UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

--------------------------

FORM 10-K

☑ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2022

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ___ to ___

Commission File Number 1-12273

ROPER TECHNOLOGIES, INC.

(Exact name of Registrant as specified in its charter)

---------------- | | | | | |

| Delaware | 51-0263969 |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

----------------

6901 Professional Parkway, Suite 200

Sarasota, Florida 34240

(Address of principal executive offices) (Zip Code)

Registrant’s telephone number, including area code: (941) 556-2601

----------------

SECURITIES REGISTERED PURSUANT TO SECTION 12(b) OF THE ACT: | | | | | | | | | | | | | | |

| Title of Each Class | | Trading Symbol | | Name of Each Exchange On Which Registered |

| Common Stock, $0.01 Par Value | | ROP | | New York Stock Exchange |

SECURITIES REGISTERED PURSUANT TO SECTION 12(g) OF THE ACT: None

----------------

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. þ Yes ☐ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. ☐ Yes þ No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. þ Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§223.405) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). þ Yes ☐ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company (as defined in Rule 12b-2 of the Exchange Act). þ Large accelerated filer ☐ Accelerated filer ☐ Non-accelerated filer ☐ Smaller reporting company ☐ Emerging growth company

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issues its audit report. þ

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark if the registrant is a shell company (as defined in Rule 12b-2 of the Act). ☐ Yes þ No

Based on the closing sale price on the New York Stock Exchange on June 30, 2022, the aggregate market value of the voting and non-voting common stock held by non-affiliates of the registrant was: $41.6 billion.

Number of shares of registrant’s Common Stock outstanding as of February 17, 2023: 106,243,275.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s Proxy Statement to be furnished to Stockholders in connection with its 2023 Annual Meeting of Stockholders are incorporated by reference into Part III, Items 10, 11, 12, 13 and 14 of this Annual Report on Form 10-K.

ROPER TECHNOLOGIES, INC.

FORM 10-K FOR THE FISCAL YEAR ENDED DECEMBER 31, 2022

Table of Contents

Information About Forward-Looking Statements

This Annual Report on Form 10-K (“Annual Report”) includes and incorporates by reference “forward-looking statements” within the meaning of the federal securities laws. In addition, we, or our executive officers on our behalf, may from time to time make forward-looking statements in reports and other documents we file with the U.S. Securities and Exchange Commission (“SEC”) or in connection with oral statements made to the press, potential investors or others. All statements that are not historical facts are “forward-looking statements.” Forward-looking statements may be indicated by words or phrases such as “anticipate,” “estimate,” “plans,” “expects,” “projects,” “should,” “will,” “believes” or “intends” and similar words and phrases. These statements reflect management’s current beliefs and are not guarantees of future performance. They involve risks and uncertainties that could cause actual results to differ materially from those contained in any forward-looking statement. Such risks and uncertainties include any ongoing impacts of the COVID-19 pandemic on our business, operations, financial results and liquidity, which will depend on numerous evolving factors which we cannot accurately predict or assess.

Examples of forward-looking statements in this report include but are not limited to statements regarding operating results, the success of our operating plans, our expectations regarding our ability to generate cash and reduce debt and associated interest expense, profit and cash flow expectations, the prospects for newly acquired businesses to be integrated and contribute to future growth and our expectations regarding growth through acquisitions. Important assumptions relating to the forward-looking statements include, among others, demand for our products, the cost, timing and success of product upgrades and new product introductions, raw material costs, expected pricing levels, expected outcomes of pending litigation, competitive conditions and general economic conditions. These assumptions could prove inaccurate. Although we believe that the estimates and projections reflected in the forward-looking statements are reasonable, our expectations may prove to be incorrect. Important factors that could cause actual results to differ materially from estimates or projections contained in the forward-looking statements include but are not limited to:

•general economic conditions;

•difficulty making acquisitions and successfully integrating acquired businesses;

•any unforeseen liabilities associated with future acquisitions;

•failure to effectively mitigate cybersecurity threats, including any litigation arising therefrom;

•failure to comply with new data privacy laws and regulations, including any litigation arising therefrom;

•risks and costs associated with our international sales and operations;

•rising interest rates;

•limitations on our business imposed by our indebtedness;

•product liability and insurance risks;

•future competition;

•reduction of business with large customers;

•risks associated with government contracts;

•changes in the supply of, or price for, labor, energy, raw materials, parts and components, including as a result of impacts from the current inflationary environment, supply chain constraints or additional or ongoing outbreaks of COVID-19;

•potential write-offs of our goodwill and other intangible assets;

•our ability to successfully develop new products;

•failure to protect our intellectual property;

•unfavorable changes in foreign exchange rates;

•difficulties associated with exports/imports and risks of changes to tariff rates;

•increased warranty exposure;

•environmental compliance costs and liabilities;

•the effect of, or change in, government regulations (including tax);

•economic disruption caused by armed conflicts (such as the war in Ukraine), terrorist attacks, health crises (such as the COVID-19 pandemic) or other unforeseen geopolitical events; and

•the factors discussed in Item 1A to this Annual Report under the heading “Risk Factors.”

You should not place undue reliance on any forward-looking statements, which are based on current expectations. Further, forward-looking statements speak only as of the date they are made, and we undertake no obligation to publicly update any of these statements in light of new information or future events.

PART I

ITEM 1. BUSINESS

All currency amounts are in millions unless specified

Our Business

Roper Technologies, Inc. (“Roper,” the “Company,” “we,” “our” or “us”) is a diversified technology company. Roper has a proven, long-term, successful track record of compounding cash flow and shareholder value. We operate market leading businesses that design and develop vertical software and technology enabled products for a variety of defensible niche markets.

We pursue consistent and sustainable growth in revenue, earnings and cash flow by enabling continuous improvement in the operating performance of our existing businesses and by acquiring other businesses that offer high value-added software, services, technology-enabled products and solutions that we believe are capable of achieving growth and maintaining high margins. We compete in many defensible niche markets and believe we are the market leader or a competitive alternative to the market leader in most of these markets. In the last three years, we have deployed approximately $10,500 of capital toward acquisitions, including approximately $3,750 in 2022 for the acquisition of Frontline Education, a leading provider of Software-as-a-Service (“SaaS”) solutions for school administration and approximately $5,400 in 2020 for the acquisition of Vertafore, Inc., a leading provider of SaaS solutions for the property and casualty insurance industry. Additionally, we deployed approximately $1,400 towards bolt-on acquisitions to help build on the strategic position of several of our businesses.

On November 22, 2022, the Company completed the divestiture of a majority 51% equity stake in its industrial businesses, including its entire historical Process Technologies reportable segment and the industrial businesses within its historical Measurement & Analytical Solutions reportable segment, to Clayton, Dubilier & Rice, LLC. The businesses included in this transaction were Alpha, AMOT, CCC, Cornell, Dynisco, FTI, Hansen, Hardy, Logitech, Metrix, PAC, Roper Pump, Struers, Technolog, Uson, and Viatran (collectively “Indicor”). Following the sale of the majority stake, the Company retained an initial 49% minority equity interest in the new standalone parent company, Indicor, LLC. This transaction is referred to herein as the “Indicor Transaction.”

During 2021, Roper entered into definitive agreements to divest our TransCore, Zetec and CIVCO Radiotherapy businesses (“2021 Divestitures”). As of March 31, 2022, Roper had completed the 2021 Divestitures.

The aggregate of the 2021 Divestitures and Indicor Transaction have greatly reduced the cyclicality and asset intensity of the Company. In addition, the Company has an increased mix of recurring revenue and a higher margin profile. The financial results for Indicor and the 2021 Divestitures are reported as discontinued operations for all periods presented. Unless otherwise noted, discussion within Part I relates to continuing operations. Information regarding discontinued operations is included in Note 3 of the Notes to Consolidated Financial Statements.

