00008200272021FYFALSEhttp://fasb.org/us-gaap/2021-01-31#CashAndSecuritiesSegregatedUnderFederalAndOtherRegulationshttp://fasb.org/us-gaap/2021-01-31#CashAndSecuritiesSegregatedUnderFederalAndOtherRegulationsP3YP1YP2YP1YP2Yhttp://fasb.org/us-gaap/2021-01-31#OtherAssetshttp://fasb.org/us-gaap/2021-01-31#OtherAssetshttp://fasb.org/us-gaap/2021-01-31#OtherAssetshttp://fasb.org/us-gaap/2021-01-31#OtherAssetshttp://fasb.org/us-gaap/2021-01-31#OtherLiabilitieshttp://fasb.org/us-gaap/2021-01-31#OtherLiabilitieshttp://fasb.org/us-gaap/2021-01-31#LongTermDebthttp://fasb.org/us-gaap/2021-01-31#LongTermDebtP3YP3YP3YP3YP3YP3YP3YP5Y0000820027srt:ConsolidatedEntityExcludingVariableInterestEntitiesVIEMemberamp:FixedDeferredIndexedAnnuitiesCededEmbeddedDerivativesMember2021-12-31

| | | | | | | | | | | | | | |

|

|

| UNITED STATES |

| SECURITIES AND EXCHANGE COMMISSION |

| WASHINGTON, D.C. 20549 |

| FORM | 10-K | |

| | | | | | | | | | | | | | |

| ☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the Fiscal Year Ended | December 31, 2021 |

| OR |

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the Transition Period from_______________________to_______________________ |

| | | | | |

| Commission File No. | 1-32525 |

| | |

| AMERIPRISE FINANCIAL, INC. |

| (Exact name of registrant as specified in its charter) |

| | | | | | | | | | | | | | |

| Delaware | | 13-3180631 | |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| 1099 Ameriprise Financial Center | | Minneapolis | | Minnesota | | 55474 | |

| (Address of principal executive offices) | (Zip Code) |

| | | | | | | | | | | | | | |

| Registrant’s telephone number, including area code: | (612) | 671-3131 | |

| | | | | | | | | | | | | | | | | | | | |

| Securities registered pursuant to Section 12(b) of the Act: |

| Title of each class | | Trading Symbol | | Name of each exchange on which registered | |

| Common Stock (par value $.01 per share) | AMP | New York Stock Exchange |

| | | | | | | | | | | | | | |

| Securities registered pursuant to Section 12(g) of the Act: None | |

| | | | | | | | | | | | | | |

| Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. | Yes | ☒ | No | ☐ |

| | | | | | | | | | | | | | |

| Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. | Yes | ☐ | No | ☒ |

| | | | | | | | | | | | | | |

| Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. | Yes | ☒ | No | ☐ |

| | | | | | | | | | | | | | |

| Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). | Yes | ☒ | No | ☐ |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act. |

| Large Accelerated Filer | ☒ | Accelerated Filer | ☐ | Non-accelerated Filer | ☐ | Smaller reporting company | ☐ | Emerging growth company | ☐ |

| | | | | |

| If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. | ☐ |

| | | | | | | | | | | | | | |

| Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act by the registered public accounting firm that prepared or issued its audit report. | ☒ |

| | | | | | | | | | | | | | |

| Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). | Yes | ☐ | No | ☒ |

The aggregate market value, as of June 30, 2021, of voting shares held by non-affiliates of the registrant was approximately $28.4 billion.

| | | | | | | | | | | | | | |

| Indicate the number of shares outstanding of each of the registrant’s classes of common stock, as of the latest practicable date. |

| Class | | Outstanding at February 11, 2022 | |

| Common Stock (par value $.01 per share) | 110,750,945 shares |

DOCUMENTS INCORPORATED BY REFERENCEPart III: Portions of the registrant’s Proxy Statement to be filed with the Securities and Exchange Commission in connection with the Annual Meeting of Shareholders to be held on April 27, 2022 (“Proxy Statement”).

AMERIPRISE FINANCIAL, INC.

FORM 10-K

INDEX

PART I.

Item 1. Business

Overview

Ameriprise Financial is a diversified financial services company with a more than 125-year history of providing solutions to help clients confidently achieve their financial objectives. Ameriprise Financial, Inc. is a holding company incorporated in Delaware that primarily engages in business through its subsidiaries. Accordingly, references to “Ameriprise,” “Ameriprise Financial,” the “Company,” “we,” “us,” and “our” may refer to Ameriprise Financial, Inc. exclusively, to our entire family of companies, or to one or more of our subsidiaries.

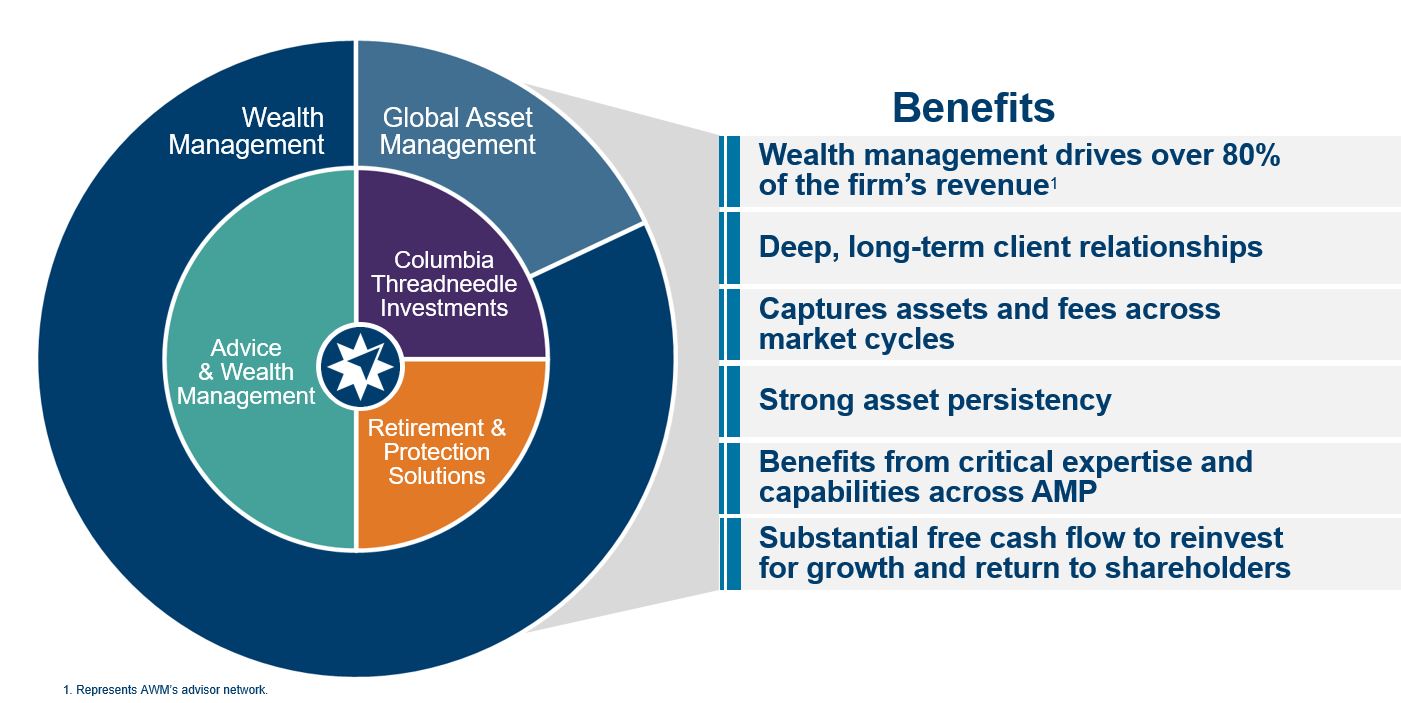

We are a long-standing leader in financial planning and advice offering a broad range of products and services designed to achieve individual and institutional clients’ financial objectives. Our strategy is centered on helping our clients confidently achieve their goals by providing holistic advice and by managing and protecting their assets and income. We utilize two go-to-market approaches in carrying out this strategy: Wealth Management and Asset Management.

