This page is intentionally left blank

Five-Year Financial Record

| AS AT AND FOR THE YEARS ENDED DEC. 31 | 2020 | 2019 | 2018 | 2017 | 2016 | |||||||||||||||||||||||||||||||||

PER SHARE1 | ||||||||||||||||||||||||||||||||||||||

Dividends2 | ||||||||||||||||||||||||||||||||||||||

| Cash | $ | 0.48 | $ | 0.43 | $ | 0.40 | $ | 0.37 | $ | 0.35 | ||||||||||||||||||||||||||||

| Special | — | — | — | 0.07 | 0.30 | |||||||||||||||||||||||||||||||||

| Net (loss) income | (0.12) | 1.73 | 2.27 | 0.89 | 1.03 | |||||||||||||||||||||||||||||||||

Funds from operations3 | 3.27 | 2.71 | 2.90 | 2.49 | 2.12 | |||||||||||||||||||||||||||||||||

Market trading price – NYSE1 | 41.27 | 38.53 | 25.57 | 29.03 | 20.01 | |||||||||||||||||||||||||||||||||

1.Adjusted to reflect the three-for-two stock split effective April 1, 2020.

2.See Corporate Dividends on page 47.

3.See definition in the MD&A Glossary of Terms beginning on page 115.

| CONTENTS | ||||||||||||||

| Brookfield at a Glance | ||||||||||||||

| Letter to Shareholders | ||||||||||||||

| Management’s Discussion & Analysis | ||||||||||||||

PART 1 – Our Business and Strategy | ||||||||||||||

PART 2 – Review of Consolidated Financial Results | ||||||||||||||

PART 3 – Operating Segment Results | ||||||||||||||

PART 4 – Capitalization and Liquidity | ||||||||||||||

PART 5 – Accounting Policies and Internal Controls | ||||||||||||||

PART 6 – Business Environment and Risks | ||||||||||||||

| Glossary of Terms | ||||||||||||||

| Internal Control Over Financial Reporting | ||||||||||||||

| Consolidated Financial Statements | ||||||||||||||

| Shareholder Information | ||||||||||||||

| Board of Directors and Officers | ||||||||||||||

| Throughout our annual report we use the following icons: | ||||||||||||||

| ||||||||||||||

2020 ANNUAL REPORT 2

Brookfield at a Glance

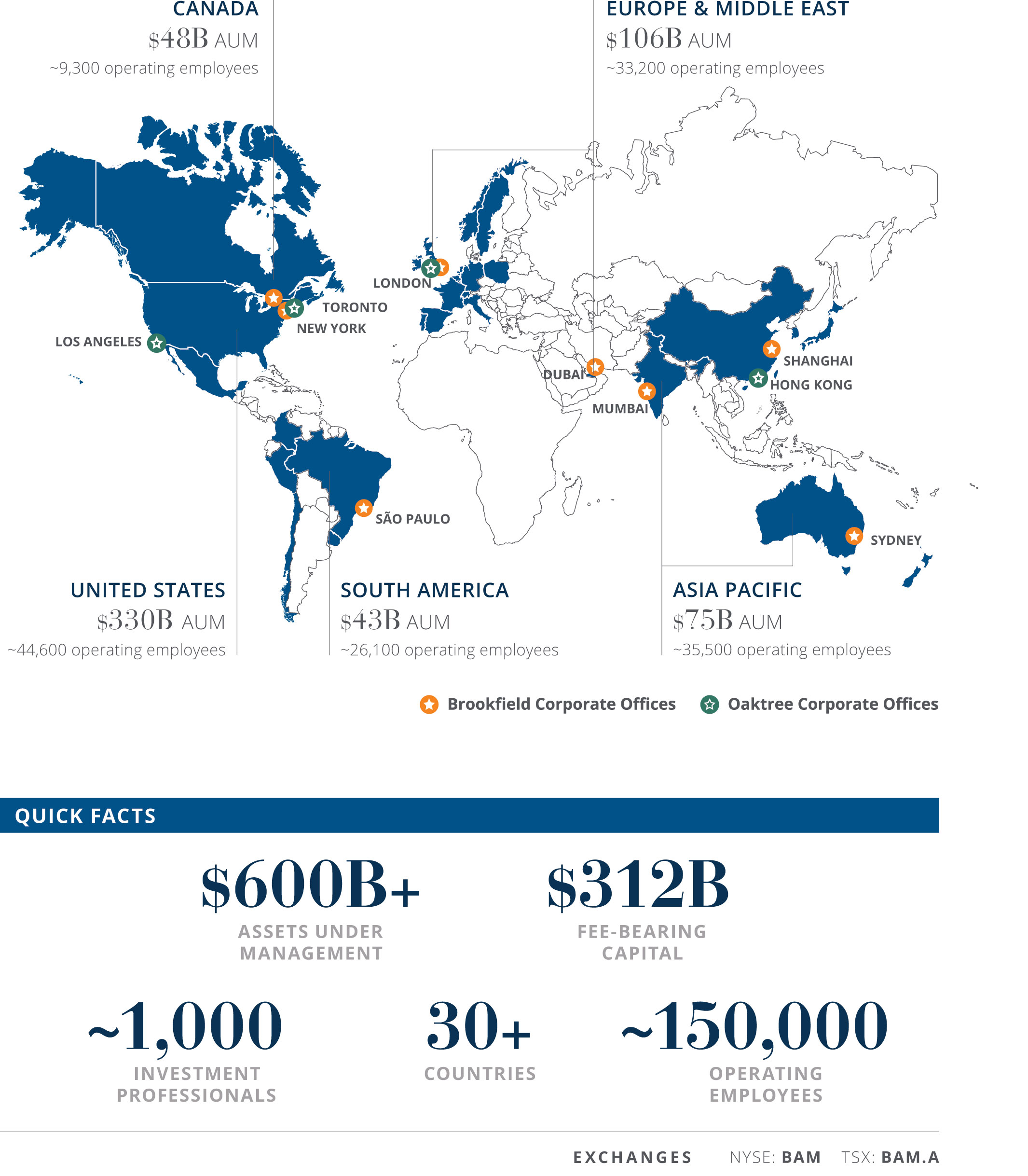

We are a leading global alternative asset manager with $600 billion of assets under management, and a focus on investing in long-life, high-quality assets and businesses that help form the backbone of the global economy. Our goal is to enable the companies and assets we invest in, as well as the communities in which we operate, to thrive over the long term.

We serve a broad range of institutional investors, sovereign wealth funds and individuals around the world. As stewards of the capital our investors entrust to us, we leverage our experience and deep operating expertise to create long-term value on their behalf, helping them meet their goals and protect their financial futures.

Our capital structure is built to allow us to finance investments by drawing from various sources—including our own balance sheet, our publicly listed affiliates’ capital and capital from our institutional investors. This access to flexible, large-scale capital allows us to pursue transactions for our investors that are significant in size, generate attractive financial returns and cash flows, and support the growth of our asset management activities. Importantly, it also means that our capital is invested alongside that of our investors, ensuring that our interests are always aligned with theirs.

At Brookfield, sound Environmental, Social and Governance (ESG) practices are integral to building resilient businesses and creating long-term value for our investors and stakeholders. These practices are routed in our philosophy of conducting business with a long-term perspective in a sustainable and ethical manner. This means operating with robust governance and other ESG principles and practices, and maintaining a disciplined focus on embedding these principles into all our activities.

Our people remain the most important element of our business, and our culture is based on integrity, collaboration and discipline. We place a strong emphasis on diversity across all our businesses, because we recognize that our success depends on fostering a wide range of perspectives, experiences and world views.

“Brookfield,” the “company,” “we,” “us” or “our” refers to Brookfield Asset Management Inc. and its consolidated subsidiaries. The “Corporation” refers to our asset management business which is comprised of our asset management and corporate business segments. Our “invested capital” includes our “listed affiliates,” Brookfield Property Partners L.P., Brookfield Property REIT Inc., Brookfield Renewable Partners L.P., Brookfield Renewable Corporation, Brookfield Infrastructure Partners L.P., Brookfield Infrastructure Corporation and Brookfield Business Partners L.P., which are separate public issuers included within our Real Estate, Renewable Power, Infrastructure and Private Equity segments, respectively. We use “private funds” to refer to our real estate funds, infrastructure funds and private equity funds. Please refer to the Glossary of Terms beginning on page 115 which defines our key performance measures that we use to measure our business.

3 BROOKFIELD ASSET MANAGEMENT

Brookfield at a Glance

GLOBAL REACH

2020 ANNUAL REPORT 4

Investment Principles

Our approach to investing is disciplined and proven—reflecting our more than 100-year history as an owner-operator. We focus on value creation and capital preservation, investing opportunistically in high-quality assets and businesses within our areas of expertise, managing them proactively and financing them conservatively—with the goal of generating stable, predictable and growing cash flows for all our investors. We recognize that generating attractive risk-adjusted returns often requires taking a contrarian approach to evaluating assets, businesses, markets or sectors.

Our business is anchored by a set of core investment principles that guide our decision-making and determine how we measure success:

| BUSINESS PHILOSOPHY | •Operate our business and conduct our relationships with integrity •Attract and retain high-caliber individuals who will grow with us over the long term •Ensure our people think and act like owners in all their decisions •Treat our investor and shareholder money like it’s our own •Embed strong ESG principles throughout our operations to help us ensure that our business model is sustainable | |||||||

| INVESTMENT APPROACH | •Acquire high-quality assets and businesses •Invest on a value basis, with the goal of maximizing return on capital •Enhance the value of investments through our operating expertise •Build sustainable cash flows to provide certainty, reduce risk and lower our cost of capital | |||||||

| MEASURES FOR SUCCESS | •Evaluate total return on capital over the long term •Encourage calculated risks, but compare returns with risk •Sacrifice short-term profit, if necessary, to achieve long-term capital appreciation •Seek profitability rather than growth, as size does not necessarily add value | |||||||

5 BROOKFIELD ASSET MANAGEMENT

Letter to Shareholders

OVERVIEW (AS OF FEBRUARY 11TH, 2021)

We ended the year with the best quarter on record. Given the environment and the extraordinary year, that says a lot for our business. Despite the turmoil and disruption, our investment strategies and the strength of our capital structure showed through. Results in our asset management business were very strong, with FFO up close to 20% over the previous year. Total FFO for the year of $5.2 billion was also a record, with realizations in the fourth quarter adding to results. On a go‑forward basis, annualized asset management revenues including carry are now running at $6.5 billion, and with our next round of fundraising for our private flagship funds just beginning, the franchise is poised for growth.

