We are continually identifying and evaluating acquisition opportunities, including acquisitions that would be significantly larger than those we have consummated to date. However, competition for producing oil and gas properties is intense and many of our competitors have financial and other resources substantially greater than those available to us. We cannot ensure that we will successfully consummate any acquisition, that we will be able to acquire producing oil and gas properties that contain economically recoverable reserves or that any acquisition will be profitably integrated into our operations.

We make, and will continue to make, substantial capital expenditures to find, acquire, develop, exploit and produce oil and natural gas reserves. Our capital expenditures for oil and gas properties were $170 million for 2005, and we have budgeted total capital expenditures of $208 million in 2006. If oil and gas prices decrease or we encounter operating difficulties that result in our cash flow from operations being less than expected, we may have to reduce the capital we can spend unless we raise additional funds through debt or equity financing. Debt or equity financing, cash generated by operations or borrowing capacity may not be available to us in sufficient amounts or on acceptable terms to meet these requirements.

Future cash flows and the availability of financing will be subject to a number of variables, such as:

Issuing equity securities to satisfy our financing requirements could cause substantial dilution to existing shareholders. Debt financing could lead to us being more vulnerable to competitive pressures and economic downturns.

If our revenues were to decrease due to lower oil and natural gas prices, decreased production or other reasons, and if we could not obtain capital through our credit facility or otherwise, our ability to execute our development plans, replace our reserves or maintain production levels could be greatly limited.

Oil and gas drilling and production activities are subject to numerous risks, including the risk that no commercially productive natural gas or oil reserves will be found. The costs of drilling, completing and operating wells are often uncertain, and drilling operations may be curtailed, delayed or canceled as a result of a variety of factors, many of which are beyond our control. These factors include:

The prevailing prices of oil and gas also affect the cost of and the demand for drilling rigs, production equipment and related services. The availability of drilling rigs can vary significantly from region to region at any particular time. Although land drilling rigs can be moved from one region to another in response to changes in levels of demand, an undersupply of rigs in any region may result in drilling delays and higher drilling costs for the rigs that are available in that region.

Another significant risk inherent in our drilling plans is the need to obtain drilling permits from state, local and other governmental authorities. Delays in obtaining regulatory approvals and drilling permits, including delays which jeopardize our ability to realize the potential benefits from leased properties within the applicable lease periods, the failure to obtain a drilling permit for a well or the receipt of a permit with unreasonable conditions or costs could have a material adverse effect on our ability to explore on or develop our properties.

The wells we drill may not be productive and we may not recover all or any portion of our investment in such wells. The seismic data and other technologies we use do not allow us to know conclusively prior to drilling a well that natural gas or oil is present or may be produced economically. The cost of drilling, completing and operating a well is often uncertain, and cost factors can adversely affect the economics of a project. Drilling activities can result in dry wells or wells that are productive but do not produce sufficient net revenues after operating and other costs to cover initial drilling costs.

Our future drilling activities may not be successful, nor can we be sure that our overall drilling success rate or our drilling success rate for activity within a particular area will not decline. Unsuccessful drilling activities could have a material adverse effect on our results of operations and financial condition. Also, we may not be able to obtain any options or lease rights in potential drilling locations that we identify. Although we have identified numerous potential drilling locations, we may not be able to economically produce oil or natural gas from all of them.

| Our business involves many operating risks that may result in substantial losses for which insurance may be unavailable or inadequate. |

Our operations are subject to all of the risks and hazards typically associated with the exploitation, development and exploration for, and the production and transportation of oil and natural gas. These operating risks include:

| • | fires, explosions, blowouts, cratering and casing collapses; |

| • | formations with abnormal pressures; |

| • | pipeline ruptures or spills; |

| • | uncontrollable flows of oil, natural gas or well fluids; |

| • | environmental hazards such as natural gas leaks, oil spills and discharges of toxic gases; and |

| • | natural disasters. |

Any of these risks could result in substantial losses resulting from injury or loss of life, damage to or destruction of property, natural resources and equipment, pollution and other environmental damages, clean-up responsibilities, regulatory investigations and penalties and suspension of operations. In addition, under certain circumstances, we may be liable for environmental damage caused by previous owners or operators of properties that we own, lease or operate. As a result, we may incur substantial liabilities to third parties or governmental entities, which could reduce or eliminate funds available for exploration, development or acquisitions or cause us to incur losses.

In accordance with industry practice, we maintain insurance against some, but not all, of the risks described above. We cannot assure you that our insurance will be adequate to cover losses or liabilities. Also, we cannot predict the continued availability of insurance at premium levels that justify its purchase. No assurance can be given that we will be able to maintain insurance in the future at rates we consider reasonable. The occurrence of a significant event, not fully insured or indemnified against, could have a material adverse affect on our financial condition and operations.

Our business depends on transportation facilities owned by others.

We deliver substantially all of our oil and natural gas production through pipelines that we do not own. The marketability of our production depends upon the availability, proximity and capacity of these pipelines as well as gathering systems and processing facilities. The unavailability of or lack of available capacity on these systems and facilities could result in the shut-in of producing wells or the delay or discontinuance of development plans for properties. Federal, state and local regulation of oil and natural gas production and transportation, tax and energy policies, changes in supply and demand, pipeline pressures, damage to or destruction of pipelines and general economic conditions could adversely affect our ability to produce, gather and market our oil and natural gas.

Competition for experienced, technical personnel may negatively impact our operations.

Our exploratory and development drilling success will depend, in part, on our ability to attract and retain experienced professional personnel. The loss of any key executives or other key personnel could have a material adverse effect on our operations. Our future profitability will depend, at least in part, on our ability to attract and retain qualified personnel, particularly individuals with a strong background in geology, geophysics, engineering and operations.

18

Estimates of oil and natural gas reserves are not precise.

This Form 10-K contains estimates of our proved oil and gas reserves and the estimated future net cash flows from such reserves. These estimates are based upon various assumptions, including assumptions required by the SEC relating to oil and natural gas prices, drilling and operating expenses, capital expenditures, taxes and availability of funds. The process of estimating oil and natural gas reserves is complex. This process requires significant decisions and assumptions in the evaluation of available geological, geophysical, engineering and economic data for each reservoir. These estimates are dependent on many variables and, therefore, changes often occur as these variables evolve and commodity prices fluctuate.

Actual future production, oil and gas prices, revenues, taxes, development expenditures, operating expenses and quantities of recoverable oil and gas reserves will most likely vary from those estimated. Any significant variance could materially affect the estimated quantities and present value of reserves disclosed by us. In addition, we may adjust estimates of proved reserves to reflect production history, results of exploration and development, prevailing oil and gas prices and other factors, many of which are beyond our control.

At December 31, 2005, approximately 26 percent of our estimated proved reserves were proved undeveloped. Estimation of proved undeveloped reserves and proved developed non-producing reserves is based on volumetric calculations and adjacent reserve performance data. Recovery of proved undeveloped reserves requires significant capital expenditures and successful drilling operations. Production revenues from proved developed non-producing reserves will not be realized until some time in the future. The reserve data assumes that we will make significant capital expenditures to develop our reserves. Although we have prepared estimates of our reserves and the costs associated with these reserves in accordance with industry standards, these estimated costs may not be accurate, development may not occur as scheduled and actual results may not occur as estimated.

