UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

100 F ST., N.E.

WASHINGTON, D.C. 20549

FORM 10-K

(Mark One)

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

FOR THE FISCAL YEAR ENDED DECEMBER 31, 2010,

OR

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

FOR THE TRANSITION PERIOD FROM TO

| | | | |

Commission

File Number | | Registrants, State of Incorporation, Address, and Telephone Number | | I.R.S. Employer

Identification No. |

| 001-09120 | | PUBLIC SERVICE ENTERPRISE GROUP INCORPORATED | | 22-2625848 |

| | (A New Jersey Corporation) | | |

| | 80 Park Plaza, P.O. Box 1171 | | |

| | Newark, New Jersey 07101-1171 | | |

| | 973 430-7000 | | |

| | http://www.pseg.com | | |

| 001-34232 | | PSEG POWER LLC | | 22-3663480 |

| | (A Delaware Limited Liability Company) | | |

| | 80 Park Plaza—T25 | | |

| | Newark, New Jersey 07102-4194 | | |

| | 973 430-7000 | | |

| | http://www.pseg.com | | |

| 001-00973 | | PUBLIC SERVICE ELECTRIC AND GAS COMPANY | | 22-1212800 |

| | (A New Jersey Corporation) | | |

| | 80 Park Plaza, P.O. Box 570 | | |

| | Newark, New Jersey 07101-0570 | | |

| | 973 430-7000 | | |

| | http://www.pseg.com | | |

Securities registered pursuant to Section 12(b) of the Act:

| | | | |

Registrant | | Title of Each Class | | Name of Each Exchange On Which Registered |

Public Service Enterprise Group Incorporated | | Common Stock without par value | | New York Stock Exchange |

| PSEG Power LLC | | 8 5/8% Senior Notes, due 2031 | | New York Stock Exchange |

| | | First and Refunding Mortgage Bonds | | |

Public Service Electric and Gas Company | | 9 1/4% Series CC, due 2021 | | New York Stock Exchange |

| | 6 3/4% Series VV, due 2016 | | |

| | 8%, due 2037 | | |

| | 5%, due 2037 | | |

Securities registered pursuant to Section 12(g) of the Act:

| | |

Registrant | | Title of Each Class |

PSEG Power LLC Public Service Electric and Gas Company | | Limited Liability Company Membership Interest Medium-Term Notes, Series A, B, C, D, E, F and G |

| |

(Cover continued on next page)

(Cover continued from previous page)

Indicate by check mark whether each registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

| | | | |

| Public Service Enterprise Group Incorporated | | Yes x | | No ¨ |

| PSEG Power LLC | | Yes¨ | | Nox |

| Public Service Electric and Gas Company | | Yesx | | No¨ |

Indicate by check mark if each of the registrants is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. Yes¨ Nox

Indicate by check mark whether each of the registrants (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrants were required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yesx No¨

Indicate by check mark whether the registrants have submitted electronically and posted on their corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrants were required to submit and post such files).

| | | | |

| Public Service Enterprise Group Incorporated | | Yes x | | No ¨ |

| PSEG Power LLC | | Yes¨ | | No¨ |

| Public Service Electric and Gas Company | | Yes¨ | | No¨ |

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.¨

Indicate by check mark whether each registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | |

| | | | |

Public Service Enterprise Group Incorporated | | Large accelerated filer x | | | Accelerated filer ¨ | | | Non-accelerated filer¨ | | Smaller reporting company¨ |

| | | | |

PSEG Power LLC | | Large accelerated filer ¨ | | | Accelerated filer¨ | | | Non-accelerated filerx | | Smaller reporting company¨ |

| | | | |

Public Service Electric and Gas Company | | Large accelerated filer¨ | | | Accelerated filer¨ | | | Non-accelerated filerx | | Smaller reporting company¨ |

Indicate by check mark whether any of the registrants is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes¨ Nox

The aggregate market value of the Common Stock of Public Service Enterprise Group Incorporated held by non-affiliates as of June 30, 2010 was $15,837,199,627 based upon the New York Stock Exchange Composite Transaction closing price.

The number of shares outstanding of Public Service Enterprise Group Incorporated’s sole class of Common Stock as of January 31, 2011 was 506,039,601.

As of January 31, 2011, Public Service Electric and Gas Company had issued and outstanding 132,450,344 shares of Common Stock, without nominal or par value, all of which were privately held, beneficially and of record by Public Service Enterprise Group Incorporated.

PSEG Power LLC and Public Service Electric and Gas Company are wholly owned subsidiaries of Public Service Enterprise Group Incorporated and each meet the conditions set forth in General Instruction I(1)(a) and (b) of Form 10-K. Each is filing its Annual Report on Form 10-K with the reduced disclosure format authorized by General Instruction I.

DOCUMENTS INCORPORATED BY REFERENCE

| | |

Part of Form 10-K of

Public Service Enterprise Group Incorporated | | Documents Incorporated by Reference |

| III | | Portions of the definitive Proxy Statement for the 2011 Annual Meeting of Stockholders of Public Service Enterprise Group Incorporated, which definitive Proxy Statement is expected to be filed with the Securities and Exchange Commission on or about March 10, 2011, as specified herein. |

i

FORWARD-LOOKING STATEMENTS

Certain of the matters discussed in this report constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These include, but are not limited to, future performance, revenues, earnings, strategies, prospects, consequences and all other statements that are not purely historical. Such forward-looking statements are subject to risks and uncertainties, which could cause actual results to differ materially from those anticipated. Such statements are based on management’s beliefs as well as assumptions made by and information currently available to management. When used herein, the words “anticipate,” “intend,” “estimate,” “believe,” “expect,” “plan,” “should,” “hypothetical,” “potential,” “forecast,” “project,” variations of such words and similar expressions are intended to identify forward-looking statements. Factors that may cause actual results to differ are often presented with the forward-looking statements themselves. Other factors that could cause actual results to differ materially from those contemplated in any forward-looking statements made by us herein are discussed in Item 1A. Risk Factors, Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations (MD&A), Item 8. Financial Statements and Supplementary Data —Note 13. Commitments and Contingent Liabilities, and other factors discussed in filings we make with the United States Securities and Exchange Commission (SEC). These factors include, but are not limited to:

| • | | adverse changes in energy industry law, policies and regulation, including market structures and a potential shift away from competitive markets toward subsidized market mechanisms, transmission planning and cost allocation rules, including rules regarding how transmission is planned and who is permitted to build transmission going forward, and reliability standards, |

| • | | any inability of our transmission and distribution businesses to obtain adequate and timely rate relief and regulatory approvals from federal and state regulators, |

| • | | changes in federal and state environmental regulations that could increase our costs or limit operations of our generating units, |

| • | | changes in nuclear regulation and/or developments in the nuclear power industry generally that could limit operations of our nuclear generating units, |

| • | | actions or activities at one of our nuclear units located on a multi-unit site that might adversely affect our ability to continue to operate that unit or other units located at the same site, |

| • | | any inability to balance our energy obligations, available supply and trading risks, |

| • | | any deterioration in our credit quality, |

| • | | availability of capital and credit at commercially reasonable terms and conditions and our ability to meet cash needs, |

| • | | any inability to realize anticipated tax benefits or retain tax credits, |

| • | | changes in the cost of, or interruption in the supply of, fuel and other commodities necessary to the operation of our generating units, |

| • | | delays in receipt of necessary permits and approvals for our construction and development activities, |

| • | | delays or unforeseen cost escalations in our construction and development activities, |

| • | | adverse changes in the demand for or price of the capacity and energy that we sell into wholesale electricity markets, |

| • | | increase in competition in energy markets in which we compete, |

| • | | adverse performance of our decommissioning and defined benefit plan trust fund investments and changes in discount rates and funding requirements, and |

| • | | changes in technology and customer usage patterns. |

Additional information concerning these factors is set forth in Part I under Item 1A. Risk Factors.

