OPTICAL CABLE CORPORATION

Annual Report

2011

TABLE OF CONTENTS

| | | | |

| | 3 | | | Selected Consolidated Financial Information |

| |

| | 4 | | | Letter from the CEO |

| |

| | 7 | | | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

| |

| | 21 | | | Consolidated Financial Statements |

| |

| | 25 | | | Notes to Consolidated Financial Statements |

| |

| | 47 | | | Report of Independent Registered Public Accounting Firm |

| |

| | 48 | | | Corporate Information |

Page intentionally left blank.

| | | | |

| Optical Cable Corporation | | 2 | | |

Selected Consolidated Financial Information

(in thousands, except per share data)

| | | | | | | | | | | | | | | | | | | | |

| | | Years ended October 31, | |

| | | 2011 | | | 2010 | | | 2009 | | | 2008 | | | 2007 | |

Consolidated Statement of Operations Information: | | | | | | | | | | | | | | | | | | | | |

Net sales | | $ | 73,339 | | | $ | 67,506 | | | $ | 58,589 | | | $ | 60,998 | | | $ | 45,503 | |

Cost of goods sold | | | 47,048 | | | | 43,746 | | | | 38,748 | | | | 36,838 | | | | 28,333 | |

| | | | | | | | | | | | | | | | | | | | |

Gross profit | | | 26,291 | | | | 23,760 | | | | 19,841 | | | | 24,160 | | | | 17,170 | |

Selling, general and administrative expenses | | | 25,169 | | | | 24,268 | | | | 22,345 | | | | 20,642 | | | | 15,300 | |

Royalty income, net | | | (783 | ) | | | (1,233 | ) | | | (878 | ) | | | (636 | ) | | | — | |

Amortization of intangible assets | | | 431 | | | | 587 | | | | 825 | | | | 469 | | | | — | |

Impairment of goodwill | | | — | | | | 5,580 | | | | — | | | | — | | | | — | |

Impairment of intangible assets (other than goodwill) | | | — | | | | — | | | | 344 | | | | — | | | | — | |

| | | | | | | | | | | | | | | | | | | | |

Income (loss) from operations | | | 1,474 | | | | (5,442 | ) | | | (2,795 | ) | | | 3,685 | | | | 1,870 | |

Other income (expense), net: | | | | | | | | | | | | | | | | | | | | |

Interest income (expense), net | | | (620 | ) | | | (542 | ) | | | 149 | | | | (147 | ) | | | 21 | |

Other, net | | | 1 | | | | 65 | | | | 16 | | | | (24 | ) | | | 27 | |

| | | | | | | | | | | | | | | | | | | | |

Income (loss) before income taxes | | | 855 | | | | (5,919 | ) | | | (2,630 | ) | | | 3,514 | | | | 1,918 | |

Income tax expense (benefit) | | | 398 | | | | 91 | | | | (706 | ) | | | 1,302 | | | | 665 | |

| | | | | | | | | | | | | | | | | | | | |

Net income (loss) | | $ | 457 | | | $ | (6,010 | ) | | $ | (1,924 | ) | | $ | 2,212 | | | $ | 1,253 | |

Net loss attributable to noncontrolling interest(2) | | | (209 | ) | | | (277 | ) | | | — | | | | — | | | | — | |

| | | | | | | | | | | | | | | | | | | | |

Net income (loss) attributable to OCC | | $ | 666 | | | $ | (5,733 | ) | | $ | (1,924 | ) | | $ | 2,212 | | | $ | 1,253 | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

Net income (loss) per share attributable to OCC | | $ | 0.11 | | | $ | (0.95 | ) | | $ | (0.34 | ) | | $ | 0.36 | | | $ | 0.21 | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

PROFORMA net loss attributable to OCC, EXCLUDING impairment of goodwill(1) | | | | | | $ | (153 | ) | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

PROFORMA net loss per share attributable to OCC, EXCLUDING impairment of goodwill: | | | | | | | | | | | | | | | | | | | | |

Basic and diluted(1) | | | | | | $ | (0.03 | ) | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

Weighted average shares: | | | | | | | | | | | | | | | | | | | | |

Basic | | | 6,305 | | | | 6,015 | | | | 5,656 | | | | 6,062 | | | | 6,089 | |

| | | | | | | | | | | | | | | | | | | | |

Diluted | | | 6,305 | | | | 6,015 | | | | 5,656 | | | | 6,062 | | | | 6,096 | |

| | | | | | | | | | | | | | | | | | | | |

Consolidated Balance Sheet Information: | | | | | | | | | | | | | | | | | | | | |

Cash and cash equivalents | | $ | 1,092 | | | $ | 2,522 | | | $ | 1,948 | | | $ | 3,910 | | | $ | 3,139 | |

Working capital | | | 23,326 | | | | 22,905 | | | | 20,070 | | | | 23,765 | | | | 15,937 | |

Total assets | | | 44,945 | | | | 45,291 | | | | 50,327 | | | | 54,837 | | | | 37,281 | |

Bank debt | | | 8,191 | | | | 9,069 | | | | 8,536 | | | | 10,953 | | | | — | |

Total shareholders’ equity attributable to OCC | | | 28,209 | | | | 27,857 | | | | 33,257 | | | | 34,832 | | | | 31,978 | |

| (1) | Proforma net loss attributable to OCC and proforma net loss per share attributable to OCC are calculated by excluding the non-cash, non-recurring net impairment of goodwill charge of $5.6 million associated with the acquisition of Applied Optical Systems, Inc. (“AOS”) that was recorded during fiscal year 2010 from the Company’s net loss attributable to OCC as reported for the fiscal year ended October 31, 2010. There is no tax benefit associated with the goodwill impairment charge, as it is considered a non-deductible permanent item for tax purposes. Accordingly, there is no change to the tax expense as reported for fiscal year 2010 in determining the proforma net loss and net loss per share to the Consolidated Financial Statements. |

| (2) | Accounting Standards Codification 810-10,Consolidation(“ASC 810-10”), was adopted by OCC in fiscal year 2010 as it relates to noncontrolling interests. There are no noncontrolling interest amounts presented for fiscal years 2009 and 2008 since the minority interest’s share of losses attributable to Centric Solutions LLC was charged against the Company’s majority interest in accordance with the previous accounting literature. |

| | | | |

| | 3 | | Optical Cable Corporation |

Letter from the CEO

Dear Shareholders:

Record Net Sales Achieved—Again!

Optical Cable Corporation (OCC®) achieved record annual net sales once again in fiscal year 2011.

The Company grew annual net sales by 8.6% to $73.3 million—the highest in OCC’s history—surpassing our previous net sales record achieved just last year.

In addition to record sales, OCC recorded a number of other notable financial achievements in fiscal year 2011, including:

| | • | | Increased gross profit: OCC grew gross profit 10.7% to $26.3 million, and slightly increased gross profit margin (gross profit as a percentage of net sales) to 35.8% for fiscal year 2011. |

| | • | | Improved profitability: OCC achieved improved profitability during fiscal year 2011, reporting net income attributable to OCC of $0.11 per share, compared to a proforma net loss attributable to OCC of $0.03 per share in fiscal year 2010.1 |

| | • | | Generated strong cash flow: OCC generated $2.4 million in net cash provided by operating activities in fiscal 2011—continuing our track-record of generating annual positive cash provided by operating activities every year since 2001 (with the exception of fiscal year 20062). |

| | • | | Provided cash dividends to shareholders: OCC declared quarterly cash dividends totaling $0.04 per share during fiscal year 2011, returning $252,000 to shareholders and continuing the regular quarterly dividend first initiated by the OCC Board of Directors in October 2010. |

| | • | | Purchased and retired shares: OCC also returned $846,000 to shareholders during the fiscal year by purchasing and retiring 183,025 shares of OCC common stock. These share repurchases completed our previously announced plan to purchase and retire a total of 325,848 shares. |

| | • | | Reduced bank debt: OCC reduced its bank indebtedness by $878,000 during the year, paying down the balance on our revolving line of credit and reducing the principal owed on our long-term real estate debt. OCC had unused and available credit of $6.0 million at year end—the full amount of our revolving credit facility. |

| 1 | Reported net loss per share attributable to OCC was $0.95 per share in fiscal year 2010. Proforma net loss per share attributable to OCC of $0.03 excludes the non-cash, non-recurring goodwill impairment charge of $5.6 million, net, recorded during fiscal year 2010. |

| 2 | In fiscal year 2006, net cash used in operating activities by OCC was $58,000. |

| | | | |

| Optical Cable Corporation | | 4 | | |

Strong Execution of Strategy Continues

OCC’s improved financial performance reflects the successful execution of our strategy.