We were incorporated on December 17, 1981 under the laws of the State of Delaware.

Market Share, Market Expansion, and Product Development

Leadership with Technology and Products for Niche Markets - We maintain a leading position in many of our markets. We believe our market positions are attributable to the applications expertise used to create high value products and solutions for our customers, the underlying critical nature of our offerings, and the inherent customer intimacy of our chosen niche markets. Our businesses realize growth from new and existing customers in their niche markets through successfully executing go-to-market strategies, developing new products and applications, and delivering professional services.

Diversified End Markets and Geographic Reach - We have a global presence, with sales to customers outside the United States (“U.S.”). totaling $806.5 in 2022. Information regarding our international operations is set forth in Note 14 of the Notes to Consolidated Financial Statements included in this Annual Report.

Our Reportable Segments

During the second quarter of 2022, we updated our reportable segment structure following the announcement of the Indicor Transaction. The Company’s new reporting segment structure is classified based on business model and delivery of performance obligations. The three updated reportable segments (and businesses within each; including changes due to acquisitions since the realignment) are as follows:

–Application Software - Aderant, CBORD/Horizon, CliniSys, Data Innovations, Deltek, Frontline Education, IntelliTrans, PowerPlan, Strata, Vertafore

–Network Software - ConstructConnect, DAT, Foundry, iPipeline, iTradeNetwork, Loadlink, MHA, SHP, SoftWriters

–Technology Enabled Products - CIVCO Medical Solutions, FMI, Inovonics, IPA, Neptune, Northern Digital, rf IDEAS, Verathon

Following the Indicor Transaction and the realignment of our reportable segments, the day-to-day operations of our businesses, our organizational structure, and our strategy remain unchanged. All prior periods have been recast to reflect the changes noted above. Financial information about our reportable segments is presented in Note 14 of the Notes to Consolidated Financial Statements included in this Annual Report.

Application Software

Our Application Software segment had net revenues of $2,639.5 for the year ended December 31, 2022, representing 49.1% of our total net revenues. Below is a description of the products offered by business that comprise the Application Software segment.

Aderant - comprehensive management software solutions for law and other professional services firms, including business development, calendar/docket matter management, time and billing and case management.

CBORD/Horizon - campus solutions software including access and cashless systems and food and nutrition service management serving primarily higher education and healthcare markets along with software, services, and technologies for foodservice operations specializing in K-12.

CliniSys - diagnostic and laboratory information management software solutions.

Data Innovations - software solutions that enable enterprise management of hospitals and independent laboratories.

Deltek - enterprise software and information solutions for government contractors, professional services firms and other project-based businesses.

Frontline Education - K-12 school administration software, connecting solutions for human capital management, student and special programs, and business operations with powerful analytics to empower educators.

IntelliTrans - transportation management software and services to bulk and break-bulk commodity producers.

PowerPlan - financial and compliance management software and solutions to large complex companies in asset-intensive industries.

Strata - cloud-based financial analytics and performance management software that is used by healthcare providers for financial planning, decision support and continuous cost improvement.

Vertafore - cloud-based software to the property and casualty insurance industry, including agency management, compliance, workflow, and data solutions.

Network Software

Our Network Software segment had net revenues of $1,378.5 for the year ended December 31, 2022, representing 25.7% of our total net revenues. Below is a description of the products offered by business that comprise the Network Software segment.

ConstructConnect - cloud-based data, collaboration and estimating automation software solutions to a network of pre-construction contractors.

DAT - electronic marketplaces that connect available capacity of trucking units with the available loads of freight throughout North America.

Foundry - software technologies used to deliver visual effects and 3D content for the entertainment and digital design industries.

iPipeline - cloud-based software solutions for the life insurance and financial services industries.

iTradeNetwork - electronic marketplaces and supply chain software that connect food suppliers, distributors and vendors, primarily in the perishable food sector.

Loadlink - electronic marketplaces that connect available capacity of trucking units with the available loads of freight throughout Canada.

MHA - health care service and software solutions to alternate site health care markets.

SHP - data analytics and benchmarking information for the post-acute healthcare provider marketplace.

SoftWriters - software solutions to pharmacies that primarily serve the long term care marketplace.

Technology Enabled Products

Our Technology Enabled Products segment had net revenues of $1,353.8 for the year ended December 31, 2022, representing 25.2% of our total net revenues. Below is a description of the products offered by business that comprise the Technology Enabled Products segment.

CIVCO Medical Solutions - accessories focused on guidance and infection control for ultrasound procedures.

FMI - dispensers and metering pumps which are utilized in a broad range of applications requiring precision fluid control.

Inovonics - high-performance wireless sensor network and solutions for a variety of applications.

IPA - automated surgical scrub and linen dispensing equipment for healthcare providers.

Neptune - water meters, enabling water utilities to remotely monitor their customers utilizing Automatic Meter Reading (AMR), Advanced Metering Infrastructure (AMI) technologies and cloud-based software supporting meter data management.

Northern Digital - optical and electromagnetic precision measurement systems for medical and industrial applications.

rf IDeas - RFID card readers used in numerous identity access management applications across a variety of vertical markets.

Verathon - medical devices that enable airway management and bladder volume measurement solutions for healthcare providers.

Materials and Suppliers

We believe most materials and supplies we use are readily available from numerous sources and suppliers throughout the world. However, some components and sub-assemblies are currently available from only a limited number of suppliers for which we regularly investigate and identify alternative sources where possible. We also believe these conditions affect our competitors. Although supply shortages have not had a material adverse effect on our revenues, we may continue to be impacted by supply chain challenges including increased material costs, component shortages and transportation disruptions and delays.

Remaining Performance Obligations and Backlog

Remaining performance obligations represents the transaction price of firm orders for which work has not been performed and excludes unexercised contract options. As of December 31, 2022 and December 31, 2021, the aggregate amount of the transaction price allocated to remaining performance obligations was $4,214.0 and $3,539.1, respectively.

Backlog is equal to our remaining performance obligations expected to be recognized as revenue within the next 12 months. Backlog was $2,912.6 at December 31, 2022, and $2,325.1 at December 31, 2021.

Distribution and Sales

Distribution and sales occur primarily through direct sales offices, manufacturers’ representatives, resellers and distributors.

Governmental Regulations

We face extensive government regulation around the world relating to the development, manufacture, marketing, sale and distribution of our software, services, and products. The following sections describe certain significant regulations to which we are subject, but these are not the only regulations to which our businesses must comply. For a description of the risks related to the regulations that our businesses are subject to, please refer to “Item 1A. Risk Factors.”

Privacy and Data Security

We are subject to privacy and data security laws around the world that may impose operational burdens on our businesses. In 2018, the General Data Protection Regulation (“GDPR”) became effective in the European Union (“EU”) and United Kingdom and imposed restrictions on how companies use and process personal information. In particular, legal challenges to the way regulators implemented GDPR have created additional operational burdens for companies transferring personal data back and forth between the EU, U.S., and India. In the U.S., several states have adopted legislation that imposes similar (but not identical) restrictions to GDPR on companies conducting business or serving customers in those states. For example, in 2020 the California Consumer Privacy Act (“CCPA”) became effective and required companies to make disclosures to consumers about their data collection, use, and sharing practices; allowed consumers to opt out of certain data sharing with third parties; and provided a private right of action for data breaches. Changes to the CCPA effective in 2023 have added to the processing restrictions and notifications requirements – particularly when companies engage in online advertising. Virginia, Colorado, Connecticut, and Utah have passed similar legislation that will also become effective in 2023. Canada (Quebec) and China have also significantly updated their privacy laws. The compliance and other burdens on our businesses imposed by these privacy laws and regulations may be substantial as we work to comply with differing legal and implementation requirements across multiple jurisdictions.

