UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| þ | ANNUAL REPORT PURSUANT TO SECTION 13 OR SECTION 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2007

OR

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from _______ to _____ .

Commission file number: 1-13648

Balchem Corporation

(Exact name of Registrant as specified in its charter)

| Maryland | 13-2578432 | |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification Number) |

P.O. Box 600, New Hampton, NY 10958

(Address of principal executive offices) (Zip Code)

Registrant’s telephone number, including area code: (845) 326-5600

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Name of each exchange on which registered | |

| Common Stock, par value $.06-2/3 per share | Nasdaq Global Market |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark whether the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No þ

Indicate by check mark whether the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No þ

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. þ

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| (Check one): | Large accelerated filer o | Accelerated filer þ |

Non-accelerated filer o | Smaller reporting company o |

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No þ

The aggregate market value of the common stock issued and outstanding and held by non-affiliates of the Registrant, based upon the closing price for the common stock on the NASDAQ Global Market on June 30, 2007 was approximately $317,332,000. For purposes of this calculation, shares of the Registrant held by directors and officers of the Registrant and under the Registrant's 401(k)/profit sharing plan have been excluded.

The number of shares outstanding of the Registrant's common stock was 18,039,214 as of March 3, 2008.

DOCUMENTS INCORPORATED BY REFERENCE

Selected portions of the Registrant’s proxy statement for its 2008 Annual Meeting of Stockholders (the “2008 Proxy Statement”) to be filed with the Securities and Exchange Commission pursuant to Regulation 14A within 120 days after Registrant’s fiscal year-end of December 31, 2007 are incorporated by reference in Part III of this Report.

Cautionary Statement Regarding Forward-Looking Statements

This Annual Report on Form 10-K contains “forward-looking statements” within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended. Forward-looking statements are not statements of historical facts, but rather reflect our current expectations or beliefs concerning future events and results. We generally use the words "believes," "expects," "intends," "plans," "anticipates," "likely," "will" and similar expressions to identify forward-looking statements. Such forward-looking statements, including those concerning our expectations, involve risks, uncertainties and other factors, some of which are beyond our control, which may cause our actual results, performance or achievements, or industry results, to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements. The risks, uncertainties and factors that could cause our results to differ materially from our expectations and beliefs include, but are not limited to, those factors set forth in this Annual Report on Form 10-K under "Item 1A. - Risk Factors" below, as well as the following:

| · | changes in laws or regulations affecting our operations; |

| · | changes in our business tactics or strategies; |

| · | acquisitions of new or complementary operations; |

| · | sales of any of our existing operations; |

| · | changing market forces or contingencies that necessitate, in our judgment, changes in our plans, strategy or tactics; and |

| · | fluctuations in the investment markets or interest rates, which might materially affect our operations or financial condition. |

We cannot assure you that the expectations or beliefs reflected in these forward-looking statements will prove correct. We undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. You are cautioned not to unduly rely on such forward-looking statements when evaluating the information presented in this Annual Report on Form 10-K.

Part I

Item 1. Business

General:

Balchem Corporation (“Balchem,” the “Company,” “we” or “us”), incorporated in the State of Maryland in 1967, is engaged in the development, manufacture and marketing of specialty performance ingredients and products for the food, nutritional, feed, pharmaceutical and medical sterilization industries. The Company has three segments: specialty products, encapsulated / nutritional products and the unencapsulated feed supplements segment (also referred to in this report as “BCP Ingredients” or “BCP”). Products relating to choline animal feed for non-ruminant animals are primarily reported in the unencapsulated feed supplements segment. Human choline nutrient products, calcium carbonate products for the pharmaceutical industry and encapsulated products are reported in the encapsulated / nutritional products segment. Chelated products and nutritional products for the animal health industry are also reported in the encapsulated / nutritional products segment.

The Company sells its products through its own sales force, independent distributors and sales agents. Financial information concerning the Company's business, business segments and geographic information appears in the Notes to our Consolidated Financial Statements included under Item 8 below, which information is incorporated herein by reference.

1

The Company operates four domestic subsidiaries, all of which are wholly-owned: BCP, Balchem Minerals Corporation (“BMC”), BCP Saint Gabriel, Inc. (“BCP St. Gabriel”), each a Delaware corporation, and Chelated Minerals Corporation (“CMC”), a Utah corporation. We also operate three wholly-owned subsidiaries in Europe: Balchem BV and Balchem Trading BV, both Dutch limited liability companies, and Balchem Italia Srl, an Italian limited liability company. Unless otherwise stated to the contrary, or unless the context otherwise requires, references to the Company in this report includes Balchem Corporation and its subsidiaries.

Encapsulated / Nutritional Products

The encapsulated / nutritional products segment provides microencapsulation, chelation and agglomeration solutions to a variety of applications in food, pharmaceutical and nutritional ingredients to enhance therapeutic performance, taste, processing, packaging and shelf-life. Major product applications are baked goods, refrigerated and frozen dough systems, processed meats, seasoning blends, confections, nutritional supplements, pharmaceuticals and animal nutrition. We also market human grade choline nutrient products through this industry segment for wellness applications. Choline is recognized to play a key role in the structural integrity of cell membranes, processing dietary fat, reproductive development and neural functions, such as memory and muscle function. Balchem’s portfolio of granulated calcium carbonate products are primarily used in, or in conjunction with, novel over-the-counter and prescription pharmaceuticals for the treatment of osteoporosis, gastric disorders and calcium deficiencies.

In animal health industries, Balchem markets REASHURE® Choline, an encapsulated choline product that improves health and production in transition and early lactation dairy cows. Also in animal health we market NITROSHURETM, an encapsulated urea supplement for lactating dairy cows, allowing for greater flexibility in feed rations for dairy nutritionists and producers, and NIASHURETM, our microencapsulated niacin product. In addition, we manufacture, sell and distribute chelated mineral supplements for use in animal feed throughout the world, utilizing our proprietary chelation technology for enhanced nutrient absorption for various species of production and companion animals.

Specialty Products

Our specialty products segment operates as ARC Specialty Products. The specialty products segment repackages and distributes the following specialty gases: ethylene oxide, blends of ethylene oxide, propylene oxide and methyl chloride.

We sell ethylene oxide, at the 100% level, as a sterilant gas, primarily for use in the health care industry. It is used to sterilize a wide range of medical devices because of its versatility and effectiveness in treating hard or soft surfaces, composites, metals, tubing and different types of plastics without negatively impacting the performance or appearance of the device being sterilized. The Company distributes its 100% ethylene oxide product in uniquely designed, recyclable double-walled stainless steel drums to assure compliance with safety, quality and environmental standards as outlined by the U.S. Environmental Protection Agency (the “EPA”) and the U.S. Department of Transportation. The Company's inventory of these specially built drums, along with the Company's three filling facilities, represent a significant capital investment. Contract sterilizers, medical device manufacturers, and medical gas distributors are the Company’s principal customers for this product. In addition, ethylene oxide blends are highly effective as a fumigant, in killing bacteria, fungi, and insects in spices and other seasoning materials. In addition, the Company also sells small, uniquely designed single use canisters of 100% ethylene oxide for use in medical device sterilization.

We sell two other products, propylene oxide and methyl chloride, principally to customers seeking smaller (as opposed to bulk) quantities and whose requirements include timely delivery and safe handling. Propylene oxide is used for fumigation in spice treatment and in various chemical synthesis applications. It is also utilized in industrial applications to make paints more durable, and for manufacturing specialty starches and textile coatings. Methyl chloride is used as a raw material in specialty herbicides, fertilizers and pharmaceuticals, as well as in malt and wine preservers.

