UNITED STATES SECURITIES AND EXCHANGE COMMISSIONWASHINGTON, D.C. 20549

FORM 20-F

| ¨ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2008

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| ¨ | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Date of event requiring this shell company report ______________

For the transition period from to

Commission file number 1-14014

CREDICORP LTD.

(Exact name of registrant as specified in its

charter)

BERMUDA

(Jurisdiction of incorporation or organization)

Of our subsidiary

Banco de Crédito del Perú:

Calle Centenario 156

La Molina

Lima 12, Perú

(Address of principal executive offices)

__________________________________________________________

Securities registered or to be registered pursuant to Section 12(b) of the Act.

| Title of each class | Name of each exchange on which registered |

| Common Shares, par value $5.00 per share | New York Stock Exchange |

Securities registered or to be registered pursuant to Section 12(g) of the Act. None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act. None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report.

Common Shares, par value $5.00 per share 94,382,317

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes x No ¨

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act.

Large accelerated filer x Accelerated filer ¨ Non-accelerated filer ¨

Indicate by check mark which financial statement item the registrant has elected to follow.

Item 17 ¨ Item 18 x

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes ¨ No x

TABLE OF CONTENTS

| PRESENTATION OF FINANCIAL INFORMATION | 1 |

| CAUTIONARY STATEMENT WITH RESPECT TO FORWARD-LOOKING STATEMENTS | 2 |

| | | |

| PART I | | |

| | | |

| ITEM 1. | IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS | 3 |

| ITEM 2. | OFFER STATISTICS AND EXPECTED TIMETABLE | 3 |

| ITEM 3. | KEY INFORMATION | 3 |

| ITEM 4. | INFORMATION ON THE COMPANY | 12 |

| ITEM 4A. | UNRESOLVED STAFF COMMENTS | 93 |

| ITEM 5. | OPERATING AND FINANCIAL REVIEW AND PROSPECTS | 93 |

| ITEM 6. | DIRECTORS, SENIOR MANAGEMENT AND EMPLOYEES | 117 |

| ITEM 7. | MAJOR SHAREHOLDERS AND RELATED PARTY TRANSACTIONS | 123 |

| ITEM 8. | FINANCIAL INFORMATION | 125 |

| ITEM 9. | THE OFFER AND LISTING | 126 |

| ITEM 10. | ADDITIONAL INFORMATION | 130 |

| ITEM 11. | QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK | 132 |

| ITEM 12. | DESCRIPTION OF SECURITIES OTHER THAN EQUITY SECURITIES | 142 |

| ITEM 13. | DEFAULTS, DIVIDEND ARREARAGES AND DELINQUENCIES | 142 |

| ITEM 14. | MATERIAL MODIFICATIONS TO THE RIGHTS OF SECURITY HOLDERS AND USE OF PROCEEDS | 142 |

| ITEM 15. | CONTROLS AND PROCEDURES | 142 |

| ITEM 16A. | AUDIT COMMITTEE FINANCIAL EXPERT | 146 |

| ITEM 16B. | CODE OF ETHICS | 146 |

| ITEM 16C. | PRINCIPAL ACCOUNTANT FEES AND SERVICES | 146 |

| ITEM 16D. | EXEMPTIONS FROM THE LISTING STANDARDS FOR AUDIT COMMITTEES | 147 |

| ITEM 16E. | PURCHASES OF EQUITY SECURITIES BY THE ISSUER AND AFFILIATED PURCHASERS | 148 |

| ITEM 16F. | CHANGE IN REGISTRANT’S CERTIFYING ACCOUNTANT | 148 |

| ITEM 16G. | CORPORATE GOVERNANCE | 148 |

| ITEM 17. | FINANCIAL STATEMENTS | 152 |

| ITEM 18. | FINANCIAL STATEMENTS | 152 |

| ITEM 19. | EXHIBITS | 153 |

| CERTIFICATIONS PURSUANT TO SECTION 302 OF THE U.S. SARBANES-OXLEY ACT OF 2002 | |

| CERTIFICATIONS PURSUANT TO SECTION 302 OF THE U.S. SARBANES-OXLEY ACT OF 2002 | |

PRESENTATION OF FINANCIAL INFORMATION

Unless otherwise specified or the context otherwise requires, references in this Form 20-F (also referred to as the Annual Report), to “$,” “US$,” “Dollars,” “U.S. Dollars,” are to United States Dollars, and references to “S/.,” “Nuevo Sol” or “Nuevos Soles” are to Peruvian Nuevos Soles and references to “foreign currency” are to U.S. Dollars. Each Nuevo Sol is divided into 100 céntimos (cents).

