| |

| UNITED STATES |

| SECURITIES AND EXCHANGE COMMISSION |

| Washington, D.C. 20549 |

| |

| FORM 10-K |

| |

| (Mark One) |

| [X] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the fiscal year ended December 31, 2009 |

| OR |

| [ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the transition period from | | to |

| Commission File Number: 1-9916 |

|

| Freeport-McMoRan Copper & Gold Inc. |

| (Exact name of registrant as specified in its charter) |

| Delaware | 74-2480931 |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

| | |

| One North Central Avenue | |

| Phoenix, Arizona | 85004-4414 |

| (Address of principal executive offices) | (Zip Code) |

| |

| (602) 366-8100 |

| (Registrant's telephone number, including area code) |

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | | Name of each exchange on which registered |

| Common Stock, par value $0.10 per share | | New York Stock Exchange |

| 7% Convertible Senior Notes due 2011 of the registrant | | New York Stock Exchange |

| 6¾% Mandatory Convertible Preferred Stock, par value $0.10 per share | | New York Stock Exchange |

| Preferred Stock Purchase Rights | | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act R Yes 0 No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. 0 Yes R No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. R Yes 0 No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). R Yes 0 No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. R

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. R Large accelerated filer 0 Accelerated filer 0 Non-accelerated filer 0 Smaller reporting company

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). 0 Yes R No

The aggregate market value of common stock held by non-affiliates of the registrant was approximately $31.4 billion on February 12, 2010, and approximately $20.5 billion on June 30, 2009.

Common stock issued and outstanding was 430,565,147 shares on February 12, 2010, and 411,783,284 shares on June 30, 2009.

DOCUMENTS INCORPORATED BY REFERENCE

| Portions of our proxy statement for our 2010 annual meeting of stockholders are incorporated by reference into Part III (Items 10, 11, 12, 13 and 14) of this report. |

| |

FREEPORT-McMoRan COPPER & GOLD INC.

| TABLE OF CONTENTS |

| | |

| | Page |

| 1 |

| 1 |

| 41 |

| 58 |

| 58 |

| 60 |

| 61 |

| | |

| 61 |

| |

| 61 |

| 63 |

| |

| 67 |

| 116 |

| 183 |

| 183 |

| 183 |

| | |

| 183 |

| 183 |

| 183 |

| |

| 183 |

| 183 |

| 183 |

| | |

| 184 |

| 184 |

| | |

| S-1 |

| | |

| F-1 |

| | |

| E-1 |

Items 1. and 2. Business and Properties.

All of our periodic reports filed with the Securities and Exchange Commission (SEC) pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended, are available, free of charge, through our web site, www.fcx.com, including our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and any amendments to those reports. These reports and amendments are available through our web site as soon as reasonably practicable after we electronically file or furnish such material to the SEC.

References to “we,” “us” and “our” refer to Freeport-McMoRan Copper & Gold Inc. (FCX) and its consolidated subsidiaries, including, except as otherwise stated, Phelps Dodge Corporation (Phelps Dodge) and its subsidiaries, which we acquired on March 19, 2007. In 2008, we changed Phelps Dodge’s legal name to Freeport-McMoRan Corporation (FMC); therefore, references to FMC and Phelps Dodge represent the same entity. References to “Notes” refer to the “Notes to Consolidated Financial Statements” included herein (see Item 8. “Financial Statements and Supplementary Data”).

GENERAL

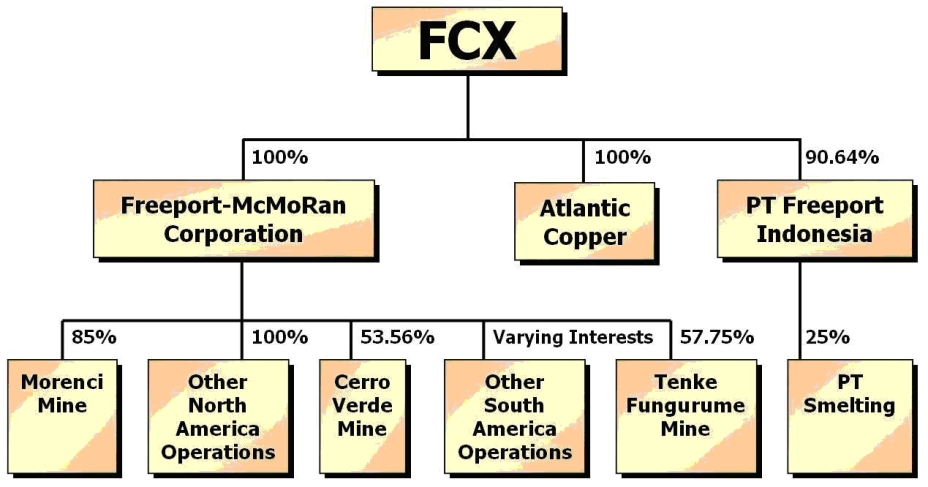

We are a leading international mining company with headquarters in Phoenix, Arizona. We are one of the world’s largest copper, gold and molybdenum mining companies in terms of reserves and production. Our portfolio of assets includes the Grasberg minerals district in Indonesia, which contains the largest single recoverable copper reserve and the largest single gold reserve of any mine in the world based on the latest available reserve data provided by third-party industry consultants; significant mining operations in North and South America; and the Tenke Fungurume minerals district in the Democratic Republic of Congo (DRC). We also operate Atlantic Copper, our wholly owned copper smelting and refining unit in Spain.

As a mining company, our principal assets are our reserves. At December 31, 2009, consolidated recoverable proven and probable reserves totaled 104.2 billion pounds of copper, 37.2 million ounces of gold, 2.59 billion pounds of molybdenum, 270.4 million ounces of silver and 0.78 billion pounds of cobalt. Approximately 33 percent of our copper reserves were in Indonesia, approximately 33 percent were in South America, approximately 26 percent were in North America and approximately eight percent were in Africa. Approximately 96 percent of our gold reserves were in Indonesia, with the majority of our remaining gold reserves located in South America. Our molybdenum reserves are primarily in North America (approximately 80 percent), with our remaining molybdenum reserves in South America (refer to “Ore Reserves”).

Our mining revenues for 2009 include sales of copper (approximately 75 percent), gold (approximately 17 percent) and molybdenum (approximately five percent). We currently have six operating copper mines in North America, four in South America, the Grasberg minerals district in Indonesia and the Tenke Fungurume minerals district in the DRC. We also have one operating primary molybdenum mine in North America. During 2009, approximately 61 percent of our consolidated copper production was from our Grasberg, Morenci and Cerro Verde mines, and more than half of our mined copper was sold in concentrate, approximately 25 percent as cathodes and approximately 21 percent as rod (principally from our North America operations). We also produce gold as a by-product at our copper mines, primarily at the Grasberg minerals district in Indonesia, which accounted for approximately 96 percent of our consolidated gold production for 2009. For 2009, approximately 50 percent of our consolidated molybdenum production was from the Henderson molybdenum mine and approximately 46 percent was produced as a by-product at our North America copper mines. Refer to “Mines” for further discussion of our mining operations.

Prior to March 19, 2007, we operated our Grasberg mine in Indonesia and Atlantic Copper. On March 19, 2007, we acquired Phelps Dodge, a fully integrated producer of copper and molybdenum with mines in North and South America, and several development projects, including Tenke Fungurume in the DRC. After completion of the Phelps Dodge acquisition, our business strategy was focused on repaying acquisition-related debt, defining the potential of our resources and developing expansion and growth plans to deliver additional volumes to a growing marketplace. During 2007, we repaid $10.0 billion in term loans using a combination of equity proceeds and internally generated cash flows. Because of the significant reduction in debt and historically high prices for copper, gold and molybdenum, our financial policy during most of 2008 was designed to use our cash flow to invest in growth projects with anticipated high rates of return and to return excess cash flows to stockholders in the form of dividends and share purchases. The dramatic declines in copper and molybdenum prices in late 2008 and the deterioration of the economic and credit environment limited our ability to invest in growth projects and

