Washington, D.C. 20549

Mr. Hal Liebes

Form N-CSR is to be used by management investment companies to file reports with the Commission, not later than 10 days after the transmission to Stockholders of any report to be transmitted to Stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to the Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Table of Contents

The Alger Institutional Funds

| Shareholders’ Letter (Unaudited) |

| April 30, 2023 |

Dear Shareholders,

The Pendulum of Market Sentiment

“In the short run, the market is a voting machine but in the long run, it is a weighing machine.” – Benjamin Graham.

Stock prices may have fluctuated over the six month period ended April 30, 2023, mostly based on interest rate movements, but we agree with Graham that over the longer term, company earnings and cash flows ultimately determine stock prices. We believe the rise in interest rates and the corresponding decline in equity valuations are subsiding, leaving Graham’s proverbial scale to determine where stocks are headed. In the final two months of 2022, optimism surrounding the potential peak of the Federal Reserve Bank’s (Fed) tightening cycle was reinforced by lower-than-expected core Consumer Price Index (CPI) readings for both November and December. Persistent inflation, particularly in wages, remained a focal point for the Fed, and the inverted yield curve amplified fears of a policy misstep or a looming economic downturn. Fed Chairman Jerome Powell indicated in December 2022, that the institution would maintain its “higher-for-longer” approach for interest rates and projected a long-run terminal rate exceeding 5.0%, which sparked concerns about the sustainability of a stock market rebound.

The first quarter of 2023 saw a reversal in the bearish investor sentiment that had marked much of the previous year. In February, the Fed reduced the pace of rate hikes to 25 basis points (bps), after a 50 bps hike in December. Powell, acknowledging the disinflation trend, did not resist the easing of financial conditions, and U.S. Treasury yields fell during the first quarter. In March, concerns around bank funding and liquidity emerged following the collapse of two regional banks, leading to significant deposit outflows at the regional level. However, the Fed, U.S. Treasury, and Federal Deposit Insurance Corporation (FDIC) took steps to contain market concerns. These steps included announcing an emergency liquidity program, guaranteeing uninsured deposits at the impacted regional banks, and allowing some bank mergers and acquisitions to take place. At the end of March, the Fed raised rates by another 25 bps, bringing the Federal Funds rate to 5.0%. In April, U.S. Gross Domestic Product (GDP) grew 1.1%, missing the 2.0% forecast and falling from the prior quarter’s 2.6%, despite robust consumer spending.

Among non-U.S. equities, developed markets saw strong performance during the fiscal six-month period ended April 30, 2023. Notable strength was driven by Europe avoiding an energy crisis due to a mild winter, and global supply chain bottlenecks seeing continued relief. As such, the MSCI EAFE Index was up 24.6%, driven by strong performance in the Financials and Industrials sectors, while the Real Estate and Energy sectors experienced relative weakness. From a broader perspective, the MSCI ACWI Index rose 13.0% during the fiscal six-month period, where the Communication Services and Information Technology sectors showed strong results, while the Health Care and Energy sectors saw weaker performance. Within Emerging Markets, notable strength was driven by China reopening its borders, and the MSCI Emerging Markets Index was up 16.5% during the fiscal six-month period. Strong performance within the Communication Services and Information Technology sectors was slightly offset by relative weakness in the Real Estate and Energy sectors.

During the fiscal six-month period, growth outperformed value, with the Russell 3000 Growth Index returning 10.8%, outperforming the Russell 3000 Value Index, which posted a return of 3.4% for the period. There was also a notable bifurcation between small- and large-cap stocks, where the -3.5% return of the Russell 2000 Index considerably underperformed the 7.2% return of the Russell 1000 Index during the fiscal six-month period.

Slow Dance into Recession

The Conference Board’s Index of Leading Economic Indicators (LEI) – a composite of economic information that includes housing, consumer confidence and durable goods orders – has historically proven to be a strong predictor of recessions, particularly when the index moves into negative territory. The LEI fell into negative territory in August 2022, and as of March 2023, it shows a year-over-year decline of 7.8%.

Further, over the past thirteen tightening cycles, the United States has only achieved a soft landing (i.e., an economic slowdown without a recession) on three occasions (1984, 1994-1995 and 2020). In each of these instances, interest rates were increased by only 300 bps. As of April 30, 2023, the Fed has increased rates by approximately 500 bps since it began its hiking cycle in March 2022. If history is any guide, we find it unlikely that the Fed can successfully orchestrate a soft landing, given the Fed has now hiked well above the approximate “soft landing” rate increase of 300 bps.

Further challenging the ability for a soft landing is the lagged impact of the Fed’s aggressive tightening cycle. It is important to note the strong historical relationship between small bank lending standards and U.S. corporate business spending, known as capital expenditures. As bank lending standards tighten, fewer loans are made and companies’ cost of capital rises. As a result, companies reduce their capital projects, either due to a lack of funds or because the higher cost makes these projects less financially attractive. In our view, bank lending standards will likely continue to tighten and slow business capital expenditures, pressuring earnings for more economically sensitive companies that rely on capital expansion projects.

As of the writing of this letter, the Fed has continued to tighten financial conditions via its interest rate increases and the roll-off of debt from its balance sheet. Further, the broader money supply growth is decelerating and is now in outright contraction for the first time since 1938, which is likely to slow economic activity. For these reasons, we believe the United States may have already entered a recession.

Going Forward

We continue to believe that unprecedented levels of innovation are creating compelling investment opportunities - corporations are digitizing their operations, cloud computing growth continues to support future innovation, and artificial intelligence, which is at an inflection point in our view, potentially enabling significant increases in productivity. In the Health Care sector, we believe that advances in surgical technologies and innovations within biotechnology offer attractive opportunities ahead. As such, we intend to continue to focus on conducting in-depth fundamental research as we seek leaders of innovation rather than taking short-term bets on market sentiment. We believe doing so is the best strategy for helping our valued shareholders reach their investment goals.

Portfolio Matters

Alger Capital Appreciation Institutional Fund

The Alger Capital Appreciation Institutional Fund returned 9.57% for the fiscal six-month period ended April 30, 2023, compared to the 11.51% return of the Russell 1000 Growth Index. During the reporting period, the largest sector weightings were Information Technology and Health Care. The largest sector overweight was Health Care and the largest sector underweight was Information Technology.

Contributors to Performance

The Consumer Discretionary and Industrials sectors provided the largest contributions to relative performance. Regarding individual positions, Microsoft Corporation; NVIDIA Corporation; TransDigm Group Incorporated; MercadoLibre, Inc.; and Apple Inc. were among the top contributors to absolute performance.

TransDigm Group specializes in the production of engineered aerospace components, systems and subsystems. Its core Power and Control segment includes operations that primarily develop, produce and market systems and components that provide power to or control power of aircrafts utilizing electronic, fluid, power and mechanical motion control technologies. During the period, the company reported solid fiscal first quarter results, where both revenues and earnings beat analyst estimates. Better-than-expected results were driven by strength in all three of their major market channels – commercial original equipment manufacturing (OEM), commercial aftermarket and defense – as well as strong order bookings. Moreover, management raised their fiscal full year guidance, noting favorable trends in the commercial aerospace market recovery.

Detractors from Performance

The Health Care and Communication Services sectors were the largest detractors from relative performance. Regarding individual positions, Tesla, Inc.; UnitedHealth Group Incorporated; Albemarle Corporation; Signature Bank; and Humana Inc. were among the top detractors from absolute performance.

UnitedHealth Group is an integrated healthcare benefits company uniquely positioned to address rising healthcare costs for its customers, due to its vertical integration, size, and scale. The Optum health benefits services unit, which accounts for approximately 45% of the company’s operating earnings, in our view, has the potential to grow even further as customers look for ways to manage rising healthcare costs. During the period, shares detracted from performance due to several factors: (1) many 2022 healthcare winners with shorter duration profiles and persistent earnings profiles, such as UnitedHealth Group, underperformed in the first quarter of 2023, (2) uncertainty surrounding Medicare Advantage reimbursement levels from the Federal government in 2023, which will be determined later in the year, and (3) increased regulatory scrutiny in the form of potential Medicare Advantage audits across the industry. While these concerns have impacted UnitedHealth in the near-term, we believe company fundamentals remain intact given its large-scale business model, competitive advantages, and medium- to long-term growth prospects.

Alger Focus Equity Fund

The Alger Focus Equity Fund returned 10.87% for the fiscal six-month period ended April 30, 2023, compared to the 11.51% return of the Russell 1000 Growth Index. During the reporting period, the largest sector weightings were Information Technology and Health Care. The largest sector overweight was Health Care and the largest sector underweight was Information Technology.

Contributors to Performance

The Consumer Discretionary and Industrials sectors provided the largest contributions to relative performance. Regarding individual positions, Microsoft Corporation; NVIDIA Corporation; TransDigm Group Incorporated; MercadoLibre, Inc.; and Flutter Entertainment Plc were among the top contributors to absolute performance.

MercadoLibre is the largest e-commerce company in Latin America, with its largest markets being Brazil, Argentina, and Mexico. The company offers a comprehensive suite of services, including an online marketplace for buyers and sellers, payment solutions through Mercado Pago, merchant and buyer financing through Mercado Credito, shipping services through Mercado Envios, and asset management through Mercado Fondo, among other services. We believe the e-commerce market within Latin America remains underpenetrated, creating a favorable backdrop for MercadoLibre, as they have been growing and investing heavily to expand its first mover advantage. Moreover, we believe that the company’s growing fintech payments business, Mercado Pago, is well-positioned to potentially emerge as a leader in Latin America, as well as an emerging online advertising presence that offers attractive margin expansion potential, in our view. During the period, shares contributed to performance after the company reported resilient fiscal fourth quarter earnings that exceeded analyst estimates. Notable drivers that contributed to the earnings beat included strong gross-merchandise-value and an increase in the average take-rate within both e-commerce and Mercado Pago.

Detractors from Performance

The Information Technology and Communication Services sectors were the largest detractors from relative performance. Regarding individual positions, UnitedHealth Group Incorporated; Tesla, Inc.; Live Nation Entertainment, Inc.; Signature Bank; and EOG Resources, Inc. were among the top detractors from absolute performance. Shares of UnitedHealth Group Incorporated detracted from performance in response to developments identified in the Alger Capital Appreciation Institutional Fund discussion.

Alger Mid Cap Growth Institutional Fund

The Alger Mid Cap Growth Institutional Fund returned 5.25% for the fiscal six-month period ended April 30, 2023, compared to the 6.60% return of the Russell Midcap Growth Index. During the reporting period, the largest sector weightings were Information Technology and Industrials. The largest sector overweight was Information Technology and the largest sector underweight was Consumer Discretionary.