2

BCP Ingredients

This segment manufactures and supplies choline chloride, an essential nutrient for animal health, predominantly to the poultry and swine industries. Choline plays a vital role in the metabolism of fat and the building and maintaining of cell structures. A choline deficiency can result in, among other symptoms, reduced growth and perosis in poultry; and fat deposits in the liver, kidney necrosis and general poor health conditions in swine. In addition, certain derivatives of choline chloride are also manufactured and sold into industrial applications. Choline chloride is manufactured and sold in both an aqueous and dry form and is sold through our own sales force, independent distributors and sales agents. Certain derivatives of choline chloride are also marketed into industrial applications. In addition to choline chloride acquired through the Akzo Nobel Acquisition, which is defined below, this segment manufactures and sells methylamines. Methylamines are a primary building block for the manufacture of choline products and are also used in a wide range of industrial applications.

Raw Materials:

The raw materials utilized by the Company in the manufacture of its products are generally available from a number of commercial sources. Such raw materials include materials derived from petrochemicals, minerals, metals and other readily available commodities and are subject to price fluctuations due to market conditions. The Company is not experiencing any current difficulties in procuring such materials and does not anticipate any such problems; however, the Company cannot assure that will always be the case.

Intellectual Property:

The Company currently holds 17 patents in the United States and overseas and uses certain trade-names and trademarks. It also uses know-how, trade secrets, formulae, and manufacturing techniques that assist in maintaining competitive positions of certain of its products. Formulae and know-how are of particular importance in the manufacture of a number of the Company’s products. The Company believes that certain of its patents, in the aggregate, are advantageous to its business. However, it is believed that no single patent or related group of patents is currently so material to the Company that the expiration or termination of any single patent or group of patents would materially affect its business. The Company believes that its sales and competitive position are dependent primarily upon the quality of its products, its technical sales efforts and market conditions, rather than on any patent protection.

Licensing:

The Company entered into a license agreement with Project Management and Development Co., Ltd., a British corporation ("PMD") in November 2005. As of August 2006, PMD assigned the license agreement in its entirety to its successor in interest, Al Kayan Petrochemical Company. On August 1, 2007 Al Kayan Petrochemical Company assigned the license agreement in its entirety to its successor in interest, Saudi Kayan Petrochemical Company (“SKPC”). Under the license agreement, SKPC has the right to utilize the Company’s proprietary continuous manufacturing technology for the production of aqueous choline chloride in connection with SKPC’s construction and operation of an aqueous choline chloride production facility at SKPC’s Al-Jubail, Saudi Arabia petrochemical facility, currently scheduled for completion in late 2010. In addition, SKPC has the exclusive right to use such technology in certain countries, as well as the non-exclusive right to market, sell and use the products derived from such technology on a world-wide basis except that the Company is to be SKPC’s exclusive North American distributor for such products.

The license agreement terminates either 10 years from the start-up of SKPC’s production facility or December 31, 2020, whichever is earlier.

3

Seasonality:

In general, the business of the Company's segments is not seasonal to any material extent.

Backlog:

At December 31, 2007, the Company had a total backlog of $7,303,000 (including $2,661,000 for the encapsulated/nutritional products segment; $354,000 for the specialty products segment and $4,288,000 for BCP Ingredients), as compared to a total backlog of $2,853,000 at December 31, 2006 (including $1,769,000 for the encapsulated/nutritional products segment; $655,000 for the specialty products segment and $429,000 for BCP Ingredients). The increase in our backlog is principally a result of acquisitions in the BCP segment as described below. It has generally been the Company’s policy and practice to maintain an inventory of finished products and/or component materials for its segments to enable it to ship products within two months after receipt of a product order. All orders in the current backlog are expected to be filled in the 2008 fiscal year.

Competition:

The Company’s competitors include many large and small companies, some of which have greater financial, research and development, production and other resources than the Company. Competition in the encapsulation markets served by the Company is based primarily on product performance, customer support, quality, service and price. The development of new and improved products is important to the Company’s success. This competitive environment requires substantial investments in product and manufacturing process research and development. In addition, the winning and retention of customer acceptance of the Company’s encapsulated products involve substantial expenditures for application testing and sales efforts. The Company also engages various universities to assist in research and provide independent third-party analysis. In the specialty products business, the Company faces competition from alternative sterilizing technologies and products. Competition in the animal feed markets served by the Company is based primarily on service and price.

Research & Development:

During the years ended December 31, 2007, 2006 and 2005, the Company incurred research and development expense of approximately $2.5 million, $2.0 million and $2.1 million, respectively, on Company-sponsored research and development for new products and improvements to existing products and manufacturing processes, principally in the encapsulated / nutritional products segment. During the year ended December 31, 2007, an average of 15 employees were devoted full time to research and development activities. The Company has historically funded its research and development programs with funds available from current operations with the intent of recovering those costs from profits derived from future sales of products resulting from, or enhanced by, the research and development effort.

The Company prioritizes its product development activities in an effort to allocate its resources to those product candidates that the Company believes have the greatest commercial potential. Factors considered by the Company in determining the products to pursue include projected markets and needs, status of its proprietary rights, technical feasibility, expected and known product attributes, and estimated costs to bring the product to market.

Acquisitions, Dispositions, and Capital Projects:

In 2007, we made two significant acquisitions.

In April, pursuant to an asset purchase agreement dated March 30, 2007, we acquired the methylamines and choline chloride business and manufacturing facilities of Akzo Nobel Chemicals S.p.A., located in Marano Ticino, Italy, through our affiliate, Balchem BV. Balchem BV subsequently assigned

4

this asset purchase agreement to its wholly-owned subsidiary, Balchem Italia Srl. In this Annual Report on Form 10-K, we refer to this acquisition as the “Akzo Nobel Acquisition”.

In March, BCP acquired certain choline chloride business assets of Chinook Global Limited ("Chinook"), a privately held Ontario corporation. In this Annual Report on Form 10-K, we refer to this acquisition as the “Chinook Acquisition”.

In addition, in August 2006, we acquired from BioAdditives, LLC, CMB Additives, LLC and CMB Realty of Louisiana, an animal feed grade aqueous choline chloride manufacturing facility and related assets located in St. Gabriel, Louisiana. In connection, we also acquired from such sellers the remaining interest in a renewable land lease (approximately 19 years remaining on the original term) relating to the realty upon which the acquired facility and related assets are located. In this Annual Report on Form 10-K, we refer to this acquisition as the “St. Gabriel Acquisition.”

In February 2006, we acquired all of the outstanding capital stock of CMC, which was then privately held. CMC is a manufacturer and global marketer of chelated mineral nutritional supplements for livestock, pet and swine feeds. In this Annual Report on Form 10-K, we refer to this acquisition as the “CMC Acquisition.”

In June 2005, we acquired Loders Croklaan USA, LLC’s encapsulation, agglomeration and granulation business. In this Annual Report on Form 10-K, we refer to this acquisition as the “Loders Croklaan Acquisition.”

Excluding our 2007 acquisitions, capital expenditures were approximately $4.9 million for 2007, as compared to $2.3 million in 2006. Capital expenditures are projected to be approximately $5.6 million for 2008.

