UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| [ X ] | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended October 3, 2008

OR

| [____] | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ______ to ______

Commission file number 0-16255

JOHNSON OUTDOORS INC.

(Exact name of registrant as specified in its charter)

| Wisconsin | | 39-1536083 |

| (State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

555 Main Street, Racine, Wisconsin 53403

(Address of principal executive offices, including zip code)

(262) 631-6600

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class | | Name of Exchange on Which Registered |

| Class A Common Stock, $.05 par value per share | | NASDAQ Global MarketSM |

Securities registered pursuant to section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes [ ] No [ X ]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes [ ] No [ X ]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [ X ] No [ ]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K, or any amendment to this Form 10-K. [ X ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definition of "large accelerated filer,” “accelerated filer" and “smaller reporting company” in Rule 12b-2 of the Exchange Act (Check one):

| Large Accelerated Filer | [ ] |

| Accelerated Filer | [X] |

| Non-Accelerated Filer | [ ] |

| Smaller Reporting Company | [ ] |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).Yes [ ] No [ X ]

As of December 5, 2008, 8,007,069 shares of Class A and 1,216,464 shares of Class B common stock of the registrant were outstanding. The aggregate market value of voting and non-voting Class A common stock of the registrant held by nonaffiliates of the registrant was approximately $73,917,159 on March 28, 2008 (the last business day of the registrant’s most recently completed second quarter) based on approximately 4,386,775 shares of Class A common stock held by nonaffiliates. For purposes of this calculation only, shares of all voting stock are deemed to have a market value of $16.85 per share, the closing price of the Class A common stock as reported on the NASDAQ Global MarketSM on March 28, 2008. Shares of common stock held by any executive officer or director of the registrant (including all shares beneficially owned by the Johnson Family) have been excluded from this computation because such persons may be deemed to be affiliates. This determination of affiliate status is not a conclusive determination for other purposes.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Proxy Statement for the 2009 Annual Meeting of the Shareholders of the Registrant are incorporated by reference into Part III of this report.

As used in this report, the terms "we," "us," "our," "Johnson Outdoors" and the "Company" mean Johnson Outdoors Inc. and its subsidiaries, unless the context indicates another meaning.

TABLE OF CONTENTS | | Page |

Business | | 1 |

Risk Factors | | 5 |

Unresolved Staff Comments | | 8 |

Properties | | 9 |

Legal Proceedings | | 10 |

Submission of Matters to a Vote of Security Holders | | 10 |

Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | | 10 |

Selected Consolidated Financial Data | | 12 |

Management’s Discussion and Analysis of Financial Condition and Results of Operations | | 14 |

Quantitative and Qualitative Disclosures about Market Risk | | 26 |

Financial Statements and Supplementary Data | | 26 |

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | | 26 |

Controls and Procedures | | 27 |

Other Information | | 28 |

Directors, and Executive Officers and Corporate Governance | | 28 |

Executive Compensation | | 28 |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | | 28 |

Certain Relationships and Related Transactions, and Director Independence | | 29 |

Principal Accountant Fees and Services | | 29 |

Exhibits and Financial Statement Schedules | | 30 |

Signatures | | 31 |

Exhibit Index | | 32 |

Consolidated Financial Statements | | F-5 |

Forward Looking Statements

Certain matters discussed in this Form 10-K are “forward-looking statements,” and the Company intends these forward-looking statements to be covered by the safe harbor provisions for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995 and is including this statement for purposes of those safe harbor provisions. These forward-looking statements can generally be identified as such because the context of the statement includes phrases such as the Company “expects,” “believes” or other words of similar meaning. Similarly, statements that describe the Company’s future plans, objectives or goals are also forward-looking statements. Such forward-looking statements are subject to certain risks and uncertainties which could cause actual results or outcomes to differ materially from those currently anticipated. Factors that could affect actual results or outcomes include the matters described under the caption "Risk Factors" in Item 1A of this report and the following: changes in consumer spending patterns; the Company’s success in implementing its strategic plan, including its focus on innovation; actions of companies that compete with the Company; the Company’s success in managing inventory; movements in foreign currencies or interest rates; unanticipated issues related to the Company’s military tent business; the success of suppliers and customers; the ability of the Company to deploy its capital successfully; unanticipated outcomes related to outsourcing certain manufacturing processes; unanticipated outcomes related to outstanding litigation matters; successful integration of acquisitions; and adverse weather conditions. Shareholders, potential investors and other readers are urged to consider these factors in evaluating the forward-looking statements and are cautioned not to place undue reliance on such forward-looking statements. The forward-looking statements included herein are only made as of the date of this filing. The Company assumes no obligation, and disclaims any obligation, to update such forward-looking statements to reflect subsequent events or circumstances.

We have registered the following trademarks, which are used in this report: Minn Kota®, Cannon®, Humminbird®, Bottom Line®, Fishin' Buddy®, Silva®, Eureka!®, Geonav®, Old Town®, Ocean Kayak™ Necky®, Escape®, Lendal™ Extrasport®, Carlisle®, Scubapro®, UWATEC® and Seemann™.

PART I

Johnson Outdoors Inc. (the Company) is a leading global manufacturer and marketer of branded seasonal, outdoor recreation products used primarily for fishing, diving, paddling and camping. The Company’s portfolio of well-known consumer brands have attained leading market positions due to continuous innovation, marketing excellence, product performance and quality and enjoy a premium reputation among outdoor recreation enthusiasts and novices alike. Company values and culture support entrepreneurism in all areas, promoting and leveraging best practices and synergies within and across its subsidiaries to advance the Company’s strategic vision set by executive management and approved by the Board of Directors. The Company is controlled by Helen P. Johnson-Leipold (Chairman and Chief Executive Officer), members of her family and related entities.

The Company was incorporated in Wisconsin in 1987 as successor to various businesses.

Marine Electronics

The Company’s marine electronic segment brands are: Minn Kota battery-powered fishing motors for quiet trolling or primary propulsion; Humminbird sonar and GPS equipment for fishfinding and navigation; Cannon downriggers for controlled-depth fishing; and Geonav chartplotters for navigation. Marine electronic brands and related accessories are sold in North America, South America, Europe and the Pacific Basin through large outdoor specialty retailers, such as Bass Pro Shops and Cabelas, large retail store chains, marine distributors, international distributors and original equipment manufacturers, such as Ranger Boats, Skeeter Boats and Stratos Champion.

Market share gains have been achieved by emphasizing innovation, quality products and marketing. Consumer marketing and promotion includes: product placements on fishing-related television shows; print advertising and editorial coverage in outdoor, general interest and sport magazines; professional angler and tournament sponsorships; packaging and point-of-purchase materials and offers to increase consumer appeal and sales; branded websites; and, on-line promotions.

On November 16, 2007, the Company acquired Geonav S.r.l. (Geonav), a marine electronics company in Italy for approximately $5.6 million, including transaction costs. Geonav is a major European brand of chart plotters based in Viareggio, Italy. Also sold under the Geonav brand are marine autopilots, VHF radios and fish finders.

The Company’s Outdoor Equipment segment brands are: Eureka! tents, sleeping bags and backpacks; Silva field compasses and digital instruments; and Tech40 performance measurement instruments.

Eureka! consumer tents, sleeping bags and backpacks are mid- to high-price range products sold in the U.S. and Canada through independent sales representatives, primarily to sporting goods stores, catalog and mail order houses and camping and backpacking specialty stores. Marketing of the Company’s tents, sleeping bags and backpacks is focused on building the Eureka! brand name and establishing the Company as a leader in tent design and innovation. Although the Company’s camping tents, sleeping bags and backpacks are produced primarily by third-party manufacturing sources, design and innovation are conducted at the Company's Binghamton, New York location. Eureka! camping products are sold under license in Japan, Australia and Europe.

Eureka! commercial tents include party tents, sold primarily to general rental stores, and other commercial tents sold directly to tent erectors. Commercial tents are manufactured by the Company at the Company’s Binghamton, New York location and the Company’s tent products range from 10’x10’ canopies to 120’ wide pole tents and other large scale frame structures.

Eureka! also designs and manufactures large, heavy-duty tents and lightweight backpacking tents for the military at its Binghamton, New York location. Tents produced in the last twelve months include modular general purpose tents, TEMPER tents, a rapid deploy tent system, and various lightweight one to four person tents. Military tent accessories like fabric floors and tent liners are also manufactured.

