UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 20-F

☐ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR 12(g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2020

OR

☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

OR

☐ | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Date of event requiring this shell company report,

Commission file number: 001-12440

ENEL AMÉRICAS S.A.

(Exact name of Registrant as specified in its charter)

ENEL AMÉRICAS S.A.

(Translation of Registrant’s name into English)

CHILE

(Jurisdiction of incorporation or organization)

Santa Rosa 76, Santiago, Chile

(Address of principal executive offices)

Nicolás Billikopf, phone: (56-9) 9343-5500, nicolas.billikopf@enel.com, Av. Santa Rosa 76, Piso 15, Comuna de Santiago, Santiago, Chile

(Name, Telephone, E-mail, and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| | |

|---|---|---|

Title of Each Class

| Trading Symbol(s) | Name of Each Exchange on Which Registered

|

American Depositary Shares Representing Common Stock | ENIA | New York Stock Exchange |

Common Stock, no par value * | * | New York Stock Exchange |

US$ 600,000,000 4.00% Notes due October 25, 2026 | ENIA26A | New York Stock Exchange |

US$ 858,000 6.60% Notes due December 1, 2026 | ENIA26 | New York Stock Exchange |

* | Listed, not for trading, but only in connection with the registration of American Depositary Shares, pursuant to the requirements of the Securities and Exchange Commission. |

Securities registered or to be registered pursuant to Section 12(g) of the Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report.

Shares of Common Stock: 76,086,311,036

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ☒ Yes ☐ No

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. ☐ Yes ☒ No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ☒ Yes ¨ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). ☒ Yes ☐ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ☒ | Accelerated filer ☐ | Non-accelerated filer ☐ | Emerging growth company |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards † provided pursuant to Section 13(a) of the Exchange Act. ☐

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ⌧

| | |

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing: | ||

| | |

U.S. GAAP ☐ | International Financial Reporting Standards as issued by the International Accounting Standards Board ☒ | Other ☐ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow. ☐ Item 17 ☐ Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ☐ Yes ☒ No

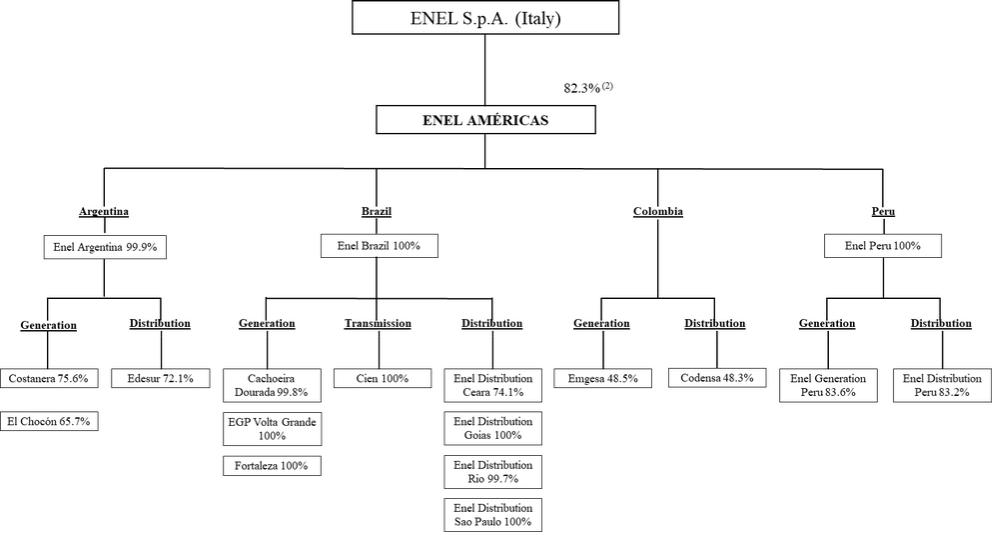

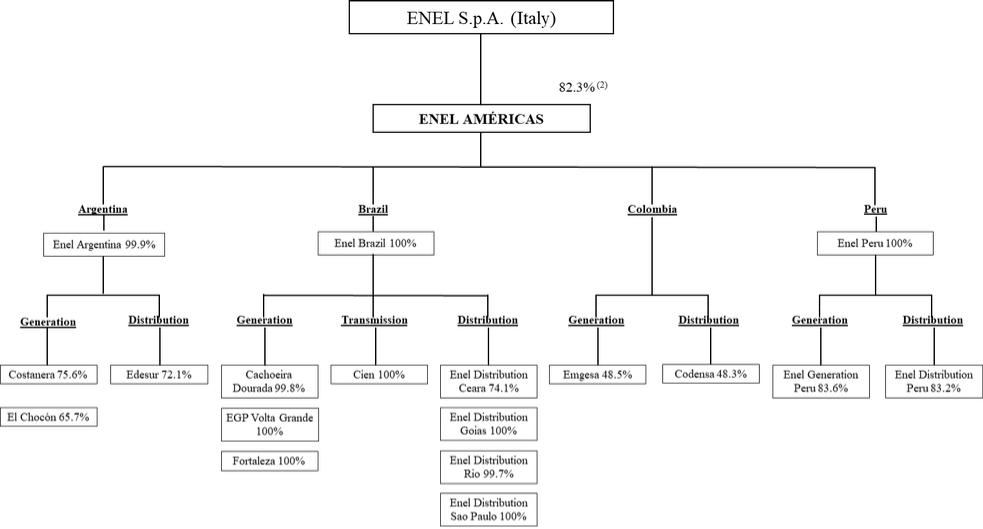

Enel Américas Simplified Organizational Structure (1)

As of the date of this Report

| (2) | As of December 31, 2020, Enel S.p.A. beneficially owned 65% of Enel Américas. Upon the effectiveness of the merger by incorporation of EGP Américas SpA into Enel Américas on April 1, 2021, Enel S.p.A.’s beneficial ownership interest in Enel Américas increased to 75.2%, and as a result of Enel S.p.A.’s tender offer launched on March 15, 2021 for up to 10% of Enel Américas’ then-outstanding shares of common stock (including shares represented by ADS), which expired on April 13, 2021, Enel S.p.A.’s beneficial ownership interest in Enel Américas increased to the current level of 82.3%. |

2

| |||

|---|---|---|---|

| Page | ||

| 4 | ||

| | ||

| 10 | ||

| | ||

| 11 | ||

| | ||

| 13 | ||

| | | |

| 14 | ||

| | | |

| | | |

| | ||

| 15 | ||

| | ||

| 15 | ||

| | ||

| 15 | ||

| | ||

| 29 | ||

| | ||

| 111 | ||

0 | | | |

| 111 | ||

| | ||

| 170 | ||

| | ||

| 178 | ||

| | ||

| 181 | ||

| | ||

| 182 | ||

| | ||

| 184 | ||

| | ||

| 200 | ||

| | ||

| 204 | ||

| | ||

| | ||

| | ||

| 205 | ||

| | ||

Material Modifications to the Rights of Security Holders and Use of Proceeds | | 205 | |

| | ||

| 205 | ||

| | ||

| 206 | ||

| | ||

| 206 | ||

| | ||

| 206 | ||

| | ||

| 207 | ||

| | ||

| 208 | ||

| | ||

Purchases of Equity Securities by the Issuer and Affiliated Purchasers | | 208 | |

| | ||

| 210 | ||

| | ||

| 210 | ||

| | ||

| 210 | ||

| | ||

| | | |

| | | |

| 211 | ||

| | | |

| 211 | ||

| | | |

| 211 | ||

3

ADR | | American Depositary Receipt | | A certificate issued by our depositary that represents ADS, or American Depositary Shares. |

| | | | |

ADS | | American Depositary Share(s) | | An equity interest in our company that is issued by Citibank, N.A., as the depositary, in respect of shares of our company held by the depositary. Each ADS represents 50 shares and ADS are traded on the New York Stock Exchange. In this Report, ADS is used in the singular and plural forms. |

| | | | |

AFP | | Administradora de Fondos de Pensiones | | A legal entity that manages a Chilean pension fund. |

| | | | |

ANEEL | | Agência Nacional de Energia Elétrica | | Brazilian governmental agency for electric energy. |

| | | | |

BNDES | | Banco Nacional de Desenvolvimento Econȏmico e Social | | The National Bank for Economic and Social Development (“BNDES”) is the principal agent of development in Brazil, focusing on sustainable social and environmental development. |

| | | | |

Brazilian MME | | Ministério de Minas y Energia | | Brazilian Ministry of Mines and Energy. |

| | | | |

Cachoeira Dourada | | Enel Green Power Cachoeira Dourada S.A. | | Brazilian generation subsidiary owned by Enel Brasil. Formerly Centrais Elétricas Cachoeira Dourada S.A. |

| | | | |

CAMMESA | | Compañía Administradora del Mercado Mayorista Eléctrico S.A. | | Argentine autonomous entity in charge of the Mercado Eléctrico Mayorista (Wholesale Electricity Market), or MEM. CAMMESA’s stockholders are generation, transmission, distribution companies, large users, and the Secretariat of Energy. |

| | | | |

CCEE | | Câmara de Comercialização de Energia Elétrica | | Electricity Trading Chamber or Wholesale Clearing House |

| | | | |

Chilean Stock Exchanges | | Chilean Stock Exchanges | | The two stock exchanges located in Chile: the Santiago Stock Exchange and the Electronic Stock Exchange. |

| | | | |

Cien | | Enel CIEN S.A. | | Brazilian transmission subsidiary, wholly-owned by Enel Brasil. Formerly Companhia de Interconexão Energética S.A. |

| | | | |

CND | | Centro Nacional de Despacho | | Colombian National Dispatch Center in charge of coordinating the efficient operation |

