UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| | For the fiscal year ended December 31, 2007 |

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| | For the transition period from to |

Commission file number 1-1070

OLIN CORPORATION

(Exact name of registrant as specified in its charter)

| | |

| Virginia | 13-1872319 |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

190 Carondelet Plaza, Suite 1530, Clayton, MO (Address of principal executive offices) | 63105-3443 (Zip code) |

Registrant’s telephone number, including area code: (314) 480-1400

Securities registered pursuant to Section 12(b) of the Act:

| | |

Title of each class | Name of each exchange on which registered |

Common Stock, par value $1 per share | New York Stock Exchange Chicago Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. Large Accelerated Filer x Accelerated Filer ¨ Non-accelerated Filer ¨ Smaller Reporting Company ¨

Indicate by check mark whether the registrant is a shell company as defined in Rule 12b-2 of the Exchange Act. Yes ¨ No x

As of June 30, 2007, the aggregate market value of registrant’s common stock, par value $1 per share, held by non-affiliates of registrant was approximately $1,548,896,370 based on the closing sale price as reported on the New York Stock Exchange.

As of January 31, 2008, 74,571,996 shares of the registrant’s common stock were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the following document are incorporated by reference in this Form 10-K

as indicated herein:

| | | |

| Document | | Part of 10-K into which incorporated |

Proxy Statement relating to Olin’s 2008 Annual Meeting of Shareholders to be held on April 24, 2008 | | Part II, Part III |

PART I

Item 1. BUSINESS

GENERAL

Olin Corporation is a Virginia corporation, incorporated in 1892, having its principal executive offices in Clayton, MO. We are a manufacturer concentrated in two business segments: Chlor Alkali Products and Winchester®. Chlor Alkali Products manufactures and sells chlorine and caustic soda, sodium hydrosulfite, hydrochloric acid, hydrogen, sodium chlorate, bleach products and potassium hydroxide, which represent 66% of 2007 sales. Winchester products, which represent 34% of 2007 sales, include sporting ammunition, reloading components, small caliber military ammunition and components, and industrial cartridges. See our discussion of our segment disclosures contained in Item 7—“Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

On October 15, 2007, we announced we entered into a definitive agreement to sell the Metals business to a subsidiary of Global Brass and Copper Holdings, Inc. (Global), an affiliate of KPS Capital Partners, LP, a New York-based private equity firm. The transaction closed on November 19, 2007. Accordingly, for all periods presented prior to the sale, Metals’ assets and liabilities are classified as "held for sale" and presented separately in the Consolidated Balance Sheets, and the related operating results and cash flows are reported as discontinued operations in the Consolidated Statements of Operations and Consolidated Statements of Cash Flows, respectively.

On August 31, 2007 we acquired Pioneer Companies, Inc. (Pioneer), whose earnings were included in the accompanying financial statements since the date of acquisition.

GOVERNANCE

We maintain an Internet website at www.olin.com. Our reports on Form 10-K, Form 10-Q, and Form 8-K, as well as amendments to those reports, are available free of charge on our website, as soon as reasonably practicable after we file the reports with the Securities and Exchange Commission (SEC). Additionally, a copy of our SEC filings can be obtained at the SEC’s Public Reference Room at 100 F Street, N.E., Washington, D.C. 20549 or by calling the SEC at 1-800-SEC-0330. Also, a copy of our electronically filed materials can be obtained at www.sec.gov. Our Principles of Corporate Governance, Committee Charters and Code of Conduct are available on our website at www.olin.com in the Governance Section under Governance Documents and Committees or from the Company by writing to: George Pain, Vice President, General Counsel and Secretary, Olin Corporation, 190 Carondelet Plaza, Suite 1530, Clayton, MO 63105.

In May 2007, our Chief Executive Officer executed the annual Section 303A.12(a) CEO Certification required by the New York Stock Exchange (NYSE), certifying that he was not aware of any violation of the NYSE’s corporate governance listing standards by Olin. Additionally, our Chief Executive Officer and Chief Financial Officer executed the required Sarbanes-Oxley Act of 2002 (SOX) Sections 302 and 906 certifications relating to this Annual Report on Form 10-K, which are filed with the SEC as exhibits to this Annual Report on Form 10-K.

PRODUCTS, SERVICES AND STRATEGIES

Chlor Alkali Products

Products and Services

We have been involved in the U.S. chlor alkali industry for more than 100 years and are a major participant in the North American chlor alkali market. Chlorine and caustic soda are co-produced commercially by the electrolysis of salt. These co-products are produced simultaneously, and in a fixed ratio of 1.0 ton of chlorine to 1.1 tons of caustic soda. The industry refers to this as an Electrochemical Unit or ECU. With a demonstrated capacity as of the end of 2007 of 1.94 million ECUs per year, including the additional capacity from the acquisition of Pioneer in August 2007 and 50% of the production from our partnership with PolyOne Corporation (PolyOne), which we refer to as SunBelt, we are the third largest chlor alkali producer, measured by production volume of chlorine and caustic soda, in North America, according to data from Chemical Market Associates, Inc. (CMAI). CMAI is a global petrochemical, plastics and fibers consulting firm established in 1979. Approximately 55% of our caustic soda production is high purity

membrane and rayon grade, which, according to CMAI data, normally commands a premium selling price in the market. According to data from CMAI, we are the largest North American producer of industrial bleach, which is manufactured using both chlorine and caustic soda.

Our manufacturing facilities in Augusta, McIntosh, Charleston, St. Gabriel, Henderson, Becancour, Dalhousie, and a portion of our facility in Niagara Falls are ISO 9002 certified. In addition, Augusta, McIntosh, Charleston, and Niagara Falls are ISO 14001 certified. ISO 9000 (which includes ISO 9001 and ISO 9002) and ISO 14000 (which includes ISO 14001) are sets of related international standards on quality assurance and environmental management developed by the International Organization for Standardization to help companies effectively document the quality and environmental management system elements to be implemented to maintain effective quality and environmental management systems. Augusta, McIntosh, Charleston, Niagara Falls, and St. Gabriel have also achieved Star status in the Voluntary Protection Program (VPP) of the Occupational Safety and Health Administration (OSHA). OSHA’s VPP is a program in which companies voluntarily participate that recognizes facilities for their exemplary safety and health programs. In 2005, Chlor Alkali Products obtained accreditation under the RC 14001 Responsible Care® (RC 14001) standard. Our Augusta, McIntosh, Charleston, and Niagara Falls chlor alkali manufacturing sites and the division headquarters are certified to this comprehensive integrated management system. Supported by the chemical industry and recognized by government and regulatory agencies, RC14001 establishes requirements for the management of safety, health, environmental, security, transportation, product stewardship, and stakeholder engagement activities for the business.

Chlorine is used as a raw material in the production of thousands of products for end-uses including vinyls, chlorinated intermediates, isocyanates, and water treatment. A significant portion of U.S. chlorine production is consumed in the manufacture of ethylene dichloride, or EDC, a precursor for polyvinyl chloride, or PVC. PVC is a plastic used in applications such as vinyl siding, plumbing and automotive parts. We estimate that approximately 9% of our chlorine produced, including the production from the acquisition of Pioneer, is consumed in the manufacture of EDC. While much of the chlorine produced in the U.S. is consumed by the producing company to make downstream products, we sell most of the chlorine we produce to third parties in the merchant market.