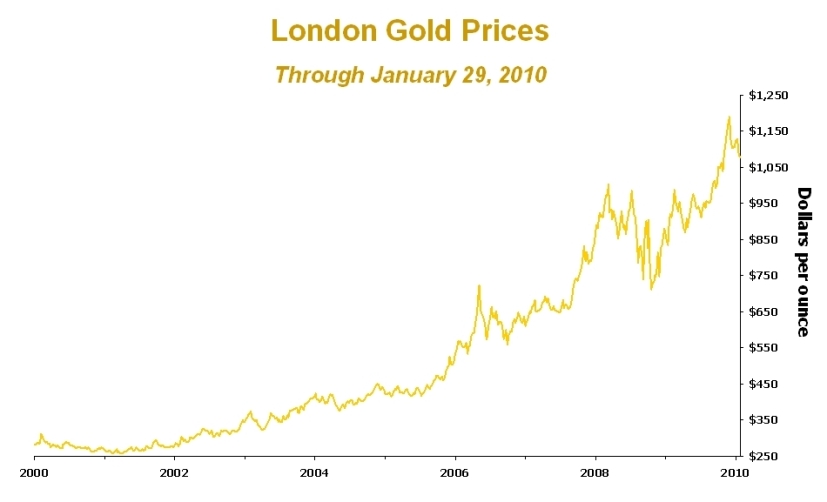

required us to make adjustments to our near-term plans in late 2008 and early 2009 (refer to Note 2 for further discussion). However, during 2009 copper prices improved from the January 2009 low of $1.38 per pound to $3.33 per pound on December 31, 2009, and subsequently closed at $3.11 per pound on January 29, 2010. Rising copper prices, along with higher volumes from the Grasberg mine and lower costs at our North America mines, enabled us to enhance our financial and liquidity position during 2009, allowing us to manage volatile conditions effectively, reduce debt and reinstate cash dividends to stockholders, while maintaining our future growth opportunities. In addition, we have announced initiatives to resume certain project development activities that were deferred in late 2008. For additional information, refer to Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

In North America, we currently have six operating copper mines – Morenci, Sierrita, Bagdad, Safford and Miami in Arizona, and Tyrone in New Mexico. In addition to copper, the Morenci, Sierrita and Bagdad mines produce molybdenum as a by-product. Although we currently are not conducting mining operations at our Chino mine in New Mexico, we continue to produce copper from leaching operations.

In South America, we have four operating copper mines – Cerro Verde in Peru, and Candelaria, Ojos del Salado and El Abra in Chile. In addition to copper, the Cerro Verde mine produces molybdenum concentrate as a by-product and the Candelaria and Ojos del Salado mines produce gold and silver as by-products.

In Indonesia, PT Freeport Indonesia operates the Grasberg minerals district. Our Grasberg minerals district also produces significant quantities of gold and silver as by-products. PT Freeport Indonesia also owns 25 percent of PT Smelting, a smelting and refining company in Gresik, Indonesia.

In Africa, we operate the Tenke Fungurume minerals district. In addition to copper, the Tenke Fungurume mine produces cobalt hydroxide. Copper production commenced in March 2009, and Tenke achieved targeted copper production rates in September 2009. We are continuing to address start-up and quality issues in the cobalt circuit and sustained targeted cobalt production rates are expected to be reached during 2010.

We produce molybdenum at our wholly owned Henderson molybdenum mine in Colorado, which is the largest primary producer of molybdenum in the world. Additionally, we own the Climax molybdenum mine in Colorado which is currently on care-and-maintenance status.

For information about our operating segments and financial data by geographic area refer to Note 20.

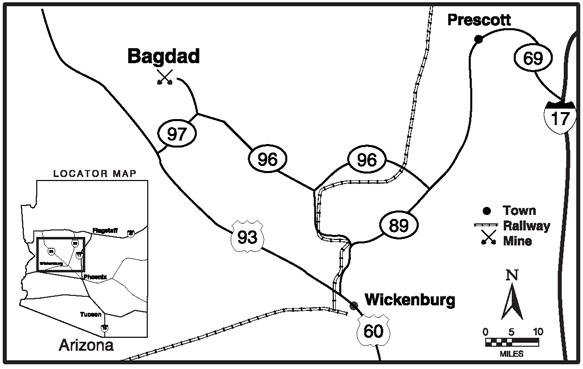

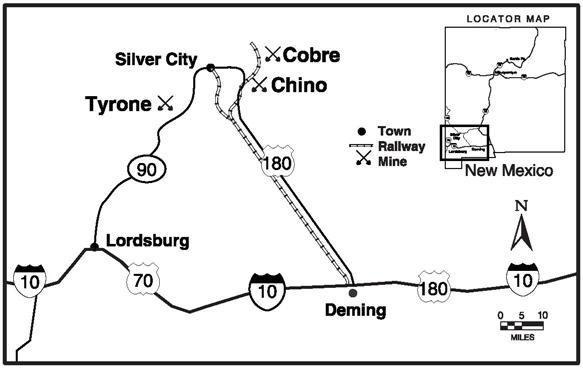

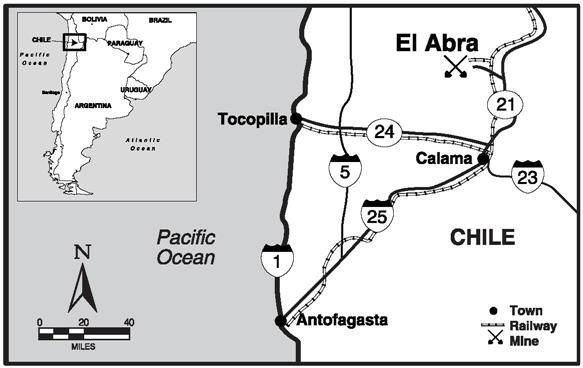

The locations of our operating mines are shown on the map below.

The diagram below shows our corporate structure.

COPPER, GOLD AND MOLYBDENUM

Our mines primarily produce copper, gold and molybdenum. A brief discussion of the production and sales of these metals appears below; discussion of markets and prices for these metals appears in Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

Copper

Copper, in the form of copper cathode, is an internationally traded commodity, and its prices are determined by the major metals exchanges – New York Mercantile Exchange (COMEX), the London Metals Exchange (LME) and the Shanghai Futures Exchange (SHFE). Prices on these exchanges generally reflect the worldwide balance of copper supply and demand and can be volatile and cyclical.

Our copper ores are generally processed either by smelting and refining or by solution extraction and electrowinning (SX/EW). Ore subject to the smelting process is crushed and further treated to produce a copper concentrate with an average copper content of about 30 percent. Copper concentrate is then smelted (subjected to extreme heat) to produce copper anodes, which weigh between 800 and 900 pounds each and have an average copper content of 99.5 percent. The anodes are further treated by electrolytic refining to produce copper cathodes, which weigh between 100 and 350 pounds each and have a copper content of 99.99 percent.

In the SX/EW process, copper is extracted from ore by dissolving it with a weak sulphuric acid solution. The copper content of the solution is increased in two additional solution-extraction stages and then the copper-bearing solution undergoes an electrowinning process to produce cathode that is 99.99 percent copper.

Our copper cathodes are used as the raw material input for copper rod, brass mill products and for other uses. In general, demand for copper reflects the rate of underlying world economic growth, particularly in industrial production and construction. According to Brook Hunt, a widely followed independent metals market consultant, copper’s end-use markets (and their estimated shares of total consumption) are:

| Construction | 35 | % |

| Electrical applications | 32 | % |

| Industrial machinery | 12 | % |

| Transportation | 11 | % |

| Consumer products | 10 | % |

Gold

Gold is used for jewelry, coinage and bullion as well as various industrial and electronic applications. Gold can be readily sold on numerous markets throughout the world. Benchmark prices are generally based on London Bullion Market Association quotations.

Molybdenum

Molybdenum is a key alloying element in steel and the raw material for several chemical-grade products used in catalysts, lubrication, smoke suppression, corrosion inhibition and pigmentation. Molybdenum as a high-purity metal is also used in electronics such as flat-panel displays and in super alloys used in aerospace. Molybdenum’s end-use markets and their share of total consumption are:

| Construction steel | 37 | % |

| Stainless steel | 21 | % |

| Chemicals | 13 | % |

| Tool and high-speed steel | 10 | % |

| Cast iron | 8 | % |

| Molybdenum metal | 7 | % |

| Super alloys | 4 | % |

Reference prices for molybdenum are available in several publications, including Platts Metals Week, Ryan’s Notes and Metal Bulletin.

PRODUCTS AND SALES

Copper Products

We are one of the world’s leading producers of copper concentrate, cathode and continuous cast copper rod. During 2009, approximately 61 percent of our consolidated copper production was from our Grasberg, Morenci and Cerro Verde mines, and more than half of our mined copper was sold in concentrate, approximately 25 percent as cathodes and approximately 21 percent as rod (principally from our North America operations).

Copper Concentrate. In 2009, we produced copper concentrate at seven mines, of which PT Freeport Indonesia is our largest producer. Approximately 50 percent of PT Freeport Indonesia’s concentrate production in 2009 was refined at affiliated smelters, Atlantic Copper and PT Smelting.

Copper concentrate was also produced at our Morenci, Sierrita and Bagdad mines in Arizona, and was generally shipped to our Miami smelter in Arizona. In South America, we produced copper concentrate at our Cerro Verde mine in Peru and our Candelaria and Ojos del Salado mines in Chile. We are initiating activities to restart the Morenci mill, which was temporarily idled in February 2009, to process available sulfide material currently being mined.

Copper Cathode. In 2009, we produced copper cathode at two electrolytic refineries and ten mines. Our refineries are located in El Paso, Texas, and Huelva, Spain. PT Smelting also produces copper cathode. We produced SX/EW cathode from our Morenci, Sierrita, Bagdad, Chino, Safford, Tyrone and Miami mines in North America and our Cerro Verde and El Abra mines in South America. In 2009, we began SX/EW production at our Tenke Fungurume mine in the DRC.

