Table of Contents

Exhibit 2

DISCUSSION

AND ANALYSIS

Management’s Discussion and Analysis (MD&A) is provided to enable a reader to assess our results of operations and financial condition for the fiscal year ended October 31, 2013, compared to the preceding two years. This MD&A should be read in conjunction with our 2013 Annual Consolidated Financial Statements and related notes and is dated December 4, 2013. All amounts are in Canadian dollars, unless otherwise specified, and are based on financial statements prepared in accordance with International Financial Reporting Standards (IFRS) as issued by the International Accounting Standards Board (IASB), unless otherwise noted.

Additional information about us, including our 2013 Annual Information Form, is available free of charge on our website at rbc.com/investorrelations, on the Canadian Securities Administrators’ website at sedar.com and on the EDGAR section of the United States (U.S.) Securities and Exchange Commission’s (SEC) website at sec.gov.

|

| 11 | ||||

| 11 | ||||

| 12 | ||||

| 12 | ||||

| 12 | ||||

| 14 | ||||

| 14 | ||||

| 14 | ||||

| 18 | ||||

| 18 | ||||

| 18 | ||||

| 19 | ||||

| 21 | ||||

| 26 | ||||

| 29 | ||||

| 32 |

| 33 | ||||

| 36 | ||||

| 37 | ||||

| 37 | ||||

| 38 | ||||

| 39 | ||||

| 40 | ||||

| 40 | ||||

| 41 | ||||

| 44 | ||||

| 44 | ||||

| 44 | ||||

| 44 | ||||

| 46 | ||||

| 50 | ||||

| 58 |

| 60 | ||||

| 64 | ||||

| 73 | ||||

| 73 | ||||

| 74 | ||||

| 74 | ||||

| 74 | ||||

| 74 | ||||

| 74 | ||||

| 76 | ||||

| 84 | ||||

| 84 | ||||

| 85 | ||||

| 90 | ||||

| 91 |

See our Glossary for definitions of terms used throughout this document

See our Glossary for definitions of terms used throughout this document

Caution regarding forward-looking statements

From time to time, we make written or oral forward-looking statements within the meaning of certain securities laws, including the “safe harbour” provisions of theUnited States Private Securities Litigation Reform Act of 1995 and any applicable Canadian securities legislation. We may make forward-looking statements in this 2013 Annual Report, in other filings with Canadian regulators or the SEC, in other reports to shareholders and in other communications. Forward-looking statements in this document include, but are not limited to, statements relating to our financial performance objectives, vision and strategic goals, the economic and market review and outlook for Canadian, U.S., European and global economies, the regulatory environment in which we operate, the outlook and priorities for each of our business segments, and the risk environment including our liquidity and funding management. The forward-looking information contained in this document is presented for the purpose of assisting the holders of our securities and financial analysts in understanding our financial position and results of operations as at and for the periods ended on the dates presented and our financial performance objectives, vision and strategic goals, and may not be appropriate for other purposes. Forward-looking statements are typically identified by words such as “believe”, “expect”, “foresee”, “forecast”, “anticipate”, “intend”, “estimate”, “goal”, “plan” and “project” and similar expressions of future or conditional verbs such as “will”, “may”, “should”, “could” or “would”.

By their very nature, forward-looking statements require us to make assumptions and are subject to inherent risks and uncertainties, which give rise to the possibility that our predictions, forecasts, projections, expectations or conclusions will not prove to be accurate, that our assumptions may not be correct and that our financial performance objectives, vision and strategic goals will not be achieved. We caution readers not to place undue reliance on these statements as a number of risk factors could cause our actual results to differ materially from the expectations expressed in such forward-looking statements. These factors – many of which are beyond our control and the effects of which can be difficult to predict – include: credit, market, liquidity and funding, insurance, regulatory compliance, operational, strategic, reputation and competitive risks and other risks discussed in the Risk management and Overview of other risks sections; the impact of regulatory reforms, including relating to the Basel Committee on Banking Supervision’s (BCBS) global standards for capital and liquidity reform, theDodd-Frank Wall Street Reform and Consumer Protection Actand the regulations issued and to be issued thereunder, over-the-counter derivatives reform, the payments system in Canada, the U.S.Foreign Account Tax Compliance Act (FATCA), and regulatory reforms in the United Kingdom (U.K.) and Europe; the high levels of Canadian household debt; cybersecurity; the business and economic conditions in Canada, the U.S. and certain other countries in which we operate; the effects of changes in government fiscal, monetary and other policies; our ability to attract and retain employees; the accuracy and completeness of information concerning our clients and counterparties; the development and integration of our distribution networks; model, information technology and social media risk; and the impact of environmental issues.

We caution that the foregoing list of risk factors is not exhaustive and other factors could also adversely affect our results. When relying on our forward-looking statements to make decisions with respect to us, investors and others should carefully consider the foregoing factors and other uncertainties and potential events. Material economic assumptions underlying the forward looking statements contained in this 2013 Annual Report are set out in the Overview and outlook section and for each business segment under the heading Outlook and priorities. Except as required by law, we do not undertake to update any forward-looking statement, whether written or oral, that may be made from time to time by us or on our behalf.

Additional information about these and other factors can be found in the Risk management and Overview of other risks sections.

Information contained in or otherwise accessible through the websites mentioned does not form part of this report. All references in this report to websites are inactive textual references and are for your information only.

10 Royal Bank of Canada: Annual Report 2013 Management’s Discussion and Analysis

Table of Contents

|

| (1) | Average amounts are calculated using methods intended to approximate the average of the daily balances for the period. This includes ROE and Average common equity. For further details, refer to the Key performance and non-GAAP measures section. |

| (2) | These measures may not have a standardized meaning under generally accepted accounting principles (GAAP) and may not be comparable to similar measures disclosed by other financial institutions. For further details, refer to the Key performance and non-GAAP measures section. |

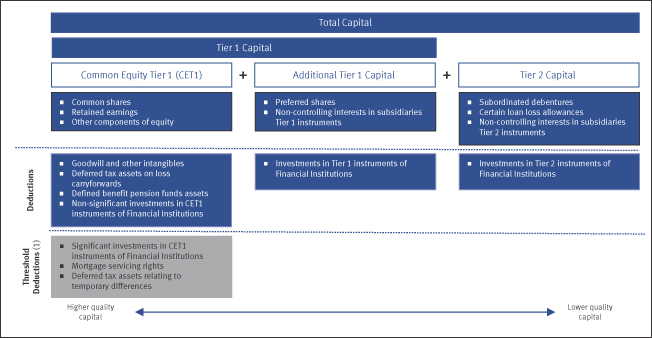

| (3) | Effective the first quarter of 2013, we calculate capital ratios and Assets-to-capital multiple using the Basel III framework. The capital ratios are calculated on the “all-in” basis. The prior periods’ capital ratios and Assets-to-capital multiple were calculated using the Basel II framework. Basel III and Basel II are not directly comparable. Capital ratios and multiples for 2011 comparative amounts in the MD&A were determined under Canadian GAAP. The CET1 ratio is a new regulatory measure under the Basel III framework. The CET1 ratio is not applicable (n.a.) for prior periods as Basel III was adopted prospectively, effective the first quarter of 2013. For further details, refer to the Capital management section. |

| (4) | Effective the first quarter of 2013, Assets-to-capital multiple is calculated on a transitional basis as per the Office of the Superintendent of Financial Institutions (OSFI) Capital Adequacy Requirements (CAR) Guideline. |

| (5) | Includes AUA from Investor Services and $32.6 billion (2012 – $38.4 billion, 2011 – $36.0 billion) of securitized mortgages and credit card loans. |

| (6) | Defined as dividends per common share divided by the average of the high and low share price in the relevant period. |

| (7) | Average amounts are calculated using month-end spot rates for the period. |

| n.m. | not meaningful |

Management’s Discussion and Analysis Royal Bank of Canada: Annual Report 2013 11

Table of Contents

|

Royal Bank of Canada (RY on TSX and NYSE) is Canada’s largest bank as measured by assets and market capitalization, and is among the largest banks in the world, based on market capitalization. We are one of North America’s leading diversified financial services companies, and provide personal and commercial banking, wealth management services, insurance, investor services and capital markets products and services on a global basis. We employ approximately 79,000 full- and part-time employees who serve more than 15 million personal, business, public sector and institutional clients through offices in Canada, the U.S. and 44 other countries. For more information, please visit rbc.com.

Our business segments are described below.

Personal & Commercial Banking comprises our personal and business banking operations, as well as certain investment businesses in Canada, the Caribbean and the U.S.

Wealth Management serves affluent, high net worth and ultra-high net worth clients from our offices in key financial centres mainly in Canada, the U.S., the U.K., continental Europe, and Asia with a comprehensive suite of investment, trust, banking, credit and other wealth management solutions. We also provide asset management products and services directly to institutional and individual clients as well as through RBC distribution channels and third-party distributors.