Caustic soda has a wide variety of end-use applications, the largest of which is in the pulp and paper industry as a bleaching agent. Caustic soda is also used in the production of detergents and soaps, alumina and a variety of other inorganic and organic chemicals.

The chlor alkali industry is cyclical, both as a result of changes in demand for each of the co-products and as a result of the large increments in which new capacity is added. Because chlorine and caustic are produced in a fixed ratio, the supply of one product can be constrained both by the physical capacity of the production facilities and/or by the ability to sell the co-product. Prices for both products respond rapidly to changes in supply and demand. Our ECU netbacks (defined as gross selling price less freight and discounts) averaged approximately $505 per ECU in the first half of 2007 and then increased in the third quarter, with fourth quarter combined 2007 netbacks averaging approximately $555 per ECU.

Electricity and salt are the major purchased raw materials for our Chlor Alkali Products segment. Raw materials represent approximately 50% of the total cost of producing an ECU. Electricity is the single largest raw material component in the production of chlor alkali products. During the past four years, we experienced an increase in the cost of electricity from our suppliers due primarily to energy cost increases and regulatory requirements. We are supplied by utilities that primarily utilize coal, hydroelectric, natural gas, and nuclear power. The commodity nature of this industry places an added emphasis on cost management and we believe that we have managed our manufacturing costs in a manner that makes us one of the low cost producers in the industry. We are currently investing in a conversion and expansion project at our St. Gabriel location. This project will increase capacity at that location from 197,000 ECU’s to 246,000 ECU’s and is expected to significantly reduce the site’s manufacturing costs. In addition, as market demand requires, we believe the design of the SunBelt plant, as well as the eventual design of the St. Gabriel plant, will enable us to expand capacity cost-effectively at these locations.

We also manufacture and sell other chlor alkali-related products and we recently invested in capacity and product upgrades in some of these areas. These products include chemically processed salt, hydrochloric acid, sodium hypochlorite, hydrogen, sodium hydrosulfite, sodium chlorate, and potassium hydroxide.

The following table lists products of our Chlor Alkali Products business, with principal products on the basis of annual sales highlighted in bold face.

| Products & Services | | Major End Uses | | Plants & Facilities | | Major Raw Materials & Components for Products/Services |

| Chlorine/caustic soda | | Pulp & paper processing, chemical manufacturing, water purification, manufacture of vinyl chloride, bleach, swimming pool chemicals & urethane chemicals | | Augusta, GA Becancour, Quebec Charleston, TN Dalhousie, New Brunswick Henderson, NV McIntosh, AL Niagara Falls, NY St. Gabriel, LA | | salt, electricity |

| | | | | | | |

Sodium hypochlorite (bleach) | | Household cleaners, laundry bleaching, swimming pool sanitizers, semiconductors, water treatment, textiles, pulp & paper and food processing | | Augusta, GA Becancour, Quebec Charleston, TN Dalhousie, New Brunswick Henderson, NV McIntosh, AL Niagara Falls, NY Santa Fe Springs, CA Tacoma, WA Tracy, CA | | chlorine, caustic soda |

| | | | | | | |

| Hydrochloric acid | | Steel, oil & gas, plastics, organic chemical synthesis, water and wastewater treatment, brine treatment, artificial sweeteners, pharmaceuticals, food processing and ore and mineral processing | | Augusta, GA Becancour, Quebec Charleston, TN Henderson, NV McIntosh, AL Niagara Falls, NY | | chlorine, hydrogen |

| | | | | | | |

| Potassium hydroxide | | Fertilizer manufacturing, soaps, detergents and cleaners, battery manufacturing, food processing chemicals and deicers | | Charleston, TN | | potassium chloride, electricity |

| | | | | | | |

| Hydrogen | | Fuel source, hydrogen peroxide and hydrochloric acid | | Augusta, GA Becancour, Quebec Charleston, TN McIntosh, AL Niagra Falls, NY St. Gabriel, LA | | salt, electricity |

| | | | | | | |

| Sodium chlorate | | Pulp and paper manufacturing | | Dalhousie, New Brunswick | | sodium chloride, electricity |

| | | | | | | |

| Sodium hydrosulfite | | Paper, textile & clay bleaching | | Charleston, TN | | caustic soda, sulfur dioxide |

Strategies

Continued Role as a Preferred Supplier to Merchant Market Customers. Based on our market research, we believe our Chlor Alkali Products business is viewed as a preferred supplier by our merchant market customers. We will continue to focus on providing quality customer service support and developing relationships with our valued customers.

Pursue Incremental Expansion Opportunities. We have invested in capacity and product upgrades in our chemically processed salt, hydrochloric acid, sodium hypochlorite, potassium hydroxide and hydrogen businesses. These expansions increase our captive use of chlorine while increasing the sales of these co-products. These niche businesses provide opportunities to upgrade chlorine and caustic to higher value-added applications. We also have the opportunity, when business conditions permit, to pursue incremental expansion through SunBelt and at St. Gabriel after completion of the current conversion and expansion project.

Winchester

Products and Services

Winchester is in its 141st year of operation and its 77th year as part of Olin. Winchester is a premier developer and manufacturer of small caliber ammunition for sale to domestic and international retailers, law enforcement agencies and domestic and international militaries. We believe we are a leading U.S. producer of ammunition for recreational shooters, hunters, law enforcement agencies and the U.S. Armed Forces. Our legendary Winchester product line includes all major gauges and calibers of shotgun shells, rimfire and centerfire ammunition for pistols and rifles, reloading components and industrial cartridges. We believe we are the leading U.S. supplier of small caliber commercial ammunition. As part of our continuous improvement initiatives, our manufacturing facility located in East Alton, IL achieved ISO 9001:2000 certification in 2006.

Winchester has strong relationships throughout the sales and distribution chain and strong ties to traditional dealers and distributors. Winchester has built its business with key high volume mass merchants and specialty sporting goods retailers. We have consistently developed industry-leading ammunition. Winchester has received the Shooting Industry Academy of Excellence “Ammunition of the Year” award for six consecutive years. In 2007, Winchester’s Supreme Elite™ XP3™ centerfire rifle product line was honored with the National Rifle Association’s “Golden Bullseye Award” in the ammunition category. In addition, two Winchester loads were selected by Outdoor Life magazine to receive the “2007 Editor’s Choice” award for new ammunition products: Winchester’s WinLite Low Recoil Target Loads received the designation in the Target/Wingshooting Shotshell category, while Winchester Supreme .460 S&W Partition Gold was honored in the Handgun ammunition category. Winchester’s 20-Gauge WinLite Low Recoil Target Load was additionally highlighted in Field & Stream magazine’s “2007 Gear of the Year” feature.

Winchester purchases raw materials such as copper-based strip and ammunition cartridge case cups and lead from vendors based on a conversion charge or premium. These conversion charges or premiums are in addition to the market prices for metal as posted on exchanges such as the Commodity Exchange, or COMEX, and London Metals Exchange, or LME. Winchester’s other main raw material is propellant, which is purchased predominantly from one of the United States’ largest propellant suppliers.

