Use these links to rapidly review the document

TABLE OF CONTENTS

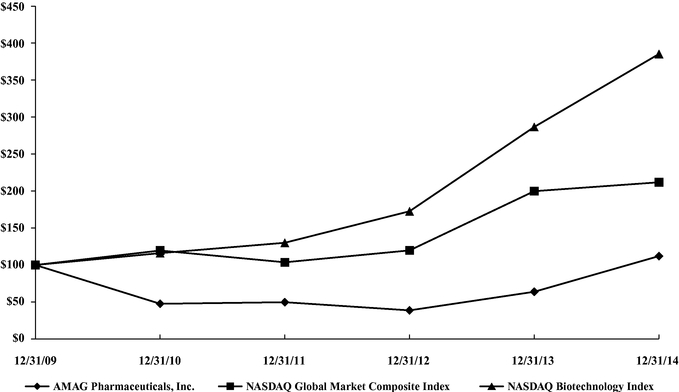

ITEM 8. FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| | |

| (Mark One) | | |

ý |

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Fiscal Year Ended December 31, 2014 |

or |

o |

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

|

Commission file number 001-10865

AMAG Pharmaceuticals, Inc.

(Exact Name of Registrant as Specified in Its Charter)

| | |

Delaware

(State or Other Jurisdiction of

Incorporation or Organization) | | 04-2742593

(I.R.S. Employer

Identification No.) |

1100 Winter Street

Waltham, Massachusetts

(Address of Principal Executive Offices) |

|

02451

(Zip Code) |

(617) 498-3300

(Registrant's Telephone Number, Including Area Code)

Securities registered pursuant to Section 12(b) of the Act:

| | |

Title of each class | | Name of each exchange on which registered |

|---|

| Common Stock, par value $0.01 per share | | NASDAQ Global Select Market |

| Preferred Share Purchase Rights | | |

Securities registered pursuant to Section 12(g) of the Act:None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ý No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ý

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definition of "accelerated filer," "large accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check one):

| | | | | | |

| Large accelerated filer o | | Accelerated filer ý | | Non-accelerated filer o

(Do not check if a

smaller reporting company) | | Smaller Reporting Company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No ý

The aggregate market value of the registrant's voting stock held by non-affiliates as of June 30, 2014 was approximately $453,000,000 based on the closing price of $20.72 of the Common Stock of the registrant as reported on the NASDAQ Global Select Market on such date. As of February 4, 2015, there were 25,615,978 shares of the registrant's Common Stock, par value $0.01 per share, outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Definitive Proxy Statement that the registrant intends to file in connection with the solicitation of proxies for the Annual Meeting of Stockholders within 120 days of the end of the fiscal year ended December 31, 2014 are incorporated by reference into Part III of this Annual Report on Form 10-K.

Table of Contents

AMAG PHARMACEUTICALS, INC.

FORM 10-K

FOR THE YEAR ENDED DECEMBER 31, 2014

TABLE OF CONTENTS

| | | | |

| | PART I | | |

Item 1. | | Business | | 2 |

Item 1A. | | Risk Factors | | 39 |

Item 1B. | | Unresolved Staff Comments | | 72 |

Item 2. | | Properties | | 72 |

Item 3. | | Legal Proceedings | | 73 |

Item 4. | | Mine Safety Disclosures | | 75 |

| | PART II | | |

Item 5. | | Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | | 76 |

Item 6. | | Selected Financial Data | | 79 |

Item 7. | | Management's Discussion and Analysis of Financial Condition and Results of Operations | | 81 |

Item 7A. | | Quantitative and Qualitative Disclosures About Market Risk | | 115 |

Item 8. | | Financial Statements and Supplementary Data | | 117 |

Item 9. | | Changes in and Disagreements With Accountants on Accounting and Financial Disclosure | | 179 |

Item 9A. | | Controls and Procedures | | 179 |

Item 9B. | | Other Information | | 179 |

| | PART III | | |

Item 10. | | Directors, Executive Officers and Corporate Governance | | 180 |

Item 11. | | Executive Compensation | | 180 |

Item 12. | | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | | 180 |

Item 13. | | Certain Relationships and Related Transactions, and Director Independence | | 180 |

Item 14. | | Principal Accountant Fees and Services | | 180 |

| | PART IV | | |

Item 15. | | Exhibits and Financial Statement Schedules | | 181 |

Table of Contents

PART I

Except for the historical information contained herein, the matters discussed in this Annual Report on Form 10-K may be deemed to be forward-looking statements that involve risks and uncertainties. We make such forward-looking statements pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995 and other federal securities laws. In this Annual Report on Form 10-K terminology such as "may," "will," "could," "should," "would," "expect," "anticipate," "continue," "believe," "plan," "estimate," "intend" or other similar words and expressions (as well as other words or expressions referencing future events, conditions or circumstances) are intended to identify forward-looking statements.

Unless the context suggests otherwise, references to "Feraheme" refer to both Feraheme (the trade name for ferumoxytol in the U.S. and Canada) and Rienso (the trade name for ferumoxytol in the EU and Switzerland).

Examples of forward-looking statements contained in this report include, without limitation, statements regarding the following: plans to pursue opportunities to make new advancements in patients' health and to enhance treatment accessibility; plans to diversify and grow our product portfolio; expectations and plans as to regulatory and commercial developments and activities, including with regard to label changes for Feraheme and our plan to work with the FDA to finalize the Feraheme label, the pursuit, if any, of a broader indication for Feraheme, commercialization efforts, if any, for Feraheme outside of the U.S., requirements and initiatives for clinical trials and studies, post-approval commitments for our products and the lifecycle management program for Makena; expectations as to what impact recent regulatory developments will have on our business and competition, including recent changes to our product information and label, and other risk minimization measures in the EU; the market opportunities for each of our products; the amount of resources that we intend to dedicate to the commercialization of Feraheme; expected transitioning activities with Takeda Pharmaceutical Company Limited ("Takeda") and the impact of Takeda's withdrawal of the application for Type II Variation to vary the marketing authorization for Rienso in the EU or our mutual decision with Takeda to initiate withdrawal of Rienso's current marketing authorizations in the EU and Switzerland; our expectations regarding the results of discussions with Health Canada, including our belief that approval of the broader indication for Feraheme in such territory is unlikely without additional clinical data and the possibility that Health Canada will impose additional restrictions on the current Feraheme CKD indication; beliefs about compounding pharmacies and the impact of recent legislation focused on compounding pharmacies; beliefs regarding possible entry of generic competitors, including timing, for both Makena and Feraheme; plans regarding our sales and marketing initiatives, including our contracting strategy and efforts to increase patient compliance and access; the impact of government regulations on our business and the pricing and reimbursement for our products, including the Branded Drug Fee under the Healthcare Reform Act and the Medicare reimbursement rate and estimates for Medicaid rebates; our expectations regarding the timing for enrollment in and commencement of our clinical trials and studies; our expectation of costs to be incurred in connection with and revenue sources to fund our future operations; our expectation for the patient populations for Makena and Feraheme; our expectations regarding the contribution of Makena and Feraheme sales to the funding of our on-going operations; the magnitude of costs and timing of integrating Lumara Health into our current business; expectations regarding the manufacture of all drug substance and drug products at our third-party manufacturers; plans to increase headcount; our expectations regarding customer returns and other revenue-related reserves and accruals; estimates regarding our net operating loss carryforwards and other tax attributes; initiatives to improve the reputation of Makena and educate industry participants on the benefits of Makena; the impact of accounting pronouncements; the effect of product price increases; expected increases in research and development expenses; expectations regarding our financial results, including revenues, cost of product sales, selling, general and administrative expenses, restructuring costs and net income (expense); the impact on revenues from the termination of our license arrangement with Takeda; our investing activities; expectations regarding our cash, cash equivalents and investments balances and capital needs; the impact and outcomes of our legal proceedings; our beliefs regarding the validity of our

1

Table of Contents

ferumoxytol patent portfolio; estimates and beliefs related to our debt, including our Convertible Notes and the Term Loan Facility; expected customer mix and utilization rates for our products; the impact of volume rebates and other incentives; provider purchase patterns and use of competitive products; the valuation of certain intangible assets, goodwill, contingent consideration, debt and other assets and liabilities, including our methodology and assumptions regarding fair value measurements; our gross to net sales adjustments; our expectations regarding competitive pressures and the impact on growth on our product sales; our plans regarding manufacturing; the timing of our planned research and development projects; the manner in which we intend or are required to settle the conversion of our Convertible Notes; plans to submit the NOL Amendment to our Rights Plan to our shareholders for approval; and our expectations for our cash, revenue, cash equivalents and investments balances and information with respect to any other plans and strategies for our business. Our actual results and the timing of certain events may differ materially from the results discussed, projected, anticipated or indicated in any forward-looking statements.