Continuous Cast Copper Rod. We manufacture continuous cast copper rod at our facilities in El Paso, Texas; Norwich, Connecticut and Miami, Arizona.

Other Copper Products. We produce specialty copper products at our Bayway operations in Elizabeth, New Jersey. These products include specialty copper alloys in the forms of rod, bar and strip. We manufacture electrode wire for use in welding steel cans at our Norwich, Connecticut and El Paso, Texas, facilities. We also produce copper sulfate pentahydrate for use in agricultural and industrial applications at our facility in Sierrita, Arizona.

Copper Sales

North America. The majority of the copper produced at our North America copper mines and refined in our El Paso refinery is consumed at our rod plants in El Paso, Texas; Norwich, Connecticut and Miami, Arizona. The remainder of our North America copper production is sold in the form of copper cathode or copper concentrate to third parties. Generally, copper rod and cathode are sold to wire and cable fabricators and brass mills under United States (U.S.) dollar-denominated, annual contracts. Cathode and rod contract prices are generally based on the prevailing COMEX monthly average spot price for the month of shipment and include a premium.

South America. Production from our South America copper mines is generally sold as copper concentrate or copper cathode under U.S. dollar-denominated, annual and multi-year contracts. Cerro Verde sells approximately 70 percent of its production as concentrate and the rest as cathode. Some of Cerro Verde’s cathode is sold under annual contract terms to South American customers. Approximately 22 percent of Cerro Verde’s and 11 percent of Candelaria’s 2009 concentrate production was sold at market rates to Atlantic Copper. A majority of our Ojos del Salado concentrate production is sold to local Chilean smelters. El Abra’s cathode production is sold primarily under annual or multi-year contracts to Asian or European rod or brass mill customers, or to merchants. The remainder of the cathode and concentrate production is primarily sold under long-term contracts to external customers, largely located in Asia, with the balance sold on a spot basis.

Our South America sales are priced based on the LME monthly average spot price. Cathode sales are generally priced in the month of arrival at the buyer’s facilities and generally include a premium. Substantially all of our concentrate sales are priced in the third calendar month following the month of arrival at the buyer’s facilities. Revenues from South America concentrate sales are recorded net of treatment and refining charges. Treatment and refining charges are fees paid to smelters and refiners and are generally negotiated annually. Moreover, because a portion of the metals contained in copper concentrates is unrecoverable from the smelting process, our revenues from concentrate sales are also recorded net of allowances based on the quantity and value of these unrecoverable metals. These allowances are a negotiated term of our contracts and vary by customer.

Indonesia. PT Freeport Indonesia sells its production in the form of copper concentrate, which contains significant quantities of by-product gold and silver, under U.S. dollar-denominated sales agreements. During 2009, approximately half of PT Freeport Indonesia’s production was sold to Atlantic Copper and PT Smelting. PT Freeport Indonesia sells substantially all of its budgeted production of copper concentrates under long-term contracts. In general, most of its concentrate sales are priced on the basis of the LME average spot price for either the first, second or third calendar month following the month of arrival at the buyer’s facilities.

PT Freeport Indonesia has a long-term contract to provide Atlantic Copper with approximately 55 percent of its current concentrate requirements at market prices.

PT Freeport Indonesia’s contract with PT Smelting provides for the supply of 100 percent of the copper concentrate requirements necessary to produce 205,000 metric tons of copper annually (essentially the smelter’s original design capacity) on a priority basis. Refer to “Smelting Facilities” for further discussion.

We anticipate that PT Freeport Indonesia will sell approximately 60 percent of its annual concentrate production to Atlantic Copper and PT Smelting in 2010. A summary of PT Freeport Indonesia’s aggregate percentage concentrate sales to PT Smelting, Atlantic Copper and to other parties for the last three years follows:

| | | 2009 | | 2008 | | 2007 |

| PT Smelting | | 32% | | 41% | | 39% |

| Atlantic Copper | | 18% | | 15% | | 25% |

| Other parties | | 50% | | 44% | | 36% |

| | | 100% | | 100% | | 100% |

| | | | | | | |

PT Freeport Indonesia’s sales to PT Smelting represented approximately 13 percent of our consolidated revenues in 2009, approximately eight percent in 2008 and approximately 11 percent in 2007. No other customer accounted for more than 10 percent of our consolidated revenues in any of the three years ended December 31, 2009.

Revenues from our Indonesia concentrate sales are recorded net of royalties (refer to “Mines – Indonesia – Contracts of Work”), and treatment and refining charges (including price participation charges, if applicable, based on the market prices of metals). Similar to our South America mines, Indonesia concentrate sales are net of allowances for unrecoverable metals. PT Freeport Indonesia sells a small amount of copper concentrates in the spot market.

Africa. Copper produced at our Tenke Fungurume mining district is generally sold as copper cathode under U.S. dollar denominated contracts priced based on the LME monthly average spot price for the month after the month of shipment.

Europe. Atlantic Copper sells copper cathode directly to rod and brass mills, primarily located in Europe. Atlantic Copper has occasionally sold copper cathode to merchants. Copper cathode is generally sold under annual contracts and priced based on the LME average spot price for the month of arrival at the buyer’s facilities.

Gold Products and Sales

We also produce gold as a by-product, primarily at the Grasberg minerals district, which accounted for approximately 96 percent of our consolidated gold production in 2009. Gold is primarily sold as a component of our copper concentrate or in slimes, which are a by-product of the smelting and refining process. Gold generally is priced at the average London Bullion Market Association price for a specified month near the month of shipment.

Molybdenum Products and Sales

We are the world’s largest producer of molybdenum and molybdenum-based chemicals. In addition to production from our Henderson molybdenum mine, we produce by-product molybdenum at our Morenci, Sierrita and Bagdad mines in Arizona and at our Cerro Verde mine in Peru. For 2009, approximately half of our consolidated molybdenum production was from the Henderson molybdenum mine and approximately 46 percent was produced as a by-product at the North America mines.

The majority of our molybdenum concentrates are processed in our own conversion facilities. Technical-grade oxide is produced from molybdenum concentrates in Sierrita, Arizona; Fort Madison, Iowa and Rotterdam, the Netherlands. Ferromolybdenum is produced from technical-grade oxide in Stowmarket, United Kingdom through a metallothermic reduction process. High-quality molybdenum concentrates are converted into molybdenum chemicals at Fort Madison, Iowa and Rotterdam, the Netherlands. Molybdenum generally is priced based on the average Platts Metals Week price for the month of shipment. Approximately 90 percent of our expected 2010 molybdenum sales are expected to be priced at prevailing market prices.

Other Products and Sales

We produce cobalt as a cobalt hydroxide intermediate by-product of copper production at the Tenke Fungurume mine in the DRC and silver as a component of our copper concentrate or in slimes. Cobalt hydroxide intermediate product is priced based on a discount to the average monthly price published by Metal Bulletin for a specified month near the month of shipment and silver generally is priced at the average London Bullion Market Association price for a specified month near the month of shipment. Sales of cobalt and silver, along with other by-product metals such as rhenium and magnetite, do not represent a significant component of our total revenues.

For an allocation of our consolidated revenues by geographic area, refer to Note 20.

MINES

Curtailed Facilities

The following table summarizes the temporary curtailments announced in late 2008 and early 2009 in response to market conditions. For additional information, refer to Note 2. In addition, refer to Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations” for further discussion of our current development projects.

| Facility | | Date of Announcement | | Announced Reductions | | Current Status |

| Copper | | | | | | |

| North America | | | | | | |

· Morenci | | December 2008 and January 2009 | | 25 percent reduction in mining and crushed-leach rates in December 2008 and an additional reduction in January 2009 for a total 50 percent reduction in mining and crushed-leach rates. | | Activities to restart mill commenced in 2010. Mine continues to operate at reduced rates. |

· Chino | | December 2008 | | Suspension of mining and milling activities. Leaching activities from stockpiles continues. | | No change. |

· Safford | | December 2008 | | 50 percent reduction in mining and stacking rates. | | Continuing to operate at reduced rates. |

· Tyrone | | December 2008 | | 50 percent reduction in mining rate. | | Operating at 80 percent of capacity. |

· Miami | | December 2008 | | Deferral of restart of the Miami mine. | | Restart activities resumed in late 2009. |

| South America | | | | | | |

· Cerro Verde | | January 2009 | | Deferral of incremental mill expansion | | Mill expansion activities resumed in late 2009; continue to study long-term expansion opportunities. |

· Candelaria/ Ojos del Salado | | January 2009 | | Reduction in mining rates. | | Continuing to operate at reduced rates. |

· El Abra | | December 2009 | | Deferral of development of sulfide ores. | | Resumed development activities. |

| | | | | | | |

| Molybdenum | | | | | | |

· Henderson | | November 2008 and January 2009 | | 40 percent reduction in mining and milling rates. | | Mining rates currently at 80 percent of capacity. |

· Climax | | November 2008 | | Deferral of restart of the Climax mine. | | No change. |

· Cerro Verde | | January 2009 | | Suspension of molybdenum by-product production. | | Molybdenum by-product production resumed in fourth quarter of 2009. |

We are continuing to closely monitor market conditions and may make further adjustments to our production and sales plans.

