UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-05349

Goldman Sachs Trust

(Exact name of registrant as specified in charter)

71 South Wacker Drive, Chicago, Illinois 60606

(Address of principal executive offices) (Zip code)

Copies to:

| Caroline Kraus, Esq. | Stephen H. Bier, Esq. | |

| Goldman Sachs & Co. LLC | Dechert LLP | |

| 200 West Street | 1095 Avenue of the Americas | |

| New York, New York 10282 | New York, NY 10036 |

(Name and address of agents for service)

Registrant’s telephone number, including area code: (312) 655-4400

Date of fiscal year end: October 31

Date of reporting period: October 31, 2021

| ITEM 1. | REPORTS TO STOCKHOLDERS. |

The Annual Report to Shareholders is filed herewith. |

Goldman Sachs Funds

| Annual Report | October 31, 2021 | |||

Dividend Focus Funds | ||||

Income Builder | ||||

Rising Dividend Growth | ||||

Goldman Sachs Dividend Focus Funds

| ∎ | INCOME BUILDER |

| ∎ | RISING DIVIDEND GROWTH |

Portfolio Management Discussion and Performance Summary — Income Builder | 1 | |||

Portfolio Management Discussion and Performance Summary — Rising Dividend Growth | 10 | |||

| 21 | ||||

| 43 | ||||

| 46 | ||||

| 46 | ||||

| 52 | ||||

| 59 | ||||

| 79 | ||||

| 80 | ||||

| NOT FDIC-INSURED | May Lose Value | No Bank Guarantee | ||

FUND RESULTS

Goldman Sachs Income Builder Fund

Investment Objective

The Fund seeks to provide income and capital appreciation.

Portfolio Management Discussion and Analysis

Below, the Goldman Sachs Fundamental Equity Team, the Goldman Sachs Fixed Income Investment Management Team, and the Goldman Sachs Multi-Asset Solutions (“MAS”) Group (formerly, the Goldman Sachs Global Portfolio Solutions Group), collectively the Goldman Sachs Income Builder Team (the “Income Builder Team”), discuss the Goldman Sachs Income Builder Fund’s (the “Fund”) performance and positioning for the 12-month period ended October 31, 2021 (the “Reporting Period”).

| Q | How did the Fund perform during the Reporting Period? |

| A | During the Reporting Period, the Fund’s Class A, Class C, Institutional, Investor, Class R6 and Class P Shares generated 18.90%, 18.01%, 19.29%, 19.22%, 19.35% and 19.31%, respectively. These returns compare to the 43.76% and 9.05% average annual total returns of the Russell 1000® Value Index (with dividends reinvested) (the “Russell Index”) and the ICE BofAML BB to B US High Yield Constrained Index (the “ICE BofAML Index”), respectively, during the same period. |

The Fund is a dynamically-managed multi-asset class portfolio with a baseline allocation of 60% to fixed income securities and 40% to equity securities. In seeking to meet its investment objective, the Fund has the flexibility to opportunistically tilt the allocation to fixed income and equity securities up to 15% above or below that baseline allocation. The Fund seeks to provide a high and stable income stream plus capital appreciation, with lower volatility than the equity market. The percentage of the portfolio invested in equity and fixed income securities will vary from time to time as the Income Builder Team evaluates such securities’ relative attractiveness based on, among other factors, income opportunities, market valuations, economic growth and inflation prospects. |

Because of these stated goals of the Fund, the Income Builder Team believes the returns of the Russell Index and the ICE BofAML Index should be considered for reference only. |

| Q | What was the Fund’s 12-month distribution rate and what was its 30-Day SEC yield during the Reporting Period? |

| A | During the Reporting Period, the Fund’s Class A, Class C, Institutional, Investor, Class R6 and Class P Shares provided 12-month distribution rates of 3.04%, 2.36%, 3.27%, 3.20%, 3.27% and 3.28%, respectively. (The 12-month distribution rate is calculated by taking the sum of all cash distributions to shareholders over the past 12 months and dividing this sum by the Fund’s month-end net asset value (“NAV”) for the last month of the period. This rate includes capital gain distributions, if any. This is not an SEC yield.) On October 31, 2021, the Fund’s 30-Day Standardized Subsidized SEC yields for its Class A, Class C, Institutional, Investor, Class R6 and Class P Shares were 2.49%, 1.89%, 2.96%, 2.88%, 2.97% and 2.97%, respectively. (The 30-Day Standardized Subsidized SEC Yield is calculated in accordance with SEC regulations and is determined by dividing the Fund’s net investment income per share earned over the 30-day period by the Fund’s maximum public offering price per share on the last day of such period, which figure is then annualized. The 30-Day Standardized Subsidized SEC Yield may differ from the distribution rate because of the exclusion of distributed capital gains. The 30-Day Standardized Subsidized SEC Yield reflects any fee waivers and/or expense reimbursements in effect during the period, without which the yield would be reduced.) |

| Q | What economic and market factors most influenced the Fund during the Reporting Period? |

| A | During the Reporting Period, an economic recovery from the depths of the COVID-19 pandemic as well as continued fiscal stimulus and ongoing accommodative monetary policies from global central banks and governments most influenced the financial markets and the Fund. |

In November and December 2020, when the Reporting Period started, U.S. equities rallied, extending a broad-based recovery from steep first quarter 2020 declines, on the prospect of an end to the global COVID-19 pandemic and its weighted economic impact following the approval and |

1

FUND RESULTS

| distribution of multiple COVID-19 vaccines. While uncertainty surrounding the U.S. elections and other policy questions created the potential for higher market volatility, the Democrat victory proved positive for equity markets. Further, after a historically sharp but short recession during the spring of 2020, many major economies, including the U.S., entered an early-cycle phase of recovery. Employment conditions improved, as temporary job losses were regained and U.S. manufacturing activity recovered. Despite this improvement, reminders of a COVID-19 ceiling for those industries hit hardest by pandemic-related restrictions persisted. In the fixed income markets, performance was bolstered by the development of COVID-19 vaccines and the beginning of immunizations despite steadily rising cases and renewed lockdowns. Investor risk sentiment was also supported by the removal of a few long-standing overhangs. Specifically, U.S. elections were resolved, the U.K. and European Union agreed to a post-Brexit deal, and another round of fiscal stimulus was provided by the U.S. federal government. (Brexit refers to the U.K.’s exit from the European Union.) |

During the first quarter of 2021, U.S. equities added to their gains, while spread (or non-government bond) sector performance was largely negative. Rising bond yields and a value-led equity market dominated these months. Two key drivers of performance were the Democrat victories in Georgia during January 2021, which paved the way for massive additional U.S. fiscal stimulus, and progress in the COVID-19 vaccine rollout. The accelerating rollout of COVID-19 vaccines boosted investors’ hopes of a sustainable reopening of the U.S. economy. To varying degrees, central banks around the world leaned against market expectations for earlier than previously expected policy normalization, indicating their respective policies would remain accommodative despite improvements in economic growth, given weak underlying inflation dynamics. |

During the second calendar quarter, U.S. equities and spread sectors recorded positive returns overall. Discussions during these months centered on the central bank liquidity tailwind, fiscal stimulus, COVID-19 vaccine rollout progress, economic reopening momentum and strong corporate profits. In May, remarkably strong U.S. inflation data, coupled with the release of a disappointing April U.S. jobs report, suggested that pandemic-related dynamics, such as temporary supply shortages, were likely to continue distorting economic data in the near term. This led to a recalibration of investors’ economic growth expectations, though the reassessment may also have reflected concerns about the spreading COVID-19 Delta variant and the potential of a sooner than consensus anticipated withdrawal of U.S. Federal Reserve (the “Fed”) policy support. Indeed, in June, Fed officials indicated they were mindful of increases in inflation and inflation expectations. |

U.S. equities increased modestly in the third quarter of 2021. In July and August, the rally continued, as the market’s focus remained on easy financial conditions, accommodative monetary policy, pent-up consumer demand, positive corporate earnings sentiment, resilient operating margins, corporate buybacks and equity inflows. Some economic indicators, including higher inflation and lower than consensus expected retail sales and manufacturing activity, were causes of concern among investors, though the market and the Fed remained largely optimistic. However, sentiment deteriorated in September 2021, as the spread of the COVID-19 Delta variant dampened economic reopening momentum and the Fed signaled for a slowdown of its asset purchases. In the fixed income markets, spread sectors were challenged by ongoing concerns about the spread of the Delta variant, especially in countries with low levels of vaccination, and the potential impact on the global economic recovery. |

In October, U.S. equities produced their best monthly gain of 2021 to date, propelled by the third calendar quarter corporate earnings season. Spread sector performance, however, was rather flat. On the economic front, inflation rose, the Institute for Supply Management’s manufacturing and services indices both beat consensus expectations, and job market data was mixed, with September’s nonfarm payroll growth significantly lower than August’s but initial jobless claims falling. On the policy front, the Fed’s narrative on inflation shifted from “transitory” to “more persistent.” |

