Use these links to rapidly review the document

Table of Contents

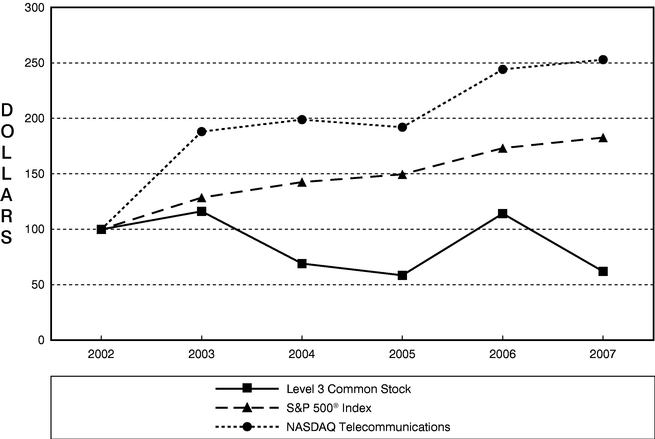

LEVEL 3 COMMUNICATIONS, INC. AND SUBSIDIARIES INDEX TO CONSOLIDATED FINANCIAL STATEMENTS

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| (Mark One) | |

ý |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2007 |

OR |

o |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to |

Commission file number: 0-15658

Level 3 Communications, Inc.

(Exact name of Registrant as specified in its charter)

Delaware

(State or other jurisdiction of

incorporation or organization) | | 47-0210602

(I.R.S. Employer

Identification No.) |

1025 Eldorado Boulevard, Broomfield, Colorado

(Address of principal executive offices) |

|

80021-8869

(Zip code) |

(720) 888-1000

(Registrant's telephone number including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Common Stock, par value $.01 per share | | The NASDAQ Stock Market LLC |

Securities registered pursuant to section 12(g) of the Act:

None

Indicate by check mark whether the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ý No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definition of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ý | | Accelerated filer o | | Non-accelerated filer o

(Do not check if a smaller reporting company) | | Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No ý

As of June 30, 2007 the aggregate market value of common stock held by non-affiliates of the registrant approximated $6.5 billion based upon the closing price of the common stock as reported on the NASDAQ Global Select Market as of the close of business on that date. Shares of common stock held by each executive officer and director and by each entity that owns 10% or more of the outstanding common stock have been excluded in that such persons may be deemed to be affiliates. This determination of affiliate status is not necessarily a conclusive determination for other purposes.

Indicate the number of shares outstanding of each of the registrant's classes of common stock, as of the latest practicable date.

Title

| | Outstanding

|

|---|

| Common Stock, par value $.01 per share | | 1,545,421,165 as of February 26, 2008 |

DOCUMENTS INCORPORATED BY REFERENCE

List hereunder the following documents if incorporated by reference and the Part of the Form 10-K (e.g., Part I, Part II, etc.) into which the document is incorporated: (1) Any annual report to security holders; (2) Any proxy or information statement; and (3) Any prospectus filed pursuant to Rule 424(b) or (c) under the Securities Act of 1933. The listed documents should be clearly described for identification purposes (e.g., annual report to security holders for fiscal year ended December 24, 1980).

Portions of the Company's Definitive Proxy Statement for the 2008 Annual Meeting of Stockholders are incorporated by reference into Part III of this Form 10-K

Table of Contents

i

Unless the context otherwise requires, when we use the words "Level 3," "we," "us" or "our company" in this Form 10-K, we are referring to Level 3 Communications, Inc., a Delaware corporation, and its subsidiaries, unless it is clear from the context or expressly stated that these references are only to Level 3 Communications, Inc. In this Form 10-K, we may refer to our former subsidiary Software Spectrum, Inc. and its subsidiaries as "Software Spectrum."

The Level 3 logo and Level 3 are registered service marks of our wholly owned subsidiary, Level 3 Communications, LLC, in the United States and other countries. All rights are reserved. This Form 10-K refers to trade names and trademarks of other companies. The mention of these trade names and trademarks in this Form 10-K is made with due recognition of the rights of these companies and without any intent to misappropriate those names or marks. All other trade names and trademarks appearing in this Form 10-K are the property of their respective owners.

Cautionary Factors That May Affect Future Results

(Cautionary Statements Under the Private Securities Litigation Reform Act of 1995)

This Form 10-K contains forward-looking statements and information that are based on the beliefs of our management as well as assumptions made by and information currently available to us. When we use the words "anticipate", "believe", "plan", "estimate" and "expect" and similar expressions in this Form 10-K, as they relate to us or our management, we are intending to identify forward-looking statements. These statements reflect our current views with respect to future events and are subject to certain risks, uncertainties and assumptions.

Should one or more of these risks or uncertainties materialize, or should underlying assumptions prove incorrect, our actual results may vary materially from those described in this document. These forward-looking statements include, among others, statements concerning:

- •

- our communications business, its advantages and our strategy for continuing to pursue our business;

- •

- anticipated development and launch of new services in our business;

- •

- anticipated dates on which we will begin providing certain services or reach specific milestones in the development and implementation of our business strategy;

- •

- growth of the communications industry;

- •

- expectations as to our future revenue, margins, expenses, cash flows and capital requirements; and

- •

- other statements of expectations, beliefs, future plans and strategies, anticipated developments and other matters that are not historical facts.

These forward-looking statements are subject to risks and uncertainties, including financial, regulatory, environmental, industry growth and trend projections, that could cause actual events or results to differ materially from those expressed or implied by the statements. The most important factors that could prevent us from achieving our stated goals include, but are not limited to, our failure to:

- •

- integrate strategic acquisitions;

- •

- increase the volume of traffic on our network;

- •

- defend our intellectual property and proprietary rights;

- •

- successfully complete commercial testing of new technology and information systems to support new services;

- •

- develop new services that meet customer demands and generate acceptable margins;

- •

- attract and retain qualified management and other personnel; and

- •

- meet all of the terms and conditions of our debt obligations.

Except as required by applicable law and regulations, we undertake no obligation to publicly update any forward-looking statements, whether as a result of new information, future events or otherwise. Further disclosures that we make on related subjects in our additional filings with the SEC or Securities and Exchange Commission should be consulted. For further information regarding the risks and uncertainties that may affect our future results, please review the information set forth below under "ITEM 1A. RISK FACTORS."

Part I

ITEM 1. BUSINESS

Unless the context otherwise requires, when we use the words "Level 3," "we," "us" or "our company" in this Form 10-K, we are referring to Level 3 Communications, Inc., a Delaware corporation, and its subsidiaries, unless it is clear from the context or expressly stated that these references are only to Level 3 Communications, Inc. Throughout this Form 10-K we use various industry terms and abbreviations, which we have defined in the Glossary of Terms at the end of this description of our business.

Through our operating subsidiaries, we engage primarily in the communications business.