Over the past three years, we have integrated acquisitions and developed innovative new product offerings to provide our diverse customer base with the products, services and solutions they want and need.

Today, OCC provides a broad offering of fiber optic and copper data communication cabling and connectivity products to customers and end-users that offerunrivaled integrated solutions™ operating as an OCC system solution, or that can seamlessly integrate with other components.

As a result, we believe OCC is exceptionally well positioned in our targeted markets, placing us in an enviable position relative to our competitors and allowing us to compete more effectively over the long term.

While we have taken great strides forward, the OCC team remains focused on maximizing the growth opportunities provided by the continued successful execution of our strategy, and on improving operating efficiencies and controlling costs.

Continued Commitment to Creating Shareholder Value

We believe the continued successful execution of our strategy will create substantial long-term value for OCC shareholders.

OCC’s total shareholder return (share price appreciation plus dividends paid) was 13.8%1 during fiscal year 2011, outperforming the return of the Russell 2000® index, the S&P 500 index, and the Dow Jones Industrial Average during the same period.

OCC also announced earlier this month a 50% increase in our regular quarterly dividend rate to $0.015 per share, implying an annual dividend rate of $0.06 per share.

Despite our achievements, we believe that OCC’s strategy, market positioning, financial strength, and underlying value still are not fully appreciated by the equity market as reflected in our share price. Today, our shares trade at a significant discount to net book value per share. At the end of fiscal year 2011, OCC’s net book value attributable to OCC was $28.2 million, or $4.49 per share.

Consistent with our view of OCC’s value and following the completion of our previous share repurchase program in October 2011, the OCC Board of Directors authorized a new share repurchase program announced in November 2011. This new repurchase program authorizes the acquisition and retirement of up to 200,000 shares of our common stock (or approximately 3% of outstanding shares), and is anticipated to be completed over a 12- to 24-month period.

| 1 | OCC shares closed at $3.18 on November 1, 2010, and at $3.58 on October 31, 2011. OCC paid dividends of $0.04 per share during fiscal year 2011. |

| | | | |

| | 5 | | Optical Cable Corporation |

Looking Forward to 2012

We have strived to position OCC for growth—and we continue to aggressively pursue that objective.

In February 2012, OCC will unveil a new family of high-density, easy access products and solutions. This new family of OCC products will be called Procyon™ and will include both cabling and connectivity products. We are excited about the opportunities this new product offering is expected to create, and look forward to releasing further details at the 2012 BICSI Winter Conference in early February.

As we look forward to fiscal year 2012, we believe we will continue to experience seasonality that results in lower net sales during the first half of our fiscal year than during the second half of our fiscal year. Past experience also has shown that our sales can vary from quarter to quarter as a result of the timing of larger projects and temporary fluctuations in demand, or as a result of changes in demand in individual markets.

Despite any quarterly variability we may experience during fiscal 2012, we are confident that fiscal year 2012 will be a year of continued growth and success for OCC.

We look forward to reporting to you future positive results from the continued execution of our strategy and our ongoing efforts to enhance value for shareholders.

Thank you for your trust, and the privilege of allowing us to lead your company.

|

| /s/ Neil D. Wilkin, Jr. |

|

| Neil D. Wilkin, Jr. |

| Chairman of the Board, |

| President and Chief Executive Officer |

|

| January 26, 2012 |

| | | | |

| Optical Cable Corporation | | 6 | | |

Management’s Discussion and Analysis of Financial Condition and Results of Operations

Forward-Looking Information

This report may contain certain forward-looking information within the meaning of the federal securities laws. The forward-looking information may include, among other information, (i) statements concerning our outlook for the future, (ii) statements of belief, anticipation or expectation, (iii) future plans, strategies or anticipated events, and (iv) similar information and statements concerning matters that are not historical facts. Such forward-looking information is subject to known and unknown variables, uncertainties, contingencies and risks that may cause actual events or results to differ materially from our expectations, and such variables, uncertainties, contingencies and risks may also adversely affect Optical Cable Corporation and its subsidiaries (collectively, the “Company” or “OCC®”), the Company’s future results of operations and future financial condition, and/or the future equity value of the Company. Factors that could cause or contribute to such differences from our expectations or could adversely affect the Company include, but are not limited to, the level of sales to key customers, including distributors; timing of certain projects and purchases by key customers; the economic conditions affecting network service providers; corporate and/or government spending on information technology; actions by competitors; fluctuations in the price of raw materials (including optical fiber, copper, gold and other precious metals, and plastics and other materials affected by petroleum product pricing); fluctuations in transportation costs; our dependence on customized equipment for the manufacture of our products and a limited number of production facilities; our ability to protect our proprietary manufacturing technology; our ability to replace royalty income as existing patented and licensed products expire by developing and licensing new products; market conditions influencing prices or pricing; our dependence on a limited number of suppliers; the loss of or conflict with one or more key suppliers or customers; an adverse outcome in litigation, claims and other actions, and potential litigation, claims and other actions against us; an adverse outcome in regulatory reviews and audits and potential regulatory reviews and audits; adverse changes in state tax laws and/or positions taken by state taxing authorities affecting us; technological changes and introductions of new competing products; changes in end-user preferences for competing technologies, relative to our product offering; economic conditions that affect the telecommunications sector, certain technology sectors or the economy as a whole; changes in demand for our products from certain competitors for which we provide private label connectivity products; terrorist attacks or acts of war, and any current or potential future military conflicts; changes in the level of military spending or other spending by the United States government; ability to retain key personnel; inability to recruit needed personnel; poor labor relations; the impact of changes in accounting policies and related costs of compliance, including changes by the Securities and Exchange Commission (SEC), the Public Company Accounting Oversight Board (PCAOB), the Financial Accounting Standards Board (FASB), and/or the International Accounting Standards Board (IASB); our ability to continue to successfully comply with, and the cost of compliance with, the provisions of Section 404 of the Sarbanes-Oxley Act of 2002 or any revisions to that act which apply to us; the impact of changes and potential changes in federal laws and regulations adversely affecting our business and/or which result in increases in our direct and indirect costs, including our direct and indirect costs of compliance with such laws and regulations; the impact of the Patient Protection and Affordable Care Act of 2010, the Health Care and Education Reconciliation Act of 2010, and any revisions to those acts that apply to us and the related legislation and regulation associated with those acts, which directly or indirectly results in increases to our costs; the impact of changes in state or federal tax laws and regulations increasing our costs; the impact of future consolidation among competitors and/or among customers adversely affecting our position with our customers and/or our market position; actions by customers adversely affecting us in reaction to the expansion of our product offering in any manner, including, but not limited to, by offering products that compete with our customers, and/or by entering into alliances with, making investments in or with, and/or acquiring parties that compete with and/or have conflicts with customers of ours; voluntary or involuntary delisting of the Company’s capital stock from any exchange on which it is traded; the deregistration by the Company from SEC reporting requirements, as a result of the small number of holders of the Company’s capital stock; adverse reactions by

| | | | |

| | 7 | | Optical Cable Corporation |

customers, vendors or other service providers to unsolicited proposals regarding the ownership or management of the Company; the additional costs of considering and possibly defending our position on such unsolicited proposals; impact of weather or natural disasters in the areas of the world in which we operate, market our products and/or acquire raw materials; an increase in the number of the Company’s capital stock issued and outstanding; economic downturns and/or changes in market demand, exchange rates, productivity, or market and economic conditions in the areas of the world in which we operate and market our products; and our success in managing the risks involved in the foregoing.

We caution readers that the foregoing list of important factors is not exclusive. Furthermore, we incorporate by reference those factors included in current reports on Form 8-K, and/or in our other filings.

Dollar amounts presented in the following discussion have been rounded to the nearest hundred thousand, unless the amounts are less than one million and except in the case of the table set forth in the “Results of Operations” section, in which cases the amounts have been rounded to the nearest thousand.

Overview of Optical Cable Corporation

Optical Cable Corporation (or OCC®) is a leading manufacturer of a broad range of fiber optic and copper data communication cabling and connectivity solutions primarily for the enterprise market, offering an integrated suite of high quality, warranted products which operate as a system solution or seamlessly integrate with other providers’ offerings. Our product offerings include designs for uses ranging from commercial, enterprise network, datacenter, residential and campus installations to customized products for specialty applications and harsh environments, including military, industrial, mining and broadcast applications. Our products include fiber optic and copper cabling, fiber optic and copper connectors, specialty fiber optic and copper connectors, fiber optic and copper patch cords, pre-terminated fiber optic and copper cable assemblies, racks, cabinets, datacom enclosures, patch panels, face plates, multi-media boxes, and other cable and connectivity management accessories, and are designed to meet the most demanding needs of end-users, delivering a high degree of reliability and outstanding performance characteristics.