Contributors to Performance

The Information Technology and Energy sectors provided the largest contributions to relative performance. Regarding individual positions, Prometheus Biosciences, Inc.; Constellation Software Inc.; Chipotle Mexican Grill, Inc.; Cadence Design Systems, Inc.; and TransDigm Group Incorporated were among the top contributors to absolute performance.

Prometheus Biosciences is a biotechnology company focused on developing precision-based medicines to treat autoimmune conditions, primarily those afflicting the intestines such as inflammatory bowel disease (IBD) indications, like ulcerative colitis and Crohn’s disease, by leveraging a proprietary bioinformatics database. Shares contributed to performance during the period as the company reported positive Phase 2 clinical trial results from its IBD study, as the drug PRA023 demonstrated significant patient improvement that was well above expectations. On April 15, 2023, the company entered into an agreement to be acquired by Merck & Co. Inc. for $9.6 billion in cash, which was approximately a 75% premium from the prior trading day’s value. The deal is expected to close in the third quarter of 2023.

Detractors from Performance

The Consumer Discretionary and Consumer Staples sectors were the largest detractors from relative performance. Regarding individual positions, CrowdStrike Holdings, Inc.; First Republic Bank; Aritzia, Inc.; Enphase Energy, Inc.; and BILL Holdings, Inc. were among the top detractors from absolute performance.

BILL Holdings is the leading provider of business-to-business (B2B) commerce solutions for small- and medium-sized businesses (SMBs), including streamlining financial operations such as accounts payables (AP) and accounts receivables (AR). Their target market is primarily U.S. SMBs with revenues up to $100 million. The company earns revenue from: (1) subscription fees charged for access to its cloud-based services; (2) usage-based transaction fees, including payments-related fees; and (3) interest earned on funds held on behalf of customers. The company is positioned as a back-office financial operations and an AP automation software-as-a-service (SaaS) platform for the SMB segment of B2B payments. According to our analysis, roughly 42% of B2B payments are still made via physical check, and 93% of businesses with less than $1 billion of annual revenue reported receiving physical checks as payment. During the period, shares detracted from performance, as the company reported weaker than expected results. Specifically, growth in total payment volume and transaction growth weakened due to the challenging macroeconomic backdrop, along with fewer net-customer additions. Despite these events, we believe company fundamentals remain intact and are well positioned to continue to penetrate the underserved SMB market with its differentiated product offerings over the long-term.

Alger Small Cap Growth Institutional Fund

The Alger Small Cap Growth Institutional Fund returned -2.85% for the fiscal six-month period ended April 30, 2023, compared to the -0.29% return of the Russell 2000 Growth Index. During the reporting period, the largest sector weightings were Health Care and Information Technology. The largest sector overweight was Information Technology and the largest sector underweight was Industrials.

Contributors to Performance

The Information Technology and Real Estate sectors provided the largest contributions to relative performance. Regarding individual positions, NeoGenomics, Inc.; Manhattan Associates, Inc.; Wingstop, Inc.; HubSpot, Inc.; and Insulet Corporation were among the top contributors to absolute performance.

Hubspot is a cloud-based marketing and sales platform for SMBs, focusing on inbound marketing strategies to attract, engage, and convert website visitors into customers. Its platform provides a comprehensive suite of applications including search engine optimization (SEO), blogging, marketing automation, customer relationship management (CRM), and analytics, utilizing a centralized database for personalized interactions. In our view, this approach fosters warmer prospect engagement compared to traditional methods like cold calling and email blasts. Over the years, the company has evolved from a small business CRM vendor to a comprehensive provider of marketing, sales and content management solutions for global SMBs. With an approximate 3% combined market share, a large customer base, robust partner network and extensive HubSpot suite, we believe the company is well positioned to capture additional market share in the large SMB front office applications industry, as well as expand in the upmarket segment (i.e., companies with 200 to 2,000 employees). Shares contributed to performance during the period, as the company reported better-than-expected operating results, noting strong quarterly execution against a difficult macroeconomic environment.

Detractors from Performance

The Health Care and Industrials sectors were the largest detractors from relative performance. Regarding individual positions, Magnolia Oil & Gas Corp.; Xometry, Inc.; HealthEquity Inc.; BILL Holdings, Inc.; and CareDx, Inc. were among the top detractors from absolute performance.

Xometry is a leading two-sided marketplace for on-demand manufacturing services. The company provides real-time access to global manufacturing demand and capacity, with sourcing and pricing available across a network of buyers and sellers. This marketplace enables buyers (e.g., engineers and product designers) to efficiently source manufacturing processes and sellers of manufacturing services to grow their businesses. Xometry’s AI-enabled technology platform is powered by proprietary machine learning algorithms, resulting in a sophisticated marketplace for manufacturing. During the period, the company reported weaker-than-expected revenues and revised their forward guidance below consensus. Management noted that suppliers accepted orders more quickly than usual on the Xometry platform due to a challenging macroeconomic environment, causing the proprietary algorithm to reduce market pricing, resulting in weaker revenue growth and gross margin compression. The company adjusted their proprietary algorithm in January and the company stated that it expects gross margins to improve throughout the year.

I thank you for putting your trust in Alger.

Sincerely,

Daniel C. Chung, CFA

Chief Executive Officer, Chief Investment Officer

Fred Alger Management, LLC

Investors cannot invest directly in an index. Index performance does not reflect the deduction for fees, expenses, or taxes.

This report and the financial statements contained herein are submitted for the general information of shareholders of the funds. This report is not authorized for distribution to prospective investors in a fund unless preceded or accompanied by an effective prospectus for the fund. Performance of funds discussed above represents the six-month period return of Class I shares.

The performance data quoted in this material represents past performance, which is not an indication or a guarantee of future results.

Standard performance results can be found on the following pages. The investment return and principal value of an investment in a Fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted. For performance data current to the most recent month-end, visit us at www.alger.com, or call us at (800) 992-3863.

The views and opinions of the funds’ management in this report are as of the date of the Shareholders’ Letter and are subject to change at any time subsequent to this date. There is no guarantee that any of the assumptions that formed the basis for the opinions stated herein are accurate or that they will materialize. Moreover, the information forming the basis for such assumptions is from sources believed to be reliable; however, there is no guarantee that such information is accurate. Any securities mentioned, whether owned in a fund or otherwise, are considered in the context of the construction of an overall portfolio of securities and therefore reference to them should not be construed as a recommendation or offer to purchase or sell any such security. Inclusion of such securities in a fund and transactions in such securities, if any, may be for a variety of reasons, including, without limitation, in response to cash flows, inclusion in a benchmark, and risk control. The reference to a specific security should also be understood in such context and not viewed as a statement that the security is a significant holding in a fund. Please refer to the Schedule of Investments for each fund which is included in this report for a complete list of fund holdings as of April 30, 2023. Securities mentioned in the Shareholders’ Letter, if not found in the Schedules of Investments, may have been held by the funds during the fiscal six-month period ended April 30, 2023.

Risk Disclosures

Alger Capital Appreciation Institutional Fund

Investing in the stock market involves risks, including the potential loss of principal. Growth stocks may be more volatile than other stocks as their prices tend to be higher in relation to their companies’ earnings and may be more sensitive to market, political, and economic developments. Local, regional or global events such as environmental or natural disasters, war, terrorism, pandemics, outbreaks of infectious diseases and similar public health threats, recessions, or other events could have a significant impact on investments. A significant portion of assets may be invested in securities of companies in related sectors, and may be similarly affected by economic, political, or market events and conditions and may be more vulnerable to unfavorable sector developments. Foreign securities involve special risks including currency fluctuations, inefficient trading, political and economic instability, and increased volatility. Active trading may increase transaction costs, brokerage commissions, and taxes, which can lower the return on investment. At times, cash may be a larger position in the portfolio and may underperform relative to equity securities.

Alger Focus Equity Fund

Investing in the stock market involves risks, including the potential loss of principal. Growth stocks may be more volatile than other stocks as their prices tend to be higher in relation to their companies’ earnings and may be more sensitive to market, political, and economic developments. Local, regional or global events such as environmental or natural disasters, war, terrorism, pandemics, outbreaks of infectious diseases and similar public health threats, recessions, or other events could have a significant impact on investments. A significant portion of assets may be invested in securities of companies in related sectors, and may be similarly affected by economic, political, or market events and conditions and may be more vulnerable to unfavorable sector developments. Foreign securities involve special risks including currency fluctuations, inefficient trading, political and economic instability, and increased volatility. Active trading may increase transaction costs, brokerage commissions, and taxes, which can lower the return on investment. At times, cash may be a larger position in the portfolio and may underperform relative to equity securities.

Alger Mid Cap Growth Institutional Fund

Investing in the stock market involves risks, including the potential loss of principal. Growth stocks may be more volatile than other stocks as their prices tend to be higher in relation to their companies’ earnings and may be more sensitive to market, political, and economic developments. Local, regional or global events such as environmental or natural disasters, war, terrorism, pandemics, outbreaks of infectious diseases and similar public health threats, recessions, or other events could have a significant impact on investments. A significant portion of assets may be invested in securities of companies in related sectors, and may be similarly affected by economic, political, or market events and conditions and may be more vulnerable to unfavorable sector developments. Investing in companies of medium capitalizations involves the risk that such issuers may have limited product lines or financial resources, lack management depth, or have limited liquidity. Foreign securities involve special risks including currency fluctuations, inefficient trading, political and economic instability, and increased volatility. Active trading may increase transaction costs, brokerage commissions, and taxes, which can lower the return on investment. At times, cash may be a larger position in the portfolio and may underperform relative to equity securities.

Alger Small Cap Growth Institutional Fund

Investing in the stock market involves risks, including the potential loss of principal. Growth stocks may be more volatile than other stocks as their prices tend to be higher in relation to their companies’ earnings and may be more sensitive to market, political, and economic developments. Local, regional or global events such as environmental or natural disasters, war, terrorism, pandemics, outbreaks of infectious diseases and similar public health threats, recessions, or other events could have a significant impact on investments. A significant portion of assets may be invested in securities of companies in related sectors, and may be similarly affected by economic, political, or market events and conditions and may be more vulnerable to unfavorable sector developments. Investing in companies of small and medium capitalizations involves the risk that such issuers may have limited product lines or financial resources, lack management depth, or have limited liquidity. Foreign securities involve special risks including currency fluctuations, inefficient trading, political and economic instability, and increased volatility. At times, cash may be a larger position in the portfolio and may underperform relative to equity securities.

