UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM10-K/A

(Amendment No. 1)

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

FOR THE FISCAL YEAR ENDED DECEMBER 31, 2017

Commission FileNo. 1-12504

THE MACERICH COMPANY

(Exact name of registrant as specified in its charter)

| MARYLAND | 95-4448705 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification Number) |

401 Wilshire Boulevard, Suite 700, Santa Monica, California 90401

(Address of principal executive office, including zip code)

Registrant’s telephone number, including area code(310) 394-6000

Securities registered pursuant to Section 12(b) of the Act

Title of each class | Name of each exchange on which registered | |

| Common Stock, $0.01 Par Value | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act YES ☒ NO ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act YES ☐ NO ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. YES ☒ NO ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 ofRegulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). YES ☒ NO ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 ofRegulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of thisForm 10-K or any amendment on to thisForm 10-K. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, anon-accelerated filer, a smaller reporting company or emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” inRule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | ☒ | Accelerated filer | ☐ | |||

| Non-accelerated filer | ☐ (Do not check if a smaller reporting company) | Smaller reporting company | ☐ | |||

| Emerging growth company | ☐ | |||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined inRule 12b-2 of the Exchange Act). YES ☐ NO ☒

The aggregate market value of voting andnon-voting common equity held bynon-affiliates of the registrant was approximately $8.2 billion as of the last business day of the registrant’s most recently completed second fiscal quarter based upon the price at which the common shares were last sold on that day.

Number of shares outstanding of the registrant’s common stock, as of February 21, 2018: 140,852,118 shares

DOCUMENTS INCORPORATED BY REFERENCE

The following documents (or parts thereof) are incorporated by reference into the following parts of this Form10-K/A: None

EXPLANATORY NOTE

This Amendment No. 1 to Form10-K (this “Amendment”) amends the Annual Report on Form10-K for the fiscal year ended December 31, 2017, originally filed on February 23, 2018 (the “Original Filing”) by The Macerich Company, a Maryland corporation, (“Macerich”, the “Company”, “we” or “us”). We are filing this Amendment to present the information required by Part III of theForm 10-K, as we will not file our definitive proxy statement within 120 days of the end of our fiscal year ended December 31, 2017.

Except as described above, no other changes have been made to the Original Filing. The Original Filing continues to speak as of the date of the Original Filing, and we have not updated the disclosures contained therein to reflect any events which occurred at a date subsequent to the filing of the Original Filing.

INDEX

ITEM | PAGE | |||||

| PART III | ||||||

| ITEM 10 | 3 | |||||

| 3 | ||||||

| 4 | ||||||

| 11 | ||||||

| 11 | ||||||

| 11 | ||||||

| 11 | ||||||

| ITEM 11 | 12 | |||||

| 12 | ||||||

| 14 | ||||||

| 15 | ||||||

| 30 | ||||||

| 46 | ||||||

| 46 | ||||||

| ITEM 12 | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 47 | ||||

| 47 | ||||||

| 48 | ||||||

| 50 | ||||||

| 51 | ||||||

| ITEM 13 | Certain Relationships and Related Transactions, and Director Independence | 53 | ||||

| 53 | ||||||

| 53 | ||||||

| 53 | ||||||

| ITEM 14 | 54 | |||||

| 54 | ||||||

| 54 | ||||||

| PART IV | ||||||

| ITEM 15 | 56 | |||||

2

Part III

Item 10.Directors, Executive Officers and Corporate Governance.

The following table sets forth, as of April 30, 2018, the names, ages and positions of our executive officers and the year each became an officer.

Name | Age | Position | Officer Since | |||||||

Arthur M. Coppola | 66 | Chairman of the Board of Directors and Chief Executive Officer | 1993 | |||||||

Edward C. Coppola | 63 | President | 1993 | |||||||

Thomas E. O’Hern | 62 | Senior Executive Vice President, Chief Financial Officer and Treasurer | 1993 | |||||||

Ann C. Menard | 55 | Executive Vice President, Chief Legal Officer and Secretary | 2018 | |||||||

On April 19, 2018, Mr. Arthur M. Coppola informed our Board that he will retire from his position as Chairman of the Board effective as of our Annual Meeting and from his position as CEO effective December 31, 2018.

Mr. Thomas J. Leanse retired from his position as Senior Executive Vice President, Chief Legal Officer and Secretary of our Company effective February 28, 2018. Ann C. Menard, who joined our Company on January 29, 2018 as an Executive Vice President, has been our Chief Legal Officer and Secretary since March 1, 2018.

On April 26, 2018, the Company announced that (i) Thomas E. O’Hern will be appointed to the role of Chief Executive Officer, effective as of January 1, 2019, (ii) Scott Kingsmore, our Senior Vice President of Finance, will be appointed to the role of Executive Vice President, Chief Financial Officer and Treasurer, effective as of January 1, 2019 and (iii) Robert D. Perlmutter notified us on April 20, 2018 that he was resigning as our Senior Executive Vice President and Chief Operating Officer, effective as of such date.

Biographical information concerning Messrs. A. Coppola and E. Coppola is set forth below under “Director Biographical Information.”

Thomas E. O’Hern became one of our Senior Executive Vice Presidents in September 2008 and has been our Chief Financial Officer and Treasurer since July 1994. Mr. O’Hern was an Executive Vice President from December 1998 through September 2008 and served as a Senior Vice President from March 1993 to December 1998. From our formation to July 1994, he served as Chief Accounting Officer, Treasurer and Secretary. From November 1984 to March 1993, Mr. O’Hern was a Chief Financial Officer at various real estate development companies. He was also a certified public accountant with Arthur Andersen & Co. and he was with that firm from 1978 through 1984. Mr. O’Hern is a member of the board of directors, the audit committee chairman and a member of the nominating and corporate governance committee of Douglas Emmett, Inc., a publicly traded REIT. Mr. O’Hern also serves on The USC Marshall School of Business Board of Leaders.

Ann C. Menard joined our Company on January 29, 2018 as an Executive Vice President and has been our Chief Legal Officer and Secretary since March 1, 2018. Prior to joining our Company, Ms. Menard was U.S. General Counsel and Managing Director for Tishman Speyer, a global real estate owner, operator, developer and fund manager from October 2005 through December 2017, where she managed legal activities and risk in connection with operations in major U.S. markets including Los Angeles, San Francisco, Silicon Valley, Seattle, Chicago and Atlanta. Prior to joining Tishman Speyer, Ms. Menard was a partner in the real estate and corporate finance departments at O’Melveny & Myers, LLP in their Los Angeles and Newport Beach offices. Ms. Menard received her JD, magna cum laude, from Loyola Law School of Los Angeles in 1991, after graduating with a Bachelor of Arts degree from the University of California, Los Angeles in 1985.

3

The following provides certain biographical information with respect to our current directors as of April 30, 2018 as well as the specific experience, qualifications, attributes and skills that led our Board to conclude that each director should serve as a member of our Board of Directors. Each director has served continuously since elected. On January 31, 2018, Mr. John M. Sullivan informed the Board that he will not stand for re-election at our 2018 Annual Meeting.

Peggy Alford

Independent Director

Director Since:2018

Age:47

Board Committees:Audit

Principal Occupation and Business Experience:

Ms. Alford is the Chief Financial Officer and Head of Operations for the Chan Zuckerberg Initiative, a philanthropic organization that brings together world-class engineering, grant-making, impact investing, policy and advocacy work, overseeing finance, real estate, facilities and general operations. Prior to joining the Chan Zuckerberg Initiative in September 2017, Ms. Alford held a variety of senior positions at PayPal from May 2011 to August 2017, including Vice President, Chief Financial Officer of Americas, Global Customer and Global Credit, where she was responsible for all finance and analytics for PayPal’s Global Merchant and Global Consumer Business Units, its Global Credit business, and its North America and Latin America regions. She also served as PayPal’s Senior Vice President of Human Resources, People Operations and Global Head of Cross Border Trade. From 2007 to 2011, Ms. Alford was President and General Manager of Rent.com (an eBay Inc. company), also serving as its Chief Financial Officer from October 2005 to March 2009. From 2002 to 2005 she served as Marketplace Controller and Director of Accounting Policy, leading accounting policy at eBay Inc. where she was instrumental in creating eBay marketplace controller’s group ensuring the financial integrity of eBay transactions. Ms. Alford started her career at Arthur Andersen LLP in 1993 as an auditor and business consultant in such industries as technology, consumer products, manufacturing, government and education. Ms. Alford earned a Bachelor of Science degree in Accounting and Business Administration from the University of Dayton and is a certified public accountant.

