UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-Q

| þ | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) |

| | OF | THE SECURITIES EXCHANGE ACT OF 1934 |

For the Quarterly Period Ended September 30, 2011

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) |

| | OF | THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File Number 1-10351

Potash Corporation of Saskatchewan Inc.

(Exact name of registrant as specified in its charter)

| | |

| Canada | | N/A |

(State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

| |

122 — 1st Avenue South Saskatoon, Saskatchewan, Canada | | S7K 7G3 (Zip Code) |

| (Address of principal executive offices) | | |

306-933-8500

(Registrant’s telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Sections 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes ¨ No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| | | | | | |

| Large accelerated filer þ | | Accelerated filer ¨ | | Non-accelerated filer ¨ (Do not check if a smaller reporting company) | | Smaller reporting company ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Exchange Act Rule 12b-2).

Yes ¨ No þ

As at October 31, 2011, Potash Corporation of Saskatchewan Inc. had 856,478,084 Common Shares outstanding.

TABLE OF CONTENTS

Part I. Financial Information

Item 1. Financial Statements

Potash Corporation of Saskatchewan Inc.

Condensed Consolidated Statements of Financial Position

(in millions of US dollars)

(unaudited)

| | | | | | | | |

| | | September 30,

2011 | | | December 31,

2010 | |

Assets | | | | | | | | |

Current assets | | | | | | | | |

Cash and cash equivalents | | $ | 394 | | | $ | 412 | |

Receivables | | | 1,327 | | | | 1,059 | |

Inventories (Note 2) | | | 581 | | | | 570 | |

Prepaid expenses and other current assets | | | 38 | | | | 54 | |

| | | 2,340 | | | | 2,095 | |

Non-current assets | | | | | | | | |

Property, plant and equipment | | | 9,408 | | | | 8,141 | |

Investments in equity-accounted investees | | | 1,166 | | | | 1,051 | |

Available-for-sale investments (Note 3) | | | 2,491 | | | | 3,842 | |

Other assets | | | 302 | | | | 303 | |

Intangible assets | | | 115 | | | | 115 | |

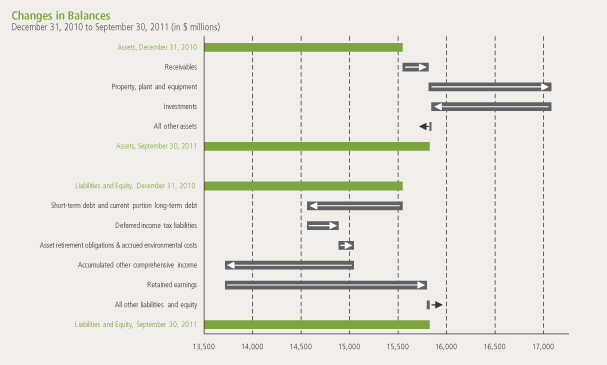

Total Assets | | $ | 15,822 | | | $ | 15,547 | |

Liabilities | | | | | | | | |

Current liabilities | | | | | | | | |

Short-term debt and current portion of long-term debt (Note 4) | | $ | 882 | | | $ | 1,871 | |

Payables and accrued charges | | | 1,201 | | | | 1,198 | |

Current portion of derivative instrument liabilities | | | 82 | | | | 75 | |

| | | 2,165 | | | | 3,144 | |

Non-current liabilities | | | | | | | | |

Long-term debt (Note 4) | | | 3,704 | | | | 3,707 | |

Derivative instrument liabilities | | | 193 | | | | 204 | |

Deferred income tax liabilities | | | 1,064 | | | | 737 | |

Accrued pension and other post-retirement benefits (Note 5) | | | 530 | | | | 468 | |

Asset retirement obligations and accrued environmental costs | | | 614 | | | | 455 | |

Other non-current liabilities and deferred credits | | | 85 | | | | 147 | |

Total Liabilities | | | 8,355 | | | | 8,862 | |

Shareholders’ Equity | | | | | | | | |

Share capital (Note 6) | | | 1,468 | | | | 1,431 | |

Contributed surplus | | | 296 | | | | 308 | |

Accumulated other comprehensive income | | | 1,058 | | | | 2,394 | |

Retained earnings | | | 4,645 | | | | 2,552 | |

Total Shareholders’ Equity | | | 7,467 | | | | 6,685 | |

Total Liabilities and Shareholders’ Equity | | $ | 15,822 | | | $ | 15,547 | |

Contingencies (Note 12) | | | | | | | | |

(See Notes to the Condensed Consolidated Financial Statements)

| | |

| 1 | | PotashCorp 2011 Third Quarter Quarterly Report on Form 10-Q |

Potash Corporation of Saskatchewan Inc.

Condensed Consolidated Statements of Income

(in millions of US dollars except per-share amounts)

(unaudited)

| | | | | | | | | | | | | | | | |

| | | Three Months Ended September 30 | | | Nine Months Ended September 30 | |

| | | 2011 | | | 2010 | | | 2011 | | | 2010 | |

Sales(Note 7) | | $ | 2,321 | | | $ | 1,575 | | | $ | 6,850 | | | $ | 4,726 | |

Freight, transportation and distribution | | | (129 | ) | | | (119 | ) | | | (410 | ) | | | (373 | ) |

Cost of goods sold | | | (1,060 | ) | | | (906 | ) | | | (3,044 | ) | | | (2,489 | ) |

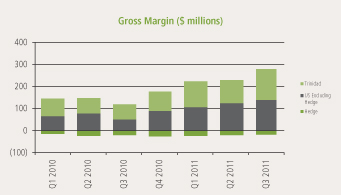

Gross Margin | | | 1,132 | | | | 550 | | | | 3,396 | | | | 1,864 | |

Selling and administrative expenses | | | (46 | ) | | | (71 | ) | | | (176 | ) | | | (164 | ) |

Provincial mining and other taxes | | | (53 | ) | | | (16 | ) | | | (147 | ) | | | (56 | ) |

Share of earnings of equity-accounted investees | | | 68 | | | | 51 | | | | 185 | | | | 122 | |

Dividend income | | | 41 | | | | 25 | | | | 94 | | | | 139 | |

Other expenses | | | — | | | | (22 | ) | | | (10 | ) | | | (43 | ) |

Operating Income | | | 1,142 | | | | 517 | | | | 3,342 | | | | 1,862 | |

Finance Costs | | | (37 | ) | | | (22 | ) | | | (125 | ) | | | (87 | ) |

Income Before Income Taxes | | | 1,105 | | | | 495 | | | | 3,217 | | | | 1,775 | |

Income Taxes(Note 9) | | | (279 | ) | | | (152 | ) | | | (819 | ) | | | (508 | ) |

Net Income | | $ | 826 | | | $ | 343 | | | $ | 2,398 | | | $ | 1,267 | |

| | | | |

Net Income Attributable to Common Shareholders | | $ | 826 | | | $ | 343 | | | $ | 2,398 | | | $ | 1,267 | |

| | | | |

Net Income per Share(Note 10) | | | | | | | | | | | | | | | | |

Basic | | $ | 0.96 | | | $ | 0.39 | | | $ | 2.80 | | | $ | 1.43 | |

Diluted | | $ | 0.94 | | | $ | 0.38 | | | $ | 2.73 | | | $ | 1.39 | |

Dividends per Share | | $ | 0.07 | | | $ | 0.03 | | | $ | 0.21 | | | $ | 0.10 | |

(See Notes to the Condensed Consolidated Financial Statements)

| | |

| PotashCorp 2011 Third Quarter Quarterly Report on Form 10-Q | | 2 |

Potash Corporation of Saskatchewan Inc.