We have also launched four new strategies, and while none of these are expected to be significant contributors to our results in the short term, they should all be meaningful in the longer term. These include investing in LP secondaries, the energy transition to net-zero carbon, technology and reinsurance.

With respect to reinsurance, as recently announced, we plan to distribute to you a new share of Brookfield Reinsurance as a special dividend. This share will be paired with BAM shares to enable us to efficiently operate this business, and it should be attractive to some of you to hold.

Post year end, we launched a tender offer to take our property company private. We did this as most property securities trade poorly in the market, despite the underlying real estate being valuable. Taking it private will offer us greater flexibility in managing assets, and by paying our co-owners of BPY an attractive price, which they can elect to receive in a combination of cash, preferred shares with a coupon commensurate with current yields, or BAM shares for continued upside in the stock market, we believe it is best for all concerned.

BAM STOCK MARKET PERFORMANCE WAS GOOD, ALL THINGS CONSIDERED

As an indication of returns that can be generated for investors, below is our latest tabulation of annualized compound investment returns over the past 30 years. For reference, $1,000 invested 30 years ago in Brookfield Asset Management is today worth $86,000. Some years have been fantastic, some were like 2020; but as demonstrated in this table, compounding reasonable returns over long periods of time is an incredible miracle of finance.

Compound Investment Performance

| Years | $1,000 Invested in Brookfield | Brookfield NYSE | S&P 500 | 10-Year U.S. Treasuries | ||||||||||

| 1 | $ 1,090 | 9% | 18% | 10% | ||||||||||

| 5 | $ 2,200 | 17% | 15% | 5% | ||||||||||

| 10 | $ 3,400 | 13% | 14% | 5% | ||||||||||

| 20 | $ 32,500 | 19% | 8% | 5% | ||||||||||

| 30 | $ 86,000 | 16% | 11% | 4% | ||||||||||

The returns earned by a company are the reflection of many factors, but over the longer term they are the result of the combination of a good strategic plan and relentless execution of that plan. Only in the longer term is it possible to look back at both strategy and execution, which if done well, tends to also compound over time. Furthermore, we believe the intrinsic value of a Brookfield share today is greater than the share price; this gives us a large margin of safety in our efforts to record reasonable returns over the longer term.

2020 ANNUAL REPORT 6

THE MARKET ENVIRONMENT WAS UNFORGETTABLE

Much has been said about 2020, and it surely was one of the most unusual years in memory. GDP in every country dropped precipitously, stock markets plummeted then recovered, central banks collapsed interest rates to zero, and money with little risk became virtually free. Many businesses were shut down, most worked from home, people were afraid, plane travel declined 98%, Brexit happened, and a new U.S. president was elected.

As the year turns over to 2021, markets are strong, borrowing costs are low, money is available to well capitalized borrowers, stock price multiples for many businesses are extremely high, and pharma companies have come through in amazing time with vaccines that are now being distributed. Our expectation is that economies will regularize as the at-risk populations are vaccinated, and as the death and hospitalization numbers decline. This is starting to happen now—albeit unevenly—and as governments and people get comfortable enough to resume a more normal life, we expect we will see a strong recovery in economic numbers starting now and into 2022.

With no meaningful inflation on the horizon and high unemployment numbers, there is an expectation that interest rates will stay low and that stocks that were not bolstered by the pandemic trade will recover. Other good companies that have elevated multiples either will be proven to deserve them, or their securities may trade sideways for a time, until their results catch up with their share prices.

Our operations are highly geared to the economic recovery. As a result, we should be able to grow the value of our businesses coming out of this recession while hopefully narrowing the gap between the intrinsic value and the trading price of a Brookfield share. Like most businesses, we are pleased to see 2020 behind us, and we look forward to 2021/2022.

OUR BUSINESS WAS STRONG, DESPITE HEADWINDS

During the fourth quarter, we generated a record $2.1 billion of FFO, an increase of 75% over the same period in 2019. Full year FFO was $5.2 billion, showcasing the resiliency of our underlying businesses. This is even more remarkable, as up to 20% of our businesses were shut for months during the year and some are still recovering. This should mean that as the global recovery takes hold, our results will get even stronger. All of this led to record total cash available to shareholders for distribution and/or reinvestment (CAFDR) of $3.1 billion or $2.01 per share in 2020.

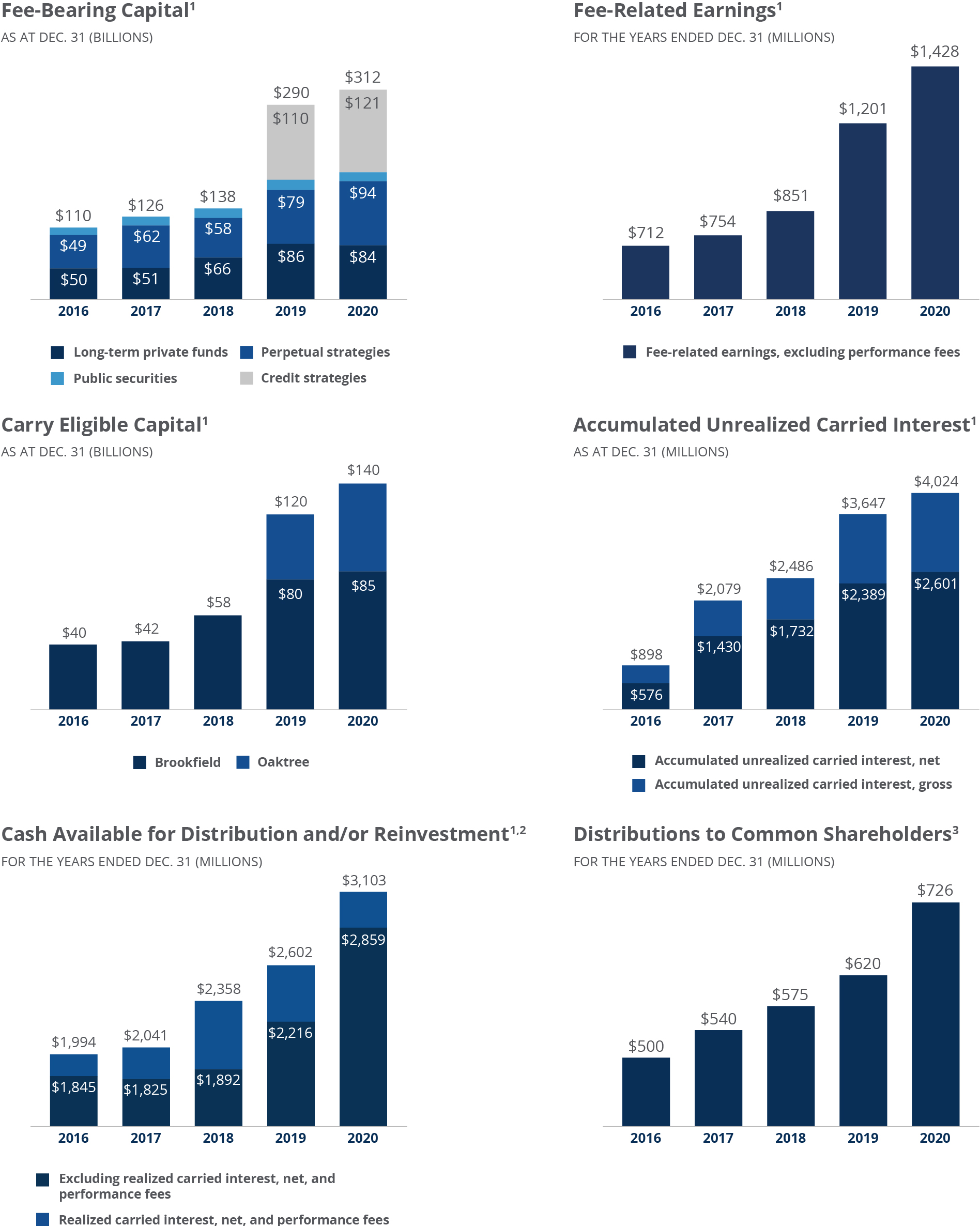

| AS AT AND FOR THE 12 MONTHS ENDED DEC. 31 (MILLIONS, EXCEPT PER SHARE AMOUNTS) | 2016 | 2017 | 2018 | 2019 | 2020 | CAGR | ||||||||||||||

| Cash available (CAFDR) – Per share | $ 1.36 | $ 1.39 | $ 1.61 | $ 1.75 | $ 2.01 | 10% | ||||||||||||||

| – Total | 1,994 | 2,041 | 2,358 | 2,602 | 3,103 | 12% | ||||||||||||||

| Fee-related earnings (before performance fees) | 712 | 754 | 851 | 1,201 | 1,428 | 19% | ||||||||||||||

| Gross annual run rate of fees plus target carry | 2,031 | 2,475 | 2,975 | 5,781 | 6,472 | 34% | ||||||||||||||

| Total assets under management | 239,825 | 283,141 | 354,736 | 544,896 | 601,983 | 26% | ||||||||||||||

Asset Management Performance was Good and is Getting Better

Our asset management franchise had a strong year in 2020. We increased total assets under management to $600 billion and fee bearing capital to $312 billion. Annualized fee-related earnings and target carried interest are now $6.5 billion on an annualized basis.

In total, we raised approximately $42 billion across our private fund strategies. This included capital for some of our flagship funds, and we also made great progress in raising capital for our perpetual core private fund offerings.

We now have approximately 20 different return strategies across our five main investment verticals that span senior debt to opportunistic equity. These included $13 billion of commitments for our latest distressed debt fund and $9 billion for perpetual core strategies. We also held a final close on our second infrastructure debt fund of $2.7 billion.