Any forward-looking statement should be considered in light of the factors discussed in Part I, Item 1A below under "Risk Factors" and elsewhere in this Annual Report on Form 10-K. We caution readers not to place undue reliance on any such forward-looking statements, which speak only as of the date they are made. We disclaim any obligation, except as specifically required by law and the rules of the U.S. Securities and Exchange Commission, to publicly update or revise any such statements to reflect any change in company expectations or in events, conditions or circumstances on which any such statements may be based, or that may affect the likelihood that actual results will differ from those set forth in the forward-looking statements.

ITEM 1. BUSINESS:

Overview

AMAG Pharmaceuticals, Inc., a Delaware corporation, was founded in 1981. We are a specialty pharmaceutical company with a focus on maternal health, anemia and cancer supportive care. We currently market Makena® (hydroxyprogesterone caproate injection), Feraheme® (ferumoxytol) Injection for Intravenous ("IV") use and MuGard® Mucoadhesive Oral Wound Rinse. The primary goal of our company is to bring to market therapies that provide clear benefits and improve patients' lives.

Currently, our two primary sources of revenue are from the sale ofMakena andFeraheme. On November 12, 2014, we acquired Lumara Health Inc. ("Lumara Health"), a privately held pharmaceutical company specializing in women's health, for approximately $600.0 million in upfront cash consideration (subject to finalization of certain adjustments related to Lumara Health's financial position at the time of closing, including adjustments related to net working capital, net debt and transaction expenses as set forth in the definitive agreement with Lumara Health (the "Lumara Agreement")) and approximately 3.2 million shares of our common stock having a fair value of approximately $112.0 million at the time of closing. The Lumara Agreement includes future contingent payments of up to $350.0 million in cash (or upon mutual agreement between us and the former Lumara Health security holders, future contingent payments may also be made in common stock or some combination thereof) payable by us to the former Lumara Health security holders based upon the achievement of certain sales milestones through calendar year 2019. In connection with the acquisition of Lumara Health, we acquiredMakena, a progestin indicated to reduce the risk of preterm birth in women with a singleton pregnancy who have a history of singleton spontaneous preterm birth. We sellMakena to specialty pharmacies and distributors, who, in turn sellMakena to healthcare providers, hospitals, government agencies and integrated delivery systems. Additional details regarding the Lumara Agreement can be found in Note C, "Business Combinations," to our consolidated financial statements included in this Annual Report on Form 10-K.

2

Table of Contents

Feraheme was approved for marketing in the U.S. in June 2009 by the U.S. Food and Drug Administration (the "FDA") for use as an IV iron replacement therapy for the treatment of iron deficiency anemia ("IDA") in adult patients with chronic kidney disease ("CKD"). We began sellingFeraheme in the U.S. in July 2009 through our commercial organization, including a specialty sales force. We sellFeraheme to authorized wholesalers and specialty distributors, who in turn, sellFeraheme to healthcare providers who administerFeraheme primarily within hospitals, hematology and oncology centers, and nephrology clinics.

In addition to continuing to pursue opportunities to make new advancements in patients' health and to enhance treatment accessibility, we intend to continue to expand and diversify our portfolio through the in-license or purchase of additional pharmaceutical products or companies. We are seeking complementary products that will leverage our corporate infrastructure, sales force call points and commercial expertise, with a particular focus on maternal health specialists, hematology and oncology centers, nephrology clinics and hospitals. We are evaluating and plan to pursue commercial products as well as late-stage development assets. In addition, we are contemplating transactions that allow us to realize cost synergies to increase cash flows, as well as transactions that potentially optimize after-tax cash flows.

In June 2014, we proposed changes to the FDA related to our current U.S. label ofFeraheme based on a review of global post-marketing data to strengthen the warnings and precautions section of the label and mitigate the risk of serious hypersensitivity reactions, including anaphylaxis, in order to enhance patient safety. After considering our June 2014 submission and other information, in January 2015, the FDA notified us that it believes new safety information should be included in the labeling forFeraheme, including, among other things, a boxed warning to highlight the risks of serious hypersensitivity/anaphylaxis reactions and revisions thatFeraheme should only be administered through an IV infusion (i.e., not by IV injection) and should be contraindicated for patients with any known history of drug allergy. The FDA's recommended label changes go beyond what we proposed in June 2014. We plan to work with the FDA to finalize an updated U.S.Feraheme label.

In December 2012, we submitted a supplemental new drug application ("sNDA") to the FDA seeking approval forFeraheme for the treatment of IDA in adult patients who had failed or could not use oral iron. In January 2014, we received a complete response letter from the FDA for the sNDA informing us that our sNDA could not be approved in its present form and stating that we have not provided sufficient information to permit labeling ofFeraheme for safe and effective use for the proposed broader indication. The FDA indicated that its decision was based on the cumulative ferumoxytol data, including the global Phase III IDA program and global post-marketing safety reports for the currently indicated CKD patient population. The FDA suggested, among other things, that we submit additional clinical trial data in the proposed broad IDA patient population with a primary composite safety endpoint of serious hypersensitivity/anaphylaxis, cardiovascular events and death, events that are included in the labels ofFeraheme and other IV irons and that have been reported in the post-marketing environment forFeraheme. Additionally, the FDA proposed potentially evaluating alternative dosing and/or administration ofFeraheme as well as potential changes to labeling that would be intended to reduce the risk of serious hypersensitivity reactions associated withFeraheme. In June 2014, we met with the FDA to discuss our proposed approach to resolving the points that were raised in the complete response letter. Based on the FDA's feedback, we submitted a revised proposal that includes the design of a potential clinical trial, a safety endpoint for such trial and alternative methods of administration ofFeraheme. We expect to receive feedback from the FDA during 2015 and expect thereafter to be able to assess and determine the path forward, if any, forFeraheme in the broad IDA patient population in the U.S., including the related timing and cost of any clinical trials.

3

Table of Contents

Further, in October 2014, we filed with the FDA a prior approval supplement to the originalMakena New Drug Application ("NDA") seeking approval of a 1 mL preservative-free vial ofMakena and we are seeking to expandMakena's formulations and drug delivery technologies as part of the product's lifecycle management program.

Outside of the U.S., ferumoxytol has been granted marketing approval in the European Union ("EU"), Canada and Switzerland for use as an IV iron replacement therapy for the treatment of IDA in adult patients with CKD. In March 2010, we entered into a License, Development and Commercialization Agreement (the "Takeda Agreement"), which was amended in June 2012 (the "Amended Takeda Agreement") with Takeda. On December 29, 2014, we entered into an agreement with Takeda to terminate the Amended Takeda Agreement and we will regain all worldwide development and commercialization rights forFeraheme following the transfer of marketing authorizations from Takeda to us (the "Takeda Termination Agreement"). Under the Amended Takeda Agreement, Takeda had an exclusive license to market and sell ferumoxytol in the EU, Canada, and Switzerland, as well as certain other geographic territories. The EU marketing authorization forRienso is valid in the 28 EU Member States as well as in Iceland, Liechtenstein and Norway. The trade name for ferumoxytol in Canada isFeraheme and outside of the U.S. and Canada the trade name isRienso. Additional details regarding the Takeda Termination Agreement can be found in Note R, "Collaborative Agreements," to our consolidated financial statements included in this Annual Report on Form 10-K.

