UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-05349

Goldman Sachs Trust

(Exact name of registrant as specified in charter)

71 South Wacker Drive, Chicago, Illinois 60606

(Address of principal executive offices) (Zip code)

Copies to:

| Robert Griffith, Esq. | Stephen H. Bier, Esq. | |

| Goldman Sachs & Co. LLC | Dechert LLP | |

| 200 West Street | 1095 Avenue of the Americas | |

| New York, New York 10282 | New York, NY 10036 |

(Name and address of agents for service)

Registrant’s telephone number, including area code: (312) 655-4400

Date of fiscal year end: October 31

Date of reporting period: October 31, 2023

| ITEM 1. | REPORTS TO STOCKHOLDERS. |

The Annual Report to Shareholders is filed herewith. |

Goldman Sachs Funds Annual Report October 31, 2023 Dividend Focus Funds Income Builder Rising Dividend Growth

Dividend Focus Funds

| ∎ |

INCOME BUILDER |

| ∎ |

RISING DIVIDEND GROWTH |

| 1 | ||||

| 19 | ||||

| 42 | ||||

| 45 | ||||

| 45 | ||||

| 51 | ||||

| 58 | ||||

| 77 | ||||

| 78 | ||||

| NOT FDIC-INSURED | May Lose Value | No Bank Guarantee | ||||

FUND RESULTS

Goldman Sachs Income Builder Fund

Investment Objective

The Fund seeks to provide income and capital appreciation. |

Portfolio Management Discussion and Analysis

Below, the Goldman Sachs Fundamental Equity Team, the Goldman Sachs Fixed Income Investment Management Team, and the Goldman Sachs Multi-Asset Solutions (“MAS”) Group, collectively the Goldman Sachs Income Builder Team (the “Income Builder Team”), discuss the Goldman Sachs Income Builder Fund’s (the “Fund”) performance and positioning for the 12-month period ended October 31, 2023 (the “Reporting Period”).

| Q | How did the Fund perform during the Reporting Period? |

| A | During the Reporting Period, the Fund’s Class A, Class C, Institutional, Investor, Class R6 and Class P Shares generated 2.30%, 1.52%, 2.61%, 2.49%, 2.62% and 2.62%, respectively. These returns compare to the 0.13% and 5.43% average annual total returns of the Russell 1000® Value Index (with dividends reinvested) (the “Russell Value Index”) and the ICE BofAML BB to B U.S. High Yield Constrained Index (the “ICE BofA Index”), respectively, during the same period. |

The Fund is a dynamically managed multi-asset class portfolio with a baseline allocation of 60% to fixed income securities and 40% to equity securities. In seeking to meet its investment objective, the Fund has the flexibility to opportunistically tilt the allocation to fixed income and equity securities up to 15% above or below that baseline allocation. The Fund seeks to provide a high and stable income stream plus capital appreciation, with lower volatility than the equity market. The percentage of the portfolio invested in equity and fixed income securities will vary from time to time as the Income Builder Team evaluates such securities’ relative attractiveness based on, among other factors, income opportunities, market valuations, economic growth and inflation prospects. |

Because of these stated goals of the Fund, the Income Builder Team believes the returns of the Russell Value Index and the ICE BofA Index should be considered for reference only. |

| Q | What was the Fund’s 12-month distribution rate and what was its 30-Day SEC yield during the Reporting Period? |

| A | During the Reporting Period, the Fund’s Class A, Class C, Institutional, Investor, Class R6 and Class P Shares provided 12-month distribution rates of 4.48%, 3.82%, 4.67%, 4.61%, 4.68% and 4.68%, respectively. (The 12-month distribution rate is calculated by taking the sum of all cash distributions to shareholders over the past 12 months and dividing this sum by the Fund’s month-end net asset value (“NAV”) for |

the last month of the period. This rate includes capital gain/loss distributions, if any. This is not an SEC yield.) On October 31, 2023, the Fund’s 30-Day Standardized Subsidized SEC yields for its Class A, Class C, Institutional, Investor, Class R6 and Class P Shares were 4.97%, 4.26%, 5.29%, 5.21%, 5.30%, and 5.30%, respectively. (The 30-Day Standardized Subsidized SEC Yield is calculated in accordance with SEC regulations and is determined by dividing the Fund’s net investment income per share earned over the 30-day period by the Fund’s maximum public offering price per share on the last day of such period, which figure is then annualized. The 30-Day Standardized Subsidized SEC Yield may differ from the distribution rate because of the exclusion of distributed capital gains. The 30-Day Standardized Subsidized SEC Yield reflects any fee waivers and/or expense reimbursements in effect during the period, without which the yield would be reduced.) |

| Q | What economic and market factors most influenced the Fund during the Reporting Period? |

| A | During the Reporting Period, the financial markets and the Fund were most influenced by Federal Reserve (“Fed”) monetary policy, rising interest rates, inflation and macroeconomic data, geopolitical events, and U.S. and European banking stress. |

In November 2022, when the Reporting Period began, U.S. equities recorded solid gains, with the S&P 500® Index marking its first back-to-back monthly gain since August 2021. The primary catalyst driving U.S. equities higher was the notion that the Fed could begin to slow the pace of interest rate hikes. Although the Fed implemented a 75 basis point rate hike at the beginning of the month, broad messaging from policymakers suggested a strong preference to slow the pace of interest rate hikes to allow them to evaluate the impact of the significant tightening during the 2022 year to date. (A basis point is 1/100th of a percentage point.) Third quarter corporate earnings season provided disappointing results, with companies reporting results below the five-year average. In fixed income, the performance of spread, or non-government bond, sectors was generally positive, as spreads, or yield differentials, narrowed on hopes |

| 1 |

FUND RESULTS

of a peak in policy hawkishness driven by tentative signs of easing inflation and rising optimism about China relaxing its stringent COVID-19 restrictions. (Hawkish tends to suggest higher interest rates; opposite of dovish.) |

In December 2022, U.S. equities and spread sectors declined amid a variety of contradictory macroeconomic developments, highlighted by a noticeably hawkish Fed, consumer resilience, and data supporting the themes of slowing economic growth. Still, there were market expectations for a reduction in the pace of tightening, which was realized when the Fed announced a 50 basis point rate hike at its December policy meeting. Positive inflation developments further supported aspirations for a peak in the Fed tightening cycle, with October and November inflation numbers coming in cooler than expected. On the geopolitical front, the most constructive takeaways came from China’s zero-COVID pivot and pro-growth focus, along with Europe’s warmer than anticipated weather, which eased worries about an energy crisis. |

During the first quarter of 2023, U.S. equities and spread sectors broadly advanced, as investors appeared optimistic that the Fed might be nearing the end of its interest rate hiking schedule. Overall, signs of disinflation tempered fears of renewed aggressive monetary tightening, while economic reopening in China and abating recession risks in Europe supported the economic growth outlook. At the beginning of February, the Fed stepped down its pace of interest rate increases to 25 basis points but also indicated policymakers thought “ongoing” rate hikes would be appropriate, a modestly hawkish surprise. Also in February, the release of unexpectedly strong U.S. economic and labor market data raised concerns about the “stickiness” (that is, the persistence) of inflation, leading market participants to anticipate further monetary policy tightening. At its March meeting, the Fed implemented another 25 basis point rate hike, projected a weak economic outlook for the rest of 2023, and struck a more cautious tone on the forward path for rate increases. Consensus forecasts for the Fed’s interest rate path subsequently took a dovish turn due to an abrupt banking sector crisis that was driven in part by rising interest rates. Meanwhile, fourth quarter 2022 corporate earnings disappointed, as margins came under pressure from persistently high input costs and weaker demand. However, the labor market outlook appeared to be positive due to supply-chain enhancements, ongoing consumer resilience, and consensus expectations for inflation pressures to diminish as 2023 progressed. |

U.S. equities rallied during the second quarter of 2023, while spread sectors were volatile. Within equites, strength was broadly driven by disinflation momentum, an upswing in soft landing expectations, consumer resilience, a better than consensus expected first quarter corporate earnings season, and persistent enthusiasm around artificial intelligence (“AI”), including the possibility of a boom in AI-related chipmakers. (A soft landing, in economics, is a cyclical downturn that avoids recession. It typically describes |

attempts by central banks to raise interest rates just enough to stop an economy from overheating and experiencing high inflation, without causing a significant increase in unemployment, or a hard landing.) Growth stocks significantly outperformed their value counterparts during the second quarter, with mega-cap technology stocks accounting for the vast majority of gains among U.S. large-cap stocks. First quarter corporate earnings were well above their one-year averages due to a combination of pricing power, supply-chain normalizations, cost-cutting initiatives and margin expansion. In fixed income, bond yields fluctuated in response to sticky inflation data, signs of moderating economic growth, developments in the banking sector and concerns over tightening credit conditions. In May, the Fed raised interest rates 25 basis points, signaling willingness to pause further interest rate actions if U.S. inflation showed signs of moderating and because tighter credit conditions from recent banking sector stress were “likely to weigh on economic activity, hiring, and inflation.” Spread sectors broadly strengthened in June, as investors priced in the view the U.S. would avoid recession and as the Fed opted for a hawkish pause. In other words, the Fed halted monetary policy action for the first time in more than a year but still maintained higher-for-longer messaging on interest rates. |