4

and dispatch of generation units to satisfy demand. | ||||

| | | | |

CNPE | | Conselho Nacional de Politica Energética | | Brazilian national energy policy council in charge of advising the Brazilian President on energy policy. |

| | | | |

CMF | | Comisión para el Mercado Financiero | | Chilean Financial Market Commission, the governmental authority that supervises the financial markets. Formerly the Chilean Superintendence of Securities and Insurance or SVS in its Spanish acronym. |

| | | | |

CMSE | | Comitê de Monitoramento do Setor Elétrico | | The Brazilian energy sector monitoring committee that evaluates the continuity and security of the energy supply across the country. |

| | | | |

Codensa | | Codensa S.A. E.S.P. | | Colombian distribution subsidiary that operates mainly in Bogotá and whose voting power is controlled by us. |

| | | | |

COES | | Comité de Operación Económica del Sistema | | Peruvian entity in charge of coordinating the efficient operation and dispatch of generation units to satisfy demand. |

| | | | |

Colombian MME | | Ministerio de Minas y Energía | | Colombian Ministry of Mines and Energy. |

| | | | |

Costanera | | Enel Generación Costanera S.A. | | A publicly held Argentine generation company controlled by us. Formerly Central Costanera S.A. |

| | | | |

CREG | | Comisión de Regulación de Energía y Gas | | Colombian Commission for the Regulation of Energy and Gas. |

| | | | |

CTM | | Compañía de Transmisión del Mercosur S.A. | | Argentine transmission company and a subsidiary of Enel Brasil. |

| | | | |

Dock Sud | | Central Dock Sud S.A. | | Argentine generation subsidiary. |

| | | | |

Edesur | | Empresa Distribuidora del Sur S.A. | | Argentine distribution subsidiary, with a concession area in the southern part of the Buenos Aires greater metropolitan area. |

| | | | |

EGP Volta Grande | | Enel Green Power Volta Grande S.A. | | Brazilian generation subsidiary located in the State of Minas Gerais, in Brazil, owned by Enel Brasil. |

| | | | |

El Chocón | | Enel Generación El Chocón S.A. | | Argentine generation company with two hydroelectric plants, El Chocón and Arroyito, both located in the Limay River, Argentina and our subsidiary. Formerly Hidroeléctrica El Chocón S.A. |

| | | | |

5

Emgesa | | Emgesa S.A. E.S.P. | | Colombian generation subsidiary whose voting power is controlled by us. |

| | | | |

Enel | | Enel S.p.A. | | Our Italian parent company with multinational operations in the power and gas markets, with a 65% and 82.3% beneficial ownership of Enel Américas as of December 31, 2020, and the date of this Report, respectively. |

| | | | |

Enel Américas | | Enel Américas S.A. | | Our company, a publicly held limited liability stock corporation incorporated under the laws of the Republic of Chile, headquartered in Chile, with subsidiaries engaged primarily in the generation and distribution of electricity in Argentina, Brazil, Colombia, and Peru, and controlled by Enel. The registrant of this Report. Formerly known as Enersis S.A. |

| | | | |

Enel Argentina | | Enel Argentina S.A. | | Argentine holding company subsidiary. |

| | | | |

Enel Brasil | | Enel Brasil S.A. | | Brazilian holding company subsidiary. Formerly known as Endesa Brasil S.A. |

| | | | |

Enel Distribution Ceara | | Companhia Energética Do Ceará S.A. | | A publicly held Brazilian distribution subsidiary operating in the state of Ceará controlled by Enel Brasil. Also commercially known as Enel Distribuição Ceará. |

| | | | |

Enel Distribution Goias | | CELG Distribuição S.A. | | Brazilian distribution subsidiary that operates a concession in the state of Goias, owned by Enel Brasil. Also commercially known as Enel Distribuição Goiás. |

| | | | |

Enel Distribution Peru | | Enel Distribución Perú S.A.A. | | A publicly held Peruvian distribution subsidiary, with a concession area in the northern part of Lima. Formerly Empresa de Distribución Eléctrica de Lima Norte S.A. or Edelnor. |

| | | | |

Enel Distribution Rio | | Ampla Energia e Serviços S.A. | | A publicly held Brazilian distribution subsidiary operating in Rio de Janeiro, owned by Enel Brasil. Also commercially known as Enel Distribuição Rio. |

| | | | |

Enel Distribution Sao Paulo | | Eletropaulo Metropolitana Eletricidade de São Paulo S.A. | | A publicly held Brazilian distribution subsidiary operating in Sao Paulo, owned by Enel Investimentos Sudeste S.A., a wholly-owned investment vehicle of Enel Brasil. Also commercially known as Enel Distribuição São Paulo. |

| | | | |

6

Enel Generation Peru | | Enel Generación Perú S.A.A. | | A publicly held Peruvian generation subsidiary. Formerly Edegel S.A.A. |

| | | | |

Enel Generation Piura | | Enel Generación Piura S.A. | | A publicly held Peruvian generation subsidiary. Formerly Empresa Eléctrica de Piura S.A. or EEPSA. |

| | | | |

Enel Peru | | Enel Perú S.A.C. | | Peruvian holding company subsidiary. |

| | | | |

| | | | |

Enel Sudeste | | Enel Investimentos Sudeste S.A. | | A former Brazilian investment holding company, owned by Enel Brasil, and parent company of Enel Distribution Sao Paulo. In 2019 Enel Sudeste was merged into Enel Distribution Sao Paulo. |

| | | | |

Enel Trading Argentina | | Enel Trading Argentina S.R.L. | | Energy trading subsidiary with operations in Argentina. Formerly Central Comercializadora de Energía S.A. or CEMSA. |

| | | | |

Enel X Brasil | | Enel X Brasil S.A. | | A Brazilian subsidiary engaged in developing, implementing, and selling products and services different from the sale of energy or energy distribution under concessions, and associated services in Brazil, owned by Enel Brasil. |

| | | | |

Enel X Colombia | | Enel X Colombia S.A.S. | | A Colombian subsidiary engaged in developing, implementing, and selling products and services different from the sale of energy or energy distribution under concessions, and associated services in Colombia, owned by Codensa. |

| | | | |

ENRE | | Ente Nacional Regulador de la Electricidad | | Argentine national regulatory authority for the energy sector. |

| | | | |

FONINVEMEM | | Fondo para Inversiones Necesarias que permitan Incrementar la Oferta de Energía Eléctrica en el Mercado Eléctrico Mayorista | | Argentine fund created to increase electricity supply in the MEM. |

| | | | |

Fortaleza | | Central Geradora Termeletrica Fortaleza S.A. | | Brazilian generation subsidiary that operates in the state of Ceará and is wholly-owned by Enel Brasil. Also commercially known as Enel Geração Fortaleza. |

| | | | |

GEB | | Grupo Energía Bogotá S.A. | | Colombian state-owned financial and energy holding company, with investments in electricity generation, transmission, trading and distribution and natural gas transmission, distribution, and trading sectors. Formerly Empresa Energía de Bogotá S.A. or EEB. |