For a more detailed discussion of the risks associated with a fund, please see the prospectus.

Before investing, carefully consider a fund’s investment objective, risks, charges, and expenses. For a prospectus and summary prospectus containing this and other information or for The Alger Institutional Funds’ most recent month-end performance data, visit www.alger.com, call (800) 992-3863 or consult your financial advisor. Read the prospectus and summary prospectus carefully before investing.

Distributor: Fred Alger & Company, LLC

NOT FDIC INSURED. NOT BANK GUARANTEED. MAY LOSE VALUE.

Definitions:

| ● | Earnings per share (EPS) is calculated as a company’s profit divided by the outstanding shares of its common stock. |

| ● | The Consumer Price Index (CPI) measures the monthly change in prices paid by U.S. consumers. The Bureau of Labor Statistics (BLS) calculates the CPI as a weighted average of prices for a basket of goods and services representative of aggregate U.S. consumer spending. |

| ● | The MSCI ACWI captures large- and mid-cap representation across developed markets and emerging markets countries. The index covers approximately 85% of the global equity opportunity set. |

| ● | The MSCI EAFE Index is designed to represent the performance of large and mid-cap securities across developed markets, including countries in Europe, Australasia and the Far East, excluding the U.S. and Canada. |

| ● | The MSCI Emerging Markets Index captures large-and mid-cap representation across Emerging Markets countries. The index covers approximately 85% of the free float-adjusted market capitalization in each country. |

| ● | The Russell 1000 Growth Index measures the performance of the large-cap growth segment of the U.S. equity universe. It includes those Russell 1000 companies with higher growth earning potential as defined by Russell’s leading style methodology. The Russell 1000 Growth Index is constructed to provide a comprehensive and unbiased barometer for the large-cap growth segment. |

| ● | The Russell 1000 Index measures the performance of the large-cap segment of the US equity universe. It is a subset of the Russell 3000 Index and includes approximately 1,000 of the largest securities based on a combination of their market cap and current index membership. |

| ● | The Russell 2000 Growth Index measures the performance of the small-cap growth segment of the U.S. equity universe. It includes those Russell 2000 companies with higher growth earning potential as defined by Russell’s leading style methodology. The Russell 2000 Growth Index is constructed to provide a comprehensive and unbiased barometer for the small-cap growth segment. |

| ● | The Russell 2000 Index measures the performance of the small-cap segment of the US equity universe. The Russell 2000 Index is constructed to provide a comprehensive and unbiased barometer of the small-cap segment. |

| ● | The Russell 3000 Growth Index combines the large-cap Russell 1000 Growth, the small-cap Russell 2000 Growth and the Russell Microcap Growth Index. It includes companies that are considered more growth oriented relative to the overall market as defined by Russell’s leading style methodology. The Russell 3000 Growth Index is constructed to provide a comprehensive, unbiased, and stable barometer of the growth opportunities within the broad market. |

| ● | The Russell 3000 Index measures the performance of the largest 3,000 US companies of the investable US equity market. The Russell 3000 Index is constructed to provide a comprehensive, unbiased and stable barometer of the broad market |

| ● | The Russell 3000 Value Index measures the performance of the broad value segment of the US equity value universe. It includes those Russell 3000 companies with lower price-to-book ratios and lower forecasted growth values. The Russell 3000 Value Index is constructed to provide a comprehensive, unbiased and stable barometer of the broad value market. |

| ● | The Russell Microcap Growth Index measures the performance of the microcap growth segment of the US equity market. It includes Russell Microcap companies with relatively higher price-to-book ratios, higher I/B/E/S forecast medium term (2 year) growth and higher sales per share historical growth (5 years). |

| ● | The Russell Microcap Index measures the performance of the microcap segment of the US equity market. The Russell Microcap Index is constructed to provide a comprehensive and unbiased barometer for the microcap segment trading on national exchanges. |

| ● | The Russell Midcap Growth Index measures the performance of the mid-cap growth segment of the U.S. equity universe. It includes those Russell Midcap Index companies with higher growth earning potential as defined by Russell’s leading style methodology. The Russell Midcap Growth Index is constructed to provide a comprehensive and unbiased barometer of the mid-cap growth market. |

| ● | The Russell Midcap Index measures the performance of the mid-cap segment of the US equity universe. The Russell Midcap Index is constructed to provide a comprehensive and unbiased barometer for the mid-cap segment. |

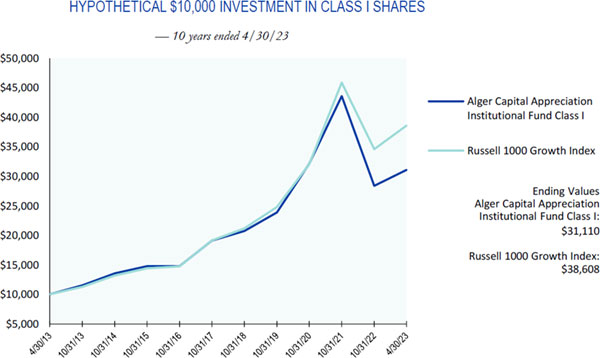

ALGER CAPITAL APPRECIATION INSTITUTIONAL FUND

Fund Highlights Through April 30, 2023 (Unaudited)

The chart above illustrates the change in value of a hypothetical $10,000 investment made in the Alger Capital Appreciation Institutional Fund Class I shares and the Russell 1000 Growth Index (an unmanaged index of common stocks) for the ten years ended April 30, 2023. Figures for the Alger Capital Appreciation Institutional Fund Class I shares and the Russell 1000 Growth Index include reinvestment of dividends. Figures for the Alger Capital Appreciation Institutional Fund Class I shares also include reinvestment of capital gains. Performance for the Alger Capital Appreciation Institutional Fund Class R, Class Y and Class Z-2 shares may vary from the results shown above due to differences in expenses each class bears. Investors cannot invest directly in any index. Index performance does not reflect deduction for fees, expenses, or taxes.

ALGER CAPITAL APPRECIATION INSTITUTIONAL FUND

Fund Highlights Through April 30, 2023 (Unaudited) (Continued)

PERFORMANCE COMPARISON AS OF 4/30/23

| AVERAGE ANNUAL TOTAL RETURNS |

| | 1 YEAR | 5 YEARS | 10 YEARS | |

| Class I | (2.78)% | 8.89% | 12.02% | |

| Class R | (3.21)% | 8.41% | 11.50% | |

| Russell 1000 Growth Index | 2.34% | 13.80% | 14.46% | |

| | | | | |

| | | | | |

| | | | Since | |

| | 1 YEAR | 5 YEARS | Inception | |

| Class Y (Inception 2/28/17) | (2.38)% | 9.33% | 11.56% | |

| Russell 1000 Growth Index | 2.34% | 13.80% | 14.86% | |

| | | | | |

| | | | | |

| | | | Since | |

| | 1 YEAR | 5 YEARS | Inception | |

| Class Z-2 (Inception 10/14/16) | (2.45)% | 9.25% | 12.28% | |

| Russell 1000 Growth Index | 2.34% | 13.80% | 15.75% | |

| | | | | |

The performance data quoted represents past performance, which is not an indication or a guarantee of future results. The Fund’s average annual total returns include changes in share price and reinvestment of dividends and capital gains. The chart and table above do not reflect the deduction of taxes that a shareholder would have paid on Fund distributions or on the redemption of Fund shares. Investment return and principal will fluctuate and the Fund’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance quoted. For updated performance, visit us at www.alger.com or call us at (800) 992-3863.

ALGER FOCUS EQUITY FUND

Fund Highlights Through April 30, 2023 (Unaudited)

The chart above illustrates the change in value of a hypothetical $10,000 investment made in the Alger Focus Equity Fund Class I shares and the Russell 1000 Growth Index (an unmanaged index of common stocks) for the ten years ended April 30, 2023. On October 15, 2018, Alger Capital Appreciation Focus Fund changed its name to Alger Focus Equity Fund. Figures for Alger Focus Equity Fund Class I shares and the Russell 1000 Growth Index include reinvestment of dividends. Figures for the Alger Focus Equity Fund Class I shares also include reinvestment of capital gains. Performance for Alger Focus Equity Fund Class A, Class C, Class Y and Class Z shares may vary from the results shown above due to differences in expenses and sales charges that those classes bear. Investors cannot invest directly in any index. Index performance does not reflect deduction for fees, expenses, or taxes.

ALGER FOCUS EQUITY FUND

Fund Highlights Through April 30, 2023 (Unaudited) (Continued)

PERFORMANCE COMPARISON AS OF 4/30/23

| AVERAGE ANNUAL TOTAL RETURNS |

| | 1 YEAR | 5 YEARS | 10 YEARS | |

| Class A | (6.42)% | 9.42% | 13.10% | |

| Class C | (2.98)% | 9.77% | 12.86% | |

| Class I | (1.22)% | 10.66% | 13.79% | |

| Class Z | (0.93)% | 10.97% | 14.10% | |

| Russell 1000 Growth Index | 2.34% | 13.80% | 14.46% | |

| | | | | |

| | | | | |

| | | | Since | |

| | 1 YEAR | 5 YEARS | Inception | |

| Class Y (Inception 2/28/17) | (0.87)% | 10.99% | 13.72% | |

| Russell 1000 Growth Index | 2.34% | 13.80% | 14.86% | |

| | | | | |

The performance data quoted represents past performance, which is not an indication or a guarantee of future results. The Fund’s average annual total returns include changes in share price and reinvestment of dividends and capital gains. Class A returns reflect the maximum initial sales charge and Class C returns reflect the applicable contingent deferred sales charge. The chart and table above do not reflect the deduction of taxes that a shareholder would have paid on Fund distributions or on the redemption of Fund shares. On October 15, 2018, the Fund changed its name from Alger Capital Appreciation Focus Fund to Alger Focus Equity Fund. Investment return and principal will fluctuate and the Fund’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance quoted. For updated performance, visit us at www.alger.com or call us at (800) 992-3863.