After strong performance during July and August 2023, U.S. equities sold off in September, recording a decline for the third quarter overall. Spread sectors also retreated amid significant interest rate volatility. While U.S. economic activity remained resilient, investor sentiment weakened due to a pickup in soft landing concerns, surging energy prices and disinflationary pressures on corporate earnings. The potential of a U.S. federal government shutdown and Fitch Ratings’ downgrade in August of the U.S. credit rating weighed further on investor sentiment. The Fed acted in line with consensus forecasts, hiking interest rates 25 basis points in July and keeping rates unchanged in September. Meanwhile, corporate earnings declined, marking a third consecutive quarter of negative earnings growth for S&P 500® Index companies. On the geopolitical front, concerns around China’s economy persisted. Weaker than consensus expected data in China reflected a short-lived service sector rebound, while exports remained soft and the country’s property sector slump persisted. |

October 2023 was a challenging month for risk assets overall. U.S. equities broadly declined, with energy stocks generally trailing the market amid a pullback in crude oil prices. Bond yields rose to multi-year highs driven by better than consensus estimated U.S. economic growth prospects and, in turn, lowered expectations for potential Fed interest rate cuts in 2024. Corporate earnings growth moderated but remained better than previously expected. Ongoing geopolitical pressures, including the outbreak of war in the Middle East, also weighed on investor sentiment. |

| 2 |

FUND RESULTS

For the Reporting Period overall, U.S. large-cap equities, as measured by the S&P 500® Index, recorded a double-digit positive absolute return. Growth-oriented stocks significantly outperformed value-oriented stocks, with both producing positive absolute returns overall. The broad fixed income market, including high yield corporate bonds and bank loans, produced positive absolute returns during the Reporting Period overall. |

| Q | What was the Fund’s asset allocation positioning during the Reporting Period, and what effect did it have on performance? |

| A | At the beginning of the Reporting Period, the Fund was invested 51.7% in fixed income and 41.9% in equities, with the balance in cash and cash equivalents. This breakout is inclusive of equity derivatives exposure but does not necessarily include the cash to support those positions. Derivatives positions are mostly supported by cash held in the Fund specifically to cover its exposure and any potential margin calls or future losses experienced. |

The Fund’s duration position increased—from approximately 3.0 years at the start of the Reporting Period to 3.23 years at the end of the Reporting Period—as the Income Builder Team moved it closer to its long-term target. (Duration is a measure of a portfolio’s sensitivity to changes in interest rates.) This was accomplished through greater exposure to risk assets, specifically interest rate derivatives and emerging markets debt. We modestly upsized the Fund’s holdings of interest rate swaps in May and July 2023, and we added an allocation to 10-year U.S. Treasury futures in September. Between November 2022 and January 2023, we increased the Fund’s allocations to external emerging markets bonds and emerging markets corporate bonds. During the Reporting Period overall, the Fund’s duration positioning strategy had a rather neutral impact on performance. |

The Fund’s fixed income allocation remained rather consistent during the Reporting Period, with the Income Builder Team actively managing allocations at the security level and in terms of credit quality. That said, as mentioned previously, we increased the Fund’s allocations to external emerging markets bonds and emerging markets corporate bonds to extend the Fund’s duration. In addition, during the course of the Reporting Period, we increased the Fund’s fixed income allocation’s credit quality, moderately increasing its exposure to investment grade corporate bonds and decreasing its exposure to bank loans. The fixed income allocation had a positive impact on the Fund’s returns during the Reporting Period overall. |

The Fund’s equity allocation also remained rather consistent during the Reporting Period, though the Income Builder Team adjusted the Fund’s positioning to reflect its dynamic views. In February 2023, we eliminated an investment in EURO STOXX® Banks futures, through which the Fund had gained long exposure to European banks equities. In June, we reduced the Fund’s allocations to global real estate |

securities and global infrastructure securities, reallocating the proceeds to an exchange-traded fund (“ETF”) through which the Fund would gain exposure to U.S. large-cap Nasdaq-100® Index equities. In October, we marginally increased the Fund’s positions in global infrastructure securities and U.S. large cap stocks, the latter through S&P 500® Index futures, while trimming the Fund’s allocation to the Nasdaq-100® Index ETF. Overall, during the Reporting Period, the Fund’s equity allocation added to the Fund’s performance. |

At the end of the Reporting Period, the Fund was invested 57.4% in fixed income and 40.9% in equities, with the balance in cash and cash equivalents. |

| Q | What key factors had the greatest impact on the performance of the Fund’s fixed income allocation during the Reporting Period? |

| A | During the Reporting Period, the Fund’s fixed income allocation recorded positive absolute returns, driven mostly by its exposure to high yield corporate bonds. High yield corporate bonds outperformed investment grade corporate bonds during the Reporting Period, with both generating gains. The fixed income allocation also benefited from exposure to bank loans, which broadly produced positive returns during the Reporting Period. In addition, the Fund’s exposures to external emerging markets bonds and emerging markets corporate bonds were advantageous, with both positions recording gains. |

| Q | Were any significant purchases or sales made within the fixed income allocation of the Fund during the Reporting Period? |

| A | During the Reporting Period, the Fund established a position in the high yield corporate bonds of Republic Services, a provider of non-hazardous waste disposal services. In our view, the company benefits from a stable revenue base due to its strong position in the U.S. solid waste management industry. In addition, we believe its 2022 acquisition of U.S. Ecology, which focuses on hazardous waste disposal, complements Republic Services’ solid waste disposal footprint. In September 2023, Fitch Ratings upgraded the company’s debt to A- from BBB+, citing the stability of the underlying business, its larger scale and an improvement in credit metrics. |

Among other notable purchases during the Reporting Period were the high yield corporate bonds of The Cigna Group (“Cigna”). The Income Builder team believes Cigna is a stable BBB-rated credit because of its scale as one of the U.S.’s largest private health insurance and health services companies and its relatively low underwriting risk due to its focus on ASO (or administrative services only). Since its 2008 acquisition of pharmacy benefit manager Express Scripts, Cigna has vertically integrated its offering, which we think will help control its health care spending growth thanks to the holistic management of medical and pharmacy costs. |

| 3 |

FUND RESULTS

Moreover, revenue diversification has substantially increased Cigna’s cash flows from unregulated sources, giving the company more financial flexibility, including in its debt reduction efforts. |

Conversely, among positions exited during the Reporting Period was the Fund’s investment in the high yield corporate bonds of CSC Holdings, a provider of broadband, video and voice services to residential and business customers. We sold the Fund’s position after Moody’s Investors Service downgraded the company’s credit rating to B3 from B2 with a stable outlook due to deteriorating credit metrics, rising leverage, elevated capital intensity and weaker financials. |

| Q | What changes were made to the Fund’s fixed income allocation during the Reporting Period? |

| A | As mentioned previously, the Fund’s fixed income allocation remained rather consistent during the Reporting Period, with the Income Builder Team actively managing allocations at the security level and in terms of credit quality. We increased the overall credit quality of the fixed income allocation by adding moderately to its exposure to investment grade corporate bonds, improving the credit quality of its holdings of high yield corporate bonds and reducing its exposure to bank loans. |

In terms of market segments, we increased the Fund’s exposure to banks during the Reporting Period, as we grew more cautious about the outlook for the global economy. Banks largely exceeded consensus expectations for second quarter 2023 earnings, with relatively stable deposits and asset quality, despite rising deposit costs, which caused net interest margins to compress. Non-financial earnings were largely in line as supply chains normalized following pandemic stresses. At the end of the Reporting Period, consensus estimates pointed to improved growth in the latter part of 2023, supported by continued strong employment. Additionally, during the Reporting Period, we increased the Fund’s energy exposure because we expected energy companies to maintain spending discipline should crude oil prices stabilize and electronics inventories decline, as widely anticipated, amid the recovery in end markets. On the other hand, we reduced the Fund’s exposure to telecommunications, as we believed these companies faced secular declines arising from meaningful challenges from cable competition and elevated capital expenditure levels needed to remedy historical network underinvestment. |

| Q | What key factors had the greatest impact on the performance of the Fund’s equity allocation during the Reporting Period? |

| A | During the Reporting Period, the Fund’s equity allocation produced positive absolute returns, with stock selection in the financials, information technology and materials sectors adding most to performance. Conversely, stock selection in the communication services and utilities sectors detracted from the Fund’s returns. |

| Q | Which stocks contributed most to the Fund’s performance during the Reporting Period? |

| A | During the Reporting Period, the Fund was helped by its positions in Eli Lilly and Company, Schneider Electric and Dell Technologies. |

Eli Lilly and Company (“Eli Lilly”), which engages in the discovery, development and sale of pharmaceutical products, was a top contributor to the Fund’s performance during the Reporting Period. The company’s share price surged on news of better than consensus estimated first and second quarter 2023 financial results, which included accelerated revenue growth, with impressive performances by growth products (i.e., those designed to increase the value and user base for an existing product) and soaring demand for new products. Eli Lilly also saw notable results from its trial of a new obesity drug, which showed greater weight loss results compared to similar products. According to certain scientific studies, anti-obesity drugs may reduce the risk of cardiovascular events. This may help weight loss treatments gain health insurance coverage, potentially leading to their increased availability for a broader market of patients. In addition, Eli Lilly’s shares benefited in October 2023 when a competitor’s weight loss drug reported positive clinical trial data for the treatment of kidney failure, suggesting there could be a positive secondary use for Eli Lilly’s own weight loss treatment in trials. At the end of the Reporting Period, we continued to believe Eli Lilly had an impressive new product suite in development and its path to further market share capture remained intact. In our view, the company was well positioned to benefit from the secular growth trend targeting obesity with its leading obesity drug and a full portfolio of next-generation obesity drugs in its pipeline. |