OCC® is internationally recognized for pioneering the design and production of fiber optic cables for the most demanding military field applications, as well as of fiber optic cables suitable for both indoor and outdoor use, and creating a broad product offering built on the evolution of these fundamental technologies. OCC also is internationally recognized for its role in establishing copper connectivity data communications standards, through its innovative and patented technologies.

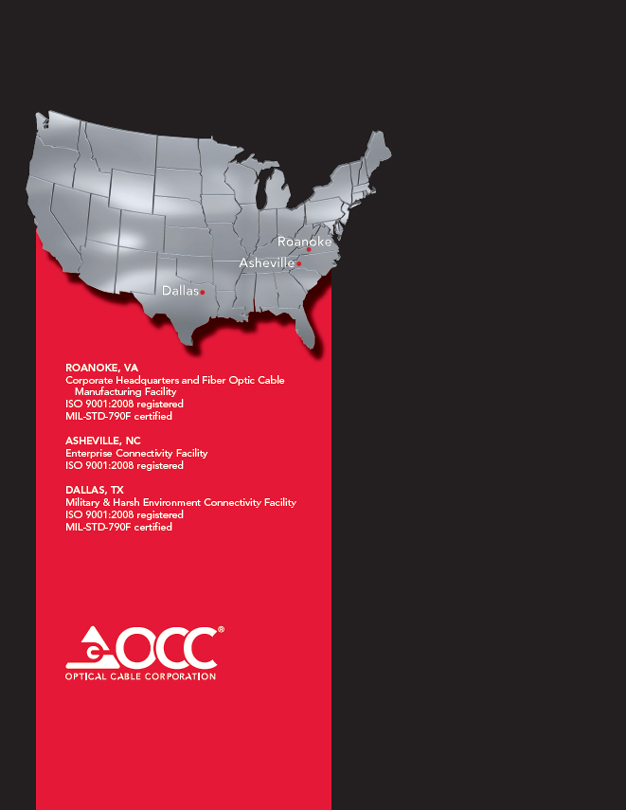

Founded in 1983, Optical Cable Corporation is headquartered in Roanoke, Virginia with offices, manufacturing and warehouse facilities located in Roanoke, Virginia, near Asheville, North Carolina and near Dallas, Texas. We primarily manufacture our fiber optic cables at our Roanoke facility which is ISO 9001:2008 registered and MIL-STD-790F certified, our enterprise connectivity products at our Asheville facility which is ISO 9001:2008 registered, and our military and harsh environment connectivity products and systems at our Dallas facility which is ISO 9001:2008 registered and MIL-STD-790F certified.

Our Asheville team designs and manufactures fiber and copper connectivity products for the commercial market, including a broad range of commercial and residential applications. We refer to these products as our enterprise connectivity product offering.

Our Dallas team designs, develops and manufactures a broad range of specialty fiber optic connectors and connectivity solutions primarily for use in military and other harsh environment applications. We refer to these products as our applied interconnect systems product offering. We market and sell the products manufactured at our Dallas facility by our wholly owned subsidiary Applied Optical Systems, Inc. (“AOS”) under the names Optical Cable Corporation and OCC through the efforts of our integrated sales team.

| | | | |

| Optical Cable Corporation | | 8 | | |

Additionally, Optical Cable Corporation owns 70% of the authorized membership interests of Centric Solutions LLC (“Centric Solutions”). Centric Solutions is a start-up business founded in 2008 to provide turnkey cabling and connectivity solutions for the datacenter market. Centric Solutions operates and goes to market separately from Optical Cable Corporation, however, in some cases, Centric Solutions may offer products from OCC’s product offering. Centric Solutions goes to market separately with its own sales team.

Optical Cable Corporation, OCC®, Superior Modular Products, SMP Data Communications, Applied Optical Systems, and associated logos are trademarks of Optical Cable Corporation.

Summary of Company Performance for Fiscal Year 2011

Our vision and strategy for Optical Cable Corporation has been to build on our strong reputation and market position in the fiber optic cable industry in commercial and specialty markets (our fiber optic cable product offering) by adding a suite of connectivity products enabling us to offer top-tier, end-to-end integrated cabling and connectivity solutions to our customers and end-users in our targeted markets. We have focused our efforts this past year on continuing to integrate our subsidiaries and streamlining the operations of all of our facilities with positive results. We have gained manufacturing efficiencies at our fiber optic cable and applied interconnect systems facilities which have positively impacted our gross profit margins. During fiscal year 2011, we also focused on reassessing our sales force and the sales resources needed to successfully bring our expanded product offerings to market for maximum effectiveness. And, we are just starting to see the positive results, as evidenced by the significant increase in net sales in fiscal year 2011.

In fiscal year 2011, we began to see the positive results of our strategic initiatives and continued integration efforts.

| | • | | During fiscal year 2011, OCC recorded the highest annual net sales in the Company’s history, exceeding the previous record for annual net sales set in fiscal year 2010. Consolidated net sales increased 8.6% to $73.3 million compared to $67.5 million for fiscal year 2010. |

| | • | | Gross profit increased 10.7% to $26.3 million for fiscal year 2011 compared to $23.8 million for fiscal year 2010. Gross profit margin (gross profit as a percentage of net sales) increased slightly to 35.8% for fiscal year 2011 from 35.2% for fiscal year 2010. |

| | • | | Net income attributable to OCC increased to $666,000, or $0.11 per share, during fiscal year 2011, compared to a net loss attributable to OCC of $5.7 million, or $0.95 per share, for fiscal year 2010. Net income attributable to OCC also increased during fiscal year 2011 compared to our proforma net loss attributable to OCC of $153,000, or $0.03 per share, for fiscal year 2010 (excluding the non-recurring, non-cash $5.6 million net goodwill impairment charge for fiscal year 2010). This proforma net loss and net loss per share for fiscal year 2010 is calculated by adding the net impairment charge of $5.6 million to our pre-tax loss as reported for fiscal year 2010. There is no tax benefit associated with the impairment charge, as it is considered a non-deductible permanent item for tax purposes, so there is no change to the tax expense as reported for fiscal year 2010 in determining the proforma net loss and net loss per share. |

| | • | | OCC generated annual positive cash flow from operating activities again this year, as we have each year after fiscal year 2000, with the exception of fiscal year 2006 when $58,000 net cash was used in operating activities by OCC. Net cash provided by operating activities was $2.4 million in fiscal year 2011. |

| | • | | We reduced our bank indebtedness during fiscal year 2011 by $878,000, by paying down our revolving line of credit and reducing the principal owed on our long-term real estate term debt. OCC ended fiscal year 2011 with $6 million in unused and available credit on our revolving line of credit. |

| | • | | OCC declared quarterly cash dividends totaling $0.04 per share during fiscal year 2011, continuing the regular return of capital to shareholders initiated when we declared our first quarterly dividend in October 2010. In January 2012, we announced an increase in our regular quarterly dividend rate to $0.015 per share per quarter, implying an annual dividend rate of $0.06 per share. |

| | | | |

| | 9 | | Optical Cable Corporation |

| | • | | We also returned $846,000 in capital to shareholders through the repurchases of OCC’s common stock during fiscal year 2011. OCC repurchased and retired 183,025 shares of common stock during the year. |

Results of Operations

We sell our products internationally and domestically through our sales force to our customers, which include major distributors, regional distributors, various smaller distributors, original equipment manufacturers and value-added resellers. All of our sales to customers located outside of the United States are denominated in U.S. dollars. We can experience fluctuations in the percentage of net sales to customers outside of the United States from period to period based on the timing of large orders, coupled with the impact of increases and decreases in sales to customers located in the United States.

Net sales consist of gross sales of products less discounts, refunds and returns. Revenue is recognized at the time of product shipment or delivery to the customer (including distributors) provided that the customer takes ownership and assumes risk of loss (based on shipping terms), collection of the relevant receivable is probable, persuasive evidence of an arrangement exists and sales price is fixed or determinable. Our customers generally do not have the right of return unless a product is defective or damaged and is within the parameters of the product warranty in effect for the sale.