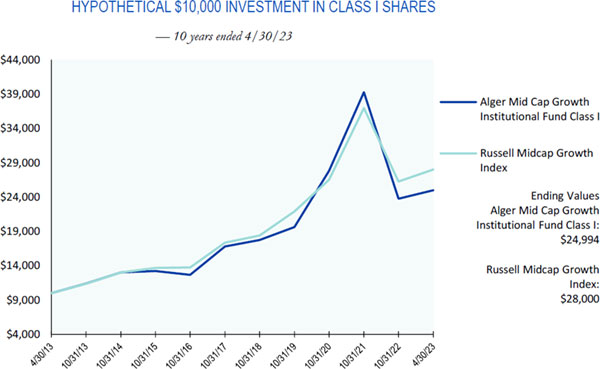

ALGER MID CAP GROWTH INSTITUTIONAL FUND

Fund Highlights Through April 30, 2023 (Unaudited)

The chart above illustrates the change in value of a hypothetical $10,000 investment made in the Alger Mid Cap Growth Institutional Fund Class I shares and the Russell Midcap Growth Index (an unmanaged index of common stocks) for the ten years ended April 30, 2023. Figures for Alger Mid Cap Growth Institutional Fund Class I shares and the Russell Midcap Growth Index include reinvestment of dividends. Figures for the Alger Mid Cap Growth Institutional Fund Class I shares also include reinvestment of capital gains. Performance for the Alger Mid Cap Growth Institutional Fund Class R and Class Z-2 shares may vary from the results shown above due to differences in expenses each class bears. Investors cannot invest directly in any index. Index performance does not reflect deduction for fees, expenses, or taxes.

ALGER MID CAP GROWTH INSTITUTIONAL FUND

Fund Highlights Through April 30, 2023 (Unaudited) (Continued)

PERFORMANCE COMPARISON AS OF 4/30/23

| AVERAGE ANNUAL TOTAL RETURNS |

| | 1 YEAR | 5 YEARS | 10 YEARS | |

| Class I | (2.43)% | 7.52% | 9.59% | |

| Class R | (2.88)% | 7.01% | 9.05% | |

| Russell Midcap Growth Index | 1.60% | 8.96% | 10.84% | |

| | | | | |

| | | | | |

| | | | Since | |

| | 1 YEAR | 5 YEARS | Inception | |

| Class Z-2 (Inception 10/14/16) | (1.99)% | 7.89% | 11.04% | |

| Russell Midcap Growth Index | 1.60% | 8.96% | 11.32% | |

| | | | | |

The performance data quoted represents past performance, which is not an indication or a guarantee of future results. The Fund’s average annual total returns include changes in share price and reinvestment of dividends and capital gains. The chart and table above do not reflect the deduction of taxes that a shareholder would have paid on Fund distributions or on the redemption of Fund shares. Investment return and principal will fluctuate and the Fund’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance quoted. For updated performance, visit us at www.alger.com or call us at (800) 992-3863.

ALGER SMALL CAP GROWTH INSTITUTIONAL FUND

Fund Highlights Through April 30, 2023 (Unaudited)

The chart above illustrates the change in value of a hypothetical $10,000 investment made in the Alger Small Cap Growth Institutional Fund Class I shares and the Russell 2000 Growth Index (an unmanaged index of common stocks) for the ten years ended April 30, 2023. Figures for the Alger Small Cap Growth Institutional Fund Class I shares and the Russell 2000 Growth Index include reinvestment of dividends. Figures for the Alger Small Cap Growth Institutional Fund Class I shares also include reinvestment of capital gains. Performance for the Alger Small Cap Growth Institutional Fund Class R and Class Z-2 shares may vary from the results shown above due to differences in expenses each class bears. Investors cannot invest directly in any index. Index performance does not reflect deduction for fees, expenses, or taxes.

ALGER SMALL CAP GROWTH INSTITUTIONAL FUND

Fund Highlights Through April 30, 2023 (Unaudited) (Continued)

PERFORMANCE COMPARISON AS OF 4/30/23

| AVERAGE ANNUAL TOTAL RETURNS |

| | 1 YEAR | 5 YEARS | 10 YEARS | |

| Class I | (11.63)% | 4.64% | 7.83% | |

| Class R | (12.10)% | 4.14% | 7.32% | |

| Russell 2000 Growth Index | 0.72% | 4.00% | 8.44% | |

| | | | | |

| | | | | |

| | | | Since | |

| | 1 YEAR | 5 YEARS | Inception | |

| Class Z-2 (Inception 8/1/16) | (11.31)% | 4.99% | 9.34% | |

| Russell 2000 Growth Index | 0.72% | 4.00% | 7.33% | |

| | | | | |

The performance data quoted represents past performance, which is not an indication or a guarantee of future results. The Fund’s average annual total returns include changes in share price and reinvestment of dividends and capital gains. The chart and table above do not reflect the deduction of taxes that a shareholder would have paid on Fund distributions or on the redemption of Fund shares. Investment return and principal will fluctuate and the Fund’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance quoted. For updated performance, visit us at www.alger.com or call us at (800) 992-3863.

PORTFOLIO SUMMARY†

April 30, 2023 (Unaudited)

| | Alger Capital | | | Alger Small Cap |

| | Appreciation | Alger Focus Equity | Alger Mid Cap Growth | Growth Institutional |

| SECTORS | Institutional Fund | Fund | Institutional Fund | Fund |

| Communication Services | 10.1 | % | 10.1 | % | 4.3 | % | 4.0 | % |

| Consumer Discretionary | 17.4 | | 15.2 | | 15.0 | | 10.8 | |

| Consumer Staples | 0.0 | | 0.0 | | 1.0 | | 6.3 | |

| Energy | 3.8 | | 3.4 | | 3.8 | | 5.0 | |

| Financials | 7.7 | | 8.9 | | 4.6 | | 2.4 | |

| Healthcare | 16.0 | | 14.3 | | 17.9 | | 29.5 | |

| Industrials | 6.3 | | 7.9 | | 16.9 | | 7.0 | |

| Information Technology | 36.2 | | 32.8 | | 27.9 | | 31.4 | |

| Materials | 2.1 | | 2.7 | | 3.4 | | 1.7 | |

| Real Estate | 0.0 | | 0.0 | | 3.5 | | 1.6 | |

| Short-Term Investments and Net Other Assets | 0.4 | | 4.7 | | 1.7 | | 0.3 | |

| | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % |

† Based on net assets for each Fund.

THE ALGER INSTITUTIONAL FUNDS

ALGER CAPITAL APPRECIATION INSTITUTIONAL FUND

Schedule of Investments April 30, 2023 (Unaudited)

| COMMON STOCKS—99.3% | | SHARES | | | VALUE | |

| ADVERTISING—0.8% | | | | | | | | |

| The Trade Desk, Inc., Cl. A* | | | 240,238 | | | $ | 15,456,913 | |

| AEROSPACE & DEFENSE—3.5% | | | | | | | | |

| HEICO Corp. | | | 99,930 | | | | 16,852,195 | |

| TransDigm Group, Inc. | | | 71,832 | | | | 54,951,480 | |

| | | | | | | | 71,803,675 | |

| APPAREL ACCESSORIES & LUXURY GOODS—1.3% | | | | | | | | |

| LVMH Moet Hennessy Louis Vuitton SE | | | 27,263 | | | | 26,223,770 | |

| APPAREL RETAIL—0.3% | | | | | | | | |

| The TJX Cos., Inc. | | | 64,974 | | | | 5,121,251 | |

| APPLICATION SOFTWARE—4.3% | | | | | | | | |

| Adobe, Inc.* | | | 34,144 | | | | 12,891,409 | |

| Cadence Design Systems, Inc.* | | | 69,050 | | | | 14,462,522 | |

| Datadog, Inc., Cl. A* | | | 162,793 | | | | 10,968,992 | |

| Intuit, Inc. | | | 82,170 | | | | 36,479,372 | |

| Salesforce, Inc.* | | | 66,214 | | | | 13,134,871 | |

| | | | | | | | 87,937,166 | |

| AUTOMOBILE MANUFACTURERS—1.1% | | | | | | | | |

| Tesla, Inc.* | | | 143,359 | | | | 23,555,317 | |

| AUTOMOTIVE PARTS & EQUIPMENT—0.1% | | | | | | | | |

| Mobileye Global, Inc., Cl. A* | | | 29,491 | | | | 1,110,041 | |

| BIOTECHNOLOGY—7.0% | | | | | | | | |

| AbbVie, Inc. | | | 174,084 | | | | 26,307,574 | |

| Biogen, Inc.* | | | 50,103 | | | | 15,242,836 | |

| Natera, Inc.* | | | 711,517 | | | | 36,088,142 | |

| Prometheus Biosciences, Inc.* | | | 142,821 | | | | 27,700,133 | |

| Regeneron Pharmaceuticals, Inc.* | | | 13,140 | | | | 10,535,521 | |

| Vaxcyte, Inc.* | | | 412,593 | | | | 17,671,358 | |

| Vertex Pharmaceuticals, Inc.* | | | 31,837 | | | | 10,847,821 | |

| | | | | | | | 144,393,385 | |

| BROADLINE RETAIL—8.0% | | | | | | | | |

| Amazon.com, Inc.* | | | 1,018,236 | | | | 107,372,986 | |

| MercadoLibre, Inc.* | | | 44,982 | | | | 57,464,055 | |

| | | | | | | | 164,837,041 | |

| CARGO GROUND TRANSPORTATION—0.4% | | | | | | | | |

| Old Dominion Freight Line, Inc. | | | 23,158 | | | | 7,419,592 | |

| CASINOS & GAMING—3.6% | | | | | | | | |

| Flutter Entertainment PLC* | | | 111,723 | | | | 22,324,219 | |

| Las Vegas Sands Corp.* | | | 520,735 | | | | 33,248,930 | |

| MGM Resorts International | | | 407,995 | | | | 18,327,135 | |

| | | | | | | | 73,900,284 | |

| COMMUNICATIONS EQUIPMENT—0.7% | | | | | | | | |

| Arista Networks, Inc.* | | | 93,518 | | | | 14,977,843 | |

| CONSTRUCTION MACHINERY & HEAVY TRANSPORTATION EQUIPMENT—0.5% | | | | | | |

| |

| Wabtec Corp. | | | 115,047 | | | | 11,236,640 | |

| CONSTRUCTION MATERIALS—1.3% | | | | | | | | |

| Martin Marietta Materials, Inc. | | | 70,756 | | | | 25,698,579 | |

| COPPER—0.1% | | | | | | | | |

| Freeport-McMoRan, Inc. | | | 77,979 | | | | 2,956,184 | |

THE ALGER INSTITUTIONAL FUNDS

ALGER CAPITAL APPRECIATION INSTITUTIONAL FUND

Schedule of Investments April 30, 2023 (Unaudited) (Continued)

