Use these links to rapidly review the document

TABLE OF CONTENTS

U.S. Securities and Exchange Commission

Washington, D.C. 20549

Form 40-F

o REGISTRATION STATEMENT PURSUANT TO SECTION 12 OF THE SECURITIES EXCHANGE ACT OF 1934

OR

ý ANNUAL REPORT PURSUANT TO SECTION 13(a) OR 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2002 Commission File Number 1-8887

TRANSCANADA PIPELINES LIMITED

(Exact Name of Registrant as specified in its charter)

Canada

(Jurisdiction of incorporation or organization)

4922, 4923, 4924, 5172

(Primary Standard Industrial Classification Code Number (if applicable))

Not Applicable

(I.R.S. Employer Identification Number (if applicable))

TransCanada Tower, 450 – 1 Street S.W.

Calgary, Alberta, Canada, T2P 5H1

(403) 920-2000

(Address and telephone number of Registrant’s principal executive offices)

CT Corporation, Suite 2610, 520 Pike Street

Seattle, Washington, 98101; (206) 622-4511; 1-800-456-4511

(Name, address (including zip code) and telephone number (including area code)

of agent for service in the United States)

Securities registered pursuant to section 12(b) of the Act:

Title of each class |

| Name of each exchange on which registered |

Common Shares (including Rights under Shareholder Rights Plan) |

| New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

For annual reports, indicate by check mark the information filed with this Form:

ý Annual Information Form ý Audited annual financial statements

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report.

At December 31, 2002, 479,502,341 TransCanada common shares

were issued and outstanding

Indicate by check mark whether the Registrant by filing the information contained in this Form is also thereby furnishing the information to the Commission pursuant to Rule 12g3-2(b) under the Securities Exchange Act of 1934 (the “Exchange Act”). If “Yes” is marked, indicate the file number assigned to the Registrant in connection with such Rule.

Yes o No ý

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during the preceding 12 months (or such shorter period that the Registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days.

Yes ý No o

The documents (or portions thereof) forming part of this Form 40-F are incorporated by reference into the following registration statements under the Securities Act of 1933, as amended:

Form |

| Registration No. |

|

|

|

|

|

S-8 |

| 33-00958 |

|

S-8 |

| 333-5916 |

|

S-8 |

| 333-8470 |

|

S-8 |

| 333-9130 |

|

F-3 |

| 33-13564 |

|

F-3 |

| 333-6132 |

|

F-10 |

| 333-101140 |

|

CONSOLIDATED AUDITED ANNUAL FINANCIAL STATEMENTS AND

MANAGEMENT’S DISCUSSION & ANALYSIS

A. Audited Annual Financial Statements

For consolidated audited financial statements, including the report of independent chartered accountants with respect thereto, see pages 44 through 77 of the TransCanada 2002 Annual Report to Shareholders included herein. See Note 20 of the Notes to Consolidated Financial Statements on pages 72 through 77 of the TransCanada 2002 Annual Report to Shareholders, reconciling the important differences between Canadian and United States generally accepted accounting principles.

B. Management’s Discussion & Analysis

For management’s discussion and analysis, see pages 7 through 42 of the TransCanada 2002 Annual Report to Shareholders included herein under the heading “Management’s Discussion & Analysis”.

For the purposes of this Report, only pages 7 through 42 and 44 through 77 of the TransCanada 2002 Annual Report to Shareholders as referred to above shall be deemed incorporated herein by reference and filed, and the balance of such 2002 Annual Report, except as otherwise specifically incorporated by reference in the TransCanada Annual Information Form, shall be deemed not filed with the Securities and Exchange Commission as part of this Report under the Exchange Act.

UNDERTAKING

Registrant undertakes to make available, in person or by telephone, representatives to respond to inquiries made by the Commission staff, and to furnish promptly, when requested to do so by the Commission staff, information relating to: the securities registered pursuant to Form 40-F; the securities in relation to which the obligation to file an Annual Report on Form 40-F arises; or transactions in said securities.

CONTROLS AND PROCEDURES

The conclusions of TransCanada's management with respect to the effectiveness of TransCanada's disclosure controls and procedures are contained on pages 37 and 38 of the TransCanada 2002 Annual Report to Shareholders.

FORWARD-LOOKING INFORMATION

Certain of the information included herein is forward-looking and relates to, among other things, anticipated financial performance, business prospects, strategies, regulatory decisions, new services, market forces, commitments and technological developments. Much of this information appears in the Management’s Discussion and Analysis at pages 7 through 42 of TransCanada’s Annual Report to Shareholders for the year ended December 31, 2002 incorporated herein by reference. By its nature, such forward-looking information is subject to various risks and uncertainties, including those discussed herein, which could cause TransCanada’s actual results and experience to differ materially from the anticipated results or other expectations expressed. Readers are cautioned not to place undue reliance on this forward-looking information, which is as of the date hereof, and TransCanada undertakes no obligation to update publicly or revise any forward-looking information, whether as a result of new information, future events or otherwise. Factors which could cause actual results or events to differ materially from current expectations include, among other things, the ability of TransCanada to successfully implement its strategic initiatives and whether such strategic initiatives will yield the expected benefits, the availability and price of energy commodities, regulatory decisions, competitive factors in the pipeline and power industry sectors, and the current economic conditions in North America.

2

SIGNATURES

Pursuant to the requirements of the Exchange Act, the Registrant certifies that it meets all of the requirements for filing on Form 40-F and has duly caused this Annual Report to be signed on its behalf by the undersigned, thereto duly authorized, in the City of Calgary, Province of Alberta, Canada.

| TRANSCANADA PIPELINES LIMITED | ||

|

|

| |

|

|

| |

| Per: | “Russell K. Girling” |

|

|

| RUSSELL K. GIRLING, Executive Vice-President, | |

|

|

| |

|

| Date: March 25, 2003 | |

|

|

| |

3

Certificate Pursuant to Section 302

Of the Sarbanes-Oxley Act

I, Harold N. Kvisle, certify that:

1. I, Harold N. Kvisle have reviewed this annual report on Form 40-F of TransCanada PipeLines Limited;

2. Based on my knowledge, this annual report does not contain any untrue statement of a material fact or omit to state a material fact necessary to make the statements made, in light of the circumstances under which such statements were made, not misleading with respect to the period covered by this annual report;

3. Based on my knowledge, the financial statements, and other financial information included in this annual report, fairly present in all material respects the financial condition, results of operations and cash flows of the registrant as of, and for, the periods presented in this annual report;

4. The registrant’s other certifying officers and I are responsible for establishing and maintaining disclosure controls and procedures (as defined in Exchange Act Rules 13a-14 and 15d-14) for the registrant and we have:

a) designed such disclosure controls and procedures to ensure that material information relating to the registrant, including its consolidated subsidiaries, is made known to us by others within those entities, particularly during the period in which this annual report is being prepared;

b) evaluated the effectiveness of the registrant’s disclosure controls and procedures as of a date within 90 days prior to the filing date of this annual report (the “Evaluation Date”); and

c) presented in this annual report our conclusions about the effectiveness of the disclosure controls and procedures based on our evaluation as of the Evaluation Date;

5. The registrant’s other certifying officers and I have disclosed, based on our most recent evaluation, to the registrant’s auditors and the audit committee of registrant’s board of directors (or persons performing the equivalent function):

a) all significant deficiencies in the design or operation of internal controls which could adversely affect the registrant’s ability to record, process, summarize and report financial data and have identified for the registrant’s auditors any material weaknesses in internal controls; and

b) any fraud, whether or not material, that involves management or other employees who have a significant role in the registrant’s internal controls; and

6. The registrant’s other certifying officers and I have indicated in this annual report whether there were significant changes in internal controls or in other factors that could significantly affect internal controls subsequent to the date of our most recent evaluation, including any corrective actions with regard to significant deficiencies and material weaknesses.