Environmental / Regulatory Matters:

The Federal Insecticide, Fungicide and Rodenticide Act, as amended (“FIFRA”), a health and safety statute, requires that certain products within our specialty products segment must be registered with the EPA because they are considered pesticides. In order to obtain a registration, an applicant typically must demonstrate, through extensive test data, that its product will not cause unreasonable adverse effects on the environment. We hold an EPA registration permitting us to sell ethylene oxide as a medical device sterilant and spice fumigant. We are in the process of reregistering this product’s use in compliance with FIFRA re-registration requirements for all pesticide products. In December 2004, the EPA informed us and the other technical registrant under the current registration that the EPA was beginning the 6-phase process to develop a Re-registration Eligibility Decision (RED) for this product. In 2006, the EPA's Office of Pesticide Programs (OPP) bifurcated the process, and dealt first with the reassessment of spice residue tolerances in order to meet the deadline mandated by the Food Quality Protection Act of 1996. On August 9, 2006, OPP issued a Tolerance Reassessment Progress and Risk Management Decision (TRED) relating to the use of ethylene oxide to treat spices. This TRED prohibits the use of ethylene oxide to treat basil, effective August 1, 2007, but allows the continuing use of ethylene oxide to treat all other spices, provided a mandated treatment method is used beginning August 1, 2008. In current published status reports, the EPA states that it will issue the RED covering all uses of ethylene oxide, including its use as a medical device sterilant, in March 2008. We have actively participated in the public access portions of the EPA’s Office of Research and Development’s assessment of the carcinogenicity of ethylene oxide and OPP's RED process, and will continue to do so until their conclusions. We believe that the use of ethylene oxide will continue to be permitted, although the EPA has indicated additional testing may be required in order to maintain the current uses after the RED is issued, and the EPA may require some additional restrictions on current uses. Additionally, the product, when used as a medical device sterilant, has no known equally effective substitute. Management believes absence of availability of this product could not be easily tolerated by various medical device manufacturers and the health care industry due to the resultant infection potential.

5

The State of California lists 100% ethylene oxide, when used as a sterilant or fumigant, as a carcinogen and reproductive toxin under California's Proposition 65 (Safe Drinking Water and Toxic Enforcement Act of 1986). As a result, the Company is required to provide a prescribed warning to any person in California who may be exposed to this product. Failure to provide such warning would result in liability of up to $2,500 per day per person exposed.

The Company’s facility in Verona, Missouri, while held by a prior owner, was designated by the EPA as a Superfund site and placed on the National Priorities List in 1983, because of dioxin contamination on portions of the site. Remediation conducted by the prior owner under the oversight of the EPA and the Missouri Department of Natural Resources (“MDNR”) included removal of dioxin contaminated soil and equipment, capping of areas of residual contamination in four relatively small areas of the site separate from the manufacturing facilities, and the installation of wells to monitor groundwater and surface water for contamination for certain organic chemicals. No ground water or surface water treatment has been required. In 1998, the EPA certified the work on the contaminated soils to be complete. In February 2000, after the conclusion of two years of monitoring groundwater and surface water, the former owner submitted a draft third party risk assessment report to the EPA and MDNR recommending no further action. The prior owner is awaiting the response of the EPA and MDNR to the draft risk assessment.

While the Company must maintain the integrity of the capped areas in the remediation areas on the site, the prior owner is responsible for completion of any further Superfund remedy. The Company is indemnified by the sellers under its May 2001 asset purchase agreement covering its acquisition of the Verona facility for potential liabilities associated with the Superfund site and one of the sellers, in turn, has the benefit of certain contractual indemnification by the prior owner that executed the above-described Superfund remedy.

In connection with normal operations at its plant facilities, the Company is required to maintain environmental and other permits, including those relating to the ethylene oxide operations.

The Company believes it is in compliance in all material respects with federal, state, local and international provisions that have been enacted or adopted regulating the discharge of materials into the environment or otherwise relating to the protection of the environment. Such compliance includes the maintenance of required permits under air pollution regulations and compliance with requirements of the Occupational Safety and Health Administration. The cost of such compliance has not had a material effect upon the results of operations or financial condition of the Company. In 1982, the Company discovered and thereafter removed a number of buried drums containing unidentified waste material from the Company’s site in Slate Hill, New York. The Company thereafter entered into a Consent Decree to evaluate the drum site with the New York Department of Environmental Conservation (“NYDEC”) and performed a Remedial Investigation/Feasibility Study that was approved by NYDEC in February 1994. Based on NYDEC requirements, the Company remediated the area and removed soil from the drum burial site. This proceeding has been substantially completed (see Item 3).

The Channahon, Illinois manufacturing facility manufactures a calcium carbonate line of pharmaceutical grade ingredients. This facility is registered with the United States Food and Drug Administration (“FDA”) as a drug manufacturing facility. These products must be manufactured in conformity with current Good Manufacturing Practice (cGMP) regulations as interpreted and enforced by the FDA. Modifications, enhancements or changes in manufacturing facilities or procedures of our pharmaceutical products are, in many circumstances, subject to FDA approval, which may be subject to a lengthy application process or which we may be unable to obtain. The Channahon, Illinois facility, as well as those of any third-party cGMP manufacturers that we may use, are periodically subject to inspection by the FDA and other governmental agencies, and operations at these facilities could be interrupted or halted if the results of these inspections are unsatisfactory.

6

Employees:

As of March 1, 2008, the Company employed approximately 320 persons. Approximately 73 employees at our Marano, Ticino, Italy facility are covered by a national collective bargaining agreement, which expires in 2010. Approximately 55 employees at the Company’s Verona, Missouri facility are covered by a collective bargaining agreement, which expires in 2012.

Available Information:

The Company’s headquarters is located at 52 Sunrise Park Road, P.O. Box 600, New Hampton, NY 10958. The Company’s telephone number is (845) 326-5600 and its Internet website address is www.balchem.com. The Company makes available through its website, free of charge, its Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q and Current Reports on Form 8-K, and amendments to such reports, as soon as reasonably practicable after they have been electronically filed with the Securities and Exchange Commission. Such reports are available via a link from the Investor Information page on the Company’s website to a list of the Company’s reports on the Securities and Exchange Commission’s EDGAR website.

Item 1A. Risk Factors

Our business involves a high degree of risk and uncertainty, including the following risks and uncertainties:

Increased competition could hurt our business and financial results.

We face competition in our markets from a number of large and small companies, some of which have greater financial, research and development, production and other resources than we do. Our competitive position is based principally on performance, quality, customer support, service, breadth of product line, manufacturing or packaging technology and the selling prices of our products. Our competitors might be expected to improve the design and performance of their products and to introduce new products with competitive price and performance characteristics. We expect to do the same to maintain our current competitive position and market share.

The loss of governmental permits and approvals would materially harm some of our businesses.

Pursuant to applicable environmental and safety laws and regulations, we are required to obtain and maintain certain governmental permits and approvals, including an EPA registration for our ethylene oxide sterilant product. We maintain an EPA registration of ethylene oxide as a medical device sterilant and fumicide. We are in the process of re-registering this product in accordance with FIFRA. The EPA may not allow re-registration of ethylene oxide for the uses mentioned above. The failure of the EPA to allow re-registration of ethylene oxide would have a material adverse effect on our business and financial results.

The Channahon, Illinois facility manufactures a calcium carbonate line of pharmaceutical ingredients. This facility is registered with the FDA as a drug manufacturing facility. These products must be manufactured in conformity with current Good Manufacturing Practice (cGMP) regulations as interpreted and enforced by the FDA. Modifications, enhancements or changes in manufacturing facilities or procedures of our pharmaceutical products are, in many circumstances, subject to FDA approval, which may be subject to a lengthy application process or which we may be unable to obtain. Our Channahon, Illinois facility, as well as those of any third-party cGMP manufacturers that we may use, are periodically subject to inspection by the FDA and other governmental agencies, and operations at these facilities could be interrupted or halted if the results of these inspections are unsatisfactory. Failure to comply with the FDA or other governmental regulations can result in fines, unanticipated compliance expenditures, recall or seizure of products, total or partial suspension of production, enforcement actions, injunctions and criminal prosecution, which could have a material adverse effect on our business and financial results.

7

Permits and approvals may be subject to revocation, modification or denial under certain circumstances. Our operations or activities (including the status of compliance by the prior owner of the Verona, Missouri facility under Superfund remediation) could result in administrative or private actions, revocation of required permits or licenses, or fines, penalties or damages, which could have an adverse effect on us. In addition, we can not predict the extent to which any legislation or regulation may affect the market for our products or our cost of doing business.