France-based Schneider Electric provides electrical power products through energy management and industrial automation. Its shares appreciated near the beginning of the Reporting Period on ongoing investor optimism following the company’s third quarter 2022 revenue beat. Schneider Electric then delivered strong earnings throughout 2023, confirming strong momentum in demand. In our opinion, Schneider has built a strong software portfolio, which should enable it to benefit from secular themes, such as data centers, electrification and grid infrastructure sustainability, across its end markets. The company has demonstrated strong cost execution through portfolio rationalization and improved productivity, in our view. At the end of the Reporting Period, we believed the company could continue to deliver on its margin expansion targets. We continued to like Schneider in the long term given its exposure to what we consider to be attractive growth opportunities and good execution capabilities. |

The Fund established a position in the stock of technology infrastructure and computer company Dell Technologies during the second quarter of 2023. In May 2023, its shares appreciated after the company announced better than consensus estimated earnings. The stock price jumped again |

| 4 |

FUND RESULTS

on news that second quarter results were well ahead of estimates, with its management stating it was seeing AI-related benefits coming to fruition. These results were driven by AI servers and better margins on personal computers. Dell Technologies also reported improved cash flow and an alleviation of working capital issues. At the end of the Reporting Period, the company had an excess of cash that should bode well for its return of capital plans, in our view. We further believed the personal computer market was close to bottoming, as units sold were back to pre-pandemic levels and channel inventory had dropped substantially. In our opinion, consensus estimated earnings were likely to move higher in the near term as Dell Technologies demonstrates its ability to execute and return to historical free cash flow conversion levels. The company maintains a strong balance sheet, in our opinion, and we expected more return of capital going forward. |

| Q | Which stocks detracted significantly from the Fund’s performance during the Reporting Period? |

| A | The largest detractors from Fund performance during the Reporting Period were its positions in Bristol-Myers Squibb, NextEra Energy and Foot Locker. |

Bristol-Myers Squibb was a top detractor from Fund returns due largely to drug development news as well as industry-wide headwinds. Although the pharmaceutical company reported mixed earnings throughout the Reporting Period, investors’ main focus was on the declining sales of Revlimid, a cancer drug threatened by generics alternatives. The decline in sales led the company to cut its earnings forecast in July 2023, increasing share price weakness. Bristol-Myers Squibb ultimately reported better than consensus expected third quarter 2023 bottom-line earnings, but the stock continued to fall as Revlimid sales continued to struggle. At the end of the Reporting Period, we thought the impact of generics was reflected in the company’s stock price and that Bristol-Myers Squibb’s future growth profile was likely to be determined by sales from its new product portfolio, which we believed was on track to potentially offset the end of some patents. Should more pipeline wins occur, as widely anticipated, we expected the stock to perform well, and at the end of the Reporting Period, we believed Bristol-Myers Squibb was well positioned financially with a strong balance sheet and with enough products in its pipeline to renew its growth trajectory. |

Shares of electric power and energy infrastructure company NextEra Energy (“NextEra”) depreciated largely in line with the utilities sector overall, as rising bond yields and a brightening economic outlook made this higher yielding and defensive sector look less attractive to investors. Although NextEra’s stock declined on news of weaker than consensus estimated fourth quarter 2022 revenue, the company still beat earnings per share expectations and its management reaffirmed forward guidance. Also during the Reporting Period, its stock came under pressure as the chief executive officer of its Florida utility retired following an internal |

probe into whether the utility had violated state campaign finance laws. In addition, NextEra Energy Partners, a company subsidiary, lowered its annual dividend growth outlook through at least 2026 in order to focus on funding growth plans, causing the stock to decline further. The clean energy complex overall was challenged by higher interest rates, which increased borrowing costs for future projects that require high upfront expenditures. At the end of the Reporting Period, we thought the sell-off had been excessive and that NextEra’s valuation versus its competitors was compelling. We continued to believe NextEra would be one of the largest beneficiaries of the Inflation Reduction Act, especially around wind development, and the company’s scale would give it a competitive advantage. |

Athletic footwear and apparel retailer Foot Locker announced disappointing second quarter earnings results, lowered its full-year guidance for a second time in 2023 and suspended its quarterly dividend in order to fund future strategic initiatives. Its earnings miss was driven by softening sales due to macro headwinds and a pullback in discretionary spending, which affected the broad consumer discretionary sector. Foot Locker also had high inventories, leading to markdowns and pressures on profits. Although its earnings results were largely expected and we believed the majority of its stock weakness was driven by macro deterioration, we decided to sell the Fund’s position in Foot Locker given the company’s decision to suspend its dividend. We reinvested the proceeds in what we saw as more attractive medium-term risk/reward opportunities. |

| Q | Were any significant purchases or sales made within the equity allocation of the Fund during the Reporting Period? |

| A | During the Reporting Period, we initiated a Fund position in Blackstone, a provider of investment and fund management services. As the capital markets anticipate an end to the Fed’s current rate hiking cycle, Blackstone managers are looking to rotate portfolios into investments that have been previously hurt by higher interest rates. A broad rebound in capital markets activity would also serve Blackstone well, in our opinion, as the company continues to grow its worldwide footprint and its fee-based assets. |

The Fund established a position in insurance company Progressive during the Reporting Period. Progressive has been under pressure in recent years due to a large number of small storms and natural disasters that have required payouts by the company. This, along with higher inflation costs surrounding Progressive’s car and home insurance business, led its stock price to trade at attractive levels, in our view. Going forward, we expect its management to focus on pricing, which should help drive the company’s growth. Furthermore, Progressive has typically paid a variable dividend during periods when the business is performing well, and we expect this to benefit its capital return profile going forward. |

| 5 |

FUND RESULTS

Conversely, in addition to Foot Locker, mentioned earlier, we exited the Fund’s investment in exploration and production company Devon Energy during the Reporting Period. Because of the underperformance of its newly acquired assets, as well as our concerns around the stock’s valuation being rather high, we decided to eliminate the Fund’s position and reallocate the capital to investment ideas in which we had greater conviction. |

We sold the Fund’s position in retail and commercial banking services provider M&T Bank during the Reporting Period. After strong performance in mid-January 2023, thanks to a better than consensus expected earnings report, we decided to exit the position amid muted loan growth guidance and because we thought interest rates were potentially peaking. Although we still liked the stock longer term, we favored other investments with what we believed were greater risk/reward opportunities. |

| Q | What changes were made to the Fund’s equity market sector exposures during the Reporting Period? |

| A | During the Reporting Period, the Income Builder Team increased the Fund’s exposures to the utilities, information technology and materials sectors. We reduced its exposures to the health care and real estate sectors. |

| Q | How did the Fund use derivatives and similar instruments during the Reporting Period? |

| A | During the Reporting Period, the Income Builder Team wrote equity index options in an effort to generate additional cash flow and potentially reduce volatility (negative impact on performance). In addition, equity index futures were employed to gain passive exposure to European bank stocks and the broad U.S. equity market (in each case, a positive impact). Interest rate swaps and U.S. Treasury futures were utilized as cost-efficient instruments to provide greater precision and versatility in the management of duration. The use of interest rate swaps and U.S. Treasury futures each had a negative impact on performance during the Reporting Period, though the U.S. Treasury futures detracted only slightly. To hedge against currency risk (that is, the risk that certain currencies might fluctuate in value), the Fund employed forward foreign currency exchange contracts (negative impact). |

| Q | What is the Income Builder Team’s tactical view and strategy for the months ahead? |

| A | At the end of the Reporting Period, the Income Builder Team expected U.S. economic growth to slow to a below-trend pace given the resumption of student loan repayments, the impact of labor strikes and elevated energy prices. While we believed the U.S. was in the late stages of the economic cycle, ongoing economic resilience and a lack of major macro data surprises supported a balanced outlook, in our view. Overall, we thought robust consumer spending, as well as continued progress on disinflation, could further bolster |

U.S. macro data in the near term. When the Reporting Period came to a close, an additional Fed interest rate hike by calendar year end was widely expected, but we believed a combination of better inflation data, further cooling of the labor market and an anticipated economic growth slowdown in the fourth quarter might sway the Fed against further rate hikes in 2023. |

Regarding equities, we noted at the end of the Reporting Period that the U.S. equity market had experienced heightened volatility and downward pressure on valuations in response to the Fed’s hawkish stance. Looking ahead, we thought U.S. equity performance would depend on the effects of future Fed monetary policy and the outlook for U.S. economic growth. Based on historical trends, we believed elevated oil prices were unlikely to challenge the disinflationary progress in core inflation. Additionally, we thought the strength of the U.S. labor market remained a positive for the broad equity market in the near term. At the end of the Reporting Period, we planned to stay true to our quality-first investment approach in the months ahead and seek to invest in businesses with healthy balance sheets, relatively stable cash flows and differentiated business models aligned to secular tailwinds. We believed a focus on higher-quality investments can help navigate heightened volatility while also positioning investors to benefit from the next upcycle. We intended to continue re-evaluating our assumptions and to stay focused on the long-term investment horizon. |