Dated March 25, 2003 |

| |

|

| |

|

| |

| / s / Harold N. Kvisle |

|

| Harold N. Kvisle | |

| President and Chief Executive Officer | |

4

Certificate Pursuant to Section 302

Of the Sarbanes-Oxley Act

I, Russell K. Girling, certify that:

1. I, Russell K. Girling have reviewed this annual report on Form 40-F of TransCanada PipeLines Limited;

2. Based on my knowledge, this annual report does not contain any untrue statement of a material fact or omit to state a material fact necessary to make the statements made, in light of the circumstances under which such statements were made, not misleading with respect to the period covered by this annual report;

3. Based on my knowledge, the financial statements, and other financial information included in this annual report, fairly present in all material respects the financial condition, results of operations and cash flows of the registrant as of, and for, the periods presented in this annual report;

4. The registrant’s other certifying officers and I are responsible for establishing and maintaining disclosure controls and procedures (as defined in Exchange Act Rules 13a-14 and 15d-14) for the registrant and we have:

(a) designed such disclosure controls and procedures to ensure that material information relating to the registrant, including its consolidated subsidiaries, is made known to us by others within those entities, particularly during the period in which this annual report is being prepared;

(b) evaluated the effectiveness of the registrant’s disclosure controls and procedures as of a date within 90 days prior to the filing date of this annual report (the “Evaluation Date”); and

(c) presented in this annual report our conclusions about the effectiveness of the disclosure controls and procedures based on our evaluation as of the Evaluation Date;

5. The registrant’s other certifying officers and I have disclosed, based on our most recent evaluation, to the registrant’s auditors and the audit committee of registrant’s board of directors (or persons performing the equivalent function):

(a) all significant deficiencies in the design or operation of internal controls which could adversely affect the registrant’s ability to record, process, summarize and report financial data and have identified for the registrant’s auditors any material weaknesses in internal controls; and

(b) any fraud, whether or not material, that involves management or other employees who have a significant role in the registrant’s internal controls; and

6. The registrant’s other certifying officers and I have indicated in this annual report whether there were significant changes in internal controls or in other factors that could significantly affect internal controls subsequent to the date of our most recent evaluation, including any corrective actions with regard to significant deficiencies and material weaknesses.

Dated March 25, 2003 |

| |

|

| |

|

| |

| / s / Russell K. Girling |

|

| Russell K. Girling | |

| Executive Vice-President, Corporate Development | |

5

DOCUMENTS FILED AS PART OF THIS REPORT

1. TransCanada PipeLines Limited Renewal Annual Information Form for the year ended December 31, 2002.

2. Management's Discussion and Analysis (included on pages 7 through 42 of the TransCanada 2002 Annual Report to Shareholders).

3. 2002 Consolidated Audited Financial Statements (included on pages 44 through 77 of the TransCanada 2002 Annual Report to Shareholders).

4. U.S. GAAP reconciliation of the 2002 Consolidated Audited Financial Statements (included on pages 72 through 77 of the TransCanada 2002 Annual Report to Shareholders).

EXHIBITS

1. Consent of KPMG, LLP Chartered Accountants.

2. Certification of Chief Executive Officer under Section 906 of Sarbanes-Oxley.

3. Certification of Chief Financial Officer under Section 906 of Sarbanes-Oxley.

6

TRANSCANADA PIPELINES LIMITED

RENEWAL

ANNUAL INFORMATION FORM

for the year ended December 31, 2002

February 25, 2003

Unless otherwise noted, the information contained in this Annual Information Form is given as at December 31, 2002 (the "Year End").

TRANSCANADA PIPELINES LIMITED i

For the reference information noted below, please refer to Schedule "A".

- •

- Exchange Rate of the Canadian Dollar

- •

- Metric Conversion Table

- •

- Glossary

Certain written and oral statements made or incorporated by reference from time to time by TransCanada or its representatives in this Annual Information Form and other reports and filings made with the securities regulatory authorities, press releases, conferences or otherwise, are forward-looking and relate to, among other things, anticipated financial performance, business prospects, strategies, regulatory developments, new services, market forces, commitments and technological developments. Much of this information also appears in the Management's Discussion and Analysis of Financial Condition and Results of Operations ("MD&A") found in TransCanada's Annual Report to Shareholders for the year ended December 31, 2002 (the "Annual Report"), which is incorporated by reference into this document. By its nature, such forward-looking information is subject to various risks and uncertainties, including those discussed herein, which could cause TransCanada's actual results and experience to differ materially from the anticipated results or other expectations expressed. Readers are cautioned not to place undue reliance on this forward-looking information, which is as of the date of this Annual Information Form, and TransCanada undertakes no obligation to update publicly or revise any forward-looking information, whether as a result of new information, future events or otherwise.

A number of factors, including but not limited to those discussed in this section, could cause actual results or events to differ materially from current expectations. Please note that capitalized terms in this section are defined later in the document and can also be found in the Glossary in Schedule "A".

TransCanada's businesses are highly complex and are dispersed over tens of thousands of square kilometres, often in remote locations. Pipeline and power facilities are subject to operational risks, including mechanical failure, physical degradation, operator error, manufacturer defects, labor disputes, sabotage, terrorism, failure of supply, catastrophic events and natural disasters. The occurrence or continuation of such events could increase TransCanada's costs and reduce its ability to transport natural gas or deliver power.

TransCanada's power business and investments rely on feedstocks of natural gas, biomass, water, coal and (as of February 2003) uranium. Failure of supplies of feedstocks could affect TransCanada's ability to generate electricity and fulfill its supply obligations, and changes in prices of feedstocks could affect TransCanada's financial results. Although TransCanada hedges against most of these risks, there can be no assurance that such hedging will be adequate in all circumstances.

TransCanada does not operate the Bruce Power facility or the assets underlying the Sundance A or Sundance B power purchase arrangements. Failure by the operators of these facilities to operate at the cost or in the manner projected by TransCanada could negatively affect TransCanada's financial position.

TransCanada does not own any of the power transmission lines over which its electricity is transmitted and delivered. Any disruption in transmission could affect TransCanada's ability to deliver electricity and could have an adverse impact on TransCanada's financial results.

ii TRANSCANADA PIPELINES LIMITED

The Canadian Mainline, the Alberta System, the BC System and the Foothills System transport natural gas from the Western Canada Sedimentary Basin. Continuing use of these systems is dependent on a number of factors including the level of exploration and development within the basin, the price of natural gas, the ability of natural gas producers to deliver natural gas to the various pipeline systems, the development of northern gas reserves, and the regulatory environment for producers, transporters and consumers of natural gas.

Information on competition risks in TransCanada's natural gas transmission business can be found under the heading "Transmission — Competition in Transmission" below.

Information on competition risks in TransCanada's power business can be found under the heading "Power — Competition in Power" below.

TransCanada carries on its businesses with numerous counterparties with a wide range of creditworthiness. While processes are followed to address the creditworthiness of certain of these counterparties, the failure of any counterparty to meet its financial obligations could have an impact on TransCanada's financial position. Such failure could result from a number of factors beyond TransCanada's control, including (but not limited to) fluctuating commodity energy prices and interest rates, changes in regulatory and economic environments, political instability and legally reviewable activities.

Political and Regulatory Risks

TransCanada's businesses are subject to regulation by the jurisdictions in which they carry on business. The regulation of the natural gas transportation business and the power generation business have changed over the past ten years, and further changes could have a material impact on TransCanada's financial results. Such changes could result from changes in environmental laws, changes to the regulatory philosophies in Canada or the United States, changes to international tax treaties and jurisdictional issues among governments and governmental bodies.

TransCanada is subject to federal, state, provincial, municipal and other applicable environmental laws and regulations. Increasingly stringent environmental laws could result in increased costs and liabilities, which could impact TransCanada's financial results. In December 2002, the Canadian federal government ratified the Kyoto Protocol, which requires Canada to reduce its greenhouse gas emissions significantly. Although the Canadian government has not yet provided details on how it intends to meet these reduction targets, the energy industry has been identified as one of the areas that will be affected. Under the rules being proposed by the federal government, TransCanada will be considered a large industrial emitter. The final rules, once known, could affect TransCanada's operations and profitability.

TransCanada maintains customary insurance for its businesses, consistent with pipeline and power industry practices. Insurance coverage is always subject to limits and exclusions, and the financial stability of the insurance carriers. In the event of a significant insurable event, insurance proceeds may not be adequate to cover completely the costs of such event. In addition, certain environmental and other risks are excluded by law from insurance coverage.