All of the forward-looking statements made in this report are qualified by these cautionary statements and we cannot assure you that the results or developments anticipated by management will be realized, or even if realized, will have the expected consequences to, or effects on, us or our business prospects, financial condition or results of operations. Readers are cautioned not to place undue reliance on these forward-looking statements in making any investment decision. Forward-looking statements made in this report only apply as of the date of this report. While we may elect to update forward-looking statements from time to time, we specifically disclaim any obligation to do so, even if internal estimates change, unless otherwise required by applicable securities laws.

The forward-looking statements contained in this report are intended to qualify for the safe harbor provisions of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended.

ii

FILING FORMAT AND GLOSSARY

This combined Annual Report on Form 10-K is separately filed by Public Service Enterprise Group Incorporated (PSEG), PSEG Power LLC (Power) and Public Service Electric and Gas Company (PSE&G). Information relating to any individual company is filed by such company on its own behalf. Power and PSE&G are each only responsible for information about itself and its subsidiaries.

Discussions throughout the document refer to PSEG and its direct operating subsidiaries, Power, PSE&G and PSEG Energy Holdings L.L.C. (Energy Holdings). Depending on the context of each section, references to “we,” “us,” and “our” relate to the specific company or companies being discussed. In addition, certain key acronyms and definitions are summarized in a glossary beginning on page 211.

WHERE TO FIND MORE INFORMATION

We file annual, quarterly and special reports, proxy statements and other information with the U.S. Securities and Exchange Commission (SEC). You may read and copy any document that we file at the Public Reference Room of the SEC at 100 F Street, N.E., Washington, D.C. 20549. Information on the operation of the Public Reference Room may be obtained by calling the SEC at 1-800-SEC-0330. You may also obtain our filed documents from commercial document retrieval services, the SEC’s internet website at www.sec.gov or our website at www.pseg.com. Information on our website should not be deemed incorporated into or as a part of this report. Our Common Stock is listed on the New York Stock Exchange under the ticker symbol PEG. You can obtain information about us at the offices of the New York Stock Exchange, Inc., 20 Broad Street, New York, New York 10005.

PART I

ITEM 1. BUSINESS

We were incorporated under the laws of the State of New Jersey in 1985 and our principal executive offices are located at 80 Park Plaza, Newark, New Jersey 07102. We conduct our business through three direct wholly owned subsidiaries, Power, PSE&G and Energy Holdings, each of which also has its principal executive offices at 80 Park Plaza, Newark, New Jersey 07102. PSEG Services Corporation (Services), our wholly owned subsidiary, provides us and these operating subsidiaries with certain management, administrative and general services at cost.

As of and for the Year Ended December 31, 2010

1

We are an energy company with a diversified business mix. Our operations are located primarily in the Northeastern and Mid Atlantic United States. Our business approach focuses on operational excellence, financial strength and disciplined investment. As a holding company, our profitability depends on our subsidiaries’ operating results. Below are descriptions of our principal operating subsidiaries.

| | | | |

| Power | | PSE&G | | Energy Holdings |

| | |

A Delaware limited liability company formed in 1999 that integrates its generating asset operations with its wholesale energy sales, fuel supply, energy trading and marketing and risk management functions. Earns revenues from selling under contract or on the spot market a range of diverse products such as electricity, natural gas, capacity, emissions credits and a series of energy-related products used to optimize the operation of the energy grid. | | A New Jersey corporation, incorporated in 1924, which is a franchised public utility in New Jersey. It is also the provider of last resort for gas and electric commodity service for end users in its service territory. Earns revenues from its regulated rate tariffs under which it provides electric transmission and electric and gas distribution to residential, commercial and industrial customers in its service territory. It also offers appliance services and repairs to customers throughout its service territory. Has also implemented several programs to improve efficiencies in customer energy use and increase the level of renewable generation within New Jersey. | | A New Jersey limited liability company (successor to a corporation which was incorporated in 1989) that invests and operates through its two primary subsidiaries. Earns revenues from managing lease investments and the operation of its generation projects. Also pursuing solar and other renewable generation projects. |

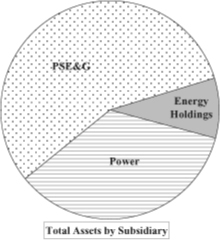

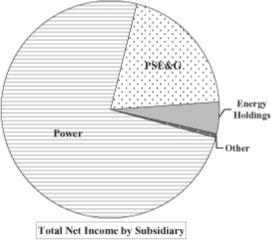

The majority of our earnings are derived from the operations of Power, which has contributed at least 70% of our Income from Continuing Operations over the past three years. While this part of the business has produced significant earnings over that period, its operations are subject to higher risks resulting from volatility in the energy markets. As a regulated public utility, PSE&G has continued to be a stable earnings contributor for us. Earnings from Energy Holdings have significantly declined over the past few years as we sold virtually all of our investments in international projects. Energy Holdings’ earnings have also been impacted by gains and losses on its asset sales and other charges and impairments taken on its remaining investments.

| | | | | | | | | | | | |

| | | |

Earnings (Losses) in millions | | 2010 | | | 2009 | | | 2008 | |

Power | | $ | 1,136 | | | $ | 1,191 | | | $ | 1,050 | |

PSE&G | | | 359 | | | | 325 | | | | 364 | |

Energy Holdings | | | 49 | | | | 72 | | | | (468 | ) |

Other | | | 13 | | | | 6 | | | | (28 | ) |

| | | | | | | | | | | | |

PSEG Income from Continuing Operations | | $ | 1,557 | | | $ | 1,594 | | | $ | 918 | |

| | | | | | | | | | | | |

2

The following is a more detailed description of our business, including a discussion of our:

| • | | Business Operations and Strategy |

| • | | Competitive Environment |

BUSINESS OPERATIONS AND STRATEGY

Power

Through Power, we seek to produce low-cost energy by efficiently operating our nuclear, coal, gas and oil-fired generation facilities, while balancing generation production, fuel requirements and supply obligations through energy portfolio management. We use commodity contracts and financial instruments, combined with our owned generation, to cover our commitments for Basic Generation Service (BGS) in New Jersey and other bilateral supply contract agreements.

Products and Services

As a merchant generator, our profit is derived from selling a range of products and services under contract to power marketers and to others, such as investor-owned and municipal utilities, and to aggregators who resell energy to retail consumers, or in the spot market. These products and services include:

| • | | Energy—the electrical output produced by generation plants that is ultimately delivered to customers for use in lighting, heating, air conditioning and operation of other electrical equipment. Energy is our principal product and is priced on a usage basis, typically in cents per kWh or dollars per MWh. |

| • | | Capacity—a product distinct from energy, is a market commitment that a given generation unit will be available to an Independent System Operator (ISO) for dispatch if it is needed to meet system demand. Capacity is typically priced in dollars per MW for a given sale period. |

| • | | Ancillary Services—related activities supplied by generation unit owners to the wholesale market, required by the ISO to ensure the safe and reliable operation of the bulk power system. Owners of generation units may bid units into the ancillary services market in return for compensatory payments. Costs to pay generators for ancillary services are recovered through charges imposed on market participants. |

| • | | Emissions Allowances and Congestion Credits—Emissions allowances (or credits) represent the right to emit a specific amount of certain pollutants. Allowance trading is used to control air pollution by providing economic incentives for achieving reductions in the emissions of pollutants. Congestion credits (or Financial Transmission Rights) are financial instruments that entitle the holder to a stream of revenues (or charges) based on the hourly congestion price differences across a transmission path. |

Power also sells wholesale natural gas, primarily through a full requirements Basic Gas Supply Service (BGSS) contract with PSE&G to meet the gas supply requirements of PSE&G’s customers. The current BGSS contract runs through March 31, 2012.

About 44% of PSE&G’s peak daily gas requirements is provided from Power’s firm transportation capacity, which is available every day of the year. Power satisfies the remainder of PSE&G’s requirements from storage contracts, liquefied natural gas, seasonal purchases, contract peaking supply, propane and refinery gas. Based upon availability, Power also sells gas to others.