Insurance offers insurance products and services through our proprietary distribution channels, comprised of the field sales force which includes retail insurance branches, our field sales representatives, call centres and online, as well as through independent insurance advisors and affinity relationships in Canada. Outside North America, we operate in reinsurance markets globally.

Investor & Treasury Services serves the needs of institutional investing clients by providing custodial asset servicing, advisory, financing and other services to safeguard assets, maximize liquidity and manage risk in multiple jurisdictions around the world. We also provide funding and liquidity management for the enterprise.

Capital Markets provides public and private companies, institutional investors, governments and central banks with a wide range of products and services. In North America, we offer a full suite of products and services which include corporate and investment banking, equity and debt origination and distribution, and structuring and trading. Outside North America, we offer a diversified set of capabilities in our key sectors of expertise such as energy, mining and infrastructure.

Our business segments are supported by Corporate Support, which consists of Technology & Operations and Functions. Technology & Operations provides the technological and operational foundation required to effectively deliver products and services to our clients, while Functions includes our finance, human resources, risk management, internal audit and other functional groups.

The following chart presents our business segments and respective lines of business:

ROYAL BANK OF CANADA

|

| Personal & Commercial Banking | Wealth Management | Insurance | Investor & Treasury Services | Capital Markets | ||||||||||||

¡ Canadian Banking ¡ Caribbean & | ¡ Canadian Wealth Management ¡ U.S. & International Wealth Management ¡ Global Asset Management | ¡ Canadian Insurance ¡ International Insurance | ¡ Corporate and Investment Banking ¡ Global Markets ¡ Other |

| Corporate Support | ||

| ¡ Technology & Operations | ¡ Functions | |

|

Our business strategies and actions are guided by our vision of“Always earning the right to be our clients’ first choice.” Our strategic goals are:

| • | In Canada, to be the undisputed leader in financial services; |

| • | Globally, to be a leading provider of capital markets, investor, and wealth management solutions; and |

| • | In targeted markets, to be a leading provider of select financial services complementary to our core strengths. |

For our progress in 2013 against our business strategies and strategic goals, refer to the Business segment results section.

Overview and outlook

|

Economic and market review and outlook – data as at December 4, 2013

Canada

The Canadian economy is expected to grow at an estimated rate of 1.7% during calendar 2013, which is below our estimate of 2.4% as at November 28, 2012. Growth continues to be driven by consumer spending and business investment, moderated by weak net exports. The unemployment rate decreased to 6.9% in October 2013, supported by improvement during the year in labour markets. Housing market activity continues to benefit from these positive employment trends and the continuing low interest rate environment. Although the Canadian economy is growing at a moderate pace, concerns about the export outlook and continued low inflation led the Bank of Canada (BoC) to maintain its overnight rate at 1% in October 2013.

In calendar 2014, we expect the Canadian economy to grow at a rate of 2.6%, driven by solid consumer and investment spending and an improvement in global demand for exports. Given the ongoing low inflation environment and the factors restraining the growth of global demand for Canadian exports, we do not expect the BoC to change its overnight rate from the current 1% until at least the second quarter of 2015.

12 Royal Bank of Canada: Annual Report 2013 Management’s Discussion and Analysis

Table of Contents

U.S.

We expect the U.S. economy to grow at an estimated rate of 1.7% during calendar 2013, below our estimate of 2.3% as at November 28, 2012. Moderate consumer spending and the improvement in the housing market more than offset a decline in government spending, and continue to drive moderate economic growth. The impact of the October 2013 federal government partial shutdown on the economy is not expected to be significant. Business investment continues to recover, and the unemployment rate improved to 7.3% in October 2013. In order to provide stimulus to the economy, the Federal Reserve (Fed) is maintaining interest rates at low levels, and maintained the size of its monthly asset purchases, despite market expectations of a reduction in the program in 2013.

In calendar 2014, we expect the U.S. economy to grow at a rate of 2.7%, driven by solid consumer spending and housing market activity as well as stronger business investment. The impact on consumer confidence of a failure by the government to complete debt negotiations could reduce spending activity in the near term. We expect the Fed to reduce its monthly asset purchases starting in March 2014 and cease making purchases by the end of 2014 as labour market conditions and the inflation rate approach the Fed’s targeted levels.

Europe

The Eurozone economy is expected to contract at an estimated rate of (0.4%) during calendar 2013, below our estimate of growth of 0.1% as at November 28, 2012. The economy emerged from recession in the second quarter of 2013, but continues to show the effects of fiscal austerity measures and limited access to funding. The unemployment rate stabilized at 12.1% in October, reflecting limited improvement in labour markets. The European Central Bank (ECB) is continuing to provide stimulus to the Eurozone economy and decreased interest rates by 25 bps in May 2013 to 0.50% and by a further 25 bps in November 2013 to 0.25%.

We expect the Eurozone economy to grow at a rate of 1.0% in calendar 2014 as the ECB’s policy actions continue to take effect. We expect the ECB to maintain its current low interest rates throughout 2014 in order to mitigate the impact of continuing fiscal austerity measures and encourage demand for credit.

Financial markets

Capital markets in Canada and the U.S. gradually improved during 2013, resulting from modest economic growth in both countries as well as the maintenance of stimulative monetary policy by the BoC and the Fed. Yields on long-term Canadian and U.S. government bonds rose from May to September 2013, following a period of historical lows as markets anticipated a reduction in the Fed’s monthly asset purchase program. Credit spreads on corporate bonds started to widen in the U.S. in the latter half of 2013 after remaining low for most of the year. Equity markets improved throughout the year, despite some uncertainty regarding the outcome of the U.S. government’s efforts to avoid hitting the debt ceiling. Despite continued uncertainty in global financial markets, there were slight signs of overall improvement in 2013.

The predictions and forecasts in this section are based on information and assumptions from sources we consider reliable. If this information or these assumptions are not accurate, actual economic outcomes may differ materially from the outlook presented in this section.

For details on risk factors from general business and economic conditions that may affect our business and financial results, refer to the Overview of other risks section.

Regulatory environment

We continue to monitor and prepare for regulatory developments by identifying and working to mitigate any potential negative business or economic impact resulting from the global proliferation of regulatory reform initiatives. These developments include prohibitions on proprietary trading and certain investment in hedge and other investment funds (the Volcker Rule) under the U.S.Dodd-Frank Wall Street Reform and Consumer Protection Act (“Dodd-Frank”), the Fed’s proposal for Enhanced Supervision of Foreign Banking Organizations, and other Dodd-Frank initiatives; changes to capital and liquidity rules under the Basel Committee on Banking Supervision’s global standards (Basel III); over-the-counter derivatives reform; the U.S.Foreign Account Tax Compliance Act (FATCA); enhanced risk disclosures recommended by the Enhanced Disclosure Task Force (EDTF) of the Financial Stability Board; and other reforms.

For a discussion on risk factors resulting from these and other regulatory developments which may affect our business and financial results, refer to the Risk management – Top and emerging risks section. For further details on our framework and activities to manage risks, refer to the Risk management and Capital management sections.

Defining and measuring success through Total Shareholder Returns (TSR)

Our focus is to maximize total shareholder returns through the achievement of top quartile performance over the medium term (3-5 years) which we believe reflects a longer term view of strong and consistent financial performance.

Maximizing TSR is aligned with our three strategic goals and we believe represents the most appropriate measure of shareholder value creation. TSR is a concept used to compare the performance of our common shares over a period of time, reflecting share price appreciation and dividends paid to common shareholders. The absolute size of the TSR will vary depending on market conditions, and the relative position reflects the market’s perception of our overall performance relative to our peers over a period of time.

Financial performance objectives are used to measure progress against our medium-term TSR objectives. We review and revise these financial performance objectives as economic, market and regulatory environments change. By focusing on our medium-term objectives in our decision-making, we believe we will be well positioned to provide sustainable earnings growth and solid returns to our common shareholders.

We compared favourably to all our performance objectives in 2013. The following table provides a summary of our performance against our financial performance objectives in 2013:

Financial performance objectives

| Table 2 | |||||||

2013 results | Achieved | |||||||

Diluted EPS growth of 7% + | 12.4% | ü | ||||||

ROE of 18% + | 19.4% | ü | ||||||

Strong capital ratios (CET1) (1) | 9.6% | ü | ||||||

Dividend payout ratio 40% – 50% | 45% | ü | ||||||

| (1) | For further details on the CET1 ratio, refer to the Capital management section. |

For 2014, our financial performance objectives will remain unchanged.