You should not assume that the present value of estimated future net cash flow referred to herein is the current fair value of our estimated oil and gas reserves. In accordance with SEC requirements, we base the estimated discounted future net cash flows from our proved reserves on prices and costs on the date of the estimate. Actual current and future prices and costs may be materially higher or lower than the prices and costs as of the date of the estimate. As a result, net present value estimates using actual prices and costs may be significantly less than the SEC estimate that is provided herein. In addition, the 10 percent discount factor, which is required by the SEC to be used in calculating discounted future net cash flows for reporting purposes, is not necessarily the most accurate discount factor for us.

We have limited control over the activities on properties we do not operate.

Other companies operate a portion of our net production. In 2005, other companies operated approximately 30 percent of our net production. Our success in properties operated by others will depend upon a number of factors outside of our control, including timing and amount of capital expenditures, the operator’s expertise and financial resources, approval of other participants in drilling wells, selection of technology and maintenance of safety and environmental standards. We have limited ability to influence or control the operation or future development of these non-operated properties or the amount of capital expenditures that we are required to fund for their operation. Our dependence on the operator and other working interest owners for these projects and our limited ability to influence or control the operation and future development of these properties could have a material adverse effect on the realization of our targeted returns or lead to unexpected future costs.

Our producing property acquisitions carry significant risks.

Acquisition of producing oil and gas properties is a key element of maintaining and growing reserves and production. Competition for these assets has been and will continue to be intense. The success of any acquisition will depend on a number of factors, many of which are beyond our control. These factors include the purchase price, future oil and gas prices, the ability to reasonably estimate or assess the recoverable volumes of reserves, rates of future production and future net revenues attainable from reserves, future operating and capital costs, results of future exploration, exploitation and development activities on the acquired properties and future abandonment and possible future environmental or other liabilities. There are numerous uncertainties inherent in estimating quantities of proved oil and gas reserves, actual future production rates and associated costs and potential liabilities with respect to prospective acquisition targets. Actual results may vary substantially from those assumed in the estimates. A customary review of subject properties will not necessarily reveal all existing or potential problems.

Additionally, significant acquisitions can change the nature of our operations and business depending upon the character of the acquired properties if they have substantially different operating and geological characteristics or are in different geographic locations than our existing properties. To the extent that acquired properties are substantially different than our existing properties, our ability to efficiently realize the expected economic benefits of such transactions may be limited.

19

Integrating acquired businesses and properties involves a number of special risks. These risks include the possibility that management may be distracted from regular business concerns by the need to integrate operations and systems and that unforeseen difficulties can arise in integrating operations and systems and in retaining and assimilating employees. Any of these or other similar risks could lead to potential adverse short-term or long-term effects on our operating results, and may cause us to not be able to realize any or all of the anticipated benefits of the acquisitions.

Responses to recent coal mining accidents could have an adverse effect on our operations.

Our conventional and CBM drilling operations in Appalachia take place in close proximity to coal mining operations. Recent coal mining disasters in West Virginia and Kentucky have received state and national attention that is resulting in increased scrutiny of current safety practices and procedures at and around coal mining operations. This scrutiny could result in the promulgation of more stringent regulations for the permitting of oil and gas wells in close proximity to coal mining operations, which could make it more difficult, time consuming and costly for us to obtain such permits and could adversely affect our natural gas production and reduce our oil and natural gas revenues.

Hedging transactions may limit our potential gains and involve other risks.

In order to manage our exposure to price risks in the marketing of our oil and natural gas, we periodically enter into oil and gas price hedging arrangements with respect to a portion of our expected production. Our hedges are limited in duration, usually for periods of two years or less. While intended to reduce the effects of volatile oil and natural gas prices, such transactions may limit our potential gains if oil or natural gas prices were to rise over the price established by the hedging arrangements. In trying to maintain an appropriate balance, we may end up hedging too much or too little, depending upon how oil or natural gas prices fluctuate in the future. We cannot assure you that our hedging transactions will reduce the risk or minimize the effect of any decline in oil or natural gas prices.

In addition, hedging transactions may expose us to the risk of financial loss in certain circumstances, including instances in which:

| • | our production is less than expected; |

| • | there is a widening of price basis differentials between delivery points for our production and the delivery point assumed in the hedge arrangement; |

| • | the counterparties to our futures contracts fail to perform under the contracts; or |

| • | a sudden, unexpected event materially impacts oil or natural gas prices. |

We account for our derivative transactions pursuant to Statement of Financial Accounting Standards (“SFAS”) No. 133, Accounting for Derivative Instruments and Hedging Activities, which requires us to record each hedging transaction as an asset or liability measured at its fair value. We must also measure the effectiveness of our hedging position in relation to the underlying commodity being hedged, and we will be required to record the ineffective portion of the hedge in our net income for that period. This accounting treatment could result in significant fluctuations in net income and shareholders’ equity from period to period.

In addition, hedging transactions using derivative instruments involve basis risk. Basis risk in a hedging contract occurs when the index upon which the contract is based is more or less variable than the index upon which the hedged asset is based, thereby making the hedge less effective. For example, a NYMEX index used for hedging certain volumes of production may have more or less variability than the regional price index used for the sale of that production.

| We are subject to complex laws and regulations that can adversely affect the cost, manner or feasibility of doing business. |

Exploration, development, production and sale of oil and gas are subject to extensive federal, state and local laws and regulations, including complex environmental laws. Future laws or regulations, any adverse changes in the interpretation of existing laws and regulations, inability to obtain necessary regulatory approvals or a failure to comply with existing legal requirements may harm our business, results of operations and financial condition. We may be required to make large expenditures to comply with environmental and other governmental regulations. Failure to comply with these laws and regulations may result in the suspension or termination of operations and subject us to administrative, civil and criminal penalties. Matters subject to regulation include discharge permits for drilling operations, drilling bonds, spacing of wells, unitization and pooling of properties, environmental protection and taxation. Our operations create the risk of environmental

20

liabilities to the government or third parties for any unlawful discharge of oil, gas or other pollutants into the air, soil or water. In the event of environmental violations, we may be charged with remedial costs. Laws and regulations protecting the environment have become more stringent in recent years, and may, in some circumstances, result in liability for environmental damage regardless of negligence or fault. In addition, pollution and similar environmental risks generally are not fully insurable. These liabilities and costs could have a material adverse effect on our financial condition and results of operations. See Item 1, “Business—Regulation—Oil and Gas—Environmental Matters.”

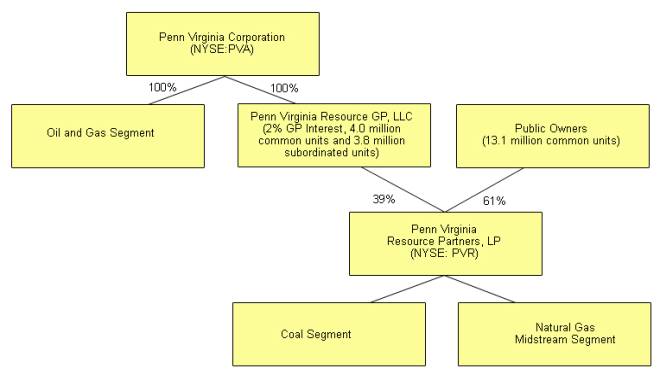

Risks Related to our Ownership in PVR

| We rely upon distributions from the Partnership, and the amount of cash that the Partnership will be able to distribute to its unitholders principally depends upon the amount of cash it can generate from its coal and natural gas midstream businesses. |