For the Reporting Period overall, U.S. large-cap equities, as measured by the S&P 500® Index, generated double-digit gains. Value stocks, as measured by the Russell Index, also produced double-digit gains. The fixed income markets, led by high yield corporate bonds, recorded positive returns during the Reporting Period overall. |

| Q | What was the Fund’s asset allocation positioning during the Reporting Period, and what effect did it have on performance? |

| A | At the beginning of the Reporting Period, the Fund was invested 63.4% in fixed income and 40.9% in equities. This breakout is inclusive of derivatives exposure in both asset classes but does not necessarily include the cash to support those positions. Derivatives positions are mostly supported by cash held in the Fund specifically to cover its exposure and any potential margin calls or future losses experienced. |

2

FUND RESULTS

During the Reporting Period, the Fund’s duration positioning remained consistent at about three years, increasing to between 3.1 and 3.2 years near the end of the Reporting Period. (Duration is a measure of the Fund’s sensitivity to changes in interest rates.) Regarding yield curve positioning, in June 2021, the Income Builder Team established a U.S. yield curve steepener, wherein the Fund held a short position in 30-year U.S. Treasury futures and a long position in five-year U.S. Treasury futures. (Yield curve is a spectrum of interest rates based on maturities of varying lengths. A steepening position seeks to take advantage of a widening differential between yields at the shorter- and longer-term ends of a range of maturities.) The Income Builder Team eliminated the Fund’s yield curve steepener at the end of the Reporting Period. During the Reporting Period overall, the duration positioning strategy detracted from the Fund’s performance, though these results were somewhat mitigated by the tactical decision to maintain a modest short duration position relative to the Fund’s history. The U.S. yield curve steepener also detracted from the Fund’s performance during the Reporting Period. |

The Fund’s fixed income allocation remained rather consistent throughout the Reporting Period, with the Income Builder Team actively managing allocations at the security level and in terms of credit quality. Overall, the Fund’s exposure to investment grade corporate bonds was moderately reduced, while exposure to high yield corporate bonds and bank loans was maintained. The Fund’s fixed income allocation added to returns during the Reporting Period. |

Regarding the Fund’s equity allocation, the Income Builder Team increased exposure to the financials and consumer staples sectors and decreased exposure to the communication services and industrials sectors during the Reporting Period. Within financials, we increased the Fund’s exposure to European bank stocks, which we accomplished through a small allocation to EURO STOXX® Banks futures, during November 2020. In our view, European bank stocks were undervalued, and we thought the European Central Bank would lift its ban on dividend payments in the near term. During February 2021, we expressed a pro-cyclical relative value view using a basket of high-beta stocks with a large-cap focus and diversified sector exposure that we believed would provide the Fund with attractive risk-return characteristics as the U.S. economy continued to recover from the COVID-19 shock. (High beta stocks are those that tend to be more volatile than the broad equity market.) Assets correlated to an economic recovery were likely to outperform, in our opinion. Furthermore, we thought that equities, especially cyclical stocks and small-cap stocks, were poised for a strong multi-year rally, driven by a significant reduction in political uncertainty and an increased probability of faster COVID-19 relief, along with other fiscal policy support from the U.S. federal government (i.e., infrastructure spending). We funded our pro-cyclical relative value view by reducing the Fund’s position in S&P 500® Index futures. Finally, during July 2021, as equity markets reached new highs, we resumed selling equity index call options on U.S. large-cap stocks and European large-cap stocks in an effort to generate additional cash flow and mitigate potential downside risk for the Fund. (A call option is an option that gives the holder the right to buy a certain quantity of an underlying security at an agreed-upon price at the time of expiry.) During the Reporting Period overall, the Fund’s allocation to EURO STOXX® Banks futures added significantly to its performance. Although the Fund’s investment in a basket of high-beta stocks bolstered returns, these positive results were more than offset by our decision to fund that position by decreasing the Fund’s position in S&P 500® Index futures, which dampened performance as the broad U.S. equity market rallied. Finally, the Fund’s equity index call writing detracted slightly from performance during the Reporting Period overall. |

At the end of the Reporting Period, the Fund was invested 56.5% in fixed income and 41.9% in equities, with the balance in cash and cash equivalents. The decrease in the fixed income exposure was driven primarily by the timing of Fund rebalancing rather than by a strategic change in the Fund’s asset allocation positioning. |

| Q | What key factors had the greatest impact on the performance of the Fund’s fixed income allocation during the Reporting Period? |

| A | During the Reporting Period, the Fund’s fixed income allocation recorded positive returns. Positions in high yield corporate bonds and bank loans added most to performance, with exposures to emerging markets debt further bolstering returns. Although holdings of U.S. investment grade corporate bonds had a positive impact on performance, the contribution was relatively muted compared to the gains produced by the Fund’s positions in high yield corporate bonds. |

| Q | Were any significant purchases or sales made within the fixed income allocation of the Fund during the Reporting Period? |

| A | During the Reporting Period, the Fund established a position in Transocean high yield corporate bonds. Our fundamental research indicated these securities were undervalued and the market was pricing in increased risks around the drilling company’s near-term liabilities. Ultimately, Transocean |

3

FUND RESULTS

| refinanced its debt and pushed out most of its near-term liabilities, which exceeded our optimistic case. These efforts led to a rally in the company’s bonds. |

Among other notable purchases during the Reporting Period were the high yield corporate bonds of Summit Midstream Holdings, LLC, which owns and operates midstream1 energy infrastructure assets. Our fundamental research led us to believe the company has multiple avenues to unlock shareholder value and deleverage its balance sheet, specifically through contracted earnings, a supportive commodity environment and a capable management team. |

Among positions exited was the Fund’s investment in the high yield corporate bonds of Carnival, the world’s largest cruise operator with more than 100 cruise ships. The company provided a mixed update for the third quarter of 2021, with good underlying operational performance offset by weakness in near-term bookings because of the public’s COVID-19 Delta variant concerns. In our opinion, the market had fully priced in the company’s recovery and, therefore, we saw limited upside potential. |

During the Reporting Period, the Fund also exited its investment in the high yield corporate bonds of MultiPlan, a leading provider of end-to-end cost containment solutions to U.S. health care companies. We were wary about the risks associated with new regulatory changes that could have a negative impact on the company’s revenues. |

| Q | What changes were made to the Fund’s fixed income allocation during the Reporting Period? |

| A | As mentioned previously, we moderately reduced the Fund’s exposure to investment grade corporate bonds during the Reporting Period. We maintained its exposure to high yield corporate bonds and bank loans. In our view, high yield corporate bonds continued to offer compelling risk-adjusted carry opportunities compared to other spread sectors. (In this context, carry refers to the yield advantage associated with high yield corporate bonds.) Furthermore, persistent investor demand for higher yielding assets, improved corporate fundamentals due to pent-up consumer demand and access to the capital markets had created a healthy technical environment for high yield corporate bonds. Within high yield corporate bonds, we increased the Fund’s exposure to the consumer cyclical market segment, as we expected the global economic backdrop to remain strong. We also increased the Fund’s exposure to the energy market segment, as we expected these credits to benefit from rising energy prices. Conversely, we decreased the Fund’s exposure to the health care market segment, largely due to idiosyncratic issues such as litigation, pricing legislation and heightened regulatory scrutiny. We also decreased the Fund’s exposure to the automotive market segment given ongoing supply constraints. Regarding bank loans, we believed those securities were likely to benefit from a number of favorable dynamics, including higher recovery rates compared to high yield corporate bonds, a comparatively lower default rate and some resiliency from inflationary pressures. |

| Q | What key factors had the greatest impact on the performance of the Fund’s equity allocation during the Reporting Period? |

| A | During the Reporting Period, the Fund’s equity allocation generated positive returns, with stock selection in the financials, industrials and health care sectors adding to performance. Investments in the utilities, consumer staples and communication services sectors detracted from results. |

| Q | Which stocks contributed most to the Fund’s performance during the Reporting Period? |

| A | The Fund benefited during the Reporting Period from its positions in Eli Lilly and Company, JPMorgan Chase and Cisco Systems. |

Eli Lilly and Company, a leading pharmaceutical company with a history of innovation and a strong drug pipeline, added most to the Fund’s performance during the Reporting Period. Its shares benefited from the strong results of the company’s Alzheimer’s drug as well as from robust earnings that beat market expectations. At the end of the Reporting Period, we remained optimistic about the stock, as the company continued to demonstrate accelerating top-line revenue growth due to drug launches and increased margins growth. |

