UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

_________________________

FORM 6-K

_________________________

Report of Foreign Private Issuer

Pursuant to Rule 13a-16 or 15d-16 under

the Securities Exchange Act of 1934

For the quarterly period ended June 30, 2021

Commission file number 1-12874

_________________________

TEEKAY CORPORATION

(Exact name of Registrant as specified in its charter)

_________________________

4th Floor, Belvedere Building,

69 Pitts Bay Road,

Hamilton, HM 08, Bermuda

(Address of principal executive office)

_________________________

| Indicate by check mark whether the registrant files or will file annual reports under cover Form 20-F or Form 40-F. | ||

Form 20-F ý Form 40-F ¨ | ||

| Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1). | ||

Yes ¨ No ý | ||

| Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7). | ||

Yes ¨ No ý | ||

Page 1

TEEKAY CORPORATION AND SUBSIDIARIES

REPORT ON FORM 6-K FOR THE QUARTERLY PERIOD ENDED JUNE 30, 2021

INDEX

| PAGE | |||||

Page 2

ITEM 1 – FINANCIAL STATEMENTS

TEEKAY CORPORATION AND SUBSIDIARIES

UNAUDITED CONSOLIDATED STATEMENTS OF (LOSS) INCOME

(in thousands of U.S. Dollars, except share and per share amounts)

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||||||||

| 2021 | 2020 | 2021 | 2020 | ||||||||||||||||||||

| $ | $ | $ | $ | ||||||||||||||||||||

Revenues (note 3) | 325,480 | 482,805 | 684,561 | 1,056,859 | |||||||||||||||||||

| Voyage expenses | (78,128) | (66,896) | (154,353) | (188,460) | |||||||||||||||||||

| Vessel operating expenses | (130,567) | (147,796) | (259,004) | (301,089) | |||||||||||||||||||

Time-charter hire expenses (note 5) | (8,005) | (17,714) | (19,126) | (44,770) | |||||||||||||||||||

| Depreciation and amortization | (59,244) | (62,936) | (117,830) | (135,853) | |||||||||||||||||||

| General and administrative expenses | (22,920) | (23,668) | (45,287) | (41,945) | |||||||||||||||||||

(Write-down) and gain (loss) on sale (note 13) | (86,686) | (10,669) | (87,401) | (105,275) | |||||||||||||||||||

Asset retirement obligation extinguishment gain (note 7) | 32,950 | 0 | 32,950 | 0 | |||||||||||||||||||

Gain on commencement of sales-type lease (note 3) | 0 | 0 | 0 | 44,943 | |||||||||||||||||||

Restructuring charges (note 15) | 0 | (4,622) | (303) | (7,010) | |||||||||||||||||||

| (Loss) income from vessel operations | (27,120) | 148,504 | 34,207 | 277,400 | |||||||||||||||||||

| Interest expense | (48,694) | (59,245) | (97,633) | (121,765) | |||||||||||||||||||

| Interest income | 1,336 | 2,314 | 3,381 | 5,117 | |||||||||||||||||||

Realized and unrealized (losses) gains on non-designated derivative instruments (note 10) | (3,389) | (9,270) | 3,932 | (30,933) | |||||||||||||||||||

Equity income (note 14 and 6b) | 28,111 | 35,343 | 65,268 | 37,656 | |||||||||||||||||||

Foreign exchange (loss) gain (notes 9 and 10) | (3,413) | (8,922) | 2,310 | (2,276) | |||||||||||||||||||

Other loss (note 7) | (4,639) | (399) | (9,154) | (1,080) | |||||||||||||||||||

| (Loss) income before income taxes | (57,808) | 108,325 | 2,311 | 164,119 | |||||||||||||||||||

Income tax recovery (note 12) | 204 | 17,175 | 1,589 | 13,383 | |||||||||||||||||||

| Net (loss) income | (57,604) | 125,500 | 3,900 | 177,502 | |||||||||||||||||||

| Net loss (income) attributable to non-controlling interests | 55,760 | (103,777) | 24,207 | (205,584) | |||||||||||||||||||

Net (loss) income attributable to the shareholders of Teekay Corporation | (1,844) | 21,723 | 28,107 | (28,082) | |||||||||||||||||||

Per common share of Teekay Corporation (note 18) | |||||||||||||||||||||||

| • Basic (loss) income attributable to shareholders of Teekay Corporation | (0.02) | 0.21 | 0.28 | (0.28) | |||||||||||||||||||

| • Diluted (loss) income attributable to shareholders of Teekay Corporation | (0.02) | 0.21 | 0.28 | (0.28) | |||||||||||||||||||

Weighted average number of common shares outstanding (note 18) | |||||||||||||||||||||||

| • Basic | 101,330,151 | 101,107,362 | 101,248,493 | 100,997,456 | |||||||||||||||||||

| • Diluted | 101,330,151 | 101,196,383 | 111,561,672 | 100,997,456 | |||||||||||||||||||

The accompanying notes are an integral part of the unaudited consolidated financial statements.

Page 3

TEEKAY CORPORATION AND SUBSIDIARIES

UNAUDITED CONSOLIDATED STATEMENTS OF COMPREHENSIVE (LOSS) INCOME

(in thousands of U.S. Dollars)

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||||||||

| 2021 | 2020 | 2021 | 2020 | ||||||||||||||||||||

| $ | $ | $ | $ | ||||||||||||||||||||

| Net (loss) income | (57,604) | 125,500 | 3,900 | 177,502 | |||||||||||||||||||

| Other comprehensive (loss) income: | |||||||||||||||||||||||

| Other comprehensive income (loss) before reclassifications | |||||||||||||||||||||||

| Unrealized (loss) gain on qualifying cash flow hedging instruments | (16,948) | (11,082) | 21,058 | (68,634) | |||||||||||||||||||

| Pension adjustments, net of taxes | (133) | (19) | (270) | (34) | |||||||||||||||||||

| Amounts reclassified from accumulated other comprehensive (loss) income relating to: | |||||||||||||||||||||||

| Realized loss on qualifying cash flow hedging instruments | |||||||||||||||||||||||

To interest expense (note 10) | 825 | 482 | 1,640 | 634 | |||||||||||||||||||

| To equity income | 5,096 | 2,427 | 10,078 | 5,931 | |||||||||||||||||||

| Other comprehensive (loss) income | (11,160) | (8,192) | 32,506 | (62,103) | |||||||||||||||||||

| Comprehensive (loss) income | (68,764) | 117,308 | 36,406 | 115,399 | |||||||||||||||||||

| Comprehensive loss (income) attributable to non-controlling interests | 62,169 | (98,543) | 4,810 | (164,063) | |||||||||||||||||||

| Comprehensive (loss) income attributable to shareholders of Teekay Corporation | (6,595) | 18,765 | 41,216 | (48,664) | |||||||||||||||||||

The accompanying notes are an integral part of the unaudited consolidated financial statements.

Page 4

TEEKAY CORPORATION AND SUBSIDIARIES

UNAUDITED CONSOLIDATED BALANCE SHEETS

(in thousands of U.S. Dollars, except share amounts)

| As at June 30, 2021 | As at December 31, 2020 | ||||||||||

| $ | $ | ||||||||||

| ASSETS | |||||||||||

| Current | |||||||||||

Cash and cash equivalents (notes 9 and 19) | 258,351 | 348,785 | |||||||||

Restricted cash – current (note 19) | 11,380 | 11,144 | |||||||||

| Accounts receivable, including non-trade of $7,964 (2020 – $7,931) | 121,014 | 150,997 | |||||||||

| Accrued revenue | 23,740 | 50,952 | |||||||||

| Prepaid expenses | 81,317 | 63,521 | |||||||||

Current portion of net investments in direct financing and sales-type leases, net (notes 3 and 6b) | 14,650 | 14,826 | |||||||||

Assets held for sale (note 13) | 11,925 | 32,974 | |||||||||

| Other current assets | 27,160 | 16,772 | |||||||||

| Total current assets | 549,537 | 689,971 | |||||||||

Restricted cash – non-current (note 19) | 40,521 | 45,961 | |||||||||

Vessels and equipment (note 9) | |||||||||||

At cost, less accumulated depreciation of $1,062,951 (2020 – $1,161,658) (note 13) | 2,254,208 | 2,325,097 | |||||||||

Vessels related to finance leases, at cost, less accumulated amortization of $270,665 (2020 – $281,786) (note 5) | 2,012,772 | 2,105,372 | |||||||||

Operating lease right-of-use assets (note 5) | 14,435 | 52,961 | |||||||||

| Total vessels and equipment | 4,281,415 | 4,483,430 | |||||||||

Net investment in direct financing and sales-type leases, net – non-current (notes 3 and 6b) | 501,485 | 513,815 | |||||||||

Investment in and loans, net to equity-accounted investments (notes 6b, 11a and 14) | 1,133,444 | 1,075,653 | |||||||||

| Goodwill, intangibles and other non-current assets | 130,199 | 137,082 | |||||||||

| Total assets | 6,636,601 | 6,945,912 | |||||||||

| LIABILITIES AND EQUITY | |||||||||||

| Current | |||||||||||

| Accounts payable | 103,987 | 124,066 | |||||||||

Accrued liabilities and other (note 7) | 210,003 | 332,086 | |||||||||

Short-term debt (note 8) | 10,000 | 10,000 | |||||||||

Current portion of long-term debt (note 9) | 374,960 | 261,366 | |||||||||

Current obligations related to finance leases (note 5) | 212,890 | 150,408 | |||||||||

Current portion of operating lease liabilities (note 5) | 14,724 | 25,108 | |||||||||

| Total current liabilities | 926,564 | 903,034 | |||||||||

Long-term debt (note 9) | 1,693,759 | 1,793,741 | |||||||||

Long-term obligations related to finance leases (note 5) | 1,384,922 | 1,550,557 | |||||||||

Long-term operating lease liabilities (note 5) | 105 | 29,182 | |||||||||

Other long-term liabilities (note 7) | 168,877 | 198,107 | |||||||||

| Total liabilities | 4,174,227 | 4,474,621 | |||||||||

Commitments and contingencies (notes 5, 8, 9, 10 and 11) | |||||||||||

| Equity | |||||||||||

Common stock and additional paid-in capital ($0.001 par value; 725,000,000 shares authorized; 101,429,683 shares outstanding and issued (2020 – 101,108,886) (note 17) | 1,052,900 | 1,057,319 | |||||||||

| Accumulated deficit | (498,797) | (527,028) | |||||||||

| Non-controlling interest | 1,944,035 | 1,989,883 | |||||||||

Accumulated other comprehensive loss (note 16) | (35,764) | (48,883) | |||||||||

| Total equity | 2,462,374 | 2,471,291 | |||||||||

| Total liabilities and equity | 6,636,601 | 6,945,912 | |||||||||

The accompanying notes are an integral part of the unaudited consolidated financial statements.