Sales ofFeraheme/Rienso outside of the U.S. do not and are not expected to materially contribute to our revenues. As such, and in light of the Takeda Termination Agreement, we have been assessing various commercialization strategies forRienso in the EU and Switzerland andFeraheme in Canada. A number of considerations influence our analysis of our commercialization opportunities outside of the U.S., including (i) regulatory developments and the potential cost of post-approval clinical trial commitments and post-marketing obligations required by regulatory authorities outside of the U.S., (ii) the product's commercial viability (sales potential relative to the cost of maintaining the product on the market) in light of the current CKD label, the possible impact of future label changes, including any impact in the U.S., and the competitive landscape, and (iii) possible approaches in different geographies, which may include seeking a licensing or distribution partner or commercializing the product ourselves. Based on these considerations, we have come to a mutual decision with Takeda to initiate withdrawal of the marketing authorization forRienso in the EU and Switzerland. We are currently assessing the commercial opportunity forFeraheme in Canada.

In the future, we may decide to seek to obtain a new marketing authorization for ferumoxytol in the EU, particularly if we generate additional clinical data to support potential approval in the broader IDA indication. There can be no assurance that we will be able to develop an approach that would be economically viable for us or a commercialization partner.

In February 2014, we issued $200.0 million of 2.5% convertible senior notes due February 15, 2019 (the "Convertible Notes"). Interest is payable semi-annually in arrears on February 15 and August 15 of each year, beginning on August 15, 2014. The initial conversion rate is 36.9079 shares of our common stock per $1,000 principal amount of the Convertible Notes, which corresponds to an initial conversion price of approximately $27.09 per share of our common stock and represents a conversion premium of approximately 35% based on the last reported sale price of our common stock of $20.07 on February 11, 2014, the date the Convertible Notes offering was priced. In addition, in connection with the pricing of the Convertible Notes and in order to reduce the potential dilution to our common stock and/or offset cash payments due upon conversion of the Convertible Notes, we also entered into convertible bond hedge and warrant transactions in February 2014. The initial exercise price of the warrants is $34.12 per share, subject to adjustment upon certain events, which is 70% above the last reported sale price of our common stock of $20.07 on February 11, 2014.

4

Table of Contents

On November 12, 2014, in connection with the acquisition of Lumara Health, we entered into the Term Loan Facility, which provides for term loans in the aggregate principal amount of $340.0 million (the "Term Loan Facility"). We used $327.5 million of the Term Loan Facility proceeds to partially finance the $600.0 million cash portion of the Lumara Health acquisition. The Term Loan Facility bears interest, at our option, at either the Eurodollar rate plus a margin of 6.25% or the prime rate plus a margin of 5.25%. The Eurodollar rate is subject to a 1.00% floor and the prime rate is subject to a 2.00% floor. As of December 31, 2014, the stated interest rate was 7.25%. We must repay the Term Loan Facility in installments of (a) $8.5 million per quarter due on the last day of each quarter beginning with the quarter ending March 31, 2015 through the quarter ending December 31, 2015, and (b) $12.8 million per quarter due on the last day of each quarter beginning with the quarter ending March 31, 2016 through the quarter ending September 30, 2020, with the balance due in a final installment on November 12, 2020. The Term Loan Facility matures on November 12, 2020, except that the Term Loan Facility will mature on September 30, 2018 if:

- (a)

- more than $25.0 million in aggregate principal amount of our Convertible Notes remain outstanding and not converted to common stock or refinanced and replaced with debt that matures following, and has no amortization prior to, the date that is six and one half years following the closing date; and

- (b)

- the aggregate principal amount of the Term Loan Facility (including all undrawn incremental commitments) is greater than $50.0 million on and as of such date.

See Note S, "Debt," to our consolidated financial statements included in this Annual Report on Form 10-K for additional information regarding the Convertible Notes, the bond hedge and warrant transactions, as well as the Term Loan Facility.

Our common stock trades on the NASDAQ Global Select Market ("NASDAQ") under the trading symbol "AMAG."

5

Table of Contents

Products

The following table summarizes the current uses and, subject to regulatory approval, potential uses of our products, the current U.S. and foreign regulatory status, and the primary markets for our products.

| | | | | | |

Product | | Uses/Potential Uses | | U.S. Regulatory Status | | Foreign

Regulatory Status |

|---|

| Makena® (hydroxyprogesterone caproate injection) (5 mL multi-use vial) | | A progestin indicated to reduce the risk of preterm birth in women with a singleton pregnancy who have a history of singleton spontaneous preterm birth. | | Approved and marketed. | | Not approved outside of the U.S. |

Makena® (hydroxyprogesterone caproate injection) (1 mL vial, preservative-free, single dose) |

|

A progestin indicated to reduce the risk of preterm birth in women with a singleton pregnancy who have a history of singleton spontaneous preterm birth. |

|

Prior approval supplement submitted to the FDA in October 2014.

Decision from the FDA expected in the second quarter 2015. |

|

Not approved outside of the U.S. |

Feraheme® (ferumoxytol) |

|

IV iron replacement therapeutic agent for the treatment of IDA in adult patients with CKD. |

|

Approved and marketed. |

|

Approved and marketed asFeraheme in Canada.

Approved and marketed asRienso in the EU.*

Approved in Switzerland and not currently marketed.* |

Feraheme® (ferumoxytol) |

|

IV iron replacement therapeutic agent for the treatment of patients with a history of unsatisfactory oral iron therapy or in whom oral iron cannot be used. |

|

sNDA filed December 2012. Complete Response Letter received January 2014.

Submitted proposal to FDA in 2014 that included the design of a potential clinical trial and we are awaiting feedback. |

|

Application for Type II Variation filed with the European Medicines Agency ("EMA") in 2013 and withdrawn in January 2015.

Decision from Health Canada on sNDS expected in the second half of 2015. |

MuGard® Mucoadhesive Oral Wound Rinse |

|

Management of oral mucocitis/stomatiits and all types of oral wounds. |

|

Cleared and marketed. |

|

We license only the U.S. commercial rights from PlasmaTech. |

- *

- As discussed above, we have come to a mutual decision with Takeda to initiate withdrawal of the marketing authorization forRienso in the EU and Switzerland. Our licensing arrangement with Takeda, and its termination, is discussed below under the heading "Collaboration, License and Other Material Agreements—Takeda."

For a discussion of the substantive regulatory requirements applicable to the development and regulatory approval process in the U.S. and other countries, see "Government Regulation" below.

Makena

On November 12, 2014, we acquired Lumara Health, a privately held pharmaceutical company specializing in women's health, including its marketed drug productMakena, the only FDA-approved drug indicated to reduce the risk of preterm birth in women with a singleton pregnancy who have a history of singleton spontaneous preterm birth.Makena is administrated intramuscularly by a healthcare professional at a dose of 250 mg (1 mL) weekly with treatment beginning between 16 weeks and

6

Table of Contents

20 weeks and six days and continuing until 37 weeks (through 36 weeks and six days) of pregnancy or delivery, whichever happens first.