Healthcare Regulations

The manufacture, sale, lease and service of medical diagnostic and surgical devices intended for commercial use are subject to extensive governmental regulation by the FDA in the U.S. and by a variety of regulatory agencies in other countries for some of our businesses. Under the Federal Food, Drug and Cosmetic Act, known as the FD&C Act, manufacturers of medical products and devices must comply with certain regulations governing the design, testing, manufacturing, packaging, servicing and marketing of medical products. FDA product approvals may be withdrawn or suspended if compliance with regulatory standards is not maintained or if problems occur following initial marketing. We are also subject to a variety of federal, state and foreign laws which broadly relate to our interactions with healthcare practitioners and other participants in the healthcare system, including, among others, anti-kickback law, and laws regulating the confidentiality of sensitive personal information and the circumstances under which such information may be released and/or collected, such as the Health Insurance Portability and Accountability Act of 1996, or HIPAA, the Health Information Technology for Economic and Clinical Health Act, or HITECH Act, and the GDPR.

Anti-Corruption and Anti-Bribery Laws and Regulations

We are subject to the U.S. Foreign Corrupt Practices Act (FCPA) and anti-corruption laws, and similar laws in foreign countries, such as the UK Anti-Bribery Act. Any violation of these laws by us or our agents or distributors could create substantial liability for us, subject our officers and directors to personal liability, and cause a loss of reputation in the market. Increased business in higher risk countries could subject us and our officers and directors to increased scrutiny and increased liability. In addition, becoming familiar with and implementing the infrastructure necessary to comply with laws, rules and regulations applicable to new business activities and mitigating and protecting against corruption risks could be quite costly.

Export Controls and Trade Policies

We are subject to numerous domestic and foreign regulations relating to our operations worldwide. In particular, our sales activities must comply with restrictions relating to the export of controlled technology and sales to denied or sanctioned parties contained in the U.S. Export Administration Regulations, U.S. International Traffic in Arms Regulations (ITAR), and sanctions administered by the Office of Foreign Asset Controls of the U.S. Treasury Department (OFAC). Our businesses may also be impacted by additional domestic or foreign trade regulations ensuring fair trade practices, including trade restrictions, tariffs and sanctions.

Environmental Regulations

Our operations and properties are subject to laws and regulations relating to environmental protection, including those governing air emissions, water discharges, waste management and workplace safety. We use, generate and dispose of hazardous substances and waste in our operations and could be subject to material liabilities relating to the investigation and clean-up of contaminated properties and related claims. We are required to conform our operations and properties to these laws and adapt to regulatory requirements in all countries as these requirements change. In connection with our acquisitions, we may assume significant environmental liabilities, some of which we may not be aware of, or may not be quantifiable, at the time of acquisition. In addition, new laws and regulations, the discovery of previously unknown contamination or the imposition of new requirements could increase our costs or subject us to new or increased liabilities.

Customers

During 2022, no customer accounted for 10% or more of any segment or total Company net revenues.

Competition

Generally, our products and solutions face significant competition, although in certain niche markets there are a limited number of competitors. We believe that we are a leader in most of our markets, and no single company competes with us over a significant number of product lines. Competitors might be large or small in size, often depending on the size of the niche market we serve. We compete primarily on product quality, performance, innovation, technology, price, applications expertise, system and service flexibility, distribution channel access and customer service capabilities.

Intellectual Property

In addition to trade secrets, including unpatented know-how and other intellectual property like software source code, we own or license the rights under numerous patents, trademarks, trade dress and copyrights relating to certain of our products and businesses. We also employ various methods, including confidentiality and non-disclosure agreements with individuals and companies we do business with, including employees, distributors, representatives, independent contractors and customers to protect our intellectual property. We believe none of our operating units are substantially dependent on any single item of intellectual property, including a trade secret, patent, trademark, trade dress, or copyright.

Human Capital Management

Roper is a diversified technology company that utilizes a decentralized operating model across our many businesses which serve a diverse set of end markets. Subject to oversight and guidance from Roper executive management, each business operates as an individual unit with its managers empowered to make day to day operating decisions, including decisions with respect to human capital management. As a result, apart from guidance with respect to: (i) compliance with regulatory requirements or corporate policies; and (ii) the implementation of compensation and benefit programs provided by corporate management, managers at individual businesses are the primary decision makers with respect to human capital management and development. Though our individual businesses are primarily responsible for these decisions, because of the importance of human capital to our enterprise, we provide guidance and share best practices on key aspects of selection, development, engagement and diversity of talent within our workforce.

As of December 31, 2022, we employed approximately 15,800 people worldwide on a consolidated basis, of which approximately 10,500 were employed in the U.S. and approximately 5,300 were outside of the U.S. Management believes that the Company's employee relations are favorable. During the COVID-19 pandemic, most of our businesses implemented broad work-from-home initiatives. Many businesses have retained work-from-home flexibility for their employees and have implemented hybrid work-from-home and in-office arrangements.

Outside the U.S., we have some employees, particularly in Europe, that are represented by an employee representative organization, such as a union, works council or employee association.

Roper has identified and implemented other human capital priorities, including providing competitive wages and benefits, and promoting a diverse and inclusive work environment. The Company is committed to increasing diversity and fostering an inclusive work environment that supports our large global workforce and helps us innovate for our customers. We continue to focus on building a pipeline for talent to create more opportunities for workplace diversity and to support greater representation within the Company.

Available Information

All reports we file electronically with the SEC, including our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and our annual proxy statements, as well as any amendments to those reports, are accessible at no cost on our website at www.ropertech.com as soon as reasonably practicable after we electronically file such material with, or furnish it to, the SEC. These filings are also accessible on the SEC’s website at www.sec.gov. Our Corporate Governance Guidelines; the charters of our Audit Committee, Compensation Committee, and Nominating and Governance Committee; and our Business Code of Ethics and Standards of Conduct are also available on our website. Any amendment to the Business Code of Ethics and Standards of Conduct and any waiver applicable to our directors, executive officers or senior financial officers will be posted on our website within the time period required by the SEC and the New York Stock Exchange (the “NYSE”). The information posted on our website is not incorporated into this Annual Report or any other filing made by Roper with the SEC.

ITEM 1A. RISK FACTORS

Risks Related to Our Business Operations

Our growth strategy includes acquisitions. We may not be able to identify suitable acquisition candidates, complete acquisitions or integrate acquisitions successfully.

Our future growth is likely to depend to some degree on our ability to acquire and successfully integrate new businesses. We intend to seek additional acquisition opportunities, both to expand into new markets and to enhance our position in existing markets. There are no assurances, however, that we will be able to successfully identify suitable candidates, negotiate appropriate terms, obtain financing on acceptable terms, complete proposed acquisitions, successfully integrate acquired businesses or expand into new markets. Once acquired, operations may not achieve anticipated levels of revenues, profitability or cash flows.

Acquisitions involve risks, including difficulties in the integration of the operations, technologies, services and products of the acquired companies and the diversion of management’s attention from other business concerns. Although our management will endeavor to evaluate the risks inherent in any particular transaction, including but not limited to cyber risks, there are no assurances that we will properly ascertain all such risks. Acquisitions may involve significant cash expenditures, debt

incurrences, equity issuances and expenses. Difficulties encountered with acquisitions may have a material adverse effect on our business, financial condition and results of operations.

