Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| x | Annual report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the fiscal year ended December 31, 2012

or

| ¨ | Transition report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the transition period from to

Commission File No. 001-12561

BELDEN INC.

(Exact Name of Registrant as Specified in Its Charter)

| Delaware | 36-3601505 | |

(State or Other Jurisdiction of Incorporation or Organization) | (IRS Employer Identification No.) |

7733 Forsyth Boulevard

Suite 800

St. Louis, Missouri 63105

(Address of Principal Executive Offices and Zip Code)

(314) 854-8000

(Registrant’s Telephone Number, Including Area Code)

Securities registered pursuant to Section 12(b) of the Act:

Title of Each Class | Name of Each Exchange on Which Registered | |

| Common Stock, $.01 par value | The New York Stock Exchange | |

| Preferred Stock Purchase Rights | The New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨.

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x.

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨.

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the Registrant has submitted electronically and posted on its corporate website, if any, every interactive data file required to be submitted and posted pursuant to Rule 405 of Regulation S-T (section 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨.

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b2 of the Exchange Act. (Check one):

| Large accelerated filer | x | Accelerated filer | ¨ | |||

| Non-accelerated filer | ¨ (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x.

At July 1, 2012, the aggregate market value of Common Stock of Belden Inc. held by non-affiliates was $1,306,632,356 based on the closing price ($33.35) of such stock on such date.

There were 44,517,866 shares of registrant’s Common Stock outstanding on February 19, 2013.

DOCUMENTS INCORPORATED BY REFERENCE

The registrant intends to file a definitive proxy statement for its annual meeting of stockholders within 120 days of the end of the fiscal year ended December 31, 2012 (the “Proxy Statement”). Portions of such proxy statement are incorporated by reference into Part III.

Table of Contents

Form 10-K Item No. | Name of Item | Page | ||||

| Part I | ||||||

| Item 1. | 1 | |||||

| Item 1A. | 8 | |||||

| Item 1B. | 14 | |||||

| Item 2. | 14 | |||||

| Item 3. | 15 | |||||

| Part II | ||||||

| Item 5. | Market for Registrant’s Common Equity and Related Shareholder Matters | 15 | ||||

| Item 6. | 18 | |||||

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 19 | ||||

| Item 7A. | 32 | |||||

| Item 8. | 35 | |||||

| Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 80 | ||||

Item 9A. Item 9B. |

| 80 83 |

| |||

| Part III | ||||||

| Item 10. | 83 | |||||

| Item 11. | 83 | |||||

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Shareholder Matters | 83 | ||||

| Item 13. | Certain Relationships and Related Transactions, and Director Independence | 83 | ||||

| Item 14. | 83 | |||||

| Part IV. | ||||||

| Item 15. | 84 | |||||

| 88 | ||||||

| 89 | ||||||

Table of Contents

| Item 1. | Business |

General

Belden Inc. (Belden) designs, manufactures, and markets cable, connectivity, and networking products in markets including industrial, enterprise, and broadcast. We focus on end markets that require highly differentiated, high-performance products. We add value through design, engineering, manufacturing excellence, product quality, and customer service.

Belden is a Delaware corporation incorporated in 1988. We report in three segments: the Americas segment, the Europe, Middle East, and Africa (EMEA) segment, and the Asia Pacific segment. Financial information about our operating segments appears in Note 5 to the Consolidated Financial Statements.

In 2012, we acquired Miranda Technologies Inc. (Miranda), a leading provider of hardware and software solutions for the broadcast infrastructure industry, and PPC Broadband, Inc. (PPC), a leading manufacturer and developer of advanced connectivity technologies for the broadband market. In 2012, we sold certain net assets of our Chinese cable business which conducted business primarily in the consumer electronics end market, and our Thermax and Raydex cable business.

In 2011, we acquired ICM Corp. (ICM), Poliron Cabos Electricos Especiais Ltda (Poliron) and Byres Security, Inc. (Byres Security).

In 2010, we acquired GarrettCom, Inc. (GarrettCom) and the Communications Products business of Thomas & Betts. We acquired Trapeze Networks, Inc. (Trapeze) in July 2008 and sold it in December 2010.

For more information regarding these transactions, see Notes 3, 4, and 9 to the Consolidated Financial Statements.

As used herein, unless an operating segment is identified or the context otherwise requires, “Belden,” the “Company”, and “we” refer to Belden Inc. and its subsidiaries as a whole.

Products and Markets

Belden’s highly differentiated, high-performance cable, connectivity and networking products can be found in a variety of end markets including power generation and distribution, data centers, oil and gas, broadcast, transportation, healthcare and industrial automation. Belden products are designed and manufactured to strict quality standards resulting in an industry leading reputation for worldwide reliability.

The main categories of cable products are (1) copper cables, including shielded and unshielded twisted pair cables, coaxial cables, and stranded cables, (2) fiber optic cables, which transmit light signals through glass or plastic fibers, and (3) composite cables, which are combinations of multiconductor, coaxial, and fiber optic cables jacketed together or otherwise joined together to serve complex applications and provide ease of installation. Connectivity products include both fiber and copper connectors for the enterprise, broadcast, broadband, and industrial markets. Networking products include Industrial Ethernet switches and related equipment and security features, fiber optic interfaces and media converters used to bridge fieldbus networks over long distances, networking infrastructure for the television broadcast, cable, satellite and IPTV industry, and load-moment indicators for mobile cranes and other load-bearing equipment.

For industrial end markets, we supply cable, connectivity, and networking products for applications ranging from advanced industrial networking and robotics to traditional instrumentation and control systems. Our cable products are used in discrete manufacturing and process operations involving the connection of computers,

1

Table of Contents

programmable controllers, robots, operator interfaces, motor drives, sensors, printers, and other devices. Many industrial environments, such as petrochemical and other harsh-environment operations, require cables with exterior armor or jacketing that can endure physical abuse and exposure to chemicals, extreme temperatures, and outside elements. Other applications require conductors, insulating, and jacketing materials that can withstand repeated flexing. In addition to cable product configurations for these applications, we supply heat-shrinkable tubing and wire management products to protect and organize wire and cable assemblies. We sell our industrial products primarily through value-added resellers, industrial distributors, and original equipment manufacturers (OEMs). We design, manufacture, and market Industrial Ethernet switches and related equipment, both rail-mounted and rack-mounted, for factory automation, power generation and distribution, process automation, and large-scale infrastructure projects such as bridges, wind farms, and airport runways. Rail-mounted switches are designed to withstand harsh conditions including electronic interference and mechanical stresses. We also design, manufacture, and market fiber optic interfaces and media converters used to bridge fieldbus networks over long distances. In addition, we design, manufacture, and market a broad range of industrial connectors for sensors and actuators, cord-sets, distribution boxes, and fieldbus communications. These products are used both as components of manufacturing equipment and in the installation and networking of such equipment. We also design, manufacture, and market load-moment indicators. Our switches, communications equipment, connectors, and load-moment indicators are sold directly to industrial equipment OEMs and through a network of distributors and system integrators.

For enterprise end markets, we supply structured cabling solutions, connectors, and networking products for the electronic and optical transmission of data, sound, and video over local- and wide- area networks. Products for this market include high-performance copper cables including 10-gigabit Ethernet technologies, fiber optic cables, connectors, wiring racks, panels, interconnecting hardware, intelligent patching devices, and cable management solutions for complete end-to-end network structured wiring systems. End-use customers include hospitals, financial institutions, governments, service providers, and data centers. Our systems are installed through a network of highly trained system integrators and are supplied through authorized distributors.