| COMMON STOCKS—99.3% (CONT.) | | SHARES | | | VALUE | |

| DIVERSIFIED BANKS—1.0% | | | | | | | | |

| JPMorgan Chase & Co. | | | 149,022 | | | $ | 20,600,801 | |

| ELECTRICAL COMPONENTS & EQUIPMENT—0.3% | | | | | | | | |

| Eaton Corp. PLC | | | 31,382 | | | | 5,244,560 | |

| ENVIRONMENTAL & FACILITIES SERVICES—1.1% | | | | | | | | |

| GFL Environmental, Inc. | | | 329,855 | | | | 11,973,736 | |

| Waste Management, Inc. | | | 62,134 | | | | 10,317,351 | |

| | | | | | | | 22,291,087 | |

| FINANCIAL EXCHANGES & DATA—2.1% | | | | | | | | |

| CME Group, Inc., Cl. A | | | 68,582 | | | | 12,740,478 | |

| S&P Global, Inc. | | | 85,196 | | | | 30,890,366 | |

| | | | | | | | 43,630,844 | |

| FOOTWEAR—0.9% | | | | | | | | |

| NIKE, Inc., Cl. B | | | 137,758 | | | | 17,456,694 | |

| HEALTHCARE DISTRIBUTORS—0.5% | | | | | | | | |

| McKesson Corp. | | | 30,137 | | | | 10,977,101 | |

| HEALTHCARE EQUIPMENT—2.9% | | | | | | | | |

| Boston Scientific Corp.* | | | 439,489 | | | | 22,906,167 | |

| Dexcom, Inc.* | | | 94,480 | | | | 11,464,203 | |

| Intuitive Surgical, Inc.* | | | 80,776 | | | | 24,331,347 | |

| | | | | | | | 58,701,717 | |

| HEALTHCARE FACILITIES—1.1% | | | | | | | | |

| Acadia Healthcare Co., Inc.* | | | 304,303 | | | | 21,998,064 | |

| HOTELS RESORTS & CRUISE LINES—1.6% | | | | | | | | |

| Booking Holdings, Inc.* | | | 5,892 | | | | 15,827,738 | |

| Trip.com Group Ltd.#,* | | | 503,066 | | | | 17,863,874 | |

| | | | | | | | 33,691,612 | |

| INTERACTIVE HOME ENTERTAINMENT—0.0% | | | | | | | | |

| Roblox Corp., Cl. A* | | | 28,525 | | | | 1,015,490 | |

| INTERACTIVE MEDIA & SERVICES—5.8% | | | | | | | | |

| Alphabet, Inc., Cl. C* | | | 660,122 | | | | 71,438,403 | |

| Meta Platforms, Inc., Cl. A* | | | 195,987 | | | | 47,099,596 | |

| | | | | | | | 118,537,999 | |

| INTERNET SERVICES & INFRASTRUCTURE—0.2% | | | | | | | | |

| MongoDB, Inc., Cl. A* | | | 16,704 | | | | 4,008,292 | |

| INVESTMENT BANKING & BROKERAGE—0.1% | | | | | | | | |

| LPL Financial Holdings, Inc. | | | 11,745 | | | | 2,452,826 | |

| LIFE SCIENCES TOOLS & SERVICES—1.3% | | | | | | | | |

| Charles River Laboratories International, Inc.* | | | 24,127 | | | | 4,587,025 | |

| Danaher Corp. | | | 94,929 | | | | 22,489,630 | |

| | | | | | | | 27,076,655 | |

| MANAGED HEALTHCARE—1.9% | | | | | | | | |

| UnitedHealth Group, Inc. | | | 80,798 | | | | 39,759,888 | |

| MOVIES & ENTERTAINMENT—3.5% | | | | | | | | |

| Liberty Media Corp. Series C Liberty Formula One* | | | 161,462 | | | | 11,655,942 | |

| Live Nation Entertainment, Inc.* | | | 132,969 | | | | 9,012,639 | |

| Netflix, Inc.* | | | 94,557 | | | | 31,197,191 | |

| The Walt Disney Co.* | | | 192,404 | | | | 19,721,410 | |

| | | | | | | 71,587,182 | |

THE ALGER INSTITUTIONAL FUNDS

ALGER CAPITAL APPRECIATION INSTITUTIONAL FUND

Schedule of Investments April 30, 2023 (Unaudited) (Continued)

| COMMON STOCKS—99.3% (CONT.) | | SHARES | | | VALUE | |

| OIL & GAS EQUIPMENT & SERVICES—1.1% | | | | | | | | |

| Schlumberger Ltd. | | | 452,341 | | | $ | 22,323,028 | |

| OIL & GAS EXPLORATION & PRODUCTION—2.2% | | | | | | | | |

| Diamondback Energy, Inc. | | | 147,408 | | | | 20,961,417 | |

| Hess Corp. | | | 52,845 | | | | 7,665,696 | |

| Pioneer Natural Resources Co. | | | 71,840 | | | | 15,628,792 | |

| | | | | | | | 44,255,905 | |

| OIL & GAS STORAGE & TRANSPORTATION—0.5% | | | | | | | | |

| Cheniere Energy, Inc. | | | 72,822 | | | | 11,141,766 | |

| PASSENGER GROUND TRANSPORTATION—0.5% | | | | | | | | |

| Uber Technologies, Inc.* | | | 354,520 | | | | 11,007,846 | |

| PHARMACEUTICALS—1.3% | | | | | | | | |

| AstraZeneca PLC# | | | 204,968 | | | | 15,007,757 | |

| Catalent, Inc.* | | | 55,588 | | | | 2,786,071 | |

| Eli Lilly & Co. | | | 15,669 | | | | 6,202,730 | |

| Reata Pharmaceuticals, Inc., Cl. A* | | | 20,443 | | | | 2,020,995 | |

| | | | | | | | 26,017,553 | |

| PROPERTY & CASUALTY INSURANCE—0.5% | | | | | | | | |

| The Progressive Corp. | | | 78,252 | | | | 10,673,573 | |

| RESTAURANTS—0.5% | | | | | | | | |

| Yum China Holdings, Inc. | | | 170,808 | | | | 10,450,033 | |

| SEMICONDUCTORS—9.2% | | | | | | | | |

| Advanced Micro Devices, Inc.* | | | 172,928 | | | | 15,454,575 | |

| First Solar, Inc.* | | | 50,273 | | | | 9,178,844 | |

| Marvell Technology, Inc. | | | 786,990 | | | | 31,070,365 | |

| NVIDIA Corp. | | | 381,352 | | | | 105,821,367 | |

| ON Semiconductor Corp.* | | | 119,098 | | | | 8,570,292 | |

| Taiwan Semiconductor Manufacturing Co., Ltd.# | | | 206,837 | | | | 17,436,359 | |

| | | | | | | | 187,531,802 | |

| SPECIALTY CHEMICALS—0.7% | | | | | | | | |

| Albemarle Corp. | | | 75,862 | | | | 14,069,366 | |

| SYSTEMS SOFTWARE—14.3% | | | | | | | | |

| Microsoft Corp. | | | 853,109 | | | | 262,126,271 | |

| Oracle Corp. | | | 104,288 | | | | 9,878,159 | |

| Palo Alto Networks, Inc.* | | | 59,641 | | | | 10,882,097 | |

| ServiceNow, Inc.* | | | 22,206 | | | | 10,201,881 | |

| | | | | | | | 293,088,408 | |

| TECHNOLOGY HARDWARE STORAGE & PERIPHERALS—7.2% | | | | | | | | |

| Apple, Inc. | | | 865,978 | | | | 146,939,147 | |

| TRANSACTION & PAYMENT PROCESSING SERVICES—4.0% | | | | | | | | |

| PayPal Holdings, Inc.* | | | 126,813 | | | | 9,637,788 | |

| Visa, Inc., Cl. A | | | 313,112 | | | | 72,870,556 | |

| | | | | | | | 82,508,344 | |

| TOTAL COMMON STOCKS | | | | | | |

| |

| (Cost $1,312,698,732) | | | | | | | 2,035,665,264 | |

THE ALGER INSTITUTIONAL FUNDS

ALGER CAPITAL APPRECIATION INSTITUTIONAL FUND

Schedule of Investments April 30, 2023 (Unaudited) (Continued)

| PREFERRED STOCKS—0.1% | | SHARES | | | VALUE | |

| DATA PROCESSING & OUTSOURCED SERVICES—0.1% | | | | | | | | |

| Chime Financial, Inc., Series G*,@,(a) | | | 38,919 | | | $ | 1,673,906 | |

| (Cost $2,688,128) | | | | | | | 1,673,906 | |

| SPECIAL PURPOSE VEHICLE—0.2% | | | | | | VALUE | |

| DATA PROCESSING & OUTSOURCED SERVICES—0.2% | | | | | | | | |

| Crosslink Ventures Capital C, LLC, Cl. A*,@,(a),(b) | | | | | | | 3,210,054 | |

| (Cost $3,075,000) | | | | | | | 3,210,054 | |

| Total Investments | | | | | | | | |

| (Cost $1,318,461,860) | | | 99.6 | % | | $ | 2,040,549,224 | |

| Affiliated Securities (Cost $3,075,000) | | | | | | | 3,210,054 | |

| Unaffiliated Securities (Cost $1,315,386,860) | | | | | | | 2,037,339,170 | |

| Other Assets in Excess of Liabilities | | | 0.4 | % | | | 8,664,429 | |

| NET ASSETS | | | 100.0 | % | | $ | 2,049,213,653 | |

| # | American Depositary Receipts. |

| (a) | Security is valued in good faith at fair value determined using significant unobservable inputs pursuant to procedures established by the Valuation Designee (as defined in Note 2). |

| (b) | Deemed an affiliate of the Fund in accordance with Section 2(a)(3) of the Investment Company Act of 1940. See Note 11 - Affiliated Securities. |

| * | Non-income producing security. |

| @ | Restricted security - Investment in security not registered under the Securities Act of 1933. Sales or transfers of the investment may be restricted only to qualified buyers. |

| Security | | Acquisition

Date(s) | | | Acquisition

Cost | | | % of net assets

(Acquisition

Date) | | | Market

Value | | | % of net assets

as of

4/30/2023 | |

| Chime Financial, Inc., Series G | | 8/24/21 | | | $ | 2,688,128 | | | | 0.06 | % | | $ | 1,673,906 | | | | 0.08 | % |

| Crosslink Ventures Capital C, LLC, Cl. A | | 10/2/20 | | | | 3,075,000 | | | | 0.08 | % | | | 3,210,054 | | | | 0.16 | % |

| Total | | |

| | | | | | | | | | | $ | 4,883,960 | | | | 0.24 | % |

See Notes to Financial Statements.