Wealth Management

Our Advice & Wealth Management business is the primary growth engine of Ameriprise with a significant market opportunity. We are in a compelling position to capitalize on significant demographic and market trends driving increased demand for financial advice and solutions. In the U.S., the ongoing transition of baby boomers into retirement, as well as Generation X and Millennials planning for retirement, continues to drive demand for financial advice and solutions. The amount of investable assets held by mass affluent and affluent households (our primary target market) is growing and now accounts for over half of U.S. investable assets. We define mass affluent and affluent as households with investable assets of more than $100,000, and we are increasingly focused on those with $500,000 to $5,000,000 in investable assets.

We are an industry-leading wealth manager with a differentiated advice value proposition. Our network of over 10,000 financial advisors (our “advisors”) is the primary channel through which we carry out our wealth management activities. Our capabilities are centered on establishing long-term personal relationships between our clients and our advisors. Through our affiliated advisors, we offer financial planning and advice, as well as banking and full-service brokerage services, primarily to retail clients.

We design products and services as solutions for our clients’ cash and liquidity, asset accumulation, income, retirement, protection, and estate and wealth transfer needs. The financial solutions we offer through our advisors also include other providers’ products as well as our own products and services. We distribute our own life and disability income insurance, as well as variable and structured annuity products through our advisor channel.

Our advisor force is among the largest in the industry and is central to how we serve our clients. We support our advisors with an integrated technology platform, training, leadership and marketing programs to assist them in serving their clients and growing their practices. Our nationally recognized brand combined with these programs and other support creates a compelling value proposition for financial advisors across the financial services industry. This is evidenced by our strong advisor retention and satisfaction and our ability to attract and retain experienced and productive advisors. We continuously invest in, develop, and refine capabilities and tools designed to maximize advisor productivity and client satisfaction.

Asset Management

Our global asset management capabilities, represented by the Columbia Threadneedle Investments® brand (which now also includes the BMO Global Asset Management (EMEA) business we purchased in November 2021), offer a broad spectrum of investment advice and products to individual, institutional and high net worth investors. We refer to the entities purchased in this transaction (BMO Global Asset Management (Europe) Limited and its subsidiaries, BMO Global Asset Management (Asia) Limited, Pyrford International Limited and LGM Investments Limited) broadly as the BMO Global Asset Management (EMEA) business. Columbia Threadneedle’s investment products are primarily offered through third parties, though we also provide our asset management products through our advisor network and through our institutional sales force. Our underlying asset management philosophy is rooted in delivering consistently strong, competitive investment performance. The quality and breadth of our asset management capabilities are demonstrated by 133 of our mutual funds globally being rated as four- and five-star funds by Morningstar.

We are positioned to continue to grow our assets under management and strengthen our asset management offerings to existing and new clients. We benefit from key strategic relationships we have established and have a strong institutional presence. Our asset management capabilities are designed to address mature markets in the U.S. and Europe as well as expanding into new global and emerging markets. In the past few years and continuing with our recent acquisition of the BMO Global Asset Management (EMEA) business, we have expanded beyond our traditional strengths in the U.S. and the United Kingdom (“U.K.”) to serve more clients and gather assets in Continental Europe, Asia, Australia and New Zealand, the Middle East, South America and Africa. We continue to pursue opportunities to leverage the collective capabilities of our global asset management business in order to enhance our investment solutions and to develop new solutions that are responsive to client demand in an increasingly complex and competitive marketplace.

History and Development

Our company has provided solutions to help clients confidently achieve their financial objectives for more than 125 years. Our earliest predecessor company, Investors Syndicate, was founded in 1894 to provide face-amount certificates to consumers. In 1983, our company was formed as a Delaware corporation in connection with American Express’ acquisition of IDS Financial Services from Alleghany Corporation. We changed our name to “American Express Financial Corporation” (“AEFC”) and began marketing our products and services under the American Express brand in 1994. In 2005, AEFC spun off from American Express to form Ameriprise Financial, Inc.

We have grown both organically in the products and services we provide, as well as inorganically through strategic acquisitions. This has allowed us to significantly enhance the scale, performance, and product offerings of our brokerage, financial planning, retail mutual funds and institutional asset management business in order to best serve our clients. Some of our acquisitions include Threadneedle Asset Management Holdings, H&R Block Financial Advisors, Inc., J. & W. Seligman & Co. Incorporated, Columbia Management, Emerging Global Advisors, LLC, Investment Professionals, Inc., and Lionstone Partners, Inc. Most recently, we acquired BMO Financial Group’s European-based asset management business on November 8, 2021, to extend our reach in EMEA and add important capabilities to Columbia Threadneedle.

In order to focus our resources and advance our corporate strategy, we have divested or reinsured some of our businesses, including the 2019 sale of our Ameriprise Auto and Home Insurance business to American Family Insurance Mutual Holding Company and our 2019 and 2021 fixed annuity reinsurance transactions of approximately $1.7 billion and $7.0 billion of fixed annuity policies, respectively.

Over the years, we have also sought to optimize the structure in which we offer certain banking products. In May 2019, we received regulatory approvals and converted Ameriprise National Trust Bank to Ameriprise Bank, FSB to expand the products and services we can provide directly to our customers. At that time, Ameriprise Financial became a savings and loan holding company that is subject to regulation, supervision and examination by the Board of Governors for the Federal Reserve System (“FRB”), and Ameriprise Financial elected to be classified as a financial holding company subject to applicable regulation under the Bank Holding Company Act of 1956, as amended. In June 2021, we filed an application to convert Ameriprise Bank, FSB to a state-chartered industrial bank regulated by the Utah Department of Financial Institutions and the Federal Deposit Insurance Corporation, as well as a separate application to transition the FSB’s personal trust services business to a new limited purpose national trust bank regulated by the Office of the Comptroller of the Currency. Our applications are currently pending.

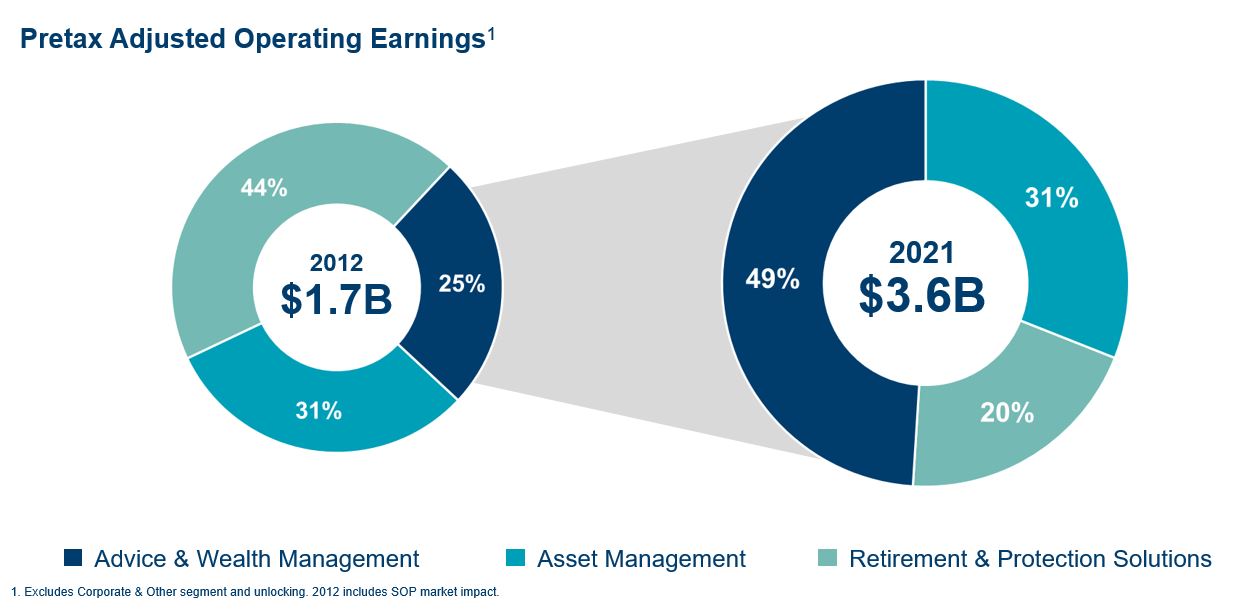

Our Shifting Business Mix and Integrated Model

The financial results from the businesses underlying our go-to-market approaches are reflected in our operating segments:

•Advice & Wealth Management;

•Asset Management;

•Retirement & Protection Solutions; and

•Corporate & Other.

