UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

|

|

ý ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the fiscal year ended December 31, 2017 |

| |

| or |

| |

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the transition period from _____ to _____ |

| Commission File Number: 0-12183 |

|

|

|

| BOVIE MEDICAL CORPORATION |

| (Exact name of registrant as specified in its charter) |

|

| | |

| Delaware | | 11-2644611 |

(State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

5115 Ulmerton Road, Clearwater, FL 33760

(Address of principal executive offices, zip code)

(727) 384-2323

(Issuer’s telephone number)

Securities registered pursuant to Section 12(b) of the Act:

|

| | |

| Title of each Class | | Name of each Exchange on which registered |

| Common Stock, $.001 Par Value | | NYSE MKT Market |

Securities registered under Section 12(g) of the Exchange Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes: o No ý

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes: o No ý

Indicate by check mark whether the registrant (1) filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes: ý No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes: ý No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act (Check one):

|

| | | | |

| Large accelerated filer | o | | Accelerated filer | o |

| Non-accelerated filer | o | (Do not check if a smaller reporting company) | Smaller reporting company | ý |

| | | | Emerging growth company | o |

| If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. | o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes: o No ý

The aggregate market value of the common stock held by non-affiliates computed by reference to the price at which the stock was sold, or the average bid and asked prices of such stock on the NYSE MKT exchange, as of June 30, 2017, the registrant’s most recently completed second fiscal quarter, was approximately $70.9 million.

As of March 9, 2018, 33,021,170 shares of the registrant’s $0.001 par value common stock were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

None.

BOVIE MEDICAL CORPORATION

INDEX TO ANNUAL REPORT ON FORM 10-K

December 31, 2017

|

| | | | |

| Part I | | | | Page |

| Item 1 | | | | |

| Item 1A | | | | |

| Item 1B | | | | |

| Item 2 | | | | |

| Item 3 | | | | |

| Item 4 | | | | |

| | | | | |

| Part II | | | | |

| Item 5 | | | | |

| Item 6 | | | | |

| Item 7 | | | | |

| Item 7A | | | | |

| Item 8 | | | | |

| Item 9 | | | | |

| Item 9A | | | | |

| Item 9B | | | | |

| | | | | |

| Part III | | | | |

| Item 10 | | | | |

| Item 11 | | | | |

| Item 12 | | | | |

| Item 13 | | | | |

| Item 14 | | | | |

| | | | | |

| Part IV | | | | |

| Item 15 | | | | |

| Signatures | | | | |

BOVIE MEDICAL CORPORATION

Cautionary Notes Regarding “Forward-Looking” Statements

We have included or incorporated by reference into this report, and fro time to time may make in our public filings, press releases or other public statements, certain statements that may constitute forward-looking statements. These include without limitation those under “Business” in Part I, Item 1, “Risk Factors” in Part I, Item 1A, “Legal Proceedings” in Part I, Item 3, “Management's Discussion and Analysis of Financial Condition and Results of Operations” in Part II, Item 7, and “Quantitative and Qualitative Disclosures about Market Risk” in Part II, Item 7A. In addition, our management my make forward-looking statements to analysts, investors, representatives of the media and others. These forward-looking statements are not historical facts and represent only our beliefs regarding future events, many of which, by their nature, are inherently uncertain and beyond our control. We may, in some cases, use words such as “project”, “believe”, “anticipate”, “plan”, “expect”, “estimate”, “intend”, “should”, “would”, “could”, “potentially”, “may” or other words that convey uncertainty of future events or outcomes to identify these forward-looking statements.

In connection with the “safe harbor” provisions of the Private Securities Litigation Reform Act of 1995, we are identifying important factors that, individually or in the aggregate, could cause actual results to differ materially from those contained in any forward- looking statements made by us. Any such forward-looking statements are qualified by reference to the following cautionary statements.

Forward-looking statements in this report are subject to a number of risks and uncertainties, some of which are beyond our control, including, among other things:

| |

| • | changes in general economic, business or demographic conditions or trends in the U.S. or throughout the world or changes in the political environment, including changes in GDP, interest rates and inflation; |

| |

| • | our ability to conclude a sufficient number of attractive growth projects, deploy growth capital in amounts consistent with our objectives in the prosecution of those and achieve targeted risk-adjusted returns on any growth project, including the commercialization of our J-Plasma technology; |

| |

| • | the regulatory environment, including our ability to gain requisite approval from the Food and Drug Administration, and the ability to estimate compliance costs, comply with any changes thereto, rates implemented by regulators, and our relationships and rights under and contracts with governmental agencies and authorities; |

| |

| • | disruptions or other extraordinary or force majeure events and the ability to insure against losses resulting from such events or disruptions; |

| |

| • | sudden or extreme volatility in commodity prices; |

| |

| • | changes in competitive dynamics affecting our business and the medical device industry as a whole; |

| |

| • | technological innovations leading to increased competition in the medical device industry; |

| |

| • | our ability to service, comply with the terms of and refinance at maturity our indebtedness, including due to dislocation in debt markets; |

| |

| • | changes in healthcare policy; |

| |

| • | our ability to make alternate arrangements to account for any disruptions or shutdowns that may affect suppliers’ facilities or the operations upon which our business is dependent; |

| |

| • | our ability to implement operating and internal growth strategies; |

| |

| • | environmental risks, including the impact of climate change and weather conditions; |

| |

| • | the impact of weather events, including potentially hurricanes, tornadoes and/or seasonal extremes; |

| |

| • | unplanned outages and/or failures of technical and mechanical systems; |

| |

| • | changes in U.S. income tax laws; |

| |

| • | work interruptions or other labor stoppages; |

Our actual results, performance, prospects or opportunities could differ materially from those expressed in or implied by the forward-looking statements. A description of risks that could cause our actual results to differ appears under the caption “Risk Factors” in Part I, Item 1A and elsewhere in this report. It is not possible to predict or identify all risk factors and you should not consider that description to be a complete discussion of all potential risks or uncertainties that could cause actual results to differ.

In light of these risks, uncertainties and assumptions, you should not place undue reliance on any forward-looking statements. The forward-looking events discussed in this report may not occur. These forward-looking statements are made as of the date of this report. We undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. You should, however, consult further disclosures we may make in future filings with the Securities and Exchange Commission (SEC). Past performance is not an indicator of future results.

BOVIE MEDICAL CORPORATION

PART I

ITEM 1. Business

General

Bovie Medical Corporation (“Company”, “Bovie Medical”, “we”, “us”, or “our”) was incorporated in 1982, under the laws of the State of Delaware and has its principal executive office at 5115 Ulmerton Road, Clearwater, FL 33760.

We are an energy-based medical device company specializing in developing, manufacturing and marketing a range of electrosurgical products and technologies, as well as related medical products used in doctor’s offices, surgery centers and hospitals worldwide. Our medical devices are marketed through Bovie’s own well-respected brands (Bovie®, IDS™ and DERMTM) and on a private label basis to distributors throughout the world. The Company also leverages its expertise in the design, development and manufacturing of electrosurgical equipment by producing equipment for large, well-known medical device manufacturers through original equipment manufacturing (OEM) agreements, as well as start-up companies with the need for our energy based designs.

We are also the developer of J-Plasma; a patented helium-based plasma surgical product which we believe has the potential to be a transformational product for surgeons.