Condensed Consolidated Statements of Comprehensive (Loss) Income

(in millions of US dollars)

(unaudited)

| | | | | | | | | | | | | | | | |

| | | Three Months Ended

September 30 | | | Nine Months Ended

September 30 | |

| (Net of related income taxes) | | 2011 | | | 2010 | | | 2011 | | | 2010 | |

Net Income | | $ | 826 | | | $ | 343 | | | $ | 2,398 | | | $ | 1,267 | |

Other comprehensive (loss) income | | | | | | | | | | | | | | | | |

Net (decrease) increase in net unrealized gains on available-for- sale investments(1) (Note 3) | | | (983 | ) | | | 924 | | | | (1,351 | ) | | | 202 | |

Net actuarial losses on defined benefit plans(2)(Note 5) | | | (125 | ) | | | — | | | | (125 | ) | | | — | |

Net losses on derivatives designated as cash flow hedges(3) | | | (18 | ) | | | (61 | ) | | | (18 | ) | | | (125 | ) |

Reclassification to income of net losses on cash flow hedges(4) | | | 10 | | | | 12 | | | | 38 | | | | 36 | |

Other | | | (5 | ) | | | 5 | | | | (5 | ) | | | 1 | |

Other Comprehensive (Loss) Income | | | (1,121 | ) | | | 880 | | | | (1,461 | ) | | | 114 | |

Comprehensive (Loss) Income | | $ | (295 | ) | | $ | 1,223 | | | $ | 937 | | | $ | 1,381 | |

| | | | |

Comprehensive (Loss) Income Attributable to Common Shareholders | | $ | (295 | ) | | $ | 1,223 | | | $ | 937 | | | $ | 1,381 | |

| (1) | Available-for-sale investments are comprised of shares in Israel Chemicals Ltd. and Sinofert Holdings Limited. |

| (2) | Net of income taxes of $(71) (2010 — $NIL) for the three and nine months ended September 30, 2011. |

| (3) | Cash flow hedges are comprised of natural gas derivative instruments, and are net of income taxes of $(11) (2010 — $(37)) for the three months ended September 30, 2011 and $(11) (2010 — $(76)) for the nine months ended September 30, 2011. |

| (4) | Net of income taxes of $7 (2010 — $8) for the three months ended September 30, 2011 and $23 (2010 — $22) for the nine months ended September 30, 2011. |

(See Notes to the Condensed Consolidated Financial Statements)

| | |

| 3 | | PotashCorp 2011 Third Quarter Quarterly Report on Form 10-Q |

Potash Corporation of Saskatchewan Inc.

Condensed Consolidated Statements of Changes in Equity

(in millions of US dollars)

(unaudited)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Equity Attributable to Common Shareholders | |

| | | Share

Capital | | | Contributed

Surplus | | | Accumulated Other Comprehensive Income | | | Retained

Earnings | | | Total

Equity | |

| | | | Net

unrealized

gains on

available-for-

sale

investments | | | Net unrealized

losses on

derivatives

designated as

cash flow

hedges | | | Net actuarial

losses on

defined

benefit

plans

(Note 5) | | | Other | | | Total

Accumulated

Other

Comprehensive

Income | | | |

Balance — January 1, 2011 | | $ | 1,431 | | | $ | 308 | | | $ | 2,563 | | | $ | (177 | ) | | $ | — | (1) | | $ | 8 | | | $ | 2,394 | | | $ | 2,552 | | | $ | 6,685 | |

Net income | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | | | | 2,398 | | | | 2,398 | |

Other comprehensive (loss) income | | | — | | | | — | | | | (1,351 | ) | | | 20 | | | | (125 | ) | | | (5 | ) | | | (1,461 | ) | | | — | | | | (1,461 | ) |

Effect of share-based compensation | | | — | | | | (12 | ) | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | | | | (12 | ) |

Dividends declared | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | | | | (180 | ) | | | (180 | ) |

Issuance of common shares | | | 37 | | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | | | | 37 | |

Transfer of actuarial losses on defined benefit plans | | | — | | | | — | | | | — | | | | — | | | | 125 | | | | — | | | | 125 | | | | (125 | ) | | | — | |

Balance — September 30, 2011 | | $ | 1,468 | | | $ | 296 | | | $ | 1,212 | | | $ | (157 | ) | | $ | — | (1) | | $ | 3 | | | $ | 1,058 | | | $ | 4,645 | | | $ | 7,467 | |

| (1) | Any amounts incurred during a period are cleared out to retained earnings at each period end. Therefore, no balance exists in the reserve at beginning or end of period. |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Equity Attributable to Common Shareholders | |

| | | | | | | | | Accumulated Other Comprehensive Income | | | | | | | |

| | | Share

Capital | | | Contributed

Surplus | | | Unrealized

gains on

available-for-

sale

investments | | | Net unrealized

losses on

derivatives

designated as

cash flow

hedges | | | Net actuarial

losses on

defined

benefit

plans | | | Other | | | Total

Accumulated

Other

Comprehensive

Income | | | Retained

Earnings | | | Total

Equity | |

Balance — January 1, 2010 | | $ | 1,430 | | | $ | 273 | | | $ | 1,900 | | | $ | (111 | ) | | $ | — | (1) | | $ | 9 | | | $ | 1,798 | | | $ | 2,804 | | | $ | 6,305 | |

Net income | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | | | | 1,267 | | | | 1,267 | |

Other comprehensive income (loss) | | | — | | | | — | | | | 202 | | | | (89 | ) | | | — | | | | 1 | | | | 114 | | | | — | | | | 114 | |

Effect of share-based compensation | | | — | | | | 66 | | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | | | | 66 | |

Dividends declared | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | | | | (89 | ) | | | (89 | ) |

Issuance of common shares | | | 52 | | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | | | | 52 | |

Balance — September 30, 2010 | | $ | 1,482 | | | $ | 339 | | | $ | 2,102 | | | $ | (200 | ) | | $ | — | (1) | | $ | 10 | | | $ | 1,912 | | | $ | 3,982 | | | $ | 7,715 | |

| (1) | Any amounts incurred during a period are cleared out to retained earnings at each period end. Therefore, no balance exists in the reserve at beginning or end of period. |

(See Notes to the Condensed Consolidated Financial Statements)

| | |

| PotashCorp 2011 Third Quarter Quarterly Report on Form 10-Q | | 4 |

Potash Corporation of Saskatchewan Inc.

Condensed Consolidated Statements of Cash Flow

(in millions of US dollars)

(unaudited)

| | | | | | | | | | | | | | | | |

| | | Three Months Ended

September 30 | | | Nine Months Ended

September 30 | |

| | | 2011 | | | 2010 | | | 2011 | | | 2010 | |

Operating Activities | | | | | | | | | | | | | | | | |

Net income | | $ | 826 | | | $ | 343 | | | $ | 2,398 | | | $ | 1,267 | |

Adjustments to reconcile net income to cash provided by operating activities | | | | | | | | | | | | | | | | |

Depreciation and amortization | | | 122 | | | | 106 | | | | 374 | | | | 325 | |

Share-based compensation | | | 3 | | | | 3 | | | | 22 | | | | 22 | |

Realized excess tax benefit related to share-based compensation | | | 6 | | | | 31 | | | | 29 | | | | 39 | |

Provision for deferred income tax | | | 189 | | | | 13 | | | | 342 | | | | 88 | |

Undistributed earnings of equity-accounted investees | | | (68 | ) | | | (50 | ) | | | (118 | ) | | | (78 | ) |

Pension and other post-retirement benefits | | | (145 | ) | | | (32 | ) | | | (131 | ) | | | (9 | ) |

Asset retirement obligations and accrued environmental costs | | | 22 | | | | 27 | | | | 40 | | | | 105 | |

Other | | | 9 | | | | 15 | | | | (23 | ) | | | 70 | |

Subtotal of adjustments | | | 138 | | | | 113 | | | | 535 | | | | 562 | |

Changes in non-cash operating working capital | | | | | | | | | | | | | | | | |

Receivables | | | (88 | ) | | | (64 | ) | | | (277 | ) | | | 326 | |

Inventories | | | 7 | | | | 147 | | | | (14 | ) | | | 117 | |

Prepaid expenses and other current assets | | | — | | | | 5 | | | | 12 | | | | (6 | ) |

Payables and accrued charges | | | (18 | ) | | | 43 | | | | (35 | ) | | | 128 | |

Subtotal of changes in non-cash operating working capital | | | (99 | ) | | | 131 | | | | (314 | ) | | | 565 | |

Cash provided by operating activities | | | 865 | | | | 587 | | | | 2,619 | | | | 2,394 | |

Investing Activities | | | | | | | | | | | | | | | | |

Additions to property, plant and equipment | | | (590 | ) | | | (562 | ) | | | (1,523 | ) | | | (1,517 | ) |

Purchase of long-term investments | | | — | | | | — | | | | — | | | | (422 | ) |

Other assets and intangible assets | | | (8 | ) | | | (28 | ) | | | (11 | ) | | | (99 | ) |

Cash used in investing activities | | | (598 | ) | | | (590 | ) | | | (1,534 | ) | | | (2,038 | ) |

Cash before financing activities | | | 267 | | | | (3 | ) | | | 1,085 | | | | 356 | |

Financing Activities | | | | | | | | | | | | | | | | |

Proceeds from long-term debt obligations | | | — | | | | — | | | | — | | | | 400 | |

Repayment of long-term debt obligations | | | — | | | | — | | | | (600 | ) | | | (400 | ) |

(Repayments of) proceeds from short-term debt obligations | | | (236 | ) | | | 1 | | | | (395 | ) | | | (332 | ) |