Key Qualifications, Experience and Attributes:

As a new Board member, Ms. Alford’s wide-ranging financial and operational experience, digital, technology and omnichannel knowledge and significant experience leading complex businesses are invaluable to our Board. Her fresh perspectives and contributions to our Company are also informed by Ms. Alford’s strong digital expertise and track record of driving growth and innovation through data analytics, areas which have become increasingly critical drivers of our business. In addition to her strong managerial and operational background, Ms. Alford brings deep financial expertise to our Board, based on which she serves on our Audit Committee and has been determined by our Board to be an audit committee financial expert.

John H. Alschuler

Independent Director

Director Since:2015

Age:70

Board Committees:Nominating and Corporate Governance

Other Public Company Boards:SL Green Realty Corporation; Xenia Hotels and Resorts, Inc.

Principal Occupation and Business Experience:

Since 2008, Mr. Alschuler has been the Chairman of HR&A Advisors Inc., an economic development, real estate and public policy consulting organization. Mr. Alschuler also is an Adjunct Associate Professor at Columbia University, where he teaches real estate development at the Graduate School of Architecture, Planning & Preservation. Mr. Alschuler currently serves on the board of directors of SL Green Realty Corporation and Xenia Hotels and Resorts, Inc., both of which are publicly traded REITs. Mr. Alschuler also serves on the board of directors of the Center for an Urban Future, a Section 501(c)(3) tax exempt organization, and Friends of the High Line Inc., a Section 501(c)(3) tax exempt organization.

4

Key Qualifications, Experience and Attributes:

Mr. Alschuler’s achievements in academia and business, as well as his extensive knowledge of commercial real estate and national and international markets for real estate, and his expertise in inter-governmental relations, allow him to assess the real estate market and our Company’s business from a knowledgeable and informed perspective. His experience on boards of other public and private companies further enhances his range of knowledge.

Arthur M. Coppola

Director

Director Since:1994

Age:66

Board Committees:Executive (Chair)

Principal Occupation and Business Experience:

Mr. A. Coppola has been our Chief Executive Officer since our formation and was elected Chairman of the Board in September 2008. Mr. A. Coppola’s term as Chairman of the Board will end at our 2018 Annual Meeting and his term as Chief Executive Officer will end December 31, 2018. As Chairman of the Board and Chief Executive Officer, Mr. A. Coppola is responsible for the strategic direction and overall management of our Company. He served as our President from our formation until his election as Chairman. Mr. A. Coppola is one of our Company’s founders and has over 42 years of experience in the shopping center industry, all of which has been with The Macerich Group and our Company. From 2005 through 2010, Mr. A. Coppola was a member of the board of governors or the executive committee of the National Association of Real Estate Investment Trusts, Inc. (“Nareit”), served as the 2007 chair of the board of governors and received the 2009 Nareit Industry Leadership Award. Mr. A. Coppola is also an attorney and a certified public accountant.

Key Qualifications, Experience and Attributes:

As Chairman and CEO, our Board has valued Mr. A. Coppola’s strategic direction and vision which has resulted in our Company growing from a privately held real estate company to a dominant national regional mall company that is part of the S&P 500, with a portfolio of approximately 53 million square feet of gross leasable area primarily in 48 regional shopping centers across the United States. He is a recognized leader within the REIT industry. Mr. A. Coppola’s knowledge of our Company and the REIT industry, as well as his extensive business relationships with investors, retailers, financial institutions and peer companies, provide our Board with critical information necessary to oversee and direct the management of our Company. His role and experiences at our Company and within our industry give him unique insights into our Company’s opportunities, operations and challenges.

Edward C. Coppola

Director

Director Since:1994

Age:63

Principal Occupation and Business Experience:

Mr. E. Coppola was elected our President in September 2008. In partnership with our Chief Executive Officer, Mr. E. Coppola oversees the strategic direction of our Company. He has broad oversight over our Company’s financial and investment strategies, including our Company’s key lender and investor relationships. He also oversees our acquisitions and dispositions, department store relationships and development/redevelopment projects. Mr. E. Coppola was previously an Executive Vice President from our formation through September 2004 and was our Senior Executive Vice President and Chief Investment Officer from October 2004 until his election as President. He has over 40 years of shopping center experience with The Macerich Group and our Company and is one of our founders. From March 16, 2006 to February 2, 2009, Mr. E. Coppola was a member of the board of directors of Strategic Hotels & Resorts, Inc., a publicly traded REIT which owns and manages high end hotels and resorts. Mr. E. Coppola is also an attorney.

5

Key Qualifications, Experience and Attributes:

Mr. E. Coppola has deep relationships and experience in our industry and in the retail and shopping center landscape. As President, Mr. E. Coppola provides our Board with important information about the overall conduct of our Company’s business and valuable knowledge and perspective regarding our operations, plans and direction. Our Board appreciates his long history and experience in the shopping center industry as well as his expertise with respect to strategic and investment planning, finance, capital markets, acquisition, disposition and development matters.

Steven R. Hash

Independent Director

Director Since:2015

Age:53

Board Committees:Audit (Chair); Compensation; Executive

Other Public Company Boards:Alexandria Real Estate Equities, Inc.

Principal Occupation and Business Experience:

Mr. Hash is the President and Chief Operating Officer of Renaissance Macro Research, LLC, an equity research and trading firm focused on macro research in the investment strategy, economics and Washington policy sectors, which heco-founded in 2012. Mr. Hash is a member of the board of directors of Alexandria Real Estate Equities, Inc., a publicly traded REIT, where he serves as the lead independent director, chair of the compensation committee and is a member of the audit committee. Mr. Hash is also a member of the board of directors of Nureen Global Cities REIT, Inc., anon-traded REIT. He is the lead independent director and a member of the audit committee. Between 1993 and 2012, Mr. Hash held various leadership positions with Lehman Brothers (and its successor, Barclays Capital), including Global Head of Real Estate Investment Banking from 2006 to 2012, Chief Operating Officer of Global Investment Banking from 2008 to 2011, Director of Global Equity Research from 2003 to 2006, Director of U.S. Equity Research from 1999 to 2003, and Senior Equity Research Analyst from 1993 to 1999 covering the Real Estate Investment Trusts sector. From 1990 to 1993, Mr. Hash held various positions with Oppenheimer & Company’s Equity Research Department, including senior research analyst. He began his career in 1988 as an auditor for the accounting and consulting firm of Arthur Andersen & Co.

Key Qualifications, Experience and Attributes:

Mr. Hash brings to our Board extensive knowledge of real estate investment strategy and economic trends through years of real estate industry research and investment banking both domestically and internationally. In addition to important insights into the equity and capital markets and investor perspectives, he has valuable experience in accounting and financial reporting based upon his years as an auditor and senior equity research analyst. He also has important corporate governance and board leadership expertise through his positions at other publicly traded companies and at our Company. He also has experience in human capital management and talent development matters. Mr. Hash serves as Chairperson of our Audit Committee and has been determined by our Board to be an audit committee financial expert. In August 2017, Mr. Hash was chosen by our independent directors to serve as our Lead Director and appointed to serve as our independent Chairman of the Board as of the 2018 Annual Meeting when our Board separates the Chair and CEO positions.