Makena was approved by the FDA in February 2011 and was granted orphan drug exclusivity through February 3, 2018. Under the Orphan Drug Act, the FDA may designate a product as an orphan drug if it is a drug intended to treat a rare disease or condition, defined, in part, as a patient population of fewer than 200,000 in the U.S. In the U.S., the company that first obtains FDA approval for a designated orphan drug for the specified rare disease or condition receives orphan drug marketing exclusivity for that drug for a period of seven years. This orphan drug exclusivity prevents the FDA from approving another application for the "same drug" for the same orphan indication during the exclusivity period, except in very limited circumstances. A designated orphan drug may not receive orphan drug exclusivity for an approved indication if that indication is for the treatment of a condition broader than that for which it received orphan designation. In addition, orphan drug exclusivity marketing rights in the U.S. may be lost if the FDA later determines that the request for designation was materially defective or if the manufacturer is unable to assure sufficient quantity of the drug to meet the needs of patients with the rare disease or condition.

Preterm birth is defined as a birth prior to 37 weeks of pregnancy. According to the Centers for Disease Control and Prevention ("CDC"), in 2012, preterm births affected more than 450,000 babies, or one of every nine infants born in the U.S. Although, the causes of preterm births are not fully understood, certain women are at a greater risk for preterm birth, including those who have had a previous preterm birth, are pregnant with multiples or have certain uterine or cervical problems.Makena is indicated only for women with a history of spontaneous singleton preterm birth who are pregnant with a singleton, which accounts for approximately 140,000 pregnancies annually in the U.S. High blood pressure, pregnancy complications (such as placental problems) and certain other health or lifestyle factors may also be contributing factors. The last few weeks of a woman's pregnancy are important to the full development of many major organ systems, including the brain, lungs, and liver. Preterm births can increase the risk of infant death and can also result in serious long-term health issues for the child, including respiratory problems, gastrointestinal conditions, cerebral palsy, developmental delays, and vision and hearing impairments. According to a 2007 report by the Institute of Medicine (US) Committee on Understanding Premature Birth and Assuring Healthy Outcome, the annual societal economic cost associated with preterm birth is at least $26.2 billion and includes medical and healthcare costs for the baby, labor and delivery costs for the mother, early intervention and special education services, and costs associated with lost work and pay.

Makena was approved under the provisions of the FDA's "Subpart H" Accelerated Approval regulations. The Subpart H regulations allow certain drugs, for serious or life-threatening conditions, to be approved on the basis of surrogate endpoints or clinical endpoints other than survival or irreversible morbidity. As a condition of approval under Subpart H, the FDA required thatMakena's sponsor perform certain adequate and well-controlled post-marketing clinical studies to verify and describe clinical benefit ofMakena as well as fulfill certain other post-approval commitments. We are currently conducting the following clinical studies; (a) an ongoing efficacy and safety clinical study ofMakena; (b) an ongoing follow-up study of the babies born to mothers from the efficacy and safety clinical study; and (c) a completed pharmacokinetic study of women takingMakena. Given the patient population (i.e., women pregnant who are at an increased high risk for recurrent preterm delivery) and the informed risk of receiving a placebo instead of the active approved drug in the U.S., the pool of prospective subjects for such clinical trials in the U.S. is small and we are therefore seeking enrollment on a global scale.

7

Table of Contents

We are pursuing a lifecycle management program forMakena, some elements of which may provide new intellectual property or data exclusivity beyond February 2018 by exploring new routes of administration and the use of new delivery technologies, as well as reformulation technologies. As part of this program, in October 2014, a prior approval supplement for a preservative-free, single-dose (1 mL) vial forMakena was filed with and is under review by the FDA. We expect a decision in the second quarter of 2015.Makena is currently available in a 5-dose (5 mL) vial.

Feraheme for the treatment of IDA in patients with CKD

In June 2009,Feraheme was approved for marketing in the U.S. by the FDA for use as an IV iron replacement therapy for the treatment of IDA in adult patients with all stages of CKD, Stage 1 through Stage 5 (end-stage renal disease). In July 2009, we began to market and sellFeraheme in the U.S. WhileFeraheme is approved for IDA in all stages of CKD, beginning in 2010, due to changes in the way the federal government reimburses providers for the care of dialysis patients, the utilization ofFeraheme shifted to non-dialysis patients. The non-dialysis CKD IDA market is made up of a range of healthcare providers who administer IV iron, including nephrologists, hematologists, oncologists, hospitals and other end-users who treat patients with CKD. We anticipate the majority of allFeraheme utilization in the U.S. will continue to be in the non-dialysis CKD patient population if and untilFeraheme receives a broader label to include non-CKD patients.

In June 2014, we proposed changes to the FDA related to our current U.S. label ofFeraheme based on a review of global post-marketing data to strengthen the warnings and precautions section of the label and mitigate the risk of serious hypersensitivity reactions, including anaphylaxis, in order to enhance patient safety. After considering our June 2014 submission and other information, on January 7, 2015, the FDA notified us that it believes new safety information should be included in the labeling forFeraheme, including, among other things, a boxed warning to highlight the risks of serious hypersensitivity/anaphylaxis reactions and revisions thatFeraheme should only be administered through an IV infusion (i.e., not by IV injection) and should be contraindicated for patients with any known history of drug allergy. The FDA's recommended label changes go beyond what we proposed in June 2014. We plan to work with the FDA to finalize an updated U.S.Feraheme label.

In Europe, Takeda has been commercializing ferumoxytol since its approval in June 2012 under the trade nameRienso, currently in nine EU countries.Rienso is subject to periodic review by the EMA's Pharmacovigilance Risk Assessment Committee ("PRAC") and in February 2014 Takeda, as the marketing authorization holder (the "MAH") forRienso, submitted to PRAC a Periodic Safety Update Report ("PSUR") concerningRienso as part of such review. A PSUR is a pharmacovigilance document submitted by the MAH at defined intervals and is intended to provide a safety update permitting an evaluation of the risk-benefit balance of a medicinal product while it is commercialized.

As part of its assessment of the PSUR, PRAC reviewed various data, including the rate of hypersensitivity reactions with fatal outcomes withRienso. Following that assessment, and in agreement with the EMA, Takeda issued a Direct Healthcare Professional Communication ("DHPC") letter in May 2014 to remind physicians in the EU of the existing risk minimization measures for all IV iron products to manage and minimize the risk of serious hypersensitivity reactions that were included in the special warnings and precautions sections of theRienso label.

In July 2014 and again in January 2015, also in connection with the PSUR evaluation, PRAC confirmed that the benefit/risk balance ofRienso in the currently approved CKD indication remains favorable. These confirmations were subject to a number of proposed changes to the product information and label and other risk minimization measures, including, among others, thatRienso

8

Table of Contents

should be administered to patients by infusion over at least 15 minutes (replacing injection) and that it should be contraindicated in patients with any known history of drug allergy (the "July Recommendations"), that the label should caution that elderly patients or patients with multiple co-morbidities who experience a serious hypersensitivity reaction due toRienso may have more severe outcomes (the "January Recommendations"), and related variations to the Summary of Product Characteristics ("SmPC"). The PRAC's recommendations were subsequently endorsed by the EMA's Committee for Medicinal Products for Human Use ("CHMP"). Takeda updated the product's label to reflect the July Recommendations and in August 2014 issued a DHPC letter informing physicians of these changes.

In December 2011, ferumoxytol was granted marketing approval in Canada, under the trade nameFeraheme, for use as an IV iron replacement therapy for the treatment of IDA in adult patients with CKD. In August 2012, ferumoxytol was granted marketing approval in Switzerland under the trade nameRienso for use as an IV iron replacement therapy for the treatment of IDA in adult patients with CKD, but has subsequently been withdrawn from the market. As discussed above, we have come to a mutual decision with Takeda to initiate withdrawal of the marketing authorization forRienso in the EU and Switzerland. We are currently assessing the commercial opportunity forFeraheme in Canada.

