UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| ☑ | ANNUAL REPORT PURSUANT TO SECTION 13 OR SECTION 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2014

OR

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from _______ to _____ .

Commission file number: 1-13648

Balchem Corporation

(Exact name of Registrant as specified in its charter)

| Maryland | 13-2578432 | |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification Number) |

52 Sunrise Park Road, New Hampton, NY 10958

(Address of principal executive offices) (Zip Code)

Registrant’s telephone number, including area code: (845) 326-5600

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Name of each exchange on which registered | |

| Common Stock, par value $.06-2/3 per share | Nasdaq Global Market |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark whether the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☑ No ☐

Indicate by check mark whether the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☑

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☑ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes ☑ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☑

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| (Check one): | Large accelerated filer ☑ | Accelerated filer ☐ |

Non-accelerated filer ☐ | Smaller reporting company o |

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes ☐ No ☑

The aggregate market value of the common stock, par value $.06-2/3 per share (the “Common Stock”), issued and outstanding and held by non-affiliates of the Registrant, based upon the closing price for the Common Stock on the NASDAQ Global Market on June 30, 2014 was approximately $1,610,000,000. For purposes of this calculation, shares of the Registrant held by directors and officers of the Registrant and under the Registrant's 401(k)/profit sharing plan have been excluded.

The number of shares outstanding of the Registrant's Common Stock was 30,945,086 as of February 20, 2015.

DOCUMENTS INCORPORATED BY REFERENCE

Selected portions of the Registrant’s proxy statement for its 2015 Annual Meeting of Stockholders (the “2015 Proxy Statement”) to be filed with the Securities and Exchange Commission pursuant to Regulation 14A within 120 days after Registrant’s fiscal year-end of December 31, 2014 are incorporated by reference in Part III of this Annual Report on Form 10-K to the extent states therein.

Cautionary Statement Regarding Forward-Looking Statements

This Annual Report on Form 10-K contains “forward-looking statements” within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended. Forward-looking statements are not statements of historical facts, but rather reflect our current expectations or beliefs concerning future events and results. We generally use the words “believes,” “expects,” “intends,” “plans,” “anticipates,” “likely,” “will,” “estimates,” “project” and similar expressions to identify forward-looking statements. Such forward-looking statements, including those concerning our expectations, involve risks, uncertainties and other factors, some of which are beyond our control, which may cause our actual results, performance or achievements, or industry results, to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements. The risks, uncertainties and factors that could cause our results to differ materially from our expectations and beliefs include, but are not limited to, those factors set forth in this Annual Report on Form 10-K under “Item 1A. - Risk Factors” below, including the following:

| · | changes in laws or regulations affecting our operations; |

| · | changes in our business tactics or strategies; |

| · | acquisitions of new or complementary operations; |

| · | sales of any of our existing operations; |

| · | changing market forces or contingencies that necessitate, in our judgment, changes in our plans, strategy or tactics; and |

| · | fluctuations in the investment markets or interest rates, which might materially affect our operations or financial condition. |

We cannot assure you that the expectations or beliefs reflected in these forward-looking statements will prove correct. We undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. You are cautioned not to unduly rely on such forward-looking statements when evaluating the information presented in this Annual Report on Form 10-K and all subsequent written and oral forward-looking statements made by us or persons acting on our behalf are expressly qualified in their entirety by the cautionary statements contained herein.

PART I

| Item1. | Business |

General:

Balchem Corporation (“Balchem,” the “Company,” “we” or “us”), incorporated in the State of Maryland in 1967, is engaged in the development, manufacture and marketing of specialty performance ingredients and products for the food, nutritional, feed, pharmaceutical and medical sterilization industries. Our reportable segments are strategic businesses that offer products and services to different markets. We presently have three reportable segments: SensoryEffects; Animal Nutrition & Health; and Specialty Products.

The Company sells its products through its own sales force, independent distributors and sales agents. Financial information concerning the Company's business, business segments and geographic information appears in Management’s Discussion and Analysis of Financial Condition and Results of Operations under Item 7 below and in the Notes to our Consolidated Financial Statements included under Item 8 below, which information is incorporated herein by reference.

The Company operates three domestic subsidiaries which are wholly-owned: Performance Chemicals and Ingredients Company (d/b/a/ SensoryEffects) (“PCI”), a Delaware corporation, BCP

1

Ingredients, Inc. (“BCP”), a Delaware corporation, and Aberco, Inc. (“Aberco”), a Maryland corporation. We also operate two wholly-owned subsidiaries in Europe: Balchem BV, a Dutch limited liability company, and Balchem Italia Srl, an Italian limited liability company. Unless otherwise stated to the contrary, or unless the context otherwise requires, references to the Company in this report includes Balchem Corporation and its subsidiaries.

SensoryEffects (formerly Food, Pharma & Nutrition (“FPN”))

On May 7, 2014, the Company acquired 100 percent (100%) of the outstanding common shares of Performance Chemicals & Ingredients Company (d/b/a SensoryEffects), a privately held supplier of customized food and ingredient systems, headquartered in St. Louis, Missouri (the “Acquisition”). The Company made payments of approximately $569 million on the purchase date, amounting to $494 million to the former shareholders, including adjustments for working capital acquired and $75 million to SensoryEffects’ lenders to pay off all SensoryEffects bank debt. SensoryEffects is a leader in powder, solid and liquid flavor systems, creamer and specialty emulsified powders, cereal-based products and other functional ingredient food and beverage delivery systems. SensoryEffects was merged with the Company’s Food, Pharma & Nutrition segment (“FPN”) and the segment was renamed “SensoryEffects.” FPN continues to provide microencapsulation solutions to a variety of applications in food, pharmaceutical and nutritional ingredients to enhance performance of nutritional fortification, processing and packaging applications and shelf-life for applications in baked, refrigerated and frozen dough, processed meats, seasoning blends, confections, and nutritional supplements. We also produce and market human grade choline for wellness applications. Choline has a key role in the development and structural integrity of brain cell membranes in infants, processing dietary fat, reproductive development and neural functions, such as memory and muscle function.

Animal Nutrition & Health

Our Animal Nutrition & Health (“ANH”) segment provides nutritional products derived from our microencapsulation and chelation technologies in addition to basic choline chloride. For ruminant animals, our microencapsulated products boosts health and milk production, delivering nutrient supplements that are biologically available, providing required nutritional levels. Our proprietary chelation technology, our KEYSHURE® line products, provides enhanced nutrient absorption for various species of production and companion animals and is marketed for use in animal feed throughout the world. ANH also manufactures and supplies choline chloride, an essential nutrient for monogastric animal health, predominantly to the poultry, pet and swine industries. Choline, which is manufactured and sold in both dry and aqueous forms, plays a vital role in the metabolism of fat. Choline deficiency can result in reduced growth and perosis in poultry; fatty liver, kidney necrosis and general poor health conditions in swine. Certain derivatives of choline chloride are also manufactured and sold into industrial applications predominately as a component for hydraulic fracturing of shale natural gas wells. The ANH segment also includes the manufacture and sale of methylamines. Methylamines are a primary building block for the manufacture of choline products and are also produced at our Italian operation and sold for a wide range of industrial applications in Europe.

Specialty Products

Our Specialty Products segment operates commercially as ARC Specialty Products.