6

Diana M. Laing

Independent Director

Director Since:2003

Age:63

Board Committees:Audit

Principal Occupation and Business Experience:

Ms. Laing is the Chief Financial Officer of American Homes 4 Rent, a publicly traded REIT focused on the acquisition, renovation, leasing and operation of single-family homes as rental properties and has served in such capacity since May 2014. From May 2004 until its merger with Parkway Properties of Orlando, Florida in December 2013, Ms. Laing was the Chief Financial Officer and Secretary of Thomas Properties Group, Inc., a publicly traded real estate operating company and institutional investment manager focused on the development, acquisition, operation and ownership of commercial properties throughout the United States. She was responsible for financial reporting, capital markets transactions and investor relations. Ms. Laing served as Chief Financial Officer of each of Triple Net Properties, LLC from January through April 2004, New Pacific Realty Corporation from December 2001 to December 2003, and Firstsource Corp. from July 2000 to May 2001. From August 1996 to July 2000, Ms. Laing was Executive Vice President, Chief Financial Officer and Treasurer of Arden Realty, Inc., a publicly traded REIT which was the largest owner and operator of commercial office properties in Southern California. From 1982 to August 1996, she served in various capacities, including Executive Vice President, Chief Financial Officer and Treasurer of Southwest Property Trust, Inc., a publicly traded multi-family REIT which owned multi-family properties throughout the southwestern United States. Ms. Laing began her career as an auditor with Arthur Andersen & Co. She serves on the advisory boards to the Dean of the Spears School of Business and the Chairman of the School of Accounting at Oklahoma State University and is a member of the Board of Trustees of the Oklahoma State University Foundation.

Key Qualifications, Experience and Attributes:

Our Board believes Ms. Laing’s over 35 years of real estate industry experience, with her particular expertise in finance, capital markets, strategic planning, budgeting and financial reporting, make her a valuable member of our Board. This financial and real estate experience is supplemented by her substantive public company and REIT experience which enhances her understanding of the issues facing our Company and industry. Based on her financial expertise, Ms. Laing serves on our Audit Committee and has been determined by our Board to be an audit committee financial expert.

Mason G. Ross

Independent Director

Director Since:2009

Age:74

Board Committees:Nominating and Corporate Governance (Chair)

Principal Occupation and Business Experience:

Mr. Ross spent 35 years at Northwestern Mutual Life, an industry-leading life insurance company, the final nine years of which he served as Executive Vice President and Chief Investment Officer. As Chief Investment Officer, his responsibilities included the design and administration of investment compensation systems, oversight of investment risk management, and the formation of the asset allocation strategy of the investment portfolio. During his prior 27 years at Northwestern Mutual Life, he held a variety of positions, including leading the company’s real estate investment and private securities operations. During that time, he also served as a director of Robert W. Baird, Inc., a regional brokerage and investment banking firm, and the Russell Investment Group, an international investment management firm. Since retiring from Northwestern Mutual Life in 2007, he has remained active in the investment business and currently serves as chairman of the board of Schroeder Manatee Ranch Inc., a privately held real estate company and as a trustee of several large private trusts. He is the past chairman of the National Association of Real Estate Investment Managers and a former trustee of the Urban Land Institute.

7

Key Qualifications, Experience and Attributes:

Our Board values the over 40 years of investment experience of Mr. Ross and his extensive involvement in commercial real estate. His real estate financing expertise acquired over a 25 year period of providing real estate financing for all types of properties provides our Board with important knowledge in considering our Company’s capital and liquidity needs.

Steven L. Soboroff

Independent Director

Director Since:2014

Age:69

Board Committees:Audit; Compensation; Nominating and Corporate Governance

Principal Occupation and Business Experience:

Steve Soboroff is the managing partner of Soboroff Partners, a shopping center development and leasing company, and has served in such capacity since 1978. In September 2017, Mr. Soboroff was selected to serve a secondtwo-year term as President of the Los Angeles Police Commission. In August 2013, Mr. Soboroff was appointed to the Board of Police Commissioners by Los Angeles Mayor Eric Garcetti and was chosen as the Commission’s President by his fellow commissioners. After serving the maximum of two consecutive years as President, he then served as the Commission’s Vice President from September 2015 to September 2017. During 2001 to 2010, he served in the roles of Chairman and CEO as well as President of Playa Vista, one of the country’s most significantmulti-use real estate projects. Mr. Soboroff also was President of the Los Angeles Recreation and Parks Commission from 1995 to 2001 and a member of the Los Angeles Harbor Commission. In addition, Mr. Soboroff is a board member of severalnon-profit philanthropic and academic organizations.

Key Qualifications, Experience and Attributes:

Mr. Soboroff is a well-recognized business and government leader with a distinguished record of public and private accomplishments. Mr. Soboroff contributes to the mix of experience and qualifications of our Board through both his real estate and government experience and leadership. During his career in both the public and private sectors, Mr. Soboroff acquired significant financial, real estate, managerial, and public policy knowledge as well as substantial business and government relationships. Our Board values his extensive real estate knowledge and insight into retail operations, developments and strategy, and his wealth of government relations experience.

8

Andrea M. Stephen

Independent Director

Director Since:2013

Age:53

Board Committees:Compensation (Chair); Executive

Other Public Company Boards:First Capital Realty, Inc.; Boardwalk Real Estate Investment Trust; Slate Retail Real Estate Investment Trust

Principal Occupation and Business Experience:

Ms. Stephen served as Executive Vice President, Investments for The Cadillac Fairview Corporation Limited (“Cadillac Fairview”), one of North America’s largest real estate companies, from October 2002 to December 2011 and as Senior Vice President, Investments for Cadillac Fairview from May 2000 to October 2002, where she was responsible for developing and executing Cadillac Fairview’s investment strategy. Prior to joining Cadillac Fairview, Ms. Stephen held the position of Director, Real Estate with the Ontario Teachers’ Pension Plan Board, the largest single profession pension plan in Canada, from December 1999 to May 2000, as well as various portfolio manager positions from September 1995 to December 1999. Previously, Ms. Stephen served as Director, Financial Reporting for Bramalea Centres Inc. for approximately two years and as an Audit Manager for KPMG LLP at the end of her over six year tenure. Ms. Stephen is a member of the board of directors of First Capital Realty Inc., Canada’s leading owner, developer and operator of supermarket and drugstore anchored neighborhood and community shopping centers, serving on the audit committee, compensation committee, governance committee and the executive committee. She is also a member of the board of trustees, serving on the audit committee, of Boardwalk Real Estate Investment Trust, Canada’s leading owner and operator of multifamily communities. In June 2017, Ms. Stephen was elected to the board of trustees of Slate Retail Real Estate Investment Trust and serves on its audit, compensation and investment committees. Ms. Stephen also previously served on the board of directors of Multiplan Empreendimentos Imobiliários, S.A., a Brazilian real estate operating company, from June 2006 to March 2012.

Key Qualifications, Experience and Attributes:

With over 25 years in the real estate industry and extensive transactional and management experience, Ms. Stephen has a broad understanding of the operational, financial and strategic issues facing real estate companies. She brings management expertise, leadership capabilities, financial knowledge and business acumen to our Board. Her significant international investment experience also provides a global perspective as well as international relationships. In addition, her service on various boards provides valuable insight and makes her an important contributor to our Board.

John M. Sullivan

Independent Director

Director Since:2014

Age:57

Other Public Company Boards:Multiplan Empreendimentos Imobiliários, S.A.; Dream Global REIT

Principal Occupation and Business Experience:

Mr. Sullivan is the President and Chief Executive Officer of Cadillac Fairview and has served in such position since January 2011. Mr. Sullivan was previously the Executive Vice President of Development of Cadillac Fairview from November 2006 to January 2011. Prior to joining Cadillac Fairview, he held positions with Brookfield Properties Corporation and Marathon Realty Company Limited. Mr. Sullivan serves on the board of directors of Multiplan Empreendimentos Imobiliários, S.A., a Brazilian real estate operating company, and is a member of the board of directors and audit committee of Dream Global REIT, an open ended Canadian REIT focusing on international commercial real estate. In addition, Mr. Sullivan serves as a trustee of the International Council of Shopping Centers, an international shopping center industry trade association, and as Chairman of the Real Property Association of Canada, a national industry association for owners and managers of investment real estate.

9

Key Qualifications, Experience and Attributes:

Our Board values Mr. Sullivan’s over 25 years of extensive real estate experience and relationships which enhances our Company and Board. Mr. Sullivan brings to our Board strong executive management expertise, leadership and financial acumen, as well as significant transactional, leasing, finance, asset management and development experience in the commercial real estate industry. As a CEO, he has a unique knowledge of the issues companies address, ranging from strategic and operational to corporate governance and risk management. In addition, Mr. Sullivan has international expertise and public company board service that augment his understanding of the commercial real estate industry and our Company.

