UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended October 31, 2008

Commission file number 0-20842

PLATO Learning, Inc.

(Exact name of Registrant as specified in its charter)

| Delaware | 36-3660532 |

| (State or other jurisdiction of incorporation or organization) | (IRS Employer Identification Number) |

| 10801 Nesbitt Avenue South, Bloomington, MN | 55437 |

| (Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, including area code:

(952) 832-1000

| Securities registered pursuant to Section 12(b) of the Act: | Name of exchange on which registered: |

| Common Stock, Par Value $.01 | NASDAQ Global Market |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes £ No T

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes £ No T

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months, and (2) has been subject to such filing requirements for the past 90 days. Yes T No £

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. £

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one)

Large Accelerated Filer £ Accelerated Filer T Non-Accelerated Filer £ Smaller Reporting Company £

(Do not check if smaller reporting company)

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Act.) Yes £ No T

The aggregate market value of common stock held by non-affiliates of the Registrant, as of April 30, 2008 (the last business day of the Registrant’s most recently completed second fiscal quarter) was approximately $66,000,000.

The number of shares of the Registrant’s common stock, par value $.01, outstanding as of December 31, 2008 was 24,080,915 shares.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Company’s definitive Proxy Statement for the Company’s Annual Meeting of Stockholders to be held on March 26, 2009 (the “2009 Proxy Statement”) are incorporated by reference in Part III.

PLATO LEARNING, INC.

Form 10-K

Fiscal Year Ended October 31, 2008

TABLE OF CONTENTS

| Page | ||

| PART I | ||

| Item 1. | 1 | |

| Item 1A. | 7 | |

| Item 1B. | 12 | |

| Item 2. | 12 | |

| Item 3. | 12 | |

| Item 4. | 12 | |

| PART II | ||

| Item 5. | 13 | |

| Item 6. | 15 | |

| Item 7. | 16 | |

| Item 7A. | 32 | |

| Item 8. | 33 | |

| Item 9. | 65 | |

| Item 9A. | 65 | |

| Item 9B. | 66 | |

| PART III | ||

| Item 10. | 67 | |

| Item 11. | 68 | |

| Item 12. | 68 | |

| Item 13. | 68 | |

| Item 14. | 68 | |

| PART IV | ||

| Item 15. | 69 | |

| 70 | ||

| 71 | ||

PART I

Forward-Looking Statements

In addition to historical information, this Form 10-K contains forward-looking statements. These forward-looking statements are made in reliance upon the safe harbor provisions of the Private Securities Litigation Reform Act of 1995 (“the Act”). The words “believe,” “expect,” “anticipate,” “intend,” “estimate,” “forecast,” “project,” “should” and similar expressions are intended to identify “forward-looking statements” within the meaning of the Act. Forward-looking statements include, among others, statements about our future performance, the sufficiency of our sources of capital for future needs, and the expected impact of recently issued accounting pronouncements. These forward-looking statements are subject to certain risks and uncertainties that could cause actual results to differ materially from those reflected in the forward-looking statements. Factors that might cause such a difference include, but are not limited to, those discussed in Part I Item 1A of this Form 10-K. Readers are cautioned not to place undue reliance on these forward-looking statements, which reflect management’s opinions only as of the date hereof. We undertake no obligation to revise or publicly release any revision to these forward-looking statements based on circumstances or events, which occur in the future. Readers should carefully review the risk factors described in Part I Item 1A of this report on Form 10-K and in other documents we file from time to time with the Securities and Exchange Commission.

ITEM 1. BUSINESS

Business Description

PLATO Learning, Inc. is a Delaware corporation that was incorporated in 1989 and is headquartered in Bloomington, Minnesota. We are a leading provider of on-line instruction, curriculum management, assessment, and related professional development services to K–12 schools, community colleges and other educational institutions across the country. Our products are used by customers principally to provide alternative instruction to students performing below their grade level in order to help those students return to the classroom, recover course credits, pass high school exit exams or prepare for college and other post-secondary studies. In addition to the value provided to students, our solutions allow school districts to retain state and federal funding tied to student enrollment. Our courseware and assessment products are designed primarily to help educators meet the demands of state and federal student achievement initiatives for intervention, dropout prevention and college readiness. We also offer online and onsite staff professional development services to ensure optimal use of our products and to help schools meet their accountability requirements and school improvement plans.

Our research-based courseware library includes thousands of hours of mastery-based instruction covering discrete learning objectives in the subject areas of reading, writing, language arts, mathematics, science, and social studies. Our web-based assessment and alignment tools ensure that instruction can be personalized to each student’s unique needs and the curriculum has alignment to local, state, and national standards. Using our web-based products, educators are able to identify each student’s instructional needs and prescribe an individual learning program of PLATO Learning courseware, educational web sites, the school’s textbooks and other core and supplemental instructional materials. A variety of reports are available to help educators identify gaps in student understanding and ensure that standard learning objectives are being addressed.

Beginning in late fiscal year 2005, we implemented a strategy to deliver our products and solutions on a subscription basis using a new internet-based learning management platform we call the PLATO Learning EnvironmentTM, or PLETM. The majority of our subscription periods range from one to three years with a dollar value weighted average subscription period of approximately two years in fiscal 2008. As of October 31, 2008, over 1,200 school districts, community colleges and other educational institutions across 50 states subscribed to our instructional solutions delivered on PLETM, and nearly 1.2 million students, teachers and administrators at these institutions were registered to use PLETM.

We operate our principal business in one industry segment, which is the development and marketing of educational software and related services.

Market

Based on recent market data from Simba Information (“Simba”), approximately $9.1 billion is spent annually on print and electronic instructional materials in the U.S. K-12 market. Of that spending, approximately $1.8 billion is spent on electronic instructional materials which Simba classifies into three categories of products: courseware, modular software and videos. Our instructional products fall primarily into the courseware category, which, according to Simba, is the fastest growing market in the K-12 instructional materials market, growing 8.5% in 2007, and projected to grow 9.3% to $928 million in 2008.

Our newest instructional products are delivered on a subscription basis over the internet, via our learning management system, the PLATO Learning EnvironmentTM, or PLETM. Today, 99% of the nation’s K-12 public schools have Internet access, and as a result, schools are increasingly turning to web-based methods of instruction as a supplement to their instructor-led programs due to their flexibility, cost-efficiency, and effectiveness.

Some of our customers have integrated our products into their core classroom instruction, but most use them to provide alternative instructional programs to students who, for various reasons, have not been successful learning in the classroom environment. These remedial programs help students return to the classroom or recover course credits needed to move to the next grade level, pass high school exit exams and graduate. Earning a high-school diploma represents a key milestone in an individual's schooling and social and economic advancement, but according to the National Center for Education Statistics, more than 25% of incoming freshman do not finish high school. Statistics like these raise the awareness of the effectiveness of U.S. public schools and have led to legislative requirements and public demand for increased accountability and improvements in U.S. K-12 schools. These trends have led to increasing demand for solutions like ours and others that address the need to improve school effectiveness and graduation rates. As a result, we believe that technology-based instructional materials have the ability to cost effectively create a personalized and flexible instructional environment, and are generally preferred over print-based materials by today’s students, and will continue to grow faster than the total instructional materials market.