Raw material shortages or price increases could adversely affect our business and financial results.

The principal raw materials that we use in the manufacture of our products can be subject to price fluctuations. While the selling prices of our products tend to increase or decrease over time with the cost of raw materials, these changes may not occur simultaneously or to the same degree. At times, we may be unable to pass increases in raw material costs through to our customers. Such increases in the price of raw materials, if not offset by product price increases, or substitute raw materials, would have an adverse impact on our profitability. We believe we have reliable sources of supply for our raw materials under normal market conditions. We cannot, however, predict the likelihood or impact of any future raw material shortages. Any shortages could have a material adverse impact on our results of operations.

Our financial success depends in part on the reliability and sufficiency of our manufacturing facilities.

Our revenues depend on the effective operation of our manufacturing, packaging, and processing facilities. The operation of our facilities involves risks, including the breakdown, failure, or substandard performance of equipment, power outages, the improper installation or operation of equipment, explosions, fires, natural disasters, failure to achieve or maintain safety or quality standards, work stoppages, supply or logistical outages, and the need to comply with environmental and other directives of governmental agencies. The occurrence of material operational problems, including, but not limited to, the above events, could adversely affect our profitability during the period of such operational difficulties.

Our failure or inability to protect our intellectual property could harm our business and financial results.

We hold 17 patents in the United States and overseas. Third parties could seek to challenge, invalidate or circumvent our patents. Moreover, there could be successful claims against us alleging that we infringe the intellectual property rights of others. If we are unable to protect all of our intellectual property rights, or if we are found to be infringing the intellectual property rights of others, there could be an adverse effect on our business and financial results. Our competitive position also depends on our use of unpatented trade secrets. Competitors could independently develop substantially equivalent proprietary information, which could hurt our business and financial results.

We face risks associated with our sales to customers and manufacturing operations outside the United States.

For the year ended December 31, 2007, approximately 25% of our net sales consisted of sales outside the United States, predominately to Europe, Japan and China. In addition, we conduct a portion of our manufacturing outside the United States. International sales are subject to inherent risks. The majority of our foreign sales occur through our foreign sales subsidiaries and the remainder of our foreign sales result from exports to foreign distributors, resellers and customers. Our foreign sales and operations are subject to a number of risks, including: longer accounts receivable collection periods; the impact of recessions and other economic conditions in economies outside the United States; export duties and quotas; unexpected changes in regulatory requirements; certification requirements; environmental regulations; reduced protection for intellectual property rights in some countries; potentially adverse tax consequences; political and economic instability; and preference for locally produced products. These factors could have a material adverse impact on our ability to increase or maintain our international sales.

8

We may, from time to time, experience problems in our labor relations.

In North America, approximately 55 employees, or 23% of our North American workforce, as of December 31, 2007, are represented by a union under a single collective bargaining agreement. This agreement expires in 2012. In Europe, approximately 73 employees are covered by a collective bargaining agreement. This agreement expires in 2010. We believe that our present labor relations with all of our unionized employees are satisfactory, however, our failure to renew these agreements on reasonable terms could result in labor disruptions and increased labor costs, which could adversely affect our financial performance. Similarly, if our relations with the unionized portion of our workforce do not remain positive, such employees could initiate a strike, work stoppage or slowdown in the future. In the event of such an action, we may not be able to adequately meet the needs of our customers using our remaining workforce and our operations and financial condition could be adversely affected.

Our international operations subject us to currency translation risk and currency transaction risk which could cause our results to fluctuate from period to period.

The financial condition and results of operations of our foreign subsidiaries are reported in Euros and then translated into U.S. dollars at the applicable currency exchange rate for inclusion in our consolidated financial statements. Exchange rates between these currencies in recent years have fluctuated significantly and may do so in the future. In the past year, as a result of the strength of the Euro compared to the U.S. dollar, our operating results in U.S. dollars were positively affected upon translation. The positive impact of the strengthening Euro may not continue in the future and may even reverse if the Euro declines in value compared to the U.S. dollar. Furthermore, we incur currency transaction risk whenever we enter into either a purchase or a sales transaction using a currency different than the functional currency. Given the volatility of exchange rates, we may not be able to effectively manage our currency transactions and/or translation risks. Volatility in currency exchange rates could impact our business and financial results.

Our success depends in large part on our key personnel.

Our operations significantly depend on the continued efforts of our senior executives. The loss of the services of certain executives for an extended period of time could have a material adverse effect on our business and financial results.

Litigation could be costly and can adversely affect our business and financial results.

We, like all companies involved in the food and pharmaceutical industries, are subject to potential claims for product liability relating to our products. Such claims, irrespective of their outcomes or merits, could be time-consuming and expensive to defend, and could result in the diversion of management time and attention. Any of these situations could have a material adverse effect on our business and financial results.

Item 1B. Unresolved Staff Comments

None.

Item 2. Properties

In February 2002, the Company entered into a ten (10) year lease for approximately 20,000 square feet of office space in New Hampton, New York. The office space is serving as the Company’s general offices and as laboratory facilities for the Company’s encapsulated / nutritional products business.

Manufacturing facilities owned by the Company for its encapsulated products segment and a blending, drumming and terminal facility for the Company’s ethylene oxide business, are presently housed in three buildings located in Slate Hill, New York comprising a total of approximately 51,000 square feet. The Company owns a total of approximately 16 acres of land on two parcels in this community.

9

The Company owns a facility located on an approximately 24 acre parcel of land in Green Pond, South Carolina. The site consists of a drumming facility, a canister filling facility, a maintenance building and an office building comprising a total of approximately 34,000 square feet. The Company uses this site for processing products in its specialty products segment.

The Company’s Verona, Missouri site, which is located on approximately 100 acres, consists of manufacturing facilities relating to animal feed grade choline, human choline nutrients, a drumming facility for the Company’s ethylene oxide business, together with buildings utilized for warehousing such products. The Verona operation buildings comprise a total of approximately 151,000 square feet. The facility, while under prior ownership, was designated by the EPA as a Superfund site (see Item 1 – “Business - Environmental / Regulatory Matters”).

The Company leases production and warehouse space in Channahon, Illinois as a result of the Loders Croklaan Acquisition. The Company uses this facility for production related to the Company’s pharmaceutical line of business. The initial term of the lease is effective through September 30, 2010, subject to earlier termination by Balchem upon sixty days notice, or by the landlord upon sixty days notice. The Company’s leased space in Channahon, Illinois totals approximately 26,000 square feet.

The Company, through CMC, owns a manufacturing facility and warehouse, comprising approximately 16,500 square feet, located on approximately 5 acres of land in Salt Lake City, Utah. The Company manufactures and distributes its chelated mineral nutrients for animal feed products at this location.

The Company, through BCP, acquired in the St. Gabriel Acquisition a manufacturing facility located upon approximately 11 acres of realty leased from Taminco Higher Amines, Inc. in St. Gabriel, Louisiana. The Company manufactures and distributes animal feed grade choline chloride at this location.

The Company, through its European subsidiary, Balchem Italia Srl, acquired in the Akzo Nobel Acquisition a facility located on an approximately 30 acre parcel of land in Marano Ticino, Italy. The Company manufactures and distributes methylamines, animal feed grade choline and human choline nutrients at this location.

Item 3. Legal Proceedings

In 1982 the Company discovered and thereafter removed a number of buried drums containing unidentified waste material from the Company’s site in Slate Hill, New York. The Company thereafter entered into a Consent Decree to evaluate the drum site with the New York Department of Environmental Conservation (“NYDEC”) and performed a Remedial Investigation/Feasibility Study that was approved by NYDEC in February 1994. Based on NYDEC requirements, the Company remediated the area and removed soil from the drum burial site. Clean-up was completed in 1996, and NYDEC required the Company to monitor the site through 1999. The Company continues to be involved in discussions with NYDEC to evaluate monitoring results and determine what, if any, additional actions will be required on the part of the Company to close out the remediation of this site. Additional actions, if any, would likely require the Company to continue monitoring the site. The cost of such monitoring has recently been less than $5,000 per year.