We received $21.2 million of distributions from the Partnership in 2005. A significant decline in the Partnership’s earnings or cash distributions would have a negative impact on us. The amount of cash that the Partnership will be able to distribute each quarter to its unitholders, including us, principally depends upon the amount of cash it can generate from its coal and midstream businesses. The amount of cash that the Partnership will generate will fluctuate from quarter to quarter based on, among other things:

| • | the amount of coal its lessees are able to produce; |

| • | the price at which its lessees are able to sell the coal; |

| • | the lessees’ timely receipt of payment from their customers; |

| • | the amount of natural gas transported in its gathering systems; |

| • | the amount of throughput in its processing plants; |

| • | the price of natural gas; |

| • | the price of NGLs; |

| • | the relationship between natural gas and NGL prices; |

| • | the fees it charges and the margins it realizes for its midstream services; and |

| • | its hedging activities. |

In addition, the actual amount of cash that the Partnership will have available for distribution will depend on other factors, some of which are beyond its control, including:

| • | the level of capital expenditures it makes; |

| • | the cost of acquisitions, if any; |

| • | its debt service requirements; |

| • | fluctuations in its working capital needs; |

| • | restrictions on distributions contained in its debt agreements; |

| • | prevailing economic conditions; and |

| • | the amount of cash reserves established by its general partner in its sole discretion for the proper conduct of its business. |

Because of these factors, the Partnership may not have sufficient available cash each quarter to pay its current declared quarterly distribution of $0.70 per unit or any other amount. You should also be aware that the amount of cash that the Partnership will have available for distribution depends primarily upon its cash flow, including cash flow from financial reserves and working capital borrowings, and is not solely a function of profitability, which will be affected by non-cash items. As a result, the Partnership may make cash distributions during periods when it records losses and may not make cash distributions during periods when it records profits.

Risks Related to PVR’s Coal Business

| If the Partnership’s lessees do not manage their operations well, their production volumes and the Partnership’s coal royalty revenues could decrease. |

The Partnership depends on its lessees to effectively manage their operations on its properties. The Partnership’s lessees make their own business decisions with respect to their operations, including decisions relating to:

| • | the method of mining; |

| • | credit review of their customers; |

21

| • | marketing of the coal mined; |

| • | coal transportation arrangements; |

| • | negotiations with unions; |

| • | employee wages; |

| • | permitting; |

| • | surety bonding; and |

| • | mine closure and reclamation. |

If the Partnership’s lessees do not manage their operations well, their production could be reduced, which would result in lower coal royalty revenues to the Partnership and could adversely affect its ability to make its quarterly distributions.

| Coal mining operations are subject to numerous operational risks that could result in lower coal royalty revenues. |

The Partnership’s coal royalty revenues are largely dependent on the level of production from its coal reserves achieved by its lessees. The level of its lessees’ production is subject to operating conditions or events beyond their or its control, including:

| • | the inability to acquire necessary permits; |

| • | changes or variations in geologic conditions, such as the thickness of the coal deposits and the amount of rock embedded in or overlying the coal deposit; |

| • | changes in governmental regulation of the coal industry; |

| • | mining and processing equipment failures and unexpected maintenance problems; |

| • | adverse claims to title or existing defects of title; |

| • | interruptions due to power outages; |

| • | adverse weather and natural disasters, such as heavy rains and flooding; |

| • | labor-related interruptions; |

| • | employee injuries or fatalities; and |

| • | fires and explosions. |

These conditions may increase the Partnership’s lessees’ cost of mining and delay or halt production at particular mines for varying lengths of time. Any interruptions to the production of coal from the Partnership’s reserves could reduce its coal royalty revenues and adversely affect its ability to make its quarterly distributions.

In addition, the Partnership’s coal royalty revenues are based upon sales of coal by its lessees to their customers. If its lessees do not receive payments for delivered coal on a timely basis from their customers, their cash flow would be adversely affected, which could cause the Partnership’s cash flow to be adversely affected and could adversely affect the Partnership’s ability to make its quarterly distributions.

| A substantial or extended decline in coal prices could reduce the Partnership’s coal royalty revenues and the value of its coal reserves. |

A substantial or extended decline in coal prices from recent levels could have a material adverse effect on the Partnership’s lessees’ operations and on the quantities of coal that may be economically produced from the Partnership’s properties. This, in turn, could reduce the Partnership’s coal royalty revenues, its coal services revenues and the value of its coal reserves. Additionally, volatility in coal prices could make it difficult to estimate with precision the value of the Partnership’s coal reserves and any coal reserves that the Partnership may consider for acquisition.

| The Partnership depends on a limited number of primary operators for a significant portion of its coal royalty revenues and the loss of or reduction in production from any of its major lessees could reduce its coal royalty revenues. |

The Partnership depends on a limited number of primary operators for a significant portion of its coal royalty revenues. During 2005, five primary operators, each with multiple leases, accounted for 78 percent of its coal royalty revenues. If any of these operators enters bankruptcy or decide to cease operations or significantly reduce its production, the Partnership’s coal royalty revenues could be reduced.

A failure on the part of the Partnership’s lessees to make coal royalty payments could give the Partnership the right to terminate the lease, repossess the property or obtain liquidation damages and/or enforce payment obligations under the lease. If the Partnership repossessed any of its properties, it would seek to find a replacement lessee. It may not be able to find a replacement lessee and, if it finds a replacement lessee, it may not be able to enter into a new lease on favorable terms within

22

a reasonable period of time. In addition, the outgoing lessee could be subject to bankruptcy proceedings that could further delay the execution of a new lease or the assignment of the existing lease to another operator. If the Partnership enters into a new lease, the replacement operator might not achieve the same levels of production or sell coal at the same price as the lessee it replaced. In addition, it may be difficult for the Partnership to secure new or replacement lessees for small or isolated coal reserves, since industry trends toward consolidation favor larger-scale, higher technology mining operations to increase productivity rates.

| The Partnership’s coal business will be adversely affected if it is unable to replace or increase its reserves through acquisitions. |

Because its reserves decline as its lessees mine its coal, the Partnership’s future success and growth depends, in part, upon its ability to acquire additional coal reserves that are economically recoverable. If the Partnership is unable to negotiate purchase contracts to replace or increase its coal reserves on acceptable terms, its coal royalty revenues will decline as its coal reserves are depleted. In addition, if the Partnership is unable to successfully integrate the companies, businesses or properties it is able to acquire, its coal royalty revenues may decline and the Partnership could, therefore, experience a material adverse effect on its business, financial condition or results of operations. If the Partnership acquires additional coal reserves, there is a possibility that any acquisition could be dilutive to earnings and reduce its ability to make distributions to unitholders, including us, or to pay interest on, or the principal of, its debt obligations. Any debt the Partnership incurs to finance an acquisition may similarly affect its ability to make distributions to unitholders, including us, or to pay interest on, or the principal of, its debt obligations. The Partnership’s ability to make acquisitions in the future also could be limited by restrictions under its existing or future debt agreements, competition from other coal companies for attractive properties or the lack of suitable acquisition candidates.

| Lessees could satisfy obligations to their customers with coal from properties other than the Partnership’s, depriving it of the ability to receive amounts in excess of the minimum royalty payments. |

The Partnership does not control its lessees’ business operations. Its lessees’ customer supply contracts do not generally require its lessees to satisfy their obligations to their customers with coal mined from the Partnership’s reserves. Several factors may influence a lessee’s decision to supply its customers with coal mined from properties the Partnership does not own or lease, including the royalty rates under the lessee’s lease with the Partnership, mining conditions, transportation costs and availability and customer coal specifications. If a lessee satisfies its obligations to its customers with coal from properties the Partnership does not own or lease, production under its lease will decrease, and it will receive lower coal royalty revenues.