Chronic kidney disease, anemia, and iron deficiency

CKD is the gradual and permanent loss of kidney function. It is a progressive illness that contributes to the development of many complications, including anemia, hypertension, fluid and electrolyte imbalances, acid/base abnormalities, bone disease and cardiovascular disease. According to the National Kidney Foundation, 26 million Americans are living with CKD and millions of others are at risk. Anemia, a common condition among CKD patients, is associated with cardiovascular complications, decreased quality of life, hospitalizations, and increased mortality. Anemia develops early during the course of CKD and worsens with advancing kidney disease. Patients with anemia can look pale, feel fatigued, experience shortness of breath, low energy, headaches, palpitations or chest pains, and have a loss of appetite, trouble sleeping and trouble concentrating. Anemia in CKD patients is most often considered to be caused by an insufficient production of erythropoietin, a hormone made by the kidneys which tells the body to produce red blood cells, and iron deficiency, due to inadequate iron intake, blood loss or because the body cannot use iron stores. Regardless of the cause of the iron deficiency, iron replacement therapy is essential to increase iron stores and raise hemoglobin levels. Iron is also essential for effective treatment with erythropoiesis stimulating agents ("ESAs"), which are commonly used in anemic patients to stimulate red blood cell production. Based on data contained in a 2009 publication in theJournal of the American Society of Nephrology, we estimate that there are approximately 1.6 million adults in the U.S. diagnosed with IDA and stages 3 through 5 CKD, who are patients in the mid to later stages of CKD but not yet on dialysis and could therefore benefit from receiving iron.

Currently there are two methods used to treat IDA in CKD patients: oral iron supplements and IV iron. The National Kidney Foundation's Kidney Disease Outcomes Quality Initiative guidelines recommend either oral or IV iron for peritoneal dialysis patients and non-dialysis patients with stages 1 through 5 CKD. Oral iron is currently the first-line iron replacement therapy of choice of most physicians in both the U.S. and abroad. However, oral iron supplements are poorly absorbed by many patients, which may adversely impact their effectiveness, and are associated with certain side effects, such as constipation, diarrhea, and cramping, that may adversely affect patient compliance in using such products. In addition, it can take an extended time for hemoglobin levels to improve following the initiation of oral iron treatment, and even then the targeted hemoglobin levels may not be reached. Conversely, iron given intravenously allows larger amounts of iron to be provided to patients while avoiding many of the side effects and treatment compliance issues associated with oral iron, and can result in faster rises in hemoglobin levels. The administration of IV iron has been shown to be effective

9

Table of Contents

in treating anemia either when used alone or in combination with an ESA. Current U.S. treatment guidelines indicate that treating first with iron alone may delay or reduce the need for ESA therapy. Iron supplementation is widely used in CKD patients to treat iron deficiency, prevent its development in ESA-treated patients, raise hemoglobin levels in the presence or absence of ESA treatment, and reduce ESA doses in patients receiving ESA treatment. We believe that a small fraction of non-dialysis CKD patients in the U.S. who are diagnosed with IDA are currently being treated with IV iron, and thus a significant opportunity remains to grow the market for IV iron in this patient population.

We have initiated a randomized, active-controlled pediatric study ofFeraheme for the treatment of IDA in pediatric CKD patients to meet our FDA post-approval Pediatric Research Equity Act requirement to support pediatric labeling ofFeraheme in the U.S. The study covers both dialysis-dependent and non-dialysis dependent CKD pediatric patients and will assess the safety and efficacy ofFeraheme treatment as compared to oral iron in approximately 288 pediatric patients.

Our pediatric investigation plan, which was a requirement for submission of the marketing authorization application for ferumoxytol, was approved by the EMA in December 2009 and amended in 2012 and 2014. It includes the pediatric study, as described above, and two additional pediatric studies requested by the EMA. These additional studies include a rollover extension study in pediatric CKD patients and a study in pediatric patients with IDA regardless of the underlying cause. The rollover study is open for enrollment. The pediatric IDA study will commence once the appropriate dose ofFeraheme is determined from the study data resulting from the pediatric study ofFeraheme, described above.

As part of our post-approval commitments to the EMA, we are conducting a global multi-center clinical trial to determine the safety and efficacy of repeat doses of ferumoxytol for the treatment of IDA in patients with hemodialysis-dependent CKD. As part of the commitment we made to the EMA as a condition of the approval of the marketing authorization for ferumoxytol in the EU, this study includes a treatment arm with iron sucrose using a magnetic resonance imaging sub-analysis to evaluate the potential for iron to accumulate in the body following treatment with IV iron, specifically in the heart and liver, and, where possible, other major organs following repeated IV iron administration over a two year period (the "hd-CKD Study"). Enrollment has been completed.

We have assumed any post-marketing obligations of Takeda as part of the Takeda Termination Agreement, including costs that otherwise would have been Takeda's obligation under the Amended Takeda Agreement for the ongoing pediatric studies and the ongoing multi-center clinical trial discussed above. In connection with our decision to withdraw the marketing authorization forRienso in the EU and Switzerland, we may modify or terminate clinical trials being conducted as part of our post-approval commitments to the EMA.

Feraheme for the treatment of IDA in a broad range of patients

IDA not associated with CKD is widely prevalent in many different patient populations. For many of these patients, treatment with oral iron is unsatisfactory. In the U.S., approximately 900,000 grams of IV iron were administered for the treatment of non-dialysis patients with IDA in 2014. We believe that approximately half, or 450,000 grams, of the IV iron administered in the U.S. was for the treatment of non-dialysis patients with CKD and the other half was for non-CKD patients with IDA due to other causes, including patients with gastrointestinal diseases or disorders, abnormal uterine bleeding, inflammatory diseases, and chemotherapy-induced anemia. It is estimated that more than 4.5 million patients in the U.S. have IDA (CKD and non-CKD). We estimate that approximately 5% to 10% of these patients are currently treated with IV iron.

10

Table of Contents

As discussed above, in December 2012, we submitted an sNDA to the FDA seeking approval forFeraheme for the treatment of IDA in adult patients who had failed or could not use oral iron. The sNDA included data from two controlled, multi-center Phase III clinical trials ("IDA-301 and IDA-302"), including more than 1,400 patients, which evaluated the safety and efficacy of ferumoxytol for the treatment of IDA in this broader patient population. Both studies met the primary efficacy endpoints related to improvements in hemoglobin. In these studies no new safety signals were observed withFeraheme treatment and the types of reported adverse events were consistent with those seen in previous studies and those contained in the approved U.S. package insert forFeraheme. In addition, patients from IDA-301 were eligible to enroll in an open-label extension study ("IDA-303") and receive treatment withFeraheme, as defined in the protocol.

In January 2014, we received a complete response letter from the FDA for the sNDA informing us that our sNDA could not be approved in its present form and stating that we have not provided sufficient information to permit labeling ofFeraheme for safe and effective use for the proposed broader indication. The FDA indicated that its decision was based on the cumulative ferumoxytol data, including the global Phase III IDA program and global post-marketing safety reports for the currently indicated CKD patient population. The FDA suggested, among other things, that we submit additional clinical trial data in the proposed broad IDA patient population with a primary composite safety endpoint of serious hypersensitivity/anaphylaxis, cardiovascular events and death, events that are included in the labels ofFeraheme and other IV irons and that have been reported in the post-marketing environment forFeraheme. Additionally, the FDA proposed potentially evaluating alternative dosing and/or administration ofFeraheme as well as potential changes to labeling that would be intended to reduce the risk of serious hypersensitivity reactions associated withFeraheme. In June 2014, we met with the FDA to discuss our proposed approach to resolving the points that were raised in the complete response letter. Based on the FDA's feedback, we submitted a revised proposal that includes the design of a potential clinical trial, a safety endpoint for such trial and alternative methods of administration ofFeraheme. We expect to receive feedback from the FDA during 2015 and expect thereafter to be able to assess and determine the path forward, if any, forFeraheme in the broad IDA patient population in the U.S., including the related timing and cost of any clinical trials.