We are a facilities based provider (that is, a provider that owns or leases a substantial portion of the plant, property and equipment necessary to provide its services) of a broad range of integrated communications services. We have created our communications network generally by constructing our own assets, but also through a combination of purchasing and leasing other companies and facilities. Our network is an advanced, international, facilities based communications network. We designed our network to provide communications services, which employ and take advantage of rapidly improving underlying optical, Internet Protocol, computing and storage technologies.

Market and Technology Opportunity. We believe that ongoing technology advances in both optical and Internet Protocol technologies have been revolutionizing the communications industry. We also believe that these advances have, and will continue to, facilitate decreases in unit costs for communications service providers that are able to most effectively take advantage of these technology advances. Service providers that can effectively take advantage of technology improvements and reduce unit costs will be able to offer lower prices, which, we believe, will stimulate substantial increases in the demand for communications services. We believe there are two primary factors that are continuing to drive this market dynamic:

- •

- Rapidly Improving Technologies. Over the past few years, both Internet Protocol or IP and optical based networking technologies have undergone extremely rapid innovation, due, in large part, to market based development of underlying technologies. This rapid technology innovation has resulted in both an improvement in price-performance for optical and Internet Protocol systems, as well as rapid improvement in the functionality and applications supported by these technologies. For example, these improvements are enabling voice over IP services or VoIP that are challenging traditional telephone network or PSTN services. We believe that this rapid innovation will continue well into the future across a number of different aspects of the communications marketplace.

- •

- High Demand Elasticity. We believe decreases in communications services costs and prices cause the development of new bandwidth-intensive applications, which, over time, result in even more significant increases in bandwidth demand. In addition, we believe that communications services are direct substitutes for other, existing modes of information distribution from sources such as traditional broadcast entertainment as well as distribution of software, audio and video content using physical media delivered using motor transportation systems. An example of this dynamic is the use of the Internet for the distribution of video entertainment.

2

We believe that as communications services improve more rapidly than these alternative content distribution systems, significant demand will be generated from these sources of information. We also believe that high elasticity of demand from both these new applications and the substitution for existing distribution systems will continue for the foreseeable future. We believe that while high demand elasticity will be manifested over time, government regulation and communications supply chain inefficiencies may cause realization of demand to be delayed.

We also believe that there are significant implications that result from this market dynamic. These implications include the following:

- •

- Incorporating Technology Changes. Given the rapid rate of improvement in optical and Internet Protocol technologies, communications service providers that are most effective at rapidly deploying new services that take advantage of these technologies will have an inherent cost and service advantage over companies that are less effective at deploying new services that use these technologies.

- •

- Capital Intensity. The rapid improvements in these technologies and the need to move to new technologies more quickly results in shortened economic lives of underlying assets. To achieve improvements in service capabilities and unit cost reductions, service providers will need to deploy new generations of technology sooner, resulting in a more capital-intensive business model. Those providers with the technical, operational and financial ability to take advantage of the rapid advancements in these technologies are expected to have higher absolute capital requirements, shortened asset lives, rapidly decreasing unit costs and prices, rapidly increasing unit demand and higher cash flows and profits.

Our Communications Business Strategy

We are seeking to capitalize on the opportunities presented by the expanded coverage of our communications network as well as the significant and rapid advancements in optical and Internet Protocol technologies. Key elements of our strategy include:

- •

- Offer a Comprehensive Range of Communications Services Over Our End-to-End Network. We provide a comprehensive range of communications services designed to meet the needs of our customers over our network. Beginning in 2006, we expanded our targeted customer base to include enterprise or business customers through the acquisitions we completed during 2006 and early 2007.

- •

- Internet Protocol and data services—including (1) Internet access and IP and Ethernet Virtual Private Networks and (2) broadband transport services such as wavelengths, dark fiber and private line services (transoceanic, backhaul, intercity, metro and unprotected private line services);

- •

- content distribution services including caching and video broadcast services;

- •

- colocation services; and

- •

- Softswitch and voice services—including wholesale VoIP component services, enterprise or business voice services, wholesale voice origination and termination services and managed modem for the dial-up access business.

The availability of these services varies by location.

For several years we have been developing services that take advantage of the investment that we have made in our network and that generally target large, existing markets for communications services. We have also expanded our existing markets for communications

3

services through the acquisitions we completed in 2006 and early 2007 that enabled us to offer services directly to enterprise or business customers. Through these efforts we have increased significantly our addressable market by adding new targeted customers as well as new voice and data services that take advantage of the geographic coverage and cost advantages of our network.

With respect to our wholesale customers, we provide these customers with several options for accessing our intercity network—including our metropolitan networks and colocation facilities. Our metropolitan networks enable us to connect directly to points of high traffic aggregation. These traffic aggregation facilities are typically locations where our customers wish to interconnect with our intercity network. Our metropolitan networks allow us to extend our network services to these aggregation points at low costs. With respect to our enterprise customers, we provide these customers with access to our network either by directly connecting to their location or by serving that location with a connection from another communications services provider. As of December 31, 2007, we have:

- •

- approximately 77,000 intercity route miles in North America and Europe, which we expect to reduce to approximately 48,000 intercity route miles after we complete the integration of acquired companies, connecting 20 countries;

- •

- approximately 125 markets having metropolitan fiber networks containing approximately 27,000 route miles in the United States and Europe; and

- •

- approximately 7,300 traffic aggregation points and buildings in the aggregate.

We believe that providing colocation services in facilities directly connected to our network attracts communications intensive customers by allowing us to offer those customers reduced bandwidth costs, rapid provisioning of additional bandwidth, interconnection with other third party networks and improved network performance.

Additionally, our metropolitan networks allow us to compete for certain local communications traffic, which constitutes a significant percentage of the communications market. As of December 31, 2007, we had secured approximately 6.9 million square feet of space for our Gateway and transmission facilities and other technical space and had completed the build-out of approximately 4.6 million square feet of this space.

- •

- Provide Low Cost Backbone Services Through An Upgradeable Backbone Network. Many portions of our originally constructed intercity and metropolitan networks were designed to provide high quality communications services at a lower cost. As we continue to integrate our acquired operations, our network and business processes will seek to enable us to cost effectively deploy future generations of optical and IP networking components (both fiber and transmission electronics and optronics) and thereby expand capacity and reduce unit costs. In addition, our strategy is to maximize the use of open, non-proprietary interfaces in the design of our network software and hardware. This approach is intended to provide us with the ability to purchase the most cost effective network equipment from multiple vendors and allow us to deploy new technology more rapidly and effectively.

- •

- Target Top Global Bandwidth Customers. With respect to our wholesale service offerings, our primary distribution strategy is to use a national, direct sales force focused on high bandwidth usage businesses. These businesses include incumbent local exchange carriers, international carriers also known as PTTs, major internet service providers or ISPs, broadband cable television operators, wireless providers, major interexchange carriers, the U.S. government and enhanced service providers. Providing communications services to many of these businesses is at the core of our market enabling strategy. We identify as wholesale customers those customers that purchase significant amounts of capacity to serve the needs of their customers.