Dividends | | | (60 | ) | | | (30 | ) | | | (148 | ) | | | (89 | ) |

Issuance of common shares | | | 15 | | | | 25 | | | | 40 | | | | 40 | |

Cash used in financing activities | | | (281 | ) | | | (4 | ) | | | (1,103 | ) | | | (381 | ) |

Decrease in Cash and Cash Equivalents | | | (14 | ) | | | (7 | ) | | | (18 | ) | | | (25 | ) |

Cash and Cash Equivalents, Beginning of Period | | | 408 | | | | 367 | | | | 412 | | | | 385 | |

Cash and Cash Equivalents, End of Period | | $ | 394 | | | $ | 360 | | | $ | 394 | | | $ | 360 | |

Cash and cash equivalents comprised of: | | | | | | | | | | | | | | | | |

Cash | | $ | 78 | | | $ | 91 | | | $ | 78 | | | $ | 91 | |

Short-term investments | | | 316 | | | | 269 | | | | 316 | | | | 269 | |

| | | $ | 394 | | | $ | 360 | | | $ | 394 | | | $ | 360 | |

Supplemental cash flow disclosure | | | | | | | | | | | | | | | | |

Interest paid | | $ | 35 | | | $ | 38 | | | $ | 168 | | | $ | 143 | |

Income taxes paid (recovered) | | $ | 91 | | | $ | 64 | | | $ | 415 | | | $ | (76 | ) |

(See Notes to the Condensed Consolidated Financial Statements)

| | |

| 5 | | PotashCorp 2011 Third Quarter Quarterly Report on Form 10-Q |

Potash Corporation of Saskatchewan Inc.

Notes to the Condensed Consolidated Financial Statements

For the Three and Nine Months Ended September 30, 2011

(in millions of US dollars except share, per-share and percentage amounts)

(unaudited)

| 1. | Significant Accounting Policies |

Basis of Presentation

With its subsidiaries, Potash Corporation of Saskatchewan Inc. (“PCS”) — together known as “PotashCorp” or “the company” except to the extent the context otherwise requires — forms an integrated fertilizer and related industrial and feed products company.

The company previously prepared its financial statements in accordance with Canadian generally accepted accounting principles (“Canadian GAAP”) as set out in the Handbook of the Canadian Institute of Chartered Accountants (“CICA Handbook”). In 2010, the CICA Handbook was revised to incorporate International Financial Reporting Standards (“IFRS”), and required publicly accountable enterprises to apply such standards effective for years beginning on or after January 1, 2011, with early adoption permitted. Accordingly, these unaudited interim condensed consolidated financial statements are based on IFRS, as issued by the International Accounting Standards Board (“IASB”). In these unaudited interim condensed consolidated financial statements, the term “Canadian GAAP” refers to Canadian GAAP before the company’s adoption of IFRS.

These unaudited interim condensed consolidated financial statements have been prepared in accordance with International Accounting Standard (“IAS”) 34, “Interim Financial Reporting”, and IFRS 1, “First-Time Adoption of International Financial Reporting Standards” (“IFRS 1”). Subject to certain transition elections disclosed in Note 13 to the financial statements included in Part I Item 1 of the company’s 2011 First Quarter Quarterly Report on Form 10-Q, the company has consistently applied the same accounting policies throughout all periods presented. Note 13 referred to above describes the impact of the transition to IFRS on the company’s reported financial position and financial performance, including the nature and effect of significant changes in accounting policies from those used in its Canadian GAAP consolidated financial statements as at January 1, 2010 and December 31, 2010, and for the year ended December 31, 2010. Note 15 describes the impact of the transition to IFRS on the company’s reported financial position and financial performance as at and for the periods ended September 30, 2010. Except as disclosed in Note 14, these policies are consistent with accounting principles generally accepted in the United States (“US GAAP”) in all material respects.

These unaudited interim condensed consolidated financial statements were authorized by the Audit Committee of the Board of Directors for issue on November 4, 2011. The company will ultimately prepare its opening statement of financial position and financial statements for 2010 and 2011 by applying existing IFRS with an effective date of December 31, 2011 or prior. Accordingly, the financial statements for 2010 and 2011 may differ from these unaudited interim condensed consolidated financial statements.

These unaudited interim condensed consolidated financial statements include the accounts of PCS and its wholly owned subsidiaries; however, they do not include all disclosures normally provided in annual consolidated financial statements and should be read in conjunction with the 2010 annual consolidated financial statements and Part I Item 1, Notes 1 and 13 of the company’s 2011 First Quarter Quarterly Report on Form 10-Q. Certain information and note disclosures which are considered material to the understanding of the company’s unaudited interim condensed consolidated financial statements and which are normally included in annual consolidated financial statements prepared in accordance with IFRS were provided in Part I Item 1, Notes 1 and 13 of the company’s 2011 First Quarter Quarterly Report on Form 10-Q, along with reconciliations and descriptions of the effect of the transition from Canadian GAAP to IFRS on financial performance and financial position. In management’s opinion, the unaudited interim condensed consolidated financial statements include all adjustments (consisting solely of normal recurring adjustments) necessary to fairly present such information. Interim results are not necessarily indicative of the results expected for the fiscal year.

These unaudited interim condensed consolidated financial statements were prepared under the historical cost convention, except for certain items not carried at historical cost as discussed in Note 1 to the financial statements included in Part I Item 1 of the company’s 2011 First Quarter Quarterly Report on Form 10-Q.

| | |

| PotashCorp 2011 Third Quarter Quarterly Report on Form 10-Q | | 6 |

Recent Accounting Pronouncements

The following new standards and amendments or interpretations to existing standards have been published and are mandatory for periods beginning on or after January 1, 2011, or later:

IFRS 9, Financial Instruments

In November 2009, the IASB issued guidance relating to the classification and measurement of financial assets. Under IFRS 9, financial assets will generally be measured initially at fair value plus particular transaction costs, and subsequently at either amortized cost or fair value. In October 2010, the IASB issued additions to IFRS 9 relating to accounting for financial liabilities. Under the new requirements, an entity choosing to measure a financial liability at fair value will present the portion of any change in its fair value due to changes in the entity’s own credit risk in other comprehensive income (“OCI”), rather than within profit or loss. The standard is to be applied retrospectively and will be effective for periods commencing on or after January 1, 2013. The company is currently reviewing the standard to determine the potential impact, if any, on its consolidated financial statements.

Amendments to IFRIC 14, Prepayments of a Minimum Funding Requirement

In November 2009, the International Financial Reporting Interpretations Committee (“IFRIC”) issued amendments to IFRIC 14 relating to the prepayments of a minimum funding requirement for an employee defined benefit plan. The amendments apply when an entity is subject to minimum funding requirements and makes an early payment of contributions to cover those requirements. The amendments permit such an entity to treat the benefit of such an early payment as an asset. The amendment must be applied from the beginning of the first comparative period presented in the first financial statements in which the amendment is applied and became effective for periods commencing on or after January 1, 2011. The company has applied these amendments, which had no effect on these unaudited interim condensed consolidated financial statements.

Amendments to IFRS 7, Financial Instruments: Disclosures

In May 2010, the IASB issued amendments to IFRS 7 as part of its annual improvements process. The amendments addressed various requirements relating to the disclosure of financial instruments and are effective for annual periods commencing on or after January 1, 2011.

Amendments to IFRS 7, Disclosures — Transfers of Financial Assets

In October 2010, the IASB issued amendments to IFRS 7, “Financial Instruments: Disclosures”. The amendments require entities to provide additional disclosures to assist users of financial statements in evaluating the risk exposures relating to transfers of financial assets that are not derecognized or for which the entity has a continuing involvement in the transferred asset. The amendments became effective for annual periods beginning on or after July 1, 2011. The company does not typically retain any continuing involvement in financial assets once transferred. It has applied these amendments, which had no effect on these unaudited interim condensed consolidated financial statements.

IFRS 10, Consolidated Financial Statements

In May 2011, the IASB issued guidance establishing principles for the presentation and preparation of consolidated financial statements when an entity controls one or more other entities. IFRS 10 (which supersedes IAS 27 and Standing Interpretations Committee (“SIC”) 12) builds on existing principles by identifying the concept of control as the determining factor in whether an entity should be included within the consolidated financial statements of the parent company. The standard provides additional guidance to assist in the determination of control where this is difficult to assess. The standard is to be applied retrospectively, in most circumstances, and will be effective for annual periods commencing on or after January 1, 2013, with earlier application permitted. The company is currently reviewing the standard to determine the potential impact, if any, on its consolidated financial statements.

