UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-4085

Fidelity Income Fund

(Exact name of registrant as specified in charter)

245 Summer St., Boston, MA 02210

(Address of principal executive offices) (Zip code)

Marc Bryant, Secretary

245 Summer St.

Boston, Massachusetts 02210

(Name and address of agent for service)

Registrant's telephone number, including area code:

617-563-7000

| |

Date of fiscal year end: | August 31 |

|

|

Date of reporting period: | February 28, 2017 |

Item 1.

Reports to Stockholders

Fidelity® Government Income Fund

Semi-Annual Report February 28, 2017 |

|

Contents

To view a fund's proxy voting guidelines and proxy voting record for the 12-month period ended June 30, visit http://www.fidelity.com/proxyvotingresults or visit the Securities and Exchange Commission's (SEC) web site at http://www.sec.gov.

You may also call 1-800-544-8544 to request a free copy of the proxy voting guidelines.

Standard & Poor's, S&P and S&P 500 are registered service marks of The McGraw-Hill Companies, Inc. and have been licensed for use by Fidelity Distributors Corporation.

Other third-party marks appearing herein are the property of their respective owners.

All other marks appearing herein are registered or unregistered trademarks or service marks of FMR LLC or an affiliated company. © 2017 FMR LLC. All rights reserved.

This report and the financial statements contained herein are submitted for the general information of the shareholders of the Fund. This report is not authorized for distribution to prospective investors in the Fund unless preceded or accompanied by an effective prospectus.

A fund files its complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. Forms N-Q are available on the SEC’s web site at http://www.sec.gov. A fund's Forms N-Q may be reviewed and copied at the SEC’s Public Reference Room in Washington, DC. Information regarding the operation of the SEC's Public Reference Room may be obtained by calling 1-800-SEC-0330.

For a complete list of a fund's portfolio holdings, view the most recent holdings listing, semiannual report, or annual report on Fidelity's web site at http://www.fidelity.com, http://www.institutional.fidelity.com, or http://www.401k.com, as applicable.

NOT FDIC INSURED •MAY LOSE VALUE •NO BANK GUARANTEE

Neither the Fund nor Fidelity Distributors Corporation is a bank.

Investment Summary (Unaudited)

The information in the following tables is based on the combined investments of the Fund and its pro-rata share of the investments of Fidelity's Fixed-Income Central Funds.

Coupon Distribution as of February 28, 2017

| | % of fund's investments | % of fund's investments 6 months ago |

| Zero coupon bonds | 0.0 | 0.0 |

| 0.01 - 0.99% | 1.9 | 7.9 |

| 1 - 1.99% | 31.8 | 26.9 |

| 2 - 2.99% | 22.1 | 16.8 |

| 3 - 3.99% | 22.4 | 23.2 |

| 4 - 4.99% | 12.8 | 15.0 |

| 5 - 5.99% | 8.3 | 8.6 |

| 6 - 6.99% | 0.6 | 0.4 |

| 7 - 7.99% | 0.5 | 0.1 |

| 8% and above | 0.0 | 0.4 |

Coupon distribution shows the range of stated interest rates on the fund's investments, excluding short-term investments.

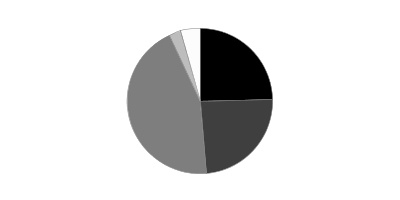

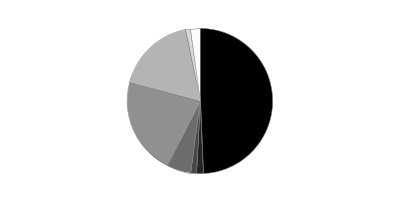

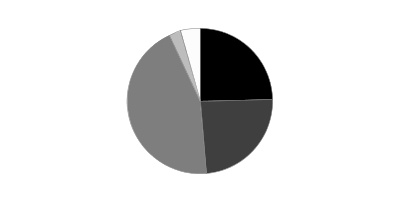

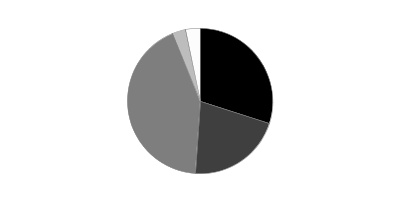

Asset Allocation (% of fund's net assets)

| As of February 28, 2017*,** |

| | Mortgage Securities | 24.8% |

| | CMOs and Other Mortgage Related Securities | 24.1% |

| | U.S. Treasury Obligations | 44.8% |

| | U.S. Government Agency Obligations*** | 2.7% |

| | Foreign Government & Government Agency Obligations | 4.3% |

| | Short-Term Investments and Net Other Assets (Liabilities)† | (0.7)% |

* Foreign investments - 4.3%

** Futures and Swaps - 5.7%

*** Includes NCUA Guaranteed Notes

† Short-Term Investments and Net Other Assets (Liabilities) are not included in the pie chart

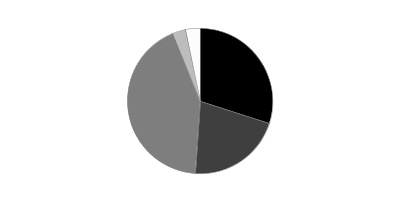

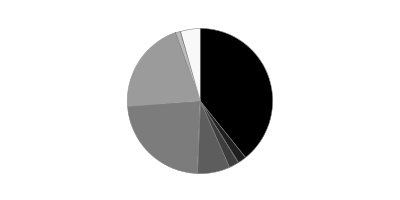

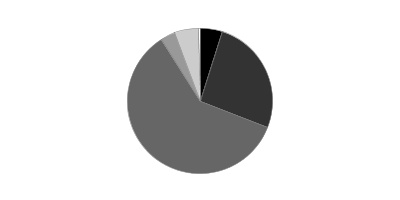

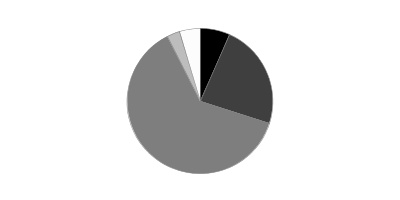

| As of August 31, 2016*,** |

| | Mortgage Securities | 31.5% |

| | CMOs and Other Mortgage Related Securities | 22.1% |

| | U.S. Treasury Obligations | 44.9% |

| | U.S. Government Agency Obligations*** | 3.1% |

| | Foreign Government & Government Agency Obligations | 3.3% |

| | Short-Term Investments and Net Other Assets (Liabilities)† | (4.9)% |

* Foreign investments - 3.3%

** Futures and Swaps - 1.1%

*** Includes NCUA Guaranteed Notes

† Short-Term Investments and Net Other Assets (Liabilities) are not included in the pie chart

An unaudited holdings listing for the Fund, which presents direct holdings as well as the pro-rata share of any securities and other investments held indirectly through its investment in underlying non-money market Fidelity Central Funds, is available at fidelity.com and/or institutional.fidelity.com, as applicable.

Percentages in the above tables are adjusted for the effect of TBA Sale Commitments.

Percentages shown as 0.0% may reflect amounts less than 0.05%.

Investments February 28, 2017 (Unaudited)

Showing Percentage of Net Assets

| U.S. Government and Government Agency Obligations - 47.5% | | | |

| | | Principal Amount (000s) | Value (000s) |

| U.S. Government Agency Obligations - 0.8% | | | |

| Fannie Mae: | | | |

| 0.875% 8/2/19 | | $131 | $129 |

| 1% 2/26/19 | | 326 | 324 |

| 1.125% 12/14/18 | | 240 | 240 |

| Small Business Administration guaranteed development participation certificates: | | | |