Page 5

TEEKAY CORPORATION AND SUBSIDIARIES

UNAUDITED CONSOLIDATED STATEMENTS OF CASH FLOWS

(in thousands of U.S. Dollars)

| Six Months Ended June 30, | |||||||||||

| 2021 | 2020 | ||||||||||

| $ | $ | ||||||||||

| Cash, cash equivalents and restricted cash provided by (used for) | |||||||||||

| OPERATING ACTIVITIES | |||||||||||

| Net income | 3,900 | 177,502 | |||||||||

| Non-cash and non-operating items: | |||||||||||

| Depreciation and amortization | 117,830 | 135,853 | |||||||||

Unrealized (gain) loss on derivative instruments (note 10) | (34,145) | 27,544 | |||||||||

Write-down and (gain) loss on sale (note 13) | 87,401 | 105,275 | |||||||||

Asset retirement obligation extinguishment gain (note 7) | (32,950) | 0 | |||||||||

Gain on commencement of sales-type lease (note 3) | 0 | (44,943) | |||||||||

| Equity income, net of dividends received $28,589 (2020 - $14,852) | (36,679) | (22,804) | |||||||||

| Foreign currency exchange loss (gain) and other | 13,967 | (7,250) | |||||||||

| Change in operating assets and liabilities: | |||||||||||

| Receipts from direct financing and sales-type leases | 7,285 | 334,146 | |||||||||

| Change in other operating assets and liabilities | (85,312) | 75,978 | |||||||||

| Asset retirement obligation expenditures | (1,419) | 0 | |||||||||

| Expenditures for dry docking | (21,014) | (5,608) | |||||||||

| Net operating cash flow | 18,864 | 775,693 | |||||||||

| FINANCING ACTIVITIES | |||||||||||

| Proceeds from issuance of long-term debt, net of issuance costs | 315,230 | 931,871 | |||||||||

| Prepayments of long-term debt | (151,543) | (1,302,389) | |||||||||

| Scheduled repayments of long-term debt | (156,142) | (240,355) | |||||||||

| Proceeds from short-term debt | 25,000 | 205,000 | |||||||||

| Prepayment of short-term debt | (25,000) | (245,000) | |||||||||

| Prepayment of obligations related to finance leases | (56,724) | 0 | |||||||||

| Repayments of obligations related to finance leases | (46,429) | (47,162) | |||||||||

| Repurchase of Teekay LNG common units | 0 | (15,635) | |||||||||

| Distributions paid from subsidiaries to non-controlling interests | (42,933) | (35,519) | |||||||||

| Other financing activities | (388) | (794) | |||||||||

| Net financing cash flow | (138,929) | (749,983) | |||||||||

| INVESTING ACTIVITIES | |||||||||||

| Expenditures for vessels and equipment | (20,090) | (12,824) | |||||||||

Proceeds from sale of vessels and equipment (note 13) | 32,687 | 60,915 | |||||||||

Proceeds from the sale of assets, net of cash sold (note 13) | 0 | 12,221 | |||||||||

| Proceeds from repayments of advances to equity-accounted joint ventures | 11,830 | 3,500 | |||||||||

| Other investing activities | 0 | (6,430) | |||||||||

| Net investing cash flow | 24,427 | 57,382 | |||||||||

| (Decrease) increase in cash, cash equivalents, restricted cash and cash held for sale | (95,638) | 83,092 | |||||||||

| Cash, cash equivalents, restricted cash and cash held for sale, beginning of the period | 405,890 | 456,325 | |||||||||

| Cash, cash equivalents and restricted cash, end of the period | 310,252 | 539,417 | |||||||||

Supplemental cash flow information (note 19) | |||||||||||

The accompanying notes are an integral part of the unaudited consolidated financial statements.

Page 6

TEEKAY CORPORATION AND SUBSIDIARIES

UNAUDITED CONSOLIDATED STATEMENTS OF CHANGES IN TOTAL EQUITY

(in thousands of U.S. Dollars, except share amounts)

| TOTAL EQUITY | |||||||||||||||||||||||||||||||||||

Thousands of Shares of Common Stock Outstanding # | Common Stock and Additional Paid-in Capital $ | Accumulated Deficit $ | Accumulated Other Compre- hensive Loss $ | Non- controlling Interests $ | Total $ | ||||||||||||||||||||||||||||||

| Balance as at December 31, 2020 | 101,109 | 1,057,319 | (527,028) | (48,883) | 1,989,883 | 2,471,291 | |||||||||||||||||||||||||||||

| Net income | — | — | 29,951 | — | 31,553 | 61,504 | |||||||||||||||||||||||||||||

| Other comprehensive income | — | — | — | 17,860 | 25,806 | 43,666 | |||||||||||||||||||||||||||||

| Dividends declared: | |||||||||||||||||||||||||||||||||||

| Other dividends | — | — | — | — | (19,174) | (19,174) | |||||||||||||||||||||||||||||

| Employee stock compensation and other | 177 | 939 | — | — | — | 939 | |||||||||||||||||||||||||||||

Change in accounting policy (note 2) | — | (6,334) | — | — | — | (6,334) | |||||||||||||||||||||||||||||

| Changes to non-controlling interest from equity contributions and other | — | — | (20) | 4 | 693 | 677 | |||||||||||||||||||||||||||||

| Balance as at March 31, 2021 | 101,286 | 1,051,924 | (497,097) | (31,019) | 2,028,761 | 2,552,569 | |||||||||||||||||||||||||||||

| Net loss | — | — | (1,844) | — | (55,760) | (57,604) | |||||||||||||||||||||||||||||

| Other comprehensive loss | — | — | — | (4,751) | (6,409) | (11,160) | |||||||||||||||||||||||||||||

| Dividends declared: | — | ||||||||||||||||||||||||||||||||||

| Other dividends | — | — | — | — | (23,759) | (23,759) | |||||||||||||||||||||||||||||

| Employee stock compensation and other | 144 | 976 | — | — | — | 976 | |||||||||||||||||||||||||||||

| Changes to non-controlling interest from equity contributions and other | — | — | 144 | 6 | 1,202 | 1,352 | |||||||||||||||||||||||||||||

| Balance as at June 30, 2021 | 101,430 | 1,052,900 | (498,797) | (35,764) | 1,944,035 | 2,462,374 | |||||||||||||||||||||||||||||

Page 7

TEEKAY CORPORATION AND SUBSIDIARIES

UNAUDITED CONSOLIDATED STATEMENTS OF CHANGES IN TOTAL EQUITY

(in thousands of U.S. Dollars, except share amounts)

| TOTAL EQUITY | |||||||||||||||||||||||||||||||||||||||||

| Thousands of Shares of Common Stock Outstanding # | Common Stock and Additional Paid-in Capital $ | Accumulated Deficit $ | Accumulated Other Compre- hensive Loss $ | Non- controlling Interests $ | Total $ | ||||||||||||||||||||||||||||||||||||

| Balance as at December 31, 2019 | 100,784 | 1,052,284 | (546,684) | (23,737) | 2,089,730 | 2,571,593 | |||||||||||||||||||||||||||||||||||

| Net (loss) income | — | — | (49,805) | — | 101,807 | 52,002 | |||||||||||||||||||||||||||||||||||

| Other comprehensive loss | — | — | — | (17,624) | (36,287) | (53,911) | |||||||||||||||||||||||||||||||||||

| Dividends declared: | |||||||||||||||||||||||||||||||||||||||||

| Other dividends | — | — | — | — | (16,353) | (16,353) | |||||||||||||||||||||||||||||||||||

| Employee stock compensation and other | 324 | 1,238 | — | — | — | 1,238 | |||||||||||||||||||||||||||||||||||

Change in accounting policy (note 2) | — | — | (17,216) | — | (36,084) | (53,300) | |||||||||||||||||||||||||||||||||||

| Changes to non-controlling interest from equity contributions and other | — | — | 2,912 | (321) | (17,196) | (14,605) | |||||||||||||||||||||||||||||||||||

| Balance as at March 31, 2020 | 101,108 | 1,053,522 | (610,793) | (41,682) | 2,085,617 | 2,486,664 | |||||||||||||||||||||||||||||||||||

| Net income | — | — | 21,723 | — | 103,777 | 125,500 | |||||||||||||||||||||||||||||||||||

| Other comprehensive loss | — | — | — | (2,958) | (5,234) | (8,192) | |||||||||||||||||||||||||||||||||||

| Dividends declared: | |||||||||||||||||||||||||||||||||||||||||

| Other dividends | — | — | — | — | (19,166) | (19,166) | |||||||||||||||||||||||||||||||||||

| Employee stock compensation and other | (1) | 1,368 | — | — | — | 1,368 | |||||||||||||||||||||||||||||||||||

| Changes to non-controlling interest from equity contributions and other | — | — | 116,818 | (9,030) | (106,721) | 1,067 | |||||||||||||||||||||||||||||||||||

| Balance as at June 30, 2020 | 101,107 | 1,054,890 | (472,252) | (53,670) | 2,058,273 | 2,587,241 | |||||||||||||||||||||||||||||||||||

The accompanying notes are an integral part of the unaudited consolidated financial statements.