IFRS 11, Joint Arrangements

In May 2011, the IASB issued guidance establishing principles for financial reporting by parties to a joint arrangement. IFRS 11 (which supersedes IAS 31 and SIC 13) requires a party to a joint arrangement to determine the type of joint arrangement in which it is involved, either a joint operation or a joint venture, by assessing its rights and obligations arising from the arrangement. The existing policy choice of proportionate consolidation for jointly controlled entities has been eliminated and under IFRS 11, equity accounting is mandatory for participants in joint ventures. The standard is to be applied prospectively and will be effective for annual periods commencing on or after January 1, 2013, with earlier application permitted. The company is currently reviewing the standard to determine the potential impact, if any, on its consolidated financial statements.

| | |

| 7 | | PotashCorp 2011 Third Quarter Quarterly Report on Form 10-Q |

IFRS 12, Disclosure of Interest in Other Entities

In May 2011, the IASB issued guidance relating to the disclosure requirements of interests in other entities. IFRS 12 is a new and comprehensive standard on disclosure requirements for all forms of interest in other entities, including subsidiaries, joint arrangements, associates and unconsolidated structured entities. The standard is to be applied prospectively and is effective for annual periods commencing on or after January 1, 2013, with earlier application permitted. The company is currently reviewing the standard to determine the potential impact, if any, on its consolidated financial statements.

IFRS 13, Fair Value Measurement

In May 2011, the IASB issued guidance establishing a single source for fair value measurement. IFRS 13 defines fair value, sets out a framework for measuring fair value and introduces consistent requirements for disclosures on fair value measurements. It does not determine when an asset, a liability or an entity’s own equity instrument is measured at fair value. Rather, the measurement and disclosure requirements of IFRS 13 apply when another IFRS requires or permits the item to be measured at fair value, with limited exceptions. The standard is to be applied prospectively and will be effective for annual periods commencing on or after January 1, 2013, with earlier application permitted. The company is currently reviewing the standard to determine the potential impact, if any, on its consolidated financial statements.

Amendments to IAS 1, Presentation of Financial Statements

In June 2011, the IASB issued amendments to IAS 1 requiring items within OCI that may be reclassified to the profit or loss section of the income statement to be grouped together. The amendments are to be applied retrospectively and will be effective for annual periods commencing on or after July 1, 2012, with earlier application permitted. The company is currently reviewing these amendments to determine the potential impact on its consolidated financial statements.

Amendments to IAS 19, Employee Benefits

In June 2011, the IASB issued amendments to IAS 19 relating to the recognition and measurement of post-employment defined benefit expense and termination benefits, and to the disclosures for all employee benefits. The amendments are to be applied retrospectively, except for changes to the carrying value of assets that include capitalized employee benefit costs, which are to be applied prospectively. The amendments will be effective for annual periods commencing on or after January 1, 2013, with earlier application permitted. The company is currently reviewing these amendments to determine the potential impact on its consolidated financial statements.

IFRIC 20, Stripping Costs in the Production Phase of a Surface Mine

In October 2011, the IFRIC issued IFRIC 20 clarifying the requirements for accounting for stripping costs in the production phase of a surface mine. This interpretation clarifies when production stripping should lead to the recognition of an asset and how that asset should be measured, both initially and in subsequent periods. The interpretation will be effective for annual periods commencing on or after January 1, 2013, with earlier application permitted. The company is currently reviewing this interpretation to determine the potential impact, if any, on its consolidated financial statements.

| | | | | | | | |

| | | September 30,

2011 | | | December 31,

2010 | |

Finished products | | $ | 252 | | | $ | 255 | |

Intermediate products | | | 100 | | | | 127 | |

Raw materials | | | 88 | | | | 65 | |

Materials and supplies | | | 141 | | | | 123 | |

| | | $ | 581 | | | $ | 570 | |

| 3. | Available-for-Sale Investments |

The company assesses at the end of each reporting period whether there is objective evidence that a financial asset or group of financial assets is impaired. In the case of equity instruments classified as available-for-sale, for which unrealized gains and losses are generally recognized in OCI, a significant or prolonged decline in the fair value of the investment below its cost may be evidence that the assets are impaired. If objective evidence of impairment were to exist, the impaired amount (i.e., the unrealized loss) would be recognized in net income; any subsequent reversals would be recognized in OCI and would not flow back into net income.

At September 30, 2011, the company assessed whether there was objective evidence that its investment in Sinofert Holdings Limited (“Sinofert”) was impaired. The fair value of the investment, recorded in the consolidated statements of financial position, was $396 compared to the cost of $575. Factors considered in assessing impairment included the length of time and extent to which fair value had been below cost, and current financial and market conditions specific to Sinofert and the Chinese market.

The company concluded that objective evidence of impairment did not exist as at September 30, 2011 and, as a result, the unrealized holding loss of $179 was included in OCI. Impairment will be assessed again in future reporting periods if the fair value is below cost.

| | |

| PotashCorp 2011 Third Quarter Quarterly Report on Form 10-Q | | 8 |

On May 31, 2011, the company fully repaid $600 of 7.750 percent 10-year senior notes.

| 5. | Pension and Other Post-Retirement Benefits |

During the nine months ended September 30, 2011, the company contributed $156 to its defined benefit pension plans.

A remeasurement of the defined benefit plan assets and liabilities was performed at September 30, 2011. As a result of a loss on pension plan assets and a significant change in the discount rate, the company recorded net actuarial losses on defined benefit plans of $125 in OCI, which was recognized immediately in retained earnings at September 30, 2011. The company’s pension plan assets decreased by $33, defined benefit pension and other post-retirement benefit liabilities increased by $163 and deferred income tax liabilities decreased by $71 at September 30, 2011.

The discount rate used to determine the benefit obligation for the company’s significant plans at September 30, 2011 was 4.75 percent.

The benefit obligations and plan assets for the company’s pension and other post-retirement plans were as follows:

| | | | | | | | |

| | | September 30,

2011 | | | December 31,

2010 | |

Present value of defined benefit obligations | | $ | (1,379 | ) | | $ | (1,191 | ) |

Fair value of plan assets | | | 875 | | | | 753 | |

Funded status | | | (504 | ) | | | (438 | ) |

Past service costs not recognized in statements of financial position | | | (12 | ) | | | (13 | ) |

Accrued pension and other post-retirement benefit liabilities | | $ | (516 | ) | | $ | (451 | ) |

Amounts included in: | | | | | | | | |

Other assets | | $ | 23 | | | $ | 26 | |

Liabilities | | | | | | | | |

Current | | | (9 | ) | | | (9 | ) |

Long-term | | | (530 | ) | | | (468 | ) |

| | | $ | (516 | ) | | $ | (451 | ) |

Authorized

The company is authorized to issue an unlimited number of common shares without par value and an unlimited number of first preferred shares. The common shares are not redeemable or convertible. The first preferred shares may be issued in one or more series with rights and conditions to be determined by the Board of Directors. No first preferred shares have been issued.

Issued

| | | | | | | | |

| | | Number of

Common Shares | | | Consideration | |

Balance — December 31, 2010 | | | 853,122,693 | | | $ | 1,431 | |

Issued under option plans | | | 3,234,318 | | | | 35 | |

Issued for dividend reinvestment plan | | | 30,663 | | | | 2 | |

Balance — September 30, 2011 | | | 856,387,674 | | | $ | 1,468 | |

| | |

| 9 | | PotashCorp 2011 Third Quarter Quarterly Report on Form 10-Q |

The company’s operating segments have been determined based on reports reviewed by the Chief Executive Officer, its chief operating decision maker, that are used to make strategic decisions. The company has three reportable operating segments: potash, phosphate and nitrogen. These operating segments are differentiated by the chemical nutrient contained in the product that each produces. Inter-segment sales are made under terms that approximate market value. The accounting policies of the segments are the same as those described in Note 1.

| | | | | | | | | | | | | | | | | | | | |

| | | Three Months Ended September 30, 2011 | |

| | | Potash | | | Phosphate | | | Nitrogen | | | All Others | | | Consolidated | |

Sales | | $ | 1,035 | | | $ | 690 | | | $ | 596 | | | $ | — | | | $ | 2,321 | |

Freight, transportation and distribution | | | (59 | ) | | | (46 | ) | | | (24 | ) | | | — | | | | (129 | ) |

Net sales — third party | | | 976 | | | | 644 | | | | 572 | | | | — | | | | | |

Cost of goods sold | | | (276 | ) | | | (475 | ) | | | (309 | ) | | | — | | | | (1,060 | ) |

Gross margin | | | 700 | | | | 169 | | | | 263 | | | | — | | | | 1,132 | |

Depreciation and amortization | | | (33 | ) | | | (55 | ) | | | (32 | ) | | | (2 | ) | | | (122 | ) |

Inter-segment sales | | | — | | | | — | | | | 56 | | | | — | | | | — | |

| | | | | | | | | | | | | | | | | | | | |

| | | Three Months Ended September 30, 2010 | |

| | | Potash | | | Phosphate | | | Nitrogen | | | All Others | | | Consolidated | |