As a diversified financial services firm, we believe our ability to gather assets is best measured by our aggregate assets under management and administration metric. As of December 31, 2021, we had $1.4 trillion in assets under management and administration compared to $1.1 trillion as of December 31, 2020. For a more detailed discussion of assets under management and administration, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations” included in Part II, Item 7 of this Annual Report on Form 10-K.

We continue to execute on our strategy to shift our business mix toward lower capital, fee-based business. The following chart shows our current business mix represented by the contributions of each segment to our pretax adjusted operating earnings (excluding Corporate & Other segment) as well as a historical comparison.

Our Principal Brands

Our diversified products and services are offered through our brands:

| | | | | |

|

We use the Ameriprise Financial® brand as our enterprise brand, as well as the name of our advisor network and certain of our retail products and services. |

| Our global Columbia Threadneedle Investments® brand represents the combined capabilities, resources and reach of Columbia Management Investment Advisers, LLC (including its subsidiaries, “Columbia Management”) and Threadneedle. The foreign operations of Ameriprise Financial, Inc. are conducted primarily through Columbia Threadneedle Investments UK International Limited, TAM UK International Holdings Limited and Ameriprise Asset Management Holdings Singapore (Pte.) and their respective subsidiaries (collectively, “Threadneedle”). We plan to rebrand the BMO Global Asset Management (EMEA) business over the course of 2022 under the Columbia Threadneedle Investments brand, and we are currently using the BMO mark under a license during a transition period. |

| We use our RiverSource® brand for our annuity and protection products issued by RiverSource Life Insurance Company (“RiverSource Life”) and RiverSource Life Insurance Co. of New York (“RiverSource Life of NY” and, together with RiverSource Life, the “RiverSource Life companies”). |

Our Segments - Advice & Wealth Management

We provide financial planning and advice, as well as full-service brokerage services, primarily to retail clients through our financial advisors. These services are centered on long-term, personal relationships between our advisors and our clients and focus on helping clients confidently achieve their financial goals. Our financial advisors provide a distinctive, holistic approach to financial planning and have access to a broad selection of both affiliated and non-affiliated products to help clients meet their financial needs and goals.

A significant portion of revenues in this segment are fee-based and driven by the level of client assets, which is impacted by both market movements and net asset flows. We also earn net investment income on owned assets from Ameriprise Certificate Company and Ameriprise Bank, both wholly owned subsidiaries of Ameriprise, and we earn financial planning fees as well as transaction and other fees. In addition, this segment earns revenue from distribution fees for providing non-affiliated products and intersegment revenues from distribution fees for providing our affiliated products and services to our retail clients. Intersegment expenses for this segment include investment management services provided by our Asset Management segment. All intersegment activity is eliminated in our consolidated results.

Our Financial Advisor Platform

With over 10,000 advisors, we are one of the top branded advisor platforms in the U.S. market where we provide our services. Advisors can choose to affiliate with us in multiple ways as noted below, and each option offers different levels of support and compensation.

We offer the following products and services through our Advice & Wealth Management segment:

•Financial planning and advice services to provide personalized financial planning and financial solutions for which we charge fees and may receive sales commissions for selling products that aid in the client’s plan.

•Discretionary and non-discretionary investment advisory accounts for which we receive fees based on the assets held in that account, as well as related fees or costs associated with the underlying securities held in that account.

•Brokerage products and services for retail and institutional clients.

•Mutual fund offerings from our own Columbia Management family as well as approximately 150 unaffiliated mutual fund families, representing more than 2,200 mutual funds on our brokerage platform for which mutual fund families and other companies generally pay us a portion of the revenue generated from sales of those funds, administrative fees, and fees from the ongoing management attributable to our clients’ ownership in the fund.

•Insurance and annuities products from both RiverSource Life companies as well as certain third parties, and we receive a portion of the revenue generated from the sale of unaffiliated products and certain administrative fees.

•Cash management and banking products including broker sweep programs, cash management accounts, credit cards, margin loans and pledged asset lines of credit.

•Face-Amount Certificates through the Ameriprise Certificate Company, a wholly owned subsidiary, and our earnings are based on the difference between the interest rates credited to certificate holders and the interest earned on the cash invested.

Our Segments - Asset Management

Through Columbia Threadneedle Investments (including our newly acquired BMO Global Asset Management (EMEA) business), we provide investment management, advice and products to retail, high net worth and institutional clients on a global scale.

Columbia Management primarily provides products and services in the United States. Threadneedle, which is integrating our newly acquired BMO Global Asset Management (EMEA) business, primarily provides products and services internationally. Additional subsidiaries beyond Columbia Management and Threadneedle are also included in our Asset Management segment.

Revenues in the Asset Management segment are primarily earned based on managed asset balances, which are impacted by market movements, net asset flows, asset allocation and product mix. We may also earn performance fees from certain accounts where investment performance meets or exceeds certain pre-identified targets. As of December 31, 2021, our Asset Management segment had $754 billion in worldwide managed assets.

Our Asset Management segment also provides intercompany asset management services for Ameriprise Financial subsidiaries. The fees for such services are reflected within the Asset Management segment results through intersegment transfer pricing. Intersegment expenses for this segment include distribution expenses for services provided by our Advice & Wealth Management and Retirement & Protection Solutions segments. All intersegment activity is eliminated in our consolidated results.

Managed assets include external client assets and owned assets. Managed external client assets include client assets for which we provide investment management services, such as the assets of the Columbia Threadneedle Investments fund families and the assets of institutional clients. Managed external client assets also include assets managed by sub-advisers we select but do not include client assets that we advise on a non-discretionary basis such as those assets where we provide voting recommendations and engagement services but do not manage the underlying assets. Our external client assets are not reported on our Consolidated Balance Sheets, although certain investment funds marketed to investors may be consolidated at certain times. See Note 2 and Note 5 to our Consolidated Financial Statements included in Part II, Item 8 of this Annual Report on Form 10-K for additional information on consolidation principles and details regarding the consolidated collateralized loan obligations (“CLOs”). Managed owned assets include certain assets on our Consolidated Balance Sheets (such as the assets of the general account and the variable product funds held in the separate accounts of our life insurance subsidiaries) for which the Asset Management segment provides management services and receives management fees. For additional details regarding our assets under management and administration, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations” included in Part II, Item 7 of this Annual Report on Form 10-K.

Investment Management Capabilities and Products

The investment management activities of Columbia Threadneedle Investments are conducted through specialized investment management teams located around the globe, including Amsterdam, Boston, Chicago, Hong Kong, Houston, London, Los Angeles, Menlo Park, Minneapolis, New York, Portland and Singapore.

Our investment management capabilities and products span a broad range of asset classes and investment styles to meet a variety of client needs. Looking at the type of the $754 billion in assets we manage, we have approximately 54% in equity, 37% in fixed income, 5% in alternatives (which includes real estate, CLOs, private equity, hedge funds, infrastructure and commodities), 3% in hybrids and other and 1% in money market.

We offer or make available the following products and services through our Asset Management segment with a range of investment strategies across these different vehicles and accounts:

•U.S. Registered Funds to the Columbia Management family of funds including retail mutual funds, exchange-listed exchange-traded funds and U.S. closed-end funds and variable insurance trust funds (“VIT Funds”) on which we earn management fees for managing the assets of the Columbia Management family of mutual funds based on the underlying value of the assets and service fees.