THE ALGER INSTITUTIONAL FUNDS | ALGER FOCUS EQUITY FUND

Schedule of Investments April 30, 2023 (Unaudited)

| COMMON STOCKS—95.3% | | SHARES | | | VALUE | |

| ADVERTISING—0.7% | | | | | | | | |

| The Trade Desk, Inc., Cl. A* | | | 132,943 | | | $ | 8,553,553 | |

| AEROSPACE & DEFENSE—3.5% | | | | | | | | |

| TransDigm Group, Inc. | | | 52,889 | | | | 40,460,085 | |

| APPAREL ACCESSORIES & LUXURY GOODS—1.3% | | | | | | | | |

| LVMH Moet Hennessy Louis Vuitton SE | | | 15,944 | | | | 15,336,236 | |

| APPLICATION SOFTWARE—3.0% | | | | | | | | |

| Datadog, Inc., Cl. A* | | | 102,796 | | | | 6,926,394 | |

| Intuit, Inc. | | | 62,326 | | | | 27,669,628 | |

| | | | | | | | 34,596,022 | |

| AUTOMOBILE MANUFACTURERS—1.1% | | | | | | | | |

| Tesla, Inc.* | | | 78,085 | | | | 12,830,146 | |

| AUTOMOTIVE PARTS & EQUIPMENT—0.3% | | | | | | | | |

| Mobileye Global, Inc., Cl. A* | | | 95,406 | | | | 3,591,082 | |

| BIOTECHNOLOGY—5.4% | | | | | | | | |

| AbbVie, Inc. | | | 105,136 | | | | 15,888,152 | |

| Biogen, Inc.* | | | 30,460 | | | | 9,266,846 | |

| Natera, Inc.* | | | 500,216 | | | | 25,370,956 | |

| Vaxcyte, Inc.* | | | 272,559 | | | | 11,673,702 | |

| | | | | | | | 62,199,656 | |

| BROADLINE RETAIL—8.0% | | | | | | | | |

| Amazon.com, Inc.* | | | 545,373 | | | | 57,509,583 | |

| MercadoLibre, Inc.* | | | 27,795 | | | | 35,507,834 | |

| | | | | | | | 93,017,417 | |

| CASINOS & GAMING—3.4% | | | | | | | | |

| Flutter Entertainment PLC* | | | 134,676 | | | | 26,910,632 | |

| MGM Resorts International | | | 270,921 | | | | 12,169,771 | |

| | | | | | | | 39,080,403 | |

| COMMUNICATIONS EQUIPMENT—0.8% | | | | | | | | |

| Arista Networks, Inc.* | | | 60,290 | | | | 9,656,046 | |

| CONSTRUCTION MACHINERY & HEAVY TRANSPORTATION EQUIPMENT—1.2% | | | | | | | | |

| Wabtec Corp. | | | 145,397 | | | | 14,200,925 | |

| CONSTRUCTION MATERIALS—1.9% | | | | | | | | |

| Martin Marietta Materials, Inc. | | | 60,273 | | | | 21,891,154 | |

| DIVERSIFIED BANKS—1.0% | | | | | | | | |

| JPMorgan Chase & Co. | | | 85,098 | | | | 11,763,948 | |

| ELECTRICAL COMPONENTS & EQUIPMENT—0.5% | | | | | | | | |

| Eaton Corp., PLC | | | 31,987 | | | | 5,345,667 | |

| ENVIRONMENTAL & FACILITIES SERVICES—2.0% | | | | | | | | |

| GFL Environmental, Inc. | | | 656,770 | | | | 23,840,751 | |

| FINANCIAL EXCHANGES & DATA—3.1% | | | | | | | | |

| CME Group, Inc., Cl. A | | | 71,127 | | | | 13,213,263 | |

| S&P Global, Inc. | | | 62,227 | | | | 22,562,266 | |

| | | | | | | | 35,775,529 | |

| HEALTHCARE DISTRIBUTORS—0.6% | | | | | | | | |

| McKesson Corp. | | | 18,179 | | | | 6,621,519 | |

THE ALGER INSTITUTIONAL FUNDS | ALGER FOCUS EQUITY FUND

Schedule of Investments April 30, 2023 (Unaudited) (Continued)

| COMMON STOCKS—95.3% (CONT.) | | SHARES | | | VALUE | |

| HEALTHCARE EQUIPMENT—2.8% | | | | | | | | |

| Boston Scientific Corp.* | | | 271,899 | | | $ | 14,171,376 | |

| TransMedics Group, Inc.* | | | 226,854 | | | | 17,944,151 | |

| | | | | | | | 32,115,527 | |

| HEALTHCARE FACILITIES—1.1% | | | | | | | | |

| Acadia Healthcare Co., Inc.* | | | 174,808 | | | | 12,636,870 | |

| HOTELS RESORTS & CRUISE LINES—1.1% | | | | | | | | |

| Trip.com Group Ltd.#,* | | | 351,582 | | | | 12,484,677 | |

| INTERACTIVE MEDIA & SERVICES—6.2% | | | | | | | | |

| Alphabet, Inc., Cl. C* | | | 362,365 | | | | 39,215,140 | |

| Meta Platforms, Inc., Cl. A* | | | 134,637 | | | | 32,355,964 | |

| | | | | | | | 71,571,104 | |

| INVESTMENT BANKING & BROKERAGE—0.3% | | | | | | | | |

| LPL Financial Holdings, Inc. | | | 16,214 | | | | 3,386,132 | |

| LIFE SCIENCES TOOLS & SERVICES—1.1% | | | | | | | | |

| Danaher Corp. | | | 52,446 | | | | 12,424,982 | |

| MANAGED HEALTHCARE—2.0% | | | | | | | | |

| UnitedHealth Group, Inc. | | | 47,536 | | | | 23,391,990 | |

| METAL, GLASS & PLASTIC CONTAINERS—0.8% | | | | | | | | |

| Ball Corp. | | | 166,257 | | | | 8,841,547 | |

| MOVIES & ENTERTAINMENT—3.2% | | | | | | | | |

| Liberty Media Corp. Series C Liberty Formula One* | | | 271,711 | | | | 19,614,817 | |

| Netflix, Inc.* | | | 54,200 | | | | 17,882,206 | |

| | | | | | | | 37,497,023 | |

| OIL & GAS EQUIPMENT & SERVICES—1.0% | | | | | | | | |

| Schlumberger Ltd. | | | 243,292 | | | | 12,006,460 | |

| OIL & GAS EXPLORATION & PRODUCTION—2.4% | | | | | | | | |

| EOG Resources, Inc. | | | 237,973 | | | | 28,430,634 | |

| PASSENGER GROUND TRANSPORTATION—0.7% | | | | | | | | |

| Uber Technologies, Inc.* | | | 255,997 | | | | 7,948,707 | |

| PHARMACEUTICALS—1.3% | | | | | | | | |

| AstraZeneca PLC# | | | 203,319 | | | | 14,887,017 | |

| SEMICONDUCTORS—8.7% | | | | | | | | |

| Advanced Micro Devices, Inc.* | | | 101,844 | | | | 9,101,798 | |

| First Solar, Inc.* | | | 27,751 | | | | 5,066,778 | |

| Marvell Technology, Inc. | | | 470,666 | | | | 18,581,894 | |

| NVIDIA Corp. | | | 225,783 | | | | 62,652,525 | |

| ON Semiconductor Corp.* | | | 74,894 | | | | 5,389,372 | |

| | | | | | | | 100,792,367 | |

| SYSTEMS SOFTWARE—13.4% | | | | | | | | |

| Microsoft Corp. | | | 485,324 | | | | 149,120,652 | |

| ServiceNow, Inc.* | | | 13,418 | | | | 6,164,498 | |

| | | | | | | | 155,285,150 | |

| TECHNOLOGY HARDWARE STORAGE & PERIPHERALS—6.9% | | | | | | | | |

| Apple, Inc. | | | 471,571 | | | | 80,016,167 | |

THE ALGER INSTITUTIONAL FUNDS | ALGER FOCUS EQUITY FUND

Schedule of Investments April 30, 2023 (Unaudited) (Continued)

| COMMON STOCKS—95.3% (CONT.) | | SHARES | | | VALUE | |

| TRANSACTION & PAYMENT PROCESSING SERVICES—4.5% | | | | | | | | |

| PayPal Holdings, Inc.* | | | 87,788 | | | $ | 6,671,888 | |

| Visa, Inc., Cl. A | | | 198,307 | | | | 46,151,988 | |

| | | | | | | | 52,823,876 | |

| TOTAL COMMON STOCKS | | | | | | |

| |

| (Cost $855,114,159) | | | | | | | 1,105,300,369 | |

| PREFERRED STOCKS—0.0% | | SHARES | | | VALUE | |

| BIOTECHNOLOGY—0.0% | | | | | | | | |

| Prosetta Biosciences, Inc., Series D*,@,(a),(b) | | | 76,825 | | | | — | |

| (Cost $345,713) | | | | | | | — | |

| SHORT—TERM INVESTMENTS—3.1% | | SHARES | | | VALUE | |

| U.S. GOVERNMENT—3.1% | | | | | | |

| |

| U.S. Treasury Bill, 0.0%, 5/2/23 | | | 36,000,000 | | | | 35,996,632 | |

| (Cost $35,996,632) | | | | | | | 35,996,632 | |

| Total Investments | | | | | | | | |

| (Cost $891,456,504) | | | 98.4 | % | | $ | 1,141,297,001 | |

| Affiliated Securities (Cost $345,713) | | | | | | | — | |

| Unaffiliated Securities (Cost $891,110,791) | | | | | | | 1,141,297,001 | |

| Other Assets in Excess of Liabilities | | | 1.6 | % | | | 19,082,170 | |

| NET ASSETS | | | 100.0 | % | | $ | 1,160,379,171 | |

| # | American Depositary Receipts. |

| (a) | Deemed an affiliate of the Fund in accordance with Section 2(a)(3) of the Investment Company Act of 1940. See Note 11 - Affiliated Securities. |

| (b) | Security is valued in good faith at fair value determined using significant unobservable inputs pursuant to procedures established by the Valuation Designee (as defined in Note 2). |

| * | Non-income producing security. |

| @ | Restricted security - Investment in security not registered under the Securities Act of 1933. Sales or transfers of the investment may be restricted only to qualified buyers. |

| | | | | | | | |

| | | | | |

| |

| | |

| | |

| | |

| | |

| | |

| |

| Security | | Acquisition

Date(s) | | | Acquisition

Cost | | | % of net assets

(Acquisition

Date) | | | Market

Value | | | % of net assets

as of

4/30/2023 | |

| Prosetta Biosciences, Inc., Series D | | 2/6/15 | | | $ | 345,713 | | | | 0.80 | % | | $ | 0 | | | | 0.00 | % |

| Total | | | | | | | | | | | | | | $ | 0 | | | | 0.00 | % |

See Notes to Financial Statements.