Management’s Discussion and Analysis Royal Bank of Canada: Annual Report 2013 13

Table of Contents

Medium-term objectives – three and five year TSR vs. peer group average

|

|

Table 3

|

| |||||

| three year TSR (1) | five year TSR (1) | |||||||

Royal Bank of Canada | 13% | 13% | ||||||

| Second quartile | Second quartile | |||||||

Peer group average (excluding RBC) (2) | 11% | 9% |

| (1) | The three and the five year average annual TSR are calculated based on our common share price appreciation plus reinvested dividends for the period October 31, 2010 to October 31, 2013 and October 31, 2008 to October 31, 2013 respectively, based on information as disclosed by Bloomberg L.P. |

| (2) | We compare our TSR to that of a global peer group approved by our Board of Directors and consisting of the following 20 financial institutions: seven large Canadian financial institutions in addition to us (Bank of Montreal, Canadian Imperial Bank of Commerce, Manulife Financial Corporation, National Bank of Canada, Power Financial Corporation, The Bank of Nova Scotia and The Toronto-Dominion Bank), five U.S. financial institutions (Bank of America Corporation, JPMorgan Chase & Co., The Bank of New York Mellon Corporation, U.S. Bancorp and Wells Fargo & Company), five European financial institutions (Banco Bilbao Vizcaya Argentaria Group (BBVA), Barclays PLC, BNP Paribas, Credit Suisse Group AG and Deutsche Bank Group) and two Australian financial institutions (National Australia Bank and Westpac Banking Corporation). |

Our three and five year average annual TSR of 13% ranked us in the second quartile for both periods within our global peer group. The three year and five year average annual TSR for our global peer group was 11% and 9% respectively.

Common share and dividend information

|

|

Table 4

|

| |||||||||||||||||

| For the year ended October 31 | 2013 | 2012 | 2011 | 2010 | 2009 | |||||||||||||||

Common share price (RY on TSX) – close, end of period | $ | 70.02 | $ | 56.94 | $ | 48.62 | $ | 54.39 | $ | 54.80 | ||||||||||

Dividends paid per share | 2.46 | 2.22 | 2.04 | 2.00 | 2.00 | |||||||||||||||

Increase (decrease) in share price | 23.0% | 17.1% | (10.6)% | (0.7)% | 17.0% | |||||||||||||||

Total shareholder return | 28.0% | 22.0% | (6.7)% | 2.9% | 22.7% | |||||||||||||||

|

Canadian auto finance and deposit business of Ally Financial Inc. (Ally Canada)

On February 1, 2013, we completed the acquisition of Ally Canada for total cash consideration of $3.7 billion. Ally Canada’s operations provide financial services, including floor plan financing, directly to auto dealers and also offer financing for consumers through dealerships. The acquisition adds scale to our existing consumer and commercial auto financing businesses. For further details, refer to Note 11 of our 2013 Annual Consolidated Financial Statements.

|

|

2013 vs. 2012

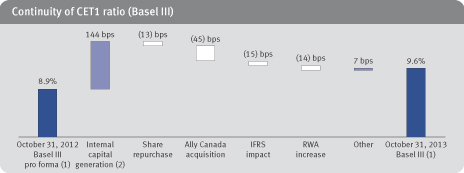

Net income of $8,429 million was up $890 million or 12% from a year ago. Diluted earnings per share (EPS) of $5.54 was up $0.61 and return on common equity (ROE) of 19.4% increased from 19.3% in 2012. At October 31, 2013, our Common Equity Tier 1 (CET1) ratio was 9.6%.

Our results reflected strong earnings growth across most of our business segments and were driven by solid volume growth across all our Canadian Banking businesses, partially offset by spread compression, strong growth in our corporate and investment banking businesses, and higher average fee-based client assets in Wealth Management. Favourable income tax adjustments in 2013 of $214 million related to prior years, lower provision for credit losses (PCL) reflecting improved credit quality, improved business performance in Investor Services, and continuing benefits from our ongoing focus on efficiency management activities also contributed to the increase. These factors were partially offset by lower trading revenue in Capital Markets and a charge of $160 million ($118 million after-tax) in Insurance as a result of proposed legislation in Canada, which would affect the policyholders’ tax treatment of certain individual life insurance policies.

In addition, our prior year results were impacted by net favourable adjustments of $60 million after-tax including a release of $128 million of tax uncertainty provisions and interest income of $72 million ($53 million after-tax) related to a refund of taxes paid due to the settlement of several tax matters with the Canada Revenue Agency (CRA), an adjustment related to a change in estimate of mortgage prepayment interest of $125 million ($92 million after-tax), and a loss of $224 million ($213 million after-tax) related to the acquisition of the remaining 50% stake of RBC Dexia Investor Services Limited (RBC Dexia).

Our ROE was up 10 basis points (bps) despite holding higher common equity as a result of Basel lll capital requirements effective the first quarter of 2013, reflecting our solid earnings growth.

For further details on our results and CET1 ratio, refer to the Business segment results and Capital management sections, respectively.

Summary of 2012 vs. 2011

In 2012, net income of $7,539 million was up $1,095 million or 17% from 2011. Diluted EPS of $4.93 was up $0.74 and ROE of 19.3% was up 60 bps.

Effective the third quarter of 2012, we no longer have discontinued operations, as the sale of our U.S. regional retail banking operations closed in the second quarter of 2012. Net loss from discontinued operations in 2012 was $51 million due to operating losses related to our U.S. regional retail banking operations.

Continuing operations

In 2012, net income from continuing operations of $7,590 million was up $620 million or 9% from 2011. The increase in net income was driven by higher fixed income trading and corporate and investment banking results as well as strong volume growth across most of our domestic banking businesses. Lower claims costs in Insurance, higher funding and liquidity trading in Investor & Treasury Services, increased average fee-based client assets in Wealth Management, and continuing benefits from our ongoing focus on efficiency management activities also contributed to the increase. In addition, net income in 2012 was favourably impacted by the release of tax uncertainty provisions and interest income and the adjustment related to a change in estimate of mortgage prepayment interest, as described above. These factors were partially offset by higher costs in support of business growth, increased PCL in Capital Markets and our Caribbean portfolio, and lower transaction

14 Royal Bank of Canada: Annual Report 2013 Management’s Discussion and Analysis

Table of Contents

volumes in Wealth Management. The loss related to the acquisition of the remaining 50% stake of RBC Dexia also negatively impacted net income in 2012.

Discontinued operations

In 2012, net loss from discontinued operations was $51 million as compared to a net loss of $526 million in 2011, primarily reflecting a loss on sale of our U.S. regional retail banking operations in 2011. Net loss from discontinued operations in 2012 included only four months of operating losses related to our U.S. regional retail banking operations compared to a full year of results in 2011.

Estimated impact of foreign currency translation on our consolidated financial results

Our foreign currency-denominated results are impacted by exchange rate fluctuations. Revenue, PCL, insurance policyholder benefits, claims and acquisition expense (PBCAE), non-interest expense and net income denominated in foreign currency are translated at the average rate of exchange for the year.

The estimated impact of foreign currency translation on our results was not significant in 2013 as compared to 2012.

Changes in the relevant average exchange rates that impact our business are shown in the following table:

Table 5

| ||||||||||||

| (Average foreign currency equivalent of C$1.00) (1) | 2013 | 2012 | 2011 | |||||||||

U.S. dollar | 0.977 | 0.997 | 1.015 | |||||||||

British pound | 0.626 | 0.630 | 0.631 | |||||||||

Euro | 0.740 | 0.771 | 0.727 | |||||||||

| (1) | Average amounts are calculated using month-end spot rates for the period. |

Total revenue

Table 6

| ||||||||||||

| (Millions of Canadian dollars) | 2013 | 2012 | 2011 | |||||||||

Interest income | $ | 21,150 | $ | 20,852 | $ | 20,813 | ||||||

Interest expense | 7,899 | 8,354 | 9,456 | |||||||||

Net interest income | $ | 13,251 | $ | 12,498 | $ | 11,357 | ||||||

Investments (1) | $ | 6,408 | $ | 5,375 | $ | 5,305 | ||||||

Insurance (2) | 3,911 | 4,897 | 4,474 | |||||||||

Trading | 867 | 1,298 | 655 | |||||||||

Banking (3) | 4,244 | 3,799 | 3,596 | |||||||||

Underwriting and other advisory | 1,569 | 1,434 | 1,485 | |||||||||

Other (4) | 617 | 471 | 766 | |||||||||

Non-interest income | $ | 17,616 | $ | 17,274 | $ | 16,281 | ||||||

Total revenue | $ | 30,867 | $ | 29,772 | $ | 27,638 | ||||||

Additional trading information | ||||||||||||

Total trading revenue | ||||||||||||

Net interest income | $ | 1,661 | $ | 1,532 | $ | 1,377 | ||||||

Non-interest income | 867 | 1,298 | 655 | |||||||||

Total trading revenue | $ | 2,528 | $ | 2,830 | $ | 2,032 | ||||||

Total trading revenue by product | ||||||||||||

Interest rate and credit | $ | 1,611 | $ | 1,923 | $ | 1,218 | ||||||

Equities | 594 | 516 | 463 | |||||||||

Foreign exchange and commodities | 323 | 391 | 351 | |||||||||

Total trading revenue | $ | 2,528 | $ | 2,830 | $ | 2,032 | ||||||

Trading revenue (teb) by product | ||||||||||||

Interest rate and credit | $ | 1,611 | $ | 1,923 | $ | 1,218 | ||||||

Equities | 972 | 945 | 920 | |||||||||

Foreign exchange and commodities | 323 | 391 | 351 | |||||||||

Total trading revenue (teb) | $ | 2,906 | $ | 3,259 | $ | 2,489 | ||||||

Trading revenue (teb) by product – Capital Markets | ||||||||||||

Interest rate and credit | $ | 1,350 | $ | 1,584 | $ | 968 | ||||||

Equities | 942 | 925 | 906 | |||||||||

Foreign exchange and commodities | 286 | 323 | 289 | |||||||||

Total Capital Markets trading revenue (teb) | $ | 2,578 | $ | 2,832 | $ | 2,163 | ||||||