•Non-U.S. retail focused funds through Threadneedle, and now expanded with the BMO Global Asset Management (EMEA) business, include different risk-return options across regions, markets, asset classes and product structures, which include retail funds that are similar to U.S. mutual funds (such as Undertakings for the Collective Investment in Transferable Securities (“UCITS”) funds organized as Luxembourg-based investment companies with variable capital (“SICAVs”) and Irish and UK open-end investment companies (“OEICs”). In addition, as a result of acquisition of the BMO Global Asset Management (EMEA) business, this now also includes a range of listed Investment Trusts, including F&C Investment Trust PLC established in 1868.

•European-based pooled investment funds designed for pensions, insurance companies and other institutional investors seeking solutions for liability or balance sheet asset management (“Liability Driven Investment” or “LDI”).

•Institutional and retail separately managed accounts for a range of clients, including pension, profit-sharing, employee savings, sovereign wealth funds and endowment funds, accounts of large- and medium-sized businesses and governmental clients, as well as the accounts of high net worth individuals and smaller institutional clients, including tax-exempt and not-for-profit organizations for which we receive management and performance-related fees.

•Other separately managed accounts, including those offered through models that represent assets under advisement.

•Management of owned assets such as assets held in the general account of our RiverSource Life companies, Ameriprise Certificate Company, and Ameriprise Bank.

•Management of CLOs, which includes providing collateral management services to special purpose vehicles which primarily invest in syndicated bank loans and issue multiple tranches of securities collateralized by the assets to provide investors with various maturity and credit risk characteristics for which we earn fees based on the value of assets and performance-based fees.

•Private funds of various types where we provide investment management and related services to private, pooled investment vehicles organized as limited partnerships, limited liability companies, or non-U.S. entities for which we may receive fees based on the value of the assets or performance-based fees.

•Collective funds and separately managed accounts sponsored by Ameriprise Trust Company (“ATC”) and offered to certain qualified institutional clients such as retirement, pension, and profit-sharing plans for which it receives management fees.

•Sub-advised accounts for certain U.S. and non-U.S. funds, private banking individually managed accounts, common trust funds, and other portfolios sponsored or advised by other firms for which we earn management fees and possibly performance-based fees.

Distribution

We maintain distribution teams and capabilities that aid the sales, marketing, and support of the products and services of our global asset management business. These distribution activities are generally organized into two major categories: retail distribution and institutional/high net worth distribution. However, alternatives and certain other areas have a level of specialized distribution.

Retail Distribution

Columbia Management funds are sold through both unaffiliated third-party financial intermediaries and our Advice & Wealth Management segment. Fees and reimbursements paid to such intermediaries may vary based on sales, redemptions, asset values, asset allocation, product mix, and marketing and support activities provided by the intermediary. Intersegment distribution expenses for services provided by our Advice & Wealth Management segment are eliminated in our consolidated results. Columbia Management Investment Distributors, Inc. acts as the principal underwriter and distributor of our Columbia Management family of funds. Pursuant to distribution agreements with the funds, we offer and sell fund shares on a continuous basis and pay certain costs associated with the marketing and selling of shares. We earn commissions for distributing the Columbia Management funds through sales charges on certain classes of shares and distribution (12b-1) and servicing-related fees based on a percentage of fund assets and receive intersegment allocation payments. This revenue is impacted by overall asset levels and mix of the funds.

Threadneedle and BMO Global Asset Management (EMEA) funds are sold primarily through financial intermediaries and institutions, including banks, life insurance companies, independent financial advisers, wealth managers and platforms offering a variety of investment products. Threadneedle and BMO Global Asset Management (EMEA) also distribute directly to certain clients. In particular, the BMO Global Asset Management (EMEA) business operates direct to consumer savings plans that allow retail investors to purchase at their discretion shares in the investment trusts managed by this business. Various affiliates serve as the distributors of these fund offerings and are authorized to engage in such activities in numerous countries across Europe, the Middle East, the Asia-Pacific region, Latin America and Africa. Certain Threadneedle and BMO Global Asset Management (EMEA) fund offerings, such as its EU UCITS products, may be distributed on a cross-border basis while others are distributed exclusively in local markets.

Institutional and High Net Worth Distribution

We offer separately managed account services and certain funds to high net worth clients and to a wide variety of institutional clients, including pension plans, employee savings plans, foundations, sovereign wealth funds, endowments, corporations, banks, trusts, governmental entities, high net worth individuals and not-for-profit organizations. We provide investment management services for insurance companies, including our insurance subsidiaries. We also provide a variety of services for our institutional clients that sponsor retirement plans. We have dedicated institutional sales teams that market directly to such institutional clients. We concentrate on establishing strong relationships with both institutional clients as well as leading global and national consultancy firms across North America, Europe, the Middle East, Asia, New Zealand and Australia.

Our Segments - Retirement & Protection Solutions

RiverSource solutions help deliver on the Ameriprise client experience and Confident Retirement approach. We offer clients annuities, life insurance, and disability insurance options to meet their needs or current stage in life—whether that is covering essentials, ensuring lifestyle, preparing for the unexpected or leaving a legacy. RiverSource seeks to partner with our advisors to address clients’ goals and long-term needs at a differentiated level and provide a strong risk profile given the clients our advisors serve.

Retirement Solutions

We provide RiverSource variable annuity products to clients to help individuals address their asset accumulation and income goals through our advisors. Our advisor network is the only distributor of RiverSource annuity products, although advisors can offer fixed and variable annuities from selected unaffiliated insurers as well. As part of the continued evolution of our business model, we are continuing to shift our focus away from annuities with living benefit guarantees and toward the accumulation solutions clients want (such as the structured solutions annuity we introduced in 2020). We discontinued new sales of substantially all of our living benefit annuity solutions at the end of 2021. Further, in 2020, we discontinued new sales of fixed annuities and moved the Fixed Annuities and Fixed Indexed Annuities blocks to the Corporate & Other segment as a closed block in addition to reinsuring over 90% of the fixed annuities in this closed block (as discussed below in more detail).

Revenues for our variable annuity products are primarily earned as fees based on a contractholder’s benefit base, contract value or separate account values, which is impacted by both market movements and net asset flows. We also earn net investment income on general account assets supporting reserves for immediate annuities with a non-life contingent feature, structured variable annuities, for certain guaranteed benefits and fixed investment options offered with variable annuities, and on capital supporting the business. In addition, we receive fees charged on assets allocated to our separate accounts to cover administrative costs and a portion of the management fees from the underlying investment accounts in which assets are invested. Revenues for our immediate annuities with a

life contingent feature are earned as premium revenue. Intersegment revenues for this segment reflect fees paid by our Asset Management segment for marketing support and other services provided in connection with the availability of VIT Funds previously discussed. Intersegment expenses for this segment include distribution expenses for services provided by our Advice & Wealth Management segment, as well as expenses for investment management services provided by our Asset Management segment. All intersegment activity is eliminated in our consolidated results.

Protection

We provide life and disability income insurance products to address the protection and risk management needs of our retail clients. Though our advisors may also offer insurance products of unaffiliated carriers, we offer RiverSource insurance products exclusively through our advisors. The primary sources of revenues for our protection business are premiums, fees and charges we receive to assume insurance-related risk. We earn net investment income on owned assets supporting insurance reserves and capital supporting the business. We also receive fees based on the level of the RiverSource Life companies’ separate account assets supporting variable universal life investment options. The protection products earn intersegment revenues from fees paid by our Asset Management segment for marketing support and other services provided in connection with the availability of VIT Funds under the variable universal life contracts. Intersegment expenses for the protection products include distribution expenses for services provided by our Advice & Wealth Management segment, as well as expenses for investment management services provided by our Asset Management segment. All intersegment activity is eliminated in our consolidated results.

RiverSource Insurance Products

Through the RiverSource Life companies and our Retirement & Protection Solutions segment we currently offer the following products:

•Structured Variable Annuities use the performance of an underlying equity market index to determine earnings, up to either a cap or floor.

•Variable Annuities provide returns linked to underlying investments of the contractholder’s choice of certain funds, as well as additional benefits, such as guaranteed minimum death benefits (but without living benefits after the discontinuance of substantially all of those products in 2021).

•Variable Universal Life insurance provides life insurance coverage along with investment returns linked to underlying investment accounts of the policyholder’s choice.

