Filed by Western Digital Corporation pursuant to Rule 425 under the Securities Act of 1933 and

deemed filed pursuant to Rule 14a-12 of the Securities Exchange Act of 1934

Subject Company: SanDisk Corporation

Commission File No. 000-26734

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 8-K

CURRENT REPORT

Pursuant to Section 13 or 15(d)

of the Securities Exchange Act of 1934

Date of Report (Date of earliest event reported): November 17, 2015

Western Digital Corporation

(Exact Name of Registrant as Specified in its Charter)

| Delaware | 001-08703 | 33-0956711 | ||

(State or other jurisdiction of incorporation) | (Commission File Number) | (IRS Employer Identification No.) |

3355 Michelson Drive, Suite 100 Irvine, California | 92612 | |

| (Address of principal executive offices) | (Zip Code) |

(949) 672-7000

(Registrant’s Telephone Number, Including Area Code)

Not applicable

(Former name or former address, if changed since last report)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions (see General Instruction A.2. below):

x Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425)

¨ Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12)

¨ Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b))

¨ Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c))

| Item 7.01. | Regulation FD Disclosure. |

The management of Western Digital Corporation (“Western Digital” or the “Company”) will be meeting with investors in the United States on November 17, 2015 through November 19, 2015, to present its views on the Company’s proposed acquisition of SanDisk Corporation (“SanDisk”), as well as other recent announcements by the Company, including the planned investment in Western Digital by Unisplendour Corporation Limited (“Unis”), the integration decision by the Ministry of Commerce of the People’s Republic of China and the joint venture of Western Digital with Unis and its subsidiary, Unissoft (Wuxi) Group Co., Ltd.

A copy of the materials that may be referenced in these meetings is attached hereto as Exhibits 99.1 and 99.2. From time to time thereafter, Western Digital may continue to use the presentation materials in conversations with investors and analysts.

The information set forth in this Item 7.01, including Exhibits 99.1 and 99.2 hereto, is being “furnished” and shall not be deemed “filed” for purposes of Section 18 of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), or otherwise subject to the liability of such Section, nor shall it be deemed incorporated by reference in any filing made by the Company under the Securities Act of 1933, as amended, or the Exchange Act.

Forward-Looking Statements

This document contains forward-looking statements within the meaning of the federal securities laws. These forward-looking statements include, but are not limited to, statements regarding product and technology positioning, Western Digital’s proposed merger with SanDisk (including financing of the proposed transaction and the benefits, results, effects and timing of a transaction), the investment in Western Digital by Unis, the joint venture with Unis and its subsidiary Unissoft, all statements regarding Western Digital’s (and Western Digital’s and SanDisk’s combined) expected future financial position, results of operations, cash flows, dividends, financing plans, business strategy, budgets, capital expenditures, competitive positions, growth opportunities, plans and objectives of management, and statements containing the use of forward-looking words, such as “may,” “will,” “could,” “would,” “should,” “project,” “believe,” “anticipate,” “expect,” “estimate,” “continue,” “potential,” “plan,” “forecast,” “approximate,” “intend,” “upside,” and the like, or the use of future tense. Statements contained herein concerning the business outlook or future economic performance, anticipated profitability, revenues, expenses, dividends or other financial items, and product or services line growth of Western Digital (and the combined businesses of Western Digital and SanDisk), together with other statements that are not historical facts, are forward-looking statements that are estimates reflecting the best judgment of Western Digital and SanDisk based upon currently available information. Statements concerning current conditions may also be forward-looking if they imply a continuation of current conditions.

Such forward-looking statements are inherently uncertain, and stockholders and other potential investors must recognize that actual results may differ materially from Western Digital’s and SanDisk’s expectations as a result of a variety of factors, including, without limitation, those discussed below. Such forward-looking statements are based upon the current expectations of Western Digital’s and SanDisk’s management and include known and unknown risks, uncertainties and other factors, many of which Western Digital and SanDisk are unable to predict or control, that may cause Western Digital’s or SanDisk’s actual results, performance or plans to differ materially from any future results, performance or plans expressed or implied by such forward-looking statements. These statements involve risks, uncertainties and other factors discussed below and detailed from time to time in Western Digital’s and SanDisk’s filings with the Securities and Exchange Commission (the “SEC”).

Risks and uncertainties related to the proposed merger include, but are not limited to, the risk that SanDisk’s stockholders do not approve the merger or that Western Digital’s stockholders do not approve the issuance of stock in the merger (to the extent such approval is required), potential adverse reactions or changes to business relationships resulting from the announcement, pendency or completion of the merger, uncertainties as to the timing of the merger, the possibility that the closing conditions to the proposed merger may not be satisfied or waived, including that a governmental entity may prohibit, delay or refuse to grant a necessary approval, adverse effects on Western Digital’s stock price resulting from the announcement or completion of the merger, competitive responses to the announcement or completion of the merger, costs and difficulties related to the integration of SanDisk’s businesses and operations with Western Digital’s businesses and operations, the inability to obtain, or delays in obtaining, cost savings and synergies from the merger, uncertainties as to whether the completion of the merger or any transaction will have the accretive effect on Western Digital’s earnings or cash flows that it expects, unexpected costs, liabilities, charges or expenses resulting from the merger, litigation relating to the merger, the inability to retain key personnel, and any changes in general economic and/or industry-specific conditions.

In addition to the factors set forth above, other factors that may affect Western Digital’s or SanDisk’s plans, results or stock price are set forth in Western Digital’s and SanDisk’s respective filings with the SEC, including Western Digital’s and SanDisk’s most recent Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q and Current Reports on Form 8-K.

Many of these factors are beyond Western Digital’s and SanDisk’s control. Western Digital and SanDisk caution investors that any forward-looking statements made by Western Digital or SanDisk are not guarantees of future performance. Neither Western Digital nor SanDisk intend, or undertake any obligation, to publish revised forward-looking statements to reflect events or circumstances after the date of this document or to reflect the occurrence of unanticipated events.

Important Additional Information and Where to find It

This communication does not constitute an offer to sell or the solicitation of an offer to buy any securities or a solicitation of any vote or approval. This communication may be deemed to be solicitation material in respect of the proposed merger between Western Digital and SanDisk. In connection with the proposed merger, Western Digital intends to file a registration statement on Form S-4 with the SEC that contains a preliminary joint proxy statement of SanDisk and Western Digital that also constitutes a preliminary prospectus of Western Digital. After the registration statement is declared effective, Western Digital and SanDisk will mail the definitive joint proxy statement/prospectus to their respective stockholders. This material is not a substitute for the joint proxy statement/prospectus or registration statement or for any other document that Western Digital or SanDisk may file with the SEC and send to Western Digital’s and/or SanDisk’s stockholders in connection with the proposed merger. INVESTORS AND SECURITY HOLDERS OF WESTERN DIGITAL AND SANDISK ARE URGED TO READ ALL RELEVANT DOCUMENTS FILED WITH THE SEC, INCLUDING THE JOINT PROXY STATEMENT/PROSPECTUS, BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION ABOUT THE PROPOSED MERGER. Investors and security holders will be able to obtain copies of the joint proxy statement/prospectus (when filed) as well as other filings containing information about Western Digital and SanDisk, without charge, at the SEC’s website, http://www.sec.gov. Copies of the documents filed with the SEC by Western Digital will be available free of charge on Western Digital’s website at http://www.wdc.com. Copies of the documents filed with the SEC by SanDisk will be available free of charge on SanDisk’s website at http://www.sandisk.com.

Participants in Solicitation

Western Digital, SanDisk and their respective directors, executive officers and certain other members of management and employees may be soliciting proxies from their respective stockholders in favor of the proposed transaction. Information regarding the persons who may, under the rules of the SEC, be considered participants in the solicitation of stockholders in connection with the proposed transaction will be set forth in the joint proxy statement/prospectus when it is filed with the SEC. You can find information about Western Digital’s executive officers and directors in Western Digital’s definitive proxy statement filed with the SEC on September 23, 2015. You can find information about SanDisk’s executive officers and directors in its definitive proxy statement filed with the SEC on April 27, 2015. You can obtain free copies of these documents from Western Digital and SanDisk, respectively, using the contact information above. Investors may obtain additional information regarding the interest of such participants by reading the joint proxy statement/prospectus regarding the proposed merger when it becomes available.

| Item 9.01. | Financial Statements and Exhibits. |

(d) Exhibits

Exhibit No. | Description | |

| 99.1 | Presentation regarding Acquisition of SanDisk. | |

| 99.2 | FAQ on Topics of Interest. | |

2

SIGNATURE

Pursuant to the requirements of the Securities Exchange Act of 1934, the Registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

| Western Digital Corporation | ||||||

| Date: November 16, 2015 | By: | /s/ Michael C. Ray | ||||

Michael C. Ray Executive Vice President, Chief Legal Officer and Secretary | ||||||

3

Exhibit 99.1

|

Western Digital’s Acquisition of SanDisk

Non-Deal Roadshow

NOVEMBER 17-19, 2015

|

Safe Harbor/Disclaimers

Forward-Looking Statements

This document contains forward-looking statements within the meaning of the federal securities laws. These forward-looking statements include, but are not limited to, statements regarding product and technology positioning, the proposed merger of Western Digital Corporation (“Western Digital”) with SanDisk Corporation (“SanDisk”) (including financing of the proposed transaction and the benefits, results, effects and timing of a transaction), the investment in Western Digital by Unisplendour Corporation Limited (“Unis”), the joint venture with Unis and its subsidiary Unissoft (Wuxi) Group Co., Ltd. (“Unissoft”), all statements regarding Western Digital’s (and Western Digital’s and SanDisk’s combined) expected future financial position, results of operations, cash flows, dividends, financing plans, business strategy, budgets, capital expenditures, competitive positions, growth opportunities, plans and objectives of management, and statements containing the use of forward-looking words, such as “may,” “will,” “could,” “would,” “should,” “project,” “believe,” “anticipate,” “expect,” “estimate,” “continue,” “potential,” “plan,” “forecast,” “approximate,” “intend,” “upside,” and the like, or the use of future tense. Statements contained herein concerning the business outlook or future economic performance, anticipated profitability, revenues, expenses, dividends or other financial items, and product or services line growth of Western Digital (and the combined businesses of Western Digital and SanDisk), together with other statements that are not historical facts, are forward-looking statements that are estimates reflecting the best judgment of Western Digital and SanDisk based upon currently available information. Statements concerning current conditions may also be forward-looking if they imply a continuation of current conditions.

