UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| | x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| | For the fiscal year ended December 31, 2012 |

OR

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

For the transition period from ____________ to ____________

Commission file number 001-09148

THE BRINK’S COMPANY

(Exact name of registrant as specified in its charter)

| Virginia | | | 54-1317776 | |

| (State or other jurisdiction of | | (I.R.S. Employer | |

| incorporation or organization) | | Identification No.) | |

| | | | | |

| P.O. Box 18100, | | | | |

| 1801 Bayberry Court | | | | |

| Richmond, Virginia | | | 23226-8100 | |

| (Address of principal executive offices) | | (Zip Code) | |

| | | | | |

| Registrant’s telephone number, including area code | | | (804) 289-9600 | |

| | | | | |

| Securities registered pursuant to Section 12(b) of the Act: | | | | |

| | | Name of each exchange on | |

| Title of each class | | which registered | |

| The Brink’s Company Common Stock, Par Value $1 | | New York Stock Exchange | |

| | | | | |

| Securities registered pursuant to Section 12(g) of the Act: None | | | | |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes x No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes ¨ No x

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definition of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer x Accelerated filer ¨ Non-accelerated filer ¨ Smaller reporting company ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes ¨ No x

As of February 21, 2013, there were issued and outstanding 47,861,370 shares of common stock. The aggregate market value of shares of common stock held by non-affiliates as of June 30, 2012, was $1,101,142,720.

Documents incorporated by reference: Part III incorporates information by reference from portions of the Registrant’s definitive 2013 Proxy Statement to be filed pursuant to Regulation 14A.

THE BRINK’S COMPANY

FORM 10-K

FOR THE YEAR ENDED DECEMBER 31, 2012

TABLE OF CONTENTS

PART I

| | | Page |

| Item 1. | Business | 1 |

| Item 1A. | Risk Factors | 9 |

| Item 1B. | Unresolved Staff Comments | 15 |

| Item 2. | Properties | 15 |

| Item 3. | Legal Proceedings | 16 |

| Item 4. | Mine Safety Disclosures | 16 |

| | | |

| | Executive Officers of the Registrant | 17 |

| | | |

| | PART II | |

| | | |

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer | |

| | Purchases of Equity Securities | 18 |

| Item 6. | Selected Financial Data | 20 |

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 21 |

| Item 7A. | Quantitative and Qualitative Disclosures About Market Risk | 67 |

| Item 8. | Financial Statements and Supplementary Data | 69 |

| Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 111 |

| Item 9A. | Controls and Procedures | 111 |

| Item 9B. | Other Information | 111 |

| | | |

| | PART III | |

| | | |

| Item 10. | Directors, Executive Officers and Corporate Governance | 112 |

| Item 11. | Executive Compensation | 112 |

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 112 |

| Item 13. | Certain Relationships and Related Transactions, and Director Independence | 112 |

| Item 14. | Principal Accountant Fees and Services | 112 |

| | | |

| | PART IV | |

| | | |

| Item 15. | Exhibits and Financial Statement Schedules | 113 |

The Brink’s Company is a premier provider of secure logistics and security solutions services to banks and financial institutions, retailers, government agencies, mints, jewelers and other commercial operations around the world. These services include:

| · | armored vehicle transportation, which we refer to as cash-in-transit (“CIT”) |

| · | automated teller machine - replenishment and servicing, and network infrastructure services (“ATM Services”) |

| · | secure international transportation of valuables (“Global Services”) |

| · | supply chain management of cash (“Cash Management Services”) including cash logistics services, deploying and servicing safes and safe control devices (e.g., our patented CompuSafe® service), coin sorting and wrapping, integrated check and cash processing services (“Virtual Vault Services”) |

| · | bill payment acceptance and processing services to utility companies and other billers (“Payment Services”) |

| · | security and guarding services (including airport security) |

The Brink’s Company, along with its subsidiaries, is referred to as “we,” “our,” “Brink’s,” or “the Company” throughout this Form 10-K.

Brink’s brand and reputation span across the globe. Our international network serves customers in more than 100 countries and employs approximately 70,000 people. Our operations include approximately 1,100 facilities, including our Richmond, Virginia headquarters, and 13,300 vehicles. Our globally recognized brand, global infrastructure, and expertise are important competitive advantages.

Our operating segments consist of four geographies: Latin America; Europe, Middle East, and Africa (“EMEA”); Asia Pacific; and North America, which are aggregated into two reportable segments: International and North America. Financial information related to our two reportable segments and non-segment income and expense is included in the consolidated financial statements on pages 69–110.

A significant portion of our business is conducted internationally, with 82% of our $3.8 billion in revenues earned outside the United States. Financial results are reported in U.S. dollars and are affected by fluctuations in the relative value of foreign currencies. Our business is also subject to other risks customarily associated with operating in foreign countries including changing labor and economic conditions, political instability, restrictions on repatriation of earnings and capital, as well as nationalization, expropriation and other forms of restrictive government actions. The future effects of these risks cannot be predicted. Additional information about risks associated with our foreign operations is provided on pages 9, 46 and 68.

We have significant liabilities associated with our retirement plans, a portion of which has been funded. See pages 54–57 and 61–64 for more information on these liabilities. Additional risk factors are described on pages 9–13.

Available Information and Corporate Governance Documents

The following items are available free of charge on our website (www.brinks.com) as soon as reasonably possible after filing or furnishing them with the Securities and Exchange Commission (the “SEC”):

| · | Annual reports on Form 10-K |

| · | Quarterly reports on Form 10-Q |

| · | Current reports on Form 8-K, and amendments to those reports |

In addition, the following documents are also available free of charge on our website:

| · | Corporate governance policies |

| · | Business Code of Ethics |

| · | The charters of the following committees of our Board of Directors (the “Board”): Audit and Ethics, Compensation and Benefits, and Corporate Governance and Nominating |

Printed versions of these items will be mailed free of charge to shareholders upon request. Such requests can be made by contacting the Corporate Secretary at 1801 Bayberry Court, P. O. Box 18100, Richmond, Virginia 23226-8100.

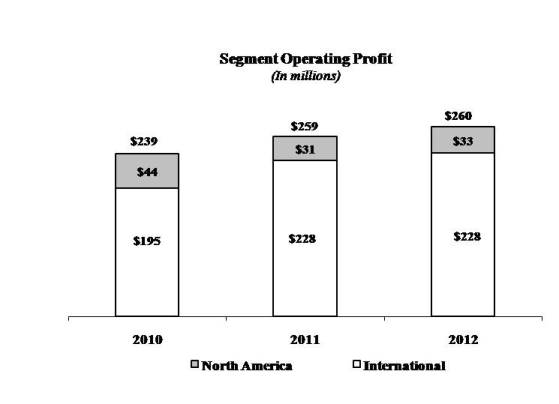

Business and Financial Highlights

Our 2012 segment operating profit was $260 million on revenues of $3.8 billion, resulting in a segment operating profit margin of 6.8%.

The following charts show Brink’s revenues and segment operating profit for each of 2010, 2011, and 2012 on both a U.S. generally accepted accounting principles (“GAAP”) basis and a Non-GAAP basis:

GAAP

Non-GAAP*

| | *Reconciliation to GAAP results appears on page 42 |

Amounts may not add due to rounding.

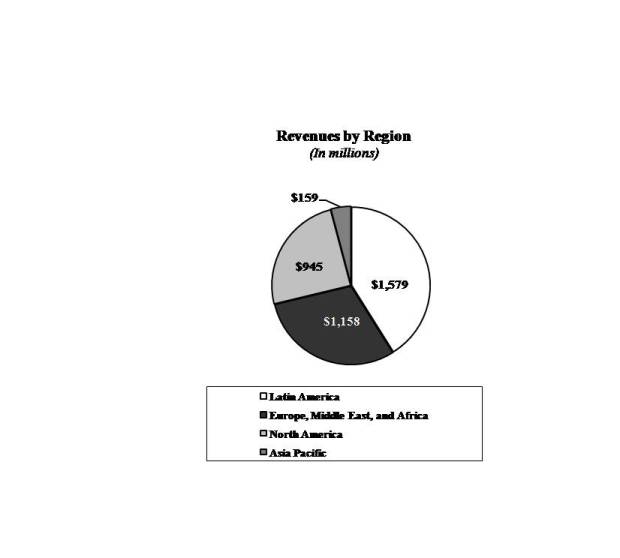

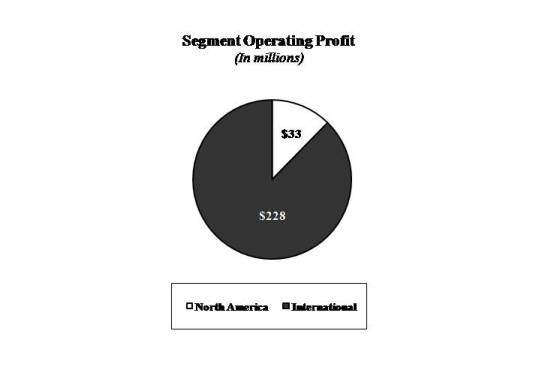

Brink’s operations are located around the world with the majority of our revenues (75%) and segment operating profit (88%) earned outside of North America.