Silva field compasses are manufactured by third parties and marketed exclusively in North America where the Company owns Silva trademark rights. Tech40 digital instruments are manufactured by third parties and are primarily sold in the North American market.

Watercraft

The Company’s Watercraft brands are: Old Town canoes and kayaks; Ocean Kayak; Necky kayaks; Carlisle and Lendal paddles; and Extrasport personal flotation devices.

The Company manufactures its Watercraft products in two locations in the U.S. and one in New Zealand. The Company also contracts for manufacturing of Watercraft products with third parties in Michigan, Tunisia and the Czech Republic.

In its Old Town, Maine facility, the Company produces high quality Old Town kayaks, canoes and accessories for family recreation, touring and tripping. The Company uses a rotational-molding process for manufacturing polyethylene kayaks and canoes to compete in the high volume, low and mid-priced range of the market. These kayaks and canoes feature stiffer and more durable hulls than higher priced boats. The Company also manufactures canoes from fiberglass, Royalex (ABS) and wood.

Sit-on-top Ocean Kayaks and high-performance Necky sea touring kayaks are manufactured in the Company’s Ferndale, Washington facility.

Watercraft accessory brands, including Extrasport personal flotation devices and wearable paddle gear, as well as Carlisle branded paddles are produced primarily by third-party sources. Lendal paddles are produced in-house at the Old Town Canoe facility.

The Company’s kayaks, canoes and accessories are sold primarily to specialty stores, marine dealers, sporting goods stores and catalog and mail order houses such as L. L. Bean® in the U.S., Europe and Australasia.

The Company manufactures and markets underwater diving products for technical and recreational divers, which it sells and distributes under the SCUBAPRO, UWATEC and Seemann brand names.

The Company markets a complete line of underwater diving and snorkeling equipment, including regulators, stabilizing jackets, dive computers and gauges, wetsuits, masks, fins, snorkels and accessories. SCUBAPRO and UWATEC diving equipment are marketed to the premium segment of the market for both diving enthusiasts and more technical, advanced divers. Seemann products are marketed to the recreational diver interested in owning quality equipment at an affordable price. Products are sold via selected distribution to independent specialty dive stores worldwide. These specialty dive stores generally provide a wide range of services to divers, including sales, service and repair, diving education and travel.

The Company focuses on maintaining SCUBAPRO and UWATEC as the market leaders in innovation. The Company maintains research and development functions in the U.S. and Europe and holds a number of patents on proprietary products. The Company’s consumer communication focuses on building the brand and highlighting exclusive product features and consumer benefits of the SCUBAPRO and UWATEC product lines. The Company’s communication and distribution reinforce the SCUBAPRO and UWATEC brands’ position as the industry’s quality and innovation leader. The Company markets its equipment in diving magazines, via websites and through dive specialty stores. Seemann’s full-line of dive equipment and accessories are marketed and sold primarily in Europe. Seemann products compete in the mid-market on the basis of quality at an affordable price.

The Company maintains manufacturing and assembly facilities in Italy and Indonesia and is currently in the process of moving the Swiss manufacturing operation to Batam, Indonesia, as described in Note 2 to the Company’s Consolidated Financial Statements attached to this report. The Company sources stabilizing jackets from a third-party manufacturer in Mexico. The majority of the Company’s rubber, proprietary materials, plastic products and other components are also sourced from third-parties.

Financial Information for Business Segments

As noted above, the Company has four reportable business segments. See Note 12 to the Consolidated Financial Statements included elsewhere in this report for financial information concerning each business segment.

See Note 12 to the Consolidated Financial Statements included elsewhere in this report for financial information regarding the Company’s domestic and international operations. See Note 1, subheading “Foreign Operations and Related Derivative Financial Instruments,” to the Consolidated Financial Statements included elsewhere in this report for information regarding risks related to the Company’s foreign operations.

The Company commits significant resources to new product research and development. The Company expenses these costs as incurred except for software development for new fishfinder products which are capitalized once technological feasibility is established and then amortized over the expected life of the software. The amounts expensed by the Company in connection with research and development activities for each of the last three fiscal years are set forth in the Company’s Consolidated Statements of Operations included elsewhere in this report.

The Company believes its products compete favorably on the basis of product innovation, product performance and marketing support and, to a lesser extent, price.

Marine Electronics: The main competitor in electric trolling motors is Motor Guide, owned by Brunswick Corporation, which manufactures and sells a full range of trolling motors and accessories. Competition in this business is focused on product quality and durability as well as product benefits and features for fishing. The main competitors in the fishfinder market are Lowrance, Garmin, Navman, and Ray Marine. Competition in this business is primarily focused on the quality of sonar imaging and display as well as the integration of mapping and GPS technology. The main competitors in the downrigger market are Big Jon, Walker and Scotty. Competition in this business primarily focuses on ease of operation, speed and durability.

Outdoor Equipment: The Company’s brands and products compete in the sporting goods and specialty segments of the outdoor equipment market. Competitive brands with a strong position in the sporting goods channel include Coleman and private label brands. The Company also competes with specialty companies such as The North Face and Kelty on the basis of materials and innovative designs for consumers who want performance products priced at a value. Commercial tent market competitors include Anchor Industries and Aztec for tension and frame tents along with canopies based on structure and styling. The Company also competes for military tent contracts under the U.S. Government bidding process; competitors include Base-X, DHS Systems and Alaska Structures, Camel, Outdoor Ventures, and Diamond Brands.

Watercraft: The Company primarily competes in the paddle boat segment of kayaks and canoes. The Company’s main competitors in this segment are Confluence Watersports, Pelican, Wenonah Canoe and Legacy Paddlesports, each of which primarily competes on the basis of their design, performance and quality.

Diving: The main competitors in Diving include Aqualung/U.S. Divers, Oceanic, Mares, Cressi-sub, and Suunto, each of which primarily competes on the basis of product innovation, performance, quality and safety.

At October 3, 2008, the Company had approximately 1,400 regular, full-time employees. The Company considers its employee relations to be excellent. Temporary employees are utilized primarily to manage peaks in the seasonal manufacturing of products.

Unfilled orders for future delivery of products totaled approximately $38.2 million at October 3, 2008 and $36.0 million September 28, 2007. For the majority of its products, the Company’s businesses do not receive significant orders in advance of expected shipment dates, with the exception of the military tent business which has orders outstanding based on contractual agreements.

Patents, Trademarks and Proprietary Rights

The Company owns no single patent that is material to its business as a whole. However, the Company holds various patents, principally for diving products, electric motors and fishfinders and regularly files applications for patents. The Company has numerous trademarks and trade names which it considers important to its business, many of which are noted on the preceding pages. Historically, the Company has vigorously defended its intellectual property rights and the Company expects to continue to do so.

Sources and Availability of Materials

The Company’s products are made using materials that are generally in adequate supply and are available from a variety of third-party suppliers.

The Company has an exclusive supply contract with a single vendor for materials used in its military tent business. Interruption or loss in the availability of these materials could have a material adverse impact on the sales and operating results of the Company’s Outdoor Equipment business.

The Company’s products are outdoor recreation related which results in seasonal variations in sales and profitability. This seasonal variability is due to customers increasing their inventories in the quarters ending March and June, the primary selling season for the Company’s outdoor recreation products. The following table shows, for the past three fiscal years, the total net sales and operating profit or loss of the Company for each quarter, as a percentage of the total year.