Credicorp Ltd. is a Bermuda limited liability company (and is referred to in this Annual report as Credicorp, we, or us, and means either Credicorp as a separate entity or as an entity together with our consolidated subsidiaries as the context may require). We maintains our financial books and records in U.S. Dollars and present our financial statements in accordance with International Financial Reporting Standards (IFRS), as issued by the International Accounting Standards Board (IASB). IFRS differ in certain respects from United States Generally Accepted Accounting Principles (U.S. GAAP).

We operate primarily through our four principal subsidiaries, Banco de Crédito del Perú (which together with its consolidated subsidiaries is referred to as BCP), Atlantic Security Holding Corporation (which together with its consolidated subsidiaries is referred to as ASHC), El Pacífico-Peruano Suiza Compañía de Seguros y Reaseguros (which together with its consolidated subsidiaries is referred to as Pacífico Peruano Suiza or PPS) and Grupo Crédito S.A. (which together with its consolidated subsidiaries is referred to as Grupo Crédito). BCP’s activities include commercial banking, investment banking and retail banking. As of and for the year ended December 31, 2008, BCP accounted for 75.1% of our total revenues, 87.3% of our total assets, 117.9% of our net income and 80.6% of our net equity. Unless otherwise specified, the individual financial information for BCP, ASHC, PPS and Grupo Crédito included in this Annual Report has been derived from the audited consolidated financial statements of each such entity. See “Item 3. Key Information—(A) Selected Financial Data” and “Item 4. Information on the Company—(A) History and Development of the Company.”

“Item 3. Key Information—(A) Selected Financial Data” contains key information related to our performance. This information was obtained mainly from our consolidated financial statements as of December 31, 2004, 2005, 2006, 2007 and 2008.

Our management’s criteria on foreign currency translation for the purpose of preparing the Credicorp Consolidated Financial Statements is described in “Item 5. Operating and Financial Review and Prospects—(A) Operating Results—(1) Critical Accounting Policies—Foreign Currency Translation.”

Some of our subsidiaries maintain their operations and balances in Nuevo Soles. As a result, this Annual Report contains certain Nuevo Sol amounts translated into U.S. Dollars which is solely for the convenience of the reader. You should not construe any of these translations as representations that the Nuevo Sol amounts actually represent such equivalent U.S. Dollar amounts or could be converted into U.S. Dollars at the rate indicated as of the dates mentioned herein, or at all. Unless otherwise indicated, these U.S. Dollar amounts have been translated from Nuevos Soles at an exchange rate of S/.3.140 = US$1.00, which is the December 31, 2008 exchange rate set by the Peruvian Superintendencia de Banca, Seguros y AFP (the Superintendency of Banks, Insurance and Pension Funds, or the SBS). The average of the bid and offered free market exchange rates published by the SBS for June 25, 2009 was S/.3.024 per US$1.00. Translating amounts expressed in Nuevos Soles on a specified date (at the prevailing exchange rate on that date) may result in the presentation of U.S. Dollar amounts that are different from the U.S. Dollar amounts that would have been obtained by translating Nuevos Soles on another specified date (at the prevailing exchange rate on that different specified date). See also “Item 3. Key Information—(A) Selected Financial Data—Exchange Rates” for information regarding the average rates of exchange between the Nuevo Sol and the U.S. Dollar for the periods specified therein. The Federal Reserve Bank of New York does not publish a noon buying rate for Nuevos Soles.

CAUTIONARY STATEMENT WITH RESPECT TO

FORWARD-LOOKING STATEMENTS

Certain statements contained in this Annual Report are not historical facts, including, without limitation, certain statements made in the sections entitled “Item 3. Key Information,” “Item 4. Information on the Company,” “Item 5. Operating and Financial Review and Prospects” and “Item 11. Quantitative and Qualitative Disclosures about Market Risk,” which are forward-looking statements within the meaning of Section 27A of the U.S. Securities Act of 1933 and Section 21E of the U.S. Securities Exchange Act of 1934 (or the Exchange Act). These forward-looking statements are based on our management’s current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in the forward-looking statements. Therefore, actual results, performance or events may be materially different from those in the forward-looking statements due to, without limitation:

| | · | general economic conditions, including in particular economic conditions in Peru; |

| | · | performance of financial markets, including emerging markets; |

| | · | the frequency and severity of insured loss events; |

| | · | currency exchange rates, including the Nuevo Sol/U.S. Dollar exchange rate; |

| | · | increasing levels of competition in Peru and other emerging markets; |

| | · | changes in laws and regulations; |

| | · | changes in the policies of central banks and/or foreign governments; and |

| | · | general competitive factors, in each case on a global, regional and/or national basis. |

See “Item 3. Key Information—(D) Risk Factors,” and “Item 5. Operating and Financial Review and Prospects.”