JPMorgan Chase, a global financial services company, reported strong earnings with record low credit losses during the Reporting Period. At the end of the Reporting Period, we had a positive view of the company’s ability to continue to grow loans and gain market share. In addition, we were encouraged by its management’s continued focus on using technology to reduce costs and improve efficiencies across business lines and to potentially implement crypto-currency strategies. At the end of the Reporting Period, we also had a favorable view of JPMorgan Chase’s business outlook and continued to find the stock compelling from a risk-reward perspective. |

| 1 | The midstream component of the energy industry is usually defined as those companies providing products or services that help link the supply side, i.e., energy producers, and the demand side, i.e., energy end-users, for any type of energy commodity. Such midstream businesses can include, but are not limited to, those that process, store, market and transport various energy commodities. |

4

FUND RESULTS

Cisco Systems, a communications and information technology company, was another notable contributor to the Fund’s performance during the Reporting Period. At the end of the Reporting Period, we had a positive view of Cisco Systems’ efforts to transition its business model toward more recurring and/or durable income streams, which we thought might lead to better than consensus expected multiples expansion. We also believed the company was well positioned to benefit from the cyclical economic recovery. |

| Q | Which stocks detracted significantly from the Fund’s performance during the Reporting Period? |

| A | During the Reporting Period, the major detractors from Fund performance were AT&T, Coca-Cola Europacific Partners Plc and McCormick & Company. |

AT&T, a multinational telecommunications company, detracted most from the Fund’s returns during the Reporting Period. Its shares suffered on news AT&T would spin off WarnerMedia’s assets and combine them with Discovery Communications into a stand-alone company. Although there was investor skepticism about the spin-off, we believed AT&T’s scale and global footprint would allow the company to launch a successful OTT platform in the future. (OTT, or over-the-top media service, is a media service offered directly to viewers via the Internet.) In addition, we thought AT&T’s new lower dividend would be more sustainable, based on the company’s projected free cash flow, than its prior dividend. |

Coca-Cola European Partners Plc is a U.K.-headquartered bottling company. Its shares were challenged during the Reporting Period by the company’s cautious forward guidance based on its management’s concerns about cooler weather and renewed COVID-19 restrictions. At the end of the Reporting Period, we remained constructive on the business’ longer-term prospects as consumers continue to recover from the COVID-19-induced recession. In our view, Coca-Cola European Partners remained a well-run company with a prudent and shareholder friendly management team. |

McCormick & Company (“McCormick”) manufactures, markets and distributes spices. Supply chain and inflationary pressures had a negative impact on the company’s margins and sales during the Reporting Period. Although demand for McCormick’s products stayed strong, we believed cost pressures might impact margins in the near term. That said, McCormick has a track record of passing through costs over time, and given its strong competitive position, we expected the company to weather inflationary pressures better than most other packaged food companies. We continued to favor the stock at the end of the Reporting Period due in part to McCormick’s comparatively higher pricing power. |

| Q | Were any significant purchases or sales made within the equity allocation of the Fund during the Reporting Period? |

| A | During the Reporting Period, the Fund initiated positions in Bank of America and Nordea Bank. We believed banks would broadly benefit from rising interest rates through increased profit margins. In addition, we thought Bank of America had a strong balance sheet and a well-covered dividend. As for Finland-based Nordea Bank, we were encouraged by its strong growth across Nordic countries and what we viewed as its quality income growth. |

Among sales completed during the Reporting Period was the Fund’s position in Verizon Communications, which we eliminated to fund an investment in AT&T. In our view, AT&T had a more attractive return profile than Verizon Communications because of the spin-off of WarnerMedia. Additionally, we favored AT&T over Verizon Communications due to the AT&T management team’s approach toward value creation rather than Verizon’s approach, which we considered “empire building.” (Empire building is attempting to increase the size and scope of a company’s power and influence wherein managers or executives seem more concerned with expansion (i.e., acquisition of competitors) than they are with developing and implementing ways to benefit shareholders.) |

The Fund also exited its position in Comcast during the Reporting Period. We thought the company’s merger and acquisition activity might be destructive to the stock’s value, as its management team has a history of what we viewed as “empire building,” and there was press speculation about the potential purchase of significant media assets. We decided the risk was too high and decided to eliminate the Fund’s position in the stock. |

| Q | What changes were made to the Fund’s equity market sector weightings during the Reporting Period? |

| A | As mentioned previously, we increased the Fund’s exposures to the financials and consumer staples sectors during the Reporting Period. In the financials sector, we preferred high-quality diversified companies over pure asset management companies. We reduced the Fund’s exposures to the communication services and industrials sectors. In the case of communication services, the Fund’s decrease in exposure was largely the result of stock-specific sales. |

| Q | How did the Fund use derivatives and similar instruments during the Reporting Period? |

| A | During the Reporting Period, the Income Builder Team wrote equity index options in an effort to generate additional |

5

FUND RESULTS

| cash flow and potentially reduce volatility (negative impact on performance). In addition, equity index futures were employed to gain passive exposure to European bank stocks and the broad U.S. equity market (each had a positive impact). Total return swaps were used within a pro-cyclical tactical view that sought to provide the Fund with attractive risk-return characteristics as the U.S. economy continued to recover from the COVID-19 shock (positive impact). Interest rate swaps and U.S. Treasury futures were utilized as cost-efficient instruments to provide greater precision and versatility in the management of duration (each had a negative impact). U.S. Treasury futures were also employed to facilitate specific yield curve strategies (negative impact). To hedge against currency risk (that is, the risk that certain currencies might fluctuate in value), the Fund employed currency forwards (neutral impact). Credit default swaps were used to implement specific credit-related investment strategies (neutral impact) during the Reporting Period. |

| Q | Were there any changes to the Fund’s portfolio management team during the Reporting Period? |

| A | Effective May 24, 2021, Christopher Lvoff no longer served as a portfolio manager of the Fund, and Neill Nuttall became a portfolio manager of the Fund. (Effective January 3, 2022, after the end of the Reporting Period, Alexandra Wilson-Elizonda is expected to become a portfolio manager of the Fund.) By design, all investment decisions for the Fund are performed within a team structure, with multiple subject matter experts. This strategic decision making has been the cornerstone of our approach and ensures continuity in the Fund. At the end of the Reporting Period, Ashish Shah, Ron Arons, Collin Bell, Charles “Brook” Dane and Neill Nuttall served as portfolio managers of the Fund. |

| Q | What is the Income Builder Team’s tactical view and strategy for the months ahead? |

| A | At the end of the Reporting Period, the Income Builder Team remained optimistic, yet vigilant, about the overall strength of the global economy. Although we thought the recovery was likely to slow in the near term relative to its pace during the Reporting Period, we expected the global economic growth backdrop would remain strong due to high consumer savings rates, a favorable inventory cycle and new developments that would help in the fight against COVID-19. In our view, the pace of economic growth would be determined by whether supply constraints on goods and labor ease rather than by whether demand grows. Although inventory scarcity had driven goods price inflation to high levels by the end of the Reporting Period, we expected inventories to stabilize and goods price inflation to diminish in 2022. We noted that U.S. producers had reported the main obstacles to meeting demand were shortages of critical inputs and labor, not insufficient plant and equipment, and we thought 2022 should see meaningful progress on resolving input shortages, labor shortages and shipping delays. |

Regarding equities, we planned to stay true to our quality-first investment approach and seek to invest in businesses with healthy balance sheets, relatively stable cash flows and differentiated business models aligned to secular tailwinds. We intended to continue re-evaluating our assumptions and to stay focused on the long-term investment horizon. In our opinion, this fundamental approach can generate excess return in the long run for investors. Overall, we believed income-oriented equities had lower risk relative to other segments of the equity market because their underlying companies generally have higher and more predictable cash flows. We also thought income-oriented equities had less exposure to U.S. government risk, as their underlying businesses tend to produce substantial domestic revenues and might not be significantly affected by higher corporate taxes since many of them do not pay taxes and some (e.g., real estate investment trusts, master limited partnerships and utilities) pass through taxes to investors. In addition, at the end of the Reporting Period, we believed select sectors, such as utilities and transportation infrastructure, might benefit from the U.S. government’s increased fiscal spending. Lastly, while income-oriented equities are generally more volatile than fixed income, we thought such volatility could be mitigated using call writing, and many investors may have more duration and credit risk than in the past, which may make the risk associated with volatility smaller than it has been in the past. |

As for fixed income, we believed at the end of the Reporting Period that the Fund would remain resilient to inflationary risks. The Fund’s fixed income holdings were largely composed of credits with the ability to pass through price increases in an inflationary environment. Overall, we thought our fundamental approach had been verified by strong earnings momentum and earnings guidance from companies represented in the Fund. In the near term, we planned to continue positioning the Fund to perform well even in an environment where global economic growth may decelerate to more normalized levels by shifting its investments toward non-cyclical market segments and by reducing its exposure to lower quality market segments, such as CCC-rated credits. We believed the potential risks to such positioning would be a sharp deceleration in economic growth, a sustained increase in inflation expectations and/or a more hawkish Fed. (Hawkish tends to imply higher interest rates; opposite of dovish.) We remained cognizant of these risks at the end of the Reporting Period and intended to focus on issuers we thought would be resilient against these factors. |