Year Ended | |

| | | October 3, 2008 | | | September 28, 2007 | | | September 29, 2006 | |

Quarter Ended | | Net Sales | | | Operating Profit (Loss) | | | Net Sales | | | Operating Profit (Loss) | | | Net Sales | | | Operating Profit (Loss) | |

December | | | 18 | % | | | (12 | )% | | | 17 | % | | | (11 | )% | | | 19 | % | | | (1 | )% |

| March | | | 29 | | | | 10 | | | | 28 | | | | 23 | | | | 27 | | | | 38 | |

| June | | | 34 | | | | 38 | | | | 35 | | | | 74 | | | | 34 | | | | 62 | |

| September | | | 19 | | | | (136 | ) | | | 20 | | | | 14 | | | | 20 | | | | 1 | |

| | | | 100 | % | | | (100 | )% | | | 100 | % | | | 100 | % | | | 100 | % | | | 100 | % |

Available Information

The Company maintains a website at www.johnsonoutdoors.com. On its website, the Company makes available, free of charge, its Annual Report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports, as soon as reasonably practical after the reports have been electronically filed or furnished to the Securities and Exchange Commission. In addition, the Company makes available on its website, free of charge, its (a) Code of Business Conduct; (b) Code of Ethics for its Chief Executive Officer and Senior Financial and Accounting Officers; and (c) the charters for the following committees of the Board of Directors: Audit; Compensation; Executive; and Nominating and Corporate Governance. The Company is not including the information contained on or available through its website as a part of, or incorporating such information by reference into, this Annual Report on Form 10-K. This report includes all material information about the Company that is included on the Company’s website and is otherwise required to be included in this report.

The risks described below are not the only risks we face. Additional risks that we do not yet know of or that we currently think are immaterial may also impair our future business operations. If any of the events or circumstances described in the following risks actually occur, our business, financial condition or results of operations could be materially adversely affected. In such cases, the trading price of our common stock could decline.

Our net sales and profitability depend on our ability to continue to conceive, design and market products that appeal to our consumers.

The introduction of new products is critical in our industry and to our growth strategy. Our business depends on our ability to continue to conceive, design, manufacture and market new products and upon continued market acceptance of our product offering. Rapidly changing consumer preferences and trends make it difficult to predict how long consumer demand for our existing products will continue or what new products will be successful. Our current products may not continue to be popular or new products that we may introduce may not achieve adequate consumer acceptance for us to recover development, manufacturing, marketing and other costs. A decline in consumer demand for our products, our failure to develop new products on a timely basis in anticipation of changing consumer preferences or the failure of our new products to achieve and sustain consumer acceptance could reduce our net sales and profitability.

Competition in our markets could reduce our net sales and profitability.

We operate in highly competitive markets. We compete with several large domestic and foreign companies such as Brunswick, Lowrance, Confluence and Aqualung/U.S. Divers, with private label products sold by many of our retail customers and with other producers of outdoor recreation products. Some of our competitors have longer operating histories, stronger brand recognition and greater financial, technical, marketing and other resources than us. In addition, we may face competition from new participants in our markets because the outdoor recreation product industries have limited barriers to entry. We experience price competition for our products, and competition for shelf space at retailers, all of which may increase in the future. If we cannot compete successfully in the future, our net sales and profitability will likely decline.

General economic conditions affect our results.

Our revenues are affected by economic conditions and consumer confidence worldwide, but especially in the United States and Europe. In times of economic uncertainty, consumers tend to defer expenditures for discretionary items, which affects demand for our products. Our businesses are cyclical in nature, and their success is dependent upon favorable economic conditions, the overall level of consumer confidence and discretionary income levels. Any substantial deterioration in general economic conditions that diminishes consumer confidence or discretionary income can reduce our sales and adversely affect our financial results including the potential for future impairments of goodwill and other intangible assets. The impact of weakening consumer credit markets; corporate restructurings; layoffs; declines in the value of investments and residential real estate; higher fuel prices and increases in federal and state taxation all can negatively affect our results.

Trademark infringement or other intellectual property claims relating to our products could increase our costs.

Our industry is susceptible to litigation regarding trademark and patent infringement and other intellectual property rights. We could be either a plaintiff or defendant in trademark and patent infringement claims and claims of breach of license from time to time. The prosecution or defense of intellectual property litigation is both costly and disruptive of the time and resources of our management even if the claim or defense against us is without merit. We could also be required to pay substantial damages or settlement costs to resolve intellectual property litigation.

Impairment charges could reduce our profitability.

In accordance with the provisions of Statement of Financial Accounting Standards No. 142, Goodwill and Other Intangible Assets, the Company tests goodwill and other intangible assets with indefinite useful lives for impairment on an annual basis or on an interim basis if an event occurs that might reduce the fair value of the reporting unit below its carrying value. We conduct testing for impairment during the fourth quarter of our fiscal year. Various uncertainties, including changes in consumer preferences, deterioration in the political environment, continued adverse conditions in the capital markets or changes in general economic conditions, could impact the expected cash flows to be generated by an intangible asset or group of intangible assets, and may result in an impairment of those assets. Although any such impairment charge would be a non-cash expense, any impairment of our intangible assets could materially increase our expenses and reduce our profitability. If we are required to record an impairment charge, the charge could affect our compliance with the debt covenants in our credit facility. Additionally, should we violate a covenant under our debt agreements, the cost of obtaining an amendment or waiver could be significant, or the lenders could be unwilling to provide a waiver or agree to an amendment. For our fiscal year ending October 3, 2008, we recorded an impairment charge of $41.0 million.

Sales of our products are seasonal, which causes our operating results to vary from quarter to quarter.

Sales of our products are seasonal. Historically, our net sales and profitability have peaked in the second and third fiscal quarters due to the buying patterns of our customers. Seasonal variations in operating results may cause our results to fluctuate significantly in the first and fourth quarters and may tend to depress our stock price during the first and fourth quarters.

The trading price of shares of our common stock fluctuates and investors in our common stock may experience substantial losses.

The trading price of our common stock has been volatile and may continue to be volatile in the future. The trading price of our common stock could decline or fluctuate in response to a variety of factors, including:

| · | the timing of our announcements or those of our competitors concerning significant product developments, acquisitions or financial performance; |

| · | fluctuation in our quarterly operating results; |

| · | substantial sales of our common stock; |

| · | general stock market conditions; or |

| · | other economic or external factors. |

You may be unable to sell your stock at or above your purchase price.

A limited number of our shareholders can exert significant influence over the Company.

As of December 5, 2008, Helen P. Johnson-Leipold, members of her family and related entities (hereinafter the Johnson Family) held approximately 78% of the voting power of both classes of our common stock taken as a whole. This voting power would permit these shareholders, if they chose to act together, to exert significant influence over the outcome of shareholder votes, including votes concerning the election of directors, by-law amendments, possible mergers, corporate control contests and other significant corporate transactions.

We may experience difficulties in integrating strategic acquisitions.

As part of our growth strategy, we intend to pursue acquisitions that are consistent with our mission and that will enable us to leverage our competitive strengths. Over the past three fiscal years we have acquired:

| · | certain assets of Computrol, Inc. on October 3, 2005, including, without limitation certain intellectual property used in its business; |

| · | Lendal Products Ltd. on October 3, 2006, including, without limitation certain intellectual property used in its business; |

| · | Seemann Sub GmbH & Co. KG on April 2, 2007, including, without limitation certain intellectual property used in its business; and |

| · | Geonav S.r.l. on November 16, 2007, including without limitation certain intellectual property used in its business. |

Risks associated with integrating strategic acquisitions include:

| · | the acquired business may experience losses which could adversely affect our profitability; |

| · | unanticipated costs relating to the integration of acquired businesses may increase our expenses; |

| · | possible failure to obtain any necessary consents to the transfer of licenses or other agreements of the acquired company; |

| · | possible failure to maintain customer, licensor and other relationships after the closing of the transaction of the acquired company; |

| · | difficulties in achieving planned cost-savings and synergies may increase our expenses; |

| · | diversion of our management’s attention could impair their ability to effectively manage our other business operations; and |

| · | unanticipated management or operational problems or liabilities may adversely affect our profitability and financial condition. |

We are dependent upon certain key members of management.

Our success will depend to a significant degree on the abilities and efforts of our senior management. Moreover, our success depends on our ability to attract, retain and motivate qualified management, marketing, technical and sales personnel. These people are in high demand and often have competing employment opportunities. The labor market for skilled employees is highly competitive due to limited supply, and we may lose key employees or be forced to increase their compensation to retain these people. Employee turnover could significantly increase our training and other related employee costs. The loss of key personnel, or the failure to attract qualified personnel, could have a material adverse effect on our business, financial condition or results of operations and on the value of our securities.

Sources of and fluctuations in market prices of raw materials can affect our operating results.

