006. The increase in Insurance Revenues during 2007 was attributable primarily to commission income from Keach and Grove Insurance, Inc. which was acquired October 1, 2006 and thereby not included in the Company results during the first nine months of 2006. Insurance Revenues increased 8% for 2006 as compared 2005. The increased Insurance Revenues were primarily the result of a higher level of contingency revenues during 2006 compared with 2005, and the revenues generated from the previously mentioned insurance agency acquisition completed in the fourth quarter of 2006. For more information on the business combination, see Note 18 to the Company’s consolidated financial statements included in Item 8 of this Report.

Net Gains on Sales of Loans and Related Assets declined $95,000 or 10% during 2007 compared with 2006. The decline was attributable to the sale of the Company’s mortgage servicing rights portfolio during the second quarter of 2006. The Company sold its mortgage servicing rights relating to approximately $344.5 million of mortgage loans serviced for others for a total sales price of $3.6 million resulting in a net gain of $198,000. The gain on the sale of residential mortgage loans increased by $103,000 or 14% during 2007 due to an increase in the level of loans sold in the secondary market. Loan sales for 2007, 2006, and 2005 were $67.0 million, $55.6 million, and $64.1 million, respectively.

The Net Gain / (Loss) on Securities declined by $1,631,000 during 2007 compared with 2006. During 2007 the Company recognized a $680,000 net loss on securities related to the Company’s portfolio of non-controlling investments in other banking organizations. The net loss resulted from the sale of one of the investment holdings at a modest gain and the recognition of an other-than-temporary impairment expense in connection with the valuation of other holdings within the portfolio. The Company recognized a gain on the sale of its portfolio of FHLMC and FNMA preferred stock during 2006. The gain from the sale of this agency preferred stock portfolio totaled $951,000. The portfolio had a book value at the time of the sale of approximately $12.1 million. The Company had previously recorded a non-cash other-than-temporary impairment charge of $3.7 million on this portfolio during 2004.

NON-INTEREST EXPENSE