| (1) | Includes securities brokerage commissions, investment management and custodial fees, and mutual fund revenue. |

| (2) | Includes premiums and investment and fee income. Investment income includes the change in fair value of investments backing policyholder liabilities and is largely offset in PBCAE. |

| (3) | Includes service charges, foreign exchange revenue other than trading, card service revenue and credit fees. |

| (4) | Includes other non-interest income, net gain (loss) on available-for-sale (AFS) securities and share of profit in associates. |

Management’s Discussion and Analysis Royal Bank of Canada: Annual Report 2013 15

Table of Contents

2013 vs. 2012

Total revenue increased $1,095 million or 4% from last year.

Net interest income increased $753 million or 6%, mainly due to solid volume growth across all businesses in Canadian Banking. The inclusion of our acquisition of Ally Canada and strong growth in our lending portfolio in Capital Markets also contributed to the increase. These factors were partially offset by spread compression. In addition, the prior year was favourably impacted by a mortgage prepayment interest adjustment (prepayment adjustment) of $125 million resulting from a change in methodology with respect to the timing of recognition of mortgage prepayment interest, and interest income of $72 million related to a refund of taxes paid of $128 million due to the settlement of several tax matters with the CRA.

Investments revenue increased $1,033 million or 19%, mainly due to higher average fee-based client assets across all businesses in Wealth Management resulting from net sales and capital appreciation, and incremental revenue related to our additional 50% ownership of Investor Services.

Insurance revenue decreased $986 million or 20%, mainly due to a change in fair value of investments backing our policyholder liabilities resulting from an increase in long-term interest rates, largely offset in PBCAE.

Trading revenue in Non-interest income decreased $431 million or 33%. Total trading revenue of $2,528 million, which comprises trading-related revenue recorded in Net interest income and Non-interest income, decreased $302 million, or 11%, mainly due to lower fixed income trading revenue, largely in Europe, as a result of challenging market conditions.

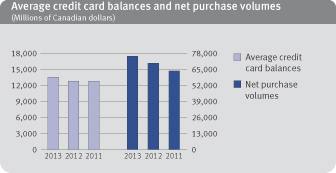

Banking revenue increased $445 million or 12%, mainly due to strong growth in our loan syndication business primarily in the U.S. Higher service fee revenue and higher credit card transaction volumes in Personal & Commercial Banking, and increased foreign exchange revenue in Investor Services primarily driven by higher transaction volumes also contributed to the increase.

Underwriting and other advisory revenue increased $135 million or 9%, mainly due to higher debt origination reflecting solid issuance activity. Higher mergers and acquisitions (M&A) activity reflecting increased mandates mainly in Canada and the U.S. also contributed to the increase.

Other revenue increased $146 million or 31%, mainly due to gains on the disposition of our London Metal Exchange (LME) shares. In addition, the prior year was unfavourably impacted by our proportionate share of a securities exchange and trading loss of $36 million ($26 million after-tax) related to the acquisition of RBC Dexia.

2012 vs. 2011

Total revenue increased $2,134 million or 8% from 2011, mainly due to strong trading revenue reflecting improved market conditions compared to the unfavourable conditions in 2011 and strong growth in lending and increased loan syndication activity in our corporate and investment banking businesses. Strong volume growth across most of our Canadian banking businesses, higher average fee-based client assets in Wealth Management, and incremental revenue related to our additional 50% ownership of Investor Services also contributed to the increase. Volume growth across most insurance products, and the change in fair value of investments backing our policyholder liabilities, which was largely offset in PBCAE, also contributed to the increase. These factors were partially offset by losses compared to gains in 2011 in Other revenue and lower transaction volumes mainly in Wealth Management.

Provision for credit losses

2013 vs. 2012

Total PCL decreased $62 million or 5% from a year ago, mainly reflecting improved credit quality in our Canadian Banking and Caribbean portfolios, partially offset by higher provisions in Capital Markets and Wealth Management.

2012 vs. 2011

Total PCL increased $168 million or 15% as compared to 2011, mainly due to higher provisions related to Capital Markets and our Caribbean portfolios. Higher average loan balances reflecting volume growth in Canadian home equity products also contributed to the increase. These factors were partially offset by lower PCL in our Canadian credit card portfolio.

For further details on PCL, refer to the Credit quality performance section.

Insurance policyholder benefits, claims and acquisition expense

2013 vs. 2012

PBCAE decreased $837 million or 23% from a year ago, mainly due to the change in fair value of investments backing our policyholder liabilities, which was largely offset in insurance revenue. Favourable actuarial adjustments reflecting management actions and assumption changes also contributed to the decrease. These factors were partially offset by the charge of $160 million as a result of proposed legislation in Canada, which would affect the policyholders’ tax treatment of certain individual life insurance policies.

2012 vs. 2011

PBCAE increased $263 million or 8% as compared to 2011, mainly due to the change in fair value of investments backing our policyholder liabilities, largely offset in insurance revenue, and volume growth across most products. These factors were partially offset by lower claims costs in Canadian insurance products and a reduction of policy acquisition cost-related liabilities reflecting changes to our proprietary distribution channel.

16 Royal Bank of Canada: Annual Report 2013 Management’s Discussion and Analysis

Table of Contents

Non-interest expense

|

Table 7

|

| ||||||||||||

| (Millions of Canadian dollars) | 2013 | 2012 | 2011 | |||||||||||

Salaries | $ | 4,665 | $ | 4,313 | $ | 4,074 | ||||||||

Variable compensation | 3,924 | 3,650 | 3,300 | |||||||||||

Benefits and retention compensation | 1,345 | 1,185 | 1,099 | |||||||||||

Share-based compensation | 256 | 139 | 188 | |||||||||||

Human resources | $ | 10,190 | $ | 9,287 | $ | 8,661 | ||||||||

Impairment of goodwill and other intangibles | 10 | 168 | – | |||||||||||

Equipment | 1,135 | 1,020 | 960 | |||||||||||

Occupancy | 1,246 | 1,170 | 1,076 | |||||||||||

Communications | 742 | 764 | 746 | |||||||||||

Professional and other external services | 1,003 | 949 | 958 | |||||||||||

Other expenses | 1,901 | 1,802 | 1,766 | |||||||||||

Non-interest expense | $ | 16,227 | $ | 15,160 | $ | 14,167 | ||||||||

2013 vs. 2012

Non-interest expense increased $1,067 million or 7%, primarily reflecting incremental costs related to our additional 50% ownership of Investor Services and higher variable compensation mainly driven by higher revenue in Wealth Management. The inclusion of our acquisition of Ally Canada, higher costs in support of business growth, and higher litigation provisions and related legal costs in Capital Markets also contributed to the increase. These factors were partially offset by continued benefits from our ongoing focus on efficiency management activities, and lower variable compensation in Capital Markets reflecting a lower compensation to revenue ratio. In addition, the prior year was unfavourably impacted by an impairment loss and other costs of $188 million related to the acquisition of RBC Dexia.

2012 vs. 2011

Non-interest expense increased $993 million or 7% as compared to 2011, primarily due to higher variable compensation, largely driven by improved results in Capital Markets and higher revenue in Wealth Management. Higher costs in support of business and volume growth and the impact of a full quarter of non-interest expense related to our additional 50% ownership of Investor Services also contributed to the increase. In addition, our non-interest expense was negatively impacted by the loss relating to the acquisition of RBC Dexia noted above. The increase in non-interest expense was partially offset by continuing benefits from our efficiency management activities.