Our objective is to achieve profitable, sustainable growth by increasing our market share in the advanced energy category, including the commercialization of products that have the potential to be transformational with respect to the results they produce for surgeons and patients. In order to achieve this objective, we plan to leverage our long history in the industry, along with the reputation for quality and reliability that the Bovie brand enjoys within the medical community. At the same time, we will expand our product offerings beyond radio frequency devices, move forward with research and developments projects aimed at creating value within our existing product portfolio, build our pipeline of new complementary products, and utilize multiple channels to bring new and existing products to market.

We are working to build our position in advanced electrosurgical generators and disposables, which can be used in diversified niche markets with minimally invasive surgical instruments, while furthering our status as a pioneer in plasma technology and its various medical applications.

Significant Subsidiaries

Aaron Medical Industries, Inc. is a wholly-owned Florida corporation based in Clearwater, Florida. It is principally engaged in the business of marketing our medical products through distributors worldwide under the Bovie name.

Bovie Bulgaria, EOOD is a wholly-owned limited liability company incorporated under Bulgarian law, located in Sofia, Bulgaria. It is engaged in the business of engineering and manufacturing our electrosurgical and OEM generators and accessories.

Industry

Healthcare reform has caused consolidation among providers, with hospitals merging, physician practices joining hospitals and institutions combining to form Accountable Care Organizations, to manage patients on an interdisciplinary basis. Although the medical device industry can be challenging and very competitive, we believe it will continue to have a positive, long-term growth trajectory with the number of surgical procedures performed increasing annually as a result of the aging “baby boomer” population and other healthcare trends. Additionally, we also anticipate a continued increase in minimally invasive surgical procedures due to ongoing advancements in technology coupled with continued overall pressure to reduce healthcare costs via a reduction in patient trauma and recovery time. Markets will also continue to provide growth opportunities for the medical device industry.

We believe that Bovie Medical has sustainable, competitive advantages in the medical device market for several reasons. We have a long history in electrosurgery. Our inspiration dates back to the first use of an electrosurgical generator in an operating room in the U.S. in 1926 where Dr. William T. Bovie was present. Thus, the Bovie name is recognized by surgeons the world over for having pioneered the electrosurgery field and is recognized for its outstanding product quality supported by strong engineering and research and development capabilities. This history equates to very strong recognition of the Bovie brand. We believe that our equipment and devices have and will continue to provide better experiences for patients at a lower cost to the healthcare system.

BOVIE MEDICAL CORPORATION

Intellectual Property

We rely on our intellectual property that we have developed or acquired over the years including patents, trade secrets, technical innovations and various licensing agreements to provide our future growth and build our competitive position. We have been issued 41 patents in the United States and 23 foreign patents. We have 12 pending patent applications in the United States and 9 pending foreign applications. Our intellectual property portfolio for the technology and products related to Advanced Energy products is included in these totals and continues to grow. Specific to Advanced Energy products, we have been issued 21 U.S. and 6 foreign patents and we have 12 U.S. and 9 foreign applications pending. As we continue to expand our intellectual property portfolio we believe it is critical for us to continue to invest in filing patent applications to protect our technology, inventions and improvements. However, we can give no assurance that competitors will not infringe on our patent rights or otherwise create similar or non-infringing competing products that are technically patentable in their own right.

Manufacturing and Suppliers

We are committed to producing the most technically advanced and highest quality products of their kind available on the market. We manufacture the majority of our products on our premises in Clearwater, Florida and at our facility located in Sofia, Bulgaria, which are certified under the ISO international quality standards and are subject to continuing regulation and routine inspections by the FDA to ensure compliance with regulations relating to our quality system, medical device complaint reporting and adherence to FDA restrictions on promotion and advertising. In addition, we are subject to regulations under the Occupational Safety and Health Act, the Environmental Protection Act and other federal, state and local regulations.

During the fourth quarter of 2015, we acquired all of the outstanding shares of Bovie Bulgaria, EOOD. Bovie Bulgaria operates an 18,745 square foot ISO13485 certified and FDA registered manufacturing facility located in the capital city of Sofia, which houses manufacturing, development and assembly operations.

We also have collaborative arrangements with three foreign suppliers under which we request the development of certain items and components, which we purchase pursuant to purchase orders. Our purchase order commitments are never more than one year in duration and are supported by our sales forecasts.

Backlog

The value of unshipped factory orders is not material.

Employees

At December 31, 2017, we had 211 full-time employees world-wide, of whom 4 were executive officers, 36 supervisory personnel, 14 sales personnel and 157 technical support, administrative and production employees. None of our current employees are covered by a collective bargaining agreement and we have never experienced a work stoppage. We consider our employee relations to be good.

BOVIE MEDICAL CORPORATION

Our Three Business Segments

We manage our business through three reportable operating segments: Core, OEM, and Advanced Energy.

For the year ended December 31, 2017, our Core segment contributed 73.7% of our consolidated total revenue, our OEM segment contributed 6.7% of our consolidated total revenue and our Advanced Energy segment contributed 19.6% of our consolidated total revenue.

Core Segment

Overview

Our Core segment manufactures and markets various medical products, both under private label and the Bovie brands (Bovie, IDS and DERM), to distributors worldwide, which distribute to more than 6,000 hospitals and to doctors and other healthcare facilities. New distributors are contacted through responses to our advertising in international and domestic medical journals and our presence at domestic and international trade shows.

Customers

We sell our Core products through major distributors which include Cardinal Health, Independent Medical Co-Op Inc. (IMCO), McKesson Medical Surgical, Inc., National Distribution and Contracting Inc. (NDC), Henry Schein, Medline, and Owens & Minor and have manufacturing agreements for private label of certain products with these and others.

Products

Core products consist of electrosurgery generators and accessories, battery-operated cauteries, lighting, nerve locators, eye-bubbles, penlights, and a variety of other products.

Electrosurgery Products

Electrosurgery is our largest product line and includes desiccators, generators, electrodes, electrosurgical pencils and various ancillary disposable products. These electrosurgical products are used during surgical procedures in gynecology, urology, plastic surgery, dermatology and other surgical markets, including veterinary, for the cutting and coagulation of tissue. It is estimated that electrosurgery is used in 80% of all surgical procedures. Our electrosurgery products fall under two categories, monopolar and bipolar. Monopolar products require the use of a grounding pad attached to the patient for the return of the electrical current, while bipolar products consist of two electrodes; one for the inbound current and one for the return current and therefore do not require the use of a grounding pad.

DERM 101 and DERM 102

These effective and economical 10 watt high frequency desiccators provide a low wattage platform for minor in-office skin procedures. We designed these products specifically for family practice physicians, pediatricians and other general practitioners, enabling them to perform simple skin procedures in their offices instead of referring the patient to a specialist saving the patient time and providing additional revenue generating procedures for the physician.

DERM A942™, Bantam|Pro A952™ and Specialist|Pro A1250S

Bovie’s line of electrosurgical generators has been recently updated with added features and to provide a more modern look for today’s physician office.

The new Bovie DERM A942 is a low powered 40-watt high frequency desiccator designed primarily for dermatology. These units are used mainly for removing skin lesions and growths as well as for coagulation in office-based procedures.

BOVIE MEDICAL CORPORATION

The Bovie Bantam|Pro A952 is a 50-watt high frequency desiccator with the added feature of a cut capacity for outpatient surgical procedures. In effect, the Bovie Bantam|Pro is two independent surgical devices in one small package. The Bantam|Pro replaces the Aaron A950 but with the added feature of Bovie NEM (neutral electrode monitoring), a safety feature that reduces the potential for alternate site burns. This unit is designed mainly for use in doctors’ offices and is used in a broad range of specialties including dermatology, gynecology, family practice, urology, plastic surgery and ophthalmology.