Strategy

Since late 2005, we have been executing a strategy focused on four core strategic initiatives:

| · | Leverage our strong brand and extensive library of curriculum to grow market share in the intervention market. Our traditional strength has been the intervention market - solutions that help students who are one or more grade levels behind and at risk of not being promoted to the next grade or not graduating. Instruction delivered using technology provides an ideal solution for this market need as instructional intervention generally occurs outside the traditional classroom and requires self-paced learning personalized for each student’s unique learning needs. The technology solutions currently sold to this market are characterized by a large number of smaller competitors. We believe that providing new and differentiated solutions on an Internet-based platform such as PLE, combined with our strong brand in this market, uniquely positions us to be a dominant provider of technology-based solutions in the fragmented intervention market. |

| · | Create a core competency in software product development. By the end of fiscal 2006, we completed a restructuring of our software development organization centered on an off-shore development capability and structured software development processes that has greatly lowered development costs and improved product quality and time to market. |

| · | Deliver our instructional solutions on a single, Internet-based delivery platform. Emerging trends over the last several years are driving acknowledgement of the benefits of delivering curriculum into the K–12 market over the Internet. These trends include improving Internet technology, significant investments by school districts in technology infrastructure, the high cost of ownership of multi-vendor, on-site applications, growing use and acceptance of Internet-based resources in the K–12 market, ubiquitous Internet accessibility outside the classroom, and student and teacher demographics with respect to technology expectations and adoption. Targeting these trends, we developed and launched PLE™ in July 2006, an intuitive, web-based Learning Management System that is available to students, teachers and administrators anywhere an Internet connection and browser are available. As of the end of fiscal year 2007, the majority of our instructional content had been refreshed and transitioned to PLE™, and in 2008 we added assessments and personalized learning capabilities that prescribe instructional content based on each individual student’s needs. |

| · | Transition our business model from sales of perpetual licenses, to a subscription-based, on-demand, software-as-a-service (“SaaS”) application. Historically, we operated a traditional software business model in which software products were licensed to customers on a perpetual basis for installation and use on their own technology. This business model had many undesirable characteristics including high product maintenance and support costs, high volatility and low visibility of financial results, and a dependence on large sales at or near quarter-end to achieve financial targets, often resulting in significant price discounting and a short-term business focus. We believe the subscription-based business model provides significant advantages in that it produces significant operating leverage, a predictable recurring revenue stream through subscription renewals, and greater visibility and stability to future operating results. In fiscal year 2008, approximately 85% of our product orders were for subscription-based products, up from approximately 68% in fiscal year 2007. |

Products

Our products consist of a comprehensive portfolio of technology-based instructional content, classroom assessment, and related professional development that we market to K–12 schools, community colleges and other educational institutions. Our products are used by these customers principally to provide alternative instruction to students performing below their grade level in order to help those students return to the classroom, recover course credits, pass high school exit exams or prepare for college and other post-secondary studies.

Instructional Content

Our content library consists of rich, interactive, multimedia instructional content that is highly engaging for both students and teachers. This research-based courseware library includes more than 6,000 hours of mastery-based instruction material covering the primary K-12 subject areas of mathematics, science, reading/language arts, and social studies.

Our content can be applied to multiple student learning profiles (e.g. general education, special education, at-risk) and tailored for students across multiple grade-levels. Content offerings are classified as intervention solutions when applied to students performing below grade-level, as core or supplemental instructional solutions for mainstream students performing at grade level, and as advanced placement offerings for students performing above grade level. We believe our content provides the following differentiating factors:

| · | Interactive, engaging multimedia instruction that is highly differentiated from the static text-biased content provided by many other companies; |

| · | Content that is cross-referenced to academic standards set by states, the federal government, and other standard-setting bodies; |

| · | Assessments that are tied to these standards and generate personalized lesson plans based on an individual student’s test results; |

| · | Content arranged into a series of semester-long pre-configured online courses for grades 7–12 that can be employed both inside and outside of the classroom; |

| · | Fully customizable by schools to fit their unique instructional needs; |

| · | Correlated to all primary textbooks used in K–12 schools. |

Learning Management System

In July 2006, we launched the PLATO Learning Environment™ (PLE), a web-based platform to deliver all of our instructional solutions, providing a unified curriculum management and delivery system that requires only an Internet connection and a browser. In addition to anytime-anywhere delivery of our products, PLE provides the following differentiating factors:

| · | Automated alignments of instructional content to learning standards in all states and the major national standards such as SAT, ACT, GED, and NAEP; |

| · | Access to pre-set teacher materials used to supplement the online curriculum; |

| · | Built-in links to many popular websites containing other K–12 curriculum; |

| · | Functionality allowing school districts to create customized courses tailored to their specific instructional scope and sequence, including the ability for teachers to upload documents they have created for access by students; |

| · | Search functionality that allows users to find resources and content based on standards applicable to their instructional requirements; |

| · | Preparation of assessment tests and generation of recommendations for relevant follow-up content based on results; |

| · | Automated grading and reporting for whole course or supplemental programs. |

Classroom Formative Assessment

Formative assessment involves collecting feedback from learning activities to adapt instruction to a learner’s needs. Our assessment database consists of more than 180,000 test items linked to state, district, and national learning objectives across all subject areas of reading, math, science and social studies. In conjunction with powerful data management tools, our assessment solutions can provide assessment results by student demographic category and facilitate data-driven decision making for school curriculum development, textbook choices and providing personalized learning. PLATO® Test Packs with Prescriptions prescribe individual learning paths to PLATO® content based on student performance, which can then be completed at the student’s own learning pace. As a result, PLATO Test Packs give teachers the flexibility to allow PLE to automatically prescribe assignments or to make manual adjustments before assigning lessons.

Instructional Solutions

We combine our large library of interactive content and assessments with the unique features of PLE to deliver a variety of instructional solutions to educational institutions. In K-12 schools, these solutions primarily address at-risk students who have fallen behind in the classroom, allowing these students to recover credits, move to the next grade level, avoid dropping out of school or prepare for their high school exit exam. In the post-secondary market, our developmental algebra products, sold under the Academic Systems® brand, are primarily intended for students who have completed high school but are not yet ready for college level math courses. We also provide instructional solutions to adult education markets for GED preparation, workforce readiness, and life and career skills.

Services and Product Support

Our professional services offerings ensure that customers receive the consultation, training and services needed to successfully implement our solutions and integrate educational technology into their day-to-day teaching and learning environment. Services are delivered in face-to-face sessions as well as synchronous and asynchronous online delivery methods.

We provide telephone and online product support to our customers. Subscription customers are entitled to support as part of their subscription fees to our online products. Customers who purchased perpetual license products can choose to obtain telephone support by paying an annual software maintenance fee.

Sales and Marketing

Our sales channel consists of direct sales representatives located throughout the U.S. and inside sales representatives operating out of our corporate headquarters in Bloomington, Minnesota. We also utilize distributors and resellers in certain geographic markets.

In the K–12 market we sell to school districts of all sizes, but generally target larger school districts. In the post-secondary market, we target community colleges, four-year universities, adult education centers, and correctional institutions.

Competition

The market for electronic instructional materials is served by hundreds of companies that offer a range of instructional products and services. At one end of the market are companies offering modular software applications or videos that consist of a single element of instructional content or an individual course or application. At the other end are companies like PLATO Learning that provide full course offerings that span multiple grade levels and/or subject areas. These companies are “comprehensive” in terms of being able to package a solution that covers multiple grade levels, subjects, and associated reports and assessments. Between the comprehensive and non-comprehensive categories there are as many variations as there are companies.

We estimate that the five largest companies serving this market – PLATO Learning, Pearson Education, Renaissance Learning, Houghton Mifflin/RiverDeep, and Scholastic – have an estimated combined market share of approximately 40%. PLATO Learning and Pearson Education provide courseware across all K–12 grade levels, while Houghton Mifflin/Riverdeep, Renaissance Learning, and Scholastic limit the breadth of grade levels and/or subject areas their solutions address. In the intervention market we compete against a number of smaller competitors, including Compass Learning, OdysseyWare, Apex Learning, American Education Corporation (A+), and others. Many of these smaller, non-comprehensive companies focus on a geographic segment or district size, rather than the national market. The needs, size, and location of school districts often influence the opportunities for which companies choose to compete.