Brink’s serves customers in over 100 countries. We have ownership interests in operations in approximately 50 countries and have agency relationships with companies in other countries to complete our global network. In some instances, local laws limit the extent of Brink’s ownership interest.

International operations have three regions: Latin America; Europe, Middle East and Africa (“EMEA”); and Asia Pacific. On a combined basis, international operations generated 2012 revenues of $2.9 billion (75% of total) and segment operating profit of $228 million (88% of total).

Brink’s Latin America generated $1.6 billion in revenues in 2012, representing 41% of Brink’s consolidated 2012 revenues, and operates 331 branches in 12 countries. Its largest operations are in Mexico, Brazil, Venezuela and Colombia. Mexico had $424 million or 27% of Latin America revenues in 2012. Brazil accounted for $388 million or 25% of Latin America revenues in 2012. Venezuela accounted for $343 million or 22% of Latin America revenues in 2012.

Brink’s EMEA generated $1.2 billion in revenues in 2012, representing 30% of Brink’s consolidated 2012 revenues and operates 270 branches in 25 countries. Its largest operations are in France and the Netherlands. In 2012, France accounted for $536 million or 46% of EMEA revenues.

Brink’s Asia-Pacific generated $159 million in revenues in 2012 (4%) and operates 103 branches in ten countries.

North American operations include 147 branches in the U.S. and 56 branches in Canada. North American operations generated 2012 revenues of $945 million, representing 25% of Brink’s consolidated 2012 revenues and segment operating profit of $33 million, representing 12% of consolidated segment operating profit.

The following charts show the Company’s revenues by region and segment operating profit:

The majority of Brink’s consolidated revenues in 2012 was earned in operations located in 9 countries, each contributing in excess of $100 million of revenues. The 2012 revenues from these countries totaled $3.0 billion or 79% of consolidated revenues. These operations, in declining order of revenues, were the U.S., France, Mexico, Brazil, Venezuela, Canada, Colombia, Argentina and the Netherlands.

| (In millions) | | 2012 | % total | % change | | | 2011 | | % total | % change | | | 2010 | | % total | % change |

| | | | | | | | | | | | | | | | | |

| Revenues by region: | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| Latin America: | | | | | | | | | | | | | | | | |

| Mexico | $ | 424.0 | 11 | 2 | | $ | 415.2 | | 11 | fav | | $ | 51.7 | | 2 | - |

| Brazil | | 388.3 | 10 | - | | | 386.8 | | 10 | 28 | | | 303.3 | | 10 | 18 |

| Venezuela | | 342.6 | 9 | 27 | | | 269.2 | | 7 | 45 | | | 185.9 | | 6 | (51) |

| Other | | 424.5 | 11 | 9 | | | 389.5 | | 10 | 16 | | | 336.5 | | 11 | 24 |

| Total | | 1,579.4 | 41 | 8 | | | 1,460.7 | | 38 | 66 | | | 877.4 | | 29 | (3) |

| | | | | | | | | | | | | | | | | |

| EMEA | | | | | | | | | | | | | | | | |

| France | | 535.5 | 14 | (2) | | | 545.2 | | 14 | 7 | | | 508.6 | | 17 | (17) |

| Other | | 622.9 | 16 | (2) | | | 632.5 | | 17 | 16 | | | 545.9 | | 18 | 12 |

| Total | | 1,158.4 | 30 | (2) | | | 1,177.7 | | 31 | 12 | | | 1,054.5 | | 35 | (4) |

| | | | | | | | | | | | | | | | | |

| Asia Pacific | | 158.9 | 4 | 3 | | | 153.7 | | 4 | 22 | | | 126.5 | | 4 | 61 |

| Total International | | 2,896.7 | 75 | 4 | | | 2,792.1 | | 74 | 36 | | | 2,058.4 | | 69 | (1) |

| | | | | | | | | | | | | | | | | |

| North America | | | | | | | | | | | | | | | | |

| U.S. | | 706.7 | 18 | (4) | | | 733.5 | | 19 | - | | | 732.4 | | 25 | - |

| Canada | | 238.7 | 6 | (1) | | | 240.7 | | 6 | 30 | | | 185.4 | | 6 | 14 |

| Total | | 945.4 | 25 | (3) | | | 974.2 | | 26 | 6 | | | 917.8 | | 31 | 3 |

| | | | | | | | | | | | | | | | | |

| Total Revenues | $ | 3,842.1 | 100 | 2 | | $ | 3,766.3 | | 100 | 27 | | $ | 2,976.2 | | 100 | - |

| Amounts may not add due to rounding. |

Geographic financial information related to revenues and long-lived assets is included in the consolidated financial statements on page 83.

Services

Brink’s typically provides customized services under separate contracts designed to meet the distinct needs of customers. Contracts usually cover an initial term of at least one year and range up to five years, depending on the service. The contracts generally remain in effect after the initial term until canceled by either party.

Core Services (55% of total revenues in 2012)

CIT and ATM Services are core services we provide to customers throughout the world. Core services generated approximately $2.1 billion of revenues in 2012.

CIT – Serving customers since 1859, our success in CIT is driven by a combination of rigorous security practices, high-quality customer service, risk management and logistics expertise. CIT services generally include the secure transportation of:

| · | cash between businesses and financial institutions such as banks and credit unions, |

| · | cash, securities and other valuables between commercial banks, central banks and investment banking and brokerage firms, and |

| · | new currency, coins, bullion and precious metals for central banks and other customers. |

ATM Services – We provide a comprehensive, integrated solution for payments processing and ATM managed services. We offer a variety of products and services, including forecasting, cash optimization, ATM remote monitoring, service call dispatching, transaction processing, installation services, first and second line maintenance, and cash replenishment. By providing these services, financial institutions and retailers worldwide can benefit from innovative, best-in-class solutions. Collectively, we manage nearly 96,000 ATMs worldwide.

High-value Services (36% of total revenues in 2012)

Our core services, combined with our brand and global infrastructure, provide a substantial platform from which we offer additional high-value services. High-value services generated approximately $1.4 billion of revenues in 2012.

Global Services – Serving customers in more than 100 countries, Brink’s is a leading global provider of secure logistics for valuables including diamonds, jewelry, precious metals, securities, currency, high-tech devices, electronics and pharmaceuticals. The comprehensive suite of services provides packing, pickup, secure storage, inventory management, customs clearance, consolidation and secure transport and delivery through a combination of armored vehicles and secure

air and sea transportation to leverage our extensive global network. Our specialized diamond and jewelry operations have offices in the major diamond and jewelry centers of the world.

Cash Management Services – Brink’s offers a fully integrated approach to managing the supply chain of cash, from point-of-sale through transport, vaulting, bank deposit and related credit. Cash Management Services include:

| · | money processing and cash management services, |

| · | deploying and servicing “intelligent” safes and safe control devices, including our patented CompuSafeâ service, |

| · | integrated check and cash processing services (“Virtual Vault”), and |

Money processing services generally include counting, sorting and wrapping currency. Other currency management services include cashier balancing, counterfeit detection, account consolidation and electronic reporting. Retail and bank customers use Brink’s to count and reconcile coins and currency, prepare bank deposit information and replenish coins and currency in specific denominations.