10

Section 16(a) Beneficial Ownership Reporting Compliance

Section 16(a) of the Exchange Act requires our executive officers and directors, and persons who own more than 10% of a registered class of our equity securities, to file reports of ownership and changes in ownership with the SEC and the NYSE. Officers, directors and greater than 10% stockholders are required by the SEC’s regulations to furnish our Company with copies of all Section 16(a) forms they file. To our knowledge, based solely on our review of the copies of such reports furnished to our Company during and with respect to the fiscal year ended December 31, 2017, all Section 16(a) filing requirements applicable to our executive officers, directors and greater than 10% beneficial owners were satisfied on a timely basis, with the exception of a failure to file a Form 5 by Mr. O’Hern to report one gift transaction of 1,063 shares of the Company’s Common Stock.

The Board has a separately-designated Audit Committee established in accordance with Section 3(a)(58)(A) and Section 10A(m) of the Exchange Act. The following table identifies the current members of the Audit Committee, its principal functions and the number of meetings held in 2017.

Name of Committee and Current Members | Committee Functions | Number of Meetings | ||

Audit: Steven R. Hash, Chair* Peggy Alford** Diana M. Laing* Steven L. Soboroff

* Audit Committee Financial Expert ** Audit Committee Financial Expert; Appointed to the Audit Committee March 29, 2018 | • appoints, evaluates, approves the compensation of, and, where appropriate, replaces our independent registered public accountants

• reviews our financial statements with management and our independent registered public accountants

• reviews and approves with our independent registered public accountants the scope and results of the audit engagement

• pre-approves audit and permissiblenon-audit services provided by our independent registered public accountants

• reviews the independence and qualifications of our independent registered public accountants

• reviews the adequacy of our internal accounting controls and legal and regulatory compliance

• reviews and approves related-party transactions in accordance with our Related Party Transaction Policies and Procedures | 8 |

Code of Business Conduct and Ethics

The company has adopted a Code of Business Conduct and Ethics that provides principles of conduct and ethics for its directors, officers and employees. This Code complies with the requirements of the Sarbanes-Oxley Act of 2002 and applicable rules of the SEC and the NYSE. In addition, our Company adopted a Code of Ethics for our CEO and senior financial officers which supplements our Code of Business Conduct and Ethics applicable to all employees and complies with the additional requirements of the Sarbanes-Oxley Act of 2002 and applicable SEC rules. To the extent required by applicable SEC rules and NYSE Rules, we intend to promptly disclose future amendments to certain provisions of these Codes or waivers of such provisions granted to directors and executive officers, including our principal executive officer, principal financial officer, principal accounting officer or persons performing similar functions, on our website atwww.macerich.com under “Investors—Corporate Governance—Code of Ethics.” Each of these Codes of Conduct is available on our website atwww.macerich.com under “Investors—Corporate Governance.”

Procedures for Recommending Director Nominees

During 2017, there were no material changes to the procedures described in the Company’s proxy statement relating to the 2017 Annual Meeting of Stockholders by which stockholders may recommend director nominees to the Company.

11

Item 11.Executive Compensation

Compensation ofNon-Employee Directors

Ournon-employee directors are compensated for their services according to an arrangement approved by our Board of Directors and recommended by the Compensation Committee. The Compensation Committee generally reviews director compensation annually. A Board member who is also an employee of our Company or a subsidiary does not receive compensation for service as a director. Messrs. A. Coppola and E. Coppola are currently the only directors who are also employees of our Company or a subsidiary. Upon his election to our Board of Directors in place of Mr. A. Coppola, Mr. O’Hern will be a director who is also an employee of the Company. Mr. Sullivan received no compensation from our Company as a director because his employer’s policies do not allow it, but he was reimbursed for his reasonable expenses.

In July 2016, FW Cook conducted a competitive review of ournon-employee director compensation program, including the review of the director compensation programs of companies within our peer group, and suggested changes for the Compensation Committee’s consideration. Based on the recommendations of the Compensation Committee, our Board of Directors revised certain aspects of ournon-employee director compensation. The following sets forth the compensation structure effective July 21, 2016:

| Annual Retainer for Service on our Board | $70,000 | |

| Annual Equity Award for Service on our Board | $125,000 of restricted stock units based upon the closing price of our Common Stock on the grant date, which is in March of each year. The restricted stock units are granted under our 2003 Incentive Plan and have aone-year vesting period. | |

| Annual Retainer for Lead Director | $50,000 | |

Annual Retainers for Chairs of Audit, Compensation and Nominating & Corporate Governance Committees (in addition to membership retainer) | Audit: $20,000 Compensation: $20,000 Nominating & Corp. Governance: $12,500 | |

| Annual Retainer for Committee Membership | $12,500 | |

| Expenses | The reasonable expenses incurred by each director (including employee directors) in connection with the performance of their duties are reimbursed. |

Non-Employee Director Equity Award Programs

In addition, our Director Phantom Stock Plan offers ournon-employee directors the opportunity to defer cash compensation otherwise payable and to receive that compensation (to the extent that it is actually earned by service during that period) in cash or in shares of Common Stock as elected by the director, after termination of the director’s service or on a specified payment date. Such compensation includes the annual cash retainers payable to ournon-employee directors. A majority of ournon-employee directors serving in 2017 elected to receive all or a portion of their 2017 cash retainers in Common Stock. Deferred amounts are generally credited as stock units at the beginning of the applicable deferral period based on the present value of such deferred compensation divided by the average fair market value of our Common Stock for the preceding 10 trading days. Stock unit balances are credited with additional stock units as dividend equivalents and are ultimately paid out in shares of our Common Stock on aone-for-one basis. A maximum of 500,000 shares of our Common Stock may be issued in total under our Director Phantom Stock Plan, subject to certain customary adjustments for stock splits, stock dividends and similar events. The vesting of the stock units is accelerated in case of the death or disability of a director or, upon the termination of service as a director at the time of or after a change of control event. Our Company has a deferral program for the equity compensation of ournon-employee directors which allows them to defer the receipt of all or a portion of their restricted stock unit awards and receive the underlying Common Stock after termination of service or a specified payment date. Any dividends payable with respect to those deferred restricted stock units will also be deferred and will be paid in accordance with their payment election. The deferred dividend equivalents may be paid in cash or converted into additional restricted stock units and ultimately paid in shares of our Common Stock on aone-to-one basis. The vesting of the deferred restricted stock units is accelerated in case of the death or disability of a director or upon a change of control event.

12

2017Non-Employee Director Compensation

The following table sets forth the compensation paid, awarded or earned with respect to each of ournon-employee directors during 2017. We do not provide ournon-employee directors with initial inducement awards upon joining our Board other than the regular annual equity award granted to our existing directors. Mr. Hubbell resigned from our Board on March 29, 2018 and Ms. Alford joined our Board on March 29, 2018.

Name | Fees Earned or Paid in Cash ($)(1) | Stock Awards ($)(2) | Total ($) | |||||||||

John H. Alschuler | 82,500 | 125,000 | 207,500 | |||||||||

Steven R. Hash | 139,658 | 125,000 | 264,658 | |||||||||

Fred S. Hubbell | 125,274 | 125,000 | 250,274 | |||||||||

Diana M. Laing | 82,500 | 125,000 | 207,500 | |||||||||

Mason G. Ross | 95,000 | 125,000 | 220,000 | |||||||||

Steven L. Soboroff | 107,500 | 125,000 | 232,500 | |||||||||

Andrea M. Stephen | 115,000 | 125,000 | 240,000 | |||||||||

John M. Sullivan(3) | — | — | — | |||||||||

| (1) | Pursuant to our Director Phantom Stock Plan, each director receiving compensation, except Messrs. Hash, Ross and Soboroff, elected to defer fully his or her annual cash retainers for 2017 and to receive such compensation in Common Stock at a future date. Therefore, for 2017 compensation, Messrs. Alschuler and Hubbell and Mses. Laing and Stephen were credited with 1,191, 1,356, 953 and 1,660 stock units, respectively, which vested during 2017 as their service was provided. |

| (2) | The amounts shown represent the grant date fair value computed in accordance with Statement of Financial Accounting Standards Bulletin ASC Topic 718 referred to as “FASB ASC Topic 718,” of restricted stock awards granted under our 2003 Incentive Plan. Any estimated forfeitures were excluded from the determination of these amounts and there were no forfeitures of stock awards during 2017 by our directors. Assumptions used in the calculation of these amounts are set forth in footnote 19 to our audited financial statements for the fiscal year ended December 31, 2017 included in our Annual Report on Form10-K filed with the SEC on February 23, 2018. |