The primary raw materials we use are metals, resins and packaging materials. These materials are generally available from a number of suppliers, but we have chosen to concentrate our sourcing with a limited number of vendors for each commodity or purchased component. We believe our sources of raw materials are reliable and adequate for our needs. However, the development of future sourcing issues related to the availability of these materials as well as significant fluctuations in the market prices of these materials may have an adverse affect on our financial results.

Currency exchange rate fluctuations could increase our expenses.

We have significant foreign operations, for which the functional currencies are denominated primarily in euros, Swiss francs, Japanese yen and Canadian dollars. As the values of the currencies of the foreign countries in which we have operations increase or decrease relative to the U.S. dollar, the sales, expenses, profits, losses, assets and liabilities of our foreign operations, as reported in our consolidated financial statements, increase or decrease, accordingly. Approximately 29% of our revenues for the year ended October 3, 2008 were denominated in currencies other than the U.S. dollar. Approximately 17% were denominated in euros, with the remaining 12% denominated in various other foreign currencies. In the past, we have mitigated a portion of the fluctuations in certain foreign currencies through the purchase of foreign currency swaps, forward contracts and options to hedge known commitments, primarily for purchases of inventory and other assets denominated in foreign currencies; however, no such transactions were entered into during fiscal years 2008 or 2007.

We are subject to environmental and safety regulations.

We are subject to federal, state, local and foreign laws and other legal requirements related to the generation, storage, transport, treatment and disposal of materials as a result of our manufacturing and assembly operations. These laws include the Resource Conservation and Recovery Act (as amended), the Clean Air Act (as amended) and the Comprehensive Environmental Response, Compensation and Liability Act (as amended). We believe that our existing environmental management system is adequate and we have no current plans for substantial capital expenditures in the environmental area. We do not currently anticipate any material adverse impact on our results of operations, financial condition or competitive position as a result of compliance with federal, state, local and foreign environmental laws or other legal requirements. However, risk of environmental liability and changes associated with maintaining compliance with environmental laws is inherent in the nature of our business and there is no assurance that material liabilities or changes would not arise.

We rely on our credit facility to provide us with sufficient working capital to operate our business.

Historically, we have relied upon our existing credit facilities to provide us with adequate working capital to operate our business. The availability of borrowing amounts under our credit facilities are dependent upon our compliance with the debt covenants set forth in the facilities. Violation of those covenants, whether as a result of recording goodwill impairment charges, incurring operating losses or otherwise, could result in our lenders restricting or terminating our borrowing ability under our credit facilities. If our lenders reduce or terminate our access to amounts under our credit facilities, we may not have sufficient capital to fund our working capital needs and/or we may need to secure additional capital or financing to fund our working capital requirements or to repay outstanding debt under our credit facilities. We can make no assurance that we will be successful in ensuring our availability to amounts under our credit facilities or in connection with raising additional capital and that any amount, if raised, will be sufficient to meet our cash requirements. If we are not able to maintain our borrowing availability under our credit facilities and/or raise additional capital when needed, we may be forced to sharply curtail our efforts to manufacture and promote the sale of our products or to curtail our operations.

Our debt covenants may limit our ability to complete acquisitions, incur debt, make investments, sell assets, merge or complete other significant transactions.

Our credit agreement and certain other of our debt instruments include financial measure requirements that if breached may result in limitations on a number of our activities, including our ability to:

| · | create liens on our assets or make guarantees; |

| · | make certain investments or loans; |

| · | dispose of or sell assets or enter into a merger or similar transaction. |

These debt covenants could restrict our ability to pursue opportunities to expand our business operations, including engaging in strategic acquisitions. In addition, a violation of covenants under our credit facilities could cause a cross-default under our interest rate swap contract or other financial agreements. A cross-default under our interest rate swap could accelerate our obligation to perform under the terms of the interest rate swap contract.

Because our common stock is thinly traded, its market price may fluctuate significantly more than the stock market in general or the stock prices of similar companies, which are exchanged, listed or quoted on NASDAQ. We believe there are 4,375,894 shares of our Class A common stock held by nonaffiliates as of December 5, 2008. Thus, our common stock will be less liquid than the stock of companies with broader public ownership, and as a result, the trading prices for our shares of common stock may be more volatile. Among other things, trading of a relatively small volume of our common stock may have a greater impact on the trading price for our stock than would be the case if our public float were larger.

| ITEM 1B. | UNRESOLVED STAFF COMMENTS |

None.

The Company maintains both leased and owned manufacturing, warehousing, distribution and office facilities throughout the world. The Company believes that its manufacturing, warehousing, distribution, and office facilities are well maintained and have capacity adequate to meet its current needs.

See Note 5 to the Consolidated Financial Statements included elsewhere in this report for a discussion of the Company’s lease obligations.

The Company’s principal manufacturing (identified with an asterisk) and other locations are:

| Alpharetta, Georgia (Marine Electronics) |

| Antibes, France (Diving) |

| Barcelona, Spain (Diving) |

| Basingstoke, Hampshire, England (Diving) |

| Batam, Indonesia* (Diving and Outdoor Equipment) |

| Binghamton, New York* (Outdoor Equipment) |

| Brignais, France (Watercraft) |

| Brussels, Belgium (Diving) |

| Burlington, Ontario, Canada (Marine Electronics, Outdoor Equipment) |

| Chai Wan, Hong Kong (Diving) |

| Chatswood, Australia (Diving) |

| El Cajon, California (Diving) |

| Eufaula, Alabama* (Marine Electronics) |

| Ferndale, Washington* (Watercraft) |

| Genoa, Italy* (Diving) |

| Great Yarmouth, Norfolk, United Kingdom (Watercraft) |

| Hallwil, Switzerland (Diving) |

| Henggart, Switzerland (Diving) |

| Mankato, Minnesota* (Marine Electronics) |

| Napier, New Zealand* (Watercraft) |

| Old Town, Maine* (Watercraft) |

Silverdale, New Zealand* (Watercraft) Viareggio, Italy (Marine Electronics) |

| Wendelstein, Germany (Diving) |

| Yokohama, Japan (Diving) |

| |

The Company’s corporate headquarters is leased and located in Racine, Wisconsin.

See Note 14 to the Consolidated Financial Statements included elsewhere in this report for a discussion of legal proceedings.

| ITEM 4. | SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS |

No matters were submitted to a vote of security holders during the fourth quarter of the fiscal year ended October 3, 2008.

PART II

| ITEM 5. | MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

Certain information with respect to this item is included in Notes 9 and 10 to the Company's Consolidated Financial Statements included elsewhere in this report. The Company’s Class A common stock is traded on the NASDAQ Global MarketSM under the symbol: JOUT. There is no public market for the Company’s Class B common stock. However, the Class B common stock is convertible at all times at the option of the holder into shares of Class A common stock on a share for share basis. As of December 16, 2008, the Company had 735 holders of record of its Class A common stock and 35 holders of record of its Class B common stock. We believe the number of beneficial owners of our Class A common stock on that date was substantially greater.

A summary of the high and low prices for the Company’s Class A common stock during each quarter of the years ended October 3, 2008 and September 28, 2007 is as follows:

| | | First Quarter | | | Second Quarter | | | Third Quarter | | | Fourth Quarter | |

| | | 2008 | | | 2007 | | | 2008 | | | 2007 | | | 2008 | | | 2007 | | | 2008 | | | 2007 | |

Stock prices: | | | | | | | | | | | | | | | | | | | | | | | | |

| High | | $ | 23.50 | | | $ | 19.13 | | | $ | 22.50 | | | $ | 18.83 | | | $ | 17.77 | | | $ | 20.25 | | | $ | 16.06 | | | $ | 23.91 | |

| Low | | | 21.44 | | | | 17.06 | | | | 16.00 | | | | 17.00 | | | | 15.40 | | | | 18.02 | | | | 12.40 | | | | 17.00 | |