•Universal Life Insurance credits interest at fixed interest rates. Universal Life Insurance may also contain product features that credit interest at a rate linked to an underlying equity market index. In the fourth quarter of 2021, we discontinued new sales of the Universal Life Insurance with secondary guarantees and single-pay fixed Universal Life with a long term care rider products.

•Term Life Insurance provides a death benefit, but it does not accumulate cash value.

•Disability Income Insurance provides monthly benefits to individuals who are unable to earn income either at their occupation at time of disability or at any suitable occupation for premium payments that are guaranteed not to change.

We also offer our clients various riders and alternatives. Our sales of RiverSource individual life insurance in 2021, as measured by scheduled annual premiums, lump sum and excess premiums and single premiums, consisted of approximately 85% variable universal life, 12% universal life and 3% term life.

Reinsurance

We reinsure a portion of the insurance risks associated with our currently offered life, disability income and life contingent immediate annuity products (as well as previously sold fixed annuity, fixed indexed annuity and long-term care products included in our Corporate & Other segment) through reinsurance agreements with unaffiliated reinsurance companies. We use reinsurance to limit losses, reduce exposure to large risks, and provide additional capacity for future growth. To manage exposure to losses from reinsurer insolvencies, we evaluate the financial condition of reinsurers prior to entering into new reinsurance treaties and on a periodic basis during the terms of the treaties. Our insurance companies remain primarily liable as the direct insurers on all risks reinsured. See Note 7 and Note 8 to our Consolidated Financial Statements included in Part II, Item 8 of this Annual Report on Form 10-K for additional information on reinsurance. At a general level, we reinsure all or part of the following (with the closed blocks in our Corporate & Other segment):

| | | | | | | | |

| Product | | Reinsurance Type |

| Term Life and Disability Income | | Coinsurance |

| Universal Life & Variable Universal Life | | Yearly Renewable Term |

| Life Contingent Immediate Annuity | | Coinsurance |

| Fixed Annuity (closed block in Corporate & Other) | | Coinsurance |

| Long Term Care (closed block in Corporate & Other) | | Coinsurance |

Our Segments - Corporate & Other

Our Corporate & Other segment consists of closed blocks of business and net investment income or loss on corporate level assets, including excess capital held in our subsidiaries and other unallocated equity and other revenues as well as unallocated corporate expenses.

Closed Block Long Term Care Insurance

Prior to December 31, 2002, the RiverSource Life companies underwrote stand-alone long term care (“LTC”) insurance. We discontinued offering LTC insurance as of December 31, 2002. A large majority of our closed block LTC is comprised of nursing home indemnity LTC or comprehensive reimbursement LTC. Generally, our policyholders are eligible for LTC benefits if they become cognitively impaired or unable to perform certain activities of daily living.

Nursing home indemnity LTC policies provide a predefined daily benefit if the insured is confined to a nursing home, subject to various maximum benefit periods, regardless of actual expenses of the policyholder. Our older generation nursing home indemnity LTC policies were primarily written between 1989 through 1999 and represent half of our policies.

Comprehensive reimbursement LTC policies provide a predefined maximum daily benefit if the insured is confined to a nursing home and covers a variety of LTC expenses including assisted living, home and community care, adult day care and similar placement programs, subject to various maximum total benefit payment pools, on a cost-reimbursement basis. Our second generation comprehensive reimbursement LTC policies were written from 1997 until 2002.

Our closed block LTC was sold on a guaranteed renewable basis which allows us to re-price in force policies, subject to regulatory approval. Premium rates for LTC policies vary by age, benefit period, elimination period, home care coverage and benefit increase option. Premium rates are based on assumptions concerning morbidity, mortality, persistency, administrative expenses, investment income and profit. We develop our assumptions based on our own claims and persistency experience. In line with the market, we have pursued nationwide premium rate increases for many years and expect to continue to pursue rate increases over the next several years. In general, since very little of our LTC business is subject to rate stability regulation, we have historically followed a policy of pursuing smaller, more frequent increases in order to align policyholder and historic shareholder objectives, but have recently pursued larger increases as an additional method to manage the LTC business. We also provide policyholders with options to reduce their coverage to lessen or eliminate the additional financial outlay that would otherwise result.

For existing LTC policies, RiverSource Life has continued ceding 50% of the risk on a coinsurance basis to subsidiaries of Genworth Financial, Inc. (“Genworth”) and retains the remaining risk. For RiverSource Life of NY, this reinsurance arrangement applies for 1996 and later issues only. Under these agreements, we have the right, but never the obligation, to recapture some, or all, of the risk ceded to Genworth.

For more information regarding LTC, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Corporate and Other” included in Part II, Item 7 of this Annual Report on Form 10-K.

Closed Block Fixed Annuities

In 2020, we discontinued new sales of fixed annuities and moved the Fixed Annuities and Fixed Indexed Annuities blocks to the Corporate & Other segment as a closed block. In this closed block, we have $7.6 billion of account value associated with our fixed annuities of which 91% has been ceded by RiverSource Life on a coinsurance basis to Global Atlantic Financial Group’s subsidiary Commonwealth Annuity and Life Insurance Company (“Commonwealth”) under customary reinsurance arrangements with a comfort trust. For the ceded policies, RiverSource Life ceded 100% of the risk on a coinsurance basis.

Competition

We operate in a highly competitive global industry. As a diversified financial services firm, we compete directly with a variety of financial institutions, including registered investment advisors, securities brokers, asset managers, banks and insurance companies. We directly compete for the provision of products and services to clients, as well as for our financial advisors and investment management personnel. Certain of our competitors offer web-based or mobile-based financial services and discount brokerage services, usually with lower levels of service, to individual clients.

Our Advice & Wealth Management segment competes with securities broker-dealers, independent broker-dealers, financial planning firms, registered investment advisors, insurance companies and other financial institutions to attract and retain financial advisors and clients. Competitive factors influencing our ability to attract and retain financial advisors include compensation structures, brand recognition and reputation, product offerings, and technology and service capabilities and support. Further, our financial advisors compete for clients with a range of other advisors, broker-dealers and direct channels. This includes wirehouses, regional broker-dealers, independent broker-dealers, insurers, banks, asset managers, registered investment advisers and direct distributors. Competitive factors influencing our ability to attract and retain clients include quality of advice provided, price, reputation, advertising and brand recognition, product offerings, technology offerings and service quality.

Our Asset Management segment competes on a global basis to acquire and retain managed and administered assets against a substantial number of firms, including those in the categories listed above. Competitive factors influencing our performance in this industry include investment performance, product offerings and innovation, product ratings, fee structures, advertising, service quality,

brand recognition, reputation and the ability to attract and retain investment personnel. Furthermore, changes in investment preferences or investment management strategy (for example, “active” or “passive” investing styles), client interest in funds with particular environmental, social, or governance practices, client or regulatory requirements on use of client commissions for research, and downward pressure on fees present various challenges to our business and may favor different competitors that focus more on “passive” investing styles. The impact of these factors on our business may vary from country to country and certain competitors may have certain competitive advantage in certain jurisdictions. As an example, the implementation of the terms of the United Kingdom’s exit from the European Union (“EU”) (commonly known as “Brexit”) and other regulatory or political impacts may ultimately favor certain types of asset managers in the EU over non-EU firms.

Competitors of our Retirement & Protection Solutions segment consist of both stock and mutual insurance companies. Competitive factors affecting the sale of variable annuity and insurance products include distribution capabilities, price, product features, hedging capability, investment performance, commission structure, perceived financial strength and financial strength ratings, claims-paying ratings, service, advertising, brand recognition and financial strength ratings from rating agencies such as A.M. Best.

Human Capital Management

Ameriprise Financial has a strong values-driven and inclusive culture that is the foundation of all that we do. While our individual business lines serve different client needs, we have a common vision and values that drive our business and how we work with clients and each other. Our values are the following:

•Client focused;

•Integrity always;

•Excellence in all we do; and

•Respect for the individuals and for the communities in which we live and work.