| Competition within the coal industry may adversely affect the ability of the Partnership’s lessees to sell coal at high prices, which could reduce its coal royalty revenues. |

The coal industry is intensely competitive primarily as a result of the existence of numerous producers. The Partnership’s lessees compete with coal producers in various regions of the United States for domestic sales. The industry has undergone significant consolidation which has led to some of the competitors of the Partnership’s lessees having significantly larger financial and operating resources than most of its lessees. The Partnership’s lessees compete on the basis of coal price at the mine, coal quality (including sulfur content), transportation cost from the mine to the customer and the reliability of supply. Continued demand for the Partnership’s coal and the prices that its lessees obtain are also affected by demand for electricity, demand for metallurgical coal, access to transportation, environmental and government regulations, technological developments and the availability and price of alternative fuel supplies, including nuclear, natural gas, oil and hydroelectric power. Demand for the Partnership’s low sulfur coal and the prices its lessees will be able to obtain for it will also be affected by the price and availability of high sulfur coal, which can be marketed in tandem with emissions allowances which permit the high sulfur coal to meet federal Clean Air Act requirements. Competition among coal producers could result in excess production capacity in the industry, resulting in downward pressure on prices. Declining prices reduce the Partnership’s coal royalty revenues and adversely affect its ability to make distributions to unitholders, including us, and to service its debt obligations.

| Fluctuations in transportation costs and the availability or reliability of transportation could reduce the production of coal mined from the Partnership’s properties. |

Transportation costs represent a significant portion of the total cost of coal for the customers of the Partnership’s lessees. Increases in transportation costs could make coal a less competitive source of energy or could make coal produced by some or all of the Partnership’s lessees less competitive than coal produced from other sources. On the other hand, significant decreases in transportation costs could result in increased competition for the Partnership’s lessees from coal producers in other parts of the country.

23

The Partnership’s lessees depend upon rail, barge, trucking, overland conveyor and other systems to deliver coal to their customers. Disruption of these transportation services due to weather-related problems, strikes, lockouts, bottlenecks and other events could temporarily impair the ability of the Partnership’s lessees to supply coal to their customers. The Partnership’s lessees’ transportation providers may face difficulties in the future and impair the ability of its lessees to supply coal to their customers, thereby resulting in decreased coal royalty revenues to the Partnership.

| The Partnership’s lessees could experience labor disruptions, and its lessees’ workforces could become increasingly unionized in the future. |

Two of the Partnership’s lessees each have one mine operated by unionized employees. One of these mines was the Partnership’s second largest mine on the basis of coal reserves as of December 31, 2005. All of the Partnership’s lessees could become increasingly unionized in the future. If some or all of the Partnership’s lessees’ non-unionized operations were to become unionized, it could adversely affect their productivity and increase the risk of work stoppages. In addition, the Partnership’s lessees’ operations may be adversely affected by work stoppages at unionized companies, particularly if union workers were to orchestrate boycotts against its lessees’ operations. Any further unionization of the Partnership’s lessees’ employees could adversely affect the stability of production from its reserves and reduce its coal royalty revenues.

| The Partnership’s reserve estimates depend on many assumptions that may be inaccurate, which could materially adversely affect the quantities and value of its reserves. |

The Partnership’s estimates of its reserves may vary substantially from the actual amounts of coal its lessees may be able to economically recover. There are numerous uncertainties inherent in estimating quantities of reserves, including many factors beyond the Partnership’s control. Estimates of coal reserves necessarily depend upon a number of variables and assumptions, any one of which may, if incorrect, result in an estimate that varies considerably from actual results. These factors and assumptions relate to:

| • | geological and mining conditions, which may not be fully identified by available exploration data or which differ from the Partnership’s experiences in areas where its lessees currently mine; |

| • | the amount of ultimately recoverable coal in the ground; |

| • | the effects of regulation by governmental agencies; and |

| • | future coal prices, operating costs, capital expenditures, severance and excise taxes and development and reclamation costs. |

Actual production, revenues and expenditures with respect to the Partnership’s reserves will likely vary from estimates, and these variations may be material. As a result, you should not place undue reliance on the coal reserve data provided herein.

| Any change in fuel consumption patterns by electric power generators away from the use of coal could affect the ability of the Partnership’s lessees to sell the coal they produce and thereby reduce its coal royalty revenues. |

According to the U.S. Department of Energy, domestic electric power generation accounts for approximately 90 percent of domestic coal consumption. The amount of coal consumed for domestic electric power generation is affected primarily by the overall demand for electricity, the price and availability of competing fuels for power plants such as nuclear, natural gas, fuel oil and hydroelectric power and environmental and other governmental regulations. The Partnership believes that most new power plants will be built to produce electricity during peak periods of demand. Many of these new power plants will likely be fired by natural gas because of lower construction costs compared to coal-fired plants and because natural gas is a cleaner burning fuel. The increasingly stringent requirements of the Clean Air Act may result in more electric power generators shifting from coal to natural gas-fired power plants. See Item 1, “Business—Regulation—Coal—Air Emissions.”

| Extensive environmental laws and regulations affecting electric power generators could have corresponding effects on the ability of the Partnership’s lessees to sell the coal they produce and thereby reduce its coal royalty revenues. |

Federal, state and local laws and regulations extensively regulate the amount of sulfur dioxide, particulate matter, nitrogen oxides, mercury and other compounds emitted into the air from electric power plants, which are the ultimate consumers of the coal the Partnership’s lessees produce. These laws and regulations can require significant emission control expenditures for many coal-fired power plants, and various new and proposed laws and regulations may require further

24

emission reductions and associated emission control expenditures. There is also continuing pressure on state and federal regulators to impose limits on carbon dioxide emissions from electric power plants, particularly coal-fired power plants. As a result of these current and proposed laws, regulations and trends, electricity generators may elect to switch to other fuels that generate less of these emissions, possibly further reducing demand for the coal that the Partnership’s lessees produce and thereby reducing its coal royalty revenues. See Item 1, “Business—Regulation—Coal—Air Emissions.”

| Delays in the Partnership’s lessees obtaining mining permits and approvals, or the inability to obtain required permits and approvals, could have an adverse effect on its coal royalty revenues. |

Mine operators, including the Partnership’s lessees, must obtain numerous permits and approvals that impose strict conditions and obligations relating to various environmental and safety matters in connection with coal mining. The permitting rules are complex and can change over time. The public has the right to comment on permit applications and otherwise participate in the permitting process, including through court intervention. Accordingly, permits required by the Partnership’s lessees to conduct operations may not be issued, maintained or renewed, or may not be issued or renewed in a timely fashion, or may involve requirements that restrict its lessees’ ability to economically conduct their mining operations. Limitations on the Partnership’s lessees’ ability to conduct their mining operations due to the inability to obtain or renew necessary permits could have an adverse effect on its coal royalty revenues. See Item 1, “Business—Regulation—Coal—Mining Permits and Approvals.”

| The Partnership’s lessees’ mining operations are subject to extensive and costly laws and regulations, and such current and future laws and regulations could increase operating costs and limit its lessees’ ability to produce coal, which could have an adverse effect on its coal royalty revenues. |

The Partnership’s lessees are subject to numerous and detailed federal, state and local laws and regulations affecting coal mining operations, including laws and regulations pertaining to employee health and safety, permitting and licensing requirements, air quality standards, water pollution, plant and wildlife protection, reclamation and restoration of mining properties after mining is completed, the discharge of materials into the environment, surface subsidence from underground mining and the effects that mining has on groundwater quality and availability. Numerous governmental permits and approvals are required for mining operations. The Partnership’s lessees are required to prepare and present to federal, state or local authorities data pertaining to the effect or impact that any proposed exploration for or production of coal may have upon the environment. The costs, liabilities and requirements associated with these regulations may be significant and time-consuming and may delay commencement or continuation of exploration or production operations. The possibility exists that new laws or regulations (or judicial interpretations of existing laws and regulations) may be adopted in the future that could materially affect the Partnership’s lessees’ mining operations, either through direct impacts such as new requirements impacting its lessees’ existing mining operations, or indirect impacts such as new laws and regulations that discourage or limit coal consumers’ use of coal. Any of these direct or indirect impacts could have an adverse effect on the Partnership’s coal royalty revenues. See Item 1, “Business—Regulation.”