6

FUND BASICS

Income Builder Fund

as of October 31, 2021

| TOP TEN EQUITY HOLDINGS AS OF 10/31/21‡ | ||||||||

| Holding | % of Net Assets | Line of Business | ||||||

| JPMorgan Chase & Co. | 1.4 | % | Banks | |||||

| Schneider Electric SE ADR | 0.9 | Electrical Equipment | ||||||

| Bank of America Corp. | 0.9 | Banks | ||||||

| Johnson & Johnson | 0.8 | Pharmaceuticals | ||||||

| UnitedHealth Group, Inc. | 0.8 | Health Care Providers & Services | ||||||

| Nordea Bank Abp ADR | 0.8 | Banks | ||||||

| Medtronic PLC | 0.8 | Health Care Equipment & Supplies | ||||||

| Chevron Corp. | 0.7 | Oil, Gas & Consumable Fuels | ||||||

| AT&T, Inc. | 0.7 | Diversified Telecommunication Services | ||||||

| Cisco Systems, Inc. | 0.7 | Communications Equipment | ||||||

| ‡ | The top 10 holdings may not be representative of the Fund’s future investments. |

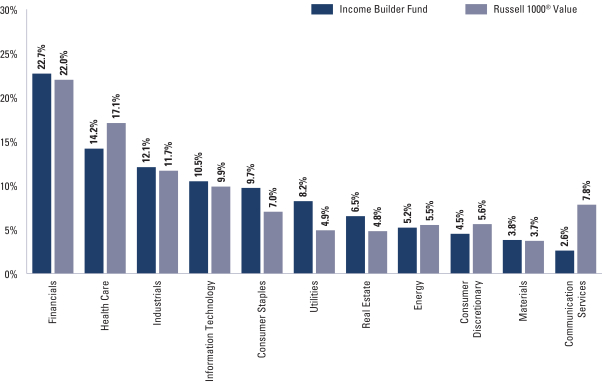

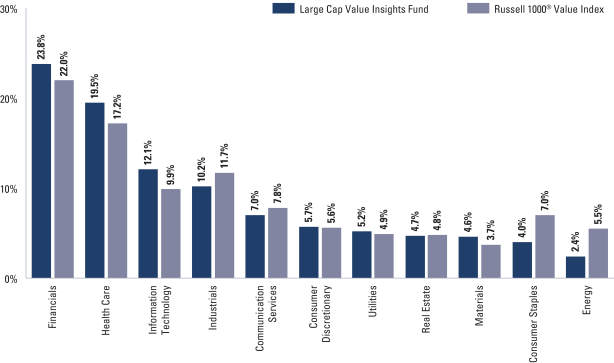

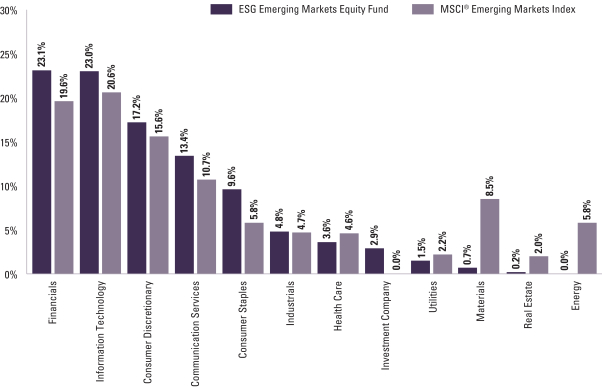

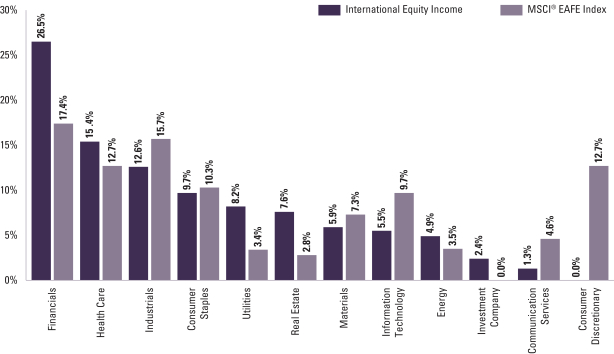

| FUND’S EQUITY SECTOR ALLOCATIONS VS. BENCHMARK† | ||||||

| As of October 31, 2021 | ||||||

| † | The Fund is actively managed and, as such, its composition may differ over time. Consequently, the Fund’s overall sector allocations may differ from the percentages contained in the graph above. The graph categorizes investments using the Global Industry Classification Standard (“GICS”), however, the sector classifications used by the portfolio management team may differ from GICS. The percentage shown for each investment category reflects the value of investments in that category as a percentage of the total value of the Fund’s Equity investments. The graph depicts the Fund’s investments but may not represent the Fund’s market exposure due to the exclusion of certain derivatives, if any, as listed in the Additional Investment Information section of the Schedule of Investments. |

7

FUND BASICS

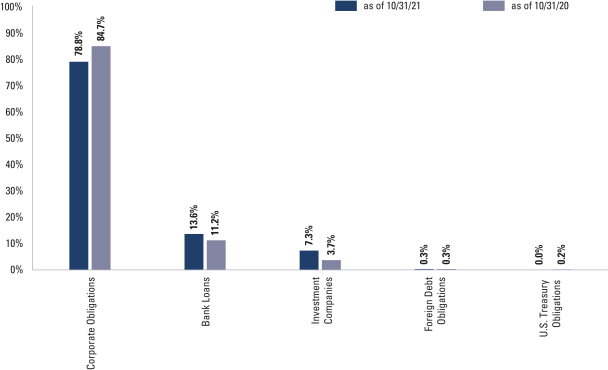

| FUND’S FIXED INCOME COMPOSITION† |

| † | The percentage shown for each investment category reflects the value of investments in that category as a percentage of the Fund’s Fixed Income investments. The graph depicts the Fund’s investments but may not represent the Fund’s market exposure due to the exclusion of certain derivatives, if any, as listed in the Additional Investment Information section of the Schedule of Investments. |

For more information about your Fund, please refer to www.GSAMFUNDS.com. There, you can learn more about your Fund’s investment strategies, holdings, and performance.

8

GOLDMAN SACHS INCOME BUILDER FUND

Performance Summary

October 31, 2021

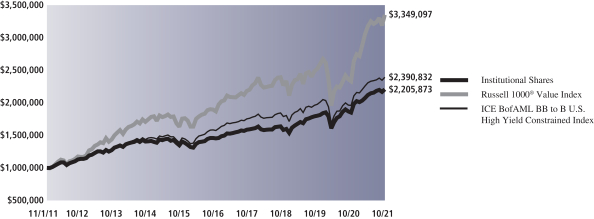

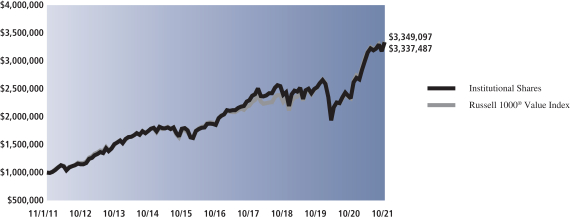

The following graph shows the value, as of October 31, 2021, of a $1,000,000 investment made on November 1, 2011 in Institutional Shares. For comparative purposes, the performance of the Fund’s current benchmarks, the Russell 1000® Value Index and the ICE BofAML BB to B U.S. High Yield Constrained Index, are shown. Performance reflects applicable fee waivers and/or expense limitations in effect during the periods shown and in their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The returns set forth below represent past performance. Past performance does not guarantee future results. The Fund’s investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted below. Please visit our web site at www.GSAMFUNDS.com to obtain the most recent month-end returns.

| Income Builder Fund’s 10 Year Performance |

Performance of a $1,000,000 Investment, with distributions reinvested, from November 1, 2011 through October 31, 2021.

| Average Annual Total Return through October 31, 2021* | One Year | Five Years | Ten Years | Since Inception | ||||||||||

Class A | ||||||||||||||

Excluding sales charges | 18.90% | 8.30% | 7.80% | — | ||||||||||

Including sales charges | 12.37% | 7.08% | 7.19% | — | ||||||||||

| ||||||||||||||

Class C | ||||||||||||||

Excluding contingent deferred sales charges | 18.01% | 7.50% | 7.00% | — | ||||||||||

Including contingent deferred sales charges | 16.98% | 7.50% | 7.00% | — | ||||||||||

| ||||||||||||||

Institutional | 19.29% | 8.71% | 8.23% | — | ||||||||||

| ||||||||||||||

Investor | 19.22% | 8.57% | 8.07% | — | ||||||||||

| ||||||||||||||

Class R6 (Commenced July 31, 2015) | 19.35% | 8.73% | N/A | 7.20% | ||||||||||

| ||||||||||||||

Class P (Commenced April 16, 2018) | 19.31% | N/A | N/A | 9.45% | ||||||||||

| ||||||||||||||

| * | These returns assume reinvestment of all distributions at NAV and reflect a maximum initial sales charge of 5.50% for Class A and the assumed contingent deferred sales charge for Class C Shares (1% if redeemed within 12 months of purchase). Because Institutional, Investor, Class R6 and Class P Shares do not involve a sales charge, such a charge is not applied to their Average Annual Total Return. |

9

FUND RESULTS

Goldman Sachs Rising Dividend Growth Fund

Investment Objective

The Fund seeks long-term growth of capital and current income.