3

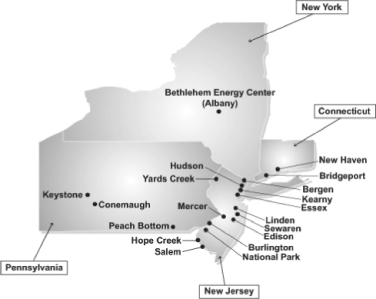

How Power Operates

We own approximately 13,500 MWs of generation capacity located in the Northeast and Mid Atlantic regions of the U.S. in some of the country’s largest and most developed electricity markets.

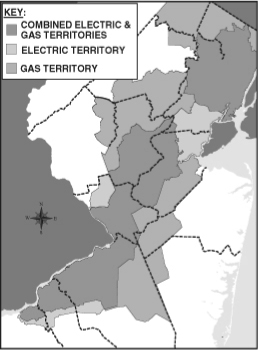

The map below shows the locations of Power’s Northeast and Mid Atlantic generation facilities.

We have recently entered into agreements to sell our 2,000 MW of generation capacity in Texas. See Item 8. Financial Statements and Supplementary Data—Note 1. Organization, Basis of Presentation and Summary of Significant Accounting Policies and Note 4. Discontinued Operations and Dispositions, for additional information.

For additional information on each of our generation facilities, see Item 2. Properties.

Our installed capacity utilizes a diverse mix of fuels: 45% gas, 27% nuclear, 18% coal, 9% oil and 1% pumped storage. This fuel diversity helps to mitigate risks associated with fuel price volatility and market demand cycles. Our total generating output in 2010, excluding amounts related to the Texas generation facilities which are being sold, was approximately 56,700 GWh. The following table indicates the proportionate share of generating output by fuel type.

| | | | |

Generation by Fuel Type | | Actual2010 | |

Nuclear: | | | | |

New Jersey facilities | | | 36 | % |

Pennsylvania facilities | | | 16 | % |

Fossil: | | | | |

Coal: | | | | |

New Jersey facilities | | | 7 | % |

Pennsylvania facilities | | | 10 | % |

Connecticut facilities | | | 2 | % |

Oil and Natural Gas: | | | | |

New Jersey facilities | | | 21 | % |

New York facilities | | | 8 | % |

| | | | |

Total | | | 100 | % |

| | | | |

4

While overall generation has increased over the past several years, the mix by fuel type has changed slightly in recent years due to the relatively favorable price of natural gas as compared to coal, making it more economical to run certain of our gas units than our coal units.

Our generation units are typically characterized as serving one or more of three general energy market segments: base load; load following; and peaking, based on their operating capability and performance. On a capacity basis, our portfolio of generation assets consists of 36% base load, 42% load following and 22% peaking. This diversity helps to reduce the risk associated with market demand cycles and allows us to participate in the market at each segment of the dispatch curve.

| | • | | Base Load Unitsoperate whenever they are available. These units generally derive revenues from energy and capacity sales. Variable operating costs are low due to the combination of highly efficient operations and the use of relatively lower cost fuels. Performance is generally measured by the unit’s “capacity factor,” or the ratio of the actual output to the theoretical maximum output. Our base load nuclear unit capacity factors were as follows: |

| | | | |

Unit | | 2010

Capacity

Factor | |

Salem Unit 1 | | | 85.3 | % |

| Salem Unit 2 | | | 96.9 | % |

Hope Creek | | | 89.1 | % |

| Peach Bottom Unit 2 | | | 89.8 | % |

Peach Bottom Unit 3 | | | 97.0 | % |

No assurances can be given that these capacity factors will be achieved in the future.

| | • | | Load Following Units operate between 20% and 80% of the time. The operating costs are higher per unit of output due to lower efficiency and/or the use of higher cost fuels such as oil, natural gas and, in some cases, coal. They operate less frequently than base load units and derive revenues from energy, capacity and ancillary services. |

| | • | | Peaking Units run the least amount of time and utilize higher-priced fuels. These units operate less than 20% of the time. Costs per unit of output tend to be much higher than for base load units. The majority of revenues are from capacity and ancillary service sales. The characteristics of these units enable them to capture energy revenues during periods of high energy prices. |

5

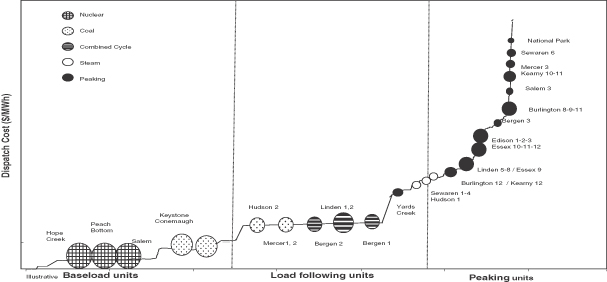

In the energy markets in which we operate, owners of power plants specify to the ISO prices at which they are prepared to generate and sell energy based on the marginal cost of generating energy from each individual unit. The ISOs will dispatch in merit order, calling on the lowest variable cost units first and dispatching progressively higher-cost units until the point that the entire system demand for power (known as the system “load”) is satisfied. Base load units are dispatched first, with load following units next, followed by peaking units. The following chart depicts the merit order of dispatch in PJM, where most of our generation units are located, based on illustrative historical dispatch cost. It should be noted that recent market price fluctuations have resulted in changes from historical norms, with lower gas prices allowing some gas generation to displace some coal generation:

The bid price of the last unit dispatched by an ISO establishes the energy market-clearing price. After considering the market-clearing price and the effect of transmission congestion and other factors, the ISO calculates the locational marginal pricing (LMP) for every location in the system. The ISO pays all units that are dispatched their respective LMP for each MWh of energy produced, regardless of their specific bid prices. Since bids generally approximate the marginal cost of production, units with lower marginal costs typically generate higher operating profits than units with comparatively higher marginal costs.

During periods when one or more parts of the transmission grid are operating at full capability, thereby resulting in a constraint on the transmission system, it may not be possible to dispatch units in merit order without violating transmission reliability standards. Under such circumstances, the ISO will dispatch higher-cost generation out of merit order within the congested area and power suppliers will be paid an increased LMP in congested areas, reflecting the bid prices of those higher-cost generation units.

6

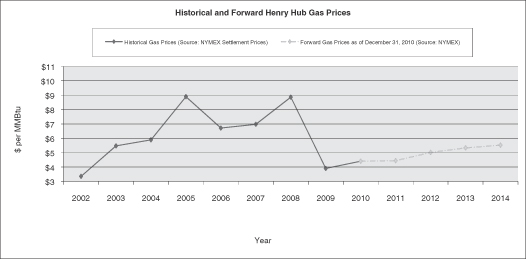

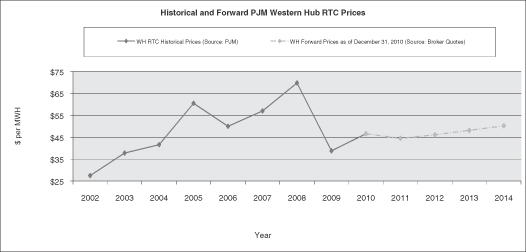

This method of determining supply and pricing creates an environment in the markets such that natural gas prices often have a major impact on the price that generators will receive for their output, especially in periods of relatively strong demand. Therefore, significant changes in the price of natural gas will often translate into significant changes in the wholesale price of electricity. This can be seen in the graphs below which present historical annual spot prices and forward calendar prices as averaged over each year.

Historical data and forward prices would imply that the price of natural gas will continue to have a strong influence on the price of electricity in the primary markets in which we operate.

The prices reflected in the tables above do not necessarily illustrate our contract prices, but they are representative of market prices at relatively liquid hubs, with nearer-term forward pricing generally resulting from more liquid markets than pricing for later years. In addition, the prices do not reflect locational differences resulting from congestion or other factors, which can be considerable. While these prices provide some perspective on past and future prices, the forward prices are highly volatile and there is no assurance that such prices will remain in effect nor that we will be able to contract output at these forward prices.