Because of extensive and comprehensive regulatory requirements, violations during mining operations are not unusual in the industry and, notwithstanding compliance efforts, the Partnership does not believe violations by its lessees can be eliminated completely. Failure to comply with these laws and regulations may result in the assessment of administrative, civil and criminal penalties, the imposition of cleanup and site restoration costs and liens and, to a lesser extent, the issuance of injunctions to limit or cease operations. The Partnership’s lessees may also incur costs and liabilities resulting from claims for damages to property or injury to persons arising from their operations. If the Partnership’s lessees are required to pay these costs and liabilities and if their financial viability is affected by doing so, then their mining operations and, as a result, the Partnership’s coal royalty revenues and its ability to make distributions, could be adversely affected.

Recent mining accidents in West Virginia and Kentucky have received national attention and instigated responses at the state and national level that are likely to result in increased scrutiny of current safety practices and procedures at all mining operations, particularly underground mining operations. These recent events could also potentially result in the promulgation of more stringent mine safety laws and regulations, or amendments to existing mine safety laws, including increased sanctions for non-compliance. These potential future mine safety laws and regulations or amendments to existing mine safety laws and regulations, and the cost of compliance with such, could adversely affect the Partnership’s lessees’ coal production which could have an adverse affect on its coal royalty revenues and its ability to make distributions.

25

Risks Related to PVR’s Midstream Business

| The success of the Partnership’s midstream business depends upon its ability to find and contract for new sources of natural gas supply. |

In order to maintain or increase throughput levels on the Partnership’s gathering systems and asset utilization rates at its processing plants, the Partnership must contract for new natural gas supplies. The primary factors affecting its ability to connect new supplies of natural gas to its gathering systems include its success in contracting for existing natural gas supplies that are not committed to other systems and the level of drilling activity creating new gas supply near its gathering systems. The Partnership may not be able to obtain additional contracts for natural gas supplies.

Fluctuations in energy prices can greatly affect production rates and investments by third parties in the development of new oil and natural gas reserves. Drilling activity generally decreases as oil and natural gas prices decrease. The Partnership has no control over the level of drilling activity in its areas of operations, the amount of reserves underlying the wells and the rate at which production from a well will decline. In addition, the Partnership has no control over producers or their production decisions, which are affected by, among other things, prevailing and projected energy prices, demand for hydrocarbons, the level of reserves, geological considerations, governmental regulation and the availability and cost of capital.

A substantial portion of the Partnership’s midstream assets, including its gathering systems and processing plants, are connected to natural gas reserves and wells for which the production will naturally decline over time. The Partnership’s cash flows associated with these systems will decline unless it is able to access new supplies of natural gas by connecting additional production to these systems. A material decrease in natural gas production in its areas of operation, as a result of depressed commodity prices or otherwise, would result in a decline in the volume of natural gas the Partnership handles, which would reduce its revenues and operating income. In addition, the Partnership’s future growth will depend, in part, upon whether it can contract for additional supplies at a greater rate than the rate of natural decline in its currently connected supplies.

| The Partnership may not be able to retain existing customers or acquire new customers, which would reduce its revenues and limit its future profitability. |

The renewal or replacement of existing contracts with the Partnership’s customers at rates sufficient to maintain current revenues and cash flows depends on a number of factors beyond its control, including competition from other pipelines, and the price of, and demand for, natural gas in the markets the Partnership serves.

| The profitability of the Partnership’s midstream business is dependent upon prices and market demand for natural gas and NGLs, which are beyond its control and have been volatile. |

The Partnership is subject to significant risks due to fluctuations in commodity prices. During 2005, it generated a majority of its gross margin from two types of contractual arrangements under which its margin is exposed to increases and decreases in the price of natural gas and NGLs—percentage-of-proceeds and keep-whole arrangements.

Virtually all of the natural gas gathered on the Crescent System and the Hamlin System is contracted under percentage-of-proceeds arrangements. The natural gas gathered on the Beaver System is contracted primarily under either percentage-of proceeds or gas purchase/keep-whole arrangements. Under both types of arrangements, the Partnership provides gathering and processing services for natural gas received. Under percentage-of-proceeds arrangements, the Partnership generally sells the NGLs produced from the processing operations and the remaining residue gas at market prices and remits to the producers an agreed upon percentage of the proceeds based upon an index price for the gas and the price received for the NGLs. Under these percentage-of-proceeds arrangements, revenues and gross margins decline when natural gas prices and NGL prices decrease. Accordingly, a decrease in the price of natural gas or NGLs could have a material adverse effect on the Partnership’s results of operations. Under gas purchase/keep-whole arrangements, the Partnership generally buys natural gas from producers based upon an index price and then sells the NGLs and the remaining residue gas to third parties at market prices. Because the extraction of the NGLs from the natural gas during processing reduces the volume of natural gas available for sale, profitability is dependent on the value of those NGLs being higher than the value of the volume of gas reduction or “shrink.” Under these arrangements, revenues and gross margins decrease when the price of natural gas increases relative to the price of NGLs. Accordingly, a change in the relationship between the price of natural gas and the price of NGLs could have a material adverse effect on the Partnership’s results of operations.

26

In the past, the prices of natural gas and NGLs have been extremely volatile, and the Partnership expects this volatility to continue. The markets and prices for residue gas and NGLs depend upon factors beyond the Partnership’s control. These factors include demand for oil, natural gas and NGLs, which fluctuates with changes in market and economic conditions, and other factors, including:

| • | the impact of weather on the demand for oil and natural gas; |

| • | the level of domestic oil and natural gas production; |

| • | the availability of imported oil and natural gas; |

| • | actions taken by foreign oil and gas producing nations; |

| • | the availability of local, intrastate and interstate transportation systems; |

| • | the availability and marketing of competitive fuels; |

| • | the impact of energy conservation efforts; and |

| • | the extent of governmental regulation and taxation. |

| The Partnership encounters competition from other midstream companies. |

The Partnership experiences competition in all of its midstream markets. Competition is based on many factors, including geographic proximity to production, costs of connection, available capacity, rates and access to markets. The Partnership’s competitors include major integrated oil companies, interstate and intrastate pipelines and companies that gather, compress, process, transport and market natural gas. Many of the Partnership’s competitors have greater financial resources and access to larger natural gas supplies than it does.

| Expanding the Partnership’s midstream business by constructing new gathering systems, pipelines and processing facilities subjects it to construction risks. |