The following table lists products and services of our Winchester business, with principal products on the basis of annual sales highlighted in bold face.

| Products & Services | | Major End Uses | | Plants & Facilities | | Major Raw Materials & Components for Products/Services |

| Winchester® sporting ammunition (shot-shells, small caliber centerfire & rimfire ammunition) | | Hunters & recreational shooters, law enforcement agencies | | East Alton, IL Oxford, MS Geelong, Australia | | brass, lead, steel, plastic, propellant, explosives |

| | | | | | | |

| Small caliber military ammunition | | Infantry and mounted weapons | | East Alton, IL | | brass, lead, propellant, explosives |

| | | | | | | |

| Industrial products (8 gauge loads & powder-actuated tool loads) | | Maintenance applications in power & concrete industries, powder-actuated tools in construction industry | | East Alton, IL Oxford, MS Geelong, Australia | | brass, lead, plastic, propellant, explosives |

Strategies

Leverage Existing Strengths. Winchester plans to seek new opportunities to leverage the legendary Winchester brand name and will continue to offer a full line of ammunition products to the markets we serve, with specific focus on investments that lower our costs and that make Winchester ammunition the retail brand of choice.

Focus on Product Line Growth. With a long record of pioneering new product offerings, Winchester has built a strong reputation as an industry innovator. This includes the introduction of reduced-lead and non-lead products, which are growing in popularity for use in indoor shooting ranges and for outdoor hunting.

INTERNATIONAL OPERATIONS

Our subsidiary, PCI Chemicals Canada Company/Société PCI Chimie Canada, operates two chlor alkali facilities, Becancour and Dalhousie, in Canada, which sells chlor alkali-related products within Canada and to the United States. Our subsidiary, Winchester Australia Limited, loads and packs sporting and industrial ammunition in Australia. See the Note “Segment Information” of the Notes to Consolidated Financial Statements in Item 8, for geographic segment data. We are incorporating our segment information from that Note into this section of our Form 10-K.

CUSTOMERS AND DISTRIBUTION

During 2007, no single customer accounted for more than 9% of consolidated sales. Sales to all U.S. government agencies and sales under U.S. government contracting activities in total accounted for approximately 6% of consolidated sales in 2007. Products we sell to industrial or commercial users or distributors for use in the production of other products constitute a major part of our total sales. We sell some of our products, such as caustic soda and sporting ammunition, to a large number of users or distributors, while we sell others, such as chlorine, in substantial quantities to a relatively small number of industrial users. We discuss the customers for each of our two businesses in more detail above under “Products and Services.”

We market most of our products and services primarily through our sales force and sell directly to various industrial customers, wholesalers, other distributors, and the U.S. Government and its prime contractors.

Because we engage in some government contracting activities and make sales to the U.S. Government, we are subject to extensive and complex U.S. Government procurement laws and regulations. These laws and regulations provide for ongoing government audits and reviews of contract procurement, performance and administration. Failure to comply, even inadvertently, with these laws and regulations and with laws governing the export of munitions and other controlled products and commodities could subject us or one or more of our businesses to civil and criminal penalties, and under certain circumstances, suspension and debarment from future government contracts and the exporting of products for a specified period of time.

COMPETITION

We are in active competition with businesses producing the same or similar products, as well as, in some instances, with businesses producing different products designed for the same uses.

Chlor alkali manufacturers in North America, with approximately 15.0 million tons of chlorine and 15.9 million tons of caustic soda capacity, account for approximately 21% of worldwide chlor alkali production capacity. According to CMAI, the Dow Chemical Company (Dow), and the Occidental Chemical Corporation (OxyChem), are the two largest chlor alkali producers in North America. Approximately 70% of the total North American capacity is located in the U.S. Gulf Coast region.

Many of our competitors are integrated producers of chlorine, using some of, or all, of their chlorine production in the manufacture of other downstream products. In contrast, we are primarily a merchant producer of chlorine and sell the majority of our chlorine to merchant customers. We do utilize chlorine to manufacture industrial bleach and hydrochloric acid. As a result, we supply a greater share of the merchant chlorine market than our share of overall industry capacity. There is a worldwide market for caustic soda, which attracts imports and allows exports depending on market conditions. All of our competitors sell caustic soda into the North American market.

The chlor alkali industry in North America is highly competitive, and many of our competitors, including Dow and OxyChem, are substantially larger and have greater financial resources than we do. While the technologies to manufacture and transport chlorine and caustic soda are widely available, the production facilities require large capital investments, and are subject to significant regulatory and permitting requirements.

We are among the largest manufacturers in the United States of commercial small caliber ammunition based on data provided by the Sporting Arms and Ammunition Manufacturers’ Institute (SAAMI). Founded in 1926, SAAMI is an association of the nation’s leading manufacturers of sporting firearms, ammunition and components. According to

SAAMI, in addition to our Winchester business, Alliant Techsystems Inc. (ATK) and Remington Arms Company, Inc. (Remington) are the three largest commercial ammunition manufacturers in the United States. The ammunition industry is highly competitive with us, ATK, Remington, numerous smaller domestic manufacturers and foreign producers competing for sales to the commercial ammunition customers. Many factors influence our ability to compete successfully, including price, delivery, service, performance, product innovation and product recognition and quality, depending on the product involved.

EMPLOYEES

As of December 31, 2007, we had approximately 3,600 employees, with 3,300 working in the United States and 300 working in foreign countries, primarily Canada. Various labor unions represent a majority of our hourly-paid employees for collective bargaining purposes.

The following labor contracts are scheduled to expire in 2008:

| Location | | Number of Employees | | Expiration Date |

| McIntosh (Chlor Alkali) | | 200 | | April |

| East Alton (Winchester) | | 1,420 | | December |

| Tacoma (Chlor Alkali) | | 15 | | December |

While we believe our relations with our employees and their various representatives are generally satisfactory, we cannot assure that we can conclude these labor contracts or any other labor agreements without work stoppages and cannot assure that any work stoppages will not have a material adverse effect on our business, financial condition, or results of operations.

RESEARCH ACTIVITIES; PATENTS

Our research activities are conducted on a product-group basis at a number of facilities. Company-sponsored research expenditures were $2.0 million in 2007, $1.8 million in 2006, and $1.7 million in 2005.

We own or license a number of patents, patent applications, and trade secrets covering our products and processes. We believe that, in the aggregate, the rights under our patents and licenses are important to our operations, but we do not consider any individual patent or license or group of patents and licenses related to a specific process or product to be of material importance to our total business.

RAW MATERIALS AND ENERGY

We purchase the major portion of our raw material requirements. The principal basic raw materials for our production of chlor alkali products are salt, electricity, sulfur dioxide, and hydrogen. A portion of the salt used in our Chlor Alkali Products segment is produced from internal resources. Lead, brass, and propellant are the principal raw materials used in the Winchester business. We typically purchase our electricity, salt, sulfur dioxide, ammunition cartridge case cups and copper-based strip, and propellants pursuant to multi-year contracts. We provide additional information with respect to specific raw materials in the tables above under “Products and Services.”

Electricity is the predominant energy source for our manufacturing facilities. Most of our facilities are served by utilities which generate electricity principally from coal, hydroelectric and nuclear power except at St. Gabriel and Henderson which use natural gas.

ENVIRONMENTAL AND TOXIC SUBSTANCES CONTROLS

In the United States, the establishment and implementation of federal, state and local standards to regulate air, water and land quality affect substantially all of our manufacturing locations. Federal legislation providing for regulation of the manufacture, transportation, use and disposal of hazardous and toxic substances, and remediation of contaminated sites has imposed additional regulatory requirements on industry, particularly the chemicals industry. In addition, implementation of environmental laws, such as the Resource Conservation and Recovery Act and the Clean Air Act, has required and will continue to require new capital expenditures and will increase operating costs. Our Canadian facilities are governed by federal environmental laws administered by Environment Canada and by

provincial environmental laws enforced by administrative agencies. Many of these laws are comparable to the U.S. laws described above. We employ waste minimization and pollution prevention programs at our manufacturing sites and we are a party to various governmental and private environmental actions associated with waste disposal sites and manufacturing facilities. Charges or credits to income for investigatory and remedial efforts were material to operating results in the past three years and may be material to net income in future years.

