UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-Q

| |

☒ | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended March 31, 2024

| |

☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to .

Commission file number: 001-06615

SUPERIOR INDUSTRIES INTERNATIONAL, INC.

(Exact Name of Registrant as Specified in Its Charter)

| |

Delaware | 95-2594729 |

(State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) |

| |

26600 Telegraph Road, Suite 400 |

|

Southfield, Michigan | 48033 |

(Address of Principal Executive Offices) | (Zip Code) |

Registrant’s Telephone Number, Including Area Code: (248) 352-7300

Securities registered pursuant to Section 12(b) of the Act:

| | | | |

| | | | |

Title of Each Class | | Trading Symbol |

| Name of Each Exchange on Which Registered |

Common Stock, $0.01 par value | | SUP |

| New York Stock Exchange |

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| | | |

Large Accelerated Filer | ☐ | Accelerated Filer | ☒ |

Non-Accelerated Filer | ☐ | Smaller Reporting Company | ☒ |

|

| Emerging Growth Company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

Number of shares of common stock outstanding as of April 26, 2024: 28,600,152

TABLE OF CONTENTS

PART I

FINANCIAL INFORMATION

Item 1. Financial Statements

SUPERIOR INDUSTRIES INTERNATIONAL, INC.

CONDENSED CONSOLIDATED STATEMENTS OF INCOME (LOSS)

(Dollars in thousands, except per share amounts)

(Unaudited)

| | | | | | | | |

| | Three Months Ended | |

| | March 31,

2024 | | | March 31,

2023 | |

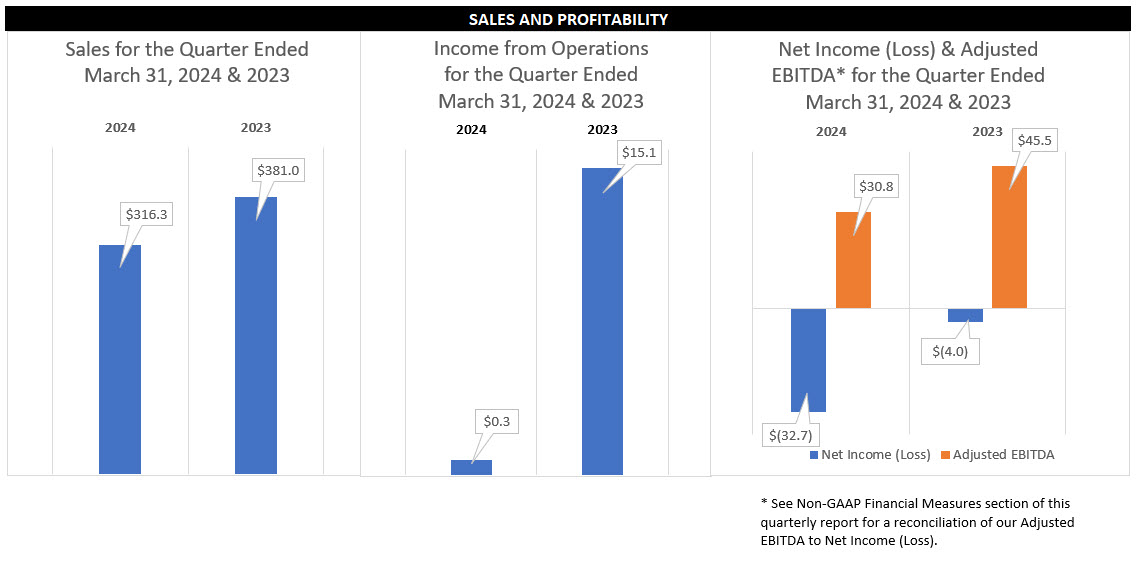

NET SALES | | $ | 316,276 | | | $ | 380,966 | |

Cost of sales | | | 295,130 | | | | 346,388 | |

GROSS PROFIT | | | 21,146 | | | | 34,578 | |

Selling, general and administrative expenses | | | 20,832 | | | | 19,442 | |

INCOME FROM OPERATIONS | | | 314 | | | | 15,136 | |

Interest expense, net | | | (15,878 | ) | | | (15,698 | ) |

Other expense, net | | | (537 | ) | | | (187 | ) |

LOSS BEFORE INCOME TAXES | | | (16,101 | ) | | | (749 | ) |

Income tax provision | | | (16,648 | ) | | | (3,298 | ) |

NET LOSS | | $ | (32,749 | ) | | $ | (4,047 | ) |

LOSS PER SHARE – BASIC | | $ | (1.52 | ) | | $ | (0.49 | ) |

LOSS PER SHARE – DILUTED | | $ | (1.52 | ) | | $ | (0.49 | ) |

The accompanying unaudited notes are an integral part of these condensed consolidated financial statements.

SUPERIOR INDUSTRIES INTERNATIONAL, INC.

CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME (LOSS)

(Dollars in thousands)

(Unaudited)

| | | | | | | | |

| | Three Months Ended | |

| | March 31,

2024 | | | March 31,

2023 | |

Net loss | | $ | (32,749 | ) | | $ | (4,047 | ) |

Other comprehensive income (loss), net of tax: | | | | | | |

Foreign currency translation gain | | | 2,499 | | | | 14,631 | |

Change in unrecognized gains on derivative instruments: | | | | | | |

Change in fair value of derivatives | | | 3,466 | | | | 19,453 | |

Tax provision | | | (772 | ) | | | (1,333 | ) |

Change in unrecognized gains on derivative instruments, net of tax | | | 2,694 | | | | 18,120 | |

Defined benefit pension plan: | | | | | | |

Amortization of actuarial losses on pension obligation | | | — | | | | — | |

Tax benefit | | | 178 | | | | — | |

Pension changes, net of tax | | | 178 | | | | — | |

Other comprehensive income, net of tax | | | 5,371 | | | | 32,751 | |

Comprehensive (loss) income | | $ | (27,378 | ) | | $ | 28,704 | |

The accompanying unaudited notes are an integral part of these condensed consolidated financial statements.

SUPERIOR INDUSTRIES INTERNATIONAL, INC.

CONDENSED CONSOLIDATED BALANCE SHEETS

(Dollars in thousands)

(Unaudited)

| | | | | | | | |

| | March 31,

2024 | | | December 31,

2023 | |

ASSETS | | | | | | |

Current assets: | | | | | | |

Cash and cash equivalents | | $ | 191,071 | | | $ | 201,606 | |

Accounts receivable, net | | | 66,170 | | | | 56,393 | |

Inventories, net | | | 149,030 | | | | 144,609 | |

Income taxes receivable | | | 2,175 | | | | 1,559 | |

Derivative financial instruments | | | 40,598 | | | | 38,298 | |

Other current assets | | | 24,455 | | | | 17,464 | |

Total current assets | | | 473,499 | | | | 459,929 | |

Property, plant and equipment, net | | | 386,277 | | | | 398,599 | |

Deferred income tax assets, net | | | 35,106 | | | | 52,213 | |

Intangibles, net | | | 27,637 | | | | 33,242 | |

Derivative financial instruments | | | 39,670 | | | | 40,471 | |

Other noncurrent assets | | | 43,323 | | | | 46,117 | |

Total assets | | $ | 1,005,512 | | | $ | 1,030,571 | |

LIABILITIES, MEZZANINE EQUITY AND SHAREHOLDERS’ EQUITY (DEFICIT) | | | | | | |

Current liabilities: | | | | | | |

Accounts payable | | $ | 139,856 | | | $ | 124,907 | |

Short-term debt | | | 4,571 | | | | 5,322 | |

Accrued expenses | | | 65,818 | | | | 66,838 | |

Income taxes payable | | | 1,920 | | | | 1,844 | |

Total current liabilities | | | 212,165 | | | | 198,911 | |

Long-term debt (less current portion) | | | 605,046 | | | | 610,632 | |

Noncurrent income tax liabilities | | | 5,795 | | | | 8,129 | |

Deferred income tax liabilities, net | | | 1,403 | | | | 1,903 | |

Other noncurrent liabilities | | | 48,296 | | | | 47,821 | |

Commitments and contingent liabilities (Note 17) | | | — | | | | — | |

Mezzanine equity: | | | | | | |

Preferred stock, $0.01 par value | | | | | | |

Authorized – 1,000,000 shares | | | | | | |

Issued and outstanding – 150,000 shares outstanding at

March 31, 2024 and December 31, 2023 | | | 255,032 | | | | 248,222 | |

European noncontrolling redeemable equity | | | 682 | | | | 893 | |

Shareholders’ deficit: | | | | | | |

Common stock, $0.01 par value | | | | | | |

Authorized – 100,000,000 shares | | | | | | |

Issued and outstanding – 28,600,152 and 28,091,440 shares at

March 31, 2024 and December 31, 2023 | | | 115,924 | | | | 115,340 | |

Accumulated other comprehensive loss | | | (16,920 | ) | | | (22,291 | ) |

Retained earnings | | | (221,911 | ) | | | (178,989 | ) |

Total shareholders’ deficit | | | (122,907 | ) | | | (85,940 | ) |

Total liabilities, mezzanine equity and shareholders’ deficit | | $ | 1,005,512 | | | $ | 1,030,571 | |

The accompanying unaudited notes are an integral part of these condensed consolidated financial statements.