| Series 2002-20J Class 1, 4.75% 10/1/22 | | 754 | 791 |

| Series 2002-20K Class 1, 5.08% 11/1/22 | | 1,213 | 1,283 |

| Series 2004-20H Class 1, 5.17% 8/1/24 | | 484 | 509 |

| Tennessee Valley Authority: | | | |

| 1.75% 10/15/18 | | 23,006 | 23,191 |

| 5.25% 9/15/39 | | 2,807 | 3,550 |

| 5.375% 4/1/56 | | 3,438 | 4,438 |

| | | | 34,455 |

| U.S. Treasury Inflation-Protected Obligations - 0.5% | | | |

| U.S. Treasury Inflation-Indexed Bonds 1% 2/15/46 | | 23,359 | 24,139 |

| U.S. Treasury Obligations - 44.3% | | | |

| U.S. Treasury Bonds: | | | |

| 2.5% 2/15/46 | | 30,232 | 27,382 |

| 2.875% 8/15/45 | | 112,441 | 110,179 |

| 2.875% 11/15/46 | | 18,519 | 18,172 |

| 3% 11/15/44 | | 29,032 | 29,167 |

| 3% 11/15/45 | | 40,000 | 40,169 |

| 3% 2/15/47 | | 7,000 | 7,048 |

| 3.625% 2/15/44 | | 45,031 | 50,648 |

| 4.375% 5/15/40 | | 3,000 | 3,755 |

| 4.75% 2/15/37 | | 72,700 | 95,672 |

| 5% 5/15/37 (a)(b) | | 39,142 | 53,105 |

| U.S. Treasury Notes: | | | |

| 0.75% 7/15/19 | | 12,074 | 11,907 |

| 0.875% 6/15/19 | | 26,866 | 26,594 |

| 1.125% 1/31/19 | | 58,397 | 58,288 |

| 1.125% 7/31/21 | | 29,606 | 28,697 |

| 1.125% 9/30/21 | | 119,876 | 115,943 |

| 1.25% 10/31/21 | | 40,000 | 38,872 |

| 1.375% 2/28/19 | | 43,570 | 43,691 |

| 1.375% 12/15/19 | | 46,112 | 46,011 |

| 1.375% 3/31/20 | | 93,656 | 93,213 |

| 1.375% 4/30/20 | | 4,172 | 4,148 |

| 1.375% 8/31/20 | | 5,000 | 4,955 |

| 1.375% 1/31/21 | | 27,500 | 27,111 |

| 1.375% 4/30/21 | | 20,000 | 19,662 |

| 1.375% 5/31/21 | | 20,000 | 19,641 |

| 1.5% 10/31/19 | | 5,655 | 5,666 |

| 1.5% 1/31/22 | | 46,220 | 45,326 |

| 1.5% 8/15/26 | | 11,629 | 10,769 |

| 1.625% 6/30/19 | | 51,223 | 51,559 |

| 1.625% 12/31/19 | | 35,368 | 35,524 |

| 1.625% 6/30/20 | | 4,710 | 4,713 |

| 1.625% 7/31/20 | | 30,000 | 30,000 |

| 1.75% 9/30/19 | | 54,087 | 54,573 |

| 1.75% 10/31/20 | | 18,000 | 18,045 |

| 1.75% 12/31/20 | | 119,701 | 119,788 |

| 1.75% 2/28/22 | | 3,773 | 3,740 |

| 1.875% 1/31/22 | | 10,819 | 10,804 |

| 1.875% 2/28/22 | | 30,000 | 29,968 |

| 2% 9/30/20 | | 107,107 | 108,391 |

| 2% 12/31/21 | | 32,945 | 33,094 |

| 2% 7/31/22 | | 18,845 | 18,855 |

| 2% 2/15/25 | | 37,274 | 36,473 |

| 2% 8/15/25 (a) | | 35,960 | 35,039 |

| 2% 11/15/26 | | 74,817 | 72,374 |

| 2.125% 6/30/21 | | 22,000 | 22,274 |

| 2.125% 12/31/21 | | 2,000 | 2,020 |

| 2.125% 6/30/22 | | 1,146 | 1,154 |

| 2.125% 2/29/24 | | 84,321 | 83,965 |

| 2.125% 5/15/25 | | 38,251 | 37,710 |

| 2.25% 7/31/21 | | 26,021 | 26,463 |

| 2.25% 1/31/24 | | 70,482 | 70,782 |

| 2.25% 2/15/27 | | 15,000 | 14,854 |

| | | | 1,957,953 |

| Other Government Related - 1.9% | | | |

| National Credit Union Administration Guaranteed Notes: | | | |

| Series 2010-A1 Class A, 1.1156% 12/7/20 (NCUA Guaranteed) (c) | | 3,074 | 3,070 |

| Series 2011-R4 Class 1A, 1.1456% 3/6/20 (NCUA Guaranteed) (c) | | 985 | 985 |

| National Credit Union Administration Guaranteed Notes Master Trust 3.45% 6/12/21 (NCUA Guaranteed) | | 74,000 | 77,990 |