See our discussion of our environmental matters in Item 3, “Legal Proceedings” below, the Note “Environmental” of the Notes to Consolidated Financial Statements contained in Item 8, and Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

Item 1A. RISK FACTORS

In addition to the other information in this Form 10-K, the following factors should be considered in evaluating Olin and our business. All of our forward-looking statements should be considered in light of these factors. Additional risks and uncertainties that we are unaware of or that we currently deem immaterial also may become important factors that affect us.

Sensitivity to Global Economic Conditions and Cyclicality—Our operating results could be negatively affected during economic downturns.

The business of most of our customers, particularly our vinyl, urethanes, and pulp and paper customers are, to varying degrees, cyclical and have historically experienced periodic downturns. These economic and industry downturns have been characterized by diminished product demand, excess manufacturing capacity and, in some cases, lower average selling prices. Therefore, any significant downturn in our customers’ businesses or in global economic conditions could result in a reduction in demand for our products and could adversely affect our results of operations or financial condition.

Although we do not generally sell a large percentage of our products directly to customers abroad, a large part of our financial performance is dependent upon a healthy economy beyond the United States. Our customers sell their products abroad. As a result, our business is affected by general economic conditions and other factors in Western Europe and most of East Asia, particularly China and Japan, including fluctuations in interest rates, customer demand, labor costs, currency changes, and other factors beyond our control. The demand for our customers’ products, and therefore, our products, is directly affected by such fluctuations. In addition, our customers could decide to move some or all of their production to lower cost, offshore locations, and this could reduce demand in the United States for our products. We cannot assure you that events having an adverse effect on the industries in which we operate will not occur or continue, such as a downturn in the Western European, Asian or world economies, increases in interest rates, or unfavorable currency fluctuations.

Cyclical Pricing Pressure—Our profitability could be reduced by declines in average selling prices of our products, particularly declines in the ECU netback for chlorine and caustic.

Our historical operating results reflect the cyclical and sometimes volatile nature of the chemical and ammunition industries. We experience cycles of fluctuating supply and demand in each of our business segments, particularly in Chlor Alkali Products, which results in changes in selling prices. Periods of high demand, tight supply and increasing operating margins tend to result in increases in capacity and production until supply exceeds demand, generally followed by periods of oversupply and declining prices. No new significant chlor alkali capacity became available during 2005, 2006, or 2007, and currently, the capacity increases expected in 2008 and 2009 are at our St. Gabriel facility and the Shintech facility in Plaquemine, LA. In October 2006, Dow closed its Fort Saskatchewan Chlor Alkali facility in Western Canada. Closure of this plant had limited impact on Olin. Another factor influencing demand and pricing for chlorine and caustic soda is the price of natural gas. Higher natural gas prices increase our customers’ and competitors’ manufacturing costs, and depending on the ratio of crude oil to gas prices, could make them less than competitive in world markets; and therefore, may result in reduced demand for our products. Continued expansion offshore, particularly in Asia, will continue to have an impact on the ECU values as imported caustic soda replaces some capacity in the U.S.

Price in the chlor alkali industry is a major supplier selection criterion. We have little or no ability to influence prices in this large commodity market. Decreases in the average selling prices of our products could have a material adverse effect on our profitability. For example, assuming all other costs remain constant and internal consumption remains approximately the same, a $10 per ECU selling price change equates to an approximate $17.0 million annual change in our revenues and pretax profit when we are operating at full capacity, including the capacity acquired with Pioneer. While we strive to maintain or increase our profitability by reducing costs through improving production efficiency, emphasizing higher margin products, and by controlling transportation, selling, and administration expenses, we cannot assure you that these efforts will be sufficient to offset fully the effect of changes in pricing on operating results.

Because of the cyclical nature of our businesses, we cannot assure you that pricing or profitability in the future will be comparable to any particular historical period, including the most recent period shown in our operating results. We cannot assure you that the chlor alkali industry will not experience adverse trends in the future, or that our operating results and/or financial condition will not be adversely affected by them.

Our Winchester segment is also subject to changes in operating results as a result of cyclical pricing pressures, but to a lesser extent than the Chlor Alkali Products segment. Selling prices of ammunition are affected by changes in raw material costs and availability and customer demand, and declines in average selling prices of our Winchester segment could adversely affect our profitability.

Imbalance in Demand for Our Chlor Alkali Products—A loss of a substantial customer for our chlorine or caustic soda could cause an imbalance in demand for these products, which could have an adverse effect on our results of operations.

Chlorine and caustic soda are produced simultaneously and in a fixed ratio of 1.0 ton of chlorine to 1.1 tons of caustic soda. The loss of a substantial chlorine or caustic soda customer could cause an imbalance in demand for our chlorine and caustic soda products. An imbalance in demand may require us to reduce production of both chlorine and caustic soda or take other steps to correct the imbalance. Since we cannot store chlorine, we may not be able to respond to an imbalance in demand for these products as quickly or efficiently as some of our competitors. If a substantial imbalance occurred, we would need to reduce prices or take other actions that could have a negative impact on our results of operations and financial condition.

Environmental Costs—We have ongoing environmental costs, which could have a material adverse effect on our financial position or results of operations.

The nature of our operations and products, including the raw materials we handle, exposes us to the risk of liabilities or claims with respect to environmental matters. We have incurred, and expect to incur, significant costs and capital expenditures in complying with environmental laws and regulations.

The ultimate costs and timing of environmental liabilities are difficult to predict. Liabilities under environmental laws relating to contaminated sites can be imposed retroactively and on a joint and several basis. One liable party could be held responsible for all costs at a site, regardless of fault, percentage of contribution to the site or the legality of the original disposal. We could incur significant costs, including cleanup costs, natural resources damages, civil or criminal fines and sanctions and third-party lawsuits claiming, for example, personal injury and/or property damage, as a result of past or future violations of, or liabilities under, environmental or other laws.

In addition, future events, such as changes to or more rigorous enforcement of environmental laws, could require us to make additional expenditures, modify or curtail our operations and/or install pollution control equipment.

Accordingly, it is possible that some of the matters in which we are involved or may become involved may be resolved unfavorably to us, which could materially adversely affect our financial position or results of operations. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations-Environmental Matters.”

Litigation and Claims—We are subject to litigation and other claims, which could cause us to incur significant expenses.

We are a defendant in a number of pending legal proceedings relating to our present and former operations. These include proceedings alleging injurious exposure of plaintiffs to various chemicals and other substances (including proceedings based on alleged exposures to asbestos). Frequently, such proceedings involve claims made by numerous plaintiffs against many defendants. However, because of the inherent uncertainties of litigation, we are unable to predict the outcome of these proceedings and therefore cannot determine whether the financial impact, if any, will be material to our financial position or results of operations.

Pension Plans—The impact of declines in global equity markets on asset values and any declines in interest rates used to value the liabilities in our pension plan may result in higher pension costs and the need to fund the pension plan in future years in material amounts.