The Bovie Specialist|Pro A1250S is a 120-watt multipurpose electrosurgery generator. The unit features monopolar and bipolar functions with pad sensing and is designed to operate like the larger operating room generator in a reduced size. This product is considered to be ideally suited for office-based procedures in the specialties of gynecology, plastic surgery and urology.

Bovie Surgi-Center|Pro A2350 - IDS210 and Bovie OR|Pro A3350 - IDS310

To address market demand for more powerful electrosurgical generators, Bovie developed 200, 300 and 400-watt multipurpose digital electrosurgery generators designed for the surgi-center market and the hospital outpatient and inpatient markets. This equipment includes digital hardware that enables very high parallel data processing throughout the operation or procedure. All data is sampled and processed digitally. For the first time in electrosurgery, generators are able to measure tissue impedance in real time (5,000 times a second) thanks to the utilization of digital technology. The design of these units is based on a digital feedback system. By using dedicated digital hardware in place of a general purpose controller for processing data, our equipment enables the power to be adjusted as the impedance varies, to deliver a consistent clinical effect.

Bovie Surgi-Center|Pro A2350 and IDS210 are 200-watt generators that have the capability to be used in the majority of procedures performed today in surgi-center or outpatient settings. Although 200 watts is adequate to do most procedures in the operating room, 300 watts is considered the standard and believed to be what most hospitals and surgi-centers will require. To meet this requirement, we developed the Bovie OR|Pro A3350 - IDS 310. The Bovie OR|Pro and IDS 310 incorporate the best features of the IDS 300 and upgrade its capabilities by providing additional bipolar options, including the 225-watt Bovie bipolar and an auto bipolar feature. The 300 watt units also offer the capability to utilize two pencils with simultaneous activation in fulguration mode. In addition, these newer models meet new standards required to sell these products in many of the global markets. The Bovie IDS 400 is a 400-watt generator designed primarily for sale in markets outside of the United States. These units feature both monopolar and bipolar functions, have pad and tissue sensing and include nine blended cutting setting.

Electrosurgical Disposables

Resistick™ II

Resistick II is a trademarked and proprietary coating that is applied to stainless steel that resist eschar (scab or scar tissue caused by burning) during surgery. We have experienced strong demand for this product since its introduction in 2011 and it represents our continued expansion of the Bovie line of electrosurgical disposables.

Disposable Laparoscopic Electrodes

We have introduced a line of disposable laparoscopic electrodes in Resistick coated and stainless steel for use by physicians from a broad group of specialties including gynecology, general surgery and urology. These electrodes are offered in J-hook, L-hook, needle, ball and spatula design and have an adapter included which makes these laparoscopic electrodes usable with a 3/32“ or 4mm plug.

Cauteries

Battery Operated Cauteries

Battery operated cauteries were originally designed for precise hemostasis (to stop bleeding) in ophthalmology. The current use of cauteries has been substantially expanded to include a broad range of applications. Battery operated cauteries are primarily sterile one-time use products. We have continued to improve our offering and in 2016, had a patent issued covering our snap design cautery. It features a switch mechanism that dramatically reduces the potential for accidental activation. We manufacture one of the broadest lines of cauteries in the world, including but not limited to, a line of replaceable battery and replaceable tip cauteries, which are popular in veterinary and overseas markets.

BOVIE MEDICAL CORPORATION

Other Products

Battery Operated Medical Lights

We manufacture and market a variety of specialty lighting instruments for use in ophthalmology as well as distribute specialty lighting instruments for general surgery, hip replacement surgery and for the placement of endotracheal tubes in emergency and surgical procedures. We also manufacture and market physicians’ office use penlights.

Nerve Locator Stimulator

We manufacture a nerve locator stimulator primarily used for identifying motor nerves in hand and facial reconstructive surgery. This instrument is a sterile, self-contained, battery-operated unit, for one time use.

Competition

We compete with numerous manufacturers and distributors of medical supplies and devices, many of which are large and well-established. With the exception of endoscopic instrumentation, which are sold directly or through distribution partners to the end-user under our own brand, many of our products are private labeled. The majority of the products in our core business are sold through distributors under the Bovie label. The balance is private labeled for major distributors who sell it under their own name. By having private labeled and branded distribution, we are able to increase our position in the marketplace and compete with much larger organizations. While our private label customers distribute products through their internal sales force, the majority of our products are sold through distributors which increase our sales potential and help level the playing field relative to our large competitors that sell direct. Domestically, we continue to believe that we have a substantial market share in the field of electrosurgical generator manufacturing through our Bovie branded and OEM units.

Our main competitors in electrosurgical and accessory markets are Valleylab (a division of Medtronic), Conmed and Erbe Electromedizine. In the battery-operated cautery market, our main competitor is Beaver Visitec and in the endoscopic instrumentation market, it is Ethicon (a division of Johnson and Johnson) and Covidien Surgical Solutions.

OEM Segment

Overview

The Company leverages its expertise in the design, development and manufacturing of electrosurgical equipment by producing equipment for large, well-known medical device manufacturers through original equipment manufacturing (OEM) agreements, as well as start-up companies with the need for our energy based designs. These OEM and private label arrangements and our use of the Bovie brands enable us to gain greater market share for the distribution of our products.

Advanced Energy Segment

Overview

The Advanced Energy Segment consists primarily of J-Plasma; a patented helium-based plasma surgical product which we believe has the potential to be a transformational product for surgeons. J-Plasma has US FDA clearance, CE mark, and clearance for sale in multiple other countries and is generally indicated for the cutting, coagulation and ablation of soft tissue. The J-Plasma system consists of an electrosurgical generator unit (ESU), a handpiece and a supply of helium gas. Radiofrequency (RF) energy is delivered to the handpiece by the ESU and used to energize an electrode. When helium gas passes over the energized electrode, helium plasma is generated which allows for conduction of the RF energy from the electrode to the patient in the form of a precise helium plasma beam. The energy delivered to the patient via the helium plasma beam is very precise and cooler in temperature in comparison to other surgical energy modalities such as standard RF monopolar energy. J-Plasma has been the subject of ten white papers and has been cited therein for its clinical utility in gynecological and plastic surgery procedures.

BOVIE MEDICAL CORPORATION

Our J-Plasma product initially received FDA clearance in 2012 and a CE mark in December, 2014, which enables us to sell the product in the European Union. In 2014, we created and trained a direct sales force dedicated to J-Plasma. In 2015, we continued the commercialization process for J-Plasma with a multi-faceted strategy designed to accelerate adoption of the product. This strategy primarily involved deployment of a dedicated sales force, extending and customizing the J-Plasma product line and expanding the surgical specialties in which J-Plasma can become the “standard of care“ for certain procedures.

By the end of 2017, we had 17 field-based selling professionals and a network of 14 independent manufacturing representatives, resulting in a total sales force of 31. This is a surgery based selling organization with its focus on the use of J-Plasma for surgical procedures.

From 2015 through 2017, we launched numerous new J-Plasma products in an effort to target new surgical procedures, users, and markets. As a result of our sales, marketing and product development initiatives, we have significantly increased the number of physicians using J-Plasma by expanding usage to include the surgical oncology market and the cosmetic surgery market.