7

| | | | |

IFRS | | International Financial Reporting Standards | | International Financial Reporting Standards as issued by the International Accounting Standards Board (IASB). |

| | | | |

LNG | | Liquefied Natural Gas. | | Liquefied natural gas. |

| | | | |

MADS | | Ministerio de Ambiente y Desarrollo Sostenible | | Colombian Ministry of Environment and Sustainable Development. |

| | | | |

MEM | | Mercado Eléctrico Mayorista | | Wholesale Electricity Market. There are such markets in each of Argentina, Colombia, and Peru. |

| | | | |

MINEM | | Ministerio de Energia y Minas | | Peruvian Ministry of Energy and Mines. |

| | | | |

NIS | | Sistema Interconectado Nacional | | National interconnected electric system. There are such systems in each of Argentina, Brazil, and Colombia. |

| | | | |

OEF | | Obligación de Energía Firme | | Colombian firm energy commitment of generators to guarantee energy in the long term. |

| | | | |

ONS | | Operador Nacional do Sistema Elétrico | | National Electric System Operator. Brazilian non-profit private entity responsible for the planning and coordination of operations in interconnected systems. |

| | | | |

Osinergmin | | Organismo Supervisor de la Inversión en Energía y Minería | | Energy and Mining Investment Supervisory Authority, the Peruvian regulatory electricity authority. |

| | | | |

OSM | | Ordinary Shareholders’ Meeting | | Ordinary Shareholders’ Meeting |

| | | | |

PPA | | Power Purchase Agreement | | Power Purchase Agreement |

| | | | |

PLD | | Preço de Liquidação das Diferenças | | Settlement price for differences. It is the price assigned to sales and purchases of energy on the Brazilian spot market. |

| | | | |

SAIDI | | System Average Interruption Duration Index | | Index of average duration of interruptions in the power supply. |

| | | | |

SAIFI | | System Average Interruption Frequency Index | | Index of average frequency of interruptions in the power supply. |

| | | | |

SEE | | Secretaria de Energía Argentina | | The Argentine Ministry of Energy and Mining manages the electricity industry through the Argentine Secretary of Energy. |

| | | | |

SEIN | | Sistema Eléctrico Interconectado Nacional | | Peruvian national interconnected electricity system. |

| | | | |

8

SENACE | | Servicio Nacional de Certificación Ambiental para las Inversiones Sostenibles | | Peruvian autonomous national environmental certification service for sustainable investments that reports to the Peruvian Ministry of the Environment. |

| | | | |

TESA | | Transportadora de Energía S.A. | | Transmission company with operations in Argentina and a subsidiary of Enel Brasil, our subsidiary. |

| | | | |

UF | | Unidad de Fomento | | Chilean inflation-indexed, Chilean peso-denominated monetary unit equivalent to Ch$ 29,070.33 as of December 31, 2020. |

| | | | |

UPME | | Unidad de Planificación Minero Energética | | Colombian energy and mining planning unit responsible for planning the expansion of the generation and transmission systems. |

| | | | |

UTA | | Unidad Tributaria Anual | | Chilean annual tax unit. One UTA equals 12 Unidades Tributarias Mensuales (“UTM”), a Chilean inflation-indexed monthly tax unit used to define fines, among other purposes. As of December 31, 2020, one UTM was equivalent to Ch$ 51,029, and one UTA was equal to Ch$ 612,348. |

| | | | |

VAD | | Valor Agregado de Distribución | | Value-added from distribution of electricity. |

| | | | |

XM | | Expertos de Mercado S.A. E.S.P. | | A subsidiary of Interconexión Eléctrica S.A. (“ISA”), a Colombian company that provides system management in real-time services in electrical, financial, and transportation sectors. |

| | | | |

| | | | |

9

As used in this Report on Form 20-F (“Report”), first-person personal pronouns such as “we,” “us” or “our” as well as “Enel Américas” and “the Company” refer to Enel Américas S.A. and our consolidated subsidiaries unless the context indicates otherwise. Unless otherwise noted, our interest in our principal subsidiaries and jointly controlled companies and associates is expressed in terms of our economic interest as of December 31, 2020.

We are a Chilean company engaged through our subsidiaries and jointly controlled companies in the electricity generation, transmission, and distribution businesses in Argentina, Brazil, Colombia, and Peru. We participate in the generation and transmission businesses mainly through our subsidiaries Costanera, Dock Sud, and El Chocón in Argentina; Cachoeira Dourada, Fortaleza, EGP Volta Grande, and Cien in Brazil; Emgesa in Colombia; and Enel Generation Peru and Enel Generation Piura in Peru. In the distribution business, our principal subsidiaries are Edesur in Argentina; Enel Distribution Ceara, Enel Distribution Rio, Enel Distribution Sao Paulo, and Enel Distribution Goias in Brazil; Codensa in Colombia; and Enel Distribution Peru in Peru. For additional information relating to our principal subsidiaries and associates, please see “Item 4. Information on the Company — C. Organizational Structure — Principal Subsidiaries and Affiliates.”

We are a publicly held limited liability stock corporation headquartered in Chile and organized on June 19, 1981, under the laws of the Republic of Chile. During 2016, we completed a corporate reorganization to separate our Chilean businesses from our non-Chilean businesses. As part of this process, the former Enersis S.A. changed its name to Enel Américas S.A. on December 1, 2016. For additional information relating to the company and the corporate reorganization completed in 2016, please see “Item 4. Information on the Company — A. History and Development of the Company — History” and “— The 2016 Reorganization.”

As of the date of this Report, Enel S.p.A. (“Enel”), an Italian energy company with multinational operations in the power and gas markets, owns a beneficial interest of 82.3% of us and is our ultimate controlling shareholder. For additional information relating to the Merger with EGP Americas, please see “Item 4. Information on the Company — A. History and Development of the Company — Merger with EGP Américas and Related Tender Offer.”

10

Financial Information

In this Report, unless otherwise specified, references to “U.S. dollars” or “US$” are to dollars of the United States of America (“United States”); references to “Ar$” or “Argentine pesos” are to the currency of Argentina; references to “R$,” or “reais” are to Brazilian reais, the currency of Brazil; references to “pesos” or “Ch$” are to Chilean pesos, the currency of Chile; references to “COP$” or “Colombian pesos” are to the currency of Colombia; references to “soles” are to Peruvian Soles, the currency of Peru; references to “EUR” are to Euro, the currency of the European Union and references to “UF” are to Unidades de Fomento. The UF is a Chilean inflation-indexed, peso-denominated monetary unit that is adjusted daily to reflect changes in the official Consumer Price Index (“CPI”) of the Chilean National Institute of Statistics (Instituto Nacional de Estadísticas or “INE”). The UF is adjusted in monthly cycles. Each day in the period beginning on the tenth day of the current month through the ninth day of the succeeding month, the nominal peso value of the UF is indexed to reflect a proportionate amount of the change in the Chilean CPI during the prior calendar month. As of December 31, 2020, one UF was equivalent to Ch$ 29,070.33. The U.S. dollar equivalent of one UF was US$ 40.89 as of December 31, 2020, using the Observed Exchange Rate reported by the Central Bank of Chile (Banco Central de Chile) as of December 31, 2020, of Ch$ 710.95 per US$ 1.00. The U.S. dollar observed exchange rate (dólar observado) (the “Observed Exchange Rate”), which is reported by the Central Bank of Chile and published daily on its webpage, is the weighted average exchange rate of the previous business day’s transactions in the Formal Exchange Market. Unless the context specifies otherwise, all amounts translated from Chilean pesos to U.S. dollars or vice versa, or from UF to Chilean pesos, have been carried out at the rates applicable as of December 31, 2020.

Since 2017, our functional currency has been the U.S. dollar, and therefore our consolidated financial statements and other financial information concerning us included in this Report are presented in U.S. dollars. The change of our functional currency was recorded as of January 1, 2017, by translating all items of our consolidated financial statements to the new functional currency, using the exchange rate of Ch$ 669.47 as of January 1, 2017. We also changed the presentation currency of our consolidated financial statements from the Chilean peso to the U.S. dollar. The change in the presentation currency was applied retrospectively as if the U.S. dollar had always been the presentation currency of the consolidated financial statements. The consolidated financial statements for the year ended December 31, 2016, were restated in U.S. dollars using the average exchange rate for each period. For further information about our functional currency, please refer to Note 2.8 of the Notes to our consolidated financial statements.

We have prepared our consolidated financial statements in accordance with International Financial Reporting Standards (“IFRS”), as issued by the International Accounting Standards Board (“IASB”). All our subsidiaries are integrated, and all their assets, liabilities, income, expenses, and cash flows are included in the consolidated financial statements after making the adjustments and eliminations related to intra-group transactions. Our interest in associated companies over which we exercise significant influence is included in our consolidated financial statements using the equity method. For detailed information regarding consolidated entities, jointly controlled entities, and associated companies, see Notes 2.4 and 2.5 of the Notes to our consolidated financial statements.