In fiscal 2008 and 2007, the Company declared the following dividends:

| · | A cash dividend declared on June 14, 2007, with a record date of July 12, 2007, payable on July 26, 2007 of $0.055 per share to Class A common stockholders and $0.05 per share to Class B common stockholders. |

| · | A cash dividend declared on September 19, 2007, with a record date of October 11, 2007, payable on October 25, 2007 of $0.055 per share to Class A common stockholders and $0.05 per share to Class B common stockholders. |

| · | A cash dividend declared on December 7, 2007, with a record date of January 10, 2008, payable on January 25, 2008 of $0.055 per share to Class A common stockholders and $0.05 per share to Class B common stockholders. |

| · | A cash dividend declared on February 28, 2008, with a record date of April 10, 2008, payable on April 24, 2008 of $0.055 per share to Class A common stockholders and $0.05 per share to Class B common stockholders. |

| · | A cash dividend declared on May 28, 2008, with a record date of July 10, 2008, payable on July 24, 2008 of $0.055 per share to Class A common stockholders and $0.05 per share to Class B common stockholders. |

| · | A cash dividend declared on October 1, 2008, with a record date of October 16, 2008, payable on October 30, 2008 of $0.055 per share to Class A common stockholders and $0.05 per share to Class B common stockholders. |

The following limitations apply to the ability of the Company to pay dividends:

| · | Pursuant to the Company’s revolving credit agreement, dated as of October 7, 2005, by and among the Company, the subsidiary borrowers from time to time parties thereto and JPMorgan Chase Bank N.A., the Company is limited in the amount of restricted payments (primarily dividends and purchases of treasury stock) made during each fiscal year. The limitation was approximately $27 million for the fiscal year ending October 3, 2008. |

| · | The Company’s Articles of Incorporation provide that no dividend, other than a dividend payable in shares of the Company’s common stock, may be declared or paid upon the Class B common stock unless such dividend is declared or paid upon both classes of common stock. Whenever a dividend (other than a dividend payable in shares of Company common stock) is declared or paid upon any shares of Class B common stock, at the same time there must be declared and paid a dividend on shares of Class A common stock equal in value to 110% of the amount per share of the dividend declared and paid on shares of Class B common stock. Whenever a dividend is payable in shares of Company common stock, such dividend must be declared or paid at the same rate on the Class A common stock and the Class B common stock. |

On December 4, 2008, the Company’s Board of Directors voted to suspend quarterly dividends to shareholders.

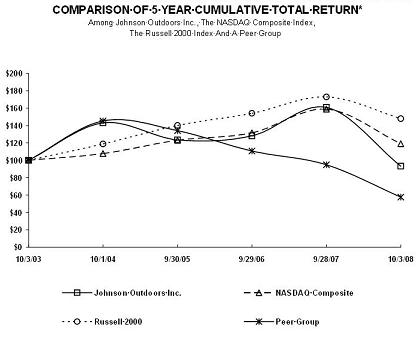

Total Shareholder Return

The graph below compares on a cumulative basis the yearly percentage change since October 3, 2003 in the total return (assuming reinvestment of dividends) to shareholders on the Class A common stock with (a) the total return (assuming reinvestment of dividends) on The NASDAQ Stock Market-U.S. Index; (b) the total return (assuming reinvestment of dividends) on the Russell 2000 Index; and (c) the total return (assuming reinvestment of dividends) on a self-constructed peer group index. The peer group consists of Arctic Cat Inc., Brunswick Corporation, Callaway Golf Company, Escalade Inc., Marine Products Corporation and Nautilus, Inc. The graph assumes $100 was invested on October 3, 2003 in the Company’s Class A common stock, The NASDAQ Stock Market-U.S. Index, the Russell 2000 Index and the peer group indices.

| | | | | | | |

| | 10/3/03 | 10/1/04 | 9/30/05 | 9/29/06 | 9/28/07 | 10/3/08 |

| Johnson Outdoors | 100.00 | 142.96 | 123.41 | 128.07 | 160.85 | 93.21 |

| NASDAQ Composite | 100.00 | 107.74 | 123.03 | 131.60 | 158.88 | 119.05 |

| Russell 2000 Index | 100.00 | 118.77 | 140.09 | 154.00 | 173.00 | 147.94 |

| Peer Group | 100.00 | 145.24 | 134.04 | 110.69 | 94.86 | 57.47 |

The information in this section titled “Total Shareholder Return” shall not be deemed to be “soliciting material” or “filed” with the Securities and Exchange Commission or subject to Regulation 14A or 14C promulgated by the Securities and Exchange Commission or subject to the liabilities of section 18 of the Securities Exchange Act of 1934, as amended, and this information shall not be deemed to be incorporated by reference into any filing under the Securities Act of 1933, as amended, or the Securities Exchange Act of 1934, as amended.

ITEM 6. SELECTED CONSOLIDATED FINANCIAL DATA

The following table presents selected consolidated financial data, which should be read along with the Company’s consolidated financial statements and the notes to those statements and with “Item 7 – Management’s Discussion and Analysis of Financial Condition and Results of Operations” included or referred to elsewhere in this report. The consolidated statements of operations for the years ended October 3, 2008, September 28, 2007 and September 29, 2006, and the consolidated balance sheet data as of October 3, 2008 and September 28, 2007, are derived from the Company’s audited consolidated financial statements included elsewhere herein. The consolidated statements of operations for the years ended September 30, 2005 and October 1, 2004, and the consolidated balance sheet data as of September 29, 2006, September 30, 2005 and October 1, 2004, are derived from the Company’s audited consolidated financial statements which are not included herein.

(thousands, except per share data) | | October 3 2008 | (6) | | September 28 2007 | (7) | | September 29 2006 | (8) | | September 30 2005 | | | October 1 2004 | |

Operating Results(1) | | | | | | | | | | | | | | | |

| Net sales | | $ | 420,789 | | | $ | 430,604 | | | $ | 393,950 | | | $ | 377,146 | | | $ | 351,813 | |

| Gross profit | | | 159,551 | | | | 175,496 | | | | 165,277 | | | | 155,678 | | | | 146,511 | |

Operating expenses (2) | | | 197,604 | | | | 155,470 | | | | 141,918 | | | | 137,216 | | | | 127,813 | |

Operating (loss) profit | | | (38,053 | ) | | | 20,026 | | | | 23,359 | | | | 18,462 | | | | 18,698 | |

| Interest expense | | | 5,695 | | | | 5,162 | | | | 4,989 | | | | 4,792 | | | | 5,283 | |

| Other expense (income) | | | 549 | | | | (931 | ) | | | (128 | ) | | | (1,250 | ) | | | (670 | ) |

(Loss) Income before income taxes | | | (44,297 | ) | | | 15,795 | | | | 18,498 | | | | 14,920 | | | | 14,085 | |

Income tax expense (3) | | | 24,178 | | | | 5,246 | | | | 8,061 | | | | 6,044 | | | | 5,806 | |

| (Loss) Income from continuing operations | | | (68,475 | ) | | | 10,549 | | | | 10,437 | | | | 8,876 | | | | 8,279 | |

| (Loss) Income from discontinued operations | | | (2,559 | ) | | | (1,315 | ) | | | (1,722 | ) | | | (1,775 | ) | | | 410 | |

Net (Loss) Income | | $ | (71,034 | ) | | $ | 9,234 | | | $ | 8,715 | | | $ | 7,101 | | | $ | 8,689 | |

Balance Sheet Data | | | | | | | | | | | | | | | | | | | | |

Current assets (4) | | $ | 189,714 | | | $ | 205,221 | | | $ | 185,290 | | | $ | 186,591 | | | $ | 194,847 | |

| Total assets | | | 255,069 | | | | 319,679 | | | | 284,227 | | | | 283,326 | | | | 293,719 | |

Current liabilities (5) | | | 55,386 | | | | 66,260 | | | | 57,651 | | | | 55,457 | | | | 59,115 | |

| Long-term debt, less current maturities | | | 60,000 | | | | 10,006 | | | | 20,807 | | | | 37,800 | | | | 50,797 | |

| Total debt | | | 60,003 | | | | 42,806 | | | | 37,807 | | | | 50,800 | | | | 67,019 | |

Shareholders’ equity | | | 122,284 | | | | 200,165 | | | | 180,881 | | | | 166,434 | | | | 160,644 | |

Common Share Summary | | | | | | | | | | | | | | | | | | | | |

Earnings per share, continuing operations – Dilutive: | | | | | | | | | | | | | | | | | | | | |

Class A | | $ | (7.53 | ) | | $ | 1.14 | | | $ | 1.14 | | | $ | 1.01 | | | $ | 0.94 | |