When competing with any company, we differentiate our solutions by emphasizing the depth of our multimedia rich courseware aligned to standards, the benefits of a single learning management system that delivers all content over the Internet for all grades and core subject areas, the completeness of alignments to state and national standards, and the unique diagnostic and prescriptive capabilities of our products to improve performance on state exams and standards. We also believe that our record of student improvement and product development capabilities differentiate us from the competition. Based on our experience, we believe that these are key factors that buyers use in evaluating competitive offerings.

Product Development

Our product development group develops, enhances, and maintains our courseware, assessment, instructional management software, and delivery system platforms. We utilize both domestic and offshore resources. In fiscal year 2008, approximately 45% of our total product development spending was incurred offshore.

Proprietary Rights

Our courseware is proprietary and we protect it primarily under a combination of the laws of copyrights, trademarks, and trade secrets. We also utilize copyright and trademark protection, license agreements, employment agreements, employment termination agreements, third-party non-disclosure agreements, and other methods to protect our proprietary rights. We regard many of our intellectual property rights as essential to our business and enforce our intellectual property rights when we become aware of any infringements or potential infringements and believe they warrant such action.

Backlog

We consider backlog to be the total of deferred revenue reported on our balance sheet plus unbilled amounts due under non-cancelable subscription agreements. On this basis, backlog was $53.9 million and $49.1 million at October 31, 2008 and 2007, respectively, broken down as follows:

| October 31, | ||||||||

| 2008 | 2007 | |||||||

| Subscription | $ | 41,694 | $ | 32,938 | ||||

| License fees | 467 | 622 | ||||||

| Services | 11,705 | 15,563 | ||||||

| Total deferred revenue | $ | 53,866 | $ | 49,123 | ||||

At October 31, 2008, we expect approximately $13.3 million of our deferred revenue to be recognized subsequent to fiscal year 2009.

Seasonality

Our quarterly financial results fluctuate as a result of a number of factors including public education budget cycles and the mix of perpetual license fee and subscription product sales. Historically we have experienced our lowest order levels, cash balances and revenues in the first and second quarters of our fiscal year, and higher levels of orders, cash and revenues in our third and fourth quarters. More recently, our increasing emphasis on sales of subscription products has moderated the seasonality of our revenues. Because of these factors, the results for interim periods are not necessarily indicative of the results to be expected for the full fiscal year.

Employees

As of October 31, 2008, we had approximately 384 employees. We also contract with offshore resources in the development of new products. We have never experienced a work stoppage as a result of a labor dispute, and none of our employees are represented by a labor organization.

Non-Audit Services Performed by Independent Registered Public Accounting Firm

Pursuant to Section 10A(i)(2) of the Securities Exchange Act of 1934, as added by Section 202 of the Sarbanes-Oxley Act of 2002, we are responsible for disclosing to investors the non-audit services approved by our Audit Committee to be performed by, our independent registered public accounting firm. Non-audit services are defined as services other than those provided in connection with an audit or a review of our financial statements. During the period covered by this Annual Report on Form 10-K, our Audit Committee pre-approved non-audit services, consisting of fees paid for online research materials.

Web Site Access to Reports

Our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Definitive Proxy Statements on Schedule 14A, Current Reports on Form 8-K, and any amendments to those reports, are made available free of charge on our web site (www.plato.com) as soon as reasonably practicable after such reports are filed with the Securities and Exchange Commission (“SEC”). Statements of changes in beneficial ownership of our securities on Form 4 by our executive officers and directors are made available on our web site by the end of the business day following the submission of such filings to the SEC. All reports mentioned above are also available from the SEC’s web site (www.sec.gov).

ITEM 1A. RISK FACTORS

We operate in a market environment that involves significant risks, many of which are beyond our control. The following risk factors may adversely impact our results of operations, financial position, cash flow and the market price of our common stock. Although we believe that we have identified and discussed below the key risk factors affecting our business, they are not the only ones facing us. There may be additional risks and uncertainties that are not presently known or that are not currently believed to be significant that also may affect our results of operations and financial condition.

Risks Relating to Our Industry

We derive a substantial portion of our revenues from public school funding, which is dependent on support from federal, state, and local governments. Changes in funding for public school systems could reduce our revenues and cash flows and impede the growth of our business.

The availability of funding to purchase our products is subject to many factors that can affect government funding. These factors include downturns in general economic conditions, like those which we are currently experiencing, that can reduce government tax revenues and may affect education funding, emergence of other priorities that can divert government funding from educational objectives, periodic changes in government leadership that can change spending priorities, and the government appropriations process, which is often slow and unpredictable. In many instances, customers rely on specific funding appropriations to purchase our products. Curtailments, delays, or reductions in this funding can delay or reduce revenues and cash flow we had otherwise forecasted to receive.

The growth of our business depends on continued investment by public school systems in interactive educational technology and products. Changes to funding of public school systems can slow this type of investment and adversely affect our revenues and market opportunities.

Competition in our industry is intense and growing, which could adversely affect our performance.

Our industry is intensely competitive, rapidly evolving, and subject to technological change. We compete primarily against organizations offering educational and training software and services, including comprehensive curriculum software publishers, companies providing single-title retail products, and Internet content and service providers. Some of our competitors have substantially greater financial, technical and marketing resources than us. The demand for e-learning products and services has grown significantly with the advent of on-line educational institutions, improvements in Internet access and reductions in the cost of technology. While this growing demand presents opportunities for us, it also results in the addition or consolidation of competitors. Increased competition in our industry could result in price reductions, reduced operating margins, or loss of market share, which could seriously harm our business, cash flows, and operating results.

Risks Relating to Our Company

The success of our business model is dependent on growth in market acceptance of online subscription products delivered over the Internet. If this acceptance does not grow or is otherwise diminished, our revenues will continue to decline and may affect our ability to achieve profitability.

Our ability to generate revenue growth and to become profitable is dependent on significant growth of subscription fees to our Internet-based products. Market acceptance of software solutions delivered over the Internet can be negatively affected by factors such as customers’ confidentiality concerns with regard to student information that is stored outside of their controlled computing environments, existing investments in owned courseware, technology infrastructure and related personnel, customer preferences with regard to perpetual licenses vs. annual subscription decisions, and availability, reliability and security of access to the Internet within a school district.

Adverse changes in these factors could result in a decline in the acceptance of web-based courseware solutions making it difficult for us to execute our current business model. As a result, we may need to reevaluate that business model, which may affect our ability to achieve profitability.

The success of our product investment strategy and our ability to remain competitive against companies with access to larger amounts of capital is dependent on our ability to maintain our cost-effective off-shore development resources. If we are unable to do so, we would experience significant product delays and increases in product development costs which would adversely affect our strategy, competitive position, revenues and profitability.

More than 45% of our total product development and maintenance spending in fiscal year 2008 was incurred on off-shore development resources. We believe the use of these resources provides us greater flexibility, cost savings, and a greater return on our development investments. These resources are also critical to our ability to quickly transition our products to a subscription-based business model, respond quickly to market changes and to compete against companies with access to larger amounts of capital than we have. However, this dependence introduces risks common to many outsourcing relationships. These risks include the supplier’s ability to maintain sufficient capacity, control costs, and hire, train, and retain qualified resources, as well as risks associated with our limited direct control and physical access to these resources. Our supplier agreements contain provisions intended to limit some of these risks; however, there can be no assurance that they will be effective at doing so. If our supplier relationships are suddenly and adversely affected, it would cause significant product delays and increased development costs, which would have a material negative effect on our competitive position, revenues and profitability.