Portfolio Management Discussion and Analysis

Below, the Goldman Sachs Quantitative Investment Strategies (“QIS”) portfolio management team, the Goldman Sachs Global Portfolio Solutions Group and the Goldman Sachs Energy Infrastructure & Renewables Team (“EI&R Team”) discuss the Goldman Sachs Rising Dividend Growth Fund’s (the “Fund”) performance and positioning for the 12-month period ended October 31, 2021 (the “Reporting Period”).

| Q | How did the Fund perform during the Reporting Period? |

| A | During the Reporting Period, the Fund’s Class A, Class C, Institutional, Investor, Class R6, Class R and Class P Shares generated average annual total returns, without sales charges, of 46.88%, 45.74%, 47.16%, 47.09%, 47.22%, 46.38% and 47.17%, respectively. These returns compare to the 42.91% average annual total return of the Fund’s benchmark, the Standard & Poor’s® 500 Index (with dividends reinvested) (the “S&P 500 Index”), during the same time period. |

| Q | What economic and market factors most influenced the U.S. equity markets as a whole during the Reporting Period? |

| A | The S&P 500 Index gained 10.95% in November 2020 and 3.84% in December 2020. Stocks rallied, extending a broad-based recovery from steep first quarter 2020 declines, on the prospect of an end to the global COVID-19 pandemic and its weighted economic impact with approval and distribution of multiple COVID-19 vaccines. While uncertainty surrounding the U.S. elections and other policy questions created the potential for higher market volatility, the Democrat victory for Joe Biden proved positive for equity markets. Further, after a historically sharp but short recession during the spring of 2020, many major economies, including the U.S., entered an early-cycle phase of recovery. Employment conditions improved, as temporary job losses were regained and U.S. manufacturing activity recovered. Despite this improvement, reminders of a COVID-19 ceiling for industries hit hardest by the restrictions caused by the pandemic persisted. |

The S&P 500 Index gained 6.17% in the first quarter of 2021. Rising bond yields and a value-led equity market dominated these months. Two key drivers of performance were the Democrat victory in Georgia in January 2021, paving the way for massive additional U.S. fiscal stimulus, and progress in the COVID-19 vaccine rollout. An increase in the 10-year U.S. Treasury yield benefited financials and value-oriented stocks. The accelerating rollout of COVID-19 vaccines boosted investors’ hopes of a sustainable reopening of the economy. Small-cap stocks, which tend to be more cyclical and domestically focused, performed particularly well. The passage of President Biden’s stimulus package led to upgrades in consensus forecasts for U.S. Gross Domestic Product in 2021. Some investors worried the size of the U.S. fiscal stimulus could provoke a pickup in inflation. However, despite upgrading its growth forecasts for the calendar year and expecting unemployment to decline, the U.S. Federal Reserve (the “Fed”) did not believe inflation would be meaningfully above target and did not expect to raise interest rates before 2024. |

The S&P 500 Index increased 8.54% in the second quarter of 2021. Discussions during these months centered on the central bank liquidity tailwind, fiscal stimulus, COVID-19 vaccine rollout progress, economic reopening momentum, strong corporate profits and robust equity inflows. While inflation concerns were fairly pervasive, the Fed remained consistent in its messaging around expectations that price pressures would be transitory. The peak inflation theme gained traction as the quarter progressed, even as economists suggested the transitory period may be longer than expected. Corporate earnings season brought another round of outsized beats over consensus estimates, along with corporate commentary highlighting some input pressure offset for companies with above-average pricing power or productivity initiatives. Despite a late-quarter agreement between the White House and a bipartisan group of Senators on the framework of a physical infrastructure package, the path to additional fiscal stimulus remained complicated. |

10

FUND RESULTS

The S&P 500 Index increased only marginally in the third quarter of 2021, with a total return of 0.58%. In July and August 2021, the U.S. equity market rally continued, as the focus remained on easy financial conditions, accommodative monetary policy, pent-up consumer demand, positive corporate earnings sentiment, resilient operating margins, corporate buybacks and equity inflows. Some economic indicators, including higher inflation and lower than consensus expected retail sales and manufacturing activity, were causes of concern among investors, though the market and the Fed remained largely optimistic. However, sentiment deteriorated in September 2021, as the spread of the COVID-19 Delta variant dampened economic reopening momentum and the Fed signaled for a slowdown of its asset purchases. Also, the still-complicated path to fiscal stimulus in the House of Representatives, the looming debt ceiling discussion and global risk events, including supply chain disruptions and input price pressures, all put a strain on the U.S. equity market. September also saw a global risk asset sell-off on the heels of Chinese real estate developers’ leverage concerns and a spike in energy prices. |

In a sharp reversal, the S&P 500 Index gained 7.01% in October 2021, its best monthly gain in 2021 to date, propelled by the third calendar quarter corporate earnings season. More than half of the S&P 500 Index constituents reported their earnings, with more than 80% reporting positive earnings surprises even as supply chain disruptions, input cost pressures and tight labor markets were highlighted in many companies’ earnings reports. On the policy front, the Fed’s narrative on inflation shifted from “transitory” to “more persistent.” Chatters and negotiations around fiscal stimulus continued, but it was not until the end of the month that the White House announced a $1.75 trillion social spending framework, a lower figure than initially proposed. On the economic front, inflation rose; the Institute for Supply Management’s manufacturing and services indices both reported better than consensus expectations; and job market data was mixed, with September’s nonfarm payroll growth significantly lower than August’s but initial jobless claims falling. |

For the Reporting Period overall, energy, financials and information technology were the best performing sectors in the S&P 500 Index. The weakest performing sectors in the S&P 500 Index were utilities and consumer staples, followed at some distance by health care. |

Within the U.S. equity market, small-cap stocks, as measured by the Russell 2000® Index, performed best, followed by mid-cap stocks, as measured by the Russell Midcap® Index, and then large-cap stocks, as measured by the Russell 1000® Index, each capitalization segment posting robust double-digit positive absolute returns. From a style perspective, value-oriented stocks outpaced growth-oriented stocks across the capitalization spectrum, though the margin of differentiation among large-cap stocks was quite narrow. (All as measured by the FTSE Russell indices.) |

| Q | What economic and market factors most influenced energy MLPs as a whole during the Reporting Period? |

| A | During the Reporting Period, commodity prices saw significant strength, with West Texas Intermediate (“WTI”) crude oil and natural gas prices up 133.50% and 78.61%, respectively. Strength was largely underpinned by an improving macroeconomic backdrop, with global demand recovering alongside COVID-19 vaccine rollouts and heightened economic activity as well as supply-side discipline from oil-producing countries. China and other parts of Asia, which were the first regions affected by the COVID-19 outbreak, saw a full recovery in oil demand, with consumption rising above 2019 levels by the end of the Reporting Period. Toward the end of the Reporting Period, crude oil and natural gas prices experienced a surge, as the market positioned itself for a potential “energy crisis,” as commodities supply struggled to keep pace with higher demand. Outside of higher demand and global supply restraint, oil and gas prices were also positively impacted by weather-related events, such as colder than anticipated weather and hurricanes that further affected an already tight supply market. |

On the supply side, global producers showed great discipline. The Organization of the Petroleum Exporting Countries (“OPEC”) and Russia, known as OPEC+, demonstrated a commitment to balanced global oil markets but seemingly focused on maximizing revenue instead of growing market share, with production still down approximately 8% compared to 2019 levels. In the U.S., we also saw unprecedented supply discipline, with crude production down about 10% versus 2019 levels. In addition, many observers thought U.S. production appeared less price elastic than it had once been given that—despite the rise in crude oil prices—U.S. oil rig counts were down more than 70% at the end of the Reporting Period compared to 2019 levels. In our view, U.S. producers were focused on free cash flow generation, with management incentives aligned to prioritize return of capital to investors after several years of criticism that had led |

11

FUND RESULTS

| to significant multiples compression and equity price declines. (Multiple compression is when a company’s multiples, such as the price/earnings ratio, is reduced due to increased earnings without an increase in stock price.) |