4

- •

- Further Develop Existing Enterprise Customer Business. With respect to our business markets customers, our primary distribution strategy is to use a locally based direct sales force to target business customers, state governments, higher education institutions and academic consortia with high demands for mission critical communications services. In this category we also target regional carriers that make communications services buying decisions locally.

- •

- Develop Market Leading Content Distribution Service Offerings. At December 31, 2007, we operated one of the largest Internet Protocol backbones in the world. In other words, we operate one of the largest networks over which Internet content is transported from content sources to third party owned access networks connected directly to end users. As a result of this network scale, in early 2007 we embarked on a strategy to refine our capabilities to address the communications needs of those organizations that produce the content that individuals want to view over the Internet. This service offering includes high speed IP services, colocation services and services that cost effectively distribute the content that is produced for consumption over the Internet. We believe that one of the largest sources of future incremental demand for communications services will be derived from customers that are seeking to distribute their feature rich content or video over the Internet. Furthermore, we believe that we are the only services provider with a single source, full portfolio of end-to-end content distribution solutions, and that we are in a unique position to offer a range of building blocks to meet these customers' needs.

- •

- Expand Metropolitan Network Coverage. We expect to selectively extend the current reach of our existing metropolitan networks by opportunistically adding additional connections to buildings and other traffic aggregation points from these networks. These connections will enable us to reach additional potential customers and reduce our costs for the termination of our customers' communications traffic on other carriers' networks.

- •

- Pursue Acquisition Opportunities. For a number of years, we have engaged in significant acquisition activities. In evaluating potential acquisition opportunities, among other criteria, we evaluate the potential acquisition according to the transaction's ability to generate positive cash flow from high credit quality customers. For these opportunities, we generally look for companies with recurring revenue that comes predominantly from services we already provide, in geographic areas that are already served, with customers that are consistent with our existing customer base. It is this group of acquisitions that generally also provide significant synergy opportunities as a result of overlapping network and service offerings.

As we seek to expand the addressable market for our services, we also evaluate opportunities that would expand our service capabilities. Transactions that would be included in this category would expand the geographic scope of our network or would provide capabilities for additional services or distribution channels. For these opportunities, we generally consider whether the targeted company's distribution strategy is consistent with our strategy and whether management believes that the target's current and/or future revenues can be significantly increased and/or expenses can be significantly reduced as a result of a combination with our operations. Generally these acquisition opportunities will not provide the same level of synergy opportunity that the category of acquisitions describe above provide to us.

- •

- Develop Advanced Operational Processes and Business Support Systems. We have developed and continue to develop substantial and scalable operational processes and business support systems specifically designed to enable us to offer services efficiently to our targeted customers. We believe that over time these systems will reduce our operating costs, give our customers direct control over some of the services they buy from us and allow us to grow rapidly while minimizing redesign of our business support systems.

5

- •

- Attract and Motivate High Quality Employees. We have developed programs designed to attract and retain employees with the technical and business skills necessary for our business. The programs include our long term incentive programs.

Our Strengths

We believe that the following strengths will assist us in implementing our strategy:

- •

- Experienced Management Team. We have assembled a management team that we believe is well suited for our business objectives and strategy. Our senior management has substantial experience in leading the development, marketing and sale of communications services and in managing, designing and constructing metropolitan, intercity and international networks.

- •

- A Comprehensive Range of Communications Services. We provide a comprehensive range of communications services designed to meet the needs of our customers over our network. Beginning in 2006, we expanded our targeted customer base to include enterprise or business customers.

The availability of these services varies by location.

For several years we have been developing services that take advantage of the investment that we have made in our network and that generally target large, existing markets for communications services. We have also expanded our existing markets for communications services through our acquisitions that enabled us to offer services directly to enterprise or business customers. Through these efforts we have increased significantly our addressable market by adding new targeted customers as well as new voice and data services that take advantage of the geographic coverage and cost advantages of our network.

- •

- Significant metropolitan network platform. As of December 31, 2007, we have metropolitan fiber networks in approximately 125 markets in North America and Europe, which contain approximately 26,000 route miles and connect in the aggregate approximately 7,300 traffic aggregation points and buildings. Our metropolitan networks enable us to connect directly to points of high traffic aggregation and customer locations and reduce our costs for the termination of our customers' communications traffic on other carriers' networks.

- •

- End-to-End Network Platform. Our strategy has been and continues to be to deploy network infrastructure in major metropolitan areas and to link these networks with significant intercity and trans-oceanic networks in North America and Europe. We believe that the integration of our metropolitan and intercity networks with our colocation facilities will expand the scope and reach of our on-net customer coverage, facilitate the uniform deployment of technological innovations as we manage our future upgrade paths and allow us to grow or scale our service

6

7

Our Communications Services

Customer Focused Organization

Beginning in August 2006, we realigned the customer interacting or customer facing aspects of our communications business into four groups to focus more effectively on the needs of our customers. These four groups are:

- •

- Wholesale Markets Group

- •

- Business Markets Group

- •

- Content Markets Group; and

- •

- Europe

This realignment was implemented to enable those employees in these customer facing roles to develop and deliver high quality communications services that are based on the needs of the customers that the group is seeking to serve. Each of these groups is supported by dedicated employees in sales and segment marketing. Each of the groups is also supported by centralized service or product management and development, general marketing, global network services, engineering, information technology, and corporate functions including legal, finance, strategy and human resources. It is through the Wholesale Markets, Business Markets, Content Markets and Europe groups that we offer a comprehensive range of communications services.

Wholesale Markets Group. The Wholesale Markets Group is focused on delivering communications services to meet the high bandwidth needs of many of the largest global communications services providers on a wholesale basis. The Wholesale Markets Group's customers integrate or package our services into their own products and services to offer voice, video and data services to their end-user customers.

The market segments that the Wholesale Markets Group addresses include:

- •

- domestic and international carriers;

- •

- voice service providers, which include calling card companies, conferencing providers, and contact centers that use VoIP technology to better manage costs and enable advanced applications;

- •

- wireless providers;

- •

- broadband cable television operators;

- •

- system integrators; and

- •

- the U.S. government.

Business Markets Group. The Business Markets Group is focused on delivering communications services to meet the telecommunications needs of: small, medium and large enterprises; regional carriers; higher education institutions and academic consortia; and state and local governments. Local and regional carriers include ISPs, enhanced service providers, application service providers, wireless providers, mobile virtual network operators, VoIP providers as well as datacenters and hosting facilities. The Business Markets Group focuses on providing its targeted customers with the full suite of data, Internet, transport and voice services.

Content Markets Group. As we believe that one of the largest sources of future incremental demand for communications services will be derived from customers that are seeking to distribute their feature rich content or video over the Internet, the Content Markets Group focuses on offering a range

8

of end-to-end communications services building blocks to meet the content distribution needs of its customers. Customers that the Content Markets Group serves include:

- •

- video distribution companies;

- •

- providers of online gaming and mega-portals;

- •

- software service providers;

- •

- social networking providers; and

- •

- traditional media distribution companies including broadcasters, television networks and sports leagues.