In June 2013, Takeda filed an application for Type II Variation to vary the marketing authorization forRienso in the EU with the EMA to extend the therapeutic indication from adult patients with IDA associated with CKD to adult patients with iron deficiency from any underlying cause. During the course of CHMP's review of the Type II Variation, Takeda received inquiries and reports from regulators indicating that approval of the Type II Variation would be unlikely without additional confirmative clinical data. As a result, in January 2015, we and Takeda mutually agreed that Takeda withdraw the Type II Variation.

In addition, in October 2013, Takeda filed an sNDS with Health Canada seeking marketing approval forFeraheme for the treatment of IDA in a broad range of patients. In October 2014, Takeda received inquiries from Health Canada and in January 2015, we submitted a response to these inquiries. Based on these inquiries and interactions, we believe that approval in the broader indication is unlikely in Canada without additional clinical data. We believe that we will receive Health Canada's final decision on the sNDS in the second half of 2015, however we cannot guarantee that Health Canada will issue a final decision on the expected timeline. In addition, until we have further conversations with Health Canada, we cannot predict whether their concerns with regard to approval of the broader IDA indication, including with regard to the need for additional clinical data, will cause Health Canada to impose additional restrictions on the current CKD indication.

As discussed above, we are in the process of regaining all worldwide development and commercialization rights forFeraheme from Takeda and have come to a mutual decision with Takeda to initiate withdrawal of the marketing authorization forRienso in the EU and Switzerland. We are currently assessing the commercial opportunity forFeraheme in Canada.

11

Table of Contents

MuGard

In June 2013, we entered into the License Agreement with PlasmaTech Biopharmaceuticals, Inc. ("PlasmaTech") (formerly known as Access Pharmaceuticals, Inc.), under which we acquired the U.S. commercial rights toMuGard for the management of oral mucositis (the "MuGard License Agreement").MuGard was launched in the U.S. by PlasmaTech in 2010 after receiving 510(k) clearance from the FDA and is indicated for the management of oral mucositis/stomatitis (that may be caused by radiotherapy and/or chemotherapy) and all types of oral wounds (mouth sores and injuries), including aphthous ulcers/canker sores and traumatic ulcers, such as those caused by oral surgery or ill-fitting dentures or braces. Mucositis is the painful inflammation and ulceration of the mucous membranes of the mouth and gastrointestinal tract that can be caused by high-dose chemotherapy and/or radiotherapy. Oral mucositis is a common and often debilitating complication of cancer treatment that may impair oral nutritional intake or result in delays, unplanned breaks or decreases in dose for chemotherapy and/or radiation treatments, leading to sub-optimal cancer treatment results. In the U.S., there are approximately 400,000 people per year who experience oral mucositis and approximately 80% of patients with mucositis experience severe oral pain. The incidence rate and severity of symptoms depends on the type of anti-cancer treatment and patient-related risk factors. For example, based on data reported in a 2001 article inCA: A Cancer Journal for Clinicians, the incidence of oral mucositis for patients undergoing radiation for the treatment of head and neck cancer could approximate 80%. The incidence of oral mucositis for bone marrow transplant patients undergoing high dose chemotherapy and/or radiation pre-conditioning and patients undergoing conventional chemotherapy is approximately 70% and 40%, respectively.

There are few effective treatments for oral mucositis and the products in this market remain mostly undifferentiated. There are a number of approaches used to treat or manage oral mucositis, including the use of ice chips during chemotherapy treatments, various medicinal mouthwashes, topical anesthetics and analgesics, and oral gel treatments. We sellMuGard through a distribution network of specialty pharmacies and wholesalers, who in turn supply it to hospitals or hematology/oncology clinics. Currently,MuGard is used by a small percentage of the oral mucositis patients in the U.S., which represents a significant opportunity for us to address an unmet medical need and grow the sales ofMuGard in the oral mucositis market.

Our Core Proprietary Technology

Our core proprietary technology for ferumoxytol is based on coated superparamagnetic iron oxide particles and their characteristic properties. Our core competencies for ferumoxytol include the ability to design such particles for particular applications and to manufacture the particles in controlled sizes. Our technology and expertise enable us to synthesize, sterilize and stabilize these iron oxide particles in a manner necessary for use in pharmaceutical products such as IV iron replacement therapeutics.

Our iron oxide particles are composed of bioavailable iron that is easily utilized by the body and incorporated into the body's iron stores. As a result, our core technology for ferumoxytol is well-suited for use as an IV iron replacement therapy product.

Our rights to the technology are derived from and/or protected by license agreements, patents, patent applications and trade secret protections. See "Patents and Trade Secrets" below. There are no patents coveringMakena. Our rights toMuGard are governed by the MuGard License Agreement. See Note C, "Business Combinations," to our consolidated financial statements included in this Annual Report on Form 10-K.

12

Table of Contents

Collaboration, License and Other Material Agreements

Takeda

In March 2010, we entered into the Takeda Agreement, as amended in June 2012, under which we granted exclusive rights to Takeda to develop and commercializeFeraheme as a therapeutic agent in certain agreed-upon territories. In February 2014, we entered into the Supply Agreement with Takeda, which provides the terms under which we sellFeraheme to Takeda in order for Takeda to meet its requirements for commercial use ofFeraheme in its licensed territories. On December 29, 2014, we entered into the Takeda Termination Agreement, under which the Amended Takeda Agreement will be terminated and we will regain all worldwide development and commercialization rights forFeraheme following the transfer of the outstanding marketing authorizations. Pursuant to the Takeda Termination Agreement, we and Takeda have agreed to effectuate the termination of the Amended Takeda Agreement on a rolling basis, whereby the termination will be effective for a particular geographic territory (e.g., countries under the regulatory jurisdictions of Health Canada, the EMA and SwissMedic) upon the earlier of effectiveness of the transfer to us or a Withdrawal (as defined below) of the marketing authorization for such territory, with the final effective termination date to be on the third such effective date ("Termination Date").

In connection with each Termination Date and in accordance with the terms of the Takeda Termination Agreement, Takeda is obligated, with respect to the applicable terminated territory, to transfer and assign to us all applicable regulatory materials and approvals and certain product data, unlabeled inventory, third party contracts intellectual property rights and know-how to us, and to grant us an exclusive license for certain Takeda technology used and applied to commercializeFeraheme in the applicable territory. The Takeda Termination Agreement also details the regulatory activities each party is required to perform in connection with transferring the marketing authorization from Takeda to us in each of the territories and the allocation of the costs of such activities. We and Takeda have agreed to use commercially reasonable efforts to transfer all required activities to us on a territory-by-territory basis within 60 days after the applicable Termination Date (subject to a 30-day extension upon our request and Takeda's consent). In addition, Takeda is obligated pursuant to the Takeda Termination Agreement to provide transition assistance to us, at no cost to us, for up to 180 days after each Termination Date for the applicable termination territory. With Takeda's consent (which shall not be unreasonably withheld or delayed), we may extend the transition services period for a terminated territory for a period of time reasonably necessary to complete any services that cannot be reasonably transitioned to us during the initial 180-day period, which extension will not exceed an additional 180 days. If we request, and Takeda agrees to conduct, additional transition services after the end of the applicable transition services period, as may be extended, we will reimburse Takeda's fully burdened costs for such additional services plus 5%.

The Takeda Termination Agreement also provides that if the marketing authorization for the product is suspended in a particular territory and the parties are prevented from completing the transfer of such marketing authorization to us within 120 days after such suspension due to applicable laws or any regulatory requirements or restrictions, or if we do not fulfill our obligations to initiate marketing authorization transfer by the agreed-upon, territory-specific deadline, Takeda will have the right, in Takeda's sole discretion, to withdraw such marketing authorization (a "Withdrawal").

In consideration for the early termination of the Amended Takeda Agreement and the activities to be performed by us earlier than contemplated under the Amended Takeda Agreement, and in lieu of any future cost-sharing and milestone payments contemplated by the Amended Takeda Agreement, Takeda agreed to make certain payments to us, subject to certain terms and conditions, including up to approximately $6.7 million in connection with clinical study obligations, pharmacovigilance activities, regulatory filings and support, commercialization and back-office support and distribution expenditures and a $3.0 million milestone payment payable subject to certain regulatory conditions.