SUPERIOR INDUSTRIES INTERNATIONAL, INC.

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(Dollars in thousands)

(Unaudited)

| | | | | | | | |

| | Three Months Ended | |

| | March 31, 2024 | | | March 31, 2023 | |

CASH FLOWS FROM OPERATING ACTIVITIES: | | | | | | |

Net loss | | $ | (32,749 | ) | | $ | (4,047 | ) |

Adjustments to reconcile net income to net cash provided by operating activities: | | | | | | |

Depreciation and amortization | | | 21,946 | | | | 22,841 | |

Income tax, noncash changes | | | 16,257 | | | | 2,292 | |

Stock-based compensation | | | 1,720 | | | | 801 | |

Amortization of debt issuance costs | | | 1,170 | | | | 1,186 | |

Other noncash items | | | 2,782 | | | | 2,377 | |

Changes in operating assets and liabilities: | | | | | | |

Accounts receivable | | | (12,446 | ) | | | (13,346 | ) |

Inventories | | | (5,612 | ) | | | (7,169 | ) |

Other assets and liabilities | | | (3,107 | ) | | | 4,060 | |

Accounts payable | | | 16,305 | | | | 32,181 | |

Income taxes | | | (2,796 | ) | | | (2,438 | ) |

NET CASH PROVIDED BY OPERATING ACTIVITIES | | | 3,470 | | | | 38,738 | |

CASH FLOWS FROM INVESTING ACTIVITIES: | | | | | | |

Additions to property, plant, and equipment | | | (6,618 | ) | | | (15,589 | ) |

NET CASH USED IN INVESTING ACTIVITIES | | | (6,618 | ) | | | (15,589 | ) |

CASH FLOWS FROM FINANCING ACTIVITIES: | | | | | | |

Repayments of debt | | | (1,707 | ) | | | (2,228 | ) |

Cash dividends paid | | | (3,338 | ) | | | (3,330 | ) |

Financing costs paid and other | | | (217 | ) | | | (23 | ) |

Payments related to tax withholdings for stock-based compensation | | | (1,136 | ) | | | (3,303 | ) |

Finance lease payments | | | (150 | ) | | | (288 | ) |

NET CASH USED IN FINANCING ACTIVITIES | | | (6,548 | ) | | | (9,172 | ) |

Effect of exchange rate changes on cash | | | (839 | ) | | | 1,639 | |

Net changes in cash and cash equivalents | | | (10,535 | ) | | | 15,616 | |

Cash and cash equivalents at the beginning of the period | | | 201,606 | | | | 213,022 | |

Cash and cash equivalents at the end of the period | | $ | 191,071 | | | $ | 228,638 | |

The accompanying unaudited notes are an integral part of these condensed consolidated financial statements.

SUPERIOR INDUSTRIES INTERNATIONAL, INC.

CONDENSED CONSOLIDATED STATEMENTS OF SHAREHOLDERS’ EQUITY (DEFICIT)

(Dollars in thousands, except share amounts)

(Unaudited)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Common Stock | | | Accumulated Other Comprehensive (Loss)

Income | | | | | | | |

| | Number of

Shares | | | Amount | | | Unrecognized

Gains (Losses)

on Derivative

Instruments | | | Pension

Obligations | | | Cumulative

Translation

Adjustment | | | Retained

Earnings | | | Total | |

BALANCE AT JANUARY 1, 2024 | | | 28,091,440 | | | $ | 115,340 | | | $ | 59,859 | | | $ | 852 | | | $ | (83,002 | ) | | $ | (178,989 | ) | | $ | (85,940 | ) |

Net loss | | | — | | | | — | | | | — | | | | — | | | | — | | | | (32,749 | ) | | | (32,749 | ) |

Change in unrecognized gains on

derivative instruments, net of tax | | | — | | | | — | | | | 2,694 | | | | — | | | | — | | | | — | | | | 2,694 | |

Change in defined benefit plans, net of taxes | | | — | | | | — | | | | — | | | | 178 | | | | — | | | | — | | | | 178 | |

Net foreign currency translation adjustment | | | — | | | | — | | | | — | | | | — | | | | 2,499 | | | | — | | | | 2,499 | |

Common stock issued, net of shares

withheld for employee taxes | | | 508,712 | | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | |

Stock-based compensation | | | — | | | | 584 | | | | — | | | | — | | | | — | | | | — | | | | 584 | |

Redeemable preferred 9% dividend

and accretion | | | — | | | | — | | | | — | | | | — | | | | — | | | | (10,166 | ) | | | (10,166 | ) |

European noncontrolling redeemable equity

dividend | | | — | | | | — | | | | — | | | | — | | | | — | | | | (7 | ) | | | (7 | ) |

BALANCE AT MARCH 31, 2024 | | | 28,600,152 | | | $ | 115,924 | | | $ | 62,553 | | | $ | 1,030 | | | $ | (80,503 | ) | | $ | (221,911 | ) | | $ | (122,907 | ) |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Common Stock | | | Accumulated Other Comprehensive (Loss)

Income | | | | | | | |

| | Number of

Shares | | | Amount | | | Unrecognized

Gains (Losses)

on Derivative

Instruments | | | Pension

Obligations | | | Cumulative

Translation

Adjustment | | | Retained

Earnings | | | Total | |

BALANCE AT JANUARY 1, 2023 | | | 27,016,125 | | | $ | 111,105 | | | $ | 19,844 | | | $ | 1,591 | | | $ | (110,704 | ) | | $ | (47,133 | ) | | $ | (25,297 | ) |

Net loss | | | — | | | | — | | | | — | | | | — | | | | — | | | | (4,047 | ) | | | (4,047 | ) |

Change in unrecognized gains (losses) on

derivative instruments, net of tax | | | — | | | | — | | | | 18,120 | | | | — | | | | — | | | | — | | | | 18,120 | |

Change in defined benefit plans, net of taxes | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | |

Net foreign currency translation adjustment | | | — | | | | — | | | | — | | | | — | | | | 14,631 | | | | — | | | | 14,631 | |

Common stock issued, net of shares

withheld for employee taxes | | | 892,544 | | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | |

Stock-based compensation | | | — | | | | (2,502 | ) | | | — | | | | — | | | | — | | | | — | | | | (2,502 | ) |

Redeemable preferred 9% dividend

and accretion | | | — | | | | — | | | | — | | | | — | | | | — | | | | (9,440 | ) | | | (9,440 | ) |

European noncontrolling redeemable equity

dividend | | | — | | | | — | | | | — | | | | — | | | | — | | | | (10 | ) | | | (10 | ) |

BALANCE AT MARCH 31, 2023 | | | 27,908,669 | | | $ | 108,603 | | | $ | 37,964 | | | $ | 1,591 | | | $ | (96,073 | ) | | $ | (60,630 | ) | | $ | (8,545 | ) |

| | | | | | | | | | | | | | | | | | | | | |

The accompanying unaudited notes are an integral part of these condensed consolidated financial statements.

Superior Industries International, Inc.

Notes to Condensed Consolidated Financial Statements

March 31, 2024

(Unaudited)

NOTE 1 – NATURE OF OPERATIONS AND PRESENTATION OF CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

Nature of Operations

The principal business of Superior Industries International, Inc. (referred herein as the “Company,” “Superior,” or “we” and “our”) is the design and manufacture of aluminum wheels for sale to original equipment manufacturers (“OEMs”) in North America and Europe and to the aftermarket in Europe. We employ approximately 6,800 full-time employees, operating in seven manufacturing facilities in North America and Europe. We are one of the largest aluminum wheel suppliers to global OEMs and one of the leading European aluminum wheel aftermarket manufacturers and suppliers. Our OEM aluminum wheels accounted for approximately 92 percent of our sales in the first three months of 2024 and are primarily sold for factory installation on vehicle models manufactured by BMW (including Mini), Ford, GM, Honda, Jaguar-Land Rover, Lucid Motors, Mazda, Mitsubishi, Nissan, Peugeot, Renault, Stellantis, Subaru, Suzuki, Toyota, VW Group (Volkswagen, Audi, Skoda and Porsche) and Volvo. We sell aluminum wheels to the European aftermarket under the brands ATS, RIAL, ALUTEC and ANZIO. North America and Europe represent the principal markets for our products, but we have a diversified global customer base consisting of North American, European and Asian OEMs. We have determined that our North American and European operations should be treated as separate reportable segments as further described in Note 5, “Business Segments.”

Presentation of Condensed Consolidated Financial Statements

The accompanying unaudited condensed consolidated financial statements have been prepared in conformity with U.S. Generally Accepted Accounting Principles (“GAAP”) pursuant to the rules and regulations of the Securities and Exchange Commission (the “SEC”) for interim financial information. Accordingly, they do not include all the information and notes required by U.S. GAAP for complete financial statements. These unaudited condensed consolidated financial statements, in our opinion, include all adjustments, of a normal and recurring nature, which are necessary for fair presentation of the financial statements. This Quarterly Report on Form 10-Q should be read in conjunction with our consolidated financial statements and notes thereto filed with the SEC in our 2023 Annual Report on Form 10-K.

These unaudited condensed consolidated financial statements include the accounts of the Company and its subsidiaries. All intercompany transactions are eliminated in consolidation.