Brink’s offers a variety of advanced technology applications, including online cash tracking, cash inventory management, check imaging for real-time deposit processing, and a variety of other web-based information tools that enable banks and other customers to reduce costs while improving service to their customers.

Brink’s CompuSafeâ service offers customers an integrated, closed-loop system for preventing theft and managing cash. We market CompuSafe services to a variety of cash-intensive customers such as convenience stores, gas stations, restaurants, retail chains and entertainment venues. Once the specialized safe is installed, the customer’s employees deposit currency into the safe’s cassettes, which can only be removed by Brink’s personnel. Upon removal, the cassettes are securely transported to a vault for processing where contents are verified and transferred for deposit. Our CompuSafe system features currency-recognition and counterfeit-detection technology, multi-language touch screens and an electronic interface between the point-of-sale, back-office systems and external banks. Our electronic reporting interface with external banks enables our CompuSafe service customers to receive same-day credit on their cash balances, even if the cash remains on the customer’s premises.

Virtual Vault services combine CIT, Cash Management Services, vaulting and electronic reporting technologies to help banks expand into new markets while minimizing investment in vaults and branch facilities. In addition to secure storage, we process deposits, provide check imaging and reconciliation services, currency inventory management, ATM replenishment orders, and electronically transmit debits and credits.

We believe the quality and scope of our cash processing and information systems differentiate our Cash Management Services from competitive offerings.

Payment Services – We provide bill payment acceptance and processing services to utility companies and other billers. Consumers can pay their bills at our payment locations or locations that we operate on behalf of billers and bank customers.

Commercial Security Systems – In certain markets in Asia-Pacific and Europe, we provide commercial security system services. The services include the design and installation of the security systems, including alarms, motion detectors, closed-circuit televisions, digital video recorders, access control systems including card and biometric readers, electronic locks, and optical turnstiles. Monitoring services may also be provided after systems have been installed.

Other Security Services (9% of total revenues in 2012)

Security and Guarding – We protect airports, offices, warehouses, stores, and public venues with electronic surveillance, access control, fire prevention and highly trained patrolling personnel.

Our guarding services are generally offered in European markets, including France, Germany, Luxembourg and Greece. A significant portion of this business involves long-term contracts related primarily to guarding services at airports and embassies. Generally, other guarding contracts are for a one-year period, the majority of which are extended. Our security officers are typically stationed at customer sites, and responsibilities include detecting and deterring specific security threats.

Growth Strategy

Our growth strategy is summarized below:

| · | Maximize profits in developed markets (primarily North America and Europe) |

| · | Accelerate productivity investments and cost control efforts. |

| · | Invest in higher-margin solutions; shift revenue mix to High-Value Services (primarily Cash Management Services and Global Services). |

· | Reduce presence in underperforming markets. |

| · | Invest in emerging markets that meet internal metrics for projected growth, profitability and return on investment. |

| · | Invest in adjacent security-related markets where we can create value for customers with our brand, security expertise, global infrastructure and other competitive advantages. Current examples include full-service ATM management (Threshold) and payment processing (ePago and Brink’s Money™ prepaid cards). |

Industry and Competition

Brink’s competes with large multinational, regional and smaller companies throughout the world. Our largest multinational competitors are G4S plc (headquartered in the U.K.); Loomis AB, formerly a division of Securitas AB (Sweden); Prosegur, Compania de Seguridad, S.A. (Spain); and Garda World Security Corporation (Canada).

We believe the primary factors in attracting and retaining customers are security expertise, service quality, and price. Our competitive advantages include:

| · | brand name recognition; |

| · | reputation for a high level of service and security; |

| · | risk management and logistics expertise; |

| · | global infrastructure and customer base; |

| · | proprietary cash processing and information systems; |

| · | proven operational excellence; and |

| · | high-quality insurance coverage and general financial strength. |

Our cost structure is generally competitive, although certain competitors may have lower costs due to a variety of factors, including lower wages, less costly employee benefits, or less stringent security and service standards.

Although we face competitive pricing pressure in many markets, we resist competing on price alone. We believe our high levels of service and security, as well as value added solutions differentiate us from competitors.

The availability of high-quality and reliable insurance coverage is an important factor in our ability to attract and retain customers and manage the risks inherent in our business. We purchase insurance coverage for losses in excess of what we consider to be prudent levels of self-insurance. Our insurance policies cover losses from most causes, with the exception of war, nuclear risk and certain other exclusions typical in such policies.

Insurance for security is provided by different groups of underwriters at negotiated rates and terms. Premiums fluctuate depending on market conditions. The security loss experience of Brink’s and, to a limited extent, other armored carriers affects our premium rates.

Revenues are generated from charges per service performed or based on the value of goods transported. As a result, revenues are affected by the level of economic activity in various markets as well as the volume of business for specific customers. CIT and ATM contracts usually cover an initial term of at least one year and in many cases one to three years, and generally remain in effect thereafter until canceled by either party. Contracts for Cash Management Services are typically longer. Costs are incurred when preparing to serve a new customer or to transition away from an existing customer. Operating profit is generally stronger in the second half of the year, particularly in the fourth quarter, as economic activity is typically stronger during this period.

As part of the spin-off of our former monitored home security business, Brink’s Home Security Holdings, Inc. (“BHS”), we agreed to not compete with BHS in the United States, Canada and Puerto Rico with respect to certain activities related to BHS’s security system monitoring and surveillance business until October 31, 2013.

Service Mark and Patents

BRINKS is a registered service mark in the U.S. and certain foreign countries. The BRINKS mark, name and related marks are of material significance to our business. We own patents for safes, including our integrated CompuSafeâ service, which expire between 2015 and 2027. These patents provide us with important advantages; however, we are not dependent on the existence of these patents.

We have licensed the Brink’s name to a limited number of companies, including a distributor of security products (padlocks, door hardware, etc.) offered for sale to consumers through major retail chains.

Government Regulation

Our U.S. operations are subject to regulation by the U.S. Department of Transportation with respect to safety of operations, equipment and financial responsibility. Intrastate operations in the U.S. are subject to state regulation. Our International operations are regulated to varying degrees by the countries in which we operate.

Employee Relations

At December 31, 2012, our company had approximately 70,000 full-time and contract employees, including approximately 7,600 employees in the United States (of whom approximately 700 were classified as part-time employees) and approximately 62,400 employees outside the United States. At December 31, 2012, Brink’s was a party to twelve collective bargaining agreements in North America with various local unions covering approximately 1,800 employees. The agreements have various expiration dates from 2013 to 2016. Outside of North America, approximately 58% of employees are represented by trade union organizations. We believe our employee relations are satisfactory.

Acquisitions

Below is a summary of our recent acquisitions. Our largest acquisitions in the last three years were operations based in Mexico and Canada. See note 6 to the consolidated financial statements for more information on the acquisitions.

2010

France. We acquired Est Valeurs S.A., a provider of CIT and cash services in Eastern France, in March 2010. Est Valeurs employs approximately 100 people and at the acquisition date had annual revenues of $13 million.

Russia. We acquired a majority stake in a Russian cash processing business in April 2010 that complements a Russian CIT business that was acquired in January 2009. With principal operations in Moscow and approximately 500 employees, the combined operations offer a full range of CIT, ATM, money processing and Global Services operations for domestic and international markets.

Mexico. We acquired a controlling interest in Servicio Pan Americano de Proteccion, S.A. de C.V. (“SPP”), a CIT, ATM and money processing business, for $60 million in November 2010. We previously owned a 21% interest in SPP and we acquired an additional 79% of the outstanding shares. SPP is the largest secure logistics company in Mexico and this acquisition expands our operations in one of the world’s largest CIT markets. At the acquisition date, SPP had approximately $400 million in annual revenues with approximately 12,000 full-time and contract employees, 80 branches and 1,350 armored vehicles across its nationwide network of CIT, ATM and money processing operations.

Canada. We acquired Threshold Financial Technologies Inc. (“Threshold”) from Versent Corporation for $39 million in December 2010. Threshold is a leading provider of payments solutions in Canada, specializing in managed ATM and transaction processing services for financial institutions and retailers. At the acquisition date, Threshold’s annual revenues were approximately $48 million, about half of which was generated by providing outsourced ATM network administration and transaction processing solutions. The company, which employs approximately 160 people, also owns and operates a network of private-label ATMs in Canada.

