Washington, D.C. 20549

Mr. Hal Liebes

Form N-CSR is to be used by management investment companies to file reports with the Commission, not later than 10 days after the transmission to Stockholders of any report to be transmitted to Stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to the Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Many Investors Shun Powerful Wealth Creator

In 1924, economist John Maynard Keynes wrote that companies that reinvest profits can create “an element of compound interest operating in favour of a sound industrial investment." At Alger, we believe reinvesting profits and producing compounding earnings growth is a powerful wealth creator. To that end, we seek companies that we believe have strong potential for compounding earnings growth, and we seek to avoid cyclical companies, including “short-duration” companies, or businesses with high current earnings that return most of their profits to shareholders. In most instances, these cyclical companies, in our view, have little or no potential for future long-term earnings growth.

As Warren Buffett has observed, investors “occasionally do crazy things,” which creates opportunities for investors who can “disregard mob fears or enthusiasms….and focus on a few simple fundamentals." We believe recent concerns about interest rates, inflation and valuations have caused many investors to act irrationally by focusing on cyclical short- duration companies while shunning the "sound industrial investment" identified by Keynes.

Setting the Stage for a Difficult Six-Month Period

The strong trend of investors rejecting the appeal of long-term earnings growth, in our view, played a major role in our disappointing fund performance during the fiscal six-month period ended April 30, 2022. The fiscal period included the continuation of a dramatic rotation by many investors seeking instant gratification by favoring companies with high current earnings. This rotation was initially fueled prior to the reporting period by optimism that scaling back or eliminating measures to curtail the COVID-19 pandemic combined with unprecedented levels of fiscal stimulus would drive strong economic growth. More recently, however, optimism gave way to concerns that equities may be overvalued at a time when the economy could overheat and require the U.S. Federal Reserve (the “Fed”) to continue to raise interest rates to fight inflation.

These concerns were supported by the following developments:

| • | U.S. gross domestic product (“GDP”), which declined 3.4% in 2020 due to the economy shutting down to contain the pandemic, jumped 5.7% in 2021. |

| • | After climbing to 6.3% at the end of 2020, the seasonally adjusted unemployment rate declined to 4.2% as of the November 2021 start of the fiscal six-month reporting period. It eventually reached 3.6% as of the end of the six-month period, during which concerns about inflation grew, a result of a tight labor market, among other things. |

| • | Data appeared to validate inflation concerns. After hitting a 6.8% year-over- year increase (or increase during the past 12-month period) in November 2021 and increasing each subsequent month, the Consumer Price Index hit 8.5% as of March 2022. |

In response, the Fed shifted its outlook-it no longer maintained that inflation was a transitory result of supply chain issues and the economy reopening, and in March, the Fed raised the federal funds rate by 25 basis points ("BPS"), its first hike since cutting the rate to zero in 2020. Furthermore, Fed statements in March led many investors to anticipate a 50BPS rate hike in May and 200BPS in aggregate hikes by the end of 2022. Fears that rate hikes could eventually spark a recession also weighed upon investor sentiment.

Interest Rates Support Rotation Away from Quality

The rotation to short-duration companies was also partially supported by investors reacting to higher interest rates in a fairly typical fashion-they adjusted their cash flow modeling by increasing the rate at which they discount future cash flows back to the present, thereby lowering the value of long-duration companies. This process is similar to how long-term bonds are impacted more by rising rates than short-term bonds.

Not Just Growth, But High-Quality Small Cap Growth, Underperforms

Many small cap growth companies tend to have little or no current earnings, but strong potential for significant sales and earnings growth. Within the Russell 2000 Growth Index, for example, we believe many Healthcare companies are high-quality businesses even though they may not generate profits due to their investments in new initiatives, their products or potential products can have high gross margins and potential for capturing market share.

As a result of investors dismissing the appeal of potential earnings growth, the Healthcare sector was one of the worst performing sectors within the small cap growth category. From a broader perspective, sectors that generally consist of companies that provide dividends and appear to be less susceptible to inflation, such as Energy and Consumer Staples, led.

Also during the fiscal six-month period, growth underperformed value across the market cap spectrum, with the -26.77% return of the Russell 2000 Growth Index being a noteworthy laggard when compared to the -9.5% return of the Russell 2000 Value Index. The broad market, as measured by the S&P 500 Index, dropped 8.17%.

International Markets Also Struggle

Concerns about interest rates, inflation and the Russian invasion of Ukraine also extended beyond the U.S. Investors also assessed the spread of COVID-19 in China. Among non-U.S. equities, emerging markets significantly underperformed with the MSCI Emerging Markets Index declining 14.04% during the fiscal six-month reporting period. Within the index, the Utilities sector was the only sector to generate positive performance, as investors focused on companies that they perceived as having recession resistant fundamentals that provide a relatively high return of cash to shareholders. Consumer Discretionary, Healthcare and Energy were among the worst performing sectors. The selloff also included developed markets with the MSCI EAFE Index declining 11.58%. From a broader perspective, the MSCI ACWI Index declined 11.45%.

Irrational Behavior Creates Opportunity

As a result of investors’ rotation out of quality companies, growth equities, we believe, are trading at attractive valuations. Notably, the Russell 2000 Growth Index price-to-earnings (P/E) ratio based on the next 12-months' earnings, declined from 50.2x to approximately 33.5x during the six-month fiscal reporting period while the Russell 1000 Growth Index declined from 30.7x to 23.8x.

Navigating Fed Rate Hikes

Investors who are concerned about monetary policy may want to consider two points:

First, Fed rate increases don’t always lead to recessions. In fact, since 1965 there have been three instances in which the Fed increased the federal funds rate 300 BPS or more that resulted in continued real economic growth and slowing inflation rather than recessions. Additionally, during the 12-months following the end of Fed tightening in 1985 and 1995, as well as after the Fed relented in 2018, equities generated double-digit returns.

Second, the later phases of monetary tightening have been accompanied by growth stocks outperforming value equities. The six-month periods starting approximately three months after the beginning of Fed tightening cycles initiated in 1994, 1999, 2004, and 2015 illustrate this point. Based on the returns of the Russell 3000 Growth and Russell 3000 Value indices, the median outperformance of growth during those periods was 400BPS. During later phases of rate hikes, economic growth slows, so investors may be more willing to pay a premium for companies that can increase their earnings.

Going Forward

We continue to believe that unprecedented levels of innovation, such as healthcare advancements in genetic science, and digital technologies including artificial intelligence, e-commerce, the metaverse, streaming entertainment, and cloud computing are providing opportunities for leading companies to reward investors by generating long-term earnings growth. We will continue to focus on conducting in-depth fundamental research as we seek leaders of innovation rather than take short-term bets on the fickle nature of investor sentiment. We believe doing so is the best strategy for helping our valued shareholders reach their investment goals.

Portfolio Matters

Alger Capital Appreciation Institutional Fund

The Alger Capital Appreciation Institutional Fund returned -26.65% for the fiscal six- month period ended April 30, 2022, compared to the -17.84% return of its benchmark, the Russell 1000 Growth Index.

During the reporting period, the largest portfolio sector weightings were Information Technology and Consumer Discretionary. The largest sector overweight was Information Technology and the largest sector underweight was Consumer Staples.

Contributors to Performance

The Communication Services and Real Estate sectors provided the largest contributions to relative performance during the reporting period. Regarding individual positions, Alibaba Group Holding Ltd. Sponsored ADR; AbbVie, Inc.; UnitedHealth Group Inc.; Vertex Pharmaceuticals Inc.; and Qualcomm, Inc. were among the top contributors to absolute performance. Alibaba is a leading e-commerce and cloud computing company in China. It also serves the big data analytics, digital media and entertainment markets. Alibaba’s shares have previously suffered from concerns about heightened regulatory oversight of the Chinese internet sector by the Chinese Communist Party. Additionally, many investors became concerned about the potential for U.S. exchange listed Chinese ADRs to be delisted if they failed to meet U.S. financial reporting standards by 2024. These issues caused investors to sell shares of Alibaba, which we believe created attractive valuations. In the later portion of the fiscal six-month reporting period, the shares outperformed in response to statements by the Chinese government supporting stable markets and overseas listings. The Chinese government also stated that its intensified regulatory efforts aimed at tech companies may end soon.