7 BROOKFIELD ASSET MANAGEMENT

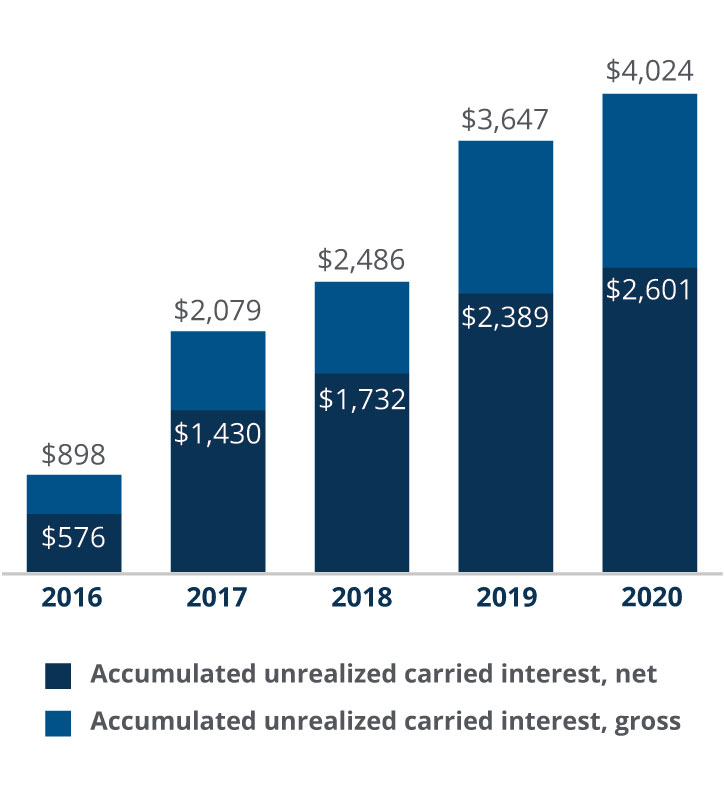

Despite the challenges of 2020, we generated approximately $1.2 billion of carried interest during the year and now have $4.7 billion of accrued unrealized carried interest on capital that has been invested. The benefits of the focus our funds have on critical service assets with contracted, leased or regulated cash flows were also highlighted in 2020, with valuations holding, and in some cases even increasing as a result of their income durability. We have re-initiated asset sales that had been delayed earlier in 2020, and demand for these assets has been strong. We recently announced a number of sales that we expect to close in the coming months; if they close as expected, 2021 should be another strong year.

At our Investor Day, we laid out our plans for the next round of flagship fundraising, with a target of $100 billion. Our flagship credit fund is off to a great start. We recently launched both our fourth flagship real estate fund and our new Global Transition Fund, which is focused on decarbonizing the global energy grid.

Operations were Resilient

Our renewable power operations continued to deliver strong results in 2020, supported by a globally diversified asset base and long-dated, take-or-pay power contracts. During the year, BEP completed the privatization of TerraForm Power, and we recently announced the acquisition of a distributed generation platform in the U.S. Combined, these scale operations in solar, wind, hydro, storage and distributed generation position us well to participate in the decarbonization of the world’s energy supply.

Our infrastructure businesses were extremely durable during the year. With 95% of the cash flows backed by regulated or contracted revenue streams stemming from critical infrastructure assets, earnings were largely unimpacted by the economic shutdown. We continued to expand our investment in data, which is in a multi-year growth trend. We acquired a portfolio of 137,000 communication towers in India, which will capitalize on the rollout of 5G and other future technologies. We are also well positioned to participate in the global infrastructure investment and privatizations that are likely to follow as a result of both the sizeable debt that governments have taken on in recent months and their need to stimulate their economies.

Within our real estate business, most of our assets performed well in 2020. Our office portfolio is largely backed by long-dated leases to high-quality tenants, and rent collection was only marginally impacted. While our retail and hospitality assets faced challenges, in those markets where governments began slowly lifting restrictions, we have seen a steady rebound in performance. Foot traffic and sales per customer have increased significantly in our U.S. mall portfolio, and forward bookings for our hospitality assets are slowly recovering. During the year, we closed on the sale of a London office property, sold our U.S. self-storage business, and also disposed of a life sciences office portfolio—each well above both its acquisition cost and IFRS value.

Our private equity operations continued to grow, and we made a number of acquisitions, including a leading non-bank financial corporation specialized in commercial vehicle lending in India, and an Asia-based technology services platform focused on customer management services. We also announced the privatization of Canada’s leading mortgage insurer, and the merger of Norbord into West Fraser. We now own approximately 20% of this combined entity, which is the pre-eminent forest products business in North America.

Our credit platform delivered strong results in 2021. We were able to deploy $22 billion during the year, capitalizing on the March/April market dislocation, and other opportunities. We expect further opportunities to arise as government stimulus rolls off and companies need to recapitalize. The final close of our distressed debt fund is likely to take place in the first half of this year; it already is the largest distressed debt fund we have raised.

PRIVATIZING OUR PROPERTY BUSINESS

In early January, we announced a proposal to acquire the balance of BPY that we do not already own. The simple story is that while the assets are exceptional and the tangible value is higher than the share price, property securities show no signs of trading near their intrinsic value. As a result, we believe our BPY partners will realize value far more quickly with the deal we are offering them.

2020 ANNUAL REPORT 8

Over the years, we have worked hard to execute our property business plans, with great success, but unfortunately the public markets have consistently struggled to appropriately value its assets. This is not unique to BPY; many property company securities have struggled to trade at NAV for years. In fact, we have taken private numerous real estate companies in our private funds for this very reason.

It has been evident to us for some time now that this portfolio and our approach to creating value are not well suited to the current public markets. To be clear, our view of the value of the portfolio has not changed. This is simply a classic example of assets not being what public market investors currently wish to invest into.

Privatizing the company will give us flexibility to realize the true value of the portfolio in the longer term by redeveloping some assets, constructing new ones, selling some assets outright, and using various assets to create or grow perpetual, private, core real estate funds. The conviction we have in the latter has been enhanced by our recent success with our series of perpetual private real estate funds that we now have in North America, Europe and Australia.

Although the immediate impact of the transaction will be an increase to the size of our balance sheet, this will quickly reverse, and we expect that over the next five years we will end up with fewer real estate assets than we have today—because of this transaction and the flexibility it will offer us. In time, we will also re-create the fee streams in the private markets, benefiting our clients who have a desire to own this highest quality real estate.

THE NEXT BEGINNING HAS ALREADY BEGUN

We are onto the next beginning for Brookfield. With all our funds performing well during last year, our balance sheets in extremely good financial shape, and our alternative investment management franchise now one of the pre-eminent businesses around the world, we are onto the next phase of growth for Brookfield. We have widened the moat of our business globally and continue to add new products for our clients. With interest rates low, alternatives are the investment category that offers an attractive return for our clients, and we are innovating to provide them with new products.

We are also scaling up the size of our large flagship funds. Their size differentiates us and therefore enhances our returns. In addition, our clients are looking for income replacement with less volatility, and we are continuing to add perpetual core-plus products to our platform.

New areas of focus for us are investing in the transition of the economy to net-zero carbon emissions; reinsurance; technology investing, where we are moving from venture into full-scale technology private equity investing; and LP secondaries, where our clients are increasingly looking for scale managers. Each of these areas has the potential to provide a meaningful opportunity for our clients and for our business.

CLIMATE TRANSITION TO NET ZERO IS REAL AND ACCELERATING

As we have noted for many years, overall, Brookfield is already net negative on scope 1 and 2 across our entire $600 billion of assets under management on an avoided emissions basis. We believe we are similarly net-zero carbon on a scope 3 basis and are now measuring the scope 3 emissions of our portfolio companies in detail. Having transformed our own business from a very intensive generator of carbon decades ago to net-zero carbon today, we believe we are well positioned to assist others with this change.

With decades of expertise and the access to capital that we possess, we plan to raise capital from our clients to assist other companies in moving to net-zero carbon. We are committing over $2 billion of our own capital to our Global Transition Fund and will be investing that alongside institutional clients who are like-minded in their goals. We believe this represents a unique opportunity to create a new asset class while addressing one of society’s current greatest needs.

We believe the world is at the beginning of a 30-year movement to net-zero carbon. This transition will affect virtually every business in every country. China, currently one of the largest generators of electricity from coal, has

9 BROOKFIELD ASSET MANAGEMENT

recently committed to being net-zero carbon across its entire economy before 2060. The new U.S. administration has committed to clean energy by 2035, and the EU, the U.K. and Canada are all accelerating their energy transitions. There is now no disputing that the world overall is moving from fossil fuels to lower carbon energy—renewables, nuclear energy and potentially hydrogen.

Within the envelope of net-zero carbon, we will continue to own and operate certain essential infrastructure assets globally that transport fuel. We believe that natural gas will play an important role in this energy transition, particularly in Asia, and potentially serve as a bridge to hydrogen. Rest assured, when we acquire these assets, we will be laser focused on the duration of cash flows, and we will operate them with their contributions to the transition to net-zero carbon in mind and with plans to ensure they continuously do better. We believe the operating experience we have gained in transitioning from carbon-intensive to net-zero carbon ourselves will make us better owners of many of these assets.

Our Global Transition Fund is focused on the build out of new renewables globally, as well as the operations surrounding investment by businesses to accelerate the transition to net-zero carbon. There are many companies that will have the capital and skills to do this themselves. Equally, there will be many that need our operating expertise and access to capital to achieve their goals. This is the objective of our new fund, and we are excited about what it can accomplish.

A FEW THEMES ARE DRIVING OUR INVESTING IN 2021/2022

We invest in all of our businesses to maintain and grow them, but we seek to deploy the most capital in businesses or regions at opportunistic points in time when the opportunity to create greater incremental value exists. This changes constantly, but simply stated, we try to stay away from fairly valued markets and invest where capital is in short supply.

Our investing is also driven by themes that generally cross all of our funds and are longer term in nature. The themes that we believe are relevant for our business today are as follows:

•Low interest rates will continue to drive demand for alternative investments. Interest rates appear to be set to stay in a lowish band for several years. As a result, alternatives are very attractive to investors. This provides an exceptional backdrop for our overall business.

•Renewable energy is growing. The global electricity make-up is currently 25% from renewable sources, and this is set to grow to 50% or more over the next 30 years. The investment required to accomplish this is in the tens of trillions of dollars.

•Technology is affecting all business, as it always has. The difference today is the pace of change, which brings with it great opportunity, but also risk. We are embracing this.

•Alternative credit is here to stay. Capital from institutions and reinsurers will increasingly drive the credit markets. Alternative managers have the opportunity to scale up credit as a fixed income replacement for institutional investors.

•Most real estate withstood the dramatic shutdowns in 2020, and while some property will be used in new ways in the future, there will be no major paradigm shift. Great real estate in great cities will continue to be just that. This will become evident once the global economy recovers.