The Company is also involved in other legal proceedings through the normal course of business. Management believes that any unfavorable outcome related to these proceedings will not have a material effect on the Company’s financial position, results of operations or liquidity.

Item 4. Submission of Matters to a Vote of Security Holders

None.

10

PART II

| Item 5. | Market for the Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities |

| (a) | Market Information. |

On December 8, 2006, the Board of Directors of the Company approved a three-for-two split of the Company’s common stock to be effected in the form of a stock dividend to shareholders of record on December 29, 2006. Such stock dividend was made on January 19, 2007. The stock split was recognized by reclassifying the par value of the additional shares resulting from the split, from additional paid-in capital to common stock.

On December 15, 2005, the Board of Directors of the Company approved a three-for-two split of the Company’s common stock to be effected in the form of a stock dividend to shareholders of record on December 30, 2005. Such stock dividend was made on January 20, 2006. The stock split was recognized by reclassifying the par value of the additional shares resulting from the split, from additional paid-in capital to common stock.

On December 16, 2004, the Board of Directors of the Company approved a three-for-two split of the Company’s common stock to be effected in the form of a stock dividend to shareholders of record on December 30, 2004. Such stock dividend was made on January 20, 2005. The stock split was recognized by reclassifying the par value of the additional shares resulting from the split, from additional paid-in capital to common stock.

Since December 22, 2006, the Company’s common stock has traded on the Nasdaq Global Market under the trading symbol BCPC. Prior to that, our common stock traded on the American Stock Exchange under the trading symbol BCP. The high and low closing prices for the common stock as recorded for each quarterly period during the years ended December 31, 2007 and 2006, adjusted for the December 2006 three-for-two stock split (effected by means of a stock dividend) were as follows:

| Quarterly Period | High | Low | ||||||

| Ended March 31, 2007 | $ | 18.56 | $ | 14.09 | ||||

| Ended June 30, 2007 | 19.17 | 17.15 | ||||||

| Ended September 30, 2007 | 21.25 | 15.60 | ||||||

| Ended December 31, 2007 | 24.00 | 20.16 | ||||||

| Quarterly Period | High | Low | ||||||

| Ended March 31, 2006 | $ | 15.99 | $ | 13.57 | ||||

| Ended June 30, 2006 | 15.85 | 13.41 | ||||||

| Ended September 30, 2006 | 15.93 | 13.07 | ||||||

| Ended December 31, 2006 | 19.25 | 12.80 | ||||||

On March 3, 2008 the closing price for the common stock on the Nasdaq Global Market was $20.63.

(b) Record Holders.

As of March 3, 2008, the approximate number of holders of record of the Company’s common stock was 192. Such number does not include stockholders who hold their stock in street name. The total number of beneficial owners of the Company's common stock is estimated to be approximately 10,411.

11

(c) Dividends.

The Company declared cash dividends of $0.11 and $0.09 per share on its common stock during its fiscal years ended December 31, 2007 and 2006, respectively.

For information concerning prior stockholder approval of and other matters relating to our equity incentive plans, see Item 12 in this Annual Report on Form 10-K.

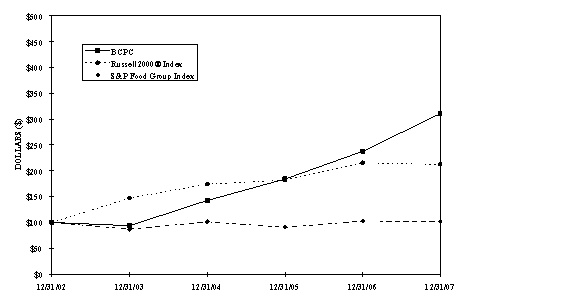

(d) Performance Graph.

The graph below sets forth the cumulative total stockholder return on the Company's Common Stock (referred to in the table as "BCPC") for the five years ended December 31, 2007, the overall stock market return during such period for shares comprising the Russell 2000® Index (which the Company believes includes companies with market capitalization similar to that of the Company), and the overall stock market return during such period for shares comprising the Standard & Poor's 500 Food Group Index, in each case assuming a comparable initial investment of $100 on December 31, 2002 and the subsequent reinvestment of dividends. The Russell 2000® Index measures the performance of the shares of the 2000 smallest companies included in the Russell 3000® Index. In light of the Company's industry segments, the Company does not believe that published industry-specific indices are necessarily representative of stocks comparable to the Company. Nevertheless, the Company considers the Standard & Poor's 500 Food Group Index to be potentially useful as a peer group index with respect to the Company in light of the Company's encapsulated / nutritional products segment. The performance of the Company's Common Stock shown on the graph below is historical only and not indicative of future performance.

Item 6. Selected Financial Data

The selected statements of operations data set forth below for the three years in the period ended December 31, 2007 and the selected balance sheet data as of December 31, 2007 and 2006 have been derived from our Consolidated Financial Statements included elsewhere herein. The selected financial data as of December 31, 2005, 2004 and 2003 and for the years ended December 31, 2004 and 2003 have been derived from audited Consolidated Financial Statements not included herein, but which were previously filed with the SEC. The following information should be read in conjunction with Item 7 — “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the Consolidated Financial Statements and notes thereto included elsewhere herein.

12

Earnings per share and dividend amounts have been adjusted for the December 2006, 2005 and 2004 three-for-two stock splits (effected by means of stock dividends).

(In thousands, except per share data)

| Year ended December 31, | 2007 (1)(2)(3)(4)(5) | 2006 (1)(2)(3) | 2005 (1) | 2004 | 2003 | |||||||||||||||

| Statement of Operations Data | ||||||||||||||||||||

| Net sales | $ | 176,201 | $ | 100,905 | $ | 83,095 | $ | 67,406 | $ | 61,875 | ||||||||||

Earnings before income tax expense | 24,829 | 19,101 | 17,191 | 12,715 | 8,763 | |||||||||||||||

| Income tax expense | 8,711 | 6,823 | 6,237 | 4,689 | 3,125 | |||||||||||||||

| Net earnings | 16,118 | 12,278 | 10,954 | 8,026 | 5,638 | |||||||||||||||

Basic net earnings per common share | $ | .91 | $ | .70 | $ | .63 | $ | .48 | $ | .35 | ||||||||||

Diluted net earnings per common share | $ | .87 | $ | .67 | $ | .61 | $ | .46 | $ | .33 | ||||||||||

| At December 31, | 2007 | 2006 | 2005 | 2004 | 2003 | |||||||||||||||

| Balance Sheet Data | ||||||||||||||||||||

| Total assets | $ | 154,424 | $ | 92,333 | $ | 75,141 | $ | 60,405 | $ | 56,906 | ||||||||||

| Long-term debt | 17,398 | - | - | - | 7,839 | |||||||||||||||

Other long-term obligations | 1,529 | 784 | 1,043 | 1,003 | 985 | |||||||||||||||

| Total stockholders’ equity | 93,080 | 75,362 | 60,933 | 50,234 | 39,781 | |||||||||||||||

| Dividends per common share | $ | .11 | $ | .09 | $ | .06 | $ | .04 | $ | .023 | ||||||||||

| (1) | Includes the operating results, cash flows, and assets relating to the Loders Croklaan Acquisition from the date of acquisition (July 1, 2005) forward. |

| (2) | Includes the operating results, cash flows, and assets relating to the CMC Acquisition from the date of acquisition (February 8, 2006) forward. |

| (3) | Includes the operating results, cash flows, and assets relating to the St. Gabriel Acquisition from the date of acquisition (August 24, 2006) forward. |

| (4) | Includes the operating results, cash flows, and assets relating to the Chinook Acquisition from the date of acquisition (March 19, 2007) forward. |

| (5) | Includes the operating results, cash flows, and assets relating to the Akzo Nobel Acquisition from the date of acquisition (May 1, 2007) forward. |

Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations

Overview

The Company develops, manufactures, distributes and markets specialty performance ingredients and products for the food, nutritional, pharmaceutical, feed and medical sterilization industries. The Company’s reportable segments are strategic businesses that offer products and services to different markets. The Company presently has three reportable segments: specialty products; encapsulated / nutritional products; and BCP Ingredients.