2011

There were no significant acquisitions in 2011.

2012

France. We acquired Kheops, SAS, a provider of logistics software and related services, for approximately $17 million in January 2012. This acquisition gives us proprietary control of software used primarily in our cash-in-transit and money processing operations in France.

2013

Brazil. On January 31, Brink’s acquired Brazil-based Rede Transacoes Eletronicas Ltda. (“Redetrel”) for approximately $26 million. Redetrel distributes electronic prepaid products, including mobile phone airtime, via a network of approximately 20,000 retail locations across Brazil. Redetrel’s strong distribution network supplements Brink’s existing payments business, ePago, which has operations in Brazil, Mexico, Colombia and Panama.

Discontinued Operations

Certain CIT and Guarding Operations in Europe. In 2012, we agreed to sell our cash-in-transit operations in Germany and Poland as well as event security operations in France. The divestiture in France closed in January 2013 and the divestitures in Germany and Poland are expected to be completed in the first half of 2013. We completed the divestiture of guarding operations in Morocco in December 2012.

Our former cash-in-transit operation in Belgium filed for bankruptcy in November 2010, after a restructuring plan was rejected by local union employees, and was placed in bankruptcy on February 2, 2011. We deconsolidated the Belgium subsidiary in 2010.

The results of the above European operations in Germany, Poland, France, Morocco and Belgium have been excluded from continuing operations and are reported as discontinued operations for the current and prior periods.

We will continue to operate our Global Services business in each of these countries.

Former Coal Businesses. We have significant liabilities related to benefit plans that pay medical costs for retirees of our former coal operations. A portion of these liabilities has been funded. We expect to have ongoing expenses within continuing operations and future cash outflow for these liabilities. See notes 3 and 17 to the consolidated financial statements for more information.

We operate in highly competitive industries.

We compete in industries that are subject to significant competition and pricing pressures in most markets. Because we believe we have competitive advantages such as brand name recognition and a reputation for a high level of service and security, we resist competing on price alone. However, continued pricing pressure from competitors or failure to achieve pricing based on the competitive advantages identified above could affect our customer base or pricing structure and have an adverse effect on our business, financial condition, results of operations and cash flows. In addition, given the highly competitive nature of our industries, it is important to develop new solutions and product and service offerings to help retain and expand our customer base. Failure to develop, sell and execute new solutions and offerings in a timely and efficient manner could also negatively affect our ability to retain our existing customer base or pricing structure and have an adverse effect on our business, financial condition, results of operations and cash flows.

Decreased use of cash could have a negative impact on our business.

The proliferation of payment options other than cash, including credit cards, debit cards, stored-value cards, mobile payments and on-line purchase activity, could result in a reduced need for cash in the marketplace and a decline in the need for physical bank branches and retail stores. To mitigate this risk, we are developing new lines of business, but there is a risk that these initiatives may not offset the risks associated with our traditional cash-based business and that our business, financial condition, results of operations and cash flows could negatively impacted.

We have significant operations outside the United States.

We currently serve customers in more than 100 countries, including approximately 50 countries where we operate subsidiaries. Eighty-two percent (82%) of our revenue in 2012 came from operations outside the U.S. We expect revenue outside the U.S. to continue to represent a significant portion of total revenue. Business operations outside the U.S. are subject to political, economic and other risks inherent in operating in foreign countries, such as:

| · | the difficulty of enforcing agreements, collecting receivables and protecting assets through foreign legal systems; |

| · | trade protection measures and import or export licensing requirements; |

| · | difficulty in staffing and managing widespread operations; |

| · | required compliance with a variety of foreign laws and regulations; |

| · | enforcement of our global compliance program in foreign countries with a variety of laws, cultures and customs; |

| · | varying permitting and licensing requirements in different jurisdictions; |

| · | foreign ownership laws; |

| · | changes in the general political and economic conditions in the countries where we operate, particularly in emerging markets; |

| · | threat of nationalization and expropriation; |

| · | potential termination of the use of the euro and adoption of weaker new currencies as a result of the continued crisis in the Euro zone; |

| · | higher costs and risks of doing business in a number of foreign jurisdictions; |

| · | laws or other requirements and restrictions associated with organized labor; |

| · | limitations on the repatriation of earnings; |

| · | fluctuations in equity, revenues and profits due to changes in foreign currency exchange rates, including measures taken by governments to devalue official currency exchange rates; |

| · | inflation levels exceeding that of the U.S; and |

| · | inability to collect for services provided to government entities. |

We are exposed to certain risks when we operate in countries that have high levels of inflation, including the risk that:

| · | the rate of price increases for services will not keep pace with the cost of inflation; |

| · | adverse economic conditions may discourage business growth which could affect demand for our services; |

| · | the devaluation of the currency may exceed the rate of inflation and reported U.S. dollar revenues and profits may decline; and |

| · | these countries may be deemed “highly inflationary” for U.S. generally accepted accounting principles (“GAAP”) purposes. |

We manage these risks by monitoring current and anticipated political and economic developments, monitoring adherence to our global compliance program and adjusting operations as appropriate. Changes in the political or economic environments of the countries in which we operate could have a material adverse effect on our business, financial condition, results of operations and cash flows.

Our growth strategy may not be successful.

One element of our growth strategy is to extend our brand, strengthen our brand portfolio and expand our geographic reach through selective acquisitions and divestitures. While we may identify numerous acquisitions and divestitures opportunities, our due diligence examinations and positions that we may take with respect to appropriate valuations and other transaction terms and conditions may hinder our ability to successfully complete business transactions to achieve our strategic goals. In addition, acquisitions present risks of failing to achieve efficient and effective integration, strategic objectives, anticipated revenue and segment operating profit improvements. There can be no assurance that:

| · | we will be able to acquire attractive businesses on favorable terms, |

| · | all future acquisitions will be accretive to earnings, or |

| · | future acquisitions will be rapidly and efficiently integrated into existing operations. |

We may not realize the expected benefits of strategic acquisitions because of integration difficulties and other challenges, which may adversely affect our financial condition, results of operations or cash flows.

Our ability to realize the anticipated benefits from recent acquisitions will depend, in part, on successfully integrating each business with our company as well as improving operating performance and profitability through our management efforts and capital investments. The risks to a successful integration and improvement of operating performance and profitability include, among others, failure to implement our business plan, unanticipated issues in integrating operations with ours, unanticipated changes in laws and regulations, labor unrest resulting from union operations, regulatory, environmental and permitting issues, the effect on our internal controls and compliance with the regulatory requirements under the Sarbanes-Oxley Act of 2002, and difficulties in fully identifying and evaluating potential liabilities, risks and operating issues. The occurrence of any of these events may adversely affect our expected benefits of the recent acquisitions and may have a material adverse effect on our financial condition, results of operations or cash flows.

We have significant deferred tax assets in the United States that may not be realized.

Deferred tax assets are future tax deductions that result primarily from net operating losses and the net tax effects of temporary differences between the carrying amount of assets and liabilities for financial statement and income tax purposes. We have $363 million of U.S. deferred tax assets recorded at the end of 2012. These future tax deductions may not be realized if our expectations of future margin improvements of our U.S. business are not attained. Consequently, not realizing our U.S. deferred tax assets may significantly and materially affect our financial condition, results of operations and cash flows.

Restructuring charges may be required in the future.

There is a possibility we will take restructuring actions in one or more of our markets in the future to reduce expenses if a major customer is lost, if recurring operating losses continue, or if one of the risks described above in connection with our foreign operations materializes. These actions could result in significant restructuring charges at these subsidiaries, including recognizing impairment charges to write down assets, and recording accruals for employee severance and operating leases. These charges, if required, could significantly and materially affect results of operations and cash flows.

We have significant retirement obligations. Poor investment performance of retirement plan holdings and / or lower interest rates used to discount the obligations could unfavorably affect our liquidity and results of operations.

We have substantial pension and retiree medical obligations, a portion of which have been funded. The amount of these obligations is significantly affected by factors that are not in our control, including interest rates used to determine the present value of future payment streams, investment returns, medical inflation rates, participation rates and changes in laws and regulations. The funded status of the primary U.S. pension plan was approximately 74% as of December 31, 2012. Based on actuarial assumptions at the end of 2012, we expect that we will be required to make contributions totaling $239 million to the plan over a nine-year period ending in 2021. This could adversely affect our liquidity and our ability to use our resources to make acquisitions and to otherwise grow our business.