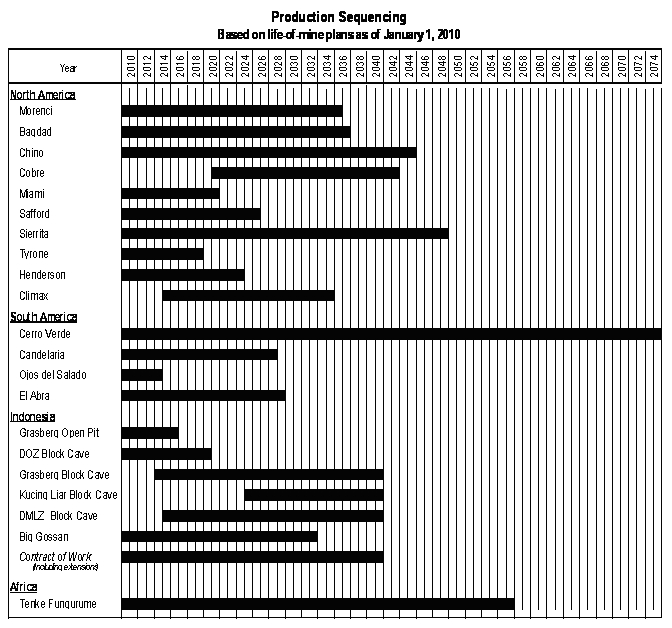

Following are maps and descriptions of our North America (including Molybdenum operations), South America, Indonesia and Africa mining operations.

North America

In the U.S., most of the land occupied by our copper and molybdenum mines, concentrators, SX/EW facilities, smelter, refinery, rod mills, molybdenum roasters and processing facilities is generally owned by us or is located on unpatented mining claims owned by us. Certain portions of our Sierrita, Bagdad, Miami, Tyrone, Chino, Cobre and Henderson operations are located on government-owned land and are operated under a Mine Plan of Operations or other use permit. Various federal and state permits or leases on government land are held for purposes incidental to mine operations.

Morenci

We own an 85 percent undivided interest in Morenci, with the remaining 15 percent owned by affiliates of Sumitomo Corporation. Each partner takes in kind its share of Morenci’s production.

Morenci is an open-pit copper mining complex that has been in continuous operation since 1939 and previously was mined through underground workings. Morenci is located in Greenlee County, Arizona, approximately 50 miles northeast of Safford on U.S. Highway 191. The site is accessible by a paved highway and a railway spur. The Morenci mine is a porphyry copper deposit that has oxide and secondary sulfide mineralization, and primary sulfide mineralization. The predominant oxide copper mineral is chrysocolla. Chalcocite is the most important secondary copper sulfide mineral with chalcopyrite as the dominant primary copper sulfide. The Morenci operation consists of a 49,000 metric ton-per-day concentrator, that when operating produces copper and molybdenum concentrate; a 72,000 metric ton-per-day crushed-ore leach pad and stacking system; a large low-grade run-of-mine (ROM) leaching system; four SX plants; and three EW tank houses that produce copper cathode. Total EW tank house capacity is approximately 916 million pounds of copper per year. Copper production for 2009 was 504 million pounds, including our partner’s share, which reflects the revised operating plan reducing the mining and crushed leach rate by 50 percent beginning in late 2008 and early 2009. The available mining fleet consists of 102 235-metric ton haul trucks loaded by 18 shovels with bucket sizes ranging from 47 to 55 cubic meters, which are capable of moving over 750,000 metric tons of material per day.

The concentrate leach, direct-electrowinning facility at Morenci was commissioned in third-quarter 2007 and produced copper concentrate until early 2009. We placed this facility on care-and-maintenance in first-quarter 2009 as part of our revised operating plan.

Morenci is located in a desert environment with rainfall averaging 13 inches per year. The highest bench elevation is 1,950 meters above sea level and the ultimate pit bottom is expected to have an elevation of 900 meters above sea level. The Morenci operation encompasses approximately 53,944 acres, comprising 47,609 acres of patented mining claims and other fee lands, 5,914 acres of unpatented mining claims, and 421 acres of land held by state or federal permits, easements and rights-of-way.

Morenci receives electrical power from Tucson Electric Power Company, Arizona Public Service Company and the Luna Energy facility in Deming, New Mexico (in which we own a one-third interest). Although we believe the Morenci operation has sufficient water sources to support currently planned mining operations, we are a party to litigation that could adversely affect our water rights at Morenci and at our other properties in Arizona. Refer to Item 3. “Legal Proceedings,” for information concerning the status of these proceedings.

Sierrita

Our wholly owned Sierrita mine has been in operation since 1959 and is an open-pit copper and molybdenum mining complex located in Pima County, Arizona, approximately 20 miles southwest of Tucson and seven miles west of the town of Green Valley and Interstate Highway 19. The site is accessible by a paved highway and by rail. The Sierrita mine is a porphyry copper deposit that has oxide and secondary sulfide mineralization, and primary sulfide mineralization. The predominant oxide copper minerals are malachite, azurite and chrysocolla. Chalcocite is the most important secondary copper sulfide mineral, and chalcopyrite and molybdenite are the dominant primary sulfides.

The Sierrita operation includes a 102,000 metric ton-per-day concentrator that produces copper and molybdenum concentrates. Sierrita also produces copper from a ROM oxide-leaching system. Cathode copper is plated at the Twin Buttes EW facility, which has a design capacity of approximately 50 million pounds of copper per year. In 2004, a copper sulfate crystal plant began production. The facility has the capacity to produce 40 million pounds of copper sulfate per year. The Sierrita operation also has molybdenum facilities consisting of a leaching circuit, two molybdenum roasters and a packaging facility. The molybdenum facilities process Sierrita concentrate, concentrate from our other mines and concentrate from third-party sources. Copper production for 2009 was 170 million pounds and molybdenum production was 19 million pounds. The available mining fleet has the capacity to move an average of 200,000 metric tons of material per day using 24 235-metric ton haul trucks loaded by four shovels with bucket sizes ranging from 34 to 56 cubic meters.

Sierrita is located in a desert environment with rainfall averaging 12 inches per year. The highest bench elevation is 1,350 meters above sea level and the ultimate pit bottom is expected to be 550 meters above sea level. The Sierrita operation, including the recently acquired Twin Buttes site, encompasses approximately 23,418 acres, comprising 13,282 acres of patented mining claims and other fee lands, 9,644 acres of unpatented mining claims, 5,913 acres of Arizona state mineral leases and 2,024 acres of leased lands.

Sierrita receives electrical power through long-term contracts with the Tucson Electric Power Company. Although we believe the Sierrita operation has sufficient water resources to support currently planned mining operations, we are a party to litigation that could adversely affect our water rights at Sierrita and at our other properties in Arizona. Refer to Item 3. “Legal Proceedings,” for information concerning the status of these proceedings.

Bagdad

Bagdad is a wholly owned open-pit copper and molybdenum mining complex located in Yavapai County in west-central Arizona. It is approximately 60 miles west of Prescott and 100 miles northwest of Phoenix. The property can be reached by Arizona Highway 96, which ends at the town of Bagdad. The closest railroad siding is at Hillside, Arizona, approximately 24 miles southeast on Arizona Highway 96. The open-pit mining operation has been ongoing since 1945, and prior mining was conducted through underground workings. The Bagdad mine is a porphyry copper deposit containing both sulfide and oxide mineralization. Chalcopyrite and molybdenite are the dominant primary sulfides and are the primary economic minerals in the mine. Chalcocite is the most common secondary copper sulfide mineral, and the predominant oxide copper minerals are chrysocolla, malachite and azurite.

The Bagdad operation consists of a 75,000 metric ton-per-day concentrator that produces copper and molybdenum concentrates, an SX/EW plant that can produce up to 25 million pounds per year of copper cathode from solution generated by low-grade dump leaching and a pressure leach plant to process molybdenum concentrate. Copper production for 2009 was 225 million pounds and molybdenum production was six million pounds. The available mining fleet has the capacity to move in excess of 180,000 metric tons of material per day using 24 235-metric ton haul trucks loaded by five shovels with bucket sizes ranging from 40 to 56 cubic meters.

Bagdad is located in a desert environment with rainfall averaging 15 inches per year. The highest bench elevation is 1,200 meters above sea level and the ultimate pit bottom is expected to be 475 meters above sea level. The Bagdad operation encompasses approximately 21,743 acres, comprising 21,143 acres of patented mining claims and other fee lands, and 600 acres of unpatented mining claims.

Bagdad receives electrical power from Arizona Public Service Company. Although we believe the Bagdad operation has sufficient water resources to support currently planned mining operations, we are a party to litigation that could adversely affect our water rights at Bagdad and at our other properties in Arizona. Refer to Item 3. “Legal Proceedings,” for information concerning the status of these proceedings.