We aspire to provide an excellent employee and advisor experience for all of our people. This includes approximately 12,000 global employees(1) made up of more than 2,000 employee advisors and more than 10,000 corporate employees, and additionally approximately 8,000 franchise advisors. Our long-term success requires us to attract, retain, engage and develop a diverse, high-performing workforce with a best-in-class development curriculum, strong leadership and comprehensive employee benefits and wellness programs, including diversifying our benefit offerings to increase mental health and resiliency resources during the pandemic. We continually invest in our human capital programs and capabilities to ensure a highly competitive employee value proposition. In 2021, a year when the persistency of the coronavirus disease 2019 (“COVID-19”) pandemic continued to impact the global marketplace:

•We continued to have strong employee engagement, including our industry-leading engagement results (84%) and high leadership effectiveness scores (90%) in our annual engagement survey where our results exceeded external benchmarks. 93% of employees participated in our survey.

•91% of our employees participated in development training. We continue to invest in our employees’ development, and, in addition to annual training requirements, we encourage all employees to participate in our professional development programs, including core curriculum for new hires and a Transformational Leader Program for officers for officers. Leaders are further supported by a broad selection of online courses, workshops, mentoring opportunities, networking events, and peer-to-peer programs.

•We retained 92% of our high-performing employees.

•The retention rate among affiliated advisors who have been with us for more than 10 years is 95%.

•We have also continued to attract experienced, productive advisors, with 325 experienced advisors moving their practices to Ameriprise in 2021 and approximately 1,618 over the last 5 years.

•Of our global employees, 40% self-identify as women, and among our U.S.-based employees 18% identify as ethnically diverse. More detail on our workforce composition with a summary of our EEO metrics can be found in our 2022 Ameriprise Responsible Business report, which is available on our website. Information contained on or accessible through our websites is not incorporated into and does not form a part of this Form 10-K or any other report or document we file with the SEC, and any references to our websites are intended to be inactive textual references only.

Our diversity, equity and inclusion vision is to foster an inclusive culture and diverse workforce so that everyone at Ameriprise feels like they belong, grow and contribute in a culture that helps them realize their potential. This includes ensuring meaningful conversations between leaders and employees on current diversity topics, leveraging programs to attract, retain and advance diverse talent, and continuing to evolve our leadership development curriculum and training for employees and advisors. In 2021, we added resources to support our strategy, including adding new positions on the diversity, equity and inclusion team, developing business unit specific programs, and enhancing our measurement and diagnostic capabilities. Our focus on fostering a diverse and inclusive culture is also reflected in the policies and practices that promote a safe, inclusive and respectful workplace. Our 13 business resource networks engage more than 9,000 participants globally each year to promote cultural awareness and community involvement while providing employees and advisors with wellness and career development resources.

Importantly, our compensation programs are designed to attract, retain, and motivate employees with deliberate alignment of rewards with performance. Weighing both individual goal achievement (the “what”) and leadership performance (the “how”) is critical to driving strong business results. Employees receive base pay, and all are eligible for annual incentive awards and many are eligible for additional long-term incentives. Additionally, employees receive a competitive benefits package that addresses employees’ physical, social, emotional, and financial wellness.

Ameriprise was well prepared to manage through the unexpected COVID-19 pandemic and its associated impacts because of the strategic investments and actions we have taken over many years. From the start and throughout this extended period of multiple variants, our priority has remained on serving our clients, as well as the health and safety of our employees. As we continue to navigate this challenging environment, our balance sheet strength, technology infrastructure and risk management foundation remain key to our success.

Importantly, throughout the ongoing pandemic, we have remained focused on protecting the health and safety of our employees and advisors through a variety of strategic actions, including having the vast majority of our workforce work-from-home during 2020, using safety protocols in our offices, and increased communications and resources for our employees during the pandemic. During 2021, we began the transition to returning to work in our offices in our locations where people could gather safely. We know flexibility is increasingly important, and flexibility has been and continues to be a tenant of our operating model and are offering balanced flexibility that meets the needs of our clients, advisors, employees and shareholders. Going forward, we are building on our learnings from the ongoing pandemic and listening to our clients, advisors, employees, and shareholders to continue to reinforce our culture, strengthen relationships, meet our business objectives, and serve our clients well.

(1) This does not include employees who joined in November 2021 as part of our acquisition of the BMO Global Asset Management (EMEA) business.

Intellectual Property

We rely on a combination of contractual rights and copyright, trademark, patent and trade secret laws and registrations to establish and protect our intellectual property. In the U.S. and other jurisdictions, we have established and registered, or filed applications to register, certain trademarks and service marks that we consider important to the marketing of our products and services, including but not limited to Ameriprise Financial, Threadneedle, RiverSource, Columbia Threadneedle Investments and the BMO Global Asset Management (EMEA) business. We have in the past and will continue to establish and protect our intellectual property rights.

Enterprise Risk Management

Enterprise risk management and our risk management program is an important component in how we manage our business. All subsidiaries of Ameriprise must comply with Ameriprise’s enterprise risk management policy and framework, which: (i) establishes a structure for effective enterprise risk management, including oversight and governance; (ii) delineates key constituent roles and responsibilities; and (iii) imposes a number of core risk management processes. The enterprise risk management policy is designed to manage risks that may impact Ameriprise, including capital, credit, market, liquidity, operational, strategic, reputational, legal and compliance, and product. The enterprise risk management policy is supported by underlying risk policies at each Ameriprise business unit that provide further detail on the business unit’s risk governance, appetite, and tolerance.

Regulation

Virtually all aspects of our business, including the activities of the parent company and our subsidiaries, are subject to various federal, state, local and foreign laws and regulations. These laws and regulations provide broad regulatory, administrative and enforcement powers to supervisory agencies and other bodies, including U.S. federal and state regulatory and law enforcement agencies, foreign government agencies or regulatory bodies and U.S. and foreign securities exchanges. The costs of complying with such laws and regulations are significant, and the consequences for the failure to comply may include civil or criminal charges, fines, censure, the suspension of individual employees, restrictions on or prohibitions from engaging in certain lines of business (or in certain states or countries), revocation of certain registrations and reputational damage. We have made and expect to continue to make significant investments in our compliance and supervision processes, enhancing policies, procedures and oversight to monitor our compliance with the numerous legal and regulatory requirements applicable to our business.

We operate in a highly scrutinized regulatory environment and it remains subject to change. Regulatory developments, both in and outside of the U.S., have resulted or are expected to result in greater regulatory oversight and internal compliance obligations for firms across the financial services industry. In addition, we continue to see enhanced legislative and regulatory interest regarding retirement investing and fiduciary initiatives, as well as environmental, social and governance (“ESG”), cybersecurity, responsible information and data use, financial crime and privacy matters, and we will continue to closely review and monitor any legislative or regulatory proposals and changes. States in the U.S. and jurisdictions outside the U.S. continue to add new complexity to the patchwork of laws already in existence relating to privacy and cybersecurity and we are expecting similar new laws this year in multiple states in the U.S. The same complexity resulting from multiple standards exists for retirement investing where individual states and federal regulators continue to propose or enact their own rules. These legal and regulatory changes have impacted and may in the future impact how we are regulated and how we operate and govern our businesses.

The discussion and overview set forth below provides a general framework of the primary laws and regulations impacting our businesses. Certain of our subsidiaries may be subject to one or more elements of this regulatory framework depending on the nature

of their business, the products and services they provide and the geographic locations in which they operate. To the extent the discussion includes references to statutory and regulatory provisions, it is qualified in its entirety by reference to these statutory and regulatory provisions and is current only as of the date of this report.

In addition to the regulators summarized above, we are also subject to regulation by self-regulatory organizations such as the Financial Industry Regulatory Authority (“FINRA”), various federal and state securities, insurance and financial regulators (such as regulatory agencies and bodies like the Federal Deposit Insurance Corporation and the U.S. Department of Labor (“DOL”)) in the U.S. and in foreign jurisdictions (such as the European Securities and Markets Authority, the national financial regulator for each European country, Australian Securities and Investment Commission and various Canadian provinces) where we do business.