In May 2007 and September 2006, we made voluntary pension plan contributions of $100.0 million and $80.0 million, respectively. In September 2005, we made a voluntary pension plan contribution of $6.1 million in order to maintain a 90% funded level under the Employee Retirement Income and Security Act (ERISA) criteria used to determine funding levels.

Under Statement of Financial Accounting Standards (SFAS) No. 158, “Employers’ Accounting for Defined Benefit Pension and Other Postretirement Plans,” (SFAS No. 158), we recorded a $138.3 million after-tax credit ($226.6 million pretax) to Shareholders’ Equity as of December 31, 2007 for our pension and other postretirement plans. This credit reflected a 25-basis point increase in the plans’ discount rate, combined with an increase in the value of the plan assets from favorable plan performance and the $100.0 million contribution. In 2006, we recorded an after-tax credit of $54.5 million ($89.2 million pretax) to Shareholders’ Equity as a result of a decrease in the accumulated pension benefit obligation, which resulted primarily from a 25-basis point increase in the plan discount rate, combined with an increase in the value of the plan assets from favorable plan performance and the $80.0 million contribution. In 2006, we adopted SFAS No. 158, which required us to record a net liability or asset to report the funded status of our defined benefit pension and other postretirement plans on our balance sheet. As a result, we recorded after-tax charges to Shareholders’ Equity of $39.7 million and $33.6 million for the pension and other postretirement plans, respectively ($65.0 million and $55.0 million pretax, respectively). In 2005, a 25-basis point decline in interest rates and the cost impact of contractual pension plan changes more than offset the increase in the value of the plan assets. Therefore, we recorded in December 2005 an additional after-tax charge of $29.2 million ($47.8 million pretax) as a result of an increase in the accumulated pension benefit obligation. The non-cash credits or charges to Shareholders’ Equity do not affect our ability to borrow under our revolving credit agreement.

During 2007, the asset allocation in the plan was adjusted to insulate the plan from discount rate risk and reduce the plan’s exposure to equity investments. On October 5, 2007, we announced that we would freeze our defined benefit pension plan for salaried and certain non-bargained hourly workers effective January 1, 2008. Effective January 1, 2008, these employees will participate in a defined contribution pension plan. In 2008, we expect pension expense associated with the defined benefit plan to be approximately $19 million lower compared to 2007. This reduction reflects an additional 25-basis point increase in the discount rate, the benefits of the $100.0 million voluntary contribution made in May 2007, favorable asset performance in 2007, and the benefits of the plan freeze. This reduction will be partially offset by an approximate $6 million increase in expenses associated with the defined contribution plan that replaced the defined benefit plan.

The determinations of pension expense and pension funding are based on a variety of rules and regulations. Changes in these rules and regulations could impact the calculation of pension plan liabilities and the valuation of pension plan assets. They may also result in higher pension costs, additional financial statement disclosure, and accelerate and increase the need to fully fund the pension plan. During the third quarter of 2006, the “Pension Protection Act of 2006” became law. Among the stated objectives of the law were the protection of both pension beneficiaries and the financial health of the Pension Benefit Guaranty Corporation (PBGC). To accomplish these objectives, the new law required sponsors to fund defined benefit pension plans earlier than previous requirements and to pay increased PBGC premiums. Based on the combination of the asset allocation adjustment, the favorable asset performance in 2006 and 2007, the $100.0 and $80.0 voluntary contributions, and the benefits from the plan freeze, it is likely that the defined benefit pension plan will meet the full funding requirements of the Pension Protection Act of 2006 without any additional contributions. At December 31, 2007, the market value of assets in our defined pension plan exceeded the accumulated benefit obligation of our defined pension plan by $139.7 million.

In addition, the impact of declines in global equity and bond markets on asset values may result in higher pension costs and may increase and accelerate the need to fund the pension in future years. For example, holding all other assumptions constant, a 100-basis point decrease or increase in the assumed rate of return on plan assets would have increased or decreased, respectively, the 2007 qualified pension plan cost by approximately $14.0 million.

Holding all other assumptions constant, a 50-basis point decrease in the discount rate used to calculate pension costs for 2007 and the projected benefit obligation as of December 31, 2007 would have increased pension costs by $5.7 million and the projected benefit obligation by $88.0 million. A 50-basis point increase in the discount rate used to calculate pension costs for 2007 and the projected benefit obligation as of December 31, 2007 would have decreased pension costs by $6.5 million and the projected benefit obligation by $88.0 million.

Production Hazards—Our facilities are subject to operating hazards, which may disrupt our business.

We are dependent upon the continued safe operation of our production facilities. Our production facilities are subject to hazards associated with the manufacture, handling, storage and transportation of chemical materials and products and ammunition, including leaks and ruptures, explosions, fires, inclement weather and natural disasters, unexpected utility disruptions or outages, unscheduled downtime and environmental hazards. From time to time in the past, we have had incidents that have temporarily shut down or otherwise disrupted our manufacturing, causing production delays and resulting in liability for workplace injuries and fatalities. Some of our products involve the manufacture and/or handling of a variety of explosive and flammable materials. Use of these products by our customers could also result in liability if an explosion, fire, spill or other accident were to occur. We cannot assure you that we will not experience these types of incidents in the future or that these incidents will not result in production delays or otherwise have a material adverse effect on our business, financial condition or results of operations.

Security and Chemicals Transportation—New regulations on the transportation of hazardous chemicals and/or the security of chemical manufacturing facilities and public policy changes related to transportation safety could result in significantly higher operating costs.

The chemical industry, including the chlor alkali industry, has proactively responded to the issues related to national security and environmental concerns by starting new initiatives relating to the security of chemicals industry facilities and the transportation of hazardous chemicals in the United States. Government at the local, state, and federal levels also has begun regulatory processes which could lead to new regulations that would impact the security of chemical plant locations and the transportation of hazardous chemicals. Our Chlor Alkali business could be adversely impacted by the cost of complying with any new regulations. Our business also could be adversely affected because of an incident at one of our facilities or while transporting product. The extent of the impact would depend on the requirements of future regulations and the nature of an incident, which are unknown at this time.

Cost Control—Our profitability could be reduced if we continue to experience increasing raw material, utility, transportation or logistics costs, or if we fail to achieve our targeted cost reductions, including the synergies expected to be realized by the Pioneer acquisition.

Our operating results and profitability are dependent upon our continued ability to control, and in some cases further reduce, our costs. If we are unable to do so, or if costs outside of our control, particularly our costs of raw materials, utilities, transportation and similar costs, increase beyond anticipated levels, our profitability will decline.

Labor Matters—We cannot assure you that we can conclude future labor contracts or any other labor agreements without work stoppages.

Various labor unions represent a majority of our hourly-paid employees for collective bargaining purposes. The following labor contracts are scheduled to expire in 2008:

| Location | | Number of Employees | | Expiration Date |

| McIntosh (Chlor Alkali) | | 200 | | April |

| East Alton (Winchester) | | 1,420 | | December |

| Tacoma (Chlor Alkali) | | 15 | | December |

While we believe our relations with our employees and their various representatives are generally satisfactory, we cannot assure that we can conclude future labor contracts or any other labor agreements without work stoppages and cannot assure that any work stoppages will not have a material adverse effect on our business, financial condition, or results of operations.

Indebtedness—Our indebtedness could adversely affect our financial condition and limit our ability to grow and compete, which could prevent us from fulfilling our obligations under our indebtedness.