This Report may contain translations of Chilean peso amounts into U.S. dollars at specified rates. Unless otherwise indicated, the Chilean peso equivalent for information in U.S. dollars is based on the Observed Exchange Rate for December 31, 2020, as defined in “Item 3. Key Information — A. Selected Financial Data — Exchange Rates”. The Federal Reserve Bank of New York does not report a noon buying rate for Chilean pesos. No representation is made that the Chilean peso or U.S. dollar amounts disclosed in this Report could have been or could be converted into U.S. dollars or Chilean pesos at such rate or any other rate. See “Item 3. Key Information — A. Selected Financial Data — Exchange Rates.”

Technical Terms

References to “TW” are to terawatts (1012 watts or a trillion watts); references to “GW” and “GWh” are to gigawatts (109 watts or a billion watts) and gigawatt-hours, respectively; references to “MW” and “MWh” are to megawatts (106 watts or a million watts) and megawatt-hours, respectively; references to “kW” and “kWh” are to kilowatts (103 watts or a thousand watts) and kilowatt-hours, respectively; references to “kV” are to kilovolts, and references to “MVA” are to megavolt amperes. References to “BTU” and “MBTU” are to a British thermal unit and million British thermal units, respectively. A “BTU” is an energy unit equal to approximately 1,055 joules. References to “Hz” are to hertz, and references to “mtpa” are to metric tons per annum. Unless otherwise indicated, statistics provided in this

11

Report concerning the installed capacity of electricity generation facilities are expressed in MW. One TW equals 1,000 GW, one GW equals 1,000 MW, and one MW equals 1,000 kW. Starting in 2018, the installed capacity we present in this Report corresponds to the net installed capacity, which considers the MW that each power plant consumes for its operation. Prior to 2018, the installed capacity we present in this Report corresponds to the gross installed capacity, without considering the MW that each power plant consumes for its operation. Starting in 2020, the electricity sales we present in this Report correspond to gross energy sales. 2019 amounts have been updated to correspond to this new presentation, but 2018 amounts have not been updated to correspond to this new presentation. Beginning in 2020, in calculating the number of customers we consider all customers with a current contract in a given period (rather than only those customers with a current contract who were supplied with energy and billed for it in a given period). 2019 amounts have been updated to correspond to this new presentation, but 2018 amounts have not been updated to correspond to this new presentation.

Statistics relating to aggregate annual electricity production are expressed in GWh and based on a year of 8,760 hours, except for a leap year like 2020, which is based instead on 8,784 hours. Statistics relating to installed capacity and production of the electricity industry do not include electricity of self-generators.

Energy losses experienced by generation companies during transmission are calculated by subtracting the number of GWh of energy sold from the number of GWh of energy generated (excluding their energy consumption and losses on the part of the power plant) within a given period. Losses are expressed as a percentage of total energy generated.

Energy losses during distribution are calculated as the difference between total energy purchased (GWh of electricity demand, including own generation) and the energy sold excluding tolls and energy consumption not billed (also measured in GWh) within a given period. Distribution losses are expressed as a percentage of the total energy purchased. Losses in distribution arise from illegally tapped energy as well as technical losses.

Calculation of Economic Interest

In this report, references are made to the “economic interest” of Enel Américas in its related companies. We could have a direct and indirect interest in such companies. In circumstances in which we do not directly own an interest in a related company, our economic interest in such ultimate affiliated company is calculated by multiplying the percentage of economic interest in a directly held related company by the percentage of economic interest of any entity in the ownership chain of such affiliated company. For example, if we directly own a 6% equity stake in an affiliated company and 40% is directly held by our 60%-owned subsidiary, our economic interest in such associate would be 60% times 40% plus 6%, equal to 30%.

Rounding

Figures included in this Report have been rounded for ease of presentation. Due to rounding, the sums in tables do not always exactly equal the sums of the entries.

12

This Report contains statements that are or may constitute forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). These statements appear throughout this Report and include statements regarding our intent, belief, or current expectations, including but not limited to any statements concerning:

● | our capital investment program; |

● | trends affecting our financial condition or results of operations; |

● | our dividend policy; |

● | the future impact of competition and regulation; |

● | political and economic conditions in the countries in which our related companies or we operate or may operate in the future; |

● | any statements preceded by, followed by, or that include the words “believes,” “expects,” “predicts,” “anticipates,” “intends,” “estimates,” “should,” “may,” or similar expressions; and |

● | other statements contained or incorporated by reference in this Report regarding matters that are not historical facts. |

Because such statements are subject to risks and uncertainties, actual results may differ materially from those expressed or implied by such forward-looking statements. Factors that could cause actual results to differ materially include but are not limited to:

● | demographic developments, political events, economic fluctuations, social unrest, public health crises and pandemics, and interventionist measures by authorities in the markets in South America in which we operate; |

● | hydrology, droughts, flooding, and other weather conditions; |

● | changes in the environmental regulations and the regulatory framework of the electricity industry in one or more of the countries in which we operate; |

● | our ability to implement proposed capital expenditures, including our ability to arrange financing where required; |

● | the nature and extent of future competition in our principal markets; and |

● | the factors discussed below under “Risk Factors.” |

You should not place undue reliance on such statements, which speak only as of the date that they were made. Our independent registered public accounting firm has not examined or compiled the forward-looking statements and, accordingly, does not provide any assurance concerning such statements. You should consider these cautionary statements together with any written or oral forward-looking statements that we may issue in the future. We do not undertake any obligation to release publicly any revisions to forward-looking statements contained in this Report to reflect later events or circumstances or the occurrence of unanticipated events, except as required by law.

For all these forward-looking statements, we claim the protection of the safe harbor for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995.

13

On April 1, 2021, we completed the acquisition of EGP Américas SpA, a wholly-owned subsidiary of Enel S.p.A., our controlling shareholder, through a merger of EGP Américas SpA with and into Enel Américas. Prior to the merger, EGP Américas SpA, a newly-formed company, held the renewable energy generation businesses in Central and South America (outside of Chile) previously held by Enel Green Power S.p.A. As a result of the merger, we have now strengthened our renewable energy generation business and diversified geographically through exposure to Costa Rica, Guatemala, and Panama, in addition to acquiring new assets in South American countries where we were already present. Enel S.p.A.’s ownership interest in us increased to 75.2% as of April 1, 2021.

On March 15, 2021, Enel S.p.A. launched dual Chilean and U.S. partial public tender offers to acquire shares and ADS of Enel Américas, representing 10% of our then-current share capital, for a cash purchase price of Ch$ 140 per share and the U.S. dollar equivalent of Ch$ 7,000 per ADS. The tender offers expired on April 13, 2021, and the shares and ADSs were accepted for purchase by Enel S.p.A. on April 16, 2021. As a result of the merger and the tender offers, Enel S.p.A. owns 82.3% of our share capital as of the date of this Report.

After giving effect to the issuance of new shares in connection with the merger, and as of the date of this Report, there are 107,281,698,561 shares of common stock outstanding. For additional information on the merger and the tender offers, please see “Item 4. Information on the Company — A. History and Development of the Company — History” and “— Merger with EGP Américas and Related Tender Offer.”

14

Item 1. Identity of Directors, Senior Management and Advisers

Not applicable.

Item 2. Offer Statistics and Expected Timetable

Not applicable.

A. Selected Financial Data.

The following selected consolidated financial data should be read in conjunction with our consolidated financial statements included in this Report. The selected consolidated financial data as of December 31, 2020 and 2019, and for the three years ended December 31, 2020, are derived from our audited consolidated financial statements included in this Report. The selected consolidated financial data as of December 31, 2018, 2017, and 2016, and for the years ended December 31, 2017, and 2016 are derived from our consolidated financial statements not included in this Report. Our consolidated financial statements were prepared in accordance with IFRS, as issued by the IASB.