Detractors from Performance

The Information Technology and Financial sectors were among the sectors that detracted from relative performance during the reporting period. Regarding individual positions, Amazon.com, Inc.; Microsoft Corp.; Shopify, Inc., Cl. A; Alphabet, Inc., Cl. C; and PayPal Holdings, Inc. were the top detractors from absolute performance. Microsoft is a positive dynamic change beneficiary of corporate America's transformative digitization. In a previous earnings call, Microsoft's CEO expects that technology spending as a percent of GDP is likely to jump from about 5% today to 10% in a few years, and that Microsoft will continue to take market share within the technology industry. Microsoft’s enterprise cloud product, Azure, is rapidly growing and accruing market share. Microsoft reported that Azure grew 46% in the quarter ended December 31, 2021, and the company’s total revenue growth exceeded 20%. Microsoft's share price declined despite its high unit volume growth as the broad equity market and technology stocks declined due to higher interest rates and the Russia/Ukraine conflict.

Alger Focus Equity Fund

The Alger Focus Equity Fund returned -25.17% for the fiscal six-month period ended April 30, 2022, compared to the -17.84% return of its benchmark, the Russell 1000 Growth Index.

During the reporting period, the largest sector weightings were Information Technology and Consumer Discretionary. The largest sector overweight was Communication Services and the largest sector underweight was Consumer Staples.

Contributors to Performance

The Communication Services and Real Estate sectors provided the greatest contributions to relative performance during the reporting period. Regarding individual positions, Alibaba Group Holding Ltd. Sponsored ADR; UnitedHealth Group, Inc.; Qualcomm, Inc.; Starbucks Corp.; and Xilinx, Inc. were the top contributors to absolute performance. Shares of Alibaba outperformed in response to developments identified in the Alger Capital Appreciation Institutional Fund discussion.

Detractors from Performance

The Information Technology and Financials sectors were among the sectors that detracted from relative performance during the reporting period. Regarding individual positions, Amazon.com, Inc.; Microsoft Corp.; Shopify, Inc., Cl. A; Intuit, Inc.; and Alphabet, Inc., Cl. C were the most significant detractors from absolute performance. Shares of Microsoft underperformed in response to developments identified in the Alger Capital Appreciation Institutional Fund discussion.

Alger Mid Cap Growth Institutional Fund

The Alger Mid Cap Growth Institutional Fund returned -34.74% for the fiscal six-month period ended April 30, 2022, compared to the -25.44% return of its benchmark, the Russell Midcap Growth Index.

During the reporting period, the largest sector weightings were Information Technology and Healthcare. The largest sector overweight was Energy and the largest underweight was Industrial.

Contributors to Performance

The Consumer Discretionary and Real Estate sectors provided the largest contributions to relative performance during the reporting period.

Regarding individual positions, Diamondback Energy, Inc.; Palo Alto Networks, Inc.; Vail Resorts, Inc.; Lucid Group, Inc.; and Xilinx, Inc. were among the top contributors to absolute performance. Vail Resorts is a premier luxury mountain resort operator whose properties include locations in Vail, Breckenridge, Beaver Creek, Park City, and Whistler. Given its strong industry position, shares of Vail Resorts positively contributed to portfolio performance as it capitalized on consumers’ embrace of travel and social activity as the economy reopened from pandemic restrictions.

Detractors from Performance

The Information Technology and Healthcare sectors were among the sectors that detracted from relative performance during the reporting period. Among individual positions, Upstart Holdings, Inc.; Natera, Inc.; Marqeta, Inc., Cl. A; Affirm Holdings, Inc., Cl. A; and Paycom Software, Inc. were among the most significant detractors from absolute performance. Natera is a specialty lab providing genetic testing services in reproductive health, oncology and transplant. Non-invasive prenatal testing (NIPT), part of the company’s reproductive health franchise, has generated the majority of revenue historically; however, we believe Natera's oncology business has potential to contribute toward a larger share of revenue as customers increasingly adopt these tests following positive insurance reimbursement decisions and favorable clinical trial results. Natera’s share underperformed after the publication of short report by Hindenburg Research. The company also lost a false advertisement lawsuit by CareDx, and high-growth, high-valuation companies were out of favor with many investors during the fiscal reporting period. We believe many of the allegations in the short report regarding sales and the company’s relationship with a third-party billing vendor are irrelevant to Natera’s outlook and its oncology franchise, which we view as the company’s key growth engine.

Alger Small Cap Growth Institutional Fund

The Alger Small Cap Growth Institutional Fund returned -34.99% for the fiscal six-month period ended April 30, 2022, compared to the -26.77% return of its benchmark, the Russell 2000 Growth Index.

During the reporting period, the largest portfolio sector weightings were Healthcare and Information Technology. The largest sector overweight was Healthcare and the largest underweight was Industrials.

Contributors to Performance

The Financials and Industrials sectors provided the largest contributions to relative performance during the reporting period. Regarding individual positions, Vocera Communications, Inc.; Magnolia Oil & Gas Corp., Cl. A; US Foods Holding Corp.; Chefs' Warehouse, Inc.; and HealthEquity, Inc. were among the top contributors to absolute performance. Vocera Communications is a leading provider of cloud-based communication and workflow solutions, primarily for the healthcare industry. Vocera's core solution is an enterprise-class server software platform that allows users to communicate and collaborate using voice or Health Insurance Portability and Accountability Act (HIPAA) compliant secure texting through a variety of Vocera-designed and third-party devices. On January 6, 2022, Stryker Corp. announced an agreement to acquire Vocera for $79.25 per share, or an approximate $3.1 billion enterprise value, which was a 26.8% premium to the prior day's closing price. The deal was completed on February 23, 2022.

Detractors from Performance

The Information Technology and Healthcare sectors were among the sectors that detracted from relative performance during the reporting period. Regarding individual positions, InMode Ltd.; Joint Corp.; HubSpot, Inc.; Everbridge, Inc.; and Avalara, Inc. were among the top detractors from absolute performance. InMode designs, develops, manufactures and commercializes innovative minimally invasive and non-invasive aesthetic medical products. InMode’s platforms harness novel radio frequency (RF) technology for emerging minimally invasive procedures that bridge the gap between temporary treatments like facials and more invasive surgical procedures like facelifts across several specialty categories such as plastic surgery, gynecology, dermatology, ophthalmology and otolaryngology (ear, nose and throat care). The aesthetics market experienced strong tailwinds coming out of the COVID-19 pandemic. These tailwinds include the “Zoom effect,” or dissatisfaction with one’s personal appearance after viewing one’s own face on Zoom, which resulted in more people deciding to undergo aesthetic procedures. De-stigmatization of aesthetic procedures, aided by social media platforms, has also supported InMode's results. However, the stock price declined during the first quarter, in part due to a rotation out of high-valuation names. Some investors also feared a wallet share shift away from aesthetics and have concerns about InMode’s exposure to international markets due to the Ukraine/Russia conflict; however, our research suggests the company's revenue exposure to Europe is minimal.

I thank you for putting your trust in Alger.

Sincerely,

Daniel C. Chung, CFA

Chief Executive Officer

Fred Alger Management, LLC

Investors cannot invest directly in an index. Index performance does not reflect the deduction for fees, expenses or taxes.

This report and the financial statements contained herein are submitted for the general information of shareholders of the funds. This report is not authorized for distribution to prospective investors in a fund unless preceded or accompanied by an effective prospectus for the fund. Performance of funds discussed represents the return of Class I shares.

The performance data quoted represents past performance, which is not an indication or guarantee of future results.

Standardized performance results can be found on the following pages. The investment return and principal value of an investment in a fund will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted. For performance data current to the most recent month-end, visit us at www.alger.com, or call us at (800) 992-3863.