Fuel Supply

| • | | Nuclear Fuel Supply—To run our nuclear units we have long-term contracts for nuclear fuel. These contracts provide for: |

| | • | | purchase of uranium (concentrates and uranium hexafluoride); |

| | • | | conversion of uranium concentrates to uranium hexafluoride; |

7

| | • | | enrichment of uranium hexafluoride; and |

| | • | | fabrication of nuclear fuel assemblies. |

| • | | Coal Supply—Coal is the primary fuel for our Hudson, Mercer, Keystone, Conemaugh and Bridgeport stations. We have contracts with numerous suppliers. Coal is delivered to our units through a combination of rail, truck, barge or ocean shipments. |

In order to minimize emissions levels, our Bridgeport 3 unit uses a specific type of coal obtained from Indonesia. If the supply from Indonesia or equivalent coal from other sources was not available for this facility, our near-term operations would be adversely impacted. In the longer-term, additional material capital expenditures would be required to modify our Bridgeport 3 station to enable it to operate using a broader mix of coal sources. In the past, this coal was also used for our Hudson 2 unit; however, during 2010 we completed the installation of pollution control equipment at that facility which will provide us more flexibility in the types of coal we can use there in the future. For additional information see Item 8. Financial Statements and Supplementary Data—Note 13. Commitments and Contingent Liabilities.

| • | | Gas Supply—Natural gas is the primary fuel for the bulk of our load following and peaking fleet. We purchase gas directly from natural gas producers and marketers. These supplies are transported to New Jersey by four interstate pipelines with whom we have contracted. In addition, we have firm gas transportation contracts to serve our Bethlehem Energy Center (BEC) in New York. |

We have 1.3 billion cubic feet-per-day of firm transportation capacity under contract to meet our obligations under the BGSS contract. On an as available basis, this firm transportation capacity may also be used to serve the gas supply needs of our generation fleet. We supplement that supply with a total storage capacity of 78 billion cubic feet.

| • | | Oil—Oil is used as the primary fuel for two load following steam units and nine combustion turbine peaking units and can be used as an alternate fuel by several load following and peaking units that have dual-fuel capability. Oil for operations is drawn from on-site storage and is generally purchased on the spot market and delivered by truck, barge or pipeline. |

We expect to be able to meet the fuel supply demands of our customers and our own operations. However, the ability to maintain an adequate fuel supply could be affected by several factors not within our control, including changes in prices and demand, curtailments by suppliers, severe weather and other factors. For additional information, see Item 7. MD&A—Overview of 2010 and Future Outlook and Item 8. Financial Statements and Supplementary Data -Note 13. Commitments and Contingent Liabilities.

Markets and Market Pricing

Power’s assets are located in three centralized, competitive electricity markets operated by ISO organizations all of which are subject to the regulatory oversight of the Federal Energy Regulatory Commission (FERC):

| • | | PJM Regional Transmission Organization—PJM conducts the largest centrally dispatched energy market in North America. It serves over 51 million people, nearly 17% of the total U.S. population and a peak demand of over 144,000 MW. The PJM Interconnection coordinates the movement of electricity through all or parts of Delaware, Illinois, Indiana, Kentucky, Maryland, Michigan, New Jersey, North Carolina, Ohio, Pennsylvania, Tennessee, Virginia, West Virginia and the District of Columbia. The majority of Power’s generating stations operate in PJM. |

| • | | New York—The NYISO is the market coordinator for New York State and is now responsible for managing the New York Power Pool and for administering its energy marketplace. This service area has a population of about 19 million and a peak demand of over 33,900 MW. Power’s BEC station operates in New York. |

| • | | New England—ISO NE coordinates the movement of electricity in a region covering Maine, New Hampshire, Vermont, Massachusetts, Connecticut and Rhode Island. This service area has a population of about 14 million and a peak demand of over 28,000 MW. Power’s Bridgeport and New Haven stations operate in Connecticut. |

8

The price of electricity varies by location in each of these markets. Depending upon our production and our obligations, these price differentials can serve to increase or decrease our profitability.

Commodity prices, such as electricity, gas, coal, oil and emissions, as well as the availability of our diverse fleet of generation units to produce these products, also have a considerable effect on our profitability. These commodity prices have been, and continue to be, subject to significant market volatility.

Since the majority of the power we generate has generally been sourced from lower-cost nuclear and coal units, the historical rise in electric prices has yielded higher margins for us. Over a longer-term horizon, the higher the forward prices are, the more attractive an environment exists for us to contract for the sale of our anticipated output. However, higher prices also increase the cost of replacement power, thereby placing us at risk should any of our generating units fail to function effectively or otherwise become unavailable.

Over the past two years, a decline in wholesale natural gas prices has resulted in lower electricity prices. One of the reasons for the decline in natural gas prices is greater supply from shale production. This trend has reduced margin on forward sales as we recontract our expected generation output.

In addition to energy sales, we also earn revenue from capacity payments for our assets in the Northeast and Mid-Atlantic U.S. These payments are compensation for committing a portion of our capacity to the ISO for dispatch at its discretion. Capacity payments reflect the value to the ISO of assurance that there is sufficient generating capacity available at all times to meet system reliability and energy requirements. Currently, there is sufficient capacity in the markets in which we operate. However, in certain areas of these markets there are transmission system constraints, raising concerns about reliability and creating a more acute need for capacity. Previously, some generators, including us, announced the retirement or potential retirement of certain older generating facilities due to insufficient revenues to support their continued operation. To enable the continued availability of these facilities, in separate instances, both PJM and ISO-NE agreed to enter into Reliability-Must-Run (RMR) arrangements to compensate operators for those units’ contribution to reliability. While the RMRs for our units in the ISO-NE expired in 2010, the RMR arrangement for our Hudson 1 generating unit remains in effect and was recently extended until September 2012.

In PJM and ISO-NE, where we operate most of our generation, the market design for capacity payments provides for a structured, forward-looking, transparent capacity pricing mechanism. This is through the Reliability Pricing Model (RPM) in PJM and the Forward Capacity Market (FCM) in ISO-NE. These mechanisms provide greater clarity regarding the value of capacity, resulting in an improved pricing signal to prospective investors in new generating facilities so as to encourage expansion of capacity to meet future market demands.

The prices to be received by generating units in PJM for capacity have been set through RPM base residual auctions and depend upon the zone in which the generating unit is located. The majority of our PJM generating units are located in zones where the following prices have been set.

| | | | | | | | |

Delivery Year | | MW-day | | | kW-yr | |

| June 2010 to May 2011 | | $ | 174.29 | | | $ | 63.62 | |

| June 2011 to May 2012 | | $ | 110.00 | | | $ | 40.16 | |

| June 2012 to May 2013 | | $ | 139.73 | | | $ | 51.70 | |

| June 2013 to May 2014 | | $ | 245.00 | | | $ | 89.43 | |

Identical prices were set for all zones for the periods from June 2010 to May 2012 under these auctions. For all other periods the prices differ in the various areas of PJM, depending on the constraints in each area of the transmission system, with Keystone and Conemaugh receiving lower prices than the majority of our PJM generating units since there are fewer constraints in that region and our generating units in northern New Jersey receiving higher pricing.

9

The price that must be paid by an entity serving load in the various zones is also set through these auctions. These prices can be higher or lower than the prices noted in the table above due to import and export capability to and from lower-priced areas.

Like PJM and ISO-NE, the NYISO provides capacity payments to its generating units, but unlike these other two markets, the New York market does not provide a forward price signal beyond a six month auction period.

On a prospective basis, many factors may affect the capacity pricing, including but not limited to:

| • | | changes in load and demand; |

| • | | changes in the available amounts of demand response resources; |

| • | | changes in available generating capacity (including retirements, additions, derates, forced outages, etc.); |

| • | | increases in transmission capability between zones; |

| • | | changes to the pricing mechanism, including potentially increasing the number of zones to create more pricing sensitivity to changes in supply and demand, as well as other potential changes that PJM may propose over time; and |

| • | | changes driven by legislative and/or regulatory action, that permit states to subsidize local electric power generation through the consummation of standard offer capacity agreements. |

For additional information on our collection of RMR payments in PJM and the RPM and FCM markets, see Regulatory Issues—Federal Regulation.