| | | | 82,045 |

| TOTAL U.S. GOVERNMENT AND GOVERNMENT AGENCY OBLIGATIONS | | | |

| (Cost $2,112,243) | | | 2,098,592 |

|

| U.S. Government Agency - Mortgage Securities - 3.4% | | | |

| Fannie Mae - 2.0% | | | |

| 2.458% 2/1/44 (c) | | 505 | 520 |

| 2.459% 4/1/44 (c) | | 694 | 712 |

| 2.474% 12/1/34 (c) | | 155 | 160 |

| 2.511% 2/1/44 (c) | | 410 | 422 |

| 2.54% 6/1/42 (c) | | 286 | 297 |

| 2.546% 3/1/35 (c) | | 77 | 79 |

| 2.556% 5/1/44 (c) | | 774 | 796 |

| 2.563% 3/1/36 (c) | | 355 | 370 |

| 2.576% 1/1/44 (c) | | 729 | 750 |

| 2.608% 2/1/33 (c) | | 50 | 51 |

| 2.63% 4/1/44 (c) | | 1,762 | 1,814 |

| 2.632% 7/1/35 (c) | | 58 | 61 |

| 2.646% 5/1/44 (c) | | 1,338 | 1,382 |

| 2.654% 10/1/33 (c) | | 110 | 113 |

| 2.666% 10/1/33 (c) | | 49 | 51 |

| 2.69% 3/1/37 (c) | | 115 | 120 |

| 2.699% 2/1/42 (c) | | 1,607 | 1,665 |

| 2.715% 2/1/36 (c) | | 47 | 50 |

| 2.73% 7/1/34 (c) | | 92 | 95 |

| 2.772% 1/1/42 (c) | | 1,251 | 1,296 |

| 2.798% 10/1/33 (c) | | 102 | 108 |

| 2.802% 6/1/36 (c) | | 142 | 149 |

| 2.833% 3/1/35 (c) | | 66 | 69 |

| 2.915% 11/1/33 (c) | | 81 | 84 |

| 2.943% 9/1/41 (c) | | 161 | 167 |

| 2.946% 7/1/35 (c) | | 172 | 178 |

| 2.956% 11/1/36 (c) | | 71 | 74 |

| 2.973% 11/1/40 (c) | | 124 | 131 |

| 2.975% 10/1/41 (c) | | 90 | 95 |

| 2.977% 5/1/36 (c) | | 98 | 103 |

| 3.187% 3/1/40 (c) | | 1,452 | 1,539 |

| 3.241% 7/1/41 (c) | | 250 | 263 |

| 3.364% 10/1/41 (c) | | 143 | 149 |

| 3.55% 7/1/41 (c) | | 333 | 348 |

| 4% 5/1/29 to 2/1/42 | | 53,440 | 56,384 |

| 4.5% 11/1/25 to 4/1/39 | | 8,065 | 8,629 |

| 5% 7/1/35 | | 7,262 | 8,009 |

| 5.5% 1/1/29 | | 1,541 | 1,714 |

| 6.5% 3/1/22 to 5/1/27 | | 271 | 305 |

| 9.5% 10/1/20 | | 8 | 8 |

| 11.5% 1/15/21 | | 1 | 1 |

| | | | 89,311 |

| Freddie Mac - 0.6% | | | |

| 2.57% 3/1/35 (c) | | 288 | 296 |

| 2.936% 5/1/37 (c) | | 188 | 196 |

| 2.997% 2/1/36 (c) | | 19 | 20 |

| 3% 2/1/31 | | 11,016 | 11,354 |

| 3.026% 10/1/41 (c) | | 2,473 | 2,572 |

| 3.066% 9/1/41 (c) | | 1,603 | 1,690 |

| 3.07% 7/1/35 (c) | | 748 | 797 |

| 3.099% 10/1/42 (c) | | 1,009 | 1,067 |

| 3.14% 3/1/33 (c) | | 7 | 7 |

| 3.198% 9/1/41 (c) | | 192 | 201 |

| 3.231% 4/1/41 (c) | | 157 | 163 |

| 3.282% 6/1/41 (c) | | 202 | 213 |

| 3.295% 7/1/36 (c) | | 275 | 293 |

| 3.392% 5/1/41 (c) | | 162 | 172 |

| 3.626% 5/1/41 (c) | | 226 | 238 |

| 3.665% 6/1/41 (c) | | 223 | 235 |

| 3.887% 10/1/35 (c) | | 138 | 147 |

| 4.5% 5/1/39 to 10/1/41 | | 2,942 | 3,185 |

| 5.5% 7/1/29 | | 31 | 34 |

| 6% 1/1/24 | | 1,105 | 1,197 |

| 9.5% 6/1/18 to 8/1/21 | | 8 | 9 |

| | | | 24,086 |

| Ginnie Mae - 0.8% | | | |

| 4.3% 8/20/61 (d) | | 3,436 | 3,521 |

| 4.649% 2/20/62 (d) | | 2,754 | 2,861 |

| 4.682% 2/20/62 (d) | | 3,541 | 3,674 |

| 4.684% 1/20/62 (d) | | 20,735 | 21,471 |

| 5.47% 8/20/59 (d) | | 246 | 248 |

| 6% 6/15/36 | | 4,272 | 4,946 |

| | | | 36,721 |

| TOTAL U.S. GOVERNMENT AGENCY - MORTGAGE SECURITIES | | | |

| (Cost $149,817) | | | 150,118 |

|

| Collateralized Mortgage Obligations - 17.0% | | | |

| U.S. Government Agency - 17.0% | | | |

| Fannie Mae: | | | |

| floater: | | | |

| Series 2001-38 Class QF, 1.7583% 8/25/31 (c) | | 101 | 102 |

| Series 2002-49 Class FB, 1.3806% 11/18/31 (c) | | 89 | 90 |

| Series 2002-60 Class FV, 1.7783% 4/25/32 (c) | | 37 | 38 |

| Series 2002-75 Class FA, 1.7783% 11/25/32 (c) | | 76 | 77 |

| Series 2010-15 Class FJ, 1.7083% 6/25/36 (c) | | 5,849 | 5,934 |

| planned amortization class: | | | |

| Series 2005-19 Class PA, 5.5% 7/25/34 | | 1,589 | 1,673 |

| Series 2005-27 Class NE, 5.5% 5/25/34 | | 632 | 639 |

| Series 2005-64 Class PX, 5.5% 6/25/35 | | 1,746 | 1,892 |

| Series 2005-68 Class CZ, 5.5% 8/25/35 | | 4,458 | 4,995 |

| Series 2006-45 Class OP, 6/25/36 (e) | | 812 | 709 |

| Series 2010-118 Class PB, 4.5% 10/25/40 | | 6,956 | 7,381 |

| sequential payer: | | | |

| Series 2003-117 Class MD, 5% 12/25/23 | | 902 | 960 |

| Series 2004-91 Class Z, 5% 12/25/34 | | 5,636 | 6,196 |

| Series 2005-117 Class JN, 4.5% 1/25/36 | | 567 | 600 |

| Series 2005-14 Class ZB, 5% 3/25/35 | | 1,712 | 1,879 |

| Series 2006-72 Class CY, 6% 8/25/26 | | 3,583 | 3,887 |

| Series 2009-59 Class HB, 5% 8/25/39 | | 2,474 | 2,714 |

| Series 2010-97 Class CX, 4.5% 9/25/25 | | 10,927 | 11,770 |

| Series 2009-85 Class IB, 4.5% 8/25/24 (f) | | 298 | 17 |

| Series 2009-93 Class IC, 4.5% 9/25/24 (f) | | 433 | 23 |

| Series 2010-139 Class NI, 4.5% 2/25/40 (f) | | 3,846 | 451 |

| Series 2010-39 Class FG, 1.6983% 3/25/36 (c) | | 3,647 | 3,725 |

| Series 2010-97 Class CI, 4.5% 8/25/25 (f) | | 1,041 | 69 |

| Series 2012-27 Class EZ, 4.25% 3/25/42 | | 7,175 | 7,675 |

| Series 2016-26 Class CG, 3% 5/25/46 | | 23,324 | 23,842 |

| Freddie Mac: | | | |

| floater: | | | |

| Series 2530 Class FE, 1.37% 2/15/32 (c) | | 51 | 51 |

| Series 2630 Class FL, 1.27% 6/15/18 (c) | | 17 | 17 |

| Series 2682 Class FB, 1.67% 10/15/33 (c) | | 3,157 | 3,202 |

| Series 2711 Class FC, 1.67% 2/15/33 (c) | | 1,734 | 1,759 |

| planned amortization class: | | | |

| Series 1141 Class G, 9% 9/15/21 | | 37 | 41 |

| Series 2682 Class LD, 4.5% 10/15/33 | | 732 | 774 |

| Series 3415 Class PC, 5% 12/15/37 | | 529 | 564 |

| Series 3763 Class QA, 4% 4/15/34 | | 803 | 811 |

| Series 3840 Class VA, 4.5% 9/15/27 | | 4,014 | 4,182 |

| Series 3857 Class ZP, 5% 5/15/41 | | 2,918 | 3,426 |

| sequential payer: | | | |

| Series 2004-2802 Class ZG, 5.5% 5/15/34 | | 7,983 | 8,927 |

| Series 2587 Class AD, 4.71% 3/15/33 | | 3,052 | 3,230 |

| Series 2773 Class HC, 4.5% 4/15/19 | | 215 | 219 |

| Series 2877 Class ZD, 5% 10/15/34 | | 6,806 | 7,467 |

| Series 3007 Class EW, 5.5% 7/15/25 | | 5,516 | 5,940 |

| Series 3745 Class KV, 4.5% 12/15/26 | | 6,562 | 7,079 |

| Series 3806 Class L, 3.5% 2/15/26 | | 8,900 | 9,368 |

| Series 3871 Class KB, 5.5% 6/15/41 | | 13,870 | 16,181 |

| Series 3889 Class DZ, 4% 1/15/41 | | 34,107 | 34,983 |

| Series 3843 Class PZ, 5% 4/15/41 | | 2,496 | 2,890 |

| Freddie Mac Multi-family Structured pass-thru certificates sequential payer: | | | |

| Series 4335 Class AL, 4.25% 3/15/40 | | 8,104 | 8,534 |

| Series 4341 Class ML, 3.5% 11/15/31 | | 10,816 | 11,296 |

| Ginnie Mae guaranteed REMIC pass-thru certificates: | | | |

| floater: | | | |

| Series 2008-2 Class FD, 1.2606% 1/20/38 (c) | | 264 | 265 |

| Series 2008-73 Class FA, 1.6406% 8/20/38 (c) | | 2,012 | 2,034 |

| Series 2008-83 Class FB, 1.6806% 9/20/38 (c) | | 1,808 | 1,845 |

| Series 2009-108 Class CF, 1.37% 11/16/39 (c) | | 1,195 | 1,203 |

| Series 2011-H20 Class FA, 1.1967% 9/20/61 (c)(d) | | 9,074 | 9,056 |

| Series 2011-H21 Class FA, 1.2467% 10/20/61 (c)(d) | | 6,060 | 6,059 |

| Series 2012-H01 Class FA, 1.3467% 11/20/61 (c)(d) | | 5,194 | 5,210 |

| Series 2012-H03 Class FA, 1.4717% 1/20/62 (c)(d) | | 3,281 | 3,291 |

| Series 2012-H06 Class FA, 1.2767% 1/20/62 (c)(d) | | 4,893 | 4,897 |

| Series 2012-H07 Class FA, 1.2767% 3/20/62 (c)(d) | | 3,028 | 3,031 |

| Series 2012-H21 Class DF, 1.2967% 5/20/61 (c)(d) | | 5,105 | 5,113 |

| Series 2013-H19: | | | |

| Class FC, 1.3717% 8/20/63 (c)(d) | | 1,153 | 1,153 |

| Class FD, 1.3717% 8/20/63 (c)(d) | | 3,016 | 3,015 |

| Series 2014-H02 Class FB, 1.4217% 12/20/63 (c)(d) | | 37,527 | 37,588 |

| Series 2014-H03 Class FA, 1.3717% 1/20/64 (c)(d) | | 14,761 | 14,757 |

| Series 2015-H07 Class FA, 0.3% 3/20/65 (c)(d) | | 17,166 | 17,112 |

| Series 2015-H13 Class FL, 1.0517% 5/20/63 (c)(d) | | 19,538 | 19,515 |

| Series 2015-H19 Class FA, 0.9717% 4/20/63 (c)(d) | | 18,838 | 18,797 |

| Series 2016-H20 Class FM, 1.1717% 12/20/62 (c)(d) | | 16,468 | 16,462 |

| planned amortization class Series 2010-31 Class BP, 5% 3/20/40 | | 11,191 | 12,368 |

| sequential payer: | | | |

| Series 2011-69 Class GX, 4.5% 5/16/40 | | 10,205 | 11,097 |

| Series 2013-H06 Class HA, 1.65% 1/20/63 (d) | | 5,507 | 5,490 |

| Series 2013-H26 Class HA, 3.5% 9/20/63 (d) | | 45,422 | 46,796 |

| Series 2014-H12 Class KA, 2.75% 5/20/64 (d) | | 5,972 | 6,033 |

| Series 2016-H02 Class FM, 1.2717% 9/20/62 (c)(d) | | 22,561 | 22,564 |

| Series 2016-H04 Class FE, 1.4217% 11/20/65 (c)(d) | | 5,577 | 5,583 |

| Series 2010-169 Class Z, 4.5% 12/20/40 | | 6,674 | 7,146 |

| Series 2010-H15 Class TP, 5.15% 8/20/60 (d) | | 14,962 | 15,652 |

| Series 2010-H17 Class XP, 5.2976% 7/20/60 (c)(d) | | 17,939 | 18,662 |

| Series 2010-H18 Class PL, 5.01% 9/20/60 (c)(d) | | 14,674 | 15,283 |

| Series 2012-64 Class KI, 3.5% 11/20/36 | | 1,466 | 116 |

| Series 2013-124: | | | |

| Class ES, 7.6259% 4/20/39 (c)(g) | | 5,682 | 6,015 |

| Class ST, 7.7593% 8/20/39 (c)(g) | | 11,471 | 12,438 |

| Series 2015-H17 Class HA, 2.5% 5/20/65 (d) | | 15,070 | 15,228 |

| Series 2015-H21: | | | |

| Class HA, 2.5% 6/20/63 (d) | | 47,135 | 47,594 |

| Class JA, 2.5% 6/20/65 (d) | | 5,588 | 5,643 |

| Series 2015-H30 Class HA, 1.75% 9/20/62 (c)(d) | | 44,258 | 43,951 |

| Series 2016-H13 Class FB, 1.18% 5/20/66 (c)(d) | | 26,613 | 26,557 |

| Series 2017-H06 Class FA, 1.17% 8/20/66 (c)(d) | | 23,810 | 23,836 |

| Series 2090-118 Class XZ, 5% 12/20/39 | | 13,745 | 15,621 |

| | | | 752,355 |

| TOTAL COLLATERALIZED MORTGAGE OBLIGATIONS | | | |

| (Cost $756,772) | | | 752,355 |

|

| Commercial Mortgage Securities - 4.6% | | | |

| FMPRE Multifamily Agency floater Series 2017-KT01 Class A, 1.09% 2/25/20 (c) | | 43,722 | 43,735 |

| Freddie Mac: | | | |

| floater Series K707 Class A2, 2.22% 12/25/18 | | 34,545 | 34,860 |

| pass-thru certificates sequential payer Series K011 Class A2, 4.084% 11/25/20 | | 3,740 | 3,986 |

| sequential payer: | | | |

| Series K009 Class A2, 3.808% 8/25/20 | | 5,591 | 5,903 |

| Series K027 Class A2, 2.637% 1/25/23 | | 6,437 | 6,518 |

| Series K029 Class A2, 3.32% 2/25/23 (c) | | 3,110 | 3,260 |

| Series K034 Class A1, 2.669% 2/25/23 | | 12,819 | 13,021 |

| Series K709 Class A2, 2.086% 3/25/19 | | 17,210 | 17,331 |

| Series K710 Class A2, 1.883% 5/25/19 | | 16,814 | 16,861 |

| Series K713 Class A2, 2.313% 3/25/20 | | 5,437 | 5,500 |

| Series K717 Class A2, 2.991% 9/25/21 | | 4,531 | 4,676 |

| Series K032 Class A1, 3.016% 2/25/23 | | 21,645 | 22,223 |

| Series K504 Class A2, 2.566% 9/25/20 (c) | | 3,629 | 3,696 |

| Series K724 Class A1, 2.776% 3/25/23 | | 19,621 | 19,988 |

| TOTAL COMMERCIAL MORTGAGE SECURITIES | | | |

| (Cost $201,792) | | | 201,558 |

|

| Foreign Government and Government Agency Obligations - 4.3% | | | |

| Israeli State: | | | |

| (guaranteed by U.S. Government through Agency for International Development): | | | |