Such forward-looking statements are inherently uncertain, and stockholders and other potential investors must recognize that actual results may differ materially from Western Digital’s and SanDisk’s expectations as a result of a variety of factors, including, without limitation, those discussed below. Such forward-looking statements are based upon the current expectations of Western Digital’s and SanDisk’s management and include known and unknown risks, uncertainties and other factors, many of which Western Digital and SanDisk are unable to predict or control, that may cause Western Digital’s or SanDisk’s actual results, performance or plans to differ materially from any future results, performance or plans expressed or implied by such forward-looking statements. These statements involve risks, uncertainties and other factors discussed below and detailed from time to time in Western Digital’s and SanDisk’s filings with the Securities and Exchange Commission (the “SEC”).

Risks and uncertainties related to the proposed merger include, but are not limited to, the risk that SanDisk’s stockholders do not approve the merger or that Western Digital’s stockholders do not approve the issuance of stock in the merger (to the extent such approval is required), potential adverse reactions or changes to business relationships resulting from the announcement, pendency or completion of the merger, uncertainties as to the timing of the merger, the possibility that the closing conditions to the proposed merger may not be satisfied or waived, including that a governmental entity may prohibit, delay or refuse to grant a necessary approval, adverse effects on Western Digital’s stock price resulting from the announcement or completion of the merger, competitive responses to the announcement or completion of the merger, costs and difficulties related to the integration of SanDisk’s businesses and operations with Western Digital’s businesses and operations, the inability to obtain, or delays in obtaining, cost savings and synergies from the merger, uncertainties as to whether the completion of the merger or any transaction will have the accretive effect on Western Digital’s earnings or cash flows that it expects, unexpected costs, liabilities, charges or expenses resulting from the merger, litigation relating to the merger, the inability to retain key personnel, and any changes in general economic and/or industry-specific conditions.

In addition to the factors set forth above, other factors that may affect Western Digital’s or SanDisk’s plans, results or stock price are set forth in Western Digital’s and SanDisk’s respective filings with the SEC, including Western Digital’s and SanDisk’s most recent Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q and Current Reports on Form 8-K.

Many of these factors are beyond Western Digital’s and SanDisk’s control. Western Digital and SanDisk caution investors that any forward-looking statements made by Western Digital or SanDisk are not guarantees of future performance. Neither Western Digital nor SanDisk intend, or undertake any obligation, to publish revised forward-looking statements to reflect events or circumstances after the date of this document or to reflect the occurrence of unanticipated events.

2 |

| © 2015 WESTERN DIGITAL CORP. ALL RIGHTS RESERVED. |

|

Safe Harbor/Disclaimers

Important Additional Information and Where to find It

This communication does not constitute an offer to sell or the solicitation of an offer to buy any securities or a solicitation of any vote or approval. This communication may be deemed to be solicitation material in respect of the proposed merger between Western Digital and SanDisk. In connection with the proposed merger, Western Digital intends to file a registration statement on Form S-4 with the SEC that contains a preliminary joint proxy statement of SanDisk and Western Digital that also constitutes a preliminary prospectus of Western Digital. After the registration statement is declared effective, Western Digital and SanDisk will mail the definitive joint proxy statement/prospectus to their respective stockholders. This material is not a substitute for the joint proxy statement/prospectus or registration statement or for any other document that Western Digital or SanDisk may file with the SEC and send to Western Digital’s and/or SanDisk’s stockholders in connection with the proposed merger. INVESTORS AND SECURITY HOLDERS OF WESTERN DIGITAL AND SANDISK ARE URGED TO READ ALL RELEVANT DOCUMENTS FILED WITH THE SEC, INCLUDING THE JOINT PROXY STATEMENT/ PROSPECTUS, BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION ABOUT THE PROPOSED MERGER. Investors and security holders will be able to obtain copies of the joint proxy statement/prospectus (when filed) as well as other filings containing information about Western Digital and SanDisk, without charge, at the SEC’s website, http://www.sec.gov. Copies of the documents filed with the SEC by Western Digital will be available free of charge on Western Digital’s website at http://www.w dc.com. Copies of the documents filed with the SEC by SanDisk will be available free of charge on SanDisk’s website at http://www.sandisk.com.

Participants in Solicitation

Western Digital, SanDisk and their respective directors, executive officers and certain other members of management and employees may be soliciting proxies from their respective stockholders in favor of the proposed transaction. Information regarding the persons who may, under the rules of the SEC, be considered participants in the solicitation of stockholders in connection with the proposed transaction will be set forth in the joint proxy statement/prospectus when it is filed with the SEC. You can find information about Western Digital’s executive officers and directors in Western Digital’s definitive proxy statement filed with the SEC on September 23, 2015. You can find information about SanDisk’s executive officers and directors in its definitive proxy statement filed with the SEC on April 27, 2015. You can obtain free copies of these documents from Western Digital and SanDisk, respectively, using the contact information above. Investors may obtain additional information regarding the interest of such participants by reading the joint proxy statement/prospectus regarding the proposed merger when it becomes available.

3 |

| © 2015 WESTERN DIGITAL CORP. ALL RIGHTS RESERVED. |

|

Western Digital’s Acquisition of SanDisk

Western Digital is acquiring SanDisk for approximately $19 billion in a cash and stock transaction

Combination of Western Digital and SanDisk creates a global leader in storage technology

Acquisition at $86.50 a share financed with balance sheet cash,

$17.4 billion of new debt and equity consideration

4 |

| © 2015 WESTERN DIGITAL CORP. ALL RIGHTS RESERVED. |

|

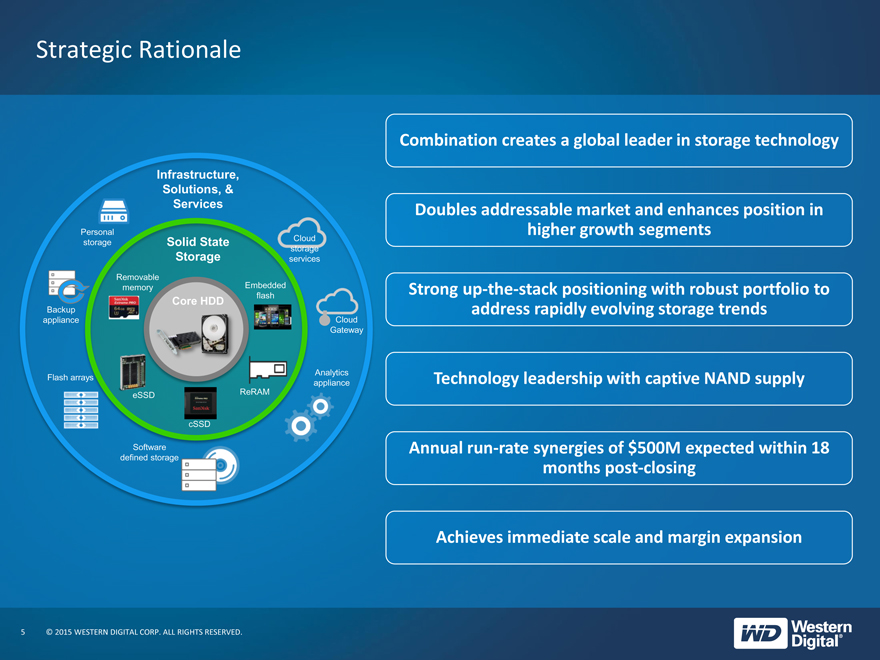

Strategic Rationale

Infrastructure, Solutions, & Services

Personal

Cloud

storage Solid State

storage

Storage services Remov mem bedded flash

Backup Core HDD

appliance Gateway

Analytics Flash arrays appliance eSSD ReRAM

cSSD

Software defined storage

Combination creates a global leader in storage technology

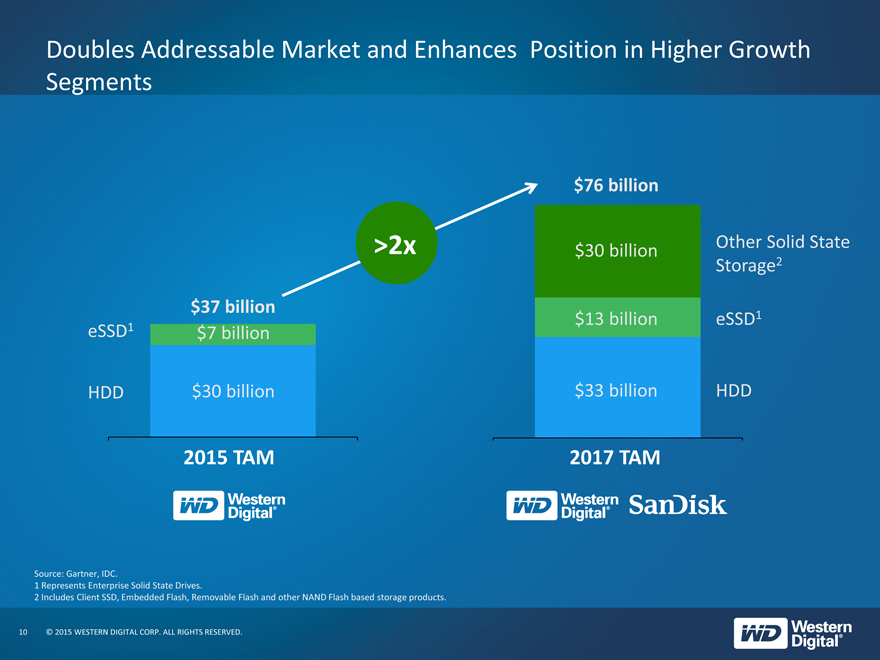

Doubles addressable market and enhances position in higher growth segments

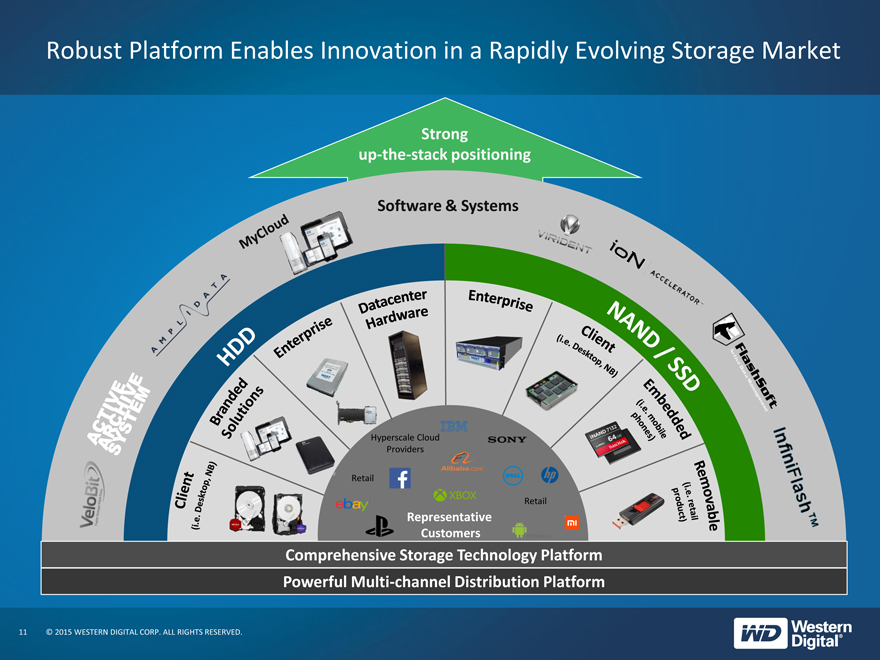

Strong up-the-stack positioning with robust portfolio to address rapidly evolving storage trends