Class B | | $ | (7.53 | ) | | $ | 1.14 | | | $ | 1.14 | | | $ | 1.01 | | | $ | 0.94 | |

Net earnings per share – Dilutive: | | | | | | | | | | | | | | | | | | | | |

Class A | | $ | (7.81 | ) | | $ | 1.00 | | | $ | 0.95 | | | $ | 0.81 | | | $ | 0.99 | |

Class B | | $ | (7.81 | ) | | $ | 1.00 | | | $ | 0.95 | | | $ | 0.81 | | | $ | 0.99 | |

Cash dividends per share: | | | | | | | | | | | | | | | | | | | | |

| Class A | | $ | 0.22 | | | $ | 0.11 | | | $ | 0.00 | | | $ | 0.00 | | | $ | 0.00 | |

| Class B | | $ | 0.20 | | | $ | 0.10 | | | $ | 0.00 | | | $ | 0.00 | | | $ | 0.00 | |

| (1) | The year ended October 3, 2008 included 53 weeks. All other years include 52 weeks. |

| (2) | The year ended October 3, 2008 includes goodwill and other impairment charges of $41.0 million. |

| (3) | The year ended October 3, 2008 includes a deferred tax asset valuation allowance of $29.5 million. |

| (4) | Includes cash and cash equivalents of $41,791, $39,232, $51,689, $72,111 and $69,572, as of the years ended 2008, 2007, 2006, 2005 and 2004, respectively. |

| (5) | Excluding short-term debt and current maturities of long-term debt. |

| (6) | The results in 2008 contain approximately ten months of operating results of the acquired Geonav business and a full year of operating results of the acquired Seemann business. |

| (7) | The results in 2007 contain a full year of operating results of the acquired Lendal Products Ltd. business and six months of operating results of the acquired Seemann business. |

| (8) | The results in 2006 contain a full year of operating results of the acquired Cannon/Bottom Line business. |

| ITEM 7. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

The Company designs, manufactures and markets top-quality recreational products for the outdoor enthusiast. Through a combination of innovative products, strong marketing, a talented and passionate workforce and efficient distribution, the Company sets itself apart from the competition. Its subsidiaries operate as a network that promotes entrepreneurialism and leverages best practices and synergies, following the strategic vision set by executive management and approved by the Company’s Board of Directors.

Recent Developments

The Company’s senior debt agreement in place at October 3, 2008 requires that it meet certain operating requirements and financial ratios in order to avoid a default or event of default under the agreement. The Company was in non-compliance with its net worth covenant at October 3, 2008. On December 31, 2008, the Company entered into an amended financing arrangement with its lenders, effective January 2, 2009. Changes to the senior debt agreement include shortening the maturity date of the term loan, adjusting financial covenants and interest rates. Additionally, the Company’s revolving credit facility was reduced from $75.0 million to $35.0 million, with an additional reduction of $5.0 million required by January 31, 2009. Due to the fact the Company has entered into this amended agreement, the Company’s debt has been classified as long-term at October 3, 2008, in accordance with the terms of the amended debt agreement. See further information regarding the Company’s indebtedness at Note 4 to the Consolidated Financial Statements included elsewhere in this report.

On December 29, 2008, the Company and JPMorgan Chase (“the Counterparty”) agreed to amend the terms of its $60.0 million LIBOR interest rate swap (“the Swap”) contract to include an automatic termination clause. The Company and the Counterparty are negotiating a modification of the terms of the Swap to accommodate the new debt agreements. If the Company and the Counterparty cannot agree to acceptable modification terms, the Swap will automatically terminate on January 8, 2009. Early termination of the Swap would require the Company and the Counterparty to settle their respective obligations to each other under the Swap contract terms. If such a termination had occurred on December 29, 2008, it would have required the Company to pay the Counterparty approximately $6.5 million, which was the fair value of the Swap on that date. If the Swap were to terminate on January 8, 2009, the amount required to be paid by the Company to settle this contract could be materially different.

As of October 3, 2008, the Company recorded a non-cash charge for impairment of goodwill and other indefinite lived intangible assets of $41.0 million related to all four of the Company’s business segments based on assessments performed in the fourth quarter of fiscal 2008. In accordance with Statement of Financial Accounting Standards No. 142, Accounting for Goodwill and Other Intangible Assets (“SFAS No. 142”), we are required to test goodwill and other indefinite lived intangible assets at least annually for impairment. We determined that as of October 3, 2008, portions of our goodwill and portions of our indefinite lived intangible assets were impaired due to our expectations of lower future profitability and increases in our cost of capital.

During 2008, the Company recorded a valuation allowance of $29.5 million in respect of the net deferred tax assets recorded in our U.S., Germany, Spain, United Kingdom and New Zealand tax jurisdictions. Given the current market conditions of the outdoor recreation equipment market as well as other factors arising during fiscal 2008 which may impact future operating results, the Company considered both positive and negative evidence in evaluating the need for a valuation allowance relating to the deferred tax assets of these tax jurisdictions. The Company determined that it was more likely than not that the deferred tax assets will not be realized and a valuation allowance of $29.2 million, $1.8 million, $0.2 million, $0.4 million and $0.1 million was recorded against the net deferred tax assets in the U.S., Germany, Spain, United Kingdom, and New Zealand tax jurisdictions respectively.

On December 17, 2007, management committed to divest the Company’s Escape business. This decision resulted in the reporting of the Escape business as a discontinued operation in the current year and the reclassification of the results of this business as discontinued operations for comparable reporting periods. Individual lines of boats in this business have either been sold or are in the process of being divested. The Company will continue to explore strategic alternatives for the remaining lines of the Escape business through the first quarter of 2009 at which point we expect to have either sold or otherwise disposed of the remaining assets of the Escape business. We believe we have adequately reserved for any losses that could result from the disposal of the remaining lines.

Summary consolidated financial results from continuing operations for the fiscal years presented were as follows:

(millions, except per share data) | | 2008 | (2) | | 2007 | (3) | | 2006 | |

Operating Results | | | | | | | | | |

Net sales | | $ | 420.8 | | | $ | 430.6 | | | $ | 394.0 | |

| Gross profit | | | 159.6 | | | | 175.5 | | | | 165.3 | |

| Impairment charges | | | 41.0 | | | | — | | | | — | |

| Other operating expenses | | | 156.7 | | | | 155.5 | | | | 141.9 | |

| Operating (loss) profit | | | (38.1 | ) | | | 20.0 | | | | 23.4 | |

| Interest expense | | | 5.7 | | | | 5.2 | | | | 5.0 | |

| (Loss) income from continuing operations | | | (68.5 | ) | | | 10.5 | | | | 10.4 | |

Net (loss) income (1) | | | (71.0 | ) | | | 9.2 | | | | 8.7 | |

(1) The results of 2008 contain a deferred tax asset valuation allowance of $29.5 million.

(2) The results of 2008 contain a full year of operating results of the acquired Seemann business and approximately ten months of operating results of the acquired Geonav business.

(3) The results in 2007 contain a full year of operating results of the acquired Lendal Products Ltd. business and six months of operating results of the acquired Seemann business.

The Company’s sales and operating earnings by business segment are summarized as follows:

(millions) | | 2008 | | | 2007 | | | 2006 | |

Net sales: | | | | | | | | | |

| Marine Electronics | | $ | 186.7 | | | $ | 198.0 | | | $ | 164.5 | |

| Outdoor Equipment | | | 48.3 | | | | 55.9 | | | | 65.9 | |

| Watercraft | | | 88.1 | | | | 88.8 | | | | 85.5 | |

| Diving | | | 98.2 | | | | 88.7 | | | | 78.5 | |

| Other/corporate/eliminations | | | (0.5 | ) | | | (0.8 | ) | | | (0.4 | ) |

Total | | $ | 420.8 | | | $ | 430.6 | | | $ | 394.0 | |

Operating profit (loss): | | | | | | | | | | | | |

| Marine Electronics | | $ | 0.4 | | | $ | 22.9 | | | $ | 21.6 | |

| Outdoor Equipment | | | 2.0 | | | | 8.5 | | | | 8.2 | |

| Watercraft | | | (8.3 | ) | | | (4.2 | ) | | | 0.2 | |

| Diving | | | (21.5 | ) | | | 6.9 | | | | 5.6 | |

| Other/corporate/eliminations | | | (10.7 | ) | | | (14.1 | ) | | | (12.2 | ) |

Total | | $ | (38.1 | ) | | $ | 20.0 | | | $ | 23.4 | |

See Note 12 in the notes to the Consolidated Financial Statements included elsewhere in this report for the definition of segment net sales and operating profit.