Ethylene oxide, at the 100% level, is sold as a sterilant gas, primarily for use in the health care industry. It is used to sterilize a wide range of medical devices because of its versatility and effectiveness in treating hard or soft surfaces, composites, metals, tubing and different types of plastics without negatively impacting the performance of the device being sterilized. Our 100% ethylene oxide product is distributed in uniquely designed, reusable, double-walled, stainless steel drums to assure compliance with safety, quality and environmental standards as outlined by the U.S. Environmental Protection Agency ("EPA") and the U.S. Department of Transportation (“DOT”). Our inventory of these specially built drums, along with our two filling facilities, represents a significant capital investment. Contract sterilizers and medical device

2

manufacturers are principal customers for this product. We also sell single use canisters with 100% ethylene oxide for sterilizing re-usable devices typically processed in autoclave units in hospitals. As a fumigant, ethylene oxide blends are highly effective in killing bacteria, fungi, and insects in spices and other seasoning materials.

Propylene oxide is marketed and sold as a fumigant to aid in the control of insects and microbiological spoilage; and to reduce bacterial and mold contamination on certain shell and processed nut meats, processed spices, cacao beans, cocoa powder, raisins, figs and prunes. We distribute our propylene oxide product primarily in recyclable, single-walled, carbon steel cylinders according to standards outlined by the EPA and the DOT. Our inventory of these cylinders also represents a significant capital investment. Propylene oxide is also sold to customers seeking smaller (as opposed to bulk) quantities and whose requirements include utilization in various chemical synthesis applications, such as increasing paint durability and manufacturing specialty starches and textile coatings.

Raw Materials

The raw materials utilized by the Company in the manufacture of its products are sourced from suppliers both domestically and internationally. Such raw materials include materials derived from petrochemicals, minerals, metals, agricultural commodities and other readily available commodities and are subject to price fluctuations due to market conditions. The Company is not experiencing any current difficulties in procuring such materials and does not anticipate any such problems; however, we cannot assure that will always be the case.

Intellectual Property

The Company currently holds 16 patents in the United States and overseas and uses certain trade-names and trademarks. It also uses know-how, trade secrets, formulae, and manufacturing techniques that assist in maintaining competitive positions of certain of its products. Formulae and know-how are of particular importance in the manufacture of a number of the Company’s proprietary products. The Company believes that certain of its patents, in the aggregate, are advantageous to its business. However, it is believed that no single patent or related group of patents is currently so material to the Company that the expiration or termination of any single patent or group of patents would materially affect its business. Our U.S. patents expire between 2016 and 2024. The Company believes that its sales and competitive position are dependent primarily upon the quality of its products, technical sales efforts and market conditions, rather than on patent protection.

Seasonality

In general, the businesses of our segments are not seasonal to any material extent.

Backlog

At December 31, 2014, the Company had a total backlog of $38,798,000 (including $23,703,000 for the SensoryEffects segment; $14,396,000 for the ANH segment and $699,000 for the Specialty Products segment), as compared to a total backlog of $12,496,000 at December 31, 2013 (including$2,606,000 for the SensoryEffects segment; $9,236,000 for the ANH segment and $654,000 for the Specialty Products segment). It has generally been the Company’s policy and practice to maintain an inventory of finished products and/or component materials for its segments to enable it to ship products within two months after receipt of a product order. All orders in the current backlog are expected to be filled in the 2015 fiscal year.

Competition

3

Our competitors include many large and small companies, some of which have greater financial, research and development, production and other resources than the Company. Competition in the food and ingredient markets served by the Company is based primarily on product performance, customer support, quality, service and price. The development of new and improved products is important to the Company’s success. This competitive environment requires substantial investments in product and manufacturing process research and development. In addition, the winning and retention of customer acceptance of the Company’s food and nutrition products involve substantial expenditures for application testing, either internally or at customer/prospect sites, and sales efforts. Our competition in this market includes a variety of ingredient and nutritional supplement companies many of which are privately-held. Therefore, it is difficult to assess the size of all of our segment competitors or where we rank in comparison to such privately-held competitors.

Competition in the animal feed and industrial markets served by the Company is based primarily on quality, service and price. The markets for our products are subject to competitive risks because these markets are highly price competitive. Our competition in this market includes a variety of animal nutrition and health ingredient companies, along with certain industrial companies, many of which are privately-held. Therefore, we are unable to assess the size of all of our competitors or where we rank in comparison to such privately-held competitors.

In the Specialty Products segment, the Company’s products face competition from alternative sterilizing technologies and products. Competition in this marketplace is based primarily on medical device compositions, product performance, customer support, quality, service and price. Our competition in this market includes sterilization companies, a number of which are privately-held. Therefore, we are unable to assess the size of all of our competitors or where we rank in comparison to such privately-held competitors. We do, however, conduct an informal survey which indicates that our market share is modestly growing. We are focused on the North American market due to EPA, United States Food and Drug Administration (“FDA”) and DOT regulations that are not yet required globally.

Research & Development

During the years ended December 31, 2014, 2013 and 2012, the Company incurred research and development expenses of approximately $4.8 million, $3.6 million and $3.4 million, respectively, on Company-sponsored research and development for new products and improvements to existing products and manufacturing processes. At December 31, 2014, approximately 40 employees were devoted full time to research and development activities. The Company has historically funded its research and development programs with funds available from current operations with the intent of recovering those costs from profits derived from future sales of products resulting from, or enhanced by, the research and development effort.

The Company prioritizes its product development activities in an effort to allocate resources to those product candidates that, the Company believes, have the greatest commercial potential. Factors considered by the Company in determining the products to pursue include projected markets and needs, status of its proprietary rights, technical feasibility, expected and known product attributes, and estimated costs to bring the product to market.

Capital Projects

The Company continues to invest in projects across all production facilities and capital expenditures were approximately $13.2 million, $8.2 million and $13.9 million for 2014, 2013 and 2012, respectively. In 2014, capital expenditures of $4.8 million were related to expanding the Company’s Animal Nutrition & Health capacity in the manufacturing facility located in Verona, Missouri. For 2013 and 2012, respectively, $3.3 million and $7.3 million of the capital expenditures were for the Company’s new manufacturing facility in Covington, Virginia. Capital expenditures are projected to range from $30.0 million to $40.0 million for 2015.

Environmental / Regulatory Matters

4

The Federal Insecticide, Fungicide and Rodenticide Act (“FIFRA”), a health and safety statute, requires that certain products within our specialty products segment must be registered with the EPA because they are considered pesticides. In order to obtain a registration, an applicant typically must demonstrate, through extensive test data, that its product will not cause unreasonable adverse effects on human health or the environment. We hold EPA registrations permitting us to sell ethylene oxide as a medical device sterilant and spice fumigant, and propylene oxide as a fumigant of nuts and spices.

With respect to the treatment of spices with ethylene oxide, the EPA allows the use of EO on the vast majority of spices. However, EPA prohibited its use for the treatment of basil, effective August 1, 2007, but allows the continuing use of ethylene oxide to treat all other spices, provided specific treatment parameters are used. During 2009, the EPA mandated that a toxicity study be performed on ethylene chlorohydrin, which is a “residue of concern”, according to the EPA. This study was financed by an industry trade association of which we are a member, and was submitted to the EPA in March 2012. At this time, review of this study has not been completed. When the review is completed, we anticipate the results will not negatively impact the use of ethylene oxide to treat spices.

In April 2008, the EPA issued a RED (“Reregistration Eligibility Decision”) for ethylene oxide which permitted the continued use of ethylene oxide “to sterilize medical or laboratory equipment, pharmaceuticals, and aseptic packaging, or to reduce microbial load on musical instruments, cosmetics, whole and ground spices and other seasoning materials and artifacts, archival material or library objects”. Currently, the EPA has initiated a new registration review of ethylene oxide, in line with and part of the registration review scheduled for a large number of other pesticides. A Final Work Plan was issued in March 2014, with a target date of September 2021 for final registration decision. As part of the process, EPA has identified several potential additional testing requirements. The EPA and the registrants are in discussions regarding the additional testing. While some additional testing will be necessary, we believe that the use of ethylene oxide will continue to be permitted. The product, when used as a sterilant for certain medical devices, has no known equally effective substitute. Management believes the lack of availability of this product could not be easily tolerated by various medical device manufacturers or the health care industry due to the resultant infection potential.