The views and opinions of the funds’ management in this report are as of the date of the Shareholders' Letter and are subject to change at any time subsequent to this date. There is no guarantee that any of the assumptions that formed the basis for the opinions stated herein are accurate or that they will materialize. Moreover, the information forming the basis for such assumptions is from sources believed to be reliable; however, there is no guarantee that such information is accurate. Any securities mentioned, whether owned in a fund or otherwise, are considered in the context of the construction of an overall portfolio of securities and therefore reference to them should not be construed as a recommendation or offer to purchase or sell any such security. Inclusion of such securities in a fund and transactions in such securities, if any, may be for a variety of reasons, including, without limitation, in response to cash flows, inclusion in a benchmark, and risk control. The reference to a specific security should also be understood in such context and not viewed as a statement that the security is a significant holding in a fund. Please refer to the Schedule of Investments for each fund that is included in this report for a complete list of fund holdings as of April 30, 2022. Securities mentioned in the Shareholders' Letter, if not found in the Schedules of Investments, may have been held by the funds during the fiscal six-month period ended April 30, 2022.

Risk Disclosures

Alger Capital Appreciation Institutional Fund

Investing in the stock market involves risks, including the potential loss of principal. Growth stocks may be more volatile than other stocks as their prices tend to be higher in relation to their companies’ earnings and may be more sensitive to market, political, and economic developments. Local, regional, or global events such as environmental or natural disasters, war, terrorism, pandemics, outbreaks of infectious diseases and similar public health threats, recessions, or other events could have a significant impact on investments. A significant portion of assets may be invested in securities of companies in related sectors, and may be similarly affected by economic, political, or market events and conditions and may be more vulnerable to unfavorable sector developments. Foreign securities involve special risks including currency fluctuations, inefficient trading, political and economic instability, and increased volatility.

Alger Focus Equity Fund

Investing in the stock market involves risks, including the potential loss of principal. Growth stocks may be more volatile than other stocks as their prices tend to be higher in relation to their companies’ earnings and may be more sensitive to market, political, and economic developments. Local, regional, or global events such as environmental or natural disasters, war, terrorism, pandemics, outbreaks of infectious diseases and similar public health threats, recessions, or other events could have a significant impact on investments. A significant portion of assets may be invested in securities of companies in related sectors, and may be similarly affected by economic, political, or market events and conditions and may be more vulnerable to unfavorable sector developments. Foreign securities involve special risks including currency fluctuations, inefficient trading, political, and economic instability, and increased volatility. Assets may be focused in a small number of holdings, making them susceptible to risks associated with a single economic, political or regulatory event than a more diversified portfolio. Active trading may increase transaction costs, brokerage commissions, and taxes, which can lower the return on investment.

Alger Mid Cap Growth Institutional Fund

Investing in the stock market involves risks, including the potential loss of principal. Growth stocks may be more volatile than other stocks as their prices tend to be higher in relation to their companies’ earnings and may be more sensitive to market, political, and economic developments. Local, regional or global events such as environmental or natural disasters, war, terrorism, pandemics, outbreaks of infectious diseases and similar public health threats, recessions, or other events could have a significant impact on investments. A significant portion of assets may be invested in securities of companies in related sectors, and may be similarly affected by economic, political, or market events and conditions and may be more vulnerable to unfavorable sector developments. Investing in companies of medium capitalizations involve the risk that such issuers may have limited product lines or financial resources, lack management depth, or have limited liquidity. Foreign securities involve special risks including currency fluctuations, inefficient trading, political and economic instability, and increased volatility. Active trading may increase transaction costs, brokerage commissions, and taxes, which can lower the return on investment.

Alger Small Cap Growth Institutional Fund

Investing in the stock market involves risks, including the potential loss of principal. Growth stocks may be more volatile than other stocks as their prices tend to be higher in relation to their companies’ earnings and may be more sensitive to market, political, and economic developments. Local, regional or global events such as environmental or natural disasters, war, terrorism, pandemics, outbreaks of infectious diseases and similar public health threats, recessions, or other events could have a significant impact on investments. A significant portion of assets may be invested in securities of companies in related sectors, and may be similarly affected by economic, political, or market events and conditions and may be more vulnerable to unfavorable sector developments. Investing in companies of small and medium capitalizations involve the risk that such issuers may have limited product lines or financial resources, lack management depth, or have limited liquidity. Foreign securities involve special risks including currency fluctuations, inefficient trading, political and economic instability, and increased volatility. At times, the Fund may hold a large cash position, which may underperform relative to equity securities.

For a more detailed discussion of the risks associated with a fund, please see the Prospectus.

Before investing, carefully consider a fund's investment objective, risks, charges, and expenses.

For a prospectus and summary prospectus containing this and other information or for the Alger Institutional Funds' most recent month-end performance data, visit www.alger.com, call (800) 992-3863 or consult your financial advisor. Read the prospectus and summary prospectus carefully before investing.

Distributor: Fred Alger & Company, LLC.

NOT FDIC INSURED. NOT BANK GUARANTEED. MAY LOSE VALUE.

Definitions:

| • | The Consumer Price Index is a measure of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services. |

| • | Price-to-earnings is the ratio for valuing a company that measures its current share price relative to its earnings per share (EPS). |

| • | The Russell 3000 Growth Index combines the large-cap Russell 1000 Growth, the small-cap Russell 2000 Growth and the Russell Microcap Growth Index. It includes companies that are considered more growth oriented relative to the overall market as defined by Russell's leading style methodology. The Russell 3000 Growth Index is constructed to provide a comprehensive, un- biased, and stable barometer of the growth opportunities within the broad market. |

| • | The Russell 3000 Value Index measures the performance of the broad value segment of the US equity value universe. It includes those Russell 3000 companies with lower price-to-book ratios and lower forecasted growth values. The Russell 3000 Value Index is constructed to provide a comprehensive, unbiased and stable barometer of the broad value market. |

| • | The MSCI ACWI Index (gross) is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed and emerging markets. The MSCI ACWI captures large and mid cap representation across developed markets and emerging markets countries. |

| • | The MSCI Emerging Markets Index (gross) is a free float-adjusted market capitalization index that is designed to measure equity market performance in the global emerging markets. The MSCI EAFE Index is designed to repre- sent the performance of large and mid-cap securities across developed mar- kets, including countries in Europe, Australasia and the Far East, excluding the U.S. and Canada. |

| • | The MSCI EAFE Index is designed to represent the performance of large and mid-cap securities across developed markets, including countries in Eu- rope, Australasia and the Far East, excluding the U.S. and Canada. |

| • | The Russell 1000 Growth Index measures the performance of the large-cap growth segment of the U.S. equity universe. It includes those Russell 1000 companies with higher growth earning potential as defined by Russell's lead- ing style methodology. The Russell 1000 Growth Index is constructed to provide a comprehensive and unbiased barometer for the large-cap growth segment. |

| • | The Russell Midcap Growth Index measures the performance of the mid- cap growth segment of the U.S. equity universe. It includes those Russell Midcap Index companies with higher growth earning potential as defined by Russell's leading style methodology. The Russell Midcap Growth Index is constructed to provide a comprehensive and unbiased barometer of the mid-cap growth market. |

| • | The S&P 500 Index is an index of large company stocks considered to be representative of the U.S. stock market. |

| • | The Russell 2000 Growth Index measures the performance of the small- cap growth segment of the U.S. equity universe. It includes those Russell 2000 companies with higher growth earning potential as defined by Russell's leading style methodology. The Russell 2000 Growth Index is constructed to provide a comprehensive and unbiased barometer for the small-cap growth segment. |

| • | The Russell 2000 Value Index measures the performance of the small cap value segment of the U.S. equity universe. It includes those Russell 2000 companies with lower price-to-book ratios and lower forecasted growth values. The Russell 2000 Value Index is constructed to provide a comprehensive and unbiased barometer for the large-cap growth segment. |