TRANSCANADA PIPELINES LIMITED iii

Because TransCanada operates in Canada and the United States, its financial results can be impacted by interest rates and foreign exchange rates. TransCanada has an active hedging program in place to address interest and foreign exchange rate risks, but there can be no assurances that such hedging will be adequate to address the risks.

TransCanada's growth strategy is dependent upon the acquisition and construction of facilities and businesses that align with its current businesses. TransCanada may incur costs in the pursuit of acquisitions or development of power or transmission assets that may not be completed. Failure by TransCanada to consummate negotiated acquisitions or new developments may result in contractual liabilities, liquidated damages, additional costs and expenses which could affect profitability.

TransCanada's growth strategy is also dependent on access to capital markets in the United States and Canada. Although significant credit facilities are currently available, changing market conditions could result in a materially increased cost of capital which would reduce TransCanada's ability to pursue this strategy.

Since the terrorist attacks of September 11, 2001, certain energy assets (including the pipeline and power generation infrastructure in the United States) may be a target of future terrorist attacks. This risk has been heightened by the current situation in Iraq. Subsequent to the terrorist attacks of September 11, 2001, many insurers have reduced or eliminated insurance coverage for terrorist attacks. Terrorist attacks on TransCanada's assets or the assets of its customers or suppliers could have a negative impact on TransCanada's operations or financial results which may not be covered by insurance.

iv TRANSCANADA PIPELINES LIMITED

TransCanada PipeLines Limited ("TransCanada") is a Canadian public company. Significant dates and events are set forth below.

| Date | Event | |

|---|---|---|

| March 21, 1951 | Incorporated by Special Act of Parliament as Trans-Canada Pipe Lines Limited. | |

April 19, 1972 | Continued under theCanada Corporations Act by Letters Patent, which included the alteration of its capital and change of name to TransCanada PipeLines Limited. | |

June 1, 1979 | Continued under theCanada Business Corporations Act. Since then, TransCanada has had several amendments to its Articles with respect to its authorized share capital, and several restatements of its Articles to consolidate the various amendments to its Articles and for the creation of certain classes of preferred shares. | |

July 2, 1998 | Received a Certificate of Arrangement in connection with the Plan of Arrangement between TransCanada and NOVA Corporation ("NOVA") through which the companies merged and then split off the commodity chemicals business carried on by NOVA into a separate public company. | |

January 1, 1999 | Received a Certificate of Amalgamation reflecting TransCanada's vertical short form amalgamation with a wholly-owned subsidiary, Alberta Natural Gas Company Ltd. | |

January 1, 2000 | Received a Certificate of Amalgamation reflecting TransCanada's vertical short form amalgamation with a wholly-owned subsidiary, NOVA Gas International Ltd. |

Unless the context indicates otherwise, a reference in this Annual Information Form to "TransCanada" includes TransCanada PipeLines Limited and the subsidiaries through which its various business operations are conducted.

TransCanada's registered office and executive office are located at 450 - 1st Street S.W., Calgary, Alberta, T2P 5H1.

At Year End, TransCanada had approximately 2,475 employees in Canada and the United States, with two employees posted abroad under contract.

TransCanada's significant subsidiaries at Year End are noted below. The list excludes certain of TransCanada's subsidiaries where:

- •

- the total assets and total revenue of the individual excluded subsidiaries do not constitute more than ten percent of the consolidated assets and revenues of TransCanada at the most recent year end; and

- •

- the aggregate assets and operating revenues of the excluded subsidiaries represent less than 20-percent of the consolidated assets and revenues of TransCanada at the most recent year end.

| Subsidiary(1) | Organized Under the Laws of | Percentage Ownership by TransCanada of Voting Shares | |||

|---|---|---|---|---|---|

| NOVA Gas Transmission Ltd. | Alberta | 100 | |||

TransCanada PipeLine USA Ltd. | Nevada | 100 | |||

| TransCanada Energy USA Inc. | Delaware | 100 | |||

701671 Alberta Ltd. | Alberta | 100 | |||

| TransCanada Energy Ltd. | Canada | 100 | |||

Note:

- (1)

- Names shown without indentation are direct subsidiaries of TransCanada. The indentation of the name of a subsidiary indicates that such subsidiary is held by a subsidiary of TransCanada. The percentage ownership shown for a subsidiary is the share in that subsidiary held directly by its immediate parent.

TRANSCANADA PIPELINES LIMITED 1

This Annual Information Form has been prepared to reflect the presentation of TransCanada's continuing operations and its discontinued operations as they are presented in TransCanada's 2002 Audited Consolidated Financial Statements. The MD&A, together with Notes 1, 2, 18 and 19 of TransCanada's 2002 Audited Consolidated Financial Statements as found in the Annual Report, are hereby incorporated by reference.

GENERAL DEVELOPMENT OF THE BUSINESS

The general development of TransCanada's business during the last three financial years, and the significant events or conditions which have had an influence on that development, are summarized below. Most of these events are discussed in greater detail under the heading "Business of TransCanada" in this Annual Information Form.

TransCanada has substantial Canadian natural gas pipeline holdings, including:

- •

- a Canadian mainline natural gas transmission system (the "Canadian Mainline");

- •

- a natural gas transmission system throughout the province of Alberta (the "Alberta System");

- •

- a natural gas transmission system in southeastern British Columbia (the "BC System");

- •

- a 50-percent interest in Foothills Pipe Lines Ltd. ("Foothills");

- •

- both directly and through its interest in Foothills,

- •

- a 69.5-percent interest in Foothills Pipe Lines (Sask.) Ltd.,

- •

- a 74.5-percent interest in Foothills Pipe Lines (Alta.) Ltd., and

- •

- a 74.5-percent interest in Foothills Pipe Lines (South B.C.) Ltd.,

(collectively, the "Foothills System"); and

- •

- a 50-percent interest in Trans Québec & Maritimes Pipeline Inc. ("TQM").

TransCanada's natural gas pipeline holdings in the United States include:

- •

- a 50-percent interest in Great Lakes Gas Transmission Limited Partnership ("Great Lakes");

- •

- a 40.96-percent interest in the Iroquois Gas Transmission System ("Iroquois");

- •

- a 33.29-percent interest in the Portland Natural Gas Transmission System ("Portland");

- •

- a 12.25-percent voting interest in Northern Border Pipeline Company ("Northern Border"); and

- •

- a one-percent interest in Tuscarora Gas Transmission Company ("Tuscarora").

TC PipeLines, LP is a publicly held limited partnership of which TransCanada holds indirectly a 33.4-percent interest and of which TransCanada, through a subsidiary, acts as the general partner. TC PipeLines, LP holds:

- •

- a 30-percent interest in Northern Border; and

- •

- a 49-percent interest in Tuscarora.

Developments in 2002 — Transmission Business

In August 2002, TransCanada completed the acquisition of a portion of the two-percent general partnership interest in Northern Border Partners, L.P. ("NBPLP"), a publicly held limited partnership. This acquisition provides TransCanada with a 17.5-percent voting interest on the partnership policy committee of NBPLP.

2 TRANSCANADA PIPELINES LIMITED

NBPLP owns interests in pipelines and gas processing plants in the United States and Canada, including a 70-percent interest in Northern Border.

TransCanada owns and/or operates (or has under construction) a number of power plants, and purchases power under a number of power purchase arrangements. TransCanada's power plants and power purchase arrangements, in the aggregate, represent in excess of 4,000 megawatts ("MW") of power generation capacity.

TransCanada holds a 35.6-percent interest in, and is the general partner of, TransCanada Power, L.P. ("Power LP"), with the remaining interest being widely held by the public. Power LP owns seven power plants which are managed by subsidiaries of TransCanada.

Developments in 2002 — Power Business

In November 2002, TransCanada completed the acquisition of the 300 MW ManChief power plant, situated approximately 145 kilometres northeast of Denver, Colorado. The ManChief power plant is operated under contract by an unaffiliated third party.