Similarly, the EPA issued a RED for propylene oxide in August 2006. At that time, the EPA “determined that products containing the active ingredient PPO [propylene oxide] are eligible for reregistration provided that…risk mitigation measures…are adopted.” Our product label was amended as required to reflect these mitigation measures and also to show that propylene oxide has been reclassified as a restricted use pesticide. Currently, the EPA has initiated a new registration review of propylene oxide, in line with and part of the registration review scheduled for a large number of other pesticides. A Final Work Plan was issued in March 2014. The EPA anticipates this review process will take approximately seven years. As part of the process, the EPA has identified several potential additional testing requirements. The Company has committed to conduct an additional study, and is in discussions with the EPA regarding other studies. While it is possible that we will be required to perform additional testing, we believe that the use of propylene oxide to treat nuts and spices will continue to be permitted.

The Company’s facility in Verona, Missouri, while held by a prior owner, was designated by the EPA as a Superfund site and placed on the National Priorities List in 1983, because of dioxin contamination on portions of the site. Remediation conducted by the prior owner under the oversight of the EPA and the Missouri Department of Natural Resources (“MDNR”) included removal of dioxin contaminated soil and equipment, capping of areas of residual contamination in four relatively small areas of the site separate from the manufacturing facilities, and the installation of wells to monitor groundwater and surface water for contamination for certain organic chemicals. No ground water or surface water treatment has been required. In 1998, the EPA certified the work on the contaminated soils to be complete. In February 2000, after the conclusion of two years of monitoring groundwater and surface water, the former owner submitted a draft third party risk assessment report to the EPA and MDNR recommending no further action. The prior owner is awaiting the response of the EPA and MDNR to the draft risk assessment.

5

While the Company must maintain the integrity of the capped areas in the remediation areas on the site, the prior owner is responsible for completion of any further Superfund remedy. The Company is indemnified by the sellers under its May 2001 asset purchase agreement covering its acquisition of the Verona facility for potential liabilities associated with the Superfund site and one of the sellers, in turn, has the benefit of certain contractual indemnification by the prior owner that executed the above-described Superfund remedy.

In connection with normal operations at its plant facilities, the Company is required to maintain environmental and other permits, including those relating to the ethylene oxide operations.

The Company believes it is in compliance in all material respects with federal, state, local and international provisions that have been enacted or adopted regulating the discharge of materials into the environment or otherwise relating to the protection of the environment. Such compliance includes the maintenance of required permits under air pollution regulations and compliance with requirements of the Occupational Safety and Health Administration. The cost of such compliance has not had a material effect upon the results of operations or financial condition of the Company. In 1982, the Company discovered and thereafter removed a number of buried drums containing unidentified waste material from the Company’s site in Slate Hill, New York. The Company thereafter entered into a Consent Decree to evaluate the drum site with the New York Department of Environmental Conservation (“NYDEC”) and performed a Remedial Investigation/Feasibility Study that was approved by NYDEC in February 1994. Based on NYDEC requirements, the Company remediated the area and removed soil from the drum burial site. This proceeding has been substantially completed (see Item 3).

In June 2011, we terminated our lease and ceased operations at a manufacturing facility in Channahon, Illinois, which had previously served as our pharmaceutical grade ingredient manufacturing facility, which was registered with the FDA as a drug manufacturing facility. We will continue to produce products which are required to be manufactured in conformity with current Good Manufacturing Practice (“cGMP”) regulations as interpreted and enforced by the FDA, but will do so through third party contract arrangement. Modifications, enhancements or changes in contracted manufacturing facilities or procedures relating to our pharmaceutical products are, in many circumstances, subject to FDA approval, which may be subject to a lengthy application process or which we may be unable to obtain. Any contracted manufacturing facilities that manufacture our pharmaceutical products are periodically subject to inspection by the FDA and other governmental agencies, and operations at these facilities could be interrupted or halted if the results of these inspections are unsatisfactory.

Employees

As of January 31, 2015, the Company employed approximately 845 persons. Approximately 85 employees at our Marano, Ticino, Italy facility are covered by a national collective bargaining agreement, which expires in 2015. Approximately 70 employees at the Company’s Verona, Missouri facility are covered by a collective bargaining agreement, which expires in 2017.

Available Information

The Company’s headquarters is located at 52 Sunrise Park Road, New Hampton, NY 10958. The Company’s telephone number is (845) 326-5600 and its Internet website address is www.balchem.com. The Company makes available through its website, free of charge, its Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q and Current Reports on Form 8-K, and amendments to such reports, as soon as reasonably practicable after they have been electronically filed with the Securities and Exchange Commission. Such reports are available via a link from the Investor Relations page on the Company’s website to a list of the Company’s reports on the Securities and Exchange Commission’s EDGAR website.

| Item1A. | Risk Factors |

6

Our business is subject to a high degree of risk and uncertainty, including the following risks and uncertainties, which could adversely affect our business, financial condition, results of operation, cash flows and the trading price of our Common Stock:

Global economic conditions may adversely affect our business, operating results and financial condition.

Unfavorable changes in economic conditions, including inflation, recession, or other changes in economic conditions, may adversely impact the markets in which we operate. These conditions may make it extremely difficult for our customers, our vendors and us to accurately forecast and plan future business activities, and they could cause U.S. and foreign businesses to slow spending on our products which would reduce our revenues and profitability. Furthermore, during challenging economic times our customers may face issues gaining timely access to sufficient credit, which could result in an impairment of their ability to make timely payments to us. If that were to occur, we may be required to increase our allowance for doubtful accounts and cash flow would be negatively impacted. We cannot predict the timing, depth or duration of any economic slowdown or subsequent economic recovery, worldwide, or in the markets in which we operate. Also, at any point in time we have funds in our cash accounts that are with third party financial institutions. These balances in the U.S. exceed the Federal Deposit Insurance Corporation (“FDIC”) insurance limits. While we monitor the cash balances in our accounts, these balances could be impacted if the underlying financial institutions fail or could be subject to other adverse conditions in the financial markets.

Increased competition could hurt our business and financial results.

We face competition in our markets from a number of large and small companies, some of which have greater financial, research and development, production and other resources than we do. Our competitive position is based principally on performance, quality, customer support, service, breadth of product line, manufacturing or packaging technology and the selling prices of our products. Our competitors may improve the design and performance of their products and introduce new products with competitive price and performance characteristics. We expect to do the same to maintain our current competitive position and market share.

The loss of governmental permits and approvals would materially harm some of our businesses.

Pursuant to applicable environmental and safety laws and regulations, we are required to obtain and maintain certain governmental permits and approvals, including EPA registrations under FIFRA for two of our products. We maintain EPA FIFRA registrations for ethylene oxide as a medical device sterilant and spice fumigant and for propylene oxide as a fumigant of nuts and spices. The EPA has issued Reregistration Eligibility Decisions for both products in recent years and these uses have been approved for the time being. The EPA may re-examine the registrations in the future in accordance with the provisions of FIFRA. Any future failure of the EPA to allow reregistration of ethylene oxide or propylene oxide would have a material adverse effect on our business and financial results.

Commercial supply of pharmaceutical products that we may develop, subject to cGMP manufacturing regulations, will be performed by third-party cGMP manufacturers. Modifications, enhancements or changes in third-party manufacturing facilities or procedures of our pharmaceutical products are, in many circumstances, subject to FDA approval, which may be subject to a lengthy application process or which we may be unable to obtain. Any third-party cGMP manufacturers that we may use are periodically subject to inspection by the FDA and other governmental agencies, and operations at these facilities could be interrupted or halted if the results of these inspections are unsatisfactory. Failure to comply with the FDA or other governmental regulations can result in fines, unanticipated compliance expenditures, recall or seizure of products, total or partial suspension of production, enforcement actions, injunctions and criminal prosecution, which could have a material adverse effect on our business and financial results.