In 2017 specifically, we launched an updated version of the Bovie Ultimate generator, and a new J-Plasma handpiece for open surgical procedures. The updated version of the Bovie Ultimate generator and the new handpieces allow for the combination of our trademarked Cool-Coag technology and J-Plasma into one, multiple purpose handpiece. Cool-Coag combines standard monopolar coagulation waveforms with helium to provide three distinct modes to stop bleeding including a high fulguration/spray effect. During the second quarter of 2017, we refocused our U.S. sales team into the cosmetic surgery market. Since that time, we have seen a significant increase in the number of physicians using J-Plasma in the cosmetic surgery market.

In order to assist us in leveraging J-Plasma’s precision and effectiveness in multiple surgical specialties, we launched a Medical Advisory Board in 2015 which is currently comprised of surgeons who are recognized leaders in GYN, urology, cardiovascular and cardiothoracic surgery. In 2017, we added an additional surgeon to this board from the cosmetic surgical specialty.

In 2018, our J-Plasma commercial strategy in the U.S. will be primarily focused on advancing the usage of J-Plasma in the cosmetic surgery market. In our international markets, we will also focus on cosmetic surgery and will continue to focus on the surgical oncology market. Our primary international focus will be on advancing the adoption of J-Plasma in the hospital setting. We believe the majority of our targeted procedures in international markets take place in the hospital surgical suite and believe the sales process is shorter in hospitals in international markets as compared to those in the United States. Also, in 2018, we will initiate a clinical and regulatory strategy to support our market focus, once complete, we will launch a corresponding marketing campaign.

We are continuing to make substantial investments in the development and marketing of our J-Plasma technology for the long term benefit of the Company and its stakeholders and this may adversely affect our short term profitability and cash flow, particularly over the next 12 to 24 months. While we believe that these investments have the potential to generate additional revenues and profits in the future, there can be no assurance that J-Plasma will be successful or that such future revenues and profitability will be realized.

Customers

We primarily sell our J-Plasma products through our direct sales force to physicians, surgical centers and hospitals.

Products

During 2017, Advanced Energy Products consisted of the J-Plasma line of products and the Plazxact arthroscopic bipolar ablator. The J-Plasma system consists of an electrosurgical generator unit (ESU), a handpiece and a supply of helium gas. Radiofrequency (RF) energy is delivered to the handpiece by the ESU and used to energize an electrode. When helium gas passes over the energized electrode, helium plasma is generated which allows for conduction of the RF energy from the electrode to the patient in the form of a precise helium plasma beam. The energy delivered to the patient via the helium plasma beam is very precise and cooler in temperature in comparison to other surgical energy modalities such as standard RF monopolar energy. The Plazxact arthroscopic bipolar ablator is used to ablate damaged, soft tissue in joint procedures to help improve function or reduce pain. The Plazxact system is designed with a very efficient tip design that allows the ablator to be activated with any standard electrosurgical generator. This eases and shortens the sales cycle for the product by removing the need to sell capital equipment to the hospital.

BOVIE MEDICAL CORPORATION

J-Plasma Generator

In June 2017, we launched the newest version of the Bovie Ultimate™ generator. The Bovie Ultimate 2.0 is a high frequency electrosurgical generator that can be used for delivery of RF energy and/or helium gas plasma to cut, coagulate and ablate soft tissue during open and laparoscopic surgical procedures. The generator offers users monopolar, bipolar and J-Plasma features in a single generator. It also powers the Cool-Coag technology that has been incorporated into the new Precise Open and Precise FLEX J-Plasma handpieces that were released in December 2017. These 2017 new product releases continue to expand the procedure base for J-Plasma by providing the surgeons with the tools they need to access additional anatomic locations and perform specific procedures.

J-Plasma Disposable Portfolio

We offer different hand pieces for open and laparoscopic procedures. The helium-based plasma generated from these devices have been shown to cause less thermal damage to tissue than CO2 laser, argon plasma and RF energy products currently available on the market. The technology has a general indication and can be used for cutting, coagulating and ablating soft tissue. The two primary specialties that are targeted in phase one of the product launch are surgical oncology and cosmetic surgery. The advantages of helium plasma continue to be studied throughout the medical and scientific communities. We believe that surgical applications are just one area of opportunity for this technology.

Competition

Currently, we are the only company with helium-based plasma and retractable blade products. However, there are RF based competitors, argon plasma competitors, and CO2 laser competitors for our target market. We believe our competitive position did not change in 2017.

BOVIE MEDICAL CORPORATION

ITEM 1A. Risk factors

In addition to risks and uncertainties in the ordinary course of business, important risk factors that may affect us are discussed below. Additional risks not presently known to us or that we currently believe are immaterial may also significantly impair our business operations.

Risks Related to Our Industry

The medical device industry is highly competitive and we may be unable to compete effectively.

The medical device industry is highly competitive. Many competitors in this industry are well-established, do a substantially greater amount of business and have greater financial resources and facilities than we do.

Domestically, we believe we rank third in the number of units sold in the field of electrosurgical generator manufacturing and we sell our products and compete with other manufacturers in various ways. In addition to advertising, attending trade shows and supporting our distribution channels, we strive to enhance product quality and functionality, improve user friendliness and expand product exposure.

We have also invested and continue to invest, substantial resources to develop and monetize our J-Plasma technology. If we are unable to gain acceptance in the marketplace of J-Plasma, our business and results of operations may be materially and adversely affected.

We also compete by private labeling our products for major distributors under their label. This allows us to increase our position in the marketplace and thereby compete from two different approaches, our Bovie label and our customers’ private label. Our private label customers distribute our products under their name through their internal sales force. We believe our main competitors do not private label their products.

Lastly, at this time, we sell the majority of our products through distributors. Many of the companies we compete with sell direct, thus competing directly with distributors they sometimes use.

Our industry is highly regulated by the U.S. Food and Drug Administration and international regulatory authorities, as well as other governmental, state and federal agencies which have substantial authority to establish criteria which must be complied with in order for us to continue in operation.

United States

Our products and research and development activities are subject to regulation by the FDA and other regulatory bodies. FDA regulations govern, among other things, the following activities:

•Product development

•Product testing

•Product labeling

•Product storage

•Pre-market clearance or approval

•Advertising and promotion

•Product traceability and

•Product indications.

In the United States, medical devices are classified on the basis of control deemed necessary to reasonably ensure the safety and effectiveness of the device. Class I devices are subject to general controls. These controls include registration and listing, labeling, pre-market notification and adherence to the FDA Quality System Regulation. Class II devices are subject to general and special controls. Special controls include performance standards, post market surveillance, patient registries and FDA guidelines. Class III devices are those which must receive pre-market approval by the FDA to ensure their safety and effectiveness. Currently, we only manufacture Class I and Class II devices. Pre-market notification clearance must be obtained for some Class I and most Class II devices when the FDA does not require pre-market approval. All of our products have been cleared by, or are exempt from, the pre-market notification process.

BOVIE MEDICAL CORPORATION

A pre-market approval application is required for most Class III devices. A pre-market approval application must be supported by valid scientific evidence to demonstrate the safety and effectiveness of the device. The pre-market approval application typically includes:

•Results of bench and laboratory tests, animal studies and clinical studies

•A complete description of the device and its components; and

| |

| • | A detailed description of the methods, facilities and controls used to manufacture the device and proposed labeling. |

The pre-market approval process can be expensive, uncertain and lengthy. A number of devices for which pre-market approval has been sought by other companies have never been approved for marketing.

International Regulation

To market products in the European Union, our products must bear the “CE” mark. Manufacturers of medical devices bearing the CE mark have gone through a conformity assessment process that assures that products are manufactured in compliance with a recognized quality system and to comply with the European Medical Devices Directive.