Page 8

TEEKAY CORPORATION AND SUBSIDIARIES

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

(all tabular amounts stated in thousands of U.S. Dollars, other than share and per share data)

1.Basis of Presentation

The unaudited interim consolidated financial statements have been prepared in accordance with United States generally accepted accounting principles (or GAAP). They include the accounts of Teekay Corporation (or Teekay), which is incorporated under the laws of the Republic of the Marshall Islands, its wholly-owned or controlled subsidiaries and any variable interest entities (or VIEs) of which Teekay is the primary beneficiary (collectively, the Company).

Certain information and footnote disclosures required by GAAP for complete annual financial statements have been omitted from these unaudited interim consolidated financial statements and, therefore, these financial statements should be read in conjunction with the Company’s audited consolidated financial statements for the year ended December 31, 2020, included in the Company’s Annual Report on Form 20-F, filed with the U.S. Securities and Exchange Commission (or SEC) on April 1, 2020. In the opinion of management, these unaudited interim consolidated financial statements reflect all adjustments, consisting of a normal recurring nature, necessary to present fairly, in all material respects, the Company’s consolidated financial position, results of operations, cash flows and changes in total equity for the interim periods presented. The results of operations for the three and six months ended June 30, 2021, are not necessarily indicative of those for a full fiscal year. Significant intercompany balances and transactions have been eliminated upon consolidation.

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the amounts reported in the unaudited financial statements and accompanying notes. Actual results could differ from those estimates. It is possible that the amounts recorded as derivative assets and liabilities could vary by material amounts prior to their settlement.

In March 2020, the World Health Organization declared the outbreak of a novel coronavirus (or COVID-19) as a pandemic. Given the dynamic nature of these circumstances, the full extent to which the COVID-19 global pandemic may have direct or indirect impact on the Company's business and the related financial reporting implications cannot be reasonably estimated at this time, although it could materially affect the Company's business, results of operations and financial condition in the future. COVID-19 has resulted and may continue to result in a significant decline in global demand for oil. As the Company's business includes the transportation of crude oil and refined petroleum products on behalf of customers, any significant decrease in demand for the cargo the Company transports could adversely affect demand for the Company's vessels and services. Spot tanker rates have come under pressure since mid-May 2020 as a result of record OPEC+ oil production cuts and lower production from other oil producing countries, which reduced crude exports, and the unwinding of floating storage and the delivery of newbuilding vessels to the world tanker fleet. COVID-19 has also been a contributing factor to the decline in short-term tanker charter rates and the increase in certain crewing-related costs, which has had an impact on the Company's cash flows. COVID-19 was a contributing factor to the write-down of certain tankers of Teekay Tankers during the three and six months ended June 30, 2021, and was also a contributing factor to the write-down of 6 of Teekay LNG's multi-gas vessels and 1 floating production storage and offloading (or FPSO) unit of Teekay Parent during the six months ended June 30, 2020 (see Note 13) .

2. Recent Accounting Pronouncements

In December 2019, the FASB issued Accounting Standards Update (or ASU) 2019-12 - Income Taxes (Topic 740) Simplifying the Accounting for Income Taxes (or ASU 2019-12), as part of its initiative to reduce complexity in the accounting standards. The amendments in ASU 2019-12 eliminate certain exceptions related to the approach for intraperiod tax allocation, the methodology for calculating income taxes in an interim period and the recognition of deferred tax liabilities for outside basis differences, among other changes. The guidance becomes effective for annual reporting periods beginning after December 15, 2020 and interim periods within those fiscal years with early adoption permitted, including adoption in any interim period. The adoption did not have an impact on the Company's consolidated financial statements and related disclosures.

In March 2020, the FASB issued ASU 2020-04 - Reference Rate Reform (Topic 848) Facilitation of the Effects of Reference Rate Reform on Financial Reporting. This update provides optional guidance for a limited period of time to ease potential accounting impacts associated with transitioning away from reference rates that are expected to be discontinued, such as the London Interbank Offered Rate (or LIBOR). This update applies only to contracts, hedging relationships and other transactions that reference LIBOR or another reference rate expected to be discontinued. This update is effective through December 31, 2022. The Company is currently evaluating the effect of adopting this new guidance.

In August 2020, the FASB issued ASU 2020-06 - Debt - Debt with Conversion and Other Options (Subtopic 470-20) and Derivatives and Hedging - Contracts in Entity’s Own Equity (Subtopic 815-40). This update simplified the accounting for convertible debt instruments and convertible preferred stock by reducing the number of accounting models and the number of embedded conversion features that could be recognized separately from the primary contract. This update also enhanced transparency and improved disclosures for convertible instruments and earnings per share guidance. This update is mandatory beginning January 1, 2022; however, the Company early adopted this update effective January 1, 2021 using the modified retrospective method of transition. The adoption of ASU 2020-06 has impacted the accounting for the Company’s Convertible Senior Notes due January 15, 2023 (or the Convertible Notes) whereby the existing debt and equity components have been recombined into a single component accounted for as a single liability, at its amortized cost. On adoption, the Company increased the carrying value of long-term debt by $6.3 million and decreased common stock and additional paid-in capital by $6.3 million. Adoption of ASU 2020-06 also decreased the Company's interest expense by $0.7 million and $1.5 million for the three and six months ended June 30, 2021. In addition, the adoption of ASU 2020-06 resulted in the Company having to change from the use of the

Page 9

TEEKAY CORPORATION AND SUBSIDIARIES

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

(all tabular amounts stated in thousands of U.S. Dollars, other than share and per share data)

treasury stock method to the if-converted method to determine the dilutive impact of the Convertible Notes when calculating diluted earnings per share attributable to shareholders of Teekay Corporation. For the three and six months ended June 30, 2021, the change to the if-converted method increased the Company's diluted income attributable to shareholders of Teekay Corporation by $1.6 million and $3.2 million, respectively, increased the denominator of the diluted earnings per share calculation by 9,588,378 shares for both periods, and increased the diluted earnings per share attributable to shareholders of Teekay Corporation by $0.01 and $0.02, respectively (see Note 18).

3. Revenues

The Company’s primary source of revenue is chartering its vessels and offshore units to its customers. The Company utilizes four primary forms of contracts, consisting of time-charter contracts, voyage charter contracts, bareboat charter contracts and contracts for FPSO units. The Company also generates revenue from the management and operation of vessels owned by third parties and by equity-accounted investments as well as by providing corporate management services to such third-party entities. For a description of these contracts, see "Item 18 – Financial Statements: Note 2" in the Company’s Annual Report on Form 20-F for the year ended December 31, 2020.

Revenue Table

The following tables contain the Company’s revenue for the three and six months ended June 30, 2021 and 2020, by contract type, by segment and by business lines within segments.

| Three Months Ended June 30, 2021 | |||||||||||||||||||||||

Teekay LNG Liquefied Gas Carriers | Teekay Tankers Conventional Tankers | Teekay Parent Offshore Production | Teekay Parent Other | Total | |||||||||||||||||||

| $ | $ | $ | $ | $ | |||||||||||||||||||

| Time charters | 135,595 | 7,065 | 0 | 0 | 142,660 | ||||||||||||||||||

| Voyage charters | 10,318 | 113,998 | 0 | 0 | 124,316 | ||||||||||||||||||

| FPSO contracts | 0 | 0 | 12,290 | 0 | 12,290 | ||||||||||||||||||

| Management fees and other | 2,856 | 2,357 | 0 | 41,001 | 46,214 | ||||||||||||||||||

| 148,769 | 123,420 | 12,290 | 41,001 | 325,480 | |||||||||||||||||||

| Three Months Ended June 30, 2020 | |||||||||||||||||||||||

Teekay LNG Liquefied Gas Carriers | Teekay Tankers Conventional Tankers | Teekay Parent Offshore Production | Teekay Parent Other | Total | |||||||||||||||||||

| $ | $ | $ | $ | $ | |||||||||||||||||||

| Time charters | 135,761 | 34,986 | 0 | 4,096 | 174,843 | ||||||||||||||||||

| Voyage charters | 10,383 | 207,926 | 0 | 0 | 218,309 | ||||||||||||||||||

| FPSO contracts | 0 | 0 | 28,787 | 0 | 28,787 | ||||||||||||||||||

| Management fees and other | 2,061 | 3,580 | 0 | 55,225 | 60,866 | ||||||||||||||||||

| 148,205 | 246,492 | 28,787 | 59,321 | 482,805 | |||||||||||||||||||

| Six Months Ended June 30, 2021 | |||||||||||||||||||||||

Teekay LNG Liquefied Gas Carriers | Teekay Tankers Conventional Tankers | Teekay Parent Offshore Production | Teekay Parent Other | Total | |||||||||||||||||||

| $ | $ | $ | $ | $ | |||||||||||||||||||

| Time charters | 277,232 | 35,350 | 0 | 2,255 | 314,837 | ||||||||||||||||||

| Voyage charters | 19,585 | 226,199 | 0 | 0 | 245,784 | ||||||||||||||||||

| FPSO contracts | 0 | 0 | 23,107 | 0 | 23,107 | ||||||||||||||||||

| Management fees and other | 4,754 | 4,620 | 0 | 91,459 | 100,833 | ||||||||||||||||||

| 301,571 | 266,169 | 23,107 | 93,714 | 684,561 | |||||||||||||||||||

Page 10

TEEKAY CORPORATION AND SUBSIDIARIES

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

(all tabular amounts stated in thousands of U.S. Dollars, other than share and per share data)

| Six Months Ended June 30, 2020 | |||||||||||||||||||||||

Teekay LNG Liquefied Gas Carriers | Teekay Tankers Conventional Tankers | Teekay Parent Offshore Production | Teekay Parent Other | Total | |||||||||||||||||||

| $ | $ | $ | $ | $ | |||||||||||||||||||

| Time charters | 266,306 | 50,553 | 0 | 9,053 | 325,912 | ||||||||||||||||||

| Voyage charters | 17,700 | 525,404 | 0 | 0 | 543,104 | ||||||||||||||||||

| FPSO contracts | 0 | 0 | 74,720 | 0 | 74,720 | ||||||||||||||||||

| Management fees and other | 4,086 | 12,435 | 0 | 96,602 | 113,123 | ||||||||||||||||||

| 288,092 | 588,392 | 74,720 | 105,655 | 1,056,859 | |||||||||||||||||||

The following table contains the Company's total revenue for the three and six months ended June 30, 2021 and 2020, by those contracts or components of contracts accounted for as leases and by those contracts or components not accounted for as leases.

| Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||||||||||||||

| 2021 | 2020 | 2021 | 2020 | |||||||||||||||||||||||

| $ | $ | $ | $ | |||||||||||||||||||||||

| Lease revenue | ||||||||||||||||||||||||||

| Lease revenue from lease payments of operating leases | 251,842 | 390,407 | 530,744 | 876,590 | ||||||||||||||||||||||

| Interest income on lease receivables | 12,294 | 12,877 | 24,822 | 25,543 | ||||||||||||||||||||||

Variable lease payments – cost reimbursements (1) | 9,670 | 13,658 | 17,322 | 26,848 | ||||||||||||||||||||||

Variable lease payments – other (2) | 0 | 0 | 0 | 5,218 | ||||||||||||||||||||||

| 273,806 | 416,942 | 572,888 | 934,199 | |||||||||||||||||||||||

| Non-lease revenue | ||||||||||||||||||||||||||

| Non-lease revenue – related to sales-type or direct financing leases | 5,460 | 4,997 | 10,840 | 9,537 | ||||||||||||||||||||||

| Management fees and other income | 46,214 | 60,866 | 100,833 | 113,123 | ||||||||||||||||||||||

| 51,674 | 65,863 | 111,673 | 122,660 | |||||||||||||||||||||||

| Total | 325,480 | 482,805 | 684,561 | 1,056,859 | ||||||||||||||||||||||

(1)Reimbursement for vessel operating expenditures and dry-docking expenditures received from the Company's customers relating to such costs incurred by the Company to operate the vessel for the customer.

(2)Compensation from time-charter contracts based on spot market rates in excess of a base daily hire amount, production tariffs based on the volume of oil produced, the price of oil and other monthly or annual operational performance measures.

Operating Leases

As at June 30, 2021, the minimum scheduled future rentals to be received by the Company in each of the next five years for time charters, bareboat charters and FPSO contracts that were accounted for as operating leases were approximately $265.4 million (remainder of 2021), $429.8 million (2022), $322.8 million (2023), $252.9 million (2024) and $197.4 million (2025).

Minimum scheduled future revenues should not be construed to reflect total charter hire revenues for any of the years. Minimum scheduled future revenues do not include revenue generated from new contracts entered into after June 30, 2021, revenue from unexercised option periods of contracts that existed on June 30, 2021, revenue from vessels in the Company’s equity-accounted investments, or variable or contingent revenues accounted for under Accounting Standards Codification (or ASC) 842 Leases. In addition, minimum scheduled future operating lease revenues presented in this paragraph have been reduced by estimated off-hire time for any periodic maintenance and do not reflect the impact of revenue sharing arrangements whereby time-charter revenues are shared with other revenue sharing arrangement participants. The amounts may vary given unscheduled future events such as vessel maintenance.

Page 11

TEEKAY CORPORATION AND SUBSIDIARIES

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

(all tabular amounts stated in thousands of U.S. Dollars, other than share and per share data)

Net Investment in Direct Financing Leases and Sales-Type Leases

On March 27, 2020, the Company entered into a bareboat charter with Britoil Limited (or BP), a subsidiary of BP p.l.c., for the Petrojarl Foinaven FPSO for a period up to December 2030. BP may cancel the charter on six-months' notice. Under the terms of this charter, Teekay received a cash payment of approximately $67 million in April 2020 and will receive a nominal per day rate over the life of the contract and a fixed lump sum payment at the end of the contract period. The charter was classified and accounted for as a sales-type lease. Consequently, as at March 31, 2020, the Company recognized a net investment in sales-type lease of $81.9 million and an asset retirement obligation of $6.1 million, derecognized the carrying value of the Petrojarl Foinaven FPSO and related customer contract, and recognized a gain of $44.9 million in the three months ended March 31, 2020. As at June 30, 2021, the net investment in sales-type lease was $14.6 million, with the majority of the reduction from inception relating to the cash payment of $67 million received in April 2020. In April 2021, BP announced its decision to suspend production from the Foinaven oil fields and permanently remove the Petrojarl Foinaven FPSO unit from the site. The Company expects the FPSO unit to be redelivered to Teekay Parent in the third quarter of 2022, at which point the Company intends to green-recycle the FPSO unit. At the end of the contract, the Company will receive a fixed lump sum payment from BP which the Company expects will cover the cost of green-recycling the FPSO unit.

As at June 30, 2021, Teekay LNG had 3 liquefied natural gas (or LNG) carriers, excluding vessels in its equity-accounted joint ventures, which are accounted for as direct financing leases. For a description of Teekay LNG's LNG carriers accounted for as direct financing leases, see "Item 18 – Financial Statements: Note 2" to the Company's Annual Report on Form 20-F for the year ended December 31, 2020.

As at December 31, 2019, Teekay LNG had 2 additional LNG carriers, the WilForce and the WilPride, that were chartered to Awilco LNG ASA (or Awilco) and were accounted for as sales-type leases. In January 2020, Awilco purchased both carriers from Teekay LNG and paid Teekay LNG the associated purchase obligation amounts, deferred hire amounts and interest on deferred hire amounts, totaling $260.4 million relating to these 2 vessels.

As at June 30, 2021, estimated minimum lease payments to be received related to direct financing and sales-type leases in each of the next five years were approximately $32.3 million (remainder of 2021), $64.2 million (2022), $64.0 million (2023), $64.3 million (2024), $64.2 million (2025) and an aggregate of $446.5 million thereafter. The leases are expected to end between 2028 and 2039.

Contract Liabilities

The Company enters into certain customer contracts that result in situations where the customer will pay consideration upfront for performance to be provided in the following month or months. These receipts are contract liabilities and are presented as deferred revenue until performance is provided. As at June 30, 2021 and December 31, 2020, there were contract liabilities of $14.0 million and $30.7 million, respectively. During the three and six months ended June 30, 2021, the Company recognized revenues of $21.7 million and $30.7 million, respectively, (three and six months ended June 30, 2020 - $28.1 million and $32.4 million, respectively) included in contract liability at the beginning of such periods.

4. Segment Reporting

The Company’s segments are described in "Item 18 – Financial Statements: Note 3" to the Company’s Annual Report on Form 20-F for the year ended December 31, 2020. The Company allocates capital and assesses performance from the separate perspectives of its 2 publicly-traded subsidiaries Teekay LNG and Teekay Tankers (together, the Daughter Entities), Teekay and its remaining subsidiaries (or Teekay Parent), as well as from the perspective of the Company's lines of business. The primary focus of the Company’s organizational structure, internal reporting and allocation of resources by the chief operating decision maker is on the Daughter Entities and Teekay Parent (the Legal Entity approach) and its segments are presented accordingly on this basis. The Company has 3 primary lines of business: (1) offshore production (FPSO units), (2) LNG and liquefied petroleum gas (or LPG) carriers, and (3) conventional tankers. The Company manages these businesses for the benefit of all stakeholders. The Company incorporates the primary lines of business within its segments, as in certain cases there is more than one line of business in each Daughter Entity and the Company believes this information allows a better understanding of the Company’s performance and prospects for future net cash flows.

The following table includes the Company’s revenues by segment for the three and six months ended June 30, 2021 and 2020:

Page 12

TEEKAY CORPORATION AND SUBSIDIARIES

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

(all tabular amounts stated in thousands of U.S. Dollars, other than share and per share data)

| Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||

| 2021 | 2020 | 2021 | 2020 | |||||||||||

| $ | $ | $ | $ | |||||||||||

| Teekay LNG | ||||||||||||||

| Liquefied Gas Carriers | 148,769 | 148,205 | 301,571 | 288,092 | ||||||||||

| Teekay Tankers | ||||||||||||||

| Conventional Tankers | 123,420 | 246,492 | 266,169 | 588,392 | ||||||||||

| Teekay Parent | ||||||||||||||

| Offshore Production | 12,290 | 28,787 | 23,107 | 74,720 | ||||||||||

| Other | 41,001 | 59,321 | 93,714 | 105,655 | ||||||||||

| 53,291 | 88,108 | 116,821 | 180,375 | |||||||||||

| 325,480 | 482,805 | 684,561 | 1,056,859 | |||||||||||

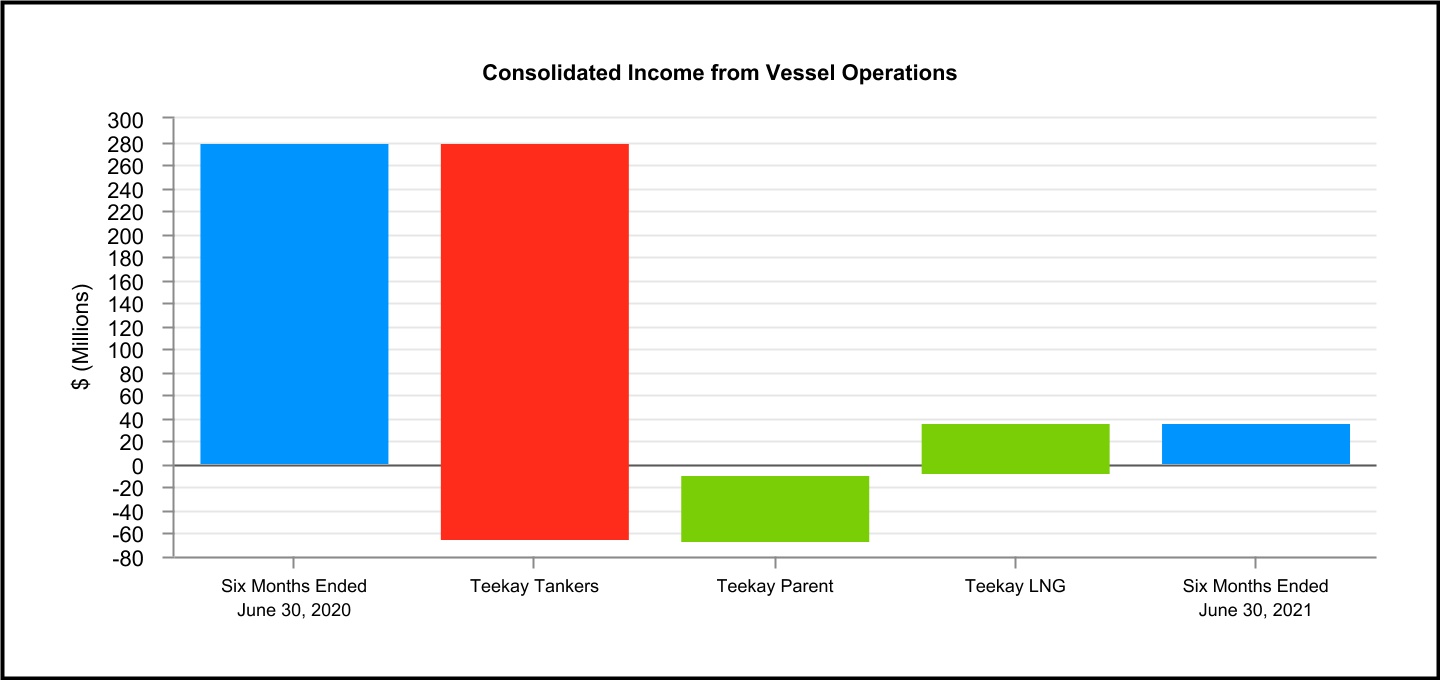

The following table includes the Company’s (loss) income from vessel operations by segment for the three and six months ended June 30, 2021 and 2020:

(Loss) income from Vessel Operations(1) | ||||||||||||||

| Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||

| 2021 | 2020 | 2021 | 2020 | |||||||||||

| $ | $ | $ | $ | |||||||||||

| Teekay LNG | ||||||||||||||

| Liquefied Gas Carriers | 64,736 | 69,589 | 135,347 | 91,327 | ||||||||||

| Teekay Tankers | ||||||||||||||

| Conventional Tankers | (119,434) | 92,986 | (131,277) | 213,112 | ||||||||||

| Teekay Parent | ||||||||||||||

| Offshore Production | 30,543 | (11,540) | 32,515 | (23,808) | ||||||||||

| Other | (2,965) | (2,531) | (2,378) | (3,231) | ||||||||||

| 27,578 | (14,071) | 30,137 | (27,039) | |||||||||||

| (27,120) | 148,504 | 34,207 | 277,400 | |||||||||||

(1)Includes direct general and administrative expenses and indirect general and administrative expenses (allocated to each segment based on estimated use of corporate resources).

A reconciliation of total segment assets to consolidated total assets presented in the accompanying unaudited consolidated balance sheets is as follows:

Page 13

TEEKAY CORPORATION AND SUBSIDIARIES

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

(all tabular amounts stated in thousands of U.S. Dollars, other than share and per share data)

| June 30, 2021 | December 31, 2020 | |||||||

| $ | $ | |||||||

| Teekay LNG – Liquefied Gas Carriers | 4,661,759 | 4,647,242 | ||||||

| Teekay Tankers – Conventional Tankers | 1,593,712 | 1,743,013 | ||||||

| Teekay Parent – Offshore Production | 18,372 | 30,845 | ||||||

| Teekay Parent – Other | 19,148 | 60,002 | ||||||

| Cash and cash equivalents | 258,351 | 348,785 | ||||||

| Other assets not allocated | 98,435 | 132,425 | ||||||

| Eliminations | (13,176) | (16,400) | ||||||

| Consolidated total assets | 6,636,601 | 6,945,912 | ||||||

5. Leases

Obligations Related to Finance Leases

| June 30, 2021 | December 31, 2020 | ||||||||||

| $ | $ | ||||||||||

| Teekay LNG | |||||||||||

| LNG Carriers | 1,305,055 | 1,340,922 | |||||||||

| Teekay Tankers | |||||||||||

| Conventional Tankers | 292,757 | 360,043 | |||||||||

| Total obligations related to finance leases | 1,597,812 | 1,700,965 | |||||||||

| Less current portion | (212,890) | (150,408) | |||||||||

| Long-term obligations related to finance leases | 1,384,922 | 1,550,557 | |||||||||

Teekay LNG

As at June 30, 2021 and December 31, 2020, Teekay LNG was a party to finance leases on 9 LNG carriers. These 9 LNG carriers were sold by Teekay LNG to third parties (or Lessors) and leased back under 7.5- to 15-year bareboat charter contracts ending in 2026 through 2034. At inception of these leases, the weighted-average interest rate implicit in these leases was 5.1%. The bareboat charter contracts are presented as obligations related to finance leases on the Company's unaudited consolidated balance sheets and have purchase obligations at the end of the lease terms.

The obligations of Teekay LNG under the bareboat charter contracts for the 9 LNG carriers are guaranteed by Teekay LNG. The guarantee agreements require Teekay LNG to maintain minimum levels of tangible net worth and aggregate liquidity, and not to exceed a maximum amount of leverage. As at June 30, 2021, Teekay LNG was in compliance with all covenants in respect of the obligations related to its finance leases.

As at June 30, 2021, the remaining commitments related to the financial liabilities of these 9 LNG carriers, including the amounts to be paid for the related purchase obligations, approximated $1.7 billion, including imputed interest of $366.8 million, repayable for the remainder of 2021 through 2034, as indicated below:

| Commitments | ||||||||

| At June 30, 2021 | ||||||||

| Year | $ | |||||||

| Remainder of 2021 | 69,063 | |||||||

| 2022 | 136,959 | |||||||

| 2023 | 135,459 | |||||||

| 2024 | 132,011 | |||||||

| 2025 | 129,725 | |||||||

| Thereafter | 1,068,641 | |||||||

Page 14

TEEKAY CORPORATION AND SUBSIDIARIES

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

(all tabular amounts stated in thousands of U.S. Dollars, other than share and per share data)

Teekay Tankers

From 2017 to 2019, Teekay Tankers completed sale-leaseback financing transactions with financial institutions relating to 16 of Teekay Tankers' vessels. Under these arrangements, Teekay Tankers transferred the vessels to subsidiaries of the financial institutions (collectively, the Lessors) and leased the vessels back from the Lessors on bareboat charters ranging from 9 to 12-year terms. In October 2020, Teekay Tankers completed the purchases of 2 of these vessels for a total cost of $29.6 million and in May 2021, Teekay Tankers completed the purchases of 2 more of these vessels for a total cost of $56.7 million. In March 2021, Teekay Tankers also declared purchase options to acquire 6 additional vessels for a total cost of $128.8 million with an expected completion date of September 2021. Teekay Tankers has the option to purchase each of the remaining 6 vessels, four of which can be purchased between now and the end of their respective lease terms, while the remaining two can be purchased starting in November 2021 until the end of their respective lease terms.

The bareboat charters related to these vessels require that Teekay Tankers maintain a minimum liquidity (cash, cash equivalents and undrawn committed revolving credit lines with at least six months to maturity) of the greater of $35.0 million and at least 5.0% of Teekay Tankers' consolidated debt and obligations related to finance leases.

NaN of the bareboat charters were entered into with subsidiaries of a financial institution in July 2017 and November 2018. NaN of these bareboat charters, entered into in July 2017, require Teekay Tankers to maintain, for each vessel, a minimum hull coverage ratio of 90% of the total outstanding principal balance during the first three years of the lease period and 100% of the total outstanding principal balance thereafter. As at June 30, 2021, these ratios were 102% (December 31, 2020 – ranged from 121% to 143%). The remaining 2 of these bareboat charters, entered into in November 2018, require Teekay Tankers to maintain, for each vessel, a minimum hull coverage ratio of 100% of the total outstanding principal balance. As at June 30, 2021, these ratios ranged from 122% to 127% (December 31, 2020 – ranged from 145% to 156%). Should any of these ratios drop below the required amount, the lessor may request that the Company prepay additional charter hire.

NaN bareboat charters, entered into with subsidiaries of a financial institution in September 2018, require Teekay Tankers to maintain, for each vessel, a minimum hull coverage ratio of 75% of the total outstanding principal balance during the first year of the lease period, 78% for the second year, 80% for the following two years and 90% of the total outstanding principal balance thereafter. As at June 30, 2021, these ratios ranged from 98% to 104% (December 31, 2020 – ranged from 80% to 88%). Should any of these ratios drop below the required amount, and Teekay Tankers is unable to cure any such breach within the prescribed cure period, Teekay Tankers' obligations may become immediately due and payable at the election of the relevant lessor. In certain circumstances, this could lead to cross-defaults under Teekay Tankers' other financing agreements, which in turn could result in obligations becoming due and commitments being terminated under such agreements.

The requirements of the bareboat charters are assessed annually or quarterly with reference to vessel valuations compiled by one or more agreed upon third parties. As at June 30, 2021, Teekay Tankers was in compliance with all covenants in respect of its obligations related to finance leases.

The weighted average interest rate on Teekay Tankers’ obligations related to finance leases as at June 30, 2021 was 7.5% (December 31, 2020 – 7.8%).