Europe. The Europe group focuses on the communications needs of European customers and the European aspects of customers located outside of Europe. The Europe group target customers are similar to the target customers of the Wholesale Markets Group and the Content Markets Group.

Service Offerings

We offer a comprehensive range of communications services, which currently include the following services. All of these services are available to customers of each of the customer facing groups, however their availability varies by location. The following is an overview description of some of the services that we offer.

- •

- Network and Internet Services. We offer both wholesale-oriented communications services to enable large scale networks and high speed access to the Internet as well as similar services designed for the enterprise marketplace. We offer a portfolio of data communications services ranging from basic network infrastructure components such as dark fiber, wavelength, and private line services to higher level routed data services such as Ethernet, Internet Transit and IP VPN. Our Network and Internet Services include the following.

- •

- Transport Services. Transport services include wavelengths (Level 3 Intercity Wavelength Services and Level 3 Metro Wavelength Services) and private lines (Level 3 Intercity Private Line Services and Level 3 Metro Services). These services are available across our metropolitan and intercity fiber network. Wavelength services provide unprotected point-to-point connections of a fixed amount of bandwidth with Ethernet or SONET interfaces. Wavelength services are available at 2.5 Gbps and 10 Gbps speeds, which represent the largest capacity of dedicated transport services. This service offering targets customers that require significant amounts of bandwidth, desire more direct control and provide their own network management. Private line services are also point-to-point connections of dedicated bandwidth but usually include SONET or SDH protection to provide resiliency to fiber or equipment outages. Private line services are available in a range of speeds. Level 3 also offers Metro and Intercity Ethernet Private Line Services with Fast-E and Gig-E interfaces. Customers generally use our transport services to create their own SONET/SDH, ATM and IP networks. We typically offer transport services in annual contracts with monthly payments or long-term pre-paid agreements.

Level 3 also provides transport services within our transatlantic cable system connecting North America and Europe as well as via leased bulk capacity on other transoceanic systems. "International Backhaul" transport services, interconnecting cable landing stations and the terrestrial North American and European networks, are also available.

- •

- High Speed Internet Protocol (IP) Service. Level 3 operates one of the largest international Internet backbones providing connectivity among customer IP, content and application networks. Built on our own intercity and metropolitan networks in North America and

9

Europe, we provide customers with high performance, reliability and scalability. Access to the Internet is enabled through interconnection among our customers across our network as well as interconnections with other Internet Service provider "peers."

- •

- Dedicated Internet Access. Dedicated Internet Access, or DIA, is Level 3's Enterprise focused Internet access product leveraging the same core Internet backbone as our other Internet Services. Level 3 operates one of the largest international Internet backbones in the world and is regularly considered one of the most connected Internet networks. Level 3's Dedicated Internet Access service provides Internet connectivity over a Tier One Internet backbone through a wide variety of access methods and speeds. The service also includes Domain Name services, primary, secondary and caching and is available as either a stand-alone service or as a complement to our other communications services.

- •

- VPN Services. Built on our optical transport and MPLS networks, we offer customers the ability to create private point-to-point, point-to-multipoint, and full-mesh networks based on IP VPN, Virtual Private LAN Service, or VPLS, ATM and Frame Relay technologies. These services allow service providers, corporations, government entities, and distribution businesses to replace multiple networks with a single, cost-effective solution that simplifies the transmission of voice, video, and data over a single or converged network. The service allows the customer to achieve this convergence without sacrificing the quality of service or security levels of traditional dedicated transport offerings. These solutions are used for service provider and corporate data and voice networks, data center networking, disaster recovery and out-of-region or redundant customer connectivity for other service providers.

- •

- Colocation Service. We offer high quality, data center space where customers can locate servers, content storage devices and communications network equipment in a safe and secure technical operating environment. At our colocation sites, we offer high-speed, reliable connectivity to our network and to other networks, including metro and intercity networks, the traditional telephone network and the Internet.

- •

- Dark Fiber Service. Level 3 Intercity Dark Fiber and Level 3 Metro Dark Fiber provide carriers, service providers, government entities and large enterprises a complete infrastructure when a fiber solution is required based on unique applications, control or scale requirements. The services include fiber, colocation space in our Gateway and in our network facilities, power and physical operations and maintenance of the fiber and associated infrastructure.

- •

- Content Distribution. Our primary Content Distribution products and services include the following.

- •

- Content Delivery Network. Our content delivery network services combine our IP network, gateway facilities and patented technology that directs a requestor or end user to the best location or server cluster in our network to retrieve the requested content based on location and network conditions. Our CDN services provide customers with improved cost performance, scalability, reliability and reach for their web applications. Our Caching and Download Services provide efficient delivery of large files such as video, software, security patches, audio and graphics to mass audiences. Our Streaming Services can be used to deliver high performance streams, either live or on-demand, to end users using leading proprietary protocols. We also offer storage solutions enabling customers to upload and store content to our network as part of an optimized delivery platform. In addition to our delivery services, our Intelligent Traffic Management software continuously monitors systems and Internet conditions and enables customers to set rules to dynamically route traffic to meet failover or dual vendor objectives.

10

- •

- Media Delivery Services. Since the acquisition of Servecast in July 2007, we offer media delivery services to customers seeking to manage, protect and monetize content delivered over the internet. Media Delivery Services provide customers with means to ingest and digitize live video content and to manage the organization and presentation of both live and on demand video to end users via a content management system. Content may be secured to prevent unauthorized access, redistribution or syndication. Additionally, support for content monetization via paid and advertising supported models is provided. Media Delivery Services leverage our Content Delivery Network for the delivery of managed content to end users.

- •

- Fiber Optic and Satellite Video Transport Services. We offer various products to provide audio and video feeds over fiber or satellite for broadcast and production customers. These products vary in capacity provided, frequency of use (that is, may be provided on an occasional or dedicated basis) and price. In 2004, Super Bowl® XXXVIII was the first live broadcast event ever carried using our new high definition (HD) transport product.

- •

- Advertising Distribution Services. These services include Audio Distribution and Video Distribution. Our Audio Distribution services distribute radio spots to stations via electronic and physical distribution. Spots are distributed to over 10,500 stations in North America via the Internet using no proprietary hardware. Our Video Distribution services offer customers the capability to deliver video content electronically and physically to television stations, broadcast networks and cable networks across the United States.

On December 19, 2007, we announced that our wholly owned subsidiaries, WilTel Communications, LLC, Level 3 Communications, LLC and Vyvx, LLC, as the sellers, had entered into an Asset Purchase Agreement with DG FastChannel, Inc. Pursuant to the terms of the Purchase Agreement, the sellers will sell to DG FastChannel for cash certain assets relating to the Advertising Distribution Services business. Under the terms of the Purchase Agreement, we will receive $129 million in cash upon the closing of the transaction. The purchase price is subject to certain post closing working capital adjustments. Consummation of the transaction is subject to customary closing conditions, including receipt of applicable federal regulatory approvals.

- •

- Switched Services. We pioneered and developed the Softswitch—a distributed computer system that emulates the functions performed by traditional circuit switches—which enables us to control and process voice and data calls over an Internet Protocol network. We also offer several traditional circuit switch-based voice services. Our Switched Services include the following.