We are not under any obligation to, and we expressly disclaims any such obligation to, update or alter our forward-looking statements, whether as a result of new information, future events or otherwise.

PART I

ITEM 1. | IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS |

Not applicable.

ITEM 2. | OFFER STATISTICS AND EXPECTED TIMETABLE |

Not applicable.

(A) | Selected Financial Data |

The following table presents summary of our consolidated financial information at the dates and for the periods indicated. This selected financial data is presented in U.S. Dollars. You should read this information in conjunction with, and qualify this information in its entirety by reference to, the Credicorp Consolidated Financial Statements, also presented in U.S. Dollars.

The summary of our consolidated financial data as of, and for the years ended, December 31, 2004, 2005, 2006, 2007 and 2008 is derived from the Credicorp Consolidated Financial Statements audited by Medina, Zaldívar, Paredes & Asociados S.C.R.L, member of Ernst & Young Global, independent registered public accountants.

The report of Medina, Zaldívar, Paredes & Asociados S.C.R.L on the Credicorp Consolidated Financial Statements as of December 31, 2007 and 2008 and for the years ended December 31, 2006, 2007 and 2008 appears elsewhere in this Annual Report.

SELECTED FINANCIAL DATA

| | | Year ended December 31, | |

| | | 2004 | | | 2005 | | | 2006 | | | 2007 | | | 2008 | |

| | | (U.S. Dollars in thousands, except percentages, ratios, and per common share data) | |

| INCOME STATEMENT DATA: | | | | | | | | | | | | | | | |

| IFRS: | | | | | | | | | | | | | | | |

| Interest income | | US$ | 542,842 | | | US$ | 612,432 | | | US$ | 782,002 | | | US$ | 1,065,974 | | | US$ | 1,400,334 | |

| Interest expense | | | (160,298 | ) | | | (173,159 | ) | | | (283,478 | ) | | | (432,000 | ) | | | (577,411 | ) |

| Net Interest income | | | 382,544 | | | | 439,273 | | | | 498,524 | | | | 633,974 | | | | 822,923 | |

| Provision for loan losses (1) | | | (16,131 | ) | | | 6,356 | | | | 4,243 | | | | (28,439 | ) | | | (48,760 | ) |

| Net interest income after provision for loan losses | | | 366,413 | | | | 445,629 | | | | 502,767 | | | | 605,535 | | | | 774,163 | |

| Fees and commissions from banking services | | | 201,474 | | | | 206,163 | | | | 243,778 | | | | 324,761 | | | | 394,247 | |

| Net gains (loss) from sales of securities | | | 10,135 | | | | 8,965 | | | | 27,281 | | | | 46,376 | | | | 51,936 | |

| Net gains on foreign exchange transactions | | | 24,165 | | | | 29,286 | | | | 41,638 | | | | 61,778 | | | | 108,709 | |

| Net premiums earned | | | 192,672 | | | | 218,955 | | | | 251,261 | | | | 297,272 | | | | 393,903 | |

| Other income | | | 8,105 | | | | 21,571 | | | | 26,197 | | | | 90,022 | | | | 37,672 | |

| Claims on insurance activities | | | (154,325 | ) | | | (175,500 | ) | | | (186,522 | ) | | | (238,600 | ) | | | (341,910 | ) |

| Operating expenses | | | (459,928 | ) | | | (477,073 | ) | | | (585,058 | ) | | | (747,089 | ) | | | (922,299 | ) |

| Merger costs | | | (3,742 | ) | | | 0 | | | | (5,706 | ) | | | 0 | | | | 0 | |

| Income before translation result and income tax | | | 184,969 | | | | 277,996 | | | | 315,636 | | | | 440,055 | | | | 496,421 | |

| Translation result | | | 2,040 | | | | (9,597 | ) | | | 15,216 | | | | 34,627 | | | | (17,650 | ) |

| Income tax | | | (45,497 | ) | | | (73,546 | ) | | | (83,587 | ) | | | (102,287 | ) | | | (109,508 | ) |

| Net income | | | 141,512 | | | | 194,853 | | | | 247,265 | | | | 372,395 | | | | 369,263 | |