Technology leadership with captive NAND supply

Annual run-rate synergies of $500M expected within 18 months post-closing

Achieves immediate scale and margin expansion

5 |

| © 2015 WESTERN DIGITAL CORP. ALL RIGHTS RESERVED. |

|

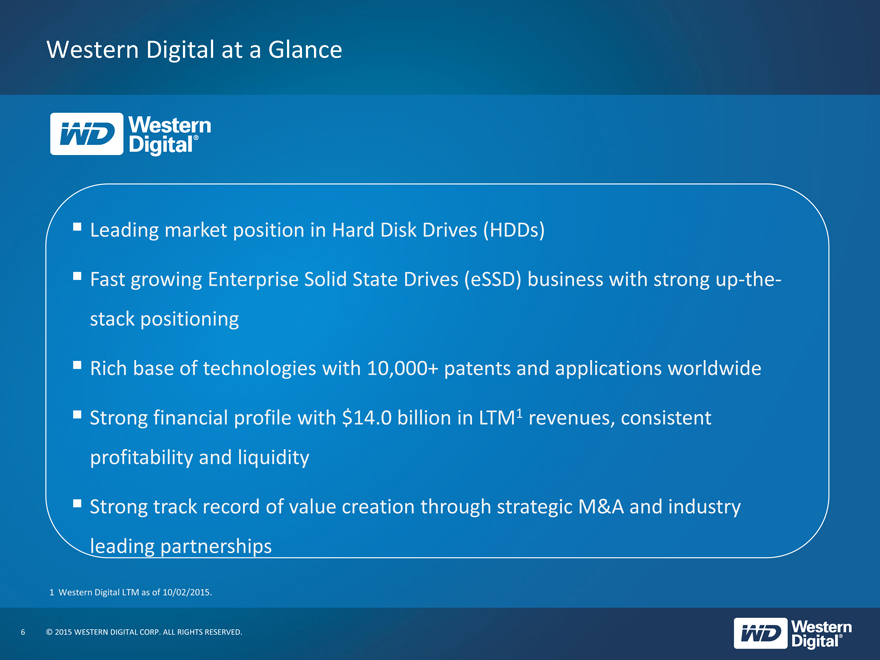

Western Digital at a Glance

Leading market position in Hard Disk Drives (HDDs)

Fast growing Enterprise Solid State Drives (eSSD) business with strong up-the-stack positioning

Rich base of technologies with 10,000+ patents and applications worldwide Strong financial profile with $14.0 billion in LTM1 revenues, consistent profitability and liquidity

Strong track record of value creation through strategic M&A and industry leading partnerships

1 |

| Western Digital LTM as of 10/02/2015. |

6 |

| © 2015 WESTERN DIGITAL CORP. ALL RIGHTS RESERVED. |

|

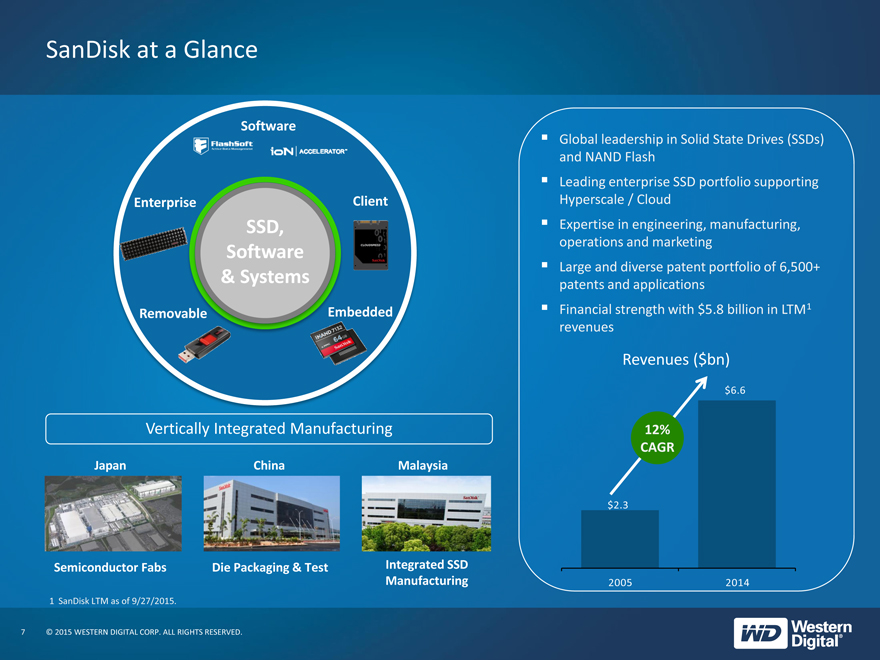

SanDisk at a Glance

Software

Enterprise Client

SSD, Software

& Systems

Removable Embedded

Vertically Integrated Manufacturing

Japan China Malaysia

Semiconductor Fabs Die Packaging & Test Integrated SSD

Manufacturing

1 |

| SanDisk LTM as of 9/27/2015. |

Global leadership in Solid State Drives (SSDs) and NAND Flash

Leading enterprise SSD portfolio supporting Hyperscale / Cloud Expertise in engineering, manufacturing, operations and marketing Large and diverse patent portfolio of 6,500+ patents and applications Financial strength with $5.8 billion in LTM1 revenues

Revenues ($bn)

$6.6

12%

CAGR

$2.3

2005 2014

7 |

| © 2015 WESTERN DIGITAL CORP. ALL RIGHTS RESERVED. |

|

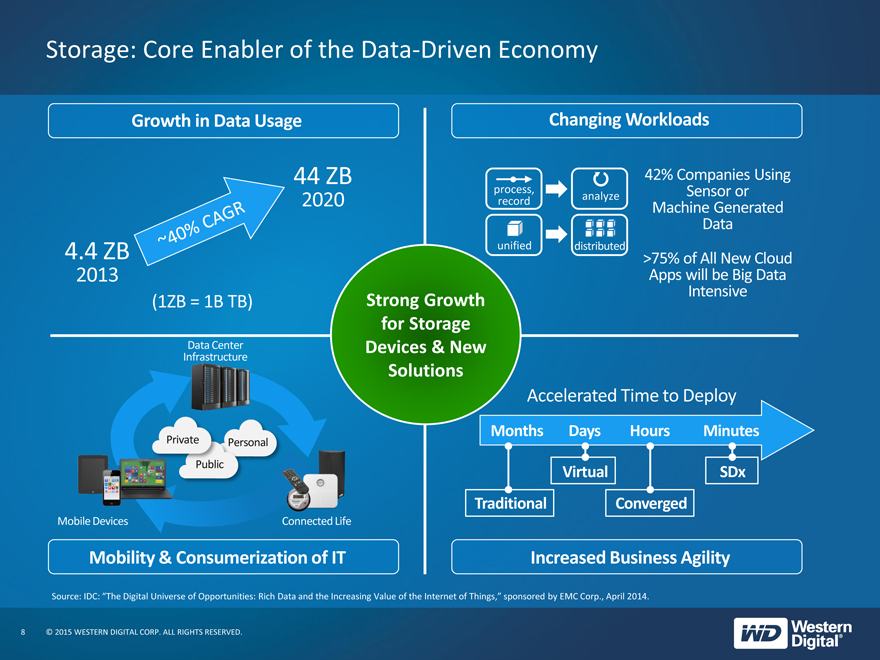

Storage: Core Enabler of the Data-Driven Economy

Growth in Data Usage

44 ZB

2020

4.4 ZB

2013

(1ZB = 1B TB)

Changing Workloads

42% Companies Using

process, Sensor or record analyze

Machine Generated

Data

unified distributed >75% of All New Cloud

Apps will be Big Data

Intensive

Strong Growth for Storage Devices & New Solutions

Infrastructure

Private onal Public

Mobile Devices Connected Life

Mobility & Consumerization of IT

Accelerated Time to Deploy

Months Days Hours Minutes

Virtual SDx

Traditional Converged

Increased Business Agility

Source: IDC: “The Digital Universe of Opportunities: Rich Data and the Increasing Value of the Internet of Things,” sponsored by EMC Corp., April 2014.

8 |

| © 2015 WESTERN DIGITAL CORP. ALL RIGHTS RESERVED. |

|

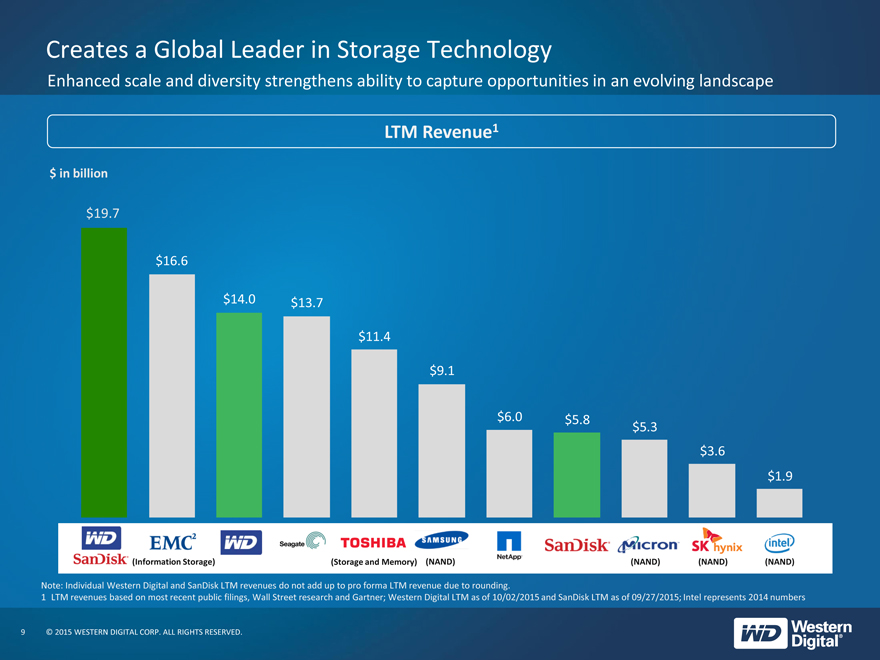

Creates a Global Leader in Storage Technology

Enhanced scale and diversity strengthens ability to capture opportunities in an evolving landscape

LTM Revenue1

$ in billion

$19.7

$16.6

$14.0 $13.7

$11.4 $9.1

$6.0 $5.8 $5.3 $3.6

$1.9

(Information Storage) (Storage and Memory) (NAND) (NAND) (NAND) (NAND)

Note: Individual Western Digital and SanDisk LTM revenues do not add up to pro forma LTM revenue due to rounding.