Our technology is important to our success and our failure to protect this technology could put us at a competitive disadvantage.

Many of our products and services rely on proprietary technology; therefore we believe that the development and protection of intellectual property rights through patents, copyrights, trade secrets, trademarks, confidentiality agreements and other contractual provisions are important to the future success of our business. Despite our efforts to protect proprietary rights, unauthorized parties or competitors may copy or otherwise obtain and use our products or technology. Actions to enforce these rights may result in substantial costs and diversion of resources, and we make no assurances that any such actions will be successful.

Unfavorable changes in foreign exchange rates may harm our business.

Several of our operating companies have transactions and balances denominated in currencies other than the U.S. dollar. Most of these transactions and balances are denominated in euros, Canadian dollars, or British pounds. Sales by our operating companies whose functional currency is not the U.S. dollar represented 11% and 12% of our total net revenues for the years ended December 31, 2022 and 2021, respectively. Unfavorable changes in exchange rates between the U.S. dollar and those currencies could significantly reduce our reported revenues and earnings.

We rely on information and technology, including third-party cloud computing platforms, for many of our business operations which could fail and cause disruption to our business operations.

Our business operations are dependent upon information technology networks and systems to securely transmit, process and store electronic information and to communicate among our locations around the world and with clients and suppliers. A shutdown of, or inability to access, one or more of our facilities, a power outage or a failure of one or more of our information technology, telecommunications or other systems could significantly impair our ability to perform such functions on a timely basis. Our compliance, cyber and data privacy programs, cybersecurity technology and risk management cannot eliminate all system risk. Cyberattacks, configuration or human error and/or other external hazards could result in the misappropriation of assets or sensitive information, corruption of data or operational disruption.

We increasingly rely on third-party data centers and cloud platforms, such as Amazon Web Services, Google Cloud Platform, and Microsoft Azure to host enterprise and customer systems. Our ability to monitor such third parties’ security measures and the full impact of the systemic risk is limited. If any cloud platform that we use is unavailable to us for any reason, our customers may experience service interruptions, which could significantly impact our operations, reputation, business, and financial results. Failure of our systems or those of our third-party service providers, may result in interruptions in our service and loss of data or processing capabilities, all of which may cause a loss in customers, refunds of product fees, material harm to our reputation and operating results.

Global cybersecurity threats are rapidly evolving and becoming increasingly more sophisticated and attacks to networks, systems and endpoints can range from uncoordinated individual attempts to sophisticated and targeted measures known as advanced persistent threats, directed at the Company, its businesses, its customers and/or its third-party service providers, including, but not limited to, cloud providers and providers of network management services. These may include such things as unauthorized access, phishing attacks, denial of service, introduction of malware or ransomware and other disruptive problems caused by threat actors. While we have experienced, and expect to continue to experience, these types of threats and incidents, none of them to date have been material to the Company.

We seek to deploy measures to protect, detect, respond and recover from cyber threats, including identity and access controls, data protection, vulnerability management, incident response, secure product development, continuous monitoring of our networks, endpoints and systems, and maintenance of resilient backup and recovery capabilities. Our customers are increasingly requiring cybersecurity protections and mandating cybersecurity standards in our products and services, and we may incur additional costs to comply with such demands. Despite these efforts, we can make no assurance that we will be able to mitigate, detect, prevent, timely and adequately respond, or fully recover from the negative effects of cyberattacks or other security compromises, and such cybersecurity incidents, depending on their nature and scope, could potentially result in the misappropriation, destruction, corruption or unavailability of critical data and confidential or proprietary information (our own or that of third parties) and the disruption of business operations. The potential consequences of a material cybersecurity incident include financial loss, reputational damage, damage to our IT systems, data loss, litigation with third parties, theft of intellectual property, fines, diminution in the value of our investment in research and development, and increased cybersecurity

protection and remediation costs due to the increasing sophistication and proliferation of threats, which in turn could adversely affect our competitiveness and results of operations. Any imposition of liability, particularly liability that is not covered by insurance or is in excess of insurance coverage, could materially harm our operating results and financial condition.

Product liability, insurance risks and increased insurance costs could harm our operating results.

Our business exposes us to product liability risks in the design, manufacture and distribution of our products. We currently have product liability insurance; however, we may not be able to maintain our insurance at a reasonable cost or in sufficient amounts to adequately protect us against losses. We also maintain other insurance policies, including directors’ and officers’ liability insurance and cyber insurance. We believe we have adequately accrued estimated losses, principally related to deductible amounts under our insurance policies, with respect to all product liability and other claims, based upon our past experience and available facts. However, a successful product liability or other claim or series of claims brought against us could have a material adverse effect on our business, financial condition and results of operations. In addition, a significant increase in our insurance costs or the imposition of a liability that is not covered by insurance or is in excess of insurance coverage, could have an adverse impact on our operating results.

Our operating results could be adversely affected by a reduction of business with our large customers.

In some of our businesses, we derive a significant amount of revenue from large customers. The loss or reduction of any significant contracts with any of these customers could reduce our revenues and cash flows. Additionally, many of our customers are government entities. In many situations, government entities can unilaterally terminate or modify our existing contracts without cause and without penalty to the government agency.

We face intense competition. If we do not compete effectively, our business may suffer.

We face intense competition from numerous competitors in our various businesses. Our products compete primarily on the basis of product quality, performance, innovation, technology, price, applications expertise, system and service flexibility, distribution channel access and established customer service capabilities. We may not be able to compete effectively on all of these fronts or with all of our competitors. Moreover, competition may require us to adjust prices to stay competitive. In addition, new competitors may emerge, and product lines may be threatened by new technologies or market trends that reduce the value of these product lines. To remain competitive, we must develop new products, respond to new technologies and enhance our existing products in a timely manner.

Our indebtedness may affect our business and may restrict our operating flexibility.

As of December 31, 2022, we had $6,661.7 in total consolidated indebtedness. In addition, we had approximately $3,482 undrawn availability under our senior unsecured credit facility. Subject to restrictions contained in our credit facility, we may incur additional indebtedness in the future, including indebtedness incurred to finance acquisitions.

Our level of indebtedness and the debt servicing costs associated with that indebtedness could have important effects on our operations and business strategy. For example, our indebtedness could:

•limit our ability to borrow additional funds;

•limit our ability to complete future acquisitions;

•limit our ability to pay dividends;

•limit our ability to make capital expenditures;

•place us at a competitive disadvantage relative to our competitors, some of which have lower debt service obligations and greater financial resources; and

•increase our vulnerability to general adverse economic and industry conditions.

Our ability to make scheduled principal payments of, to pay interest on, or to refinance our indebtedness and to satisfy our other debt obligations will depend upon our future operating performance, which may be affected by factors beyond our control. In addition, there can be no assurance that future borrowings or equity financing will be available to us on favorable terms for the payment or refinancing of our indebtedness. If we are unable to service our indebtedness, our business, financial condition and results of operations would be materially adversely affected.

Our credit facility contains covenants requiring us to achieve certain financial and operating results and maintain compliance with specified financial ratios. Our ability to meet the financial covenants or requirements in our credit facility may be affected by events beyond our control, and we may not be able to satisfy such covenants and requirements. A breach of these covenants

or our inability to comply with the financial ratios, tests or other restrictions contained in our facility could result in an event of default under this facility. Upon the occurrence of an event of default under our credit facility, and the expiration of any grace periods, the lenders could elect to declare all amounts outstanding under the facility, together with accrued interest, to be immediately due and payable. If this were to occur, our assets may not be sufficient to fully repay the amounts due under this facility or our other indebtedness.