Our future success may be dependent on our ability to compete in the broader instructional materials market against larger competitors with significantly greater resources than we have.

The instructional materials market has been dominated for many years by a small number of large publishers that provide textbooks and other printed materials to the school market. These companies have well-established distribution channels and significantly greater marketing, curriculum and financial resources than us. As electronic instructional materials continue to grow and take market share from print materials, competition from these companies will increase and we may not be able to compete effectively.

Our future success is dependent on Internet and other technology developments, our ability to adapt to these and other technological changes and to meet evolving industry standards.

Our ability to execute our strategy of delivering our products on a subscription basis over the Internet and generating the related expected revenues is dependent on the development and maintenance of Internet technology as well as our ability to adapt and respond to changes in Internet and other software technologies.

We may encounter difficulties responding to these and other technological changes that could delay our introduction of products and services or require us to make larger than anticipated investments to maintain existing products. Software industries are characterized by rapid technological change and obsolescence, frequent product introductions, and evolving industry standards. Our future success will, to a significant extent, depend on our ability to maintain and enhance our existing products, develop and introduce new products, satisfy an expanded range of customer needs, and achieve market acceptance. We may not have sufficient resources to make the necessary investments to develop and implement the technological advances required to maintain our competitive position.

Since fiscal 2005 we have been transitioning our business from products that are licensed on a perpetual basis to those that are licensed on a subscription basis. The different revenue recognition characteristics of these products affect the comparability of our financial results. Until we fully complete this transition, our business will be difficult to predict and compare from period to period. Our business is also seasonal. As a result of these factors, we may continue to experience unexpected fluctuations in our quarterly cash flows, revenues and results from operations, which may adversely affect our stock price and the implementation of our strategy.

We expect sales of perpetual license products to continue to decline as we fully complete our transition to subscription-based products. As a result, our operating results will continue to be difficult to predict, may be difficult to compare to historical periods, and may fluctuate from quarter-to-quarter due to factors such as the size, timing, and product mix of license vs. subscription orders. In addition, public school budget cycles result in purchases that have historically been concentrated in the last two quarters of our fiscal year. Accordingly, our annual operating performance can be materially and adversely affected if factors such as school budget constraints, availability of federal and state funding, sales productivity and new product introductions do not align with these purchasing patterns. If such annual results are not achieved we may have to delay or adjust components of our strategy implementation which may affect our ability to achieve profitability.

Our transition from perpetual to subscription-based products has resulted in an increasing trend whereby cash receipts from the sale of our products has shifted from payment shortly after the time of sale, to payment over the subscription period. This trend, together with the seasonality of our business previously discussed, may adversely affect our short-term liquidity.

We generally require that one-year subscriptions and sales of perpetual licenses be paid in full within a short time after completion of the sale. Multi-year subscription customers may be given an option to pay for these subscriptions annually in advance, and these customers are increasingly electing, or negotiating, to make multi-year payments. This increasing delay in the receipt of payment for the sales of our products, together with the seasonality of our business discussed above, has adversely affected our cash flows and may increase our short-term liquidity needs.

Misuse or misappropriation of our proprietary rights or inadvertent infringement by us on the rights of others could adversely affect our results of operations.

We regard many of our intellectual property rights as essential to our business. We rely on a combination of the laws of copyrights, trademarks, and trade secrets, as well as license agreements, employment and employment termination agreements, third-party non-disclosure agreements, and other methods to protect our proprietary rights. We enforce our intellectual property rights when we become aware of any infringements or potential infringements and believe they warrant such action. If we were unsuccessful in our ability to protect these rights, our operating results could be adversely affected.

Although we believe our products and services have been independently developed and that none of our products or services infringes on the rights of others, third parties may assert infringement claims against us in the future. We may be required to modify our products, services or technologies or obtain a license to permit our continued use of those rights. We may not be able to do so in a timely manner or upon reasonable terms and conditions. Failure to do so could harm our business and operating results.

We have a number of technological mechanisms to prevent or inhibit unauthorized copying of our software products and generally require the execution of a written license agreement, which restricts use and copying of our software products. However, if such copying or misuse were to occur to any substantial degree, our operating results could be adversely affected.

If our security measures are breached and unauthorized access is obtained to our web-based products, they may be perceived as not being secure, customers may curtail or stop using these products and we may incur significant legal and financial exposure and liabilities.

The use of our web-based subscription products involves the storage of certain personal information with regard to the teachers and students using these products. If our security measures are breached and unauthorized access to this information occurs, our reputation will be damaged, our business may suffer and we could incur significant liability. Because the techniques used to attempt unauthorized access to systems such as ours change frequently and generally are not recognized until attempted on a target, we may be unable to anticipate these techniques or to implement adequate preventative measures. If an actual or perceived breach of our security occurs, the market perception of the security of our system could be harmed and we could lose sales and customers.

Claims relating to content available on or accessible from, our web sites may subject us to liabilities and additional expense.

Our web-based subscription products incorporate content from, and links to, third-party web sites which are not under our direct control. As a result, we could be subject to claims relating to this content. In addition to exposing us to potential liability, claims of this type could require us to change our web sites in a manner that could be less attractive to our customers and divert our financial and development resources.

Interruptions or delays in service from our third-party Web hosting facilities could impair the delivery of our service and harm our business.

Our subscription products are delivered using standard computer hardware located in two, third-party Web hosting facilities, with the primary facility located on the west coast of the United States. We do not control the operation of these facilities, and they are vulnerable to damage or interruption from earthquakes, floods, fires, power loss, telecommunications failures and similar events. Despite precautions taken at these facilities, the occurrence of a natural disaster or other unanticipated problems at these facilities could result in lengthy interruptions in our service. Even with disaster recovery arrangements in place, our service could be interrupted. Interruptions in our service may reduce our revenue, cause us to issue credits, cause customers to terminate their subscriptions and adversely affect our renewal rates and our ability to attract new customers. Our business will also be harmed if our customers and potential customers believe our service is unreliable.

ITEM 1B. UNRESOLVED STAFF COMMENTS

None.

We lease all of our facilities, including our corporate headquarters in Bloomington, Minnesota. We continue to be a party to two leases for unoccupied office space in the United Kingdom. Our leased facilities are adequate to meet our current and expected business requirements.

From time to time, we may become involved in litigation arising out of operations in the normal course of business. As of October 31, 2008, we were not party to any pending legal proceedings the outcome of which could reasonably be expected to have a material unfavorable or favorable effect on our operating results, financial position or cash flows.

ITEM 4. SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS

None.

PART II.

ITEM 5. MARKET FOR THE REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

Market Information

Our common stock has traded publicly on the NASDAQ Global Market under the symbol “TUTR” since December 23, 1992. The quarterly ranges of high and low prices per share of our common stock were as follows:

| 2008 | 2007 | |||||||||||||||

| Fiscal Quarter | High | Low | High | Low | ||||||||||||

| First | $ | 4.70 | $ | 2.90 | $ | 5.96 | $ | 4.90 | ||||||||

| Second | 3.88 | 2.44 | 5.59 | 3.70 | ||||||||||||

| Third | 3.04 | 1.84 | 4.73 | 3.81 | ||||||||||||

| Fourth | 3.22 | 1.30 | 4.80 | 3.00 | ||||||||||||

Holders

As of December 31, 2008, there were approximately 512 record holders of our common stock, excluding stockholders whose stock is held either in nominee name and/or street name brokerage accounts. Based on information available to us, there were approximately 1,807 holders of our common stock whose stock is held either in nominee name and/or street name brokerage accounts.