Against this backdrop, midstream1 energy markets moved higher alongside improving commodity prices, with the Alerian MLP Index2, which measures energy infrastructure master limited partnerships (“MLPs”), and the Alerian Midstream Energy Index3, which measures the broader midstream sector inclusive of both energy MLPs and “C” corporations, generating total returns of 85.70% and 76.23%, respectively, during the Reporting Period. |

Despite a challenging operating environment given the COVID-19 pandemic, midstream company earnings before interest, taxes, depreciation and amortization (“EBITDA”) proved resilient overall, largely due to the contractual nature of their cash flow streams and a focus from management teams on reducing operational expenses and asset optimization. During the 2020 calendar year, the collective EBITDA for a group of the largest U.S. midstream energy companies fell only about 1%. This compared to an 8% decline in U.S. crude oil production and a 12% decline in U.S. refined product consumption during the same year. Interestingly, the emergence of COVID-19 sparked a significant operational shift from midstream management teams, which dramatically reduced capital budgets and operating expenses and also indicated they would maintain cost discipline going forward. |

In our view, the COVID-19 pandemic accelerated the broader energy sector’s transformation from “growth at all costs” to one more focused on capital discipline, free cash flow generation and returning capital to shareholders. In addition, commodity price uncertainty during 2020 led many U.S.-based exploration and production companies to significantly reduce rig count and planned capital expenditures, which, in turn, lowered crude oil production estimates for 2021 and 2022, with these companies broadly prioritizing free cash flow. |

Lower production estimates also led many midstream energy companies to cancel or delay planned projects, as the additional capacity was no longer needed. The direct impact of the midstream sector’s capital discipline, paired with resilient cash flow, was a meaningful uptick in free cash flow generation on relatively unchanged earnings power during a volatile period. The sharp upswing in free cash flow generation enabled rapid de-leveraging while also leaving substantial discretionary cash flow that can be used to drive further shareholder returns through potential buybacks and/or dividend growth. |

At the end of the Reporting Period, the midstream sector was offering some of the highest yields in the equity space, with the Alerian MLP Index yielding more than 7%, which was five times the yield of the S&P 500 Index and twice the yields of both utilities and real estate investment trusts. At the same time, robust free cash flow generation had led to rapid de-leveraging and materially improved free cash flow-to dividend ratios. |

| Q | What key factors were responsible for the Fund’s performance during the Reporting Period? |

| A | The Fund outperformed the S&P 500 Index on a relative basis for the Reporting Period. |

During the Reporting Period, the Fund’s dividend-paying investments outperformed the S&P 500 ex-Energy Index, the benchmark used for the dividend-paying growers portion of the Fund. Stock selection contributed most positively to relative results within this portion of the Fund. Sector allocation also added value. |

The Fund’s MLP & Energy Infrastructure Sleeve posted robust double-digit absolute gains but underperformed the Alerian MLP Index, the benchmark used for the MLP & Energy Infrastructure Sleeve of the Fund, on a relative basis. In managing the MLP & Energy Infrastructure Sleeve, the EI&R Team remained focused on high quality midstream companies with strong dividend and distribution coverage, cash flow growth potential and what it considered to be a |

| 1 | The midstream component of the energy industry is usually defined as those companies providing products or services that help link the supply side (i.e., energy producers) and the demand side (i.e., energy end-users for any type of energy commodity. Such midstream businesses can include, but are not limited to, those that process, store, market and transport various energy commodities. |

| 2 | Source: Alerian. The Alerian MLP Index is the leading gauge of energy infrastructure MLPs. The capped, float-adjusted, capitalization-weighted index, whose constituents earn the majority of their cash flow from midstream activities involving energy commodities, is disseminated real-time on a price-return basis (AMZ) and on a total-return basis (AMZX). It is not possible to invest directly in an unmanaged index. |

| 3 | Source: Alerian. The Alerian Midstream Energy Index is a broad-based composite of North American energy infrastructure companies. The capped, float-adjusted, capitalization-weighted index, whose constituents earn the majority of their cash flow from midstream activities involving energy commodities, is disseminated real-time on a price-return basis (AMNA), total-return basis (AMNAX), net total-return (AMNAN), and adjusted net total return (AMNTR) basis. It is not possible to invest directly in an unmanaged index. |

12

FUND RESULTS

| robust outlook for free cash flow generation and healthy balance sheets. The EI&R Team believes this quality bias ultimately led to relative underperformance during a Reporting Period of market exuberance. |

Midstream energy markets experienced a strong performance rally following the COVID-19 vaccination announcement, with lower quality midstream stocks, which we defined as smaller-cap, higher-beta companies with non-investment balance sheets, leading the way. These companies had experienced severe equity price weakness during the COVID-19 market downturn. In addition, these higher-beta companies generally have more commodity price sensitivity and, therefore, on a relative basis, benefited to a greater degree from the rally in commodity prices. The MLP & Energy Infrastructure Sleeve’s underweight position in lower quality, high beta stocks compared to the Alerian MLP Index detracted from relative performance. |

In addition, the MLP & Energy Infrastructure Sleeve’s higher relative exposure to clean energy infrastructure companies detracted from relative performance. After strong performance in 2020, the clean energy infrastructure sector fell in sympathy with the broader pullback in clean energy equities. The weakness in the clean energy sector was driven primarily by the rapid move in interest rates off of a relatively low starting point at the beginning of 2021 as well as by concerns around inflation and the potential for higher input costs, worries that competition may compress returns, clean energy exchange-traded fund rebalances and, lastly, potential government intervention due to high energy prices. |

| Q | Which equity market sectors most significantly affected Fund performance during the Reporting Period? |

| A | The dividend-paying growers portion of the Fund does not take explicit sector bets relative to the S&P 500 ex-Energy Index but rather allocations are the result of stock selection. That said, the sectors that contributed most positively on a relative basis to the S&P 500 ex-Energy Index during the Reporting Period were consumer discretionary, consumer staples and health care. Only partially offsetting these positive contributors were industrials, information technology and communication services, which detracted from this portion of the Fund’s relative results. |

| Q | What were some of the Fund’s best-performing individual stocks during the Reporting Period? |

| A | The top individual contributors to the Fund’s relative performance during the Reporting Period were an underweight position in e-commerce retailing leader Amazon.com and overweight positions in semiconductor wafer fabrication equipment manufacturer Applied Materials, retail department store operator Dillard’s, semiconductor producer and distributor KLA and media and advertising organization Interpublic Group of Cos. Amazon.com underperformed the S&P 500 ex-Energy Index, and Applied Materials, Dillard’s, KLA and Interpublic Group of Cos. outperformed the S&P 500 ex-Energy Index during the Reporting Period. |

| Q | Which stocks detracted significantly from the Fund’s performance during the Reporting Period? |

| A | Detracting most from the Fund’s results relative to the S&P 500 ex-Energy Index during the Reporting Period were underweight positions in Google parent company Alphabet, software behemoth Microsoft, electric vehicle maker Tesla and three-dimensional (“3D”) graphics processors developer NVIDIA and an overweight position in interactive entertainment software developer Activision Blizzard. Alphabet, Microsoft, Tesla and NVIDIA outperformed the S&P 500 ex-Energy Index, and Activision Blizzard underperformed the S&P 500 ex-Energy Index during the Reporting Period. |

| Q | Which sub-industries within the Alerian MLP Index most significantly affected Fund performance during the Reporting Period? |

| A | Relative overweights to the power generation, gathering & processing and services/midstream sub-industries detracted most from the MLP & Energy Infrastructure Sleeve’s performance. Most notably within the power generation sub-industry, exposure to renewable power generation dampened relative results. After strong performance in 2020, the renewable power generation segment experienced some weakness alongside the broader clean energy sector in 2021 through October, and, as a result, lagged the traditional midstream market. Weak security selection within the gathering & processing and services/midstream sub-industries also detracted from relative performance. |

As measured by the Alerian MLP Index, a relative underweight to the other/liquefication sub-industry and relative overweight positions in the pipeline transportation/natural gas and integrated sub-industries contributed most positively during the Reporting Period, with these latter two sub-industries’ exposure to the strong commodity price environment boosting their relative results. Effective security selection helped most within the other/liquefication sub-industry. |

13

FUND RESULTS

| Q | Which MLPs and energy infrastructure companies detracted significantly from the Fund’s performance during the Reporting Period? |

| A | Among those MLPs and energy infrastructure companies detracting most from the Fund’s results relative to the Alerian MLP Index were EnLink Midstream LLC, Western Midstream Partners LP and Genesis Energy LP, each of which outperformed the Alerian MLP Index during the Reporting Period but in which the MLP & Energy Infrastructure Sleeve held an underweight position. |