Our goodwill and intangible assets are a significant amount of our total assets, and any write-off of our intangible assets would negatively affect our results of operations.

Our total assets reflect substantial intangible assets, primarily goodwill. At December 31, 2022, goodwill totaled $15,946.1 compared to $16,037.8 of stockholders’ equity, and represented 59% of our total assets of $26,980.8. The goodwill results from our acquisitions, representing the excess purchase price over the fair value of the net identifiable assets acquired. We assess at least annually whether there has been an impairment in the value of our goodwill and indefinite lived intangible assets. If future operating performance at one or more of our business units were to fall significantly below current levels, if competing or alternative technologies emerge, if interest rates rise or if business valuations decline, we could incur a non-cash charge to operating income. Any determination requiring the write-off of a significant portion of goodwill or unamortized intangible assets would negatively affect our results of operations, the effect of which could be material.

We depend on our ability to develop new products and software, and any failure to develop or market new products and software could adversely affect our business.

The future success of our business will depend, in part, on our ability to design and manufacture new competitive products, including software, and to enhance existing products and software offerings. This product development may require substantial internal investment. There can be no assurance that unforeseen problems will not occur with respect to the development, performance or market acceptance of new technologies, products, or software or that we will otherwise be able to successfully develop and market new products and software. Failure of our products or software offerings to gain market acceptance or our failure to successfully develop and market new products and software could reduce our margins, which would have an adverse effect on our business, financial condition and results of operations.

Changes in the supply of, or price for, raw materials, parts and components used in our products or for third-party services used in the delivery of our SaaS solutions could affect our business.

The availability and prices of raw materials, parts and components are subject to curtailment or change due to, among other things, suppliers’ allocations to other purchasers, interruptions in production by suppliers, supply chain delays and disruptions, changes in exchange rates and prevailing price levels. For example, we expect to continue to be impacted by supply chain challenges, including increased material costs, component shortages and transportation disruptions and delays, all of which could escalate in the future. In addition, some of our products are provided by sole source suppliers and our SaaS offerings are increasingly reliant on a limited number of third-party cloud computing platforms. Any change in the supply of, or price for, these parts and components, as well as any increases in commodity prices or the price and availability of third-party cloud computing platforms could affect our business, financial condition and results of operations.

Our operating results may be adversely impacted by the performance of Indicor, in which we own a minority interest.

In 2022, we divested a 51% majority equity stake of our industrial businesses to Clayton, Dubilier & Rice, LLC (“CD&R”) and retained an initial 49% minority equity interest in the new parent entity, Indicor. Although we have certain limited consent, board representation and other governance rights under existing contractual arrangements, we are a minority owner of Indicor and do not control its management, its policies or the operation of its business, and have no further funding requirements associated with our investment. As a result, our ability to realize the ultimate anticipated benefits of the transaction depend upon operation and management of Indicor by CD&R and the Indicor management team. In addition, Indicor is an industrial business that is subject to risks that are different than the risks associated with our existing businesses. Many of these risks are outside CD&R’s or Indicor’s control and could materially impact Indicor’s business, financial condition and results of operations. Moreover, CD&R may have economic or other business interests that are inconsistent with ours, and we may be unable to prevent strategic decisions that may adversely affect the value of our investment in Indicor. We have applied the fair value option to value our equity investment in Indicor. The assessment of fair value requires significant judgments to be made. Although we believe that our judgments and assumptions are reasonable, changes in estimates or the application of alternative assumptions could produce significantly different results, as a result we could incur non-cash charges within non-operating income and a corresponding reduction in fair value.

Divestitures or other dispositions could negatively impact our business.

Divestitures pose risks and challenges that could negatively impact our business. For example, when we decide to sell or otherwise dispose of a business or assets, we may be unable to do so on satisfactory terms within our anticipated timeframe or at all, and even after reaching a definitive agreement to sell or dispose a business the sale is typically subject to satisfaction of pre-closing conditions which may not become satisfied. The consummation of any divestiture can be difficult, time-consuming and costly, and we may not be able to successfully complete identified divestitures. They may also cause diversion of management time and focus away from operating our business. In addition, divestitures or other dispositions may have other adverse financial and accounting impacts, and disputes may arise with buyers or with partners in businesses in which we own a minority interest that could be difficult or costly to resolve.

Risks Related to Government Regulations

Regulation of privacy and data security may adversely affect sales of our products and services and result in increased compliance costs.

There has been, and likely will continue to be, increased regulation with respect to the collection, use and handling of an individual’s personal and financial information. Regulatory authorities around the world have passed or are considering legislative and regulatory proposals concerning data protection, privacy and data security. In the United States, Virginia, Colorado, Connecticut, and Utah have passed new comprehensive privacy legislation, and joined California (which further enhanced its existing privacy laws) in directly regulating the collection, use and sharing of personal information. In addition, there has been an increased focus on industry-specific privacy laws, including in the financial, healthcare, and educational sectors. These statutes and regulations create civil penalties for violations, and in the case of California, creates a private right of action for data breaches, that increases the risk of data breach litigation. Absent a pre-emptive Federal privacy law, as more states pass privacy legislation, there is a strong possibility that we will be required to comply with a patchwork of inconsistent privacy regulations.

Globally, personal information collected within the European Union and United Kingdom remains subject to the 2018 General Data Protection Regulation (GDPR), which is a UK and European Union-wide legal framework that governs data collection, use, and sharing of an individual’s personal data and creates a range of consumer privacy rights. GDPR provides significant penalties for non-compliance (up to 4% of global revenue) and EU data protection authorities have already issued significant fines.

The interpretation and application of consumer and data protection laws and industry standards in the United States, Europe, China and elsewhere can be uncertain and currently is in flux. Cloud-based solutions may be subject to further regulation, including data localization requirements and other restrictions limiting the international transfer of data. The operational and cost impact of these cannot be fully known at this time. In addition to the possibility of fines, application of these existing laws in a manner inconsistent with our data and privacy practices require that we change our data and privacy practices, which could have an adverse effect on our business and results of operations. Complying with these various laws could cause us to incur substantial costs or require us to change our business practices in a manner adverse to our business. Also, any new law or regulation imposing greater fees or taxes or restriction on the collection, use or transfer of information or data internationally or over the Internet, could result in a decline in the use of our products and services and adversely affect sales and our results of operations. Finally, as we increasingly become a provider of technology solutions, our customers and regulators will expect that we can demonstrate compliance with current data privacy and security regulations as well as new industry-developed standards, and our inability to do so may adversely impact sales of our solutions and services to certain customers. This is particularly true for customers in highly-regulated industries, such as the healthcare industry and government contractors, and could result in regulatory actions, fines, legal proceedings and negatively impact our brand, reputation and our business.

Expectations relating to environmental, social and governance considerations expose the Company to potential liabilities, increased costs, reputational harm and other adverse effects on the Company’s business.

Many governments, regulators, investors, employees, customers and other stakeholders are increasingly focused on environmental, social and governance considerations relating to businesses, including climate change and greenhouse gas emissions, human capital and diversity, equity and inclusion. The Company makes statements about its environmental, social and governance goals and initiatives through information provided on its website, press statements and other communications, including through its ESG Report. Responding to these environmental, social and governance considerations and implementation of these goals and initiatives involves risks and uncertainties, including those described under “Forward-Looking Statements,” requires investments and are impacted by factors that may be outside the Company’s control. In addition,

some stakeholders may disagree with the Company’s goals and initiatives and the focus of stakeholders may change and evolve over time. Stakeholders also may have very different views on where environmental, social and governance focus should be placed, including differing views of regulators in various jurisdictions in which we operate. Any failure, or perceived failure, by the Company to achieve its goals, further its initiatives, adhere to its public statements, comply with federal, state or international environmental, social and governance laws and regulations, or meet evolving and varied stakeholder expectations and standards could result in legal and regulatory proceedings against the Company and materially adversely affect the Company’s business, reputation, results of operations, financial condition and stock price.