7

Permits and approvals may be subject to revocation, modification or denial under certain circumstances. Our operations or activities (including the status of compliance by the prior owner of the Verona, Missouri facility under Superfund remediation) could result in administrative or private actions, revocation of required permits or licenses, or fines, penalties or damages, which could have an adverse effect on us. In addition, we cannot predict the extent to which any legislation or regulation may affect the market for our products or our cost of doing business.

Raw material shortages or price increases could adversely affect our business and financial results.

The principal raw materials that we use in the manufacture of our products can be subject to price fluctuations due to market conditions. Such raw materials include materials derived from petrochemicals, minerals, metals, agricultural commodities and other commodities. While the selling prices of our products tend to increase or decrease over time with the cost of raw materials, these changes may not occur simultaneously or to the same degree. At times, we may be unable to pass increases in raw material costs through to our customers due to certain contractual obligations. Such increases in the price of raw materials, if not offset by product price increases, or substitute raw materials, would have an adverse impact on our profitability. We believe we have reliable sources of supply for our raw materials under normal market conditions. We cannot, however, predict the likelihood or impact of any future raw material shortages. Any shortages could have a material adverse impact on our results of operations.

Our financial success depends in part on the reliability and sufficiency of our manufacturing facilities.

Our revenues depend on the effective operation of our manufacturing, packaging, and processing facilities. The operation of our facilities involves risks, including the breakdown, failure, or substandard performance of equipment, power outages, the improper installation or operation of equipment, explosions, fires, natural disasters, failure to achieve or maintain safety or quality standards, work stoppages, supply or logistical outages, and the need to comply with environmental and other directives of governmental agencies. The occurrence of material operational problems, including, but not limited to, the above events, could adversely affect our profitability during the period of such operational difficulties.

Our business exposes us to potential product liability claims and recalls, which could adversely impact our financial condition and performance.

Our development, manufacture and sales of food ingredient, pharmaceutical and nutritional supplement products involve an inherent risk of exposure to product liability claims, product recalls, product seizures and related adverse publicity. A product liability judgment against us could also result in substantial and unexpected expenditures, affect consumer confidence in our products, and divert management’s attention from other responsibilities. Although we maintain product liability insurance coverage in amounts we believe are customary within the industry, there can be no assurance that this level of coverage is adequate or that we will be able to continue to maintain our existing insurance or obtain comparable insurance at a reasonable cost, if at all. A product recall or a partially or completely uninsured judgment against us could have a material adverse effect on results of operations and financial condition.

We face risks associated with our sales to customers and manufacturing operations outside the United States.

For the year ended December 31, 2014, approximately 22% of our net sales consisted of sales outside the United States. In addition, we conduct a portion of our manufacturing outside the United States. International sales are subject to inherent risks. The majority of our foreign sales occur through our foreign subsidiaries and the remainder of our foreign sales result from exports to foreign distributors, resellers and customers. Our foreign sales and operations are subject to a number of risks, including: longer accounts

8

receivable collection periods; the impact of recessions and other economic conditions in economies outside the United States; export duties and quotas; unexpected changes in regulatory requirements; certification requirements; environmental regulations; reduced protection for intellectual property rights in some countries; potentially adverse tax consequences; political and economic instability; and preference for locally produced products. These factors could have a material adverse impact on our ability to increase or maintain our international sales.

We may, from time to time, experience problems in our labor relations.

In North America, approximately 70 employees, or 9% of our North American workforce, as of December 31, 2014, are represented by a union under a single collective bargaining agreement, which was re-negotiated and is effective as of July 9, 2012. It will expire in 2017. In Europe, approximately 85 employees are covered by a collective bargaining agreement, which was also re-negotiated in 2012 and will expire in 2015. We believe that our present labor relations with all of our union employees are satisfactory, however, our failure to renew these agreements on reasonable terms could result in labor disruptions and increased labor costs, which could adversely affect our financial performance. Similarly, if our relations with the union portion of our workforce do not remain positive, such employees could initiate a strike, work stoppage or slowdown in the future. In the event of such an action, we may not be able to adequately meet the needs of our customers using our remaining workforce and our operations and financial condition could be adversely affected.

Our international operations subject us to currency translation risk and currency transaction risk which could cause our results to fluctuate from period to period.

The financial condition and results of operations of our foreign subsidiaries are reported in Euros and then translated into U.S. dollars at the applicable currency exchange rate for inclusion in our consolidated financial statements. Exchange rates between these currencies in recent years have fluctuated and may do so in the future. Furthermore, we incur currency transaction risk whenever we enter into either a purchase or a sales transaction using a currency different than the functional currency. Given the volatility of exchange rates, we may not be able to effectively manage our currency transactions and/or translation risks. Volatility in currency exchange rates could impact our business and financial results.

Our debt instruments impose operating and financial restrictions which could have an adverse impact on our business and results of operations.

Our recent incurrence of indebtedness could have negative consequences to us, including the following:

| • | limiting our ability to borrow additional monies for our working capital, capital expenditures, acquisitions; debt service requirements or other general corporate purposes; |

| • | limiting our flexibility in planning for, or reacting to, changes in our operations, our business or the industries in which we compete; |

| • | our leverage may place us at a competitive disadvantage by limiting our ability to invest in the business or in further research and development; |

| • | making us more vulnerable to downturns in our business or the economy; and |

| • | there would be a material adverse effect on our business and financial condition if we were unable to service our indebtedness or obtain additional financing, as needed. |

Our ability to make payments on our indebtedness depends on our ability to generate cash in the future. If we do not generate sufficient cash flow to meet our debt service and working capital requirements, we may need to seek additional financing or sell assets. This may make it more difficult for us to obtain financing on terms that are acceptable to us, or at all. Without any such financing, we could be forced to sell assets to make up for any shortfall in our payment obligations under unfavorable circumstances.

9

Interest payable in accordance with our credit agreement is based on LIBOR. In light of potential fluctuations, we are exposed to risk resulting from adverse changes in interest rates.

Adverse publicity or consumer concern regarding the safety or quality of food products containing our products, or health concerns, whether with our products, products in the same general class as our products or for food products containing our products, may result in the loss of sales. Also, consumer preferences for products containing our products may change.

We are dependent upon consumers' perception of the safety, quality and possible dietary benefits of products containing our food ingredient products. As a result, substantial negative publicity concerning our products or other foods and beverages in which our products are used could lead to a loss of consumer confidence in those products, removal of those products from retailers' shelves and reduced sales and prices of our products. Product quality issues, actual or perceived, or allegations of product contamination, even when false or unfounded, could hurt the image of our products or of brands of products containing our products, and cause consumers to choose other products. Further, any product recall, whether our own or by a third party, whether due to real or unfounded allegations, could impact demand on food products containing our products or even our products. Any of these events could have a material adverse effect on our business, results of operations and financial condition. Consumer preferences, as well as trends, within the food industries change often and our failure to anticipate, identify or react to changes in these preferences and trends could, among other things, lead to reduced demand and price reductions, and could have an adverse effect on our business, results of operations and financial condition. While we continue to diversify our product offerings, developing new products entails risks and we cannot be certain that demand for our products and products containing our products will continue at current levels or increase in the future.

Demand for certain of our products is dependent on the levels of productivity by the oil and gas industry, particularly as it relates to shale gas fracturing. A substantial or an extended decline in oil and gas prices could result in lower expenditures by the oil and gas industry, which could have an adverse effect on our results of operations.