Hedging Strategy

In an attempt to mitigate volatility in our results, we seek to contract in advance for a significant portion of our anticipated electric output, capacity and fuel needs. We seek to sell a portion of our anticipated lower-cost nuclear and coal-fired generation over a multi-year forward horizon, normally over a period of two to three years. We believe this hedging strategy increases stability of earnings.

Among the ways in which we hedge our output are: (1) sales at PJM West and (2) BGS contracts. Sales at PJM West reflect block energy sales at the liquid PJM Western Hub and other transactions that seek to secure price certainty for our generation related products. In addition, the BGS-Fixed Price contract, a full requirements contract that includes energy and capacity, ancillary and other services, is awarded for three-year periods through an auction process managed by the New Jersey Board of Public Utilities (BPU). The volume of BGS contracts and the electric utilities that our generation operations will serve vary from year to year. Pricing for the BGS contracts for recent and future periods by purchasing utility, including a capacity component, is as follows:

| | | | | | | | | | | | | | | | |

Load Zone ($/MWh) | | 2008-2011 | | | 2009-2012 | | | 2010-2013 | | | 2011-2014 | |

| PSE&G | | $ | 111.50 | | | $ | 103.72 | | | $ | 95.77 | | | $ | 94.30 | |

| Jersey Central Power and Light | | $ | 114.09 | | | $ | 103.51 | | | $ | 95.17 | | | $ | 92.56 | |

| Atlantic City Electric | | $ | 116.50 | | | $ | 105.36 | | | $ | 98.56 | | | $ | 100.95 | |

| Rockland Electric Company | | $ | 120.49 | | | $ | 112.70 | | | $ | 103.32 | | | $ | 106.84 | |

A portion of our total capacity is hedged through the BGS auctions. On average, tranches won in the BGS auctions require 100 MW to 120 MW of capacity on a daily basis.

We have obtained price certainty for all of our PJM and New England capacity through May 2014 through the RPM and FCM pricing mechanisms.

We enter into these hedges in an effort to provide price certainty for a large portion of our anticipated generation. There is, however, variability in both our actual output as well as in our hedges. Our actual output

10

will vary based upon total market demand, the relative cost position of our units compared to all units in the market and the operational flexibility of our units. Our hedge volume can also vary, depending on the type of hedge into which we have entered. The BGS auction, for example, results in a contract that provides for the supplier to serve a percentage of the default load of a New Jersey electric delivery company, that is, the load that remains after some customers have chosen to be served directly by third party suppliers. The amount of power supplied varies based on the level of the delivery company’s default load, which is affected by the number of customers who choose a third party supplier, as well as by other factors such as weather and the economy. Historically, the number of customers that have switched to third party suppliers was relatively constant, but in 2010, as market prices declined from past years’ historic highs, there has been an incentive for more of the smaller commercial and industrial electric customers to switch. In a falling price environment, this has a negative impact on Power’s margins, as the anticipated BGS pricing is replaced by lower market pricing. We are unable to determine the degree to which this switching, or “migration,” will continue, but the impact on our results could be material.

To support our contracted sales of energy, we enter into contracts for the future purchase and delivery of our anticipated nuclear fuel and coal needs, which include some market-based pricing components. As of February 15, 2011, we had contracted for the following percentages of our nuclear and coal generation output and related fuel supplies for the next three years with modest amounts beyond 2013.

| | | | | | |

Nuclear and Coal Generation | | 2011 | | 2012 | | 2013 |

| Generation Sales | | 90%-95% | | 40%-50% | | 15%-30% |

| Nuclear Fuel Purchases | | 100% | | 100% | | 100% |

| Coal Supply and Transportation Costs | | 100% | | 70%-80% | | 20%-30% |

We take a more opportunistic approach in hedging our anticipated natural gas-fired generation. The generation from these units is less predictable, as these units are generally dispatched when aggregate market demand has exceeded the supply provided by lower-cost units. The natural gas-fired units have generally provided a lower contribution to our margin than either the nuclear or coal units, although recent market price dynamics of coal and gas moderated this historical relationship for 2010.

In a changing market environment, this hedging strategy may cause our realized prices to differ materially from current market prices. In a rising price environment, this strategy normally results in lower margins than would have been the case if little or no hedging activity had been conducted. Alternatively, in a falling price environment, this hedging strategy will tend to create margins higher than those implied by the then current market.

11

PSE&G

Our public utility, PSE&G, distributes electric energy and gas to customers within a designated service territory running diagonally across New Jersey where approximately 5.5 million people, or about 70% of the State’s population, reside.

Products and Services

Our utility operations primarily earn margins through the transmission and distribution of electricity and the distribution of gas.

| • | | Transmission—is the movement of electricity at high voltage from generating plants to substations and transformers, where it is then reduced to a lower voltage for distribution to homes, businesses and industrial customers. Our revenues for these services are based upon tariffs approved by the FERC. |

| • | | Distribution—is the delivery of electricity and gas to the retail customer’s home, business or industrial facility. Our revenues for these services are based upon tariffs approved by the BPU. |

We also earn margins through non-tariff competitive services, such as appliance repair services. The commodity supply portion of our utility business’ electric and gas sales are managed by BGS and BGSS suppliers. Pricing for those services are set by the BPU as a pass-through, resulting in no margin for our utility operations.

In addition to our current utility products and services, we have implemented several programs to improve efficiencies in customer energy use and increase the level of renewable generation including:

| • | | a program to help finance the installation of solar power systems throughout our electric service area, |

| • | | a program to develop, own and operate solar power systems, and |

| • | | a set of energy efficiency programs to encourage conservation and energy efficiency by providing energy and money saving measures directly to businesses and families. |

For additional information concerning these programs and the components of our tariffs, see Regulatory Issues.

12

How PSE&G Operates

We provide network transmission and point-to-point transmission services, which are coordinated with PJM, and provide distribution service to 2.2 million electric customers and 1.8 million gas customers in a service area that covers approximately 2,600 square miles running diagonally across New Jersey. We serve the most heavily populated, commercialized and industrialized territory in New Jersey, including its six largest cities and approximately 300 suburban and rural communities.

Transmission

We use formula rates for our existing and future transmission investments. Formula-type rates provide a method of rate recovery where the transmission owner annually determines its revenue requirements through a fixed formula which considers Operations and Maintenance expenditures, Rate Base and capital investments and applies an approved return on equity (ROE) in developing the weighted average cost of capital. Currently, approved rates provide for a base ROE of 11.68% on existing and new transmission investment, while certain investments are entitled to earn incentive rates. For more information on current transmission construction activities, see Regulatory Issues, Federal Regulation—Transmission Regulation.

| | | | | | | | |

Transmission Statistics | |

| December 31, 2010 | | | Historical Annual Load | |

Network Circuit Miles | | Billing Peak (MW) | | | Growth 2006-2010 | |

1,357 | | | 10,761 | | | | -0.1% | |

Distribution

Our primary business is the distribution of gas and electricity to end users in our service territory. Our load requirements were split among residential, commercial and industrial customers, as described below for 2010. We believe that we have all the non-exclusive franchise rights (including consents) necessary for our electric and gas distribution operations in the territory we serve.

| | | | | | | | |

| | | % of 2010 Sales | |

Customer Type | | Electric | | | Gas | |

Commercial | | | 57% | | | | 36% | |

Residential | | | 33% | | | | 61% | |

Industrial | | | 10% | | | | 3% | |

| | | | | | | | |

| Total | | | 100% | | | | 100% | |

| | | | | | | | |

While our customer base has remained steady, electric and gas load has declined, as illustrated:

| | | | | | | | | | | | |

Electric and Gas Distribution Statistics | |

| December 31, 2010 | | | | Historical Annual | |

| | | Number of

Customers | | | Electric Sales and Gas

Sold and Transported | | | Load Growth

2006-2010 | |

Electric | | | 2.2 Million | | | | 43,645 GWh | | | | -0.5% | |

Gas | | | 1.8 Million | | | | 3,465 Million Therms | | | | -1.0% | |

13

Supply

Although commodity revenues make up more than 59% of our revenues, we make no profit on the supply of energy since the actual costs are passed through to our customers.