One of the ways the Partnership may grow its midstream business is through the construction of additions to existing gathering, compression and processing systems. The construction of a new gathering system or pipeline or the expansion of an existing pipeline, by adding additional horsepower or pump stations or by adding a second pipeline within an existing right of way, and the construction of new processing facilities, involve numerous regulatory, environmental, political and legal uncertainties beyond the Partnership’s control and require the expenditure of significant amounts of capital. If the Partnership undertakes these projects, they may not be completed on schedule, or at all, or at the budgeted cost. Moreover, the Partnership’s revenues may not increase immediately upon the expenditure of funds on a particular project. For example, the construction of gathering facilities requires the expenditure of significant amounts of capital, which may exceed the Partnership’s estimates. Generally, the Partnership may have only limited natural gas supplies committed to these facilities prior to their construction. Moreover, the Partnership may construct facilities to capture anticipated future growth in production in a region in which anticipated production growth does not materialize. As a result, there is the risk that new facilities may not be able to attract enough natural gas to achieve the Partnership’s expected investment return, which could adversely affect its financial position or results of operations.

| If the Partnership is unable to obtain new rights-of-way or the cost of renewing existing rights-of-way increases, then it may be unable to fully execute its growth strategy and its cash flows could be reduced. |

The construction of additions to the Partnership’s existing gathering assets may require it to obtain new rights-of-way before constructing new pipelines. The Partnership may be unable to obtain rights-of-way to connect new natural gas supplies to its existing gathering lines or capitalize on other attractive expansion opportunities. Additionally, it may become more expensive for the Partnership to obtain new rights-of-way or to renew existing rights-of-way. If the cost of obtaining new rights-of-way or renewing existing rights-of-way increases, then the Partnership’s cash flows could be reduced.

| The Partnership is exposed to the credit risk of its midstream customers, and nonpayment or nonperformance by its customers could reduce its cash flows. |

The Partnership is subject to risk of loss resulting from nonpayment or nonperformance by its customers. The Partnership depends on a limited number of customers for a significant portion of its midstream revenue. For 2005, two customers represented 46 percent of total natural gas midstream revenues and 23 percent of our total consolidated revenues. Any nonpayment or nonperformance by our customers could reduce our cash flows.

27

| Any reduction in the capacity of, or the allocations to, the Partnership in interconnecting third-party pipelines could cause a reduction of volumes processed, which would adversely affect its revenues and cash flow. |

The Partnership is dependent upon connections to third-party pipelines to receive and deliver residue gas and NGLs. Any reduction of capacities of these interconnecting pipelines due to testing, line repair, reduced operating pressures or other causes could result in reduced volumes gathered and processed in its midstream facilities. Similarly, if additional shippers begin transporting volumes of residue gas and NGLs on interconnecting pipelines, the Partnership’s allocations in these pipelines would be reduced. Any reduction in volumes gathered and processed in the Partnership’s facilities would adversely affect its revenues and cash flow.

Hedging transactions may limit the Partnership’s potential gains and involve other risks.

In order to manage its exposure to price risks in the marketing of its natural gas and NGLs, the Partnership periodically enters into natural gas and NGL price hedging arrangements with respect to a portion of its expected production. Its hedges are limited in duration, usually for periods of two years or less. However, in connection with acquisitions, sometimes its hedges are for longer periods. While intended to reduce the effects of volatile natural gas and NGL prices, such transactions may limit the Partnership’s potential gains if natural gas or NGL prices were to rise over the price established by the hedging arrangements. In trying to maintain an appropriate balance, the Partnership may end up hedging too much or too little, depending upon how natural gas or NGL prices fluctuate in the future. We cannot assure you that the Partnership’s hedging transactions will reduce the risk or minimize the effect of any decline in natural gas or NGL prices.

In addition, hedging transactions may expose the Partnership to the risk of financial loss in certain circumstances, including instances in which:

| • | its production is less than expected; |

| • | there is a widening of price basis differentials between delivery points for its production and the delivery point assumed in the hedge arrangement; |

| • | the counterparties to its futures contracts fail to perform under the contracts; or |

| • | a sudden, unexpected event materially impacts natural gas or NGL prices. |

The Partnership accounts for its derivative transactions pursuant to SFAS No. 133, which requires it to record each hedging transaction as an asset or liability measured at its fair value. The Partnership must also measure the effectiveness of its hedging position in relation to the underlying commodity being hedged, and the Partnership will be required to record the ineffective portion of the hedge in its net income for that period. This accounting treatment could result in significant fluctuations in our net income and shareholders’ equity from period to period.

In addition, hedging transactions using derivative instruments involve basis risk. Basis risk in a hedging contract occurs when the index upon which the contract is based is more or less variable than the index upon which the hedged asset is based, thereby making the hedge less effective. For example, a NYMEX index used for hedging certain volumes of production may have more or less variability than the regional price index used for the sale of that production.

| The Partnership’s midstream business involves many hazards and operational risks, some of which may not be fully covered by insurance. |

The Partnership’s midstream operations are subject to the many hazards inherent in the gathering, compression, treating, processing and transportation of natural gas and NGLs, including:

| • | damage to pipelines, related equipment and surrounding properties caused by hurricanes, tornadoes, floods, fires and other natural disasters and acts of terrorism; |

| • | inadvertent damage from construction and farm equipment; |

| • | leaks of natural gas, NGLs and other hydrocarbons; and |

| • | fires and explosions. |

These risks could result in substantial losses due to personal injury or loss of life, severe damage to and destruction of property and equipment and pollution or other environmental damage and may result in curtailment or suspension of the Partnership’s related operations. The Partnership’s midstream operations are concentrated in Texas and Oklahoma, and a natural disaster or other hazard affecting these areas could have a material adverse effect on its operations. The Partnership is not fully insured against all risks incident to its midstream business. The Partnership does not have property insurance on all of its underground pipeline systems that would cover damage to the pipelines. The Partnership is not insured against all environmental accidents that might occur, other than those considered to be sudden and accidental. If a significant accident or event occurs that is not fully insured, it could adversely affect the Partnership’s operations and financial condition.

28

| Federal, state or local regulatory measures could adversely affect the Partnership’s midstream business. |

Cantera Gas Company (“CGC”), a wholly owned subsidiary of PVR Midstream LLC, owns and operates an 11-mile interstate natural gas pipeline which, pursuant to the NGA, is subject to the jurisdiction of the FERC. The FERC has granted CGC waivers of various requirements otherwise applicable to conventional FERC-jurisdictional pipelines, including the obligation to file a tariff governing rates, terms and conditions of open access transportation service. The FERC has determined that CGC will have to comply with the filing requirements if the natural gas company ever desires to apply for blanket transportation authority to transport third-party gas on the 11-mile pipeline. We cannot assure you that the FERC will maintain these waivers.

The Partnership’s natural gas gathering facilities generally are exempt from the FERC’s jurisdiction under the NGA, but FERC regulation nevertheless could significantly affect its gathering business and the market for its services. In recent years, the FERC has pursued pro-competitive policies in its regulation of interstate natural gas pipelines into which the Partnership’s gathering pipelines deliver. However, we cannot assure you that the FERC will continue this approach as it considers matters such as pipeline rates and rules and policies that may affect rights of access to natural gas transportation capacity.

In Texas, the Partnership’s gathering facilities are subject to regulation by the Texas Railroad Commission, which has the authority to ensure that rates, terms and conditions of gas utilities, including certain gathering facilities, are just and reasonable and not discriminatory. The Partnership’s operations in Oklahoma are regulated by the Oklahoma Corporation Commission, which prohibits it from charging any unduly discriminatory fees for its gathering services. We cannot predict whether the Partnership’s gathering rates will be found to be unjust, unreasonable or unduly discriminatory.