Cost of goods sold consists of the cost of materials, product warranty costs and compensation costs, and overhead and other costs related to our manufacturing operations. The largest percentage of costs included in cost of goods sold is attributable to costs of materials.

Our gross profit margin percentages are heavily dependent upon product mix on a quarterly basis and may vary based on both anticipated and unanticipated changes in product mix. Additionally, gross profit margins tend to be higher when we achieve higher net sales levels, as certain fixed manufacturing costs are spread over higher sales volumes.

Selling, general and administrative expenses (“SG&A expenses”) consist of the compensation costs for sales and marketing personnel, shipping costs, trade show expenses, customer support expenses, travel expenses, advertising, bad debt expense, the compensation costs for administration and management personnel, legal and accounting fees, costs incurred to settle litigation or claims and other actions against us, and other costs associated with our operations.

Royalty income, net consists of royalty income earned on licenses associated with our patented products, net of royalty and related expenses.

Amortization of intangible assets consists of the amortization of developed technology acquired in the acquisition of Superior Modular Products Incorporated, doing business as SMP Data Communications (“SMP Data Communications” or “SMP”) on May 30, 2008, and the amortization of intellectual property and customer list acquired in the acquisition of AOS on October 31, 2009. Amortization of intangible assets is calculated using an accelerated method and the straight line method over the estimated useful lives of the intangible assets.

Other income (expense), net consists of interest income, interest expense, and other miscellaneous income and expense items not directly attributable to our operations.

| | | | |

| Optical Cable Corporation | | 10 | | |

The following table sets forth and highlights fluctuations in selected line items from our consolidated statements of operations for the periods indicated:

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Fiscal Years Ended

October 31, | | | | | | Fiscal Years Ended

October 31, | | | | |

| | | 2011 | | | 2010 | | | Percent

Change | | | 2010 | | | 2009 | | | Percent

Change | |

Net sales | | $ | 73,300,000 | | | $ | 67,500,000 | | | | 8.6 | % | | $ | 67,500,000 | | | $ | 58,600,000 | | | | 15.2 | % |

Gross profit | | | 26,300,000 | | | | 23,800,000 | | | | 10.7 | | | | 23,800,000 | | | | 19,800,000 | | | | 19.8 | |

SG&A expenses | | | 25,200,000 | | | | 24,300,000 | | | | 3.7 | | | | 24,300,000 | | | | 22,300,000 | | | | 8.6 | |

Impairment of goodwill | | | — | | | | 5,600,000 | | | | (100.0 | ) | | | 5,600,000 | | | | — | | | | 100.0 | |

Net income (loss) attributable to OCC | | | 666,000 | | | | (5,700,000 | ) | | | 111.6 | | | | (5,700,000 | ) | | | (1,900,000 | ) | | | 197.9 | |

Net Sales

OCC recorded the highest annual net sales in the Company’s history during fiscal year 2011. Net sales increased 8.6% to $73.3 million in fiscal year 2011 compared to $67.5 million in fiscal year 2010. The increase in net sales when comparing fiscal years 2011 and 2010 is due primarily to the increase in net sales of our applied interconnect systems products and our fiber optic cable products. Applied interconnect systems products were added to the OCC product offering in fiscal year 2010, with the acquisition of AOS effective October 31, 2009. As a result of successful integration processes over the past year, we gained synergies due to our integrated sales force and also gained efficiencies associated with throughput in the AOS production facility, resulting in significant increases in net sales in the second half of fiscal year 2010 and throughout fiscal year 2011.

OCC recorded the second highest annual net sales in the Company’s history during fiscal year 2010. Net sales increased 15.2% to $67.5 million in fiscal year 2010 compared to $58.6 million in fiscal year 2009. The increase in net sales during fiscal year 2010 when compared to fiscal year 2009 was attributable to the fact that we experienced increases in both our commercial markets and our specialty markets during fiscal year 2010 when compared to fiscal year 2009. The acquisition of AOS by OCC on October 31, 2009 also contributed to the net sales growth totaling $8.0 million in fiscal year 2010.

Net sales to customers located outside of the United States were 24%, 27% and 27% of total net sales for fiscal years 2011, 2010 and 2009, respectively. Net sales to customers located in the United States increased 12.2% during fiscal year 2011 compared to fiscal year 2010 while net sales to customers located outside of the United States decreased 1.2%. The increase in net sales to customers located in the United States is due to the fact that we experienced increases in net sales of our fiber optic cable products and our existing applied interconnect systems products to U.S. customers during fiscal year 2011.

We typically expect net sales to be relatively lower in the first half of each fiscal year and relatively higher in the second half of each fiscal year. We believe this historical seasonality pattern is generally indicative of an overall trend and reflective of the buying patterns and budgetary cycles of our customers. However, this pattern may be substantially altered during any quarter or year by the timing of larger projects, other economic factors impacting our industry or impacting the industries of our customers and end-users and macro-economic conditions. While we believe seasonality may be a factor that impacts our quarterly net sales results, we are not able to reliably predict net sales based on seasonality because these other factors can also substantially impact our net sales patterns during the year.

We believe our consolidated net sales may be negatively impacted by the continuing global economic recession. However, when comparing net sales for fiscal year 2011 to fiscal year 2010, the sale of our fiber optic cable and applied interconnect systems products have improved. We believe our improvement in net sales may indicate we have achieved market share gains in certain of our markets and may indicate the beginning of some improvements in certain of our markets. However, we cannot be sure at this time if these gains and/or this improvement are an indication of a trend or predict whether or not they will continue.

| | | | |

| | 11 | | Optical Cable Corporation |

Gross Profit

Gross profit increased 10.7% to $26.3 million in fiscal year 2011 from $23.8 million in fiscal year 2010. Gross profit margin, or gross profit as a percentage of net sales, increased slightly to 35.8% for fiscal year 2011, compared to 35.2% for fiscal year 2010.

Gross profit increased 19.8% to $23.8 million in fiscal year 2010 from $19.8 million in fiscal year 2009. Gross profit margin, or gross profit as a percentage of net sales, increased to 35.2% for fiscal year 2010, compared to 33.9% for fiscal year 2009.

Our gross profit margin percentages are heavily dependent upon product mix on a quarterly basis and may deviate from expectations based on both anticipated and unanticipated changes in product mix. Additionally, our gross profit margins for our product lines tend to be higher when we achieve higher net sales levels of those product lines as certain fixed manufacturing costs are spread over higher sales volumes.

Selling, General and Administrative Expenses

SG&A expenses increased to $25.2 million in fiscal year 2011 from $24.3 million in fiscal year 2010. SG&A expenses as a percentage of net sales were 34.3% in fiscal year 2011 compared to 35.9% in fiscal year 2010.

The increase in SG&A expenses during fiscal year 2011 compared to fiscal year 2010 was primarily due to increased compensation costs including increases in commissions, increased shipping costs, and increased selling and marketing related expenses. Compensation costs increased in fiscal year 2011 largely as a result of strategic new hires in our sales and marketing teams. Commissions increased due to the increase in net sales in fiscal year 2011 and changes in the manner in which we incent the sales force, made in an effort to increase net sales. Shipping costs increased due primarily to increases in the cost of our international shipments.

SG&A expenses increased to $24.3 million in fiscal year 2010 from $22.3 million in fiscal year 2009. SG&A expenses as a percentage of net sales decreased to 35.9% in fiscal year 2010 compared to 38.1% in fiscal year 2009.

But for the acquisition of AOS on October 31, 2009, we believe our SG&A expenses would have decreased by at least $984,000 during fiscal year 2010, compared to fiscal year 2009. The acquisition of AOS added at least $2.9 million to our consolidated SG&A expenses in fiscal year 2010, including $988,000 of employee related costs and $666,000 of legal fees (related to litigation in the patent infringement lawsuit to which AOS is a party). Excluding the impact of the acquisition of AOS, affecting consolidated SG&A expenses were: our continued efforts to reduce costs, work force reductions initiated during the third quarter of fiscal year 2009, and savings and costs (net) related to continued integration efforts of the acquisitions of SMP Data Communications and AOS.

Royalty Income, Net

We recognized royalty income, net of royalty and related expenses, totaling $783,000 during fiscal year 2011, compared to $1.2 million during fiscal year 2010. The decrease in sales of licensed products by licensees during fiscal year 2011 contributed to the decrease in royalty income, net when compared to fiscal year 2010. This income is largely offset by the expense of the amortization of the intangible assets associated with our royalty income, net (as further described in theAmortization of Intangible Assets section included herein), resulting from recording of identifiable intangible assets at fair value when acquired as part of the acquisition of SMP Data Communications on May 30, 2008. Certain patents which generate a portion of our royalty income will begin to expire during our 2012 fiscal year. As a result, we expect to see a trend of declining royalty income and we expect amortization of intangible assets expense to continue to decline.