Stock Performance Graph

The following stock performance graph does not constitute soliciting material, and should not be deemed filed or incorporated by reference into any other Company filing under the Securities Act of 1933 or the Securities Exchange Act of 1934, except to the extent the Company specifically incorporates this stock performance graph by reference therein.

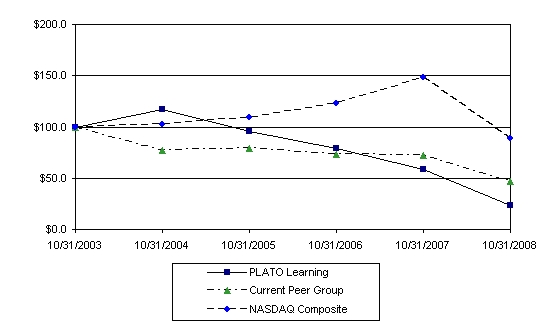

In accordance with Securities and Exchange Commission regulations, the following performance graph compares the cumulative total stockholder return on our common stock to the cumulative total return on the NASDAQ Composite Index and the weighted average return of our peer group (described below) for the five years ended October 31, 2008, assuming an initial investment of $100 and the reinvestment of all dividends.

Our current peer group consists of the following: LeapFrog Enterprises, Inc., Nobel Learning Communities, Princeton Review, Inc., Renaissance Learning, Inc., Scholastic Corp., School Specialty, Inc. and Scientific Learning, Inc.

| 10/31/2003 | 10/31/2004 | 10/31/2005 | 10/31/2006 | 10/31/2007 | 10/31/2008 | |||||||||||||||||||

| PLATO Learning, Inc. | $ | 100.00 | $ | 116.88 | $ | 95.24 | $ | 78.91 | $ | 58.81 | $ | 23.47 | ||||||||||||

| Current Peer Group | $ | 100.00 | $ | 77.33 | $ | 79.11 | $ | 72.75 | $ | 72.52 | $ | 46.63 | ||||||||||||

| NASDAQ | $ | 100.00 | $ | 102.21 | $ | 109.73 | $ | 122.49 | $ | 147.97 | $ | 89.07 | ||||||||||||

Dividends

We did not declare or pay cash dividends on our common stock in fiscal years 2008 or 2007. While future cash dividend payments are at the discretion of our Board of Directors, our current intentions are to reinvest all earnings in the development and growth of our business.

Securities Authorized for Issuance Under Equity Compensation Plans

The information required by Item 201(d) of Regulation S-K is set forth under Item 12 of this Annual Report on Form 10-K.

Repurchases

We repurchased 1,550 and 36,836 shares of our common stock for an aggregate cost of approximately $4,000 and $105,000 during the second and third quarters of fiscal 2008, respectively. The shares were repurchased in accordance with employee elections to withhold shares to fund tax withholdings due upon vesting of restricted stock. Shares repurchased but not reissued are presented as treasury stock in the Consolidated Balance Sheet.

ITEM 6. SELECTED FINANCIAL DATA

| (In thousands, except per share amounts) | 2008 | 2007 | 2006 | 2005 | 2004 | |||||||||||||||

| For the year ended October 31: | ||||||||||||||||||||

| Revenues(1) | $ | 68,401 | $ | 69,632 | $ | 90,719 | $ | 121,804 | $ | 141,801 | ||||||||||

| Gross profit (2) | 26,933 | 32,113 | 49,936 | 56,996 | 91,248 | |||||||||||||||

| Operating expenses: | ||||||||||||||||||||

| Sales and marketing | 27,632 | 29,849 | 38,598 | 49,996 | 61,586 | |||||||||||||||

| General and administrative | 10,366 | 12,095 | 16,619 | 18,420 | 19,469 | |||||||||||||||

| Product maintenance and development | 4,060 | 4,334 | 5,496 | 5,646 | 5,973 | |||||||||||||||

| Amortization of intangibles | 1,550 | 1,740 | 3,711 | 4,322 | 4,308 | |||||||||||||||

| Goodwill impairment (3) | 71,865 | - | - | - | - | |||||||||||||||

| Restructuring, impairment and other charges | 6,748 | (478 | ) | 9,093 | 6,025 | - | ||||||||||||||

| Operating loss | (95,288 | ) | (15,427 | ) | (23,581 | ) | (27,413 | ) | (88 | ) | ||||||||||

| Other income, net | 254 | 1,159 | 1,701 | 586 | 290 | |||||||||||||||

| Income tax expense (benefit) | (3,137 | ) | 608 | 600 | 860 | 2,030 | ||||||||||||||

| Net loss | (91,897 | ) | (14,876 | ) | (22,480 | ) | (27,687 | ) | (1,828 | ) | ||||||||||

| Basic and diluted loss per share | $ | (3.85 | ) | $ | (0.63 | ) | $ | (0.95 | ) | $ | (1.18 | ) | $ | (0.08 | ) | |||||

| At October 31: | ||||||||||||||||||||

| Cash and cash equivalents | $ | 20,018 | $ | 24,297 | $ | 33,094 | $ | 46,901 | $ | 29,235 | ||||||||||

| Marketable securities | - | - | - | 213 | 16,223 | |||||||||||||||

| Accounts receivable, net (4) | 6,834 | 11,752 | 17,497 | 22,768 | 41,852 | |||||||||||||||

| Total assets | 68,967 | 162,780 | 175,198 | 197,328 | 232,744 | |||||||||||||||

| Long-term debt, excluding current portion | - | - | 18 | 57 | 42 | |||||||||||||||

| Deferred revenue (4) | 44,921 | 44,600 | 40,814 | 40,431 | 51,575 | |||||||||||||||

| Total liabilities | 58,911 | 62,045 | 60,748 | 62,501 | 73,294 | |||||||||||||||

| Stockholders' equity | $ | 10,056 | $ | 100,735 | $ | 114,450 | $ | 134,827 | $ | 159,450 | ||||||||||

| (1) | In 2006, we began transitioning our business model from one that sells one-time perpetual licenses to our software, for which revenue is generally recognized up-front upon delivery, to one that sells subscription-based products, for which revenue is recognized over the subscription period. As a result, this transition will affect the comparability of our revenues and profitability from period to period until it is complete. |

| (2) | Gross profit was reduced by asset impairment charges related to: |

| 2008 | 2007 | 2006 | 2005 | 2004 | ||||||||||||||||

| Capitalized product development | $ | 5,085 | $ | 531 | $ | - | $ | 4,412 | $ | - | ||||||||||

| Purchased technology intangible assets | - | - | 1,089 | 8,782 | - | |||||||||||||||

| $ | 5,085 | $ | 531 | $ | 1,089 | $ | 13,194 | $ | - | |||||||||||

See Notes 7 and 8 to the Consolidated Financial Statements.

| (3) | For additional detailed information see Note 8 to the Consolidated Financial Statements. |

| (4) | To conform to the Balance Sheet presentation used in 2008, we reduced accounts receivable and deferred revenue for 2007 and 2006 by amounts not billed under non-cancelable subscription agreements. These amounts totaled $4,523 and $1,032 as of October 31, 2007 and 2006, respectively. |

ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

Fiscal Year

Our fiscal year is from November 1 to October 31. Unless otherwise stated, references to the years 2008, 2007, and 2006 relate to the fiscal years ended October 31, 2008, 2007, and 2006, respectively. References to future years also relate to our fiscal year ending October 31.