1 LTM revenues based on most recent public filings, Wall Street research and Gartner; Western Digital LTM as of 10/02/2015 and SanDisk LTM as of 09/27/2015; Inte l represents 2014 numbers

9 © 2015 WESTERN DIGITAL CORP. ALL RIGHTS RESERVED.

|

Doubles Addressable Market and Enhances Position in Higher Growth Segments

$37 billion eSSD1 $7 billion

HDD $30 billion

2015 TAM

>2x

$76 billion

Other Solid State $30 billion 2 Storage

$13 billion eSSD1

$33 billion HDD

2017 TAM

Source: Gartner, IDC.

1 |

| Represents Enterprise Solid State Drives. |

2 |

| Includes Client SSD, Embedded Flash, Removable Flash and other NAND Flash based storage products. |

10 © 2015 WESTERN DIGITAL CORP. ALL RIGHTS RESERVED.

|

Robust Platform Enables Innovation in a Rapidly Evolving Storage Market

Strong up-the-stack positioning

Software & Systems

Hyperscale Cloud

Providers

Retail

Retail

Representative Customers

Comprehensive Storage Technology Platform Powerful Multi-channel Distribution Platform

11 © 2015 WESTERN DIGITAL CORP. ALL RIGHTS RESERVED.

|

Technology Leadership Driven by IP and Talent

10,000+ patents / applications

One of the storage industry’s largest portfolios

9,700+ engineers

Leading HDD and eSSD supplier

First and only supplier of helium-filled HDD World’s first 10TB drive for archive applications

6,500+ patents / applications

NAND memory, systems & packaging

3,000+ engineers

World’s most advanced 2D NAND (15nm)

Strong 3D IP portfolio – commercializing 2nd generation 3D NAND in 2016

ReRAM technology development

Broadest portfolio of storage technology solutions in the industry

12 © 2015 WESTERN DIGITAL CORP. ALL RIGHTS RESERVED.

|

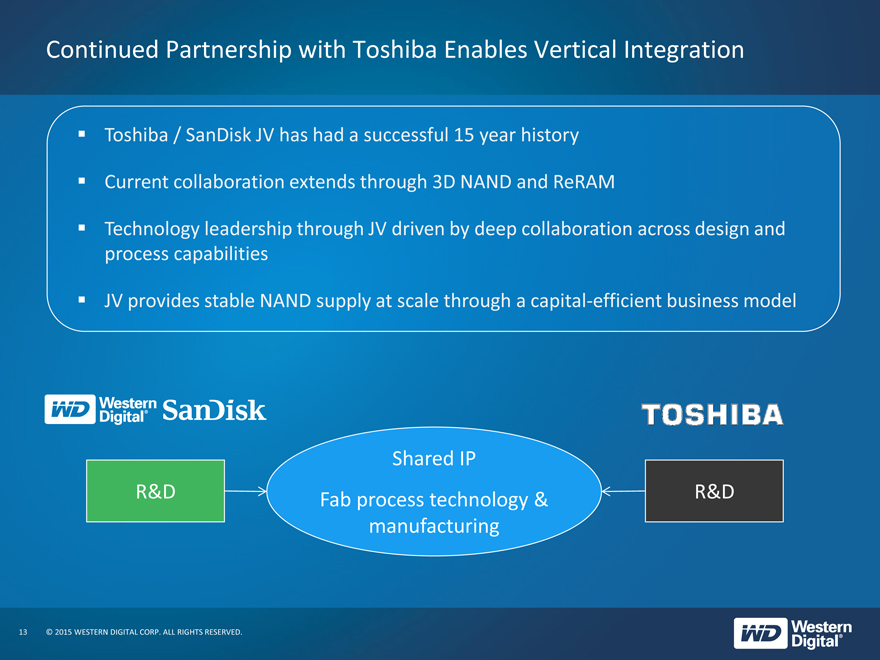

Continued Partnership with Toshiba Enables Vertical Integration

Toshiba / SanDisk JV has had a successful 15 year history

Current collaboration extends through 3D NAND and ReRAM

Technology leadership through JV driven by deep collaboration across design and process capabilities

JV provides stable NAND supply at scale through a capital-efficient business model

Shared IP

R&D Fab process technology & R&D manufacturing

13 © 2015 WESTERN DIGITAL CORP. ALL RIGHTS RESERVED.

|

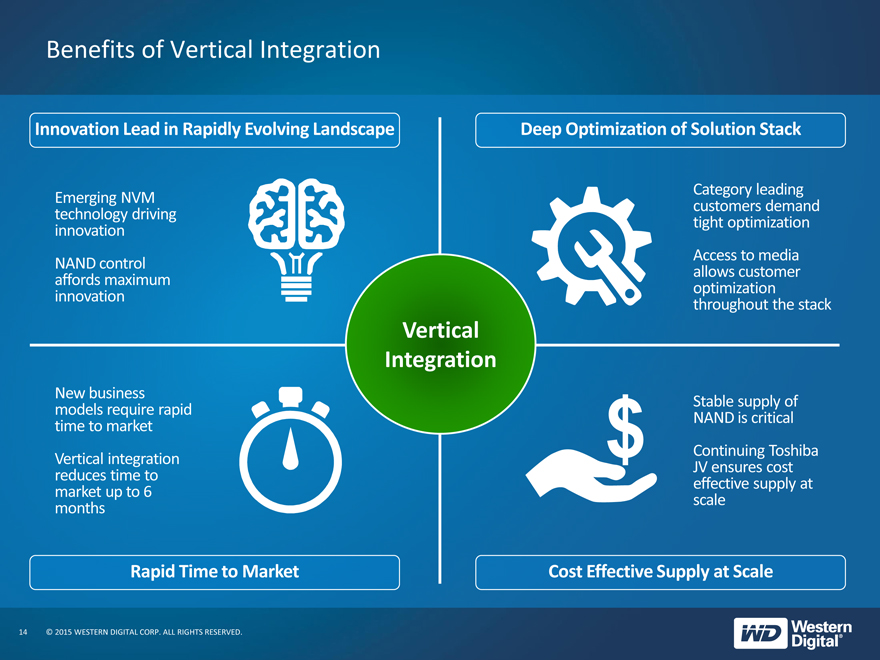

Benefits of Vertical Integration

Innovation Lead in Rapidly Evolving Landscape

Emerging NVM technology driving innovation

NAND control affords maximum innovation

Deep Optimization of Solution Stack

Category leading customers demand tight optimization

Access to media allows customer optimization throughout the stack

Vertical Integration

New business models require rapid time to market

Vertical integration reduces time to market up to 6 months

Rapid Time to Market

Stable supply of NAND is critical

Continuing Toshiba

JV ensures cost effective supply at scale

Cost Effective Supply at Scale

14 © 2015 WESTERN DIGITAL CORP. ALL RIGHTS RESERVED.

|

Significant Synergy Opportunities

Vertical integration

G&A consolidation

Overlapping go-to-market (GTM) consolidation

R&D efficiency

Annual run-rate synergies of $500M expected within 18 months post-closing

15 © 2015 WESTERN DIGITAL CORP. ALL RIGHTS RESERVED.

|

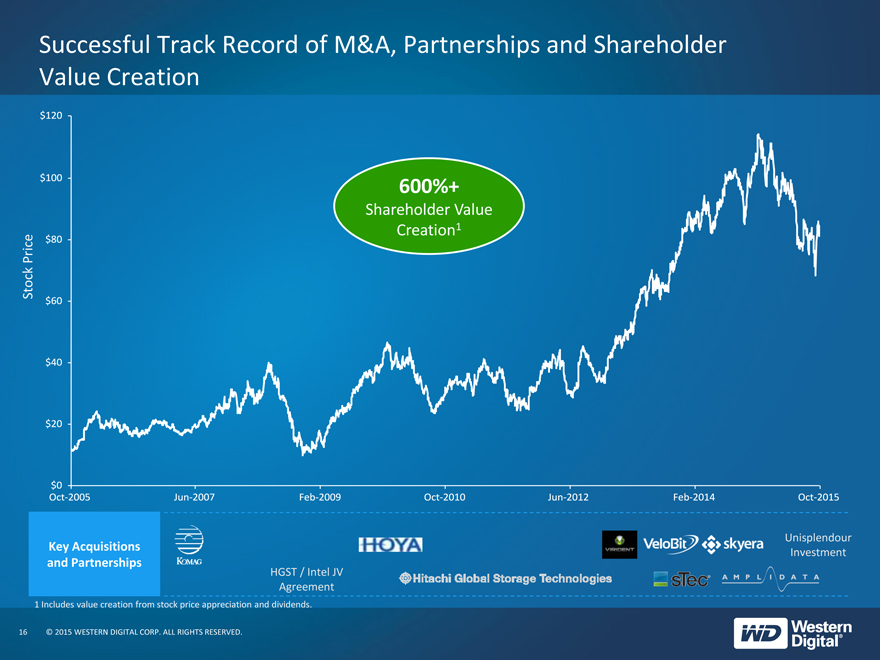

Successful Track Record of M&A, Partnerships and Shareholder Value Creation

600%+

Shareholder Value

1 |

|

Price Creation

Stock

Key Acquisitions Unisplendour and Partnerships Investment

HGST / Intel JV Agreement

1 |

| Includes value creation from stock price appreciation and dividends. |

16 © 2015 WESTERN DIGITAL CORP. ALL RIGHTS RESERVED.

|

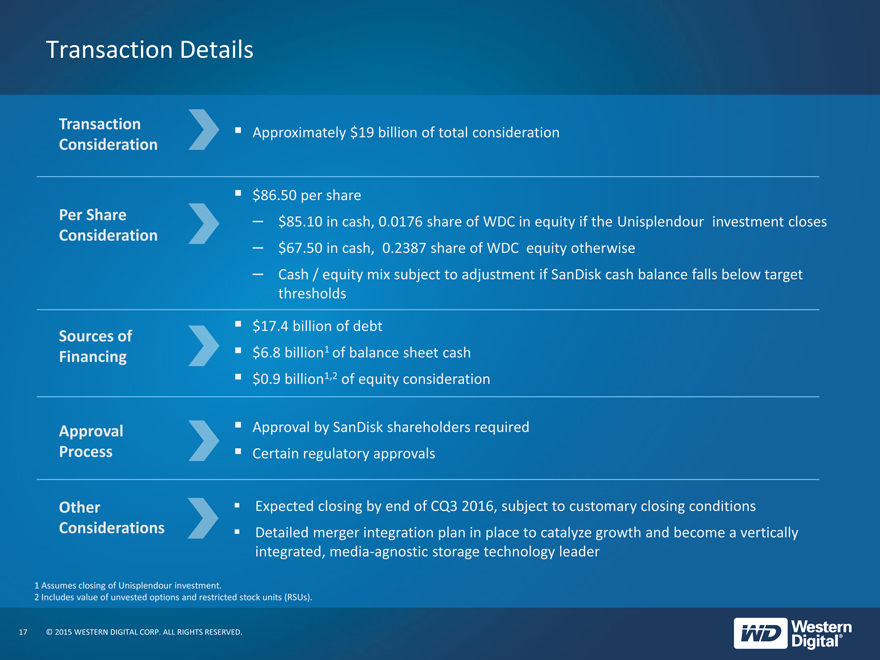

Transaction Details

Transaction Approximately $ 19 billion of total consideration

Consideration

$86.50 per share

Per Share – $ 85.10 in cash, 0.0176 share of WDC in equity if the Unisplendour investment closes