Our consolidated financial statements are presented in U.S. dollars because of our functional currency’s change from Chilean pesos to U.S. dollars in 2017. The change of our functional currency was recorded as of January 1, 2017, by translating all items of our consolidated financial statements to the new functional currency, using the closing exchange rate at the date of exchange. We also changed the presentation currency of our consolidated financial statements from Chilean pesos to U.S. dollars. The change in the presentation currency was applied retrospectively as if the U.S. dollar had always been the consolidated financial statements’ presentation currency. The consolidated statement of financial position data as of December 31, 2016, was translated into U.S. dollars using the closing U.S. dollar Observed Exchange Rate (dólar observado) of Ch$ 669.47 per US$ 1.00. The consolidated statement of comprehensive income data for the year ended December 31, 2016, was translated into U.S. dollars using the average exchange rate of Ch$ 676.19 per US$ 1.00. For further information about our functional currency, please refer to Note 2.8 of the Notes to our consolidated financial statements The Observed Exchange Rate, which is reported and published daily on the Central Bank of Chile’s web page, corresponds to the weighted-average exchange rate of the previous business day’s transactions in the Formal Exchange Market. For more information concerning historical exchange rates, see “— Exchange Rates” below. The tables are expressed in millions of U.S. dollars, except for ratios, operating data, and data for shares and American Depositary Shares (“ADS”).

15

The following tables set forth our selected consolidated financial data for the years indicated and the operating data of our principal subsidiaries:

| | | | | | | | | | |

| | As of and for the year ended December 31, | ||||||||

|

| 2020 |

| 2019 |

| 2018 |

| 2017 |

| 2016 |

| | (US$ millions) | ||||||||

Consolidated Statement of Comprehensive Income Data | | | | | | | | | | |

Revenues and other operating income | | 12,193 | | 14,314 | | 12,990 | | 10,438 | | 7,643 |

Operating costs(1) | | (10,140) | | (11,545) | | (10,555) | | (8,219) | | (5,843) |

Operating income from continuing operations | | 2,053 | | 2,769 | | 2,435 | | 2,219 | | 1,800 |

Financial results(2) | | (313) | | (378) | | (333) | | (582) | | (439) |

Other gains | | 5 | | 14 | | 1 | | 5 | | 12 |

Share of profit (loss) of associates and joint venture accounted for using the equity method | | 3 | | 1 | | 2 | | 3 | | 3 |

Income from continuing operations before income tax | | 1,748 | | 2,406 | | 2,105 | | 1,646 | | 1,376 |

Income tax expenses, continuing operations | | (567) | | (236) | | (438) | | (519) | | (531) |

Net Income from continuing operations | | 1,181 | | 2,170 | | 1,667 | | 1,127 | | 845 |

Profit after tax from discontinued operations | | — | | — | | — | | — | | 170 |

Net income | | 1,181 | | 2,170 | | 1,667 | | 1,127 | | 1,015 |

Net income attributable to the parent Company | | 825 | | 1,614 | | 1,201 | | 709 | | 566 |

Net income attributable to non-controlling interests | | 356 | | 556 | | 466 | | 417 | | 448 |

Basic and diluted earnings from continuing operations per average number of shares (US$ per share) | | 0.011 | | 0.025 | | 0.021 | | 0.012 | | 0.009 |

Basic and diluted earnings from continuing operations per average number of ADS (US$ per ADS) | | 0.542 | | 1.233 | | 1.045 | | 0.617 | | 0.453 |

Basic and diluted earnings from discontinued operations per average number of shares (US$ per share) | | ― | | ― | | ― | | ― | | 0.002 |

Basic and diluted earnings from discontinued operations per average number of ADS (US$ per ADS) | | ― | | ― | | ― | | ― | | 0.116 |

Total basic and diluted earnings per average number of shares (US$ per share) | | 0.011 | | 0.025 | | 0.021 | | 0.012 | | 0.009 |

Total basic and diluted earnings per average number of ADS (US$ per ADS) | | 0.542 | | 1.233 | | 1.045 | | 0.617 | | 0.453 |

Cash dividends per share (US$ per share) | | 0.011 | | 0.008 | | 0.006 | | 0.005 | | 0.007 |

Cash dividends per ADS (US$ per ADS) | | 0.530 | | 0.419 | | 0.309 | | 0.249 | | 0.332 |

Weighted average number of shares of common stock (millions) | | 76,086 | | 65,481 | | 57,453 | | 57,453 | | 49,769 |

| | | | | | | | | | |

Consolidated Statement of Financial Position Data | | | | | | | | | | |

Total assets | | 26,934 | | 29,776 | | 27,396 | | 20,169 | | 16,851 |

Non-current liabilities | | 9,323 | | 10,794 | | 8,914 | | 6,956 | | 5,150 |

Equity attributable to the parent company | | 8,106 | | 9,966 | | 6,724 | | 6,481 | | 6,200 |

Equity attributable to non-controlling interests | | 2,228 | | 2,280 | | 2,108 | | 1,798 | | 1,680 |

Total equity | | 10,334 | | 12,246 | | 8,832 | | 8,279 | | 7,880 |

Capital stock(3) | | 9,763 | | 9,784 | | 6,763 | | 6,763 | | 6,904 |

| | | | | | | | | | |

Other Consolidated Financial Data | | | | | | | | | | |

Capital expenditures (CAPEX)(4) | | 1,553 | | 1,659 | | 1,541 | | 1,371 | | 1,230 |

Depreciation, amortization and impairment losses(5) | | 1,100 | | 1,225 | | 923 | | 728 | | 630 |

| (1) | Operating expenses represent raw materials and consumables used, other work performed by the entity and capitalized, employee benefit expenses, depreciation and amortization expenses, impairment loss recognized in the period’s profit or loss, and other expenses. |

| (2) | Financial results represent (+) financial income, (-) financial expenses, (+/-) foreign currency exchange differences, and net gains/losses from indexed assets and liabilities. |

| (3) | Capital stock represents issued capital. |

| (4) | CAPEX figures represent cash flows used to purchase property, plant, and equipment, and intangible assets for each year. |

| (5) | Please refer to Note 31 of the Notes to our consolidated financial statements for further detail. |

16

| | | | | | | | | | |

| | As of and for the year ended December 31, | ||||||||

|

| 2020 |

| 2019 |

| 2018 |

| 2017 |

| 2016 |

OPERATING DATA OF PRINCIPAL SUBSIDIARIES(1) | | | | | | | | | | |

| | | | | | | | | | |

Edesur (Argentina) | | | | | | | | | | |

Electricity sold (GWh) | | 15,888 | | 16,798 | | 17,548 | | 17,736 | | 18,493 |

Number of customers (thousands) | | 2,508 | | 2,490 | | 2,530 | | 2,529 | | 2,505 |

Total energy losses (%)(2) | | 18.9 | | 15.5 | | 14.2 | | 12.0 | | 12.0 |

| | | | | | | | | | |

Enel Distribution Rio (Brazil) | | | | | | | | | | |

Electricity sold (GWh) | | 11,228 | | 11,568 | | 11,019 | | 11,091 | | 11,181 |

Number of customers (thousands) | | 2,948 | | 2,940 | | 2,959 | | 3,030 | | 3,054 |

Total energy losses (%)(2) | | 22.1 | | 22.5 | | 21.0 | | 20.4 | | 19.4 |

| | | | | | | | | | |

Enel Distribution Ceara (Brazil) | | | | | | | | | | |

Electricity sold (GWh) | | 11,866 | | 12,197 | | 11,843 | | 11,522 | | 11,628 |

Number of customers (thousands) | | 4,011 | | 3,956 | | 3,933 | | 4,017 | | 3,890 |

Total energy losses (%)(2) | | 15.9 | | 14.0 | | 13.9 | | 13.6 | | 12.5 |

| | | | | | | | | | |

Enel Distribution Goias (Brazil) | | | | | | | | | | |

Electricity sold (GWh) | | 14,469 | | 14,365 | | 13,755 | | 12,264 | | ― |

Number of customers (thousands) | | 3,207 | | 3,114 | | 3,027 | | 2,928 | | ― |

Total energy losses (%)(2) | | 11.4 | | 12.3 | | 11.6 | | 11.7 | | ― |

| | | | | | | | | | |

Enel Distribution Sao Paulo (Brazil) | | | | | | | | | | |

Electricity sold (GWh) | | 40,350 | | 43,148 | | 24,693 | | ― | | ― |

Number of customers (thousands) | | 7,896 | | 7,777 | | 7,224 | | ― | | ― |

Total energy losses (%)(2) | | 10.6 | | 9.6 | | 9.5 | | ― | | ― |

| | | | | | | | | | |

Codensa (Colombia) | | | | | | | | | | |

Electricity sold (GWh) | | 13,834 | | 14,307 | | 14,024 | | 13,790 | | 13,632 |

Number of customers (thousands) | | 3,615 | | 3,527 | | 3,439 | | 3,340 | | 3,248 |