We recognized royalty income, net of related expenses, totaling $1.2 million during fiscal year 2010, compared to royalty income, net of related expenses, totaling $878,000 during fiscal year 2009. The increase was due to the increase in sales of licensed products by licensees during fiscal year 2010 compared to fiscal year 2009.

| | | | |

| Optical Cable Corporation | | 12 | | |

Amortization of Intangible Assets

We recognized $431,000 of amortization expense, associated with intangible assets, during fiscal year 2011, compared to amortization expense of $587,000 during fiscal year 2010. The decrease in amortization expense, when comparing the two fiscal years, is primarily due to the fact that the purchased developed technology asset, acquired in connection with the acquisition of SMP Data Communications, is being amortized using a declining balance method over the useful life of the asset; therefore, the amortization expense decreases as the asset ages.

We recognized $587,000 of amortization expense, associated with intangible assets, during fiscal year 2010, compared to amortization expense of $825,000 during fiscal year 2009. The decrease in amortization expense, when comparing the two fiscal years, is due to the fact that the trade name and customer list intangible assets, acquired in connection with the acquisition of SMP Data Communications, were written off during fiscal year 2009 when it was concluded that these assets were impaired. The decrease was partially offset by the addition in fiscal year 2009 of intangible assets acquired in the acquisition of AOS on October 31, 2009 and the related amortization of those intangible assets beginning in fiscal year 2009.

Impairment of Goodwill

During fiscal year 2010, we performed an annual impairment analysis of goodwill (associated with the acquisition of AOS) as required by U.S. GAAP. We analyzed the carrying value of goodwill as of April 30, 2010 and determined that it was appropriate to write-off the carrying value of goodwill on our consolidated balance sheet. As a result, we recorded a non-recurring, non-cash impairment charge of $5.6 million during fiscal year 2010—consisting of (i) a $6.2 million goodwill impairment charge recognized during the second quarter of fiscal year 2010 and (ii) a $666,000 reversal of the goodwill charge associated with a purchase accounting adjustment recognized during the fourth quarter of fiscal year 2010. The purchase accounting adjustment made during the fourth quarter was primarily the result of the Company’s adjustment to the valuation of certain deferred tax assets acquired in the purchase of AOS, and is not a result of a re-evaluation of the goodwill impairment recorded during the second quarter of fiscal year 2010.

No such impairment charge was incurred in fiscal year 2011 or 2009.

Impairment of Intangible Assets (other than goodwill)

During fiscal year 2009, we discontinued marketing our connectivity products under the SMP Data Communications trade name and began to market these products under the names Optical Cable Corporation and OCC®. Additionally, we re-evaluated the value assigned to the customer list asset using more current post-acquisition financial information. As a result, we determined the trade name and customer list assets were impaired and recorded a non-cash, non-recurring impairment charge totaling $344,000 during fiscal year 2009.

No such impairment charge was incurred in fiscal years 2011 or 2010.

Other Income (Expense), Net

We recognized other expense, net of $619,000 in fiscal year 2011 compared to $477,000 in fiscal year 2010. Other expense, net for fiscal year 2011 is comprised of: interest income totaling $5,000; interest expense totaling $625,000 related primarily to monies borrowed in connection with the acquisition of SMP Data Communications in fiscal year 2008, borrowings under our revolving credit facility, and other interest incurred in the normal course of business; and other miscellaneous items which may fluctuate from period to period.

We recognized other expense, net of $477,000 in fiscal year 2010 compared to other income, net of $165,000 in fiscal year 2009. Other expense, net for fiscal year 2010 is comprised of: interest income totaling $80,000; interest expense totaling $622,000 related primarily to monies borrowed in connection with the acquisition of SMP Data Communications in fiscal year 2008, borrowings under our revolving credit facility, and other interest incurred in the normal course of business; and other miscellaneous items which may fluctuate from period to period. Other income, net for fiscal year 2009 is comprised of: interest income totaling $831,000, of which

| | | | |

| | 13 | | Optical Cable Corporation |

$819,000 was recognized during the fourth quarter of fiscal year 2009 in connection with accounting for the acquisition of AOS on October 31, 2009, and related to our note receivable from AOS; interest expense totaling $682,000 related to monies borrowed in connection with the acquisition of SMP Data Communications in fiscal year 2008; and other miscellaneous items which fluctuate from period to period.

Income (Loss) Before Income Taxes

We reported income before income taxes of $856,000 for fiscal year 2011 compared to a loss before income taxes of $5.9 million for fiscal year 2010. This change was due to the increase in gross profit of $2.5 million in fiscal year 2011 compared to fiscal year 2010, partially offset by the increase in SG&A expenses of $901,000, and the non-recurring loss on the impairment of goodwill of $5.6 million recorded in fiscal year 2010. Excluding the goodwill impairment charge, we would have reported a net loss before income taxes of $339,000 in fiscal year 2010.

We reported a loss before income taxes of $5.9 million for fiscal year 2010 compared to a loss before income taxes of $2.6 million in fiscal year 2009. The increase was primarily due to the impairment of goodwill of $5.6 million and the increase in SG&A expenses of $1.9 million in fiscal year 2010 compared to fiscal year 2009. The increase in the loss before income taxes was partially offset by the increase in gross profit of $3.9 million. But for the goodwill impairment charge of $5.6 million during fiscal year 2010, we would have reported a loss before income taxes of $339,000 compared to a loss before income taxes of $2.6 million for fiscal year 2009.

Income Tax Expense (Benefit)

Income tax expense totaled $398,000 for fiscal year 2011, compared to $91,000 for fiscal year 2010. Our effective tax rate was 46.5% in fiscal year 2011, compared to negative 1.5% in fiscal year 2010.

Fluctuations in our effective tax rates are primarily due to permanent differences in U.S. GAAP and tax accounting for various tax deductions and benefits, but can also be significantly different from the statutory tax rate when income or loss before taxes is at a level, generally close to breakeven, that permanent differences in U.S. GAAP and tax accounting treatment have a disproportional impact on the projected effective tax rate.

During fiscal year 2010, we recorded a non-recurring, non-cash impairment charge in the amount of $5.6 million to write-off the carrying value of goodwill. Since our tax basis in the goodwill was zero, this resulted in a permanent $5.6 million difference between book and taxable income and was the primary cause of our significantly lower effective tax rate in that year.

Income tax expense totaled $91,000 for fiscal year 2010, compared to income tax benefit of $706,000 for fiscal year 2009. Our effective tax rate was negative 1.5% in fiscal year 2010, compared to 26.8% in fiscal year 2009.

Net Income (Loss)

Net income attributable to OCC for fiscal year 2011 was $666,000 compared to a net loss attributable to OCC of $5.7 million for fiscal year 2010. This change was primarily due to the increase in income before income taxes of $6.8 million for fiscal year 2011 compared to fiscal year 2010.

Net loss attributable to OCC for fiscal year 2010 was $5.7 million compared to a net loss of $1.9 million in fiscal year 2009. This increase was due primarily to the increase in the loss before income taxes of $3.3 million for fiscal year 2010 compared to fiscal year 2009 and the recognition of tax expense of $91,000 in fiscal year 2010 compared to a tax benefit of $706,000 in fiscal year 2009.

| | | | |

| Optical Cable Corporation | | 14 | | |

Financial Condition

Total assets decreased $346,000, or less than one percent, to $44.9 million at October 31, 2011, from $45.3 million at October 31, 2010. This decrease is due primarily to a $1.4 million decrease in cash, a $581,000 decrease in property, plant and equipment, and a $400,000 decrease in intangible assets, partially offset by a $2.1 million increase in inventories, net. Further detail regarding the decrease in cash is provided in our discussion of “Liquidity and Capital Resources”. The decrease in property, plant and equipment is due to the fact that depreciation expense was greater than asset additions for fiscal year 2011. The decrease in intangible assets is due to the continued amortization of the intangible assets acquired in connection with our previous acquisitions. The increase in inventories is largely due to the timing of raw material purchases and efforts to decrease lead times by increasing certain standard stock items.

Total liabilities decreased $488,000, or 2.8%, to $17.2 million at October 31, 2011, from $17.7 million at October 31, 2010. This decrease is primarily due to the $700,000 repayment of our note payable to bank under our revolving credit facility during fiscal year 2011.