Consideration – $ 67.50 in cash, 0.2387 share of WDC equity otherwise

– Cash / equity mix subject to adjustment if SanDisk cash balance falls below target

thresholds

$17.4 billion of debt

Sources of

Financing $6.8 billion1 of balance sheet cash

$0.9 billion1,2 of equity consideration

Approval Approval by SanDisk shareholders required

Process Certain regulatory approvals

Other Expected closing by end of CQ3 2016, subject to customary closing conditions

Considerations Detailed merger integration plan in place to catalyze growth and become a vertically

integrated, media-agnostic storage technology leader

1 |

| Assumes closing of Unisplendour investment. |

2 |

| Includes value of unvested options and restricted stock units (RSUs). |

17 © 2015 WESTERN DIGITAL CORP. ALL RIGHTS RESERVED.

|

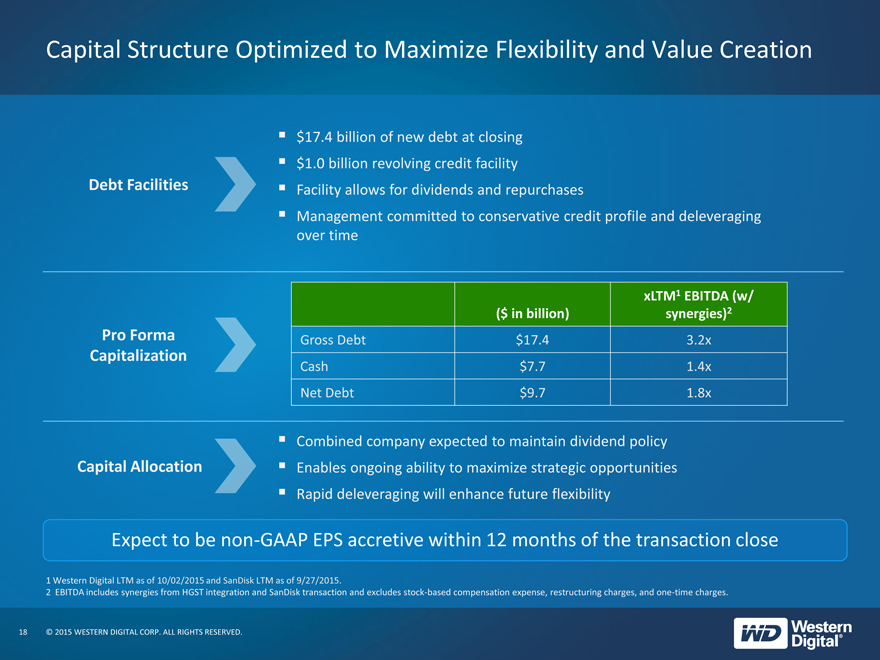

Capital Structure Optimized to Maximize Flexibility and Value Creation

$ 17.4 billion of new debt at closing

$ 1.0 billion revolving credit facility

Debt Facilities Facility allows for dividends and repurchases

Management committed to conservative credit profile and deleveraging

over time

xLTM1 EBITDA (w/

($ in billion) synergies)2

Pro Forma Gross Debt $17.4 3.2x

Capitalization

Cash $7.7 1.4x

Net Debt $9.7 1.8x

Combined company expected to maintain dividend policy

Capital Allocation Enables ongoing ability to maximize strategic opportunities

Rapid deleveraging will enhance future flexibility

Expect to be non-GAAP EPS accretive within 12 months of the transaction close

1 |

| Western Digital LTM as of 10/02/2015 and SanDisk LTM as of 9/27/2015. |

2 EBITDA includes synergies from HGST integration and SanDisk transaction and excludes stock-based compensation expense, restructuring charges, and one-time charges.

18 © 2015 WESTERN DIGITAL CORP. ALL RIGHTS RESERVED.

|

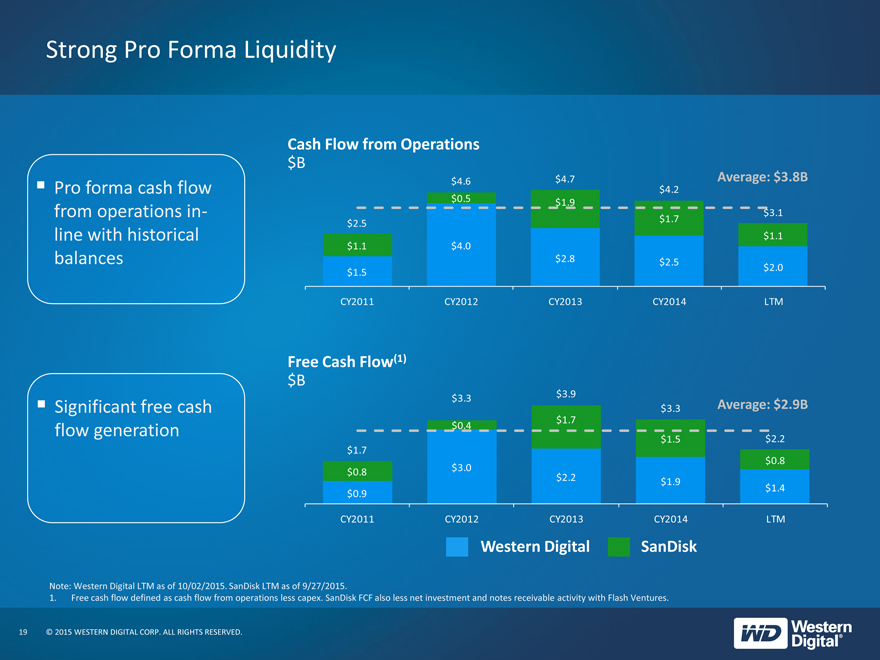

Strong Pro Forma Liquidity

Pro forma cash flow from operations inline with historical balances

Cash Flow from Operations $B

$4.6 $4.7 Average: $3.8B

$4.2

$0.5 $1.9

$3.1

$1.7

$2.5

$1.1

$1.1 $4.0

$2.8 $2.5

$2.0

$1.5

CY2011 CY2012 CY2013 CY2014 LTM

Significant free cash flow generation

Free Cash Flow(1) $B

$3.9

$3.3

$3.3 Average: $2.9B

$1.7

$0.4

$1.5 $2.2

$1.7

$0.8

$3.0

$0.8

$2.2

$1.9

$1.4

$0.9

CY2011 CY2012 CY2013 CY2014 LTM

Western Digital SanDisk

Note: Western Digital LTM as of 10/02/2015. SanDisk LTM as of 9/27/2015.

1. Free cash flow defined as cash flow from operations less capex. SanDisk FCF also less net investment and notes receivable activity with Flash Ventures.

19 © 2015 WESTERN DIGITAL CORP. ALL RIGHTS RESERVED.

|

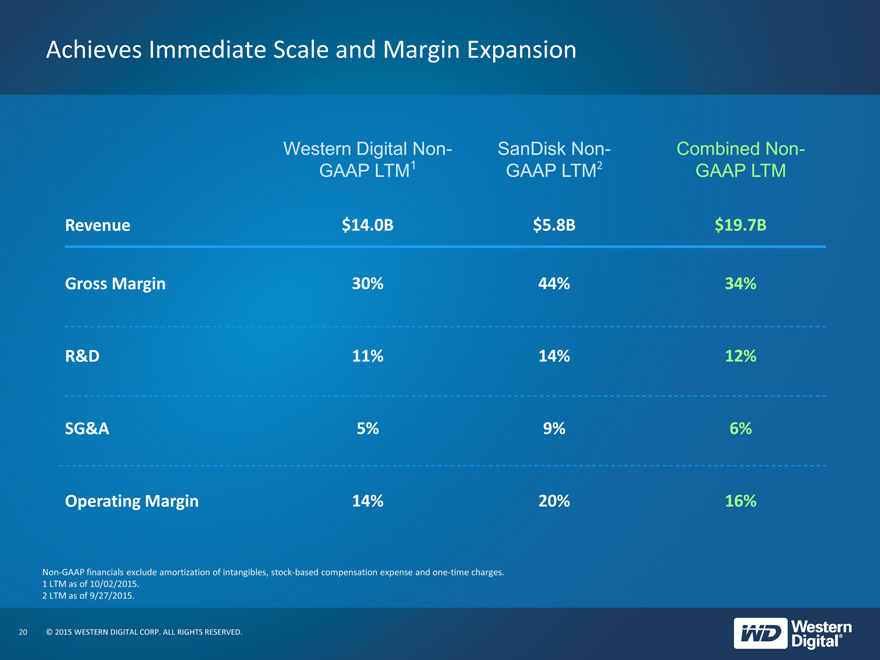

Achieves Immediate Scale and Margin Expansion

Western Digital Non- SanDisk Non- Combined Non-

GAAP LTM1 GAAP LTM2 GAAP LTM

Revenue $14.0B $5.8B $19.7B

Gross Margin 30% 44% 34%

R&D 11% 14% 12%

SG&A 5% 9% 6%

Operating Margin 14% 20% 16%

Non-GAAP financials exclude amortization of intangibles, stock-based compensation expense and one-time charges.

1 |

| LTM as of 10/02/2015. |

2 |

| LTM as of 9/27/2015. |

20 © 2015 WESTERN DIGITAL CORP. ALL RIGHTS RESERVED.

|

GAAP to Non-GAAP Reconciliation1

Western Digital SanDisk Combined

LTM LTM LTM

Revenue $13,989 $5,757 $19,746

GAAP Gross Profit $4,027 $2,372 $6,399

Stock-based Compensation 16 19 35

Amortization 112 115 227

Inventory Step-up — 3 3

Other 40 — 40

Non-GAAP Gross Profit $4,195 $2,510 $6,705

Non-GAAP Gross Margin 30% 44% 34%

GAAP R&D $1,594 $879 $2,473

Stock-based Compensation2 (62) (84) (146)

Amortization — — —

Other (3) — (3)

Non-GAAP R&D $1,529 $795 $2,324

% Revenue 11% 14% 12%

Note: Dollars in millions. Western Digital LTM as of 10/02/2015. SanDisk LTM as of 9/27/2015

Source: Company public filings.