Total energy losses (%)(2) | | 7.6 | | 7.7 | | 7.7 | | 7.8 | | 7.1 |

| | | | | | | | | | |

Enel Distribution Peru (Peru) | | | | | | | | | | |

Electricity sold (GWh) | | 7,578 | | 8,211 | | 8,045 | | 7,934 | | 7,782 |

Number of customers (thousands) | | 1,456 | | 1,434 | | 1,423 | | 1,397 | | 1,367 |

Total energy losses (%)(2) | | 8.8 | | 8.2 | | 8.1 | | 8.2 | | 7.8 |

| | | | | | | | | | |

Enel Américas | | | | | | | | | | |

Installed capacity in Argentina (MW)(3) | | 4,419 | | 4,419 | | 4,419 | | 4,419 | | 4,537 |

Installed capacity in Brazil (MW)(3)(4) | | 1,354 | | 1,354 | | 1,354 | | 1,354 | | 1,372 |

Installed capacity in Colombia (MW)(3) | | 3,506 | | 3,506 | | 3,499 | | 3,467 | | 3,509 |

Installed capacity in Peru (MW)(3) | | 1,990 | | 1,987 | | 1,985 | | 1,979 | | 2,026 |

Generation in Argentina (GWh) | | 13,901 | | 12,974 | | 13,949 | | 14,825 | | 13,124 |

Generation in Brazil (GWh)(4) | | 4,823 | | 5,292 | | 3,755 | | 4,034 | | 4,034 |

Generation in Colombia (GWh) | | 14,009 | | 15,250 | | 14,052 | | 14,765 | | 14,952 |

Generation in Peru (GWh) | | 7,722 | | 8,244 | | 8,106 | | 7,430 | | 8,698 |

| (1) | Some information may be different than reported in previous periods. For further details, please refer to “Item 4. Information on the Company — B. Business Overview. — Electricity Distribution Business.” |

| (2) | Energy losses in distribution arise from illegally tapped energy and technical losses. They are calculated as the difference between total energy generated and purchased (GWh) and energy sold, excluding tolls and energy consumption not billed (GWh) within a given period. Losses are expressed as a percentage of the total energy purchased. |

| (3) | Installed capacity figures may differ from previous years due to the fact that, starting in 2018, we began reporting the net installed capacity instead of the gross installed capacity. |

| (4) | Since 2017, data includes Volta Grande hydroelectric plant’s capacity and generation due to its acquisition and consolidation since November 2017. |

17

Exchange Rates

Fluctuations in the exchange rate between the Chilean peso and the U.S. dollar will affect the U.S. dollar equivalent of the price in Chilean pesos of our shares of common stock on the Santiago Stock Exchange (Bolsa de Comercio de Santiago) and the Chilean Electronic Stock Exchange (Bolsa Electrónica de Chile). These fluctuations in the exchange rate affect the price of our ADS and the dividends we pay (see “Item 8. Financial Information — A. Consolidated Statements and Other Financial Information — Dividends”). Also, to the extent that significant financial liabilities are denominated in foreign currencies, fluctuations in the exchange rate may significantly impact our earnings.

For further details regarding fluctuation in the exchange rates between the U.S. dollar and the local currency in each of the countries in which we operate, please refer to “Item 5. Operating and Financial Review and Prospects — a. Operating Results. — 1. Discussion of Main Factors Affecting Operating Results and Financial Condition of the Company — d. Economic Conditions — Local Currency Exchange Rate.”

B. Capitalization and Indebtedness.

Not applicable.

C. Reasons for the Offer and Use of Proceeds.

Not applicable.

D. Risk Factors.

Risk Related to Our Business

Our businesses depend heavily on hydrology and are affected by droughts, flooding, storms, ocean currents, and other inclement weather conditions.

Approximately 55% of our consolidated installed generation capacity in 2020 was hydroelectric. Accordingly, arid hydrological conditions could negatively affect our business, results of operations, and financial condition. Regional hydrological conditions have often been subject to two weather phenomena dealing with ocean currents - El Niño and La Niña - that influence rainfall and may result in drought or flooding, depending on the region affected. Droughts may affect our ability to dispatch energy from our hydroelectric facilities.

In the past, El Niño has affected Colombian hydrologic conditions, where 88% of our installed capacity is hydroelectric, leading to rainfall deficits, high temperatures, and higher energy prices. In March 2017, “El Niño Costero” in Peru led to unusually intensive rains that flooded the Santa Eulalia River, caused innumerable landslides and avalanches in the coastal basins, and resulted in the stoppage of several of our hydroelectric power plants, mainly Callahuanca (84 MW) and Moyopampa (69 MW). Each ocean current event is unique and, depending on its intensity and duration, the magnitude of the social and economic effects could be material.

Our distribution business is also affected by inclement weather, mainly in Argentina. With extreme temperatures, demand can increase significantly within a short period, affecting service and resulting in service outages that may result in fines. Depending on weather conditions, results obtained by our distribution business can vary from year to year.

Our operating expenses increase during drought periods when thermal power plants, which have higher operating costs relative to hydroelectric power plants, are dispatched more frequently. Depending on our commercial obligations, we may need to buy electricity at higher spot prices to comply with our contractual supply obligations. Beyond increasing operating costs, the cost of these electricity purchases may exceed our contracted electricity sale prices, thus potentially producing losses from those contracts. For further information concerning the effect of hydrology on our business and financial results, please refer to “Item 5. Operating and Financial Review and Prospects— A. Operating Results — 1. Discussion of Main Factors Affecting Operating Results and Financial Condition of the Company—a. Generation and Transmission Business.”

18

Droughts also indirectly affect the operation of our thermal power plants, including our facilities that use natural gas, fuel oil, or coal, in the following manner:

● | Our thermal power plants require water for cooling, and droughts may reduce water availability and increase transportation costs. As a result, we may have to purchase water from agricultural areas that are also experiencing water shortages. These water purchases may increase our operating costs and require us to negotiate further with the local communities. |

● | Thermal power plants generate emissions such as nitrogen oxide (NO), carbon dioxide (CO2), carbon monoxide (CO), sulfur dioxide (SO2), and particulate matter into the atmosphere. Therefore, greater use of thermal power plants during droughts generally increases the risk of producing higher greenhouse gas (GHG) emissions. |

A full recovery from the drought affecting the regions where most of our hydroelectric power plants are located may last for an extended period, and new drought periods may recur in the future. Prolonged droughts may exacerbate the risks described above and have a further negative effect on our business, results of operations, and financial condition.

We depend on payments from our subsidiaries and associates to meet our payment obligations.

We rely on cash from dividends, loans, interest payments, capital reductions, and other distributions from our subsidiaries and equity affiliates to pay our obligations. Such payments and distributions are subject to legal constraints, such as dividend restrictions, fiduciary obligations, contractual limitations, and foreign exchange controls imposed by local authorities.

Historically, we have not always accessed some of our operating subsidiaries’ cash flows due to government regulations, strategic considerations, economic conditions, and credit restrictions. In the future, we may not always be able to immediately rely on cash flows from operating subsidiaries to repay our debt.

Dividend Limits and Other Legal Restrictions: Some of our subsidiaries are subject to legal reserve requirements and other restrictions on dividend payments. Other legal restrictions, such as foreign currency controls, may limit our subsidiaries and equity affiliates’ ability to pay dividends and make loan payments or other distributions to us. Their directors’ fiduciary duties to their minority shareholders may restrict the ability of any of our subsidiaries that are not wholly-owned to distribute cash to us. Furthermore, local authorities may force some of our subsidiaries, under applicable regulation, to reduce or eliminate dividend payments. These restrictions could impede our subsidiaries from distributing cash to us under certain circumstances.

Contractual Constraints: Distribution restrictions included in the credit agreements of our subsidiaries, including most of our subsidiaries in Brazil, may prevent dividends and other distributions to shareholders if they do not comply with specified financial ratios. Our credit agreements typically prohibit any distributions in the event of ongoing default.

Operating Results of Our Subsidiaries: Our subsidiaries and equity affiliates’ ability to pay dividends or make loan payments or other distributions to us is limited by their operating results. To the extent that any of our subsidiaries’ cash requirements exceed their available cash, they will not be able to make funds available to us.

The currency of any dividend paid by our subsidiaries is subject to depreciation in relation to our functional currency, which may adversely affect our ability to pay dividends to shareholders.

The situations described above could adversely affect our business, results of operations, and financial condition.

We are involved in litigation proceedings.