Total shareholders’ equity attributable to OCC at October 31, 2011 increased $352,000, or 1.3%, during fiscal year 2011. The increase resulted from net income attributable to OCC of $666,000 and share-based compensation, net of $631,000, partially offset by the repurchase and retirement of 183,025 shares of our common stock for $846,000.

Liquidity and Capital Resources

Our primary capital needs during fiscal year 2011 have been to fund working capital requirements and capital expenditures, to repay the outstanding balance on our revolving credit facility, as well as the repurchase and retirement of our common stock. Our primary source of capital for these purposes has been existing cash and cash provided by operations. As of October 31, 2011, we did not have an outstanding loan balance under our revolving credit facility. As of October 31, 2010, we had an outstanding loan balance under our revolving credit facility totaling $700,000. As of October 31, 2011 and 2010, we had outstanding loan balances, excluding our revolving credit facility, totaling $8.2 million and $8.4 million, respectively.

Our cash totaled $1.1 million as of October 31, 2011, a decrease of $1.4 million, compared to $2.5 million as of October 31, 2010. The decrease in cash for the fiscal year ended October 31, 2011, resulted from net cash used in financing activities of $2.3 million (primarily related to the repurchase and retirement of our common stock totaling $846,000, the repayment of our note payable to bank under our revolving credit facility of $700,000 and cash dividends paid totaling $252,000), and net cash used in investing activities of $1.5 million (primarily related to capital expenditures), partially offset by net cash provided by operating activities of $2.4 million.

On October 31, 2011, we had working capital of $23.3 million, compared to $22.9 million as of October 31, 2010. The ratio of current assets to current liabilities as of October 31, 2011, was 3.8 to 1 compared to 4.0 to 1 as of October 31, 2010. The increase in working capital during fiscal year 2011 was primarily due to the $2.1 million increase in inventories, partially offset by the $1.4 million decrease in cash.

Net Cash

Net cash provided by operating activities was $2.4 million in fiscal year 2011 compared to $1.2 million in fiscal year 2010, and $2.8 million in fiscal year 2009.

Net cash provided by operating activities during fiscal year 2011 primarily resulted from net income of $457,000 and certain adjustments to reconcile net income to net cash provided by operating activities, including depreciation and amortization of $2.7 million and share-based compensation expense of $893,000. All of the aforementioned factors positively affecting cash provided by operating activities were partially offset by an increase in inventories of $2.1 million.

| | | | |

| | 15 | | Optical Cable Corporation |

Net cash provided by operating activities during fiscal year 2010 primarily resulted from certain adjustments to reconcile net loss to net cash provided by operating activities including the impairment of goodwill of $5.6 million, depreciation, amortization and accretion of $3.0 million and share-based compensation expense of $943,000. Additionally, the decrease in income taxes refundable in the amount of $1.5 million further contributed to net cash provided by operating activities. All of the aforementioned factors positively affecting cash provided by operating activities were partially offset by the increase in inventories of $2.1 million, the increase in accounts receivable totaling $1.2 million, and a net loss totaling $6.0 million.

Net cash provided by operating activities during fiscal year 2009 primarily resulted from certain adjustments to reconcile net loss to net cash provided by operating activities including depreciation and amortization of $3.1 million and share-based compensation expense of $920,000. Additionally, the decrease in accounts receivable in the amount of $1.9 million and a decrease in inventories in the amount of $1.9 million, in both cases exclusive of assets and liabilities of AOS at the date of acquisition, further contributed to net cash provided by operating activities. All of the aforementioned factors positively affecting cash provided by operating activities were partially offset by the increase in income taxes refundable of $1.8 million and a decrease in accounts payable and accrued expenses (including accrued compensation and payroll taxes) totaling $2.0 million, again exclusive of assets and liabilities of AOS at the date of acquisition, and a net loss totaling $1.9 million.

Net cash used in investing activities totaled $1.5 million in fiscal year 2011 compared to $533,000 in fiscal year 2010 and $1.5 million in fiscal year 2009. Net cash used in investing activities during fiscal years 2011 and 2010 resulted primarily from the purchases of property and equipment and deposits for the purchase of property and equipment. Net cash used in investing activities during fiscal year 2009 resulted primarily from the acquisition of AOS and purchases of property and equipment and deposits for the purchase of property and equipment.

Net cash used in financing activities was $2.3 million in fiscal year 2011 compared to $44,000 in fiscal year 2010 and $3.3 million in fiscal year 2009. Net cash used in financing activities in fiscal year 2011 resulted primarily from the repurchase and retirement of 183,025 shares of our common stock totaling $846,000 and the repayment of our note payable to bank under our revolving credit facility of $700,000. Net cash used in financing activities in fiscal year 2010 resulted primarily from proceeds from a note payable to our bank under our line of credit in the amount of $700,000, partially offset by the repurchase and retirement of 143,000 shares of our common stock for $425,000. Net cash used in financing activities in fiscal year 2009 resulted primarily from the repayment of long-term debt of $2.4 million.

Credit Facilities

On May 30, 2008, we established $17.0 million in credit facilities (collectively, the “Credit Facilities”) with Valley Bank to provide for our working capital needs and to finance the acquisition of SMP Data Communications. The Credit Facilities provided a working capital line of credit (the “Revolving Loan”), a real estate term loan (the “Virginia Real Estate Loan”), a supplemental real estate term loan (the “North Carolina Real Estate Loan”), and a capital acquisitions term loan (the “Capital Acquisitions Term Loan”). The Capital Acquisitions Term Loan was fully funded in fiscal year 2008 and repaid in fiscal year 2009. Therefore, the $2.3 million portion of the original credit facility related to the Capital Acquisitions Term Loan is no longer available. On April 30, 2010, we entered into a revolving credit facility with SunTrust Bank (further described below) which replaced the Valley Bank Revolving Loan.

On April 22, 2011, OCC and Valley Bank entered into a Third Loan Modification Agreement (the “Agreement”) to the Credit Agreement dated May 30, 2008 entered into between the Company, Superior Modular Products Incorporated and Valley Bank. Under the Agreement, the interest rate and the applicable repayment installments of the Virginia Real Estate Loan and the North Carolina Real Estate Loan were revised and the maturity date of the loans was extended. The fixed interest rate of the two term loans was lowered to 5.85% from 6.0%, and the maturity date of the loans was extended from June 1, 2013 to April 30, 2018.

The Virginia Real Estate Loan was fully funded on May 30, 2008. Under the Agreement with Valley Bank, the Virginia Real Estate Loan accrues interest at 5.85% and payments of principal and interest are based on a 25 year amortization from the closing date of the Agreement. The remainder of the payments on the Virginia Real Estate Loan will be made in 83 equal monthly installments of principal and interest in the amount of $41,686 beginning May 1, 2011. The balance of the Virginia Real Estate Loan will be due April 30, 2018. As of October 31, 2011, we had outstanding borrowings of $6.1 million under our Virginia Real Estate Loan.

The North Carolina Real Estate Loan was fully funded on May 30, 2008. Under the Agreement with Valley Bank, the North Carolina Real Estate Loan accrues interest at 5.85% and payments of principal and interest are based on a 25 year amortization from the

| | | | |

| Optical Cable Corporation | | 16 | | |

closing date of the Agreement. The remainder of the payments on the North Carolina Real Estate Loan will be made in 83 equal monthly installments of principal and interest in the amount of $14,366 beginning May 1, 2011. The balance of the North Carolina Real Estate Loan will be due April 30, 2018. As of October 31, 2011, we had outstanding borrowings of $2.1 million under our North Carolina Real Estate Loan.

On April 30, 2010, we entered into a revolving credit facility with SunTrust Bank consisting of a Commercial Note and Agreement to Commercial Note under which SunTrust Bank provides us with a revolving line of credit for our working capital needs (the “Commercial Loan”). The Commercial Loan was due to mature on May 31, 2012. On July 25, 2011, we entered into a binding letter of renewal with SunTrust Bank of the commercial note extending the Commercial Loan to May 31, 2013. Concurrently with the renewal, we also entered into a Fourth Loan Modification Agreement with Valley Bank to amend the definition of ‘SunTrust Debt’ to provide for the extension of the revolver’s maturity date.

The Commercial Loan provides us the ability to borrow an aggregate principal amount at any one time outstanding not to exceed the lesser of (i) $6.0 million, or (ii) the sum of 85% of certain receivables aged 90 days or less plus 35% of the lesser of $1.0 million or certain foreign receivables plus 25% of certain raw materials inventory. Within the Revolving Loan Limit, we may borrow, repay, and reborrow, at any time until May 31, 2013.