In December 2002, TransCanada announced that it had, as part of a consortium, reached an agreement for the acquisition of a 31.6-percent interest in Bruce Power L.P. ("Bruce Power") and an approximate 33.3-percent interest in Bruce Power Inc., the general partner of Bruce Power. The acquisition was completed on February 14, 2003. Bruce Power leases its generation facilities from Ontario Power Generation Inc. ("OPG"). The facilities consist of eight nuclear reactors, four of which are currently operational with a capacity of 3,140 MW. It is anticipated that two of the four idle reactors will be restarted by mid-2003, adding additional capacity of approximately 1,500 MW.

The members of the purchasing consortium of Bruce Power have severally, on a pro-rata basis, guaranteed certain contingent financial obligations of Bruce Power related to operator licenses, the lease agreement, power sales agreements and contractor services. Bruce Power will continue to be operated by its current management which is comprised of experienced nuclear operators. Spent fuel and decommissioning liabilities remain with OPG under the terms of the lease.

Also in December 2002, TransCanada and OPG announced the formation of an equal limited partnership called Portlands Energy Centre L.P. ("PEC"). The partnership will assess the viability of developing a natural gas-fuelled energy centre at OPG's former R.L. Hearn Generating Station in the Portlands area of the downtown waterfront in Toronto, Ontario. As currently envisaged, PEC would construct a 550 MW combined cycle natural gas-fuelled cogeneration facility.

Developments in 2003 — Corporate

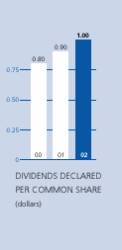

On January 28, 2003, the Board of Directors approved an increase in TransCanada's quarterly dividend on common shares from $0.25 to $0.27 per quarter for the quarter ending March 31, 2003.

On February 25, 2003, Board of Directors unanimously recommended that common shareholders vote in favor of a plan of arrangement to establish a holding company — named TransCanada Corporation — as TransCanada's parent. Upon the plan of arrangement becoming effective, existing common shareholders of TransCanada exchange each of their common shares for one common share of TransCanada Corporation; TransCanada Corporation will then hold all of the common shares of TransCanada; and the assets and liabilities of TransCanada remain with TransCanada. Establishing the holding company addresses a covenant contained in trust indentures governing some of TransCanada's debt securities that could limit the company's ability to pay dividends if it invests in certain businesses. This plan of arrangement is subject to approval by the common shareholders of TransCanada, and certain legal and regulatory approvals.

TRANSCANADA PIPELINES LIMITED 3

The following table shows TransCanada's revenues from continuing operations by segment, classified geographically, for the years ended December 31, 2002 and 2001.

| | 2002 | 2001 | |||

|---|---|---|---|---|---|

| | (millions of dollars) | (millions of dollars) | |||

| Transmission | |||||

| Canada — Domestic Deliveries | 2,076 | 2,469 | |||

| Canada — Export Deliveries(1) | 1,641 | 1,239 | |||

| United States | 204 | 172 | |||

| 3,921 | 3,880 | ||||

Power | |||||

| Canada — Domestic Deliveries | 655 | 834 | |||

| Canada — Export Deliveries(1) | — | 90 | |||

| United States | 638 | 471 | |||

| 1,293 | 1,395 | ||||

| Total Revenues(2) | 5,214 | 5,275 | |||

Notes:

- (1)

- Export deliveries are deliveries to customers serving United States markets.

- (2)

- Revenues are attributed to countries, based on country of origin of product or service.

TransCanada's transmission business includes the operation of the Canadian Mainline, the Alberta System, the BC System, and TransCanada's other investments in natural gas pipelines located in Canada and the United States.

Canadian natural gas transmission services are provided under gas transportation tariffs that provide for cost recovery and return on investment as approved by the applicable regulatory authorities. In some cases, such tariffs are determined under agreements with customers and other interested parties, subject to regulatory approval. The net income of the transmission business is generated based on such tariffs. Net income is not directly affected by fluctuations in the commodity price of natural gas, but such fluctuations influence both production levels and the natural gas basin from which North American natural gas users elect to purchase natural gas supplies. Under the current regulatory model, TransCanada's net income from its wholly-owned pipelines is not materially affected by fluctuations in throughput.

The volume of natural gas shipments on the Alberta System, the Canadian Mainline, and the BC System depends on the volume of natural gas produced and sold both in and outside of Alberta, and on the construction and availability of other pipeline capacity. The natural gas transported by TransCanada comes primarily from the Western Canada Sedimentary Basin ("WCSB"). Based on TransCanada's 2001 year-end estimates, the WCSB had remaining established reserves of natural gas of approximately 56 trillion cubic feet ("Tcf") with a remaining reserves-to-production ratio of approximately nine years at current levels of production. Incremental reserves are continually being discovered, and generally maintain the reserve-to-production ratio at close to nine years. Production of natural gas from the WCSB has increased fifteen percent overall since 1995. With the expansion of capacity on TransCanada's wholly and partly owned pipelines over the past decade and the competition provided by other pipelines, combined with significant growth in natural gas demand in Alberta, TransCanada anticipates there will be excess pipeline capacity out of the WCSB for the next several years.

In addition to the information concerning the transmission segment of TransCanada's business set out herein, further information is found in the MD&A under the heading "Transmission — Wholly-Owned Pipelines — Business Risks".

4 TRANSCANADA PIPELINES LIMITED

Alberta System

The Alberta System — held by NOVA Gas Transmission Ltd. ("NGTL"), a wholly-owned subsidiary of TransCanada — is an Alberta-wide natural gas transmission system that collects and transports natural gas for use in Alberta and for delivery to connecting pipelines, such as the Canadian Mainline, the Foothills System and the BC System, as well as to other unaffiliated pipelines, at the Alberta border for delivery to eastern Canada, British Columbia and the United States. The Alberta System includes approximately 22,700 kilometres of mainlines and laterals.

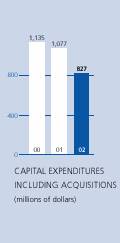

Capital expenditures, which are dependent in part upon requests for increased transportation service by customers, were $165 million in 2002. TransCanada anticipates approximately $121 million of capital spending on the Alberta System in 2003. As in 2002, these capital expenditures will be primarily related to capacity expansion.

The following table sets forth the annual volumes delivered off the Alberta System for the years ended December 31, 2002 and 2001.

| | 2002 | 2001 | ||||||

|---|---|---|---|---|---|---|---|---|

| Delivery Points | ||||||||

| Volume(1) | Percent | Volume(2) | Percent | |||||

| | (Bcf) | | (Bcf) | | ||||

| Alberta | 475 | 11 | 423 | 10 | ||||

| Eastern Canada and Eastern United States | 1,738 | 42 | 1,665 | 41 | ||||

| Western United States | 750 | 18 | 833 | 21 | ||||

| Midwestern United States | 1,156 | 28 | 1,097 | 27 | ||||

| British Columbia | 28 | 1 | 41 | 1 | ||||

| Total | 4,146 | 100 | 4,059 | 100 | ||||

Notes:

- (1)

- Of the total volumes transported in 2002, 2.09 Tcf of natural gas was delivered to the Canadian Mainline, 773 Bcf of natural gas was delivered to the BC System (including Foothills South B.C. Ltd.) and 779 Bcf of natural gas was delivered to the Foothills System.

- (2)

- Of the total volumes transported in 2001, 1.99 Tcf of natural gas was delivered to the Canadian Mainline, 855 Bcf of natural gas was delivered to the BC System (including Foothills South B.C. Ltd.) and 762 Bcf of natural gas was delivered to the Foothills System.

Alberta System Contracted Firm Transportation Services

As of Year End, the Alberta System was providing transportation for 232 shippers pursuant to approximately 17,240 firm service transportation contracts.

As of Year End, the weighted average remaining term of transportation contracts was approximately three years. Currently, these contracts are renewable by the customer by providing notice to NGTL at least twelve months prior to the expiry of the current contract term. The Alberta System has seen a 21-percent decrease in firm contracted capacity since the 1998-1999 contract year; and over the same period, total deliveries of natural gas in Alberta decreased by nine percent. For further information on the Alberta System, refer to the heading "Transmission — Wholly-Owned Pipelines — Business Risks" in the MD&A.