Except for Mr. Sullivan, each of ournon-employee directors received 1,877 restricted stock units on March 3, 2017 under our 2003 Incentive Plan. The closing price per share of our Common Stock on that date was $66.57.

| (3) | Mr. Sullivan’s employer has a policy that does not allow him to hold shares of stock of our Company. |

13

As of December 31, 2017, ournon-employee directors held the following number of unpaid phantom stock units and unvested restricted stock units:

Name | Unpaid Phantom Stock Units (#) | Unvested Restricted Stock Units (#) | ||||||

John H. Alschuler | 2,860 | 1,877 | ||||||

Steven R. Hash | — | 1,877 | ||||||

Fred S. Hubbell | 72,589 | 1,877 | ||||||

Diana M. Laing | 34,232 | 1,877 | ||||||

Mason G. Ross | 10,382 | 1,877 | ||||||

Steven L. Soboroff | — | 1,877 | ||||||

Andrea M. Stephen | 10,025 | 1,877 | ||||||

John M. Sullivan | — | — | ||||||

The Compensation Committee of the Board of Directors of The Macerich Company, a Maryland corporation, has reviewed and discussed the Compensation Discussion and Analysis in this Amendment with management. Based on such review and discussion, the Compensation Committee recommended to our Board of Directors that the Compensation Discussion and Analysis be included in our Annual Report onForm 10-K for the year ended December 31, 2017.

| The Compensation Committee |

Andrea M. Stephen, Chair Steven R. Hash Steven L. Soboroff |

14

COMPENSATION DISCUSSION AND ANALYSIS

The Compensation Discussion & Analysis (“CD&A”) describes the material elements of our executive compensation program, how it is designed to support the achievement of our key strategic and financial objectives, and the compensation decisions the Compensation Committee made under the program for our named executive officers, who for 2017 were:

Named Executive Officers | Title | |

| Arthur M. Coppola(1) | Chairman of the Board of Directors and Chief Executive Officer | |

| Edward C. Coppola | President | |

| Thomas E. O’Hern | Senior Executive Vice President, Chief Financial Officer and Treasurer | |

| Robert D. Perlmutter(2) | Former Senior Executive Vice President and Chief Operating Officer | |

| Thomas J. Leanse(3) | Former Senior Executive Vice President, Chief Legal Officer and Secretary | |

| (1) | Mr. A. Coppola will retire from his position as Chairman of the Board effective as of our 2018 Annual Meeting and from his position as CEO effective December 31, 2018. |

| (2) | Mr. Perlmutter resigned as Senior Executive Vice President and Chief Operating Officer on April 20, 2018. |

| (3) | Mr. Leanse retired from his full time position as Senior Executive Vice President, Chief Legal Officer and Secretary on February 28, 2018; he will continue to consult with the Company on several projects and advise on other matters, as requested. |

For purposes of this CD&A, we refer to the Compensation Committee as the “Committee.”

15

Executive Summary

Business Highlights

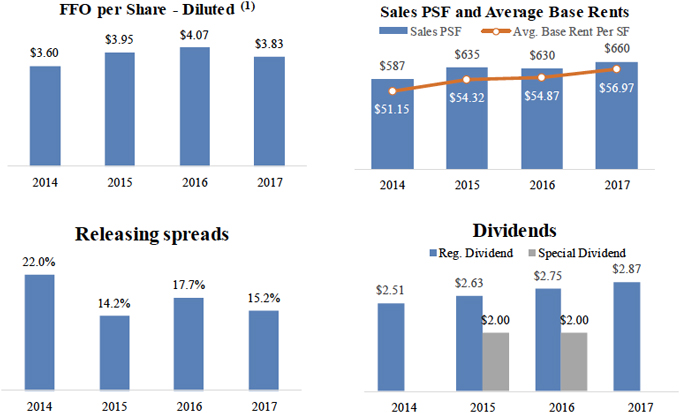

2017 demonstrated continued strength in our operating results and portfolio metrics. As a result of our strong leadership, we continued to seize opportunities and further strengthen our Company and our growth opportunities, as evidenced by our accomplishments below:

| Operational | • Mall tenant annual sales per square foot for the portfolio increased by 4.8% to $660 for the year ended December 31, 2017 compared to $630 for the year ended December 31, 2016.

• Same Center NOI grew 2.73%

• FFO per diluted share was $3.83 in 2017

| |

| Leasing | • Occupancy levels continued to be stable, ending the year at 95.0%

• Releasing spreads for 2017 were up 15.2% from 2016

• Average rent per square foot increased to $56.97, up 3.8% from $54.87 at December 31, 2016

| |

Development and Redevelopment

| • $250 millionin-process pipeline in Philadelphia and New York

• Kings Plaza Shopping Center $100 million redevelopment nears completion

| |

| Sustainability | Macerich is focused on sustainability as a long-term, fully-integrated business approach

• Retail “Leader in the Light” Environmental Award for the fourth consecutive year from the National Association of Real Estate Investment Trusts

• #1 ranking in the U.S. Retail Sector for sustainability performance for real estate portfolios around the world for third straight year, according to scores published by Global Real Estate Sustainability Benchmark (GRESB)

• Recipient of U.S. BREEAM in use building certification at 11 properties

| |

16

In 2017, our Company continued the sector-leading progress we have made in recent years, demonstrating our ability to consistently seize opportunities and further strengthen our Company and our growth prospects.For additional information about the following financial metrics, see Exhibit 99.1 of this Amendment and “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Funds for Operations” in the Original Filing.

| (1) | FFO per share-diluted represents funds from operations per share on a diluted basis, excluding the gain or loss on early extinguishment of debt. For 2015, FFO per share-diluted also excludes costs related to an unsolicited hostile takeover attempt and proxy contest. For the definition of FFO per share-diluted and a reconciliation of FFO per share-diluted to net income per share attributable to common stockholders-diluted, see Exhibit 99.1 of this Amendment and “Management’s Discussion and Analysis of Financial Condition and Results of Operations-Funds from Operations” in the Original Filing. |

17

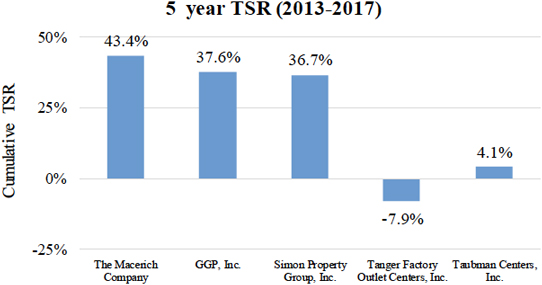

Despite our strong operating performance, our total stockholder return (“TSR”) in 2017 underperformed the S&P 500 Index and FTSE NAREIT All Equity REITs Index.

| 1 year (2017) | 3 year (2015-2017) | 5 year (2013-2017) | ||||||||||

The Macerich Company | -2.8 | % | -7.2 | % | 43.4 | % | ||||||

S&P 500 Index | 21.8 | % | 38.3 | % | 108.1 | % | ||||||

FTSE NAREIT All Equity REITs Index | 8.7 | % | 21.4 | % | 59.8 | % | ||||||

In 2016 and 2017, REIT TSRs were generally lower than the broader market, and regional mall REITs in particular underperformed other REITs. We believe that our negative TSR in 2016 and 2017 has been driven primarily by bearish investor sentiment for the mall REIT sector in general, in the wake of store closings and tenant bankruptcies announced by several high-profile retailers. However, our performance versus other mall REITs has been strong. Over the past five years we have generated a higher total return to our stockholders than any of our direct competitors, as illustrated in the following graph.

While store closings and tenant bankruptcies have adversely impacted our short-term TSR, these bankruptcies often present opportunities to secure more productive and more contemporary tenants that will generate higher sales productivity in the coming years. We remain well-positioned to take advantage of these opportunities.