Advances under the Commercial Loan accrue interest at the greater of (x) LIBOR plus 2.0%, or (y) 3.0%. Accrued interest on the outstanding principal balance is due on the first day of each month, with all then outstanding principal, interest, fees and costs due at the Commercial Loan Termination Date of May 31, 2013.

As of October 31, 2011, we had no outstanding borrowings on our Commercial Loan and $6.0 million in available credit.

The Commercial Loan is secured by a first priority lien on all of our inventory, accounts, general intangibles, deposit accounts, instruments, investment property, letter of credit rights, commercial tort claims, documents and chattel paper. The Virginia Real Estate Loan and the North Carolina Real Estate Loan are secured by a first priority lien on all of our personal property and assets, except for our inventory, accounts, general intangibles, deposit accounts, instruments, investment property, letter of credit rights, commercial tort claims, documents and chattel paper, as well as a first lien deed of trust on our real property.

Capital Expenditures

We did not have any material commitments for capital expenditures as of October 31, 2011. During our 2011 fiscal year budgeting process, we included an estimate for capital expenditures for the year of $2.0 million. We actually incurred capital expenditures totaling $1.5 million, for items including new manufacturing equipment, improvements to existing manufacturing equipment, new information technology equipment and software, upgrades to existing information technology equipment and software, furniture and other capitalizable expenditures for property, plant and equipment for fiscal year 2011.

During our 2012 fiscal year budgeting process, we included an estimate for capital expenditures of $2.5 million for the year. These expenditures will be funded out of our working capital or borrowings under our credit facilities. This amount includes estimates for capital expenditures for similar types of items as those purchased in fiscal year 2011. Capital expenditures are reviewed and approved based on a variety of factors including, but not limited to, current cash flow considerations, the expected return on investment, project

| | | | |

| | 17 | | Optical Cable Corporation |

priorities, impact on current or future product offerings, availability of personnel necessary to implement and begin using acquired equipment, and economic conditions in general. Historically, we have spent less than our budgeted capital expenditures in any given year.

Corporate acquisitions and other strategic investments are considered outside of our annual capital expenditure budgeting process.

Future Cash Flow Considerations

We believe that our cash flow from operations, our cash on hand and our existing credit facilities will be adequate to fund our operations for at least the next twelve months.

From time to time, we are involved in various claims, legal actions and regulatory reviews arising in the ordinary course of business. In the opinion of management, the ultimate disposition of these matters will not have a material adverse effect on our financial position, results of operations or liquidity.

Seasonality

Historically, net sales are relatively lower in the first half of each fiscal year and relatively higher in the second half of each fiscal year, which we believe may be partially due to construction cycles and budgetary considerations of our customers. For example, our trend has been that an average of approximately 45% of our net sales occurred during the first half of the fiscal year and an average of approximately 55% of our net sales occurred during the second half of the fiscal year for the past ten fiscal years, excluding fiscal years 2001, 2002 and 2009. Fiscal years 2001, 2002 and 2009 are excluded because we believe net sales did not follow this pattern due to overall economic conditions in the industry and/or in the world during these years.

As a result, we typically expect net sales to be relatively lower in the first half of each fiscal year and relatively higher in the second half of each fiscal year. We believe this historical seasonality pattern is generally indicative of an overall trend and reflective of the buying patterns and budgetary cycles of our customers. However, this pattern may be substantially altered during any quarter or year by the timing of larger projects, other economic factors impacting our industry or impacting the industries of our customer and end-users and macro-economic conditions. While we believe seasonality may be a factor that impacts our quarterly net sales results, we are not able to reliably predict net sales based on seasonality because these other factors can also substantially impact our net sales patterns during the year.

Critical Accounting Policies and Estimates

Our discussion and analysis of financial condition and results of operations is based on the consolidated financial statements and accompanying notes that have been prepared in accordance with U.S. generally accepted accounting principles. The preparation of these consolidated financial statements requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and the disclosure of contingent assets and liabilities at the date of the consolidated financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates.

Note 1 to the consolidated financial statements provides a summary of our significant accounting policies. The following are areas requiring significant judgments and estimates due to uncertainties as of the reporting date: revenue recognition, trade accounts receivable and the allowance for doubtful accounts, inventories, long-lived assets and commitments and contingencies.

Application of the critical accounting policies discussed in the section that follows requires management’s significant judgments, often as a result of the need to make estimates of matters that are inherently uncertain. If actual results were to differ materially from the estimates made, the reported results could be materially affected. We are not currently aware of any reasonably likely events or circumstances that would result in materially different results.

| | | | |

| Optical Cable Corporation | | 18 | | |

Revenue Recognition

Management views revenue recognition as a critical accounting estimate since we must estimate an allowance for sales returns for the reporting period. This allowance reduces net sales for the period and is based on our analysis and judgment of historical trends, identified returns and the potential for additional returns. The estimates for sales returns did not materially differ from actual results for the year ended October 31, 2011.

Trade Accounts Receivable and the Allowance for Doubtful Accounts

Management views trade accounts receivable and the related allowance for doubtful accounts as a critical accounting estimate since the allowance for doubtful accounts is based on judgments and estimates concerning the likelihood that individual customers will pay the amounts included as receivable from them. In determining the amount of allowance for doubtful accounts to be recorded for individual customers, we consider the age of the receivable, the financial stability of the customer, discussions that may have occurred with the customer and our judgment as to the overall collectibility of the receivable from that customer. In addition, we establish an allowance for all other receivables for which no specific allowances are deemed necessary. This general allowance for doubtful accounts is based on a percentage of total trade accounts receivable with different percentages used based on different age categories of receivables. The percentages used are based on our historical experience and our current judgment regarding the state of the economy and the industry.

Inventories

Management views the determination of the net realizable value of inventories as a critical accounting estimate since it is based on judgments and estimates regarding the salability of individual items in inventory and an estimate of the ultimate selling prices for those items. Individual inventory items are reviewed and adjustments are made based on the age of the inventory and our judgment as to the salability of that inventory in order for our inventories to be valued at the lower of cost or net realizable value.

Long-lived Assets

Management views the determination of the carrying value of long-lived assets as a critical accounting estimate since we must determine an estimated economic useful life in order to properly amortize or depreciate our long-lived assets and because we must consider if the value of any of our long-lived assets have been impaired, requiring adjustment to the carrying value.

Economic useful life is the duration of time the asset is expected to be productively employed by us, which may be less than its physical life. Management’s assumptions on wear and tear, obsolescence, technological advances and other factors affect the determination of estimated economic useful life. The estimated economic useful life of an asset is monitored to determine if it continues to be appropriate in light of changes in business circumstances. For example, technological advances or excessive wear and tear may result in a shorter estimated useful life than originally anticipated. In such a case, we would depreciate the remaining net book value of an asset over the new estimated remaining life, thereby increasing depreciation expense per year on a prospective basis. We must also consider similar issues when determining whether or not an asset has been impaired to the extent that we must recognize a loss on such impairment.

The Company amortizes intangible assets (other than goodwill) over their respective finite lives up to their estimated residual values.

Commitments and Contingencies

Management views accounting for contingencies as a critical accounting estimate since loss contingencies arising from product warranties and defects, claims, assessments, litigation, fines and penalties and other sources require judgment as to any probable liabilities incurred. For example, accrued product warranty costs recorded by us are based primarily on historical experience of actual warranty claims and costs as well as current information with respect to warranty claims and costs. Actual results could differ from the expected results determined based on such estimates.

| | | | |

| | 19 | | Optical Cable Corporation |

Quantitative and Qualitative Disclosures About Market Risk

We do not engage in transactions in derivative financial instruments or derivative commodity instruments. As of October 31, 2011 our financial instruments were not exposed to significant market risk due to interest rate risk, foreign currency exchange risk, commodity price risk or equity price risk.