- •

- Level 3 VoIP Enhanced Local. Level 3 VoIP Enhanced Local is a VoIP solution that enables broadband cable operators, IXCs, voice over IP providers, and other companies operating their own switching infrastructure to launch IP-based local and long-distance voice to residential and business customers via any broadband connection. With the purchase of Level 3 VoIP Enhanced Local service, a customer obtains the essential building blocks required to offer residential or business voice over IP phone service such as local phone numbers, local number portability, local and long distance calling, E-911, operator assistance, directory listings, and directory assistance.

- •

- Level 3 Local Inbound. Level 3 Local Inbound service terminates traditional telephone network originated calls to Internet Protocol termination points. Customers, such as call centers, conferencing providers, and voice over IP service providers, can obtain telephone numbers from us or port-in local telephone numbers that the customer already controls. These local calls are then converted to IP and transported over our backbone to a customer's IP voice application at a customer-selected IP voice end point.

11

- •

- Level 3 E-911 Direct. Level 3 E-911 Direct is a portfolio of E-911, or Enhanced 911, solutions, including a fixed-location solution with network connections to public safety answering points or PSAPs that serve approximately 70 percent of all U.S. households, and a solution for nomadic voice over IP providers that takes advantage of the same network connections as the fixed-location solution. Enhanced 911 service allows an emergency services operator to automatically receive information related to a 911 caller's registered address and callback phone number. A nomadic voice over IP provider is a company that permits its end user customer to use VoIP services from more than one location. Level 3 E-911 Direct provides the network capabilities that route and complete 911 calls to appropriate selective routers and PSAPs on the traditional telephone 911 network. When used with the services provided by a third party VoIP Positioning Center, or VPC, to collect, update and report subscriber location information, our Level 3 E-911 Direct service enables VoIP service providers to supply 911 services to their subscribers.

- •

- Level 3 One Plus. Level 3 One Plus service provides non-facilities-based resellers, or carriers with regional networks, the ability to originate PSTN calls from anywhere in the continental US. Level 3 then terminates the domestic, international and Operator Services calls over our nationwide network, or customers may choose to have calls handed back to them over a dedicated facility. This service suite features Automatic Number Identification (ANI)-based and Carrier Identification Code (CIC)-based services as well as a dedicated end-user service.

- •

- Level 3 Enterprise Local and Long Distance Voice Services. Level 3 Enterprise Local Voice Services provide PSTN connectivity for customer telephone equipment; telephone numbers, which include associated directory listings; standard services, which include operator services, directory assistance, and 911 services; and long-distance access, which provides equal access to all long-distance carriers, including Level 3. Level 3 Enterprise Long Distance services offer intrastate and interstate voice service at simple, cost-effective rates as well as access to over 290 international locations.

- •

- Level 3 Enterprise Toll-Free Services. Level 3 Enterprise Toll-Free Services offer customers the ability to receive and pay for inbound calls, rather than those calls being paid for by the call originator. Additionally, a number of routing and call information features are available.

- •

- Level 3 Voice Termination. Level 3 Voice Termination consists of long distance transport and termination services, offered over circuit switch or Softswitch technologies. These services are offered primarily to inter-exchange carriers, or IXCs, wireless providers, local phone companies, cable companies and voice over IP providers. We also offer the termination of international voice traffic over circuit switch or Softswitch technologies. Customers for these services include local phone companies, wireless providers, cable companies and voice over IP providers.

- •

- Level 3 Toll Free. Level 3 Toll Free consists of services that terminate toll free calls that are originated or placed on the traditional telephone network. These toll free calls are carried over either a circuit switch or Softswitch network and delivered to customers in Internet Protocol or traditional TDM format. Customers for these services include call centers, conferencing providers, and voice over IP providers.

- •

- Level 3 Managed Modem. Level 3 Managed Modem is an outsourced, turn-key infrastructure solution for the management of dial up access to the public Internet. ISPs comprise a majority of the customer base for Level 3 Managed Modem and are provided a fully managed dial up network infrastructure. As part of this service, Level 3 arranges for the provision of local network coverage, dedicated local telephone numbers, racks and modems as well as dedicated connectivity from the customer's location to the Level 3 Gateway facility.

12

For a discussion of certain geographic information regarding our revenue from external customers and long-lived assets, please see the notes to our Consolidated Financial Statements appearing elsewhere in this Form 10-K. For a discussion of our communications revenue, please also see Management's Discussion and Analysis of Financial Condition and Results of Operations appearing later in this Form 10-K. Our management continues to review our existing lines of business and service offerings to determine how those lines of business and service offerings assist with our focus on the delivery of communications services and meeting our financial objectives. This exercise takes place both with respect to integration activities and in the ordinary course of our business. To the extent that certain lines of business or service offerings are not considered to be compatible with the delivery of communications or with obtaining our financial objectives, we may exit those lines of business or stop offering those services.

Our communications network

Our network is an advanced, international, facilities based communications network. Today, we primarily provide services over our own facilities. At December 31, 2007, our network encompasses:

- •

- approximately 67,000 intercity route miles in North America, which we expect to reduce to approximately 38,000 intercity route miles after we complete the integration of acquired companies;

- •

- approximately 125 markets having metropolitan fiber networks containing approximately 27,000 route miles in the United States and Europe, connecting approximately 7,300 traffic aggregation points and buildings in the aggregate;

- •

- local networks in approximately 116 North American markets;

- •

- an intercity network covering approximately 10,000 miles across Europe;

- •

- local networks in approximately 9 European markets;

- •

- approximately 6.9 million square feet of Gateway and transmission facilities in North America and Europe; and

- •

- a 1.28 Tbps capable transatlantic cable system currently equipped at 640 Gbps.

Intercity Networks. Our approximately 67,000 mile fiber optic intercity network in North America, which we expect will be approximately 38,000 miles after we complete our integration of acquired companies, consists of the following:

- •

- Multiple conduits. In approximately 30,000 miles of our intercity network, we have installed groups of multiple conduits. We believe that the availability of spare conduit will allow us to deploy future technological innovations in optical networking components as well as providing us with the flexibility to offer conduit to other entities.

- •

- Initial installation of optical fiber strands designed to accommodate dense wave division multiplexing transmission technology. In addition, we believe that the installation of newer optical fibers will allow a combination of greater wavelengths of light per strand, higher transmission speeds and longer physical spacing between network electronics. We also believe that each new generation of optical fiber will allow increases in the performance of these network design aspects and will therefore enable lower unit costs.