•Many businesses and governments require capital. While businesses have survived thus far by borrowing heavily, they now need equity. As a result, there will be attractive opportunities to invest in businesses, and to acquire infrastructure from governments.

2020 ANNUAL REPORT 10

PLEASE REMEMBER THAT YOU OWN A PIECE OF OUR BUSINESS

Lastly, we encourage you to focus on our business, not the share price. If there was ever a year to emphasize this point, it was 2020. Consider that the Price of BAM in US$ on a split adjusted basis, started the year at $38.58 and ended the year at $41.27. With a dividend of 1.25%, you earned a respectable 8% on your investment based on the share price. Except, given the extremes in the market seen in 2020, and depending on when you looked at the Price, you might have concluded that you had gained 18% if you looked in February, or a month later that you were down 44% when our shares traded at $21.57 in March. This is the behavior of Price; but not Value.

In the short run, Price is a function of supply and demand at any point in time, which is often influenced by the news of the day, short-term results, and the investor view of macro events that often have nothing to do with the company. This has always been true, and is even more so today with the emergence of ETFs, indexing, social media, the 24‑hour news cycle and all the information bombarding investors. Value, on the other hand, is the net present value of future cash flows based on assumptions for growth, discounted back to the present at an appropriate interest rate. The Price of a publicly traded security is very often not the Value of it; sometimes it is higher, and sometimes lower. From time to time they can converge—but not that often.

The Value of Brookfield based on our published plan value metrics was $57 at the start of 2020 and $66 at the end. After accounting for the dividend, your Value increased 17% over the year. This was very respectable, especially given the environment, and it included write-downs from some businesses that got hit in the short term with the shutdowns.

If we were a private company, we would simply report our Value calculation and the metrics behind it. You would likely have been thrilled with 2020. We actually were. On the other hand, the movement of Price often distracts investors from focusing on the Value of a business. We encourage you to focus on Value and try to not be distracted by Price.

CLOSING

We remain committed to being a world-class asset manager, and to investing capital for you and the rest of our investment partners in high-quality assets that earn solid cash returns on equity, while emphasizing downside protection for the capital employed. The primary objective of the company continues to be to generate increasing cash flows on a per-share basis, and as a result, higher intrinsic value per share over the longer term.

And do not hesitate to contact any of us should you have suggestions, questions, comments or ideas you wish to share.

Sincerely,

Bruce Flatt

Chief Executive Officer

February 11, 2021

Note: In addition to the disclosures set forth in the cautionary statements included elsewhere in this Report, there are other important disclosures that must be read in conjunction with, and that have been incorporated in, this letter as posted on our website at https://bam.brookfield.com/en/reports-and-filings.

11 BROOKFIELD ASSET MANAGEMENT

Value Creation

We create value for our shareholders by increasing both the value of our Asset Management franchise and of our Invested Capital, as follows:

ASSET MANAGEMENT

1.Increasing fee-bearing capital, which increases our fee-related earnings. We track the value thereby created by applying a multiple to our current fee-related earnings.

2.Achieving attractive investment returns, which enables us to earn performance income (carried interest). We measure the value thereby created by applying a multiple to our target carried interest, net of costs.1

INVESTED CAPITAL

3.Increasing the cash income generated by the investments as well as capital appreciation, through operational improvements and disciplined recycling of the underlying assets. We measure the value thereby created using a combination of market values and fair values as determined under IFRS.

| Asset Management | |||||||||||||||||

| FOR THE YEAR ENDED DEC. 31, 2020 (MILLIONS) | Actual | Current1 | |||||||||||||||

| Fee revenues | $ | 2,840 | $ | 3,283 | |||||||||||||

| Direct costs | (1,296) | (1,606) | |||||||||||||||

| 1,544 | 1,677 | ||||||||||||||||

| Oaktree earnings not attributable to BAM | (116) | (112) | |||||||||||||||

| Fee-related earnings, net | 1,428 | 1,565 | |||||||||||||||

| Carried interest, gross | 1,167 | 3,189 | |||||||||||||||

| Direct costs | (494) | (1,218) | |||||||||||||||

| 673 | 1,971 | ||||||||||||||||

| Oaktree carried interest not attributable to BAM | (117) | (251) | |||||||||||||||

Carried interest, net6 | 556 | 1,720 | |||||||||||||||

| Total | $ | 1,984 | $ | 3,285 | |||||||||||||

| Invested Capital | |||||||||||||||||

| AS AT DEC. 31, 2020 (MILLIONS) | Quoted2 | IFRS3 | Blended4 | ||||||||||||||

| BPY | $ | 8,378 | $ | 15,538 | $ | 15,538 | |||||||||||

| BEP | 15,015 | 4,573 | 15,015 | ||||||||||||||

| BIP | 6,743 | 1,920 | 6,743 | ||||||||||||||

| BBU | 3,546 | 2,175 | 3,546 | ||||||||||||||

Other listed5 | 6,113 | 5,937 | 6,113 | ||||||||||||||

| Total listed investments | $ | 39,795 | 30,143 | 46,955 | |||||||||||||

| Unlisted investments and working capital, net | 10,055 | 11,323 | |||||||||||||||

| Invested capital | 40,198 | 58,278 | |||||||||||||||

| Leverage | (13,452) | (13,452) | |||||||||||||||

| Invested capital, net | $ | 26,746 | $ | 44,826 | |||||||||||||

1. See definition in the Notice to Readers on page 15.

2. Quoted based on December 31, 2020 public pricing.

3. Total IFRS invested capital excludes $4.9 billion of common equity in our Asset Management segment.

4. For business planning purposes, we consider the value of invested capital to be the quoted value of listed investments and IFRS value of unlisted investments, subject to two adjustments. First, we reflect BPY at IFRS values as we believe that this best reflects the fair value of the underlying properties. Second, we adjust Brookfield Residential values to approximate public pricing using industry comparables.

5. Includes $4.5 billion of corporate cash and financial assets.

6. For the purposes of value creation, “current” carried interest, net represents target carried interest, net. Target carried interest, net, is defined in the Notice to Readers on page 15.

2020 ANNUAL REPORT 12

Financial Profile

We measure value creation for business planning and performance measurement purposes using a consistent set of metrics as shown in the table below. This analysis is similar to what we and our Board of Directors use when assessing performance and growth in our business, and we believe it helps readers to understand our business. These plan values are for illustrative purposes only and are not intended to forecast or predict future events or to measure intrinsic value.

| AS AT AND FOR THE YEARS ENDED DEC. 31 | Base1 | Plan Value Factor2 | 2020 | 2019 | ||||||||||||||||||||||||||||||||||

| (MILLIONS) | (BILLIONS, EXCEPT FOR PER SHARE AMOUNT) | |||||||||||||||||||||||||||||||||||||

| Asset management activities | ||||||||||||||||||||||||||||||||||||||

Current fee-related earnings3 | $ | 1,565 | 25x | $ | 39.1 | $ | 35.9 | |||||||||||||||||||||||||||||||

Target carried interest, net3 | 1,720 | 10x | 17.2 | 15.5 | ||||||||||||||||||||||||||||||||||

| Accumulated unrealized carried interest, net | 2.6 | 2.4 | ||||||||||||||||||||||||||||||||||||

| 58.9 | 53.8 | |||||||||||||||||||||||||||||||||||||

| Invested Capital, net | ||||||||||||||||||||||||||||||||||||||

| Listed investments | 47.0 | 37.8 | ||||||||||||||||||||||||||||||||||||

| Unlisted investments and net working capital | 11.3 | 9.2 | ||||||||||||||||||||||||||||||||||||

| Invested capital, gross | 58.3 | 47.0 | ||||||||||||||||||||||||||||||||||||

| Total asset management activities and invested capital | 117.2 | 100.8 | ||||||||||||||||||||||||||||||||||||

Leverage4 | (13.5) | (11.2) | ||||||||||||||||||||||||||||||||||||

Total plan value3 | $ | 103.7 | $ | 89.6 | ||||||||||||||||||||||||||||||||||

| Total plan value (per share) | $ | 65.90 | $ | 56.73 | ||||||||||||||||||||||||||||||||||

Plan Value

AS AT DEC. 31 (BILLIONS)

1. Base fee-related earnings and target carried interest, net, represent our annualized fee revenues and target carried interest, as at December 31, 2020, net of associated direct costs. We assume a fee-related earnings margin of 60% and 30% for Brookfield and Oaktree, respectively. We assume a 70% and 50% margin on gross target carried interest for Brookfield and Oaktree, respectively.

2. Reflects our estimates of appropriate multiples applied to fee-related earnings and carried interest in the alternative asset management industry based on, among other things, current industry reports. These factors are used to translate earnings metrics into value in order to measure performance and value creation for business planning purposes. These factors may differ from those used by other alternative asset management companies and other industry experts in determining value.

3. See definition of Plan Value in the Notice to Readers on page 15.

4. Includes $230 million of perpetual subordinated notes issued in November 2020 by a wholly owned subsidiary of Brookfield, included within non-controlling interest.

13 BROOKFIELD ASSET MANAGEMENT

Performance Highlights

1. See definition in MD&A Glossary of Terms beginning on page 115.

1. See definition in MD&A Glossary of Terms beginning on page 115.2. Comparative numbers have been revised to reflect new definition.

3. Excludes special dividends.

2020 ANNUAL REPORT 14

NOTICE TO READERS

Pages 1 through 14 of the 2020 Annual Report must be read in conjunction with the cautionary statements included elsewhere in the 2020 Annual Report. Except where otherwise indicated, the information provided herein is based on matters as they exist as of December 31, 2020 and not as any future date.

In addition, for pages 1 through 14 of the 2020 Annual Report, the following terms have the definitions provided below:

Current fee-related earnings are annualized fee revenues net of associated direct costs. Annualized fee revenues are the sum of (i) base management fees on current fee-bearing capital based on the associated contractual fee rates; (ii) incentive distributions based on BEP, BIP and BPY’s current annual distribution policies; (iii) performance fees from BBU assuming a 10% annualized unit price appreciation; and (iv) transaction and public securities performance fees equal to a simple average of the last two years’ revenues. We assume that direct costs represent 40% of current fee revenues from Brookfield funds and 70% on Oaktree funds.

Plan value is used to measure value creation for business planning and performance measurement. The metrics used in the measurement of plan value include current fee-related earnings, target carried interest, net, accumulated unrealized carried interest, net and invested capital, net. The multiples applied to current fee-related earnings and target carried interest, net to determine plan value reflect Brookfield’s estimates of appropriate multiples used in the alternative asset management industry based on, among other things, industry reports.