Advice & Wealth Management Regulation

Certain of our subsidiaries are registered with the U.S. Securities and Exchange Commission (“SEC”) as broker-dealers under the Securities Exchange Act of 1934 (“Exchange Act”) and with certain states, the District of Columbia and other U.S. territories. Our broker-dealer subsidiaries are also members of self-regulatory organizations, including FINRA, and are subject to the regulations of these organizations. The SEC and FINRA have stringent rules with respect to the net capital requirements (which includes rules around customer protection) and the marketing and trading activities of broker-dealers. Our broker-dealer subsidiaries, as well as our financial advisors and other personnel, must obtain all required state and FINRA licenses and registrations to engage in the securities business and take certain steps to maintain such registrations in good standing. SEC regulations also impose notice requirements and capital limitations on the payment of dividends by a broker-dealer to a parent.

Our financial advisors are representatives of a dual registrant, meaning it is registered both as an investment adviser under the Investment Advisers Act of 1940 (“Advisers Act”) and as a broker-dealer. Our advisors are subject to various regulations that impact how they operate their practices, including those related to supervision, sales methods, trading practices, record-keeping and financial reporting. In addition, because our independent contractor advisor platform is structured as a franchise system, we are also subject to Federal Trade Commission and state franchise requirements. As noted earlier, we continue to see enhanced legislative and regulatory interest regarding retirement investing and financial advisors, including proposed rules, regulatory priorities or general discussions around transparency and disclosure in advisor compensation and recruiting, identifying and managing conflicts of interest and enhanced data collection.

The SEC’s Regulation Best Interest standard of care became effective June 30, 2020 and the SEC continues to issue various statements and other pieces of guidance on complying with the regulation. Furthermore, several states have either issued their own best interest or fiduciary rules or are considering doing so and those rules may be limited to certain types of products (e.g. insurance and annuities, financial planning, etc.) or may broadly cover all recommendations made by financial advisors. The DOL finalized its voluntary exemption for providing investment advice to retirement account clients and has reinstated prior guidance for determining who is an investment advice fiduciary under pension regulations. While not a regulator, the Certified Financial Planner Board professional standards of conduct includes a fiduciary standard that applies to financial advisors who hold a Certified Financial Planner designation. Considering the various fiduciary rules and regulations that continue to be proposed, finalized, and sometimes withdrawn or amended, we continue to exert significant efforts to evaluate and prepare to comply with each rule.

Other agencies, exchanges and self-regulatory organizations of which certain of our broker-dealer subsidiaries are members, and subject to applicable rules and regulations of, include the Commodities Futures Trading Commission (“CFTC”) and the National Futures Association (“NFA”). Certain subsidiaries may also be registered as insurance agencies and may be subject to the regulations described in the following sections.

Asset Management Regulation

U.S. Regulation

In the U.S., certain of our asset management subsidiaries are registered as investment advisers under the Advisers Act and are subject to regulation by the SEC. The Advisers Act imposes numerous obligations on registered investment advisers, including fiduciary duties, disclosure obligations and record-keeping, and operational and marketing restrictions. Our registered investment advisers may also be subject to certain obligations of the Investment Company Act based on their status as investment advisers to U.S. registered investment companies that we, or third parties, sponsor. As noted earlier, we continue to see enhanced legislative and regulatory interest regarding financial services in the U.S. through rules, regulatory priorities or general discussion. This trend is especially true globally where regulators remain active, including in Europe. Any future regulation could potentially require new approaches which increase our regulatory burdens and costs.

Many aspects of the regulation that applies to our Advice & Wealth Management segment also apply to our Asset Management segment. For example, Columbia Management Investment Distributors, Inc. is registered as a broker-dealer for the limited purpose of acting as the principal underwriter and distributor for Columbia Management funds and other products. Additionally, the Employee Retirement Income Security Act of 1974, as amended (“ERISA”), the SEC’s best interest standards, state and other fiduciary or best interest rules, as well as other similar standards and any rulemaking from the DOL would be relevant to our global asset management business. We continue to review and analyze the potential impact of these regulations across each of our business lines.

In addition, certain of our asset management subsidiaries are registered with the CFTC as a commodity trading advisor and commodity pool operator and are also members of the NFA. In this regard, we are subject to additional registration and reporting requirements with respect to certain registered investment companies and other pooled vehicles that use or trade in futures, swaps and other derivatives that are subject to CFTC regulation.

Non-U.S. Regulation

U.K. Regulation

Outside of the U.S., Columbia Threadneedle Investments, now including the BMO Global Asset Management (EMEA) business, is authorized to conduct its financial services business in the U.K. under the Financial Services and Markets Act 2000. A number of legal entities in the Threadneedle and BMO Global Asset Management (EMEA) business are currently regulated by the Financial Conduct Authority (“FCA”) and one entity in the Threadneedle business is also regulated by the Prudential Regulation Authority (“PRA”). FCA and PRA rules impose certain capital, operational and compliance requirements and allow for disciplinary action in the event of noncompliance. As with the U.S. regulatory environment, we continue to see enhanced legislative and regulatory interest regarding financial services. Key U.K. regulatory developments and trends include the following:

•Operational Resilience. Under this new U.K. regulatory requirement, in scope firms must identify their important business services, which if unavailable, could cause intolerable harm to clients, which they could not reasonably recover, or market disruption. The regulations introduce a new concept of impact tolerance and firms are also required to stress test their important business services and appoint a senior manager accountable for the regime.

•Financial Resilience. EU and U.K. regulators regulators have revised the prudential regime applying to asset managers and investment firms. This will be phased in over a five-year period and introduces a number of new concepts, including new capital requirements.

•FCA Consumer Duty. The FCA is proposing to introduce a new Consumer Duty that will set higher expectations for the standard of care that firms provide to retail consumers.

In addition, following Brexit the trade and cooperation agreement between the U.K. and EU does not include cross-border financial services. As a result, our U.K. asset management business is no longer able to market its services into the EU on a passporting basis and must now comply with local EU and country requirements as a non-EU firm, which includes leveraging our various EU-based affiliated entities (such as those in Luxembourg and the Netherlands) to provide services and marketing to EU clients and investors. We continue to actively monitor the dynamic Brexit situation and political activity around Brexit, including with respect to the continued permissibility of the delegation of asset management services from the EU to non-EU countries such as the US and UK. We have an established fund range domiciled in Luxembourg (both UCITS and Alternative Investment Funds), Ireland and the Netherlands, along with Luxembourg-based and Netherlands-based affiliated management companies. Our Luxembourg and Netherlands affiliates may perform fund management, administration and distribution functions. Therefore, we are well placed to continue to serve investors in the EU.

Pan-European and Other Non-U.S. Regulation

In addition to the above, certain of our asset management subsidiaries and branches are required to comply with pan-European directives as issued by the European Commission and adopted by EU member states. Certain of these directives have impacted and will continue to impact our global asset management business. For example, certain of our asset management subsidiaries are required to comply with the Markets in Financial Instruments Directive (“MiFID II”), Markets in Financial Instruments Regulation (“MiFIR”), Alternative Investment Fund Managers Directive (“AIFMD”), European Market Infrastructure Regulation (“EMIR”) , Undertakings for Collective Investment in Transferable Securities Directives (“UCITS”) and the Sustainable Finance Disclosure Regulation (“SFDR”) These requirements impact the way we manage assets and place, settle and report on trades for our clients, as well as market to clients and prospects. EMIR provides a framework for the regulation of over the counter and exchange-traded derivative markets. Similar to the developments in the U.S., we continue to see enhanced legislative and regulatory interest regarding financial services through international markets, including in the U.K. and EU where we have a substantial asset management business. These international rules, proposed rules, regulatory priorities or general discussions may impact us directly or indirectly, including as a regulated entity or as a service provider to, or a business receiving services from or engaging in transactions with, regulated entities. In addition to regulations noted in this section, within the EU and the U.K. we have been and will continue to address regulatory reforms or structural changes including but not limited to: enhanced regulatory focus and specific EU regulations on sustainable finance and ESG; Senior Manager and Certification Regime U.K. only); Solvency II; Packaged Retail and Insurance-based Investment Products; Market Abuse Regulation; Transparency Directive II; Fifth Money Laundering Directive; EU Benchmarks Regulation; Money Market Fund Regulation; Shareholder Rights Directive; Securitisation Regulation; and Criminal Finance Act. In addition, although the U.K. has now left the EU, the U.K. regulators may choose to implement future EU regulations and apply them in the U.K. potentially with significant variation from the EU regulations and potentially increasing the complexity and costs for our compliance.