Risks Related to Economic and Political Conditions

Economic, political and other risks associated with our international operations could adversely affect our business.

For the year ended December 31, 2022, 14% of our net revenues and 8% of our long-lived assets, excluding goodwill and intangibles, were attributable to operations outside the U.S. We expect our international operations to contribute materially to our business for the foreseeable future. Our international operations are subject to varying degrees of risk inherent in doing business outside the U.S. including, without limitation, the following:

•adverse changes in a specific country’s or region’s political or economic conditions, particularly in emerging markets;

•oil price volatility;

•trade protection measures, tariffs, and import or export requirements;

•subsidies or increased access to capital for firms that are currently, or may emerge as, competitors in countries in which we have operations;

•partial or total expropriation;

•potentially negative consequences from changes in tax laws;

•difficulty in staffing and managing widespread operations;

•differing labor regulations;

•differing protection of intellectual property;

•differing and unexpected changes in regulatory requirements, including any measures implemented to address the impacts of climate change; and

•potentially negative consequences from the United Kingdom’s exit from the European Union.

Any business disruptions due to political instability, armed hostilities, incidents of terrorism, incidents of directed cyber-attacks, public health crisis, extreme weather events or other natural disasters could adversely impact our financial performance.

If terrorist activity, armed conflict, directed cyber-attacks, political instability, public health crisis, such as an epidemic or pandemic, or extreme weather events or other natural disasters occur in the U.S. or other locations, such events may negatively impact our operations, cause general economic conditions to deteriorate or cause demand for our products to decline. A prolonged economic slowdown or recession could reduce the demand for our products, and therefore, negatively affect our future sales and profits. Any of these events could have a significant impact on our business, financial condition or results of operations.

Our business, financial condition and results of operations could be adversely affected by disruptions in the global economy caused by the ongoing conflict between Russia and Ukraine.

The global economy has been negatively impacted by the military conflict between Russia and Ukraine. Furthermore, governments in the United States, United Kingdom and European Union have each imposed export controls on certain products and financial and economic sanctions on certain industry sectors and parties in Russia. We have historically had limited operations in Russia and a limited number of suppliers in Ukraine. Nevertheless, the Russia-Ukraine military conflict could have a negative impact on the global economy. Further escalation of geopolitical tensions related to the military conflict, including increased trade barriers or restrictions on global trade, could result in, among other things, cyberattacks, supply disruptions, lower consumer demand, and changes to foreign exchange rates and financial markets, any of which may adversely affect our business and supply chain.

General Risk Factors

Impacts related to the COVID-19 pandemic could have an adverse effect on our business, financial condition, results of operations and cash flows.

We continue to closely monitor the impact of the COVID-19 global pandemic on our business, including how it has and will impact our customers, employees, suppliers, vendors and business partners. The COVID-19 global pandemic has created significant volatility, uncertainty and economic disruption, which may continue to affect our business operations and may materially and adversely affect our results of operations, cash flows and financial position.

The COVID-19 global pandemic has caused certain disruptions to our business and operations and could cause material disruptions to our business and operations in the future as a result of, among other things, quarantines, worker absenteeism as a result of illness or other factors, social distancing measures and other travel, health-related, business or other restrictions. The effects of the pandemic have created and exacerbated challenges with the attraction and retention of talent.

The COVID-19 global pandemic has and may continue to adversely impact, our suppliers and customers. As a result of the effects of the COVID-19 global pandemic our ability to obtain products or services from certain suppliers and to operate at certain locations have been and may continue to be impacted. As a result, our business, financial condition and results of operations have been adversely impacted and could be materially adversely affected if the COVID-19 global pandemic continues or there are resurgences of COVID-19 and its variants.

The extent to which the coronavirus continues to impact our business, results of operations and financial condition will depend on future developments, which are highly uncertain and are difficult to predict, including, but not limited to, ongoing or additional outbreaks of the virus or its variants in the jurisdictions in which we operate, the duration and spread of any such outbreaks, its severity, and the actions to contain the virus and its variants whether through the distribution and administration of available vaccines, vaccine mandates or otherwise could have a material impact on our results of operations and heighten many of our known risks described below in this “Risk Factors” section.

The potential insolvency or financial distress of third parties could adversely impact our business and results of operations.

We are exposed to the risk that third parties to various arrangements who owe us money or goods and services, or who purchase goods and services from us, will not be able to perform their obligations or continue to place orders due to insolvency or financial distress. In addition, the global COVID-19 pandemic has created heightened risk that third parties may be unable to perform their obligations or suffer financial distress due to the global economic impact of the pandemic and the regulatory measures that have been enacted by governments to contain the spread of the virus, however, we are unable predict the impact that COVID-19 will have on any of our customers, suppliers, vendors, and other business partners, and each of their financial conditions or their ability to perform their obligations. If third parties fail to perform their obligations under arrangements with us, we may be forced to replace the underlying commitment at current or above market prices or on other terms that are less favorable to us. In such events, we may incur losses, or our results of operations, financial condition or liquidity could otherwise be adversely affected.

Changes to our executive leadership team and any future loss of members of such team, and the resulting management transitions, could harm our operating results.

We have experienced significant changes to our executive leadership team in the past and may do so in the future. Leadership transitions and changes can be inherently difficult to manage and may cause uncertainty or disruption to our business or may increase the likelihood of turnover in key leadership positions. If we cannot effectively manage leadership transitions and changes, it could make it more difficult to successfully operate our business.

Legal proceedings in which we are, or may be, a party may adversely affect us.

We are currently, and may in the future, become subject to legal proceedings and commercial or contractual disputes. These are typically claims that arise in the normal course of business including, without limitation, commercial or contractual disputes with our suppliers or customers, intellectual property matters, third party liability, including product liability claims, and employment claims. We are and may in the future become subject to litigation regarding data or privacy incidents, as more fully described above in “We rely on information and technology for many of our business operations which could fail and cause disruption to our business operations”.

A downgrade in the ratings of our debt could restrict our ability to access the debt capital markets and increase our interest costs.

Unfavorable changes in the ratings that rating agencies assign to our debt may ultimately negatively impact our access to the debt capital markets and increase the costs we incur to borrow funds. Additionally, our credit agreement includes an increase in interest rates if the ratings for our debt are downgraded. Further, an increase in the level of our indebtedness may increase our vulnerability to adverse general economic and industry conditions and may affect our ability to obtain additional financing.

ITEM 1B. UNRESOLVED STAFF COMMENTS

None

ITEM 2. PROPERTIES

Our corporate offices, consisting of 29,000 square feet of leased space, are located at 6901 Professional Parkway, Sarasota, Florida. As of December 31, 2022, we owned approximately 0.3 million square feet, and leased approximately 2.8 million square feet. Of the total 3.1 million square feet, 76% is concentrated in the United States. We consider our facilities to be in good operating condition and adequate for their present use and believe we have sufficient capacity to meet our anticipated operating requirements.

ITEM 3. LEGAL PROCEEDINGS

Information pertaining to legal proceedings can be found in Note 13 to the Consolidated Financial Statements included in this Annual Report, and is incorporated by reference herein.