Each device that bears a CE mark has an associated technical documentation that includes a description of the following:

•Description of the device and its components,

•A Summary of how the device complies with the essential requirements of the medical devices directive,

•Safety (risk assessment) and performance of the device,

•Clinical evaluations with respect to the device,

•Methods, facilities and quality controls used to manufacture the device and

•Proposed labeling for the device.

Manufacturing and distribution of a device is subject to ongoing surveillance by the appropriate regulatory body to ensure continued compliance with quality system and reporting requirements.

We began CE marking of devices for sale in the European Union in 1999. In addition to the requirement to CE mark, each member country of the European Union maintains the right to impose additional regulatory requirements.

Outside of the European Union, regulations vary significantly from country to country. The time required to obtain approval to market products may be longer or shorter than that required in the United States or the European Union. Certain European countries outside of the European Union do recognize and give effect to the CE mark certification. We are permitted to market and sell our products in those countries.

If we are unable to successfully introduce new products or fail to keep pace with competitive advances in technology, our business, financial condition and results of operations could be adversely affected. In addition, our research and development efforts rely upon investments and alliances and we cannot guarantee that any previous or future investments or alliances will be successful.

Our research and development activities are an essential component of our efforts to develop new and innovative products for introduction in the marketplace. New and improved products play a critical role in our sales growth. We continue to place emphasis on the development of proprietary products, such as our J-Plasma technology, and product improvements to complement and expand our existing product lines. We maintain close working relationships with physicians and medical personnel in hospitals and universities who assist in product research and areas of development. Our research and development activities are primarily conducted internally and are expensed as incurred. These expenses include direct expenses for wages, materials and services associated with the development of our products net of any reimbursements from customers. Research and development expenses do not include any portion of general and administrative expenses. Our research and development activities are conducted at our Clearwater, Florida and Sofia, Bulgaria facilities. We expect to continue making future investments to enable us to develop and market new technologies and products to further our strategic objectives and strengthen our existing business. However, we cannot guarantee that any of our previous or future investments in both facilities will be successful or that our new products such as J-Plasma and PlazXact arthroscopic ablator, will gain market acceptance, the failure of which would have a material adverse effect on our business and results of operations.

BOVIE MEDICAL CORPORATION

The amount expended by us on research and development of our products during the years 2017, 2016 and 2015, totaled approximately $2.5 million, $2.6 million and $2.2 million, respectively. During the past three years, we invested substantial resources in the development and marketing of our Advanced Energy product technology. We have not incurred any direct costs relating to environmental regulations or requirements. For 2018, we expect to invest 6.5% to 7.0% of revenue for research and development activities.

Even if we are successful in developing and obtaining approval for our new product candidates, there are various circumstances that could prevent the successful commercialization of the products.

Our ability to successfully commercialize our products, including our J-Plasma technology, will depend on a number of factors, any of which could delay or prevent commercialization, including:

| |

| • | our product is determined to be ineffective or unsafe following approval and is removed from the market or we are required to perform additional research and development to further prove the safety and effectiveness of the product before re-entry into the market; |

| |

| • | the regulatory approvals of our new products are delayed or we are required to conduct further research and development of our products prior to receiving regulatory approval; |

| |

| • | we are unable to build a sales and marketing group to successfully launch and sell our new products; |

| |

| • | we are unable to raise the additional funds needed to successfully develop and commercialize our products or acquire additional products for growth; |

| |

| • | we are required to allocate available funds to litigation matters; |

| |

| • | we are unable to manufacture the quantity of product needed in accordance with current good manufacturing practices to meet market demand, or at all; |

| |

| • | competition from other products or technologies prevents or reduces market acceptance of our products; |

| |

| • | we do not have and cannot obtain the intellectual property rights needed to manufacture or market our products without infringing on another company’s patents; or |

| |

| • | we are unsuccessful in defending against patent infringement or other intellectual property rights, claims that could be brought against us, our products or technologies; |

The failure to successfully acquire or develop and commercialize new products will have a material and adverse effect on the future growth of our business, financial condition and results of operations.

Our international operations subject us to foreign currency fluctuations and other risks associated with operating in foreign countries.

We operate internationally and enter into transactions denominated in foreign currencies. To date, we have not hedged our exposure to changes in foreign currency exchange rates and as a result, we are subject to foreign currency transaction and translation gains and losses. We purchase goods and services in U.S. dollars and Euros. Foreign exchange risk is managed primarily by satisfying foreign denominated expenditures with cash flows or assets denominated in the same currency therefore we are subject to some foreign currency fluctuation risk. Our currency value fluctuations were not material for 2017. In addition, political changes or instability throughout the world could adversely affect our business internationally.

Our operations and cash flows may be adversely impacted by healthcare reform legislation.

The Patient Protection and Affordable Care Act and Health Care and Education Affordability Reconciliation Act were enacted into law in the U.S. in March 2010. Among other initiatives, this legislation imposes a 2.3% excise tax on domestic sales of Class I, II and III medical devices beginning in 2013. The Consolidated Appropriations Act, 2016, signed into law on Dec. 18, 2015, includes a two year moratorium on the medical device excise tax imposed by Internal Revenue Code section 4191. Thus, the medical device excise tax does not apply to the sale of a taxable medical device by the manufacturer, producer, or importer of the device during the period beginning on Jan. 1, 2016 and ending on Dec. 31, 2017. H.R. 195, signed into law on January 22, 2018, extends the moratorium for an additional two years, ending on December 31, 2019. As approximately 85.2% of our 2017 sales were derived in the U.S., we cannot predict if any additional regulations will be implemented at the federal or state level, or the effect of any future legislation or regulation in the U.S. or internationally.

BOVIE MEDICAL CORPORATION

Our operations may experience higher costs to produce our products as a result of changes in prices for oil, gasoline and other commodities.

We use plastics and other petroleum-based materials along with precious metals contained in electronic components as raw materials in many of our products. Prices of oil and gasoline also significantly affect our costs for freight and utilities. Oil, gasoline and precious metal prices are volatile and may increase, resulting in higher costs to produce and distribute our products. Due to the highly competitive nature of the healthcare industry and the cost-containment efforts of our customers we may be unable to pass along cost increases through higher prices. If we are unable to fully recover these costs through price increases or offset through other cost reductions, our results of operations could be materially and adversely affected.

Our manufacturing facilities are located in Clearwater, Florida and Sophia, Bulgaria and could be affected due to multiple weather risks, including risks to our Florida facility from hurricanes and similar phenomena.

Our manufacturing facilities are located in Clearwater, Florida and Sophia, Bulgaria and could be affected by multiple weather risks. Most notably hurricanes in Clearwater, Florida. Although we carry property and casualty insurance and business interruption insurance, future possible disruptions of operations or damage to property, plant and equipment due to hurricanes or other weather risks could result in impaired production and affect our ability to meet our commitments to our customers and impair important business relationships, the loss of which could adversely affect our operations and profitability. We do however maintain a backup generator at our Clearwater facility and a disaster recovery plan is in place to help mitigate this risk.

Risks Relating to Our Business

We have historically done a substantial amount of business with seven of our top ten customers, who are also major distributors of our products, which as a group have produced substantial revenues for our Company. Loss of business from a major customer will likely materially and adversely affect our business.