Interim financial reporting standards require us to make estimates that are based on assumptions regarding the outcome of future events and circumstances not known at that time. Inevitably, some assumptions will not materialize, unanticipated events or circumstances may occur which vary from those estimates and such variations may significantly affect our future results. Additionally, interim results may not be indicative of our results for future interim periods or our annual results.

Cash Paid for Interest and Taxes and Noncash Investing Activities

Cash paid for interest was $12.2 million and $11.9 million for the three months ended March 31, 2024 and March 31, 2023, respectively. Net cash paid for income taxes was $3.2 million and $3.5 million for the three months ended March 31, 2024 and March 31, 2023, respectively. As of March 31, 2024 and March 31, 2023, $3.4 million and $2.9 million, respectively, of equipment had been purchased but not yet paid and was included in accounts payable in our condensed consolidated balance sheets.

Accounting Standards Issued But Not Yet Adopted

Accounting Standards Update (ASU) 2023-07, “Segment Reporting.” In November 2023, the FASB issued ASU 2023-07, “Segment Reporting (Topic 280): Improvements to Reportable Segment Disclosures,” which is intended to improve reportable segment disclosure requirements, primarily through enhanced disclosures about significant segment expenses, allowing financial statement users to better understand the components of a segment's profit or loss to assess potential future cash flows for each reportable segment and the entity as a whole. The amendments expand a public entity's segment disclosures by requiring disclosure of significant segment expenses that are regularly provided to the chief operating decision maker (“CODM”), clarifying when an entity may report one or more additional measures to assess segment performance, requiring enhanced interim disclosures, providing new disclosure requirements for entities with a single reportable segment, and requiring other new disclosures. The amendments are effective for fiscal years beginning after December 15, 2023, and interim periods within fiscal years beginning after December 15, 2024, and early adoption is permitted. The Company is currently evaluating the impact of adopting this guidance.

Accounting Standards Update (ASU) 2023-09, “Income Taxes (Topic 740).” In December 2023, the FASB issued ASU 2023-09, “Income Taxes (Topic 740): Improvements to Income Tax Disclosures,” which is intended to enhance the transparency, decision

usefulness and effectiveness of income tax disclosures. The amendments in this ASU require a public entity to disclose a tabular tax rate reconciliation, using both percentages and currency, with specific categories. A public entity is also required to provide a qualitative description of the states and local jurisdictions that make up the majority of the effect of the state and local income tax category and the net amount of income taxes paid, disaggregated by federal, state and foreign taxes and also disaggregated by individual jurisdictions. The amendments are effective prospectively for annual periods beginning after December 15, 2024, and early adoption and retrospective application are permitted. The Company is currently evaluating the impact of adopting this guidance.

NOTE 2 – REVENUE

The Company disaggregates revenue from contracts with customers into our reportable segments, North America and Europe. Revenues by segment for the three-month periods ended March 31, 2024 and March 31, 2023, respectively, are summarized in Note 5, “Business Segments.”

The opening and closing balances of the Company’s customer receivables and current and long-term contract liabilities balances are as follows:

| | | | | | | | | | | | |

| | March 31,

2024 | | | December 31,

2023 | | | Change | |

(Dollars in thousands) | | | | | | | | | |

Customer receivables | | $ | 53,907 | | | $ | 41,879 | | | $ | 12,028 | |

Contract liabilities—current | | | 1,680 | | | | 2,982 | | | | (1,302 | ) |

Contract liabilities—noncurrent | | | 10,623 | | | | 8,530 | | | | 2,093 | |

NOTE 3 – FAIR VALUE MEASUREMENTS

The Company applies fair value accounting for all financial assets and liabilities and nonfinancial assets and liabilities that are recognized or disclosed at fair value in the financial statements on a recurring basis, while other assets and liabilities are measured at fair value on a nonrecurring basis, such as an asset impairment. Fair value is estimated by applying the following hierarchy, which prioritizes the inputs used to measure fair value into three levels and bases the categorization within the hierarchy upon the lowest level of input that is available and significant to the fair value measurement:

Level 1 - Quoted prices in active markets for identical assets or liabilities.

Level 2 - Observable inputs other than quoted prices in active markets for identical assets and liabilities, quoted prices for identical or similar assets or liabilities in inactive markets, or other inputs that are observable or can be corroborated by observable market data for substantially the full term of the assets or liabilities.

Level 3 - Inputs that are generally unobservable and typically reflect management’s estimate of assumptions that market participants would use in pricing the asset or liability.

The carrying amounts for cash and cash equivalents, accounts receivable, accounts payable and accrued expenses approximate their fair values due to the short period of time until maturity.

Derivative Financial Instruments

Our derivatives are over-the-counter customized derivative instruments and are not exchange traded. We estimate the fair value of these instruments using the income valuation approach. Under this approach, we project future cash flows and discount the future amounts to a present value using market-based expectations for interest rates, foreign exchange rates, commodity prices and the contractual terms of the derivative instruments. The discount rate used is the relevant benchmark rate (e.g., the secured overnight financing rate, “SOFR”) plus an adjustment for counterparty risk.

The following tables categorize items measured at fair value as of March 31, 2024 and December 31, 2023:

| | | | | | | | | | | | | | | | |

| | | | | Fair Value Measurement at Reporting Date Using | |

March 31, 2024 | | | | | Quoted Prices in

Active Markets

for Identical

Assets (Level 1) | | | Significant

Other

Observable

Inputs (Level 2) | | | Significant

Unobservable

Inputs

(Level 3) | |

(Dollars in thousands) | | | | | | | | | | | | |

Assets | | | | | | | | | | | | |

Derivative contracts | | $ | 80,268 | | | $ | — | | | $ | 80,268 | | | $ | — | |

Total | | $ | 80,268 | | | $ | — | | | $ | 80,268 | | | $ | — | |

Liabilities | | | | | | | | . | | | | |

Derivative contracts | | $ | 3,723 | | | $ | — | | | $ | 3,723 | | | $ | — | |

Total | | $ | 3,723 | | | $ | — | | | $ | 3,723 | | | $ | — | |

| | | | | | | | | | | | | | | | |

| | | | | Fair Value Measurement at Reporting Date Using | |

December 31, 2023 | | | | | Quoted Prices in

Active Markets

for Identical Assets (Level 1) | | | Significant

Other

Observable

Inputs (Level 2) | | | Significant

Unobservable

Inputs

(Level 3) | |

(Dollars in thousands) | | | | | | | | | | | | |

Assets | | | | | | | | | | | | |

Derivative contracts | | $ | 78,769 | | | $ | — | | | $ | 78,769 | | | $ | — | |

Total | | $ | 78,769 | | | $ | — | | | $ | 78,769 | | | $ | — | |

Liabilities | | | | | | | | . | | | | |

Derivative contracts | | $ | 4,836 | | | $ | — | | | $ | 4,836 | | | $ | — | |

Total | | $ | 4,836 | | | $ | — | | | $ | 4,836 | | | $ | — | |

Debt Instruments

The carrying values of the Company’s debt instruments vary from their fair values. The fair values were determined by reference to transacted prices and quotes for these instruments (Level 2). The estimated fair value, as well as the carrying value, of the Company’s debt instruments are shown below:

| | | | | | | | |

| | March 31,

2024 | | | December 31,

2023 | |

(Dollars in thousands) | | | | | | |

Estimated aggregate fair value | | $ | 629,227 | | | $ | 627,008 | |

Aggregate carrying value (1) | | | 630,201 | | | | 637,509 | |

(1)Total debt excluding the impact of unamortized debt issuance costs.

NOTE 4 - DERIVATIVE FINANCIAL INSTRUMENTS

We use derivatives to partially offset our exposure to foreign currency, interest rate, aluminum and other commodity price risks. We may enter into forward contracts, option contracts, swaps, collars or other derivative instruments to offset some of the risk on expected future cash flows and on certain existing assets and liabilities. However, we may choose not to hedge certain exposures for a variety of reasons including, but not limited to, accounting considerations and the prohibitive economic cost of hedging particular exposures. There can be no assurance the hedges will fully offset the financial impact resulting from movements in foreign currency exchange rates, interest rates, and aluminum or other commodity prices.

To help mitigate gross margin and cash flow fluctuations due to changes in foreign currency exchange rates, certain of our subsidiaries, whose functional currency is the U.S. dollar or the Euro, hedge a portion of their forecasted foreign currency costs denominated in the Mexican Peso and Polish Zloty, respectively. We may hedge portions of our forecasted foreign currency exposure up to 48 months.

We account for our derivative instruments as either assets or liabilities and adjust them to fair value each period. For derivative instruments that hedge the exposure to variability in expected future cash flows and are designated as cash flow hedges, the gain or loss on the derivative instrument is recorded in accumulated other comprehensive income (“AOCI”) or loss in shareholders’ equity or deficit until the hedged item is recognized in earnings, at which point accumulated gains or losses are recognized in earnings and classified with the underlying hedged transactions. Derivatives that do not qualify or have not been designated as hedges are adjusted to fair value through earnings in the financial statement line item to which the derivative relates.