Sales | | $ | 637 | | | $ | 536 | | | $ | 402 | | | $ | — | | | $ | 1,575 | |

Freight, transportation and distribution | | | (55 | ) | | | (44 | ) | | | (20 | ) | | | — | | | | (119 | ) |

Net sales — third party | | | 582 | | | | 492 | | | | 382 | | | | — | | | | | |

Cost of goods sold | | | (243 | ) | | | (396 | ) | | | (267 | ) | | | — | | | | (906 | ) |

Gross margin | | | 339 | | | | 96 | | | | 115 | | | | — | | | | 550 | |

Depreciation and amortization | | | (28 | ) | | | (49 | ) | | | (27 | ) | | | (2 | ) | | | (106 | ) |

Inter-segment sales | | | — | | | | — | | | | 27 | | | | — | | | | — | |

| | | | | | | | | | | | | | | | | | | | |

| | | Nine Months Ended September 30, 2011 | |

| | | Potash | | | Phosphate | | | Nitrogen | | | All Others | | | Consolidated | |

Sales | | $ | 3,265 | | | $ | 1,872 | | | $ | 1,713 | | | $ | — | | | $ | 6,850 | |

Freight, transportation and distribution | | | (212 | ) | | | (129 | ) | | | (69 | ) | | | — | | | | (410 | ) |

Net sales — third party | | | 3,053 | | | | 1,743 | | | | 1,644 | | | | — | | | | | |

Cost of goods sold | | | (817 | ) | | | (1,258 | ) | | | (969 | ) | | | — | | | | (3,044 | ) |

Gross margin | | | 2,236 | | | | 485 | | | | 675 | | | | — | | | | 3,396 | |

Depreciation and amortization | | | (112 | ) | | | (159 | ) | | | (97 | ) | | | (6 | ) | | | (374 | ) |

Inter-segment sales | | | — | | | | — | | | | 133 | | | | — | | | | — | |

| | | | | | | | | | | | | | | | | | | | |

| | | Nine Months Ended September 30, 2010 | |

| | | Potash | | | Phosphate | | | Nitrogen | | | All Others | | | Consolidated | |

Sales | | $ | 2,170 | | | $ | 1,301 | | | $ | 1,255 | | | $ | — | | | $ | 4,726 | |

Freight, transportation and distribution | | | (202 | ) | | | (107 | ) | | | (64 | ) | | | — | | | | (373 | ) |

Net sales — third party | | | 1,968 | | | | 1,194 | | | | 1,191 | | | | — | | | | | |

Cost of goods sold | | | (688 | ) | | | (985 | ) | | | (816 | ) | | | — | | | | (2,489 | ) |

Gross margin | | | 1,280 | | | | 209 | | | | 375 | | | | — | | | | 1,864 | |

Depreciation and amortization | | | (87 | ) | | | (145 | ) | | | (87 | ) | | | (6 | ) | | | (325 | ) |

Inter-segment sales | | | — | | | | — | | | | 81 | | | | — | | | | — | |

| | |

| PotashCorp 2011 Third Quarter Quarterly Report on Form 10-Q | | 10 |

| | | | | | | | | | | | | | | | | | | | |

| Assets | | Potash | | | Phosphate | | | Nitrogen | | | All Others | | | Consolidated | |

Assets at September 30, 2011 | | $ | 7,143 | | | $ | 2,672 | | | $ | 1,891 | | | $ | 4,116 | | | $ | 15,822 | |

Assets at December 31, 2010 | | $ | 5,773 | | | $ | 2,395 | | | $ | 1,808 | | | $ | 5,571 | | | $ | 15,547 | |

Change in assets | | $ | 1,370 | | | $ | 277 | | | $ | 83 | | | $ | (1,455 | ) | | $ | 275 | |

Additions to property, plant and equipment

(nine months ended September 30, 2011) | | $ | 1,238 | | | $ | 133 | | | $ | 117 | | | $ | 35 | | | $ | 1,523 | |

| 8. | Share-Based Compensation |

On May 12, 2011, the company’s shareholders approved the 2011 Performance Option Plan under which the company may, after February 22, 2011 and before January 1, 2012, issue options to acquire up to 3,000,000 common shares. Under the plan, the exercise price shall not be less than the quoted market closing price of the company’s common shares on the last trading day immediately preceding the date of the grant, and an option’s maximum term is 10 years. In general, options will vest, if at all, according to a schedule based on the three-year average excess of the company’s consolidated cash flow return on investment over weighted average cost of capital. As of September 30, 2011, options to purchase a total of 1,144,100 common shares had been granted under the plan. The weighted average fair value of options granted was $23.64 per share, estimated as of the date of grant using the Black-Scholes-Merton option-pricing model with the following weighted average assumptions:

| | | | |

Expected dividend | | $ | 0.28 | |

Expected volatility | | | 52% | |

Risk-free interest rate | | | 2.29% | |

Expected life of options | | | 5.5 years | |

A separate estimated average annual effective tax rate is determined for each taxing jurisdiction and applied individually to the interim period pre-tax income of each jurisdiction.

For the three months ended September 30, 2011, the company’s income tax expense was $279 (2010 — $152). For the nine months ended September 30, 2011, its income tax expense was $819 (2010 — $508). The actual effective tax rate including discrete items for the three and nine months ended September 30, 2011 was 25 percent (2010 — 31 percent and 29 percent, respectively). Total discrete tax adjustments that impacted the rate in the three months ended September 30, 2011 resulted in an income tax recovery of $5 compared to an income tax expense of $17 in the same period last year. Total discrete tax adjustments that impacted the rate in the nine months ended September 30, 2011 resulted in an income tax recovery of $29 compared to an income tax expense of $42 in the same period last year. Significant items recorded included the following:

| Ÿ | | In first-quarter 2011, a current tax recovery of $21 for previously paid withholding taxes; |

| Ÿ | | In third-quarter 2011, a current tax recovery of $12 due to income tax losses in a foreign jurisdiction; |

| Ÿ | | In the first nine months of 2010, a tax expense of $34 to adjust the 2009 income tax provision to the income tax returns filed for that year. |

Income tax balances within the consolidated statements of financial position were comprised of the following:

| | | | | | | | | | |

| Income tax assets (liabilities) | | Statements of Financial Position Location | | September 30,

2011 | | | December 31,

2010 | |

Current income tax assets: | | | | | | | | | | |

Current | | Receivables | | $ | 28 | | | $ | 46 | |

Non-current | | Other assets | | | 114 | | | | 122 | |

Deferred income tax assets | | Other assets | | | 22 | | | | 38 | |

Total income tax assets | | | | $ | 164 | | | $ | 206 | |

Current income tax liabilities: | | | | | | | | | | |

Current | | Payables and accrued charges | | $ | (179 | ) | | $ | (167 | ) |

Non-current | | Other non-current liabilities and deferred credits | | | (80 | ) | | | (142 | ) |

Deferred income tax liabilities | | Deferred income tax liabilities | | | (1,064 | ) | | | (737 | ) |

Total income tax liabilities | | | | $ | (1,323 | ) | | $ | (1,046 | ) |

| | |

| 11 | | PotashCorp 2011 Third Quarter Quarterly Report on Form 10-Q |

Basic net income per share for the quarter is calculated on the weighted average number of shares issued and outstanding for the three months ended September 30, 2011 of 856,022,000 (2010 — 890,913,000). Basic net income per share for the nine months ended September 30, 2011 is calculated based on the weighted average number of shares issued and outstanding for the period of 855,024,000 (2010 — 889,475,000).

Diluted net income per share is calculated based on the weighted average number of shares issued and outstanding during the period. The denominator is: (1) increased by the total of the additional common shares that would have been issued assuming the exercise of all stock options with exercise prices at or below the average market price for the period; and (2) decreased by the number of shares that the company could have repurchased if it had used the assumed proceeds from the exercise of stock options to repurchase them on the open market at the average share price for the period. For performance-based stock option plans, the number of contingently issuable common shares included in the calculation is based on the number of shares, if any, that would be issuable if the end of the reporting period were the end of the performance period and the effect were dilutive. The weighted average number of shares outstanding for the diluted net income per share calculation for the three months ended September 30, 2011 was 876,959,000 (2010 — 915,694,000) and for the nine months ended September 30, 2011 was 876,844,000 (2010 — 914,448,000).

Excluded from the calculation of diluted net income per share were weighted average options outstanding of 1,392,450 relating to the 2008 Performance Option Plan, as the options’ exercise prices were greater than the average market price of common shares for the period.

The company’s sales of fertilizer can be seasonal. Typically, the second quarter of the year is when fertilizer sales will be highest, due to the North American spring planting season. However, planting conditions and the timing of customer purchases will vary each year and sales can be expected to shift from one quarter to another.