As of December 31, 2007, we had $259.0 million of indebtedness outstanding, including $6.6 million representing the fair value related to $101.6 million of interest rate swaps in effect at December 31, 2007 and excluding our guarantee of $60.9 million of indebtedness of SunBelt. This does not include our $220.0 million senior credit facility of which we had $177.3 million available on that date because we had issued $42.7 million of letters of credit. As of December 31, 2007, our indebtedness represented 28.1% of our total capitalization. At December 31, 2007, we had $9.8 million of our indebtedness due within one year.

Our indebtedness could adversely affect our financial condition and limit our ability to grow and compete, which in turn could prevent us from fulfilling our obligations under our indebtedness. Despite our level of indebtedness, the terms of our senior credit facility and our existing indentures permit us to borrow additional money. If we borrow more money, the risks related to our indebtedness could increase significantly.

Debt Service—We may not be able to generate sufficient cash to service our debt, which may require us to refinance our indebtedness or default on our scheduled debt payments.

Our ability to generate sufficient cash flow from operations to make scheduled payments on our debt depends on a range of economic, competitive and business factors, many of which are outside our control. We cannot assure you that our business will generate sufficient cash flow from operations. If we are unable to meet our expenses and debt obligations, we may need to refinance all or a portion of our indebtedness on or before maturity, sell assets or raise equity. We cannot assure you that we would be able to refinance any of our indebtedness, sell assets or raise equity on commercially reasonable terms or at all, which could cause us to default on our obligations and impair our liquidity. Our inability to generate sufficient cash flow to satisfy our debt obligations, or to refinance our obligations on commercially reasonable terms, would have an adverse effect on our business, financial condition and results of operations, as well as on our ability to satisfy our debt obligations. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

At December 31, 2007, we had interest rate swaps of $101.6 million, which convert a portion of our fixed rate debt to a variable rate. As a result, 42% of our indebtedness bears interest at variable rates that are linked to short-term interest rates. If interest rates rise, our costs relative to those obligations would also rise. See Item 7A—“Quantitative and Qualitative Disclosures about Market Risk” and “Liquidity and Other Financing Arrangements.”

Item 1B. UNRESOLVED STAFF COMMENTS

Not applicable.

Item 2. PROPERTIES

We have manufacturing sites at 14 separate locations in ten states, Canada and Australia. Most manufacturing sites are owned although a number of small sites are leased. We listed the locations at or from which our products and services are manufactured, distributed, or marketed in the tables set forth under the caption “Products and Services.”

We lease warehouses, terminals and distribution offices and space for executive and branch sales offices and service departments.

Item 3. LEGAL PROCEEDINGS

Saltville

We have completed all work in connection with remediation of mercury contamination at the site of our former mercury cell chlor alkali plant in Saltville, VA required to date. In mid-2003, the Trustees for natural resources in the North Fork Holston River, the Main Stem Holston River, and associated floodplains, located in Smyth and Washington Counties in Virginia and in Sullivan and Hawkins Counties in Tennessee notified us of, and invited our participation in, an assessment of alleged injuries to natural resources resulting from the release of mercury. The Trustees also notified us that they have made a preliminary determination that we are potentially liable for natural resource damages in said rivers and floodplains. We have agreed to participate in the assessment. We and the Trustees have agreed to enter into discussions concerning a resolution of this matter. In light of the early stage, and inherent uncertainties, of the assessment, we cannot at this time determine whether the financial impact, if any, of this matter will be material to our financial position or results of operations. See “Environmental Matters” contained in Item 7—“Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

St. Gabriel Mercury Vapor Emissions Release

Our recently acquired subsidiary, Pioneer, discovered in October 2004 that the carbon-based system used to remove mercury from the hydrogen gas stream at the St. Gabriel facility was not at that time sufficiently effective, resulting in mercury vapor emissions that were above the permit limits approved by the Louisiana Department of Environmental Quality (LDEQ). Pioneer immediately reduced the plant’s operating rate and, in late November 2004, completed the installation of the necessary equipment and made the other needed changes, and the plant resumed its normal operations. Pioneer’s emissions monitoring since that time confirmed that the air emissions are below the permit limits. In January 2005, the LDEQ issued a violation notice to Pioneer as a result of this mercury vapor emissions release. In December 2005, the LDEQ issued a penalty assessment of $0.4 million with respect to the notice of violation. Pioneer has administratively appealed the penalty assessment. Given the facts and circumstances, Pioneer requested that the LDEQ reconsider the penalty assessment.

Other

As part of the continuing environmental investigation by federal, state, and local governments of waste disposal sites, we have entered into a number of settlement agreements requiring us to participate in the investigation and cleanup of a number of sites. Under the terms of such settlements and related agreements, we may be required to manage or perform one or more elements of a site cleanup, or to manage the entire remediation activity for a number of parties, and subsequently seek recovery of some or all of such costs from other Potentially Responsible Parties (PRPs). In many cases, we do not know the ultimate costs of our settlement obligations at the time of entering into particular settlement agreements, and our liability accruals for our obligations under those agreements are often subject to significant management judgment on an ongoing basis. Those cost accruals are provided for in accordance with generally accepted accounting principles and our accounting policies set forth in the environmental matters section in Item 7—“Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

We and our subsidiaries are defendants in various other legal actions (including proceedings based on alleged exposures to asbestos) incidental to our past and current business activities. While we believe that none of these legal actions will materially adversely affect our financial position, in light of the inherent uncertainties of litigation, we cannot at this time determine whether the financial impact, if any, of these matters will be material to our results of operations.

Item 4. SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS

We did not submit any matter to a vote of security holders during the three months ended December 31, 2007.

Executive Officers of the Registrant as of February 27, 2008

| Name and Age | | Office | | Served as an Olin Officer Since |

| | Chairman, President and Chief Executive Officer | | |

| | Vice President and Treasurer | | |

| | Vice President and Chief Financial Officer | | |

| | Vice President, Strategic Planning | | |

| | Vice President and President, Winchester Division | | |

| | Vice President, Human Resources | | |

| | Vice President and President, Chlor Alkali Products Division | | |

| | Vice President, General Counsel and Secretary | | |

| | Vice President and Controller | | |

No family relationship exists between any of the above named executive officers or between any of them and any of our directors. Such officers were elected to serve, subject to the By-laws, until their respective successors are chosen.

J. D. Rupp, J. L. McIntosh, and G. H. Pain have served as executive officers more than five years.

Stephen C. Curley re-joined Olin on August 18, 2003 as Chief Tax Counsel. He was elected Vice President and Treasurer effective January 1, 2005. From 1997-2001, he served as Vice President and Treasurer of Primex Technologies, Inc., a manufacturer and provider of ordnance and aerospace products and services, which was spun off from Olin in 1996.

John E. Fischer re-joined Olin on January 2, 2004 as Vice President, Finance. On June 24, 2004, he was elected Vice President, Finance and Controller, and effective May 27, 2005, he was elected Vice President and Chief Financial Officer. From 1997-2001, he served as Vice President and Chief Financial Officer of Primex Technologies, Inc. During 2002 and 2003, Mr. Fischer did independent consulting for several companies including Olin.