The following discussion and analysis of our financial condition and results of operations should be read in conjunction with Item 6 — “Selected Financial Data” and our Consolidated Financial Statements and the related notes included in this report. Those statements in the following discussion that are not historical in nature should be considered to be forward-looking statements that are inherently uncertain. See “Cautionary Statement Regarding Forward-Looking Statements”.

13

Specialty Products

The specialty products segment repackages and distributes the following specialty gases: ethylene oxide, blends of ethylene oxide, propylene oxide and methyl chloride.

Ethylene oxide, at the 100% level, is sold as a chemical sterilant gas, primarily for use in the health care industry to sterilize medical devices. Contract sterilizers, medical device manufacturers and medical gas distributors are the Company’s principal customers for this product. Blends of ethylene oxide are sold as fumigants and are highly effective in killing bacteria, fungi, and insects in spices and other seasoning type materials. Propylene oxide and methyl chloride are also sold, principally to customers seeking smaller (as opposed to bulk) quantities.

Management believes that future success in this segment is highly dependent on the Company’s ability to maintain its strong reputation for excellent quality, safety and customer service.

Encapsulated / Nutritional Products

The encapsulated / nutritional products segment provides microencapsulation, chelation and agglomeration solutions to a variety of applications in the food, pharmaceutical, human and animal nutrition markets to enhance therapeutic performance, taste, processing, packaging and shelf-life. Major end product applications are baked goods, refrigerated and frozen dough systems, processed meats, seasoning blends, confections, nutritional supplementations, pharmaceuticals and animal nutrition. We also market human grade choline nutrient products through this industry segment for wellness applications. Choline is recognized to play a key role in the structural development of brain cell membranes, processing dietary fat, reproductive development and neural functions, such as memory and muscle function. Balchem’s portfolio of granulated calcium carbonate products are primarily used in novel over-the-counter and prescription pharmaceuticals for the treatment of osteoporosis, gastric disorders and calcium deficiencies in the United States.

Management believes this segment’s key strengths are its proprietary technology and end-product application capabilities. The success of the Company’s efforts to increase revenue in this segment is highly dependent on the timing of marketing launches of new products in the U.S. and international food and nutrition markets by the Company’s customers and prospects. The Company, through its innovative proprietary technology and applications expertise, continues to develop new products designed to solve and respond to customer problems and innovative needs. Sales of specialty products for the animal nutrition and health industry are highly dependent on dairy industry economics as well as the ability of the Company to leverage the results of existing successful university research on the animal health benefits of the Company’s products.

BCP Ingredients

BCP Ingredients manufactures and supplies choline chloride, an essential nutrient for animal health, to the poultry and swine industries. In addition, certain derivatives of choline chloride are also marketed into industrial applications. BCP also manufactures and sells methylamines. Methylamines are a primary building block for the manufacture of choline products and are also used in a wide range of industrial applications.

Management believes that success in this commodity-oriented marketplace is highly dependent on the Company’s ability to maintain its strong reputation for excellent product quality and customer service. In addition, the Company must continue to increase production efficiencies in order to maintain its low-cost position to effectively compete in a highly competitive global marketplace.

The Company sells products for all three segments through its own sales force, independent distributors, and sales agents.

14

The following tables summarize consolidated net sales by segment and business segment earnings from operations for the three years ended December 31, 2007, 2006 and 2005 (in thousands):

Business Segment Net Sales:

| 2007 | 2006 | 2005 | ||||||||||

| Specialty Products | $ | 33,057 | $ | 32,026 | $ | 29,433 | ||||||

| Encapsulated/Nutritional Products | 49,919 | 41,565 | 32,499 | |||||||||

| BCP Ingredients | 93,225 | 27,314 | 21,163 | |||||||||

| Total | $ | 176,201 | $ | 100,905 | $ | 83,095 | ||||||

Business Segment Earnings From Operations:

| 2007 | 2006 | 2005 | ||||||||||

| Specialty Products | $ | 11,824 | $ | 11,315 | $ | 11,007 | ||||||

| Encapsulated/Nutritional Products | 7,194 | 4,200 | 3,217 | |||||||||

| BCP Ingredients | 6,888 | 3,647 | 2,679 | |||||||||

| Total | $ | 25,906 | $ | 19,162 | $ | 16,903 | ||||||

Fiscal Year 2007 compared to Fiscal Year 2006

(All amounts in thousands, except share and per share data)

Net Sales

Net sales for 2007 were $176,201, as compared with $100,905 for 2006, an increase of $75,296 or 74.6%. Net sales for the specialty products segment were $33,057 for 2007, as compared with $32,026 for 2006, an increase of $1,031 or 3.2%. This increase was principally due to an increase in sales volume, along with modest price increases for products in this segment. Net sales for the encapsulated / nutritional products segment were $49,919 for 2007, as compared with $41,565 for 2006, an increase of $8,354 or 20.1%. This result was driven principally by increased global sales of human nutritional and choline products, and includes $1,952 from the Akzo Nobel Acquisition. Sales of REASHURE®, Niashure and chelated minerals, our specialty animal nutrition and health products targeted for ruminant animals, and increases in the companion animal market also contributed to this growth. Net sales for the BCP Ingredients segment was $93,225 in 2007, as compared with $27,314 for 2006, an increase of $65,911 or 241.3%. This result reflects sales from the Chinook Acquisition and the Akzo Nobel Acquisition in 2007, which contributed in the aggregate approximately $62,495 of the revenue in this segment. The remaining increase (approximately 12.5%) was due to increased volumes sold in the core dry and aqueous choline, as well as the specialty industrial product lines.

Operating Expenses

Operating expenses for 2007 increased to $21,024 from $14,844 for 2006, an increase of $6,180 or 41.6%. This increase was due primarily to $2,300 of additional amortization expense, plus sales and technical personnel expense associated with the Chinook and Akzo Nobel acquisitions. We also incurred approximately $1,224 of commercial development expenses toward our pharmaceutical market initiatives in 2007. With these increases, operating expenses were 11.9% of sales or 2.8 percentage points less than the operating expenses as a percent of sales incurred in 2006. During 2007 and 2006, the Company spent $2,514 and $2,019 respectively, on research and development programs, substantially all of which pertained to the Company’s encapsulated / nutritional products segment for both human and animal health.

Business Segment Earnings From Operations

As a result of the foregoing, earnings from operations for 2007 were $25,906 as compared to $19,162 for 2006, reflecting a 35.2% increase from year to year. Earnings from operations for the specialty products segment increased to $11,824 in 2007 from $11,315 in 2006, an increase of $509 or 4.5%, due largely to increases in sales volume and modest sales price increases. These increases were partially offset

15

by higher raw material prices. Earnings from operations for the encapsulated / nutritional products segment increased to $7,194 in 2007 from $4,200 in 2006, an increase of $2,994 or 71.3%, as this segment was favorably affected by the Akzo Nobel Acquisition, increased volumes sold principally in the human choline markets and specialty animal nutrition and health markets. Earnings from operations for the BCP Ingredients segment, increased to $6,888 in 2007 from $3,647 in 2006, an increase of $3,241 or 88.9%, as a result of the previously noted increased sales volumes and improved productivity, partially offset by certain petro-chemical raw material cost increases.