FUND PERFORMANCE AS OF 3/31/22 (Unaudited)

AVERAGE ANNUAL TOTAL RETURNS

| | 1 YEAR | | | 5 YEARS | | | 10 YEARS | | | SINCE INCEPTION | |

Alger Capital Appreciation Institutional Class I (Inception 11/8/93) | | | 2.01 | % | | | 17.82 | % | | | 15.31 | % | | | 12.82 | % |

Alger Capital Appreciation Institutional Class R (Inception 1/27/03)* | | | 1.56 | % | | | 17.29 | % | | | 14.78 | % | | | 12.27 | % |

Alger Capital Appreciation Institutional Class Y (Inception 2/28/17) | | | 2.38 | % | | | 18.28 | % | | | n/a | | | | 18.33 | % |

Alger Capital Appreciation Institutional Class Z-2 (Inception 10/14/16) | | | 2.36 | % | | | 18.20 | % | | | n/a | | | | 18.79 | % |

Alger Focus Equity Class A (Inception 12/31/12) | | | (2.73 | )% | | | 18.74 | % | | | n/a | | | | 17.32 | % |

Alger Focus Equity Class C (Inception 12/31/12) | | | 0.98 | % | | | 19.12 | % | | | n/a | | | | 17.11 | % |

Alger Focus Equity Class I (Inception 11/8/93) | | | 2.69 | % | | | 20.09 | % | | | 16.05 | % | | | 10.46 | % |

Alger Focus Equity Class Y (Inception 2/28/17) | | | 3.02 | % | | | 20.47 | % | | | n/a | | | | 20.55 | % |

Alger Focus Equity Class Z (Inception 12/31/12) | | | 2.99 | % | | | 20.42 | % | | | n/a | | | | 18.40 | % |

Alger Mid Cap Growth Institutional Class I (Inception 11/8/93) | | | (13.25 | )% | | | 15.39 | % | | | 13.17 | % | | | 12.21 | % |

Alger Mid Cap Growth Institutional Class R (Inception 1/27/03)* | | | (13.61 | )% | | | 14.85 | % | | | 12.60 | % | | | 11.65 | % |

Alger Mid Cap Growth Institutional Class Z-2 (Inception 10/14/16) | | | (12.92 | )% | | | 15.75 | % | | | n/a | | | | 17.16 | % |

Alger Small Cap Growth Institutional Class I (Inception 11/8/93) | | | (20.97 | )% | | | 15.31 | % | | | 11.81 | % | | | 10.03 | % |

Alger Small Cap Growth Institutional Class R (Inception 1/27/03)* | | | (21.30 | )% | | | 14.78 | % | | | 11.28 | % | | | 9.50 | % |

Alger Small Cap Growth Institutional Class Z-2 (Inception 8/1/16) | | | (20.68 | )% | | | 15.70 | % | | | n/a | | | | 16.52 | % |

The performance data quoted represents past performance, which is not an indication or a guarantee of future results. The Fund’s average annual total returns include changes in share price and reinvestment of dividends and capital gains.

Previously, the Alger Focus Equity Fund followed different investment strategies under the name "Alger Large Cap Growth Institutional Fund" and was managed by different portfolio managers. Performance prior to December 31, 2012 reflects those management styles and does not reflect the current investment personnel and strategies of the Fund. On October 15, 2018, Alger Capital Appreciation Focus Fund changed its name to Alger Focus Equity Fund.

| * | Since inception performance is calculated from 11/8/93. Performance ftgures prior to 1/27/03, inception of Class R shares, are those of the Fund's Class I shares. The performance ftgures prior to 1/27/03 have been reduced to reflect the higher operating expenses of Class R shares. |

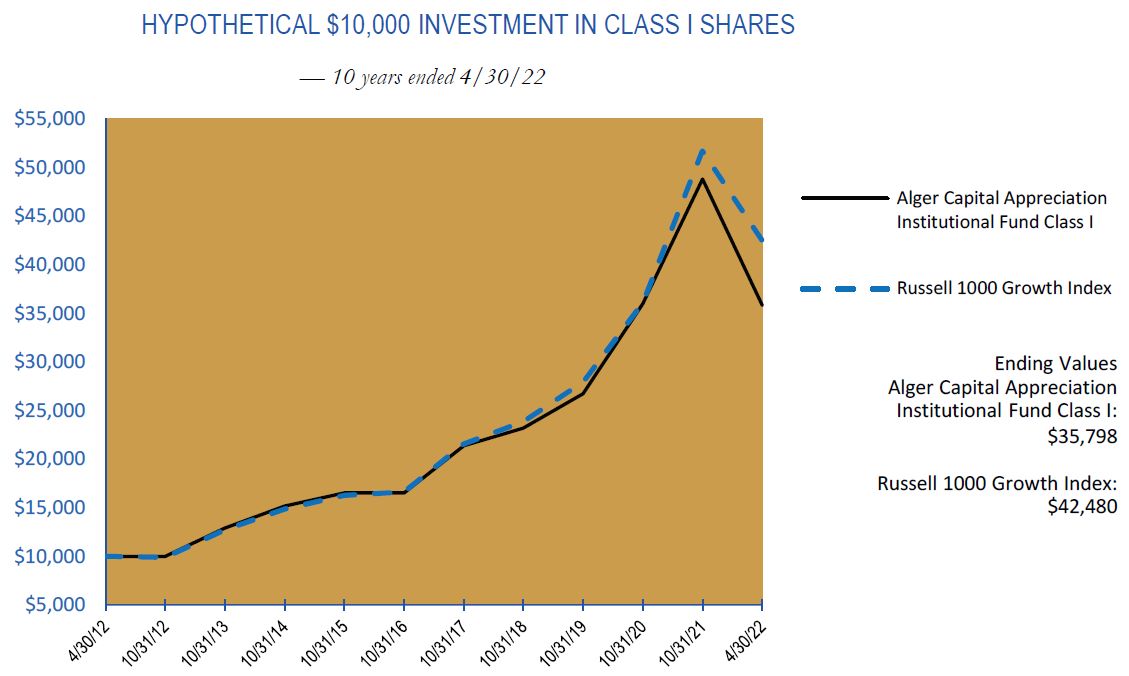

ALGER CAPITAL APPRECIATION INSTITUTIONAL FUND

Fund Highlights Through April 30, 2022 (Unaudited)

The chart above illustrates the change in value of a hypothetical $10,000 investment made in the Alger Capital Appreciation Institutional Fund Class I shares and the Russell 1000 Growth Index (an unmanaged index of common stocks) for the ten years ended April 30, 2022. Figures for the Alger Capital Appreciation Institutional Fund Class I shares and the Russell 1000 Growth Index include reinvestment of dividends. Figures for the Alger Capital Appreciation Institutional Fund Class I shares also include reinvestment of capital gains. Performance for the Alger Capital Appreciation Institutional Fund Class R, Class Y and Class Z-2 shares may vary from the results shown above due to differences in expenses each class bears. Investors cannot invest directly in any index. Index performance does not reflect deduction for fees, expenses, or taxes.