During the Reporting Period, the MLP & Energy Infrastructure Sleeve of the Fund had established a position in EnLink Midstream LLC (ENLC) but remained underweight relative to the Alerian MLP Index. ENLC is a midstream operator involved in natural gas gathering treating, processing, transmission, distribution, supply and marketing, and crude oil marketing. The company has assets across the U.S. shale basins, including exposure to the Permian Basin and STACK region. (STACK is derived from Sooner Trend (oil field), Anadarko (basin), Canadian and Kingfisher (counties).) ENLC benefited during the Reporting Period from an increase in customer activity across its operating segments. More specifically, one of ENLC’s biggest customers in the STACK region announced a joint venture that would result in a substantial increase in drilling activity on ENLC’s acreage. As the company previously had reset its distribution level during the COVID-19 sell-off, the increase in activity levels led to growth in free cash flow for ENLC. Additionally, due to customer activity increasing, the company increased its 2020 adjusted EBITDA guidance in June 2021. |

Western Midstream Partners LP (WES) is a midstream company that owns, develops and operates assets that are involved in gathering, compressing, treating, processing and transporting natural gas, crude oil and water. WES primarily serves customers in the Permian Basin and the DJ Basin. While the EI&R Team added to the position during the Reporting Period, the MLP & Energy Infrastructure Sleeve of the Fund remained underweight relative to the Alerian MLP Index, which detracted as WES outperformed the Alerian MLP Index during the Reporting Period. WES benefited from increased customer activity along its acreage as well as from the increased health of its key counterparty, namely Occidental Petroleum. Further, due to previously cutting its distribution, WES was able to substantially de-lever its balance sheet. As a result, the company put itself, in our view, in a strong free cash flow generating position. This, in turn, enabled the company to re-start distribution growth, as its management announced a 5% annual distribution growth plan for 2021 and plans to repurchase units. The strong free cash flow potential and operating leverage to increasing production supported strong performance for WES during the Reporting Period. |

Genesis Energy LP (GEL) is a midstream company that owns and operates crude oil gathering, marketing and pipeline operations. The company has a large presence in the U.S. Gulf Coast and is also a large producer of sodium hydrosulfide, or soda ash. On the company’s second quarter 2021 earnings call held in August 2021, the company stated it expects pricing for its soda ash business to continue to recover in 2022 to levels almost near its pre-COVID-19 levels. Additionally, the company benefited during the Reporting Period from a recovery in volumes in its offshore business. We trimmed the MLP & Energy Infrastructure Sleeve’s already underweight position in GEL during the Reporting Period to allocate to names we believed offered better potential risk-adjusted returns. |

| Q | What were some of the Fund’s best-performing MLPs and energy infrastructure companies during the Reporting Period? |

| A | Relative to the Alerian MLP Index, among those MLPs and energy infrastructure companies that contributed most to the Fund’s performance during the Reporting Period were Targa Resources Corp., NGL Energy Partners LP and ONEOK, Inc. |

Targa Resources Corp. (TRGP) is an independent midstream services provider primarily engaged in gathering, storing, processing and transporting oil, natural gas and refined petroleum products. The COVID-19 vaccine news in November 2020 improved the outlook for energy demand in 2021 and beyond, benefiting TRGP due to the integrated nature of the company’s assets and its significant operating leverage to the Permian Basin, especially compared to its peers. Further supporting TRGP’s strong performance during the Reporting Period was its first quarter 2021 results in which it reported substantially beating consensus EBITDA expectations. The company also raised its full year 2021 guidance driven by both the one-time Texas winter storm benefit and higher commodity prices, which was viewed positively by the market. Toward the end of the Reporting Period, supply constraints, coupled with strong demand, led to lower than consensus expected inventories across commodities, including natural gas and natural gas liquids (NGLs). This pushed prices even higher ahead of normal winter weather demand. We believe investors favored TRGP, |

14

FUND RESULTS

| as they felt the company was well positioned to benefit due to the integrated NGL value chain and exposure to the Permian Basin. This supportive fundamental backdrop combined with TRGP’s disciplined capital allocation, which was expected to support free cash flow growth that can be utilized for de-leveraging as well as for potential share buybacks, helped drive strong equity price performance during the Reporting Period. |

NGL Energy Partners LP (NGL) is a diversified midstream MLP with operations focused on crude oil logistics, water treatment services, NGL logistics and retail propane. Having no exposure to this weakly-performing MLP during the Reporting Period contributed positively to results relative to the Alerian MLP Index. During the Reporting Period, NGL significantly underperformed the Alerian MLP Index because its initial adjusted EBITDA guidance was below consensus expectations. Additionally, the company restructured one of its largest assets, the Grand Mesa Pipeline, agreeing to a settlement with its main counterparty, who previously had undergone bankruptcy proceedings. Additionally, NGL suspended its distribution completely during the Reporting Period, after previously cutting it for a second time in 2020. NGL was forced to suspend its distribution as a result of a negotiation with its lenders around its credit facility. |

ONEOK, Inc. (OKE) is a midstream service provider that owns one of the nation’s premier NGL systems, connecting NGL supply in the Rocky Mountain, Permian and Mid-Continent regions with key market centers and an extensive network of natural gas gathering, processing, storage and transportation assets. It serves customers such as petrochemical companies, propane distributors, heating fuel users, ethanol producers, refineries and exporters. The MLP & Energy Infrastructure Sleeve benefited from its overweight position in OKE, as the company benefited during the Reporting Period from an increase in both volumes and commodity prices across its systems. During the Reporting Period, OKE posted strong and growing earnings. After guiding to 2021 adjusted EBITDA in February 2021, the company increased its financial guidance for the calendar year in April 2021 on its first quarter 2021 earnings and then guided above the mid-point on its second quarter 2021 earnings in August 2021. OKE was a beneficiary of the increase in demand for commodities and consequent price increases during the Reporting Period, especially compared to the COVID-19 impacts in the prior Reporting Period. Additionally, as supply was not able to keep pace with demand, we saw a strong increase in commodity prices, with WTI crude oil prices up more than 133% and NGL prices up approximately 139% during the Reporting Period. |

| Q | How did the Fund use derivatives during the Reporting Period? |

| A | The MLP & Energy Infrastructure Sleeve of the Fund did not use derivatives during the Reporting Period. The dividend-paying equity investments portion of the Fund used equity index futures on an opportunistic basis during the Reporting Period to equitize its modest cash position. In other words, we put the Fund’s excess cash holdings to work by using them as collateral for the purchase of equity index futures. The use of these derivatives did not have a material impact on Fund results during the Reporting Period. |

| Q | Did the Fund make any significant equity purchases or sales during the Reporting Period? |

| A | The dividend-paying growers portion of the Fund uses a systematic, rules-based approach and thus equity purchases and sales are based solely on that quantitative process. |

| Q | Did the Fund make any significant purchases or sales of MLPs and energy infrastructure companies during the Reporting Period? |

| A | On the company’s Initial Public Offering, we established a position in DT Midstream, Inc., an owner, operator and developer of natural gas midstream interstate pipelines. The company focuses on intrastate and gathering lateral pipelines, storage, gathering systems and compression, treatment and surface facilities. We initiated the position based on our positive view of the company’s asset profile, leverage position, corporate structure and potential growth opportunities. |

We initiated a position in Cheniere Energy, Inc., an energy company focused on liquefied natural gas (“LNG”)-related businesses, including owning and operating LNG terminals. We established the position based on what we viewed as the company’s strong fundamental outlook, exposure to the global LNG market and long-term contracted business profile. |

Conversely, we sold the Fund’s position in Suburban Propane Partners, L.P., a retail propane gas marketer that serves residential, commercial, industrial and agriculture customers throughout service centers in the U.S. We exited the position due to what we considered to be better opportunities elsewhere with more potential upside exposure to the strong commodity recovery that occurred. |

We eliminated the Fund’s position in Enbridge Inc., which provides energy transportation, distribution and related |