The oil and gas industry historically experiences periodic downturns. Demand for certain of our products depends on the level of expenditures by the oil and gas industry for the exploration, development and production of oil and natural gas reserves. These expenditures are generally dependent on the industry’s view of future oil and natural gas prices and are sensitive to the industry’s view of future economic growth and the resulting impact on demand for oil and natural gas. Declines in oil and gas prices could result in significant downturn in the oil and gas industry and thereby result in a reduction in demand for oilfield services and related products, which could lead to reduced demand for our products and downward pressure on the prices we charge. These effects could have an adverse effect on our results of operations and cash flows.

We may not be able to successfully consummate and manage acquisition, joint venture and divestiture activities which could have an impact on our results.

From time to time, we may acquire other businesses, enter into joint ventures and, based on an evaluation of our business portfolio, divest existing businesses. These acquisitions, joint ventures and divestitures may present financial, managerial and operational challenges, including diversion of management attention from existing businesses, difficulty with integrating or separating personnel and financial and other systems, increased expenses, assumption of unknown liabilities and indemnities, and potential disputes with the buyers or sellers. In addition, we may be required to incur asset impairment charges (including charges related to tangible asset, goodwill and other intangible assets) in connection with acquired businesses which may reduce our profitability. If we are unable to consummate such transactions, or successfully integrate and grow acquisitions and achieve contemplated revenue synergies and cost savings, our financial results could be adversely affected. Additionally, joint ventures inherently involve a lesser degree of control over business operations, thereby potentially increasing the financial, legal, operational and/or compliance risks.

10

Technology failures or cyber security breaches could have an adverse effect on the Company’s operations.

The Company relies on information technology systems to process, transmit, store, and protect electronic information. For example, a significant portion of the communications between the Company’s personnel, customers, and suppliers depends on information technology. Information technology systems of the Company may be vulnerable to a variety of interruptions due to events beyond its control including, but not limited to, natural disasters, terrorist attacks, telecommunications failures, computer viruses, hackers, and other security issues. The Company has technology and information security processes and disaster recovery plans in place to mitigate its risk to these vulnerabilities; however, these measures may not be adequate to ensure that its operations will not be disrupted, should such an event occur.

| Item1B. | Unresolved Staff Comments |

None.

| Item 2. | Properties |

We and our affiliates own or lease several manufacturing facilities and sales offices throughout the United States, and we own a single manufacturing facility in Europe. The following table sets forth a list of our principal offices, production and other facilities throughout the world as of December 31, 2014.

| Site | Leased/Owned | Sq. Footage | Products/Functions | ||||

| Corporate Offices | |||||||

| New Hampton, NY | Leased | 20,000 | Corporate headquarters | ||||

| St. Louis, MO | Leased (SensoryEffects) | 4,437 | Administrative offices SensoryEffects | ||||

| Manufacturing Facilities | |||||||

| Verona, MO | Owned (BCP) | 151,000 | aqueous and dry choline chloride, animal feed products, human choline nutrients, repackaging for Specialty Products, and warehousing | ||||

| Slate Hill, NY | Owned | 51,000 | encapsulated products, blending and repackaging for Specialty Products | ||||

| Green Pond, SC | Owned | 34,000 | repackaging for Specialty Products | ||||

| Salt Lake City, UT | Owned | 16,500 | chelated mineral nutrients, and warehousing | ||||

| Covington, VA | Owned | 70,000 | encapsulated animal feed products, and warehousing | ||||

| St. Gabriel, LA | Owned (BCP) | 15,130 | aqueous choline chloride | ||||

| Marano Ticino, Italy | Owned (Balchem Italia) | 342,734 | methylamines, metam sodium, animal, human and industrial grade choline, and warehousing | ||||

| Sleepy Eye, MN | Owned (SensoryEffects) | 32,000 | spray drying of dairy creamers and cocoa blends | ||||

| Bridgeton, MO | Owned (SensoryEffects) | 84,000 | creamer products, cocoa powders, liquid and solid flavor inclusions |

11

| Marshfield, WI | Owned (SensoryEffects) | 70,000 | spray drying of lipid based powders and blending | ||||

| Reading, PA | Owned (SensoryEffects) | 39,750 | spray drying of human nutritional products | ||||

| Defiance, OH | Owned (SensoryEffects) | 140,700 | spray drying of creamer products, solid flavor inclusions for baking and blending | ||||

| Lincoln, NE | Leased (SensoryEffects) | 87,650 | cereal products, and warehousing |

| Item 3. | Legal Proceedings |

In 1982, the Company discovered and thereafter removed a number of buried drums containing unidentified waste material from the Company’s site in Slate Hill, New York. The Company thereafter entered into a Consent Decree to evaluate the drum site with the New York Department of Environmental Conservation (“NYDEC”) and performed a Remedial Investigation/Feasibility Study that was approved by NYDEC in February 1994. Based on NYDEC requirements, the Company remediated the area and removed soil from the drum burial site. Clean-up was completed in 1996, and NYDEC required the Company to monitor the site through 1999. The Company continues to be involved in discussions with NYDEC to evaluate monitoring results and determine what, if any, additional actions will be required on the part of the Company to close out the remediation of this site. Additional actions, if any, would likely require the Company to continue monitoring the site. The cost of such monitoring has recently been less than $5,000 per year.

The Company is also involved in other legal proceedings through the normal course of business. Management believes that any unfavorable outcome related to these proceedings will not have a material effect on the Company’s financial position, results of operations or liquidity.

| Item 4. | Mine Safety Disclosures |

None.

PART II

| Item 5. | Market for the Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities |

| (a) | Market Information. |

Our Common Stock is listed on the Nasdaq Global Market under the symbol “BCPC.”

The high and low closing prices for the Common Stock as recorded for each quarterly period during the years ended December 31, 2014 and 2013 were as follows:

| Quarterly Period | High | Low | ||||||

| Ended March 31, 2014 | $ | 57.87 | $ | 49.63 | ||||

| Ended June 30, 2014 | 63.98 | 52.48 | ||||||

| Ended September 30, 2014 | 58.48 | 49.08 | ||||||

| Ended December 31, 2014 | 68.46 | 52.01 | ||||||

12

| Quarterly Period | High | Low | ||||||

| Ended March 31, 2013 | $ | 43.94 | $ | 36.07 | ||||

| Ended June 30, 2013 | 48.52 | 41.67 | ||||||

| Ended September 30, 2013 | 53.44 | 44.45 | ||||||

| Ended December 31, 2013 | 59.43 | 50.12 | ||||||

On February 20, 2015, the closing price for the Common Stock on the Nasdaq Global Market was $58.90.

| (b) | Record Holders. |

As of February 20, 2015, the approximate number of holders of record of the Company’s Common Stock was 115. Such number does not include stockholders who hold their stock in street name. As of February 20, 2015, the total number of beneficial owners of the Company's Common Stock is estimated to be approximately 21,990.

| (c) | Dividends. |

The Company declared cash dividends of $0.30 and $0.26 per share on its Common Stock during its fiscal years ended December 31, 2014 and 2013, respectively.

| (d) | Securities Authorized for Issuance Under Equity Compensation Plans. |

For information concerning prior stockholder approval of and other matters relating to our equity incentive plans, see Item 12 in this Annual Report on Form 10-K.