18

Compensation Highlights

Compensation Elements. The following chart summarizes, for each component of our executive compensation program, the objectives and key features and the compensation decisions made by the Committee for our named executive officers for 2017:

Pay Element | Objectives and Key Features | Highlights for 2017 | ||||||

| Salary | Cash | • Relatively small, fixed cash pay based on the scope and complexity of each position, the officer’s experience, competitive pay levels and general economic conditions

| • 2017 salaries for each named executive officer remained unchanged from 2016 levels | |||||

Annual Incentive Bonus | Equity | • Variable short-term incentive

• Rewards achievement of both corporate and individual performance

• Performance measured using annual scorecard designed to support our Company’s short-term financial and strategic objectives

• Corporate goals (Same Center NOI growth, FFO per diluted share, releasing spreads, replacing lost rents, and succession planning) were weighted 80%, and evaluated formulaically againstpre-established threshold, target, and maximum goals

• Individual performance againstpre-established goals was weighted 20%

| • Based on achievements versus the goals, 2017 earned annual bonuses ranged from 82% to 87% of target for each named executive officer

• All such earned bonuses were paid in fully-vested LTIP units to further promote stockholder alignment | |||||

| Long-Term Incentives | Performance-Based (75%) | Equity | • Variable long-term incentive

• Provides incentive for our executive officers to take actions that contribute to the creation of stockholder value and outperform other equity REITs which are investment alternatives for our stockholders

• Performance-based LTIP Units granted in 2017 may be earned from 0% to 150% of target based on our TSR over the three-year performance period compared to all publicly-traded equity REITs (the “Equity Peer REITs”) | • Performance-based and service-based LTIP Units for the 2017-2019 performance/vesting period were granted to the named executive officers on January 1, 2017. Target grant values remained the same as in 2016, except for Mr. Perlmutter, whose target LTIP was increased to reflect his promotion to Sr. EVP and Chief Operating Officer in early 2016.

• Our shift from aone-year to a three-year performance period commenced with the 2016 performance-based LTIP Units

• As a result, no performance-based LTIP Units vested in 2017

| ||||

| Service-Based (25%) | Equity | • Service-based LTIP units vest in annual installments over a three-year period to promote retention and stability of our management team | ||||||

19

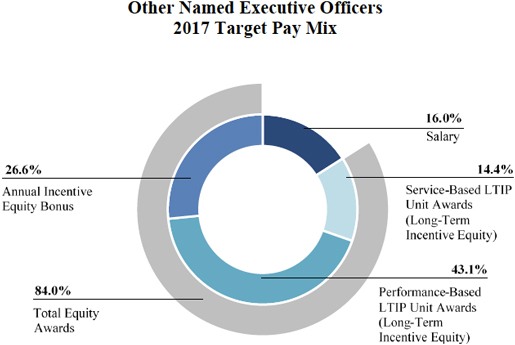

Target Total Direct Compensation Mix

20

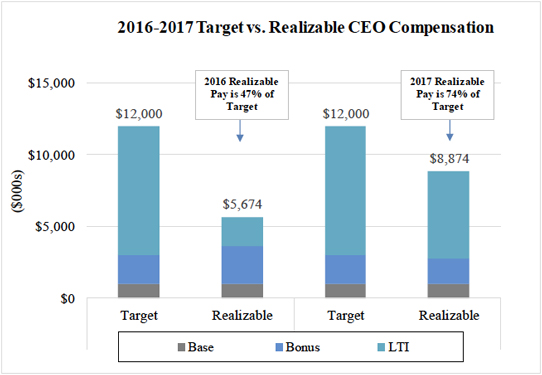

Target vs. Realizable CEO Compensation

As illustrated above, the majority of our CEO’s compensation opportunity is “at risk” and tied to performance goals and our absolute and relative TSR. Ourpay-for-performance philosophy is further illustrated by comparing target total direct compensation to “realizable” compensation, after taking into account actual performance.

Despite solid operating performance during 2016 and 2017, our TSR lagged the Equity Peer REITs. As a result, as of December 31, 2017, “realizable” compensation for our CEO was substantially below target for each of 2016 and 2017.

Target pay includes base salary, target annual incentive, and the target grant-date fair value of long-term incentives in each of 2016 and 2017 for Mr. A. Coppola. Realizable pay includes: (i) annual base salary earned; (ii) actual annual incentive earned in respect of the applicable year; and (iii) the value of performance-based LTIP Units (assuming the performance period had ended December 31, 2017) and service-based LTIP Units as of December 31, 2017, including earned dividend equivalents. None of the performance-based LTIP Units granted in 2016 and only 60% of the target number of performance-based LTIP Units granted in 2017 would have been earned at December 31, 2017 based on our relative TSR performance as of such date. The value of the service-based LTIP Units is based on our closing stock price on December 29, 2017, the last trading day of fiscal 2017. This chart and the total realizable pay reported in this chart provides supplemental information regarding the compensation paid to our CEO and should not be viewed as a substitute for the 2017 Summary Compensation Table. We believe that showing realizable compensation illustrates for stockholders the alignment between pay and performance.

21

2017Say-on-Pay Vote

At our 2017 annual stockholders’ meeting, approximately 89% of the votes cast were in favor of thenon-binding advisory resolution to approve the compensation of our named executive officers. Although the results of thesay-on-pay vote are advisory and not binding on the Company, the Board of Directors or the Committee, the Board of Directors and the Committee value the opinions of our stockholders and take the results of thesay-on-pay vote into account when making decisions regarding the compensation of our named executive officers. Following our 2015 annual meeting, the Committee, working with FW Cook, made meaningful changes to our executive compensation program in response to our stockholders’ feedback, including switching from aone-year performance period for our performance-based LTIP Units to a three-year performance period. In addition, we engaged in stockholder outreach on executive compensation matters throughout 2016. The Committee has considered the result of the 2017say-on-pay vote and, as a result of the high percentage of votes cast in favor of this proposal, the Committee believes that the changes made to our compensation program in 2016 were supported by stockholders. Accordingly, the Committee decided to maintain our general approach to executive compensation and made no significant changes to our executive compensation program during 2017.

Throughout 2017, we continued engagement with stockholders on a variety of issues, including executive compensation and corporate governance. As part of our commitment to ongoing, transparent communication with our stockholders, we will continue this open dialogue to ensure we understand stockholder views on these important issues.

Compensation Governance Highlights

Our executive compensation and corporate governance programs are designed to closely link pay with operational performance and increases in long-term stockholder value while minimizing excessive risk taking. To help us accomplish these important objectives, we have adopted the following policies and practices:

No Excessive Risk Taking. Our compensation program is designed to not incentivize excessive risk taking by participants. We conduct an annual risk assessment of all of our compensation programs.

No Tax Gross-Ups. None of our Company’s executives are entitled to any taxgross-ups.

Double-Trigger Equity Vesting. Effective with the 2016 equity grants, our equity awards are subject to double-trigger vesting acceleration in connection with a change of control.

Robust Stock Ownership Guidelines. We have robust stock ownership policies for our named executive officers and directors and each individual who is subject to them is in compliance with those policies. See “Stock Ownership Policies” onpages 28-29 of this Amendment.

Holding Period. Until the minimum required stock ownership level is achieved, our named executive officers must retain 50% of theirnet-after-tax profit shares from equity compensation awards. See “Stock Ownership Policies” onpages 28-29 of this Amendment.

Clawback Policy. We have a clawback policy that allows us to recover cash and equity incentive compensation paid to our executive officers if the compensation was based on achieving financial results that were subsequently restated and the amount of the executive officer’s incentive compensation would have been lower had the financial results been properly reported.

No Repricing. We do not permit repricing of underwater options or SARs or permit exchange of underwater options or SARs for other awards or cash, without prior stockholder approval.

Anti-Hedging Policy. We have a policy prohibiting all of our directors, officers and employees from engaging in any hedging or monetization transactions that are designed to hedge or offset any decrease in the market value of our securities. This policy also prohibits short sales and the purchase and sale of publicly traded options of our Company.

Anti-Pledging Policy. In addition, we have a policy (a) prohibiting all our directors and executive officers from pledging our securities if they are unable to meet our stock ownership requirements without reference to such pledged shares and (b) recommending that our directors and executive officers not pledge our Company’s securities. Currently, no shares of our Company are pledged by our directors and executive officers.

22

Independent Compensation Consultant. The Committee engages an independent compensation consulting firm that provides us with no other services.

AnnualSay-on-Pay. We annually submit our executive compensation program for our named executive officers tosay-on-pay advisory votes for stockholder consideration.