ALGER CAPITAL APPRECIATION INSTITUTIONAL FUND

Fund Highlights Through April 30, 2022 (Unaudited) (Continued)

PERFORMANCE COMPARISON AS OF 4/30/22

AVERAGE ANNUAL TOTAL RETURNS

| | | 1 YEAR | | | 5 YEARS | | | 10 YEARS | | | Since 11/8/1993 | |

| Class I (Inception 11/8/93) | | | (18.11 | )% | | | 13.56 | % | | | 13.60 | % | | | 12.16 | % |

| Class R (Inception 1/27/03)* | | | (18.45 | )% | | | 13.06 | % | | | 13.07 | % | | | 11.61 | % |

| Russell 1000 Growth Index | | | (5.35 | )% | | | 17.28 | % | | | 15.56 | % | | | 10.37 | % |

| | 1 YEAR | | | 5 YEARS | | | 10 YEARS | | | Since Inception | |

| Class Y (Inception 2/28/17) | | | (17.80 | )% | | | 14.02 | % | | | n/a | | | | 14.48 | % |

| Russell 1000 Growth Index | | | (5.35 | )% | | | 17.28 | % | | | n/a | | | | 17.45 | % |

| | 1 YEAR | | | 5 YEARS | | | 10 YEARS | | | Since Inception | |

| Class Z-2 (Inception 10/14/16) | | | (17.85 | )% | | | 13.93 | % | | | n/a | | | | 15.17 | % |

| Russell 1000 Growth Index | | | (5.35 | )% | | | 17.28 | % | | | n/a | | | | 18.35 | % |

The performance data quoted represents past performance, which is not an indication or a guarantee of future results. The Fund's average annual total returns include changes in share price and reinvestment of dividends and capital gains. The chart and table above do not reflect the deduction of taxes that a shareholder would have paid on Fund distributions or on the redemption of Fund shares. Investment return and principal will fluctuate and the Fund's shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance quoted. For updated performance, visit us at www.alger.com or call us at (800) 992-3863.

| * | Performance ftgures prior to 1/27/03, inception of Class R shares, are those of the Fund's Class I shares. The performance ftgures prior to 1/27/03 have been reduced to reflect the higher operating expenses of Class R shares. |

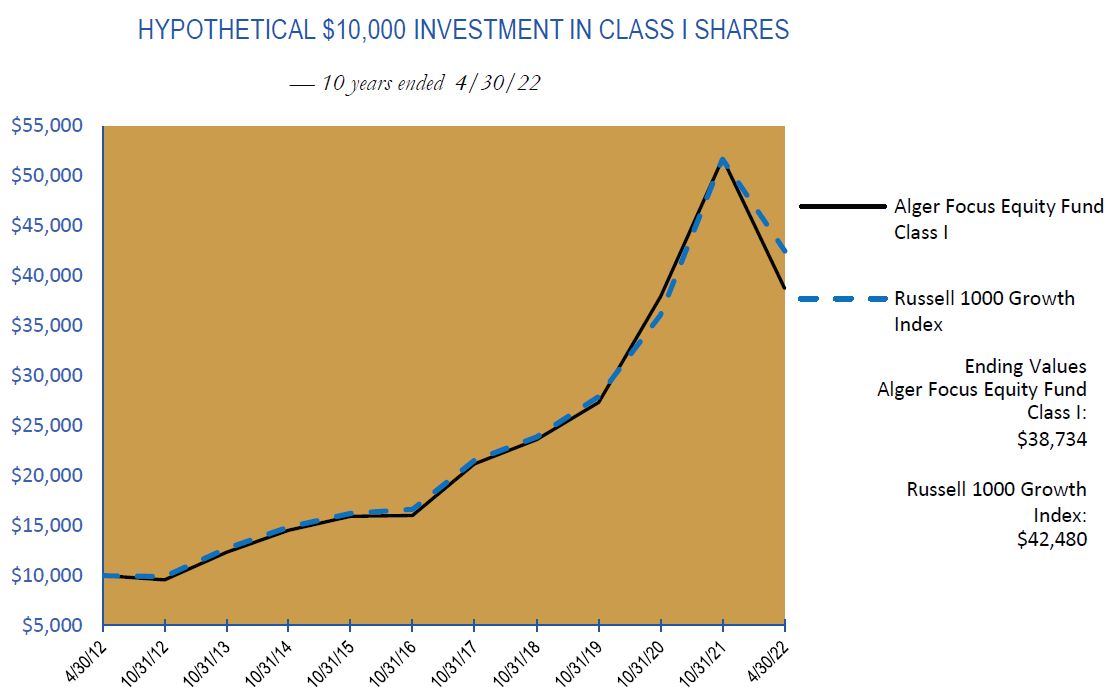

ALGER FOCUS EQUITY FUND

Fund Highlights Through April 30, 2022 (Unaudited)

The chart above illustrates the change in value of a hypothetical $10,000 investment made in the Alger Focus Equity Fund Class I shares and the Russell 1000 Growth Index (an unmanaged index of common stocks) for the ten years ended April 30, 2022. Previously, the Fund followed different investment strategies under the name "Alger Large Cap Growth Institutional Fund" and was managed by different portfolio managers. Performance prior to December 31, 2012 reflects those management styles and does not reflect the current investment personnel and strategies of the Fund. On October 15, 2018, Alger Capital Appreciation Focus Fund changed its name to Alger Focus Equity Fund. Figures for Alger Focus Equity Fund Class I shares and the Russell 1000 Growth Index include reinvestment of dividends. Figures for the Alger Focus Equity Fund Class I shares also include reinvestment of capital gains. Performance for Alger Focus Equity Fund Class A, Class C, Class Y and Class Z shares may vary from the results shown above due to differences in expenses and sales charges that those classes bear. Investors cannot invest directly in any index. Index performance does not reflect deduction for fees, expenses, or taxes.

ALGER FOCUS EQUITY FUND

Fund Highlights Through April 30, 2022 (Unaudited) (Continued)

PERFORMANCE COMPARISON AS OF 4/30/22

AVERAGE ANNUAL TOTAL RETURNS

| | 1 YEAR | | | 5 YEARS | | | 10 YEARS | | | Since Inception | |

| Class I (Inception 11/8/93) | | | (17.34 | )% | | | 15.90 | % | | | 14.50 | % | | | 9.85 | % |

Russell 1000 Growth Index | | | (5.35 | )% | | | 17.28 | % | | | 15.56 | % | | | 10.37 | % |

| | 1 YEAR | | | 5 YEARS | | | 10 YEARS | | | Since Inception | |

| Class A (Inception 12/31/12) | | | (21.71 | )% | | | 14.60 | % | | | n/a | | | | 15.29 | % |

| Class C (Inception 12/31/12) | | | (18.71 | )% | | | 14.97 | % | | | n/a | | | | 15.09 | % |

| Class Z (Inception 12/31/12) | | | (17.10 | )% | | | 16.23 | % | | | n/a | | | | 16.36 | % |

Russell 1000 Growth Index | | | (5.35 | )% | | | 17.28 | % | | | n/a | | | | 16.69 | % |

| | 1 YEAR | | | 5 YEARS | | | 10 YEARS | | | Since Inception | |

| Class Y (Inception 2/28/17) | | | (17.08 | )% | | | 16.27 | % | | | n/a | | | | 16.78 | % |

Russell 1000 Growth Index | | | (5.35 | )% | | | 17.28 | % | | | n/a | | | | 17.45 | % |

The performance data quoted represents past performance, which is not an indication or a guarantee of future results. The Fund's average annual total returns include changes in share price and reinvestment of dividends and capital gains. Class A returns reflect the maximum initial sales charge and Class C returns reflect the applicable contingent deferred sales charge. The chart and table above do not reflect the deduction of taxes that a shareholder would have paid on Fund distributions or on the redemption of Fund shares. Previously, the Fund followed different investment strategies under the name "Alger Large Cap Growth Institutional Fund" and was managed by different portfolio managers. Performance prior to December 31, 2012 reflects those management styles and does not reflect the current investment personnel and strategies of the Fund. On October 15, 2018, the Fund changed its name from Alger Capital Appreciation Focus Fund to Alger Focus Equity Fund. Investment return and principal will fluctuate and the Fund's shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance quoted. For updated performance, visit us at www.alger.com or call us at (800) 992-3863.