As at June 30, 2021, the total remaining commitments (including vessel purchase options declared) related to the financial liabilities of these vessels were approximately $352.1 million (December 31, 2020, $480.9 million), including imputed interest of $59.3 million (December 31, 2020 $120.9 million), repayable from 2021 through 2030, as indicated below:

| Commitments | ||||||||

| At June 30, 2021 | ||||||||

| Year | $ | |||||||

| Remainder of 2021 | 142,913 | |||||||

| 2022 | 21,848 | |||||||

| 2023 | 21,846 | |||||||

| 2024 | 21,903 | |||||||

| 2025 | 21,841 | |||||||

| Thereafter | 121,782 | |||||||

Operating Lease Liabilities

The Company charters-in vessels from other vessel owners on time-charter-in and bareboat charter contracts, whereby the vessel owner provides use of the vessel to the Company, and, in the case of time-charter-in contracts, also operates the vessel for the Company. A time-charter-in contract is typically for a fixed period of time, although in certain cases the Company may have the option to extend the charter. The Company typically pays the owner a daily hire rate that is fixed over the duration of the charter. The Company is generally not required to pay the daily hire rate for time charters during periods the vessel is not able to operate.

Page 15

TEEKAY CORPORATION AND SUBSIDIARIES

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

(all tabular amounts stated in thousands of U.S. Dollars, other than share and per share data)

In March 2021, the charter contracts relating to the Suksan Salamander FSO unit were novated to Altera Infrastructure L.P. (or Altera), and the in-charter contract relating to the unit was terminated at the same time. This contract termination resulted in the Company derecognizing the associated right-of use asset and liability of $29.7 million and $29.5 million, respectively.

As at June 30, 2021, total minimum commitments to be incurred by the Company under time-charter-in and bareboat charter contracts were approximately $17.1 million (remainder of 2021), $22.8 million (2022), $9.6 million (2023), $6.8 million (2024), $6.8 million (2025) and $25.0 million (thereafter), including 1 LR2 tanker delivered to the Company in September 2021 to commence an 18-month time charter-in contract, 1 ship-to-ship (or STS) support vessel expected to be delivered to the Company in September 2021 to commence a 2-year time charter-in contract, and 1 Aframax tanker newbuilding expected to be delivered to the Company in the fourth quarter of 2022 to commence a 7-year time charter-in contract. The minimum commitments exclude 2 time charter-in contracts for 2 Aframax tankers that were entered into by Teekay Tankers subsequent to June 30, 2021.

6. Financial Instruments

a)Fair Value Measurements

For a description of how the Company estimates fair value and for a description of the fair value hierarchy levels, see "Item 18 – Financial Statements: Note 11" in the Company’s Annual Report on Form 20-F for the year ended December 31, 2020.

The following table includes the estimated fair value and carrying value of those assets and liabilities that are measured at fair value on a recurring and non-recurring basis, as well as the estimated fair value of the Company’s financial instruments that are not accounted for at fair value on a recurring basis.

| June 30, 2021 | December 31, 2020 | ||||||||||||||||||||||||||||

| Fair Value Hierarchy Level | Carrying Amount Asset (Liability) $ | Fair Value Asset (Liability) $ | Carrying Amount Asset (Liability) $ | Fair Value Asset (Liability) $ | |||||||||||||||||||||||||

| Recurring | |||||||||||||||||||||||||||||

Cash, cash equivalents and restricted cash (note 19) | Level 1 | 310,252 | 310,252 | 405,890 | 405,890 | ||||||||||||||||||||||||

Derivative instruments (note 10) | |||||||||||||||||||||||||||||

Interest rate swap agreements – assets (1) | Level 2 | 1,465 | 1,465 | 0 | 0 | ||||||||||||||||||||||||

Interest rate swap agreements – liabilities (1) | Level 2 | (41,072) | (41,072) | (77,873) | (77,873) | ||||||||||||||||||||||||

Cross currency interest swap agreements – assets (1) | Level 2 | 5,806 | 5,806 | 4,505 | 4,505 | ||||||||||||||||||||||||

Cross currency interest swap agreements – liabilities (1) | Level 2 | (18,510) | (18,510) | (20,022) | (20,022) | ||||||||||||||||||||||||

| Forward freight agreements | Level 2 | (336) | (336) | 0 | 0 | ||||||||||||||||||||||||

| Non-recurring | |||||||||||||||||||||||||||||

Vessels and equipment (2) | Level 2 | 125,125 | 125,125 | 99,967 | 99,967 | ||||||||||||||||||||||||

Vessels related to finance leases (2) | Level 2 | 26,250 | 26,250 | 0 | 0 | ||||||||||||||||||||||||

Vessels held for sale (3) | Level 2 | 11,270 | 11,270 | 31,680 | 31,680 | ||||||||||||||||||||||||

Operating lease right-of-use assets (note 13) | Level 2 | 0 | 0 | 1,799 | 1,799 | ||||||||||||||||||||||||

| Other | |||||||||||||||||||||||||||||

| Loans to equity-accounted investees – current | (4) | 26,899 | (4) | 16,772 | (4) | ||||||||||||||||||||||||

| Advances to equity-accounted investees and joint venture partners – long-term | (4) | 105,436 | (4) | 111,338 | (4) | ||||||||||||||||||||||||

Short-term debt (note 8) | Level 2 | (10,000) | (10,000) | (10,000) | (10,000) | ||||||||||||||||||||||||

Long-term debt – public (note 9) | Level 1 | (589,513) | (612,233) | (587,913) | (597,281) | ||||||||||||||||||||||||

Long-term debt – non-public (note 9) | Level 2 | (1,479,206) | (1,504,140) | (1,467,194) | (1,481,093) | ||||||||||||||||||||||||

Obligations related to finance leases, including current portion (note 5) | Level 2 | (1,597,812) | (1,695,527) | (1,700,965) | (1,868,667) | ||||||||||||||||||||||||

(1)The fair value of the Company's interest rate swap and cross currency swap agreements at June 30, 2021 includes $3.6 million (December 31, 2020 – $6.1 million) of accrued interest expense which is recorded in accrued liabilities on the unaudited consolidated balance sheet.

(2)In June 2021, the carrying values of three Suezmax tankers, three LR2 tankers and one Aframax tankers were written down to their estimated fair values, using appraised values. See Note 13.

(3)In June 2021, the carrying value of one Aframax tanker was written down to its estimated sales price, less selling costs. See Note 13.

(4)In these unaudited interim consolidated financial statements, the Company’s loans to and investments in equity-accounted investments form the aggregate carrying value of the Company’s interests in entities accounted for by the equity method. The fair value of the individual components of such aggregate interests is not determinable.

Page 16

TEEKAY CORPORATION AND SUBSIDIARIES

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

(all tabular amounts stated in thousands of U.S. Dollars, other than share and per share data)

b) Credit Losses

For a description of the Company's exposure to potential credit losses under ASC 326, see "Item 18 – Financial Statements: Note 11b" in the Company’s Annual Report on Form 20-F for the year ended December 31, 2020.

The following table includes the amortized cost basis of the Company's direct interests in financing receivables and net investment in direct financing leases by class of financing receivables and by period of origination and their associated credit quality.

| Amortized Cost Basis by Origination Year | ||||||||||||||||||||||||||||||||||||||

Credit Quality Grade (1) | 2020 | 2018 | 2016 and prior | Total | ||||||||||||||||||||||||||||||||||

| As at June 30, 2021 | $ | $ | $ | $ | ||||||||||||||||||||||||||||||||||

| Sales-type lease – Teekay Parent | ||||||||||||||||||||||||||||||||||||||

Petrojarl Foinaven FPSO | Performing | 14,574 | 0 | 0 | 14,574 | |||||||||||||||||||||||||||||||||

| Direct financing leases – Teekay LNG | ||||||||||||||||||||||||||||||||||||||

Tangguh Hiri and Tangguh Sago | Performing | 0 | 0 | 326,166 | 326,166 | |||||||||||||||||||||||||||||||||

| Bahrain Spirit | Performing | 0 | 210,795 | 0 | 210,795 | |||||||||||||||||||||||||||||||||

| 0 | 210,795 | 326,166 | 536,961 | |||||||||||||||||||||||||||||||||||

| Loans to equity-accounted joint ventures | ||||||||||||||||||||||||||||||||||||||

| Exmar LPG Joint Venture | Performing | 0 | 0 | 32,266 | 32,266 | |||||||||||||||||||||||||||||||||

| Bahrain LNG Joint Venture | Performing | 0 | 0 | 73,375 | 73,375 | |||||||||||||||||||||||||||||||||

| Other | Performing | 660 | 0 | 0 | 660 | |||||||||||||||||||||||||||||||||

| 660 | 0 | 105,641 | 106,301 | |||||||||||||||||||||||||||||||||||

| 15,234 | 210,795 | 431,807 | 657,836 | |||||||||||||||||||||||||||||||||||

| As at December 31, 2020 | ||||||||||||||||||||||||||||||||||||||

| Sales-type lease – Teekay Parent | ||||||||||||||||||||||||||||||||||||||

Petrojarl Foinaven FPSO | Performing | 15,472 | 0 | 0 | 15,472 | |||||||||||||||||||||||||||||||||

| Direct financing leases – Teekay LNG | ||||||||||||||||||||||||||||||||||||||

Tangguh Hiri and Tangguh Sago | Performing | 0 | 0 | 332,308 | 332,308 | |||||||||||||||||||||||||||||||||

| Bahrain Spirit | Performing | 0 | 211,939 | 0 | 211,939 | |||||||||||||||||||||||||||||||||

| 0 | 211,939 | 332,308 | 544,247 | |||||||||||||||||||||||||||||||||||

| Loans to equity-accounted joint ventures | ||||||||||||||||||||||||||||||||||||||

| Exmar LPG Joint Venture | Performing | 0 | 0 | 42,266 | 42,266 | |||||||||||||||||||||||||||||||||

| Bahrain LNG Joint Venture | Performing | 0 | 0 | 73,375 | 73,375 | |||||||||||||||||||||||||||||||||

| Other | Performing | 991 | 0 | 0 | 991 | |||||||||||||||||||||||||||||||||

| 991 | 0 | 115,641 | 116,632 | |||||||||||||||||||||||||||||||||||

| 16,463 | 211,939 | 447,949 | 676,351 | |||||||||||||||||||||||||||||||||||

(1)For a description of how the Company's credit quality grades are determined see "Item 18 – Financial Statements: Note 11b" in the Company’s Annual Report on Form 20-F for the year ended December 31, 2020. As at June 30, 2021, all direct financing and sales-type leases held by the Company and Teekay LNG's equity-accounted joint ventures had a credit quality grade of performing.