Target carried interest, net is target carried interest net of associated direct costs. Target carried interest represents the carried interest we will earn, straight-lined over the life of the fund, assuming that we achieve the target fund returns. This is calculated by multiplying carry eligible fund capital by the net target return of a fund and the fund’s carried interest percentage. Target gross returns are typically 20%+ for opportunistic funds; 13% to 15% for value add funds; 12% to 15% for credit and core funds. Fee terms vary by investment strategy (carried interest is approximately 15% to 20% subject to a preferred return and catch-up) and may change over time. Target carried interest on uncalled fund commitments is discounted for two years at 10%. We assume that direct costs represent 30% of target carried interest on Brookfield funds and 50% on Oaktree funds. There can be no assurance that targeted returns will be met.

15 BROOKFIELD ASSET MANAGEMENT

Management’s Discussion and Analysis

ORGANIZATION OF THE MANAGEMENT’S DISCUSSION AND ANALYSIS (“MD&A”)

PART 1 – OUR BUSINESS AND STRATEGY | Infrastructure | ||||||||||

| Overview | Private Equity | ||||||||||

PART 2 – REVIEW OF CONSOLIDATED | Residential Development | ||||||||||

| FINANCIAL RESULTS | Corporate Activities | ||||||||||

| Overview | PART 4 – CAPITALIZATION AND LIQUIDITY | ||||||||||

| Income Statement Analysis | Capitalization | ||||||||||

| Balance Sheet Analysis | Liquidity | ||||||||||

| Consolidation and Fair Value Accounting | Review of Consolidated Statement of Cash Flows | ||||||||||

| Foreign Currency Translation | Contractual Obligations | ||||||||||

| Corporate Dividends | Exposures to Selected Financial Information | ||||||||||

| Summary of Quarterly Results | PART 5 – ACCOUNTING POLICIES AND INTERNAL | ||||||||||

PART 3 – OPERATING SEGMENT RESULTS | CONTROLS | ||||||||||

| Basis of Presentation | Accounting Policies, Estimates and Judgments | ||||||||||

| Summary of Results by Operating Segment | Management Representations and Internal Controls | ||||||||||

| Asset Management | Related Party Transactions | ||||||||||

| Real Estate | PART 6 – BUSINESS ENVIRONMENT AND RISKS | ||||||||||

| Renewable Power | GLOSSARY OF TERMS | ||||||||||

“Brookfield,” “BAM,” the “company,” “we,” “us” or “our” refers to Brookfield Asset Management Inc. and its consolidated subsidiaries. The “Corporation” refers to our asset management business which is comprised of our asset management and corporate business segments. Our “invested capital” includes our “listed affiliates,” Brookfield Property Partners L.P., Brookfield Property REIT Inc., Brookfield Renewable Partners L.P., Brookfield Renewable Corporation, Brookfield Infrastructure Partners L.P., Brookfield Infrastructure Corporation and Brookfield Business Partners L.P., which are separate public issuers included within our Real Estate, Renewable Power, Infrastructure and Private Equity segments, respectively. Additional discussion of their businesses and results can be found in their public filings. We use “private funds” to refer to our real estate funds, infrastructure funds and private equity funds.

Please refer to the Glossary of Terms beginning on page 115 which defines our key performance measures that we use to measure our business. Other businesses include Residential Development and Corporate.

Additional information about the company, including our Annual Information Form, is available on our website at www.brookfield.com, on the Canadian Securities Administrators’ website at www.sedar.com and on the EDGAR section of the U.S. Securities and Exchange Commission’s (“SEC”) website at www.sec.gov.

We are incorporated in Ontario, Canada, and qualify as an eligible Canadian issuer under the Multijurisdictional Disclosure System and as a “foreign private issuer” as such term is defined in Rule 405 under the U.S. Securities Act of 1933, as amended, and Rule 3b-4 under the U.S. Securities Exchange Act of 1934, as amended. As a result, we comply with U.S. continuous reporting requirements by filing our Canadian disclosure documents with the SEC; our MD&A is filed under Form 40-F and we furnish our quarterly interim reports under Form 6-K.

Information contained in or otherwise accessible through the websites mentioned throughout this report does not form part of this report. All references in this report to websites are inactive textual references and are not incorporated by reference. Any other reports of the company referred to herein are not incorporated by reference unless explicitly stated otherwise.

2020 ANNUAL REPORT 16

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS AND INFORMATION

This Report contains “forward-looking information” within the meaning of Canadian provincial securities laws and “forward-looking statements” within the meaning of Section 27A of the U.S. Securities Act of 1933, as amended, Section 21E of the U.S. Securities Exchange Act of 1934, as amended, “safe harbor” provisions of the United States Private Securities Litigation Reform Act of 1995 and in any applicable Canadian securities regulations. We may provide such information and make such statements in the Report, in other filings with Canadian regulators or the U.S. Securities and Exchange Commission or in other communications. Forward-looking statements include statements that are predictive in nature, depend upon or refer to future events or conditions, include statements which reflects management’s expectations regarding the operations, business, financial condition, expected financial results, performance, prospects, opportunities, priorities, targets, goals, ongoing objectives, strategies and outlook of the Corporation and its subsidiaries, as well as the outlook for North American and international economies for the current fiscal year and subsequent periods, and include words such as “expects,” “anticipates,” “plans,” “believes,” “estimates,” “seeks,” “intends,” “targets,” “projects,” “forecasts” or negative versions thereof and other similar expressions, or future or conditional verbs such as “may,” “will,” “should,” “would” and “could.” In particular, the forward-looking statements contained in this Report include statements referring to the impact of current market or economic conditions on our businesses and the impact of COVID-19 and the global economic shutdown on the market, economic conditions, or our businesses.

Although we believe that our anticipated future results, performance or achievements expressed or implied by the forward-looking statements and information are based upon reasonable assumptions and expectations, the reader should not place undue reliance on forward-looking statements and information contained in this Report. The statements and information involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, including the ongoing and developing COVID-19 pandemic and the global economic shutdown, which may cause the actual results, performance or achievements of the Corporation to differ materially from anticipated future results, performance or achievement expressed or implied by such forward-looking statements and information.

Factors that could cause actual results to differ materially from those contemplated or implied by forward-looking statements include, but are not limited to: (i) investment returns that are lower than target; (ii) the impact or unanticipated impact of general economic, political and market factors in the countries in which we do business, including as a result of COVID-19 and the global economic shutdown; (iii) the behavior of financial markets, including fluctuations in interest and foreign exchange rates; (iv) global equity and capital markets and the availability of equity and debt financing and refinancing within these markets; (v) strategic actions including dispositions; the ability to complete and effectively integrate acquisitions into existing operations and the ability to attain expected benefits; (vi) changes in accounting policies and methods used to report financial condition (including uncertainties associated with critical accounting assumptions and estimates); (vii) the ability to appropriately manage human capital; (viii) the effect of applying future accounting changes; (ix) business competition; (x) operational and reputational risks; (xi) technological change; (xii) changes in government regulation and legislation within the countries in which we operate; (xiii) governmental investigations; (xiv) litigation; (xv) changes in tax laws; (xvi) ability to collect amounts owed; (xvii) catastrophic events, such as earthquakes, hurricanes, or pandemics/epidemics, including COVID-19; (xviii) the possible impact of international conflicts and other developments including terrorist acts and cyberterrorism; (xix) the introduction, withdrawal, success and timing of business initiatives and strategies; (xx) the failure of effective disclosure controls and procedures and internal controls over financial reporting and other risks; (xxi) health, safety and environmental risks; (xxii) the maintenance of adequate insurance coverage; (xxiii) the existence of information barriers between certain businesses within our asset management operations; (xxiv) risks specific to our business segments including our real estate, renewable power, infrastructure, private equity, credit and residential development activities; and (xxv) factors detailed from time to time in our documents filed with the securities regulators in Canada and the U.S., including in “Part 6 – Business Environment and Risks” of our Annual Report available on SEDAR at www.sedar.com and EDGAR at www.sec.gov.

We caution that the foregoing list of important factors that may affect future results is not exhaustive. Readers are urged to consider the foregoing risks, as well as other uncertainties, factors and assumptions carefully in evaluating the forward-looking information and are cautioned not to place undue reliance on such forward-looking information. Except as required by law, the Corporation undertakes no obligation to publicly update or revise any forward-looking statements or information, whether written or oral, that may be as a result of new information, future events or otherwise.

Past performance is not indicative nor a guarantee of future results. There can be no assurance that comparable results will be achieved in the future, that future investments will be similar to the historic investments discussed herein (because of economic conditions, the availability of investment opportunities or otherwise), that targeted returns, diversification or asset allocations will be met or that an investment strategy or investment objectives will be achieved.

17 BROOKFIELD ASSET MANAGEMENT

STATEMENT REGARDING USE OF NON-IFRS MEASURES

We disclose a number of financial measures in this Report that are calculated and presented using methodologies other than in accordance with International Financial Reporting Standards (“IFRS”), as issued by the International Accounting Standards Board (“IASB”). We utilize these measures in managing the business, including for performance measurement, capital allocation and valuation purposes and believe that providing these performance measures on a supplemental basis to our IFRS results is helpful to investors in assessing the overall performance of our businesses. These financial measures should not be considered as the sole measure of our performance and should not be considered in isolation from, or as a substitute for, similar financial measures calculated in accordance with IFRS. We caution readers that these non-IFRS financial measures or other financial metrics may differ from the calculations disclosed by other businesses and, as a result, may not be comparable to similar measures presented by other issuers and entities. Reconciliations of these non-IFRS financial measures to the most directly comparable financial measures calculated and presented in accordance with IFRS, where applicable, are included within this Report. Please refer to our Glossary of Terms beginning on page 115 for all non-IFRS measures.