As for fixed income, we maintained a balanced outlook overall at the end of the Reporting Period, despite downbeat economic signals emanating from Europe and China, especially with regard to the Fund’s near-term credit exposures. In our opinion, sources of resilience remained in place. Tight labor markets, for example, were supporting consumer spending, and private sector balance sheets were healthy, in our view. However, given that risk asset valuations were broadly consistent with this macro assessment and interest rates had risen to cycle highs, we thought near-term risks were skewed to the downside, especially when considering the potential for incoming economic data to fall short of market expectations or to appear outright weak. At the end of the Reporting Period, therefore, we intended to remain alert to the growing impact of higher interest rates on lower quality corporate borrowers and lower income households, as well as on the U.S. economy broadly. We planned to maintain the up in quality bias of the Fund’s fixed income allocation. |

| 6 |

FUND BASICS

Income Builder Fund

as of October 31, 2023

TOP TEN EQUITY HOLDINGS AS OF 10/31/23‡ |

Holding | % of Net Assets | Line of Business | ||

JPMorgan Chase & Co. | 1.0% | Banks | ||

Exxon Mobil Corp. | 0.8 | Oil, Gas & Consumable Fuels | ||

Shell PLC ADR | 0.8 | Oil, Gas & Consumable Fuels | ||

Rio Tinto PLC ADR | 0.8 | Metals & Mining | ||

Blackstone, Inc. | 0.7 | Capital Markets | ||

ConocoPhillips | 0.7 | Oil, Gas & Consumable Fuels | ||

Progressive Corp. | 0.7 | Insurance | ||

Bank of America Corp. | 0.7 | Banks | ||

Walmart, Inc. | 0.6 | Consumer Staples Distribution & Retail | ||

Eli Lilly & Co. | 0.7 | Pharmaceuticals | ||

| ‡ | The top 10 holdings may not be representative of the Fund’s future investments. |

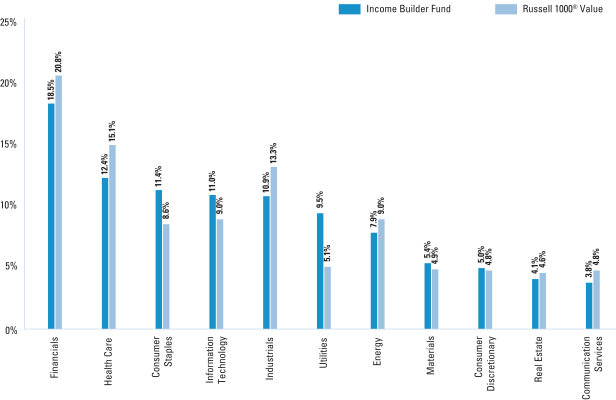

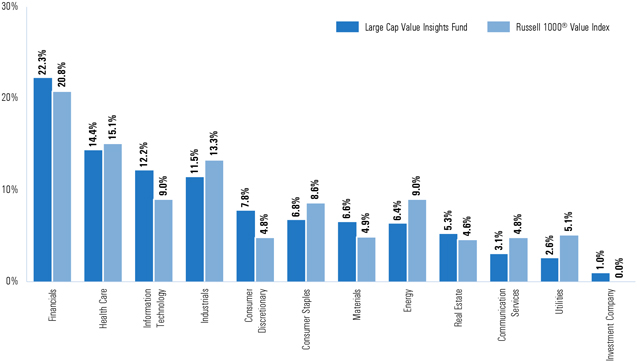

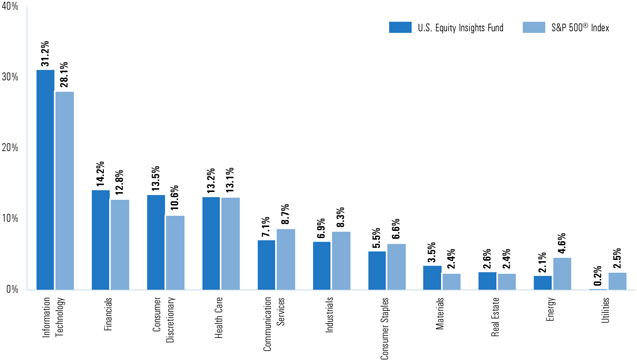

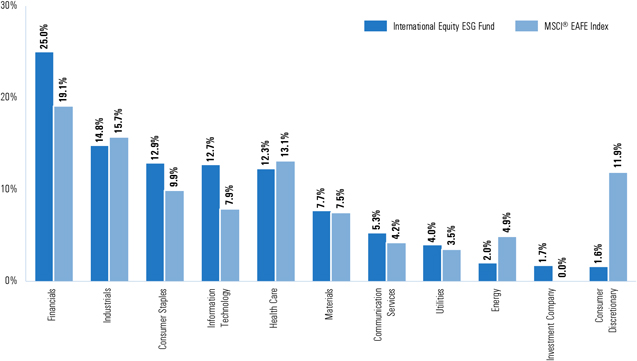

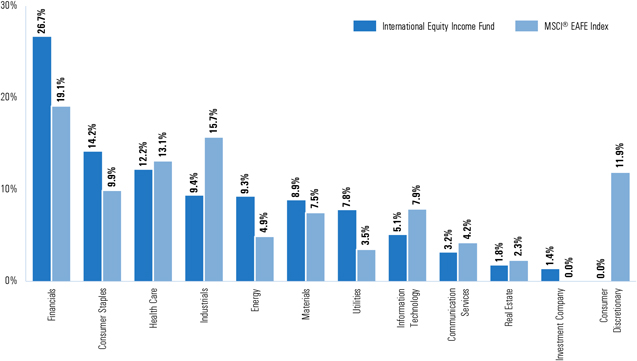

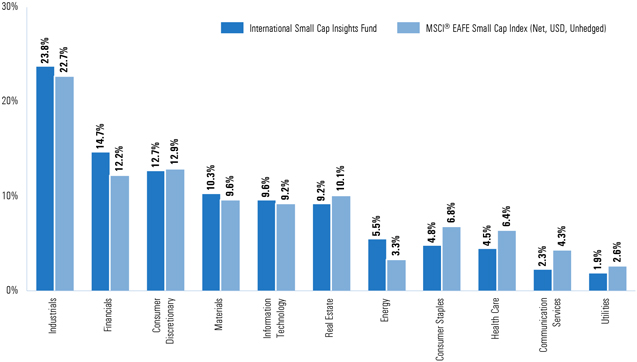

FUND’S EQUITY SECTOR ALLOCATIONS VS. BENCHMARK† |

As of October 31, 2023 |

| † | The Fund is actively managed and, as such, its composition may differ over time. Consequently, the Fund’s overall sector allocations may differ from the percentages contained in the graph above. The graph categorizes investments using the Global Industry Classification Standard (“GICS”), however, the sector classifications used by the portfolio management team may differ from GICS. The percentage shown for each investment category reflects the value of investments in that category as a percentage of the total value of the Fund’s equity investments. The graph depicts the Fund’s investments but may not represent the Fund’s market exposure due to the exclusion of certain derivatives, if any, as listed in the Additional Investment Information section of the Schedule of Investments. Underlying sector allocations of exchange traded funds and other investment companies held by the Fund are not reflected in the graph above. |

| 7 |

FUND BASICS

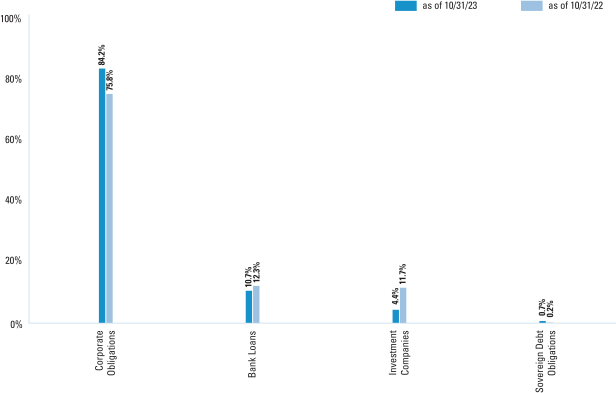

FUND’S FIXED INCOME COMPOSITION* |

As of October 31, 2023 |

| * | The percentage shown for each investment category reflects the value of investments in that category as a percentage of the Fund’s Fixed Income investments. The graph depicts the Fund’s investments but may not represent the Fund’s market exposure due to the exclusion of certain derivatives, if any, as listed in the Additional Investment Information section of the Schedule of Investments. |