13

Table of Contents

Additionally, the Supply Agreement, which continues in effect until the expiration or termination of the Amended Takeda Agreement, will also terminate as of the respective Termination Date in the applicable geographic territory.

We have assumed any post-marketing obligations of Takeda as part of the Takeda Termination Agreement, including costs that otherwise would have been Takeda's obligation under the Amended Takeda Agreement for the ongoing pediatric studies, and the hd-CKD Study. As discussed above, we have come to a mutual decision with Takeda to initiate withdrawal of the marketing authorization forRienso in the EU and Switzerland. We are currently assessing the commercial opportunity forFeraheme in Canada. In connection with our decision to withdraw the marketing authorization forRienso in the EU and Switzerland, we may modify or terminate clinical trials being conducted as part of our post-approval commitments to the EMA.

Additional details regarding the Takeda Termination Agreement and related revenue can be found in Note R, "Collaborative Agreements," to our consolidated financial statements included in this Annual Report on Form 10-K.

PlasmaTech

In June 2013, we entered into the MuGard License Agreement under which PlasmaTech granted us an exclusive, royalty-bearing license, with the right to grant sublicenses, to certain intellectual property rights, including know-how, patents and trademarks, to use, import, offer for sale, sell, manufacture and commercializeMuGard in the U.S. and its territories (the "U.S. Territory") for the management of all diseases or conditions of the oropharyngeal cavity, including mucositis.

In consideration for the license, we paid PlasmaTech an upfront license fee of $3.3 million in June 2013. We are required to pay royalties to PlasmaTech on net sales ofMuGard until the later of (a) the expiration of the licensed patents or (b) the tenth anniversary of the first commercial sale ofMuGard in the U.S. Territory (the "Royalty Term"). These tiered, double-digit royalty rates decrease after the expiration of the licensed patents and are subject to off-set against certain of our expenses. After the expiration of the Royalty Term, the license shall become a fully paid-up, royalty-free and perpetual license in the U.S. Territory.

PlasmaTech remains responsible for the manufacture ofMuGard and we have entered into a quality agreement and a supply agreement with PlasmaTech under which we purchaseMuGard inventory from PlasmaTech. Our inventory purchases are at the price actually paid by PlasmaTech to purchase it from a third-party plus a mark-up to cover administration, handling and overhead.

PlasmaTech is responsible for maintenance of the licensed patents at its own expense, and we retain the first right to enforce any licensed patent against third party infringement. The MuGard License Agreement terminates at the end of the Royalty Term, but is subject to early termination by us for convenience and by either party upon an uncured breach by or bankruptcy of the other party.

3SBio

In 2008, we entered into the 3SBio License Agreement and the 3SBio Supply Agreement with 3SBio Inc. ("3SBio") for the development and commercialization ofFeraheme as an IV iron replacement therapeutic agent in China. In consideration of the grant of the license, we received an upfront payment of $1.0 million. In late January 2014, we mutually terminated the agreement with 3SBio, effective immediately, due to the fact that, despite the best efforts of the parties, regulatory approval in China could not be obtained within the agreed upon time period.

14

Table of Contents

Manufacturing

We currently rely solely on third parties for the manufacture ofFeraheme andMakena for our commercial and clinical use. Our third-party contract manufacturing facilities forFeraheme andMakena are subject to current good manufacturing practices ("cGMP"), regulations enforced by the FDA and equivalent foreign regulatory agencies through periodic inspections to confirm such compliance. Although we are currently working to establish and qualify alternative manufacturing facilities for both drug substance and drug product ofFeraheme and drug product forMakena, we do not currently have alternative manufacturers for ourFeraheme andMakena drug substance and drug product, as applicable. In addition, we currently do not have a supply agreement forMakena drug substance and, until we do, we plan to obtainMakena drug substance on a purchase order basis. We target to maintain sufficient inventory levels throughout our supply chain to meet our projected U.S. near-term demand ofFeraheme andMakena drug product in order to minimize risks of supply disruption at points in our single source supply chain. We intend to continue to outsource the manufacture and distribution ofFeraheme andMakena for the foreseeable future, and we believe this manufacturing strategy will enable us to direct more of our financial resources to the commercialization of our products. Under the terms of the MuGard License Agreement, PlasmaTech is responsible for all aspects of manufacturingMuGard. We have entered into a quality agreement and a supply agreement with PlasmaTech under which we purchaseMuGard inventory from PlasmaTech.

To support the commercialization of our products, we have developed a fully integrated manufacturing support system, including quality assurance, quality control, regulatory affairs and inventory control policies and procedures. These support systems are intended to enable us to maintain high standards of quality for our products.

We have also established certain testing and release specifications with the FDA and other foreign regulatory agencies. This release testing must be performed in order to allow the finished product to be used for commercial sale.

Makena

TheMakena drug product for our commercial and clinical use is currently manufactured by Hospira Worldwide, Inc. ("Hospira") under a Development and Supply Agreement, originally dated September 17, 2009, by and between Hologic, Inc. (from whom Lumara Health, then-named K-V Pharmaceutical Company ("K-V Pharmaceutical") originally purchased the worldwide rights toMakena) and Hospira, which was fully assigned to K-V Pharmaceutical in December 2012, and was amended on March 28, 2014 (as amended, the "Hospira Agreement"). Under the terms of the Hospira Agreement, Hospira was manufacturingMakena at certain agreed-upon pricing through December 31, 2014 and currently Hospira can increase the price (subject to certain limitations) ofMakena for both commercial and clinical uses, upon advance written notice to us. In addition, under the terms of the Hospira Agreement we are obligated to make certain minimum purchase requirements. The term of the Hospira Agreement applies to the manufacture of certain dosage forms and provides for an option to extend the term based on the occurrence, timing and amount of certain forecasts and purchase orders related to other dosage forms. We cannot make any guarantees that we will be able to extend the term of the Hospira Agreement on favorable terms, if at all.

Lumara Health, as our wholly owned subsidiary following consummation of the acquisition, is subject to certain continuing obligations under a Consent Decree of Permanent Injunction (the "Consent Decree") among the FDA, Lumara Health's predecessor company, K-V Pharmaceutical and certain former officers and affiliates of K-V Pharmaceutical. In particular, Lumara Health is bound by a number of provisions and requirements in the Consent Decree including, but not limited to, inspection of Lumara Health's places of business by the FDA without prior notice, and notification of FDA of particular actions and events. If Lumara Health fails to comply with applicable provisions in the

15

Table of Contents

Consent Decree, the Federal Food, Drug, and Cosmetic Act (the "FDC Act") or the FDC Act's implementing regulations, the FDA may impose specific sanctions including, but not limited to, the requirement to cease any of Lumara Health's manufacturing operations, the imposition of substantial financial penalties, and the requirement to implement additional corrective actions.

Feraheme

We currently have the following contracts in place related to the manufacture ofFeraheme:

In August 2012, we entered into a Commercial Supply Agreement, as amended in October 2013 and December 2014, with Sigma-Aldrich, Inc. ("SAFC") pursuant to which SAFC agreed to manufacture and we agreed to purchase from SAFC, the active pharmaceutical ingredient ("API") or the drug product intermediate ("DPI") for use in the finished product of ferumoxytol for U.S. commercial sale, for sale outside of the U.S., as well as for use in clinical trials (as amended, the "SAFC Agreement"). Subject to certain conditions, the SAFC Agreement provides that we purchase from SAFC certain minimum quantities of API or DPI each year, but we are not obligated to use SAFC as our sole supplier of API or DPI. In addition, the prices for each batch will decline as batches are produced in greater quantities throughout each year of the agreement. The SAFC Agreement has an initial term that ends December 31, 2020, which may be automatically extended thereafter for additional two year periods, unless cancelled by us or SAFC within an agreed-upon notice period.