2020 ANNUAL REPORT 18

PART 1 – OUR BUSINESS AND STRATEGY

OVERVIEW

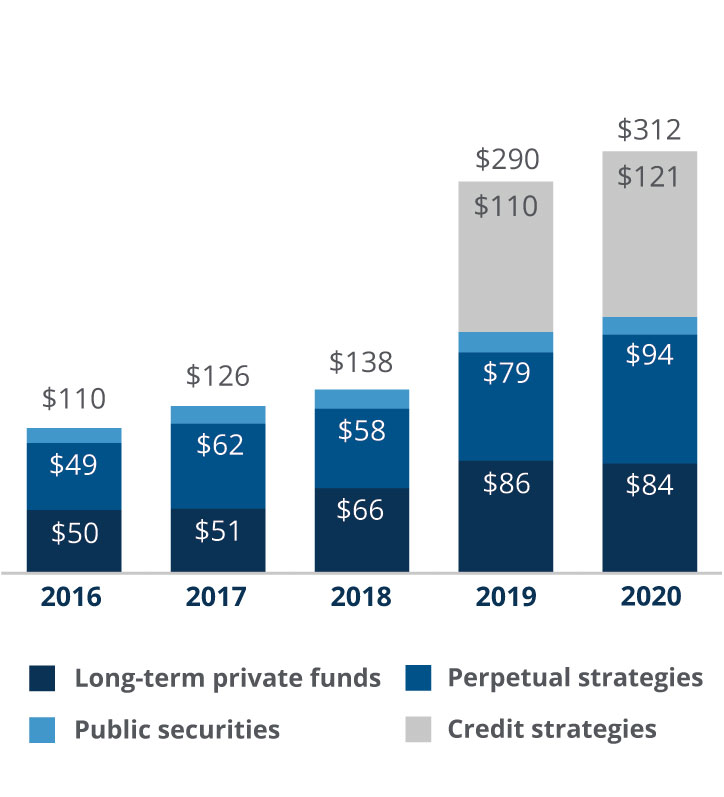

We are a leading global alternative asset manager1 with a history spanning over 100 years. We have $600 billion of assets under management1 across a broad portfolio of real estate, infrastructure, renewable power, private equity and credit. Our $312 billion in fee-bearing capital1 is invested on behalf of some of the world’s largest institutional investors, sovereign wealth funds and pension plans, along with thousands of individuals.

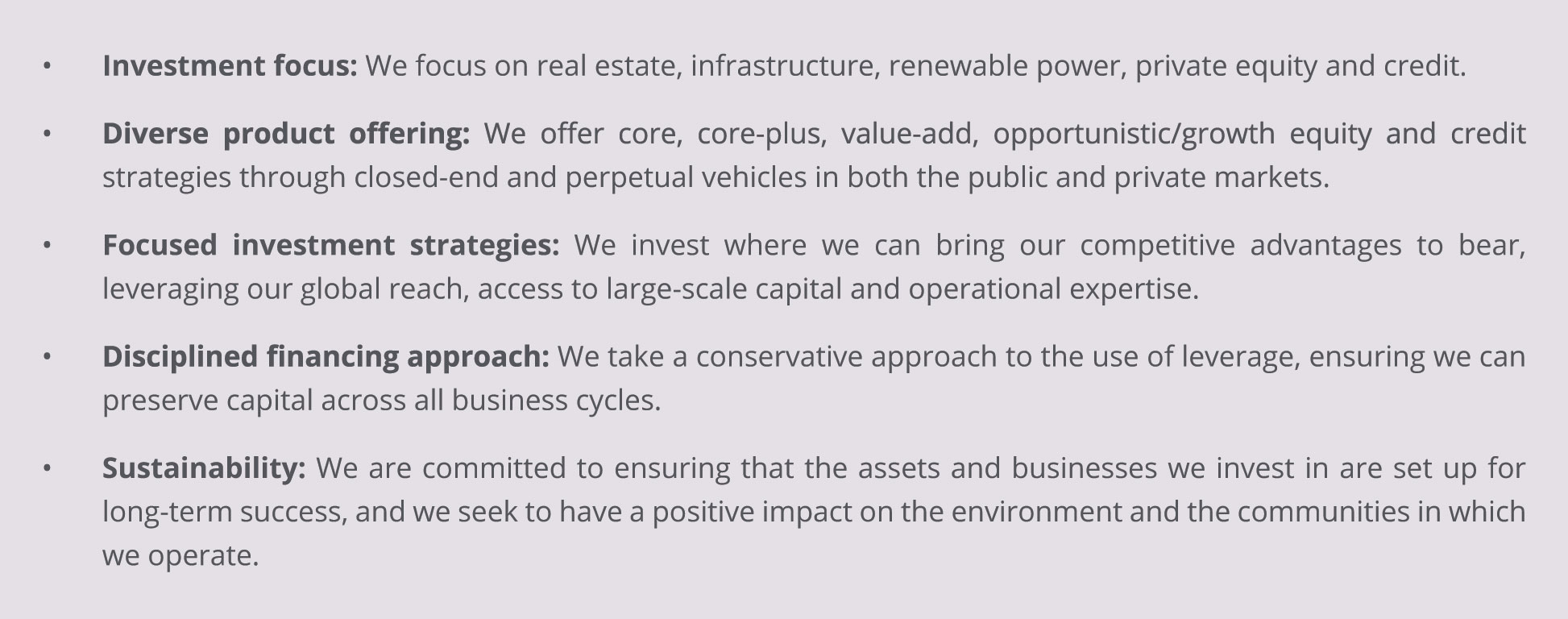

We provide a diverse product mix of private funds1 and dedicated public vehicles, which allow investors to invest in our five key asset classes and participate in the strong performance of the underlying portfolio. We invest in a disciplined manner, targeting returns of 12-15% over the long-term with strong downside protection, allowing our investors and their stakeholders to meet their goals and protect their financial futures.

ü Investment focus

We predominantly invest in real assets across real estate, infrastructure, renewable power and private equity, and hold a significant investment in Oaktree Capital Management (“Oaktree”)1, which is a leading global alternative investment management firm with an expertise in credit.

ü Diverse product offering

We offer public and private vehicles to invest across a number of product lines, including core, value-add, and opportunistic growth equity and credit strategies in both closed-end and perpetual vehicles.

ü Focused investment strategies

We invest where we can bring our competitive advantages to bear, such as our strong capabilities as an owner-operator, our large-scale capital and our global reach.

ü Disciplined financing approach

We employ leverage1 in a prudent manner to enhance returns while preserving capital throughout business cycles. Underlying investments are typically funded at investment-grade levels on a standalone and non-recourse basis, providing us with a stable capitalization. Only 6% of the total leverage reported in our consolidated financial statements has recourse to the Corporation.

ü Sustainability

We are committed to ensuring that the assets and businesses in which we invest are set up for long-term success, and we seek to have a positive impact on the environment and the communities in which we operate.

In addition, we maintain significant invested capital1 on the Corporation’s balance sheet where we invest alongside our investors. This capital generates annual cash flows that enhance the returns we earn as an asset manager, create a strong alignment of interest, and enable us to bring the following strengths to bear on all our investments:

1.Large-scale capital

We have approximately $600 billion in assets under management and $312 billion in fee-bearing capital.

2.Operating expertise

We have approximately 150,000 operating employees worldwide focused on maximizing value and cash flows from our assets and businesses.

3.Global reach

We operate in more than 30 countries on five continents around the world.

1.See definition in Glossary of Terms beginning on page 115.

19 BROOKFIELD ASSET MANAGEMENT

The value of the business is comprised of two key components: Our asset management activities that we refer to as Asset Management, and our balance sheet investments that we refer to as Invested Capital. Our financial returns are represented by the combination of the earnings of our Asset Management business, as well as capital appreciation and distributions from our Invested Capital. The primary performance measure we use is funds from operations (“FFO”)1 which we use to evaluate the performance of our segments.

Asset Management

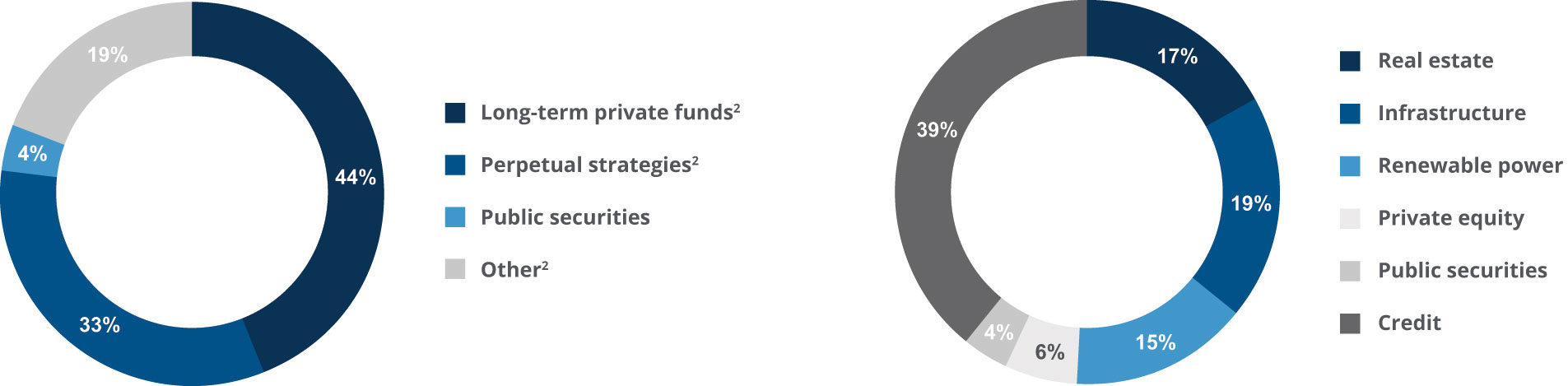

Our Asset Management activities encompass $312 billion of fee-bearing capital across a broad portfolio of real estate, infrastructure, renewable power, private equity and credit, and we have approximately $33 billion of additional committed capital that will be fee-bearing when invested. This capital is managed within long-term private funds, perpetual strategies and public securities1. Together with our investment in Oaktree, we have approximately 2,000 unique institutional investors across our private funds business.

Fee-Bearing Capital Diversification

AS AT DEC. 31, 2020

Long-term Private Funds – $84 billion fee-bearing capital

We manage and earn fees on a diverse range of real estate, renewable power, infrastructure, private equity and credit funds. These funds are long duration in nature and include closed-end value-add, credit and opportunistic strategies. On long-term private fund capital, we earn:

1.Diversified and long-term base management fees1 on capital that is typically committed for ten years with two one-year extension options.

2.Carried interest1, which enables us to receive a portion of overall fund profits provided that our investors receive a minimum prescribed preferred return. Carried interest is recognized when a fund’s cumulative returns are in excess of preferred returns and when it is highly probable that a significant reversal will not occur.