Safford

Safford is a wholly owned open-pit copper mining complex located in Graham County, Arizona, approximately eight miles north of the town of Safford and 170 miles east of Phoenix. The site is accessible by paved county road off U.S. Highway 70. The Safford mine includes two copper deposits that have oxide mineralization overlaying primary copper sulfide mineralization. The predominant oxide copper minerals are chrysocolla and copper-bearing iron oxides with the predominant copper sulfide material being chalcopyrite.

Initial production commenced in late 2007 and ramped up to full production capacity during 2008 before operating plans were revised in fourth-quarter 2008 to curtail production.

The property is a mine-for-leach project and produces copper cathodes. The operation consists of two open pits feeding a crushing facility with a capacity of 103,000 metric tons per day of crushed ore. The crushed ore is delivered to a single leach pad by a series of overland and portable conveyors. Leach solutions feed an SX/EW facility with a capacity of 240 million pounds of copper per year. Copper production for 2009 was 184 million pounds, which reflects the revised operating plan reducing the mining and stacking rate by 50 percent beginning in late 2008. The available mining fleet consists of 23 235-metric ton haul trucks loaded by five shovels with

bucket sizes ranging from 31 to 34 cubic meters, which are capable of moving an average of approximately 285,000 metric tons of material per day.

Safford is located in a desert environment with rainfall averaging 10 inches per year. The highest bench elevation is 1,250 meters above sea level and the ultimate pit bottom is expected to have an elevation of 750 meters above sea level. The Safford operation encompasses approximately 24,957 acres, comprising 20,994 acres of patented lands, 3,932 acres of unpatented lands and 31 acres of land held by federal permit.

The Safford operation’s electrical power is provided by Morenci Water and Electric Company, a wholly owned subsidiary of FCX, through the transmission systems of Southwest Transmission Cooperative, a subsidiary of Arizona Electric Power Cooperative, Inc., with most of the power sourced from the Luna Energy facility. Although we believe the Safford operation has sufficient water resources to support currently planned mining operations, we are a party to litigation that could adversely impact the water rights at Safford and at our other properties in Arizona. Refer to Item 3. “Legal Proceedings,” for information concerning the status of these proceedings.

Miami

Miami is a wholly owned open-pit copper mining complex located in Gila County, Arizona, approximately 90 miles east of Phoenix and six miles west of the city of Globe on U.S. Highway 60. The site is accessible by a paved highway and by rail. The Miami mine is developed on a porphyry copper deposit that has leachable oxide and secondary sulfide mineralization. The predominant oxide copper minerals are chrysocolla, copper-bearing clays, malachite and azurite; chalcocite and covellite are the most important secondary copper sulfide minerals.

Since about 1915, the Miami mining operation had processed copper ore using both flotation and leaching technologies; currently, and since 2002, operations have consisted of residual leaching of stockpiles with copper recovered (from solution) by the SX/EW process. The design capacity of the SX/EW plant is 200 million pounds of copper per year. Copper production for 2009 was 16 million pounds. The available mining fleet consists of 24 227-metric ton haul trucks loaded by 3 shovels with bucket sizes ranging from 31 to 34-cubic meters, which are capable of moving an average of approximately 155,000 metric tons of material per day.

In fourth-quarter 2009, we initiated plans to restart limited mining activities at the Miami mine, which will improve efficiencies of ongoing reclamation projects associated with historical mining activities at the site. During the approximate five-year mine life, we expect to ramp up production to approximately 100 million pounds of copper per year by the second half of 2011. We will be investing approximately $40 million in this project, which will benefit from the use of existing mine equipment.

Miami is located in a desert environment with rainfall averaging 18 inches per year. The highest bench elevation is 1,390 meters above sea level, and the ultimate pit bottom will have an elevation of 810 meters above sea level. The Miami operation encompasses approximately 9,058 acres comprising 8,725 acres of patented mining claims and other fee lands, and 333 acres of unpatented mining claims.

Miami receives electrical power through long-term contracts with the Salt River Project and natural gas through long-term contracts with El Paso Natural Gas as the transporter. Although we believe the Miami operation has sufficient water resources to support currently planned mining operations, we are a party to litigation that could

adversely impact the water rights at Miami and at our other properties in Arizona. Refer to Item 3. “Legal Proceedings,” for information concerning the status of these proceedings.

Tyrone

Our wholly owned Tyrone mine is an open-pit copper mining complex which has been in operation since 1967. It is located in southwestern New Mexico in Grant County, approximately 10 miles south of Silver City, New Mexico, along State Highway 90. The site is accessible by paved road. The Tyrone mine is a porphyry copper deposit. Mineralization is predominantly secondary sulfide consisting of chalcocite.

Copper processing facilities consist of an SX/EW operation with a maximum capacity of 168 million pounds of copper cathodes per year. Copper production for 2009 was 86 million pounds, reflecting the revised operating plan which reduced the mining rate by 50 percent beginning in late 2008. The mining rate increased during 2009, and the mine is currently operating at approximately 80 percent of capacity. The available mining fleet has the capacity to move an average of 120,000 metric tons of material per day using 15 240-metric ton haul trucks loaded by three shovels with bucket sizes ranging from 17 to 42 cubic meters.

Tyrone is located in a desert environment with rainfall averaging 16 inches per year. The highest bench elevation is 2,000 meters above sea level and the ultimate pit bottom is expected to have an elevation of 1,500 meters above sea level. The Tyrone operation encompasses approximately 35,200 acres, comprising 18,755 acres of patented mining claims and other fee lands, and 16,445 acres of unpatented mining claims (includes 1,116 acres overlaying federal minerals on previously counted fee lands).

Tyrone receives electrical power from the Luna Energy facility and from the open market. Tyrone also has the ability to self-generate power. We believe the Tyrone operation has sufficient water resources to support currently planned mining operations.

Henderson

Our wholly owned Henderson molybdenum mine has been in operation since 1976 and is located approximately 42 miles west of Denver, Colorado, off U.S. Highway 40. Nearby communities include the towns of Empire, Georgetown and Idaho Springs. The Henderson mill site is located approximately 15 miles west of the mine and is accessible from Colorado State Highway 9. The Henderson mine and mill are connected by a 10-mile conveyor tunnel under the Continental Divide and an additional five-mile surface conveyor. The tunnel portal is located five miles east of the mill. The Henderson mine is a porphyry molybdenum deposit with molybdenite as the primary sulfide mineral.

The Henderson operation consists of a large block-cave underground mining complex feeding a concentrator with a current capacity of approximately 29,000 metric tons-per-day. Henderson has the capacity to produce approximately 40 million pounds of molybdenum per year. The majority of the molybdenum concentrate produced is shipped to our Fort Madison, Iowa, processing facility. Molybdenum production for 2009 was 27 million pounds, which reflects the revised operating plan reducing Henderson’s annual production by 40 percent beginning in late 2008 and early 2009. Conditions improved somewhat during 2009 and Henderson is currently operating at approximately 80 percent of capacity. The available underground mining equipment fleet consists of 13 nine-metric ton load-haul-dump (LHD) units and seven 36- and 73-metric ton haul trucks, which feed a gyratory crusher feeding a series of three overland conveyors to the mill stockpiles.

The Henderson mine is located in a mountain region with the main access shaft at 3,180 meters above sea level. The main production levels are currently at elevations of 2,200 and 2,350 meters above sea level. This region experiences significant snowfall during the winter months.

The Henderson mine and mill operations encompass approximately 11,878 acres, comprising 11,843 acres of patented mining claims and other fee lands, and a 35-acre easement with the U.S. Forest Service for the surface portion of the conveyor corridor.

Henderson operations receive electrical power through long-term contracts with Xcel Energy and natural gas through long-term contracts with BP Energy, with Xcel Energy as the transporter. We believe the Henderson operation has sufficient water resources to support currently planned mining operations.

Non-Operating North America Mines

In addition to the currently operating mines described above, we have three non-operating copper mines in Arizona: Ajo, Bisbee and Tohono; two in New Mexico: Chino (with limited residual copper production from leaching operations) and Cobre; and the Climax molybdenum mine in Colorado, all of which are currently on care-and-maintenance status.

In response to market conditions during fourth-quarter 2008, we placed the Chino mine on care-and-maintenance status in December 2008. The remainder of these copper mines have been on care-and-maintenance status for several years and would require significant capital investment to return them to operating status. Several of the non-operating Arizona and New Mexico copper mines continue to produce copper cathode from stockpiles. Copper production in 2009 from these mines totaled 36 million pounds.

During fourth-quarter 2008, we also suspended construction activities associated with the project to restart the Climax molybdenum mine, which would have an annual capacity of 30 million pounds of molybdenum with expansion options. We continue to monitor market conditions to determine timing for restarting construction of this project. Once a decision is made to resume construction activities, the project could be completed within 18 months. Remaining costs for the project are estimated to approximate $350 million.