The following tables display the fair value of derivatives by balance sheet line item at March 31, 2024 and December 31, 2023:

| | | | | | | | | | | | | | | | |

| | March 31, 2024 | |

| | Derivative Financial Instruments (Current Asset) | | | Derivative Financial Instruments (Noncurrent Asset) | | | Accrued

Liabilities | | | Other

Noncurrent

Liabilities | |

(Dollars in thousands) | | | | | | | | | | | | |

Foreign exchange forward contracts designated as

hedging instruments | | $ | 36,021 | | | $ | 38,573 | | | $ | 332 | | | $ | 168 | |

Foreign exchange forward contracts not

designated as hedging instruments | | | 713 | | | | — | | | | 118 | | | | — | |

Aluminum forward contracts designated as

hedging instruments | | | 165 | | | | — | | | | — | | | | — | |

Natural gas forward contracts designated as

hedging instruments | | | 192 | | | | 71 | | | | 2,371 | | | | 734 | |

Interest rate swap contracts designated as hedging

instruments | | | 3,507 | | | | 1,026 | | | | — | | | | — | |

Total derivative financial instruments | | $ | 40,598 | | | $ | 39,670 | | | $ | 2,821 | | | $ | 902 | |

| | | | | | | | | | | | | | | | |

| | December 31, 2023 | |

| | Derivative Financial Instruments (Current Asset) | | | Derivative Financial Instruments (Noncurrent Asset) | | | Accrued

Liabilities | | | Other

Noncurrent

Liabilities | |

(Dollars in thousands) | | | | | | | | | | | | |

Foreign exchange forward contracts designated as

hedging instruments | | $ | 33,075 | | | $ | 39,902 | | | $ | 440 | | | $ | 596 | |

Foreign exchange forward contracts not

designated as hedging instruments | | | 1,512 | | | | — | | | | 677 | | | | — | |

Aluminum forward contracts designated as

hedging instruments | | | 366 | | | | — | | | | 36 | | | | — | |

Natural gas forward contracts designated as

hedging instruments | | | 183 | | | | 115 | | | | 2,358 | | | | 729 | |

Interest rate swap contracts designated as hedging

instruments | | | 3,162 | | | | 454 | | | | — | | | | — | |

Total derivative financial instruments | | $ | 38,298 | | | $ | 40,471 | | | $ | 3,511 | | | $ | 1,325 | |

The following table summarizes the notional amount and estimated fair value of our derivative financial instruments:

| | | | | | | | | | | | | | | | |

| | March 31, 2024 | | | December 31, 2023 | |

| | Notional

U.S. Dollar

Amount | | | Fair

Value | | | Notional

U.S. Dollar

Amount | | | Fair

Value | |

(Dollars in thousands) | | | | | | | | | | | | |

Foreign exchange forward contracts designated as

hedging instruments | | $ | 382,274 | | | $ | 74,094 | | | $ | 432,529 | | | $ | 71,941 | |

Foreign exchange forward contracts not designated

as hedging instruments | | | 35,690 | | | | 595 | | | | 34,764 | | | | 835 | |

Aluminum forward contracts designated as

hedging instruments | | | 7,092 | | | | 165 | | | | 15,751 | | | | 330 | |

Natural gas forward contracts designated as hedging

instruments | | | 12,741 | | | | (2,842 | ) | | | 11,262 | | | | (2,789 | ) |

Interest rate swap contracts designated as hedging

instruments | | | 200,000 | | | | 4,533 | | | | 200,000 | | | | 3,616 | |

Total derivative financial instruments | | $ | 637,797 | | | $ | 76,545 | | | $ | 694,306 | | | $ | 73,933 | |

Notional amounts are presented on a net basis. The notional amounts of the derivative financial instruments do not represent amounts exchanged by the parties and, therefore, are not a direct measure of our exposure to the financial risks described above. The amounts exchanged are calculated by reference to the notional amounts and by other terms of the derivatives, such as interest rates, foreign currency exchange rates or commodity prices.

The following tables summarize the gain or loss recognized in AOCI, the amounts reclassified from AOCI into earnings and the amounts recognized directly into earnings for the three months ended March 31, 2024 and March 31, 2023:

| | | | | | | | | | | | |

Three Months Ended March 31, 2024 | | Amount of Gain or

(Loss) Recognized in

AOCI on Derivatives | |

| Amount of Pre-tax

Gain or (Loss) Reclassified

from AOCI into Income | | | Amount of Pre-tax

Gain or (Loss)

Recognized in Income

on Derivatives | |

(Dollars in thousands) | | | | | | | | | |

Derivative contracts | | $ | 2,694 | | | $ | 9,177 | | | $ | 225 | |

| | | | | | | | | | | | |

Three Months Ended March 31, 2023 | | Amount of Gain or

(Loss) Recognized in

AOCI on Derivatives | |

| Amount of Pre-tax

Gain or (Loss) Reclassified

from AOCI into Income | | | Amount of Pre-tax

Gain or (Loss)

Recognized in Income

on Derivatives | |

(Dollars in thousands) | | | | | | | | | |

Derivative contracts | | $ | 18,120 | | | $ | 3,928 | | | $ | 2,595 | |

Hedge accounting gains reclassified from AOCI into earnings in the first quarter of 2024 included $8.0 million recognized as a credit to cost of sales and $1.2 million recognized as a credit to interest expense, net. Hedge accounting gains and (losses) reclassified from AOCI into earnings in the first quarter of 2023 included $3.0 million recognized as a credit to cost of sales and $0.9 million recognized as a debit to interest expense, net. Loss on nondesignated hedges are recognized as a debit to other expense, net. Gains on nondesignated hedges are recognized as a credit to other expense, net.

NOTE 5 - BUSINESS SEGMENTS

The North American and European businesses represent separate operating segments in view of the different markets, customers and products in each of these regions. Within each of these regions, markets, customers, products, and production processes are similar. Moreover, our business within each region generally leverages common systems, processes and infrastructure. Accordingly, North America and Europe comprise the Company’s reportable segments.

| | | | | | | | | | | | | | | | |

(Dollars in thousands) | | Net Sales | | | Income from Operations | |

Three Months Ended | | March 31,

2024 | | | March 31,

2023 | | | March 31,

2024 | | | March 31,

2023 | |

North America | | $ | 193,508 | | | $ | 211,618 | | | $ | 8,082 | | | $ | 21,715 | |

Europe | | | 122,768 | | | | 169,348 | | | | (7,768 | ) | | | (6,579 | ) |

| | $ | 316,276 | | | $ | 380,966 | | | $ | 314 | | | $ | 15,136 | |

| | | | | | | | | | | | | | | | |

(Dollars in thousands) | | Depreciation and Amortization | | | Capital Expenditures | |

Three Months Ended | | March 31,

2024 | | | March 31,

2023 | | | March 31,

2024 | | | March 31,

2023 | |

North America | | $ | 10,343 | | | $ | 9,047 | | | $ | 4,557 | | | $ | 11,443 | |

Europe | | | 11,603 | | | | 13,794 | | | | 2,061 | | | | 4,146 | |

| | $ | 21,946 | | | $ | 22,841 | | | $ | 6,618 | | | $ | 15,589 | |

| | | | | | | | | | | | | | | | |

(Dollars in thousands) | | Property, Plant and Equipment, net | | | Intangible Assets | |

| | March 31,

2024 | | | December 31,

2023 | | | March 31,

2024 | | | December 31,

2023 | |

North America | | $ | 217,327 | | | $ | 220,951 | | | $ | — | | | $ | — | |

Europe | | | 168,950 | | | | 177,648 | | | | 27,637 | | | | 33,242 | |

| | $ | 386,277 | | | $ | 398,599 | | | $ | 27,637 | | | $ | 33,242 | |

| | | | | | | | |

(Dollars in thousands) | | Total Assets | |

| | March 31,

2024 | | | December 31,

2023 | |

North America | | $ | 615,752 | | | $ | 625,612 | |

Europe | | | 389,760 | | | | 404,959 | |

| | $ | 1,005,512 | | | $ | 1,030,571 | |

Geographic information

Net sales and property, plant and equipment by location are as follows:

| | | | | | | | |

| | | | | | |

(Dollars in thousands) | | Net Sales | |

Three Months Ended | | March 31,

2024 | | | March 31,

2023 | |

U.S. | | $ | 1,401 | | | $ | 983 | |

Mexico | | | 192,107 | | | | 210,635 | |

Germany | | | 17,350 | | | | 42,859 | |

Poland | | | 105,418 | | | | 126,489 | |

Consolidated net sales | | $ | 316,276 | | | $ | 380,966 | |

| | | | | | |

(Dollars in thousands) | | Property, Plant and Equipment, net | |

| | March 31,

2024 | | | December 31,

2023 | |

U.S. | | $ | 1,142 | | | $ | 1,228 | |

Mexico | | | 216,185 | | | | 219,723 | |

Germany | | | 1,838 | | | | 1,933 | |

Poland | | | 167,112 | | | | 175,715 | |

Property, plant and equipment, net | | $ | 386,277 | | | $ | 398,599 | |

NOTE 6 - INVENTORIES

| | | | | | | | |

| | March 31,

2024 | | | December 31,

2023 | |

(Dollars in thousands) | | | | | | |

Raw materials | | $ | 49,601 | | | $ | 44,539 | |

Work in process | | | 30,629 | | | | 25,289 | |

Finished goods | | | 68,800 | | | | 74,781 | |

Inventories, net | | $ | 149,030 | | | $ | 144,609 | |

Service wheel and supplies inventory included in other noncurrent assets in the condensed consolidated balance sheets totaled $11.0 million and $11.7 million at March 31, 2024 and December 31, 2023, respectively.