We have $854 million of actuarial losses recorded in accumulated other comprehensive income (loss) at the end of 2012, which are the result of decreasing interest rates used to discount the obligations for accounting purposes, investment returns that have been lower than expected and changes in other actuarial estimates in the last several years. These losses will be recognized in earnings in future periods to the extent they are not offset by future actuarial gains.

If our retirement plans have additional investment or other actuarial losses, our future cash requirements and costs for these plans will be further adversely affected.

Currency restrictions in Venezuela limit our ability to use earnings and cash flows and may negatively affect ongoing operations in Venezuela.

Currency exchange restrictions prevent us from converting local currency in Venezuela to U.S. dollars, which limits our ability to repatriate earnings and to purchase certain goods and services needed to operate our Venezuelan business. We do not expect to be able to repatriate cash from Venezuela for the foreseeable future because of the local currency restrictions. At December 31, 2012, our Venezuelan subsidiaries held $0.5 million of cash and short-term investments denominated in U.S. dollars and $47.9 million of cash denominated in bolivar fuertes. We do not expect to be able to use this cash that is included in our balance sheet for general corporate purposes, including reducing our debt. In addition, our Venezuelan subsidiaries purchase various goods and services that are paid for in U.S. dollars. We believe that currency exchange restrictions in Venezuela may disrupt the operation of our business in Venezuela because we may be unable to pay for these goods and services in the future. This could reduce our ability to provide services to our customers in Venezuela, or could increase the cost of delivering the services, which would negatively affect our earnings and cash flows, and could result in a loss of control, shutdown or loss of the business in Venezuela.

Our earnings and cash flow could be materially affected by increased losses of customer valuables.

We purchase insurance coverage for losses of customer valuables for amounts in excess of what we consider prudent deductibles and/or retentions. Insurance is provided by different groups of underwriters at negotiated rates and terms. Coverage is available to us in major insurance markets, although premiums charged are subject to fluctuations depending on market conditions. Our loss experience and that of other armored carriers affects premium rates charged to us. We are self-insured for losses below our coverage limits and recognize expense up to these limits for actual losses. Our insurance policies cover losses from most causes, with the exception of war, nuclear risk and various other exclusions typical for such policies. The availability of high-quality and reliable insurance coverage is an important factor in order for us to obtain and retain customers and to manage the risks of our business. If our losses increase, or if we are unable to obtain adequate insurance coverage at reasonable rates, our financial condition, results of operations and cash flows could be materially and adversely affected.

We have risks associated with confidential individual information.

In the normal course of business, we collect, process and retain sensitive and confidential information about individuals. Despite the security measures we have in place, our facilities and systems, and those of third-party service providers, could be vulnerable to security breaches (including cybersecurity breaches), acts of vandalism, computer viruses, misplaced or lost data, programming or human errors or other similar events. Any security breach involving the misappropriation, loss or other unauthorized disclosure of confidential information, whether by us or by third-party service providers, could damage our reputation, expose us to the risks of litigation and liability, disrupt our business or otherwise have a material adverse effect on our business, financial condition, results of operations and cash flows.

Negative publicity to our name or brand could lead to a loss of revenue or profitability.

We are in the security business and our success and longevity are based to a large extent on our reputation for trust and integrity. Our reputation or brand, particularly the trust placed in us by our customers, could be negatively impacted in the event of perceived or actual breaches in our ability to conduct our business ethically, securely and responsibly. Any damage to our brand could have a material adverse effect on our business, financial condition, results of operations and cash flows.

Failures of our IT system could have a material adverse effect on our business.

We are heavily dependent on our information technology (IT) infrastructure. Significant problems with our infrastructure, such as telephone or IT system failure, cybersecurity breaches, or failure to develop new technology platforms to support new initiatives and product and service offerings, could halt or delay our ability to service our customers, hinder our ability to conduct and expand our business and require significant remediation costs. In addition, we continue to evaluate and implement upgrades to our IT systems. We are aware of inherent risks associated with replacing these systems, including accurately capturing data and system disruptions, and believe we are taking appropriate action to mitigate these risks through testing, training, and staging implementation. However, there can be no assurances that we will successfully launch these systems as planned or that they will occur without disruptions to our operations. Any of these events could have a material adverse effect on our business, financial condition, results of operations and cash flows.

We operate in regulated industries.

Our U.S. operations are subject to regulation by the U.S. Department of Transportation with respect to safety of operations and equipment and financial responsibility. Intrastate operations in the U.S. are subject to regulation by state regulatory authorities and interprovincial operations in Canada are subject to regulation by Canadian and provincial regulatory authorities. Our international operations are regulated to varying

degrees by the countries in which we operate. Many countries have permit requirements for security services and prohibit foreign companies from providing different types of security services.

Changes in laws or regulations could require a change in the way we operate, which could increase costs or otherwise disrupt operations. In addition, failure to comply with any applicable laws or regulations could result in substantial fines or revocation of our operating permits and licenses. If laws and regulations were to change or we failed to comply, our business, financial condition, results of operations and cash flows could be materially and adversely affected.

Our inability to access capital or significant increases in our cost of capital could adversely affect our business.

Our ability to obtain adequate and cost-effective financing depends on our credit ratings as well as the liquidity of financial markets. A negative change in our ratings outlook or any downgrade in our current investment-grade credit ratings by the rating agencies could adversely affect our cost and/or access to sources of liquidity and capital. Additionally, such a downgrade could increase the costs of borrowing under available credit lines. Disruptions in the capital and credit markets could adversely affect our ability to access short-term and long-term capital. Our access to funds under short-term credit facilities is dependent on the ability of the participating banks to meet their funding commitments. Those banks may not be able to meet their funding commitments if they experience shortages of capital and liquidity. Longer disruptions in the capital and credit markets as a result of uncertainty, changing or increased regulation, reduced alternatives, or failures of significant financial institutions could adversely affect our access to capital needed for our business.

We have retained obligations from the sale of BAX Global.

In January 2006 we sold BAX Global (the Company’s former international freight forwarding and logistics operations). We retained some of the obligations related to these operations, primarily for taxes owed prior to the date of sale and for any amounts paid related to one pending litigation matter for which we paid $11.5 million in 2010. In addition, we provided indemnification customary for these sorts of transactions. Future unfavorable developments related to these matters could require us to record additional expenses or make cash payments in excess of recorded liabilities. The occurrence of these events could have a material adverse effect on our financial condition, results of operations and cash flows.

We are subject to covenants for our credit facilities and for our unsecured notes.

Our credit facilities as well as our unsecured notes are subject to financial covenants, including a limit on the ratio of debt to earnings before interest, taxes, depreciation, and amortization, limits on the ability to pledge assets, limits on the total amount of indebtedness we can incur, limits on the use of proceeds of asset sales and minimum coverage of interest costs. Although we believe none of these covenants are presently restrictive to operations, the ability to meet the financial covenants can be affected by changes in our results of operations or financial condition. We cannot provide assurance that we will meet these covenants. A breach of any of these covenants could result in a default under existing credit facilities. Upon the occurrence of an event of default under any of our credit facilities, the lenders could cause amounts outstanding to be immediately payable and terminate all commitments to extend further credit. The occurrence of these events would have a significant effect on our liquidity and cash flows.

Our effective income tax rate could change.

We serve customers in more than 100 countries, including approximately 50 countries where we operate subsidiaries, all of which have different income tax laws and associated income tax rates. Our effective income tax rate can be significantly affected by changes in the mix of pretax earnings by country and the related income tax rates in those countries. In addition, our effective income tax rate is significantly affected by the ability to realize deferred tax assets, including those associated with net operating losses. Changes in income tax laws, income apportionment, or estimates of the ability to realize deferred tax assets, could significantly affect our effective income tax rate, financial position and results of operations.

We have certain environmental and other exposures related to our former coal operations.

We may incur future environmental and other liabilities in connection with our former coal operations, which could materially and adversely affect our financial condition, results of operations and cash flows.

We may be exposed to certain regulatory and financial risks related to climate change.