- •

- High speed Intercity Dense Wave Division Multiplexing, or DWDM, equipment providing high quality, reliable and cost effective transmission across our fiber backbone. We are continually evaluating advancements in technology that will enable us to scale, lower our cost and provide higher speed services over our intercity network. We believe that the market will continue to move toward Ethernet based services and higher speed interfaces. Through our technology

13

During the first quarter of 2001, we completed our construction activities relating to our North American intercity network. Also during 2001, we completed the migration of customer traffic from our original leased capacity network to our completed North America intercity network. Deployment of the North American intercity network was accomplished through simultaneous construction efforts in multiple locations, with different portions being completed at different times. In 2003, we added approximately 2,985 miles to our North America intercity network as part of the Genuity transaction, and in 2005, we added approximately 30,000 miles (including IRUs) to our intercity network as part of the WilTel Communications transaction. In 2006 and January 2007, we added approximately 26,000 miles (including IRUs) to our North America intercity network as part of the various acquisitions during that period.

In Europe, we have completed construction of our fiber optic intercity network with characteristics similar to those of the North American intercity network in a multiple ring architecture. During 2000, we completed the construction of Ring 1 and Ring 2 of our European network. Ring 1, which is approximately 1,900 miles, connects the major European cities of Paris, Frankfurt, Amsterdam, Brussels and London and was operational at December 31, 2000. Ring 2, which is approximately 1,650 miles, connects the major German cities of Berlin, Cologne, Dusseldorf, Frankfurt, Hamburg, and Munich. Ring 2 became operational during the first quarter of 2001. Subsequently, we created two additional rings generally through IRU acquisitions to connect to our expanded operations in Europe that are described below. The first ring is approximately 2,150 miles and connects Copenhagen, Stockholm and Oslo and the second ring is approximately 1,700 miles and connects Milan, Zurich and Geneva.

During 2002, we completed an expansion of our European operations to seven additional cities. Our expansion to these additional locations was facilitated through the acquisition of available capacity from other carriers in the region. During 2003, we completed an expansion of our European operations to four additional cities. In addition, during 2004, we completed an expansion of our European operations to two cities. During 2005, we completed an expansion of our European operations to one city. During 2006, we obtained dark fiber primarily in those cities currently served by leased wavelength capacity and additionally in 2006 we completed an expansion of our European operations to 9 additional cities. During 2007, we obtained dark fiber in three cities that had been served by leased wavelength capacity and additionally in 2007 we completed an expansion of our European operations to 9 additional cities. In 2008, we expect to continue our European expansion to one additional city using leased wavelength capacity. We expect to use the dark fiber with appropriate transmission equipment to sell a full suite of transport and IP services.

Our European network is linked to our North American intercity network by the Level 3 transatlantic 1.28 Tbps capable cable system, which was also completed and placed into service during 2000. The transatlantic cable system—which we refer to as the Yellow system—has a current capacity of 640 Gbps and was upgradeable to 1.28 Tbps when brought into service. The deployment of the Yellow system was completed pursuant to a co-build agreement announced in February 2000, whereby Global Crossing Ltd. participated in the construction of, and obtained a 50% ownership interest in, the Yellow system. Under the co-build agreement, Level 3 and Global Crossing Ltd. each now separately own and operate two of the four fiber pairs on the Yellow system. We also acquired additional capacity on Global Crossing Ltd.'s transatlantic cable, Atlantic Crossing 1, during 2000 to serve as redundant capacity for our fiber pairs on the Yellow system. We also own capacity in the TAT14 cable system. In connection with the WilTel acquisition, we have secured additional capacity on Global Crossing's transatlantic cable, Atlantic Crossing 1, and TAT-14. In 2006, we purchased 300 Gigabits of transatlantic

14

capacity with the right to purchase 300 Gigabits of additional capacity from Apollo Submarine Cable System Ltd. In January 2007 we purchased 150 Gigabits of the additional capacity available from Apollo Submarine Cable System Ltd, 300 Gigabits in May 2007 and an additional 100 Gigabits in November 2007. We are also an owner on the Japan-US, and China-US cable systems, an IRU holder on Southern Cross cable system as well as an owner on the Americas II cable and an IRU holder on the Arcos system.

Local Market Infrastructure. Our local facilities include fiber optic metropolitan networks connecting our intercity network and Gateways to buildings housing communications-intensive end users and traffic aggregation points—including ILEC and CLEC central offices, long distance carrier points-of-presence or POPs, cable head-ends, wireless providers' facilities and Internet peering and transit facilities. As of December 31, 2007, we had in the aggregate approximately 7,300 traffic aggregation points and buildings connected to our metropolitan networks. Our high fiber count metropolitan networks allow us to extend our services directly to our customers' locations at low costs, because the availability of this network infrastructure does not require extensive multiplexing equipment to reach a customer location, which is required in ordinary fiber constrained metropolitan networks.

We had secured approximately 6.9 million square feet of space for our Gateway and transmission facilities as of December 31, 2007, and had completed the buildout of approximately 4.6 million square feet of this space. Our initial Gateway facilities were designed to house local sales staff, operational staff, our transmission and Internet Protocol routing and Softswitch facilities and technical space to accommodate colocation services—that is, the colocation of equipment by high-volume Level 3 customers, in an environmentally controlled, secure site with direct access to Level 3's network generally through dual, fault tolerant connections. Some of our facilities are larger than our initial facilities and were designed to include a smaller percentage of total square feet for our transmission and Internet Protocol routing/Softswitch facilities and a larger percentage of total square feet to support the sale of colocation services. Availability of these services varies by location.

As of December 31, 2007, we had operational, facilities-based, local metropolitan networks in 116 U.S. markets and 9 European markets.

As of December 31, 2007, we had approximately 145 markets in service in North America and approximately 42 markets in service in Europe.

Our Patent Portfolio

Through acquisitions and through our own research and development, we have created an extensive patent portfolio, consisting of approximately 880 patents and patent applications filed in the United States and around the world. Our patent portfolio includes patents filed in each of the last three decades covering technologies ranging from data and voice services to content distribution to transmission and networking equipment. Most of our issued patents are not scheduled to expire for more than ten years.

In addition to the patents and patent applications we own, we have received licenses to patents held by others, including through a recently-announced cross-license with IBM, giving us access to that company's more than 40,000 patents covering many technologies relevant to our business. While patents give us the right to prevent others, particularly competitors, from using our proprietary technologies, patent licenses give us the freedom to operate our business without the risk of interruption from the holder of the patent that has been licensed to us.

15

We have used our patent portfolio in a number of ways. First, developing or acquiring technologies and receiving the legal right to preclude others from using them may give us a competitive advantage. By way of example, at the end of 2007, we initiated a lawsuit against competitor Limelight Networks, Inc., alleging that that company infringes three of our patents relating to the distribution of content. That lawsuit is expected to go to trial before the end of 2008 and, if successful, could result in a court order prohibiting Limelight from using our patented technology in relevant service offerings. Second, the breadth and depth of our patent portfolio may deter others, particularly telecommunications operators, from bringing patent infringement claims against us for fear of counter-claim by us. There have been relatively few patent infringements brought against us to date. Most of those have been initiated by patent-holding companies who do not operate telecommunications businesses and who are less likely to be subject to a counter-claim of infringement by us. Finally, the extensiveness of our patent portfolio allows us to cross-license with others having similarly broad portfolios on terms acceptable to us, mitigating the risk that others will be able to assert patent infringement claims against us.