1 Non-GAAP statistics exclude amortization of intangibles, the impact of SFAS 123(R) stock-based compensation expense and one-time charges.

2 The items included within the GAAP to Non-GAAP reconciliation on this slide are only for demonstration and comparability purposes and are not necessarily indicative of the items that will appear in future GAAP to Non-GAAP reconciliations. For example, WDC currently does not exclude stock-based compensation expense from its Non-GAAP results, but it has done so here solely to achieve comparability with SanDisk’s past practice.

21 © 2015 WESTERN DIGITAL CORP. ALL RIGHTS RESERVED.

|

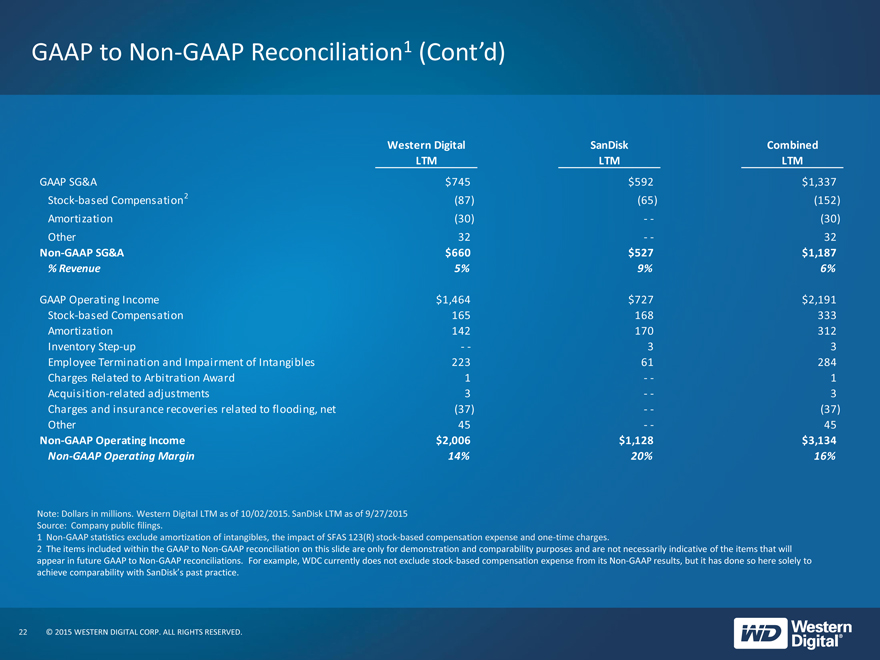

GAAP to Non-GAAP Reconciliation1 (Cont’d)

Western Digital SanDisk Combined

LTM LTM LTM

GAAP SG&A $745 $592 $ 1,337

Stock-based Compensation2 (87) (65) (152)

Amortization (30) — (30)

Other 32 — 32

Non-GAAP SG&A $660 $527 $ 1,187

% Revenue 5% 9% 6%

GAAP Operating Income $1,464 $727 $ 2,191

Stock-based Compensation 165 168 333

Amortization 142 170 312

Inventory Step-up — 3 3

Employee Termination and Impairment of Intangibles 223 61 284

Charges Related to Arbitration Award 1 — 1

Acquisition-related adjustments 3 — 3

Charges and insurance recoveries related to flooding, net (37) — (37)

Other 45 — 45

Non-GAAP Operating Income $2,006 $1,128 $ 3,134

Non-GAAP Operating Margin 14% 20% 16%

Note: Dollars in millions. Western Digital LTM as of 10/02/2015. SanDisk LTM as of 9/27/2015

Source: Company public filings.

1 Non-GAAP statistics exclude amortization of intangibles, the impact of SFAS 123(R) stock-based compensation expense and one-time charges.

2 The items included within the GAAP to Non-GAAP reconciliation on this slide are only for demonstration and comparability purposes and are not necessarily indicative of the items that will appear in future GAAP to Non-GAAP reconciliations. For example, WDC currently does not exclude stock-based compensation expense from its Non-GAAP results, but it has done so here solely to achieve comparability with SanDisk’s past practice.

22 © 2015 WESTERN DIGITAL CORP. ALL RIGHTS RESERVED.

|

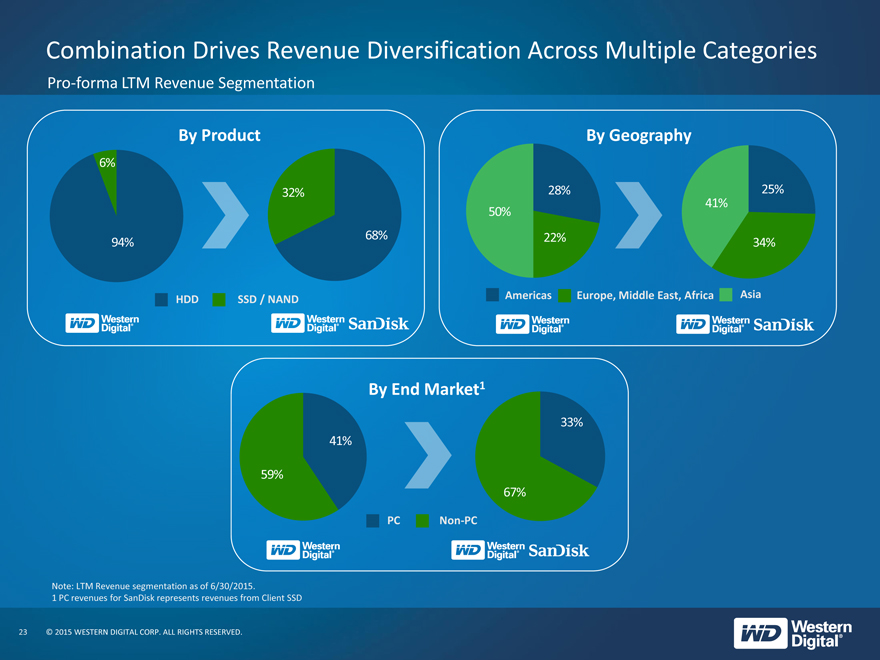

Combination Drives Revenue Diversification Across Multiple Categories

Pro-forma LTM Revenue Segmentation

By Product

6%

32%

68% 94%

HDD SSD / NAND

By Geography

28% 25% 41% 50%

22% 34%

Americas Europe, Middle East, Africa Asia

By End Market1

33% 41%

59%

67%

PC Non-PC

Note: LTM Revenue segmentation as of 6/30/2015.

1 |

| PC revenues for SanDisk represents revenues from Client SSD |

23 © 2015 WESTERN DIGITAL CORP. ALL RIGHTS RESERVED.

|

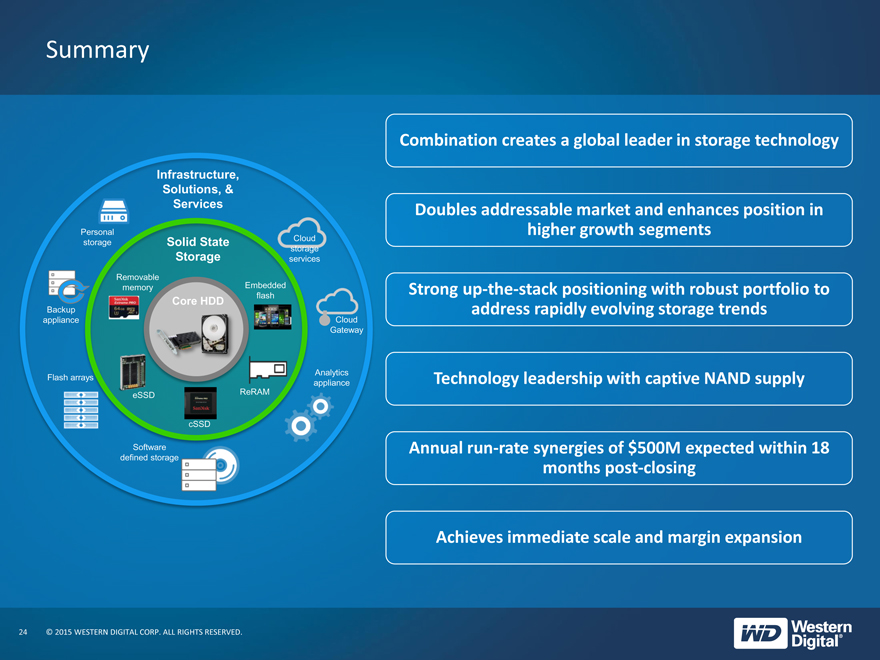

Summary

Infrastructure, Solutions, & Services

Personal

Cloud

storage Solid State

storage

Storage services Remov mem bedded flash

Backup Core HDD

appliance Gateway

Analytics Flash arrays appliance eSSD ReRAM

cSSD

Software defined storage

Combination creates a global leader in storage technology

Doubles addressable market and enhances position in higher growth segments

Strong up-the-stack positioning with robust portfolio to address rapidly evolving storage trends

Technology leadership with captive NAND supply

Annual run-rate synergies of $500M expected within 18 months post-closing

Achieves immediate scale and margin expansion

24 © 2015 WESTERN DIGITAL CORP. ALL RIGHTS RESERVED.

|

Q & A

25 © 2015 WESTERN DIGITAL CORP. ALL RIGHTS RESERVED.

Exhibit 99.2

|

FAQ on Topics of Interest

© 2015 Western Digital Corporation. All Rights Reserved.

|

SAFE HARBOR

Forward-Looking Statements

This document contains forward-looking statements within the meaning of the federal securities laws. These forward-looking statements include, but are not limited to, statements regarding product and technology positioning, the proposed merger of Western Digital Corporation (“Western Digital”) with SanDisk Corporation (“SanDisk”) (including financing of the proposed transaction and the benefits, results, effects and timing of a transaction), the investment in Western Digital by Unisplendour Corporation Limited (“Unis”), the joint venture with Unis and its subsidiary Unissoft (Wuxi) Group Co., Ltd. (“Unissoft”), all statements regarding Western Digital’s (and Western Digital’s and SanDisk’s combined) expected future financial position, results of operations, cash flows, dividends, financing plans, business strategy, budgets, capital expenditures, competitive positions, growth opportunities, plans and objectives of management, and statements containing the use of forward-looking words, such as “may,” “will,” “could,” “would,” “should,” “project,” “believe,” “anticipate,” “expect,” “esti mate,” “continue,” “potential,” “plan,” “forecast,” “approximate,” “intend,” “upside,” and the like, or the use of future ten se. Statements contained herein concerning the business outlook or future economic performance, anticipated profitability, revenues, expenses, dividends or other financial items, and product or services line growth of Western Digital (and the combined businesses of Western Digital and SanDisk), together with other statements that are not historical facts, are forwar d-looking statements that are estimates reflecting the best judgment of Western Digital and SanDisk based upon currently available information. Statements concerning current conditions may also be forward-looking if they imply a continuation of current conditions.