Attributable to: | | | | | | | | | | | | | | | | | | | | |

| Net income attributable to Credicorp’s equity holders | | | 130,747 | | | | 181,885 | | | | 230,013 | | | | 350,735 | | | | 357,756 | |

| Minority interest | | | 10,765 | | | | 12,968 | | | | 17,252 | | | | 21,660 | | | | 11,507 | |

| | | | | | | | | | | | | | | | | | | | | |

| Net income per common share attributable to Credicorp´s equity holders (2) | | | 1.64 | | | | 2.28 | | | | 2.88 | | | | 4.40 | | | | 4.49 | |

| Cash dividends declared per common share | | | 0.80 | | | | 1.10 | | | | 1.30 | | | | 1.50 | | | | 1.50 | |

| BALANCE SHEET DATA: | | | | | | | | | | | | | | | | | | | | |

| IFRS: | | | | | | | | | | | | | | | | | | | | |

| Total assets | | | 9,087,560 | | | | 11,036,075 | | | | 12,881,529 | | | | 17,705,898 | | | | 20,821,069 | |

| Total loans (3) | | | 4,559,018 | | | | 4,972,975 | | | | 5,877,361 | | | | 8,183,845 | | | | 10,456,284 | |

| Reserves for loan losses (1) | | | (271,873 | ) | | | (218,636 | ) | | | (210,586 | ) | | | (229,700 | ) | | | (248,063 | ) |

| Total deposits | | | 6,270,972 | | | | 7,067,754 | | | | 8,799,134 | | | | 11,299,671 | | | | 13,877,028 | |

| Equity attributable to Credicorp’s equity holders | | | 1,065,197 | | | | 1,190,440 | | | | 1,396,822 | | | | 1,676,009 | | | | 1,689,172 | |

| Minority interest | | | 85,253 | | | | 101,515 | | | | 136,946 | | | | 139,264 | | | | 106,933 | |

| Net Equity | | | 1,150,450 | | | | 1,291,955 | | | | 1,533,768 | | | | 1,815,273 | | | | 1,796,105 | |

| SELECTED RATIOS | | | | | | | | | | | | | | | | | | | | |

| IFRS: | | | | | | | | | | | | | | | | | | | | |

| Net interest margin (4) | | | 4.85 | % | | | 4.90 | % | | | 4.64 | % | | | 4.50 | % | | | 4.47 | % |

| Return on average total assets (5) | | | 1.50 | % | | | 1.81 | % | | | 1.92 | % | | | 2.29 | % | | | 1.86 | % |

| Return on average equity attributable to Credicorp’s equity holders (6) | | | 13.55 | % | | | 16.39 | % | | | 18.44 | % | | | 22.67 | % | | | 20.21 | % |

| Operating expenses as a percentage of net interest and non-interest income (7) | | | 49.18 | % | | | 46.25 | % | | | 50.26 | % | | | 50.62 | % | | | 40.23 | % |

| | | Year ended December 31, | |

| | | 2004 | | | 2005 | | | 2006 | | | 2007 | | | 2008 | |

| | | (U.S. Dollars in thousands, except percentages, ratios, and per common share data) |

| Operating expenses as a percentage of average assets | | | 5.28 | % | | | 4.74 | % | | | 4.89 | % | | | 4.88 | % | | | 4.79 | % |

| Equity attributable to Credicorp’s equity holders as a percentage of period end total assets | | | 11.72 | % | | | 10.79 | % | | | 10.84 | % | | | 9.47 | % | | | 8.11 | % |

| Regulatory capital as a percentage of risk weighted assets (8) | | | 14.04 | % | | | 13.10 | % | | | 11.98 | % | | | 12.80 | % | | | 12.33 | % |

| Total past-due loan amounts as a percentage of total loans (9) | | | 3.49 | % | | | 1.93 | % | | | 1.31 | % | | | 0.75 | % | | | 0.79 | % |

| Reserves for loan losses as a percentage of total loans | | | 5.96 | % | | | 3.97 | % | | | 3.24 | % | | | 2.58 | % | | | 2.15 | % |

| Reserves for loan losses as a percentage of total loans and other contingent credits (10) | | | 4.99 | % | | | 3.19 | % | | | 2.59 | % | | | 2.17 | % | | | 1.84 | % |

| Reserves for loan losses as a percentage of total past-due loans (11) | | | 170.93 | % | | | 206.22 | % | | | 247.85 | % | | | 343.68 | % | | | 270.72 | % |