We will continue to file new patent applications as we enhance and develop products and services, we will continue to seek opportunities to expand our patent portfolio through strategic acquisitions and licensing, and we will continue to enforce our patents against infringement by others.

Our Content Delivery Network

Content Delivery Network, or CDN, describes a system of computers networked together across the Internet to provide content to users in the most efficient manner to enable an optimal user experience. In a CDN, nodes or groups of computers are deployed in multiple locations closer to the end user, also known as the "edge of the network" and cooperate with each other to satisfy requests for content by end users, transparently moving content behind the scenes to optimize the delivery process. Requests for content are directed intelligently through sophisticated software applications to nodes that provide optimal performance for end users.

Our content delivery network is a unique configuration of our hosting and network assets located in approximately 17 countries, which is designed to improve the performance, reliability, and reach of web applications.

We believe that as a result of the combination of our CDN assets and our other network infrastructure, we are strongly positioned to grow our market share in the CDN business. This belief is based on several factors.

- •

- Network Scale. Because we own our own network, our ability to increase capacity to meet the needs of content providers is greater than other CDN providers who do not have the flexibility to quickly increase their available network capacity.

- •

- Network Reach. Our customers reach global Internet destinations using an average number of "hops" that are fewer than with most any other provider, enabling our customers to easily reach their audiences and provide better performance. The fewer number of hops required by our customers to reach their Internet destinations serves to reduce latency and jitter.

- •

- Low Cost Position. Because we own the underlying network infrastructure, we believe that we are positioned to offer cost advantages to our customers. By moving content at scale, our customers can take advantage of lower unit costs for bandwidth, colocation, servers and disk space.

CDN Applications

There are an increasing number of applications for CDN, across many types of customers, particularly Internet-centric businesses and businesses that desire to accommodate increasingly larger

16

file sizes for transmission over the Internet. The media and entertainment industries use CDN services to provide on-demand streaming and live streaming. Social Networking businesses require CDN to provide their customers with fast reliable music and video downloads. Likewise, through the use of CDN, software companies are able to provide software downloads for their customers. Online retailers and advertisers use CDN services to provide images and flash files and to download advertisements. Online gaming companies provide for game downloads, applications updates and delivery of demos and trailers through CDN.

Content Distribution Services Architecture

The CDN platform uses our existing physical network and infrastructure, and is composed of the Edge server or computer, which provides caching and streaming functions and the Global server, which provides load balancing—that is, a computer that directs the traffic to the most efficient server to meet the end users request. The Edge server enables the storage of popular content in a location that is closer to the end user and thereby reduces bandwidth requirements and improves client response times for content stored in the cache. The Global server or computer load balancing components of the CDN directs end user requests to the content source that is best able to serve the request of the particular end user, such as routing to the service noted that is closest to the end user or to the one with enough capacity to service the request of the end user.

We also transmit audio and video programming for our customers over our fiber-optic network and via satellite. We use our network to carry many live traditional broadcast and cable television events from the site of the event to the network control centers of the broadcasters of the event. These events include live sporting events of the major professional sports leagues. For live events where the location is not known in advance, such as breaking news stories in remote locations, we provide an integrated satellite and fiber-optic network based service to transmit the content to our customers. Most of our customers for these services contract for the service on an event-by-event basis; however, we have some customers who have purchased a dedicated point-to-point service, which enables these customers to transmit programming at any time.

We also distribute advertising spots to radio and television stations throughout the United States, both electronically and in physical form. Customers for these services can utilize a network-based method for aggregating, managing, storing and distributing content for content owners and rights holders. On December 19, 2007, we announced that our wholly owned subsidiaries, WilTel Communications, LLC, Level 3 Communications, LLC and Vyvx, LLC, as the sellers, had entered into an Asset Purchase Agreement with DG FastChannel, Inc. Pursuant to the terms of the Purchase Agreement, the sellers will sell to DG FastChannel for cash certain assets relating to the Advertising Distribution Services business. Under the terms of the Purchase Agreement, we will receive $129 million in cash upon the closing of the transaction. The purchase price is subject to certain post closing working capital adjustments. Consummation of the transaction is subject to customary closing conditions, including receipt of applicable federal regulatory approvals.

Distribution Strategy

Our communications services sales strategy with respect to our Wholesale Markets Group and Europe is to utilize a direct sales force focused on companies with high bandwidth and/or voice requirements. These businesses include incumbent local exchange carriers, established next generation carriers, international carriers also known as PTTs, major ISPs, broadband cable television operators, major interexchange carriers, wireless carriers, systems integrators, governments, emerging VoIP service providers, calling card providers, conferencing providers and call centers.

With respect to our Business Markets Group, medium to large enterprises will be serviced by a field based direct sales force. Smaller business opportunities are serviced by an inside sales force

17

generally selling pre-defined bundles of services. We also compliment our direct sales force with an indirect sales channel of agent partners.

Our communications services sales strategy with respect to the Content Markets Group is also to utilize a direct sales force. Targeted customers include video distribution companies; providers of online gaming and mega-portals; software service providers; social networking providers; and traditional media distribution companies including broadcasters, television networks and sports leagues.

We have in place policies and procedures to review the financial condition of potential and existing customers. We apply these procedures to determine whether collectability of services billed is probable prior to the time that we begin delivering services to a customer. If the financial condition of an existing customer deteriorates to a point where payment for services is in doubt, we will not recognize revenue attributable to that customer until we receive cash. Based on these policies and procedures, we believe our exposure to collection risk within the communications business and the possible effect on our financial statements is limited. We may also experience the effects of possible downturns in the economy and specifically the telecommunications industry; however, we believe the concentration of credit risk with respect to receivables is mitigated due to the dispersion of our customer base among geographic areas and remedies provided by terms of contracts and statutes.

For the year ended December 31, 2007, our top ten customers represented approximately 34% of our consolidated total revenue. Revenue from our largest customer, AT&T Inc. and its subsidiaries, including SBC Communications, BellSouth and Cingular, (assuming those subsidiaries were wholly owned by AT&T for all of 2007), represented approximately 15% of our consolidated total revenue for 2007. The next largest customer accounted for approximately 5% of our consolidated total revenue and the remaining top ten customers each account for 3% or less of our consolidated total revenue.

In connection with the acquisition of WilTel in December 2005, we acquired a large customer contract between WilTel and SBC Communications, a subsidiary of AT&T. We expect that the revenue generated under this contract will continue to decline over time as SBC Communications migrates its traffic from our network to the merged SBC and AT&T Communications network that SBC Communications acquired from the former AT&T.

Business Support Systems

In order to pursue our sales and distribution strategies, we have developed and are continuing to develop and implement a set of integrated software applications designed to automate our operational processes. These development activities also relate to the integration of the systems that were used by the companies that we have acquired. Through the development of a robust, scalable business support system, we believe that we have the opportunity to develop a competitive advantage relative to traditional telecommunications companies. In addition, we recognize that for the success of certain of our services that some of our business support systems will need to be easily accessible and usable directly by our customers.