| 5.5% 9/18/23 | | 72,266 | 85,814 |

| 5.5% 12/4/23 | | 48 | 57 |

| 5.5% 4/26/24 | | 6,065 | 7,236 |

| Jordanian Kingdom: | | | |

| 2.503% 10/30/20 | | 41,050 | 42,039 |

| 3% 6/30/25 | | 19,267 | 19,757 |

| Ukraine Government 1.471% 9/29/21 | | 34,809 | 34,095 |

| TOTAL FOREIGN GOVERNMENT AND GOVERNMENT AGENCY OBLIGATIONS | | | |

| (Cost $177,317) | | | 188,998 |

| | | Shares | Value (000s) |

|

| Fixed-Income Funds - 22.7% | | | |

| Fidelity Mortgage Backed Securities Central Fund (h) | | | |

| (Cost $968,200) | | 9,301,310 | 1,003,983 |

|

| Money Market Funds - 0.8% | | | |

| Fidelity Cash Central Fund, 0.60% (i) | | | |

| (Cost $35,046) | | 35,039,068 | 35,046 |

| TOTAL INVESTMENT PORTFOLIO - 100.3% | | | |

| (Cost $4,401,187) | | | 4,430,650 |

| NET OTHER ASSETS (LIABILITIES) - (0.3)% | | | (14,243) |

| NET ASSETS - 100% | | | $4,416,407 |

| TBA Sale Commitments | | |

| | Principal Amount (000s) | Value (000s) |

| Fannie Mae | | |

| 4% 3/1/47 | | |

| (Proceeds $3,997) | $(3,800) | $(3,993) |

| Futures Contracts | | | |

| | Expiration Date | Underlying Face Amount at Value (000s) | Unrealized Appreciation/(Depreciation) (000s) |

| Purchased | | | |

| Treasury Contracts | | | |

| 658 CBOT 10-Year U.S. Treasury Note Contracts (United States) | June 2017 | 81,972 | $600 |

| 600 CBOT 2-Year U.S. Treasury Note Contracts (United States) | June 2017 | 129,844 | 214 |

| 85 CBOT Long Term U.S. Treasury Bond Contracts (United States) | June 2017 | 12,891 | 195 |

| TOTAL FUTURES CONTRACTS | | | $1,009 |

The face value of futures purchased as a percentage of Net Assets is 5.1%

Swaps

| Clearinghouse/Counterparty(1) | Expiration Date | Notional Amount (000s)(1) | Payment Received | Payment Paid | Value (000s) | Upfront Premium Received/(Paid) (000s)(2) | Unrealized Appreciation/(Depreciation) (000s) |

| Interest Rate Swaps | | | | | | | |

| CME | Mar. 2027 | USD 24,100 | 1.75% | 3-month LIBOR | $130 | $0 | $130 |

| CME | Mar. 2047 | 1,200 | 2.25% | 3-month LIBOR | 22 | 0 | 22 |

|

| TOTAL INTEREST RATE SWAPS | | | | | $152 | $0 | $152 |

|

(1) Swaps with CME Group (CME) are centrally cleared over-the-counter (OTC) swaps.

(2) Any premiums for centrally cleared over-the-counter (OTC) swaps are recorded periodically throughout the term of the swap to variation margin and included in unrealized appreciation (depreciation).

Legend

(a) Security or a portion of the security was pledged to cover margin requirements for futures contracts. At period end, the value of securities pledged amounted to $1,837,000.

(b) Security or a portion of the security was pledged to cover margin requirements for centrally cleared OTC swaps. At period end, the value of securities pledged amounted to $1,050,000.

(c) Coupon rates for floating and adjustable rate securities reflect the rates in effect at period end.

(d) Represents an investment in an underlying pool of reverse mortgages which typically do not require regular principal and interest payments as repayment is deferred until a maturity event.

(e) Principal Only Strips represent the right to receive the monthly principal payments on an underlying pool of mortgage loans.

(f) Security represents right to receive monthly interest payments on an underlying pool of mortgages or assets. Principal shown is the outstanding par amount of the pool as of the end of the period.

(g) Coupon is inversely indexed to a floating interest rate multiplied by a specified factor. The price may be considerably more volatile than the price of a comparable fixed rate security.

(h) Affiliated fund that is generally available only to investment companies and other accounts managed by Fidelity Investments. A complete unaudited schedule of portfolio holdings for each Fidelity Central Fund is filed with the SEC for the first and third quarters of each fiscal year on Form N-Q and is available upon request or at the SEC's website at www.sec.gov. An unaudited holdings listing for the Fund, which presents direct holdings as well as the pro-rata share of securities and other investments held indirectly through its investment in underlying non-money market Fidelity Central Funds, is available at fidelity.com and/or institutional.fidelity.com, as applicable. In addition, each Fidelity Central Fund's financial statements are available on the SEC's website or upon request.

(i) Affiliated fund that is generally available only to investment companies and other accounts managed by Fidelity Investments. The rate quoted is the annualized seven-day yield of the fund at period end. A complete unaudited listing of the fund's holdings as of its most recent quarter end is available upon request. In addition, each Fidelity Central Fund's financial statements are available on the SEC's website or upon request.

Affiliated Central Funds

Information regarding fiscal year to date income earned by the Fund from investments in Fidelity Central Funds is as follows:

| Fund | Income earned |

| | (Amounts in thousands) |

| Fidelity Cash Central Fund | $133 |

| Fidelity Mortgage Backed Securities Central Fund | 17,896 |

| Total | $18,029 |

Additional information regarding the Fund's fiscal year to date purchases and sales, including the ownership percentage, of the non Money Market Central Funds is as follows:

| Fund (Amounts in thousands) | Value, beginning of period | Purchases | Sales Proceeds | Value, end of period | % ownership, end of period |

| Fidelity Mortgage Backed Securities Central Fund | $1,224,994 | $17,896 | $207,900 | $1,003,983 | 16.0% |

| Total | $1,224,994 | $17,896 | $207,900 | $1,003,983 | |

Investment Valuation

The following is a summary of the inputs used, as of February 28, 2017, involving the Fund's assets and liabilities carried at fair value. The inputs or methodology used for valuing securities may not be an indication of the risk associated with investing in those securities. For more information on valuation inputs, and their aggregation into the levels used below, please refer to the Investment Valuation section in the accompanying Notes to Financial Statements.

| | Valuation Inputs at Reporting Date: |

| Description | Total | Level 1 | Level 2 | Level 3 |

| (Amounts in thousands) | | | | |

| Investments in Securities: | | | | |

| U.S. Government and Government Agency Obligations | $2,098,592 | $-- | $2,098,592 | $-- |

| U.S. Government Agency - Mortgage Securities | 150,118 | -- | 150,118 | -- |

| Collateralized Mortgage Obligations | 752,355 | -- | 752,355 | -- |

| Commercial Mortgage Securities | 201,558 | -- | 201,558 | -- |

| Foreign Government and Government Agency Obligations | 188,998 | -- | 188,998 | -- |

| Fixed-Income Funds | 1,003,983 | 1,003,983 | -- | -- |

| Money Market Funds | 35,046 | 35,046 | -- | -- |

| Total Investments in Securities: | $4,430,650 | $1,039,029 | $3,391,621 | $-- |

| Derivative Instruments: | | | | |

| Assets | | | | |

| Futures Contracts | $1,009 | $1,009 | $-- | $-- |

| Swaps | 152 | -- | 152 | -- |

| Total Assets | $1,161 | $1,009 | $152 | $-- |

| Total Derivative Instruments: | $1,161 | $1,009 | $152 | $-- |

| Other Financial Instruments: | | | | |

| TBA Sale Commitments | $(3,993) | $-- | $(3,993) | $-- |

| Total Other Financial Instruments: | $(3,993) | $-- | $(3,993) | $-- |

Value of Derivative Instruments

The following table is a summary of the Fund's value of derivative instruments by primary risk exposure as of February 28, 2017. For additional information on derivative instruments, please refer to the Derivative Instruments section in the accompanying Notes to Financial Statements.

| Primary Risk Exposure / Derivative Type | Value |

| | Asset | Liability |

| (Amounts in thousands) | | |

| Interest Rate Risk | | |

| Futures Contracts(a) | $1,009 | $0 |

| Swaps(b) | 152 | 0 |

| Total Interest Rate Risk | 1,161 | 0 |

| Total Value of Derivatives | $1,161 | $0 |

(a) Reflects gross cumulative appreciation (depreciation) on futures contracts as presented in the Schedule of Investments. In the Statement of Assets and Liabilities, the period end daily variation margin is included in receivable or payable for daily variation margin for derivative instruments, and the net cumulative appreciation (depreciation) is included in net unrealized appreciation (depreciation).

(b) For centrally cleared over-the-counter (OTC) swaps, reflects gross cumulative appreciation (depreciation) as presented in the Schedule of Investments. In the Statement of Assets and Liabilities, the period end daily variation margin for centrally cleared OTC swaps is included in receivable or payable for daily variation margin for derivative instruments, and the net cumulative appreciation (depreciation) for centrally cleared OTC swaps is included in net unrealized appreciation (depreciation).

See accompanying notes which are an integral part of the financial statements.

Financial Statements

Statement of Assets and Liabilities

| Amounts in thousands (except per-share amounts) | | February 28, 2017 (Unaudited) |

| Assets | | |

Investment in securities, at value — See accompanying schedule:

Unaffiliated issuers (cost $3,397,941) | $3,391,621 | |

| Fidelity Central Funds (cost $1,003,246) | 1,039,029 | |

| Total Investments (cost $4,401,187) | | $4,430,650 |

| Cash | | 999 |

| Receivable for investments sold | | 30,028 |

| Receivable for TBA sale commitments | | 3,997 |

| Receivable for fund shares sold | | 5,099 |

| Interest receivable | | 12,682 |

| Distributions receivable from Fidelity Central Funds | | 37 |

| Receivable for daily variation margin for derivative instruments | | 31 |

| Other receivables | | 53 |

| Total assets | | 4,483,576 |

| Liabilities | | |

| Payable for investments purchased | $52,476 | |

| TBA sale commitments, at value | 3,993 | |

| Payable for fund shares redeemed | 8,547 | |

| Distributions payable | 243 | |

| Accrued management fee | 1,143 | |

| Distribution and service plan fees payable | 148 | |

| Other affiliated payables | 567 | |

| Other payables and accrued expenses | 52 | |

| Total liabilities | | 67,169 |

| Net Assets | | $4,416,407 |

| Net Assets consist of: | | |

| Paid in capital | | $4,467,322 |

| Distributions in excess of net investment income | | (5,151) |

| Accumulated undistributed net realized gain (loss) on investments | | (76,392) |

| Net unrealized appreciation (depreciation) on investments | | 30,628 |

| Net Assets | | $4,416,407 |

| Calculation of Maximum Offering Price | | |

| Class A: | | |

| Net Asset Value and redemption price per share ($220,544 ÷ 21,566 shares) | | $10.23 |

| Maximum offering price per share (100/96.00 of $10.23) | | $10.66 |

| Class T: | | |

| Net Asset Value and redemption price per share ($166,605 ÷ 16,294 shares) | | $10.22 |

| Maximum offering price per share (100/96.00 of $10.22) | | $10.65 |

| Class C: | | |

| Net Asset Value and offering price per share ($78,352 ÷ 7,663 shares)(a) | | $10.22 |

| Government Income: | | |

| Net Asset Value, offering price and redemption price per share ($3,479,347 ÷ 340,790 shares) | | $10.21 |

| Class I: | | |

| Net Asset Value, offering price and redemption price per share ($471,559 ÷ 46,116 shares) | | $10.23 |

(a) Redemption price per share is equal to net asset value less any applicable contingent deferred sales charge.