Growing concerns about climate change may result in the imposition of additional environmental regulations to which we are subject. Some form of federal regulation may be forthcoming with respect to greenhouse gas emissions (including carbon dioxide) and/or "cap and trade" legislation. The outcome of this legislation may result in new regulation, additional charges to fund energy efficiency activities or other

regulatory actions. Compliance with these actions could result in the creation of additional costs to us, including, among other things, increased fuel prices or additional taxes or emission allowances. We may not be able to recover the cost of compliance with new or more stringent environmental laws and regulations from our customers, which could adversely affect our business. Furthermore, the potential effects of climate change and related regulation on our customers are highly uncertain and may adversely affect our operations.

Forward-Looking Statements

This document contains both historical and forward-looking information. Words such as “anticipates,” “estimates,” “expects,” “projects,” “intends,” “plans,” “believes,” “may,” “should” and similar expressions may identify forward-looking information. Forward-looking information in this document includes, but is not limited to, statements regarding future performance of The Brink’s Company and its global operations, including organic revenue growth and segment operating profit margin in 2013; execution of the Company’s growth strategy, pending acquisitions and dispositions, expenses and cash outflows related to former operations, future contributions to our Pension-Retirement Plan, the repatriation of cash from our Venezuelan operations, the anticipated financial effect of pending litigation, the pursuit of higher margin business opportunities, investments in information technology, profit growth and expected margins in the Company’s regional markets, growth of our Global Services business, the acquisition of new vehicles in the United States with capital leases, expected non-segment income and expenses, 2013 projected interest expense, the realization of deferred tax assets, our anticipated effective tax rate for 2013 and our tax position, the reinvestment of earnings on operations outside the United States, net income attributable to noncontrolling interests, projected currency impact on revenue, capital expenditures, capital leases and depreciation and amortization, the funding of our acquisition strategy and pension obligations, the trend of capital expenditures exceeding depreciation and amortization, the ability to meet liquidity needs, future payment of bonds issued by the Peninsula Ports Authority of Virginia, contribution of shares of common stock to satisfy pension contribution requirements, estimated contractual obligations for the next five years and beyond, projected contributions, expenses and payouts for the U.S. retirement plans and the non-U.S. pension plans and the expected long-term rate of return and funded status of the primary U.S. pension plan, expected liability for and future contributions to the UMWA plans, liability for black lung obligations, the projected impact of future excise tax on the UMWA plans, our ability to obtain U.S. dollars to operate our business in Venezuela, the effect of accounting rule changes, the performance of counterparties to hedging agreements, the recognition of unrecognized tax positions, future amortizations into net periodic pension cost, the deductibility of goodwill, projected minimum repayments of long-term debt, the replacement of operating leases, future minimum lease payments, and the recognition of costs related to stock option grants. Forward-looking information in this document is subject to known and unknown risks, uncertainties, and contingencies, which could cause actual results, performance or achievements to differ materially from those that are anticipated.

These risks, uncertainties and contingencies, many of which are beyond our control, include, but are not limited to:

| · | continuing market volatility and commodity price fluctuations and their impact on the demand for our services; |

| · | our ability to continue profit growth in Latin America; |

| · | the effect of current macro-economic uncertainty on our operations in Europe; |

| · | our ability to maintain or improve volumes at favorable pricing levels and increase cost efficiencies in the United States and Europe; |

| · | investments in information technology and value-added services and their impact on revenue and profit growth; |

| · | our ability to implement high-value solutions; |

| · | risks customarily associated with operating in foreign countries including changing labor and economic conditions, currency devaluations, safety and security issues, political instability, restrictions on repatriation of earnings and capital, nationalization, expropriation and other forms of restrictive government actions; |

| · | the strength of the U.S. dollar relative to foreign currencies and foreign currency exchange rates; |

| · | the stability of the Venezuelan economy, changes in Venezuelan policy regarding foreign-owned businesses, and changes in exchange rates; |

| · | fluctuations in value of the Venezuelan bolivar fuerte; |

| · | regulatory and labor issues in many of our global operations, including negotiations with organized labor and the possibility of work stoppages; |

| · | our ability to identify and execute further cost and operational improvements and efficiencies in our core businesses; |

| · | our ability to integrate successfully recently acquired companies and improve their operating profit margins; |

| · | the actions of competitors; |

| · | our ability to identify acquisitions and other strategic opportunities in emerging markets; |

| · | the willingness of our customers to absorb fuel surcharges and other future price increases; |

| · | the impact of turnaround actions responding to current conditions in Europe and North America and our productivity and cost control efforts in those regions; |

| · | our ability to obtain necessary information technology and other services at favorable pricing levels from third party service providers; |

| · | variations in costs or expenses and performance delays of any public or private sector supplier, service provider or customer; |

| · | our ability to obtain appropriate insurance coverage, positions taken by insurers with respect to claims made and the financial condition of insurers, safety and security performance, our loss experience, changes in insurance costs; |

| · | security threats worldwide and losses of customer valuables; |

| · | costs associated with the purchase and implementation of cash processing and security equipment; |

| · | employee and environmental liabilities in connection with our former coal operations, black lung claims incidence; |

| · | the impact of the Patient Protection and Affordable Care Act on black lung liability and the Company's ongoing operations; |

| · | changes to estimated liabilities and assets in actuarial assumptions due to payments made, investment returns, interest rates and annual actuarial revaluations, the funding requirements, accounting treatment, investment performance and costs and expenses of our pension plans, the VEBA and other employee benefits, mandatory or voluntary pension plan contributions, the nature of our hedging relationships; |

| · | changes in estimates and assumptions underlying our critical accounting policies; |

| · | the outcome of pending and future claims and litigation; |

| · | access to the capital and credit markets; |

| · | seasonality, pricing and other competitive industry factors; and |

| · | the promulgation and adoption of new accounting standards and interpretations, new government regulations and interpretations of existing regulations. |

The information included in this document is representative only as of the date of this document, and The Brink’s Company undertakes no obligation to update any information contained in this document.

ITEM 1B. UNRESOLVED STAFF COMMENTS

Not applicable.

We have property and equipment in locations throughout the world. Branch facilities generally have office space to support operations, a vault to securely process and store valuables and a garage to house armored vehicles and serve as a vehicle terminal. Many branches have additional space to repair and maintain vehicles.

We own or lease armored vehicles, panel trucks and other vehicles that are primarily service vehicles. Our armored vehicles are of bullet-resistant construction and are specially designed and equipped to provide security for the crew and cargo.

The following table discloses leased and owned facilities and vehicles for Brink’s most significant operations as of December 31, 2012.

| | | | Facilities | Vehicles | |

| | Region | | Leased | | Owned | | Total | | | Leased | | Owned | | Total | |

| | | | | | | �� | | | | | | | | | | | | | | | | |

| | U.S. | | 141 | | | 26 | | | 167 | | | | 1,990 | | | 202 | | | 2,192 | | |

| | Canada | | 43 | | | 14 | | | 57 | | | | 392 | | | 19 | | | 411 | | |

| | | North America | | 184 | | | 40 | | | 224 | | | | 2,382 | | | 221 | | | 2,603 | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | Latin America | | 400 | | | 110 | | | 510 | | | | 477 | | | 5,855 | | | 6,332 | | |

| | EMEA | | 261 | | | 36 | | | 297 | | | | 728 | | | 2,984 | | | 3,712 | | |

| | Asia Pacific | | 110 | | | - | | | 110 | | | | 4 | | | 609 | | | 613 | | |

| | | International | | 771 | | | 146 | | | 917 | | | | 1,209 | | | 9,448 | | | 10,657 | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | Total | | 955 | | | 186 | | | 1,141 | | | | 3,591 | | | 9,669 | | | 13,260 | | |

As of December 31, 2012, we had approximately 17,500 units for our CompuSafe® service installed worldwide, of which approximately 14,900 units were located in the U.S.

ITEM 3. LEGAL PROCEEDINGS

We are involved in various lawsuits and claims in the ordinary course of business. We are not able to estimate the range of losses for some of these matters. We have recorded accruals for losses that are considered probable and reasonably estimable. We do not believe that the ultimate disposition of any of these matters will have a material adverse effect on our liquidity, financial position or results of operations.