For more information about your Fund, please refer to www.GSAMFUNDS.com. There, you can learn more about your Fund’s investment strategies, holdings, and performance. |

| 8 |

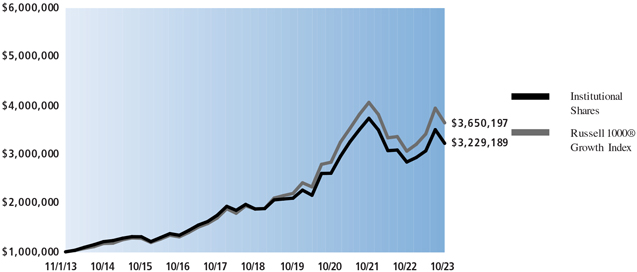

INCOME BUILDER FUND

Performance Summary

October 31, 2023

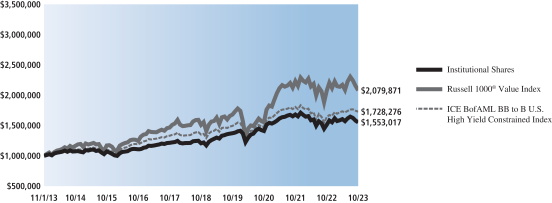

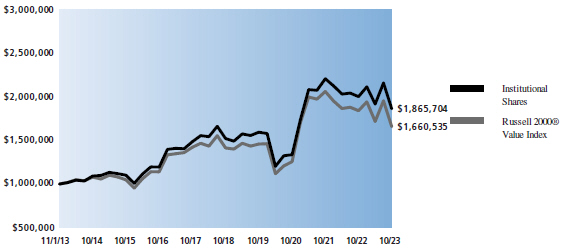

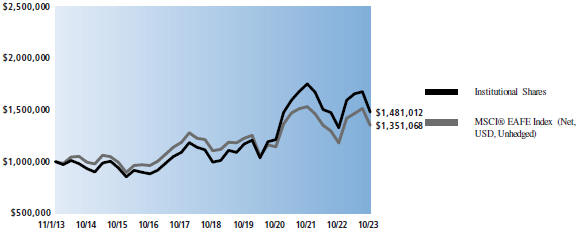

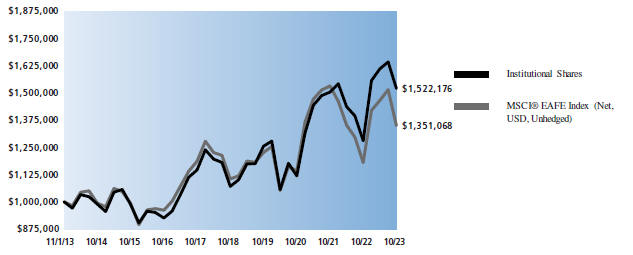

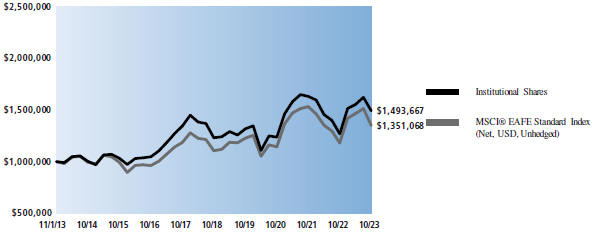

The following graph shows the value, as of October 31, 2023, of a $1,000,000 investment made on November 1, 2013 in Institutional Shares. For comparative purposes, the performance of the Fund’s current benchmarks, the Russell 1000® Value Index and the ICE BofAML BB to B U.S. High Yield Constrained Index, are shown. Performance reflects applicable fee waivers and/or expense limitations in effect during the periods shown and in their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The returns set forth below represent past performance. Past performance does not guarantee future results. The Fund’s investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted below. Please visit our web site at www.GSAMFUNDS.com to obtain the most recent month-end returns.

Income Builder Fund’s 10 Year Performance |

Performance of a $1,000,000 investment, with distributions reinvested, from November 1, 2013 through October 31, 2023. |

| Average Annual Total Return through October 31, 2023* | One Year | Five Years | Ten Years | Since Inception | ||||||||||||||

| Class A | ||||||||||||||||||

Excluding sales charges | 2.30% | 4.80% | 4.11% | — | ||||||||||||||

Including sales charges | -3.33% | 3.62% | 3.52% | — | ||||||||||||||

| ||||||||||||||||||

| Class C | ||||||||||||||||||

Excluding contingent deferred sales charges | 1.52% | 4.02% | 3.33% | — | ||||||||||||||

Including contingent deferred sales charges | 0.51% | 4.02% | 3.33% | — | ||||||||||||||

| ||||||||||||||||||

| Institutional | 2.61% | 5.17% | 4.50% | — | ||||||||||||||

| ||||||||||||||||||

| Investor | 2.49% | 5.05% | 4.37% | — | ||||||||||||||

| ||||||||||||||||||

| Class R6 (Commenced July 31, 2015) | 2.62% | 5.17% | N/A | 4.40% | ||||||||||||||

| ||||||||||||||||||

| Class P (Commenced April 16, 2018) | 2.62% | 5.17% | N/A | 4.42% | ||||||||||||||

| ||||||||||||||||||

| * | These returns assume reinvestment of all distributions at NAV and reflect a maximum initial sales charge of 5.50% for Class A Shares and the assumed contingent deferred sales charge for Class C Shares (1% if redeemed within 12 months of purchase). Because Institutional, Investor, Class R6 and Class P Shares do not involve a sales charge, such a charge is not applied to their Average Annual Total Return. |

| 9 |

FUND RESULTS

Goldman Sachs Rising Dividend Growth Fund

Investment Objective

The Fund seeks long-term growth of capital and current income. |

Portfolio Management Discussion and Analysis

Below, the Goldman Sachs Quantitative Equity Solutions (“QES”) portfolio management team, the Goldman Sachs Global Portfolio Solutions Group and the Goldman Sachs Energy & Infrastructure Team (“E&I Team”) discuss the Goldman Sachs Rising Dividend Growth Fund’s (the “Fund”) performance and positioning for the 12-month period ended October 31, 2023 (the “Reporting Period”).

| Q | How did the Fund perform during the Reporting Period? |

| A | During the Reporting Period, the Fund’s Class A, Class C, Institutional, Investor, Class R6, Class R and Class P Shares generated average annual total returns, without sales charges, of 3.71%, 2.90%, 4.02%, 3.95%, 4.03%, 3.41% and 4.02%, respectively. These returns compare to the 10.14% average annual total return of the Fund’s benchmark, the Standard & Poor’s® 500 Index (with dividends reinvested) (the “S&P 500 Index”), during the same time period. |

| Q | What economic and market factors most influenced the U.S. equity markets as a whole during the Reporting Period? |

| A | The S&P 500 Index returned 5.59% in November 2022, marking its first back-to-back monthly gain since August 2021. The primary catalyst driving U.S. equities higher was the notion that the Federal Reserve (“Fed”) could begin to slow the pace of interest rate hikes. Economic data mainly supported the Fed’s goal of a controlled economic slowdown, including consumers proving resilient in the face of high inflation. Still, the third calendar quarter corporate earnings season provided disappointing results, with companies in aggregate reporting earnings 2.0% above consensus expectations, well below the five-year average of 8.7%. Additionally, China’s zero-COVID policy remained top of mind for the market in November. |

The S&P 500 Index fell 5.76% in December 2022. Investors witnessed a variety of contradictory macroeconomic developments, highlighted by a noticeably hawkish Fed, consumer resilience and economic data supporting the themes of slowing economic growth. (Hawkish tends to suggest higher interest rates; opposite of dovish.) Still, there was a dovish tilt surrounding expectations for a reduction in the pace of tightening, which was realized when the Fed announced a 50 basis point rate hike in December following four successive 75 basis point hikes. (A basis point is 1/100th of a percentage point.) Positive inflation developments further supported aspirations for a peak in the Fed tightening cycle, with October and November inflation numbers coming |

in lower than consensus expected. On the geopolitical front, the most constructive takeaways came from China’s zero-COVID policy pivot and pro-growth focus as well as Europe’s warmer than anticipated weather, which helped settle concerns about an energy crisis. |

In the first quarter of 2023, the S&P 500 Index gained 7.53%, marking its second straight quarterly gain. Among the factors behind the market’s strength were disinflation narrative momentum, soft economic landing expectations, and a lowered bar for fourth quarter 2022 corporate earnings. Following a stellar start to the year, February proved to be a setback for the disinflation path after nonfarm payrolls illustrated the largest job growth in six months, and the unemployment rate fell to a 53-year low, which pushed market forecasts for the Fed’s terminal rate up. In addition, January inflation data saw their largest monthly increases since mid-2022, illustrating that more work was needed to combat inflation. While fourth quarter 2022 corporate earnings did disappoint as margins came under pressure by persistently high input costs and weaker demand, the labor market outlook appeared to be positive due to supply-chain enhancements, ongoing consumer resilience and consensus expectations for inflation pressures to diminish as 2023 progressed. Consensus forecasts for the Fed’s interest rate path took a dovish turn in March due to an abrupt banking crisis that escalated the risk of raising rates. Economic data in March also contributed to the dovish sentiment. |

The S&P 500 Index returned 8.74% in the second quarter of 2023. The market’s strength was predominately driven by disinflation momentum, an upswing in soft landing expectations, consumer resilience, a better than consensus expected first quarter corporate earnings season, and persistent enthusiasm around artificial intelligence (“AI”), including the possibility for a boom in AI-related chipmakers. Growth stocks significantly outperformed their value counterparts, as mega-cap technology stocks accounted for the vast majority of the S&P 500 Index’ rally in the quarter. Inflation reached its lowest level in more than two years on the back of lower energy prices. The soft landing narrative took form with a still-tight labor market and robust housing market helping to counteract the possibility of a |

| 10 |

FUND RESULTS

recession. First quarter corporate earnings metrics, though supported by a lower bar, were well above their one-year averages due to a combination of pricing power, supply-chain normalizations, cost-cutting initiatives and margin expansion. Despite U.S. equity market strength in the quarter, the implacable “higher for longer” messaging from the Fed remained an overhang. Concentrated leadership was another critical concern for investors that raised doubts about the sustainability of the U.S. equity market rally. On the geopolitical front, a slower than consensus expected economic recovery in China presented a setback for the market. |