For broadcast end markets, we are a provider of hardware and software solutions for the television broadcast, cable, satellite and IPTV industry. Our solutions also span the full breadth of television operations, including production, playout and delivery. We also manufacture a variety of multiconductor and coaxial cable and connector products, which distribute audio and video signals for use in broadcast television including digital television and high definition television, broadcast radio, pre- and post-production facilities, recording studios, and public facilities such as casinos, arenas, and stadiums. Our audio/video cables are also used in connection with microphones, musical instruments, audio mixing consoles, effects equipment, speakers, paging systems, and consumer audio products. We also manufacture networking infrastructure products for the television broadcast, cable, satellite and IPTV industry. Our primary market channels for these broadcast, music, and entertainment products are broadcast specialty distributors and audio systems installers. We also sell directly to music OEMs and the major television networks including ABC, CBS, Fox, and NBC. We also provide specialized cables for security applications such as video surveillance systems, airport baggage screening, building access control, motion detection, public address systems, and advanced fire alarm systems. These products are sold primarily through distributors and also directly to specialty system integrators. We manufacture flexible, copper-clad coaxial cable and associated connector products for the high-speed transmission of data, sound, and video (broadband) that are used for the “drop” section of cable television (CATV) systems and satellite direct broadcast systems. These cables are sold primarily through distributors. For the broadband end market, Belden manufactures and develops connectivity solutions in several major product categories: coax connector products that allow for connections from the provider network to the subscribers’ devices, hardline connectors that allow service providers to distribute their services within a city, a town or a neighborhood and entry devices that serve to manage and remove network signal noise that could impair performance for the subscriber, and traps and filtering devices that allow service providers to control the signals that are transmitted to the subscriber.

2

Table of Contents

Segments

The Americas segment contributed approximately 64%, 60%, and 57% of our consolidated revenues in 2012, 2011, and 2010, respectively. This segment sells the full array of our products for the industrial, enterprise, and broadcast markets.

The EMEA segment contributed approximately 19%, 21%, and 23% of our consolidated revenues in 2012, 2011, and 2010, respectively. This segment sells the full array of our products for the industrial, enterprise, and broadcast markets.

The Asia Pacific segment contributed approximately 17%, 19%, and 20% of our consolidated revenues in 2012, 2011, and 2010, respectively. This segment sells the full array of our products for the industrial, enterprise, and broadcast markets.

Customers

We sell to distributors, OEMs, installers, and end-users. Sales to the distributor Anixter International Inc. represented approximately 16% of our consolidated revenues in 2012. No other customer accounted for more than 10% of our revenues in 2012.

We have supply agreements with distributors and OEM customers in the Americas, Europe, the Middle East, and Asia. In general, our customers are not contractually obligated to buy our products exclusively, in minimum amounts, or for a significant period of time. The loss of one or more large customers or distributors could result in lower total revenues and profits. However, we believe that our relationships with our customers and distributors are good and that they choose Belden products, among other reasons, due to our reputation, the breadth of our product offering, the quality and performance characteristics of our products, and our service and technical support.

There are potential risks in our relationships with distributors. Changes in the inventory levels of our products held by our distributors can result in significant variability in our revenues. Adjustments to inventory levels may be accelerated through consolidation among distributors. In addition, if the costs of materials used in our products fall and competitive conditions make it necessary for us to reduce our list prices, we may be required, according to the terms of contracts with certain of our distributors, to reimburse them for a portion of the price they paid for our products in their inventory. Further, certain distributors are allowed to return certain inventory in exchange for an order of equal or greater value. We have recorded reserves for the estimated impact of these inventory policies.

International Operations

In addition to manufacturing facilities in the United States, we have manufacturing facilities in Canada, China, Mexico, and Brazil, as well as in various countries in Europe. During 2012, approximately 55% of Belden’s sales were to customers outside the United States. Our primary channels to international markets include both distributors and direct sales to end users and OEMs.

The effect of changes in the relative value of currencies impacts our results of operations. However, our revenues and costs are typically in the same currency, reducing our overall currency risk.

A risk associated with our European manufacturing operations is the higher relative expense and length of time required to reduce manufacturing employment. In addition, some of our foreign operations are subject to economic and political risks inherent in maintaining operations abroad, such as economic and political destabilization, international conflicts, restrictive actions by foreign governments, and unfavorable foreign tax laws.

Financial information for Belden by geographic area is shown in Note 5 to the Consolidated Financial Statements.

3

Table of Contents

Competition

We face substantial competition in our major markets. The number and size of our competitors vary depending on the product line and operating segment. Some multinational competitors have greater financial, engineering, manufacturing, and marketing resources than we have. There are also many regional competitors that have more limited product offerings.

For each of our operating segments, the market can be generally categorized as highly competitive with many players. The market can be influenced by economic downturns as some competitors that are highly leveraged both financially and operationally could become more aggressive in their pricing of products.

The principal competitive factors in all our product markets are product features, availability, price, customer support, and distribution coverage. The relative importance of each of these factors varies depending on the customer. Some products are manufactured to meet published industry specifications and are less differentiated on the basis of product characteristics. We believe that Belden stands out in many of its markets on the basis of our reputation, the breadth of our product offering, the quality and performance characteristics of our products, and our service and technical support.

Although we believe that we have certain technological and other advantages over our competitors, realizing and maintaining such advantages requires continued investment in engineering, research and development, capital equipment, marketing, and customer service and support. There can be no assurance that we will be successful in maintaining such advantages.

Research and Development

We conduct research and development on an ongoing basis, including new and existing product development, testing and analysis, and process and equipment development and testing. See the Consolidated Statements of Operations for amounts incurred for research and development.

Patents and Trademarks

We have a policy of seeking patents when appropriate on inventions concerning new products, product improvements, and advances in equipment and processes as part of our ongoing research, development, and manufacturing activities. We own many patents and registered trademarks worldwide that are used by our operating segments, with pending applications for numerous others. Although in the aggregate our patents are of considerable importance to the manufacturing and marketing of many of our products, we do not consider any single patent to be material to the business as a whole. Our most prominent trademarks or group of related patents are: Belden®, Alpha™, Mohawk®, West Penn Wire/CDT®, Hirschmann®, Lumberg Automation™, Telecast™, Snap-N-Seal®, GarrettCom®, Poliron™, Byres Security™, Tofino®, Miranda Technologies®, and PPC Broadband®.

Raw Materials

The principal raw material used in many of our products is copper. Other materials we purchase in large quantities include fluorinated ethylene-propylene (both Teflon® and other FEP), polyvinyl chloride (PVC), polyethylene, aluminum-clad steel and copper-clad steel conductors, other metals, optical fiber, printed circuit boards, and electronic components. With respect to all major raw materials used by us, we generally have either alternative sources of supply or access to alternative materials. Supplies of these materials are generally adequate and are expected to remain so for the foreseeable future.

Over the past three years, the prices of metals, particularly copper, have been highly volatile. During 2010, copper prices continued to increase with the price at the end of 2010 approximately 33% greater than at the

4

Table of Contents

beginning of the year. During 2011, copper prices decreased with the price at the end of 2011 approximately 23% less than at the beginning of the year. During 2012, copper prices increased with the price at the end of 2012 approximately 6% higher than that at the beginning of the year. Prices for materials such as PVC and other plastics derived from petrochemical feedstocks have also fluctuated. Since Belden utilizes the first in, first out (FIFO) inventory costing methodology, the impact of copper and other raw material cost changes on our cost of goods sold is delayed by approximately two months based on our inventory turns.