Regulation of the Alberta System

The construction and operation of the Alberta System is regulated by the Alberta Energy and Utilities Board (the "Alberta Regulator") primarily under the provisions of theGas Utilities Act (Alberta) and thePipeline Act (Alberta). NGTL also requires the Alberta Regulator's approval for rates, tolls and charges, and the terms and conditions under which it provides its services. Under the provisions of thePipeline Act, the Alberta Regulator oversees various matters, including the economic, orderly and efficient development of the pipeline, the operation and abandonment of the pipeline, and certain related pollution and environmental conservation

TRANSCANADA PIPELINES LIMITED 5

issues. In addition to requirements under thePipeline Act, the construction and operation of natural gas pipelines in Alberta are subject to certain provisions of, and require certain approvals under, other provincial legislation such as theEnvironmental Protection and Enhancement Act (Alberta).

Alberta System tolls are designed to generate sufficient revenues for TransCanada to recover operating expenses, depreciation, taxes and financing costs of the Alberta System, including interest on debt and payments on securities attributable to the Alberta System, together with a return on deemed common equity.

In 2001 the Alberta System Rate Settlement ("ASRS") was negotiated with shippers and other interested parties for the years 2001 and 2002. Under the ASRS, approved by the Alberta Regulator on May 29, 2001, the revenue to be collected for services provided was fixed for each year, subject to a number of adjustments, including adjustments for taxes, variances from previous agreements, pipe integrity spending and the costs associated with providing service to the Fort McMurray area. The rates were determined by the fixed revenue (subject to the adjustments above) and throughput. The ASRS also enabled the Alberta System to offer two new services: a service to meet shippers' one-year firm service requirements, and another to meet short-haul, point-to-point transportation needs within the province. The ASRS also provided TransCanada with an incentive to reduce costs below the fixed revenue requirement, by accruing any savings to TransCanada's account.

On December 31, 2002, the Alberta Regulator approved interim rates effective January 1, 2003, which will remain in place until final 2003 rates are determined. On January 23, 2003, NGTL filed a tariff application with the Alberta Regulator requesting modifications to intra-Alberta delivery service tolls to reflect better the actual costs that such deliveries impose on the Alberta System, and two new services to enhance the Alberta System's competitive position. On February 7, 2003, TransCanada announced a one year settlement with customers and other interested parties regarding NGTL's 2003 revenue requirement. NGTL expects to file an application for approval of the settlement and final 2003 rates with the Alberta Regulator by February 28, 2003.

Tolling Methodology for the Alberta System

The current tolling methodology and rate design for the Alberta System features differentiated pricing for each gas receipt-point on the Alberta System. The receipt-point price is dependent on geographic location, the diameter of the pipe through which the customer's gas travels and the term of the transportation contract.

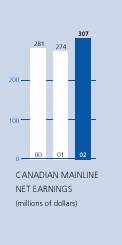

Canadian Mainline

The Canadian Mainline consists of approximately 14,900 kilometres of pipeline system transporting natural gas from the Alberta border east to various delivery points in Canada and at the United States border.

Capital expenditures on the Canadian Mainline in 2002 were approximately $57 million. These expenditures were primarily maintenance related. TransCanada anticipates approximately $76 million of capital spending on the Canadian Mainline in 2003. These capital expenditures will also be primarily maintenance related.

6 TRANSCANADA PIPELINES LIMITED

The following table sets forth the revenues earned and volumes delivered for the years ended December 31, 2002 and 2001 for the Canadian Mainline.

| | 2002 | 2001 | ||||||

|---|---|---|---|---|---|---|---|---|

| | Revenues(1) | Percent | Revenues | Percent | ||||

| Revenues | (millions of dollars) | | (millions of dollars) | | ||||

| Domestic | 610 | 28 | 973 | 45 | ||||

| Export | 1,568 | 72 | 1,168 | 55 | ||||

| Total | 2,178 | 100 | 2,141 | 100 | ||||

| | 2002 | 2001 | ||||||

|---|---|---|---|---|---|---|---|---|

Volume(2) | Percent | Volume(3) | Percent | |||||

| Volumes Transported | (Bcf) | | (Bcf) | | ||||

| Domestic | 1,223 | 47 | 1,216 | 50 | ||||

| Export | 1,407 | 53 | 1,234 | 50 | ||||

| Total | 2,630 | 100 | 2,450 | 100 | ||||

Notes:

- (1)

- Domestic revenue was reduced as a result of transportation service credits introduced in 2002. Total credits of $662 million were reported within 2002 domestic revenues.

- (2)

- Effective December 2001, TransCanada sold the subsidiary referred to in note 3, and therefore no volumes were transported for that subsidiary in 2002.

- (3)

- Of the total volumes transported in 2001, 345 Bcf or 14 percent of total volumes were transported for a wholly-owned subsidiary of TransCanada.

Canadian Mainline Contracted Firm Transportation Services

As of Year End, the Canadian Mainline was providing transportation for 118 shippers pursuant to 312 firm service transportation contracts. Approximately 53 percent of the total daily transportation volume represented by these contracts relates to contracts for delivery of natural gas at United States border points.

As of Year End, the weighted average remaining term of firm transportation contracts on the Canadian Mainline was approximately 3.7 years compared to 4.3 years at December 31, 2001. These contracts are renewable by the customer providing notice to TransCanada at least six months prior to the expiry of the current contract term. The Canadian Mainline last operated at capacity with one year or longer firm service contracts during the 1998-1999 contract year. The Canadian Mainline has since seen a 31-percent decrease in firm contracted deliveries and an 11-percent decrease in total deliveries originating at the Alberta border and in Saskatchewan. For further information, refer to the heading "Transmission — Wholly-Owned Pipelines — Business Risks" in the MD&A.

Regulation of the Canadian Mainline

Under the terms of theNational Energy Board Act (Canada), the National Energy Board (the "Federal Regulator") regulates the construction, operation, tolls and tariffs of the Canadian Mainline. The Federal Regulator is a responsible authority under theCanadian Environmental Assessment Act to consider the environmental and social impacts of proposed pipeline projects. The Canadian Mainline tolls are designed to generate sufficient revenues for TransCanada to recover operating expenses, depreciation, taxes and financing costs of the Canadian Mainline, including interest on debt and payments on preferred securities attributable to the Canadian Mainline, together with a return on deemed common equity.

The tolls are composed of a demand charge component and a commodity charge component. The demand charge is independent of the volumes shipped and is designed to recover fixed costs, such as fixed operating expenses, financing costs (including a return on deemed common equity), taxes and depreciation. The

TRANSCANADA PIPELINES LIMITED 7

commodity charge is designed to recover variable operating costs. These charges are paid by shippers under transportation contracts with TransCanada.

In November 2001 the Federal Regulator approved the 2001 and 2002 Canadian Mainline Service and Pricing Settlement ("S&P Settlement"). The S&P Settlement featured:

- •

- a two-year term that expired on December 31, 2002;

- •

- a cost of service framework;

- •

- revenue requirement components, excluding cost of capital, and certain cost and revenue incentives that provided mutual benefits for TransCanada and its shippers;

- •

- enhancements to firm transportation service through the implementation of firm transportation make-up and authorized overrun service credits; and

- •

- a framework for resolving several rate design and service issues during its term.

In June 2002, the Federal Regulator denied TransCanada's request to adopt an after-tax weighted average cost of capital methodology for establishing investment return and an after-tax weighted average cost of capital of 7.5 percent, equivalent to a 12.5 percent rate of return on deemed common equity of 40 percent. The Federal Regulator instead affirmed a formula established in 1995 for setting return on common equity. Under this formula, the rate of return on common equity for the Canadian Mainline was 9.61 percent in 2001 and 9.53 percent in 2002. The Federal Regulator increased deemed common equity to 33 percent from the previously approved level of 30 percent.

In September 2002, TransCanada filed an application with the Federal Regulator for new tolls on the Canadian Mainline to be effective January 1, 2003. The proposed new tolls include a requested increase in depreciation rates. Such increase is proposed to reflect better the risk of recovery of TransCanada's investments in the Canadian Mainline and to be fair to both current and future shippers. Concurrently, TransCanada filed an application with the Federal Regulator to review and vary its June 2002 decision respecting TransCanada's cost of capital for 2001 and 2002, which was declined by the Federal Regulator in a decision released February 20, 2003. On December 6, 2002, the Federal Regulator approved interim rates effective January 1, 2003, which will remain in place until final 2003 tolls are determined.