Page 17

TEEKAY CORPORATION AND SUBSIDIARIES

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

(all tabular amounts stated in thousands of U.S. Dollars, other than share and per share data)

Changes in the allowance for credit losses for the three and six months ended June 30, 2021 are as follows:

Direct Financing and Sales-Type Leases (1)(2) $ | Direct Financing and Sales-Type Leases and Other within Equity-Accounted Joint Ventures (1)(2) $ | Loans to Equity-Accounted Joint Ventures (1)(2) $ | Guarantees of Debt (1)(2) $ | Total $ | |||||||||||||||||||||||||

Three and Six Months Ended June 30, 2021 | |||||||||||||||||||||||||||||

| As at December 31, 2020 | 31,078 | 54,937 | 4,726 | 2,080 | 92,821 | ||||||||||||||||||||||||

Provision for (reversal of) potential credit losses | 4,726 | 6,677 | (981) | 218 | 10,640 | ||||||||||||||||||||||||

| As at March 31, 2021 | 35,804 | 61,614 | 3,745 | 2,298 | 103,461 | ||||||||||||||||||||||||

Reversal of (provision for) potential credit losses | (404) | 722 | 255 | (298) | 275 | ||||||||||||||||||||||||

| As at June 30, 2021 | 35,400 | 62,336 | 4,000 | 2,000 | 103,736 | ||||||||||||||||||||||||

Three and Six Months Ended June 30, 2020 | |||||||||||||||||||||||||||||

| As at January 1, 2020 | 11,155 | 36,292 | 3,714 | 2,139 | 53,300 | ||||||||||||||||||||||||

(Reversal of) provision for potential credit losses | (100) | 8,980 | 0 | 0 | 8,880 | ||||||||||||||||||||||||

| As at March 31, 2020 | 11,055 | 45,272 | 3,714 | 2,139 | 62,180 | ||||||||||||||||||||||||

Provision for (reversal of) potential credit losses | 465 | (423) | 83 | (288) | (163) | ||||||||||||||||||||||||

| As at June 30, 2020 | 11,520 | 44,849 | 3,797 | 1,851 | 62,017 | ||||||||||||||||||||||||

(1)For a description of how the credit loss provision for direct financing leases, direct financing and sales-type leases and other within equity-accounted joint ventures, loans to equity-accounted joint ventures and guarantees of debt was determined for the three months ended March 31, 2021 and 2020, see "Item 18 – Financial Statements: Note 11b" in the Company’s Annual Report on Form 20-F for the year ended December 31, 2020.

(2)The changes in credit loss provision of ($0.4) million and $4.3 million for the three and six months ended June 30, 2021, respectively ($0.5 million and $0.4 million for the three and six months ended June 30, 2020, respectively), relating to the Company's consolidated vessels, are included in other expense on the unaudited consolidated statements of income. The change in the credit loss provision for the six months ended June 30, 2021 primarily reflects a decline in the estimated charter-free valuations for certain types of Teekay LNG's LNG carriers at the end of their time-charter contract, which are accounted for as direct financing leases. These estimated future charter-free values are subject to change based on the underlying LNG shipping market fundamentals.

The changes in credit loss provision of $0.7 million and $7.4 million for the three and six months ended June 30, 2021, respectively (($0.4) million and $8.6 million for the three and six months ended June 30, 2020, respectively), relating to the direct financing and sales-type leases and other within Teekay LNG's equity-accounted joint ventures are included in equity income. The change in credit loss provision for the six months ended June 30, 2021 primarily reflects a decline in the estimated charter-free valuations for certain types of LNG carriers at the end of their time-charter contract, which are accounted for as direct financing and sales-type leases.

The changes in the credit loss provision for the Company's consolidated vessels and the vessels within Teekay LNG's equity-accounted joint ventures for the six months ended June 30, 2021 do not reflect any material change in expectations of the charterers' ability to make their time-charter hire payments as they come due compared to the beginning of the year.

Page 18

TEEKAY CORPORATION AND SUBSIDIARIES

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

(all tabular amounts stated in thousands of U.S. Dollars, other than share and per share data)

7. Accrued Liabilities and Other and Other Long-Term Liabilities

Accrued Liabilities and Other

| June 30, 2021 | December 31, 2020 | ||||||||||

| $ | $ | ||||||||||

| Accrued liabilities | |||||||||||

| Voyage and vessel expenses | 91,854 | 140,029 | |||||||||

| Interest and distributions | 27,987 | 31,765 | |||||||||

| Payroll and related liabilities | 38,455 | 37,349 | |||||||||

| Deferred revenues – current | 17,800 | 34,461 | |||||||||

Current portion of derivative liabilities (note 10) | 27,248 | 58,186 | |||||||||

| Office lease liability – current | 2,416 | 1,607 | |||||||||

| Loans from equity-accounted investments | 4,243 | 16,689 | |||||||||

| Asset retirement obligation – current | 0 | 12,000 | |||||||||

| 210,003 | 332,086 | ||||||||||

Other Long-Term Liabilities

| June 30, 2021 | December 31, 2020 | ||||||||||

| $ | $ | ||||||||||

| Deferred revenues and gains | 21,567 | 23,732 | |||||||||

| Guarantee liabilities | 10,741 | 11,818 | |||||||||

| Asset retirement obligation | 10,839 | 37,996 | |||||||||

| Pension liabilities | 10,267 | 9,172 | |||||||||

Derivative liabilities (note 10) | 29,130 | 33,566 | |||||||||

Unrecognized tax benefits (note 12) | 71,008 | 70,738 | |||||||||

| Office lease liability – long-term | 11,465 | 9,396 | |||||||||

| Other | 3,860 | 1,689 | |||||||||

| 168,877 | 198,107 | ||||||||||

Asset Retirement Obligations

In the first quarter of 2020, CNR International (U.K.) Limited (or CNRI) provided formal notice to Teekay of its intention to cease production in June 2020 and to decommission the Banff field shortly thereafter. As such, in the third quarter of 2020, the Company removed the Petrojarl Banff FPSO from the Banff field and redelivered the Apollo Spirit FSO to its owners. The Company is currently in the process of recycling the FPSO unit at an EU-approved shipyard and is also required to recycle the subsea equipment following removal from the field (or Phase 2). During the first half of 2020, the asset retirement obligation (or ARO) relating to the Petrojarl Banff FPSO unit and Phase 2 was increased based on changes to cost estimates and the carrying value of the unit was fully written down.

In April 2021, Teekay and CNRI, on behalf of the Banff joint venture, entered into a Decommissioning Services Agreement (or DSA), whereby Teekay engaged CNRI to assume full responsibility for Teekay’s remaining Phase 2 obligations. The DSA was subject to certain conditions precedent that needed to be satisfied by June 1, 2021 (or any agreed extension thereto), failing which the DSA could have been terminated by either party. On May 27, 2021, all conditions precedent of the DSA that needed to be satisfied by June 1, 2021 were met. As such, Teekay was deemed to have fulfilled all of its prior decommissioning obligations associated with the Banff field and the Company derecognized the ARO and its associated receivable, resulting in a $33.0 million gain that has been included in asset retirement obligation extinguishment gain in the consolidated statements of (loss) income for the three and six months ended June 30, 2021.

In March 2020, Teekay Parent entered into a new bareboat charter contract with the existing charterer of the Petrojarl Foinaven FPSO unit, which can be extended up to December 2030. Under the terms of the new contract, Teekay received a cash payment of $67 million in April 2020, and will receive a nominal per day rate over the life of the contract and a fixed lump sum payment at the end of the contract period, which is expected to cover the costs of recycling the FPSO unit in accordance with the EU Ship Recycling Regulation. However, the extent to which this lump sum payment covers the costs of recycling the FPSO unit will depend on a number of factors when the recycling is completed, including the nature and extent of prevailing EU Ship Recycling Regulation, the condition of the FPSO unit, and the availability of recycling facilities, among other factors.

In April 2021, the charterer of the Petrojarl Foinaven FPSO unit announced its decision to suspend production from the Foinaven oil fields and permanently remove the Petrojarl Foinaven FPSO unit from the site. The Company currently expects the FPSO unit will be redelivered to Teekay Parent in the third quarter of 2022, at which point the Company expects to receive the fixed lump sum payment from the charterer and intends to green-recycle the FPSO unit. Although the Company has not changed its cost estimate to recycle the Petrojarl

Page 19

TEEKAY CORPORATION AND SUBSIDIARIES

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

(all tabular amounts stated in thousands of U.S. Dollars, other than share and per share data)

Foinaven FPSO unit, during the three months ended June 30, 2021, the Company increased the present value of its estimated ARO liability relating to the FPSO unit by $2.7 million as a result of the earlier than expected redelivery of the FPSO unit, which has been included in other loss in the consolidated statements of (loss) income. As of June 30, 2021, the carrying value of the related lease asset was $14.6 million, which is comprised of the expected fixed lump sum payment, the expected residual value of the asset and the day rate to be received over the remaining life of the contract. As of June 30, 2021, the present value of the Petrojarl Foinaven FPSO unit's estimated ARO relating to recycling costs was $10.7 million.