NOTE 7 - PROPERTY, PLANT AND EQUIPMENT

| | | | | | | | |

| | March 31,

2024 | | | December 31,

2023 | |

(Dollars in thousands) | | | | | | |

Land and buildings | | $ | 147,534 | | | $ | 145,912 | |

Machinery and equipment | | | 942,443 | | | | 934,223 | |

Leasehold improvements and others | | | 3,213 | | | | 2,943 | |

Construction in progress | | | 25,721 | | | | 30,252 | |

| | | 1,118,911 | | | | 1,113,330 | |

Accumulated depreciation | | | (732,634 | ) | | | (714,731 | ) |

Property, plant and equipment, net | | $ | 386,277 | | | $ | 398,599 | |

Depreciation expense for the three months ended March 31, 2024 and 2023 was $17.1 million and $18.0 million, respectively.

NOTE 8 – INTANGIBLE ASSETS

The Company’s finite-lived intangible assets as of March 31, 2024 and December 31, 2023 are summarized in the following table.

| | | | | | | | | | | | | | | | | | | |

As of March 31, 2024 | | Gross

Carrying

Amount | | | Accumulated

Amortization | | | Currency

Translation | | | Net Carrying Amount | | | Remaining

Weighted

Average

Amortization

Period | |

(Dollars in thousands) | | | | | | | | | | | | | | | |

Customer relationships | | $ | 167,000 | | | $ | (138,981 | ) | | $ | (382 | ) | | $ | 27,637 | | | 1-4 | |

| | | | | | | | | | | | | | | | | | | |

Year Ended December 31, 2023 | | Gross

Carrying

Amount | | | Accumulated

Amortization | | | Currency

Translation | | | Net Carrying Amount | | | Remaining

Weighted

Average

Amortization

Period | |

(Dollars in thousands) | | | | | | | | | | | | | | | |

Customer relationships | | $ | 167,000 | | | $ | (134,097 | ) | | $ | 339 | | | $ | 33,242 | | | 1-5 | |

Amortization expense for these intangible assets was $4.9 million and $4.8 million for the three months ended March 31, 2024 and 2023, respectively. The anticipated annual amortization expense for these intangible assets is $19.4 million for 2024, $9.5 million for 2025, $2.5 million for 2026, and $1.0 million for 2027.

NOTE 9 – DEBT

A summary of long-term debt and the related weighted average interest rates is shown below:

| | | | | | | | | | | | | | | | |

| | March 31, 2024 | |

Debt Instrument | | Total

Debt | | | Debt Discount and

Issuance Costs (1) | | | Total

Debt, Net | | | Weighted Average

Interest Rate | |

(Dollars in thousands) | | | | | | | | | | | | |

Term Loan Facility | | $ | 395,000 | | | $ | (19,355 | ) | | $ | 375,645 | | | | 13.3 | % |

6.00% Senior Notes | | | 234,197 | | | | (1,229 | ) | | | 232,968 | | | | 6.0 | % |

European CapEx loans | | | 67 | | | | — | | | | 67 | | | | 2.2 | % |

Finance leases | | | 937 | | | | — | | | | 937 | | | | 2.4 | % |

| | $ | 630,201 | | | $ | (20,584 | ) | | | 609,617 | | | | |

Less: Current portion | | | | | | | | | (4,571 | ) | | | |

Long-term debt | | | | | | | | $ | 605,046 | | | | |

| | | | | | | | | | | | | | | | |

| | December 31, 2023 | |

Debt Instrument | | Total

Debt | | | Debt Discount and

Issuance Costs (1) | | | Total

Debt, Net | | | Weighted Average

Interest Rate | |

(Dollars in thousands) | | | | | | | | | | | | |

Term Loan Facility | | $ | 396,000 | | | $ | (20,080 | ) | | $ | 375,920 | | | | 13.4 | % |

6.00% Senior Notes | | | 239,601 | | | | (1,475 | ) | | | 238,126 | | | | 6.0 | % |

European CapEx loans | | | 784 | | | | — | | | | 784 | | | | 2.2 | % |

Finance leases | | | 1,124 | | | | — | | | | 1,124 | | | | 2.4 | % |

| | $ | 637,509 | | | $ | (21,555 | ) | | | 615,954 | | | | |

Less: Current portion | | | | | | | | | (5,322 | ) | | | |

Long-term debt | | | | | | | | $ | 610,632 | | | | |

Senior Notes

On June 15, 2017, the Company issued €250 million aggregate principal amount of 6.00% Senior Notes due June 15, 2025 (the “Notes”). Interest on the Notes is payable semiannually, on June 15 and December 15. The Company may redeem the Notes, in whole or in part, at a redemption price of 100 percent, plus any accrued and unpaid interest to, but not including, the applicable redemption date. If we experience a change of control or sell certain assets, the Company may be required to offer to purchase the Notes from the holders. The Notes are senior unsecured obligations ranking equally in right of payment with all of its existing and future senior indebtedness and senior in right of payment to any subordinated indebtedness. The Notes are effectively subordinated in right of payment to the existing and future secured indebtedness of the Company, including the Senior Secured Credit Facilities (as defined below), to the extent of the assets securing such indebtedness.

Guarantee

The Notes are unconditionally guaranteed by all material wholly owned direct and indirect domestic restricted subsidiaries of the Company (the “Notes Subsidiary Guarantors”), with customary exceptions including, among other things, where providing such guarantees is not permitted by law, regulation or contract, or would result in adverse tax consequences.

Covenants

Subject to certain exceptions, the indenture governing the Notes contains restrictive covenants that, among other things, limit the ability of the Company and the Notes Subsidiary Guarantors to: (i) incur additional indebtedness or issue certain preferred stock; (ii) pay dividends on, or make distributions in respect of, their capital stock; (iii) make certain investments or other restricted payments; (iv) sell certain assets or issue capital stock of restricted subsidiaries; (v) create liens; (vi) merge, consolidate, transfer or dispose of substantially all of their assets; and (vii) engage in certain transactions with affiliates. These covenants are subject to several important limitations and exceptions that are described in the indenture.

The indenture provides for customary events of default that include, among other things (subject in certain cases to customary grace and cure periods): (i) nonpayment of principal, premium, if any, and interest, when due; (ii) failure for 60 days to comply with any obligations, covenants or agreements in the indenture after receipt of written notice from the Bank of New York Mellon, London Branch (the “Trustee”) or holders of at least 30 percent in principal amount of the then outstanding Notes of such failure (other than defaults referred to in the foregoing clause (i)); (iii) default under any mortgage, indenture or instrument for money borrowed by the Company or certain of its subsidiaries; (iv) a failure to pay certain judgments; and (v) certain events of bankruptcy and insolvency. If an event of default occurs and is continuing, the Trustee or holders of at least 30 percent in principal amount of the then outstanding Notes may declare the principal, premium, if any, and accrued and unpaid interest on all the Notes to be due and payable. These events of default are subject to several important qualifications, limitations and exceptions that are described in the indenture. As of March 31, 2024, the Company was in compliance with all covenants under the indenture governing the Notes.

Senior Secured Credit Facilities

On December 15, 2022, the Company entered into a $400.0 million term loan facility (the “Term Loan Facility”) pursuant to a credit agreement (the “Term Loan Credit Agreement”) with Oaktree Fund Administration L.L.C., in its capacity as the administrative agent, JPMorgan Chase Bank, N.A., in its capacity as collateral agent, and other lenders party thereto. Concurrent with the execution of the Term Loan Facility, the Company entered into a $60.0 million revolving credit facility (the “Revolving Credit Facility” and, together with the Term Loan Facility, the “Senior Secured Credit Facilities” or “SSCF”) pursuant to a credit agreement (the “Revolving Credit Agreement” and, together with the Term Loan Credit Agreement, the “Credit Agreements”) with JPMorgan Chase Bank, N.A., in its

capacity as administrative agent, collateral agent and issuing bank, and other lenders and issuing banks thereunder. The previously outstanding $107.5 million U.S. revolving credit facility and €60.0 million European revolving credit facility were terminated.

The Revolving Credit Facility and the Term Loan Facility are scheduled to mature on December 15, 2027 and December 15, 2028, respectively. However, in the event the Company has not repaid, refinanced or otherwise extended the maturity date of the Notes beyond the maturity date of the Term Loan Facility by the date 91 days prior to June 15, 2025, the Term Loan Facility and Revolving Credit Facility would mature 91 days prior to June 15, 2025. Similarly, in the event the Company has not redeemed, refinanced or otherwise extended the redemption date of the redeemable preferred stock beyond the maturity date of the Term Loan Facility by the date 91 days prior to September 14, 2025, the Term Loan Facility and Revolving Credit Facility would mature 91 days prior to September 14, 2025. The Term Loan Facility requires quarterly principal payments of $1.0 million. Additional principal payments may be due with respect to asset sales, debt issuances and as a percentage of cash flow in excess of a specified threshold.