We manufacture the majority of our products at our Clearwater, Florida and Sofia, Bulgaria facilities. Labor-intensive sub-assemblies and labor-intensive products may be out-sourced to our specification. Although we sell through distributors, we market our products through national trade journal advertising, direct mail, distributor sales representatives and trade shows, under the Bovie name and private label. Major distributors include Cardinal Health, Independent Medical Co-Op Inc. (IMCO), McKesson Medical Surgical, Inc., Medline, National Distribution and Contracting Inc. (NDC) and Owens & Minor. If any of these distributor relationships are terminated or not replaced, our revenue from the territories served by these distributors could be adversely affected.

We are also dependent on OEM customers who have no legal obligation to purchase products from us. Should such customers fail to give us purchase orders for the product after development, our future business could be negatively affected. Furthermore, no assurance can be given that such customers will give sufficient high priority to our products. Finally, disagreements or disputes may arise between us and our customers, which could adversely affect production and sales of our products.

We rely on certain suppliers and manufacturers for raw materials and other products and are vulnerable to fluctuations in the availability and price of such products and services.

Fluctuations in the price, availability and quality of the raw materials we use in our manufacturing could have a negative effect on our cost of sales and our ability to meet the demands of our customers. Inability to meet the demands of our customers could result in the loss of future sales.

In addition, the costs to manufacture our products depend in part on the market prices of the raw materials used to produce them. We may not be able to pass along to our customers all or a portion of our higher costs of raw materials due to competitive and marketing pressures, which could decrease our earnings and profitability.

We also have collaborative arrangements with three key foreign suppliers under which we request the development of certain items and components and we purchase them pursuant to purchase orders. Our purchase order commitments are never more than one year in duration and are supported by our sales forecasts. The majority of our raw materials are purchased from sole-source suppliers. While we believe we could ultimately procure other sources for these components, should we experience any significant disruptions in this key supply chain, there are no assurances that we could do so in a timely manner which could render us unable to meet the demands of our customers, resulting in a material and adverse effect on our business and operating results.

BOVIE MEDICAL CORPORATION

If we are unable to protect our patents or other proprietary rights, or if we infringe on the patents or other proprietary rights of others, our competitiveness and business prospects may be materially damaged.

We have been issued 41 patents in the United States and 23 foreign patents. We have 12 pending patent applications in the United States and 9 pending foreign applications. Our intellectual property portfolio for the technology and products related to Advanced Energy products are included in these totals and continues to grow. Specific to Advanced Energy products, we have been issued 21 U.S. and 6 foreign patents and we have 12 U.S. and 9 foreign applications pending. We intend to continue to seek legal protection, primarily through patents, for our proprietary technology. Seeking patent protection is a lengthy and costly process and there can be no assurance that patents will be issued from any pending applications, or that any claims allowed from existing or pending patents will be sufficiently broad or strong to protect our proprietary technology. There is also no guarantee that any patents we hold will not be challenged, invalidated or circumvented, or that the patent rights granted will provide competitive advantages to us. Our competitors have developed and may continue to develop and obtain patents for technologies that are similar or superior to our technologies. In addition, the laws of foreign jurisdictions in which we develop, manufacture or sell our products may not protect our intellectual property rights to the same extent as do the laws of the United States.

Adverse outcomes in current or future legal disputes regarding patent and other intellectual property rights could result in the loss of our intellectual property rights, subject us to significant liabilities to third parties, require us to seek licenses from third parties on terms that may not be reasonable or favorable to us, prevent us from manufacturing, importing or selling our products, or compel us to redesign our products to avoid infringing third parties’ intellectual property. As a result, our product offerings may be delayed and we may be unable to meet customers’ requirements in a timely manner. Regardless of the merit of any related legal proceeding, we have incurred in the past and may be required to incur in the future substantial costs to prosecute, enforce or defend our intellectual property rights. Even in the absence of infringement by our products of third parties’ intellectual property rights, or litigation related to trade secrets, we have elected in the past and may in the future elect to enter into settlements to avoid the costs and risks of protracted litigation and the diversion of resources and management’s attention. However, if the terms of settlements entered into with certain of our competitors are not observed or enforced, we may suffer further costs and risks. Any of these circumstances could have a material adverse effect on our business, financial condition and resources or results of operations.

Our ability to develop intellectual property depends in large part on hiring, retaining and motivating highly qualified design and engineering staff with the knowledge and technical competence to advance our technology and productivity goals. To protect our trade secrets and proprietary information, generally we have entered into confidentiality agreements with our employees, as well as with consultants and other parties. If these agreements prove inadequate or are breached, our remedies may not be sufficient to cover our losses.

We have been and may in the future become subject to litigation proceedings that could materially and adversely affect our business.

The medical device industry is characterized by frequent claims and litigation, and we are and may become subject to various claims, lawsuits and proceedings in the ordinary course of our business, including claims by current or former employees, distributors and competitors, and with respect to our products and product liability claims, lawsuits and proceedings.

We are involved in a number of legal actions relating to the use of our J-Plasma technology. The outcomes of these legal actions are not within our complete control and may not be known for prolonged periods of time. In the opinion of management, the Company has meritorious defenses, and such claims are adequately covered by insurance, or are not expected, individually or in the aggregate, to result in a material, adverse effect on our financial condition. However, in the event that damages exceed the aggregate coverage limits of our policy or if our insurance carriers disclaim coverage, we believe it is possible that costs associated with these claims could have a material adverse impact on our consolidated earnings, financial position or cash flows.

In accordance with authoritative guidance, we record a liability in our consolidated financial statements for these actions when a loss is known or considered probable and the amount can be reasonably estimated. If the reasonable estimate of a known or probable loss is a range, and no amount within the range is a better estimate than any other, the minimum amount of the range is accrued. If a loss is reasonably possible, but not known or probable, and can be reasonably estimated, the estimated loss or range of loss is disclosed in the notes to the consolidated financial statements. In most cases, significant judgment is required to estimate the amount and timing of a loss to be recorded.

BOVIE MEDICAL CORPORATION

Intellectual Property Litigation or Trade Secrets

We have in the past, experienced certain allegations of infringement of intellectual property rights and use of trade secrets and may receive other such claims, with or without merit, in the future. Previously, claims of infringement of intellectual property rights have sometimes evolved into litigation against us and they may continue to do so in the future. It is inherently difficult to assess the outcome of litigation. Although we believe we have had adequate defenses to these claims and that the outcome of the litigation will not have a material adverse impact on our business, financial condition, or results of operations, there can be no assurances that we will prevail. Any such litigation could result in substantial cost to us, significantly reduce our cash resources and create a diversion of the efforts of our technical and management personnel, which could have a material and adverse effect on our business, financial condition and operating results. If we are unable to successfully defend against such claims, we could be prohibited from future sales of the allegedly infringing product or products, which could materially and adversely affect our future growth.

Our business is subject to the potential for defects or failures associated with our products which could lead to recalls or safety alerts and negative publicity.

Manufacturing flaws, component failures, design defects, off-label uses or inadequate disclosure of product-related information could result in an unsafe condition or the injury or death of a patient. These problems could lead to a recall of, or issuance of a safety alert relating to our products and result in significant costs and negative publicity. Due to the strong name recognition of our brands, an adverse event involving one of our products could result in reduced market acceptance and demand for all products within that brand and could harm our reputation and our ability to market our products in the future. In some circumstances, adverse events arising from or associated with the design, manufacture or marketing of our products could result in the suspension or delay of our current regulatory reviews of our applications for new product approvals. We also may undertake voluntarily to recall products or temporarily shut down certain production lines based on internal safety and quality monitoring and testing data. Any of the foregoing problems could disrupt our business and have a material adverse effect on our business, results of operations, financial condition and cash flows.