G. Bruce Greer, Jr. joined Olin on May 2, 2005 as Vice President, Strategic Planning. Prior to joining Olin and since 1997, Mr. Greer was employed by Solutia, Inc., an applied chemicals company. From 2003 to April 2005, he served as President of Pharma Services, a Division of Solutia and Chairman of Flexsys, an international rubber chemicals company which was a joint venture partially owned by Solutia and Akzo Nobel. Prior to that, Mr. Greer served as a Vice President of Corporate Development, Technology, and Information Technology for Solutia.

Richard M. Hammett was elected Vice President and President, Winchester Division effective January 1, 2005. Prior to that time and since September 2002, he served as President, Winchester Division. From November 1998 until September 2002, he served as Vice President, Marketing and Sales for the Winchester Division.

Dennis R. McGough was elected Vice President, Human Resources effective January 1, 2005. Prior to that time and since 1999, he served as Corporate Vice President, Human Resources.

Todd A. Slater was elected Vice President and Controller, effective May 27, 2005. From April 2004 until May 2005, he served as Operations Controller. From January 2003 until April 2004, he served as Vice President and Financial Officer for Olin’s Metals Group. Prior to 2003, Mr. Slater served as Vice President, Chief Financial Officer and Secretary for Chase Industries Inc. (which was merged into Olin on September 27, 2002).

PART II

| Item 5. MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

As of January 31, 2008, we had 5,325 record holders of our common stock.

Our common stock is traded on the New York Stock Exchange and the Chicago Stock Exchange.

The high and low sales prices of our common stock during each quarterly period in 2007 and 2006 are listed below. A dividend of $0.20 per common share was paid during each of the four quarters in 2007 and 2006.

| 2007 | | First Quarter | | | Second Quarter | | | Third Quarter | | | Fourth Quarter | |

Market price of common stock per New York Stock Exchange composite transactions | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

Market price of common stock per New York Stock Exchange composite transactions | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

Issuer Purchases of Equity Securities

| Period | | Total Number of Shares (or Units) Purchased | | | Average Price Paid per Share (or Unit) | | | Total Number of Shares (or Units) Purchased as Part of Publicly Announced Plans or Programs | | | Maximum Number of Shares (or Units) that May Yet Be Purchased Under the Plans or Programs | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| (1) | On April 30, 1998, we announced a share repurchase program approved by our board of directors for the purchase of up to 5 million shares of common stock. Through December 31, 2007, 4,845,924 shares had been repurchased, and 154,076 shares remain available for purchase under that program, which has no termination date. |

Equity Compensation Plan Information

| | | (a) | | | (b) | | | (c) | |

| Plan Category | | Number of securities to be issued upon exercise of outstanding options, warrants and rights (1) | | | Weighted-average exercise price of outstanding options, warrants and rights | | | Number of securities remaining available for future issuance under equity compensation plans excluding securities reflected in column (a)(1) | |

Equity compensation plans approved by security holders(2) | | | | | | | | | | | | |

Equity compensation plans not approved by security holders(4) | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | |

| (1) | Number of shares is subject to adjustment for changes in capitalization for stock splits and stock dividends and similar events. |

| (2) | Consists of the 2000 Long Term Incentive Plan, the 2003 Long Term Incentive Plan, the 2006 Long Term Incentive Plan and the 1997 Stock Plan for Non-employee Directors. Does not include information about the equity compensation plans listed in the table below, which have expired. No additional awards may be granted under those expired plans. As of December 31, 2007: |

| Plan Name | | Expiration Date | | Number of Securities Issuable Under Outstanding Options | | | Weighted Average Exercise Price | | Weighted Average Remaining Term |

1988 Stock Option Plan for Key Employees of Olin Corporation and Subsidiaries | | | | | | | | | | | |

Olin 1991 Long Term Incentive Plan | | | | | | | | | | | |

1996 Stock Option Plan for Key Employees of Olin Corporation and Subsidiaries | | | | | | | | | | | |

| | • | 2,690,540 shares issuable upon exercise of options with a weighted average exercise price of $18.59, and a weighted average remaining term of 6.5 years, (which include 474,000 shares subject to performance accelerated vesting options, that vest on the earlier of December 27, 2009, or the tenth day in any 30 calendar day period upon which the average of the high and low per share sales prices of Olin’s common stock as reported on the consolidated transaction system for New York Stock Exchange issues is at or above $28.00), |

| | • | 50,700 shares issuable under restricted stock unit grants, with a weighted average remaining term of 1.33 years, |

| | • | 297,988 shares issuable in connection with outstanding performance share awards, with a weighted average term of 1.21 years remaining in the performance measurement period, and |

| | • | 171,683 shares under the 1997 Stock Plan for Non-employee Directors which represent stock grants for retainers, other board and committee fees, and dividends on deferred stock under the plan. |

| (4) | Does not include information about equity compensation plans assumed in connection with the acquisition of Chase Industries Inc. (Chase) in September 2002 by merger. No additional awards may be granted under those assumed plans. As of December 31, 2007, options for a total of 125,799 shares, with a weighted average exercise price of $22.13 per share, and a weighted average remaining term of 0.9 years, were outstanding under the various plans assumed in connection with that acquisition. |

| | Does not include a total of 210,022 shares issuable upon the exercise of outstanding options under the Arch Chemicals, Inc. (Arch) 1999 Long Term Incentive Plan, with a weighted average exercise price of $27.17, and a weighted average remaining term of 0.1 years. No additional options or other awards may be issued under that plan. |

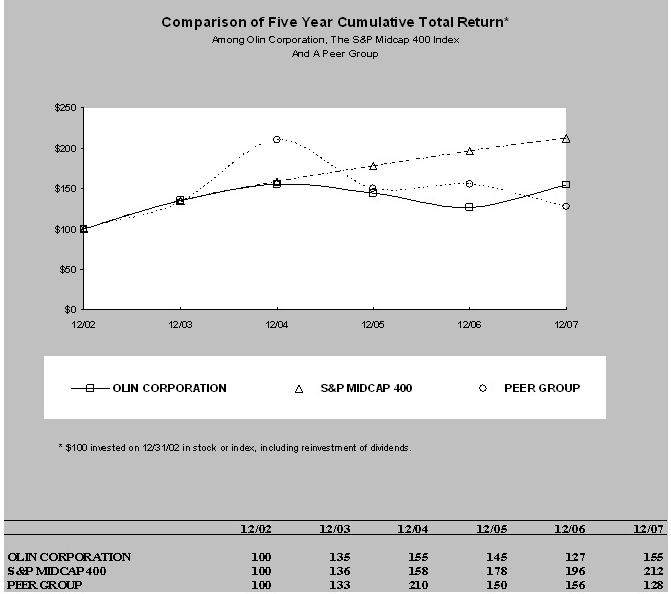

Performance Graph

This graph compares the total shareholder return on our common stock with the total return on the S&P Midcap 400 and our Peer Group, as defined below, for the five-year period from December 31, 2002 through December 31, 2007. The cumulative return includes reinvestment of dividends.

Our Peer Group consists of Georgia Gulf Corporation, Brush Engineered Materials Inc., Mueller Industries, Inc., and Wolverine Tube, Inc. Our Peer Group is weighted in accordance with market capitalization (closing stock price multiplied by the number of shares outstanding) as of the beginning of each of the five years covered by the performance graph. We calculated the weighted return for each year by multiplying (a) the percentage that each corporation’s market capitalization represented of the total market capitalization for all corporations in our Peer Group for such year by (b) the total shareholder return for that corporation for such year.