All electric and gas customers in New Jersey have the ability to choose their own electric energy and/or gas supplier. However, pursuant to BPU requirements, we serve as the supplier of last resort for electric and gas customers within our service territory who have not chosen another supplier. As a practical matter, this means we are obligated to provide supply to a vast majority of residential customers and a smaller portion of commercial and industrial customers.

We procure the supply to meet our BGS obligations through two concurrent auctions authorized by the BPU for New Jersey’s total BGS requirement. These auctions take place annually in February. Results of these auctions determine which energy suppliers are authorized to supply BGS to New Jersey’s electric distribution companies (EDCs). Once validated by the BPU, electricity prices for BGS service are set.

PSE&G procures the supply requirements of our default service gas customers (BGSS) through a full requirements contract with Power. The BPU has approved a mechanism designed to recover all gas commodity costs related to BGSS for residential customers. BGSS filings are made annually by June 1 of each year, with an effective date of October 1. Any difference between rates charged under the BGSS contract and rates charged to our residential customers is deferred and collected or refunded through adjustments in future rates. Commercial and industrial customers that do not have third party suppliers are also supplied under the BGSS arrangement. These customers are charged a market based price largely determined by prices for commodity futures contracts.

Markets and Market Pricing

There continues to be significant volatility in commodity prices. Such volatility can have a considerable impact on us since a rising commodity price environment results in higher delivered electric and gas rates for customers. This could result in decreased demand for both electricity and gas, increased regulatory pressures and greater working capital requirements as the collection of higher commodity costs may be deferred under our regulated rate structure. A declining commodity price on the other hand, would be expected to have the opposite effect. For additional information, including the impact of natural gas commodity prices on electricity prices such as BGS, see Item 7. MD&A.

14

Energy Holdings

Our focus at Energy Holdings is on managing our portfolio of lease investments and exploring opportunities to participate in solar, wind and alternative energy developments in the U.S., as discussed below.

Since 2008, we have pursued opportunities to terminate international leveraged leases with lessees willing to meet certain economic thresholds in order to reduce the cash tax exposure related to these leases. As of December 31, 2010, we had terminated all of these leveraged lease investments and reduced the related cash tax exposure by $1.1 billion. Over the past several years, we have also reduced our international risk by opportunistically monetizing the majority of our previous investments. We are continuing to explore options for our remaining international investment in Venezuela as well as our projects in California, Hawaii and New Hampshire totaling 240 MW. For additional information on these generation facilities, see Item 2. Properties.

Products and Services

The majority of our remaining $1.3 billion of domestic lease investments are energy-related leveraged leases. As of December 31, 2010, the single largest lease investment represented 26% of total lease investments.

Our leveraged leasing portfolio is designed to provide a fixed rate of return. Leveraged lease investments involve three parties: an owner/lessor, a creditor and a lessee. In a typical leveraged lease financing, the lessor purchases an asset to be leased. The purchase price is typically financed 80% with debt provided by the creditor and the balance comes from equity funds provided by the lessor. The creditor provides long-term financing to the transaction secured by the property subject to the lease. Such long-term financing is non-recourse to the lessor and, with respect to our lease investments, is not presented in our Consolidated Balance Sheets.

The lessor acquires economic and tax ownership of the asset and then leases it to the lessee for a period of time no greater than 80% of its remaining useful life. As the owner, the lessor is entitled to depreciate the asset under applicable federal and state tax guidelines. The lessor receives income from lease payments made by the lessee during the term of the lease and from tax benefits associated with interest and depreciation deductions with respect to the leased property. Our ability to realize these tax benefits is dependent on operating gains generated by our other operating subsidiaries and allocated pursuant to the consolidated tax sharing agreement between us and our operating subsidiaries.

Lease rental payments are unconditional obligations of the lessee and are set at levels at least sufficient to service the non-recourse lease debt. The lessor is also entitled to any residual value associated with the leased asset at the end of the lease term. An evaluation of the after-tax cash flows to the lessor determines the return on the investment. Under accounting principles generally accepted in the U.S., the lease investment is recorded net of non-recourse debt and income is recognized as a constant return on the net unrecovered investment.

For additional information on leases, including the credit, tax and accounting risks, see Item 1A. Risk Factors, Item 7A. Quantitative and Qualitative Disclosures About Market Risk—Credit Risk—Energy Holdings, Item 8. Financial Statements and Supplementary Data—Note 8. Financing Receivables and Note 13. Commitments and Contingent Liabilities.

Through Energy Holdings, we have solar project investments in New Jersey, Florida and Ohio totaling 29 MW, all of which are fully operational. See Item 2. Properties for additional information.

A joint venture owned equally by us and an unaffiliated private developer has been awarded a $3 million grant by the New Jersey Office of Clean Energy (OCE) to advance the development of a wind site to be located approximately 16 miles off the shore of southern New Jersey. Numerous issues will need to be resolved in order to successfully develop such a project. The State of New Jersey has taken steps to stimulate the development of offshore wind generation by enacting the Offshore Wind Economic Development Act. This Act requires BGS and third-party suppliers in New Jersey to procure Offshore Renewable Energy Certificates (ORECs) from qualified off-shore facilities for a 20-year term. The BPU is currently in the process of developing and implementing regulations that will establish an OREC program under which the BPU can review applications to construct, finance and operate off-shore wind facilities.

15

We also have invested in a joint venture to license technology that stores energy in the form of compressed air which can later be released to generate electricity through specialized equipment. This technology could be used to optimize an intermittent energy source, such as wind, by storing energy for when it is needed.

COMPETITIVE ENVIRONMENT

Power

Various market participants compete with us and one another in buying and selling in wholesale power pools, entering into bilateral contracts and selling to aggregated retail customers. Our competitors include:

| • | | domestic and multi-national utility generators, |

| • | | banks, funds and other financial entities, |

| • | | fuel supply companies, and |

| • | | affiliates of other industrial companies. |

New additions of lower-cost or more efficient generation capacity could make our plants less economical in the future. Although it is not clear if this capacity will be built or, if so, what the economic impact will be, such additions could impact market prices and our competitiveness.

Our business is also under competitive pressure due to demand side management (DSM) and other efficiency efforts aimed at changing the quantity and patterns of usage by consumers which could result in a reduction in load requirements. A reduction in load requirements can also be caused by economic cycles, customer migration and other factors. It is also possible that advances in technology, such as distributed generation, will reduce the cost of alternative methods of producing electricity to a level that is competitive with that of most central station electric production. To the extent that additions to the transmission system relieve or reduce congestion in eastern PJM where most of our plants are located, our revenues could be adversely affected. Changes in the rules governing transmission planning or cost allocation could also impact our revenues.

We are also at risk if one or more states in which we operate should decide to turn away from competition. This is now occurring in the State of New Jersey where a new law was enacted on January 28, 2011 establishing a long-term capacity agreement pilot program (LCAPP) which provides for 2,000 MW of subsidized base load or mid-merit electric power generation. This bill may have the effect of artificially depressing prices in the competitive wholesale market and thus has the potential to harm competitive markets, on both a short-term and a long-term basis. Other states, such as Maryland, are also examining similar programs. Construction of new subsidized local generation also has the potential to reduce the need for the construction of new transmission to transport remote generation and alleviate system constraints. The lack of consistent rules in energy markets can negatively impact the competitiveness of our plants.