Columbia Threadneedle companies or activities (including those we acquired as part of the BMO Global Asset Management (EMEA) business) are also subject to various local country or jurisdiction regulations and to corresponding regulators in Europe, Canada, Dubai, Hong Kong, Singapore, South Korea, South America and Australia. With our growth in the EU, including the recent acquisition of the BMO Global Asset Management (EMEA) business, we expect to have greater engagement with the Luxembourg, Irish and Dutch regulators.

Other Securities Regulation

Ameriprise Certificate Company is regulated as an investment company under the Investment Company Act. As a registered investment company, Ameriprise Certificate Company must observe certain governance, disclosure, record-keeping, operational and

marketing requirements. Ameriprise Certificate Company pays dividends to the parent company and is subject to capital requirements under applicable law and understandings with the SEC and the Minnesota Department of Commerce (Banking Division).

Ameriprise Trust Company is primarily regulated by the Minnesota Department of Commerce (Banking Division) and is subject to capital adequacy requirements under Minnesota law. It is prohibited from accepting deposits or making personal or commercial loans. As a provider of products and services to tax-qualified retirement plans and IRAs, certain aspects of our business, including the activities of our trust company, fall within the compliance oversight of the DOL and the Department of Treasury, particularly regarding the enforcement of ERISA, and the tax reporting requirements applicable to such accounts. Ameriprise Trust Company, as well as our investment adviser subsidiaries, may be subject to ERISA, and the regulations thereunder, insofar as they act as a “fiduciary” under ERISA with respect to certain ERISA clients.

Insurance Regulation

Our insurance subsidiaries are subject to supervision and regulation by states and other territories where they are domiciled or otherwise licensed to do business. These regulations impact our Retirement & Protection Solutions segment and our closed-blocks included in Corporate & Other segment. The primary purpose of this regulation and supervision is to protect the interests of contract holders and policyholders. In general, state insurance laws and regulations govern standards of solvency, capital requirements, the licensing of insurers and their agents, premium rates, policy forms, the nature of and limitations on investments, periodic reporting requirements and other matters. In addition, state regulators conduct periodic examinations into insurer market conduct and compliance with insurance and securities laws. The Minnesota Department of Commerce, and the New York State Department of Financial Services (the “Domiciliary Regulators”) regulate certain of the RiverSource Life companies. In addition to being regulated by their Domiciliary Regulators, our RiverSource Life companies are regulated by each of the insurance regulators in the states where each is authorized to transact business. Financial regulation of our RiverSource Life companies is extensive, and their financial transactions (such as intercompany dividends and investment activity) may be subject to pre-approval and/or continuing evaluation by the Domiciliary Regulators.

Aspects of the regulation applicable to our Advice & Wealth Management segment also apply to our Retirement & Protection Solutions segment and the closed blocks in our Corporate & Other segment. For example, RiverSource Distributors is registered as a broker-dealer for the limited purpose of acting as the principal underwriter and/or distributor for our RiverSource annuities and insurance products sold through Ameriprise Financial Services, LLC (“AFS”) and third-party channels. Additionally, ERISA, the SEC’s best interest standards, state and other fiduciary or best interest rules, as well as other similar standards and any rulemaking from the DOL are relevant to our insurance and annuities business or products. We continue to review and analyze the potential impact of these regulations across each of our business lines.

All states require participation in insurance guaranty associations, which assess fees (subject to statutory limits) to insurance companies in order to fund claims of policyholders and contract holders of insolvent insurance companies. These assessments are generally based on a member insurer’s proportionate share of all premiums written by member insurers in the state during a specified period prior to an insurer’s insolvency. See Note 26 to our Consolidated Financial Statements included in Part II, Item 8 of this Annual Report on Form 10-K for additional information regarding guaranty association assessments.

Certain variable annuity and variable life insurance contracts offered by the RiverSource Life companies, and certain separate accounts supporting such contracts, constitute and are registered as securities under the Securities Act of 1933 and as investment companies under the Investment Company Act of 1940, as amended. As such, these products are subject to regulation by the SEC and FINRA.

The Federal Insurance Office (“FIO”) within the U.S. Department of Treasury does not have substantive regulatory responsibilities, though it is tasked with monitoring the insurance industry and the effectiveness of its regulatory framework in addition to providing periodic reports to the President and Congress. We monitor the FIO’s activity to identify and assess emerging regulatory priorities with potential application to our business.

Each of our insurance subsidiaries is subject to risk-based capital (“RBC”) requirements designed to assess the adequacy of an insurance company’s total adjusted capital in relation to its investment, insurance and other risks. The National Association of Insurance Commissioners (“NAIC”) has established RBC standards that all state insurance departments have adopted. The RBC requirements are used by the NAIC and state insurance regulators to identify companies that merit regulatory actions designed to protect policyholders. The NAIC RBC report is completed as of December 31 and filed annually, along with the statutory financial statements.

Our RiverSource Life companies are subject to various levels of regulatory intervention if their total adjusted statutory capital falls below defined RBC action levels. At the “company action level,” defined as total adjusted capital level between 100% and 75% of the RBC requirement, an insurer must submit a plan for corrective action with its primary state regulator. The level of regulatory intervention is greater at lower levels of total adjusted capital relative to the RBC requirement. RiverSource Life and RiverSource Life of NY maintain capital levels well in excess of the company action level required by state insurance regulators as noted below as of December 31, 2021:

| | | | | | | | | | | | | | | | | | | | |

| Entity | | Company Action Level RBC | | Total Adjusted Capital | | % of Company Action Level RBC |

| | (in millions, except percentages) |

| RiverSource Life | | $ | 502 | | | $ | 3,419 | | | 681 | % |

| RiverSource Life of NY | | $ | 42 | | | $ | 310 | | | 741 | % |

Ameriprise Financial, as a direct and indirect owner of its insurance subsidiaries, is subject to the insurance holding company laws of Minnesota and New York (the states where its insurance subsidiaries are domiciled). These laws generally require insurance holding companies to register with the insurance department of the insurance company’s state of domicile and to provide certain financial and other information about the operations of the companies within the holding company structure.

As part of its Solvency Modernization Initiative, in 2010 the NAIC adopted revisions to its Insurance Holding Company System Regulatory Act (“Holding Company Act”) to enhance insurer group supervision and create a new Risk Management and Own Risk and Solvency Assessment (“ORSA”) Model Act. The Holding Company Act revisions focus on the overall insurance holding company system, establish a framework of regulator supervisory colleges, enhancements to corporate governance, and require the annual filing of an Enterprise Risk Management Report. The ORSA Model Act requires that an insurer create and file, annually, its Own Risk Solvency Assessment, which is a complete self-assessment of its risk management functions and capital adequacy. These laws were enacted by the domiciliary states of RiverSource Life: Minnesota and New York. We completed and filed these reports as required by the laws and regulations of those states.

Federal Banking and Financial Holding Company Regulation

Ameriprise Bank is subject to regulation by the Office of the Comptroller of the Currency (“OCC”), which is the primary regulator of federal savings banks, and by the Federal Deposit Insurance Corporation (“FDIC”) in its role as insurer of Ameriprise Bank's deposits. As a federally chartered savings bank, Ameriprise Bank is subject to numerous rules and regulations governing all aspects of the banking business, including lending practices and transactions with affiliates. Ameriprise Bank is also subject to specific capital rules and limits on capital distributions, including payment of dividends. If Ameriprise Bank's capital falls below certain levels, the OCC would be required to take remedial actions and could take other actions, including imposing further limits on dividends or business activities. In addition, an array of Community Reinvestment Act (“CRA”), fair lending and other consumer protection laws and regulations apply to Ameriprise Bank.