15

FUND RESULTS

| services in North America and internationally. The company operates across oil, natural gas and NGLs as well as a growing renewables business. We sold the position due to what we saw as better opportunities elsewhere with more potential upside exposure to the strong commodity recovery that occurred. |

| Q | Were there any notable changes in the Fund’s equity sector weightings during the Reporting Period? |

| A | As mentioned earlier, under the QIS team’s investment approach, the dividend-paying growers portion of the Fund does not take sector bets by design. Therefore, the dividend-paying investments portion of the Fund, using a quantitative process, strove to be similar to the S&P 500 ex-Energy Index in terms of sector allocation. We seek to provide exposure to high quality, dividend-paying growers within each sector. |

| Q | Were there any notable changes in the Fund’s MLP and energy infrastructure company weightings during the Reporting Period? |

| A | There were no notable changes in the Fund’s MLP and energy infrastructure company weightings during the Reporting Period. At the end of the Reporting Period, the MLP & Energy Infrastructure Sleeve had its largest allocations in the petroleum pipeline transportation, natural gas pipeline transportation and gathering & processing segments of the Alerian MLP Index. |

| Q | How was the dividend-paying investments portion of the Fund positioned relative to the S&P 500 ex-Energy Index at the end of the Reporting Period? |

| A | As mentioned earlier, it is not part of the dividend-paying investments portion of the Fund’s approach to take sector bets. Thus, at the end of October 2021, the dividend-paying investments portion of the Fund had rather neutral positions in each sector of the S&P 500 ex-Energy Index, with the exception of communication services, wherein an underweighted position was held. |

| Q | Were there any changes to the Fund’s portfolio management team during the Reporting Period? |

| A | Effective May 24, 2021, Christopher Lvoff no longer served as a portfolio manager of the Fund, and Siwen Wu became a portfolio manager of the Fund. By design, all investment decisions for the Fund are performed within a team structure, with multiple subject matter experts. This strategic decision making has been the cornerstone of our approach and ensures continuity in the Fund. At the end of the Reporting Period, Monali Vora, Aron Kershner, Kyri Loupis and Siwen Wu served as portfolio managers of the Fund. |

| Q | What is the Fund’s tactical view and strategy for the months ahead? |

| A | The Fund seeks long-term growth of capital and current income. Within the dividend-paying growers sleeve, we maintained confidence at the end of the Reporting Period in high quality business models that have demonstrated commitment to grow their dividend in a rather stable manner. |

On the energy side, we had a positive outlook for commodity prices and oil-related equities at the end of the Reporting Period, a view supported by a healthy commodity backdrop underpinned by an ongoing recovery in economic activity and oil demand along with supply discipline from both OPEC+ and U.S. shale producers. Barring an unforeseen demand setback from COVID-19 variants and/or a breakdown in the OPEC+ agreement, we expected commodity prices to continue to move higher, perhaps to the $75 to $85 per barrel price range in the near-to-intermediate term. Longer term, we believed oil and gas would remain a critical source of global energy, with significant oil demand support coming from economic growth in developing countries. In our view, this should help offset some of the consensus expected oil and gas disruption from renewable generation sources and electric vehicle adoption. |

As for natural gas, we believed at the end of the Reporting Period that there was a substantial opportunity, as the world can use the commodity as a source of “cleaner” energy. We believed natural gas is important in the growth of renewable energy sources given that existing wind and solar technologies cannot fully power an economy. We also believed natural gas would remain essential as a baseload power source, since it has lower carbon emissions compared to other types of fuel, such as coal and oil. Liquefied natural gas specifically is a key component of this global growth story, with the U.S. alone expected to see more than 60% growth in LNG export capacity by 2025. |

Regarding midstream energy companies, we believed at the end of the Reporting Period that fundamentals were some of the most attractive on record, with midstream cash flow inflecting higher alongside strong oil and natural gas prices and management teams demonstrating capital and cost discipline. The sector was generating significant amounts of free cash flow at the end of the Reporting Period, which not only adequately supports current distributions/dividends but also leaves plenty of excess cash to further de-lever, buy |

16

FUND RESULTS

| back stock and/or grow distributions/dividends. Looking forward, we believed there was still significant room for equity price appreciation in midstream equities from a valuation perspective. In our view, the sector’s pivot to free cash flow warrants the inclusion of free cash flow valuation methods in addition to traditional enterprise value/EBITDA methodologies given that the sector has shifted from that of a consumer of capital to a distributor of capital. On both enterprise value/EBITDA and free cash flow yield metrics, the midstream sector screened cheap relative to its own history and versus other income-oriented equity asset classes at the end of the Reporting Period. |

While there are certainly still risks, such as further variants and/or waves of COVID-19, we believed the risk/reward profile for the midstream sector at the end of the Reporting Period remained meaningfully positive. |

In managing the MLP & Energy Infrastructure Sleeve, we intend to remain focused on high quality companies with strong dividend/distribution coverage, cash flow growth potential and what we see as a robust outlook for free cash flow generation and healthy balance sheets. At the end of the Reporting Period, we believed the MLP & Energy Infrastructure Sleeve was well positioned to benefit from improvements in supply/demand dynamics. As always, we continue to monitor domestic and global economies, geopolitical factors, interest rates and equity market fundamentals as we actively manage the Fund. |

17

FUND BASICS

Rising Dividend Growth Fund

as of October 31, 2021

| TOP TEN HOLDINGS AS OF 10/31/21‡ | ||||||||

| Holding | % of Net Assets | Line of Business | ||||||

| Comcast Corp. Class A | 2.3 | % | Media | |||||

| Activision Blizzard, Inc. | 2.0 | Entertainment | ||||||

| MPLX LP | 1.8 | Oil, Gas & Consumable Fuels | ||||||

| Energy Transfer LP | 1.6 | Oil, Gas & Consumable Fuels | ||||||

| Microsoft Corp. | 1.5 | Software | ||||||

| UnitedHealth Group, Inc. | 1.5 | Health Care Providers & Services | ||||||

| ViacomCBS, Inc. Class B | 1.4 | Media | ||||||

| Accenture PLC Class A | 1.4 | IT Services | ||||||

| Magellan Midstream Partners LP | 1.3 | Oil, Gas & Consumable Fuels | ||||||

| The Interpublic Group of Cos., Inc. | 1.3 | Media | ||||||

| ‡ | The top 10 holdings may not be representative of the Portfolio’s future investments. The top 10 holdings exclude investments in money market funds. |

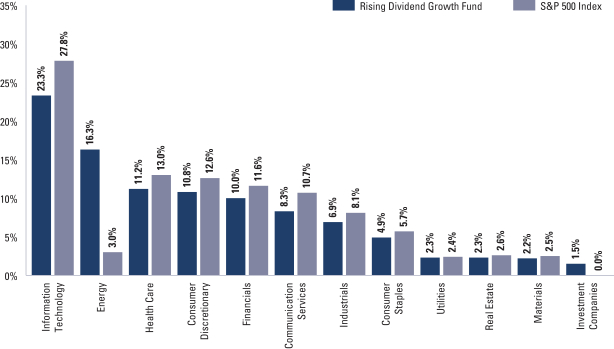

| FUND VS. BENCHMARK SECTOR ALLOCATION† |

| As of October 31, 2021 |

| † | The Fund is actively managed and, as such, its composition may differ over time. Consequently, the Fund’s overall sector allocations may differ from the percentages contained in the graph above. The graph categorizes investments using the Global Industry Classification Standard (“GICS”), however, the sector classifications used by the portfolio management team may differ from GICS. The percentage shown for each investment category reflects the value of investments in that category as a percentage of market value. The graph depicts the Fund’s investments but may not represent the Fund’s market exposure due to the exclusion of certain derivatives, if any, as listed in the Additional Investment Information section of the Schedule of Investments. |

For more information about your Fund, please refer to www.GSAMFUNDS.com. There, you can learn more about your Fund’s investment strategies, holdings, and performance.

18

GOLDMAN SACHS RISING DIVIDEND GROWTH FUND

Performance Summary

October 31, 2021

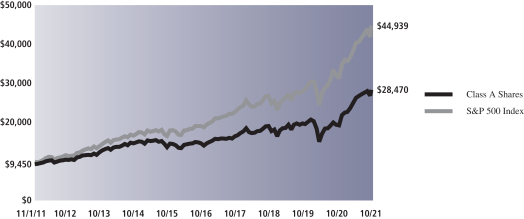

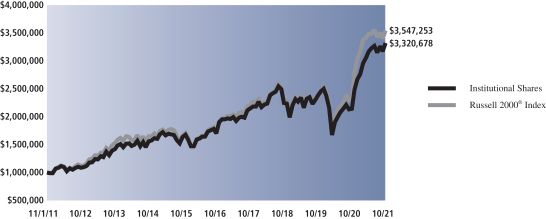

The following graph shows the value, as of October 31, 2021, of a $10,000 investment made on November 1, 2011 in Class A Shares (with the maximum sales charge of 5.50%). For comparative purposes, the performance of the Fund’s benchmark, the S&P 500 Index (with dividends reinvested), is shown. Performance reflects applicable fee waivers and/or expense limitations in effect during the periods shown and in their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The returns set forth below represent past performance. Past performance does not guarantee future results. The Fund’s investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted below. Please visit our web site at www.GSAMFUNDS.com to obtain the most recent month-end returns.

| Rising Dividend Growth Fund’s 10 Year Performance |

Performance of a $10,000 Investment, including any applicable sales charge, with distributions reinvested, from November 1, 2011 through October 31, 2021.

| Average Annual Total Return through October 31, 2021* | One Year | Five Years | Ten Years | Since Inception | ||||||||||

Class A | ||||||||||||||

Excluding sales charges | 46.88% | 14.94% | 11.65% | — | ||||||||||

Including sales charges | 38.81% | 13.65% | 11.02% | — | ||||||||||

| ||||||||||||||