BC System

The BC System consists of approximately 200 kilometres of pipeline that carries natural gas from a connecting point with the Alberta System through the southeastern corner of British Columbia to connect with unaffiliated pipeline systems which further connect to California and the northwestern United States.

In 2002, capital expenditures on the BC System were approximately $50 million, primarily for capacity expansion. TransCanada anticipates approximately $3 million of capital spending on the BC System in 2003, primarily for capital maintenance.

The BC System is regulated by the Federal Regulator on a complaint basis and the tolls are based on a cost-of-service methodology. In December 2002, the Federal Regulator adopted interim rates and charges for 2003 pending the resolution of certain issues with shippers on the BC System.

TransCanada actively pursues gas pipeline and pipeline-related development, acquisition and operation opportunities in Canada and the United States, where these opportunities are driven by strong customer demand.

8 TRANSCANADA PIPELINES LIMITED

Great Lakes

Great Lakes, a 3,387-kilometre pipeline system in which TransCanada holds a 50-percent interest, transports Canadian natural gas from its interconnection with the Canadian Mainline at Emerson, Manitoba to markets in central Canada at St. Clair, Ontario and serves markets in the eastern and midwestern United States. Great Lakes has received approval from the U.S. Federal Energy Regulatory Commission (the "US Regulator") regarding a settlement agreement on its rates through to October 31, 2005.

TC PipeLines, LP

TC PipeLines, LP, a U.S. publicly-held limited partnership, was formed to acquire, own and participate in the management of U.S.-based pipeline assets. In May 1999, TransCanada's 30-percent general partner interest in Northern Border was conveyed to TC PipeLines, LP in exchange for cash and a 33.4-percent interest in TC PipeLines, LP, 31.4 percent of which is comprised of common units and subordinated units, and two percent of which is a general partnership interest. TC PipeLines, LP also issued common units to the public. Northern Border, in which TransCanada now indirectly holds an approximate ten percent interest through its investment in TC PipeLines, LP, operates a 2,010-kilometre natural gas pipeline system which connects with the Foothills System in Saskatchewan and serves the midwestern United States, terminating at North Hayden, Indiana. In October 2001, Northern Border completed a 55-kilometre pipeline extension and installed additional compression that provides 545 MMcf/d of incremental transportation capacity to North Hayden, Indiana and expands Northern Border's delivery capability into the Chicago area by approximately 30 percent.

On September 1, 2000, TC PipeLines, LP acquired a 49-percent general partner interest in Tuscarora from TransCanada, and TransCanada, through a wholly-owned subsidiary, retains a one-percent general partner interest in Tuscarora. Tuscarora is a 386-kilometre natural gas pipeline system which has been in operation since December 1995. This system transports natural gas from Malin, Oregon to Wadsworth, Nevada and delivers to points in northeastern California. The Hungry Valley lateral extension, Tuscarora's second city-gate connection into Reno, Nevada, was completed in January 2001. On December 1, 2002, Tuscarora completed construction and placed into service an expansion of its pipeline system, consisting of two compressor stations and a 17-kilometre pipeline extension from the previous terminus near Reno, Nevada to Wadsworth, Nevada. The expansion serves growing power generation and residential requirements in northern Nevada. Tuscarora's current capacity is approximately 182 MMcf/d.

A subsidiary of TransCanada acts as the general partner of TC PipeLines, LP.

Iroquois

Iroquois connects with the Canadian Mainline in eastern Ontario. This 604-kilometre pipeline delivers gas to customers in the northeastern United States and currently terminates on Long Island, New York. TransCanada's total interest in Iroquois, through two wholly-owned subsidiaries, is 40.96 percent. Iroquois has a settlement agreement on a rate structure with the US Regulator effective until January 1, 2004.

Construction on Iroquois' Eastchester expansion is underway and partially complete. Portions of the project's compression additions went into service in November 2002 with the remainder of the project anticipated to be completed mid-2003. This extension will extend Iroquois' system from Long Island into New York City and will provide an additional 230 MMcf/d of new service into this market.

Trans Québec & Maritimes

TransCanada holds a 50-percent interest in the 572-kilometre TQM pipeline, which connects with the Canadian Mainline. TQM serves markets in Québec and connects with the Portland system. In 2002, TransCanada agreed to provide various operating and administrative services to TQM effective January 2003.

Portland

TransCanada's 33.29-percent interest in Portland is held through two wholly-owned subsidiaries. Portland is a 471-kilometre interstate pipeline that interconnects with the pipeline system of TQM at the United States/

TRANSCANADA PIPELINES LIMITED 9

Canadian border at Pittsburg, New Hampshire and with the Tennessee Gas Pipeline in Haverhill and Dracut, Massachusetts. The southern sections of Portland, consisting of 163 kilometres, are part of the joint facilities shared with Maritimes and Northeast Pipeline. Portland holds a one-third ownership interest in the joint facilities.

Portland filed a rate application with the US Regulator in October 2001 which was accepted and went into effect subject to refund in April 2002. Portland and customer representatives reached an agreement on new rates and Portland submitted an uncontested agreement to the US Regulator in October 2002, which was approved in its entirety in January 2003.

Foothills System

The Foothills System is a 1,040-kilometre natural gas pipeline that transports western Canadian natural gas from central Alberta to connecting pipelines for transportation to markets in the United States.

Northern Development

TransCanada is actively pursuing northern gas development opportunities. Foothills holds the regulatory certificate for the Canadian portion of the Alaska Highway project, and together, TransCanada and Foothills hold the Alaskan certificate for the project. TransCanada believes that the Alaska Natural Gas Transportation System ("ANGTS") has significant advantages over alternative proposals to deliver Alaskan gas to market, and that a successful completion of the project would meet the needs of both the Alaskan producers and North American consumers.

TransCanada continues to work with Mackenzie Delta producers in Canada to bring Mackenzie Delta natural gas to market by accessing gas resources through new pipeline infrastructure in the Northwest Territories which would connect to the Alberta System.

Ventures LP

TransCanada Pipeline Ventures Limited Partnership ("Ventures LP") is a business created by TransCanada to provide energy solutions for its customers operating in the WCSB. It currently owns two natural gas pipelines providing service from the Alberta System, one to the Fort McMurray oil sands region in northern Alberta, and the other to a large petrochemical complex at Joffre, Alberta.

CrossAlta

TransCanada holds a 60-percent interest in Crossfield Storage Joint Venture and is thereby entitled to a proportional share of the earnings of CrossAlta Gas Storage & Services Ltd., which owns a gas storage facility near Crossfield, Alberta.

TransGas

TransCanada holds a 46.5-percent interest in TransGas de Occidente S.A. ("TransGas"), a 344-kilometre natural gas pipeline, extending from Mariquita to Cali, Colombia. TransCanada is also the operator of TransGas.

Regulation of North American Pipelines

The operations of TQM and the Foothills System and their subsidiaries are regulated by the Federal Regulator. The Foothills System is also regulated by the Northern Pipeline Agency of Canada. Under theNational Energy Board Act (Canada), the Federal Regulator regulates the construction and operation of interprovincial pipelines and the Canadian portion of international pipelines. The Federal Regulator also approves pipeline tolls and the import and export of natural gas.

The construction and operations of Ventures LP's Fort McMurray oilsands pipeline and Joffre pipeline are regulated by the Alberta Regulator.

10 TRANSCANADA PIPELINES LIMITED

With respect to TransCanada's United States pipeline investments, theNatural Gas Act of 1938 ("NGA") establishes the framework for regulation of interstate natural gas transportation, facilities construction and terms and conditions of service. The US Regulator is charged with implementing the NGA's requirements. The volumes of natural gas transported for TransCanada on Great Lakes are subject to NGA authorizations issued by the US Regulator. Interconnected natural gas pipelines and other United States interstate pipeline projects in which TransCanada has investments are subject to the US Regulator and NGA regulation, as well as certain state regulatory requirements.