Income and other taxes

|

Table 8

|

| ||||||||||

| (Millions of Canadian dollars, except percentage amounts) | 2013 | 2012 | 2011 | |||||||||

Income taxes | $ | 2,188 | $ | 2,100 | $ | 2,010 | ||||||

Other taxes | ||||||||||||

Goods and services sales taxes | $ | 370 | 343 | 338 | ||||||||

Payroll taxes | 384 | 371 | 349 | |||||||||

Capital taxes | 85 | 80 | 75 | |||||||||

Property taxes | 119 | 124 | 107 | |||||||||

Insurance premium taxes | 50 | 50 | 49 | |||||||||

Business taxes | 25 | 21 | 18 | |||||||||

| $ | 1,033 | $ | 989 | $ | 936 | |||||||

Total income and other taxes | $ | 3,221 | $ | 3,089 | $ | 2,946 | ||||||

Net income before income taxes | $ | 10,617 | $ | 9,690 | $ | 8,980 | ||||||

Effective income tax rate | 20.6% | 21.7% | 22.4% | |||||||||

Effective total tax rate(1) | 27.6% | 28.9% | 29.7% | |||||||||

| (1) | Total income and other taxes as a percentage of net income before income taxes and other taxes. |

2013 vs. 2012

Income tax expense increased $88 million or 4% from the prior year, mainly due to higher earnings before income tax. The effective income tax rate of 20.6% decreased 110 bps from 21.7% in the prior year, mainly due to favourable income tax adjustments in 2013 related to prior years. Our prior year results were favourably impacted by the release of $128 million of tax uncertainty provisions and interest income of $72 million ($53 million after-tax) related to a refund of taxes paid due to the settlement of several tax matters with the CRA in 2012.

Other taxes increased $44 million or 4%, mainly due to higher sales taxes and payroll taxes. In addition to the income and other taxes reported in our Consolidated Statements of Income, we recorded income tax recoveries of $352 million, as compared to income taxes of $72 million in 2012, in shareholders’ equity, primarily reflecting foreign currency translation losses from hedging activities.

2012 vs. 2011

Income tax expense increased $90 million or 4% from 2011, mainly due to higher earnings before income taxes. The effective income tax rate of 21.7% decreased 70 bps from 22.4% in 2011, mainly due to a reduction in statutory Canadian corporate income tax rates and the release of the tax uncertainty provisions noted above. These factors were partially offset by a loss related to our acquisition of the remaining 50% stake of RBC Dexia, which was not deductible for tax purposes.

Other taxes increased $53 million or 6% from 2011, mainly due to higher payroll and property taxes.

Management’s Discussion and Analysis Royal Bank of Canada: Annual Report 2013 17

Table of Contents

|

|

|

Table 9

|

| |||||||||||||||||||||||||||||||||||

| 2013 | 2012 | 2011 | ||||||||||||||||||||||||||||||||||||

| (Millions of Canadian dollars, except percentage amounts) | Personal & Commercial Banking | Wealth Management | Insurance | Investor & Treasury Services | Capital Markets (1) | Corporate Support (1) | Total | Total | Total | |||||||||||||||||||||||||||||

Net interest income | $ | 9,435 | $ | 396 | $ | – | $ | 671 | $ | 2,872 | $ | (123 | ) | $ | 13,251 | $ | 12,498 | $ | 11,357 | |||||||||||||||||||

Non-interest income | 3,788 | 5,091 | 3,928 | 1,133 | 3,708 | (32 | ) | 17,616 | 17,274 | 16,281 | ||||||||||||||||||||||||||||

Total revenue | $ | 13,223 | $ | 5,487 | $ | 3,928 | $ | 1,804 | $ | 6,580 | $ | (155 | ) | $ | 30,867 | $ | 29,772 | $ | 27,638 | |||||||||||||||||||

PCL | 997 | 51 | – | – | 188 | 3 | 1,239 | 1,301 | 1,133 | |||||||||||||||||||||||||||||

PBCAE | – | – | 2,784 | – | – | – | 2,784 | 3,621 | 3,358 | |||||||||||||||||||||||||||||

Non-interest expense | 6,240 | 4,201 | 549 | 1,343 | 3,844 | 50 | 16,227 | 15,160 | 14,167 | |||||||||||||||||||||||||||||

Net income before income taxes | $ | 5,986 | $ | 1,235 | $ | 595 | $ | 461 | $ | 2,548 | $ | (208 | ) | $ | 10,617 | $ | 9,690 | $ | 8,980 | |||||||||||||||||||

Income tax | 1,548 | 336 | (2 | ) | 118 | 838 | (650 | ) | 2,188 | 2,100 | 2,010 | |||||||||||||||||||||||||||

Net income from continuing operations | $ | 4,438 | $ | 899 | $ | 597 | $ | 343 | $ | 1,710 | $ | 442 | $ | 8,429 | $ | 7,590 | $ | 6,970 | ||||||||||||||||||||

Loss from discontinued operations | – | – | – | – | – | – | – | (51 | ) | (526 | ) | |||||||||||||||||||||||||||

Net income | $ | 4,438 | $ | 899 | $ | 597 | $ | 343 | $ | 1,710 | $ | 442 | $ | 8,429 | $ | 7,539 | $ | 6,444 | ||||||||||||||||||||

ROE from continuing operations | 31.0% | 16.1% | 41.6% | 16.7% | 14.2% | n.m. | 19.4% | 19.5% | 20.3% | |||||||||||||||||||||||||||||

ROE | 19.4% | 19.3% | 18.7% | |||||||||||||||||||||||||||||||||||

Average assets | $ | 356,000 | $ | 21,600 | $ | 11,900 | $ | 83,100 | $ | 368,300 | $ | 12,300 | $ | 853,200 | $ | 810,600 | $ | 778,900 | ||||||||||||||||||||

| (1) | Net interest income, total revenue and net income before income taxes are presented in Capital Markets on a taxable equivalent basis (tab). The taxable equivalent basis adjustment is eliminated in the Corporate Support segment. For a further discussion, refer to the How we measure and report our business segments section. |

How we measure and report our business segments

|

Our management reporting framework is intended to measure the performance of each business segment as if it were a stand-alone business and reflect the way that the business segment is managed. This approach is intended to ensure that our business segments’ results include all applicable revenue and expenses associated with the conduct of their business and depicts how management views those results. The following highlights the key aspects of how our business segments are managed and reported:

| • | Personal & Commercial Banking reported results include securitized Canadian residential mortgage and credit card loans and related amounts for income and provisions for credit losses on impaired loans. |

| • | Wealth Management reported results also include disclosure in U.S. dollars as we review and manage the results of certain businesses largely in this currency. |

| • | Insurance reported results include the change in fair value of investments mainly backing our Canadian life policyholder liabilities recorded as revenue, which is largely offset in PBCAE. |

| • | Capital Markets results are reported on a taxable equivalent basis (teb), which grosses up net interest income from certain tax-advantaged sources (Canadian taxable corporate dividends) to their effective taxable equivalent value with a corresponding offset recorded in the provision for income taxes. We record the elimination of the teb adjustments in Corporate Support. We believe these adjustments are useful and reflect how Capital Markets manages its business, since it enhances the comparability of revenue and related ratios across taxable revenue and our principal tax-advantaged source of revenue. The use of teb adjustments and measures may not be comparable to similar GAAP measures or similarly adjusted amounts disclosed by other financial institutions. |

| • | Corporate Support results include all enterprise-level activities that are undertaken for the benefit of the organization that are not allocated to our five business segments, including residual asset/liability management results, impact from income tax adjustments, net charges associated with unattributed capital and PCL on loans not yet identified as impaired. |

Key methodologies

The following outlines the key methodologies and assumptions used in our management reporting framework. These are periodically reviewed by management to ensure they remain valid.

Expense allocation

To ensure that our business segments’ results include expenses associated with the conduct of their business, we allocate costs incurred or services provided by Technology & Operations and Functions, which were directly undertaken or provided on the business segments’ behalf. For other costs not directly attributable to our business segments, including overhead costs and other indirect expenses, we use our management reporting framework for allocating these costs to each business segment in a manner that is intended to reflect the underlying benefits.

Capital attribution

Our framework also determines the attribution of capital to our business segments in a manner that is intended to consistently measure and align economic costs with the underlying benefits and risks associated with the activities of each business segment. The amount of capital assigned to each business segment is referred to as attributed capital. Unattributed capital and associated net charges are reported in Corporate Support. For further information, refer to the Capital management section.

Funds transfer pricing

A funds transfer pricing methodology is used to allocate interest income and expense by product to each business segment. This allocation considers the interest rate risk, liquidity and funding risk and regulatory requirements of each of our business segments. We base transfer pricing on external market costs and each business segment fully absorbs the costs of running its business. Our business segments may retain certain interest rate exposures subject to management approval that would be expected in the normal course of operations.