While we seek to be neutral in our pricing for fluctuations in commodity prices, we can experience short-term favorable or unfavorable variances. When the cost of raw materials increases, we are generally able to recover these costs through higher pricing of our finished products. The majority of our products are sold through distribution, and we manage the pricing of these products through published price lists, which we update from time to time, with new prices typically taking effect a few weeks after they are announced. Some OEM customer contracts have provisions for passing through raw material cost changes, generally with a lag of a few weeks to three months.

Backlog

Our business is characterized generally by short-term order and shipment schedules. Our backlog consists of product orders for which we have received a customer purchase order or purchase commitment and which have not yet been shipped. Orders are subject to cancellation or rescheduling by the customer, generally with a cancellation charge. At December 31, 2012, our backlog of orders believed to be firm was $201.9 million compared with $128.8 million at December 31, 2011. The majority of the backlog at December 31, 2012 is scheduled to be shipped in 2013.

Environmental Matters

We are subject to numerous federal, state, provincial, local and foreign laws and regulations relating to the storage, handling, emission, and discharge of materials into the environment, including the Comprehensive Environmental Response, Compensation, and Liability Act, the Clean Water Act, the Clean Air Act, the Emergency Planning and Community Right-To-Know Act, and the Resource Conservation and Recovery Act. We believe that our existing environmental control procedures and accrued liabilities are adequate, and we have no current plans for substantial capital expenditures in this area.

We do not currently anticipate any material adverse effect on our results of operations, financial condition, cash flow, or competitive position as a result of compliance with federal, state, provincial, local or foreign environmental laws or regulations, including clean-up costs. However, some risk of environmental liability and other costs is inherent in the nature of our business, and there can be no assurance that material environmental costs will not arise. Moreover, it is possible that future developments, such as increasingly strict requirements of environmental laws and enforcement policies thereunder, could lead to material costs of environmental compliance and clean-up.

Employees

As of December 31, 2012, we had approximately 6,700 employees worldwide. We also utilized about 300 workers under contract manufacturing arrangements. Approximately 1,600 employees are covered by collective bargaining agreements at various locations around the world. We believe our relationship with our employees is generally good.

Importance of New Products and Product Improvements;

Impact of Technological Change; Impact of Acquisitions

Many of the markets we serve are characterized by advances in information processing and communications capabilities, including advances driven by the expansion of digital technology, which require increased

5

Table of Contents

transmission speeds and greater bandwidth. Our markets are also subject to increasing requirements for mobility and information security. The relative costs and merits of copper and fiber optic cable solutions could change in the future as various competing technologies address the market opportunities. We believe that our future success will depend in part upon our ability to enhance existing products and to develop and manufacture new products that meet or anticipate such changes.

Fiber optic technology presents a potential substitute for certain of the copper-based products that comprise the majority of our sales. Fiber optic cables have certain advantages over copper-based cables in applications where large amounts of information must travel significant distances and where high levels of information security are required. While the cost to interface electronic and optical light signals and to terminate and connect optical fiber remains high, we expect that in future years the cost difference will diminish. We produce and market fiber optic cables and many customers specify these products in combination with copper cables.

The final stage of most networks remains almost exclusively copper-based and we expect that it will continue to be copper for some time. However, if a significant decrease in the cost of fiber optic systems relative to the cost of copper-based systems were to occur, such systems could become superior on a price/performance basis to copper systems. We do not control our own source of optical fiber production and, although we include optical fiber components in the manufacture of our cable products, we could be at a cost disadvantage to competitors who both produce optical fiber and cable optical fiber components.

In the industrial automation market, there is a growing trend toward adoption of Industrial Ethernet technology, bringing to the factory floor the advantages of digital communication and the ability to network devices made by different manufacturers and then link them to enterprise systems. Adoption of this technology is at a more advanced stage among European manufacturers than those in the United States and Asia, but we believe that the trend will globalize.

Our strategy includes continued acquisitions to support our signal transmission solutions strategy. There can be no assurance that future acquisitions will occur or that those that do occur will be successful.

Available Information

We file annual, quarterly, and current reports, proxy statements and other information with the Securities and Exchange Commission (SEC). These reports, proxy statements, and other information contain additional information about us. You may read and copy these materials at the SEC’s Public Reference Room at 100 F Street, N.E., Washington, D.C. 20549. Please call the SEC at 1-800-SEC-0330 for more information about the operation of the Public Reference Room. The SEC also maintains a web site that contains reports, proxy and information statements, and other information about issuers who file electronically with the SEC. The Internet address of the site iswww.sec.gov.

Belden maintains an Internet web site atwww.belden.com where our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, proxy statements, and all amendments to those reports and statements are available without charge, as soon as reasonably practicable following the time they are filed with or furnished to the SEC.

We will provide upon written request and without charge a printed copy of our Annual Report on Form 10-K. To obtain such a copy, please write to the Corporate Secretary, Belden Inc., 7733 Forsyth Boulevard, Suite 800, St. Louis, MO 63105.

6

Table of Contents

Executive Officers

The following table sets forth certain information with respect to the persons who were Belden executive officers as of February 25, 2013. All executive officers are elected to terms that expire at the organizational meeting of the Board of Directors following the Annual Meeting of Shareholders.

Name | Age | Position | ||

| John S. Stroup | 46 | President, Chief Executive Officer, and Director | ||

| Steven Biegacki | 54 | Senior Vice President, Global Sales and Marketing | ||

| Kevin L. Bloomfield | 61 | Senior Vice President, Secretary and General Counsel | ||

| Henk Derksen | 44 | Senior Vice President, Finance, and Chief Financial Officer | ||

| Christoph Gusenleitner | 48 | Executive Vice President, EMEA Operations and Global Connectivity Products | ||

| John S. Norman | 52 | Vice President, Controller and Chief Accounting Officer | ||

| Denis Suggs | 47 | Executive Vice President, Americas Operations and Global Cable Products | ||

| Nancy Wolfe | 43 | Senior Vice President, Human Resources |

John S. Stroup was appointed President, Chief Executive Officer and member of the Board in October 2005. From 2000 to the date of his appointment with the Company, he was employed by Danaher Corporation, a manufacturer of professional instrumentation, industrial technologies, and tools and components. At Danaher, he initially served as Vice President, Business Development. He was promoted to President of a division of Danaher’s Motion Group and later to Group Executive of the Motion Group. Earlier, he was Vice President of Marketing and General Manager with Scientific Technologies Inc. He has a B.S. in Mechanical Engineering from Northwestern University and an M.B.A. from the University of California at Berkeley Haas School of Business.

Steven Biegacki was appointed Vice President, Global Sales and Marketing (title subsequently changed as reflected in the above table) in March 2008. Mr. Biegacki was previously Vice President, Marketing for Rockwell Automation. At Rockwell, he initially served as DeviceNet Program Manager, was promoted to Business Manager, Automation Networks in 1997, Vice President, Integrated Architecture Commercial Marketing in 1999, and Vice President, Components and Power Control Commercial Marketing in 2005. Previously, he was an Automation Systems Architecture Marketing Manager for Allen-Bradley Company. He has a B.S. in Electrical Engineering Technology from ETI Technical College in Cleveland, Ohio.