Critical Accounting Policies and Estimates

Our discussion and analysis of financial condition and results of operations is based upon our consolidated financial statements, which have been prepared in accordance with accounting principles generally accepted in the United States of America. The preparation of these financial statements requires us to make estimates and judgments that affect the reported amounts of assets, liabilities, revenues, and expenses. We continually evaluate our critical accounting policies and estimates, and have identified the policies relating to the following areas as those that are significant to our financial statement presentation, and require difficult, subjective, or complex judgments:

| · | Revenue recognition |

| · | Capitalized product development costs |

| · | Valuation of our deferred income taxes |

| · | Valuation and impairment analysis of goodwill and identified intangible assets |

Our discussion of these policies is intended to supplement, but not replace, the more detailed discussion of these and other accounting policies and disclosures contained in the Notes to Consolidated Financial Statements.

Revenue Recognition. We derive our revenues from three sources: (1) subscription revenues, which are comprised of subscription fees from customers accessing our online, web-based products; (2) license revenues from non-cancelable perpetual license agreements; and (3) related professional and support services and other revenue.

We recognize revenue when all of the following conditions are met:

| · | There is persuasive evidence of an arrangement; |

| · | Access to our online subscription products has been provided to the customer or the perpetual courseware has been delivered; |

| · | The amount of fees to be paid by the customer is fixed and determinable; and |

| · | The collectability of the fee is probable. |

Revenue from the licensing of software under subscription arrangements is recognized on a ratable basis over the subscription period starting the later of the first day of the subscription period or when all revenue recognition criteria identified above have been met. Amounts that have been invoiced are recorded in accounts receivable and in deferred revenue or revenue, depending on whether the revenue recognition criteria have been met. Amounts due under non-cancelable subscription agreements are not recognized in accounts receivable or deferred revenue until such amounts are invoiced to the customer.

We also provide professional services, which consist of training and implementation services, as well as ongoing customer support and maintenance. Training and implementation services are not essential to the functionality of our software products. Revenues from these services are recognized separately upon delivery where there is objective and reliable evidence of fair value of each deliverable. Software support revenue is deferred and recognized ratably over the support period.

For revenue arrangements with multiple deliverables, we allocate the total amount the customer will pay to the separate units of accounting based on their relative fair values, as determined by the price of the undelivered items when sold separately.

If collectability of the fee is not probable, revenue is recognized as payments are received from the customer provided all other revenue recognition criteria have been met. If the fee due from the customer is not fixed or determinable, revenue is recognized as the payments become due provided all other revenue recognition criteria have been met.

Capitalized Product Development Costs. Our investments in product development are significant, and the rules that govern how these costs are accounted for in our financial statements can have a significant impact on our operating results from period to period.

Our product development costs relate to the research, development, enhancement, and maintenance of our perpetual and subscription-based software products. We account for software development costs in accordance with the provisions of SFAS No. 86. “Accounting for the Costs of Computer Software to be Sold, Leased or Otherwise Marketed.” Costs related to the initial design and development of new products and the routine enhancement and maintenance of existing products are expensed as incurred. When projects reach technological feasibility we begin capitalization of the related project costs. Capitalization ends when a product is available for general release to our customers, at which time amortization of the capitalized costs begins. The amortization of these costs is included in cost of revenues related to license fees and subscriptions.

We evaluate our capitalized costs on a quarterly basis to determine if the unamortized cost related to any product, or group of products, exceeds its estimated net realizable value. Estimating net realizable value requires us to use judgment in projecting future revenues and cash flows to be generated by the product and thereby quantifying the amount, if any, to be written off. Actual cash flows realized could differ materially from those estimated. In addition, any future changes to our software product offerings could result in write-offs of previously capitalized costs and have a significant impact on our consolidated results of operations. Our analysis as of October 31, 2008 and 2007 resulted in impairment charges on these assets of $4.6 million and $0.5 million, respectively.

Valuation of Deferred Income Taxes. Our accounting policy for the valuation of deferred income taxes is considered critical for several reasons. Significant judgment is required in the assessment of the need for a valuation allowance. In addition, income tax accounting rules, in combination with purchase accounting rules applied in the acquisition of Lightspan in 2004, resulted in a complex tax accounting situation in which, until 2008, we have not recognized tax benefits on operating losses or on the realization of deferred tax assets, but regardless of our operating results, have been recognizing tax expense on future tax liabilities related to tax deductible goodwill.

The majority of our deferred tax assets represent net operating loss carryforwards which are available to offset future taxable income. These loss carryforwards include those acquired in the acquisition of Lightspan in 2004, as well as carryforward losses that existed prior to, or were incurred after, the acquisition. Our ability to realize the benefit of these loss carryforwards is dependent upon our ability to generate future taxable income., Our history of cumulative operating losses over the past several years has led to our current assessment that it is more likely than not that our net deferred taxes will not be realized. As a result, our deferred tax assets are fully reserved and will remain fully reserved until the related tax benefits are realized through the generation of taxable income in a particular year, or until we can demonstrate a history of generating taxable income.

Until 2008, our calculation of net deferred tax assets excluded a deferred tax liability related to tax deductible goodwill. The timing of the reversal of this difference was considered indefinite because it would not reverse until the underlying assets that created the goodwill were disposed of or sold. In 2008, the goodwill was determined to be fully impaired, and as a result, the deferred tax liability associated with tax deductible goodwill was reversed.

Goodwill and Identified Intangible Assets. Goodwill and identified intangible assets are recorded when the purchase price paid for an acquisition exceeds the fair value of the tangible assets acquired. Most of the companies we have acquired have not had significant tangible assets. As a result, a significant portion of the purchase price paid in acquisitions has been allocated to identified intangible assets and/or goodwill.

Identified intangible assets are amortized to expense over their expected useful lives and goodwill is not amortized. Once established, these assets are subject to periodic impairment assessments to determine if their current carrying values are recoverable based on information available at the time these assessments are made. Significant assumptions and estimates are required in making these assessments. Accordingly, the assumptions and estimates we use in implementing this policy affect the amount of identified intangible asset amortization and impairment charges, if any, reflected in our operating results. Our impairment assessments at October 31, 2008 resulted in the elimination of goodwill and a related impairment charge of $71.9 million, and impairment charges of $1.9 million on identified intangible technology and customer assets acquired in previous acquisitions. There were no impairment charges on identified intangible assets or goodwill in 2007.

General Factors Affecting our Financial Results

There are a number of general factors that affect our results from period to period. These factors are discussed below.

Revenue. We are transitioning our business model from one that sells one-time perpetual licenses to our software, for which revenue is generally recognized up-front upon delivery, to one that sells subscription-based products, for which revenue is recognized over the subscription period. As a result, this transition will affect the comparability of our revenues from period to period until it is complete. The transition became most evident in 2006 when we introduced many of our new subscription-based products. As subscription revenues grow as a percentage of total revenues, we expect our period to period revenues to become more comparable and predictable.

Because subscription revenues are recognized ratably over the future subscription period, changes in subscription revenue lag behind changes in orders for subscription products. Periods of strong subscription order growth and increasing deferred revenue balances are generally followed by periods of strong subscription revenue growth, and vice versa. In 2008, a meaningful, but declining portion of our revenues continued to be derived from sales of perpetual licenses to our software products. These revenues are reported as license fees in our consolidated statement of operations. Changes in the quantity and size of individual license fee transactions can have a significant impact on revenues in a period. Our business is also seasonal, with the largest portion of our license fees typically coming in the third and fourth quarters of our fiscal year, and professional service fees being the greatest during periods in which schools are in session. Subscription revenues are less seasoned because they are recognized ratably over the subscription period. While this seasonality does not generally impact the comparability of our annual results, it can significantly impact our results from quarter to quarter.