ITEM 4. MINE SAFETY DISCLOSURES

Not applicable.

Executive Officers of the Registrant

The following is a list as of February 21, 2013, of the names and ages of the executive and other officers of Brink’s indicating the principal positions and offices held by each. There are no family relationships among any of the officers named.

| Name | | Age | | Positions and Offices Held | | Held Since | |

| Executive Officers: | | | | | | | |

| Thomas C. Schievelbein | | | 59 | | Chairman, President and Chief Executive Officer | | | 2012 | |

| Joseph W. Dziedzic | | | 44 | | Vice President and Chief Financial Officer | | | 2009 | |

| McAlister C. Marshall, II | | | 43 | | Vice President, General Counsel and Secretary | | | 2008 | |

| Ronald F. Rokosz | | | 67 | | Vice President – International | | | 2011 | |

| Matthew A. P. Schumacher | | | 54 | | Controller | | | 2001 | |

| Holly Tyson | | | 41 | | Vice President and Chief Human Resources Officer | | | 2012 | |

| | | | | | | | | | |

| Other Officers: | | | | | | | | | |

| Jonathan A. Leon | | | 46 | | Treasurer | | | 2008 | |

| Lisa M. Landry | | | 47 | | Vice President - Tax | | | 2009 | |

| Arthur E. Wheatley | | | 70 | | Vice President – Risk Management and Insurance | | | 2005 | |

Executive and other officers of the Company are elected annually and serve at the pleasure of the Board.

Mr. Schievelbein is the Chairman, President and Chief Executive Officer of the Company and has held that position since June 2012, prior to which he served as the interim President and Chief Executive Officer of the Company from December 2011 to June 2012 and the interim Executive Chairman of the Company from November 2011 to December 2011. He has also served as a director of the Company since March 2009. He was President of Northrop Grumman Newport News, a subsidiary of the Northrop Grumman Corporation, a global defense company, from November 2001 until November 2004, and was a business consultant from November 2004 to November 2011. Mr. Schievelbein currently also serves as a director of Huntington Ingalls Industries, Inc. and New York Life Insurance Company.

Mr. Dziedzic is the Vice President and Chief Financial Officer of the Company. Mr. Dziedzic was hired in May 2009 and appointed to this position in August 2009. Before joining the Company, Mr. Dziedzic was Chief Financial Officer at GE Aviation Services, a producer, seller and servicer of jet engines, turboprop and turbo shaft engines and related replacement parts, from March 2006 to May 2009.

Mr. Marshall was appointed Vice President and General Counsel of the Company in September 2008 and Secretary of the Company in June 2012. He also previously held the office of Secretary from September 2008 to July 2009. Prior to joining the Company, Mr. Marshall was the Vice President, General Counsel and Secretary at Tredegar Corporation, a manufacturer of plastic films and aluminum extrusions, from October 2006 to September 2008.

Mr. Rokosz was appointed Vice President-International of the Company in November 2011. He also serves as Executive Vice President and Chief Operating Officer of Brink’s, Incorporated, a position he has held since January 2009. Prior to this position, Mr. Rokosz was President - Brink’s International of Brink’s, Incorporated from October 2006 to January 2009.

Mr. Schumacher has served in his present position for more than the past five years.

Ms. Tyson is the Vice President and Chief Human Resources Officer of the Company. Ms. Tyson was hired in August 2012 and appointed to this position in September 2012. Before joining the Company, Ms. Tyson was with Bristol-Myers Squibb Company, a global biopharmaceutical company, where she was Vice President U.S. Pharmaceuticals Human Resources from 2010 to 2012, Executive Director World Wide Pharmaceuticals Talent & U.S. Pharmaceutical Sales Learning from 2009 to 2010, Senior Director Human Resources & U.S. Pharmaceuticals Sales Learning from 2008 to 2009 and Director Human Resources Cardiovascular Metabolics from 2006 to 2008.

Mr. Leon is the Company’s Treasurer. Mr. Leon was hired in June 2008 and appointed to this position in July 2008. Before joining the Company, Mr. Leon was the Assistant Treasurer for Universal Corporation, a leaf tobacco merchant and processor, from January 2007 to June 2008. Prior to this position, Mr. Leon was the Assistant Treasurer of the Company from July 2005 to January 2007.

Ms. Landry was appointed Vice President-Tax of the Company in July 2009. Prior to this position, Ms. Landry was Director of Taxes and Chief Tax Counsel of the Company from December 2006 to July 2009.

Mr. Wheatley has served in his present position for more than the past five years.

ITEM 5. MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

Our common stock trades on the New York Stock Exchange under the symbol “BCO.” As of February 15, 2013, there were 1,801 shareholders of record of common stock.

The dividends declared and the high and low prices of our common stock for each full quarterly period within the last two years are as follows:

| | | 2012 Quarters | | | 2011 Quarters | |

| | | 1 st | | | 2 nd | | | 3 rd | | | 4 th | | | 1 st | | | 2 nd | | | 3 rd | | | 4 th | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| Dividends declared per common share | | $ | 0.1000 | | | | 0.1000 | | | | 0.1000 | | | | 0.1000 | | | $ | 0.1000 | | | | 0.1000 | | | | 0.1000 | | | | 0.1000 | |

| Stock prices: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| High | | $ | 29.64 | | | | 26.73 | | | | 25.82 | | | | 29.87 | | | $ | 33.24 | | | | 34.46 | | | | 31.91 | | | | 31.37 | |

| Low | | | 23.39 | | | | 20.91 | | | | 21.70 | | | | 24.67 | | | | 26.24 | | | | 26.75 | | | | 21.71 | | | | 21.53 | |

See note 16 to the consolidated financial statements for a description of limitations of our ability to pay dividends in the future.

On March 6, 2012, the Company made a contribution of 361,446 shares of the Company’s common stock (the “Shares”) to The Brink’s Company Pension-Retirement Plan Trust (the “Trust”) created under The Brink’s Company Pension-Retirement Plan (the “Plan”) in consideration for a credit against the Company’s funding obligations to the Plan. The Shares were valued for purposes of the contribution at $24.90 per share, or $9.0 million in the aggregate. The Shares were contributed to the Trust in a private placement transaction made in reliance upon the exemption from registration provided by Section 4(2) of the Securities Act of 1922, as amended.

The following graph compares the cumulative 5-year total return provided to shareholders of The Brink’s Company’s common stock compared to the cumulative total returns of the S&P Midcap 400 index and the S&P Midcap 400 Commercial Services & Supplies Index. The graph tracks the performance of a $100 investment in our common stock and in each index from December 31, 2007, through December 31, 2012. The performance of The Brink’s Company’s common stock assumes that the shareholder reinvested all dividends received during the period and reinvested the proceeds of a hypothetical sale of shares received from the spin-off of our former monitored security business on October 31, 2008.

*$100 invested on 12/31/07 in stock or index, including reinvestment of dividends.

Fiscal year ending December 31.

Copyright© 2013 S&P, a division of The McGraw-Hill Companies Inc. All rights reserved.

Source: Zacks Investment Research, Inc.