Kevin L. Bloomfield has been Vice President, Secretary and General Counsel of the Company (title subsequently changed as reflected in the above table) since July 2004. From August 1993 until July 2004, Mr. Bloomfield was Vice President, Secretary and General Counsel of Belden 1993 Inc. He was Senior Counsel for Cooper Industries from February 1987 to July 1993, and had been in Cooper’s Law Department from 1981 to 1993. He has a B.A. in Economics and a J.D. from the University of Cincinnati and an M.B.A. from The Ohio State University.

Henk Derksen has been Senior Vice President, Finance, and Chief Financial Officer since January 2012. Prior to that, he served as Vice President, Corporate Finance from July 2011 to December 2011 and Treasurer and Vice President, Financial Planning and Analysis of the Company from January 2010 to July 2011. In August of 2003, he became Vice President, Finance for the Company’s EMEA division, after joining the Company at the end of 2000. He was Vice President and Controller of Plukon Poultry, a food processing company from 1998 to 2000, and has 5 years’ experience in public accounting with Price Waterhouse and Baker Tilly. Mr. Derksen has a M.A. in Accounting from the University of Arnhem in the Netherlands and holds a doctoral degree in Business Economics in addition to an Executive Master of Finance & Control from Tias Business School in the Netherlands.

Christoph Gusenleitner joined Belden in April 2010 as Executive Vice President, EMEA Operations and Global Connectivity Products. Prior to coming to Belden, Mr. Gusenleitner was a partner at Bain & Company

7

Table of Contents

in its industrial goods and services practice in Munich. Prior to that, he was General Manager of KaVo Dental GmbH and Kaltenbach & Voigt GmbH in Biberach, Germany. KaVo is an affiliate of Danaher Corporation. During his four-year tenure at KaVo, Mr. Gusenleitner led the strategic planning process for the global Danaher Dental Equipment platform and led three business units and 18 sales subsidiaries in EMEA. He has a degree in electrical engineering from the University of Technology in Vienna, Austria and a Master of Science in Industrial Automation from Carnegie Mellon University.

John S. Norman joined Belden in May 2005 as Controller, was named Chief Accounting Officer in November 2005, and was named Vice President of Belden in February 2009. In January 2010, he became Vice President, Finance for the Company’s EMEA division. In July 2011, he became Vice President, Controller, and Chief Accounting Officer. He was vice president and controller of Graphic Packaging International Corporation, a paperboard packaging manufacturing company, from 1999 to 2003, and has 17 years’ experience in public accounting with PricewaterhouseCoopers, LLP. Mr. Norman has a B.S. in Accounting from the University of Missouri and is a Certified Public Accountant.

Denis Suggs joined Belden in June 2007 as Vice President, Americas Operations (title subsequently changed as reflected in the above table). Prior to joining Belden, Mr. Suggs held various senior management level and executive positions at IBM and Danaher Corporation; most recently as the President, Portescap and serving as the Chairman of the Board—Portescap International, Portescap Switzerland, Danaher Motion India Private Ltd., and Airpax Company. Mr. Suggs earned a Bachelors in Electrical Engineering at North Carolina State University and an M.B.A. from the Fuqua School of Business at Duke University.

Nancy Wolfe joined Belden in February 2012 as Senior Vice President, Human Resources. Prior to joining Belden, Ms. Wolfe held various human resources, benefits and finance roles at Monsanto Company, where she was employed from 1997 to February 2012. Most recently, she was the Human Resources Lead for Monsanto’s Global Vegetable Seeds Division. Ms. Wolfe holds dual B.S. degrees in Finance and Business Administration and has an M.B.A. from Washington University in St. Louis.

| Item 1A. | Risk Factors |

We make forward-looking statements in this Annual Report on Form 10-K, in other materials we file with the SEC or otherwise release to the public, and on our website. In addition, our senior management might make forward-looking statements orally to analysts, investors, the media, and others. Statements concerning our future operations, prospects, strategies, financial condition, future economic performance (including growth and earnings) and demand for our products and services, and other statements of our plans, beliefs, or expectations, including the statements contained in Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” that are not historical facts, are forward-looking statements. In some cases these statements are identifiable through the use of words such as “anticipate,” “believe,” “estimate,” “expect,” “intend,” “plan,” “project,” “target,” “can,” “could,” “may,” “should,” “will,” “would,” and similar expressions. The forward-looking statements we make are not guarantees of future performance and are subject to various assumptions, risks, and other factors that could cause actual results to differ materially from those suggested by these forward-looking statements. These factors include, among others, those set forth below and in the other documents that we file with the SEC.

We expressly disclaim any obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law. Following is a discussion of some of the more significant risks that could materially impact our business. There may be additional risks that impact our business that we currently do not recognize as, or that are not currently, material to our business.

A challenging global economic environment or a downturn in the markets we serve could adversely affect our operating results and stock price in a material manner.

A challenging global economic environment could cause substantial reductions in our revenue and results of operations as a result of weaker demand by the end users of our products and price erosion. Price erosion may

8

Table of Contents

occur through competitors or us becoming more aggressive in pricing practices, which could adversely impact our gross margins. A challenging global economy could also make it difficult for our customers, our vendors, and us to accurately forecast and plan future business activities. Our customers could also face issues gaining timely access to sufficient credit, which could have an adverse effect on our results if such events cause reductions in revenues, delays in collection or write-offs of receivables. Further, the demand for many of our products is economically sensitive and will vary with general economic activity, trends in nonresidential construction, investment in manufacturing facilities and automation, demand for information technology equipment, and other economic factors.

We face risks regarding our European operations. Economic uncertainty, such as the uncertainty arising from various European sovereign debt crises or general economic conditions, could result in a significant decline in the value of the Euro relative to the U.S. dollar, which could result in a significant adverse effect on our revenues and results of operations; could make it extremely difficult for our customers and us to accurately forecast and plan future business activities; and could cause our customers to slow spending on our products and services, which could delay and lengthen sales cycles. Similar economic risks arise from uncertainty regarding public debt or budget negotiations, particularly in the United States and Europe.

Our strategic plan includes further acquisitions.

Our strategic plan includes further acquisitions, and the extent to which appropriate acquisitions are made will affect our overall growth, operating results, financial condition, and cash flows. Our business strategy involves continued acquisitions to support our growth and product portfolio plans. Our ability to acquire businesses successfully will decline if we are unable to identify appropriate acquisition targets consistent with our strategic plan, the competition among potential buyers increases, or the cost of acquiring suitable businesses becomes too expensive. As a result, we may be unable to make acquisitions or be forced to pay more or agree to less advantageous acquisition terms for the companies that we are able to acquire. Our ability to implement our business strategy and grow our business, particularly through acquisitions, may depend on our ability to raise capital by selling equity or debt securities or obtaining additional debt financing. Market conditions may prevent us from obtaining financing when we need it or on terms acceptable to us.

We may have difficulty integrating the operations of acquired businesses, which could negatively affect our results of operations and profitability.

We may have difficulty integrating acquired businesses and future acquisitions might not meet our performance expectations. Some of the integration challenges we might face include differences in corporate culture and management styles, additional or conflicting governmental regulations, preparation of the acquired operations for compliance with the Sarbanes-Oxley Act of 2002, financial reporting that is not in compliance with U.S. generally accepted accounting principles, disparate company policies and practices, customer relationship issues, and retention of key personnel. In addition, management may be required to devote a considerable amount of time to the integration process, which could decrease the amount of time we have to manage the other businesses. We may not be able to integrate operations successfully or cost-effectively, which could have a negative effect on our results of operations or our profitability. The process of integrating operations could also cause some interruption of, or the loss of momentum in, the activities of acquired businesses.

Because we do business in many countries, our results of operations are subject to political, economic, and other uncertainties and are affected by changes in currency exchange rates.