See accompanying notes which are an integral part of the financial statements.

Statement of Operations

| Amounts in thousands | | Six months ended February 28, 2017 (Unaudited) |

| Investment Income | | |

| Interest | | $34,252 |

| Income from Fidelity Central Funds | | 18,029 |

| Total income | | 52,281 |

| Expenses | | |

| Management fee | $7,249 | |

| Transfer agent fees | 2,615 | |

| Distribution and service plan fees | 965 | |

| Fund wide operations fee | 940 | |

| Independent trustees' fees and expenses | 10 | |

| Miscellaneous | 8 | |

| Total expenses before reductions | 11,787 | |

| Expense reductions | (1) | 11,786 |

| Net investment income (loss) | | 40,495 |

| Realized and Unrealized Gain (Loss) | | |

| Net realized gain (loss) on: | | |

| Investment securities: | | |

| Unaffiliated issuers | (1,525) | |

| Fidelity Central Funds | (2,747) | |

| Futures contracts | (3,788) | |

| Swaps | (1,749) | |

| Total net realized gain (loss) | | (9,809) |

Change in net unrealized appreciation (depreciation) on:

Investment securities | (162,655) | |

| Futures contracts | 1,021 | |

| Swaps | (313) | |

| Delayed delivery commitments | (28) | |

| Total change in net unrealized appreciation (depreciation) | | (161,975) |

| Net gain (loss) | | (171,784) |

| Net increase (decrease) in net assets resulting from operations | | $(131,289) |

See accompanying notes which are an integral part of the financial statements.

Statement of Changes in Net Assets

| Amounts in thousands | Six months ended February 28, 2017 (Unaudited) | Year ended August 31, 2016 |

| Increase (Decrease) in Net Assets | | |

| Operations | | |

| Net investment income (loss) | $40,495 | $71,092 |

| Net realized gain (loss) | (9,809) | 16,993 |

| Change in net unrealized appreciation (depreciation) | (161,975) | 104,347 |

| Net increase (decrease) in net assets resulting from operations | (131,289) | 192,432 |

| Distributions to shareholders from net investment income | (37,244) | (77,548) |

| Distributions to shareholders from net realized gain | (34,956) | (39,904) |

| Total distributions | (72,200) | (117,452) |

| Share transactions - net increase (decrease) | (321,438) | 502,872 |

| Total increase (decrease) in net assets | (524,927) | 577,852 |

| Net Assets | | |

| Beginning of period | 4,941,334 | 4,363,482 |

| End of period | $4,416,407 | $4,941,334 |

| Other Information | | |

| Distributions in excess of net investment income end of period | $(5,151) | $(8,402) |

See accompanying notes which are an integral part of the financial statements.

Financial Highlights — Fidelity Government Income Fund Class A

| | Six months ended (Unaudited) February 28, | Years ended August 31, | | | | |

| | 2017 | 2016 | 2015 | 2014 | 2013 | 2012 |

| Selected Per–Share Data | | | | | | |

| Net asset value, beginning of period | $10.66 | $10.50 | $10.47 | $10.20 | $10.97 | $10.90 |

| Income from Investment Operations | | | | | | |

| Net investment income (loss)A | .076 | .135 | .126 | .138 | .105 | .141 |

| Net realized and unrealized gain (loss) | (.361) | .270 | .048 | .278 | (.454) | .327 |

| Total from investment operations | (.285) | .405 | .174 | .416 | (.349) | .468 |

| Distributions from net investment income | (.069) | (.150) | (.116) | (.139) | (.099) | (.135) |

| Distributions from net realized gain | (.076) | (.095) | (.028) | (.007) | (.322) | (.263) |

| Total distributions | (.145) | (.245) | (.144) | (.146) | (.421) | (.398) |

| Net asset value, end of period | $10.23 | $10.66 | $10.50 | $10.47 | $10.20 | $10.97 |

| Total ReturnB,C,D | (2.68)% | 3.92% | 1.67% | 4.10% | (3.29)% | 4.39% |

| Ratios to Average Net AssetsE,F | | | | | | |

| Expenses before reductions | .77%G | .76% | .77% | .77% | .77% | .77% |

| Expenses net of fee waivers, if any | .77%G | .76% | .77% | .77% | .77% | .77% |

| Expenses net of all reductions | .77%G | .76% | .77% | .77% | .77% | .77% |

| Net investment income (loss) | 1.48%G | 1.28% | 1.20% | 1.34% | .99% | 1.30% |

| Supplemental Data | | | | | | |

| Net assets, end of period (in millions) | $221 | $261 | $222 | $246 | $291 | $380 |

| Portfolio turnover rateH | 182%G | 93% | 83% | 131% | 192% | 222% |

A Calculated based on average shares outstanding during the period.

B Total returns for periods of less than one year are not annualized.

C Total returns would have been lower if certain expenses had not been reduced during the applicable periods shown.

D Total returns do not include the effect of the sales charges.

E Expense ratios reflect operating expenses of the class. Expenses before reductions do not reflect amounts reimbursed by the investment adviser or reductions from expense offset arrangements and do not represent the amount paid by the class during periods when reimbursements or reductions occur. Expenses net of fee waivers reflect expenses after reimbursement by the investment adviser but prior to reductions from expense offset arrangements. Expenses net of all reductions represent the net expenses paid by the class.

F Fees and expenses of any underlying Fidelity Central Funds are not included in the Fund's expense ratio. The Fund indirectly bears its proportionate share of the expenses of any underlying Fidelity Central Funds. Based on their most recent shareholder report date, the expenses of any underlying non-money market Fidelity Central Funds were less than .005%.

G Annualized

H Amount does not include the portfolio activity of any underlying Fidelity Central Funds.

See accompanying notes which are an integral part of the financial statements.

Financial Highlights — Fidelity Government Income Fund Class T

| | Six months ended (Unaudited) February 28, | Years ended August 31, | | | | |

| | 2017 | 2016 | 2015 | 2014 | 2013 | 2012 |

| Selected Per–Share Data | | | | | | |

| Net asset value, beginning of period | $10.66 | $10.50 | $10.47 | $10.20 | $10.97 | $10.90 |

| Income from Investment Operations | | | | | | |

| Net investment income (loss)A | .076 | .135 | .127 | .140 | .107 | .143 |

| Net realized and unrealized gain (loss) | (.371) | .270 | .048 | .277 | (.454) | .327 |

| Total from investment operations | (.295) | .405 | .175 | .417 | (.347) | .470 |

| Distributions from net investment income | (.069) | (.150) | (.117) | (.140) | (.101) | (.137) |

| Distributions from net realized gain | (.076) | (.095) | (.028) | (.007) | (.322) | (.263) |

| Total distributions | (.145) | (.245) | (.145) | (.147) | (.423) | (.400) |

| Net asset value, end of period | $10.22 | $10.66 | $10.50 | $10.47 | $10.20 | $10.97 |

| Total ReturnB,C,D | (2.78)% | 3.92% | 1.68% | 4.12% | (3.27)% | 4.41% |

| Ratios to Average Net AssetsE,F | | | | | | |

| Expenses before reductions | .77%G | .76% | .76% | .76% | .75% | .75% |

| Expenses net of fee waivers, if any | .77%G | .76% | .76% | .76% | .75% | .75% |

| Expenses net of all reductions | .77%G | .76% | .76% | .76% | .75% | .75% |

| Net investment income (loss) | 1.48%G | 1.28% | 1.20% | 1.36% | 1.01% | 1.32% |

| Supplemental Data | | | | | | |

| Net assets, end of period (in millions) | $167 | $197 | $181 | $196 | $228 | $309 |

| Portfolio turnover rateH | 182%G | 93% | 83% | 131% | 192% | 222% |

A Calculated based on average shares outstanding during the period.

B Total returns for periods of less than one year are not annualized.

C Total returns would have been lower if certain expenses had not been reduced during the applicable periods shown.

D Total returns do not include the effect of the sales charges.

E Expense ratios reflect operating expenses of the class. Expenses before reductions do not reflect amounts reimbursed by the investment adviser or reductions from expense offset arrangements and do not represent the amount paid by the class during periods when reimbursements or reductions occur. Expenses net of fee waivers reflect expenses after reimbursement by the investment adviser but prior to reductions from expense offset arrangements. Expenses net of all reductions represent the net expenses paid by the class.

F Fees and expenses of any underlying Fidelity Central Funds are not included in the Fund's expense ratio. The Fund indirectly bears its proportionate share of the expenses of any underlying Fidelity Central Funds. Based on their most recent shareholder report date, the expenses of any underlying non-money market Fidelity Central Funds were less than .005%.

G Annualized

H Amount does not include the portfolio activity of any underlying Fidelity Central Funds.

See accompanying notes which are an integral part of the financial statements.