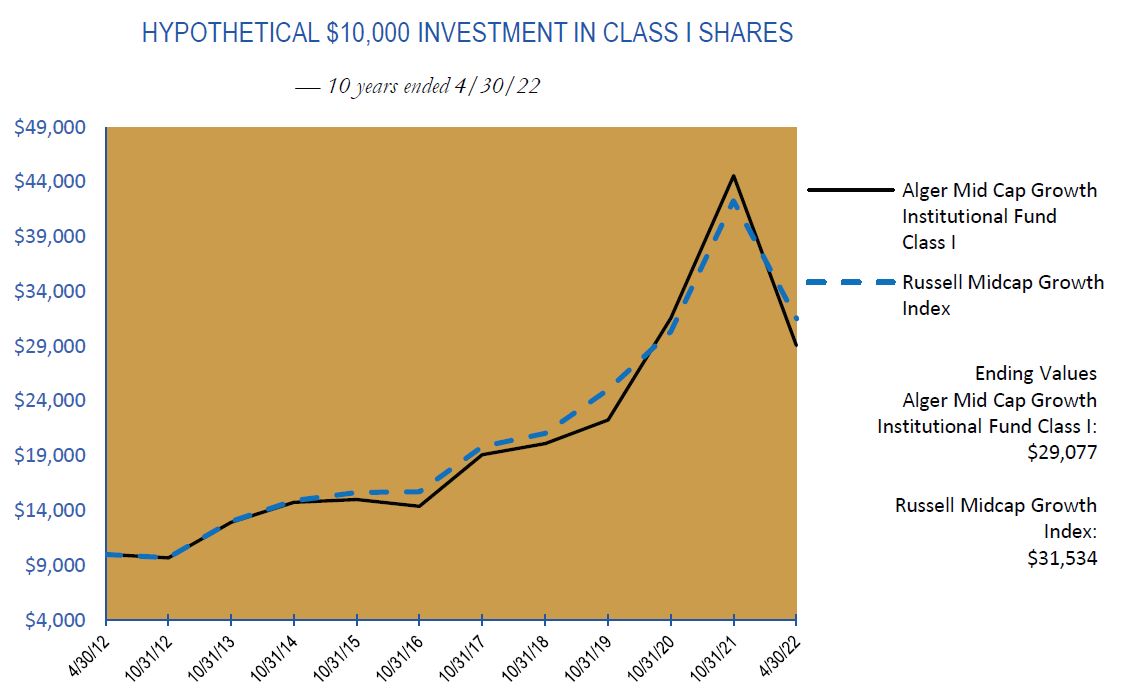

ALGER MID CAP GROWTH INSTITUTIONAL FUND

Fund Highlights Through April 30, 2022 (Unaudited)

The chart above illustrates the change in value of a hypothetical $10,000 investment made in the Alger Mid Cap Growth Institutional Fund Class I shares and the Russell Midcap Growth Index (an unmanaged index of common stocks) for the ten years ended April 30, 2022. Figures for Alger Mid Cap Growth Institutional Fund Class I shares and the Russell Midcap Growth Index include reinvestment of dividends. Figures for the Alger Mid Cap Growth Institutional Fund Class I shares also include reinvestment of capital gains. Performance for the Alger Mid Cap Growth Institutional Fund Class R and Class Z-2 shares may vary from the results shown above due to differences in expenses the class bears. Investors cannot invest directly in any index. Index performance does not reflect deduction for fees, expenses, or taxes.

ALGER MID CAP GROWTH INSTITUTIONAL FUND

Fund Highlights Through April 30, 2022 (Unaudited) (Continued)

PERFORMANCE COMPARISON AS OF 4/30/22

AVERAGE ANNUAL TOTAL RETURNS

| | | 1 YEAR | | | 5 YEARS | | | 10 YEARS | | | Since 11/8/1993 | |

| Class I (Inception 11/8/93) | | | (29.09 | )% | | | 11.42 | % | | | 11.26 | % | | | 11.55 | % |

| Class R (Inception 1/27/03)* | | | (29.42 | )% | | | 10.89 | % | | | 10.70 | % | | | 10.99 | % |

Russell Midcap Growth Index | | | (16.73 | )% | | | 12.06 | % | | | 12.17 | % | | | 9.86 | % |

| | | 1 YEAR | | | 5 YEARS | | | 10 YEARS | | | Since Inception | |

| Class Z-2 (Inception 10/14/16) | | | (28.82 | )% | | | 11.77 | % | | | n/a | | | | 13.57 | % |

Russell Midcap Growth Index | | | (16.73 | )% | | | 12.06 | % | | | n/a | | | | 13.18 | % |

The performance data quoted represents past performance, which is not an indication or a guarantee of future results. The Fund's average annual total returns include changes in share price and reinvestment of dividends and capital gains. The chart and table above do not reflect the deduction of taxes that a shareholder would have paid on Fund distributions or on the redemption of Fund shares. Investment return and principal will fluctuate and the Fund's shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance quoted. For updated performance, visit us at www.alger.com or call us at (800) 992-3863.

| * | Performance ftgures prior to 1/27/03, inception of Class R shares, are those of the Fund's Class I shares. The performance ftgures prior to 1/27/03 have been reduced to reflect the higher operating expenses of Class R shares. |

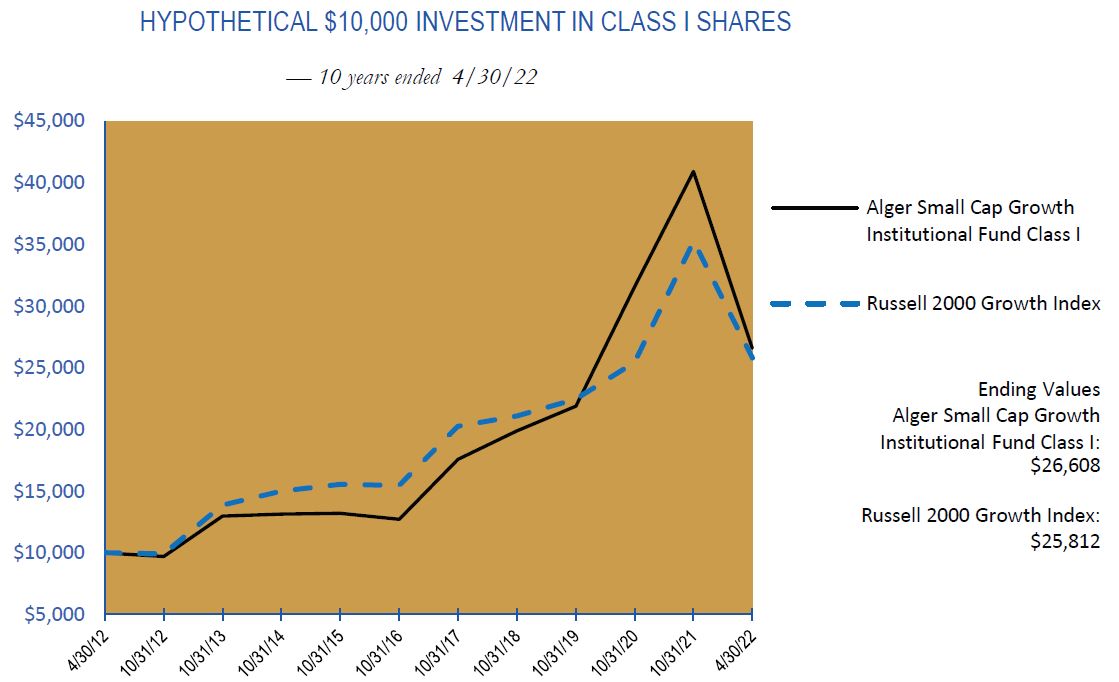

ALGER SMALL CAP GROWTH INSTITUTIONAL FUND

Fund Highlights Through April 30, 2022 (Unaudited)

The chart above illustrates the change in value of a hypothetical $10,000 investment made in the Alger Small Cap Growth Institutional Fund Class I shares and the Russell 2000 Growth Index (an unmanaged index of common stocks) for the ten years ended April 30, 2022. Figures for the Alger Small Cap Growth Institutional Fund Class I shares and the Russell 2000 Growth Index include reinvestment of dividends. Figures for the Alger Small Cap Growth Institutional Fund Class I shares also include reinvestment of capital gains. Performance for the Alger Small Cap Growth Institutional Fund Class R and Class Z-2 shares may vary from the results shown above due to differences in expenses the class bears. Investors cannot invest directly in any index. Index performance does not reflect deduction for fees, expenses, or taxes.