The cross-border import and export of natural gas is subject to authorizations granted by the Federal Regulator and the United States Department of Energy.

All three of TransCanada's wholly-owned pipelines are connected to and supplied by one of North America's largest natural gas basins, the WCSB. However, the WCSB is maturing and it will be a challenge for producers to increase production in this basin. Other pipeline systems connected to the WCSB, including some of TransCanada's interconnected pipelines, have expanded in the last few years. These expansions have provided shippers with additional flexibility and competitive choices when moving WCSB supplies to market. The WCSB gas supply is not expected to increase.

The Alberta System is the primary transporter of natural gas within the province of Alberta and to provincial boundary points. However, a number of alternative pipelines have been constructed which seek to offer price advantages and provide competition to the Alberta System. The Alliance Pipeline went into service in December 2000, and competes for supply directly with the Alberta System, the Canadian Mainline, Foothills and Northern Border pipelines. AltaGas Services' short-haul South Suffield and North Suffield bypass pipelines went into service in 2000 and 2001, respectively, and both connect with TransCanada's Canadian Mainline. These short-haul bypasses account for less than five percent of the Alberta System's throughput. The Alberta System also faces increased competition from other pipelines.

In anticipation of and in response to these developments, the Alberta System's current tolling methodology was designed to enhance TransCanada's ability to provide competitive pricing and service flexibility and to provide TransCanada with the ability to respond to potential future bypass pipelines through the offering of load retention services.

The Canadian Mainline is now one of three natural gas pipelines providing transportation service directly from the WCSB to eastern Canada and to export points serving the midwestern and northeastern United States. Increased competition has led to the non-renewal of some of the firm service contracts on the Alberta System and the Canadian Mainline, and has led to decreased utilization on certain pipeline segments. The Vector pipeline (in which TransCanada has no ownership interest) went into service in 2000 and provides additional capacity to the Canadian Mainline's core markets in eastern Canada by connecting with the Alliance Pipeline, and other pipelines in Chicago, Illinois. Together, the Alliance pipeline, the Northern Border pipeline and the Vector pipeline form a bypass of the Canadian Mainline for service to Eastern Canadian markets.

For additional information on business risks in Transmission, please see "Transmission — Business Risks" in the MD&A.

In 2002, TransCanada spent approximately $10.6 million on research and development activities of which approximately $1.8 million related to research on pipeline integrity management, approximately $3.9 million on other regulated pipeline activities and approximately $4.9 million on non-regulated pipeline ventures.

The power segment of TransCanada's business includes the construction, ownership, operation and management of power plants and the marketing of electricity, and provides electricity account services to energy and industrial customers. This segment operates in Canada and the United States.

TRANSCANADA PIPELINES LIMITED 11

TransCanada owns and operates:

- •

- a waste-heat fuelled power plant at the Cancarb facility in Medicine Hat, Alberta (27 MW);

- •

- cogeneration plants in Alberta at Carseland (80 MW), Redwater (40 MW), Bear Creek (80 MW) and MacKay River (165 MW — anticipated to be in service in late 2003);

- •

- the Curtis Palmer hydro-electric power facilities near Corinth, New York (60 MW); and

- •

- Ocean State Power in Burrillville, Rhode Island (560 MW).

TransCanada has long-term power purchase arrangements in place for:

- •

- 100-percent of the production of the Sundance A (560 MW) and 50-percent of the production of Sundance B (353 MW of 706 MW) power facilities near Wabamun, Alberta.

TransCanada operates, through Power LP:

- •

- five power plants in Ontario and one in British Columbia (264 MW); and

- •

- one power plant in the United States (64 MW).

TransCanada owns, but does not operate:

- •

- the ManChief power plant near Denver, Colorado (300 MW);

- •

- a 31.6-percent interest in the nuclear power generation facilities of Bruce Power in Ontario (3,140 MW total in operation, plus approximately 1,500 MW total expected to be operational in 2003); and

- •

- a 17-percent interest in Huron Wind L.P. (9 MW total).

TransCanada has a power marketing office in Westborough, Massachusetts to manage the Ocean State Power purchase agreements and market supply obligations, and to take advantage of additional marketing opportunities in the New England and New York markets. The office also markets the output of Power LP's Castleton-on-Hudson power plant.

TransCanada sells the entire output from the Curtis Palmer facilities under a fixed price power purchase agreement with Niagara Mohawk Power Corporation. At current rates of production, the agreement has a remaining term of more than 25 years. In 2000, the Curtis Palmer facility was re-licensed by the US Regulator to operate for a period of 40 years.

Operations and maintenance services for the ManChief power plant will continue to be supplied by the current contracted service provider.

Operations and maintenance services for the Bruce Power plants will continue to be supplied by the current management and staff of Bruce Power.

In December 2002, TransCanada and OPG created a new limited partnership, the Portlands Energy Centre L.P., to study the feasibility of developing a 550 MW combined-cycle natural gas-fuelled cogeneration power plant on a former power generation site in the Portlands area of the Toronto, Ontario downtown waterfront.

TransCanada continues to investigate potential investment opportunities in North America.

TransCanada manages, operates and is the largest unitholder of Power LP, a publicly-held limited partnership that owns seven power plants. TransCanada holds 35.6 percent of the units of Power LP.

Power LP owns combined-cycle power plants — fuelled by a combination of natural gas and waste exhaust heat from adjacent TransCanada compression facilities — in Nipigon, Kapuskasing, North Bay and Tunis, Ontario. It also owns a natural gas cogeneration plant in Castleton-on-Hudson, New York and wood-waste fuelled power plants near Hearst, Ontario and at Williams Lake, British Columbia.

TransCanada supplies the natural gas fuel for certain of Power LP's plants.

12 TRANSCANADA PIPELINES LIMITED

On October 23, 2001, Power LP completed the sale of approximately 5.7 million partnership units from treasury for net proceeds of $166 million, which was used to retire the partnership's long-term debt. This transaction resulted in TransCanada's ownership interest being reduced to 35.6 percent.

Power LP's seven plants have a total generating output of 328 MW. It is the largest publicly traded power income fund in Canada with a market capitalization of approximately $1.2 billion.

The following tables set forth the revenues earned, power volumes marketed and generation capacity in Canada and the United States for the years ended December 31, 2002 and 2001 from TransCanada's power operations.

| | 2002 | 2001 | ||||||

|---|---|---|---|---|---|---|---|---|

| | Revenues | Percent | Revenues | Percent | ||||

| Revenues(1) | (millions of dollars) | | (millions of dollars) | | ||||

| Canada — Domestic | 655 | 51 | 834 | 60 | ||||

| Canada — Export | — | — | 90 | 6 | ||||

| United States | 638 | 49 | 471 | 34 | ||||

| Total | 1,293 | 100 | 1,395 | 100 | ||||

| | 2002 | 2001 | ||||||

|---|---|---|---|---|---|---|---|---|

Volume | Percent | Volume | Percent | |||||

| Volumes Sold(2) | (gigawatt hours) | | (gigawatt hours) | | ||||

| Canada — Domestic | 11,493 | 60 | 10,140 | 71 | ||||

| Canada — Export | 10 | — | 210 | 1 | ||||

| United States | 7,541 | 40 | 3,973 | 28 | ||||

| Total | 19,044 | 100 | 14,323 | 100 | ||||

| | 2002 | 2001 | ||||||

|---|---|---|---|---|---|---|---|---|

Generation | Percent | Generation | Percent | |||||

| Generation Capacity(2)(3)(4)(5) | (megawatts) | | (megawatts) | | ||||

| Canada | 1,404 | 59 | 1,324 | 66 | ||||

| United States | 984 | 41 | 684 | 34 | ||||

| Total | 2,388 | 100 | 2,008 | 100 | ||||

Notes:

- (1)

- Includes TransCanada's revenues generated by Ocean State Power and Power LP (after eliminating intercompany transactions with TransCanada).

- (2)

- Includes 100-percent of volumes sold by, and the generation capacity of, Ocean State Power and Power LP (after eliminating intercompany transactions with TransCanada).