In the third quarter of 2023, the S&P 500 Index returned -3.27%, marking its first quarterly decline of the calendar year. The S&P 500 Index started off strong in the first two months of the quarter, reaching its year-to-date 2023 high at the end of July before a sharp pullback in September. Although economic activity remained resilient, the market declined mostly due to a pickup in soft landing concerns, surging energy prices and disinflationary pressures on corporate earnings. Concerns about a looming threat of a federal government shutdown, consumer impacts from student loan repayments resuming, and a strike against automakers by the United Auto Workers union that began in September further weighed on investor sentiment. The Fed acted in line with consensus forecasts, hiking interest rates by 25 basis points in July and keeping rates unchanged at 5.25%-5.50% in September. However, the Fed’s “higher for longer” narrative appeared to gain further recognition from investors. On the earnings front, S&P 500 Index companies saw earnings decline by 4.21% in the second calendar quarter from a year earlier, marking the third consecutive quarter of negative earnings growth. |

The S&P 500 Index fell 2.10% in October 2023, posting its third consecutive monthly decline. All sectors were weaker, except for utilities, with energy trailing the market amid a pullback in crude oil prices. U.S. equities traded lower predominantly due to a pickup in yields across longer-dated U.S. Treasury bonds, resiliency of the U.S. economy, third quarter corporate earnings results, and ongoing geopolitical pressures, including the outbreak of war in the Middle East. |

For the Reporting Period overall, communication services and information technology were by far the best performing sectors in the S&P 500 Index, followed at some distance by consumer discretionary. The weakest performing sectors in the S&P 500 Index during the Reporting Period were utilities, real estate and health care. |

Within the U.S. equity market, capitalization segment performance was mixed for the Reporting Period overall. Large-cap stocks, as measured by the Russell 1000® Index, were strongest, posting solid positive absolute returns. Mid-cap stocks, as measured by the Russell Midcap® Index, and small-cap stocks, as measured by the Russell 2000® Index, each posted negative absolute returns during the Reporting Period. From a style perspective, growth-oriented |

stocks outpaced value-oriented stocks across the capitalization spectrum, but most significantly in the large-cap segment of the U.S. equity market. (All as measured by the FTSE Russell indices.) |

| Q | What economic and market factors most influenced energy MLPs as a whole during the Reporting Period? |

| A | Energy-related equities posted mixed performance during the Reporting Period. Commodity prices declined, with Brent crude oil prices falling 5.82%, while natural gas prices were even more challenged, with U.S. Henry Hub prices down 43.75%. (Henry Hub is a distribution hub on the natural gas pipeline system in Louisiana. Due to its importance, it lends its name to the pricing point for natural gas futures contracts in the U.S.) However, broad energy equities, as measured through the S&P Energy Select Sector Index (IXE)1, fell 1.72% during the Reporting Period, while midstream2-focused businesses, as measured through the Alerian MLP Index (AMZ)3, gained 16.31% during the Reporting Period. |

As the Reporting Period began in the last two months of 2022, commodities and energy-related equities experienced a brief but sharp sell-off. The sell-off was driven by worries around a potential recession, high interest rates, geopolitical tensions given the Russia/Ukraine war, and macroeconomic uncertainty. During the first quarter of 2023, commodities and energy-related equities continued to pull back overall, as broad-based macroeconomic uncertainty, driven by rising interest rates and concerns around the banking sector, caused volatility across asset classes. Despite the challenged environment, markets remained somewhat resilient, recovering some of the lost gains toward the end of the quarter. For the first quarter of 2023 overall, however, West Texas Intermediate (“WTI”) crude oil prices were down approximately 6%. Natural gas saw a more significant decline, with the U.S. Henry Hub natural gas price down about 51% and the European TTF natural gas price down approximately 36%. (Title Transfer Facility (“TTF”) is a pricing location within the Netherlands. TTF has become the |

| 1 | All components of the S&P 500® Index are assigned to one of the eleven Select Sector Indices, which seek to track major economic segments and are highly liquid benchmarks. Stock classifications are based on the Global Industry Classification Standard (GICS®). Capping is applied to ensure diversification among companies within each index. |

| 2 | The midstream component of the energy industry is usually defined as those companies providing products or services that help link the supply side (i.e., energy producers) and the demand side (i.e., energy end-users for any type of energy commodity. Such midstream businesses can include, but are not limited to, those that process, store, market and transport various energy commodities. |

| 3 | Source: Alerian. The Alerian MLP Index is the leading gauge of energy infrastructure MLPs. The capped, float-adjusted, capitalization-weighted index, whose constituents earn the majority of their cash flow from midstream activities involving energy commodities, is disseminated real-time on a price-return basis (AMZ) and on a total-return basis (AMZX). It is not possible to invest directly in an unmanaged index. |

| 11 |

FUND RESULTS

most liquid pricing location in Europe, and as such, oftentimes serves as a pricing proxy for the overall European liquified natural gas (“LNG”) import market.) |

The second quarter of 2023 saw continued macroeconomic uncertainty, including recession concerns and consumers and businesses alike adapting to a higher interest rate environment. These concerns helped drive ongoing commodity price weakness and volatility, as Brent crude oil and European TTF gas prices fell 4.9% and 20.2%, respectively, during the quarter, though U.S. Henry Hub natural gas prices recovered 12.5% during the quarter. Despite the weakness in commodities, midstream-related energy equities remained resilient, as the Alerian Midstream Energy Index (“AMNA”)4 delivered a total return of 1.2% for the second calendar quarter following an 0.8% total return in the prior quarter. AMNA’s results stand apart from other energy equities, as the upstream5-focused SPDR® S&P Oil & Gas Exploration & Production ETF (“XOP”)6 and diversified IXE were down 3.0% and 5.4%, respectively, during the quarter. Energy sector equity underperformance versus the broader equity market continued, with the S&P 500 Index outperforming the midstream AMNA and diversified IXE significantly, reversing some of the energy sector’s outperformance delivered in 2022. |

The third quarter of 2023 reflected ongoing macroeconomic uncertainty, as market participants assessed the risks of recession, sustained elevated inflation and potential effects of a higher interest rate environment. These concerns contributed to broader equity market softness, with the S&P 500 Index finishing the quarter down 3.27% and the U.S. Treasury yield rising from 3.8% to 4.6%. Despite recession concerns, crude oil prices rose, with WTI crude oil prices up 28.%, finishing the quarter around $91 per barrel, the highest level since November 2022. Strength in commodities contributed to midstream energy equities’ resilience, despite broader equity market weakness. For the quarter, the AMNA, which includes both “C” corporations and Master Limited Partnership (“MLP”) midstream |

| 4 | Source: Alerian. The Alerian Midstream Energy Index is a broad-based composite of North American energy infrastructure companies. The capped, float-adjusted, capitalization-weighted index, whose constituents earn the majority of their cash flow from midstream activities involving energy commodities, is disseminated real-time on a price-return basis (AMNA), total-return basis (AMNAX), net total-return (AMNAN), and adjusted net total return (AMNTR) basis. It is not possible to invest directly in an unmanaged index. |

| 5 | The upstream component of the energy industry is usually defined as those operations stages in the oil and gas industry that involve exploration and production. Upstream operations deal primarily with the exploration stages of the oil and gas industry, with upstream firms taking the first steps to first locate, test and drill for oil and gas. Later, once reserves are proven, upstream firms will extract any oil and gas from the reserve. |

| 6 | The S&P Oil & Gas Exploration & Production Select Industry Index, upon which XOP is benchmarked, is an equal-weighted index that draws constituents from the oil and gas exploration and production segment of the S&P Total Market Index. Liquidity and market capitalization screens are applied to the index to ensure investability. |

companies, delivered a total return of 2.5%. Other energy equity measures also saw a strong quarter, with the upstream-focused XOP and diversified IXE up 15.4% and 12.3% on a total return basis, respectively. |

In the last month of the Reporting Period, energy-related equities remained resilient amid a pullback in crude oil prices driven by heightened geopolitical tensions with the outbreak of war in the Middle East. As of the end of the Reporting Period, there had been no certain indication of a widespread impact on the broader equities markets nor had there been any major spillover into a widespread regional conflict, though investors remained attentive to the prospect of the situation escalating. In particular, investors contemplated how a prolonged conflict there could pressure energy prices and inflation. |

| Q | What key factors were responsible for the Fund’s performance during the Reporting Period? |

| A | While absolute returns were positive, the Fund underperformed the S&P 500 Index on a relative basis for the Reporting Period. |

During the Reporting Period, the Fund’s dividend-paying investments underperformed the S&P 500 ex-Energy Index, the benchmark used for the dividend-paying growers portion of the Fund. Stock selection detracted most from relative results within this portion of the Fund. Sector allocation also dampened relative results, albeit only modestly. |

The Fund’s MLP & Energy Infrastructure Sleeve posted solid double-digit absolute gains but still underperformed the Alerian MLP Index, the benchmark used for the MLP & Energy Infrastructure Sleeve of the Fund, on a relative basis. In managing the MLP & Energy Infrastructure Sleeve, the E&I Team remained focused on high quality midstream companies with strong dividend and distribution coverage, cash flow growth potential and what it considered to be a robust outlook for free cash flow generation and healthy balance sheets. The E&I Team believes this quality bias ultimately led to relative underperformance during a Reporting Period of market exuberance. |