In addition to manufacturing facilities in the United States, we have manufacturing facilities in Canada, China, Mexico, Brazil, and several European countries. We rely on suppliers in many countries, including China. Our foreign operations are subject to economic and political risks inherent in maintaining operations abroad such as economic and political destabilization, land use risks, international conflicts, restrictive actions by foreign governments, and adverse foreign tax laws. A risk associated with our European manufacturing operations is

9

Table of Contents

the higher relative expense and length of time required to adjust manufacturing employment capacity. We also face political risks in the United States, including tax or regulatory risks or potential adverse impacts from legislative impasses over, or significant changes in, fiscal or monetary policy.

More than half of our sales are outside the United States. Other than the U.S. dollar, the principal currencies to which we are exposed through our manufacturing operations, sales, and related cash holdings are the euro, the Canadian dollar, the Hong Kong dollar, the Chinese yuan, the Mexican peso, the Australian dollar, the British pound, and the Brazilian real. In most cases, we have revenues and costs in the same currency, thereby reducing our overall currency risk, although the realignment of our manufacturing capacity among our global facilities may alter this balance. When the U.S. dollar strengthens against other currencies, the results of our non-U.S. operations are translated at a lower exchange rate and thus into lower reported earnings.

If we are unable to retain senior management and key employees, our business operations could be adversely affected.

Our success has been largely dependent on the skills, experience, and efforts of our senior management and key employees. The loss of any of our senior management or other key employees, including due to acquisitions or restructuring activities, could have an adverse effect on us. We may not be able to find qualified replacements for these individuals and the integration of potential replacements may be disruptive to our business. More broadly, a key determinant of our success is our ability to attract, develop and retain talented associates. While this is one of our strategic priorities, we may not be able to succeed in this regard.

We may be unable to achieve our strategic priorities in emerging markets.

Emerging markets are a significant focus of our strategic plan. The developing nature of these markets presents a number of risks. We may be unable to attract, develop, and retain appropriate talent to manage our businesses in emerging markets. Deterioration of social, political, labor, or economic conditions in a specific country or region may adversely affect our operations or financial results. Among the risks in emerging market countries are bureaucratic intrusions and delays, contract compliance failures, business practices that do not comply with local or U.S. law such as the Foreign Corrupt Practices Act, fluctuating currencies and interest rates, limitations on the amount and nature of investments, restrictions on permissible forms and structures of investment, unreliable legal and financial infrastructure, regime disruption and political unrest, uncontrolled inflation and commodity prices, fierce local competition by companies with better political connections, and corruption. In addition, the costs of compliance with local laws and regulations in emerging markets may negatively impact our competitive position as compared to locally owned manufacturers.

Our future success depends in part on our ability to develop and introduce new products.

Our markets are characterized by the introduction of products with increasing technological capabilities, including fiber optic and wireless signal transmission solutions that compete with the copper cable solutions that comprise the majority of our revenue. The relative costs and merits of copper cable solutions, fiber optic cable solutions, and wireless solutions could change in the future as various competing technologies address the market opportunities. We believe that our future success will depend in part upon our ability to enhance existing products and to develop and manufacture new products that meet or anticipate such changes, which will require continued investment in engineering, research and development, capital equipment, marketing, and customer service and support. We have long been successful in introducing successive generations of more capable products, but if we were to fail to keep pace with technology or with the products of competitors, we might lose market share and harm our reputation and position as a technology leader in our markets. Competing technologies could cause the obsolescence of many of our products. See the discussion above in Part I, Item 1, underImportance of New Products and Product Improvements; Impact of Technological Change; Impact of Acquisitions.

Legal compliance issues could adversely affect our business.

10

Table of Contents

We have a strong legal compliance and ethics program, including a code of business conduct and ethics, policies on anti-bribery, export controls and other legal compliance areas, and periodic training to relevant associates on these matters. While we believe that this program should reduce the likelihood of a legal compliance violation, such a violation could still occur, disrupting our business through fines, penalties, diversion of internal resources, and negative publicity.

We may experience significant variability in our quarterly and annual effective tax rate which would affect our reported net income.

We have a complex tax profile due to the global nature of our operations, which encompass multiple taxing jurisdictions. Variability in the mix and profitability of domestic and international activities, identification and resolution of various tax uncertainties, changes in tax laws and rates, and the extent to which we are able to realize net operating loss and other carryforwards included in deferred tax assets and avoid potential adverse outcomes included in deferred tax liabilities, among other matters, may significantly affect our effective income tax rate in the future.

Our effective income tax rate is the result of the income tax rates in the various countries in which we do business. Our mix of income and losses in these jurisdictions affects our effective tax rate. For example, relatively more income in higher tax rate jurisdictions or relatively more losses in lower tax rate jurisdictions would increase our effective tax rate and thus lower our net income. Similarly, if we generate losses in tax jurisdictions for which no benefits are available, our effective income tax rate will increase. Our effective income tax rate may also be impacted by the recognition of discrete income tax items, such as required adjustments to our liabilities for uncertain tax positions or our deferred tax asset valuation allowance. A significant increase in our effective income tax rate could have a material adverse impact on our earnings.

Changes in the price and availability of raw materials we use could be detrimental to our profitability.

Copper is a significant component of the cost of most of our products. Over the past few years, the prices of metals, particularly copper, have been highly volatile. Copper rose rapidly in price for much of this period and remains a volatile commodity. Prices of other materials we use, such as polyvinylchloride (PVC) and other plastics derived from petrochemical feedstocks, have also been volatile. Generally, we have recovered much of the higher cost of raw materials through higher pricing of our finished products. The majority of our products are sold through distribution, and we manage the pricing of these products through published price lists which we update from time to time, with new prices typically taking effect a few weeks after they are announced. Some OEM contracts have provisions for passing through raw material cost changes, generally with a lag of a few weeks to three months. If we are unable to raise prices sufficiently to recover our material costs, our earnings will be reduced. If we raise our prices but competitors raise their prices less, we may lose sales, and our earnings will be reduced. If the price of copper were to decline, we may be compelled to reduce prices to remain competitive, which could have a negative effect on revenue, and we may be required, according to the terms of contracts with certain of our distributors, to reimburse them for a portion of the price they paid for our products in their inventory. While we generally believe the supply of raw materials (copper, plastics, and other materials) is adequate, we have experienced instances of limited supply of certain raw materials, resulting in extended lead times and higher prices. If a supply interruption or shortage of materials were to occur, this could have a negative effect on revenue and earnings.

The global cable, connectivity, and networking industries are highly competitive.

We face competition from other manufacturers for each of our product platforms and in each of our geographic regions. These companies compete on price, reputation and quality, product technology and characteristics, and terms. Some multinational competitors have greater engineering, financial, manufacturing, and marketing resources than we have. Actions that may be taken by competitors, including pricing, business alliances, new product introductions, market penetration, and other actions, could have a negative effect on our revenue and profitability. Moreover, during economic downturns, some competitors that are highly leveraged both financially and operationally could become more aggressive in their pricing of products.

11

Table of Contents

We may be unable to implement our strategic plan successfully.