We have incurred and may in the future incur impairments to our long-lived assets.

We review our long-lived assets, including intangible assets, for impairment annually or more frequently if events or changes in circumstances indicate that the carrying amount of these assets may not be recoverable. Additionally, if in any period our stock price decreases to the point where our fair value, as determined by our market capitalization, is less than the book value of our assets, this could also indicate a potential impairment and we may be required to record an impairment charge in that period which could adversely affect our results of operations.

Our valuation methodology for assessing impairment requires management to make judgments and assumptions based on historical experience and to rely heavily on projections of future operating performance. We operate in highly competitive environments and projections of future operating results and cash flows may vary significantly from actual results. Additionally, if our analysis indicates potential impairment to a long-lived intangible asset, we may be required to record additional charges to earnings in our financial statements, which could negatively impact our results of operations.

Risks Related to Our Stock

The market price of our stock has been and may continue to be highly volatile.

Our common stock is listed on the NYSE MKT Market under the ticker symbol “BVX”. The market price of our stock has been and may continue to be highly volatile and announcements by us or by third parties may have a significant impact on our stock price. These announcements may include:

•our listing status on the NYSE MKT Market;

•our operating results falling below the expectations of public market analysts and investors;

•developments in our relationships with or developments affecting our major customers;

•negative regulatory action or regulatory non-approval with respect to our new products;

•government regulation, governmental investigations, or audits related to us or to our products;

•developments related to our patents or other proprietary rights or those of our competitors and

•changes in the position of securities analysts with respect to our stock.

BOVIE MEDICAL CORPORATION

The stock market has from time to time experienced extreme price and volume fluctuations, which have particularly affected the market prices for the medical technology sector companies and which have often been unrelated to their operating performance. These broad market fluctuations may adversely affect the market price of our common stock.

Historically, when the market price of a stock has been volatile, holders of that stock have often instituted securities class action litigation against the company that issued the stock. If any of our stockholders brought a lawsuit against us, we could incur substantial costs defending the lawsuit. The lawsuit could also divert the time and attention of our management.

In addition, future sales by existing stockholders, warrant holders receiving shares upon the exercise of warrants, or any new stockholders receiving our shares in any financing transaction may lower the price of our common stock, which could result in losses to our stockholders. Future sales of substantial amounts of common stock in the public market, or the possibility of such sales occurring, could adversely affect prevailing market prices for our common stock or our future ability to raise capital through an offering of equity securities. Substantially all of our common stock is freely tradable in the public market without restriction under the Securities Act, unless these shares are held by our “affiliates”, as that term is defined in Rule 144 under the Securities Act.

We have no present intention to pay dividends on our common stock and, even if we change that policy, we may be unable to pay dividends on our common stock.

We currently do not anticipate paying any dividends on our common stock in the foreseeable future. We currently intend to retain future earnings, if any, to finance operations and invest in our business. Any declaration and payment of future dividends to holders of our common stock will be at the discretion of our board of directors and will depend on many factors, including our financial condition, earnings, capital requirements, level of indebtedness, statutory and contractual restrictions applying to the payment of dividends and other considerations that our board of directors deems relevant.

If we change that policy and commence paying dividends, we will not be obligated to continue paying those dividends and our stockholders will not be guaranteed, or have contractual or other rights, to receive dividends. If we commence paying dividends in the future, our board of directors may decide, in its discretion, at any time, to decrease the amount of dividends, otherwise modify or repeal the dividend policy or discontinue entirely the payment of dividends. Under the Delaware law, our board of directors may not authorize the payment of a dividend unless it is either paid out of our statutory surplus.

The low trading volume of our common stock may adversely affect the price of our shares and their liquidity.

Although our common stock is listed on the NYSE MKT exchange, our common stock has experienced low trading volume. Limited trading volume may subject our common stock to greater price volatility and may make it difficult for investors to sell shares at a price that is attractive to them.

We may in the future seek to raise funds through equity offerings, which could have a dilutive effect on our common stock.

In the future we may determine to raise capital through offerings of our common stock, securities convertible into our common stock or rights to acquire these securities or our common stock. For instance, we are authorized to issue up to 75,000,000 shares of common stock and up to 10,000,000 shares of preferred stock. The result of sales of such securities, or the conversion of the shares of Preferred Stock into shares of common stock, the exercise of warrants issued in connection with such offering or the triggering of anti-dilution provisions in such securities would ultimately be dilutive to our common stock by increasing the number of shares outstanding. We cannot predict the effect this dilution may have on the price of our common stock. In addition, the shares of preferred stock may have rights which are senior or superior to those of the common stock, such as rights relating to voting, the payment of dividends, redemption or liquidation.

Exercise of warrants and options issued by us will dilute the ownership interest of existing stockholders.

As of December 31, 2017, the warrants issued by us in December 2013 were exercisable for up to approximately 40,000 shares of our common stock, representing approximately 0.1% of our outstanding common stock.

As of December 31, 2017, our outstanding stock options to our employees, officers, directors and consultants amounted to approximately 4,860,157 shares of our common stock, representing approximately 14.8% of our outstanding common stock.

BOVIE MEDICAL CORPORATION

The exercise of some or all of our warrants and stock options will dilute the ownership interests of existing stockholders. Any sales in the public market of the common stock issuable upon such conversion or exercise could adversely affect prevailing market prices of our common stock.

ITEM 1B. Unresolved Staff Comments

Not Applicable.

ITEM 2. Properties

Bovie currently maintains a 60,000 square foot facility which consists of office, warehousing, manufacturing and research space located at 5115 Ulmerton Rd., Clearwater, Florida. Monthly principal and interest payments relating to the purchase of this facility are approximately $29,000 per month.

In October, 2015, through our acquisition of Bovie Bulgaria, we acquired a lease for 18,745 square feet of office, warehousing and manufacturing facilities located in Sofia, Bulgaria. The rental cost of the facility is approximately $5,424 per month.

In March 2014, we signed a lease for offices located in Purchase, New York. The lease is for 3,650 square feet of office space with a monthly cost of approximately $9,277 per month. We decided to consolidate operations in the Purchase, NY office with the facility in Clearwater. Based on this, we determined the office in Purchase, NY was no longer necessary and decided to cease all activity at the location. The remaining lease of approximately $175,000, has been expensed in 2017, included as part of severance and related expense and will be operational cash outflows during 2018 and 2019.

ITEM 3. Legal Proceedings

The medical device industry is characterized by frequent claims and litigation, and we are and may become subject to various claims, lawsuits and proceedings in the ordinary course of our business, including claims by current or former employees, distributors and competitors, and with respect to our products and product liability claims, lawsuits and proceedings.

We are involved in a number of legal actions relating to the use of our J-Plasma technology. The outcomes of these legal actions are not within our complete control and may not be known for prolonged periods of time. In the opinion of management, the Company has meritorious defenses, and such claims are adequately covered by insurance, or are not expected, individually or in the aggregate, to result in a material, adverse effect on our financial condition. However, in the event that damages exceed the aggregate coverage limits of our policy or if our insurance carriers disclaim coverage, we believe it is possible that costs associated with these claims could have a material adverse impact on our consolidated earnings, financial position or cash flows.