South America

At our operations in South America, mine properties and facilities are controlled through mining claims or concessions under the general mining laws of the relevant country. The claims or concessions are owned or controlled by the operating companies in which we or our subsidiaries have an ownership interest. Roads, power lines and aqueducts are controlled by easements.

Cerro Verde

We have a 53.56 percent ownership interest in Cerro Verde. The remaining 46.44 percent is held by SMM Cerro Verde Netherlands B.V. (21.0 percent), Compañia de Minas Buenaventura S.A.A. (19.3 percent) and other stockholders whose shares are publicly traded on the Lima Stock Exchange (6.14 percent).

Cerro Verde is an open-pit copper and molybdenum mining complex that has been in operation since 1976 and is located 20 miles southwest of Arequipa, Peru. The site is accessible by paved highway. The Cerro Verde mine is a porphyry copper deposit that has oxide and secondary sulfide mineralization, and primary sulfide mineralization. The predominant oxide copper minerals are brochantite, chrysocolla, malachite and copper “pitch.” Chalcocite and covellite are the most important secondary copper sulfide minerals. Chalcopyrite and molybdenite are the dominant primary sulfides.

Cerro Verde’s current operation consists of an open-pit copper mine, concentrator and SX/EW leaching facilities. Leach copper production is derived from a 39,000 metric ton-per-day crushed leach facility and a ROM leach system. This leaching operation has a capacity of approximately 200 million pounds of copper per year. A 108,000 metric ton-per-day concentrator was completed in late 2006 and began processing of sulfide ore in the fourth quarter of 2006. Copper production for 2009 was 662 million pounds and molybdenum production was 2 million pounds. We have commenced a project to optimize throughput at the concentrator. The project, which is expected to be completed by the end of 2010, is designed to add 30 million pounds of additional copper production per year by increasing mill throughput from 108,000 metric tons of ore per day to 120,000 metric tons of ore per day. The total capital investment for this project is expected to approximate $50 million.

Cerro Verde has sufficient equipment to move an average of 308,000 metric tons of material per day using an available fleet of 28 180-metric ton and 230-metric ton haul trucks loaded by five shovels with bucket sizes ranging in size from 21 to 53 cubic meters.

Approximately one-third of Cerro Verde’s copper cathode production is sold locally and the remaining copper cathodes and concentrate production are transported approximately 70 miles by truck and rail to the Pacific Port of Matarani for shipment to international markets.

Cerro Verde is located in a desert environment with rainfall averaging 1.5 inches per year and is in an active seismic zone. The highest bench elevation is 2,900 meters above sea level and the ultimate pit bottom is expected to be 2,000 meters above sea level. Cerro Verde has a mining concession covering approximately 157,007 acres plus 24 acres of owned property and 79 acres of rights-of-way outside the mining concession area.

Cerro Verde receives electrical power under long-term contracts with Electroperu and Empresa de Generación Eléctrica de Arequipa. Water for our Cerro Verde processing operations comes from renewable sources through a series of storage reservoirs on the Rio Chili watershed that collect water primarily from seasonal precipitation. Cerro Verde’s participation in the Pillones Reservoir Project has secured water rights that we believe will be sufficient to support Cerro Verde’s currently planned operations. With the completion of the Bamputañe dam during 2009, an additional 40 million cubic meters of water storage was added to the system. For a discussion of risks associated with the availability of water, see Item 1A. – “Risk Factors.”

El Abra

We own a 51 percent interest in El Abra. The remaining 49 percent interest is held by the state-owned copper enterprise Corporación Nacional del Cobre de Chile (CODELCO).

El Abra is an open-pit copper mining complex that has been in operation since 1996 and is located 47 miles north of Calama in Chile’s El Loa province, Region II. The site is accessible by paved highway and by rail. The El Abra mine is a porphyry copper deposit that has oxide and sulfide mineralization. The predominant oxide copper minerals are chrysocolla and pseudomalachite. There are lesser amounts of copper-bearing clays and tenorite. The predominant primary sulfide copper minerals are bornite and chalcopyrite. There is a minor amount of secondary sulfide mineralization as chalcocite.

The El Abra operation consists of an open-pit copper mine and an SX/EW facility with a capacity of 500 million pounds of copper cathode per year from a 120,000 metric ton-per-day crushed leach circuit and a similar-sized, ROM leaching operation. Copper production for 2009 was 358 million pounds. The mining operation has sufficient equipment to move an average of 223,000 metric tons of material per day using an available fleet of 26 220-metric ton haul trucks loaded by four shovels with buckets ranging in size from 26 to 41 cubic meters.

We have resumed construction activities associated with the development of a large sulfide deposit at El Abra that will extend the mine life by over ten years. Production from the sulfide ore, which will be ramping up to approximately 300 million pounds of copper per year is expected to begin in 2012 and will replace the current oxide copper production that is expected to decline over the next several years. The project will use a portion of the existing facilities to process the additional sulfide ore. Total capital for the project is estimated to approximate $700 million through 2015, of which approximately $500 million is for the initial phase of the project that is expected to be completed in 2012.

El Abra is located in a desert environment with rainfall averaging less than one inch per year and is in an active seismic zone. The highest bench elevation is 4,180 meters above sea level and the ultimate pit bottom is expected to be 3,410 meters above sea level. El Abra controls a total of 110,268 acres of mining claims covering the ore deposit, stockpiles, process plant, and water wellfield and pipeline. In addition, El Abra has acquired land surface rights for the road between the processing plant and the mine, the water wellfield, power transmission lines and for the water pipeline from the Salar de Ascotán.

El Abra currently receives electrical power under a contract with Electroandina, which will expire at the end of 2017. Water for our El Abra processing operations comes from pumping of groundwater from the Salar de Ascotán pursuant to regulatory approval. We believe El Abra has sufficient water rights to support current operations. For a discussion of risks associated with the availability of water, see Item 1A. – “Risk Factors.”

Candelaria and Ojos del Salado

Candelaria. We have an 80 percent ownership interest in Candelaria. The remaining 20 percent interest is owned by affiliates of Sumitomo Corporation.

Candelaria’s open-pit mine has been in operation since 1993 and the underground mine has been in operation since 2005. The Candelaria copper mining complex is located approximately 12 miles south of Copiapó in northern Chile’s Atacama province, Region III. The site is accessible by two maintained dirt roads, one coming through the Tierra Amarilla community and the other off of Route 5 of the International Pan-American Highway. The Candelaria mine is an iron oxide, copper/gold deposit. Primary sulfide mineralization consists of chalcopyrite.

The Candelaria operation consists of an open-pit copper mine and a 6,000 metric ton-per-day underground copper mine, which is mined by sublevel stoping, feeding a 75,000 metric ton-per-day concentrator. On average, open-pit mining operations move 235,000 metric tons of material per day using an available fleet of 38 225-metric ton haul trucks loaded by six shovels with bucket sizes ranging from 13 to 43 cubic meters. Copper concentrates are transported by truck to the Punta Padrones port facility located in Caldera, approximately 50 miles northwest of the mine. Copper production for 2009 was 296 million pounds and gold production was 74,000 ounces.

Candelaria is located in a desert environment with rainfall averaging less than one inch per year and is in an active seismic zone. The highest bench elevation is 675 meters above sea level and the ultimate pit bottom is expected to be 30 meters below sea level. The Candelaria property encompasses approximately 13,390 acres, including approximately 125 acres for the port facility in Caldera. The remaining property consists of mineral rights owned by us in which the surface is not owned but controlled by us, which is consistent with Chilean law. Candelaria receives electrical power through long-term contracts with Empresa Eléctrica Guacolda S.A., a local energy company. Candelaria’s water supply comes from well fields in the area of Tierra Amarilla and Copiapó that draw water from the Copiapó River aquifer. Because of rapid depletion of that aquifer in recent years, ongoing studies are addressing the adequacy of this water supply for Candelaria’s currently planned operations. For a discussion of risks associated with the availability of water, see Item 1A. – “Risk Factors.”

Ojos del Salado. We have an 80 percent ownership interest in Ojos del Salado. The remaining 20 percent interest is owned by affiliates of Sumitomo Corporation.

The Ojos del Salado operation began commercial production in 1929 and consists of two underground copper mines (Santos and Alcaparrosa) and a 3,800 metric ton-per-day concentrator. The operation is located approximately 10 miles east of Copiapó in northern Chile’s Atacama province, Region III, and is accessible by paved highway. The Ojos del Salado mines are iron oxide and copper/gold deposits. Primary sulfide mineralization consists of chalcopyrite.

The Ojos del Salado operation has a capacity of 3,800 metric tons per day of ore from the Santos underground mine and 4,000 metric tons of ore per day from the Alcaparrosa underground mine. The ore from both mines is mined by sublevel stoping since both the ore and enclosing rocks are competent. The broken ore is removed from the stopes using scoops and loaded into an available fleet of 18 28-metric ton trucks, which transport the ore to the surface. The ore from the Santos mine is hauled directly to the Ojos del Salado mill for processing, and the

ore from the Alcaparrosa mine is reloaded into five 54-metric ton trucks and hauled seven miles to the Candelaria mill for processing. The Ojos del Salado concentrator has the capacity to produce over 30 million pounds of copper and 9,000 ounces of gold per year. Copper production for 2009 was 74 million pounds and gold production was 18,000 ounces. Tailings from the Ojos del Salado mill are pumped to the Candelaria tailings facility for final deposition. The Candelaria facility has sufficient capacity for the remaining Ojos del Salado tailings in addition to Candelaria’s tailings.