Our strategic plan is designed to improve revenues and profitability, reduce costs, and improve working capital management. To achieve these goals, our strategic priorities are to continue deployment of our Market Delivery System (MDS) so as to capture market share through end-user engagement, channel management, outbound marketing, and careful vertical market selection; improve our recruitment and development of talented associates; develop strong global connector and industrial networking product platforms; acquire businesses that fit our strategic plan; and become a leading Lean company. Lean refers to a business management system that strives to create value for customers and deliver that value to the right place, at the right time, and in the right quantities while reducing or eliminating waste from all processes. We have a disciplined process for deploying this strategic plan through our associates. There is a risk that we may not be successful in executing these measures to achieve the expected results for a variety of reasons, including market developments, economic conditions, shortcomings in establishing appropriate action plans, or challenges with executing multiple initiatives simultaneously. For example, our MDS initiative may not succeed or we may lose market share due to challenges in choosing the right products to market or the right customers for these products, integrating products of acquired companies into our sales and marketing strategy, or strategically bidding against OEM partners. We may not be able to acquire businesses that fit our strategic plan on acceptable business terms, and we may not achieve our other strategic priorities.

We rely on several key distributors in marketing our products.

The majority of our sales are through distributors. These distributors carry the products of competitors along with our products. Our largest distributor, Anixter International Inc., accounted for 16% of our revenue in 2012. If we were to lose a key distributor, our revenue and profits would likely be reduced, at least temporarily.

In the past, we have seen some distributors acquired and consolidated. If there were further consolidation of our distributors, this could affect our relationships with these distributors. It could also result in consolidation of distributor inventory, which would temporarily depress our revenue. In addition, changes in the inventory levels of our products held by our distributors can result in significant variability in our revenues. We have also experienced financial failure of distributors from time to time, resulting in our inability to collect accounts receivable in full. A global economic downturn could cause financial difficulties (including bankruptcy) for our distributors and customers, which would adversely affect our results of operations.

Volatility of credit markets could adversely affect our business.

Uncertainty in U.S. and global financial and equity markets could make it more expensive for us to conduct our operations and may cause us to be unable to pursue or complete acquisitions.

Potential problems with our information systems could interfere with our business and operations.

We rely on our information systems and those of third parties for processing customer orders, shipping of products, billing our customers, tracking inventory, supporting accounting functions and financial statement preparation, paying our employees, and otherwise running our business. Any disruption, whether from hackers or other sources, in our information systems or those of the third parties upon whom we rely could have a significant impact on our business. In addition, we may need to enhance our information systems to provide additional capabilities and functionality. The implementation of new information systems and enhancements is frequently disruptive to the underlying business of an enterprise. Any disruptions affecting our ability to accurately report our financial performance on a timely basis could adversely affect our business in a number of respects. If we are unable to successfully implement potential future information systems enhancements, our financial position, results of operations, and cash flows could be negatively impacted.

12

Table of Contents

We, and others on our behalf, store “personally identifiable information” with respect to employees, vendors, customers and others. While we have implemented safeguards to protect the privacy of this information, it is possible that hackers or others might obtain this information. If that occurs, in addition to having to take potentially costly remedial action, we also may be subject to fines, penalties and reputational damage.

If our goodwill or other intangible assets become impaired, we would be required to recognize charges that would reduce our income.

Under accounting principles generally accepted in the United States, goodwill and certain other intangible assets are not amortized but must be reviewed for possible impairment annually or more often in certain circumstances if events indicate that the asset values may not be recoverable. We have incurred significant charges for the impairment of goodwill and other intangible assets in the past, and we may be required to do so again in future periods if the underlying value of our business declines. Such a charge would reduce our income without any change to our underlying cash flow.

We might have difficulty protecting our intellectual property from use by competitors, or competitors might accuse us of violating their intellectual property rights.

Disagreements about patents and other intellectual property rights occur in the markets we serve. Third parties have asserted and may in the future assert claims of infringement of intellectual property rights against us or against our customers or channel partners for which we may be liable. Furthermore, a successful claimant could secure a judgment that requires us to pay substantial damages or prevents us from distributing certain products or performing certain services. We may encounter difficulty enforcing our own intellectual property rights against third parties, which could result in price erosion or loss of market share.

Some of our employees are members of collective bargaining groups, and we might be subject to labor actions that would interrupt our business.

Some of our employees, primarily outside the United States, are members of collective bargaining groups. We believe that our relations with employees are generally good. However, if there were a dispute with one of these bargaining units, the affected operations could be interrupted resulting in lost revenues, lost profit contribution, and customer dissatisfaction.

We are subject to current environmental and other laws and regulations, including the risks associated with possible climate change legislation.

We are subject to the environmental laws and regulations in each jurisdiction where we do business. We are currently and may in the future be held responsible for remedial investigations and clean-up costs of certain sites damaged by the discharge of hazardous substances, including sites that have never been owned or operated by us but with respect to which we have been identified as a potentially responsible party under federal and state environmental laws. Changes in environmental and other laws and regulations in both domestic and foreign jurisdictions and changes in enforcement policies thereunder could adversely affect our operations due to increased costs of compliance and potential liability for noncompliance.

Greenhouse gas emissions and their possible impact on climate change are becoming the subject of increased public scrutiny. Executive action related to climate change may be pursued by the President of the United States of America, and legislation related to greenhouse gas emissions is repeatedly introduced by Congress. In addition, future regulation of greenhouse gas could occur pursuant to future U.S. treaty obligations or statutory or regulatory changes under existing environmental laws. Additional climate change regulation may adversely affect our costs by increasing energy costs and raw material prices and requiring equipment modification or replacement.

13

Table of Contents

This list of risk factors is not exhaustive. Other considerations besides those mentioned above might cause our actual results to differ from expectations expressed in any forward-looking statement.

| Item 1B. | Unresolved Staff Comments |

None.

| Item 2. | Properties |

Belden has a corporate office that it leases in St. Louis, Missouri, and various manufacturing facilities, warehouses, and sales and administration offices throughout the world. The significant facilities as of December 31, 2012, were as follows.

Used by the Americas operating segment:

Number of Properties by Country | Primary Character (M=Manufacturing, W=Warehouse) | Owned or | ||

| United States-22 | 15 M, 7 W | 11 owned 11 leased | ||

| Brazil-1 | 1 M | 1 leased | ||

| Canada-3 | 2 M, 1 W | 2 owned 1 leased | ||

| Mexico-3 | 3 M | 3 leased | ||

| St. Kitts-1 | 1 M | 1 owned | ||

| England-2 | 2 W | 2 leased | ||

| Denmark-1 | 1 M | 1 owned | ||

| China-2 | 2 M | 2 leased |

Used by the EMEA operating segment:

Number of Properties by Country | Primary Character (M=Manufacturing, W=Warehouse) | Owned or | ||

| The Netherlands-3 | 1 M, 2 W | 3 leased | ||

| Germany-3 | 2 M, 1 W | 1 owned 2 leased | ||

| Italy-1 | 1 M | 1 owned | ||

| Denmark-2 | 1 M, 1 W | 1 owned 1 leased | ||

| Hungary-2 | 1 M, 1W | 2 owned | ||

| Czech Republic-2 | 1 M, 1W | 2 owned |

Used by the Asia Pacific operating segment:

Number of Properties by Country | Primary Character (M=Manufacturing, W=Warehouse) | Owned or | ||

| China-3 | 1 M, 2 W | 1 owned 2 leased | ||

| India-1 | 1 W | 1 leased | ||

| Australia-1 | 1 W | 1 leased | ||

| Singapore-1 | 1 W | 1 leased | ||

| Hong Kong-1 | 1 W | 1 leased |

14

Table of Contents

The total size of all Americas, EMEA, and Asia Pacific operating segment locations is 4.2 million square feet, 1.1 million square feet, and 1.3 million square feet, respectively. We believe our physical facilities are suitable for their present and intended purposes and adequate for our current level of operations.

| Item 3. | Legal Proceedings |

We are a party to various legal proceedings and administrative actions that are incidental to our operations. These proceedings include personal injury cases, 103 of which were pending as of February 1, 2013, in which we are one of many defendants. Electricians have filed a majority of these cases, primarily in Pennsylvania and Illinois, generally seeking compensatory, special, and punitive damages. Typically in these cases, the claimant alleges injury from alleged exposure to a heat-resistant asbestos fiber. Our alleged predecessors had a small number of products that contained the fiber, but ceased production of such products more than 20 years ago. Through February 1, 2013, we have been dismissed, or reached agreement to be dismissed, in more than 500 similar cases without any going to trial, and with only a relatively small number of these involving any payment to the claimant. In our opinion, the proceedings and actions in which we are involved should not, individually or in the aggregate, have a material adverse effect on our financial condition, operating results, or cash flows. However, since the trends and outcome of this litigation are inherently uncertain, we cannot give absolute assurance regarding the future resolution of such litigation, or that such litigation may not become material in the future.