Such forward-looking statements are inherently uncertain, and stockholders and other potential investors must recognize that actual results may differ materially from Western Digital’s and SanDisk’s expectations as a result of a variety of factors, including, without limitation, those discussed below. Such forward-looking statements are based upon the current expectations of Western Digital’s and SanDisk’s management and include known and unknown risks, uncertainties and other factors, many of which Western Digital and SanDisk are unable to predict or control, that may cause Western Digital’s or SanDisk’s actual results, performance or plans to differ materially from any future results, performance or plans expressed or implied by such forward-looking statements. These statements involve risks, uncertainties and other factors discussed below and detailed from time to time in Western Digital’s and SanDisk’s filings with the Securities and Exchange Commission (the “SEC”).

Risks and uncertainties related to the proposed merger include, but are not limited to, the risk that SanDisk’s stockholders do not approve the merger or that Western Digital’s stockholders do not approve the issuance of stock in the merger (to the extent such approval is required), potential adverse reactions or changes to business relationships resulting from the an nouncement, pendency or completion of the merger, uncertainties as to the timing of the merger, the possibility that the closing conditions to the proposed merger may not be satisfied or waived, including that a governmental entity may prohibit, delay or refuse to grant a necessary approval, adverse effects on Western Digital’s stock price resulting from the announcement or completion of the merger, competitive responses to the announcement or completion of the merger, costs and di fficulties related to the integration of SanDisk’s businesses and operations with Western Digital’s businesses and operations, the inability to obtain, or delays in obtaining, cost savings and synergies from the merger, uncertainties as to whether the completion of the merger or any transaction will have the accretive effect on Western Digital’s earnings or cash flows that it expects, unexpected costs, liabilities, charges or expenses resulting from the merger, litigation relating to the merger, the inability to retain key personnel, and any changes in general economic and/or industry-specific conditions.

In addition to the factors set forth above, other factors that may affect Western Digital’s or SanDisk’s plans, results or stock price are set forth in Western Digital’s and SanDisk’s respective filings with the SEC, including Western Digital’s and SanDisk’s most recent Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q and Current Reports on Form 8-K.

Many of these factors are beyond Western Digital’s and SanDisk’s control. Western Digital and SanDisk caution investors that any forward-looking statements made by Western Digital or SanDisk are not guarantees of future performance. Neither Western Digital nor SanDisk intend, or undertake any obligation, to publish revised forward-looking statements to reflect events or circumstances after the date of this document or to reflect the occurrence of unanticipated events.

Important Additional Information and Where to find It

This communication does not constitute an offer to sell or the solicitation of an offer to buy any securities or a solicitation of any vote or approval. This communication may be deemed to be solicitation material in respect of the proposed merger between Western Digital and SanDisk. In connection with the proposed merger, Western Digital intends to file a registration s tatement on Form S-4 with the SEC that contains a preliminary joint proxy statement of SanDisk and Western Digital that also constitutes a preliminary prospectus of Western Digital. After the registration statement is declared effective, Western Digital and SanDisk will mail the definitive joint proxy statement/prospectus to their respective stockholders. This material is not a substitute for the joint proxy statement/prospectus or registration statement or for any other document that Western Digital or SanDisk may file with the SEC and send to Western Digital’s and/or SanDisk’s stockholders in connection with the proposed merger. INVESTORS AND SECURITY HOLDERS OF WESTERN DIGITAL AND SANDISK ARE URGED TO READ ALL RELEVANT DOCUMENTS FILED WITH THE SEC, INCLUDING THE JOINT PROXY STATEMENT/PROSPECTUS, BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION ABOUT THE PROPOSED MERGER. Investors and security holders will be able to obtain copies of the joint proxy statement/prospectus (when filed) as well as other filings containing information about Western Digital and SanDisk, without charge, at the SEC’s website, http ://www.sec.gov. Copies of the documents filed with the SEC by Western Digital will be available free of charge on Western Digital’s website at http://www.wdc.com. Copies of the documents filed with the SEC by SanDisk will be available free of charge on SanDisk’s website at http://www.sandisk.com.

Participants in Solicitation

Western Digital, SanDisk and their respective directors, executive officers and certain other members of management and employees may be soliciting proxies from their respective stockholders in favor of the proposed transaction. Information regarding the persons who may, under the rules of the SEC, be considered participants in the solicitation of stockholders in connection with the proposed transaction will be set forth in the joint proxy statement/prospectus when it is filed with the SEC. You can find information about Western Digital’s executive officers and directors in Western Digital’s definitive proxy statement filed with the SEC on September 23, 2015. You can find information about SanDisk’s executive officers and directors in its definitive proxy statement filed with the SEC on April 27, 2015. You can obtain free copies of these documents from Western Digital and SanDisk, respectively, using the contact information above. Investors may obtain additional information regarding the interest of such participants by reading the joint proxy statement/prospectus regarding the proposed merger when it becomes available.

2 |

| © 2015 Western Digital Corporation. All Rights Reserved. |

|

FAQ on Recent Areas of Interest to Investors Re: WDC

In meetings with investors on November 17-19, senior management of Western Digital (WDC) will communicate its views on a series of topics related to several recent announcements by WDC, including the planned investment in WDC by Unisplendour, the HGST integration decision by MOFCOM, WDC’s planned acquisition of SanDisk (SNDK), and the joint venture (JV) with Unisplendour and its subsidiary, Unissoft.

Listed below are WDC’s responses to a number of topics related to strategy, operations, finance and regulatory review of the above transactions.

3 |

| © 2015 Western Digital Corporation. All Rights Reserved. |

|

STRATEGY

What is the strategic rationale behind the planned acquisition of SNDK?

We are excited about the combination with SNDK and believe it provides significant benefits across multiple categories, including significant long-term return to our shareholders.

We expect the combination will deliver benefits to our customers through an unparalleled breadth of products that is media-agnostic covering the full storage ecosystem (inclusive of HDD and solid state storage solutions for Enterprise and Client/Mobile).

We expect the acquisition will result in a diversification and expansion of our addressable market from $37 billion in 2015 to $76 billion in 2017.

The combination is expected to deliver technology leadership with access and control over NAND cost and result in deeper engagement in the design of NAND technology: Toshiba is the inventor of NAND technology and the SNDK/Toshiba JV has been the industry’s most successful partnership The JV provides economies of scale and competitive memory cost; SNDK and Toshiba have jointly developed NAND, but they have approached product innovation independently.

The JV is the largest supplier of NAND wafers in the market (~36%) and has scale (reference: Gartner September NAND wafer forecast for Q4CY16).

The acquisition provides a strong platform to continue our ascent up the stack (UTS) through system level offerings such as scale-out hybrid and All Flash Arrays (AFA), plus strong partnerships for next-gen storage architectures (e.g., SNDK partnership with VMWare and Nexenta).

The acquisition strengthens our enterprise presence via strong partnerships with leading industry players like HP across the NVM portfolio (SSDs & Systems with NAND & ReRAM).

WDC’s and SNDK’s enterprise SSD businesses have very little customer overlap and have different areas of focus with WDC focused on mixed use write intensive SAS solutions and SNDK focused on read intensive SAS and PCIe solutions.

Why is it important for WDC to own SNDK, versus pursuing a larger type of JV to ensure long term access to NAND? What is the importance of vertical integration?

The acquisition of SNDK will provide unparalleled product breadth, economic benefits and strengthen our position as a vendor of choice for customers for storage devices and solutions.

Owning the NAND media control point enables innovation and continued expansion of our role in the storage industry, as a leader at scale in a market with many vertically integrated competitors.

It maximizes WDC’s product value proposition through earlier and deeper technology access, translating into better economics and product features for customers. It will significantly improve economics for SNDK (due to allocation of bits to higher margin opportunities) and for WDC (due to lower cost of NAND).

NAND is more complex than a simple commodity; manufacturers have larger degrees of freedom to tune and optimize the NAND for particular applications & use cases (Examples: Benefits include improved performance, broader use of low-cost NAND, enhanced data reliability, data security and system optimization for multi-tenancy, virtualization and containers).

Technology access to the media and manufacturing process is key to innovation and to best time to market. The acquisition will enable us to match scale with scale to optimize solutions that best meet customers’ needs.

What is WDC’s view of the Toshiba relationship?

WDC has a strong existing relationship with Toshiba on NAND.

Toshiba is supportive of the acquisition of SNDK by WDC and we look forward to continuing the partnership SNDK has developed.

The SNDK-Toshiba collaboration on NAND has been successful for 15 years – it has successfully developed and manufactured 11 generations of NAND and seven generations of X3 NAND

Based on our due diligence, we are confident that the JV with Toshiba will be strong and meet our needs.

We conducted an in-depth analysis of 3D technologies available in the marketplace including the offerings from the SNDK-Toshiba JV. This gave us confidence that the SNDK-Toshiba JV will be an industry leader in 3D, building off an expected strong ramp in 2016.

4 |

| © 2015 Western Digital Corporation. All Rights Reserved. |

|

STRATEGY

What is WDC’s view of SNDK’s 3D technology and its plan to commercialize it?

SNDK’s strategy is to intersect the market with favorable technology and cost points providing a key competitive edge – similar to WDC’s time-tested strategy of time to cost vs. first to market.

Our in-depth analysis of 3D technologies available in the marketplace, including the offering from the SNDK-Toshiba JV, gives us confidence that the JV will be an industry leader in 3D, building off an expected strong ramp in 2016.

SNDK and Toshiba have high confidence in their 3D NAND technology ramp – joint announcement of operationalization plan for Fab 2. SNDK’s current 48-layer 3D (intro product in 3D) is industry competitive and will begin deploying in CY2016.

SNDK has the industry’s smallest 2D die-size, and the lowest bit cost today and expected going forward – 2D cost at par or better than 3D cost from competition today.

In SNDK’s Q215 call in July, CEO Sanjay Mehrotra said that “our 15nm 2D NAND technology is the lowest cost node in the industry this year bar none. And bar none means any – compared to any other 2D technology or 3D technology that is there today.”

What is WDC’s view of NAND supply/demand dynamics?

We believe the supply and demand for NAND over the long term is likely to be balanced. Periodic supply-demand imbalances may occur, but we believe that there is sufficient demand in the long term and sustained oversupply is unlikely.

We have worked extensively with the team at SNDK around understanding their view on the market and supply -demand dynamics and have a similar view on the industry going forward The Gartner NAND supply forecast of roughly 300EB in CY2019 is aligned with the demand forecast, growing from around 85EB in CY2015.