Additionally, the MLP & Energy Infrastructure Sleeve’s tactical allocation to upstream companies detracted from its relative performance given that these companies generally have more commodity price sensitivity. Also, the MLP & Energy Infrastructure Sleeve’s higher exposure to midstream companies with an LNG focus, compared to the Alerian MLP Index, detracted from its relative performance. |

| Q | Which equity market sectors most significantly affected Fund performance during the Reporting Period? |

| A | The dividend-paying growers portion of the Fund does not take explicit sector bets relative to the S&P 500 ex-Energy Index but rather allocations are the result of stock selection. That said, the sectors that detracted most on a relative basis |

| 12 |

FUND RESULTS

from the S&P 500 ex-Energy Index during the Reporting Period were information technology, communication services and consumer staples. Only partially offsetting these detractors were industrials and materials—the only two sectors to contribute positively to this portion of the Fund’s relative results during the Reporting Period. |

| Q | Which stocks detracted significantly from the Fund’s performance during the Reporting Period? |

| A | Detracting most from the Fund’s results relative to the S&P 500 ex-Energy Index during the Reporting Period were underweight positions in information technology companies NVIDIA and Microsoft, communication services companies Meta Platforms and Alphabet, and consumer discretionary giant Amazon.com. Each of these companies outperformed the S&P 500 ex-Energy Index during the Reporting Period. |

| Q | What were some of the Fund’s best-performing individual stocks during the Reporting Period? |

| A | The top individual contributors to the Fund’s relative performance during the Reporting Period were overweight positions in information technology companies KLA and Oracle and communication services company Comcast and underweight positions in consumer discretionary company Tesla and health care company Pfizer. KLA, Oracle and Comcast each outperformed the S&P 500 ex-Energy Index during the Reporting Period, while Tesla and Pfizer each underperformed the S&P 500 ex-Energy Index during the Reporting Period. |

| Q | Which sub-industries within the Alerian MLP Index most significantly affected Fund performance during the Reporting Period? |

| A | As measured by the Alerian MLP Index, a relative underweight to the petroleum pipeline transportation sub-industry and exposure to the production & mining/ hydrocarbon sub-industry detracted most from the MLP & Energy Infrastructure Sleeve’s performance during the Reporting Period. Weak security selection and a relative overweight to the other/liquefaction sub-industry further dampened results. |

Partially offsetting these detractors was effective security selection in the gathering & processing and in the marketing/wholesale sub-industries, which contributed positively to the MLP & Energy Infrastructure Sleeve’s performance during the Reporting Period. In addition, exposure to the refining sub-industry, which is not a component of the Alerian MLP Index, boosted relative performance. |

| Q | Which MLPs and energy infrastructure companies detracted significantly from the Fund’s performance during the Reporting Period? |

| A | Among those MLPs and energy infrastructure companies detracting most from the Fund’s results relative to the Alerian MLP Index were Cheniere Energy Inc., Magellan Midstream Partners, L.P. and NGL Energy Partners LP. |

Cheniere Energy Inc., a pure-play U.S. LNG export operator, is not a constituent of the Alerian MLP Index and underperformed the Alerian MLP Index during the Reporting Period. Cheniere Energy Inc. is a leading producer of LNG in the U.S., exporting LNG to dozens of countries worldwide. Global LNG prices weakened from historically high levels during the Reporting Period, which we believe was a drag on investor sentiment toward the company. However, by the end of the Reporting Period, Cheniere Energy Inc. had hedged out most of its spot market exposure, and so we believed the market was underestimating its earnings capacity at then-current share price levels. |

Magellan Midstream Partners, L.P. is an American energy pipeline operator based in Tulsa, Oklahoma that primarily transports, stores and distributes refined petroleum products and crude oil. It owns ammonia and petroleum pipelines in the Mid-Continent oil province. Its shares gained strongly on the back of its approved acquisition by ONEOK, Inc., completed in September 2023. However, the Fund held an underweight position in Magellan Midstream Partners, L.P., and thus it proved to be a significant detractor from relative results. We sold the Fund’s position in Magellan Midstream Partners, L.P. by the end of the Reporting Period. |

NGL Energy Partners LP is a diversified midstream MLP engaged in the transportation, storage, blending and marketing of crude oil, natural gas liquids, refined products/renewables and water solutions. The company operates in three segments: water solutions, crude oil logistics and liquids logistics. During the Reporting Period, the company generated a robust triple-digit share price gain on its announcement of an increase in adjusted earnings before interest, taxes, depreciation and amortization (“EBITDA”) guidance as well as the appointment of a new chief financial officer. The limited partnership also disclosed it had reduced its debt balances by approximately $227 million during its third fiscal quarter. The Fund held no position in NGL Energy Partners LP during the Reporting Period, and thus it was a significant detractor from relative results. The Fund held no position in the MLP because NGL Energy Partners LP is a small company with what the E&I Team sees as low quality assets and a significant amount of leverage. In addition, the company’s execution has been poor, in the E&I Team’s view. |

| 13 |

FUND RESULTS

| Q | What were some of the Fund’s best-performing MLPs and energy infrastructure companies during the Reporting Period? |

| A | Relative to the Alerian MLP Index, among those MLPs and energy infrastructure companies that contributed most to the Fund’s performance during the Reporting Period were EnLink Midstream LLC, Cheniere Energy Partners LP and Targa Resources Corp. |

EnLink Midstream LLC (ENLC) is a U.S. midstream energy company that transports, stores and sells natural gas, NGLs, crude oil and condensates to industrial end-users, utilities, marketers and other pipelines. While ENLC posted a positive absolute return during the Reporting Period, it underperformed the Alerian MLP Index, and so the Fund’s underweight position in ENLC during the Reporting Period proved beneficial. ENLC gained during the Reporting Period based in part on its increasing share in midstream indices going forward due to recent consolidation in the industry. |

Cheniere Energy Partners LP is a provider of clean, secure and affordable LNG to integrated energy companies, utilities and energy trading companies around the world. Similarly to ENLC, the company generated a positive absolute return during the Reporting Period but underperformed the Alerian MLP Index, and thus the Fund’s underweight position in Cheniere Energy Partners LP contributed positively to relative results. Notably, the company posted strong earnings during the Reporting Period, and, at the end of the Reporting Period, we remained constructive on its prospects. |

Targa Resources Corp. is a leading provider of midstream services, including gathering, processing, transporting and selling of natural gas and natural gas liquids. It is not a constituent of the Alerian MLP Index and outperformed the Alerian MLP Index during the Reporting Period, thus contributing positively to the Fund’s relative results. Targa Resources Corp.’s share price increased, as energy equities rallied late in the Reporting Period. Additionally, it was announced that Targa Resources Corp. would be included in the S&P 500 Index on its next rebalance. At the end of the Reporting Period, we continued to believe its top-tier asset base would deliver better than consensus expected earnings in a growing U.S. energy production market, and thus maintained the position. |

| Q | How did the Fund use derivatives during the Reporting Period? |

| A | The MLP & Energy Infrastructure Sleeve of the Fund did not use derivatives during the Reporting Period. The dividend-paying equity investments portion of the Fund used equity index futures on an opportunistic basis during the Reporting Period to equitize its modest cash position. In other words, we put the Fund’s excess cash holdings to work by using them as collateral for the purchase of equity index futures. The use of these derivatives did not have a material impact on Fund results during the Reporting Period. |

| Q | Did the Fund make any significant equity purchases or sales during the Reporting Period? |

| A | The dividend-paying growers portion of the Fund uses a systematic, rules-based approach and thus equity purchases and sales are based solely on that quantitative process. |

| Q | Did the Fund make any significant purchases or sales of MLPs and energy infrastructure companies during the Reporting Period? |

| A | We initiated a position on the Initial Public Offering (“IPO”) of Kodiak Gas Services, Inc. The company provides contract natural gas compression to customers in numerous basins but with the majority of its operations in the Permian Basin. We believed the IPO offered an attractive entry point into what we see as a high growth business at a compelling valuation. |

We established a position in Marathon Petroleum Corp., a U.S. petroleum refining, marketing and transportation company. We believe the company held strong valuations and fundamentals along with an attractive entry point. |

Conversely, in addition to the elimination of the Fund’s position in Magellan Midstream Partners, L.P., mentioned earlier, we exited the Fund’s position in TC Energy Corp., the largest publicly traded North American energy infrastructure company, as measured by enterprise value. TC Energy Corp. had announced spinoff plans for its liquids pipeline business, which was negatively received by investors. Separately, independent rating agency Fitch Ratings downgraded the company’s long-term issuer default rating and preferred shares from A- to BBB+ and from BBB to BBB-, respectively. |