Gross Profit. Our gross profit during a period is dependent on a number of factors. License fee revenues historically have had high gross profit due to the low direct cost of delivering these products. As a result, the mix of license fee revenues to total revenues in a given period significantly influences reported total gross profit. In addition, a large portion of our costs of revenue are fixed in nature. These costs include amortization of capitalized software development and purchased technology, depreciation and other infrastructure costs to support our hosted subscription services, customer support operations, and full-time professional services personnel who deliver our training services. Accordingly, increases in revenues allow us to leverage these costs resulting in higher gross profit, while decreases in revenues have the opposite effect.

Operating Expenses. General and administrative expenses are substantially fixed in nature. However, certain components such as our provision for bad debts, professional fees, and other expenses can vary based on business results, individual events, or initiatives we may be pursuing at various times throughout the year.

Incentive compensation is a significant variable component of our sales and marketing expenses, approximating 8% to 9% of total revenues in any given period. Sales and marketing expenses also include costs such as travel, tradeshows, and conferences that can vary with revenue activity or individual events that occur during the period.

Product maintenance and development expense in our consolidated statement of operations does not reflect our total level of spending in these areas. Costs to enhance or maintain existing products, or to develop products prior to achieving technological feasibility, are charged to product maintenance and development expense as incurred. Costs incurred to develop new products after technological feasibility is achieved, which represent the majority of our total development spending, are capitalized and amortized to cost of revenues. Accordingly, product maintenance and development expense in our consolidated statement of operations can fluctuate from period to period, in terms of both total dollars and as a percentage of revenue, based on the nature and timing of activities occurring during the period.

Amortization of intangibles represents the amortization of certain identified intangible assets acquired through various acquisitions. While these expenses are generally predictable from period to period because they are fixed over the course of their individual useful lives, they can be affected by events and other factors that result in impairment of these assets and a corresponding reduction in future amortization.

Non-GAAP Financial Measures

The following discussion and analysis of our financial condition and results of operations includes non-GAAP financial measures, identified in the reconciliations below, that is not prepared in accordance with generally accepted accounting principles and may be different from non-GAAP financial measures used by other companies. Non-GAAP financial measures should not be considered as a substitute for, or superior to, measures of financial performance prepared in accordance with GAAP. These non-GAAP financial measures have been used because we believe they are useful to investors by providing greater transparency to supplemental information used in our internal financial and operational analysis. Investors are encouraged to review the following reconciliations of the non-GAAP financial measures used herein to their most directly comparable GAAP financial measures as provided with our consolidated financial statements.

Reconciliation of GAAP Net Loss and Loss Per Share to Non-GAAP Net Loss and Loss Per Share Before Impairments, Restructuring and Other Charges and Benefits (in thousands, except per share amounts)

| 2008 | 2007 | 2006 | ||||||||||

| Net Loss: | ||||||||||||

| Net loss, as reported | $ | (91,897 | ) | $ | (14,876 | ) | $ | (22,480 | ) | |||

| Goodwill impairment | 71,865 | - | - | |||||||||

| Income tax benefit related to goodwill impairment change | (3,137 | ) | - | - | ||||||||

| Restructuring, impairment and other charges | 11,833 | 53 | 10,182 | |||||||||

| Net loss before impairments, restructuring and other charges and benefits | $ | (11,336 | ) | $ | (14,823 | ) | $ | (12,298 | ) | |||

| Loss per Share (basic and diluted): | ||||||||||||

| Loss per share , as reported | $ | (3.85 | ) | $ | (0.63 | ) | $ | (0.95 | ) | |||

| Goodwill impairment | 3.01 | - | - | |||||||||

| Income tax benefit related to goodwill impairment charge | (0.13 | ) | - | - | ||||||||

| Restructuring, impairment and other charges | 0.49 | 0.01 | 0.43 | |||||||||

| Loss per Share before impairments, restructuring and other charges and benefits | $ | (0.48 | ) | $ | (0.62 | ) | $ | (0.52 | ) | |||

| Basic and diluted weighted average common shares outstanding (GAAP) | 23,854 | 23,754 | 23,679 | |||||||||

Reconciliation of GAAP Operating Expense to Non-GAAP Operating Expenses before Impairments, Restructuring and Other Charges (in thousands)

| 2008 | 2007 | 2006 | ||||||||||

| Total operating expenses, as reported | $ | 122,221 | $ | 47,540 | $ | 73,517 | ||||||

| Goodwill impairment | 71,865 | - | - | |||||||||

| Restructuring, impairment and other charges (benefit) | 6,748 | (478 | ) | 9,093 | ||||||||

| Operating expenses before impairments, restructuring and other charges | $ | 43,608 | $ | 48,018 | $ | 64,424 | ||||||

Overview of Financial Results

The transition of our company to a software-as-a-service (“SaaS”) business model that began in 2005 continued throughout 2006, 2007 and most of 2008. Although revenues in 2008 continued to be adversely affected by declining emphasis on sales of legacy perpetual products and related software maintenance, strong growth in subscription revenues on our SaaS products have now substantially offset these declines. Compared to 2007, total 2008 revenues declined $1.2 million, or 1.8%, to $68.4 million.

Our cost management activities throughout the transition have led to significant declines in the costs of operating our business. Together with the moderating revenue declines, these cost declines led to an improvement in our 2008 non-GAAP net loss excluding impairments, restructuring and other charges and benefits, to ($11.3) million, or ($0.48) per share, from ($14.8) million, or ($0.62) per share, in 2007. On a GAAP basis, our net loss was ($91.9) million for 2008 compared to ($14.9) million for 2007, with the increase primarily attributable to the non-cash impairment charge to goodwill described below.

In each of the years of our SaaS transition we have incurred impairment, restructuring and other charges that were generally unrelated to our day-to-day operating activities, but were a necessary part of our long-term transition. In 2008 we recorded a non-cash impairment charge of $71.9 million on goodwill acquired in acquisitions made prior to launching our SaaS strategy, $6.5 million in non-cash impairment charges on software development costs and previously acquired intangible assets, and $5.3 million in cash restructuring and other charges related to a transition in our leadership and activities that we believe will ensure continued operating expense savings in 2009.

By the end of 2008, we completed the first phase of our transition strategy marked by the achievement of double-digit order and revenue growth from our new internet-based subscription products, the moderation of our product investment to levels consistent with our long-term business model, reduction in our cost structure to ensure we move closer to profitability in 2009, and the transition to a new generation of leadership to execute the next phase of our strategy.

We will continue in 2009 to execute the next phase of our long-term strategy, focusing on refining our interactions with customers, building out our product capabilities and how we package and sell them in the market, and improving the overall experience of our customers. We will continue to develop our sales organization and look forward to building continuous relationships with our customers throughout the entire subscription life cycle. The financial effects of the transition to subscription products, however, may continue to adversely affect the comparability of our year-over-year financial results in the near term. This and other risks we face in our business are discussed in more detail in Item 1A of Part I of this report.

Results of Operations

Our discussion and analysis of results of operations should be read in conjunction with the section above captioned “General Factors Affecting our Financial Results”.