Compensation Philosophy and Objectives

Our executive compensation program is designed to achieve the following objectives:

| • | Attract, retain and reward experienced, highly-motivated executives who are capable of leading our Company in executing our ambitious growth strategy. |

| • | Link compensation earned to achievement of our Company’s short-term and long-term financial and strategic goals. |

| • | Align the interests of management with those of our stockholders by providing a substantial portion of compensation in the form of equity-based incentives and maintaining robust stock ownership requirements. |

| • | Adhere to high standards of corporate governance. |

The Committee believes strongly in linking compensation to corporate performance: the annual incentive awards (which for 2017 were paid entirely in the form of equity) are primarily based on overall corporate performance and the earned value of 75% of the long-term incentive equity awards depends on our three-year TSR relative to the Equity Peer REITs. The Committee also recognizes individual performance in making its executive compensation decisions. The Committee believes this is the best program overall to attract, motivate and retain highly skilled executives whose performance and contributions benefit our Company and our stockholders. The Committee believes it utilizes the right blend of cash and equity to provide appropriate incentives for executives while aligning their interests with those of our stockholders and encouraging the executives’ long-term commitment to our Company. The Committee does not have a strict policy for allocating a specific portion of compensation to our named executive officers between cash andnon-cash or short-term and long-term compensation. Instead, the Committee considers how each component promotes retention and/or motivates performance by the executive.

Inputs to Compensation Decisions

Role of the Compensation Committee

The Committee reviews and approves the compensation for our executive officers, reviews our overall compensation structure and philosophy and administers certain of our employee benefit and stock plans, with authority to authorize awards under our incentive plans. The Committee currently consists of three independent directors, Ms. Stephen (Chair) and Messrs. Soboroff and Hash.

Role of Management

Management, under the leadership of Mr. A. Coppola, develops our Company’s strategy and corresponding internal business plans, which our executive compensation program is designed to support. Mr. A. Coppola also provides the Committee with his evaluation of the performance of and his recommendations on compensation for his direct reports, including the other named executive officers.

Role of Compensation Consultant

The Committee may, in its sole discretion, retain or obtain the advice of any compensation consultant as it deems necessary to assist in the evaluation of director or executive officer compensation and is directly responsible for the appointment, compensation and oversight of the work of any such compensation consultant. The Committee retained FW Cook as its independent compensation consultant with respect to our compensation programs. FW Cook’s role is to evaluate the existing executive andnon-employee director compensation programs, assess the design and competitive positioning of these programs, and make recommendations for change, as appropriate. The Committee considered the independence of FW Cook and determined that its engagement of FW Cook does not raise any conflicts of interest with our Company or any of our directors or executive officers. FW Cook provides no other consulting services to our Company, executive officers or directors.

23

Role of Data for Peer Companies

FW Cook periodically conducts competitive reviews of our executive compensation program, including a competitive analysis of pay opportunities for our named executive officers as compared to the relevant peer group selected by the Committee. The Committee reviews compensation practices at peer companies to inform itself and aid it in its decision-making process so it can establish compensation programs that it believes are reasonably competitive.

FW Cook conducted a comprehensive review of our program in 2015, and made subsequent updates to competitive data for selected positions in 2016 with competitive comparisons based on twenty U.S.-based, publicly traded REITs of reasonably similar size to our Company, as measured by total capitalization, and/or with a focus on the retail sector. The group included our direct mall REIT competitors, both larger and smaller than us; REITs in other asset classes were primarily selected based on size. At the time FW Cook conducted the competitive reviews, our total capitalization was in the median range compared to the peer group. The Committee believes that these REITs best reflected a complexity and breadth of operations, as well as the amount of capital and assets managed, similar to our Company at the time the studies were conducted. FW Cook again reviewed the peer group for a comprehensive review conducted in 2017. The peer group REITs resulting from the 2017 comprehensive review were:

| Alexandria Real Estate Equities, Inc. | Kimco Realty Corporation | |

| Boston Properties, Inc. | Regency Centers Corporation | |

| Brixmor Property Group, Inc. | Simon Property Group, Inc. | |

| Digital Realty Trust, Inc. | SL Green Realty Corp. | |

| Douglas Emmett, Inc. | Tanger Factory Outlets | |

| Federal Realty Investment Trust | Taubman Centers, Inc. | |

| General Growth Properties, Inc. | VEREIT, Inc. | |

| HCP, Inc. | Vornado Realty Trust | |

| Kilroy Realty Corporation |

Relative to 2016, based on the 2017 comprehensive review FW Cook recommended and the Committee approved the following changes to the peer group, which are reflected in the peer group listed above: Four REITs were removed as they had become much larger than us in total capitalization: AvalonBay Communities, Inc.; Equity Residential; Prologis, Inc. and Ventas, Inc. Host Hotels & Resorts, Inc. was also removed as its asset class was deemed too different from ours. Two REITs were added, VEREIT, Inc. and Brixmor Property Group, Inc. because they are closer in size to us and have a substantial proportion of retail assets in their portfolios, albeit primarily single-tenant and/or shopping center retail as compared to our focus on Class-A regional malls.

The Committee does not set compensation components to meet specific benchmarks. Instead the Committee focuses on a balance of annual and long-term compensation, which is heavily weighted toward “at risk” performance-based compensation. Peer group data is not used as the determining factor in setting compensation because each officer’s role and experience is unique. The Committee believes that ultimately the decision as to appropriate compensation for a particular officer should be made based on a full review of that officer’s and our Company’s performance.

Compensation for 2017 Performance

Compensation opportunities for each named executive officer consisted of a base salary, an annual bonus opportunity, and long-term incentives, each of which is described in more detail below.

24

Base Salary:No Salary Increases in 2017

As they do annually, the Committee members reviewed base salaries of the named executive officers to determine whether they remain appropriate based on the factors identified above. Based on this review, the 2017 base salaries of our named executive officers remained unchanged from 2017.

Annual Incentive Structure:Rigorous Goals to Align Compensation with Performance.

Each executive officer has a target annual incentive opportunity, expressed as a percentage of base salary. Consistent with prior years, target bonus is 200% of base salary for the CEO and President, and 150% of base salary for the other named executive officers. The Committee sets target bonuses for Messrs. A. Coppola and E. Coppola at a higher percentage of base salary than the other executives because as the CEO and President, respectively, they are our strategic leaders and manage and direct our other named executive officers. Actual bonuses can range from 0% to 200% of each executive’s target bonus, based on the Committee’s assessment of annual performance against the objectives established for the year.

Under our annual incentive program, the Committee evaluates performance against a “scorecard” of performance objectives established at the beginning of the year. These rigorous scorecard goals are designed to reward the successful execution of our strategies, and were consistent with our external guidance as disclosed in the first quarter of 2017. For 2017, five corporate measures determined 80% of each executive’s earned bonus; the remaining 20% was based on the Committee’s assessment of the executive’s individual performance. The 2017 corporate scorecard measures, as well as actual achievement versus each goal, are outlined in the following table:

2017 Corporate Goals – Weighted 80%

| Weighting | 2017 Goals | 2017 Actual | Payout (% of Target) | |||||||||||||||||||||

Measure | Threshold | Target | Max | |||||||||||||||||||||

| Payout® | 50% | 100% | 200% | |||||||||||||||||||||

Same Center NOI Growth | 20 | % | 3.0 | % | 3.5 | % | 4.0 | % | 2.73 | % | 0.0 | % | ||||||||||||

FFO per Diluted Share (1) | 20 | % | $ | 3.90 | $ | 3.95 | $ | 4.00 | $ | 3.95 | (2) | 100.0 | % | |||||||||||

Re-leasing Spreads | 20 | % | 12 | % | 14 | % | 16 | % | 15.2 | % | 160.0 | % | ||||||||||||

Replacing Lost Rents from bankrupt specialty store tenants | 10 | % | 50 | % | 65 | % | 80 | % | 51 | % | 53.3 | % | ||||||||||||

Succession Planning | 10 | % | | Deliver a uniform evaluation and documentation of a succession plan for each department | | Achieved | 100 | % | ||||||||||||||||

| (1) | Excludes the impact of any assets returned to lenders or services and the impact of acquisitions/dispositions |

| (2) | Excludes $0.09 dilutive impact from new tax rates and $0.03 of dilution from the sales of Cascade Mall and Northgate Mall. |

At the time the goals were set, the Committee believed these goals were rigorous, in particular in the context of the anticipated slowing growth in the retail REIT sector. For the target incentive amount to be earned, Same Center NOI in 2017 had to grow 3.5% over 2016 and the rent per square foot on new leases executed in 2017 had to increase by 14% over rent per square foot on expiring leases. Target FFO per diluted share for 2017 was below actual 2016 FFO per share as a result of a combination of items, including the significant number of tenant bankruptcies which occurred toward the end of 2016 and additional bankruptcies which were anticipated for 2017; asset dispositions in 2016 and anticipated for 2017; higher interest rates and reducing NOI for specific assets under development.