The Partnership is subject to ratable take and common purchaser statutes in Texas and Oklahoma. Ratable take statutes generally require gatherers to take, without undue discrimination, natural gas production that may be tendered to the gatherer for handling. Similarly, common purchaser statutes generally require gatherers to purchase without undue discrimination as to source of supply or producer. These statutes have the effect of restricting the Partnership’s right as an owner of gathering facilities to decide with whom it contracts to purchase or transport natural gas. Federal law leaves any economic regulation of natural gas gathering to the states, and Texas and Oklahoma have adopted complaint-based regulation that generally allows natural gas producers and shippers to file complaints with state regulators in an effort to resolve grievances relating to natural gas gathering rates and access. We cannot assure you that federal and state authorities will retain their current regulatory policies in the future.

Texas and Oklahoma administer federal pipeline safety standards under the NGPSA, which requires certain pipelines to comply with safety standards in constructing and operating the pipelines, and subjects pipelines to regular inspections. In response to recent pipeline accidents, Congress and the U.S. Department of Transportation have recently instituted heightened pipeline safety requirements. Certain of the Partnership’s gathering facilities are exempt from these federal pipeline safety requirements under the rural gathering exemption. We cannot assure you that the rural gathering exemption will be retained in its current form in the future.

Failure to comply with applicable regulations under the NGA, the NGPSA and certain state laws can result in the imposition of administrative, civil and criminal remedies.

The Partnership’s midstream business is subject to extensive environmental regulation.

Many of the operations and activities of the Partnership’s gathering systems, plants and other facilities are subject to significant federal, state and local environmental laws and regulations. These include, for example, laws and regulations that impose obligations related to air emissions and discharge of wastes from the Partnership’s facilities and the cleanup of hazardous substances that may have been released at properties currently or previously owned or operated by Cantera or locations to which it has sent wastes for disposal. These laws and regulations can restrict or impact the Partnership’s business activities in many ways, including restricting the manner in which it disposes of substances, requiring pre-approval for the construction or modification of certain projects or facilities expected to produce air emissions, requiring remedial action to remove or mitigate contamination, and requiring capital expenditures to comply with control requirements. Failure to comply with these laws and regulations may trigger a variety of administrative, civil and criminal enforcement measures, including the assessment of monetary penalties, the imposition of remedial requirements and the issuance of orders enjoining future operations. Certain environmental statutes impose strict, joint and several liability for costs required to clean up and restore sites where substances and wastes have been disposed or otherwise released. Moreover, it is not uncommon for neighboring landowners and other third parties to file claims for personal injury and property damage allegedly caused by the release of substances or wastes into the environment.

29

There is inherent risk of the incurrence of environmental costs and liabilities in the Partnership’s midstream business due to its handling of natural gas and other petroleum products, air emissions related to its midstream operations, historical industry operations, waste disposal practices and Cantera’s prior use of natural gas flow meters containing mercury. For example, an accidental release from one of the Partnership’s pipelines or processing facilities could subject it to substantial liabilities arising from environmental cleanup, restoration costs and natural resource damages, claims made by neighboring landowners and other third parties for personal injury and property damage, and fines or penalties for related violations of environmental laws or regulations. Moreover, the possibility exists that stricter laws, regulations or enforcement policies could significantly increase the Partnership’s compliance costs and the cost of any remediation that may become necessary. The Partnership may incur material environmental costs and liabilities. Insurance may not provide sufficient coverage in the event an environmental claim is made.

Item 1B Unresolved Staff Comments

We received no written comments from the SEC staff regarding our periodic or current reports under the Exchange Act within 180 days before the end of our fiscal year ended December 31, 2005.

Item 2 Properties

Facilities

We are headquartered in Radnor, Pennsylvania, with additional offices in Tennessee, Texas and West Virginia. All of our office facilities are leased, except for PVR’s West Virginia office, which it owns. We believe that our properties are adequate for our current needs.

30

Title to Properties

The following map shows the general locations of our oil and gas production and exploration, PVR’s coal reserves, PVR’s coal services and infrastructure investments and PVR’s natural gas gathering and processing systems:

We believe that we have satisfactory title to all of our properties and the associated oil, gas and coal reserves in accordance with standards generally accepted in the oil and natural gas, coal and natural gas midstream industries.

As is customary in the oil and gas industry, we make only a cursory review of title to farmout acreage and to undeveloped oil and gas leases upon execution of any contracts. Prior to the commencement of drilling operations, a thorough title examination is conducted and curative work is performed with respect to significant defects. To the extent title opinions or other investigations reflect defects, we cure such title defects. If we were unable to remedy or cure any title defect of a nature such that it would not be prudent to commence drilling operations on a property, we could suffer a loss of our investment in the property. Prior to completing an acquisition of producing oil and gas assets, we obtain title opinions on all material leases. Our oil and gas properties are subject to customary royalty interests, liens for current taxes and other burdens that we believe do not materially interfere with the use or materially affect the value of such properties.

Of the 689 million tons of proven and probable coal reserves to which the Partnership had rights as of December 31, 2005, PVR owned the mineral interests and the majority of related surface rights to 609 million tons, or 88 percent, and leased the remaining 80 million tons, or 12 percent, from unaffiliated third parties.

PVR’s natural gas midstream assets are primarily located in the mid-continent area of Oklahoma and the panhandle of Texas. The Partnership owns and operates a significant set of midstream assets that include approximately 3,450 miles of gas gathering pipelines and three natural gas processing facilities, which have 160 MMcfd of total capacity. PVR owns, leases or has rights-of-way to the properties where the majority of its midstream facilities are located. PVR believes it has sufficient rights-of-way to accommodate its gathering systems and pipelines.

31

Information Regarding Oil and Gas Properties

Production and Pricing

The following table sets forth production, average sales prices and production costs with respect to our oil and gas properties for the years ended December 31, 2005, 2004 and 2003:

| | 2005 | | 2004 | | 2003 | |

| |

|

| |

|

| |

|

| |

Production: | | | | | | | | | | |

Oil and condensate (MBbls) | | | 302 | | | 396 | | | 625 | |

Natural gas (MMcf) | | | 25,550 | | | 22,079 | | | 20,094 | |

Total production (MMcfe) | | | 27,362 | | | 24,455 | | | 23,844 | |

| | | | | | | | | | |

Average sales prices: | | | | | | | | | | |

Natural gas ($/Mcf) | | | | | | | | | | |

Actual price received for production | | $ | 8.86 | | $ | 6.44 | | $ | 5.59 | |

Effect of derivative hedging activities | | | (0.55 | ) | | (0.17 | ) | | (0.28 | ) |

| |

|

| |

|

| |

|

| |

Average realized price | | $ | 8.31 | | $ | 6.27 | | $ | 5.31 | |

| |

|

| |

|

| |

|

| |

Crude oil ($/Bbl) | | | | | | | | | | |

Actual price received for production | | $ | 48.51 | | $ | 39.09 | | $ | 27.77 | |

Effect of derivative hedging activities | | | (2.84 | ) | | (5.34 | ) | | (0.86 | ) |

| |

|

| |

|

| |

|

| |

Average realized price | | $ | 45.67 | | $ | 33.75 | | $ | 26.91 | |

| |

|

| |

|

| |

|

| |

Production expenses ($/Mcfe): | | | | | | | | | | |

Lease operating | | $ | 0.63 | | $ | 0.57 | | $ | 0.51 | |

Taxes other than income | | | 0.48 | | | 0.38 | | | 0.40 | |

General and administrative | | | 0.34 | | | 0.34 | | | 0.33 | |

| |

|

| |

|

| |

|

| |

Total production expenses | | $ | 1.45 | | $ | 1.29 | | $ | 1.24 | |

| |

|

| |

|

| |

|

| |

Proved Reserves

The following table presents certain information regarding our proved reserves as of December 31, 2005, 2004 and 2003. The proved reserve estimates presented below were prepared by Wright and Company, Inc., independent petroleum engineers. For additional information regarding estimates of proved reserves, the preparation of such estimates by Wright and Company, Inc. and other information about our oil and gas reserves, see Note 24 in the Notes to Consolidated Financial Statements. Our estimates of proved reserves in the table below are consistent with those filed by us with other federal agencies.