Revenues

The following tables summarize certain key information to aid in the understanding of our discussion and analysis of revenues:

Sales Order Information (in thousands)

| 2008 | 2007 | 2006 | ||||||||||||||||||

| Amount | Change from 2007 | Amount | Change from 2006 | Amount | ||||||||||||||||

| Order Value: | ||||||||||||||||||||

| Subscriptions | 43,585 | 19.8 | % | 36,368 | 38.5 | % | 26,259 | |||||||||||||

| License fees | 7,886 | (53.4 | %) | 16,931 | (54.2 | %) | 36,974 | |||||||||||||

| Services | 20,637 | (15.3 | %) | 24,377 | (16.5 | %) | 29,177 | |||||||||||||

| $ | 72,108 | (7.2 | %) | $ | 77,676 | (15.9 | %) | $ | 92,410 | |||||||||||

| Percent of Total Order Value: | ||||||||||||||||||||

| Subscriptions | 60 | % | 47 | % | 29 | % | ||||||||||||||

| License fees | 11 | % | 22 | % | 40 | % | ||||||||||||||

| Services | 29 | % | 31 | % | 31 | % | ||||||||||||||

| 100 | % | 100 | % | 100 | % | |||||||||||||||

Revenue by Category (in thousands)

| 2008 | 2007 | 2006 | ||||||||||||||||||

| Amount | Change from 2007 | Amount | Change from 2006 | Amount | ||||||||||||||||

| Subscriptions | $ | 35,221 | 45.7 | % | $ | 24,173 | 33.0 | % | $ | 18,176 | ||||||||||

| License fees | 8,458 | (52.2 | %) | 17,712 | (52.5 | %) | 37,322 | |||||||||||||

| Services | 24,722 | (10.9 | %) | 27,747 | (21.2 | %) | 35,221 | |||||||||||||

| $ | 68,401 | (1.8 | %) | $ | 69,632 | (23.2 | %) | $ | 90,719 | |||||||||||

2008 vs. 2007.

Total revenues decreased $1.2 million, or 1.8%, to $68.4 million in 2008. Subscription revenues increased $11.0 million, or 45.7%, to $35.2 million as strong growth in subscription product orders in 2007 and 2008 were recognized as revenue over the portion of the subscription periods occurring in 2008. While subscription revenue growth was strong, it was not sufficient to fully offset a decline in license fees and services revenues. Our strategic shift away from legacy perpetual software products resulted in a $9.3 million, or 52.2%, decline in license fee revenues to $8.5 million. Services revenues declined 10.9% to $24.7 million due primarily to a decline in software support revenues on previously purchased perpetual products.

Total orders declined from $77.7 million in 2007 to $72.1 million in 2008, reflecting a slowing of orders in the second half of the fourth quarter of 2008 as news worsened on the broader U.S. economy and school districts put spending decisions on hold as they evaluated the effects on their budgets. The order decline also reflects the continuing transition from selling products that are licensed on a perpetual basis, which have higher one-time selling prices, to those that are licensed on a subscription basis, which have lower selling prices but are renewable at the end of each subscription period.

2007 vs. 2006.

Total revenues decreased 23.2% to $69.6 million in 2007 from $90.7 million in 2006, due primarily to the $19.6 million decline in perpetual license fee revenues that reflected our shifting sales emphasis from legacy perpetual products to subscription products delivered on PLE. Subscription revenues increased 33.0% compared to 2006 and surpassed license revenue as a percent of total revenue. Services revenues declined 21.2% from 2006 on a decline in revenues from professional services and technical services, which are tied closely to perpetual license orders.

Gross Profit

To aid in the understanding of our discussion and analysis of gross profit, the following tables summarize the percentage of total revenue, and the gross profit percentage for each revenue category:

Gross Profit Percentage

| Increase (Decrease) | ||||||||||||||||||||

| Revenue Category | 2008 | 2007 | 2006 | 2007 to 2008 | 2006 to 2007 | |||||||||||||||

| Subscriptions | 47.0 | % | 35.7 | % | 50.5 | % | 11.3 | % | (14.8 | %) | ||||||||||

| License fees | 37.6 | % | 52.6 | % | 64.6 | % | (15.0 | %) | (12.0 | %) | ||||||||||

| Services | 49.7 | % | 53.0 | % | 50.3 | % | (3.3 | %) | 2.7 | % | ||||||||||

| Total (1) | 39.4 | % | 46.1 | % | 55.0 | % | (6.7 | %) | (8.9 | %) | ||||||||||

(1) Asset impairment charges of $5.1 million, $0.5 million and $1.1 million in 2008, 2007 and 2006, respectively, are reflected in the Total Gross Profit Percentage in the table, but are not reflected in the individual revenue category gross profit percentages.

Percentage of Total Revenue

| Revenue Category | 2008 | 2007 | 2006 | |||||||||

| Subscriptions | 51.5 | % | 34.7 | % | 20.0 | % | ||||||

| License fees | 12.4 | % | 25.4 | % | 41.2 | % | ||||||

| Services | 36.1 | % | 39.9 | % | 38.8 | % | ||||||

| Total | 100.0 | % | 100.0 | % | 100.0 | % | ||||||

2008 vs. 2007

The total gross profit percentage declined to 39.4% in 2008, and includes the negative effect of $5.1 million in asset impairment charges which had the effect of decreasing 2008 reported margins by 7.4 percentage points compared to a total gross profit margin in 2007 of 46.1%.

The changes from 2007 to 2008 in the gross profit percentages of each revenue category were as follows:

| · | The increase in the subscription gross profit percentage, from 35.7% in 2007 to 47.0% in 2008, reflects the lower delivery and support costs of our internet-based subscription products. Subscription revenues increased $11.0 million while increases in subscription related product development amortization, royalty costs and support services increased only $3.1 million, resulting in a gross profit percentage on incremental subscription revenues of approximately 72%. |

| · | The decline in the license fee gross profit percentage, from 52.6% in 2007 to 37.6% in 2008, was the result of lower license fee revenues, as discussed above, on a base of primarily fixed costs including amortization of product development and purchased intangibles, and distribution costs. |

| · | The decrease in the services gross profit percentage, from 53.0% in 2007 to 49.7% in 2008, was due to a decrease in the mix of higher margin software support services revenues which are tied closely to perpetual license orders. |

2007 vs. 2006

The 2007 total gross profit percentage decreased to 46.1% in 2007 from 55.0% in 2006, primarily due to the decline in higher margin license fee revenue. Higher margin license fee revenues decreased from 41.2% to 25.4% of total revenue, while subscription revenues, which were still in an early-stage growth period and experiencing lower margins, increased from 20.0% to 34.7% of total revenues. These changes in revenue mix were due to the factors discussed under “Revenues” above.

The changes from 2006 to 2007 in the gross profit percentages of each revenue category were as follows:

| · | The decrease in the subscription gross profit percentage, from 50.5% in 2006 to 35.7% in 2007, was due to an increase in product development amortization on new subscription products released in 2006 and 2007, combined with the reallocation of customer support resources from legacy to new subscription products in response to the growth in subscription customers, partially offset by the increase in subscription revenue. |

| · | The decline in the license fee gross profit percentage, from 64.6% in 2006 to 52.6% in 2007, was the result of lower license fee revenues, as discussed above, on a base of primarily fixed costs including amortization of product development and purchased intangibles, and distribution costs. |

| · | The increase in the services gross profit percentage, from 50.3% in 2006 to 53.0% in 2007, was due to improvements in productivity and utilization of resources in our professional services organization, and to an increase in the mix of higher margin software support services revenues which have low variable costs. |

Operating Expenses

To aid in the understanding of our discussion and analysis of our operating expenses, the following table summarizes the amount and percentage change in the amounts from the previous year for certain operating expense line items:

| Amount, in thousands | Increase (Decrease) | |||||||||||||||||||

| 2008 | 2007 | 2006 | 2007 to 2008 | 2006 to 2007 | ||||||||||||||||

| Sales and marketing | $ | 27,632 | $ | 29,849 | $ | 38,598 | (7.4 | %) | (22.7 | %) | ||||||||||

| General and administrative | 10,366 | 12,095 | 16,619 | (14.3 | %) | (27.2 | %) | |||||||||||||

| Product maintenance and development | 4,060 | 4,334 | 5,496 | (6.3 | %) | (21.1 | %) | |||||||||||||