| (e) | Performance Graph. |

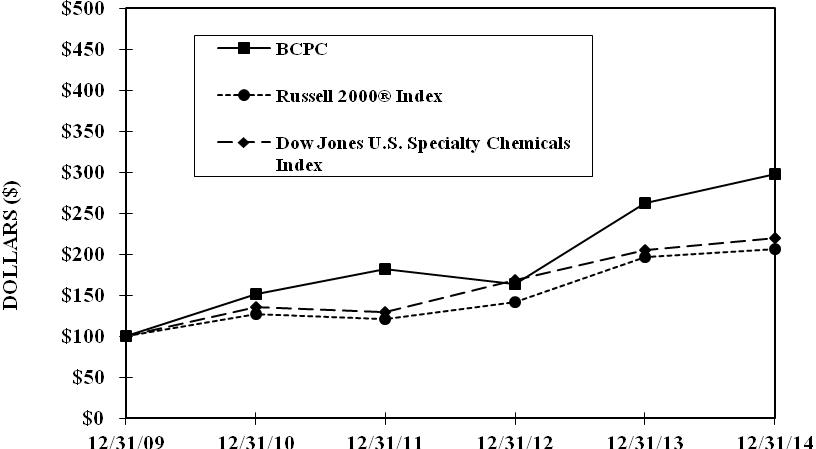

The graph below sets forth the cumulative total stockholder return on the Company's Common Stock (referred to in the table as “BCPC”) for the five years ended December 31, 2014, the overall stock market return during such period for shares comprising the Russell 2000® Index (which the Company believes includes companies with market capitalization similar to that of the Company), and the overall stock market return during such period for shares comprising the Dow Jones U.S. Specialty Chemicals Index, in each case assuming a comparable initial investment of $100 on December 31, 2009 and the subsequent reinvestment of dividends. The Russell 2000® Index measures the performance of the shares of the 2000 smallest companies included in the Russell 3000® Index. In light of the Company's industry segments, the Company does not believe that published industry-specific indices are necessarily representative of stocks comparable to the Company. Nevertheless, the Company considers the Dow Jones U.S. Specialty Chemicals Index to be potentially useful as a peer group index with respect to the Company. The performance of the Company's Common Stock shown on the graph below is historical only and not necessarily indicative of future performance.

13

| Item 6. | Selected Financial Data |

The selected statements of operations data set forth below for the three years in the period ended December 31, 2014 and the selected balance sheet data as of December 31, 2014 and 2013 have been derived from our Consolidated Financial Statements included elsewhere herein. The selected financial data as of December 31, 2012, 2011 and 2010 and for the years ended December 31, 2011 and 2010 have been derived from audited Consolidated Financial Statements not included herein, but which were previously filed with the SEC. The following information should be read in conjunction with Item 7 — “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the Consolidated Financial Statements and notes thereto included elsewhere herein.

(In thousands, except per share data)

Year ended December 31, | 2014 | 2013 | 2012 | 2011 | 2010 | |||||||||||||||

Statement of Operations Data | ||||||||||||||||||||

| Net sales | $ | 541,383 | $ | 337,173 | $ | 310,393 | $ | 291,867 | $ | 255,071 | ||||||||||

| Earnings before income tax expense | 77,052 | 65,818 | 59,844 | 56,738 | 50,131 | |||||||||||||||

| Income tax expense | 24,226 | 20,944 | 19,839 | 17,973 | 16,854 | |||||||||||||||

| Net earnings | 52,826 | 44,874 | 40,005 | 38,765 | 33,277 | |||||||||||||||

| Basic net earnings per common share | $ | 1.74 | $ | 1.51 | $ | 1.38 | $ | 1.36 | $ | 1.19 | ||||||||||

| Diluted net earnings per common share | $ | 1.69 | $ | 1.45 | $ | 1.32 | $ | 1.28 | $ | 1.12 | ||||||||||

| At December 31, | 2014 | 2013 | 2012 | 2011 | 2010 | |||||||||||||||

Balance Sheet Data | ||||||||||||||||||||

| Total assets | $ | 861,271 | $ | 376,872 | $ | 312,545 | $ | 271,717 | $ | 228,624 | ||||||||||

| Long-term debt (including current portion) | 332,500 | - | - | 1,410 | 4,914 | |||||||||||||||

| Other long-term obligations | 5,950 | 3,877 | 3,431 | 2,788 | 2,575 | |||||||||||||||

14

| Total stockholders’ equity | 391,898 | 331,358 | 273,012 | 232,009 | 187,467 | |||||||||||||||

| Dividends per common share | $ | .30 | $ | .26 | $ | .22 | $ | .18 | $ | .15 |

| Item 7. | Management's Discussion and Analysis of Financial Condition and Results of Operations |

The following discussion and analysis of our financial condition and results of operations should be read in conjunction with Item 6 — “Selected Financial Data” and our Consolidated Financial Statements and the related notes included in this report. Those statements in the following discussion that are not historical in nature should be considered to be forward-looking statements that are inherently uncertain. See “Cautionary Statement Regarding Forward-Looking Statements.”

Overview

We develop, manufacture, distribute and market specialty performance ingredients and products for the food, nutritional, pharmaceutical, animal health and medical device sterilization industries. Our three reportable segments are strategic businesses that offer products and services to different markets: SensoryEffects (formerly Food, Pharma & Nutrition); Animal Nutrition & Health; and Specialty Products.

Acquisition of Performance Chemicals & Ingredients Company (d/b/a SensoryEffects) and Long-term Debt

On May 7, 2014, the Company acquired 100 percent (the “Acquisition) of the outstanding common shares of Performance Chemicals & Ingredients Company (d/b/a SensoryEffects) a privately held supplier of customized food and ingredient systems, headquartered in St. Louis, Missouri. The Company made payments of approximately $569 million on the purchase date, amounting to $494 million to the former shareholders, including adjustments for working capital acquired and $75 million to SensoryEffects’ lenders to pay off all SensoryEffects bank debt. SensoryEffects is a leader in powder, solid and liquid flavor systems, creamer and specialty emulsified powders, cereal-based products and other functional ingredient food and beverage delivery systems. The Acquisition of SensoryEffects accelerates the Company’s growth into health and wellness markets. SensoryEffects was merged with the Company’s Food, Pharma & Nutrition segment, strengthening its market leadership position, and the segment was renamed SensoryEffects.

On May 7, 2014, the Company and a bank syndicate entered into a loan agreement providing for a senior secured term loan of $350,000 and revolving loan of $100,000 (collectively referred to as the “loans”). The term loan and $50,000 of the revolving loan were used to fund the Acquisition of SensoryEffects and for general corporate purposes. The Company has made debt payments of $67,500 related to these loans and has $100,000 available under the revolving loan.

SensoryEffects Segment

Our SensoryEffects segment supplies ingredients in the food and beverage industry; providing customized solutions in powder, solid and liquid flavor delivery systems, spray dried emulsified powder systems, and cereal systems. Our products include creamer systems, dairy replacers, powdered fats, nutritional beverage bases, beverages, juice & dairy bases, chocolate systems, ice cream bases & variegates, ready-to-eat cereals, grain based snacks, and cereal based ingredients. Additionally, we provide microencapsulation solutions to a variety of applications in food, pharmaceutical and nutritional ingredients to enhance performance of nutritional fortification, processing, mixing, and packaging applications and shelf-life. Major product applications are baked goods, refrigerated and frozen dough systems, processed meats, seasoning blends, confections, and nutritional supplements. We also produce and market human grade choline nutrient products through this segment for wellness applications. Choline is recognized to play a key role in the development and structural integrity of brain cell membranes in infants, processing dietary fat, reproductive development and neural functions, such as memory and muscle function.