We are currently deploying a unified set of simplified processes and systems that are streamlining and synchronizing our service, sales, and operational functions through our "Unity" platform. Unity has been designed to provide improved capability in service catalog management, sales opportunity management, customer management, quoting, order entry, order workflow, physical and logical network inventory management, service management, and financial management.

Key design aspects of the business support system development program are:

- •

- integrated modular applications to allow us to upgrade specific applications as new services are available;

18

- •

- a scalable architecture that allows our customers and distributors direct access to certain functions that would otherwise have to be performed by our employees;

- •

- phased completion of software releases designed to allow us to test functionality on an incremental basis;

- •

- "web-enabled" applications so that on-line access to order entry, network operations, billing, and customer care functions is available to all authorized users, including our customers;

- •

- use of a tiered, client/server architecture that is designed to separate data and applications, and is expected to enable continued improvement of software functionality at minimum cost; and

- •

- use of pre-developed or commercial "off-the-shelf" applications, where applicable, which will interface to our internally developed applications.

Our Employees

As of December 31, 2007, we had approximately 6,680 employees. We believe that our success depends in large part on our ability to attract and retain substantial numbers of qualified employees.

Competition

The communications industry is highly competitive. A number of factors in recent years have increased the number of competitors in the market. First, the Telecommunications Act of 1996 created opportunities for non-incumbent providers to enter the marketplace. Second, the capital markets responded by making funding more available to new and existing competitors. Third, enthusiasm over the opportunities created by the rapid developments of the Internet led investors and market participants in general to overestimate the rate at which demand for communications services would grow. Finally, the emergence of new IP-based services has created prospects for new entrants with non-traditional business models to compete with legacy providers.

We believe that a confluence of these factors created an unsustainable level of competition in the market. We believe that this was evidenced by both the number of competitors vying for similar business and by the amount of inventory or capacity each brought to the market for many services. The result of these actions was an oversupply of capacity and an intensely competitive environment.

While we believe the current industry structure has improved significantly, we believe that further restructuring is likely. With the growth of communications demand, excess capacity is increasingly being absorbed. Similarly, some form of industry consolidation will continue to occur based on underlying economics. Given the large ongoing fixed costs associated with operating a backbone network, we believe that the natural industry structure will continue to evolve to a more limited number of competitors with each having high traffic scale across their networks.

While we believe that the long-run industry structure will evolve toward that described above, uncertainty surrounds how the existing competitive landscape will evolve toward this new structure. For example, while a number of next-generation and incumbent providers have been consolidated, we believe there are still a number of competitors operating fundamentally poor business models, are resource constrained, and are unlikely to be long-term survivors in their current forms. In addition, the ultimate effect of the completed acquisition transactions by AT&T and Verizon is yet to be known.

We believe that each competitor's long-run success in the market will be driven by its available resources (for example, financial, personnel, marketing, customers) and the effectiveness of its business model (for example, service focus and mix, cost effectiveness, ability to adapt to new technologies, channel effectiveness). We recognize that many of our existing and potential competitors in the communications industry have resources significantly greater than ours.

19

Our primary competitors are long distance carriers, incumbent local exchange carriers, competitive local exchange carriers, PTTs, Content Delivery Network companies, and other companies that provide communications services. The following information identifies key competitors for each of our product offerings.

Our key competitors for our voice service offerings are other providers of wholesale communications services including AT&T, Verizon, Sprint and competitive local exchange carriers. Our key competitors for managed modem services are other providers of dial up Internet access including Verizon and Qwest Communications.

For our IP and Data services, we compete with companies that include Verizon, Sprint, AT&T, Qwest Communications, Global Crossing, Cogent and XO in North America, and Sprint, Verizon, France Telecom, Deutsche Telecom, Global Crossing and Cogent in Europe.

For transport services, our key competitors in the United States are other facilities based communications companies including AT&T, Verizon, Sprint, Qwest Communications and XO. In Europe, our key competitors are other carriers such as PTTs, Telia International, Colt Telecom Group plc, Verizon, and Global Crossing.

Our key competitors for our colocation services are other facilities based communications companies, and other colocation providers such as web hosting companies and third party colocation companies. In the United States, these companies include AT&T, Savvis, Equinix, Switch & Data and Qwest Communications. In Europe, competitors include Global Switch, InterXion, Redbus, Telecity and Telehouse Europe.

For enterprise services, our key competitors include incumbent local exchange carriers (such as AT&T, Verizon and Qwest), long distance services providers (such as Sprint), and competitive local exchange carriers (such as Time Warner Telecom and XO).

For content distribution network or CDN services, our key competitors include Akamai Technologies and Limelight Networks.

The communications industry is subject to rapid and significant changes in technology. For instance, recent technological advances permit substantial increases in transmission capacity of both new and existing fiber, and the introduction of new products or emergence of new technologies may reduce the cost or increase the supply of certain services similar to those which we plan on providing. Accordingly, in the future our most significant competitors may be new entrants to the communications industry, which—unlike the traditional incumbent carriers we also compete with—are not burdened by an installed base of outmoded or legacy equipment.

Regulation

The Federal Communications Commission or the FCC has jurisdiction over interstate and international communications services, among other things. The FCC's regulation of common carriers without market power, such as us, is less stringent than its regulation of dominant incumbent local exchange carriers. We have obtained FCC approval to land our transatlantic cable in the United States. We have obtained FCC authorization to provide international services on a facilities and resale basis. Under the Telecommunications Act of 1996 (the "1996 Act"), any entity, including cable television companies, electric and gas utilities, may enter any telecommunications market, subject to reasonable state regulation of safety, quality and consumer protection.

The FCC has pending a Notice of Proposed Rulemaking ("NPRM") to initiate a comprehensive review of rules governing the pricing of special access service offered by ILECs subject to price cap regulation. Special access pricing by these carriers currently is subject to price cap rules, as well as

20

pricing flexibility rules which permit these carriers to offer volume and term discounts and contract tariffs (Phase I pricing flexibility) and/or remove from price caps regulation special access service in a defined geographic area (Phase II pricing flexibility) based on showings of competition. In the NPRM the FCC tentatively concludes to continue to permit pricing flexibility where competitive market forces are sufficient to constrain special access prices, but undertakes an examination of whether the current triggers for pricing flexibility accurately assess competition and have worked as intended. The NPRM also asks for comment on whether certain aspects of ILEC special access tariff offerings (e.g., basing discounts on previous volumes of service; tying nonrecurring charges and termination penalties to term commitments; and imposing use restrictions in connection with discounts), are unreasonable. At this time, we cannot predict the impact, if any, that a ruling on the NPRM will have on our network cost structure.

Both AT&T and Verizon, in connection with large acquisitions, have agreed to abide by certain conditions that are enforceable by the FCC in connection with special access prices, terms and conditions. In December 2007, we filed a complaint against AT&T alleging, among other things, that AT&T had violated those commitments. At this stage, the proceeding is continuing and we intend to vigorously pursue our claims. We cannot at this time predict the outcome of that proceeding.