Canpotex

PCS is a shareholder in Canpotex Limited (“Canpotex”), which markets Saskatchewan potash offshore. Should any operating losses or other liabilities be incurred by Canpotex, the shareholders have contractually agreed to reimburse it for such losses or liabilities

in proportion to each shareholder’s productive capacity. Through September 30, 2011, there were no such operating losses or other liabilities.

Mining Risk

As is typical with other companies in the industry, the company is unable to acquire insurance for underground assets.

Legal and Other Matters

Significant environmental site assessment and/or remediation matters of note include the following:

| Ÿ | | The company, along with other parties, has been notified by the US Environmental Protection Agency (“USEPA”) of potential liability under the US Comprehensive Environmental Response, Compensation and Liability Act of 1980 (“CERCLA”) with respect to certain soil and groundwater conditions at a site in Lakeland, Florida that includes a former PCS Joint Venture fertilizer blending facility and certain surrounding properties. A Record of Decision (“ROD”) was issued in September 2007 and provides for a remedy that requires excavation of impacted soils and interim treatment of groundwater. The total remedy cost is estimated in the ROD to be $9. In September 2010, the USEPA approved the Remedial Design Report to address the soil contamination. While subject to final construction inspection by the USEPA, the soil remediation has been performed. |

| Ÿ | | The USEPA has identified PCS Nitrogen, Inc. (“PCS Nitrogen”) as a potentially responsible party with respect to a former fertilizer blending operation in Charleston, South Carolina known as the Planters Property or Columbia Nitrogen site, formerly owned by a company from which PCS Nitrogen acquired certain other assets. The USEPA has requested reimbursement of $3 of previously incurred response costs and the performance or financing of future site investigation and response activities from PCS Nitrogen and other named potentially responsible parties. In September 2005, Ashley II of Charleston, L.L.C. (“Ashley II”), the current owner of the Planters Property, filed a complaint in the United States District Court for the District of South Carolina seeking a declaratory judgment that PCS Nitrogen is liable to pay environmental response costs that Ashley II alleges it has incurred and will incur in connection with response activities at the site. After the Phase II trial, the district court allocated 30 percent of the liability for response costs at the site to PCS Nitrogen, as well as a proportional share of any costs that cannot be recovered from another responsible party. PCS Nitrogen and other responsible parties filed motions for amendment of the decision, and the Court ruled on those motions in May 2011. The Court’s amended judgment did not alter the 30 percent allocation of liability to PCS but did award relief to PCS under a contractual indemnification claim. PCS and another responsible party have |

| | |

| PotashCorp 2011 Third Quarter Quarterly Report on Form 10-Q | | 12 |

| | | since submitted post-judgment motions to the Court, which are pending, and PCS filed a notice of appeal to the United States Court of Appeals for the Fourth Circuit. The notice of appeal was subsequently stayed by the Fourth Circuit pending resolution of the post-judgment motions. The ultimate amount of liability for PCS Nitrogen, if any, depends upon the amount needed for remedial activities, the ability of other parties to pay and the availability of insurance. |

| Ÿ | | PCS Phosphate has agreed to participate, on a non-joint and several basis, with parties to an Administrative Settlement Agreement with the USEPA (“Settling Parties”) in the performance of a removal action and the payment of certain other costs associated with PCB soil contamination at the Ward Superfund Site in Raleigh, North Carolina (“Site”), including reimbursement of the USEPA’s past costs. The removal activities commenced at the Site in August 2007. The cost of performing the removal action at the Site is estimated at $75. The Settling Parties have initiated CERCLA contribution litigation against PCS Phosphate and more than 100 other entities. PCS Phosphate filed crossclaims and counterclaims seeking cost recovery. In addition to the removal action at the Site, the USEPA has investigated sediments downstream of the Site in what is called “Operable Unit 1”. In September 2008, the USEPA issued a final remedy for Operable Unit 1, with an estimated cost of $6. The USEPA issued a Unilateral Administrative Order (UAO) dated September 29, 2011 to a number of entities, requiring them to implement the remedy for Operable Unit 1. PCS Phosphate did not receive the UAO. At this time, the company is unable to evaluate the extent of any exposure that it may have for the matters addressed in the UAO. |

| Ÿ | | Pursuant to the 1996 Corrective Action Consent Order (the “Order”) executed between PCS Nitrogen Fertilizer, L.P., formerly known as Arcadian Fertilizer, L.P. (“PCS Nitrogen Fertilizer”) and Georgia Department of Natural Resources, Environmental Protection Division (“GEPD”) in conjunction with PCS Nitrogen Fertilizer’s purchase of real property located in Augusta, Georgia from the entity from which PCS Nitrogen Fertilizer previously leased such property, PCS Nitrogen Fertilizer agreed to perform certain activities to investigate and, if necessary, perform a corrective action for substances in soil and groundwater. The investigation has proceeded and various corrective measures for substances in groundwater have been proposed to GEPD. PCS Nitrogen Fertilizer expects that it will implement corrective measures for substances in groundwater, but until GEPD approves the investigation results and a final corrective action plan, PCS Nitrogen Fertilizer is unable to estimate with reasonable certainty the total cost of its corrective action obligations under the Order. |

| Ÿ | | In December 2009, during a routine inspection of a gypsum stack at the White Springs, Florida facility, a sinkhole was discovered that resulted in the loss of approximately 82 million gallons of water from the stack. The company is sampling production and monitoring wells on its property and drinking water wells on neighboring property to assess impacts. The company incurred costs of $17 to address the sinkhole between the time of discovery through completion of remediation in July 2011. In December 2010, the company entered into a consent order with the Florida Department of Environmental Protection pursuant to which the company agreed to, among other things, remediate the sinkhole and perform additional monitoring of the groundwater quality and hydrogeologic conditions related to the sinkhole collapse. The company also entered into an order on consent with the USEPA. In May 2011, the USEPA and the Board of Directors approved the company’s proposal to implement certain mitigation measures to meet the goals of the USEPA order on consent. The company remeasured the asset retirement obligation (“ARO”) for the White Springs gypsum stacks to account for the measures identified in the proposal. This remeasurement resulted in a $39 adjustment to the ARO, of which $33 was capitalized as an addition to the related long-lived asset and $6 was expensed in the first quarter of 2011. |

The company is also engaged in ongoing site assessment and/or remediation activities at a number of other facilities and sites. Based on current information, it does not believe that its future obligations with respect to these facilities and sites are reasonably likely to have a material adverse effect on its consolidated financial position or results of operations.

Other significant matters of note include the following:

| Ÿ | | The USEPA has an ongoing initiative to evaluate implementation within the phosphate industry of a particular exemption for mineral processing wastes under the hazardous waste program. In connection with this industry-wide initiative, the USEPA conducted inspections at numerous phosphate operations and notified the company of various alleged violations of the US Resource Conservation and Recovery Act (“RCRA”) at its plants in Aurora, North Carolina; Geismar, Louisiana; and White Springs, Florida. The company has entered into RCRA 3013 Administrative Orders on Consent and has performed certain site assessment activities at all three plants. At this time, the company does not know the scope of corrective action, if any, that may be required. The company continues to participate in settlement discussions with the USEPA but is uncertain if any resolution will be possible without litigation, or, if litigation occurs, what the outcome would be. At this time, the company is unable to evaluate the extent of any exposure that it may have in these matters. |

| | |

| 13 | | PotashCorp 2011 Third Quarter Quarterly Report on Form 10-Q |

| Ÿ | | The USEPA has also begun an initiative to evaluate compliance with the Clean Air Act at sulfuric acid and nitric acid plants. In connection with this industry-wide initiative, the USEPA has sent requests for information to numerous facilities, including the company’s plants in Augusta, Georgia; Aurora, North Carolina; Geismar, Louisiana; Lima, Ohio; and White Springs, Florida. The USEPA has notified the company of various alleged violations of the Clean Air Act at its Geismar, Louisiana plant. The government has demanded process changes and penalties that would cost a total of approximately $30, but the company denies that it has any liability for the Geismar, Louisiana matter. Although the company is proceeding with planning and permitting for the process changes demanded by the government, the company is uncertain if any resolution will be possible without litigation, or, if litigation occurs, what the outcome would be. In July 2010, without alleging any specific violation of the Clean Air Act, the USEPA requested that the company meet and demonstrate compliance with the Clean Air Act for specified projects undertaken at the White Springs, Florida sulfuric acid plants. The company participated in such meeting but, at this time, is unable to evaluate if it has any exposure. |