Other Expenses (Income)

Interest income for 2007 totaled $166, as compared to $128 for 2006. This increase is attributable to an increase in the Company’s average cash balance during 2007. Interest expense, net of capitalized interest, was $1,562 for 2007, as compared to $189 for 2006. This increase is attributable to the increase in average current and long-term debt resulting from the Chinook Acquisition and Akzo Nobel Acquisition. Other income of $319 for 2007 is the result of favorable fluctuations in foreign currency exchange rates between the U.S. dollar (the reporting currency) and functional foreign currencies.

Income Tax Expense

The Company’s effective tax rate for 2007 and 2006 was 35.1% and 35.7%, respectively. This decrease in the effective tax rate is primarily attributable to a domestic manufacturer's deduction and to a change in allocation relating to state income taxes. The adoption of Interpretation No. 48, “ Accounting for Uncertainty in Income Taxes ” (“FIN 48”) adversely affected the 2007 income tax expense by $220 and the effective tax rate by 0.9%.

Net Earnings

Primarily as a result of the above-noted increase in sales, net earnings were $16,118 for 2007, as compared with $12,278 for 2006, an increase of 31.3%.

Fiscal Year 2006 compared to Fiscal Year 2005

(All amounts in thousands, except share and per share data)

Net Sales

Net sales for 2006 were $100,905 compared with $83,095 for 2005, an increase of $17,810 or 21.4%. Net sales for the specialty products segment were $32,026 for 2006, as compared with $29,433 for 2005, an increase of $2,593 or 8.8%. This increase was principally due to an increase in sales volume along with modest price increases for our ethylene oxide products for medical device sterilization. Net sales for the encapsulated / nutritional products segment were $41,565 for 2006 compared with $32,499 for 2005, an increase of $9,066 or 27.9%. This increase was due principally to approximately $6,362 of incremental sales associated with the Company’s newly acquired pharmaceutical, food, and chelated minerals business lines resulting from the Loders Croklaan Acquisition and the CMC Acquisition (see Note 5 to our Consolidated Financial Statements). The Company also experienced increased volumes sold in the human choline market, favorable changes in product mix in the domestic and international food markets, and volume improvements in sales of REASHURE®, our animal nutrition and health product targeted for dairy cows. Net sales for the BCP Ingredients segment of $27,314 were realized for 2006 compared with $21,163 for 2005, an increase of $6,151 or 29.1%. This increase was due to increased volumes sold in dry and aqueous choline and choline derivatives, along with modest price increases in all product lines.

Operating Expenses

Operating expenses for 2006 increased to $14,844 from $11,777 for 2005, an increase of $3,067 or 26.0%. Total operating expenses as a percentage of sales were 14.7% for 2006, as compared to 14.2% for 2005. The increase in operating expenses for 2006 was principally a result of stock-based compensation

16

expense of $982 relating to the adoption of the provisions of SFAS No. 123R (revised 2004), “Share-Based Payment”, increased payroll costs and benefits of $874 primarily due to new hires, increased expenditures of $802 in support of the Company’s continuing efforts in the pharmaceutical industry, and higher amortization expense of $356 resulting from the CMC Acquisition. During 2006 and 2005, the Company spent $2,019 and $2,053, respectively, on Company-sponsored research and development programs, substantially all of which pertained to the Company’s encapsulated / nutritional products segment for both food and animal feed applications.

Business Segment Earnings From Operations

As a result of the foregoing, earnings from operations for 2006 were $19,162 as compared to $16,903 for 2005, reflecting an 13.4% increase from year to year. Earnings from operations for the specialty products segment were $11,315, an increase of $308 or 2.8%, due largely to increases in sales volume and modest sales price increases. These increases were partially offset by higher raw material prices. Earnings from operations for the encapsulated / nutritional products segment increased 30.6% as this segment was favorably affected by increased production, a result of greater sales volume as described above. The favorable impact of the increased production was partially offset by higher raw material costs and an unfavorable product mix in the pharmaceutical calcium product line. Earnings from operations for the BCP Ingredients segment were $3,647 as compared to $2,679 for 2005, reflecting a 36.1% increase from year to year. This segment was favorably affected by increased production volumes of choline chloride and specialty derivative products. This favorable impact was partially offset by higher raw material and energy costs.

Other Expenses (Income)

Interest income for 2006 was $128 as compared to $214 for 2005. This decrease is attributable to a decrease in the Company’s average cash balance during 2006. Interest expense was $189 for 2006 compared to $8 for 2005. This increase is attributable to the average outstanding current and long-term debt in 2006, resulting from the CMC Acquisition in February 2006. Other income for 2006 was $-0- as compared to $82 for 2005. This decrease is attributable to the inclusion of a gain on the sale of equipment in 2005.

Income Tax Expense

The Company’s effective tax rate for 2006 was 35.7% compared to a 36.3% rate for 2005. This decrease in the effective tax rate is primarily attributable to a change in allocation relating to state income taxes.

Net Earnings

As a result of the foregoing, net earnings were $12,278 for 2006 as compared with $10,954 for 2005, reflecting a 12.1% increase from 2005 to 2006.

17

LIQUIDITY AND CAPITAL RESOURCES

Contractual Obligations

The Company's contractual obligations and debt obligations, excluding revolver borrowings, as of December 31, 2007, are summarized in the table below:

| Payments due by period | ||||||||||||||||||||

Contractual Obligations | Total | Less than 1 year | 1-3 years | 3-5 years | More than 5 years | |||||||||||||||

| Long-term debt obligations | $ | 24,777 | $ | 7,379 | $ | 17,398 | $ | - | $ | - | ||||||||||

| Operating lease obligations (1) | 1,821 | 797 | 885 | 104 | 35 | |||||||||||||||

| Purchase obligations (2) | 8,068 | 8,068 | - | - | - | |||||||||||||||

| Total | $ | 34,666 | $ | 16,244 | $ | 18,283 | $ | 104 | $ | 35 | ||||||||||

| (1) | Principally includes obligations associated with future minimum non-cancelable operating lease obligations (including the headquarters office space entered into in 2002). |

| (2) | Principally includes open purchase orders with vendors for inventory not yet received or recorded on our balance sheet. |

As part of the June 30, 2005 Loders Croklaan Acquisition, we agreed to make contingent payments of additional consideration based upon the volume of sales associated with one particular product acquired by the Company during the three year period following the acquisition. Such contingent consideration, if and when paid, is recorded as an additional cost of the acquisition. No such contingent consideration has been earned or paid in 2007.

As a result of the adoption of FIN 48 on January 1, 2007, we recorded a liability for uncertain tax positions, net of federal tax benefit, of $511. We are unable to reasonably estimate the amount or timing of payments for this liability, if any.

The Company knows of no current or pending demands on, or commitments for, its liquid assets that will materially affect its liquidity.

The Company expects its operations to continue generating sufficient cash flow to fund working capital requirements and necessary capital investments. The Company is actively pursuing additional acquisition candidates. The Company could seek additional bank loans or access to financial markets to fund such acquisitions, its operations, working capital, necessary capital investments or other cash requirements should it deem it necessary to do so.

Acquisitions and Dispositions

Effective April 30, 2007, pursuant to an asset purchase agreement dated March 30, 2007 (the “Akzo Nobel Asset Purchase Agreement”), the Company, through its European subsidiary, Balchem B.V., completed an acquisition of the methylamines and choline chloride business and manufacturing facilities of Akzo Nobel Chemicals S.p.A., located in Marano Ticino, Italy (the “Akzo Nobel Acquisition”) for a provisional purchase price including acquisition costs of $9,165, subject to adjustment based on actual working capital and other adjustments.