We are involved in various litigation proceedings that could result in unfavorable decisions or financial penalties against us. In Colombia, we exercise control over Emgesa and Codensa through shareholder agreements with Grupo Energía Bogotá S.A. (“GEB”). In October 2018, GEB initiated arbitration proceedings for alleged breach of the shareholder agreements concerning the failure to distribute 100% of the profits in 2016, 2017, and 2018 in Emgesa and Codensa and the breach of other provisions of the shareholders’ agreement, and also requested compensation for damages. The financial claim amounts to COP$ 1,876,417,133 thousand (US$ 548.3 million) plus interest. An adverse

19

ruling could set a precedent that would oblige us always to vote in favor of a 100% distribution of distributable profits, which in turn might not always be financially prudent.

Our financial condition or results of operations could be unfavorably affected if we are unsuccessful in defending litigations or other lawsuits and proceedings against us. Please see Note 35.3 of the Notes to our consolidated financial statements for further information on litigation proceedings.

Construction and operation of power plants may encounter significant delays, stoppages, cost overruns, and stakeholder opposition that may damage our reputation and potentially impair our goodwill with stakeholders.

Our power plant projects may be delayed in obtaining regulatory approvals or may face shortages and increases in the price of equipment, materials, or labor. They may be subject to construction delays, strikes, accidents, and human error. Any such event could negatively affect our business, results of operations, and financial condition.

Market conditions may change significantly between the approval and completion of a project, which, in some cases, may decrease a project’s profitability or render it impracticable. Deviations in market conditions, such as estimates of timing and expenditures, may lead to cost overruns and delays in project completion that widely exceed our initial forecasts. In turn, this may have a material adverse effect on our business, results of operations, and financial condition.

We may develop new projects in locations that are sometimes challenging in geographical topography, such as mountain slopes, jungles, or other areas with limited access. Additionally, given some projects’ locations, there may be additional inherent risks to archeological heritage sites. These factors may also lead to significant delays and cost overruns.

Our thermal power plants’ operation, especially those that are coal-fired, may affect our goodwill with stakeholders due to GHG emissions that could unfavorably affect the environment and nearby residents. Furthermore, outside stakeholders may influence the interests and perceptions of the local communities about the Company. If we fail to address appropriately all relevant stakeholders’ concerns, including environmental, social and governance criteria (“ESG”), we may face opposition, which could negatively affect our reputation, stall operations, or lead to litigation threats or actions. Our reputation is the foundation of our relationship with key stakeholders and other constituencies. If we do not effectively manage these sensitive issues, they could adversely affect our business, results of operations, and financial condition.

Damage to our reputation may exert considerable pressure on regulators, creditors, and other stakeholders, possibly leading to the abandonment of projects and operations. This damage could cause our share prices to drop and hinder our ability to attract and retain valuable employees. Any of these outcomes could result in an impairment of our goodwill with stakeholders.

Our long-term energy sales contracts are subject to fluctuations in the market prices of certain commodities, energy, and other factors.

We have exposure to fluctuations in certain commodity market prices that affect our long-term energy sales contracts. These contracts commit our subsidiaries to material obligations as selling parties and contain prices indexed to different commodities, exchange rates, inflation, and the market price of electricity. Unfavorable changes to these indices would reduce the rates we charge under these contracts, which could adversely affect our business, results of operations, and financial condition. In our distribution business, we also have economic exposure to fluctuations in energy prices.

We are subject to incremental risks in distribution markets that are becoming more liberalized.

In some countries, our distribution customers who meet the minimum and maximum demand requirements may freely choose unregulated tariffs. This flexibility may adversely affect our operating income. In some cases, customers may choose an alternative energy provider, which could adversely affect our business, results of operations, and financial condition.

20

Our electricity business is subject to risks arising from natural disasters, catastrophic accidents, and acts of vandalism or terrorism, which could unfavorably affect our operations, earnings, and cash flow.

Our primary facilities include power plants and transmission and distribution assets that are exposed to damage from catastrophic natural disasters, such as earthquakes and fires, human causes, as well as acts of vandalism, protests, riots, and terrorism. A catastrophic event could cause prolonged unavailability of our assets, disruptions in our business, significant decreases in revenues due to lower demand, or significant additional costs not covered by our business interruption insurance. There may be lags between a significant accident or catastrophic event and the final reimbursement from our insurance policies, which typically carry a deductible and are subject to per event policy maximum amounts.

In mid-October 2019, widespread street demonstrations and protests erupted in Santiago and quickly spread throughout Chile. These actions became commonplace and, at times, were accompanied by looting, arson, and vandalism. Violent confrontations between protesters and the police and armed forces resulted in a significant loss of human lives and serious injuries. Accumulated damage to public and private property amounted to billions of dollars. Damage to the country’s economy, prospects for growth, perception of risk, and immediate repercussions in unemployment and productivity loss were also significant. Our corporate headquarters in Santiago suffered a severe arson attack on October 18, 2019, resulting in the dislocation of our management and headquarters employees for an extended period. In a globalized and interconnected world, all the countries in which we operate are subject to this risk.

Any natural or human catastrophic disruption to our electricity assets in the countries in which we operate could significantly affect our results of operations and financial condition.

We are subject to financing risks, such as those associated with funding our new projects and capital expenditures or refinancing existing obligations.

As of December 31, 2020, our consolidated debt totaled US$ 6.1 billion, and our holding company debt in Chile totaled US$ 1.1 billion. As of December 31, 2020, we held US$ 601 million in SEC-registered bonds issued in the U.S. and had drawn bank debt under Senior Unsecured Revolving Credit Agreements in the aggregate amount of US$ 325 million, all governed under the laws of the State of New York.

Our debt agreements are subject to several of the following provisions, including (1) financial covenants, (2) affirmative and negative covenants, (3) events of default, (4) mandatory prepayments for contractual breaches, (5) change of control clauses for material mergers and divestments, and (6) bankruptcy and insolvency proceeding covenants, among others.

A significant portion of our financial indebtedness is subject to cross default provisions, which have varying definitions, criteria, materiality thresholds, and applicability concerning subsidiaries that could result in cross default. Our debt may also become immediately due and payable in cases involving bankruptcy or insolvency proceedings of a significant or material subsidiary. Likewise, some of our debtholders may decide to accelerate our debt in cross default events dealing with significant or material subsidiaries, among other potential covenant defaults.

We may be unable to refinance our debt or obtain such refinancing in terms acceptable to us. In the absence of such refinancing, we could be forced to liquidate assets at unfavorable prices to make payments due on our debt. Furthermore, we may be unable to sell our assets at opportune moments or sufficiently high prices to obtain proceeds that would enable us to make such payments.

We may also be unable to raise the necessary funds required to finish our projects under development or construction. Market conditions or unforeseen project costs prevailing when we need funds could compromise our ability to finance these projects and expenditures.

As of the date of this Report, Brazil is the country with our highest refinancing risk. As of December 31, 2020, the debt of our Brazilian subsidiaries amounted to US$ 2.5 billion while the debt of our Colombian subsidiaries amounted to US$ 1.7 billion.

Our inability to finance new projects or capital expenditures, refinance our existing debt, or comply with our covenants could negatively affect our results of operations and financial condition.

21

If third-party electricity transmission facilities, gas pipeline infrastructure, or fuel supply contracts fail to provide us with adequate service, we may be unable to deliver the electricity we sell to our final customers.

We depend on transmission facilities owned and operated by other companies to deliver the electricity we sell. This dependence exposes us to several risks. If the transmission is disrupted, or its capacity is inadequate, we may be unable to sell and deliver our electricity. If a region’s power transmission infrastructure is inadequate, our recovery of sales costs and profits may be insufficient. If restrictive transmission price regulations are imposed, transmission companies may not have sufficient incentives to invest in expanding their infrastructure, which could unfavorably affect our results of operations and financial condition or affect our ability to deploy our portfolio of projects under development. The construction of new transmission lines may take longer than in the past, mainly because of sustainability, social, and environmental requirements that create uncertainties regarding project completion timing. As a result, in some of the countries in which we operate, renewable energy projects are being completed faster than new transmission projects, creating a backlog of electricity that can be transmitted through current transmission systems. In Argentina, for example, the lack of investment in transmission lines will reduce incentives for the development of renewable energy projects.

We also rely on pipelines to obtain natural gas, mainly in Peru, where more than 50% of our generation capacity is thermal. In recent years, the Peruvian system has occasionally faced gas and electricity shortages due to a lack of sufficient capacity in the pipeline and transmission lines, which led to higher spot prices. Depending on the facility type, our thermal generation power plants purchase gas, coal, diesel, and other fuels to produce electricity. Any contract breach or supply shortage may prevent our facilities from producing electricity on time.