| Ÿ | | Significant portions of the company’s phosphate reserves in Aurora, North Carolina are located in wetlands. Under the Clean Water Act, the company must obtain a permit from the US Army Corps of Engineers (the “Corps”) before mining in the wetlands. In January 2009, the Division of Water Quality of the North Carolina Department of Natural Resources issued a certification under Section 401 of the Clean Water Act that mining of phosphate in excess of 30 years from lands owned or controlled by the company, including some wetlands, would not degrade water quality. Thereafter, in June 2009, the Corps issued the company a permit that will allow the company to mine the phosphate deposits identified in the Section 401 certification. The USEPA decided not to seek additional review of the permit. In March 2009, four environmental organizations (Pamlico-Tar River Foundation, North Carolina Coastal Federation, Environmental Defense Fund and Sierra Club) filed a Petition for a Contested Case Hearing before the North Carolina Office of Administrative Hearings (“OAH”) challenging the Section 401 certification. The company has intervened in this proceeding. Cross motions for summary judgment by the Petitioners and the company have been filed, briefed and argued. The OAH has not issued a decision on them. At this time, the company is unable to evaluate the extent of any exposure that it may have in this matter. |

| Ÿ | | In May 2009, the Canadian government announced that its new industrial greenhouse gas emissions policies will be coordinated with policies that may be implemented in the US. The Province of Saskatchewan is considering the adoption of greenhouse gas emission control requirements. Regulations pursuant to the Management and Reduction of Greenhouse Gases Act in |

| | | Saskatchewan, which impose a type of carbon tax to achieve a goal of a 20 percent reduction in greenhouse gas emissions by 2020 compared to 2006 levels, may become effective in 2012. There is no certainty as to the scope or timing of any final, effective provincial requirements. Although the US Congress has not passed any greenhouse gas emission control laws, the USEPA has adopted several rules to control greenhouse gas emissions using authority under existing environmental laws. In January 2011, the USEPA began phasing in requirements for all “stationary sources,” such as the company’s plants, to obtain permits incorporating the “best available control technology” for greenhouse gas emissions at a source if it is a new source that could emit 100,000 tons of greenhouse gases per year or if it is a modified source that increases such emissions by 75,000 tons per year. The company is not currently aware of any projects at its facilities that would be subject to these requirements. The company is monitoring these developments, and, except as indicated above, their effect on its operations cannot be determined with certainty at this time. |

| Ÿ | | In December 2010, the USEPA issued a final rule to restrict nutrient concentrations in surface waters in Florida to levels below those currently permitted at the company’s White Springs, Florida plant. The revised nutrient criteria will become part of Florida’s water quality standards in March 2012. Projected capital costs resulting from the rule could be in excess of $100 for the company’s White Springs, Florida plant, and there is no guarantee that controls can be implemented that are capable of achieving compliance with the revised nutrient standards under all flow conditions. This estimate assumes that the rule survives court challenges and that none of the site-specific mechanisms for relief from the revised nutrient criteria are available to the White Springs, Florida plant. Various judicial challenges to the rule have been filed, including one lawsuit by The Fertilizer Institute (“TFI”) and White Springs. On June 15, 2011, TFI, White Springs and additional parties filed a Motion for Summary Judgment seeking, among other things, to vacate the USEPA rule. On September 15, 2011, the USEPA filed its Motion for Summary Judgment seeking to uphold its rule. The prospects for a rule to be implemented as issued by the USEPA and the availability of the site-specific mechanisms are uncertain. |

| Ÿ | | The company, having been unable to agree with Mosaic Potash Esterhazy Limited Partnership (“Mosaic”) on the remaining amount of potash that the company is entitled to receive from Mosaic pursuant to the mining and processing agreement in respect of the company’s rights at the Esterhazy mine, issued a Statement of Claim in the Saskatchewan Court of Queen’s Bench (“Court”) against Mosaic on May 27, 2009 and the claim was amended on January 19, 2010. In the Amended Statement of Claim, the company has asserted that it has the right under the mining and processing agreement to receive potash from Mosaic |

| | |

| PotashCorp 2011 Third Quarter Quarterly Report on Form 10-Q | | 14 |

| | | until at least 2012 and potentially much later, and seeks an order from the Court declaring the amount of potash which the company has the right to receive. Mosaic, in its Statement of Defence, asserts that at a delivery rate of 1.24 million tons of product per year, the company’s entitlement to receive potash under the mining and processing agreement would terminate August 30, 2010. |

In addition, at the time of filing its Statement of Defence, Mosaic commenced a counterclaim against the company, asserting that the company has breached the mining and processing agreement due to its refusal to take delivery of potash product under the agreement based on an event of force majeure.

The company was notified on May 2, 2011 that Mosaic believes that it has satisfied its obligation to produce potash at the Esterhazy mine for the company under the mining and processing agreement and as such it has no further obligation to deliver potash to the company from the Esterhazy mine, other than the company’s remaining inventory. The company disagreed and sought relief from the Court. On June 30, 2011, an injunction order was issued by the Court requiring delivery pursuant to the terms of the mining and processing agreement pending trial or a further order of the Court (“Injunction Order”). The trial is currently scheduled to commence in January 2012. Like every applicant for injunctive relief, the company was required to provide an undertaking to pay any damages that may be occasioned to Mosaic as a result of the granting of the injunction should it later be shown that Mosaic had, by reason of the injunction, sustained any damages which the company ought to pay. The company does not believe that Mosaic will be entitled to any damages arising from the issuance of the Injunction Order. On July 18, 2011, Mosaic filed a Notice of Appeal with the Court of Appeal for Saskatchewan (“Court of Appeal”) appealing the Injunction Order and seeking to set it aside. On October 24, 2011, the Court of Appeal dismissed Mosaic’s appeal of the Injunction Order.

The company will continue to assert its position in this litigation vigorously and it denies liability to Mosaic in connection with its counterclaim.

| Ÿ | | Between September and October 2008, the company and PCS Sales (USA), Inc. were named as defendants in eight similar antitrust complaints filed in US federal courts. Other potash producers are also defendants in these cases. Each of the separate complaints alleges conspiracy to fix potash prices, to divide markets, to restrict supply and to fraudulently conceal the conspiracy, all in violation of Section 1 of the Sherman Act. On September 23, 2011, the United States Court of Appeals for the Seventh Circuit issued an opinion directing the trial court to dismiss certain of the plaintiffs’ claims. The plaintiffs have petitioned for rehearing en banc and proceedings are ongoing. |

| | | The company and PCS Sales (USA), Inc. believe each of these eight private antitrust lawsuits is without merit and intend to defend them vigorously. |

In addition, various other claims and lawsuits are pending against the company in the ordinary course of business. While it is not possible to determine the ultimate outcome of such actions at this time, and inherent uncertainties exist in predicting such outcomes, it is the company’s belief that the ultimate resolution of such actions is not reasonably likely to have a material adverse effect on its consolidated financial position or results of operations.

The breadth of the company’s operations and the global complexity of tax regulations require assessments of uncertainties and judgments in estimating the taxes it will ultimately pay. The final taxes paid are dependent upon many factors, including negotiations with taxing authorities in various jurisdictions, outcomes of tax litigation and resolution of disputes arising from federal, provincial, state and local tax audits. The resolution of these uncertainties and the associated final taxes may result in adjustments to the company’s tax assets and tax liabilities.

The company owns facilities that have been either permanently or indefinitely shut down. It expects to incur nominal annual expenditures for site security and other maintenance costs at certain of these facilities. Should the facilities be dismantled, certain other shutdown-related costs may be incurred. Such costs are not expected to have a material adverse effect on the company’s consolidated financial position or results of operations and would be recognized and recorded in the period in which they are incurred.

| 13. | Related Party Transactions |

The company sells potash from its Saskatchewan mines for use outside of North America exclusively to Canpotex, a potash export, sales and marketing company owned in equal shares by the three potash producers in the Province of Saskatchewan. Sales to Canpotex for the three months ended September 30, 2011 were $497 (2010 — $283) and nine months ended September 30, 2011 were $1,537 (2010 — $874). At September 30, 2011, $334 (December 31, 2010 — $298) was owing from Canpotex. Sales to Canpotex are at prevailing market prices and account balances resulting from the Canpotex transactions are settled on normal trade terms.

| | |

| 15 | | PotashCorp 2011 Third Quarter Quarterly Report on Form 10-Q |

| 14. | Reconciliation of IFRS and US GAAP |

IFRS vary in certain significant respects from US GAAP. As required by the United States Securities and Exchange Commission, the effect of these principal differences on the company’s unaudited interim condensed consolidated financial statements is described and quantified below.

(a) Inventories: Under IFRS, when the circumstances that previously caused inventories to be written down below cost no longer exist or when there is clear evidence of an increase in net realizable value because of changed economic circumstances, the amount of the writedown is reversed. The reversal is limited to the amount of the original writedown. Under US GAAP, the reversal of a writedown is not permitted unless the reversal relates to a writedown recorded in a prior interim period during the same fiscal year.