THE ALGER INSTITUTIONAL FUNDS | ALGER MID CAP GROWTH INSTITUTIONAL FUND

Schedule of Investments April 30, 2023 (Unaudited)

| COMMON STOCKS—96.4% | | SHARES | | | VALUE | |

| ADVERTISING—2.1% | | | | | | | | |

| The Trade Desk, Inc., Cl. A* | | | 18,952 | | | $ | 1,219,372 | |

| AEROSPACE & DEFENSE—4.7% | | | | | | | | |

| HEICO Corp. | | | 7,444 | | | | 1,255,356 | |

| TransDigm Group, Inc. | | | 1,969 | | | | 1,506,285 | |

| | | | | | | | 2,761,641 | |

| APPAREL ACCESSORIES & LUXURY GOODS—1.4% | | | | | | | | |

| Lululemon Athletica, Inc.* | | | 2,134 | | | | 810,771 | |

| APPAREL RETAIL—0.5% | | | | | | | | |

| Burlington Stores, Inc.* | | | 1,496 | | | | 288,444 | |

| APPLICATION SOFTWARE—13.1% | | | | | | | | |

| Cadence Design Systems, Inc.* | | | 7,104 | | | | 1,487,933 | |

| Constellation Software, Inc. | | | 916 | | | | 1,793,000 | |

| Datadog, Inc., Cl. A* | | | 9,228 | | | | 621,783 | |

| Guidewire Software, Inc.* | | | 13,519 | | | | 1,030,013 | |

| Manhattan Associates, Inc.* | | | 5,921 | | | | 980,991 | |

| Paycom Software, Inc.* | | | 2,763 | | | | 802,292 | |

| The Descartes Systems Group, Inc.* | | | 11,763 | | | | 932,184 | |

| | | | | | | | 7,648,196 | |

| AUTOMOTIVE PARTS & EQUIPMENT—0.6% | | | | | | | | |

| Mobileye Global, Inc., Cl. A* | | | 8,632 | | | | 324,909 | |

| AUTOMOTIVE RETAIL—2.9% | | | | | | | | |

| AutoZone, Inc.* | | | 623 | | | | 1,659,242 | |

| BIOTECHNOLOGY—4.6% | | | | | | | | |

| Apellis Pharmaceuticals, Inc.* | | | 4,356 | | | | 363,421 | |

| Celldex Therapeutics, Inc.* | | | 10,445 | | | | 328,391 | |

| Natera, Inc.* | | | 22,654 | | | | 1,149,011 | |

| Prometheus Biosciences, Inc.* | | | 3,716 | | | | 720,718 | |

| Vaxcyte, Inc.* | | | 3,354 | | | | 143,652 | |

| | | | | | | | 2,705,193 | |

| BUILDING PRODUCTS—0.5% | | | | | | | | |

| Trex Co., Inc.* | | | 5,548 | | | | 303,254 | |

| CARGO GROUND TRANSPORTATION—1.8% | | | | | | | | |

| Old Dominion Freight Line, Inc. | | | 3,261 | | | | 1,044,792 | |

| CONSTRUCTION & ENGINEERING—1.5% | | | | | | | | |

| WillScot Mobile Mini Holdings Corp.* | | | 19,497 | | | | 885,164 | |

| CONSTRUCTION MACHINERY & HEAVY TRANSPORTATION EQUIPMENT—1.4% | | | | | | | | |

| Wabtec Corp. | | | 8,572 | | | | 837,227 | |

| CONSTRUCTION MATERIALS—2.0% | | | | | | | | |

| Martin Marietta Materials, Inc. | | | 3,249 | | | | 1,180,037 | |

| CONSUMER STAPLES MERCHANDISE RETAIL—1.0% | | | | | | | | |

| BJ’s Wholesale Club Holdings, Inc.* | | | 7,525 | | | | 574,684 | |

| DIVERSIFIED METALS & MINING—0.4% | | | | | | | | |

| MP Materials Corp.* | | | 10,314 | | | | 223,504 | |

| ELECTRONIC COMPONENTS—1.7% | | | | | | | | |

| Amphenol Corp., Cl. A | | | 13,142 | | | | 991,827 | |

| ELECTRONIC EQUIPMENT & INSTRUMENTS—1.8% | | | | | | | | |

| Novanta, Inc.* | | | 6,727 | | | | 1,028,155 | |

THE ALGER INSTITUTIONAL FUNDS | ALGER MID CAP GROWTH INSTITUTIONAL FUND

Schedule of Investments April 30, 2023 (Unaudited) (Continued)

| COMMON STOCKS—96.4% (CONT.) | | SHARES | | | VALUE | |

| ENVIRONMENTAL & FACILITIES SERVICES—3.6% | | | | | | | | |

| GFL Environmental, Inc. | | | 58,362 | | | $ | 2,118,541 | |

| FINANCIAL EXCHANGES & DATA—2.5% | | | | | | | | |

| MSCI, Inc., Cl. A | | | 2,980 | | | | 1,437,701 | |

| HEALTHCARE EQUIPMENT—3.4% | | | | | | | | |

| IDEXX Laboratories, Inc.* | | | 2,114 | | | | 1,040,426 | |

| Insulet Corp.* | | | 3,014 | | | | 958,573 | |

| | | | | | | | 1,998,999 | |

| HEALTHCARE FACILITIES—1.8% | | | | | | | | |

| Acadia Healthcare Co., Inc.* | | | 14,705 | | | | 1,063,024 | |

| HEALTHCARE TECHNOLOGY—1.7% | | | | | | | | |

| Veeva Systems, Inc., Cl. A* | | | 5,593 | | | | 1,001,594 | |

| HOME IMPROVEMENT RETAIL—2.3% | | | | | | | | |

| Floor & Decor Holdings, Inc., Cl. A* | | | 13,444 | | | | 1,335,527 | |

| HOMEBUILDING—2.0% | | | | | | | | |

| NVR, Inc.* | | | 195 | | | | 1,138,800 | |

| HOTELS RESORTS & CRUISE LINES—1.9% | | | | | | | | |

| Hilton Worldwide Holdings, Inc. | | | 7,755 | | | | 1,116,875 | |

| INSURANCE BROKERS—0.5% | | | | | | | | |

| Ryan Specialty Holdings, Inc., Cl. A* | | | 6,795 | | | | 277,644 | |

| INTERNET SERVICES & INFRASTRUCTURE—1.3% | | | | | | | | |

| MongoDB, Inc., Cl. A* | | | 3,164 | | | | 759,233 | |

| IT CONSULTING & OTHER SERVICES—0.5% | | | | | | | | |

| EPAM Systems, Inc.* | | | 935 | | | | 264,081 | |

| LIFE SCIENCES TOOLS & SERVICES—5.9% | | | | | | | | |

| Mettler-Toledo International, Inc.* | | | 638 | | | | 951,577 | |

| Repligen Corp.* | | | 6,300 | | | | 955,269 | |

| West Pharmaceutical Services, Inc. | | | 4,231 | | | | 1,528,406 | |

| | | | | | | | 3,435,252 | |

| METAL, GLASS & PLASTIC CONTAINERS—1.0% | | | | | | | | |

| Ball Corp. | | | 10,997 | | | | 584,820 | |

| MOVIES & ENTERTAINMENT—2.2% | | | | | | | | |

| Liberty Media Corp. Series C Liberty Formula One* | | | 14,466 | | | | 1,044,300 | |

| Live Nation Entertainment, Inc.* | | | 3,864 | | | | 261,902 | |

| | | | | | | | 1,306,202 | |

| OIL & GAS EQUIPMENT & SERVICES—1.0% | | | | | | | | |

| Baker Hughes Co., Cl. A | | | 18,941 | | | | 553,835 | |

| OIL & GAS EXPLORATION & PRODUCTION—2.8% | | | | | | | | |

| Diamondback Energy, Inc. | | | 11,245 | | | | 1,599,039 | |

| PROPERTY & CASUALTY INSURANCE—1.6% | | | | | | | | |

| Intact Financial Corp. | | | 5,984 | | | | 905,230 | |

| REAL ESTATE SERVICES—3.5% | | | | | | | | |

| FirstService Corp. | | | 13,561 | | | | 2,044,185 | |

| RESEARCH & CONSULTING SERVICES—3.4% | | | | | | | | |

| CoStar Group, Inc.* | | | 13,489 | | | | 1,037,978 | |

| Verisk Analytics, Inc., Cl. A | | | 4,917 | | | | 954,439 | |

| | | | | | | 1,992,417 | |

THE ALGER INSTITUTIONAL FUNDS | ALGER MID CAP GROWTH INSTITUTIONAL FUND

Schedule of Investments April 30, 2023 (Unaudited) (Continued)