The Gartner NAND CAPEX forecast of ramping from ~$10B (CY2015) to $18B (CY2019) supports overall bit growth – with estimated 3D NAND CAPEX at ~$40B over the next 3 years. The majority of the CAPEX is on driving technology transition in 3D while the minority is on wafer capacity increase. (Supported by bit growth of ~35% CAGR vs wafer capacity increase ~10% CAGR).

Given the breadth, scale and leadership of the combined portfolio of WDC and SNDK, the combination is well positioned in its ability to respond to industry fluctuations in the most economically efficient manner.

The primary driver of the EB growth will be from compute devices (Client & eSSD) going from c40% of total NAND EB in CY2015 to c70% of total NAND EB in CY2020 as forecasted by Gartner.

What is WDC’s view of Intel’s investment in China for 3D X-point manufacturing and of the commoditization of the NAND industry?

Given Intel’s leadership position in enterprise SSDs, this fab investment shows the importance of having a captive NAND supply to win in the solid state storage industry. It is uncertain if the added capacity will be incremental or in lieu of Intel & Micron Flash Technology JV (IMFT JV).

The added capacity is likely to have significant 3D x-Point capacity which would be closer to DRAM than SSDs.

The industry is expected to be at 300EB in supply in 5 years. This investment will not materially change that projected supply .

What is WDC’s perspective on Tsinghua China NAND fab investment?

The announcement is aligned with Tsinghua’s publicly expressed intent to establish non-volatile memory manufacturing capability in China.

It is unclear if this investment will be focused on legacy or advanced NAND or emerging NVM technology.

The investment is at a preliminary stage and a number of critical aspects to this investment have not been determined, including the selection of technology partner(s). We expect the initial proposal – which has not been approved by State Council – will evolve going forward as it progresses through the process.

Based on what we know at this time, this announcement does not change our strategic perspective or conviction on the SNDK acquisition.

Has WDC’s outlook on the HDD business changed in light of this acquisition?

Our view of HDDs is unchanged. We believe that both HDDs and SSDs will continue to play an integral role in storage solutions for the foreseeable future, with the majority of data continuing to be stored on HDDs. After the acquisition of SNDK, we will be truly agnostic as to which technology is deployed where.

5 |

| © 2015 Western Digital Corporation. All Rights Reserved. |

|

REGULATORY REVIEWS

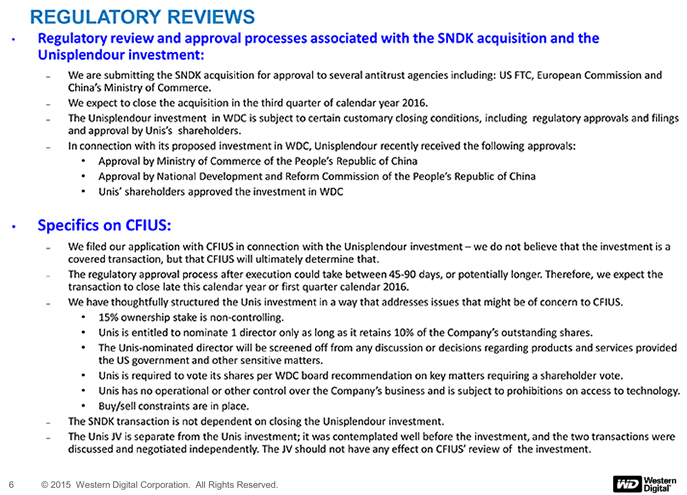

Regulatory review and approval processes associated with the SNDK acquisition and the Unisplendour investment:

We are submitting the SNDK acquisition for approval to several antitrust agencies including: US FTC, European Commission and China’s Ministry of Commerce. We expect to close the acquisition in the third quarter of calendar year 2016.

The Unisplendour investment in WDC is subject to certain customary closing conditions, including regulatory approvals and filings and approval by Unis’s shareholders.

In connection with its proposed investment in WDC, Unisplendour recently received the following approvals:

Approval by Ministry of Commerce of the People’s Republic of China

Approval by National Development and Reform Commission of the People’s Republic of China Unis’ shareholders approved the investment in WDC

Specifics on CFIUS:

We filed our application with CFIUS in connection with the Unisplendour investment out of an abundance of caution – we do not believe the investment is a covered transaction but that CFIUS will ultimately determine that.

The regulatory approval process after execution could take between 45-90 days, or potentially longer. Therefore, we expect the transaction to close late this calendar year or first quarter calendar 2016.

We have thoughtfully structured the Unis investment in a way that addresses issues that might be of concern to CFIUS.

15% ownership stake is non-controlling. Unis is entitled to nominate 1 director only as long as it retains 10% of the Company’s outstanding shares. The Unis-nominated director will be screened off from any discussion or decisions regarding products and services provided the US government and other sensitive matters. Unis is required to vote its shares per WDC board recommendation on key matters requiring a shareholder vote. Unis has no operational or other control over the Company’s business and is subject to prohibitions on access to technology.

Buy/sell constraints are in place

The SNDK transaction is not dependent on closing the Unisplendour investment.

The Unis JV is separate from the Unis investment; it was contemplated well before the investment, and the two transactions we re discussed and negotiated independently. The JV should not have any effect on CFIUS’ review of the investment.

6 |

| © 2015 Western Digital Corporation. All Rights Reserved. |

|

SNDK OPERATIONAL / FINANCIAL PERFORMANCE

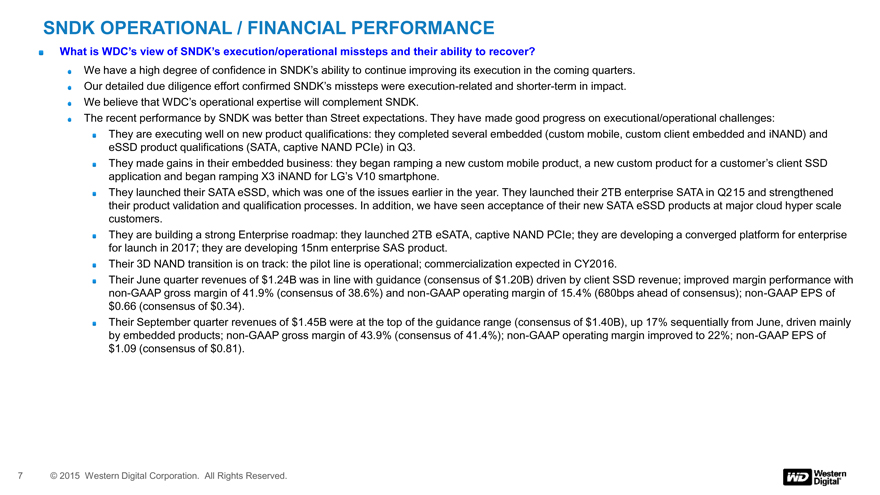

What is WDC’s view of SNDK’s execution/operational missteps and their ability to recover?

We have a high degree of confidence in SNDK’s ability to continue improving its execution in the coming quarters. Our detailed due diligence effort confirmed SNDK’s missteps were execution-related and shorter-term in impact. We believe that WDC’s operational expertise will complement SNDK.

The recent performance by SNDK was better than Street expectations. They have made good progress on executional/operational challenges:

They are executing well on new product qualifications: they completed several embedded (custom mobile, custom client embedded and iNAND) and eSSD product qualifications (SATA, captive NAND PCIe) in Q3.

They made gains in their embedded business: they began ramping a new custom mobile product, a new custom product for a customer’s client SSD application and began ramping X3 iNAND for LG’s V10 smartphone.

They launched their SATA eSSD, which was one of the issues earlier in the year. They launched their 2TB enterprise SATA in Q215 and strengthened their product validation and qualification processes. In addition, we have seen acceptance of their new SATA eSSD products at major cloud hyper scale customers.

They are building a strong Enterprise roadmap: they launched 2TB eSATA, captive NAND PCIe; they are developing a converged platform for enterprise for launch in 2017; they are developing 15nm enterprise SAS product.

Their 3D NAND transition is on track: the pilot line is operational; commercialization expected in CY2016.

Their June quarter revenues of $1.24B was in line with guidance (consensus of $1.20B) driven by client SSD revenue; improved margin performance with non-GAAP gross margin of 41.9% (consensus of 38.6%) and non-GAAP operating margin of 15.4% (680bps ahead of consensus); non-GAAP EPS of

$0.66 (consensus of $0.34).

Their September quarter revenues of $1.45B were at the top of the guidance range (consensus of $1.40B), up 17% sequentially from June, driven mainly by embedded products; non-GAAP gross margin of 43.9% (consensus of 41.4%); non-GAAP operating margin improved to 22%; non-GAAP EPS of

$1.09 (consensus of $0.81).

7 |

| © 2015 Western Digital Corporation. All Rights Reserved. |

|

FINANCE

What are WDC’s thoughts on the rationale for the premium paid for SNDK?

We believe this acquisition will provide significant return to our shareholders

We performed a comprehensive valuation of SNDK’s business, utilizing traditional methodologies such as a discounted cash flow an alysis, sum-of-the-parts, comparables analysis. We also analyzed premiums paid in the relevant precedent transactions. Additionally, our financial advisors, Bank of America Merrill Lynch and J.P. Morgan, each rendered an independent fairness opinion to our board of directors

When is the anticipated accretion associated with the SNDK acquisition?

We expect to be EPS accretive on a non-GAAP basis within 12 months of the transaction close

What are the cost synergies anticipated from the SNDK acquisition?

We anticipate annual run-rate synergies of $500 million within 18 months post-closing.

We expect the synergies to increase from the run -rate due to the benefits associated with vertical integration and having a captive NAND supply

WDC’s current eSSD business is at a c$1B run rate and it is expected to grow faster than the market for next 5 years, i.e. greater than 25% market growth rate. The majority of the cost of the product is NAND (ranging from 50% for vertically integrated suppliers and 80% for non-vertically integrated suppliers), where the COGS synergies will come from.

What is the reason for the minimum cash provision in the merger agreement?

This is in place to ensure focus on execution from SNDK prior to WDC having control of the operations and to maximize cash at SNDK to help reduce leverage.

8 |

| © 2015 Western Digital Corporation. All Rights Reserved. |

|

FINANCE

What are the details on the debt and de-levering associated with the SNDK acquisition?

The gross debt will be $17.4B

Approximately $6B will be used to retire WDC existing debt and SNDK existing convertible notes.

We expect to de-lever quickly and achieve a debt/EBITDA ratio of 1.5x in next 3 to 5 years allowing us to return to investment g rade rating.

What are WDC’s expectations for cash generation and free cash flow on a pro-forma basis?

We expect that liquidity, on a pro-forma basis, will be strong and we anticipate continued strong cash flow generation after the acquisition is completed.

9 © 2015 Western Digital Corporation. All Rights Reserved.