Financial Highlights — Fidelity Government Income Fund Class C

| | Six months ended (Unaudited) February 28, | Years ended August 31, | | | | |

| | 2017 | 2016 | 2015 | 2014 | 2013 | 2012 |

| Selected Per–Share Data | | | | | | |

| Net asset value, beginning of period | $10.66 | $10.50 | $10.47 | $10.20 | $10.96 | $10.90 |

| Income from Investment Operations | | | | | | |

| Net investment income (loss)A | .036 | .053 | .044 | .059 | .025 | .060 |

| Net realized and unrealized gain (loss) | (.371) | .270 | .048 | .278 | (.443) | .318 |

| Total from investment operations | (.335) | .323 | .092 | .337 | (.418) | .378 |

| Distributions from net investment income | (.029) | (.068) | (.034) | (.060) | (.020) | (.055) |

| Distributions from net realized gain | (.076) | (.095) | (.028) | (.007) | (.322) | (.263) |

| Total distributions | (.105) | (.163) | (.062) | (.067) | (.342) | (.318) |

| Net asset value, end of period | $10.22 | $10.66 | $10.50 | $10.47 | $10.20 | $10.96 |

| Total ReturnB,C,D | (3.15)% | 3.12% | .88% | 3.32% | (3.93)% | 3.53% |

| Ratios to Average Net AssetsE,F | | | | | | |

| Expenses before reductions | 1.55%G | 1.54% | 1.55% | 1.54% | 1.52% | 1.51% |

| Expenses net of fee waivers, if any | 1.55%G | 1.54% | 1.55% | 1.54% | 1.52% | 1.51% |

| Expenses net of all reductions | 1.55%G | 1.54% | 1.55% | 1.54% | 1.52% | 1.51% |

| Net investment income (loss) | .70%G | .50% | .42% | .57% | .24% | .56% |

| Supplemental Data | | | | | | |

| Net assets, end of period (in millions) | $78 | $94 | $54 | $58 | $73 | $98 |

| Portfolio turnover rateH | 182%G | 93% | 83% | 131% | 192% | 222% |

A Calculated based on average shares outstanding during the period.

B Total returns for periods of less than one year are not annualized.

C Total returns would have been lower if certain expenses had not been reduced during the applicable periods shown.

D Total returns do not include the effect of the contingent deferred sales charge.

E Expense ratios reflect operating expenses of the class. Expenses before reductions do not reflect amounts reimbursed by the investment adviser or reductions from expense offset arrangements and do not represent the amount paid by the class during periods when reimbursements or reductions occur. Expenses net of fee waivers reflect expenses after reimbursement by the investment adviser but prior to reductions from expense offset arrangements. Expenses net of all reductions represent the net expenses paid by the class.

F Fees and expenses of any underlying Fidelity Central Funds are not included in the Fund's expense ratio. The Fund indirectly bears its proportionate share of the expenses of any underlying Fidelity Central Funds. Based on their most recent shareholder report date, the expenses of any underlying non-money market Fidelity Central Funds were less than .005%.

G Annualized

H Amount does not include the portfolio activity of any underlying Fidelity Central Funds.

See accompanying notes which are an integral part of the financial statements.

Financial Highlights — Fidelity Government Income Fund

| | Six months ended (Unaudited) February 28, | Years ended August 31, | | | | |

| | 2017 | 2016 | 2015 | 2014 | 2013 | 2012 |

| Selected Per–Share Data | | | | | | |

| Net asset value, beginning of period | $10.65 | $10.48 | $10.45 | $10.18 | $10.95 | $10.88 |

| Income from Investment Operations | | | | | | |

| Net investment income (loss)A | .092 | .167 | .159 | .171 | .138 | .175 |

| Net realized and unrealized gain (loss) | (.371) | .281 | .048 | .278 | (.453) | .328 |

| Total from investment operations | (.279) | .448 | .207 | .449 | (.315) | .503 |

| Distributions from net investment income | (.085) | (.183) | (.149) | (.172) | (.133) | (.170) |

| Distributions from net realized gain | (.076) | (.095) | (.028) | (.007) | (.322) | (.263) |

| Total distributions | (.161) | (.278) | (.177) | (.179) | (.455) | (.433) |

| Net asset value, end of period | $10.21 | $10.65 | $10.48 | $10.45 | $10.18 | $10.95 |

| Total ReturnB,C | (2.63)% | 4.35% | 1.99% | 4.45% | (2.99)% | 4.73% |

| Ratios to Average Net AssetsD,E | | | | | | |

| Expenses before reductions | .45%F | .45% | .45% | .45% | .45% | .45% |

| Expenses net of fee waivers, if any | .45%F | .45% | .45% | .45% | .45% | .45% |

| Expenses net of all reductions | .45%F | .45% | .45% | .45% | .45% | .45% |

| Net investment income (loss) | 1.80%F | 1.59% | 1.51% | 1.66% | 1.31% | 1.62% |

| Supplemental Data | | | | | | |

| Net assets, end of period (in millions) | $3,479 | $3,896 | $3,489 | $3,157 | $3,412 | $4,313 |

| Portfolio turnover rateG | 182%F | 93% | 83% | 131% | 192% | 222% |

A Calculated based on average shares outstanding during the period.

B Total returns for periods of less than one year are not annualized.

C Total returns would have been lower if certain expenses had not been reduced during the applicable periods shown.

D Expense ratios reflect operating expenses of the class. Expenses before reductions do not reflect amounts reimbursed by the investment adviser or reductions from expense offset arrangements and do not represent the amount paid by the class during periods when reimbursements or reductions occur. Expenses net of fee waivers reflect expenses after reimbursement by the investment adviser but prior to reductions from expense offset arrangements. Expenses net of all reductions represent the net expenses paid by the class.

E Fees and expenses of any underlying Fidelity Central Funds are not included in the Fund's expense ratio. The Fund indirectly bears its proportionate share of the expenses of any underlying Fidelity Central Funds. Based on their most recent shareholder report date, the expenses of any underlying non-money market Fidelity Central Funds were less than .005%.

F Annualized

G Amount does not include the portfolio activity of any underlying Fidelity Central Funds.

See accompanying notes which are an integral part of the financial statements.

Financial Highlights — Fidelity Government Income Fund Class I

| | Six months ended (Unaudited) February 28, | Years ended August 31, | | | | |

| | 2017 | 2016 | 2015 | 2014 | 2013 | 2012 |

| Selected Per–Share Data | | | | | | |

| Net asset value, beginning of period | $10.66 | $10.50 | $10.47 | $10.20 | $10.97 | $10.90 |

| Income from Investment Operations | | | | | | |

| Net investment income (loss)A | .090 | .162 | .154 | .166 | .133 | .169 |

| Net realized and unrealized gain (loss) | (.361) | .271 | .048 | .277 | (.454) | .327 |

| Total from investment operations | (.271) | .433 | .202 | .443 | (.321) | .496 |

| Distributions from net investment income | (.083) | (.178) | (.144) | (.166) | (.127) | (.163) |

| Distributions from net realized gain | (.076) | (.095) | (.028) | (.007) | (.322) | (.263) |

| Total distributions | (.159) | (.273) | (.172) | (.173) | (.449) | (.426) |

| Net asset value, end of period | $10.23 | $10.66 | $10.50 | $10.47 | $10.20 | $10.97 |

| Total ReturnB,C | (2.55)% | 4.19% | 1.94% | 4.38% | (3.03)% | 4.66% |

| Ratios to Average Net AssetsD,E | | | | | | |

| Expenses before reductions | .50%F | .50% | .50% | .51% | .51% | .51% |

| Expenses net of fee waivers, if any | .50%F | .50% | .50% | .51% | .51% | .51% |

| Expenses net of all reductions | .50%F | .50% | .50% | .51% | .51% | .51% |

| Net investment income (loss) | 1.75%F | 1.54% | 1.46% | 1.61% | 1.26% | 1.56% |

| Supplemental Data | | | | | | |

| Net assets, end of period (in millions) | $472 | $494 | $412 | $298 | $296 | $334 |

| Portfolio turnover rateG | 182%F | 93% | 83% | 131% | 192% | 222% |

A Calculated based on average shares outstanding during the period.

B Total returns for periods of less than one year are not annualized.

C Total returns would have been lower if certain expenses had not been reduced during the applicable periods shown.

D Expense ratios reflect operating expenses of the class. Expenses before reductions do not reflect amounts reimbursed by the investment adviser or reductions from expense offset arrangements and do not represent the amount paid by the class during periods when reimbursements or reductions occur. Expenses net of fee waivers reflect expenses after reimbursement by the investment adviser but prior to reductions from expense offset arrangements. Expenses net of all reductions represent the net expenses paid by the class.

E Fees and expenses of any underlying Fidelity Central Funds are not included in the Fund's expense ratio. The Fund indirectly bears its proportionate share of the expenses of any underlying Fidelity Central Funds. Based on their most recent shareholder report date, the expenses of any underlying non-money market Fidelity Central Funds were less than .005%.

F Annualized

G Amount does not include the portfolio activity of any underlying Fidelity Central Funds.

See accompanying notes which are an integral part of the financial statements.

Notes to Financial Statements (Unaudited)

For the period ended February 28, 2017

(Amounts in thousands except percentages)

1. Organization.

Fidelity Government Income Fund (the Fund) is a fund of Fidelity Income Fund (the Trust) and is authorized to issue an unlimited number of shares. The Trust is registered under the Investment Company Act of 1940, as amended (the 1940 Act), as an open-end management investment company organized as a Massachusetts business trust. The Fund offers Class A, Class T, Class C, Government Income and Class I shares, each of which has equal rights as to assets and voting privileges. Each class has exclusive voting rights with respect to matters that affect that class.

After the close of business on June 24, 2016, all outstanding Class B shares were converted to Class A shares. All prior fiscal period dollar and share amounts for Class B presented in the Notes to Financial Statements are for the period September 1, 2015 through June 24, 2016.

In March 2017, the Board of Trustees approved a change in the name of Class T to Class M effective after the close of business on March 24, 2017.

2. Investments in Fidelity Central Funds.

The Fund invests in Fidelity Central Funds, which are open-end investment companies generally available only to other investment companies and accounts managed by the investment adviser and its affiliates. The Fund's Schedule of Investments lists each of the Fidelity Central Funds held as of period end, if any, as an investment of the Fund, but does not include the underlying holdings of each Fidelity Central Fund. As an Investing Fund, the Fund indirectly bears its proportionate share of the expenses of the underlying Fidelity Central Funds.