ALGER SMALL CAP GROWTH INSTITUTIONAL FUND

Fund Highlights Through April 30, 2022 (Unaudited) (Continued)

PERFORMANCE COMPARISON AS OF 4/30/22

AVERAGE ANNUAL TOTAL RETURNS

| | | 1 YEAR | | | 5 YEARS | | | 10 YEARS | | | Since 11/8/1993 | |

| Class I (Inception 11/8/93) | | | (34.53 | )% | | | 11.75 | % | | | 10.28 | % | | | 9.45 | % |

| Class R (Inception 1/27/03)* | | | (34.81 | )% | | | 11.24 | % | | | 9.75 | % | | | 8.92 | % |

Russell 2000 Growth Index | | | (26.44 | )% | | | 7.08 | % | | | 9.95 | % | | | 7.27 | % |

| | | 1 YEAR | | | 5 YEARS | | | 10 YEARS | | | Since Inception | |

| Class Z-2 (Inception 8/1/16) | | | (34.34 | )% | | | 12.12 | % | | | n/a | | | | 13.40 | % |

Russell 2000 Growth Index | | | (26.44 | )% | | | 7.08 | % | | | n/a | | | | 8.53 | % |

The performance data quoted represents past performance, which is not an indication or a guarantee of future results. The Fund's average annual total returns include changes in share price and reinvestment of dividends and capital gains. The chart and table above do not reflect the deduction of taxes that a shareholder would have paid on Fund distributions or on the redemption of Fund shares. Investment return and principal will fluctuate and the Fund's shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance quoted. For updated performance, visit us at www.alger.com or call us at (800) 992-3863.

* Performance ftgures prior to 1/27/03, inception of Class R shares, are those of the Fund's Class I shares. The performance ftgures prior to 1/27/03 have been reduced to reflect the higher operating expenses of Class R shares.

PORTFOLIO SUMMARY†

April 30, 2022 (Unaudited)

SECTORS | | Alger Capital Appreciation Institutional Fund | | | Alger Focus Equity Fund | | | Alger Mid Cap Growth Institutional Fund | | | Alger Small Cap Growth Institutional Fund | |

Communication Services | | | 7.3 | % | | | 7.7 | % | | | 4.9 | % | | | 5.7 | % |

Consumer Discretionary | | | 19.7 | | | | 19.9 | | | | 13.9 | | | | 11.8 | |

Consumer Staples | | | 0.4 | | | | 0.0 | | | | 0.5 | | | | 5.3 | |

Energy | | | 2.4 | | | | 2.2 | | | | 8.1 | | | | 5.9 | |

Financials | | | 3.1 | | | | 4.7 | | | | 4.3 | | | | 1.1 | |

Healthcare | | | 14.8 | | | | 11.6 | | | | 16.7 | | | | 29.7 | |

Industrials | | | 8.2 | | | | 7.1 | | | | 11.5 | | | | 6.0 | |

Information Technology | | | 42.3 | | | | 41.2 | | | | 30.1 | | | | 30.4 | |

Materials | | | 1.0 | | | | 0.3 | | | | 1.6 | | | | 2.5 | |

Real Estate | | | 0.4 | | | | 0.0 | | | | 0.5 | | | | 1.0 | |

Utilities | | | 0.3 | | | | 0.0 | | | | 2.6 | | | | 0.0 | |

Short-Term Investments and Net Other Assets | | | 0.1 | | | | 5.3 | | | | 5.3 | | | | 0.6 | |

| | | | 100.0 | % | | | 100.0 | % | | | 100.0 | % | | | 100.0 | % |

† Based on net assets for each Fund.

THE ALGER INSTITUTIONAL FUNDS

ALGER CAPITAL APPRECIATION INSTITUTIONAL FUND

Schedule of Investments April 30, 2022 (Unaudited)

| COMMON STOCKS—99.3% | | SHARES | | | VALUE | |

| AEROSPACE & DEFENSE—3.3% | | | | | | |

HEICO Corp. | | | 111,366 | | | $ | 15,728,220 | |

Lockheed Martin Corp. | | | 44,249 | | | | 19,120,878 | |

Raytheon Technologies Corp. | | | 79,528 | | | | 7,548,003 | |

TransDigm Group, Inc.* | | | 82,036 | | | | 48,795,833 | |

| | | | | | | | 91,192,934 | |

| AGRICULTURAL & FARM MACHINERY—0.5% | | | | | | | | |

Deere & Co. | | | 35,620 | | | | 13,448,331 | |

| AIR FREIGHT & LOGISTICS—0.2% | | | | | | | | |

GXO Logistics, Inc.* | | | 77,772 | | | | 4,603,325 | |

| ALUMINUM—0.1% | | | | | | | | |

Alcoa Corp. | | | 42,618 | | | | 2,889,500 | |

| APPAREL ACCESSORIES & LUXURY GOODS—1.7% | | | | | | | | |

Capri Holdings Ltd.* | | | 324,684 | | | | 15,487,427 | |

Lululemon Athletica, Inc.* | | | 20,354 | | | | 7,218,139 | |

LVMH Moet Hennessy Louis Vuitton SE | | | 36,892 | | | | 23,870,720 | |

| | | | | | | | 46,576,286 | |

| APPLICATION SOFTWARE—8.5% | | | | | | | | |

Adobe, Inc.* | | | 85,585 | | | | 33,887,381 | |

Atlassian Corp., PLC, Cl. A* | | | 66,889 | | | | 15,038,654 | |

Avalara, Inc.* | | | 100,109 | | | | 7,615,292 | |

Bill.com Holdings, Inc.* | | | 58,797 | | | | 10,037,236 | |

Cadence Design Systems, Inc.* | | | 152,306 | | | | 22,975,360 | |

Confuent, Inc , C A* | | | 125,337 | | | | 3,915,528 | |

Datadog, Inc., Cl. A* | | | 175,390 | | | | 21,183,604 | |

Intuit, Inc. | | | 196,343 | | | | 82,218,631 | |

Salesforce, Inc.* | | | 113,022 | | | | 19,885,091 | |

Unity Software, Inc.* | | | 162,585 | | | | 10,797,270 | |

Zendesk, Inc.* | | | 58,263 | | | | 7,110,416 | |

| | | | | | | | 234,664,463 | |

| AUTOMOBILE MANUFACTURERS—3.4% | | | | | | | | |

General Motors Co.* | | | 231,073 | | | | 8,759,978 | |

Tesla, Inc.* | | | 96,611 | | | | 84,124,994 | |

| | | | | | | | 92,884,972 | |

| BIOTECHNOLOGY—3.3% | | | | | | | | |

AbbVie, Inc. | | | 269,467 | | | | 39,579,313 | |

Horizon Therapeutics PLC* | | | 133,973 | | | | 13,204,379 | |

Natera, Inc.* | | | 324,110 | | | | 11,382,743 | |

Vertex Pharmaceuticals, Inc.* | | | 96,331 | | | | 26,319,556 | |

| | | | | | | | 90,485,991 | |

| CASINOS & GAMING—2.5% | | | | | | | | |

MGM Resorts International | | | 1,714,315 | | | | 70,355,488 | |

| CONSUMER FINANCE—0.4% | | | | | | | | |

Upstart Holdings, Inc.* | | | 155,886 | | | | 11,694,568 | |

| COPPER—0.4% | | | | | | | | |

Freeport-McMoRan, Inc. | | | 265,839 | | | | 10,779,772 | |

THE ALGER INSTITUTIONAL FUNDS

ALGER CAPITAL APPRECIATION INSTITUTIONAL FUND

Schedule of Investments April 30, 2022 (Unaudited) (Continued)