Fiscal 2008 vs Fiscal 2007

Net sales totaled $420.8 million in 2008 compared to $430.6 million in 2007, a decrease of 2.3% or $9.8 million. Sales declined in all but the Company’s Diving business unit. Foreign currency translations favorably impacted 2008 net sales by $9.6 million in comparison to 2007.

Net sales for the Marine Electronics business decreased $11.3 million, or 5.7%, despite incremental sales from the Geonav business, acquired in November, 2007, which added $12.4 million in sales for the year. The decline was primarily the result of general economic conditions and weakness in the domestic boat market which reduced demand for trolling motors and downriggers, and unfavorable volume comparisons due to high levels of new product purchases by customers in the prior year. This weakness was partially offset by higher sales of Humminbird fishfinder/GPS combo units.

Outdoor Equipment net sales declined $7.6 million, or 13.6%, primarily due to the expected $6.6 million decline in military tent sales. Commercial tent sales were also down from the prior year by $1.2 million due to softness in the U.S. economy driving cautious spending by tent rental companies.

Net sales for the Watercraft business decreased $0.7 million, or 0.8%, as a result of a decline in sales to big-box retailers in light of unfavorable weather conditions and economic uncertainty in the retail marketplace. This decline was partially offset by an increase in sales to outdoor specialty stores driven mainly by the timing of orders in the prior year.

The Diving business saw increased sales of $9.5 million, or 10.7%, due mainly to $4 million of incremental sales related to the Seemann business acquired in April, 2007, and $6.7 million of favorable currency translations.

Gross Profit

Gross profit of $159.6 million was 37.9% of net sales on a consolidated basis for the year ended October 3, 2008 compared to $175.5 million or 40.8% of net sales in the prior year.

Gross profit in the Marine Electronics business declined $11.2 million, from 37.5% of net sales in 2007 to 33.8% of net sales in the current year. The incremental Geonav gross profit of $2.8 million was more than offset by the effects of unfavorable overhead expense absorption due to lower production volumes for electric motors and downriggers and an unfavorable product mix. In addition, as a result of the weak consumer demand, reserves for excess and obsolete inventory increased by $1.8 million over the prior year.

Gross profit in the Outdoor Equipment business declined $3.9 million from 34.0% of net sales in 2007 to 31.3% of net sales in the current year due largely to unfavorable product mix and lower production volumes of government and commercial tents.

Gross profit in the Watercraft segment of 34.4% of net sales in 2008 was $3.9 million less than 2007 levels at 38.5% of net sales due primarily to lower volume and related operating inefficiencies, closeout pricing, and $1.2 million of increased material costs. In addition, the Company recorded an additional reserve of $1.0 million for excess and obsolete inventory in 2008 compared to 2007 as a result of lower sales and the Company’s efforts to reduce the number of unique inventory items.

Gross profit for the Diving segment increased by $3.1 million but decreased as a percent of net sales from 53.6% in 2007 to 51.6% in 2008 due largely to currency impacts on purchased product and close out sales on end-of-life products.

Operating Expenses

During fiscal 2008, the Company recorded an impairment charge of $41.0 million related to goodwill and other indefinite lived intangible assets. Excluding the impairment charge, operating expenses in 2008 would have been $156.6 million as compared to $155.5 million in 2007.

Goodwill impairment charges of $7.2 million and $7.4 million of operating expenses generated by the newly acquired Geonav business were recognized in the Marine Electronics segment during 2008. All other operating expenses decreased $3.2 million from the prior year. This decrease was due mainly to the decrease in bonus, profit sharing and other incentive compensation of $2.7 million, partially offset by increased warranty expense.

Outdoor Equipment operating expenses increased by $2.7 million from the prior year due primarily to a goodwill impairment charge of $0.6 million in the current year and the favorable impact in the prior year of $2.9 million of insurance recoveries related to the flood at the Company’s facility in Binghamton, New York in 2006.

The Company recorded a goodwill impairment charge of $6.2 million in 2008 related to the Watercraft business. Other operating expenses in the Watercraft business decreased by $6.0 million due primarily to the impact of a $4.4 million legal settlement recorded in the prior year and the reduction of bonus, profit sharing and other incentive compensation expense in the current year.

An impairment charge of $27.0 million was included in the Diving business operating expenses for 2008. Other Diving operating expenses increased $4.6 million from the prior year due to $2.5 million of restructuring costs incurred related to the relocation of dive computer manufacturing and $3.4 million due to currency impacts, offset by decreased bonus, profit sharing and other incentive compensation expenses.

Operating Results

The Company recognized an operating loss of $38.1 million in 2008 compared to an operating profit of $20 million in fiscal 2007. Primary factors driving the decrease in operating profit margins were the goodwill impairment loss, the underabsorption of overhead expenses due to significantly lower production volumes as well as higher raw material costs, close out pricing and additional inventory reserves on slow moving inventory. Operating expenses totaled $197.6 million, or 47.0% of net sales in fiscal 2008 compared to $155.5 million or 36.1% of net sales in fiscal 2007. Marine Electronics operating profit decreased by $22.5 million, or 98.2%, in fiscal 2008 from the prior year. Outdoor Equipment operating profit decreased $6.5 million, or 76.5%. Watercraft operating loss worsened by $4.1 million from the prior year. Diving operating profit turned into a loss of $21.5 million, a $28.4 million decrease from the prior year amount.

Other Income and Expenses

Interest income remained consistent with the prior year at $0.8 million in fiscal 2008. Interest expense increased $0.5 million from 2007 to $5.7 million in 2008, due largely to higher long term borrowings incurred to fund higher working capital needs. The Company realized currency losses of $1.9 million in fiscal 2008 as compared to $0.6 million in fiscal 2007. The increase was primarily due to significant weakening of the U.S. dollar against the Swiss franc and the euro.

Pretax Income and Income Taxes

The Company recognized a pretax loss of $44.3 million in fiscal 2008, compared to pretax income of $15.8 million in fiscal 2007. The Company recorded income tax expense of $24.2 million in fiscal 2008, an effective rate of (54.6%), compared to $5.2 million in fiscal 2007, an effective rate of 33.2%. The 2008 expense includes a valuation allowance of $29.5 million in respect of deferred tax assets in the U.S. and certain foreign tax jurisdictions. The effective tax rate for 2007 benefited from a German tax law change, an increased tax rate used to record federal deferred tax assets and research and development tax credits.

Loss from Continuing Operations

The loss from continuing operations was $68.5 million for the year compared to income of $10.5 million in the prior year as a result of the fluctuations discussed above.

Loss from Discontinued Operations

On December 17, 2007, the Company’s management committed to a plan to divest the Company’s Escape business and is continuing to explore strategic alternatives for its Escape brand products. In accordance with the provisions of Statement of Financial Accounting Standards (SFAS) No. 144, Accounting for the Impairment or Disposal of Long-Lived Assets (SFAS No. 144), the results of operations of the Escape business have been reported as discontinued operations in the consolidated statements of operations for the fiscal years ended October 3, 2008, September 28, 2007, and September 29, 2006 and in the consolidated balance sheets as of October 3, 2008 and September 28, 2007. The Company recorded after tax losses related to the discontinued Escape business of $2.6 million and $1.3 million for 2008 and 2007, respectively.

The Company recognized a net loss of $71.0 million in fiscal 2008, or $7.81 per diluted share, compared to net income of $9.2 million in fiscal 2007, or $1.00 per diluted share.

Fiscal 2007 vs Fiscal 2006

Net sales totaled a record $430.6 million in 2007 compared to $394.0 million in 2006, an increase of 9.3% or $36.6 million. Foreign currency translations favorably impacted 2007 net sales by $3.9 million in comparison to 2006. Sales growth in the Company’s Marine Electronics, Watercraft and Diving business units overcame a decline in the Outdoor Equipment business unit.