Based on its investment objective, each Fidelity Central Fund may invest or participate in various investment vehicles or strategies that are similar to those of the Fund. These strategies are consistent with the investment objectives of the Fund and may involve certain economic risks which may cause a decline in value of each of the Fidelity Central Funds and thus a decline in the value of the Fund. The Money Market Central Funds seek preservation of capital and current income and are managed by Fidelity Investments Money Management, Inc. (FIMM), an affiliate of the investment adviser. Annualized expenses of the Money Market Central Funds as of their most recent shareholder report date are less than .005%. The following summarizes the Fund's investment in each non-money market Fidelity Central Fund.

| Fidelity Central Fund | Investment Manager | Investment Objective | Investment Practices | Expense Ratio(a) |

| Fidelity Mortgage Backed Securities Central Fund | FIMM | Seeks a high level of income by normally investing in investment-grade mortgage-related securities and repurchase agreements for those securities. | Delayed Delivery & When Issued Securities

Futures

Swap Agreements

| Less than .005% |

(a) Expenses expressed as a percentage of average net assets and are as of each underlying Central Fund's most recent annual or semi-annual shareholder report.

An unaudited holdings listing for the Fund, which presents direct holdings as well as the pro-rata share of any securities and other investments held indirectly through its investment in underlying non-money market Fidelity Central Funds, is available at fidelity.com and/or institutional.fidelity.com. A complete unaudited list of holdings for each Fidelity Central Fund is available upon request or at the Securities and Exchange Commission (the SEC) website at www.sec.gov. In addition, the financial statements of the Fidelity Central Funds which contain the significant accounting policies (including investment valuation policies) of those funds are available on the SEC website or upon request.

3. Significant Accounting Policies.

The financial statements have been prepared in conformity with accounting principles generally accepted in the United States of America (GAAP), which require management to make certain estimates and assumptions at the date of the financial statements. Actual results could differ from those estimates. Subsequent events, if any, through the date that the financial statements were issued have been evaluated in the preparation of the financial statements. The following summarizes the significant accounting policies of the Fund:

Investment Valuation. Investments are valued as of 4:00 p.m. Eastern time on the last calendar day of the period. The Board of Trustees (the Board) has delegated the day to day responsibility for the valuation of the Fund's investments to the Fair Value Committee (the Committee) established by the Fund's investment adviser. In accordance with valuation policies and procedures approved by the Board, the Fund attempts to obtain prices from one or more third party pricing vendors or brokers to value its investments. When current market prices, quotations or currency exchange rates are not readily available or reliable, investments will be fair valued in good faith by the Committee, in accordance with procedures adopted by the Board. Factors used in determining fair value vary by investment type and may include market or investment specific events, changes in interest rates and credit quality. The frequency with which these procedures are used cannot be predicted and they may be utilized to a significant extent. The Committee oversees the Fund's valuation policies and procedures and reports to the Board on the Committee's activities and fair value determinations. The Board monitors the appropriateness of the procedures used in valuing the Fund's investments and ratifies the fair value determinations of the Committee.

The Fund categorizes the inputs to valuation techniques used to value its investments into a disclosure hierarchy consisting of three levels as shown below:

- Level 1 – quoted prices in active markets for identical investments

- Level 2 – other significant observable inputs (including quoted prices for similar investments, interest rates, prepayment speeds, etc.)

- Level 3 – unobservable inputs (including the Fund's own assumptions based on the best information available)

Valuation techniques used to value the Fund's investments by major category are as follows:

Debt securities, including restricted securities, are valued based on evaluated prices received from third party pricing vendors or from brokers who make markets in such securities. Foreign government and government agency obligations and U.S. government and government agency obligations are valued by pricing vendors who utilize matrix pricing which considers yield or price of bonds of comparable quality, coupon, maturity and type or by broker-supplied prices. Collateralized mortgage obligations, commercial mortgage securities and U.S. government agency mortgage securities are valued by pricing vendors who utilize matrix pricing which considers prepayment speed assumptions, attributes of the collateral, yield or price of bonds of comparable quality, coupon, maturity and type or by broker-supplied prices. Swaps are marked-to-market daily based on valuations from third party pricing vendors, registered derivatives clearing organizations (clearinghouses) or broker-supplied valuations. These pricing sources may utilize inputs such as interest rate curves, credit spread curves, default possibilities and recovery rates. When independent prices are unavailable or unreliable, debt securities and swaps may be valued utilizing pricing methodologies which consider similar factors that would be used by third party pricing vendors. Debt securities and swaps are generally categorized as Level 2 in the hierarchy but may be Level 3 depending on the circumstances.

Futures contracts are valued at the settlement price established each day by the board of trade or exchange on which they are traded and are categorized as Level 1 in the hierarchy. Investments in open-end mutual funds, including the Fidelity Central Funds, are valued at their closing net asset value (NAV) each business day and are categorized as Level 1 in the hierarchy.

Changes in valuation techniques may result in transfers in or out of an assigned level within the disclosure hierarchy. The aggregate value of investments by input level as of February 28, 2017 is included at the end of the Fund's Schedule of Investments.

Investment Transactions and Income. For financial reporting purposes, the Fund's investment holdings and NAV include trades executed through the end of the last business day of the period. The NAV per share for processing shareholder transactions is calculated as of the close of business of the New York Stock Exchange (NYSE), normally 4:00 p.m. Eastern time and includes trades executed through the end of the prior business day. Gains and losses on securities sold are determined on the basis of identified cost. Income and capital gain distributions from Fidelity Central Funds, if any, are recorded on the ex-dividend date. Interest income is accrued as earned and includes coupon interest and amortization of premium and accretion of discount on debt securities as applicable. The principal amount on inflation-indexed securities is periodically adjusted to the rate of inflation and interest is accrued based on the principal amount. The adjustments to principal due to inflation are reflected as increases or decreases to Interest in the accompanying Statement of Operations.

Class Allocations and Expenses. Investment income, realized and unrealized capital gains and losses, common expenses of the Fund, and certain fund-level expense reductions, if any, are allocated daily on a pro-rata basis to each class based on the relative net assets of each class to the total net assets of the Fund. Each class differs with respect to transfer agent and distribution and service plan fees incurred. Certain expense reductions may also differ by class. For the reporting period, the allocated portion of income and expenses to each class as a percent of its average net assets may vary due to the timing of recording these transactions in relation to fluctuating net assets of the classes. Expenses directly attributable to a fund are charged to that fund. Expenses attributable to more than one fund are allocated among the respective funds on the basis of relative net assets or other appropriate methods. Expense estimates are accrued in the period to which they relate and adjustments are made when actual amounts are known.

Deferred Trustee Compensation. Under a Deferred Compensation Plan (the Plan), independent Trustees may elect to defer receipt of a portion of their annual compensation. Deferred amounts are invested in a cross-section of Fidelity funds, are marked-to-market and remain in the Fund until distributed in accordance with the Plan. The investment of deferred amounts and the offsetting payable to the Trustees are included in the accompanying Statement of Assets and Liabilities.

Income Tax Information and Distributions to Shareholders. Each year, the Fund intends to qualify as a regulated investment company under Subchapter M of the Internal Revenue Code, including distributing substantially all of its taxable income and realized gains. As a result, no provision for U.S. Federal income taxes is required. The Fund files a U.S. federal tax return, in addition to state and local tax returns as required. The Fund's federal income tax returns are subject to examination by the Internal Revenue Service (IRS) for a period of three fiscal years after they are filed. State and local tax returns may be subject to examination for an additional fiscal year depending on the jurisdiction.

Dividends are declared and recorded daily and paid monthly from net investment income. Distributions from realized gains, if any, are declared and recorded on the ex-dividend date. Income dividends and capital gain distributions are declared separately for each class. Income and capital gain distributions are determined in accordance with income tax regulations, which may differ from GAAP.

Capital accounts within the financial statements are adjusted for permanent book-tax differences. These adjustments have no impact on net assets or the results of operations. Capital accounts are not adjusted for temporary book-tax differences which will reverse in a subsequent period.

Book-tax differences are primarily due to futures contracts, swaps, market discount, partnerships (including allocations from Fidelity Central Funds), deferred trustees compensation and losses deferred due to wash sales.

The federal tax cost of investment securities and unrealized appreciation (depreciation) as of period end were as follows:

| Gross unrealized appreciation | $38,179 |

| Gross unrealized depreciation | (60,556) |

| Net unrealized appreciation (depreciation) on securities | $(22,377) |

| Tax cost | $4,453,027 |

To-Be-Announced (TBA) Securities and Mortgage Dollar Rolls. During the period, the Fund transacted in TBA securities that involved buying or selling mortgage-backed securities (MBS) on a forward commitment basis. A TBA transaction typically does not designate the actual security to be delivered and only includes an approximate principal amount; however delivered securities must meet specified terms defined by industry guidelines, including issuer, rate and current principal amount outstanding on underlying mortgage pools. The Fund may enter into a TBA transaction with the intent to take possession of or deliver the underlying MBS, or the Fund may elect to extend the settlement by entering into either a mortgage or reverse mortgage dollar roll. Mortgage dollar rolls are transactions where a fund sells TBA securities and simultaneously agrees to repurchase MBS on a later date at a lower price and with the same counterparty. Reverse mortgage dollar rolls involve the purchase and simultaneous agreement to sell TBA securities on a later date at a lower price. Transactions in mortgage dollar rolls and reverse mortgage dollar rolls are accounted for as purchases and sales and may result in an increase to the Fund's portfolio turnover rate.

Purchases and sales of TBA securities involve risks similar to those discussed above for delayed delivery and when-issued securities. Also, if the counterparty in a mortgage dollar roll or a reverse mortgage dollar roll transaction files for bankruptcy or becomes insolvent, the Fund's right to repurchase or sell securities may be limited. Additionally, when a fund sells TBA securities without already owning or having the right to obtain the deliverable securities (an uncovered forward commitment to sell), it incurs a risk of loss because it could have to purchase the securities at a price that is higher than the price at which it sold them. A fund may be unable to purchase the deliverable securities if the corresponding market is illiquid.

TBA securities subject to a forward commitment to sell at period end are included at the end of the Fund's Schedule of Investments under the caption "TBA Sale Commitments." The proceeds and value of these commitments are reflected in the Fund's Statement of Assets and Liabilities as Receivable for TBA sale commitments and TBA sale commitments, at value, respectively.