Ojos del Salado is located in a desert environment with rainfall averaging less than one inch per year and is in an active seismic zone. The highest underground level is at an elevation of 500 meters above sea level, with the lowest underground level at 150 meters above sea level. The Ojos del Salado mineral rights encompass approximately 15,815 acres, which includes approximately 6,784 acres of owned land in and around the Ojos del Salado underground mines and plant site. The remaining property consists of mineral rights owned by us in which the surface is not owned but controlled by us, which is consistent with Chilean law.

Ojos del Salado receives electrical power through long-term contracts with Empresa Eléctrica Guacolda S.A. Ojos del Salado’s water supply comes from well fields in the area of Tierra Amarilla and Copiapó that draw water from the Copiapó River aquifer. Because of rapid depletion of this aquifer in recent years, ongoing studies are addressing the adequacy of this water supply for Ojos del Salado’s currently planned operations. For a discussion of risks associated with the availability of water, see Item 1A. – “Risk Factors.”

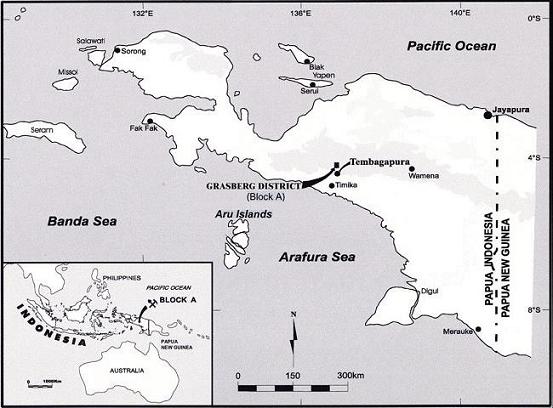

Indonesia

Ownership

PT Freeport Indonesia is a limited liability company organized under the laws of the Republic of Indonesia and incorporated in Delaware. We directly own 81.28 percent of PT Freeport Indonesia, 9.36 percent indirectly through our wholly owned subsidiary, PT Indocopper Investama, and the Government of Indonesia owns the remaining 9.36 percent. In July 2004, we received a request from the Indonesian Department of Energy and Mineral Resources that we offer to sell shares in PT Indocopper Investama to Indonesian nationals at fair market value. Refer to Note 15 for additional discussion.

In 1996, we established certain unincorporated joint ventures with Rio Tinto plc (Rio Tinto), an international mining company with headquarters in London, England. Pursuant to the joint venture agreements, Rio Tinto has a 40 percent interest in certain assets and future production exceeding specified annual amounts of copper, gold and silver through 2021 in Block A, and, after 2021, a 40 percent interest in all production from Block A. Refer to Note 3 for further discussion of the joint venture with Rio Tinto.

Contracts of Work

Through a Contract of Work (COW) with the Government of Indonesia, PT Freeport Indonesia conducts its current exploration and mining operations in Indonesia. The COW governs our rights and obligations relating to taxes, exchange controls, royalties, repatriation and other matters, and was concluded pursuant to the 1967 Foreign Capital Investment Law, which expresses Indonesia’s foreign investment policy and provides basic guarantees of remittance rights and protection against nationalization, a framework for economic incentives and basic rules regarding other rights and obligations of foreign investors. Specifically, the COW provides that the Government of Indonesia will not nationalize or expropriate PT Freeport Indonesia’s mining operations. Any disputes regarding the provisions of the COW are subject to international arbitration. We have experienced no disputes requiring arbitration during the 41 years we have operated in Indonesia.

PT Freeport Indonesia’s COW covers both Block A, which was first included in a 1967 COW that was replaced by a new COW in 1991, and Block B in which we gained rights in 1991. The initial term of our COW expires in December 2021, but we can extend it for two 10-year periods subject to Indonesian government approval that cannot be withheld or delayed unreasonably. The COW allows us to conduct exploration, mining and production activities in the 24,700-acre Block A area, located in Papua. All of PT Freeport Indonesia’s proven and probable mineral reserves and current mining operations are located in Block A. Under the COW, PT Freeport Indonesia also conducts exploration activities (which had been suspended in 2009, but will resume in 2010) in the approximate 500,000-acre Block B area, in Papua. We originally had the rights to explore 6.5 million acres in Block B, but pursuant to the COW we have only retained the rights to approximately 500,000 acres following

significant geological assessment.

PT Freeport Indonesia pays a copper royalty under its COW that varies from 1.5 percent of copper net revenue at a copper price of $0.90 or less per pound to 3.5 percent at a copper price of $1.10 or more per pound. The COW royalty rate for gold and silver sales is 1.0 percent.

A large part of the mineral royalties under Government of Indonesia regulations are designated to the provinces from which the minerals are extracted. In connection with our fourth concentrator mill expansion completed in 1998, PT Freeport Indonesia agreed to pay the Government of Indonesia additional royalties (royalties not required by our COW) to provide further support to the local governments and the people of the Indonesia province of Papua. The additional royalties are paid on production exceeding specified annual amounts of copper, gold and silver expected to be generated when PT Freeport Indonesia’s milling facilities operate above 200,000 metric tons of ore per day. The additional royalty for copper equals the COW royalty rate and for gold and silver equals twice the COW royalty rates. Therefore, PT Freeport Indonesia’s royalty rate on copper net revenues from production above the agreed levels is double the COW royalty rate, and royalty rates on gold and silver sales from production above the agreed levels are triple the COW royalty rates. PT Freeport Indonesia’s share of the combined royalties, including the additional royalties which became effective January 1, 1999, totaled $147 million in 2009, $113 million in 2008 and $133 million in 2007.

PT Irja Eastern Minerals (Eastern Minerals), of which we own 100 percent, conducts exploration through a joint venture agreement, under a separate COW in an area covering approximately 450,000 acres in Papua. The Eastern Minerals COW was under suspension during 2009.

Under a joint venture agreement through PT Nabire Bakti Mining (PTNBM), we conduct exploration activities under a separate COW in an area covering approximately 500,000 acres in five parcels contiguous to PT Freeport Indonesia’s Block B and one of Eastern Minerals’ blocks. The PTNBM COW was under suspension for much of 2009, but will resume in 2010.

In 2008, Indonesia enacted a new mining law, which will operate under a licensing system as opposed to the COW system that applies to PT Freeport Indonesia, Eastern Minerals and PTNBM. In 2010, the Government of Indonesia promulgated regulations under the 2008 mining law and certain provisions address existing COWs. The regulations provide that COWs will continue to be honored until their expiration. However, the regulations attempt to apply certain provisions of the new law to any extension periods of COWs even though our COWs provide for two ten-year extension periods under the existing terms of our COWs.

Grasberg Minerals District

PT Freeport Indonesia operates in the remote highlands of the Sudirman Mountain Range in the province of Papua, Indonesia, which is on the western half of the island of New Guinea. We and our predecessors have conducted exploration and mining operations in Block A since 1967 and have been the only operator of these operations. We currently have two mines in operation: the Grasberg open pit and the Deep Ore Zone (DOZ) underground block cave. We also have significant development projects in the Grasberg minerals district, which are discussed in more detail in “Development Projects and Exploration” below and in Item 7. “Management’s Discussion and Analysis of Financial Conditions and Results of Operations.”

Grasberg Open Pit. We began open-pit mining of the Grasberg ore body in 1990. Open-pit operations are expected to continue through mid 2016, at which time underground mining operations are scheduled to begin at our Grasberg Block Cave mine, which is currently in development. Production is currently at the 3,295- to 4,285-meter elevation level and totaled 57 million metric tons of ore in 2009 and 49 million metric tons of ore in 2008, which provided 70 percent of our 2009 mill feed and 67 percent of our 2008 mill feed. Remaining mill feed comes from our DOZ mine.

The current Grasberg equipment fleet consists of over 500 units. The larger mining equipment directly associated with production includes an available fleet of 163 haul trucks with payloads ranging from approximately 215 metric tons to 330 metric tons and 18 shovels with bucket sizes ranging from 30 cubic meters to 42 cubic meters, which in 2009 moved an average of 725,000 metric tons per day.

Grasberg crushing and conveying systems are integral to the mine and provide the capacity to transport up to 225,000 metric tons per day of Grasberg ore to the mill and 135,000 metric tons per day of overburden to the overburden stockpiles. The remaining ore and overburden is moved by haul trucks.