Net sales for the Marine Electronics business increased $33.5 million, or 20.4% primarily due to the successful launch of new products across the Marine Electronics brands. Net sales for the Company’s Watercraft business increased $3.3 million, or 3.9%, as a result of new product introductions and product offerings in the U.S. and improved volumes in international markets. Net sales for the Diving business increased $10.2 million, or 13.0% primarily due to an increase of $4.6 million from the acquired Seemann Sub business, increased volume in Europe and the far east and a $2.8 million favorable currency translation. Net sales in the Company’s Outdoor Equipment business declined $10.0 million, or 15.2%, primarily due to the expected decline in total military tent sales and a $5.3 million decline in specialty market sales. The declines in military tent sales and specialty market sales were partially offset by strong sales in the Consumer and Commercial businesses.

Operating Results

The Company recognized an operating profit of $20.0 million in fiscal 2007 compared to an operating profit of $23.4 million in fiscal 2006. Company gross profit margins decreased to 40.8% in fiscal 2007 from 42.0% in fiscal 2006. Primary factors driving the decrease in gross profit margins were production inefficiencies in Marine Electronics and Diving supply chain challenges in Europe. Operating expenses totaled $155.5 million, or 36.1% of net sales in fiscal 2007 compared to $141.9 million, or 36.0% of net sales in fiscal 2006.

Marine Electronics operating profit improved by $1.3 million, or 6.2%, in fiscal 2007 from the prior year. The increase was primarily driven by favorable net sales volume on successful launch of new products across the Marine Electronics brands, slightly offset by increased labor due to production inefficiencies incurred in meeting higher new product demand.

Outdoor Equipment operating profit increased $0.2 million, or 2.8%, mainly due to the insurance recoveries related to the 2006 Binghamton, New York flood. The Company recognized gains on the recoveries of $2.9 million compared to losses incurred in the prior year of $1.5 million. No additional costs or recoveries are expected related to this event. Without the insurance recoveries the Outdoor Equipment business operating profit would have declined as a result of lower military tent sales and $5.3 million of specialty market sales occurring in 2006 which did not recur in 2007.

Watercraft operating profit of $0.2 million in 2006 decreased by $4.4 million to an operating loss of $4.2 million for fiscal 2007. However fiscal 2007 operating losses for this segment included a one-time legal settlement of $4.4 million. Nonetheless, Watercraft saw improvements in its core Paddlesports business.

Diving operating profit increased by $1.3 million, or 23.7%, due primarily to operating profit provided by the acquired Seemann Sub business along with improved profitability on increased sales volume in far east markets. Additionally, the Diving business incurred $0.6 million in restructuring costs related to the closure of its Wendelstein, Germany facility.

Other Income and Expenses

Interest income in 2007 increased $0.2 million to $0.7 million in fiscal 2007. Interest expense increased $0.2 million to $5.2 million. Favorability resulting from lower amounts of term debt outstanding for the year was offset by higher short term borrowings incurred to fund working capital needs. The Company realized currency losses of $0.6 million in fiscal 2007 as compared to $0.2 million in fiscal 2006.

Pretax Income and Income Taxes

The Company recognized pretax income of $15.8 million in fiscal 2007, compared to $18.5 million in fiscal 2006. The Company recorded income tax expense of $5.2 million in fiscal 2007, an effective rate of 33.2%, compared to $8.1 million in fiscal 2006, an effective rate of 43.6%. The effective tax rate for 2007 benefited from a German tax law change, an increased tax rate used to record federal deferred tax assets and research and development tax credits.

Loss from Continuing Operations

The income from continuing operations was $10.5 million for the year compared to income of $10.4 million in the prior year as a result of the fluctuations discussed above.

Loss from Discontinued Operations

On December 17, 2007, the Company’s management committed to a plan to divest the Company’s Escape business and is continuing to explore strategic alternatives for its Escape brand products. In accordance with the provisions of Statement of Financial Accounting Standards (SFAS) No. 144, Accounting for the Impairment or Disposal of Long-Lived Assets (SFAS No. 144), the results of operations of the Escape business have been reported as discontinued operations in the consolidated statements of operations for the fiscal years ended October 3, 2008, September 28, 2007, and September 29, 2006 and in the consolidated balance sheets as of October 3, 2008 and September 28, 2007. The Company recorded after tax losses related to the discontinued Escape business of $1.3 million and $1.7 million for 2007 and 2006, respectively.

The Company recognized net income of $9.2 million in fiscal 2007, or $1.00 per diluted share, compared to net income of $8.7 million in fiscal 2006, or $0.95 per diluted share.

Financial Condition, Liquidity and Capital Resources

The Company’s cash flow from operating, investing and financing activities, as reflected in the consolidated statements of cash flows, is summarized in the following table:

(millions) | | 2008 | | | 2007 | | | 2006 | |

Cash provided by (used for): | | | | | | | | | |

| Operating activities | | $ | 4.9 | | | $ | 0.6 | | | $ | 7.5 | |

| Investing activities | | | (18.2 | ) | | | (22.0 | ) | | | (18.6 | ) |

| Financing activities | | | 15.5 | | | | 5.3 | | | | (12.8 | ) |

Effect of exchange rate changes | | | 0.4 | | | | 3.6 | | | | 3.5 | |

Increase (decrease) in cash and temporary cash investments | | $ | 2.6 | | | $ | (12.5 | ) | | $ | (20.4 | ) |

The following table sets forth the Company’s working capital position at the end of each of the past three years:

(millions) | | 2008 | | | 2007 | | | 2006 | |

Current assets (1) | | $ | 189.7 | | | $ | 205.2 | | | $ | 185.3 | |

Current liabilities (2) | | | 55.4 | | | | 66.3 | | | | 57.7 | |

Working capital (2) | | $ | 134.3 | | | $ | 138.9 | | | $ | 127.6 | |

Current ratio (2) | | 3.4:1 | | | 3.1:1 | | | 3.2:1 | |

| (1) | 2008, 2007 and 2006 information includes cash and cash equivalents of $41.8, $39.2 and $51.7 million, respectively. |

| (2) | Excludes short-term debt and current maturities of long-term debt. |

Cash flows provided by operations totaled $4.9 million, $0.6 million and $7.5 million in fiscal 2008, 2007 and 2006, respectively. The major driver in the increase in cash flows from operations in fiscal 2008 was a decline in accounts receivable due to collections of prior year receivables and lower sales in fiscal 2008 partially offset by fiscal 2007 incentive compensation paid out in fiscal 2008 and income tax payments.

The major driver in the decline of cash flows from operations in fiscal 2007 was created by an increase in working capital. Increases in accounts receivable of $3.1 million and inventory of $22.6 million were offset by increases in accounts payable and other accrued liabilities of $5.4 million, all of which reflect the increase in working capital in fiscal 2007.

Depreciation and amortization charges were $10.1 million in fiscal 2008, $9.4 million in fiscal 2007 and $9.2 million in fiscal 2006.

Cash flows used for investing activities were $18.2 million, $22.0 million and $18.6 million in fiscal 2008, 2007 and 2006, respectively. The acquisition of Geonav used $5.6 million of cash in fiscal 2008. The acquisition of Lendal used $1.5 million of cash in fiscal 2007. The acquisition of Seemann used $0.7 million and $7.9 million of cash in fiscal 2008 and 2007, respectively. The acquisition of Cannon/Bottom Line used $9.9 million of cash in fiscal 2006. Expenditures for property, plant and equipment were $12.4 million, $13.4 million, $8.9 million in fiscal 2008, 2007 and 2006, respectively. In general, the Company’s ongoing expenditures are primarily related to tooling for new products and facilities and information systems improvements.

Financing Activities

The following table sets forth the Company’s debt and capital structure at the end of the past three fiscal years:

(millions) | | 2008 | | | 2007 | | | 2006 | |

Current debt | | $ | — | | | $ | 32.8 | | | $ | 17.0 | |

| Long-term debt | | | 60.0 | | | | 10.0 | | | | 20.8 | |

Total debt | | | 60.0 | | | | 42.8 | | | | 37.8 | |

| Shareholders’ equity | | | 122.3 | | | | 200.2 | | | | 180.9 | |

Total capitalization | | $ | 182.3 | | | $ | 243.0 | | | $ | 218.7 | |