18 Royal Bank of Canada: Annual Report 2013 Management’s Discussion and Analysis

Table of Contents

Net interest margin

We report net interest margin (NIM) for Personal & Commercial Banking and our Canadian banking businesses based on average earning assets which includes only those assets that give rise to net interest income including deposits with other banks, certain securities and loans.

PCL

PCL are recorded to recognize estimated losses on impaired loans, as well as losses that have been incurred but are not yet identified in our loans portfolio. This portfolio includes on-balance sheet exposures, such as loans and acceptances, and off-balance sheet items such as letters of credit, guarantees and unfunded commitments. PCL on impaired loans are included in the results of each business segment to fully reflect the appropriate expenses related to the conduct of each business segment. PCL on loans not yet identified as impaired are included in Corporate Support, as Group Risk Management effectively controls this through its monitoring and oversight of various lending portfolios throughout the enterprise. For details on our accounting policy on Allowance for credit losses, refer to Note 2 of our 2013 Annual Consolidated Financial Statements.

Key performance and non-GAAP measures

|

Performance measures

|

Return on common equity

We measure and evaluate the performance of our consolidated operations and each business segment using a number of financial metrics such as net income and ROE. We use ROE, at both the consolidated and business segment levels, as a measure of return on total capital invested in our business. Management views the business segment ROE measure as a useful measure for supporting investment and resource allocation decisions because it adjusts for certain items that may affect comparability between business segments and certain competitors.

Our consolidated ROE calculation is based on net income available to common shareholders divided by total average common equity for the period. Business segment ROE calculations are based on net income available to common shareholders divided by average attributed capital for the period. For each segment, average attributed capital includes the capital required to underpin various risks as described in the Capital Management section and amounts invested in goodwill and intangibles.

The attribution of capital and risk capital involves the use of assumptions, judgments and methodologies that are regularly reviewed and revised by management as necessary. Changes to such assumptions, judgments and methodologies can have a material effect on the segment ROE information that we report. Other companies that disclose information on similar attributions and related return measures may use different assumptions, judgments and methodologies.

The following table provides a summary of our ROE calculations:

Calculation of ROE

|

|

Table 10

|

| |||||||||||||||||||||||||||||||||

| 2013 | 2012 | 2011 | ||||||||||||||||||||||||||||||||||

| (Millions of Canadian dollars, except percentage amounts) | Personal & Commercial Banking | Wealth Management | Insurance | Investor & Treasury Services | Capital Markets | Corporate Support | Total | Total | Total | |||||||||||||||||||||||||||

Net income available to common shareholders from continuing operations | $ | 4,349 | $ | 866 | $ | 589 | $ | 330 | $ | 1,640 | $ | 304 | $ | 8,078 | $ | 7,235 | $ | 6,611 | ||||||||||||||||||

Loss to common shareholders from discontinued operations | – | (51 | ) | (526 | ) | |||||||||||||||||||||||||||||||

Net income available to common shareholders | $ | 4,349 | $ | 866 | $ | 589 | $ | 330 | $ | 1,640 | $ | 304 | $ | 8,078 | $ | 7,184 | $ | 6,085 | ||||||||||||||||||

Average common equity from continuing operations (1), (2) | $ | 14,050 | $ | 5,400 | $ | 1,400 | $ | 2,000 | $ | 11,500 | $ | 7,300 | $ | 41,650 | $ | 36,750 | $ | 29,800 | ||||||||||||||||||

Average common equity from discontinued operations (1) | – | 400 | 2,800 | |||||||||||||||||||||||||||||||||

Total average common | $ | 14,050 | $ | 5,400 | $ | 1,400 | $ | 2,000 | $ | 11,500 | $ | 7,300 | $ | 41,650 | $ | 37,150 | $ | 32,600 | ||||||||||||||||||

ROE (3) | 31.0% | 16.1% | 41.6% | 16.7% | 14.2% | n.m. | 19.4% | 19.3% | 18.7% | |||||||||||||||||||||||||||

| (1) | Average common equity represent rounded figures. |

| (2) | The amounts for the segments are referred to as attributed capital or economic capital. |

| (3) | Calculated under Basel lll, including comparative periods. ROE is based on actual balances of average common equity before rounding. |

| n.m. | not meaningful |

Embedded value for Insurance operations

Embedded value is a measure of shareholder value embedded in the balance sheet of our Insurance segment, excluding any value from future new sales. We use the change in embedded value between reporting periods as a measure of the value created by the insurance operations during the period.

We define embedded value as the value of equity held in our Insurance segment and the value of in-force business (existing policies). The value of in-force business is calculated as the present value of future expected earnings on in-force business less the present value of capital required to support in-force business. We use discount rates that are consistent with those used by other insurance companies. Required capital uses the capital frameworks in the jurisdictions in which we operate.

Key drivers affecting the change in embedded value from period to period are new sales, investment performance, claims and policyholder experience, change in actuarial assumptions, changes in foreign exchange rates and changes in shareholder equity arising from transfers in capital.

Embedded value does not have a standardized meaning under GAAP and may not be directly comparable to similar measures disclosed by other companies. Given that this measure is specifically used for our Insurance segment and involves the use of discount rates to present value the future expected earnings and capital required for the in-force business, reconciliation to financial statements information is not applicable.

Management’s Discussion and Analysis Royal Bank of Canada: Annual Report 2013 19

Table of Contents

Non-GAAP measures

|

Economic profit

Economic profit is net income excluding the after-tax effect of amortization of other intangibles less a capital charge for use of attributed capital. It measures the return generated by our businesses in excess of our cost of capital, thus enabling users to identify relative contributions to shareholder value. Economic profit is a non-GAAP measure, does not have a standardized meaning under GAAP and may not be comparable to similar measures disclosed by other financial institutions.

The capital charge includes a charge for common equity and preferred shares. We prospectively revised our cost of equity in the first quarter of 2013 to 8.5% from 9.5% in 2012, largely as a result of the continuing low interest rate environment. Effective Q1 2014, our cost of equity will increase to 9.0% due to higher long-term interest rates.

The following table provides a summary of our Economic profit on a continuing basis:

Economic profit from continuing operations

|

|

|

Table 11

|

| ||||||||||||||||||||||||||||||||

| 2013 | 2012 | 2011 | ||||||||||||||||||||||||||||||||||

| (Millions of Canadian dollars) | Personal & Commercial Banking | Wealth Management | Insurance | Investor & Treasury Services | Capital Markets | Corporate Support | Total | Total | Total | |||||||||||||||||||||||||||

Net income from continuing operations | $ | 4,438 | $ | 899 | $ | 597 | $ | 343 | $ | 1,710 | $ | 442 | $ | 8,429 | $ | 7,590 | $ | 6,970 | ||||||||||||||||||

add: Non-controlling interests | (4 | ) | – | – | (1 | ) | – | (93 | ) | (98 | ) | (97 | ) | (101 | ) | |||||||||||||||||||||

After-tax effect of amortization of other intangibles | 26 | 67 | – | 21 | 1 | 2 | 117 | 112 | 123 | |||||||||||||||||||||||||||

Goodwill and intangibles writedown | – | – | – | – | – | – | – | 168 | – | |||||||||||||||||||||||||||

Adjusted net income | $ | 4,460 | $ | 966 | $ | 597 | $ | 363 | $ | 1,711 | $ | 351 | $ | 8,448 | $ | 7,773 | $ | 6,992 | ||||||||||||||||||

less: Capital charge | 1,285 | 492 | 129 | 180 | 1,053 | 653 | 3,792 | 3,744 | 3,213 | |||||||||||||||||||||||||||

Economic profit from continuing operations | $ | 3,175 | $ | 474 | $ | 468 | $ | 183 | $ | 658 | $ | (302 | ) | $ | 4,656 | $ | 4,029 | $ | 3,779 | |||||||||||||||||

Results excluding specified items

Our results include specified items as described below. We believe excluding these specified items from our results is more indicative of our ongoing operating results, which will provide readers with a better understanding of management’s perspective on our performance, and should enhance the comparability of our financial performance for the fiscal year ended October 31, 2013 with the fiscal year ended October 31, 2012. These measures are non-GAAP, do not have a standardized meaning under GAAP and may not be comparable to similar measures disclosed by other financial institutions.

A charge related to proposed legislation in Canada relating to certain individual life insurance policies in Insurance

Our Insurance results were impacted by a charge of $160 million ($118 million after-tax) recorded in the current year, as a result of proposed legislation in Canada, which would affect the policyholders’ tax treatment of certain individual life insurance policies.