Under IFRS, interim price, efficiency, spending and volume variances of a manufacturing entity are recognized in income at interim reporting dates to the same extent that those variances are recognized in income at year-end. Deferral of variances that are expected to be absorbed by year-end is not appropriate because such deferrals could result in reporting inventory at the interim date at more or less than its portion of the actual cost of manufacture. Under US GAAP, variances that are planned and expected to be absorbed by the end of the year are ordinarily deferred at the end of an interim period.

(b) Long-term investments: Certain of the company’s investments in international entities are accounted for under the equity method. Accounting principles generally accepted in those foreign jurisdictions may vary in certain respects from US GAAP. The company’s share of earnings of these equity-accounted investees under IFRS has been adjusted for the significant effects of conforming to US GAAP.

(c) Property, plant and equipment: The net book value of property, plant and equipment under IFRS differs from that under US GAAP in certain respects, including the following:

Major repairs and maintenance, including turnarounds, are capitalized under IFRS and expensed under US GAAP unless costs represent a betterment, in which case capitalization under US GAAP is appropriate.

Borrowing costs under IFRS are capitalized to property, plant and equipment based on the weighted average interest rate on all of the company’s outstanding third-party debt; under US GAAP, only the weighted average interest rate on third-party long-term debt is used to determine the capitalized amount.

(d) Impairment of assets: Upon adopting IFRS, the company elected not to restate past business combinations, which resulted in the carrying amount of goodwill under IFRS being the same amount as it had been under previous Canadian GAAP at the date of transition to IFRS. Because past provisions for asset impairment were based on undiscounted cash flows from use under Canadian GAAP and on fair value under US GAAP, the carrying amount of goodwill is lower under US GAAP.

In respect of oil and gas assets, US GAAP requires that writedowns be based on discounted cash flows, a prescribed discount rate and the unweighted average first-day-of-the-month resource prices for the prior 12 months; IFRS requires discounted cash flows using estimated future resource prices based on the best information available to the company.

Assets, except goodwill, that were previously impaired can be reversed in subsequent periods, under IFRS, if the conditions that led to the original impairment reversed. Reversals of asset impairments are prohibited under US GAAP.

(e) Depreciation and amortization: Depreciation and amortization under IFRS differ from that under US GAAP, as a result of differences in the carrying amounts of property, plant and equipment under IFRS and US GAAP, as described above.

(f) Exploration costs: Under IFRS, capitalized exploration costs are classified as exploration and evaluation assets. For US GAAP, these costs are generally expensed until such time as a final feasibility study has confirmed the existence of a commercially mineable deposit.

(g) Pension and other post-retirement benefits: Under US GAAP, the company recognizes the difference between the benefit obligation and the fair value of plan assets in the consolidated statements of financial position with the offset to OCI. Amounts in OCI are amortized to net income. Under IFRS, actuarial gains and losses are recognized directly in OCI and cleared out to retained earnings without ever being amortized to net income. Unrecognized prior service costs are not recognized in OCI, but are amortized to net income over the average remaining vesting period.

(h) Offsetting of certain amounts: US GAAP requires an entity to adopt a policy of either offsetting or not offsetting fair value amounts recognized for derivative instruments and for the right to reclaim cash collateral or the obligation to return cash collateral against fair value amounts recognized for derivative instruments executed with the same counterparty under the same master netting arrangement. The company adopted a policy to offset such amounts. Under IFRS, offsetting of margin deposits is not permitted.

| | |

| PotashCorp 2011 Third Quarter Quarterly Report on Form 10-Q | | 16 |

(i) Share-based compensation: Under IFRS, stock options are recognized over the service period, which for PotashCorp is established by the option performance period. Under US GAAP, stock options are recognized over the requisite service period, which does not commence until the option plan is approved by the company’s shareholders and options are granted thereunder.

| | | | | | | | |

Performance Option Plan Year | | Service Period Commenced | |

| | IFRS | | | US GAAP | |

2008 | | | January 1, 2008 | | | | May 8, 2008 | |

2009 | | | January 1, 2009 | | | | May 7, 2009 | |

2010 | | | January 1, 2010 | | | | May 6, 2010 | |

2011 | | | January 1, 2011 | | | | May 12, 2011 | |

This difference impacts the share-based compensation cost recorded and may impact diluted earnings per share.

Further, under IFRS the company recognized an estimate of compensation cost in relation to performance options for which service commenced but which had not yet been granted. Specifically, an estimate of compensation cost was recognized at the end of the first quarter of 2011 in relation to the 2011 Performance Option Plan, which was approved by shareholders at the company’s annual meeting on May 12, 2011, for which service commenced but for which performance options had not yet been granted. The compensation cost recognized was reconciled in the second quarter once options were granted. Under US GAAP, no compensation cost is recognized until the option plans are approved.

(j) Stripping costs: Under IFRS, the company capitalizes and amortizes costs associated with the activity of removing overburden and other mine waste minerals in the production phase. US GAAP requires such stripping costs to be attributed to ore produced in that period as a component of inventory and recognized in cost of sales in the same period as related revenue.

(k) Provisions: Asset retirement obligations under IFRS are measured and remeasured each reporting period using a current risk-free discount rate. Under US GAAP, the obligation is initially measured using a credit-adjusted risk-free discount rate. Subsequent upward revisions are measured using the current discount rate while downward revisions are valued using the historical discount rate. Under IFRS, obligations incurred through the production of inventory are included in the cost of that inventory. Under US GAAP, obligations incurred through the production of inventory are added to the carrying amount of the related long-lived asset or charged to expense as incurred. Under IFRS, provisions for asset retirement obligations include constructive obligations. Under US GAAP, only legal obligations are recognized.

Under IFRS, a provision is recognized for either a legal or constructive obligation when the applicable criteria are otherwise met. Under US GAAP, constructive obligations are recognized only when required under a specific standard.

(l) Income taxes related to the above adjustments: The income tax adjustment reflects the impact on income taxes of the US GAAP adjustments described above. Accounting for income taxes under IFRS and US GAAP is similar, except that income tax rates of enacted or substantively enacted tax law must be used to calculate deferred income tax assets and liabilities under IFRS, whereas only income tax rates of enacted tax law can be used under US GAAP.

(m) Income taxes related to US GAAP effective income tax rate: As it relates to interim periods, under IFRS a separate estimated average annual effective income tax rate is determinedfor each taxing jurisdiction and applied individually to the interim period pre-tax income of each jurisdiction, whereas under US GAAP a weighted average of the annual rates expected across all jurisdictions is applied.

(n) Income tax consequences of share-based employee compensation: Under IFRS, the income tax benefit attributable to share-based compensation that is deductible in computing taxable income but is not recorded in the consolidated financial statements as an expense of any period includes the amount realized in the period (the “realized excess benefit”), as well as the amount of future tax deductions that the company expects to receive based on the current market price of the shares (the “unrealized excess benefit”). The unrealized excess benefit is recognized as a deferred income tax asset with the offset recorded in contributed surplus. Under US GAAP, only the realized excess benefit is recorded, in additional paid-in capital.

Under IFRS, the income tax benefit associated with share-based compensation that is recorded in the consolidated financial statements as an expense in the current or previous period is reviewed at each statement of financial position date and amended to the extent that it is no longer probable that the related tax benefit will be realized. Under US GAAP, this income tax benefit is calculated without estimating the income tax effects of anticipated share-based payment transactions.

| | |

| 17 | | PotashCorp 2011 Third Quarter Quarterly Report on Form 10-Q |

(o) Uncertain income tax positions: US GAAP prescribes a comprehensive model for how a company should recognize, measure, present and disclose in its consolidated financial statements uncertain income tax positions that it has taken or expects to take on a tax return (including a decision whether to file or not to file a return in a particular jurisdiction). IFRS have no similar requirements related to uncertain income tax positions. The company accounts for uncertain income tax positions under IFRS using the standards applicable to current income tax assets and liabilities, i.e., both liabilities and assets are recorded when probable at the company’s best estimate of the amount.

(p) Income taxes related to intragroup transactions: Under IFRS, unrealized profits resulting from intragroup transactions are eliminated from the carrying amount of assets, but no equivalent adjustment is made for tax purposes. The difference between the tax rates of the two entities will result in an impact on net income. This differs from US GAAP, where the current tax payable in relation to such profits is recorded as a current asset until the transaction is realized by the group.

(q) Classification of deferred income taxes: Under IFRS, deferred income taxes are classified as long-term. Under US GAAP, deferred income taxes are separated between current and long-term on the consolidated statements of financial position.