On March 16, 2007, the Company, through BCP, entered into an asset purchase agreement (the "Asset Purchase Agreement") with Chinook Global Limited ("Chinook"), a privately held Ontario corporation, pursuant to which BCP acquired certain of Chinook's choline chloride business assets (the “Chinook Acquisition”) for a purchase price of approximately $29,000, plus the value of certain product inventories of approximately $1,840. The Chinook Acquisition closed effective the same date.

18

On August 24, 2006, pursuant to an asset purchase agreement of same date, the Company, through BCP and BCP St. Gabriel, acquired an animal feed grade aqueous choline chloride manufacturing facility and related assets located in St. Gabriel, Louisiana from BioAdditives, LLC, CMB Additives, LLC and CMB Realty of Louisiana.

On February 8, 2006, the Company, through its wholly owned subsidiary Balchem Minerals Corporation, acquired all of the outstanding capital stock of CMC, for a purchase price of $17,350 before working capital and other adjustments. CMC is a manufacturer and global marketer of chelated mineral nutritional supplements for livestock, pet and swine feeds.

On June 30, 2005, pursuant to an asset purchase agreement of same date, the Company acquired certain assets of Loders Croklaan USA, LLC relating to the encapsulation, agglomeration and granulation business for a purchase price including acquisition costs of $9,885 plus $725 for certain product inventories and $809 for certain accounts receivable. With the exception of $985, which was paid during the quarter ended June 30, 2005, all of such payment was made on July 1, 2005 from the Company’s cash reserves.

Cash

Cash and cash equivalents decreased to $2,307 at December 31, 2007 from $5,189 at December 31, 2006. Working capital amounted to $16,139 at December 31, 2007 as compared to $19,295 at December 31, 2006, a decrease of $3,156.

Operating Activities

Cash flows from operating activities provided $15,637 for 2007 compared to $16,370 for 2006. The decrease in cash flows from operating activities was primarily due to an increase in prepaid expenses and other and accounts receivable resulting from the Methylamines and Choline business acquired in the Akzo Nobel Acquisition and the customer list acquired in the Chinook Acquisition in which we did not acquire outstanding accounts receivable. Combined, they contributed approximately $62,495 of revenue in 2007. This decrease was partially offset by an increase in net earnings, accounts payable and accrued expenses and depreciation and amortization expense.

Investing Activities

Capital expenditures were $4,869 for 2007 compared to $2,279 for 2006. Cash paid in 2007 for the acquisition of certain business assets of Chinook Global Limited and the Akzo Nobel Methylamines and Choline business was $40,744. $22,872 was paid for acquisitions in 2006.

Financing Activities

In June 1999, the board of directors authorized the repurchase of shares of the Company’s outstanding common stock over a two-year period commencing July 2, 1999. Under this program, which was subsequently extended, the Company had, as of December 31, 2004, repurchased a total 1,158,692 shares at an average cost of $2.74 per share, none of which remained in treasury at December 31, 2004. In June 2005, the board of directors authorized another extension of the stock repurchase program for up to an additional 1,350,000 shares, over and above those 1,158,692 shares previously repurchased under the program. Under this extension, a total of 149,175 shares were purchased in 2005 at an average cost of $8.03 per share, none of which remained in treasury at December 31, 2007 or 2006. During 2007 and 2006, no additional shares were purchased. The Company intends to acquire shares from time to time at prevailing market prices if and to the extent it deems it advisable to do so based on its assessment of corporate cash flow, market conditions and other factors.

At December 31, 2007, we had a total of $27,986 of debt outstanding, as compared to no debt outstanding at December 31, 2006.

19

On April 30, 2007, the Company, and its principal bank entered into a Loan Agreement (the “European Loan Agreement”) providing for an unsecured term loan of $10,244 (the “European Term Loan”), the proceeds of which were used to fund the Akzo Nobel Acquisition (see Note 5) and initial working capital requirements. The European Term Loan is payable in equal monthly installments of principal, each equal to 1/84th of the principal of the European Term Loan, together with accrued interest, with remaining principal and interest payable at maturity. The European Term Loan has a maturity date of May 1, 2010 and is subject to a monthly interest rate equal to EURIBOR plus 1%. At December 31, 2007, this interest rate was 5.288%. The European Loan Agreement also provides for a short-term revolving credit facility of €2,000, translated to $2,946 as of December 31, 2007 (the "European Revolving Facility"). The European Revolving Facility is subject to a monthly interest rate equal to EURIBOR plus 1.25%, and accrued interest is payable monthly. The Company has drawn down €1,500 of the European Revolving Facility as of December 31, 2007. The European Revolving Facility has a maturity date of May 1, 2008. Management believes that such facility will be renewed in the normal course of business.

On March 16, 2007, the Company and its principal bank entered into a Loan Agreement (the “New Loan Agreement”) providing for an unsecured term loan of $29,000 (the “New Term Loan”), the proceeds of which were used to fund the Chinook Acquisition (see Note 5). The New Term Loan is payable in equal monthly installments of principal, each equal to 1/60th of the principal of the New Term Loan, together with accrued interest, with remaining principal and interest payable at maturity. The New Term Loan has a maturity date of March 16, 2010 and is subject to a monthly interest rate equal to LIBOR plus 1%. At December 31, 2007, this interest rate was 6.027%. As of December 31, 2007, the Company has prepaid $10,000 of the New Term Loan. The New Loan Agreement also provides for a short-term revolving credit facility of $6,000 (the "New Revolving Facility"). The New Revolving Facility is subject to a monthly interest rate equal to LIBOR plus 1%, and accrued interest is payable monthly. The Company has drawn down $1,000 of the New Revolving Facility as of December 31, 2007. The New Revolving Facility has a maturity date of May 31, 2009. Management believes that such facility will be renewed in the normal course of business.

Proceeds from stock options exercised totaled $1,217 and $1,239 for 2007 and 2006, respectively. Dividend payments were $1,596 and $1,045 for 2007 and 2006, respectively.

Other Matters Impacting Liquidity

The Company currently provides postretirement benefits in the form of a retirement medical plan under a collective bargaining agreement covering eligible retired employees of its Verona, Missouri facility. The amount recorded on the Company’s balance sheet as of December 31, 2007 for this obligation is $805. The postretirement plan is not funded. Historical cash payments made under such plan have approximated $50 per year.

Critical Accounting Policies

Management of the Company is required to make certain estimates and assumptions during the preparation of consolidated financial statements in accordance with accounting principles generally accepted in the United States of America. These estimates and assumptions impact the reported amount of assets and liabilities and disclosures of contingent assets and liabilities as of the date of the consolidated financial statements. Estimates and assumptions are reviewed periodically and the effects of revisions are reflected in the consolidated financial statements in the period they are determined to be necessary. Actual results could differ from those estimates.

The Company’s "critical accounting policies" are those that require application of management's most difficult, subjective or complex judgments, often as a result of the need to make estimates about the effect of matters that are inherently uncertain and that may change in subsequent periods. Management considers the following accounting policies to be critical.

20

Revenue Recognition

Revenue is recognized upon product shipment, passage of title and risk of loss, and when collection is reasonably assured. The Company reports amounts billed to customers related to shipping and handling as revenue and includes costs incurred for shipping and handling in cost of sales. Amounts received for unshipped merchandise are not recognized as revenue but rather they are recorded as customer deposits and are included in current liabilities. In addition, the Company follows the provisions of the Securities and Exchange Commission’s (SEC) Staff Accounting Bulletin (SAB) No. 104, “Revenue Recognition,” which sets forth guidelines on the timing of revenue recognition based upon factors such as passage of title, installation, payments and customer acceptance.