The following table provides calculations of our Insurance results excluding this charge:

Insurance

|

| Table 12

|

| |||||||||

| 2013 | ||||||||||||

| (Millions of Canadian dollars, except percentage amounts) | As reported | Charge related to certain individual life insurance policies | Adjusted | |||||||||

Revenue | $ | 3,928 | $ | – | $ | 3,928 | ||||||

PBCAE | 2,784 | (160 | ) | 2,624 | ||||||||

Non-interest expense | 549 | – | 549 | |||||||||

Net income before income taxes | $ | 595 | $ | 160 | $ | 755 | ||||||

Net income | $ | 597 | $ | 118 | $ | 715 | ||||||

Selected balance and other information | ||||||||||||

Net income available to common shareholders | $ | 589 | $ | 118 | $ | 707 | ||||||

Average common equity | 1,400 | – | 1,400 | |||||||||

ROE | 41.6% | – | 49.9% | |||||||||

Acquisition of the remaining 50% stake of RBC Dexia included in Investor & Treasury Services

Our Investor & Treasury Services results were impacted in the prior year by a loss of $224 million ($213 million after-tax) related to our acquisition of the remaining 50% stake of RBC Dexia.

20 Royal Bank of Canada: Annual Report 2013 Management’s Discussion and Analysis

Table of Contents

The following table provides calculations of our Investor & Treasury Services results and measures excluding this specified item:

Investor & Treasury Services

|

|

Table 13

|

| |||||||||||

| 2012 | ||||||||||||||

| (Millions of Canadian dollars, except percentage amounts) | As reported | Loss related to the acquisition of the remaining 50% stake of RBC Dexia (1) | Adjusted | |||||||||||

Net interest income | $ | 668 | $ | – | $ | 668 | ||||||||

Non-interest income | 657 | 36 | 693 | |||||||||||

Total Revenue | $ | 1,325 | 36 | $ | 1,361 | |||||||||

Non-interest expense | 1,134 | (188 | ) | 946 | ||||||||||

Net income before income taxes | $ | 191 | $ | 224 | $ | 415 | ||||||||

Net income | $ | 85 | $ | 213 | $ | 298 | ||||||||

Selected balances and other information | ||||||||||||||

Net income available to common shareholders | $ | 85 | $ | 213 | $ | 298 | ||||||||

Average common equity | 1,700 | 1,700 | ||||||||||||

ROE (2) | 4.3% | 16.9% | ||||||||||||

| (1) | Consisted of an impairment loss of $168 million (before- and after-tax), comprised of a writedown of goodwill and other intangibles, other costs relating to the acquisition of $20 million ($19 million after-tax), and a loss of $36 million ($26 million after-tax), which was our proportionate share of the loss recorded by RBC Dexia from the securities exchange with Dexia Group and trading losses on the sale of a majority of the securities received in the exchange. |

| (2) | Based on actual balances before rounding. |

|

Personal & Commercial Banking is comprised of our personal and business banking operations, as well as our expanded auto financing and certain retail investment businesses, including our online discount brokerage channel, and operates through two business lines: Canadian Banking, and Caribbean & U.S. Banking. We provide services to 13 million individual, business and institutional clients across Canada, the Caribbean and the U.S. In Canada, we provide a broad suite of financial products and services through our extensive branch, automated teller machine (ATM), online and telephone banking networks, as well as through a large number of proprietary sales professionals. In the Caribbean, we offer a broad range of financial products and services to individuals, business clients and public institutions in various markets. In the U.S., we serve the cross-border banking needs of Canadian clients within the U.S. through online channels, as well as the banking product needs of our U.S. wealth management clients.

Our banking-related operations compete in the Canadian financial services industry, which consists of other Schedule I banks, independent trust companies, foreign banks, credit unions, caisses populaires, and auto financing companies. We maintain top rankings in market share in this competitive environment for most retail and business financial product categories, and have the largest branch network, the most ATMs and the largest mobile sales network across Canada. In the Caribbean, our competition includes banks, trust companies and investment management companies serving retail and corporate customers and public institutions. We are the second largest bank as measured by assets in the English Caribbean, with 116 branches in 19 countries and territories. In the U.S., we compete primarily with other Canadian banking institutions with operations in the U.S.

Economic and market review

We continued to see solid volume growth across most of our Canadian banking businesses, reflecting gradual improvements in the Canadian economy and the continuing low interest rate environment. Improved credit loss rates across our portfolios reflected stable and improving labour markets. Our businesses continued to be impacted by spread compression and certain regulatory measures which scaled back the pace of borrowing. In the Caribbean, unfavourable economic conditions continued to negatively impact our results through spread compression and lower loan volumes.

Highlights

| • | We completed the acquisition of Ally Canada on February 1, 2013 and fully integrated it in 2013, adding scale to our existing consumer and commercial auto financing businesses and extending our leadership position in Canadian auto financing. |

| • | We were named “Best Retail Bank in North America” byRetail Banker International for the second consecutive year and we took the top spot in the highly competitive “Innovation in Customer Service” category byRetail Banker International. |

| • | We were named “Best Commercial Bank in Canada” in World Finance’s 2013 Banking Awards with strong leadership position and overall financial strength and stability in Canada. |

| • | We launched a co-branded Target‡ RBC MasterCard‡ to provide clients instant savings at Target stores or earnings towards Target‡ GiftCard Rewards based on purchases made everywhere else. |

| • | We continued to innovate by introducing RBC Secure Cloud, a mobile payments service that allows clients to more safely and securely pay for purchases using their mobile devices. |

| • | In the Caribbean, we continued to focus on improving and sustaining performance through strategic growth, client care, market focus, and sound banking practices across the region in a difficult operating environment. |

Outlook and priorities

Financial conditions in Canada are expected to remain favourable, supported by the continuing low rate environment. We expect continued volume growth across most of our products. However, due to moderating housing activity resulting from regulatory changes and elevated consumer debt levels, growth in our home equity products and personal loans is expected to slow. We anticipate our business lending will remain strong as business investment is expected to improve further, reflecting favourable credit conditions and the continuing low interest rate environment. Spread compression related to low interest rates and the highly competitive environment is expected to continue to put pressure on our net interest margins.

Management’s Discussion and Analysis Royal Bank of Canada: Annual Report 2013 21

Table of Contents

In the Caribbean, challenging market conditions and a slow economic recovery continue to constrain our outlook. Net interest margins will likely remain challenged by strong competition and spread compression. However, efficiency is expected to improve and result in volume growth as well as a reduction in expenses as we leverage our common operating model in our Caribbean platforms.

For further details on our general economic review and outlook, refer to the Economic and market review and outlook section.

Key strategic priorities for 2014

In Canada, our priorities are to continue to:

| • | Provide a superior client experience through relevant and tailored advice in order to achieve industry leading volume growth. |

| • | Leverage our sales capabilities, strategic partnerships and innovative distribution channels to help broaden our client base and strengthen our distribution channels. |

| • | Enhance our services and products in the emerging payments market. |

| • | Streamline our business processes to improve the customer experience and maintain our industry-leading efficiency. |

In the Caribbean and the U.S., we are focused on:

| • | Continuing to integrate our businesses in the Caribbean to reduce costs and enhancing the client experience by simplifying the way we do business, and improving productivity in our banking network. |

| • | Strengthening the cross-border business in the U.S. and continuing to assess the market and our strategic business development options. |

Personal & Commercial Banking

|

|

Table 14

|

| |||||||||

| (Millions of Canadian dollars, except number of and percentage amounts and as otherwise noted) | 2013 | 2012 | 2011 | |||||||||

Net interest income | $ | 9,435 | $ | 9,061 | $ | 8,515 | ||||||

Non-interest income | 3,788 | 3,582 | 3,510 | |||||||||

Total revenue | 13,223 | 12,643 | 12,025 | |||||||||

PCL | 997 | 1,167 | 1,142 | |||||||||

Non-interest expense | 6,240 | 5,932 | 5,682 | |||||||||

Net income before income taxes | 5,986 | 5,544 | 5,201 | |||||||||

Net income | $ | 4,438 | $ | 4,088 | $ | 3,740 | ||||||

Revenue by business | ||||||||||||

Canadian Banking | $ | 12,422 | $ | 11,815 | $ | 11,199 | ||||||

Caribbean & U.S. Banking | 801 | 828 | 826 | |||||||||

Key ratios | ||||||||||||

ROE | 31.0% | 31.5% | 30.9% | |||||||||

NIM (1) | 2.78% | 2.86% | 2.86% | |||||||||

Efficiency ratio (2) | 47.2% | 46.9% | 47.3% | |||||||||

Operating leverage | (0.6)% | 0.7% | n.a. | |||||||||

Selected average balance sheet information | ||||||||||||

Total assets | $ | 356,000 | $ | 331,500 | $ | 310,700 | ||||||

Total earning assets (3) | 338,900 | 316,400 | 297,200 | |||||||||

Loans and acceptances (3) | 337,700 | 315,400 | 294,800 | |||||||||

Deposits | 262,300 | 243,900 | 221,200 | |||||||||

Attributed capital | 14,050 | 12,700 | 11,800 | |||||||||

Other information | ||||||||||||

AUA (4) | $ | 192,200 | $ | 179,200 | $ | 165,900 | ||||||

AUM | 3,400 | 3,100 | 2,700 | |||||||||

Number of employees (FTE) | 37,997 | 38,231 | 38,216 | |||||||||

Effective income tax rate | 25.9% | 26.3% | 28.1% | |||||||||

Credit information | ||||||||||||

Gross impaired loans as a % of average net loans and acceptances | 0.55% | 0.58% | 0.70% | |||||||||