We may be unable to reach satisfactory collective bargaining agreements with our unionized employees or retain key employees in labor conflict cases.

A large percentage of our employees are members of unions with which we have collective bargaining agreements that must be renewed regularly. Our business, results of operations, and financial condition could be unfavorably affected by a failure to reach a collective bargaining agreement with any labor union or by a deal with a labor union that contains terms we view as unfavorable. Laws in many of the countries in which we operate provide legal mechanisms for judicial authorities to impose a collective bargaining agreement if the parties cannot come to an agreement, which may materially increase our costs.

We employ many highly specialized employees. Specific actions such as strikes, walkouts, or work stoppages by these employees could negatively impact our business, results of operations, financial conditions, and reputation.

We may be unable to enter into suitable acquisitions or successfully integrate businesses that we acquire.

We review acquisition prospects that may increase our market coverage or provide synergies with our existing businesses on an ongoing basis. However, there can be no assurance that we will be able to identify and acquire suitable companies in the future. The acquisition and integration of independent companies that we do not control is generally a complicated, costly, and time-consuming process that requires significant efforts and expenditures. For example, as a result of the acquisition of Enel Distribution Sao Paulo in 2018, our leverage at the onset increased considerably due to the new debt for the purchase itself and the consolidation of Enel Distribution Sao Paulo’s existing debt.

Integrating acquired businesses may be difficult, expensive, time-consuming, and a strain on our resources and relationships with our employees and customers. Ultimately, these acquisitions may not be successful or achieve the expected benefits. Any delays or difficulties encountered in connection with acquisitions and the integration of their operations could have a material adverse effect on our business, results of operations, or financial condition.

For example, our integration with EGP Américas may be difficult and expensive. The merger with EGP Américas involves integrating a mature business, as is the case of our conventional energy business, with EGP Américas’ non-conventional renewable energy business. Our goal in integrating the operations is to increase the revenues and earnings of the combined businesses and, as a combined company, to improve our ability to satisfy our customers’ demands. In so doing, we may encounter substantial difficulties in integrating our operations and could incur high costs as a result of, among other things:

| ● | inconsistencies in standards, controls, procedures and policies, business cultures and compensation structures between EGP Américas and us and the need to implement, integrate and harmonize various business-specific |

22

| operating procedures and systems, as well as our financial, accounting, information, and other systems and those of EGP Américas; |

| ● | diversion of management’s attention from their other responsibilities as a result of the need to deal with integration issues; |

| ● | failure to retain our customers and suppliers and those of EGP Américas; |

| ● | difficulties in achieving full utilization of our assets and resources and those of EGP Américas; and |

| ● | complications in retaining key employees (who may depart because of issues relating to the uncertainty and difficulty of integration or general discontent) or efficiently managing the broader organization. |

Under any of these circumstances, the business growth opportunities, revenue benefits, and other benefits anticipated by us to result from the completion of the merger with EGP Américas may not be achieved as expected. To the extent that we incur higher integration costs or achieve lower revenue benefits than expected, our results of operations and financial condition may suffer. The diversion of management attention and any difficulties encountered from this merger could increase costs or reduce our revenues, earnings, and operating results. Any delays encountered in the integration process could have an adverse effect on our revenues, expenses, operating results, and financial condition, which may adversely affect our securities’ value.

Interruption in or failure of our information technology, control, and communications systems or cyberattacks to or cybersecurity breaches of these systems could have a material adverse effect on our business, results of operations, and financial condition.

We operate in an industry that requires the continued operation of sophisticated information technology, control, and communications systems (“IT Systems”) and network infrastructure. We use our IT Systems and infrastructure to create, collect, use, disclose, store, dispose of, and otherwise process sensitive information, including company and customer data and personal information regarding customers, employees and their dependents, contractors, shareholders, and other individuals. IT Systems are critical to controlling and monitoring our power plants’ operations, maintaining generation and network performance, generating invoices to bill customers, achieving operating efficiencies, and meeting our service targets and standards in our generation business. The operation of our generation system is dependent not only on the physical interconnection of our facilities with the electricity network infrastructure but also on communications among the various parties connected to the network. The reliance on IT Systems to manage information and communication among those parties has increased significantly since the implementation of smart meters and intelligent grids in Brazil and Colombia.

Our generation facilities, IT Systems, and other infrastructure and the information processed in our IT Systems, could be affected by cybersecurity incidents, including those caused by human error. Our industry has begun to see an increased volume and sophistication of cybersecurity incidents from international activist organizations, nation-states, and individuals and are among the emerging risks identified in our planning process. Cybersecurity incidents could harm our business by limiting our generation capabilities, delaying our development and construction of new facilities or capital improvement projects to existing facilities, disrupting our customer operations, or exposing us to various events that could compromise our liability. Our business systems are part of an interconnected system. Therefore, a disruption caused by the impact of a cybersecurity incident in the electric transmission grid, network infrastructure, fuel sources, or our third-party service providers’ operations could also unfavorably affect our business.

Our business requires the collection and storage of personally identifiable information of our customers, employees, and shareholders, who expect that we will adequately protect the privacy of such information. Cybersecurity breaches may expose us to a risk of loss or misuse of confidential and proprietary information. Significant theft, loss, or fraudulent use of personally identifiable information may lead to high costs to notify and protect the impacted persons. It could cause us to become subject to significant litigation, losses, liability, fines, or penalties, any of which could materially and adversely affect our results of operations and reputation. We would eventually have to incur significant costs associated with governmental actions in response to such intrusions or strengthen our information and electronic control systems.

23

The cybersecurity threat is dynamic, evolving, and increasing in sophistication, magnitude, and frequency. We may be unable to implement adequate preventive measures or accurately assess the likelihood of a cybersecurity incident. We are unable to quantify the potential impact of cybersecurity incidents on our business and reputation. These potential cybersecurity incidents and corresponding regulatory action could result in a material decrease in revenues and high additional costs, including penalties, third-party claims, repair costs, increased insurance expense, litigation costs, notification and remediation costs, security costs, and compliance costs.

Risk Related to Regulatory Matters

Governmental regulations may unfavorably affect our businesses, cause delays, impede the development of new projects, or increase the costs of operations and capital expenditures.

Our businesses and the tariffs we charge to our customers are subject to extensive regulation that may negatively affect our profitability. For example, governmental authorities in any of the countries where we operate may impose material rationing policies during droughts or prolonged failures of power facilities, which may adversely affect our business, results of operations, and financial condition.

Electricity regulations issued by governmental authorities in the countries where we operate may affect our generation companies’ ability to collect revenues sufficient to offset their operating costs, which could adversely affect our business, results of operations, and financial condition. Governmental authorities may also delay the distribution tariff review process, or tariff adjustments determined by regulatory authorities may be insufficient to pass on our costs to customers.

Our operating subsidiaries are also subject to environmental regulations that, among other things, require us to perform environmental impact studies on future projects and obtain construction and operating permits from local and national regulators. Governmental authorities may withhold or delay the approval of these permits until the completion of environmental impact studies. Therefore, their processing time may be longer than expected. Environmental regulations for existing and future generation capacity have become stricter and require increased capital investments. Any delay in meeting the required emission standards may constitute a violation of the environmental regulations. Failure to certify monitoring systems’ original implementation and ongoing emission standard requirements may result in significant penalties, sanctions, or legal claims for damages. We expect that more restrictive emission limits will be established in the future.

Changes to laws and regulations or governmental authorities’ interpretation of laws and regulations could result in delays or modifications to proposed projects, which could adversely affect our business, results of operations, and financial condition.

We are subject to potential business and financial risks resulting from climate change legislation and regulation to limit GHG emissions.

Future climate change legislation and regulation restricting or regulating GHG emissions could increase our operating costs and have a material adverse effect on our business, results of operations, and financial condition. The adoption and implementation of any international treaty, legislation, or regulation imposing new or additional reporting obligations or limiting emissions of GHGs from our operations could require us to incur additional costs to comply with such requirements and possibly require the reduction or limitation of GHG emissions associated with our operations. These higher compliance standards may involve additional costs to operate and maintain our equipment and facilities, install emission controls, or pay taxes and fees relating to GHG emissions, which could have a material adverse effect on our business, results of operations, and financial condition.

Our business and profitability could be unfavorably affected if water rights are denied, if water concessions are granted with limited duration, or if the cost of water rights is increased.