The amendments to the SAFC Agreement provide updated pricing terms beginning on a certain date in the future, which are based on the amount of product produced by SAFC in a given calendar year. If SAFC is unable to offer these agreed-upon prices, we may terminate our minimum purchase commitments. In addition, if SAFC is unable to meet our actual demand requirements other than due to our acts, omissions or default, our minimum purchase commitment will be suspended for such period. Further, if after a certain date in the future, SAFC is unable to match abona fide offer from a third party to manufacture and supply product to us on better terms than provided by SAFC pursuant to the SAFC Agreement then a reduced minimum purchase commitment will apply. We have the right to terminate the SAFC Agreement and any purchase orders under certain conditions and subject to certain notice requirements. The SAFC Agreement also specifies cost-sharing arrangements relating to future process changes or capital improvements to the manufacturing process forFeraheme under the SAFC Agreement.

Patheon, Inc. (formerly DSM Pharmaceuticals, Inc.)

In January 2010, we entered into a Pharmaceutical Manufacturing and Supply Agreement, as amended in July 2014, with Patheon, Inc. (formerly DSM Pharmaceuticals, Inc.) ("Patheon") pursuant to which Patheon agreed to manufacture ferumoxytol finished drug product for U.S. commercial sale, for sale outside of the U.S., as well as for use in clinical trials at a fixed price per vial (as amended, the "Patheon Agreement"). The Patheon Agreement will continue in force until December 31, 2015. The Patheon Agreement may be terminated at any time upon mutual written agreement by us and Patheon or at any time by us subject to certain notice requirements and early termination fees. In addition, the Patheon Agreement may be terminated by either us or Patheon in the event of a material breach of the agreement by the other party provided that the breaching party fails to cure such breach within an agreed-upon notice period.

Raw Materials

We and our third-party manufacturers currently purchase certain raw and other materials used to manufactureFeraheme andMakena from third-party suppliers and, at present, do not have long-term

16

Table of Contents

supply contracts with most of these third parties. Although certain of our raw or other materials are readily available, others may be obtained only from qualified suppliers. Certain materials used inFeraheme andMakena may from time to time be procured from a single source without a qualified alternative supplier of the high-quality standards imposed on our raw and other materials used to manufactureFeraheme, we may not be able to obtain such materials of the quality required to manufactureFeraheme orMakena. The qualification of an alternative source may require repeated testing of the new materials and generate greater expenses to us if materials that we test do not perform in an acceptable manner. In addition, we or our third-party manufacturers sometimes obtain raw or other materials from one vendor only, even where multiple sources are available, to maintain quality control and enhance working relationships with suppliers, which could make us susceptible to price inflation by the sole supplier, thereby increasing our production costs. As a result of the high-quality standards imposed on our raw or other materials, we or our third-party manufacturers may not be able to obtain such materials of the quality required to manufactureFeraheme orMakena from an alternative source on commercially reasonable terms, or in a timely manner, if at all.

Patents and Trade Secrets

We consider the protection of our technology to be material to our business. Because of the substantial length of time and expense associated with bringing new products through development and regulatory approval to the marketplace, we place considerable importance on obtaining patent and trade secret protection for our products. Our success depends, in large part, on our ability to maintain the proprietary nature of our technology and other trade secrets. To do so, we must prosecute and maintain existing patents, obtain new patents and ensure trade secret protection. We must also operate without infringing the proprietary rights of third parties or allowing third parties to infringe our rights.

Our policy is to aggressively protect our competitive technology position by a variety of means, including applying for patents in the U.S. and in appropriate foreign countries. We currently hold a number of U.S. and foreign patents, which expire at various times through 2023. One of our U.S.Feraheme patents is subject to a patent term extension under U.S. patent law and FDA regulations and will expire in June 2023. There are no patents coveringMakena. We have a license to two U.S. patents relating toMuGard, that each expire in 2022. Our foreign patents may also be eligible for extension in accordance with applicable law in certain countries.

We also have patent applications pending in the U.S. and have filed counterpart patent applications in certain foreign countries directed toFeraheme. Although further patents may be issued on pending applications, we cannot be sure that any such patents will be issued on a timely basis, if at all. In addition, any issued patents may not provide us with competitive advantages or may be challenged by others, and the existing or future patents of third parties may limit our ability to commercializeFeraheme. For example, in July 2010, Sandoz GmbH ("Sandoz") filed with the European Patent Office (the "EPO") an opposition to a previously issued patent which covers ferumoxytol in EU jurisdictions. In October 2012, at an oral hearing, the Opposition Division of the EPO revoked this patent. In December 2012, our notice of appeal of that decision was recorded with the EPO, which suspended the revocation of our patent. On May 13, 2013, we filed a statement of grounds of appeal and on September 27, 2013, Sandoz filed a response to that statement. We filed a reply to that response on March 17, 2014 and oral proceedings for the appeal are scheduled for June 16, 2015. We continue to defend the validity of this patent throughout the appeals process, which we expect to take two to three years. However, in the event that we do not experience a successful outcome from the appeals process, under EU regulations ferumoxytol would still be entitled to eight years of data protection and ten years of market exclusivity from the date of approval, which we believe would create barriers to entry for any generic version of ferumoxytol into the EU market until sometime between 2020 and 2022.

17

Table of Contents

Our licensed patent rights toMuGard may not prevent competitors from independently developing and marketing a competing product that does not infringe our licensed patents or other intellectual property. Further, there are no patents coveringMakena and thus the successful commercialization ofMakena is significantly reliant on our ability to take advantage of its orphan drug exclusivity.

Frequently, the unpredictable nature and significant costs of patent litigation leads the parties to settle to remove any uncertainty related to the status of their patents. Settlement agreements between branded companies and generic applicants may allow, among other things, a generic product to enter the market prior to the expiration of any or all of the applicable patents covering the branded product, either through the introduction of an authorized generic or by providing a license to the applicant for the patents in suit.

Competition

The pharmaceutical and biopharmaceutical industries are intensely competitive and subject to rapid technological change. Many of our competitors forFeraheme are large, well-known pharmaceutical companies and may benefit from significantly greater financial, sales and marketing capabilities, greater technological or competitive advantages, and other resources. ForMakena, most of our competition comes from pharmacies that compound non-FDA approved formulations of HPC (defined below), which are sold at a lower cost thanMakena. In addition, genericFeraheme andMakena competitors could enter the market through approval of abbreviated new drug applications ("ANDAs") that useFeraheme orMakena as a reference listed drug, which would allow generic competitors to rely onFeraheme's orMakena's safety and efficacy trials instead of conducting their own studies. Because entry into the market can occur upon the expiration of the reference listed drug's exclusivity, we could face such competition in the near-term asFeraheme's U.S. market exclusivity expired in June 2014 andMakena's orphan drug exclusivity expires in February 2018. Our existing or potential new competitors forFeraheme andMakena may develop products that are more widely accepted than ours and may receive patent protection that dominates, blocks or adversely affects our product development or business.

Makena

AlthoughMakena is the only FDA-approved drug indicated to reduce the risk of preterm birth in women with a singleton pregnancy who have a history of singleton spontaneous preterm birth, it competes for market share with compounding pharmacies. Hydroxyprogesterone caproate ("HPC") is the active ingredient inMakena. Compounding pharmacies have been manufacturing formulations of HPC (which compounded formulations we refer to as "c17P") for many years and c17P formulations will likely remain available even thoughMakena has been granted orphan drug exclusivity until February 2018. We estimate that between approximately 40% and 50% of the at-risk patient population is treated with c17P.Makena currently has between approximately 20% and 30% of the market share of the at-risk patient population with at least 30% of the at-risk patient population being treated either with other therapies that are not approved for women pregnant with a singleton with a prior history of spontaneous preterm birth of a singleton, or not treated at all.