Animal Nutrition & Health

15

Our Animal Nutrition & Health (“ANH”) segment provides nutritional products derived from our microencapsulation and chelation technologies in addition to basic choline chloride. For ruminant animals, our microencapsulated products boosts health and milk production, delivering nutrient supplements that are biologically available, providing required nutritional levels. Our proprietary chelation technology provides enhanced nutrient absorption for various species of production and companion animals and is marketed for use in animal feed throughout the world. ANH also manufactures and supplies choline chloride, an essential nutrient for monogastric animal health, predominantly to the poultry, pet and swine industries. Choline, which is manufactured and sold in both dry and aqueous forms, plays a vital role in the metabolism of fat. Choline deficiency can result in reduced growth and perosis in poultry; fatty liver, kidney necrosis and general poor health condition in swine. Certain derivatives of choline chloride are also manufactured and sold into industrial applications predominately as a component for hydraulic fracturing of shale natural gas wells. The ANH segment also includes the manufacture and sale of methylamines. Methylamines are a primary building block for the manufacture of choline products and are also produced at our Italian operation and sold for a wide range of industrial applications in Europe.

Sales of specialty products for the animal nutrition and health industry are highly dependent on dairy industry economics as well as the ability of the Company to leverage the results of university and field research on the animal health benefits of the Company’s products. Management believes that success in the commodity-oriented basic choline chloride marketplace is highly dependent on the Company’s ability to maintain its strong reputation for excellent product quality and customer service. The Company continues to increase production efficiencies in order to maintain its low-cost position to effectively compete in a competitive global marketplace.

Specialty Products

Our Specialty Products segment operates commercially as ARC Specialty Products.

Ethylene oxide, at the 100% level, is sold as a sterilant gas, primarily for use in the health care industry. It is used to sterilize a wide range of medical devices because of its versatility and effectiveness in treating hard or soft surfaces, composites, metals, tubing and different types of plastics without negatively impacting the performance of the device being sterilized. Our 100% ethylene oxide product is distributed in uniquely designed, recyclable, double-walled, stainless steel drums to assure compliance with safety, quality and environmental standards as outlined by the EPA and the DOT. Our inventory of these specially built drums, along with our two filling facilities, represents a significant capital investment. Contract sterilizers and medical device manufacturers are principal customers for this product. We also sell single use canisters with 100% ethylene oxide for use in sterilizing re-usable devices typically processed in autoclave units in hospitals. As a fumigant, ethylene oxide blends are highly effective in killing bacteria, fungi, and insects in spices and other seasoning materials.

Propylene oxide is marketed and sold as a fumigant to aid in the control of insects and microbiological spoilage; and to reduce bacterial and mold contamination in certain shell and processed nut meats, processed spices, cacao beans, cocoa powder, raisins, figs and prunes. We distribute our propylene oxide product primarily in recyclable, single-walled, carbon steel cylinders according to standards outlined by the EPA and the DOT. Our inventory of these cylinders also represents a significant capital investment. Propylene oxide is also sold to customers seeking smaller (as opposed to bulk) quantities and whose requirements include utilization in various chemical synthesis applications, such as increasing paint durability and manufacturing specialty starches and textile coatings.

Management believes that future success in this segment is highly dependent on the Company’s ability to maintain its government registrations, strong reputation for excellent quality, safety and customer service.

16

The Company sells products for all three segments through its own sales force, independent distributors, and sales agents.

The following tables summarize consolidated net sales by segment and business segment earnings from operations for the three years ended December 31, 2014, 2013 and 2012 (in thousands):

Business Segment Net Sales:

| 2014 | 2013 | 2012 | ||||||||||

| Specialty Products | $ | 54,053 | $ | 51,086 | $ | 49,990 | ||||||

| SensoryEffects | 206,101 | 47,569 | 44,070 | |||||||||

| Animal Nutrition & Health | 281,229 | 238,518 | 216,333 | |||||||||

| Total | $ | 541,383 | $ | 337,173 | $ | 310,393 | ||||||

Business Segment Earnings From Operations:

| 2014 | 2013 | 2012 | ||||||||||

| Specialty Products | $ | 21,316 | $ | 20,224 | $ | 20,332 | ||||||

| SensoryEffects | 21,260 | 11,233 | 11,335 | |||||||||

| Animal Nutrition & Health | 40,219 | 34,145 | 28,110 | |||||||||

| Total | $ | 82,795 | $ | 65,602 | $ | 59,777 | ||||||

Fiscal Year 2014 compared to Fiscal Year 2013

(All amounts in thousands, except share and per share data)

Net Sales

Net sales for 2014 were $541,383 as compared with $337,173 for 2013, an increase of $204,210 or 60.6%. Net sales for the SensoryEffects segment (formerly Food, Pharma & Nutrition) were $206,101, compared with $47,569, for the year ended December 31, 2014, an increase of $158,312 or 333.3%. Net sales from the recently acquired SensoryEffects business contributed $156,192 to the overall increase. The acquired Powder & Flavor Systems and Cereal Systems product lines comprised $132,971 and $17,499 of the increase, respectively. Also contributing to the higher sales was a $2,400 or 9.5% increase in encapsulated ingredients used for baking and food preservation; due to a favorable product mix and greater volume. Net sales for the Animal Nutrition & Health segment were $281,229 for 2014 compared with $238,518 for the prior year, an increase of $42,711 or 17.9%. Sales of products targeted for ruminant animal feed markets realized sales growth of 33.2% or $12,898 from the prior period. The improvement was primarily due to higher sales volumes of Aminoshure, Nitroshure and ReaShure products due to strong dairy economics, which increased demand for our products. Global feed grade choline product sales increased $6,689 or 6.1% primarily due to increased volumes of choline products sourced from our Italian operation and sold into the European and other international markets. The Company experienced Industrial sales growth of $21,961 or 26.5% over the prior year predominately due to volume increases of various choline and choline derivatives used in North America industrial applications, most notably for shale fracking. Sales for industrial applications comprised approximately 37.2% of sales in the segment, as compared to 34.7% in 2013. Specialty Products segment sales were $54,053 for 2014, as compared with $51,086 for 2013, an increase of $2,967 or 5.8%. Increased sales of ethylene oxide products used for medical device sterilization were partially offset by lower sales volumes of propylene oxide products used for industrial applications.

17

Gross Margin

Gross margin for 2014 increased to $144,172 compared to $97,241 for 2013, an increase of $46,931 or 48.2% and was principally a result of higher sales volumes. Gross margin as a percentage of sales for 2014 decreased to 26.6% from 28.9% in the prior year comparative period. Gross margins for the SensoryEffects segment declined 10.8% in 2014 as compared to 2013. The acquired product lines within the SensoryEffects segment carry a lower gross margin and the valuation of acquired inventory to fair value increased cost of sales by $4,735. Gross margin percentage for the Animal Nutrition and Health segment was 21.0%, a slight decrease compared to 2013. A heavier weighting towards choline chloride products used in industrial applications as well as increases in certain petrochemical raw material costs were offset by operating efficiencies from higher volumes. Gross margin percentage for the Specialty Products segment was flat.

Operating Expenses

Operating expenses for 2014 were $62,029 or 11.5% of net sales as compared to $31,819 or 9.4% of net sales for 2013. The increase was primarily due to the Acquisition, including increased amortization expense of $15,072 related to the acquired intangible assets, and transaction and integration expenses of $3,652. Partially offsetting the increased expenses was a $2.9 million favorable net legal settlement. During 2014 and 2013, the Company spent $4,810 and $3,622 respectively, on research and development programs, most of which pertained to the Company’s SensoryEffects and Animal Nutrition & Health segments.