Debt issuance costs associated with the Term Loan Facility of $11.1 million are being amortized over the six-year term. Debt issuance costs and expenses associated with the Revolving Credit Facility of $3.2 million have been recognized as a deferred charge and are being amortized over the five-year term.

The Company may at any time request one or more increases in the amount of (i) commitments under the Term Loan Facility, up to an unlimited additional amount if, on a pro forma basis after the incurrence of such amount, the First Lien Net Leverage Ratio (as defined in the Term Loan Credit Agreement) does not exceed 2.00 to 1.00 and (ii) commitments under the Revolving Credit Facility, up to an aggregate maximum additional amount of $50.0 million, in each case, subject to certain conditions (including the agreement of a lender to provide such commitment increase). Amounts borrowed under the Term Loan Facility may be voluntarily prepaid subject to a prepayment premium of 2.00 percent and 1.00 percent of the loan principal during second and third years, respectively. After the third anniversary of the closing date, there is no prepayment premium.

Borrowings under the Term Loan Credit Facility bear interest at a rate equal to, at the Company’s option, either (i) the secured overnight financing rate (“SOFR”), with a floor of 1.50 percent per annum, or (ii) a base rate (“Term Base Rate”), with a floor of 1.50 percent per annum, equal to the highest of (1) the rate of interest in effect as publicly announced by the administrative agent as its prime rate, (2) the New York Federal Reserve Bank (the “NYFRB”) rate plus 0.50 percent and (3) SOFR for an interest period of one month plus 1.00 percent, in each case, plus the applicable rate. The applicable rate is determined by reference to the Company’s Secured Net Leverage Ratio (as defined in the Term Loan Credit Agreement) and ranges between 7.50 percent and 8.00 percent for SOFR loans (8.00 percent for the current fiscal quarter), and between 6.50 percent and 7.00 percent for Term Base Rate loans (7.00 percent for the current fiscal quarter). In the event of a payment default under the Term Loan Credit Agreement, past due amounts shall be subject to an additional default interest rate of 2.00 percent.

Borrowings under the Revolving Credit Facility bear interest at a rate equal to, at the Company’s option, either (i) SOFR plus 0.10 percent (or, with respect to any borrowings denominated in euros, the adjusted Euro Interbank Offered Rate, “EURIBOR”), with a floor of 0.00 percent per annum or (ii) a base rate (“Revolving Loan Base Rate”), with a floor of 1.00 percent per annum, equal to the highest of (1) the rate of interest in effect as publicly announced by the administrative agent as its prime rate, (2) the NYFRB rate plus 0.50 percent and (3) SOFR for an interest period of one month plus 1.00 percent, in each case, plus the applicable rate. The applicable rate is determined by reference to the Company’s Secured Net Leverage Ratio (as defined in the Revolving Credit Agreement) and ranges between 3.50 percent and 4.50 percent for SOFR and EURIBOR loans (3.50 percent for the current fiscal quarter), and between 2.50 percent and 3.50 percent for Revolving Base Rate loans (2.50 percent for the current fiscal quarter). The commitment fee for the unused commitment under the Revolving Credit Facility varies between 0.50 percent and 0.625 percent depending on the Company’s Secured Net Leverage Ratio (0.50 percent for the current fiscal quarter). Commitment fees are included in interest expense. In the event of a payment default under the Revolving Credit Agreement, past due amounts shall be subject to an additional default interest rate of 2.00 percent.

Guarantees and Collateral Security

Our obligations under the Credit Agreements are unconditionally guaranteed by the Notes Subsidiary Guarantors and certain other domestic and foreign subsidiaries of the Company (collectively, the “SSCF Subsidiary Guarantors”), with customary exceptions including, among other things, where providing such guarantees is not permitted by law, regulation or contract or would result in adverse tax consequences. The guarantees of such obligations, are secured, subject to permitted liens and other exceptions, by substantially all of our assets and the SSCF Subsidiary Guarantors’ assets, including but not limited to: (i) a perfected pledge of all of the capital stock issued by each of the SSCF Subsidiary Guarantors’ (subject to certain exceptions) and (ii) perfected security interests in and mortgages on substantially all tangible and intangible personal property and material fee-owned real property of the Company and the SSCF Subsidiary Guarantors (subject to certain exceptions and exclusions). The Company’s obligations under the Revolving Credit Facility are secured by liens on a super-priority basis ranking ahead of the liens securing the Term Loan Facility.

Covenants

The Credit Agreements contain a number of restrictive covenants that, among other things, restrict, subject to certain exceptions, our ability to incur additional indebtedness and guarantee indebtedness, create or incur liens, engage in mergers or consolidations, sell, transfer or otherwise dispose of assets, make investments, acquisitions, loans or advances, pay dividends, distributions or other restricted payments, or repurchase our capital stock. The Credit Agreements also restrict our ability to prepay, redeem or repurchase any subordinated indebtedness, enter into agreements which limit our ability to incur liens on our assets or that restrict the ability of restricted subsidiaries to pay dividends or make other restricted payments to us, and enter into certain transactions with our affiliates.

The Term Loan Credit Agreement requires the Company to maintain (i) a quarterly Secured Net Leverage Ratio (as defined in the Term Loan Credit Agreement) of no more than 3.50:1.00 and (ii) Liquidity (defined as the sum of unrestricted cash and cash equivalent balances and unborrowed commitments under the Revolving Credit Facility) of at least $37.5 million (subject to adjustments up to $50.0 million following any increase in the commitment under the Revolving Credit Facility). The Revolving Credit Agreement requires the Company to maintain (i) a quarterly Total Net Leverage Ratio (as defined in the Revolving Credit Agreement) of no more than 4.50:1.00; (ii) a quarterly Secured Net Leverage Ratio (as defined in the Revolving Credit Agreement) of no more than 3.50:1.00; and (iii) Liquidity of at least $37.5 million (subject to adjustments up to $50.0 million following any increase in the commitment under the Revolving Credit Facility) but only so long as loans under the Term Loan Facility are outstanding. In the event unrestricted cash and cash equivalent balances fall below $37.5 million at any quarter end (or up to a maximum of $50.0 million following any increase in borrowings available under the Revolving Credit Facility), the available commitment under the Revolving Credit Facility would be reduced by the amount of any shortfall.

The Credit Agreements contain customary default provisions that include among other things: nonpayment of principal or interest when due, failure to comply with obligations, covenants or other provisions in the Credit Agreements, any failure of representations and warranties, cross-default under other debt agreements for obligations in excess of $20.0 million, insolvency, failure to pay judgments in excess of $20.0 million within 60 days of the judicial award, failure to pay any material plan withdrawal obligations under ERISA, invalidity of the loan agreement, invalidity of any security interest in the loan collateral, change of control and failure to maintain the financial covenants. In the event a default occurs, all commitments under the Senior Secured Credit Facilities would be terminated and the lenders would be entitled to declare the principal, premium, if any, and accrued and unpaid interest on all borrowings outstanding to be due and payable.

In addition, the Credit Agreements contain customary representations and warranties and other covenants. As of March 31, 2024, the Company was in compliance with all covenants under the Credit Agreements.

Available Unused Commitments under the Revolving Credit Facility

As of March 31, 2024, the Company had no outstanding borrowings under the Revolving Credit Facility, had outstanding letters of credit of $8.4 million and had available unused commitments under the Revolving Credit Facility of $51.6 million.

Debt maturities as of March 31, 2024, which are due in the next five years are as follows:

| | | | |

Debt Maturities | | Amount | |

(Dollars in thousands) | | | |

Nine remaining months of 2024 | | $ | 3,571 | |

2025 | | | 238,554 | |

2026 | | | 4,074 | |

2027 | | | 4,016 | |

2028 | | | 379,986 | |

Total debt liabilities | | $ | 630,201 | |

NOTE 10 - SUPPLIER FINANCE PROGRAM

The Company receives extended payment terms for a portion of our purchases (90 days rather than 60 days) with one of our principal aluminum suppliers in exchange for a nominal adjustment to the product pricing. The payment terms provided to us are consistent with aluminum industry norms, as well as those offered to the supplier’s other customers. The supplier factors receivables due from us with a financial institution. We are not a party to the supplier’s factoring agreement with the financial institution. We remit payments directly to our supplier, except with respect to product purchased under extended terms which have been factored by the supplier. These payments are remitted directly to the financial institution in accordance with the payment terms originally negotiated with our supplier. These payments are included in cash flows from operations within the condensed consolidated statements of cash flows. The following table summarizes activity in the amounts owed to the financial institution for the three months ended March 31, 2024 and March 31, 2023:

| | | | | | | | |

| | Three Months Ended | |

| | March 31,

2024 | | | March 31,

2023 | |

(Dollars in thousands) | | | | | | |

Outstanding at the beginning of the period | | | 18,000 | | | | 14,371 | |

Added during the period | | | 27,995 | | | | 25,299 | |

Settled during the period | | | (28,780 | ) | | | (21,594 | ) |

Outstanding at the end of the period | | | 17,215 | | | | 18,076 | |

NOTE 11 - REDEEMABLE PREFERRED STOCK

During 2017, we issued 150,000 shares of Series A (140,202 shares) and Series B (9,798 shares) Perpetual Convertible Preferred Stock, par value $0.01 per share for $150.0 million. On August 30, 2017, the Series B shares were converted into Series A redeemable preferred stock (the “redeemable preferred stock”) after approval by our shareholders. The redeemable preferred stock has an initial stated value of $1,000 per share, par value of $0.01 per share and liquidation preference over common stock.