| COMMON STOCKS—99.3% (CONT.) | | SHARES | | | VALUE | |

| DATA PROCESSING & OUTSOURCED SERVICES—4.6% | | | | | | |

Block, Inc., Cl. A* | | | 137,735 | | | $ | 13,710,142 | |

Marqeta, Inc., Cl. A* | | | 1,548,074 | | | | 14,397,088 | |

PayPal Holdings, Inc.* | | | 220,857 | | | | 19,419,956 | |

Visa, Inc., Cl. A | | | 376,187 | | | | 80,176,735 | |

| | | | | | | | 127,703,921 | |

| ELECTRIC UTILITIES—0.3% | | | | | | | | |

NextEra Energy, Inc. | | | 129,027 | | | | 9,163,498 | |

| ELECTRICAL COMPONENTS & EQUIPMENT—2.8% | | | | | | | | |

AMETEK, Inc. | | | 154,529 | | | | 19,510,832 | |

Eaton Corp. PLC | | | 309,569 | | | | 44,893,696 | |

Generac Holdings, Inc.* | | | 60,748 | | | | 13,326,896 | |

| | | | | | | | 77,731,424 | |

| FINANCIAL EXCHANGES & DATA—1.5% | | | | | | | | |

S&P Global, Inc. | | | 112,051 | | | | 42,187,202 | |

| FOOTWEAR—0.7% | | | | | | | | |

NIKE, Inc., Cl. B | | | 154,029 | | | | 19,207,416 | |

| HEALTHCARE DISTRIBUTORS—0.9% | | | | | | | | |

McKesson Corp. | | | 83,422 | | | | 25,828,285 | |

| HEALTHCARE EQUIPMENT—2.7% | | | | | | | | |

Dexcom, Inc.* | | | 10,441 | | | | 4,265,984 | |

Edwards Lifesciences Corp.* | | | 242,623 | | | | 25,664,661 | |

Intuitive Surgical, Inc.* | | | 187,135 | | | | 44,781,405 | |

| | | | | | | | 74,712,050 | |

| HEALTHCARE FACILITIES—0.7% | | | | | | | | |

Acadia Healthcare Co., Inc.* | | | 241,935 | | | | 16,422,548 | |

Tenet Healthcare Corp.* | | | 41,235 | | | | 2,989,950 | |

| | | | | | | | 19,412,498 | |

| HOTELS RESORTS & CRUISE LINES—1.4% | | | | | | | | |

Airbnb, Inc., Cl. A* | | | 103,819 | | | | 15,906,109 | |

Expedia Group, Inc.* | | | 49,885 | | | | 8,717,404 | |

Hilton Worldwide Holdings, Inc.* | | | 96,715 | | | | 15,018,872 | |

| | | | | | | | 39,642,385 | |

| HYPERMARKETS & SUPER CENTERS—0.4% | | | | | | | | |

Costco Wholesale Corp. | | | 20,924 | | | | 11,125,709 | |

| INTERACTIVE MEDIA & SERVICES—5.8% | | | | | | | | |

Alphabet, Inc., Cl. C* | | | 57,637 | | | | 132,526,483 | |

Meta Platforms, Inc., Cl. A* | | | 39,501 | | | | 7,918,766 | |

Snap, Inc., Cl. A* | | | 678,807 | | | | 19,318,847 | |

| | | | | | | | 159,764,096 | |

| INTERNET & DIRECT MARKETING RETAIL—7.9% | | | | | | | | |

Alibaba Group Holding Ltd.#,* | | | 288,628 | | | | 28,022,893 | |

Altaba, Inc.*,(a) | | | 342,659 | | | | 1,202,733 | |

Amazon.com, Inc.* | | | 71,980 | | | | 178,915,647 | |

MercadoLibre, Inc.* | | | 11,927 | | | | 11,612,485 | |

| | | | | | | | 219,753,758 | |

THE ALGER INSTITUTIONAL FUNDS

ALGER CAPITAL APPRECIATION INSTITUTIONAL FUND

Schedule of Investments April 30, 2022 (Unaudited) (Continued)

| COMMON STOCKS—99.3% (CONT.) | | SHARES | | | VALUE | |

| INTERNET SERVICES & INFRASTRUCTURE—2.4% | | | | | | |

MongoDB, Inc., Cl. A* | | | 70,131 | | | $ | 24,891,596 | |

Shopify, Inc., Cl. A* | | | 47,675 | | | | 20,348,643 | |

Snowflake, Inc., Cl. A* | | | 128,390 | | | | 22,011,182 | |

| | | | | | | | 67,251,421 | |

| INVESTMENT BANKING & BROKERAGE—0.0% | | | | | | | | |

Morgan Stanley | | | 17,239 | | | | 1,389,291 | |

| LEISURE FACILITIES—1.2% | | | | | | | | |

Vail Resorts, Inc. | | | 132,484 | | | | 33,672,133 | |

| LIFE SCIENCES TOOLS & SERVICES—1.9% | | | | | | | | |

Danaher Corp. | | | 206,770 | | | | 51,926,150 | |

| MANAGED HEALTHCARE—3.0% | | | | | | | | |

UnitedHealth Group, Inc. | | | 161,479 | | | | 82,120,145 | |

| MOVIES & ENTERTAINMENT—1.5% | | | | | | | | |

Live Nation Entertainment, Inc.* | | | 389,747 | | | | 40,876,665 | |

| OIL & GAS EXPLORATION & PRODUCTION—1.7% | | | | | | | | |

Pioneer Natural Resources Co. | | | 206,051 | | | | 47,900,676 | |

| OIL & GAS STORAGE & TRANSPORTATION—0.7% | | | | | | | | |

Cheniere Energy, Inc. | | | 147,421 | | | | 20,021,246 | |

| PHARMACEUTICALS—2.3% | | | | | | | | |

AstraZeneca PLC# | | | 307,048 | | | | 20,387,987 | |

Bayer AG* | | | 636,798 | | | | 41,940,584 | |

| | | | | | | | 62,328,571 | |

| REGIONAL BANKS—1.2% | | | | | | | | |

Signature Bank | | | 131,384 | | | | 31,827,774 | |

| RESTAURANTS—0.9% | | | | | | | | |

Chipotle Mexican Grill, Inc., Cl. A* | | | 3,967 | | | | 5,774,405 | |

Shake Shack, Inc., Cl. A* | | | 256,688 | | | | 14,844,267 | |

Yum China Holdings, Inc. | | | 102,685 | | | | 4,292,233 | |

| | | | | | | | 24,910,905 | |

| SEMICONDUCTOR EQUIPMENT—2.1% | | | | | | | | |

Applied Materials, Inc. | | | 196,391 | | | | 21,671,747 | |

ASML Holding NV# | | | 12,160 | | | | 6,855,443 | |

Enphase Energy, Inc.* | | | 32,695 | | | | 5,276,973 | |

Lam Research Corp. | | | 30,840 | | | | 14,364,038 | |

SolarEdge Technologies, Inc.* | | | 34,243 | | | | 8,574,790 | |

| | | | | | | | 56,742,991 | |

| SEMICONDUCTORS—4.8% | | | | | | | | |

Advanced Micro Devices, Inc.* | | | 725,778 | | | | 62,068,535 | |

NVIDIA Corp. | | | 262,324 | | | | 48,653,232 | |

QUALCOMM, Inc. | | | 153,044 | | | | 21,378,716 | |

| | | | | | | | 132,100,483 | |

| SPECIALTY CHEMICALS—0.5% | | | | | | | | |

Albemarle Corp. | | | 75,109 | | | | 14,483,269 | |

| SYSTEMS SOFTWARE—13.5% | | | | | | | | |

Crowdstrike Holdings, Inc., Cl. A* | | | 133,596 | | | | 26,553,541 | |

Microsoft Corp. | | | 1,228,508 | | | | 340,935,540 | |

Palo Alto Networks, Inc.* | | | 12,300 | | | | 6,903,744 | |

| | | | | | | | 374,392,825 | |

Not applicable.

Not applicable.

Not applicable.

Not applicable.

Not applicable.

Not applicable.

Not applicable.

Not applicable.

Not applicable.

Not applicable.

Not applicable.

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, this report has been signed below by the following persons on behalf of the registrant and in the capacities and on the dates indicated.