Environmental issues, such as restrictions on carbon dioxide (CO2 ) emissions and other pollutants, may also have a competitive impact on us to the extent that it becomes more expensive for some of our plants to remain compliant, thus affecting our ability to be a lower-cost provider compared to competitors without such restrictions. In addition, most of our plants, which are located in the Northeast where rules are more stringent, can be at an economic disadvantage compared to our competitors in certain Midwest states. While our generation fleet is relatively low-emitting, additional restrictions could have a negative impact on certain of our units, including our coal units.

16

In addition, pressures from renewable resources, such as wind and solar, could increase over time, especially if government incentive programs continue to grow. For example, many parts of the country, including the mid-western region within the footprint of the Midwest Independent System Operator, the California ISO and the PJM region, have either implemented or are considering implementing changes to their respective regional transmission planning processes that will enable the construction of large amounts of transmission to move renewable generation to load centers. The FERC is considering ordering all FERC-jurisdictional regions to effectuate such changes to the planning processes to facilitate the integration of renewable resources. See discussion in Regulatory Issues—Federal Regulation below.

PSE&G

The transmission and distribution business has minimal risks from competitors. Our transmission and distribution business is minimally impacted when customers choose alternate electric or gas suppliers since we earn our return by providing transmission and distribution service, not by supplying the commodity. The demand for electric energy and gas by customers is affected by customer conservation, economic conditions, weather and other factors not within our control.

Changes in the current policies for building new transmission lines, such as the proposal by FERC to eliminate provisions for us to have the “right of first refusal” to construct projects in our service territory, could result in additional competition to build transmission lines in our area in the future and would allow us to seek opportunities to build in other service territories. Moreover, as discussed in Regulatory Issues—Federal Regulation below, the court’s elimination of national electric transmission corridors may impact upon future transmission build.

EMPLOYEE RELATIONS

As of December 31, 2010, we had approximately 9,965 employees within our subsidiaries, including 6,451 covered under collective bargaining agreements.

| | | | | | | | | | | | | | | | |

Employees as of December 31, 2010 | |

| | | Power | | | PSE&G | | | Energy

Holdings | | | Services | |

Non-Union | | | 1,292 | | | | 1,178 | | | | 18 | | | | 1,026 | |

Union | | | 1,511 | | | | 4,931 | | | | 0 | | | | 9 | |

| | | | | | | | | | | | | | | | |

Total Employees | | | 2,803 | | | | 6,109 | | | | 18 | | | | 1,035 | |

| | | | | | | | | | | | | | | | |

Number of Union Groups | | | 3 | | | | 5 | | | | N/A | | | | 1 | |

All of our collective bargaining agreements, except one will expire on April 30, 2013 or later. The one exception is an agreement at PSE&G that covers 1,218 employees. This agreement expires on April 30, 2011.

REGULATORY ISSUES

Federal Regulation

FERC

FERC is an independent federal agency that regulates the transmission of electric energy and gas in interstate commerce and the sale of electric energy and gas at wholesale pursuant to the Federal Power Act (FPA) and the Natural Gas Act. PSE&G and the generation and energy trading subsidiaries of Power are public utilities as defined by the FPA. FERC has extensive oversight over “public utilities” as defined by the FPA. FERC approval is usually required when a “public utility” company seeks to: sell or acquire an asset that is regulated by FERC (such as a transmission line or a generating station); collect costs from customers associated with a new transmission facility; charge a rate for wholesale sales under a contract or tariff; or engage in certain mergers and internal corporate reorganizations.

FERC also regulates generating facilities known as qualifying facilities (QFs). QFs are cogeneration facilities that produce electricity and another form of useful thermal energy, or small power production facilities where

17

the primary energy source is renewable, biomass, waste, or geothermal resources. QFs must meet certain criteria established by FERC. We own various QFs through Energy Holdings. QFs are subject to some, but not all, of the same FERC requirements as public utilities.

FERC also regulates RTOs/ISOs, such as PJM, and their energy and capacity markets.

For us, the major effects of FERC regulation fall into five general categories:

| • | | Regulation of Wholesale Sales—Generation/Market Issues |

| • | | Transmission Regulation |

Regulation of Wholesale Sales—Generation/Market Issues

| • | | Market Power—Under FERC regulations, public utilities must receive FERC authorization to sell power in interstate commerce. They can sell power at cost-based rates or apply to FERC for authority to make market based rate (MBR) sales. For a requesting company to receive MBR authority, FERC must first make a determination that the requesting company lacks market power in the relevant markets. FERC requires that holders of MBR tariffs file an update every three years demonstrating that they continue to lack market power. |

PSE&G and certain subsidiaries of Power have received MBR authority from FERC. Retention of MBR authority is critical to the maintenance of our generation business’ revenues.

Under MBR rules, FERC may look at sub-markets to analyze whether a company possesses market power. Applying these rules in October 2008, FERC granted PSE&G, PSEG Energy Resources & Trade LLC and PSEG Power Connecticut LLC continued MBR authority and granted both PSEG Fossil LLC and PSEG Nuclear LLC initial MBR authority. Each of these companies filed for an update of its MBR authority in December 2010. Interventions and comments with respect to this MBR filing are due at the FERC by the end of February. A decision is expected in 2011.

| • | | Cost-Based RMR Agreements—FERC has permitted public utility generation owners to enter into RMR agreements that provide cost-based compensation to a generation owner when a unit proposed for retirement is asked to continue operating for reliability purposes. On November 11, 2010, PJM officially notified Power that it will need the Hudson 1 generating station to remain in service through September 1, 2012 to ensure grid reliability during the summer of 2012 given the delays associated with the Susquehanna-Roseland project. In January 2011, Power filed at FERC for extension of the RMR agreement for Hudson Unit 1 through September 1, 2012. |

In ISO-NE, many owners of generation facilities have also filed for RMR treatment. During 2010, we collected FERC-approved monthly payments for the Bridgeport Harbor Station Unit 2 and the New Haven Harbor Station under agreements that expired in June 2010.

18

Energy Clearing Prices

Energy clearing prices in the markets in which we operate are generally based on bids submitted by generating units. Under FERC-approved rules, bids are subject to price caps and mitigation rules applicable to certain generation units. FERC rules also govern the overall design of these markets. At present, all units receive a single clearing price based on the bid of the marginal unit (i.e. the last unit that must be dispatched to serve the needs of load). These FERC rules have a direct impact on the energy prices received by our units.

Capacity Market Issues

PJM, NYISO, and ISO-NE each have capacity markets that have been approved by FERC.

RPM is a locational installed capacity market design for the PJM region, including a forward auction for installed capacity. Under RPM, generators located in constrained areas within PJM are paid more for their capacity as an incentive to ensure adequate supply where generation capacity is most needed. PJM’s RPM and related FERC orders establishing prices paid to us and other generators as a result of RPM’s transitional auctions were challenged in court by various state public utility commissions, including the BPU. On February 8, 2011 the DC Circuit Court of Appeals issued a decision upholding FERC orders denying this challenge to the transitional auction results. Moreover, the mechanics of RPM in PJM continue to evolve and be refined in stakeholder proceedings in which we are active, and there is currently significant discussion about the future role of demand response in the RPM market.

Pursuant to a settlement that established the design of ISO-NE’s market for installed capacity and which was implemented gradually over a four-year period that commenced in December 2006, all generators in New England began receiving fixed capacity payments that escalate gradually over the transition period. The market design consists of a forward-looking auction for installed capacity that is intended to recognize the locational value of generators on the system and contains incentive mechanisms to encourage generator availability during generation shortages. As in PJM, capacity market rules in the ISO-NE continue to develop. Power has challenged in court the results of the ISO-NE’s first forward capacity auction, arguing that its units received inadequate compensation notwithstanding the location of its resources in a constrained area. This case is pending at the D.C. Circuit Court of Appeals. Power and other generators have also filed a complaint at FERC regarding the ISO-NE’s capacity market design, alleging that it insufficiently reflects locational capacity values. This complaint is also pending.

NYISO operates a short-term capacity market that provides a forward price signal only for six months into the future. The NYISO capacity model recognizes only two separate zones that potentially may separate in price: New York City and Long Island. Discussions concerning potential changes to NYISO capacity markets are also ongoing.