- (3)

- Excludes MacKay River (165 MW) which was under construction at Year End. Construction of the Bear Creek plant (80 MW) was substantially complete by December 31, 2002.

- (4)

- Includes power purchase arrangements from Sundance A (560 MW) controlled by TransCanada and Sundance B (353 MW). TransCanada owns 50-percent of Sundance B's total output of 706 MW through an investment in ASTC Power Partnership.

- (5)

- Excludes the generation capacity of Bruce Power (3,140 MW, plus 1,538 MW anticipated to be on-line mid-2003).

TransCanada's investments in Ocean State Power, Curtis Palmer, ManChief, and TransCanada's United States electric power marketing activities are subject to the jurisdiction of the US Regulator under the U.S. Federal Power Act, as well as the jurisdiction of certain state regulatory authorities.

Deregulation of the power industry is proceeding at different stages throughout most of the markets in which TransCanada currently operates, namely Alberta, Ontario and the northern United States. In 2001, Alberta deregulated its generation assets and opened the market for retailers and wholesalers. In 2002, the Ontario

TRANSCANADA PIPELINES LIMITED 13

government began deregulation of its electricity market but later capped rates for small consumers. This cap does not directly affect the wholesale market where TransCanada is primarily focused.

TransCanada's power business has operated and continues to operate in highly competitive markets that are driven mainly by price. However, the majority of TransCanada's power generation business is underpinned by long-term or medium-term fixed price contracts that are unaffected by short-term price changes in the marketplace. The power industry in North America is currently in the process of deregulation, with various provinces and states at different stages in the process. TransCanada continues to monitor such deregulation and to seek investment opportunities as they arise.

For additional information on business risks in TransCanada's Power business, please see "Power — Business Risks" in the MD&A.

TransCanada owns Cancarb Limited, a thermal carbon black manufacturing facility located in Medicine Hat, Alberta.

TransCanada owns a 50-percent interest in TransCanada Turbines Ltd., a repair and overhaul business for aero-derivative industrial gas turbines. This business operates primarily out of facilities in Calgary, Alberta, with offices in Bakersfield, California; East Windsor, Connecticut; and Liverpool, England.

TransCanada owns 80 percent of TransCanada Calibrations Ltd, a gas meter calibration business certified by Measurement Canada, located at Ile des Chênes, Manitoba.

Between 1999 and 2002, TransCanada continued to focus on natural gas transmission and power generation. During that time, TransCanada sold off substantially all of its assets in international, midstream, and oil and gas marketing businesses that were identified for disposition. For further information on Discontinued Operations please refer to Note 19 of TransCanada's 2002 Audited Consolidated Financial Statements.

As of December 1, 2001, TransCanada sold substantially all of its natural gas marketing and trading operations. TransCanada retains certain contingent liabilities relating to its former gas marketing business due to the refusal of some counterparties to agree to the assignment and novation of its contracts to the purchasers of the assets. The exposures relating to these contracts are declining as the terms of the contracts expire.

TransCanada's international transmission, processing and power generation operations were focused primarily in Latin America, Europe and Asia Pacific. In December 1999, TransCanada announced its intention to exit from all of its international operations and during 2000 and 2001 sold the majority of its international businesses and assets, leaving, as at February 25, 2003, the following discontinued international operations remaining to be sold.

14 TRANSCANADA PIPELINES LIMITED

Latin America

TransCanada holds:

- •

- a 30-percent interest in Gasoducto del Pacifico ("Gas Pacifico"), a 540-kilometre natural gas pipeline from Argentina to Concepción, Chile; and

- •

- a 30-percent interest in INNERGY Holdings S.A., an industrial natural gas transportation and marketing company operating in the Concepción, Chile region, which transports gas on the Gas Pacifico system.

Asia Pacific

TransCanada holds an indirect ten percent interest in PT Paiton Energy Company, which owns a power project consisting of two 615-megawatt coal-fired power units located in Indonesia.

Regulation in International

The majority of countries in which TransCanada continues to have business interests have various government entities in charge of drafting and implementing the policies and regulations with respect to exploration, production, transportation, refining, processing and distribution of hydrocarbons, as well as all other activities related to the energy sector.

Competition in International

TransCanada's international businesses are conducted in a highly competitive environment, comprised of major energy companies and consortia with years of international experience and established relationships. Projects were generally awarded by way of international tender.

International Business Risks

TransCanada's international investments are subject to a number of risks unique to international business. These risks include exchange controls and fluctuation of the local currency, political risk, community actions, changes in laws, price control, the availability and quality of local labour skills, and labour unrest, among others. Such risks are mitigated by insurance policies, participation of local and foreign partners, prudent commercial structuring and other measures.

In 2000 and 2001, TransCanada sold substantially all of its portfolio of natural gas gathering, processing, straddle plant and extraction assets in Alberta, British Columbia and Saskatchewan.

During 2002, the Harmattan gas plant was TransCanada's only remaining midstream asset. Although a purchase and sale agreement for the plant was signed in 2001, an unrelated third party initiated litigation which delayed the sale. The litigation was settled in late 2002, and the sale closed in January 2003.

HEALTH, SAFETY AND ENVIRONMENT

TransCanada is committed to providing a safe and healthy environment for its employees and the public, and to the protection of the environment. Health, safety and environment ("HS&E") is a priority in all of TransCanada's operations. The HS&E Committee of the Board of Directors monitors compliance with the TransCanada HS&E corporate policy through regular reporting by the company's department of Community, Safety & Environment. TransCanada's senior executives are also committed to ensuring TransCanada is in compliance with its policies and is an industry leader. Senior executives are regularly advised of all important operational issues and initiatives relating to HS&E.

TRANSCANADA PIPELINES LIMITED 15

TransCanada has an HS&E management system modeled after ISO 14001 elements to facilitate the focus of resources on the areas of greatest risk to the organization's business activities relating to health, safety and environment. It highlights opportunities for improvement, enables the company to work towards defined HS&E expectations and objectives, and provides a competitive business advantage. HS&E audits, management system assessments and planned inspections are used to assess both the effectiveness of implementation of HS&E programs, processes and procedures, and TransCanada's compliance with regulatory requirements.

TransCanada employs full-time staff dedicated to HS&E matters, and incorporates HS&E policies and principles into the planning, development, construction and operation of all its projects. Environmental protection requirements have not had a material impact on the capital expenditures of TransCanada to date; however there can be no assurance that such requirements will not have a material impact on TransCanada's financial or operating results in future years. Such requirements can be dependent on a variety of factors including the regulatory environment in which TransCanada operates.

Environmental initiatives related to climate change are a strategic issue for TransCanada, particularly in light of the Canadian government's ratification of the Kyoto Protocol in December 2002. TransCanada has had a comprehensive climate change strategy in place since 1999, which includes five key areas of activity:

- •

- Participation in policy forums;

- •

- Direct emissions reduction;

- •

- Long term technology development;

- •

- Emissions offset analysis; and

- •

- Pursuit of business opportunities.

Activities in each of these areas occurred in 2002 and will continue in 2003.

In 2002, TransCanada received a fourth consecutive gold level reporting status for its 2002 Voluntary Challenge and Registry ("VCR") report. To achieve gold level status, VCR reports are rated in several categories. Gold level reporters must attain a score of at least 90/100 and must also meet mandatory criteria. Approximately twelve percent of the submissions to the registry have received gold level reporting recognition.

The Kyoto Protocol, ratified by the Canadian Federal Government in December 2002, requires Canada to reduce its greenhouse gas emissions significantly. The Canadian government has not yet provided details on how it intends to meet these reduction targets, and until it does so, TransCanada cannot predict the degree to which it will be affected.

PATENTS, LICENCES AND TRADEMARKS

TransCanada is the beneficial owner and, in some cases, the licencee of a number of trademarks, patents and licences. While these trademarks, patents and licences constitute valuable assets, TransCanada does not regard any single trademark, patent or licence as being material to its operations as a whole.

TransCanada is subject to various legal proceedings and actions arising in the normal course of business. For further information, refer to Note 18 of TransCanada's 2002 Audited Consolidated Financial Statements.

16 TRANSCANADA PIPELINES LIMITED

Three-Year Selected Consolidated Financial Information