ITEM 4. MINE SAFETY DISCLOSURES

Not Applicable

EXECUTIVE OFFICERS OF THE REGISTRANT

Pursuant to General Instruction G(3) of Form 10-K, the following list of executive officers of the Company as of February 27, 2023 is included as an unnumbered Item in Part I of this report in lieu of being included in the Company’s Proxy Statement relating to the 2023 Annual Meeting of Shareholders.

L. Neil Hunn, 50, has served as President and Chief Executive Officer since August 2018. He previously served as Executive Vice President and Chief Operating Officer from 2017 to 2018. Mr. Hunn also served as Group Vice President of Roper’s medical segment from 2011 to 2018 and helped drive significant growth in the Company’s medical technology and application software businesses. In addition to his operating responsibilities at Roper, Mr. Hunn led the execution of the majority of the company’s capital deployment since joining Roper. Prior to joining Roper, Mr. Hunn served 10 years as Executive Vice President and Chief Financial Officer at MedAssets, an Atlanta-based SaaS company, and as President of its revenue cycle technology businesses. He successfully led MedAssets’ initial public offering and the execution of several M&A transactions. Mr. Hunn also held roles at CMGI, an incubator of Internet businesses, and Parthenon Group, a strategy consulting firm.

Jason P. Conley, 47, has served as Executive Vice President and Chief Financial Officer since February 2023. Prior thereto he served as Vice President and Chief Accounting Officer from 2021 to February 2023 and as Vice President and Controller from 2017 to 2021. He previously served as the Chief Financial Officer at Managed Healthcare Associates, a Roper subsidiary, from 2013 to 2017. He also led the financial planning and investor relations activities for Roper from 2006 to 2013. Before Roper, Mr. Conley served in various finance and accounting leadership roles at Honeywell International and Deloitte.

John K. Stipancich, 54, has served as Executive Vice President, General Counsel and Corporate Secretary since 2018 and as Vice President, General Counsel and Corporate Secretary from 2016 to 2018. Prior to joining Roper, Mr. Stipancich was with Newell Brands, Inc., a consumer products company, from 2004 to 2016. At Newell Brands he served as Executive Vice President and Chief Financial Officer from 2015 to 2016. Prior thereto, he served in a number of leadership roles at Newell Brands including General Counsel and Corporate Secretary, and Executive Leader of its operations in Europe, the Middle East and Africa. Prior to his twelve years at Newell Brands, Mr. Stipancich served as Executive Vice President, General Counsel and Corporate Secretary for Evenflo Company and Assistant General Counsel for Borden, both KKR portfolio companies at the time. He started his legal career in the Cleveland office of the international law firm of Squire Patton Boggs.

PART II

ITEM 5. MARKET FOR REGISTRANT’S COMMON EQUITY RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

Our common stock trades on the NYSE under the symbol “ROP”. Based on information available to us and our transfer agent, there were approximately 202 record holders of our common stock as of February 17, 2023.

Dividends – We have declared a cash dividend in each quarter since our February 1992 initial public offering and we have annually increased our dividend rate since our initial public offering. In November 2022, our Board of Directors increased the quarterly dividend paid January 23, 2023 to $0.6825 per share from $0.62 per share, an increase of 10%. This is the thirtieth consecutive year in which the Company has increased its dividend. The timing, declaration and payment of future dividends will be at the sole discretion of our Board of Directors and will depend upon our profitability, cash flows, financial condition, capital needs, future prospects and other factors deemed relevant by our Board of Directors.

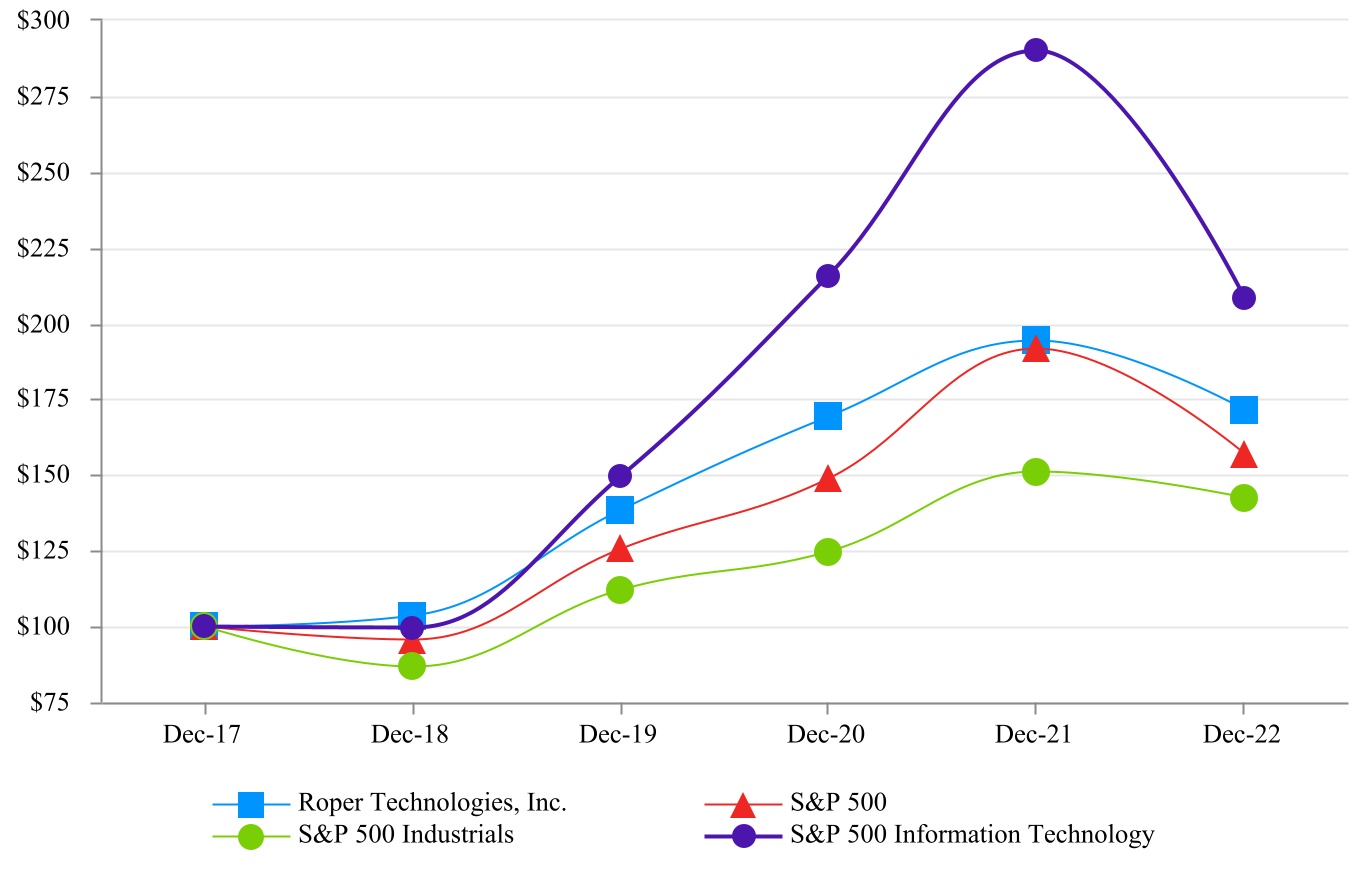

Performance Graph - This performance graph shall not be deemed “filed” for purposes of Section 18 of the Securities Exchange Act of 1934, as amended (the “Exchange Act”) or otherwise subject to the liabilities under that Section and shall not be deemed to be incorporated by reference into any of our filings under the Securities Act of 1933, as amended, or under the Exchange Act.