PCL on impaired loans as a % of average net loans and acceptances | 0.30% | 0.37% | 0.39% | |||||||||

| (1) | NIM is calculated as Net interest income divided by Average total earning assets. |

| (2) | Efficiency ratio is calculated as Non-interest expense divided by Total revenue. |

| (3) | Average total earning assets and average loans and acceptances include average securitized residential mortgages and credit card loans for the year of $53.9 billion and $7.2 billion, respectively (2012 – $44.9 billion and $7.3 billion; 2011 – $42.0 billion and $4.0 billion). |

| (4) | AUA includes securitized residential mortgages and credit card loans as at October 31, 2013 of $25.4 billion and $7.2 billion respectively (October 31, 2012 – $31.0 billion and $7.4 billion; October 31, 2011 – $32.1 billion and $3.9 billion). |

| n.a. | not applicable |

Financial performance

2013 vs. 2012

Net income increased $350 million or 9% compared to the prior year, reflecting solid volume growth across all our domestic businesses, improved credit quality in our Canadian and Caribbean portfolios, and the inclusion of our acquisition of Ally Canada. These factors were partially offset by spread compression, and a provision related to post-employment benefits and restructuring charges in the Caribbean of $40 million ($31 million after-tax). The prior year was favourably impacted by a mortgage prepayment interest adjustment (prepayment adjustment) of $125 million ($92 million after-tax) resulting from a change in methodology with respect to the timing of recognition of mortgage prepayment interest.

Total revenue increased $580 million or 5% from the previous year, mainly due to solid volume growth across all businesses in Canada, and the inclusion of our acquisition of Ally Canada, partially offset by spread compression. The prior year was favourably impacted by the prepayment adjustment as noted above.

Net interest margin decreased 8 bps as the prior year was favourably impacted by 4 bps due to the prepayment adjustment noted above. The continuing low interest rate environment and competitive pricing pressures also contributed to the decrease.

PCL decreased $170 million, and the PCL ratio decreased 7 bps, mainly due to lower PCL in both our Canadian and Caribbean portfolios, reflecting improved credit quality. For further details, refer to the Credit quality performance section.

Non-interest expense increased $308 million or 5%, mainly due to the inclusion of our acquisition of Ally Canada, higher costs in support of business growth, including higher staff costs, and higher pension expense. The provision related to post-employment benefits and restructuring charges in the Caribbean also contributed to the increase. These factors were partially offset by continuing benefits from our ongoing focus on efficiency management activities.

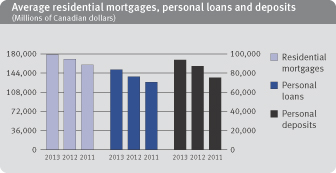

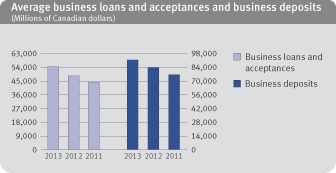

Average loans and acceptances increased $22 billion or 7%, mainly due to growth in Canadian home equity products, personal loans, and business loans. Average deposits increased $18 billion or 8%, reflecting solid growth in both business and personal deposits.

22 Royal Bank of Canada: Annual Report 2013 Management’s Discussion and Analysis

Table of Contents

2012 vs. 2011

Net income was up $348 million or 9% from 2011, reflecting strong volume growth across most of our domestic businesses, a lower effective tax rate in Canada and the favourable prepayment adjustment as noted above. These factors were partially offset by continued spread compression in Canada as well as higher PCL in the Caribbean.

Total revenue was up $618 million or 5% from 2011, reflecting strong volume growth in Canada in personal deposits, residential mortgages, business deposits and loans and personal loans. The favourable impact of the prepayment adjustment as well as higher credit card transaction volumes also contributed to the increase.

Net interest margin remained flat as the favourable impact of the prepayment adjustment was largely offset by spread compression reflecting the continuing low interest rate environment.

PCL was up $25 million or 2% from 2011, mainly due to higher provisions in our Caribbean portfolio and higher PCL in our Canadian secured retail and business lending portfolios. These factors were partially offset by lower write-offs related to our Canadian credit card portfolio.

Non-interest expense was up $250 million or 4% from 2011, mainly due to higher costs in support of business growth in Canada. Higher staff costs in the Caribbean and set-up costs in our U.S. cross border banking business also contributed to the increase. These factors were partially offset by continuing benefits from our ongoing focus on efficiency management activities. In addition, our results in 2011 included net stamp tax and accounting adjustments in Caribbean banking, which favourably impacted our results in that year.

Average loans and acceptances increased $21 billion or 7% from 2011, mainly due to continued growth in Canadian home equity and business and personal lending products. Average deposits were up $23 billion or 10% from 2011, primarily in Canada, reflecting solid growth in personal and business deposits.

In Canada, we operate through three business lines: Personal Financial Services, Business Financial Services and Cards and Payments Solutions. The following provides a discussion of our consolidated Canadian Banking results.

Canadian Banking financial highlights

|

|

Table 15

|

| |||||||||||

(Millions of Canadian dollars, except number of and percentage amounts and as otherwise noted) | 2013 | 2012 | 2011 | |||||||||||

Net interest income | $ | 8,874 | $ | 8,483 | $ | 7,960 | ||||||||

Non-interest income | 3,548 | 3,332 | 3,239 | |||||||||||

Total revenue | 12,422 | 11,815 | 11,199 | |||||||||||

PCL | 910 | 1,017 | 1,033 | |||||||||||

Non-interest expense | 5,530 | 5,258 | 5,082 | |||||||||||

Net income before income taxes | 5,982 | 5,540 | 5,084 | |||||||||||

Net income | $ | 4,414 | $ | 4,085 | $ | 3,664 | ||||||||

Revenue by business | ||||||||||||||

Personal Financial Services | $ | 6,948 | $ | 6,591 | $ | 6,192 | ||||||||

Business Financial Services | 2,990 | 2,894 | 2,750 | |||||||||||

Cards and Payment Solutions | 2,484 | 2,330 | 2,257 | |||||||||||

Key ratios | ||||||||||||||

ROE | 38.1% | 39.3% | 38.0% | |||||||||||

NIM (1) | 2.72% | 2.78% | 2.77% | |||||||||||

Efficiency ratio (2) | 44.5% | 44.5% | 45.4% | |||||||||||

Operating leverage | 0.0% | 2.0% | n.a. | |||||||||||

Selected average balance sheet information | ||||||||||||||

Total assets | $ | 338,600 | $ | 315,400 | $ | 296,100 | ||||||||

Total earning assets (3) | 326,600 | 305,300 | 287,200 | |||||||||||

Loans and acceptances (3) | 330,400 | 307,900 | 287,300 | |||||||||||

Deposits | 248,100 | 230,300 | �� | 208,600 | ||||||||||

Attributed capital | 11,400 | 10,200 | 9,450 | |||||||||||

Other information | ||||||||||||||

AUA (4) | 183,600 | 171,100 | 158,000 | |||||||||||

Number of employees (FTE) | 31,956 | 31,787 | 31,607 | |||||||||||

Effective income tax rate | 26.2% | 26.3% | 27.9% | |||||||||||

Credit information | ||||||||||||||

Gross impaired loans as a % of average net loans and acceptances | 0.36% | 0.37% | 0.44% | |||||||||||

PCL on impaired loans as a % of average net loans and acceptances | 0.28% | 0.33% | 0.36% | |||||||||||

| (1) | NIM is calculated as Net interest income divided by Average total earning assets. |

| (2) | Efficiency ratio is calculated as Non-interest expense divided by Total revenue. |

| (3) | Average total earning assets and average loans and acceptances include average securitized residential mortgages and credit card loans for the year of $53.9 billion and $7.2 billion, respectively (2012 – $44.9 billion and $7.3 billion; 2011 – $42.0 billion and $4.0 billion). |

| (4) | AUA includes securitized residential mortgages and credit card loans as at October 31, 2013 of $25.4 billion and $7.2 billion respectively (October 31, 2012 – $31.0 billion and $7.4 billion; October 31, 2011 – $32.1 billion and $3.9 billion). |

| n.a. | not applicable |

Financial performance

2013 vs. 2012