25

Individual Performance–Weighted 20%

The Committee evaluated the 2017 individual performance of our named executive officers, with Mr. A. Coppola providing the Committee with his evaluation with respect to the performance of the other executives. As part of this process, the Committee discussed with Mr. A. Coppola his evaluation of the contributions of each executive, including with respect to our 2017 corporate achievements.

The Committee noted the following:

With respect to Mr. E. Coppola: his continued leadership supporting our strategic dispositions, acquisitions and developments, including his role in the successful completion of Green Acres Commons and the redevelopment of Broadway Plaza and Sears store at Kings Plaza. Mr. E. Coppola was instrumental in building strategic relationships with key stakeholders. His knowledge of the real estate markets as well as his strong relationships with real estate owners, partners and governmental officials were also critical to the success of our dispositions, acquisitions and development strategies. Mr. E. Coppola was also actively involved in our Company’s succession planning initiatives and talent development.

With respect to Mr. O’Hern: his leadership in supporting and executing our strategic, financial and operational initiatives; success in maintaining the strength of our balance sheet; his continuing role in leading our capital market efforts, including successfully financing of $800 million including a $400 million12-year loan in Freehold Raceway Mall at an average interest rate of 3.48%, completing the $221 million share repurchases resulting in the retirement of 2.6% of total shares previously outstanding. Mr. O’Hern also led the Company’s engagement and communication efforts with the investment communities and articulating the compelling nature of our strategic plans, financial strength and business achievements.

With respect to Mr. Perlmutter: his contributions with members of the Macerich team to our industry-leading results, including strong occupancy and double-digit releasing spreads. In the face of significant tenant bankruptcies at the start of the year which increased throughout 2017, Mr. Perlmutter helped maintain, and even improve, occupancy throughout the portfolio. He was also involved in securing a commitment from Nordstrom to open at Country Club Plaza. He facilitated continuing improvements in the property/asset management groups, joint venture relationships, implementation of talent development for the leasing organization, and continued efforts to position lower-quality assets for disposition.

With respect to Mr. Leanse: his support of the executive team’s efforts in responding to and negotiating new business opportunities, his support of the Board in corporate governance issues, his work to develop a more efficient and effective way to deliver comprehensive legal services and his activities with respect to the Company’s various ongoing legal, operational and litigation matters.

With respect to Mr. A. Coppola: in determining his annual incentive bonus, the Committee reviewed with Mr. A. Coppola his 2017 accomplishments against his goals. In addition to supporting our 2017 corporate goals previously described, Mr. A. Coppola’s accomplishments for 2017 included his leadership in the Company’s efforts to advance digitally native, vertically integrated retail strategies, revitalize tenant mix, cultivate redevelopment opportunities of existing anchor stores, continue the execution of our long-term plan of recycling capital fromnon-core assets into our key development and redevelopment pipeline, and nurture succession planning and upward mobility throughout our Company. Mr. A. Coppola also guided the Company to several high profile and industry leading awards in recognition of sustainability initiatives and practices.

Based on each executive’s accomplishments as well as considering performance scores for the employees reporting to each of the named executive officers, the Committee scored the individual performance category at 100% of target for Messrs. A. Coppola, O’Hern, and Perlmutter and at 75% of target for Messrs. E. Coppola and Leanse.

Earned bonuses were awarded in the form of fully-vested LTIP Units, to further promote alignment with stockholders. Under applicable SEC rules, equity awards are reported as compensation in the tables below for the year in which the award was granted, not the year to which the performance relates. Accordingly, the LTIP Units awarded as annual incentive compensation based on 2017 performance described above will be reported in those tables in next year’s proxy statement as compensation for 2018. Thus, the compensation for our named executive officers for 2017 reflected in the Summary Compensation Table and Grants of Plan-Based Awards Table below includes the LTIP Units awarded to each executive early in 2017 for 2016 performance. See “2017 Total Compensation” below.

26

Long-Term Incentives–75% Performance-Based and Tied to Achieving Strong Relative Returns

Since 2006, our Company has utilized a long-term equity-based incentive program as an important means to align the interests of our executives and our stockholders, to encourage our executives to adopt a longer-term perspective and to reward them for creating stockholder value in apay-for-performance structure.

For 2017, the Committee approved for each named executive officer an aggregate grant date fair value for these awards, to be granted in the form of LTIP Units. That amount was divided between two types of LTIP Units as follows:

Performance-Based LTIP Units (75%). May be earned from 0% to 100% of the target number of units awarded based on our TSR performance relative to the Equity Peer REITs for the three-year performance period from January 1, 2017 through December 31, 2019. Payouts, as a percentage of target units, for the performance-based LTIP Units for various levels of absolute and relative performance are outlined in the following table, with linear interpolation for performance between performance levels.

MAC’s Relative TSR Percentile Ranking | Payout (% of Target LTIP Units) | |||

<25th Percentile | 0 | % | ||

25th Percentile | 50 | % | ||

50th Percentile | 100 | % | ||

³75th Percentile | 150 | % | ||

Performance-based LTIP Unit grants prior to 2016 had aone-year performance period. Starting with 2016 grants, we switched to a three-year performance period, to provide better alignment with long-term stockholder return performance. Due to the transition, no performance periods for performance-based LTIP units ended in 2017; as a result, no performance-based LTIP Units vested in 2017.

Service-Based LTIP Units (25%). Vest in equal annual installments over a three-year period to promote retention and further alignment of our executives’ interests with those of our stockholders.

The Committee reviewed peer group data relating to the allocation of long-term incentive equity awards between performance-based and service-based awards and determined that 75% performance-based was a higher percentage than the median mix between performance-based and service-based equity among the peer group, and therefore consistent with our emphasis on “at risk” compensation. For the performance-based component, the Committee considered the range of potential realizable values that our executives could earn to ensure that the awards would be both reasonably competitive and appropriate to motivate our leadership team.

2017 Total Compensation

We are including this supplemental information to provide a more meaningful view of the compensation of our named executive officers for their performance during 2017. The table below shows each named executive officer’s salary, annual long-term incentive equity award grant value, bonus for services performed in 2017 and all other compensation. This table, in contrast to the Summary Compensation Table on page 30 of this Amendment, includes equity awards granted under our annual incentive award program in March 2018 for services performed in 2017 and excludes equity awards granted under our annual incentive award program in March 2017 for services performed in 2016.

Executive | Salary | Annual Incentive Earned for 2017(1) | Long-Term Incentive Award Value(2) | All Other Compensation | Total Compensation | |||||||||||||||

Arthur M. Coppola | $ | 1,000,000 | $ | 1,766,000 | $ | 8,999,943 | $ | 219,745 | $ | 11,985,688 | ||||||||||

Edward C. Coppola | $ | 800,000 | $ | 1,316,800 | $ | 3,599,901 | $ | 186,597 | $ | 5,903,298 | ||||||||||

Thomas E. O’Hern | $ | 600,000 | $ | 794,700 | $ | 1,999,972 | $ | 71,588 | $ | 3,466,260 | ||||||||||

Robert D. Perlmutter | $ | 600,000 | $ | 794,700 | $ | 1,999,972 | $ | 62,327 | $ | 3,456,999 | ||||||||||

Thomas J. Leanse | $ | 500,000 | $ | 617,250 | $ | 1,374,934 | $ | 57,884 | $ | 2,550,068 | ||||||||||

27

| (1) | Earned annual incentives were awarded in the form of fully-vested LTIP Units on March 2, 2018, with the number of LTIP Units based on the closing price of our Common Stock on the New York Stock Exchange on such date. |