| COMMON STOCKS—96.4% (CONT.) | | SHARES | | | VALUE | |

| RESTAURANTS—3.4% | | | | | | | | |

| Chipotle Mexican Grill, Inc., Cl. A* | | | 696 | | | $ | 1,439,064 | |

| Domino’s Pizza, Inc. | | | 1,681 | | | | 533,667 | |

| | | | | | | | 1,972,731 | |

| SEMICONDUCTOR MATERIALS & EQUIPMENT—2.3% | | | | | | | | |

| KLA Corp. | | | 1,966 | | | | 759,938 | |

| SolarEdge Technologies, Inc.* | | | 2,003 | | | | 572,117 | |

| | | | | | | | 1,332,055 | |

| SEMICONDUCTORS—4.2% | | | | | | | | |

| Marvell Technology, Inc. | | | 15,750 | | | | 621,810 | |

| Microchip Technology, Inc. | | | 11,648 | | | | 850,187 | |

| ON Semiconductor Corp.* | | | 13,656 | | | | 982,686 | |

| | | | | | | | 2,454,683 | |

| SYSTEMS SOFTWARE—1.6% | | | | | | | | |

| Palo Alto Networks, Inc.* | | | 5,231 | | | | 954,448 | |

| TOTAL COMMON STOCKS | | | | | | |

| |

| (Cost $50,669,261) | | | | | | | 56,133,328 | |

| | | | | | | | | |

| PREFERRED STOCKS—0.0% | | SHARES | | | VALUE | |

| BIOTECHNOLOGY—0.0% | | | | | | | | |

| Prosetta Biosciences, Inc., Series D*,@,(a),(b) | | | 166,009 | | | | — | |

| (Cost $747,040) | | | | | | | — | |

| | | | | | | | | |

| RIGHTS—0.5% | | SHARES | | | VALUE | |

| BIOTECHNOLOGY—0.5% | | | | | | | | |

| Tolero CDR*,@,(b),(c) | | | 422,928 | | | | 283,362 | |

| (Cost $226,186) | | | | | | | 283,362 | |

| | | | | | | | | |

| SPECIAL PURPOSE VEHICLE—1.4% | | | | | VALUE | |

| DATA PROCESSING & OUTSOURCED SERVICES—1.4% | | | | | | | | |

| Crosslink Ventures Capital C, LLC, Cl. A*,@,(a),(b) | | | | | | | 574,156 | |

| Crosslink Ventures Capital C, LLC, Cl. B*,@,(a),(b) | | | | | | | 236,313 | |

| | | | | | | | 810,469 | |

| TOTAL SPECIAL PURPOSE VEHICLE | | | | | | |

| |

| (Cost $775,000) | | | | | | | 810,469 | |

| Total Investments | | | | | | | | |

| (Cost $52,417,487) | | | 98.3 | % | | $ | 57,227,159 | |

| Affiliated Securities (Cost $1,522,040) | | | | | | | 810,469 | |

| Unaffiliated Securities (Cost $50,895,447) | | | | | | | 56,416,690 | |

| Other Assets in Excess of Liabilities | | | 1.7 | % | | | 992,211 | |

| NET ASSETS | | | 100.0 | % | | $ | 58,219,370 | |

| (a) | Deemed an affiliate of the Fund in accordance with Section 2(a)(3) of the Investment Company Act of 1940. See Note 11 - Affiliated Securities. |

| (b) | Security is valued in good faith at fair value determined using significant unobservable inputs pursuant to procedures established by the Valuation Designee (as defined in Note 2). |

| (c) | Contingent Deferred Rights. |

| * | Non-income producing security. |

THE ALGER INSTITUTIONAL FUNDS | ALGER MID CAP GROWTH INSTITUTIONAL FUND

Schedule of Investments April 30, 2023 (Unaudited) (Continued)

| @ | Restricted security - Investment in security not registered under the Securities Act of 1933. Sales or transfers of the investment may be restricted only to qualified buyers. |

| Security | | Acquisition

Date(s) | | | Acquisition

Cost | | | % of net assets

(Acquisition

Date) | | | Market

Value | | | % of net assets

as of

4/30/2023 | |

| Crosslink Ventures Capital C, LLC, Cl. A | | 10/2/20 | | | $ | 550,000 | | | | 0.50 | % | | $ | 574,156 | | | | 0.99 | % |

| Crosslink Ventures Capital C, LLC, Cl. B | | 12/16/20 | | | | 225,000 | | | | 0.19 | % | | | 236,313 | | | | 0.40 | % |

| Prosetta Biosciences, Inc., Series D | | 2/6/15 | | | | 747,040 | | | | 0.50 | % | | | 0 | | | | 0.00 | % |

| Tolero CDR | | 2/6/17 | | | | 226,186 | | | | 0.23 | % | | | 283,362 | | | | 0.49 | % |

| Total | |

| | | | | | | | | | | $ | 1,093,831 | | | | 1.88 | % |

See Notes to Financial Statements.

THE ALGER INSTITUTIONAL FUNDS | ALGER SMALL CAP GROWTH INSTITUTIONAL FUND

Schedule of Investments April 30, 2023 (Unaudited)

| COMMON STOCKS—93.0% | | SHARES | | | VALUE | |

| ADVERTISING—0.4% | | | | | | | | |

| Magnite, Inc.* | | | 60,701 | | | $ | 570,589 | |

| AEROSPACE & DEFENSE—4.7% | | | | | | | | |

| HEICO Corp. | | | 22,868 | | | | 3,856,460 | |

| Hexcel Corp. | | | 11,302 | | | | 814,648 | |

| Mercury Systems, Inc.* | | | 39,485 | | | | 1,882,250 | |

| | | | | | | | 6,553,358 | |

| APPAREL ACCESSORIES & LUXURY GOODS—1.3% | | | | | | | | |

| Capri Holdings Ltd.* | | | 42,573 | | | | 1,766,780 | |

| APPAREL RETAIL—0.8% | | | | | | | | |

| Aritzia, Inc.* | | | 11,340 | | | | 360,436 | |

| Victoria’s Secret & Co.* | | | 22,305 | | | | 691,678 | |

| | | | | | | | 1,052,114 | |

| APPLICATION SOFTWARE—23.6% | | | | | | | | |

| ACI Worldwide, Inc.* | | | 94,568 | | | | 2,395,407 | |

| AppFolio, Inc., Cl. A* | | | 10,917 | | | | 1,524,232 | |

| Bill.com Holdings, Inc.* | | | 19,937 | | | | 1,531,361 | |

| Blackbaud, Inc.* | | | 31,325 | | | | 2,172,545 | |

| Blackline, Inc.* | | | 30,962 | | | | 1,724,893 | |

| Everbridge, Inc.* | | | 43,537 | | | | 1,144,152 | |

| Guidewire Software, Inc.* | | | 17,630 | | | | 1,343,230 | |

| HubSpot, Inc.* | | | 7,080 | | | | 2,980,326 | |

| Manhattan Associates, Inc.* | | | 28,146 | | | | 4,663,229 | |

| Paycom Software, Inc.* | | | 7,121 | | | | 2,067,725 | |

| Q2 Holdings, Inc.* | | | 50,266 | | | | 1,237,549 | |

| SEMrush Holdings, Inc., Cl. A* | | | 43,195 | | | | 417,264 | |

| Smartsheet, Inc., Cl. A* | | | 33,059 | | | | 1,351,121 | |

| Sprout Social, Inc., Cl. A* | | | 31,957 | | | | 1,574,202 | |

| SPS Commerce, Inc.* | | | 31,850 | | | | 4,691,505 | |

| Vertex, Inc., Cl. A* | | | 85,295 | | | | 1,761,342 | |

| | | | | | | | 32,580,083 | |

| ASSET MANAGEMENT & CUSTODY BANKS—0.5% | | | | | | | | |

| Affiliated Managers Group, Inc. | | | 4,626 | | | | 667,902 | |

| BIOTECHNOLOGY—5.0% | | | | | | | | |

| ADMA Biologics, Inc.* | | | 216,166 | | | | 724,156 | |

| Alkermes PLC* | | | 17,170 | | | | 490,203 | |

| Arcus Biosciences, Inc.* | | | 17,775 | | | | 317,284 | |

| Avidity Biosciences, Inc.* | | | 30,579 | | | | 379,180 | |

| Cabaletta Bio, Inc.* | | | 84,268 | | | | 874,702 | |

| Celldex Therapeutics, Inc.* | | | 22,073 | | | | 693,975 | |

| Karuna Therapeutics, Inc.* | | | 6,159 | | | | 1,222,192 | |

| MoonLake Immunotherapeutics, Cl. A* | | | 19,481 | | | | 414,945 | |

| Morphic Holding, Inc.* | | | 15,239 | | | | 720,195 | |

| RAPT Therapeutics, Inc.* | | | 31,623 | | | | 575,539 | |

| Vaxcyte, Inc.* | | | 10,891 | | | | 466,461 | |

| | | | | | | | 6,878,832 | |

| CONSUMER STAPLES MERCHANDISE RETAIL—3.3% | | | | | | | | |

| BJ’s Wholesale Club Holdings, Inc.* | | | 59,413 | | | | 4,537,371 | |

THE ALGER INSTITUTIONAL FUNDS | ALGER SMALL CAP GROWTH INSTITUTIONAL FUND

Schedule of Investments April 30, 2023 (Unaudited) (Continued)

| COMMON STOCKS—93.0% (CONT.) | | SHARES | | | VALUE | |

| DIVERSIFIED SUPPORT SERVICES—0.4% | | | | | | | | |

| Ritchie Bros. Auctioneers, Inc. | | | 10,107 | | | $ | 578,019 | |

| ELECTRICAL COMPONENTS & EQUIPMENT—0.5% | | | | | | | | |

| Sunrun, Inc.* | | | 33,174 | | | | 697,981 | |

| ELECTRONIC EQUIPMENT & INSTRUMENTS—0.9% | | | | | | | | |

| 908 Devices, Inc.* | | | 187,978 | | | | 1,270,731 | |

| FOOD DISTRIBUTORS—3.0% | | | | | | | | |

| The Chefs’ Warehouse, Inc.* | | | 41,411 | | | | 1,377,330 | |

| US Foods Holding Corp.* | | | 71,204 | | | | 2,734,234 | |

| | | | | | | | 4,111,564 | |

| FOOTWEAR—0.5% | | | | | | | | |

| On Holding AG, Cl. A* | | | 23,161 | | | | 751,575 | |

| HEALTHCARE DISTRIBUTORS—0.2% | | | | | | | | |

| PetIQ, Inc., Cl. A* | | | 26,690 | | | | 314,675 | |

| HEALTHCARE EQUIPMENT—10.4% | | | | | | | | |

| Impulse Dynamics PLC, Class E*,@,(a) | | | 532,406 | | | | 1,756,940 | |

| Inmode Ltd.* | | | 38,658 | | | | 1,440,397 | |

| Insulet Corp.* | | | 12,543 | | | | 3,989,176 | |

| Mesa Laboratories, Inc. | | | 9,862 | | | | 1,642,121 | |

| Paragon 28, Inc.* | | | 31,166 | | | | 574,078 | |

| QuidelOrtho Corp.* | | | 33,443 | | | | 3,008,198 | |

| Shockwave Medical, Inc.* | | | 2,569 | | | | 745,421 | |

| Tandem Diabetes Care, Inc.* | | | 31,294 | | | | 1,238,616 | |

| | | | | | | | 14,394,947 | |

| HEALTHCARE SERVICES—0.6% | | | | | | | | |

| Guardant Health, Inc.* | | | 12,950 | | | | 292,152 | |

| Privia Health Group, Inc.* | | | 20,774 | | | | 573,986 | |