The redeemable preferred stock is convertible into shares of our common stock equal to the number of shares determined by dividing the sum of the stated value and any accrued and unpaid dividends by the conversion price of $28.162. The redeemable preferred stock accrues dividends at a rate of 9.0 percent per annum, payable at our election either in-kind or in cash and is also entitled to participate in dividends on common stock in an amount equal to that which would have been due had the shares been converted into common stock.

We may mandate conversion of the redeemable preferred stock if the price of the common stock exceeds $84.49. The holder may redeem the shares upon the occurrence of any of the following events (referred to as a “redemption event”): a change in control, recapitalization, merger, sale of substantially all of the Company’s assets, liquidation or delisting of the Company’s common stock. In addition, the holder may unconditionally redeem the shares at any time on or after September 14, 2025. We may, at our option, redeem in whole at any time all of the shares of redeemable preferred stock outstanding. At redemption by either party, the redemption value will be the greater of two times the initial face value ($150.0 million) and any accrued unpaid dividends or dividends paid-in-kind, currently $300.0 million, or the product of the number of common shares into which the redeemable preferred stock could be converted (5.3 million shares currently) and the then current market price of the common stock. Any redemption payment would be limited to cash legally available to pay such redemption.

We have determined that the conversion option and the redemption option exercisable upon the occurrence of a “redemption event” which are embedded in the redeemable preferred stock must be accounted for separately from the redeemable preferred stock as a derivative liability.

Since the redeemable preferred stock may be redeemed at the option of the holder, but is not mandatorily redeemable, the redeemable preferred stock was classified as mezzanine equity and initially recognized at fair value of $150.0 million (the proceeds on the date of issuance), less issuance costs of $3.7 million and $10.9 million assigned to the embedded derivative liability at date of issuance, resulting in an adjusted initial value of $135.5 million.

The difference between the redemption value of the redeemable preferred stock and the carrying value (the “premium”) is being accreted over the period from the date of issuance through September 14, 2025 using the effective interest method. The accretion is treated as a deemed dividend, recorded as a charge to retained earnings and deducted in computing earnings per share (analogous to the treatment for stated and participating dividends paid on the redeemable preferred shares). The cumulative premium accretion as of March 31, 2024 and December 31, 2023 was $119.5 million and $112.7 million, respectively, resulting in adjusted redeemable preferred stock balances of $255.0 million and $248.2 million, respectively.

NOTE 12 – EARNINGS PER SHARE

Basic earnings per share is computed by dividing net income (loss), after deducting preferred dividends and accretion and European noncontrolling redeemable equity dividends, by the weighted average number of common shares outstanding. For purposes of calculating diluted earnings per share, the weighted average shares outstanding includes the dilutive effect of outstanding stock options and time and performance based restricted stock units under the treasury stock method.

The redeemable preferred shares discussed in Note 11, “Redeemable Preferred Stock” (convertible into 5,326 thousand shares) have not been included in the diluted earnings per share because the inclusion of such shares on an as converted basis would be anti-dilutive for the three months ended March 31, 2024 and 2023. In addition, the redeemable preferred shares are considered participating securities because they participate in any common share dividends. In calculating basic and diluted earnings per share, a company with participating securities must allocate earnings to the participating securities with a corresponding reduction in the earnings attributable to common shares under the two-class method. Losses are only allocated to participating securities when the security holders have a contractual obligation to share in the losses of the Company with common stockholders. Because the redeemable preferred shareholders do not have a contractual obligation to share in the Company's losses with common stockholders, the full amount of the Company’s losses for the three months ended March 31, 2024 and March 31, 2023 were attributed to the common shares.

| | | | | | | | |

| | Three Months Ended | |

| | March 31,

2024 | | | March 31,

2023 | |

(Dollars in thousands, except per share amounts) | | | | | | |

Basic (Loss) Earnings Per Share: | | | | | | |

Net loss | | $ | (32,749 | ) | | $ | (4,047 | ) |

Less: Redeemable preferred stock dividends and accretion | | | (10,166 | ) | | | (9,440 | ) |

Less: European non-controlling redeemable equity dividend | | | (7 | ) | | | (10 | ) |

Basic numerator | | $ | (42,922 | ) | | $ | (13,497 | ) |

Basic (loss) earnings per share | | $ | (1.52 | ) | | $ | (0.49 | ) |

Weighted average shares outstanding – Basic | | | 28,254 | | | | 27,299 | |

Diluted (Loss) Earnings Per Share: | | | | | | |

Net loss | | $ | (32,749 | ) | | $ | (4,047 | ) |

Less: Redeemable preferred stock dividends and accretion | | | (10,166 | ) | | | (9,440 | ) |

Less: European non-controlling redeemable equity dividend | | | (7 | ) | | | (10 | ) |

Diluted numerator | | $ | (42,922 | ) | | $ | (13,497 | ) |

Diluted (loss) earnings per share | | $ | (1.52 | ) | | $ | (0.49 | ) |

Weighted average shares outstanding – Basic | | | 28,254 | | | | 27,299 | |

Dilutive effect of common share equivalents | | | — | | | | — | |

Weighted average shares outstanding – Diluted | | | 28,254 | | | | 27,299 | |

NOTE 13 - INCOME TAXES

The estimated annual effective tax rate is forecasted quarterly using actual historical information and forward-looking estimates and applied to year-to-date ordinary income. The tax effects of unusual or infrequently occurring items, including changes in judgment about valuation allowances, settlements with taxing authorities and effects of changes in tax laws or rates, and changes due to tax restructuring are reported in the interim period in which they occur.

Income taxes for the three months ended March 31, 2024 were a $16.6 million tax provision on a pre-tax loss of $16.1, resulting in an effective income tax rate of (103.4) percent. The effective income tax rate for the three months ended March 31, 2024 differs from the statutory rate primarily due to valuation allowances, the reversal of an uncertain tax position, the mix of earnings among tax jurisdictions, and a tax charge impacting deferred tax assets related to tax restructuring of $17.8 million.

The income tax provision for the three months ended March 31, 2023 was $3.3 million on a pre-tax loss of $0.7 million, resulting in an effective income tax rate of (440.3) percent. The effective income tax rate for the three months ended March 31, 2023 differs from the statutory rate primarily due to valuation allowances, the reversal of an uncertain tax position and the mix of earnings among tax jurisdictions.

The Company continuously evaluates the realizability of our net deferred tax assets. As of March 31, 2024, certain U.S. and substantially all our German deferred tax assets, net of deferred tax liabilities, were subject to valuation allowances.

The Organization for Economic Co-operation and Development has issued Pillar Two model rules introducing a new global minimum tax of 15.0 percent effective January 1, 2024. While the United States has not yet adopted the Pillar Two rules, various other governments around the world have enacted part of the legislation. As currently designed, Pillar Two ultimately applies to our worldwide operations. Currently, enacted Pillar Two legislation does not have a material impact on our financial statements. We will continue to assess U.S. and global legislative action related to Pillar Two for potential impacts.

NOTE 14 - LEASES

The Company determines whether an arrangement is or contains a lease at the inception of the arrangement. Operating leases are included in other noncurrent assets, accrued expenses and other noncurrent liabilities in our condensed consolidated balance sheets. Finance leases are included in property, plant and equipment, net, short-term debt and long-term debt (less current portion) in our condensed consolidated balance sheets.

Right-of-use (“ROU”) assets represent our right to use an underlying asset for the lease term and lease liabilities represent our obligation to make lease payments arising from the lease. Finance and operating lease ROU assets and liabilities are recognized at the commencement date based on the present value of the lease payments over the lease term. Since we generally do not have access to the interest rate implicit in the lease, the Company uses our incremental borrowing rate (for fully collateralized debt) at the inception of the lease in determining the present value of the lease payments. The implicit rate is, however, used where readily available. Lease expense under operating leases is recognized on a straight-line basis over the term of the lease. Certain of our leases contain both lease and nonlease components, which are accounted for separately.

The Company has operating and finance leases for office facilities, a data center and certain equipment. The remaining terms of our leases range from over one year to five years. Certain leases include options to extend the lease term for up to ten years, as well as options to terminate, both of which have been excluded from the term of the lease since exercise of these options is not reasonably certain.