32

| | Oil and

Condensate | | Natural

Gas | | Natural

Gas Equivalents | | Standardized

Measure (1) | | Year-end

Prices Used | |

| |

|

| |

|

| |

|

| |

|

| |

| |

| | | (MMbbls) | | | (Bcf) | | | (Bcfe) | | | ($ millions) | | | $ / Bbl | | | $ /MMbtu | |

2005 | | | | | | | | | | | | | | | | | | | |

Developed | | | 2.0 | | | 267 | | | 279 | | $ | 833 | | | | | | | |

Undeveloped | | | 0.9 | | | 92 | | | 98 | | | 203 | | | | | | | |

| |

|

| |

|

| |

|

| |

|

| | | | | | | |

Total | | | 2.9 | | | 359 | | | 377 | | $ | 1,036 | | $ | 61.04 | | $ | 10.08 | |

| |

|

| |

|

| |

|

| |

|

| | | | | | | |

2004 | | | | | | | | | | | | | | | | | | | |

Developed | | | 2.9 | | | 243 | | | 261 | | $ | 469 | | | | | | | |

Undeveloped | | | 3.4 | | | 73 | | | 93 | | | 121 | | | | | | | |

| |

|

| |

|

| |

|

| |

|

| | | | | | | |

Total | | | 6.3 | | | 316 | | | 354 | | $ | 590 | | $ | 43.46 | | $ | 6.18 | |

| |

|

| |

|

| |

|

| |

|

| | | | | | | |

2003 | | | | | | | | | | | | | | | | | | | |

Developed | | | 3.3 | | | 231 | | | 251 | | $ | 419 | | | | | | | |

Undeveloped | | | 3.3 | | | 52 | | | 72 | | | 93 | | | | | | | |

| |

|

| |

|

| |

|

| |

|

| | | | | | | |

Total | | | 6.6 | | | 283 | | | 323 | | $ | 512 | | $ | 32.52 | | $ | 5.97 | |

| |

|

| |

|

| |

|

| |

|

| | | | | | | |

|

(1) | Standardized measure consists of future net cash flows, discounted at 10 percent. For information on the changes in the standardized measure of discounted future net cash flows, see Note 24 in the Notes to Consolidated Financial Statements. |

In accordance with the SEC’s guidelines, the engineers’ estimates of future net revenues from our properties and the standardized measure thereof are based on oil and natural gas sales prices in effect as of December 31, 2005, and estimated future costs as of December 31, 2005. The prices are held constant throughout the life of the properties except where such guidelines permit alternate treatment, including the use of fixed and determinable contractual price escalations. Prices for oil and gas are subject to substantial seasonal fluctuations as well as fluctuations resulting from numerous other factors. See Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

Proved reserves are the estimated quantities of natural gas, crude oil and condensate that geological and engineering data demonstrate with reasonable certainty to be recoverable in future years from known reservoirs under existing economic and operating conditions. Proved developed reserves are proved reserves that can be expected to be recovered through existing wells with existing equipment and operating methods. There are numerous uncertainties inherent in estimating quantities of proved reserves and in projecting future rates of production and timing of development expenditures, including many factors beyond our control. Reserve engineering is a subjective process of estimating underground accumulations of oil and natural gas that cannot be measured in an exact manner, and the accuracy of any reserve estimate is a function of the quality of available data and of engineering and geological interpretation and judgment. The quantities of crude oil and natural gas that are ultimately recovered, production and operating costs, the amount and timing of future development expenditures and future crude oil and natural gas sales prices may all differ from those assumed in these estimates. Therefore, the standardized measure amounts shown above should not be construed as the current market value of the estimated oil and natural gas reserves attributable to our properties. The information set forth in the foregoing tables includes revisions of certain volumetric reserve estimates attributable to proved properties included in the preceding year’s estimates. Such revisions are the result of additional information from subsequent completions and production history from the properties involved or the result of a decrease (or increase) in the projected economic life of such properties resulting from changes in production prices.

Acreage

The following table sets forth our developed and undeveloped acreage at December 31, 2005. The acreage is located primarily in the Appalachian, Mississippi, east Texas and Gulf Coast onshore areas of the United States.

33

| | Gross

Acreage | | Net

Acreage | |

| |

|

| |

|

| |

| | (in thousands) | |

Developed | | | 637 | | | 511 | |

Undeveloped | | | 719 | | | 482 | |

| |

|

| |

|

| |

Total | | | 1,356 | | | 993 | |

| |

|

| |

|

| |

Wells Drilled

The following table sets forth the gross and net numbers of exploratory and development wells drilled during the last three years. The number of wells drilled refers to the number of wells reaching total depth at any time during the respective year. Net wells equal the number of gross wells multiplied by our working interest in each of the gross wells. Productive wells represent either wells which were producing or which were capable of commercial production.

| | 2005 | | 2004 | | 2003 | |

| |

| |

| |

| |

| | Gross | | Net | | Gross | | Net | | Gross | | Net | |

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

Development | | | | | | | | | | | | | | | | | | | |

Productive | | | 163 | | | 130.8 | | | 134 | | | 89.7 | | | 161 | | | 117.0 | |

Non-productive | | | 3 | | | 3.0 | | | 1 | | | 0.3 | | | 1 | | | 1.0 | |

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

Total development | | | 166 | | | 133.8 | | | 135 | | | 90.0 | | | 162 | | | 118.0 | |

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

Exploratory | | | | | | | | | | | | | | | | | | | |

Productive | | | 6 | | | 2.9 | | | 7 | | | 1.5 | | | 5 | | | 1.2 | |

Non-productive | | | 3 | | | 3.0 | | | 7 | | | 4.4 | | | 3 | | | 2.9 | |

Under evaluation | | | 3 | | | 2.5 | | | 3 | | | 2.6 | | | 10 | | | 10.0 | |

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

Total exploratory | | | 12 | | | 8.4 | | | 17 | | | 8.5 | | | 18 | | | 14.1 | |

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

Total | | | 178 | | | 142.2 | | | 152 | | | 98.5 | | | 180 | | | 132.1 | |

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

The three exploratory wells under evaluation at the end of 2005 included two New Albany Shale wells in Ilinois and a Bakken Dolomite horizontal oil well in Montana. We expect to determine the commercial viability of these wells during 2006. At December 31, 2005, we had capitalized costs of $1.7 million related to these wells.

The three exploratory wells under evaluation at the end of 2004 included a horizontal Devonian shale well in West Virginia, a CBM well in Mississippi and an HCBM well in Virginia. In 2005, we determined that these wells were not commercially viable, resulting in a $3.3 million write-off.

The 10 exploratory wells under evaluation at the end of 2003 were CBM wells drilled and completed in the Cherokee Basin in Chase and Greenwood Counties, Kansas. In 2004, we determined that these wells were not commercially viable, resulting in a $4.4 million write-off.

Productive Wells

The number of productive oil and gas wells in which we had a working interest at December 31, 2005, is set forth below. Productive wells are producing wells or wells capable of commercial production.

Operated Wells | | Non-Operated Wells | | Total | |

| |

| |