We are a former owner of a property located in Kingston, Canada. The Ontario, Canada Ministry of the Environment is seeking to require current and former owners of the Kingston property to delineate and remediate soil and groundwater contamination at the site, which we believe was caused by Nortel (a former owner of the site). We are in the process of assessing whether we have any liability for the site, as well as the scope of contamination, cost of remediation, allocation of costs among the parties, and the other parties’ financial viability. Based on our current information, we do not believe this matter should have a material adverse effect on our financial condition, operating results, or cash flows. However, since the outcome of this matter is uncertain, we cannot give absolute assurance regarding its future resolution, or that such matter may not become material in the future.

Item 5. Market for Registrant’s Common Equity, Related Shareholder Matters and Issuer Purchases of Equity Securities

Our common stock is traded on the New York Stock Exchange under the symbol “BDC.”

As of February 19, 2013, there were 424 record holders of common stock of Belden Inc.

We paid a dividend of $0.05 per share in each quarter of 2012 and 2011. We anticipate that comparable cash dividends will continue to be paid quarterly in the foreseeable future.

15

Table of Contents

Common Stock Prices and Dividends

| 2012 (By Quarter) | ||||||||||||||||

| 1 | 2 | 3 | 4 | |||||||||||||

Dividends per common share | $ | 0.05 | $ | 0.05 | $ | 0.05 | $ | 0.05 | ||||||||

Common stock prices: | ||||||||||||||||

High | $ | 41.43 | $ | 38.39 | $ | 39.96 | $ | 45.00 | ||||||||

Low | $ | 34.30 | $ | 29.65 | $ | 30.93 | $ | 33.76 | ||||||||

| 2011 (By Quarter) | ||||||||||||||||

| 1 | 2 | 3 | 4 | |||||||||||||

Dividends per common share | $ | 0.05 | $ | 0.05 | $ | 0.05 | $ | 0.05 | ||||||||

Common stock prices: | ||||||||||||||||

High | $ | 40.41 | $ | 39.48 | $ | 38.26 | $ | 35.94 | ||||||||

Low | $ | 33.19 | $ | 31.21 | $ | 25.47 | $ | 23.24 | ||||||||

Set forth below is information regarding our stock repurchases for the three months ended December 31, 2012.

| Period | Total Number of Shares Purchased | Average Price Paid per Share | Total Number of Shares Repurchased as Part of Publicly Announced Plans or Programs (1) | Approximate Dollar Value of Shares that May Yet Be Purchased Under the Plans or Programs | ||||||||||||

October 1, 2012 through November 4, 2012 | — | $ | — | — | $ | 25,000,000 | ||||||||||

November 5, 2012 through December 2, 2012 | — | — | — | 225,000,000 | ||||||||||||

December 3, 2012 through December 31, 2012 | — | — | — | 225,000,000 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Total | — | $ | — | — | $ | 225,000,000 | ||||||||||

|

|

|

|

|

|

|

| |||||||||

| (1) | In July 2011, our Board of Directors authorized a share repurchase program, which allows us to purchase up to $150.0 million of our common stock through open market repurchases, negotiated transactions, or other means, in accordance with applicable securities laws and other restrictions. The program does not have an expiration date and may be suspended at any time at the discretion of the Company. As of December 31, 2012, we have repurchased 3.7 million shares of our common stock under the program for an aggregate cost of $125.0 million and an average price of $33.72. In November 2012, our Board of Directors authorized an additional share repurchase program, which allows us to purchase up to an additional $200.0 million of our common stock through open market repurchases, negotiated transactions, or other means, in accordance with applicable securities laws and other restrictions. This program will be funded by cash on hand and free cash flow. For the year ended December 31, 2012, we did not repurchase any shares of our common stock under the $200.0 million program. |

16

Table of Contents

Stock Performance Graph

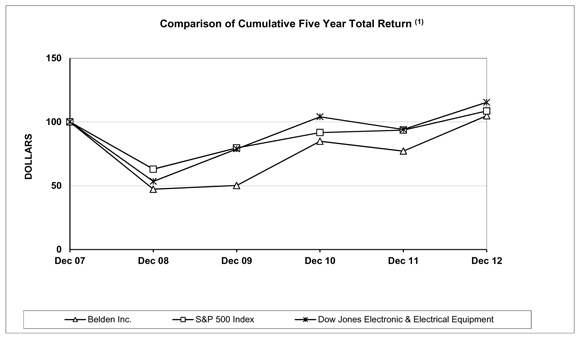

The following graph compares the cumulative total shareholder return on Belden’s common stock over the five-year period ended December 31, 2012, with the cumulative total return during such period of the Standard and Poor’s 500 Stock Index and the Dow Jones Electronic & Electrical Equipment Index. The comparison assumes $100 was invested on December 31, 2007, in Belden’s common stock and in each of the foregoing indices and assumes reinvestment of dividends. The stock performance shown on the graph below represents historical stock performance and is not necessarily indicative of future stock price performance.

Total Return To Shareholders

(Includes reinvestment of dividends)

| Annual Return Percentage | ||||||||||||||||||||

| 2008 | 2009 | 2010 | 2011 | 2012 | ||||||||||||||||

Belden Inc. | –52.8 | % | 6.2 | % | 69.1 | % | –9.1 | % | 35.9 | % | ||||||||||

S&P 500 Index | –37.0 | % | 26.5 | % | 15.1 | % | 2.1 | % | 16.0 | % | ||||||||||

Dow Jones Electronic & Electrical Equipment | –46.6 | % | 47.7 | % | 31.9 | % | –9.5 | % | 22.6 | % | ||||||||||

| Indexed Returns | ||||||||||||||||||||||||

| Years Ended December 31, | ||||||||||||||||||||||||

| 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | |||||||||||||||||||

Belden Inc. | $ | 100.00 | $ | 47.24 | $ | 50.17 | $ | 84.86 | $ | 77.15 | $ | 104.85 | ||||||||||||

S&P 500 Index | 100.00 | 63.00 | 79.67 | 91.68 | 93.61 | 108.59 | ||||||||||||||||||

Dow Jones Electronic & Electrical Equipment | 100.00 | 53.41 | 78.87 | 104.01 | 94.10 | 115.39 | ||||||||||||||||||

| (1) | This chart and the accompanying data are “furnished,” not “filed,” with the SEC. |