Perpetual Strategies – $94 billion fee-bearing capital

We manage perpetual capital in our publicly listed affiliates1, as well as core and core plus private funds, which can continually raise new capital. From our perpetual strategies, we earn:

1.Long-term perpetual base management fees, which as general partner of our listed affiliates, are based on total capitalization of our listed affiliates and the net asset value (“NAV”) of our perpetual private funds.

2.Stable incentive distributions1 which are linked to cash distributions from listed affiliates (BPY/BPYU, BEP/BEPC and BIP/BIPC) that exceed pre-determined thresholds. These cash distributions have a historical track record of growing annually and each of these listed affiliates target annual distribution growth rates within a range of 5-9%.

3.Performance fees1 based on unit price performance (BBU) and carried interest on our perpetual private funds.

1.See definition in Glossary of Terms beginning on page 115.

2.Credit Strategies have been allocated across long-term private funds, perpetual strategies and other.

2020 ANNUAL REPORT 20

Asset Management (continued)

Credit Strategies – $121 billion fee-bearing capital

We hold an approximate 62% interest in Oaktree, which provides a diverse range of long-term private fund and perpetual strategies to its investor base. Similar to our long-term private funds, we earn base management fees and carried interest on Oaktree’s fund capital.

Public Securities – $13 billion fee-bearing capital

We manage publicly listed funds and separately managed accounts, focused on fixed income and equity securities across real estate, infrastructure and natural resources. We earn base management fees, which are based on committed capital and fund NAV, and performance income based on investment returns.

Invested Capital

We have approximately $58 billion of invested capital on our balance sheet as a result of our history as an owner and operator of real assets. This capital provides attractive financial returns and important stability and flexibility to our asset management business.

Key attributes of our invested capital:

•Transparent – approximately 81% of our invested capital is in our listed affiliates and other smaller publicly traded investments. The remainder is primarily held in a residential homebuilding business, and a few other directly held investments.

•Diversified, long-term, stable cash flows – received from our underlying public investments. These cash flows are underpinned by investments in real assets which should provide inflation protection and less volatility compared to traditional equities, and higher yields compared to fixed income.

•Strong alignment of interest with our investors – we are the largest investor into each of our listed affiliates, and in turn, the listed affiliates are typically the largest investor in each of our private funds.

21 BROOKFIELD ASSET MANAGEMENT

COMPETITIVE ADVANTAGES

We have three distinct competitive advantages that enable us to consistently identify and acquire high-quality assets and create significant value in the assets that we own and operate.

Large-Scale Capital

We have approximately $600 billion in assets under management.

We offer our investors a large portfolio of private funds that have global mandates and diversified strategies. Our access to large-scale, flexible capital enables us to pursue transactions of a size that lessens competition. In addition, investing significant amounts of our own capital either through our listed affiliates or through our own balance sheet ensures strong alignment of interest with our investors.

Operating Expertise

We have approximately 150,000 operating employees worldwide who are instrumental in maximizing the value and cash flows from our operations.

We believe that strong operating experience is essential in maximizing efficiency and productivity – and ultimately, returns. We do this by maintaining a culture of long-term focus, alignment of interest and collaboration through the people we hire and our operating philosophy. This in-house operating expertise developed through our heritage as an owner-operator is invaluable in underwriting acquisitions and executing value-creating development and capital projects.

Global Reach

We operate in more than 30 countries on five continents around the world.

Our global reach allows us to diversify and identify a broad range of opportunities. We are able to invest where capital is scarce, and our scale enables us to move quickly and pursue multiple opportunities across different markets. Our global reach also allows us to operate our assets more effectively: we believe that a strong on-the-ground presence is critical to operating successfully in many of our markets, and many of our businesses are truly local. Furthermore, the combination of our strong local presence and global reach allows us to bring global relationships and operating practices to bear across markets to enhance returns.

2020 ANNUAL REPORT 22

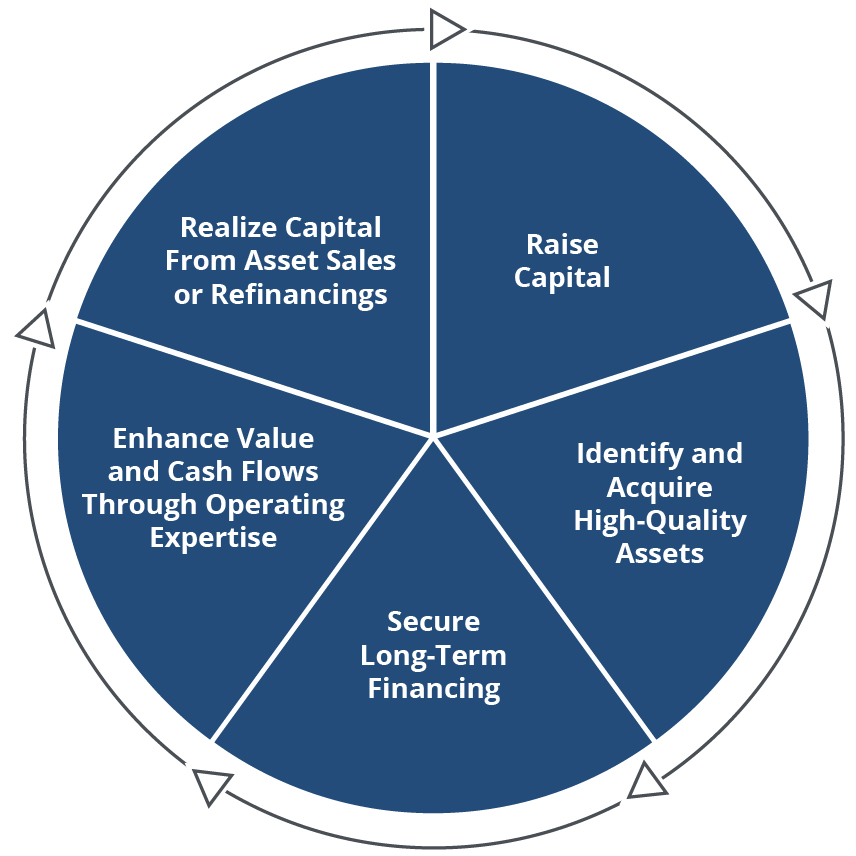

INVESTMENT CYCLE

Raise Capital As an asset manager, the starting point is establishing new funds and other investment products for investors. This in turn provides the capital to invest, from which we earn base management fees, incentive distributions and performance-based returns such as carried interest. Accordingly, we create value by increasing our amount of fee-bearing capital and by achieving strong investment performance that leads to increased cash flows and asset values. | |||||

Identify and Acquire High-Quality Assets We follow a value-based approach to investing and allocating capital. We believe that our disciplined approach, global reach and our operating expertise enable us to identify a wide range of potential opportunities, and allow us to invest at attractive valuations and generate superior risk-adjusted returns. We also leverage our considerable expertise in executing recapitalizations, operational turnarounds and large development and capital projects, providing additional opportunities to deploy capital. | |||||

Secure Long-Term Financing We finance our operations predominantly on a long-term investment-grade basis, and most of our capital consists of equity and standalone asset-by-asset financing with minimal recourse to other parts of the organization. We utilize relatively modest levels of corporate debt to provide operational flexibility and optimize returns. This provides us with considerable stability, improves our ability to withstand financial downturns and enables our management teams to focus on operations and other growth initiatives. | |||||

Enhance Value and Cash Flows Through Operating Expertise Our strong, time-tested operating capabilities enable us to increase the value of the assets within our businesses and the cash flows they produce, and they help to protect capital in adverse conditions. Our operating expertise, development capabilities and effective financing can help ensure that an investment’s full value creation potential is realized, which we believe is one of our most important competitive advantages. | |||||

Realize Capital from Asset Sales or Refinancings We actively monitor opportunities to sell or refinance assets to generate proceeds; in our limited life funds that capital is returned to investors, and in the case of our perpetual funds, we then redeploy the capital to enhance returns. In many cases, returning capital from private funds completes the investment process, locks in investor returns and gives rise to performance income. | |||||

Our Operating Cycle Leads to Value Creation We create value from earning robust returns on our investments that compound over time and grow our fee-bearing capital. By generating value for our investors and shareholders, we increase fees and carried interest received in our asset management business, and grow cash flows that compound value in our invested capital. |  | ||||

23 BROOKFIELD ASSET MANAGEMENT

LIQUIDITY AND CAPITAL RESOURCES

The Corporation has $7 billion of liquidity and $77 billion on a group basis as at December 31, 2020, and we manage our liquidity and capitalization on a group-wide basis, which we organize into three principal tiers:

i)The Corporation:

•Strong levels of liquidity are maintained to support growth and ongoing operations.

•Capitalization consists of a large common equity base, supplemented with perpetual preferred shares, long-dated corporate bonds and, from time to time, draws on our corporate credit facilities.

•Negligible guarantees are provided on the financial obligations of listed affiliates and managed funds.

•High levels of cash flows are available after payment of common share dividends.

ii)Our listed affiliates (BPY/BPYU, BEP/BEPC, BIP/BIPC and BBU):

•Strong levels of liquidity are maintained at each of the listed affiliates to support their growth and ongoing operations.

•Listed affiliates are intended to be self-funding with stable capitalization through market cycles.

•Financial obligations have no recourse to the Corporation.

iii)Managed funds, or investments, either held directly or within listed affiliates:

•Each underlying investment is typically funded on a standalone basis.

•Fund level borrowings are generally limited to subscription facilities backed by the capital commitments to the fund.

•Financial obligations have no recourse to the Corporation.

Approach to Capitalization

We maintain a prudent level of long-dated capitalization in the form of common equity, perpetual preferred shares and corporate bonds, which provides a very stable capital structure. In addition, we maintain appropriate levels of liquidity throughout the organization to fund operating, development and investment activities as well as unforeseen requirements.

A key element of our capital strategy is to maintain significant liquidity at the corporate level, primarily in the form of cash, financial assets and undrawn credit lines.

Within our listed affiliates and private funds, we strive to:

•Ensure our listed affiliates can finance their operations on a standalone basis without recourse to or reliance on the Corporation.

•Structure borrowings and other financial obligations associated with assets or portfolio companies in our private funds to provide a stable capitalization at levels that are attractive to investors, are sustainable on a long-term basis and can withstand business cycles.

•Ensure the vast majority of this debt is at investment-grade levels; however, periodically, we may borrow at sub-investment grade levels in certain parts of our business where the borrowings are carefully structured and monitored.