Recent legislative developments in the State of New Jersey have the potential to adversely impact RPM prices. On January 28, 2011, New Jersey enacted a new law establishing LCAPP. This law calls for New Jersey electric distribution companies such as PSE&G to subsidize 2,000 MWs of new generation capacity in New Jersey for a term of up to 15 years. The law also provides for the BPU to hold an expedited process to select generators to receive these subsidies and to perform a net benefits test examining economic, community and environmental benefits associated with generating projects. The BPU has commenced this process, which requires the submission of binding generator bids by March 7, 2011 and selection of eligible generators by March 30, 2011. Once generators are selected, the electric distribution companies will then be required to enter into irrevocable, financially settled, standard offer capacity agreements (SOCA). The SOCA will require that the generator bid in and clear the PJM RPM base residual auction in each year of the SOCA term. The SOCA will provide for the electric distribution companies to make capacity payments to, or receive capacity payments from, the generators as calculated based on the difference between the RPM clearing price for each year of the term and the price bid and accepted for that generator in the BPU process.

19

The LCAPP legislation is being challenged both at FERC and in court. In February, PSEG and a group of other generators filed a complaint at the FERC seeking to prevent the subsidized generation from interfering with the wholesale capacity market and a case in federal district court arguing that the legislation is unconstitutional and should be invalidated. Both actions are pending. In addition, PJM has made a filing at FERC that, if accepted by FERC, would significantly mitigate the effect of this subsidized generation on the RPM market clearing prices for capacity.

Transmission Regulation

FERC has exclusive jurisdiction to establish the rates and terms and conditions of service for interstate transmission. We currently have FERC-approved formula rates in effect to recover the costs of our transmission facilities. Under this formula, rates are put into effect in January of each year based upon our internal forecast of annual expenses and capital expenditures. Rates are then trued up the following year to reflect actual annual expenses/capital expenditures. Our allowed ROE is 11.68% for both existing and new transmission investments, and we have received incentive rates, affording a higher ROE, for certain large scale transmission investments. For additional information on our transmission rates and the annual true-ups, see Item 7. MD&A – Overview of 2010 and Future Outlook.

| • | | Transmission Policy Developments— In June 2010, FERC issued a Notice of Proposed Rulemaking (NOPR) proposing to modify current transmission planning and cost allocation processes. Specifically, FERC has proposed that transmission planning take into account “public policy” requirements established by state or federal laws or regulations, such as state Renewable Portfolio Requirements. FERC has also questioned whether it is appropriate for transmission planning to utilize a “bright line” test to identify needed transmission projects or whether “flexible criteria” should be used. These proposed changes would likely result in more transmission being planned and constructed. |

FERC has also proposed to eliminate provisions in FERC-approved tariffs or agreements that permit a transmission owner within whose franchised service territory a transmission project is being constructed to exercise a “right of first refusal” to construct the project. FERC has not yet acted to issue a Final Rule. There are also two pending FERC litigated proceedings, in which we are a party, addressing and challenging this proposed change to the “right of first refusal.” A change in FERC rules or adverse decisions in these proceedings could result in third parties constructing transmission within PSE&G’s service territory in the future.

| • | | Transmission Expansion—In June 2007, PJM identified the need for the construction of the Susquehanna-Roseland line, a new 500 kV transmission line intended to maintain the reliability of the electrical grid serving New Jersey customers. PJM assigned construction responsibility for the new line to us and PPL for the New Jersey and Pennsylvania portions of the project, respectively. The estimated cost of our portion of this construction project is up to $750 million, and PJM had originally directed that the line be placed into service by June 2012. Construction of the Susquehanna-Roseland line is contingent upon obtaining all necessary federal, state, municipal and landowner permits and approvals. The construction of the line has encountered local opposition. In February 2010, we received approval from the BPU to construct our portion of the project, which was memorialized by a written order in April 2010. Regarding environmental approvals, in June 2009, the New Jersey Highlands Council provided a favorable applicability determination with respect to the portion of the project crossing the Highlands region which was approved by the New Jersey Department of Environmental Protection (NJDEP) in January 2010. However, we have not received certain environmental approvals that are required for each of the Eastern and Western segments of the line and believe it is unlikely that we will obtain these approvals until late 2012, at the earliest. The Western portion of the line also requires certain permits from the National Park Service, whose review is not expected to be completed until late 2012. Consequently, at this time, we do not expect the Eastern portion of the line to be in service before June 2014, and do not expect the Western portion to be in service before June 2015. Further delays are possible for both portions. Delays in the construction schedule could impact the timing of expected transmission revenues. |

20

On February 3, 2011, certain environmental groups that were parties to the BPU proceeding approving the Susquehanna-Roseland line filed a motion to reopen the agency record on the grounds of “changed circumstances,” including the delay in construction of the project and PJM’s issuance of a new load forecast report. PSE&G believes that there are no grounds to reopen the record. The same parties have also appealed the BPU order to the NJ Appellate Division and this appeal remains pending.

FERC has granted our request for incentive rate treatment for the Susquehanna-Roseland line, including an adder of 125 basis points above our base ROE, recovery of 100% of Construction Work in Progress (CWIP) in rate base and authorization to recover 100% of all prudently incurred development and construction costs if the project is abandoned or cancelled, in whole or in part, for reasons beyond our control.

In December 2008, PJM approved another 500 kV transmission project, originating in Branchburg and ending in Hudson County, New Jersey, with an estimated cost of $1.1 billion. In December 2009, FERC granted our request for the same incentive rate treatment on this project as the Susquehanna-Roseland line. Subsequently, PJM approved a modified 230 kV project, in place of the 500 kV line, originating in Roseland and terminating in Hudson County, at an estimated cost of up to $700 million. The project has an expected in-service date of June 2015. Development and siting activities for this project are expected to commence in 2011. In November 2010, we filed a notice with FERC regarding the change in project scope. The BPU and the New Jersey Division of Rate Counsel each filed objections to the continuation of the previously-awarded rate incentives to the reconfigured project. We have filed responsive pleadings and believe that the modified project should be eligible for the same rate incentives as the original project, but the matter remains pending at FERC.

PJM has approved in its Regional Transmission Expansion Plan several other 230 kV transmission projects to be constructed by PSE&G. PSE&G filed at FERC for recovery of CWIP in rate base for four of these projects (Burlington-Camden project, West Orange project, Middlesex Switch Rack project and Bayonne-Marion project) and 100% abandonment cost recovery for these projects. On December 30, 2010, the FERC denied PSE&G’s request without prejudice, finding that PSE&G had not met the requirements for incentive treatment on a project-by-project basis and affording PSE&G the option to re-file and justify the requested incentives on a project-by-project, rather than on an aggregate, basis. PSE&G is currently considering this option.

In February 2011, the United States Court of Appeals for the 9th Circuit issued a decision vacating the U.S. Department of Energy’s (DOE) 2006 Congestion Study and the two national transmission corridor designations resulting from the study, including the Mid-Atlantic Corridor which encompasses all of the State of New Jersey. FERC back-stop siting authority permits an entity building transmission to site the project at FERC under certain circumstances, including a State’s failure to act within one year. However, since this authority only attaches to transmission located within a DOE-designated corridor, FERC back-stop siting authority is now unavailable to companies building transmission in New Jersey, such as PSE&G.

| • | | PJM Transmission Rate Design—In 2007, FERC addressed the issue of how transmission rates, paid by PJM transmission customers and ultimately paid by our retail customers, should be designed in PJM. FERC ruled that the cost of new high voltage (500 kV and above) transmission facilities in PJM would be regionalized and paid for by all transmission customers on a pro-rata basis. Each share is calculated annually based upon a zone’s load ratio share within PJM. For all existing facilities, costs would be allocated using the pre-existing zonal rate design. For new lower voltage transmission facilities, costs would be allocated using a “beneficiary pays” approach. This FERC decision was subsequently upheld on rehearing but was then appealed by other parties to the United States Court of Appeals for the Seventh Circuit. |

21