We eliminated the Fund’s position in Plains GP Holdings LP (Class A), one of the largest energy infrastructure and logistics companies in North America. During the Reporting Period, relative to the Alerian MLP Index, the Fund held an underweight position in Plains GP Holdings LP (Class A) and an overweight position in Plains All American Pipeline LP, an MLP engaged in pipeline transport, marketing and storage of liquefied petroleum gas and petroleum. Due to the similarities between the two, we decided to consolidate the Fund’s weightings into Plains All American Pipeline LP for technical purposes. |

| Q | Were there any notable changes in the Fund’s equity sector weightings during the Reporting Period? |

| A | As mentioned earlier, under the QES team’s investment approach, the dividend-paying growers portion of the Fund does not take sector bets by design. Therefore, the dividend-paying investments portion of the Fund, using a quantitative process, strove to be similar to the S&P 500 ex-Energy Index in terms of sector allocation. We seek to provide exposure to high quality, dividend-paying growers within each sector. |

| 14 |

FUND RESULTS

| Q | Were there any notable changes in the Fund’s MLP and energy infrastructure company weightings during the Reporting Period? |

| A | There were no notable changes in the Fund’s MLP and energy infrastructure company weightings during the Reporting Period. At the end of the Reporting Period, the MLP & Energy Infrastructure Sleeve had its largest allocations in the gathering & processing, natural gas pipeline transportation, petroleum pipeline transportation, and liquefication segments of the Alerian MLP Index. |

| Q | How was the dividend-paying investments portion of the Fund positioned relative to the S&P 500 ex-Energy Index at the end of the Reporting Period? |

| A | As mentioned earlier, it is not part of the dividend-paying investments portion of the Fund’s approach to take sector bets. Thus, at the end of October 2023, the dividend-paying investments portion of the Fund had rather neutral positions in each sector of the S&P 500 ex-Energy Index, with the exception of communication services, wherein an underweighted position was held. |

| Q | Were there any changes to the Fund’s portfolio management team during the Reporting Period? |

| A | There were no changes to the Fund’s portfolio management team in either the dividend-paying investments portion of the Fund or the MLP & Energy Infrastructure Sleeve of the Fund during the Reporting Period. |

| Q | What is the Fund’s tactical view and strategy for the months ahead? |

| A | The Fund seeks long-term growth of capital and current income. Within the dividend-paying growers sleeve, we maintained confidence at the end of the Reporting Period in high quality business models that have demonstrated commitment to grow their dividend in a rather stable manner. |

On the energy side, we had a positive view ahead for commodity prices and oil-related securities at the end of the Reporting Period. We expected oil prices to trade in the $80 to $100 per barrel range during the next several quarters, creating a strong operating environment for energy-focused businesses. Additionally, we saw energy policy shifting as the globally economy looked to address growing global energy needs, with energy security becoming a priority of many developed nations following Russia’s invasion of Ukraine. In our view, North America is rather uniquely positioned as a potential key source of safe, reliable and affordable energy for decades to come. Looking at LNG specifically, the U.S. has spent billions of dollars on LNG infrastructure during the last five years or so to supply the world with essential LNG under long-term contracts. Since 2017, the U.S. has grown natural gas production by about |

50% and LNG exports by more than 900%, making it the largest global LNG exporter, with industry expectations for U.S. LNG exports to triple by 2032 relative to 2021 levels. |

Regarding midstream energy companies, we believed at the end of the Reporting Period that their fundamentals were some of the most attractive on record, with midstream cash flow inflecting higher alongside strong oil and natural gas prices and management teams demonstrating capital and cost discipline. The sector was generating significant amounts of free cash flow at the end of the Reporting Period, which, in our opinion, not only adequately supported then-current distributions and dividends but also left plenty of excess cash to further reduce debt if needed, buy back stock and/or grow distributions and dividends. |

Overall, we believed at the end of the Reporting Period that the midstream energy sector presented a compelling investment opportunity amid a strong commodity price backdrop, healthy fundamentals and inexpensive valuations. Additionally, the sector was well positioned, in our view, to benefit from the growing need for North American energy. |

In managing the MLP & Energy Infrastructure Sleeve, we intend to remain focused on high quality companies with strong dividend/distribution coverage, cash flow growth potential and what we see as a robust outlook for free cash flow generation and healthy balance sheets. As always, we continue to monitor domestic and global economies, geopolitical factors, interest rates and equity market fundamentals as we actively manage the Fund. |

| 15 |

FUND BASICS

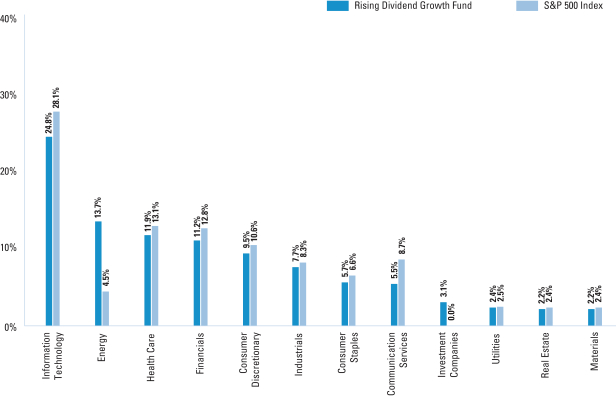

Rising Dividend Growth Fund

as of October 31, 2023

TOP TEN HOLDINGS AS OF 10/31/23± |

Holding | % of Net Assets | Line of Business | ||

Comcast Corp. Class A | 2.4% | Media | ||

Microsoft Corp. | 2.4 | Software | ||

Oracle Corp. | 2.1 | Software | ||

Intuit, Inc. | 2.0 | Software | ||

Applied Materials, Inc. | 2.0 | Semiconductors & Semiconductor Equipment | ||

Texas Instruments, Inc. | 1.9 | Semiconductors & Semiconductor Equipment | ||

KLA Corp. | 1.9 | Semiconductors & Semiconductor Equipment | ||

Roper Technologies, Inc. | 1.8 | Software | ||

Amphenol Corp. Class A | 1.8 | Electronic Equipment, Instruments & Components | ||

Motorola Solutions, Inc. | 1.8 | Communications Equipment | ||

| ± | The top 10 holdings may not be representative of the Fund’s future investments. The top 10 holdings exclude investments in money market funds. |

FUND VS. BENCHMARK SECTOR ALLOCATION† |

As of October 31, 2023 |

| † | The Fund is actively managed and, as such, its composition may differ over time. Consequently, the Fund’s overall sector allocations may differ from the percentages contained in the graph above. The graph categorizes investments using the Global Industry Classification Standard (“GICS”); however, the sector classifications used by the portfolio management team may differ from GICS. The percentage shown for each investment category reflects the value of investments in that category as a percentage of market value (excluding investments in the securities lending reinvestment vehicle, if any). The graph depicts the Fund’s investments but may not represent the Fund’s market exposure due to the exclusion of certain derivatives, if any, as listed in the Additional Investment Information section of the Schedule of Investments. Underlying sector allocations of exchange traded funds and other investment companies held by the Fund are not reflected in the graph above. Figures in the graph may not sum to 100% due to rounding and/or the exclusion of other assets and liabilities. |

For more information about your Fund, please refer to www.GSAMFUNDS.com. There, you can learn more about your Fund’s investment strategies, holdings, and performance. |

| 16 |

RISING DIVIDEND GROWTH FUND

Performance Summary

October 31, 2023

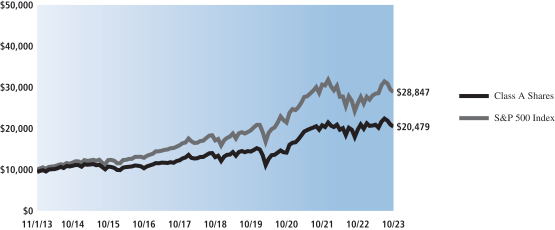

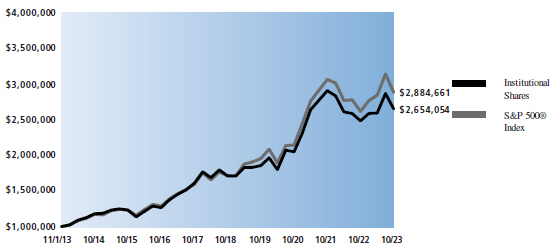

The following graph shows the value, as of October 31, 2023, of a $10,000 investment made on November 1, 2013 in Class A Shares (with the maximum sales charge of 5.50%). For comparative purposes, the performance of the Fund’s benchmark, the S&P 500 Index (with dividends reinvested), is shown. Performance reflects applicable fee waivers and/or expense limitations in effect during the periods shown and in their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The returns set forth below represent past performance. Past performance does not guarantee future results. The Fund’s investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted below. Please visit our web site at www.GSAMFUNDS.com to obtain the most recent month-end returns.

Rising Dividend Growth Fund’s 10 Year Performance |

Performance of a $10,000 investment, including any applicable sales charge, with distributions reinvested, from November 1, 2013 through October 31, 2023. |

| Average Annual Total Return through October 31, 2023* | One Year | Five Years | Ten Years | Since Inception | ||||||||||||||

| Class A | ||||||||||||||||||

Excluding sales charges | 3.71% | 9.42% | 8.04% | — | ||||||||||||||

Including sales charges | 1.99% | 8.19% | 7.43% | — | ||||||||||||||

| ||||||||||||||||||

| Class C | ||||||||||||||||||

Excluding contingent deferred sales charges | 2.90% | 8.60% | 7.23% | — | ||||||||||||||

Including contingent deferred sales charges | 1.87% | 8.60% | 7.23% | — | ||||||||||||||

| ||||||||||||||||||

| Institutional | 4.02% | 9.77% | 8.43% | — | ||||||||||||||

| ||||||||||||||||||

| Investor | 3.95% | 9.69% | 8.30% | — | ||||||||||||||

| ||||||||||||||||||

| Class R6 (Commenced February 28, 2018) | 4.03% | 9.77% | N/A | 8.86% | ||||||||||||||

| ||||||||||||||||||

| Class R | 3.41% | 9.15% | 7.77% | — | ||||||||||||||

| ||||||||||||||||||

| Class P (Commenced April 16, 2018) | 4.02% | 9.78% | N/A | 8.98% | ||||||||||||||

| ||||||||||||||||||