•Provide recourse only to the specific businesses or assets being financed, without cross-collateralization or parental guarantees.

•Match the duration of our debt to the underlying leases or contracts and match the currency of our debt to that of the assets such that our remaining exposure is on the net equity of the investment.

As at December 31, 2020, only $9 billion of long-term debt has recourse to the Corporation. The remaining debt on our Consolidated Balance Sheet is held within managed entities and has no recourse to the Corporation but is consolidated under IFRS.

2020 ANNUAL REPORT 24

Liquidity

•The Corporation has very few capital requirements. Nevertheless, we maintain significant liquidity ($7 billion in the form of cash and financial assets and undrawn credit facilities as at December 31, 2020) at the corporate level to bridge larger fund transactions, seed new fund products, invest in businesses alongside our fund investors or participate in equity issuances by our listed affiliates.

•On a group basis, we have approximately $77 billion of liquidity, which includes corporate liquidity, listed affiliate liquidity and uncalled private fund commitments. Uncalled private fund commitments are third-party commitments available for drawdown in our private funds.

| AS AT DEC. 31, 2020 (MILLIONS) | Corporate Liquidity | Group Liquidity | |||||||||

| Cash and financial assets, net | $ | 4,456 | $ | 6,823 | |||||||

| Undrawn committed credit facilities | 2,526 | 9,194 | |||||||||

Core liquidity1 | 6,982 | 16,017 | |||||||||

| Third-party uncalled private fund commitments | — | 60,594 | |||||||||

Total liquidity1 | $ | 6,982 | $ | 76,611 | |||||||

Capital Management

We utilize a metric we call the Corporation’s Capital to manage the business in a number of ways, including operating performance, value creation, credit metrics and capital efficiency. The performance of the Corporation’s Capital is closely tracked and monitored by the company’s key management personnel and evaluated relative to management’s objectives. The primary goal of the company is to earn a 12-15% return compounded over the long-term while always maintaining excess capital to support ongoing operations.

The Corporation’s Capital consists of the capital invested in its asset management activities, including investments in entities that it manages, its corporate investments that are held outside of managed entities and its net working capital, and is computed as follows:

| AS AT DEC. 31 (MILLIONS) | 2020 | 2019 | |||||||||||||||||||||

| Cash and cash equivalents | $ | 1,283 | $ | 807 | |||||||||||||||||||

| Other financial assets | 3,809 | 2,722 | |||||||||||||||||||||

| Common equity in managed investments | 33,732 | 33,839 | |||||||||||||||||||||

| Other assets and liabilities of the Corporation | 6,321 | 4,728 | |||||||||||||||||||||

| Corporation’s Capital | $ | 45,145 | $ | 42,096 | |||||||||||||||||||

The Corporation’s Capital is funded with common equity, preferred equity and corporate borrowings issued by the Corporation.

| 2020 | 2019 | ||||||||||||||||||||||

| Common equity | $ | 31,693 | $ | 30,868 | |||||||||||||||||||

| Preferred shares | 4,145 | 4,145 | |||||||||||||||||||||

| Non-controlling interest | 230 | — | |||||||||||||||||||||

| Corporate borrowings | 9,077 | 7,083 | |||||||||||||||||||||

| Corporation’s Capital | 45,145 | 42,096 | |||||||||||||||||||||

We maintain a prudent level of capitalization at the Corporation with 72% of our book capitalization in the form of common and preferred equity. Consistent with our conservative approach, our corporate borrowings represent only 18% of our corporate book capitalization and equate to just 6% of our consolidated debt.

1.See definition in Glossary of Terms beginning on page 115.

25 BROOKFIELD ASSET MANAGEMENT

The remaining 94% of our consolidated debt is non-recourse and is held within managed entities and has virtually no cross-collateralization or parental guarantees by the Corporation.

The following table presents our total capitalization on a corporate and consolidated basis. Total capitalization also includes amounts payable under long-term incentive plans, fixed annuity liabilities fully backed by financial asset portfolios, deferred tax liabilities and other working capital balances:

| AS AT DEC. 31 (MILLIONS) | Corporate | Consolidated | |||||||||||||||||||||||||||||||||||||||

| 2020 | 2019 | 2020 | 2019 | ||||||||||||||||||||||||||||||||||||||

| Corporate borrowings | $ | 9,077 | $ | 7,083 | $ | 9,077 | $ | 7,083 | |||||||||||||||||||||||||||||||||

| Non-recourse borrowings | |||||||||||||||||||||||||||||||||||||||||

| Subsidiary borrowings | — | — | 10,768 | 8,423 | |||||||||||||||||||||||||||||||||||||

| Property-specific borrowings | — | — | 128,556 | 127,869 | |||||||||||||||||||||||||||||||||||||

| 9,077 | 7,083 | 148,401 | 143,375 | ||||||||||||||||||||||||||||||||||||||

| Corporation’s Capital, excluding corporate borrowings | 36,068 | 35,013 | 36,068 | 35,013 | |||||||||||||||||||||||||||||||||||||

| Accounts payable, deferred taxes and other | 5,395 | 4,987 | 159,227 | 145,581 | |||||||||||||||||||||||||||||||||||||

| Total capitalization | $ | 50,540 | $ | 47,083 | $ | 343,696 | $ | 323,969 | |||||||||||||||||||||||||||||||||

| Debt to capitalization | 18 | % | 15 | % | 43 | % | 44 | % | |||||||||||||||||||||||||||||||||||||||||||||

Cash Flow Generation from our Capital

Our Corporation’s Capital generates significant, recurring cash flows at the corporate level, which may be used for (i) reinvestment into the business; or (ii) returning cash to shareholders. These cash flows are underpinned by:

•Fee-related earnings2 that are supported by long-term and perpetual contractual agreements.

•Distributions from listed investments that are stable and backed by high-quality operating assets.

These cash flows are supplemented with carried interest as we monetize mature investments and return capital to our investors.

Cash available for distribution and/or reinvestment1 was $3.1 billion for 2020, and over the past five years has grown at a 9% compound annual growth rate.

| FOR THE YEARS ENDED DEC. 31 (MILLIONS) | 2020 | 2019 | |||||||||

Fee-related earnings2 | $ | 1,242 | $ | 1,169 | |||||||

Realized carried interest, net2 | 244 | 386 | |||||||||

| Our share of Oaktree’s distributable earnings | 259 | 42 | |||||||||

| Distributions from investments | 1,929 | 1,589 | |||||||||

| Other invested capital earnings | |||||||||||

| Corporate activities | (539) | (483) | |||||||||

| Other wholly owned investments | 16 | (36) | |||||||||

| 3,151 | 2,667 | ||||||||||

| Preferred share dividends | (142) | (152) | |||||||||

| Add back: equity-based compensation costs | 94 | 87 | |||||||||

Total cash available for distribution and/or reinvestment2 | $ | 3,103 | $ | 2,602 | |||||||

1.See definition in Glossary of Terms beginning on page 115.

2.Excludes $186 million and $104 million of fee-related earnings and realized carried interest, net from Oaktree, respectively (2019 – $32 million and $10 million). See definition in Glossary of Terms beginning on page 115.

2020 ANNUAL REPORT 26

RISK MANAGEMENT

Our Approach

Managing risk is an integral and critical part of our business. We have a well-established, proactive and disciplined risk management approach that is based on clear operating methods and a strong risk management culture. We ensure that we have the necessary capacity and resilience to respond to changing environments by evaluating both current and emerging risks. We adhere to a robust risk management framework and methodology that is designed to enable comprehensive and consistent management of risk across the organization.

We use a thorough and integrated risk assessment process to identify and evaluate risk areas across the business such as human capital, climate change, liquidity, disruption, compliance and other strategic, financial, regulatory and operational risks. Management and mitigation approaches and practices are tailored to the specific risk areas and executed by business and functional groups for their businesses, with appropriate coordination and oversight through monitoring and reporting processes.

27 BROOKFIELD ASSET MANAGEMENT

Focus on Risk Culture

A strong risk culture is the cornerstone of our risk management program: one that promotes measured and appropriate risk-taking, addresses current and emerging risks and ensures employees conduct business with a long-term perspective and in a sustainable and ethical manner. This culture is reinforced by strong commitment and leadership from our senior executives, as well as the policies and practices we have implemented, including our compensation approach.

Shared Execution

Given the diversified and decentralized nature of our operations, we seek to ensure that risk is managed as close to its source as possible and by the management teams that have the most knowledge and expertise in the specific business or risk area. As such, business specific risks overall—such as safety, environment and other operational risks—are generally managed at the operating business group level, as the risks vary based on the nature of each business. At the same time, we monitor many of these risks organization-wide to ensure adequacy of risk management, adherence to applicable Brookfield policies, and sharing of best practices.

For risks that are more pervasive and correlated in their impact across the organization—such as liquidity, foreign exchange and interest rates or where we can bring specialized knowledge—we utilize a centralized approach amongst our corporate and our operating business groups. Management of strategic, reputational and regulatory compliance risks are similarly coordinated to ensure consistent focus and implementation across the organization.

Oversight & Coordination

We have implemented strong governance practices to monitor and oversee our risk management program. Management committees bring together required expertise to manage key risk areas, ensuring appropriate application and coordination of approaches and practices across our business and functional groups, and include the following:

•Risk Management Steering Committee – supports the overall corporate risk management program, and coordinates risk assessment and mitigation on an enterprise-wide basis

•Investment Committees – oversees the investment process and reviews and approves investment transactions

•Conflicts Committee – resolves potential conflict situations in the investment process and other corporate transactions

•Financial Risk Oversight Committee – reviews and monitors financial exposure

•Environmental, Social and Governance (ESG) Steering Committee – oversees ESG initiatives, with a focus on health, safety, security and environmental matters

•Disclosure Committee – oversees the public disclosure of material information

Brookfield’s Board of Directors oversees risk management with a focus on more significant risks, and leverages management’s monitoring processes. The Board has delegated responsibility for oversight of specific risks to the following board committees:

•Risk Management Committee – oversees the management of Brookfield’s significant financial and non-financial risk exposures, including review of risk assessment and risk management practices, and confirms that the company has an appropriate risk-taking philosophy and suitable risk capacity

•Audit Committee – oversees the management of risks related to Brookfield’s systems and procedures for financial reporting, as well as for associated audit processes (internal and external)