8. Short-Term Debt

In November 2018, Teekay Tankers Chartering Pte. Ltd. (or TTCL), a wholly-owned subsidiary of Teekay Tankers, entered into a working capital revolving loan facility (or the Working Capital Loan), which initially provided available aggregate borrowings of up to $40.0 million for TTCL, and had an initial maturity date in May 2019, subject to extension as described below. The maximum available aggregate borrowings were subsequently increased to $80.0 million, effective December 2019. The amount available for drawdown is limited to a percentage of certain receivables and accrued revenue, which is assessed weekly. The next maturity date of the Working Capital Loan is in November 2021. The Working Capital Loan maturity date is continually extended for further periods of six months thereafter unless and until the lender gives notice in writing that no further extensions shall occur. Proceeds of the Working Capital Loan are used to provide working capital in relation to certain vessels subject to the revenue sharing agreements (or RSAs). Interest payments are based on LIBOR plus a margin of 3.5%.

The Working Capital Loan is collateralized by the assets of TTCL. The Working Capital Loan requires Teekay Tankers to maintain its paid-in capital contribution under the RSAs and the retained distributions of the RSA counterparties in an amount equal to the greater of (a) an amount equal to the minimum average capital contributed by the RSA counterparties per vessel in respect of the RSA (including cash, bunkers or other working capital contributions and amounts accrued to the RSA counterparties but unpaid) and (b) a minimum capital contribution ranging from $20.0 million to $30.0 million based on the amount borrowed. As at June 30, 2021, $10.0 million (December 31, 2020 – $10.0 million) was owing under this facility, the aggregate available borrowings were $29.8 million (December 31, 2020 - $32.0 million) and the interest rate on the facility was 3.6% (December 31, 2020 – 3.6%). As at June 30, 2021, Teekay Tankers was in compliance with all covenants in respect of this facility.

9. Long-Term Debt

| June 30, 2021 | December 31, 2020 | ||||||||||

| $ | $ | ||||||||||

| Revolving Credit Facilities due through 2024 | 355,000 | 285,000 | |||||||||

| Senior Notes (9.25%) due November 15, 2022 | 243,395 | 243,395 | |||||||||

| Convertible Senior Notes (5%) due January 17, 2023 | 112,184 | 112,184 | |||||||||

| Norwegian Krone-denominated Bonds due through September 2025 | 354,486 | 355,514 | |||||||||

| U.S. Dollar-denominated Term Loans due through 2030 | 892,249 | 938,280 | |||||||||

| Euro-denominated Term Loans due through 2024 | 134,447 | 152,710 | |||||||||

| Total principal | 2,091,761 | 2,087,083 | |||||||||

| Less unamortized discount and debt issuance costs | (23,042) | (31,976) | |||||||||

| Total debt | 2,068,719 | 2,055,107 | |||||||||

| Less current portion | (374,960) | (261,366) | |||||||||

| Long-term portion | 1,693,759 | 1,793,741 | |||||||||

As at June 30, 2021, the Company had 4 revolving credit facilities (collectively, the Revolvers) available. The Revolvers, as at such date, provided for aggregate borrowings of up to $883.9 million, of which $528.9 million was undrawn. Interest payments are based on LIBOR plus a margin. At June 30, 2021 and December 31, 2020, the margins ranged between 1.40% and 4.25%. As at June 30, 2021, the aggregate amount available under the Revolvers was scheduled to decrease by $56.5 million (remainder of 2021), $560.8 million (2022), $65.3 million (2023) and $201.3 million (2024). The Revolvers are collateralized by first-priority mortgages granted on 33 of the Company’s vessels, together with other related security, and include a guarantee from Teekay or its subsidiaries for all but 1 of the Revolvers' outstanding amounts. Included in other related security are 36.0 million common units in Teekay LNG and 5.0 million Class A common shares in Teekay Tankers to secure a $150 million credit facility.

In May 2019, the Company issued $250.0 million in aggregate principal amount of 9.25% senior secured notes at par due November 2022 (or the 2022 Notes). The 2022 Notes are guaranteed on a senior secured basis by certain of Teekay's subsidiaries and are secured by a first-priority lien on 1 of Teekay Parent's FPSO units, a pledge of the equity interests in Teekay's subsidiary that owns all of Teekay's common units of Teekay LNG and all of Teekay’s Class A common shares of Teekay Tankers, and a pledge of the equity interests in Teekay's subsidiaries that own or previously owned Teekay Parent’s FPSO units.

Page 20

TEEKAY CORPORATION AND SUBSIDIARIES

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

(all tabular amounts stated in thousands of U.S. Dollars, other than share and per share data)

The Company may redeem the 2022 Notes in whole or in part at a redemption price equal to a percentage of the principal amount of the 2022 Notes to be redeemed plus accrued and unpaid interest to, but excluding, the redemption date as follows: 104.625% at any time on or after November 15, 2020, but prior to November 15, 2021; 102.313% at any time on or after November 15, 2021, but prior to August 15, 2022; and 100% at any time on or after August 15, 2022. During 2020, Teekay Parent repurchased 2022 Notes in the open market. Teekay Parent acquired $6.6 million of the principal of the 2022 Notes for total consideration of $6.2 million.

On January 26, 2018, Teekay Parent completed a private offering of $125.0 million in aggregate principal amount of 5% Convertible Senior Notes due January 15, 2023 (or the Convertible Notes). At the election of the holder, the Convertible Notes are convertible into Teekay’s common stock, initially at a rate of 85.4701 shares of common stock per $1,000 principal amount of Convertible Notes. This represents an initial effective conversion price of $11.70 per share of common stock. The initial conversion price represents a premium of 20% to the concurrent common stock offering price of $9.75 per share. On issuance of the Convertible Notes, $104.6 million of the net proceeds was reflected in long-term debt, including unamortized discount, and was being accreted to its par value over its five-year term through interest expense until the adoption of ASU 2020-06 on January 1, 2021 (see Note 2). The remaining amount of the net proceeds of $16.1 million was allocated to the conversion feature and reflected in additional paid-in capital. During 2020, Teekay Parent repurchased $12.8 million of the principal of the Convertible Notes for total consideration of $10.5 million and as such the outstanding principal value of the Convertible Notes on June 30, 2021 and January 1, 2021, was $112.2 million. As of June 30, 2021 and January 1, 2021, the net carrying amount of the Convertible Notes was $111.0 million and $110.6 million, respectively, which reflected unamortized debt issuance costs of $1.2 million and $1.6 million, respectively. The estimated fair value (Level 2) of the Convertible Notes was $110.0 million and $101.6 million, as of June 30, 2021 and January 1, 2021. For the three and six months ended June 30, 2021, total interest expense for the Convertible Notes was $1.6 million and $3.2 million, respectively, with coupon interest expense of $1.4 million and $2.8 million, respectively, and amortization of debt issuance costs of $0.2 million and $0.4 million, respectively.

As at June 30, 2021, Teekay LNG had a total of Norwegian Krone (or NOK) 3.1 billion in senior unsecured bonds issued in the Norwegian bond market that mature through 2025 (December 31, 2020 – NOK 3.1 billion). As at June 30, 2021, the total carrying amount of the senior unsecured bonds was $354.5 million (December 31, 2020 – $355.5 million). The bonds are listed on the Oslo Stock Exchange. The interest payments on the bonds are based on Norwegian Interbank Offered Rate (or NIBOR) plus a margin, which ranges from 4.60% to 6.00% as at June 30, 2021 (December 31, 2020 - 4.60% to 6.00%). The Company entered into cross currency rate swaps to swap all interest and principal payments of the bonds into U.S. Dollars, with the interest payments fixed at rates ranging from 5.74% to 7.89% (December 31, 2020 - 5.74% to 7.89%), and the transfer of the principal amount fixed at $360.5 million upon maturity in exchange for NOK 3.1 billion (see Note 10).

As at June 30, 2021, the Company had 7 U.S. Dollar-denominated term loans outstanding, which totaled $892.2 million in aggregate principal amount (December 31, 2020 – $938.3 million). Interest payments on the term loans are based on LIBOR plus a margin, of which 1 of the term loans has an additional tranche with a weighted average fixed rate of 4.26%. At June 30, 2021 and at December 31, 2020, the margins ranged between 1.85% and 3.25%. The term loans require payments in quarterly installments commencing three months after drawdown, and 6 of the term loans have balloon or bullet repayments due at maturity. The term loans are collateralized by first-priority mortgages on 19 (December 31, 2020 – 20) of the Company’s vessels, together with certain other security.

Teekay LNG has 2 Euro-denominated term loans outstanding, which, as at June 30, 2021, totaled 113.4 million Euros ($134.4 million) (December 31, 2020 – 125.0 million Euros ($152.7 million)). Teekay LNG is servicing the loans with funds generated by 2 Euro-denominated, long-term time-charter contracts. Interest payments for one of the term loans are based on Euro Interbank Offered Rate (or EURIBOR) plus a margin. Interest payments on the remaining term loan are based on EURIBOR where EURIBOR is limited to zero or above zero values, plus a margin. At June 30, 2021 and December 31, 2020, the margins ranged between 0.60% and 1.95%. The Euro-denominated term loans reduce in monthly and semi-annual payments with varying maturities through 2024, are collateralized by first-priority mortgages on 2 of Teekay LNG's vessels, together with certain other security, and are guaranteed by Teekay LNG and 1 of its subsidiaries.

Both Euro-denominated term loans and NOK-denominated bonds are revalued at the end of each period using the then-prevailing U.S. Dollar exchange rate. Due primarily to the revaluation of the Company’s NOK-denominated bonds, the Company’s Euro-denominated term loans and restricted cash and the change in the valuation of the Company’s cross currency swaps, the Company recognized a foreign exchange loss of $3.4 million (2020 – loss of $8.9 million) and a gain of $2.3 million (2020 - loss of $2.3 million) during the three and six months ended June 30, 2021 and 2020, respectively.

The weighted-average interest rate on the Company’s aggregate long-term debt as at June 30, 2021 was 3.9% (December 31, 2020 – 3.8%). This rate does not include the effect of the Company’s interest rate swap agreements (see Note 10).