4. Derivative Instruments.

Risk Exposures and the Use of Derivative Instruments. The Fund's investment objective allows the Fund to enter into various types of derivative contracts, including futures contracts and swaps. Derivatives are investments whose value is primarily derived from underlying assets, indices or reference rates and may be transacted on an exchange or over-the-counter (OTC). Derivatives may involve a future commitment to buy or sell a specified asset based on specified terms, to exchange future cash flows at periodic intervals based on a notional principal amount, or for one party to make one or more payments upon the occurrence of specified events in exchange for periodic payments from the other party.

The Fund used derivatives to increase returns, to gain exposure to certain types of assets and to manage exposure to certain risks as defined below. The success of any strategy involving derivatives depends on analysis of numerous economic factors, and if the strategies for investment do not work as intended, the Fund may not achieve its objectives.

The Fund's use of derivatives increased or decreased its exposure to the following risk:

| Interest Rate Risk | Interest rate risk relates to the fluctuations in the value of interest-bearing securities due to changes in the prevailing levels of market interest rates. |

The Fund is also exposed to additional risks from investing in derivatives, such as liquidity risk and counterparty credit risk. Liquidity risk is the risk that the Fund will be unable to close out the derivative in the open market in a timely manner. Counterparty credit risk is the risk that the counterparty will not be able to fulfill its obligation to the Fund. Counterparty credit risk related to exchange-traded futures contracts may be mitigated by the protection provided by the exchange on which they trade. Counterparty credit risk related to centrally cleared OTC swaps may be mitigated by the protection provided by the clearinghouse.

Investing in derivatives may involve greater risks than investing in the underlying assets directly and, to varying degrees, may involve risk of loss in excess of any initial investment and collateral received and amounts recognized in the Statement of Assets and Liabilities. In addition, there may be the risk that the change in value of the derivative contract does not correspond to the change in value of the underlying instrument.

Net Realized Gain (Loss) and Change in Net Unrealized Appreciation (Depreciation) on Derivatives. The table below, which reflects the impacts of derivatives on the financial performance of the Fund, summarizes the net realized gain (loss) and change in net unrealized appreciation (depreciation) for derivatives during the period as presented in the Statement of Operations.

| Primary Risk Exposure / Derivative Type | Net Realized Gain (Loss) | Change in Net Unrealized Appreciation (Depreciation) |

| Interest Rate Risk | | |

| Futures Contracts | $(3,788) | $1,021 |

| Swaps | (1,749) | (313) |

| Totals | $(5,537) | $708 |

A summary of the value of derivatives by primary risk exposure as of period end is included at the end of the Schedule of Investments.

Futures Contracts. A futures contract is an agreement between two parties to buy or sell a specified underlying instrument for a fixed price at a specified future date. The Fund used futures contracts to manage its exposure to the bond market and fluctuations in interest rates.

Upon entering into a futures contract, a fund is required to deposit either cash or securities (initial margin) with a clearing broker in an amount equal to a certain percentage of the face value of the contract. Futures contracts are marked-to-market daily and subsequent daily payments (variation margin) are made or received by a fund depending on the daily fluctuations in the value of the futures contracts and are recorded as unrealized appreciation or (depreciation). This receivable and/or payable, if any, is included in daily variation margin for derivative instruments in the Statement of Assets and Liabilities. Realized gain or (loss) is recorded upon the expiration or closing of a futures contract.

Any open futures contracts at period end are presented in the Schedule of Investments under the caption "Futures Contracts". The underlying face amount at value reflects each contract's exposure to the underlying instrument or index at period end and is representative of volume of activity during the period. Securities deposited to meet initial margin requirements are identified in the Schedule of Investments.

Swaps. A swap is a contract between two parties to exchange future cash flows at periodic intervals based on a notional principal amount. A centrally cleared OTC swap is a transaction executed between a fund and a dealer counterparty, then cleared by a futures commission merchant (FCM) through a clearinghouse. Once cleared, the clearinghouse serves as a central counterparty, with whom a fund exchanges cash flows for the life of the transaction, similar to transactions in futures contracts.

Centrally cleared OTC swaps require a fund to deposit either cash or securities (initial margin) with the FCM, at the instruction of and for the benefit of the clearinghouse. Securities deposited to meet initial margin requirements are identified in the Schedule of Investments. Centrally cleared OTC swaps are marked-to-market daily and subsequent payments (variation margin) are made or received depending on the daily fluctuations in the value of the swaps and are recorded as unrealized appreciation or (depreciation). These daily payments, if any, are included in receivable or payable for daily variation margin for derivative instruments in the Statement of Assets and Liabilities. Any premiums for centrally cleared OTC swaps are recorded periodically throughout the term of the swap to variation margin and included in unrealized appreciation (depreciation) in the Statement of Assets and Liabilities. Any premiums are recognized as realized gain (loss) upon termination or maturity of the swap.

Payments are exchanged at specified intervals, accrued daily commencing with the effective date of the contract and recorded as realized gain or (loss). Some swaps may be terminated prior to the effective date and realize a gain or loss upon termination. The net realized gain (loss) and change in net unrealized appreciation (depreciation) on swaps during the period is included in the Statement of Operations.

Any open swaps at period end are included in the Schedule of Investments under the caption "Swaps" and are representative of volume of activity during the period.

Interest Rate Swaps. Interest rate swaps are agreements between counterparties to exchange cash flows, one based on a fixed rate, and the other on a floating rate. The Fund entered into interest rate swaps to manage its exposure to interest rate changes. Changes in interest rates can have an effect on both the value of bond holdings as well as the amount of interest income earned. In general, the value of bonds can fall when interest rates rise and can rise when interest rates fall.

5. Purchases and Sales of Investments.

Purchases and sales of securities (including the Fixed-Income Central Funds), other than short-term securities and U.S. government securities, aggregated $52,705 and $207,900, respectively.

6. Fees and Other Transactions with Affiliates.

Management Fee and Expense Contract. Fidelity Management & Research Company (the investment adviser) and its affiliates provide the Fund with investment management related services for which the Fund pays a monthly management fee. The management fee is the sum of an individual fund fee rate that is based on an annual rate of .20% of the Fund's average net assets and an annualized group fee rate that averaged .11% during the period. The group fee rate is based upon the average net assets of all the mutual funds advised by the investment adviser, including any mutual funds previously advised by the investment adviser that are currently advised by Fidelity SelectCo, LLC, an affiliate of the investment adviser. The group fee rate decreases as assets under management increase and increases as assets under management decrease. For the reporting period, the total annualized management fee rate was .31% of the Fund's average net assets.

In addition, under the expense contract, the investment adviser pays class-level expenses for Government Income, so that the total expenses, except the compensation of the independent Trustees and certain other expenses such as interest expense, including commitment fees do not exceed .45% of the Class' average net assets. This agreement does not apply to any of the other classes and any change or modification that would increase expenses can only be made with shareholder approval.

Distribution and Service Plan Fees. In accordance with Rule 12b-1 of the 1940 Act, the Fund has adopted separate Distribution and Service Plans for each class of shares. Certain classes pay Fidelity Distributors Corporation (FDC), an affiliate of the investment adviser, separate Distribution and Service Fees, each of which is based on an annual percentage of each class' average net assets. In addition, FDC may pay financial intermediaries for selling shares of the Fund and providing shareholder support services. For the period, the Distribution and Service Fee rates, total fees and amounts retained by FDC were as follows:

| | Distribution

Fee | Service

Fee | Total Fees | Retained

by FDC |

| Class A | -% | .25% | $305 | $5 |

| Class T | -% | .25% | 223 | 113 |

| Class C | .75% | .25% | 437 | 104 |

| | | | $965 | $222 |

Sales Load. FDC may receive a front-end sales charge of up to 4.00% for selling Class A shares and Class T shares, some of which is paid to financial intermediaries for selling shares of the Fund. Depending on the holding period, FDC may receive contingent deferred sales charges levied on Class A, Class T, and Class C redemptions. The deferred sales charges are 1.00% for Class C shares, .75% for certain purchases of Class A shares and .25% for certain purchases of Class T shares.

For the period, sales charge amounts retained by FDC were as follows:

| | Retained

by FDC |

| Class A | $13 |

| Class T | 2 |

| Class C(a) | 7 |

| | $22 |

(a) When Class C shares are initially sold, FDC pays commissions from its own resources to financial intermediaries through which the sales are made.

Transfer Agent Fees. Fidelity Investments Institutional Operations Company, Inc., (FIIOC), an affiliate of the investment adviser, is the transfer, dividend disbursing and shareholder servicing agent for each class of the Fund. FIIOC receives account fees and asset-based fees that vary according to the account size and type of account of the shareholders of each respective class of the Fund, with the exception of Government Income. FIIOC receives an asset-based fee of .10% of Government Income's average net assets. FIIOC pays for typesetting, printing and mailing of shareholder reports, except proxy statements. For the period, transfer agent fees for each class were as follows:

| | Amount | % of

Class-Level Average

Net Assets(a) |

| Class A | $199 | .16 |

| Class T | 144 | .16 |

| Class C | 81 | .19 |

| Government Income | 1,847 | .10 |

| Class I | 344 | .14 |

| | $2,615 | |

(a) Annualized

Fund Wide Operations Fee. Pursuant to the Fund Wide Operations and Expense Agreement (FWOE), the investment adviser has agreed to provide for fund level expenses (which do not include transfer agent, Rule 12b-1 fees, compensation of the independent Trustees, interest (including commitment fees), taxes or extraordinary expenses, if any) in return for a FWOE fee equal to .35% of the Fund's average net assets less the total amount of the management fee. The FWOE paid by the Fund is reduced by an amount equal to the fees and expenses paid to the independent Trustees. For the period, the FWOE fee was equivalent to an annualized rate of .04% of average net assets.

Interfund Trades. The Fund may purchase from or sell securities to other Fidelity Funds under procedures adopted by the Board. The procedures have been designed to ensure these interfund trades are executed in accordance with Rule 17a-7 of the 1940 Act. Interfund trades are included within the respective purchases and sales amounts shown in the Purchases and Sales of Investments note.

7. Committed Line of Credit.