Item 6. SELECTED FINANCIAL DATA

TEN-YEAR SUMMARY

| ($ and shares in millions, except per share data) | | 2007 | | | 2006 | | | 2005 | | | 2004 | | | 2003 | | | 2002 | | | 2001 | | | 2000 | | | 1999 | | | 1998 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Selling and Administration | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Loss on Sales and Restructuring of Businesses and Spin-off costs | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Earnings (Loss) of Non-consolidated Affiliates | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Interest and Other Income | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Income (Loss) before Taxes from Continuing Operations | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Income Tax Provision (Benefit) | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Income (Loss) from Continuing Operations | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Discontinued Operations, Net | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Cumulative Effect of Accounting Change, Net | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Net (Loss) Income | | $ | (9 | ) | | $ | 150 | | | $ | 133 | | | $ | 55 | | | $ | (24 | ) | | $ | (31 | ) | | $ | (9 | ) | | $ | 81 | | | $ | 21 | | | $ | 78 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Cash and Cash Equivalents and Short-Term Investments | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Working Capital, excluding Cash and Cash Equivalents and Short-Term Investments | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Property, Plant and Equipment, Net | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Discontinued Operations, Net | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Discontinued Operations, Net | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | �� | | | | | | | | | | | |

Common (continuing operations) | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Market Price of Common Stock: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | �� | | | | | | | | | | | | | | |

Purchases of Common Stock | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total Debt to Total Capitalization | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Average Common Shares Outstanding - Diluted | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Our Selected Financial Data reflects the following businesses as discontinued operations: Metals business in 2007, Olin Aegis in 2004 and the spin off of Arch (our specialty chemicals business) in 1999.

(1) Employee data exclude employees who worked at government-owned/contractor-operated facilities.

| Item 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

BUSINESS BACKGROUND

The Metals business has been classified as discontinued operations during 2007 and was excluded from the segment results for all periods presented. As a result, our manufacturing operations are concentrated in two business segments: Chlor Alkali Products and Winchester. Both are capital intensive manufacturing businesses with operating rates closely tied to the general economy. Each segment has a commodity element to it, and therefore, our ability to influence pricing is quite limited on the portion of the segment’s business that is strictly commodity. Our Chlor Alkali Products business is a commodity business where all supplier products are similar and price is the major supplier selection criterion. We have little or no ability to influence prices in this large, global commodity market. Cyclical price swings, driven by changes in supply/demand, can be abrupt and significant and, given capacity in our Chlor Alkali Products business, can lead to very significant changes in our overall profitability. Winchester also has a commodity element to its business, but a majority of Winchester ammunition is sold as a branded consumer product where there are opportunities to differentiate certain offerings through innovative new product development and enhanced product performance. While competitive pricing versus other branded ammunition products is important, it is not the only factor in product selection.

RECENT DEVELOPMENTS AND HIGHLIGHTS

2007 Year

Discontinued Operations

In 2001, the industry in which the Metals business operates experienced a 25% decline in volumes that created over capacity in the marketplace, which reduced our financial returns in the Metals business. Volumes have not returned to pre-2001 levels. Over the past several years, we have undertaken a number of restructuring and downsizing actions, including multiple plant closures. The benefits of these actions have been more than offset by the escalation of both energy and commodity metal prices, specifically copper, zinc, and nickel. As a result, we have been unable to realize acceptable returns in the business. During the second half of 2006 and first half of 2007, we evaluated a number of strategic alternatives for the Metals business, and we made the decision in mid-2007 to engage Goldman, Sachs & Co. to conduct a formal strategic evaluation process, including the alternative of selling the business. The sale of Metals provides us with the financial flexibility to pursue investments in areas where we can earn the best returns.

On October 15, 2007, we announced we entered into a definitive agreement to sell the Metals business to Global for $400 million, payable in cash. The price received was subject to a customary working capital adjustment. The sale was subject to Hart-Scott-Rodino Antitrust Improvement Act clearance, but not shareholder approval. The transaction closed on November 19, 2007. Based on the Metals assets held for sale, we recognized a pretax loss of $160.0 million partially offset by a $21.0 million income tax benefit, resulting in a net loss on disposal of discontinued operations of $139.0 million for 2007. The loss on disposal of discontinued operations includes a pension curtailment charge of $6.9 million, other postretirement benefits curtailment credit of $1.1 million and estimated transaction fees of $24.6 million. The final loss recognized related to this transaction will be dependent upon the final determination of the value of working capital in the business. The loss on the disposal, which includes transaction costs, reflects a book value of the Metals business of approximately $564 million and a tax basis of approximately $419 million. The difference between the book and tax values of the business reflects primarily goodwill of $75.8 million and intangibles of $10.4 million. Based on an estimated working capital adjustment, we anticipate net cash proceeds from the transaction of $380.8 million, which is in addition to the $98.1 million of after-tax cash flow realized from the operation of Metals during 2007.

The Metals business was a reportable segment comprised of principal manufacturing facilities in East Alton, IL and Montpelier, OH. Metals produced and distributed copper and copper alloy sheet, strip, foil, rod, welded tube, fabricated parts, and stainless steel and aluminum strip. Sales for the Metals business were $1,891.7 million, $2,112.1 million, and $1,402.7 million for the period of our ownership in 2007, 2006, and 2005, respectively. The Metals business sales included commodity metal price changes that are primarily a pass-through. Intersegment sales of $81.4

million, $69.1 million and $47.7 million for the period of our ownership in 2007, 2006 and 2005, respectively, representing the sale of ammunition cartridge case cups to Winchester from Metals, at prices that approximate market, have been eliminated from Metals sales. In conjunction with the sale of the Metals business, Winchester agreed to purchase the majority of its ammunition cartridge case cups and copper-based strip requirements from Global under a multi-year agreement with pricing, terms, and conditions which approximate market. The Metals business employed approximately 2,900 hourly and salaried employees. As the criteria to treat the related assets and liabilities as “held for sale” were met in the third quarter of 2007, the related assets and liabilities were classified as “held for sale”, and the results of operations from the Metals business have been reclassified as discontinued operations for all periods presented.

In conjunction with the sale of the Metals business, we retained certain assets and liabilities including certain assets co-located with our Winchester business in East Alton, IL, assets and liabilities associated with former Metals manufacturing locations, pension assets and pension and postretirement healthcare and life insurance liabilities associated with Metals employees for service earned through the date of sale, and certain environmental obligations existing at the date of closing associated with current and past Metals manufacturing operations and waste disposal sites.

Pioneer Acquisition

On August 31, 2007, we acquired Pioneer, a manufacturer of chlorine, caustic soda, bleach, sodium chlorate, and hydrochloric acid. Pioneer owns and operates four chlor-alkali plants and several bleach manufacturing facilities in North America. Under the merger agreement, each share of Pioneer common stock was converted into the right to receive $35.00 in cash, without interest. The aggregate purchase price for all of Pioneer’s outstanding shares of common stock, together with the aggregate payment due to holders of options to purchase shares of common stock of Pioneer, was $426.1 million, which includes direct fees and expenses. We financed the merger with cash and $110.0 million of borrowings against our accounts receivable securitization facility (Accounts Receivable Facility). We assumed $120.0 million of Pioneer’s convertible debt which was redeemed in the fourth quarter of 2007 and January 2008. We paid a conversion premium of $25.8 million on the Pioneer convertible debt.

Since August 31, 2007, Pioneer sales were $183.6 million and segment income was $29.2 million, which were included in our Chlor Alkali Products segment results.