17

Table of Contents

| Item 6. | Selected Financial Data |

| Years Ended December 31, | ||||||||||||||||||||

| 2012 | 2011 | 2010 | 2009 | 2008 | ||||||||||||||||

| (In thousands, except per share amounts) | ||||||||||||||||||||

Statement of operations data: | ||||||||||||||||||||

Revenues | $ | 1,840,739 | $ | 1,882,187 | $ | 1,543,386 | $ | 1,304,088 | $ | 1,909,635 | ||||||||||

Operating income (loss) | 108,497 | 165,206 | 116,639 | 31,065 | (285,842 | ) | ||||||||||||||

Income (loss) from continuing operations | 43,236 | 101,308 | 61,276 | (10,221 | ) | (319,234 | ) | |||||||||||||

Basic income (loss) per share from continuing operations | 0.96 | 2.15 | 1.31 | (0.22 | ) | (7.14 | ) | |||||||||||||

Diluted income (loss) per share from continuing operations | 0.94 | 2.11 | 1.28 | (0.22 | ) | (7.14 | ) | |||||||||||||

Balance sheet data: | ||||||||||||||||||||

Total assets | 2,584,583 | 1,788,120 | 1,696,484 | 1,620,578 | 1,658,393 | |||||||||||||||

Long-term debt | 1,135,527 | 550,926 | 551,155 | 543,942 | 590,000 | |||||||||||||||

Long-term debt, including current maturities | 1,151,205 | 550,926 | 551,155 | 590,210 | 590,000 | |||||||||||||||

Stockholders’ equity | 811,860 | 694,549 | 638,515 | 551,048 | 570,868 | |||||||||||||||

Other data: | ||||||||||||||||||||

Basic weighted average common shares outstanding | 45,097 | 47,109 | 46,805 | 46,594 | 44,692 | |||||||||||||||

Diluted weighted average common shares outstanding | 45,942 | 48,104 | 47,783 | 46,594 | 44,692 | |||||||||||||||

Dividends per common share | $ | 0.20 | $ | 0.20 | $ | 0.20 | $ | 0.20 | $ | 0.20 | ||||||||||

In 2012, we acquired Miranda in our fiscal third quarter and PPC in our fiscal fourth quarter. The results of operations of these entities are included in our operating results from their respective acquisition dates. We sold certain assets of our Chinese cable operations that conducted business primarily in the consumer electronics end market at the end of our fiscal fourth quarter. We sold our Thermax and Raydex cable business in 2012, which has been treated as a discontinued operation. During 2012, we also recognized a loss on debt extinguishment of $52.5 million, asset impairment and loss on sale of assets of $33.7 million, and severance and other restructuring costs of $17.9 million.

In 2011, we acquired ICM, Poliron, and Byres Security. The results of operations of these entities are included in our operating results from their respective acquisition dates. During 2011, we recognized severance expense of $5.0 million and asset impairment charges of $2.5 million.

In 2010, we acquired GarrettCom and the Communications Products business of Thomas & Betts during our fiscal fourth quarter. The results of operations of these entities are included in our operating results from their respective acquisition dates. During 2010, we recognized expenses from the effects of purchase accounting of $6.5 million, severance expense of $1.1 million, and asset impairment charges of $16.6 million.

In 2009, we streamlined our manufacturing, sales and administrative functions worldwide in an effort to reduce costs and mitigate the weakening demand experienced throughout the global economy. During 2009, we recognized severance and employee relocation expenses of $29.6 million, asset impairment charges of $27.8 million, loss on sale of assets of $17.2 million, adjusted depreciation expense of $2.6 million, and other charges related to our global restructuring actions of $24.1 million.

In 2008, we recognized goodwill and other asset impairment charges of $443.7 million, severance expense of $39.9 million, loss on sale of assets of $3.7 million, and other charges related to our various restructuring actions of $4.9 million.

18

Table of Contents

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

Overview

We design and manufacture a portfolio of signal transmission solutions which address the unique needs of industrial, enterprise, and broadcast markets. We strive to create shareholder value by:

| • | Delivering highly engineered signal transmission solutions for mission-critical applications in a diverse set of global markets; |

| • | Capturing additional market share by using our Market Delivery System to improve channel and end-user relationships, and concentrate sales efforts on customers in higher growth geographies and vertical end-markets; |

| • | Investing in both organic and inorganic growth initiatives in fast-growing emerging markets and high growth vertical markets; |

| • | Continuously improving our people, processes, and systems through scalable, flexible, and sustainable business systems for talent management, Lean enterprise, and acquisition cultivation and integration; |

| • | Managing our product portfolio to eliminate low-margin revenue and increase revenue in higher margin and strategically important products; |

| • | Protecting and enhancing the value of the Belden brands. |

We believe our business system, extensive portfolio of innovative solutions, exposure to high-growth vertical end-markets, and our expanding position within emerging markets present a unique value proposition that increases shareholder value.

To accomplish these goals, we use a set of tools and processes that are designed to continuously improve business performance in the critical areas of quality, delivery, cost, and innovation. We consider revenue growth, operating margin, free cash flows, return on invested capital, and working capital management metrics to be our key operating performance indicators. We also seek to acquire businesses that we believe can help us achieve these objectives. The extent to which appropriate acquisitions are made and integrated can affect our overall growth, operating results, financial condition, and cash flows.

We generated approximately 55% of our sales outside of the United States in 2012. As a global business, our operations are affected by worldwide, regional, and industry economic and political factors. We continue to operate in a highly competitive business environment in our served markets and geographies. Our market and geographic diversity limits the impact of any one market or the economy of any single country on our consolidated operating results. Our individual businesses monitor key competitors and customers, including to the extent possible their sales, to gauge relative performance and the outlook for the future. In addition, we use indices for general economic trends to predict our outlook for the future given the broad range of products manufactured and end markets served.

We use the United States dollar as our reporting currency, although a substantial portion of our assets, liabilities, operating results, and cash flows reside in or are derived from countries other than the United States. These assets, liabilities, operating results, and cash flows are translated from local currencies into the United States dollar using exchange rates effective during the respective period. We have generally accepted the exposure to currency exchange rate movements without using derivative financial instruments to manage this risk. Both positive and negative movements in currency exchange rates relative to the United States dollar will continue to affect the reported amount of assets, liabilities, operating results, and cash flows in our Consolidated Financial Statements.

Significant Trends and Events in 2012

The following trends and events during 2012 had varying effects on our financial condition, results of operations, and cash flows.

19

Table of Contents

Commodity Prices

Our operating results can be affected by changes in prices of commodities, primarily copper, silver, and compounds, which are components in some of the products we sell. Generally, as the costs of inventory purchases increase due to higher commodity prices, we raise selling prices to customers to cover the increase in costs, resulting in higher sales revenue but a lower gross profit percentage. Conversely, a decrease in commodity prices would result in lower sales revenue but a higher gross profit percentage. Selling prices of our products are affected by many factors, including end market demand, capacity utilization, overall economic conditions, and commodity prices. Importantly, however, there is no exact measure of the effect of changing commodity prices, as there are numerous transactions in any given quarter, each of which has various factors involved in the individual pricing decisions. Therefore, all references to the effect of copper prices or other commodity prices are estimates.

Channel Inventory

Our operating results also can be affected by the levels of Belden products held as inventory by our channel partners and customers. Our channel partners and customers purchase and hold our products in their inventory in order to meet the service and on-time delivery requirements of their customers. Generally, as our channel partners and customers change the level of Belden products owned and held in their inventory, it impacts our revenues. Comparisons of our results between periods can be impacted by changes in the levels of channel inventory.

Acquisitions