Comparison of Five-Year Cumulative Total Return Among

Brink’s Common Stock, the S&P MidCap 400 Index and

the S&P Midcap 400 Commercial Services & Supplies Index (a)

| | | Years Ended December 31, | |

| | | 2007 | | | 2008 | | | 2009 | | | 2010 | | | 2011 | | | 2012 | |

| | | | | | | | | | | | | | | | | | | |

| The Brink's Company | | $ | 100.00 | | | | 81.54 | | | | 74.93 | | | | 84.19 | | | | 85.41 | | | | 92.10 | |

| S&P Midcap 400 Index | | | 100.00 | | | | 63.76 | | | | 87.59 | | | | 110.92 | | | | 108.99 | | | | 128.46 | |

| S&P Midcap 400 Commercial Services & Supplies Index | | | 100.00 | | | | 74.51 | | | | 89.69 | | | | 109.40 | | | | 119.11 | | | | 139.48 | |

| Copyright © 2013, Standard & Poor's, a division of The McGraw-Hill Companies, Inc. All rights reserved. | |

| (a) | For the line designated as “The Brink’s Company” the graph depicts the cumulative return on $100 invested in The Brink’s Company’s common stock. For the S&P Midcap 400 Index and the S&P Midcap 400 Commercial Services & Supplies Index, cumulative returns are measured on an annual basis for the periods from December 31, 2007, through December 31, 2012, with the value of each index set to $100 on December 31, 2007. Total return assumes reinvestment of dividends and the reinvestment of proceeds from the sale of the shares received related to the spin-off of our former monitored security business on October 31, 2008. We chose the S&P Midcap 400 Index and the S&P Midcap 400 Commercial Services & Supplies Index because we are included in these indices, which broadly measure the performance of mid-size companies in the United States market. |

ITEM 6. SELECTED FINANCIAL DATA

Five Years in Review

| GAAP Basis | |

| (In millions, except per share amounts) | | 2012 | | | 2011 | | | 2010 | | | 2009 | | | 2008 | |

| | | | | | | | | | | | | | | | |

| Revenues and Income | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| Revenues | | $ | 3,842.1 | | | | 3,766.3 | | | | 2,976.2 | | | | 2,978.7 | | | | 3,003.0 | |

| | | | | | | | | | | | | | | | | | | | | |

| Segment operating profit | | $ | 260.1 | | | | 259.3 | | | | 239.1 | | | | 231.2 | | | | 278.0 | |

| Non-segment income (expense) | | | (88.9 | ) | | | (59.8 | ) | | | (62.6 | ) | | | (46.6 | ) | | | (43.4 | ) |

| Operating profit | | $ | 171.2 | | | | 199.5 | | | | 176.5 | | | | 184.6 | | | | 234.6 | |

| | | | | | | | | | | | | | | | | | | | | |

| Income attributable to Brink’s: | | | | | | | | | | | | | | | | | | | | |

| Income from continuing operations | | | 106.8 | | | | 96.5 | | | | 81.6 | | | | 213.6 | | | | 138.6 | |

| (Loss) income from discontinued operations (a) | | | (17.9 | ) | | | (22.0 | ) | | | (24.5 | ) | | | (13.4 | ) | | | 44.7 | |

| Net income attributable to Brink’s | | $ | 88.9 | | | | 74.5 | | | | 57.1 | | | | 200.2 | | | | 183.3 | |

| Financial Position | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| Property and equipment, net | | $ | 793.8 | | | | 749.2 | | | | 698.9 | | | | 549.5 | | | | 534.0 | |

| Total assets | | | 2,553.9 | | | | 2,406.2 | | | | 2,270.5 | | | | 1,879.8 | | | | 1,815.8 | |

| Long-term debt, less current maturities | | | 335.6 | | | | 335.3 | | | | 323.7 | | | | 172.3 | | | | 173.0 | |

| Brink’s shareholders’ equity | | | 501.8 | | | | 408.0 | | | | 516.2 | | | | 534.9 | | | | 214.0 | |

| | | | | | | | | | | | | | | | | | | | | |

| Supplemental Information | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| Depreciation and amortization | | $ | 165.5 | | | | 156.6 | | | | 126.6 | | | | 124.6 | | | | 112.3 | |

| Capital expenditures | | | 184.5 | | | | 192.0 | | | | 137.8 | | | | 162.2 | | | | 151.2 | |

| | | | | | | | | | | | | | | | | | | | | |

| Earnings per share attributable to Brink’s common shareholders | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| Basic: | | | | | | | | | | | | | | | | | | | | |

| Continuing operations | | $ | 2.21 | | | | 2.02 | | | | 1.69 | | | | 4.52 | | | | 2.99 | |

| Discontinued operations (a) | | | (0.37 | ) | | | (0.46 | ) | | | (0.51 | ) | | | (0.28 | ) | | | 0.96 | |

| Net income | | $ | 1.84 | | | | 1.56 | | | | 1.18 | | | | 4.23 | | | | 3.96 | |

| | | | | | | | | | | | | | | | | | | | | |

| Diluted: | | | | | | | | | | | | | | | | | | | | |

| Continuing operations | | $ | 2.20 | | | | 2.01 | | | | 1.69 | | | | 4.49 | | | | 2.97 | |

| Discontinued operations (a) | | | (0.37 | ) | | | (0.46 | ) | | | (0.51 | ) | | | (0.28 | ) | | | 0.96 | |

| Net income | | $ | 1.83 | | | | 1.55 | | | | 1.18 | | | | 4.21 | | | | 3.93 | |

| | | | | | | | | | | | | | | | | | | | | |

| Cash dividends | | $ | 0.4000 | | | | 0.4000 | | | | 0.4000 | | | | 0.4000 | | | | 0.4000 | |

| | | | | | | | | | | | | | | | | | | | | |

| Weighted-average Shares | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| Basic | | | 48.4 | | | | 47.8 | | | | 48.2 | | | | 47.2 | | | | 46.3 | |

| Diluted | | | 48.6 | | | | 48.1 | | | | 48.4 | | | | 47.5 | | | | 46.7 | |

| (a) | (Loss) income from discontinued operations reflects the operations and gains and losses, if any, on disposal of our cash-in-transit operations in Germany, Poland and Belgium, event security operations in France, guarding operations in Morocco, and our former home security business. Expenses related to retained retirement obligations are recorded as a component of continuing operations after the respective disposal dates. Adjustments to contingent liabilities are recorded within discontinued operations. |

| Non-GAAP Basis* | |

| (In millions, except per share amounts) | | 2012 | | | 2011 | | | 2010 | | | 2009 | | | 2008 | |

| | | | | | | | | | | | | | | | |

| Revenues | | $ | 3,832.9 | | | | 3,755.5 | | | | 2,966.3 | | | | 2,731.1 | | | | 2,818.1 | |

| | | | | | | | | | | | | | | | | | | | | |

| Segment operating profit | | $ | 267.9 | | | | 267.2 | | | | 243.5 | | | | 192.7 | | | | 226.5 | |

| Non-segment income (expense) | | | (42.3 | ) | | | (40.6 | ) | | | (36.2 | ) | | | (34.7 | ) | | | (61.6 | ) |

| Operating profit | | $ | 225.6 | | | | 226.6 | | | | 207.3 | | | | 158.0 | | | | 164.9 | |

| | | | | | | | | | | | | | | | | | | | | |

| Amounts attributable to Brink’s: | | | | | | | | | | | | | | | | | | | | |

| Income from continuing operations | | | 112.2 | | | | 111.6 | | | | 115.7 | | | | 86.9 | | | | 101.6 | |

| Diluted EPS – Continuing operations | | $ | 2.31 | | | | 2.32 | | | | 2.39 | | | | 1.83 | | | | 2.18 | |

*Reconciliations to GAAP results are found beginning on page 42

ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

THE BRINK’S COMPANY

MANAGEMENT’S DISCUSSION AND ANALYSIS OF

FINANCIAL CONDITION AND RESULTS OF OPERATIONS

FOR THE YEAR ENDED DECEMBER 31, 2012

| | TABLE OF CONTENTS | |

| | | |

| | | Page |

| OPERATIONS | 22 |

| | | |

| RESULTS OF OPERATIONS | |

| | Consolidated Review | 26 |

| | Segment Operating Results | 29 |

| | Non-segment Income and Expense | 35 |

| | Other Operating Income and Expense | 36 |

| | Nonoperating Income and Expense | 37 |

| | Income Taxes | 38 |

| | Noncontrolling Interests | 39 |

| | Loss from Discontinued Operations | 40 |

| | Outlook | 41 |

| | Non-GAAP Results – Reconciled to Amounts Reported under GAAP | 42 |

| | Foreign Operations | 46 |

| | | |

| LIQUIDITY AND CAPITAL RESOURCES | |

| | Overview | 47 |

| | Operating Activities | 47 |

| | Investing Activities | 49 |

| | Financing Activities | 50 |

| | Capitalization | 50 |

| | Off Balance Sheet Arrangements | 53 |

| | Contractual Obligations | 54 |

| | Contingent Matters | 58 |

| | | |

| APPLICATION OF CRITICAL ACCOUNTING POLICIES | |

| | Deferred Tax Asset Valuation Allowance | 59 |

| | Goodwill, Other Intangible Assets and Property and Equipment Valuations | 60 |

| | Retirement and Postemployment Benefit Obligations | 61 |

| | Foreign Currency Translation | 65 |

| | | |

| | |