Roper has historically compared the cumulative total return on its common stock with that of the Standard & Poor’s 500 Stock Index (the “S&P 500”) and the Standard and Poor’s 500 Industrials Index (the “S&P 500 Industrials”). As a result of the divestiture activity in 2022 and 2021, the Company will use the S&P 500 Information Technology Index (the “S&P 500 IT”) in place of the S&P 500 Industrials on a go-forward basis to better reflect more relevant comparisons of our software and technology focused portfolio. The performance graph below presents the indices used in the prior year and the newly selected index.

The following graph compares, for the five year period ended December 31, 2022, the cumulative total stockholder return for our common stock, the S&P 500, the S&P 500 Industrials, and the S&P 500 IT indices. Measurement points are the last trading day of each of our fiscal years ended December 31, 2017, 2018, 2019, 2020, 2021 and 2022. The graph assumes that $100.00 was invested on December 31, 2017 in our common stock, the S&P 500, the S&P 500 Industrials, and the S&P 500 IT and assumes reinvestment of any dividends. The stock price performance on the following graph is not necessarily indicative of future stock price performance.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | 12/31/2017 | | 12/31/2018 | | 12/31/2019 | | 12/31/2020 | | 12/31/2021 | | 12/31/2022 |

| Roper Technologies, Inc. | $ | 100.00 | | | $ | 103.52 | | | $ | 138.36 | | | $ | 169.34 | | | $ | 194.20 | | | $ | 171.59 | |

| S&P 500 | 100.00 | | | 95.62 | | | 125.72 | | | 148.85 | | | 191.58 | | | 156.88 | |

| S&P 500 Industrials | 100.00 | | | 86.71 | | | 112.17 | | | 124.59 | | | 150.89 | | | 142.63 | |

| S&P 500 IT | 100.00 | | | 99.71 | | | 149.86 | | | 215.63 | | | 290.08 | | | 208.30 | |

The information set forth in Item 12 under the heading “Securities Authorized for Issuance under Equity Compensation Plans” is incorporated herein by reference.

ITEM 6. [RESERVED]

ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

All currency amounts are in millions unless specified

Overview

Roper Technologies is a diversified technology company. Roper has a proven, long-term, successful track record of compounding cash flow and shareholder value. We operate market leading businesses that design and develop vertical software and technology enabled products for a variety of defensible niche markets.

We pursue consistent and sustainable growth in revenue, earnings and cash flow by enabling continuous improvement in the operating performance of our existing businesses and by acquiring other businesses that offer high value-added software, services, technology-enabled products and solutions that we believe are capable of achieving growth and maintaining high margins.

Discontinued Operations

On November 22, 2022, the Company completed the divestiture of a majority 51% equity stake in its industrial businesses, including its entire historical Process Technologies reportable segment and the industrial businesses within its historical Measurement & Analytical Solutions reportable segment, to Clayton, Dubilier & Rice, LLC. The businesses included in this transaction were Alpha, AMOT, CCC, Cornell, Dynisco, FTI, Hansen, Hardy, Logitech, Metrix, PAC, Roper Pump, Struers, Technolog, Uson, and Viatran (collectively “Indicor”). Following the sale of the majority stake, the Company retained an initial 49% minority equity interest in the new standalone parent company, Indicor, LLC. This transaction is referred to herein as the “Indicor Transaction.”

During 2021, Roper entered into definitive agreements to divest our TransCore, Zetec and CIVCO Radiotherapy businesses (“2021 Divestitures”). As of March 31, 2022, Roper had completed the 2021 Divestitures.

The aggregate of the 2021 Divestitures and the Indicor Transaction have greatly reduced the cyclicality and asset intensity of the Company. In addition, the Company has an increased mix of recurring revenue and a higher margin profile. The financial results for Indicor and the 2021 Divestitures are reported as discontinued operations for all periods presented. Unless otherwise noted, discussion within Management’s Discussion and Analysis of Financial Condition and Results of Operations relate to continuing operations. Information regarding discontinued operations is included in Note 3 of the Notes to Consolidated Financial Statements.

Update to Segment Reporting Structure

During the second quarter of 2022, we updated our reportable segment structure following the announcement of the Indicor Transaction. The Company’s new reporting segment structure is classified based on business model and delivery of performance obligations. The three updated reportable segments (and businesses within each; including changes due to acquisitions since the realignment) are as follows:

–Application Software - Aderant, CBORD/Horizon, CliniSys, Data Innovations, Deltek, Frontline Education, IntelliTrans, PowerPlan, Strata, Vertafore

–Network Software - ConstructConnect, DAT, Foundry, iPipeline, iTradeNetwork, Loadlink, MHA, SHP, SoftWriters

–Technology Enabled Products - CIVCO Medical Solutions, FMI, Inovonics, IPA, Neptune, Northern Digital, rf IDEAS, Verathon

Following the Indicor Transaction and the realignment of our reportable segments, the day-to-day operations of our businesses, our organizational structure, and our strategy remain unchanged. All prior periods have been recast to reflect the changes noted above. Financial information about our reportable segments is presented in Note 14 of the Notes to Consolidated Financial Statements included in this Annual Report.

Application of Critical Accounting Policies

Our Consolidated Financial Statements are prepared in conformity with generally accepted accounting principles in the United States (“GAAP”). A discussion of our significant accounting policies can also be found in the Notes to Consolidated Financial Statements for the year ended December 31, 2022 included in this Annual Report.

GAAP offers acceptable alternative methods for accounting for certain issues affecting our financial results, such as determining inventory cost, depreciating long-lived assets and recognizing revenue. We have not changed the application of acceptable accounting methods or the significant estimates affecting the application of these principles in the last three years in a manner that had a material effect on our Consolidated Financial Statements.

The preparation of financial statements in accordance with GAAP requires the use of estimates, assumptions, judgments and interpretations that can affect the reported amounts of assets, liabilities, revenues and expenses, the disclosure of contingent assets and liabilities and other supplemental disclosures.

The development of accounting estimates is the responsibility of our management. Our management discusses those areas that require significant judgments with the Audit Committee of our Board of Directors. The Audit Committee has reviewed all financial disclosures in our annual filings with the SEC. Although we believe the positions we have taken with regard to uncertainties are reasonable, others might reach different conclusions and our positions can change over time as more information becomes available. If an accounting estimate changes, its effects are accounted for prospectively or through a cumulative catch up adjustment.

Our most significant accounting uncertainties are encountered in the areas of income taxes, valuation of other intangible assets, goodwill and indefinite-lived impairment analyses, and valuation of our initial 49% equity interest in Indicor. Estimates are considered to be significant if they meet both of the following criteria: (1) the estimate requires assumptions about matters that are uncertain at the time the estimate is made, and (2) changes in the estimate are reasonably likely to have a material financial impact from period-to-period.

Income taxes can be affected by estimates of whether and within which jurisdictions future earnings will occur and if, how and when cash is repatriated to the U.S., combined with other aspects of an overall income tax strategy. Additionally, taxing jurisdictions could retroactively disagree with our tax treatment of certain items, and some historical transactions have income tax effects going forward. Accounting rules require these future effects to be evaluated using current laws, rules and regulations, each of which can change at any time and in an unpredictable manner. If there is a material change in the actual effective tax rates, the time period within which the underlying temporary differences become taxable or deductible, or if the tax law changes are unfavorable there could be a resulting increase to income tax expense and the effective tax rate.

During 2022, our effective income tax rate was 23.1%, as compared to the 2021 rate of 22.0%. The rate was unfavorably impacted by the recognition of a net tax expense associated with an internal restructuring plan associated with the Indicor Transaction. We expect the effective tax rate for 2023 to be approximately 21% to 22%.