In accordance with authoritative guidance, we record a liability in our consolidated financial statements for these actions when a loss is known or considered probable and the amount can be reasonably estimated. If the reasonable estimate of a known or probable loss is a range, and no amount within the range is a better estimate than any other, the minimum amount of the range is accrued. If a loss is reasonably possible, but not known or probable, and can be reasonably estimated, the estimated loss or range of loss is disclosed in the notes to the consolidated financial statements. In most cases, significant judgment is required to estimate the amount and timing of a loss to be recorded.

ITEM 4. Mine Safety Disclosures

Not Applicable.

BOVIE MEDICAL CORPORATION

PART II

ITEM 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

Our common stock currently is traded on the NYSE MKT. The table shows the reported high and low bid prices for the common stock during each quarter of the last eight respective quarters. These prices do not represent actual transactions and do not include retail markups, markdowns or commissions.

|

| | | | | | | | | | | | | | | |

| | 2017 | | 2016 |

| | High | | Low | | High | | Low |

| 4th Quarter | $ | 4.29 |

| | $ | 2.54 |

| | $ | 5.55 |

| | $ | 3.50 |

|

| 3rd Quarter | 3.48 |

| | 2.17 |

| | 5.21 |

| | 1.68 |

|

| 2nd Quarter | 2.83 |

| | 1.87 |

| | 1.97 |

| | 1.56 |

|

| 1st Quarter | 3.95 |

| | 2.53 |

| | 2.44 |

| | 1.60 |

|

On March 9, 2018, the closing bid for our common stock as reported by the NYSE MKT exchange was $2.37 per share. As of March 9, 2018, we had 601 stockholders of record. Since many stockholders choose to hold their shares under the name of their brokerage firm, we estimate that the actual number of stockholders was over 3,500 shareholders.

Securities Authorized for Issuance Under Equity Compensation Plans

|

| | | | | | | | | |

| | Number of Securities to be Issued Upon Exercise of Outstanding Options, Warrants and Rights

(a) | | Weighted Average Exercise Price of Outstanding Options, Warrants and Rights

(b) | | Number of Securities Remaining Available for Future Issuance Under Equity Compensation Plans (excluding securities reflected in column (a))

(c) |

| Equity compensation plans approved by security holders | 2,129,674 |

| | $ | 2.86 |

| | 2,280,578 |

|

Equity compensation plans not approved by security holders (1) | 2,730,482 |

| | $ | 3.11 |

| | — |

|

| Total | 4,860,157 |

| | $ | 3.00 |

| | 2,280,578 |

|

Dividend Policy

We have never declared or paid any cash dividends on our common stock and we currently do not anticipate paying cash dividends in the foreseeable future. We currently expect to retain any future earnings to fund the operation and expansion of our business.

BOVIE MEDICAL CORPORATION

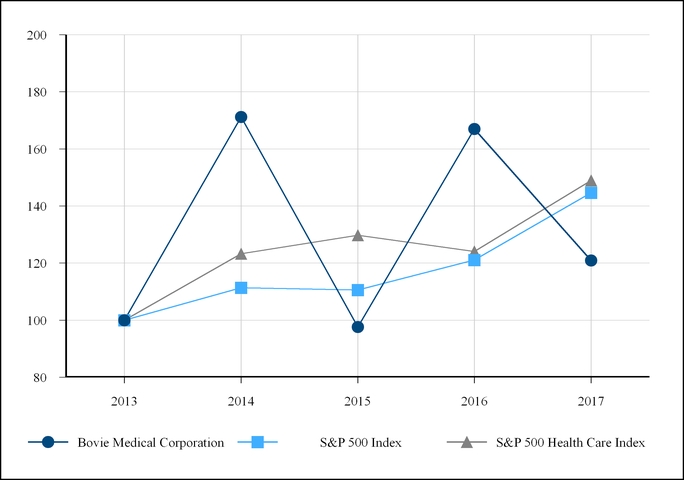

Five Year Performance Graph

The following line graph compares the cumulative total return of our common shares with the cumulative total return of the Standard & Poor’s Composite 500 Stock Index (the "S&P 500 Index") and the Standard & Poor's Composite 500 Healthcare Sector Index (the "S&P 500 Healthcare Index"). The line graph assumes, in each case, an initial investment of $100 on December 31, 2013, based on the market prices at the end of each fiscal year through and including December 31, 2017, and reinvestment of dividends.

|

| | | | | | | | | | | | | | |

| | December 31, |

| | 2013 | | 2014 | | 2015 | | 2016 | | 2017 |

| Bovie Medical Corporation | 100.00 |

| | 171.16 |

| | 97.67 |

| | 166.97 |

| | 120.93 |

|

| S&P 500 Index | 100.00 |

| | 111.39 |

| | 110.58 |

| | 121.12 |

| | 144.64 |

|

| S&P 500 Health Care Index | 100.00 |

| | 123.3 |

| | 129.72 |

| | 124.07 |

| | 148.89 |

|

BOVIE MEDICAL CORPORATION

ITEM 6. Selected Financial Data

The following selected consolidated financial data (presented in thousands, except per share amounts and employee data) are derived from our consolidated financial statements. This data should be read in conjunction with the consolidated financial statements and notes thereto and with Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

|

| | | | | | | | | | | | | | | | | | | |

| | 2017 | | 2016 | | 2015 | | 2014 | | 2013 |

| Sales | $ | 38,883 |

| | $ | 36,627 |

| | $ | 29,520 |

| | $ | 27,681 |

| | $ | 23,660 |

|

| Cost of sales | 19,122 |

| | 18,712 |

| | 16,963 |

| | 18,689 |

| | 14,462 |

|

| Gross profit | 19,761 |

| | 17,915 |

| | 12,557 |

| | 8,992 |

| | 9,198 |

|

| Other costs and expenses: | | | | | | | | | |

| Research and development | 2,455 |

| | 2,618 |

| | 2,160 |

| | 1,416 |

| | 1,260 |

|

| Professional services | 1,771 |

| | 1,486 |

| | 1,484 |

| | 1,016 |

| | 1,835 |

|

| Salaries and related costs | 7,906 |

| | 9,038 |

| | 7,482 |

| | 5,723 |

| | 3,992 |

|

| Selling, general and administrative | 11,370 |

| | 8,565 |

| | 8,417 |

| | 6,686 |

| | 5,777 |

|

| Severance and related expense | 1,524 |

| | — |

| | — |

| | — |

| | — |

|

| Total other costs and expenses | 25,026 |

| | 21,707 |

| | 19,543 |

| | 14,841 |

| | 12,864 |

|

| Loss from operations | (5,265 | ) | | (3,792 | ) | | (6,986 | ) | | (5,849 | ) | | (3,666 | ) |

| Interest expense, net | (136 | ) | | (158 | ) | | (158 | ) | | (151 | ) | | (237 | ) |

| Investor warrants issuance cost | — |

| | — |

| | — |

| | — |

| | (664 | ) |

| Fee associated with refinance | — |

| | — |

| | — |

| | — |

| | (543 | ) |

| Change in fair value of derivative liabilities | 183 |

| | 64 |

| | 1,799 |

| | (7,285 | ) | | (842 | ) |

| Total other income (loss), net | 47 |

| | (94 | ) | | 1,641 |

| | (7,436 | ) | | (2,286 | ) |

| Loss before income taxes | (5,218 | ) | | (3,886 | ) | | (5,345 | ) | | (13,285 | ) | | (5,952 | ) |

| Income tax (benefit) expense | (156 | ) | | 64 |

| | 25 |

| | 3,997 |

| | (1,613 | ) |