Deep Ore Zone. The DOZ ore body lies vertically below the now depleted Intermediate Ore Zone. We began production from the DOZ ore body in 1989 using open stope mining methods, but we suspended production in 1991 in favor of production from the Grasberg deposit. Production resumed in September 2000 using the block-cave method. Production is at the 3,110-meter elevation level and totaled 26 million metric tons of ore in 2009 and 23 million metric tons in 2008. Production at the DOZ mine is expected to continue through 2020 and we plan to ramp up production at our Deep Mill Level Zone (DMLZ) block cave mine, which is currently under development, beginning in 2015.

During 2009, we completed over 11,000 meters of development drifting in support of the block-cave mining method for the DOZ mine. Further expansion of the DOZ operation to 80,000 metric tons of ore per day is substantially complete. The success of the development of the DOZ mine, one of the world’s largest underground

mines, provides confidence in the future development of PT Freeport Indonesia’s large-scale undeveloped underground ore bodies.

The DOZ mine fleet consists of over 185 pieces of mobile heavy equipment, which in 2009 moved an average of 72,000 metric tons of ore per day. The primary mining equipment directly associated with production and development includes an available fleet of 49 load haul dump (LHD) units and 23 haul trucks. Our production LHD units typically carry approximately 11 metric tons of ore. Using ore passes and chutes, the LHD units transfer ore into 55-ton capacity haul trucks. The trucks dump into two gyratory crushers and the ore is then conveyed to the surface stockpiles.

PT Freeport Indonesia’s total production for 2009 was 1.4 billion pounds of copper and 2.6 million ounces of gold.

Our principal source of power for all our Indonesian operations is a coal-fired power plant that we built in conjunction with our fourth concentrator mill expansion. Diesel generators supply peaking and backup electrical power generating capacity. A combination of naturally occurring mountain streams and water derived from our underground operations provides water for our operations. Our Indonesian operations are in an active seismic zone and experience average annual rainfall of approximately 200 inches.

Description of Ore Bodies. Our Indonesia ore bodies are located within and around two main igneous intrusions, the Grasberg monzodiorite and the Ertsberg diorite. The host rocks of these ore bodies include both carbonate and clastic rocks that form the ridge crests and upper flanks of the Sudirman Range, and the igneous rocks of monzonitic to dioritic composition that intrude them. The igneous-hosted ore bodies (the Grasberg open pit and block cave, and portions of the DOZ block cave) occur as vein stockworks and disseminations of copper sulfides, dominated by chalcopyrite and, to a much lesser extent, bornite. The sedimentary-rock hosted ore bodies occur as “magnetite-rich, calcium/magnesian skarn” replacements, whose location and orientation are strongly influenced by major faults and by the chemistry of the carbonate rocks along the margins of the intrusions.

The copper mineralization in these skarn deposits is also dominated by chalcopyrite, but higher bornite concentrations are common. Moreover, gold occurs in significant concentrations in all of the district’s ore bodies, though rarely visible to the naked eye. These gold concentrations usually occur as inclusions within the copper sulfide minerals, though, in some deposits, these concentrations can also be strongly associated with pyrite.

The following diagram indicates the relative elevations (in meters) of our reported ore bodies.

The following map, which encompasses an area of approximately 42 square kilometers (approximately 16 square miles), indicates the relative positions and sizes of our reported ore bodies and their locations.

Africa

At Tenke Fungurume, mine properties and facilities are controlled through mining concessions under general mining laws and our mining rights remain in force as long as the concessions are exploitable. The concessions are owned or controlled by operating companies in which we or our subsidiaries have an ownership interest.

Tenke Fungurume

We own an effective 57.75 percent interest in the Tenke Fungurume minerals district. The remaining ownership interests are held by Lundin Mining Corporation (Lundin) (an effective 24.75 percent interest) and La Générale des Carrières et des Mines (Gécamines), which is wholly owned by the Government of the DRC (17.5 percent non-dilutable interest).

In 2009, we completed the approximate $2 billion initial project at the Tenke Fungurume minerals district. Pursuant to our agreement with Lundin, we were responsible for funding our share (70 percent) of the project development costs and 100 percent of certain cost overruns on the initial project. We and Lundin will be repaid our advances prior to distributions to the stockholders of Tenke Fungurume. Accordingly, we will receive a disproportionate share of cash flow until the cost overrun financing and advances are repaid. Additionally, in accordance with the terms of the agreement, Gécamines will receive asset transfer payments totaling $100 million, $80 million of which have already been paid and the remainder of which will be paid over the next two years.

The Tenke Fungurume deposits are located in the Katanga province of the DRC approximately 110 miles northwest of Lubumbashi. The deposits are accessible by unpaved roads and by rail. The Tenke Fungurume deposits are sediment-hosted copper and cobalt deposits with oxide, mixed oxide-sulfide and sulfide mineralization. The dominant oxide minerals are malachite, pseudomalachite and heterogenite. Important sulfide minerals consist of bornite, carrollite, chalcocite and chalcopyrite.

Copper and cobalt are recovered through an agitation-leach plant capable of processing 8,000 metric tons of ore per day. Copper production commenced in March 2009 and achieved targeted production rates in September 2009. The cobalt and sulphuric acid plants were commissioned in September 2009 and we continue to address start-up and quality issues in the cobalt circuit and expect to reach sustained targeted production rates during 2010. Current operations are designed to produce approximately 250 million pounds of copper and 18 million pounds of cobalt per year. The current equipment fleet includes 10 five-cubic meter front-end loaders, 29 45-metric ton haul trucks, surface miners, production drills, sampling machines and crawler dozers.

We commenced a feasibility study in fourth-quarter 2009 to evaluate a second phase of the project, which would include optimizing the current plant and potentially increasing capacity by approximately 50 percent. The feasibility study is expected to be completed by mid-year 2010. The timing of these expansions will depend on a number of factors, including general economic and market conditions.

Tenke Fungurume is located in a tropical region; however, temperatures are moderated by its higher altitudes. Weather in this region is characterized by a dry season and a wet season, each lasting about six months with average rainfall of 47 inches per year. The highest bench elevation is expected to be 1,480 meters above sea level and the ultimate pit bottom is expected to be 1,270 meters above sea level. The Tenke Fungurume deposits are located within four concessions totaling 394,455 acres.

Tenke Fungurume has entered into long-term power supply and infrastructure funding agreements with La Société Nationale d’Electricité (SNEL), the state-owned electric utility company serving the region. The results of a recent water exploration program, as well as the regional geological and hydro-geological conditions, indicate that adequate water is available for the project, and for hydro-electric generation during the expected life of the operation.

In February 2008, the Ministry of Mines, Government of the DRC, sent a letter seeking comment on proposed material modifications to the mining contracts for the Tenke Fungurume concession. We are continuing to work cooperatively with the DRC government to resolve the ongoing contract review but cannot predict the timing or outcome of the process. The contract review process has not affected our development schedule and we are continuing to operate pursuant to the terms of our contract. We believe the contract is fair and equitable, complies with Congolese law and is enforceable without modification.

PRODUCTION DATA

For comparative purposes, operating data shown below for the years ended December 31, 2007, 2006 and 2005, combines our historical data with Phelps Dodge pre-acquisition data. As the pre-acquisition operating data represent the results of these operations under Phelps Dodge management, such combined data is not necessarily indicative of what past results would have been under FCX management or of future operating results.

| COPPER | | Years Ended December 31, | |

| (millions of recoverable pounds) | | 2009 | | | 2008 | | | 2007a | | | 2006a | | | 2005a | |

| | | | | | | | | | | | | | | | |

MINED COPPER (FCX’s net interest in %) | | | | | | | | | | | | | | | |

| North America | | | | | | | | | | | | | | | |

Morenci (85%)b | | 428 | | | 626 | | | 687 | | | 693 | | | 680 | |

| Bagdad (100%) | | 225 | | | 227 | | | 202 | | | 165 | | | 201 | |

| Safford (100%) | | 184 | | | 133 | | | 1 | | | - | | | - | |

| Sierrita (100%) | | 170 | | | 188 | | | 150 | | | 162 | | | 158 | |

| Tyrone (100%) | | 86 | | | 76 | | | 50 | | | 64 | | | 81 | |

| Chino (100%) | | 36 | | | 155 | | | 190 | | | 186 | | | 210 | |

| Miami (100%) | | 16 | | | 19 | | | 20 | | | 19 | | | 25 | |

| Other (100%) | | 2 | | | 6 | | | 20 | | | 16 | | | 10 | |

| Total North America | | 1,147 | | | 1,430 | | | 1,320 | c | | 1,305 | | | 1,365 | |

| | | | | | | | | | | | | | | | |

| South America | | | | | | | | | | | | | | | |

| Cerro Verde (53.56%) | | 662 | | | 694 | | | 594 | | | 222 | | | 206 | |

| Candelaria/Ojos del Salado (80%) | | 370 | | | 446 | | | 453 | | | 429 | | | 421 | |

| El Abra (51%) | | 358 | | | 366 | | | 366 | | | 482 | | | 464 | |

| Total South America | | 1,390 | | | 1,506 | | | 1,413 | c | | 1,133 | | | 1,091 | |

| | | | | | | | | | | | | | | | |

| Indonesia | | | | | | | | | | | | | | | |