New Accounting Standards

In December 2007, the FASB issued Accounting Standards Codification 810-10,Consolidation (“ASC 810-10”). ASC 810-10 establishes accounting and reporting standards for the noncontrolling interest in a subsidiary and for the deconsolidation of a subsidiary. The statement requires consolidated net income to be reported at amounts that include the amounts attributable to both the parent and the noncontrolling interest. It also requires disclosure on the face of the consolidated statement of income, of the amounts of consolidated net income attributable to the parent and to the noncontrolling interest. In addition, this statement establishes a single method of accounting for changes in a parent’s ownership interest in a subsidiary that do not result in deconsolidation and requires that a parent recognize a gain or loss in net income when a subsidiary is deconsolidated. The adoption of ASC 810-10, effective November 1, 2009, did not have a material impact on our results of operations, financial position or liquidity. However, we have disclosed on the face of the consolidated statements of operations for the years ended October 31, 2011 and 2010, the amount of consolidated net loss attributable to the noncontrolling interest associated with Centric Solutions, LLC. Similar disclosure has also been reflected on the face of our consolidated balance sheets as of October 31, 2011 and 2010, our consolidated statements of shareholders’ equity for the years ended October 31, 2011 and 2010 and in certain notes to the consolidated financial statements. This statement now requires that the noncontrolling interest continue to be attributed its share of losses even if that attribution results in a deficit noncontrolling interest balance. In contrast, prior to the adoption of ASC 810-10, the minority interest’s share of losses attributable to Centric Solutions, LLC was required to be charged against our majority interest thereby resulting in a zero minority interest balance prior to November 1, 2009. As a result, there are no noncontrolling interest amounts to retrospectively reclassify to equity on the consolidated balance sheets or net loss attributable to noncontrolling interest on the consolidated statements of operations for any periods presented prior to November 1, 2009 upon our adoption of ASC 810-10.

In May 2011, the FASB issued Accounting Standards Update 2011-04,Amendments to Achieve Common Fair Value Measurement and Disclosure Requirements in U.S. GAAP and IFRSs (“ASU 2011-04”). The amendments are intended to improve the comparability of fair value measurements presented and disclosed in financial statements prepared in accordance with U.S. GAAP and International Financial Reporting Standards. ASU 2011-04 is to be applied prospectively upon adoption and is effective for interim and annual periods beginning after December 15, 2011. The adoption of ASU 2011-04 is not expected to have any impact on our results of operations, financial position or liquidity or our related financial statement disclosures.

There are no other new accounting standards issued, but not yet adopted by us, which are expected to materially impact our financial position, operating results or financial statement disclosures.

Disagreements with Accountants

We did not have any disagreements with our accountants on any accounting matter or financial disclosure made during our fiscal year ended October 31, 2011.

| | | | |

| Optical Cable Corporation | | 20 | | |

Consolidated Balance Sheets

October 31, 2011 and 2010

| | | | | | | | |

| | | October 31, | |

| | | 2011 | | | 2010 | |

| Assets | | | | | | | | |

| | |

Current assets: | | | | | | | | |

Cash | | $ | 1,091,513 | | | $ | 2,522,058 | |

Trade accounts receivable, net of allowance for doubtful accounts of $145,616 in 2011 and $120,450 in 2010 | | | 10,797,820 | | | | 10,659,623 | |

Other receivables | | | 510,714 | | | | 606,435 | |

Income taxes refundable | | | 434,124 | | | | 373,090 | |

Inventories | | | 16,497,185 | | | | 14,422,787 | |

Prepaid expenses and other assets | | | 374,028 | | | | 332,475 | |

Deferred income taxes - current | | | 1,817,807 | | | | 1,750,542 | |

| | | | | | | | |

| | |

Total current assets | | | 31,523,191 | | | | 30,667,010 | |

| | |

Property and equipment, net | | | 12,544,465 | | | | 13,125,114 | |

Intangible assets, net | | | 295,843 | | | | 695,580 | |

Deferred income taxes - noncurrent | | | 426,770 | | | | 626,132 | |

Other assets, net | | | 154,945 | | | | 176,930 | |

| | | | | | | | |

| | |

Total assets | | $ | 44,945,214 | | | $ | 45,290,766 | |

| | | | | | | | |

| | |

| Liabilities and Shareholders’ Equity | | | | | | | | |

| | |

Current liabilities: | | | | | | | | |

Current installments of long-term debt | | $ | 190,593 | | | $ | 177,350 | |

Accounts payable and accrued expenses | | | 5,426,467 | | | | 5,339,941 | |

Accrued compensation and payroll taxes | | | 2,579,865 | | | | 2,181,235 | |

Income taxes payable | | | — | | | | 63,590 | |

| | | | | | | | |

| | |

Total current liabilities | | | 8,196,925 | | | | 7,762,116 | |

| | |

Note payable to bank | | | — | | | | 700,000 | |

Long-term debt, excluding current installments | | | 8,000,311 | | | | 8,191,785 | |

Other noncurrent liabilities | | | 1,025,003 | | | | 1,056,803 | |

| | | | | | | | |

| | |

Total liabilities | | | 17,222,239 | | | | 17,710,704 | |

| | | | | | | | |

| | |

Shareholders’ equity: | | | | | | | | |

Preferred stock, no par value, authorized 1,000,000 shares; none issued and outstanding | | | — | | | | — | |

Common stock, no par value, authorized 50,000,000 shares; issued and outstanding 6,287,761 shares in 2011 and 6,280,173 shares in 2010 | | | 6,771,565 | | | | 5,987,777 | |

Retained earnings | | | 21,437,609 | | | | 21,869,667 | |

| | | | | | | | |

| | |

Total shareholders’ equity attributable to Optical Cable Corporation | | | 28,209,174 | | | | 27,857,444 | |

| | |

Noncontrolling interest | | | (486,199 | ) | | | (277,382 | ) |

| | | | | | | | |

| | |

Total shareholders’ equity | | | 27,722,975 | | | | 27,580,062 | |

| | |

Commitments and contingencies | | | | | | | | |

| | | | | | | | |

| | |

Total liabilities and shareholders’ equity | | $ | 44,945,214 | | | $ | 45,290,766 | |

| | | | | | | | |

See accompanying notes to consolidated financial statements.

| | | | |

| | 21 | | Optical Cable Corporation |

Consolidated Statements of Operations

Years ended October 31, 2011, 2010 and 2009

| | | | | | | | | | | | |

| | | Years ended October 31, | |

| | | 2011 | | | 2010 | | | 2009 | |

| | | |

Net sales | | $ | 73,339,591 | | | $ | 67,506,174 | | | $ | 58,588,560 | |

Cost of goods sold | | | 47,048,370 | | | | 43,746,220 | | | | 38,747,590 | |

| | | | | | | | | | | | |

| | | |

Gross profit | | | 26,291,221 | | | | 23,759,954 | | | | 19,840,970 | |

| | | |

Selling, general and administrative expenses | | | 25,168,893 | | | | 24,267,614 | | | | 22,345,311 | |

Royalty income, net | | | (783,230 | ) | | | (1,233,607 | ) | | | (877,809 | ) |

Amortization of intangible assets | | | 430,807 | | | | 587,233 | | | | 825,399 | |

Impairment of goodwill | | | — | | | | 5,580,250 | | | | — | |

Impairment of intangible assets (other than goodwill) | | | — | | | | — | | | | 343,590 | |

| | | | | | | | | | | | |

| | | |

Income (loss) from operations | | | 1,474,751 | | | | (5,441,536 | ) | | | (2,795,521 | ) |

| | | |

Other income (expense), net: | | | | | | | | | | | | |

Interest income | | | 4,659 | | | | 79,543 | | | | 831,084 | |

Interest expense | | | (624,829 | ) | | | (621,750 | ) | | | (681,851 | ) |

Other, net | | | 1,170 | | | | 64,726 | | | | 16,130 | |

| | | | | | | | | | | | |

| | | |

Other income (expense), net | | | (619,000 | ) | | | (477,481 | ) | | | 165,363 | |

| | | | | | | | | | | | |

| | | |

Income (loss) before income taxes | | | 855,751 | | | | (5,919,017 | ) | | | (2,630,158 | ) |

| | | |

Income tax expense (benefit) | | | 398,252 | | | | 91,290 | | | | (705,659 | ) |

| | | | | | | | | | | | |

| | | |

Net income (loss) | | $ | 457,499 | | | $ | (6,010,307 | ) | | $ | (1,924,499 | ) |

| | | |

Net loss attributable to noncontrolling interest | | | (208,817 | ) | | | (277,382 | ) | | | — | |

| | | | | | | | | | | | |

| | | |

Net income (loss) attributable to Optical Cable Corporation | | $ | 666,316 | | | $ | (5,732,925 | ) | | $ | (1,924,499 | ) |

| | | | | | | | | | | | |

| | | |

Net income (loss) per share attributable to Optical Cable Corporation: Basic and diluted | | $ | 0.11 | | | $ | (0.95 | ) | | $ | (0.34 | ) |

| | | | | | | | | | | | |

| | | |