Lease expense and cash flow for the three months ended March 31, 2024 and March 31, 2023 and operating and finance lease assets and liabilities, average lease term and average discount rate as of March 31, 2024 and December 31, 2023 are as follows:

| | | | | | | | |

| | Three Months Ended | |

| | March 31,

2024 | | | March 31,

2023 | |

(Dollars in thousands) | | | | | | |

Lease Expense | | | | | | |

Finance lease expense: | | | | | | |

Amortization of right-of-use assets | | $ | 135 | | | $ | 245 | |

Interest on lease liabilities | | | 6 | | | | 16 | |

Operating lease expense | | | 827 | | | | 623 | |

Total lease expense | | $ | 968 | | | $ | 884 | |

| | | | | | |

Cash Flow Components | | | | | | |

Cash paid for amounts included in the measurement of lease liabilities: | | | | | | |

Operating cash outflows from finance leases | | $ | 6 | | | $ | 16 | |

Operating cash outflows from operating leases | | | 853 | | | | 636 | |

Financing cash outflows from finance leases | | | 150 | | | | 288 | |

Right-of-use assets obtained in exchange for finance lease liabilities,

net of terminations and disposals | | | 7 | | | | 396 | |

Right-of-use assets obtained in exchange for operating lease liabilities,

net of terminations and disposals | | | 15 | | | | — | |

| | | | | | |

| | March 31,

2024 | | | December 31,

2023 | |

(Dollars in thousands, except lease term and discount rate) | | | | | | |

Balance Sheet Information | | | | | | |

Operating leases: | | | | | | |

Other noncurrent assets | | $ | 9,176 | | | $ | 10,003 | |

Accrued liabilities | | $ | (2,920 | ) | | $ | (2,987 | ) |

Other noncurrent liabilities | | | (6,221 | ) | | | (7,000 | ) |

Total operating lease liabilities | | $ | (9,141 | ) | | $ | (9,987 | ) |

| | | | | | |

Finance leases: | | | | | | |

Property, plant and equipment gross | | $ | 2,308 | | | $ | 2,301 | |

Accumulated depreciation | | | (1,017 | ) | | | (882 | ) |

Property, plant and equipment, net | | $ | 1,291 | | | $ | 1,419 | |

Current portion of long-term debt | | $ | (504 | ) | | $ | (538 | ) |

Long-term debt (less current portion) | | | (433 | ) | | | (586 | ) |

Total finance lease liabilities | | $ | (937 | ) | | $ | (1,124 | ) |

| | | | | | |

Lease Term and Discount Rates | | | | | | |

Weighted-average remaining lease term - finance leases (years) | | | 1.9 | | | | 2.0 | |

Weighted-average remaining lease term - operating leases (years) | | | 3.1 | | | | 3.3 | |

Weighted-average discount rate - finance leases | | | 2.4 | % | | | 2.4 | % |

Weighted-average discount rate - operating leases | | | 5.0 | % | | | 5.0 | % |

Future minimum payments under our leases as of March 31, 2024 are as follows:

| | | | | | | | |

| | Amount | |

(Dollars in thousands) | | | | | | |

Lease Maturities | | Finance Leases | | | Operating Leases | |

Nine remaining months of 2024 | | $ | 504 | | | $ | 2,575 | |

2025 | | | 357 | | | | 3,048 | |

2026 | | | 74 | | | | 2,902 | |

2027 | | | 16 | | | | 1,299 | |

2028 | | | 8 | | | | - | |

Total | | | 959 | | | | 9,824 | |

Less: Imputed interest | | | (22 | ) | | | (683 | ) |

Total lease liabilities, net of interest | | $ | 937 | | | $ | 9,141 | |

NOTE 15 – RETIREMENT PLANS

We have an unfunded salary continuation plan covering certain directors, officers and other key members of management. Subject to certain vesting requirements, the plan provides for a benefit based on final average compensation, which becomes payable on the employee’s death or upon attaining age 65, if retired. The plan was closed to new participants effective February 3, 2011.

For the three months ended March 31, 2024 payments to retirees or their beneficiaries totaled approximately $0.4 million. We presently anticipate benefit payments in 2024 to total $1.5 million. The following table summarizes the components of net periodic pension cost for the three months ended March 31, 2024 and March 31, 2023.

| | | | | | | | |

| | Three Months Ended | |

| | March 31,

2024 | | | March 31,

2023 | |

(Dollars in thousands) | | | | | | |

Interest cost | | $ | 290 | | | $ | 304 | |

Net amortization | | | 1 | | | | — | |

Net periodic pension cost | | $ | 291 | | | $ | 304 | |

NOTE 16 - STOCK-BASED COMPENSATION

Equity Incentive Plan

Our 2018 Equity Incentive Plan (the “Plan”) was approved by stockholders in May 2018, authorizing us to issue up to 4.35 million shares of common stock, along with non-qualified stock options, stock appreciation rights, restricted stock units and performance restricted stock units to our officers, key employees, nonemployee directors and consultants. In May 2021 and 2023, the stockholders approved amendments to the Plan that, among other things, increased the authorized shares by 2.0 million and 3.5 million, respectively. At March 31, 2024, there were 0.9 million shares available for future grants under this Plan. It is our policy to issue shares from authorized but not issued shares upon the exercise of stock options.

Under the terms of the Plan, each year eligible participants are granted time value restricted stock units (“RSUs”), vesting ratably over a three-year period, and performance restricted stock units (“PSUs”) with three-year cliff vesting. Upon vesting, each restricted stock award is exchangeable for one share of the Company’s common stock, with accrued dividends.

RSU, PSU and option activity for the three months ended March 31, 2024 and March 31, 2023 is summarized in the following table:

| | | | | | | | | | | | | | | | |

| | Equity Incentive Awards | |

| | Restricted

Stock Units | | | Weighted

Average

Grant Date

Fair Value | | | Performance

Shares | | | Weighted

Average

Grant Date

Fair Value | |

Balance at January 1, 2024 | | | 1,001,634 | | | $ | 4.39 | | | | 2,192,759 | | | $ | 5.24 | |

Granted | | | 397,496 | | | | 2.99 | | | | 762,584 | | | | 3.82 | |

Settled | | | (231,037 | ) | | | 4.90 | | | | (605,150 | ) | | | 5.80 | |

Forfeited or expired | | | — | | | | — | | | | — | | | | — | |

Balance at March 31, 2024 | | | 1,168,093 | | | $ | 3.81 | | | | 2,350,193 | | | $ | 4.63 | |

| | | | | | | | | | | | |

Awards estimated to vest in the future | | | 1,168,093 | | | $ | 3.81 | | | | 2,350,193 | | | $ | 4.63 | |

| | | | | | | | | | | | | | | | |

| | Equity Incentive Awards | |

| | Restricted

Stock Units | | | Weighted

Average

Grant Date

Fair Value | | | Performance

Shares | | | Weighted

Average

Grant Date

Fair Value | |

Balance at January 1, 2023 | | | 896,799 | | | $ | 4.16 | | | | 2,323,101 | | | $ | 6.26 | |

Granted | | | 56,818 | | | | 4.40 | | | | 56,818 | | | | 5.39 | |

Settled | | | (369,585 | ) | | | 4.04 | | | | (1,016,574 | ) | | | 5.13 | |

Forfeited or expired | | | (29,853 | ) | | | 5.80 | | | | (34,037 | ) | | | 8.50 | |

Balance at March 31, 2023 | | | 554,179 | | | $ | 4.23 | | | | 1,329,308 | | | $ | 6.78 | |

| | | | | | | | | | | | |

Awards estimated to vest in the future | | | 554,179 | | | $ | 4.23 | | | | 1,329,308 | | | $ | 6.78 | |

Stock-based compensation expense for the three months ended March 31, 2024 and 2023 was $1.7 million and $0.8 million, respectively. Unrecognized stock-based compensation expense related to nonvested awards of $10.1 million is expected to be recognized over a weighted average period of approximately 2.1 years as of March 31, 2024.

NOTE 17 – COMMITMENTS AND CONTINGENCIES

Purchase Commitments

When market conditions warrant, we may enter into purchase commitments to secure the supply of certain commodities used in the manufacture of our products, such as aluminum, electricity, natural gas and other raw materials. Prices under our aluminum contracts are based on a market index and regional premiums for processing, transportation and alloy components which are adjusted quarterly for purchases in the ensuing quarter. Certain of our purchase agreements include volume commitments, however any excess commitments are generally negotiated with suppliers and those which have occurred in the past have been carried over to future periods.

Contingencies

We are party to various legal and environmental proceedings incidental to our business. Certain claims, suits and complaints arising in the ordinary course of business have been filed or are pending against us. Based on facts now known, except as provided below, we believe all such matters are adequately provided for, covered by insurance, are without merit and/or involve such amounts that would not materially adversely affect our consolidated results of operations, cash flows or financial position.

In March 2022, the German Federal Cartel Office initiated an investigation related to European light alloy wheel manufacturers, including Superior Industries Europe AG (a wholly owned subsidiary of the Company), on suspicion of conduct restricting competition. The Company is cooperating fully with the German Federal Cartel Office. In the event Superior Industries Europe AG is deemed to have violated the applicable statutes, the Company could be subject to a fine or civil proceedings. At this point, we are unable to predict the duration or the outcome of the investigation.

The Company purchases electricity and natural gas requirements for its manufacturing operations in Poland from a single energy distributor. Superior and its energy distributor, as well as the parent company of the energy distributor, have filed various claims against one another. These claims generally request the court to determine whether Superior’s energy contracts with the energy distributor were valid during the period December 2021 through May 2022.

In December 2021, the Company’s energy distributor informed the Company it would no longer supply energy, notwithstanding its contractual obligation to continue supply. Following a request from the Company, the court issued an injunction ordering the energy distributor to continue supplying energy and gas to the Company. In 2022, the Company obtained a final and binding judgment confirming that the original contracts with the energy distributor had not been effectively dissolved, and thus remained binding.