Earnings From Operations

Principally as a result of the above-noted details, earnings from operations for 2014 were $82,143 as compared to $65,602 for 2013, an increase of $16,541 or 25.2%. Earnings from operations as a percentage of sales (“operating margin”) for 2014 was 15.2% declining from 19.5% in 2013 primarily due to the aforementioned amortization expense associated with acquired intangible assets, the impact of the valuation of the acquired inventory, transaction and integration expenses and product mix; partially offset by the legal settlement. Excluding the impact of amortization expenses, valuation of the acquired inventory, and transaction and integration expenses and legal settlement, the earnings from operations were $106,022 or 19.6% of sales. The Company is continuing to focus on leveraging its plant capabilities, driving efficiencies from core volume growth, broadening product applications of human and animal health specialty products into both the domestic and international markets, as well as capitalizing logistically on the Company’s varied choline production capabilities. Earnings from operations for SensoryEffects were $21,260, an increase of $10,027 or 89.3% primarily due to increased sales from the Acquisition partially offset by increased amortization expense and the impact of the valuation of acquired inventory. Earnings from operations for Animal Nutrition & Health increased by $6,074 or 17.8% to $40,219, principally due to the aforementioned higher sales. Earnings from operations for the Specialty Products segment were $21,260 an increase of $1,092 or 5.4%.

Other Expenses (Income)

Interest expense for 2014 was $5,145 and is primarily related to the loans entered into on May 7, 2014 to finance the Acquisition of SensoryEffects. Interest income was $64 and $277 for 2014 and 2013, respectively. The Company has invested available cash primarily in certificates of deposit and money market investments that have been classified as cash equivalents due to the short maturities of these investments. Other expense was $10 and $37 for 2014 and 2013, respectively and is primarily the result of unfavorable fluctuations in foreign currency exchange rates between the US Dollar (the reporting currency) and foreign functional currencies.

Income Tax Expense

18

The Company’s effective tax rate for 2014 and 2013 was 31.4% and 31.8%, respectively. The decrease in the effective tax rate is primarily attributable to certain tax credits and a purchase price reduction related to the SensoryEffects acquisition.

Net Earnings

Principally as a result of the above-noted details, net earnings were $52,826 for 2014, as compared with $44,874 for 2013, an increase of 17.7%.

Fiscal Year 2013 compared to Fiscal Year 2012

(All amounts in thousands, except share and per share data)

Net Sales

Net sales for 2013 were $337,173 as compared with $310,393 for 2012, an increase of $26,780 or 8.6%. Net sales for the Specialty Products segment were $51,086 for 2013, as compared with $49,990 for 2012, an increase of $1,096 or 2.2%. Approximately 79% of this increase in sales was from propylene oxide products for use in industrial applications and nutmeat fumigation. The balance of the increased sales is principally a result of higher sales from ethylene oxide products for use in medical device sterilization. Net sales for the SensoryEffects segment were $47,569 for 2013 compared with $44,070 for 2012, an increase of $3,499 or 7.9%. This result was primarily due to a 10.2% increase in sales in the food sector, principally due to higher volumes and product mix of encapsulated ingredients for baking and food preservation end markets. Also contributing to the higher sales was an increase in sales of 28.2% for VitaShure® products for nutritional enhancement, including sustained release amino acid products for sports performance products. Net sales of $238,518 were realized for 2013 for the Animal Nutrition & Health segment, as compared with $216,333 for the prior year, an increase of $22,185 or 10.3%. The ANH specialty ingredients, largely targeted to the ruminant and companion animal markets, realized 6.6% sales growth from the prior year comparable period. The improvement was due to higher sales of non-AminoShure® products, which were up 22.5% compared with prior year, and were led by strong volume growth of ReaShure, NitroShure and chelated minerals. This was partially offset by lower volumes of AminoShure products, related mainly to the adverse impact of the previously announced suspension of sales of AminoShure–L, 52% lysine (the “Product”) in the second quarter of 2012. Global feed grade choline product sales increased by approximately 5.1% due to modest price increases, implemented globally, to partially offset increased raw material costs. The Company experienced increased sales of various choline and choline derivative products used for industrial applications, predominantly in North America, including usage in fracking for natural gas. Industrial sales grew 20.4% over the prior year with the increase coming primarily from higher volumes for usage in fracking. Sales for industrial applications comprised approximately 34.7% of the sales in this segment for 2013.

Gross Margin

Gross margin for 2013 increased to $97,421 compared to $89,539 for 2012, an increase of 8.8%. This $7,882 increase was principally a result of higher sales volumes. Gross margin percentage for 2013 increased to 28.9% as compared to 28.8% in the prior year comparative period, primarily due to operating efficiencies from higher volumes, which were partially offset by increases in certain key raw material costs. Gross margin percentage for the Specialty Products segment increased by 0.7% primarily due to product mix and operating efficiencies from higher volumes. Gross margin percentage in the SensoryEffects segment decreased by 2.3% primarily due to higher raw material costs for human choline products. Gross margin percentage in the Animal Nutrition and Health segment increased by 0.9%, principally due to operating efficiencies from increased volumes.

Operating Expenses

19

Operating expenses for 2013 were $31,819, as compared to $29,762 for 2012, an increase of $2,057 or 6.9%. This was principally due to an increase of employee headcount and additional compensation-related expenses totaling $1,039, higher outside services and professional fees of $277 and increased advertising of $238. Operating expenses were 9.4% of sales or 0.2 percentage points less than the operating expenses as a percentage of sales in the prior year. During 2013 and 2012, the Company spent $3,622 and $3,422 respectively, on research and development programs, most of which pertained to the Company’s SensoryEffects and Animal Nutrition & Health segments.

Earnings From Operations

Principally as a result of the above-noted details, earnings from operations for 2013 were $65,602 as compared to $59,777 for 2012, an increase of $5,825 or 9.7%. Earnings from operations as a percentage of sales (“operating margin”) for 2013 increased to 19.5% from 19.3% for 2012. The Company is continuing to focus on leveraging its plant capabilities, driving efficiencies from core volume growth, broadening product applications of human and animal health specialty products into both the domestic and international markets, as well as capitalizing logistically on the Company’s varied choline production capabilities. Earnings from operations for the Specialty Products segment were $20,224, a decrease of $108 or 0.5%, primarily due to certain higher operating expenses, which were partially offset by the above-noted higher sales of propylene oxide and operating efficiencies from increased volumes. Earnings from operations for SensoryEffects were $11,233, a decrease of $102 or 0.9%, due largely to the aforementioned higher raw material costs for human choline products, which were partially offset by the previously-noted higher sales. Earnings from operations for Animal Nutrition & Health increased by $6,035 or 21.5% to $34,145, principally due to the aforementioned higher sales and operating efficiencies from increased volumes, partially offset by certain higher operating expenses.

Other Expenses (Income)

Interest income for 2013 totaled $277 as compared to $10 for 2012. The Company has invested available cash primarily in certificates of deposit and money market investments that have been classified as cash equivalents due to the short maturities of these investments. Interest expense was $24 for 2013 compared to $10 for 2012. Other expense of $37 for 2013 is primarily the result of unfavorable fluctuations in foreign currency exchange rates between the US Dollar (the reporting currency) and foreign functional currencies. Other income of $67 for 2012 is primarily the result of a favorable adjustment related to a prior year sale of a non-core calcium carbonate product line.

Income Tax Expense

The Company’s effective tax rate for 2013 and 2012 was 31.8% and 33.2%, respectively. This decrease in the effective tax rate is primarily attributable to the timing of certain tax credits and deductions.

Net Earnings

Principally as a result of the above-noted details, net earnings were $44,874 for 2013, as compared with $40,005 for 2012, an increase of 12.2%.

LIQUIDITY AND CAPITAL RESOURCES

(All amounts in thousands, except share and per share data)

Contractual Obligations

20

The Company's contractual obligations as of December 31, 2014, are summarized in the table below:

| Payments due by period | ||||||||||||||||||||

Contractual Obligations | Total | Less than 1 year | 1-3 years | 3-5 years | More than 5 years | |||||||||||||||