| Reserves for loan losses as a percentage of substandard loans (12) | | | 54.11 | % | | | 65.42 | % | | | 78.24 | % | | | 100.45 | % | | | 112.26 | % |

| (1) | Provision for loan losses and reserve for loan losses include provisions and reserves with respect to total loans and contingent credits, net of write-off recoveries. |

| (2) | We have 100 million authorized common shares. As of December 31, 2008, we had issued 94.4 million common shares, of which 14.6 million are held by ASHC. The per common share data given considers net outstanding shares (common shares net of shares held by BCP, ASHC and PPS) of 79.7 million in 2002 to 2008. See Notes 16 and 25 to the Credicorp Consolidated Financial Statements. |

| (3) | Net of unearned interest, but prior to reserve for loan losses. In addition to loans outstanding, we had contingent loans of US$889.1 million, US$1,220.9 million, US$1,455.4 million, US$1,564.5 million and US$1,755.9 million, as of December 31, 2004, 2005, 2006, 2007 and 2008, respectively. See Note 19 to the Credicorp Consolidated Financial Statements. |

| (4) | Net interest income as a percentage of average interest-earning assets, computed as the average of period-beginning and period-ending balances on a monthly basis. |

| (5) | Net income as a percentage of average total assets, computed as the average of period-beginning and period-ending balances. |

| (6) | Net income as a percentage of average equity attributable to our equity holders, computed as the average of period-beginning and period-ending balances, and calculated on a monthly basis. |

| (7) | Sum of the salaries and employee’s benefits, administrative expenses, depreciation and amortization, as a percentage of the sum of net interest income and non-interest income, less net gains from sales of securities and other income. |

| (8) | Regulatory capital calculated in accordance with guidelines by the Basel Committee on Banking Regulations and Supervisory Practices of International Settlements (or the BIS I Accord) as adopted by the SBS. See “Item 5. Operating and Financial Review and Prospects—(B) Liquidity and Capital Resources—Regulatory Capital and Capital Adequacy Ratios.” |

| (9) | BCP considers loans past due after 90 days for installment loans, which include mortgage loans but exclude consumer loans. ASHC considers past due all overdue loans except for consumer loans, which are considered past due when the scheduled principal and/or interest payments are overdue for more than 90 days. For IFRS 7 disclosure requirements on past-due loans, See Note 29.1 to the Credicorp Consolidated Financial Statements. See “Item 4. Information on the Company—(B) Business Overview—(12) Selected Statistical Information—(iii) Loan Portfolio—Classification of the Loan Portfolio Based on the Borrower’s Payment Performance.” |

| (10) | Other contingent credits primarily consist of guarantees, stand-by letters and letters of credit. See Note 19 to the Credicorp Consolidated Financial Statements. |

| (11) | Reserves for loan and contingent credit losses, as a percentage of all past-due loans, with no reduction for collateral securing such loans. Reserves for loan and contingent credit losses include reserves with respect to total loans and other credits. |

| (12) | Reserves for loan and contingent credit losses as a percentage of loans classified in categories C, D or E. See “Item 4. Information on the Company—(B) Business Overview—(12) Selected Statistical Information—(iii) Loan Portfolio—Classification of Loan Portfolio.” |

Exchange Rates

The following table sets forth the high and low month-end rates and the average and end-of-period rates for the sale of Nuevos Soles for U.S. Dollars for the periods indicated.

| Year ended December 31, | | High (1) | | | Low (1) | | | Average (2) | | | Period-end (3) | |

| | | (Nominal Nuevos Soles per U.S. Dollar) | |

| 2004 | | | 3.500 | | | | 3.283 | | | | 3.410 | | | | 3.283 | |

| 2005 | | | 3.440 | | | | 3.249 | | | | 3.295 | | | | 3.420 | |

| 2006 | | | 3.455 | | | | 3.195 | | | | 3.274 | | | | 3.195 | |

| 2007 | | | 3.197 | | | | 2.998 | | | | 3.125 | | | | 2.998 | |

| 2008 | | | 3.135 | | | | 2.751 | | | | 2.939 | | | | 3.135 | |

Source: Bloomberg

| (1) | Highest and lowest of the 12 month-end exchange rates for each year based on the offered rate. |

| (2) | Average of month-end exchange rates based on the offered rate. |

| (3) | End-of-period exchange rates based on the offered rate. |

The following table sets forth the high and low rates for the sale of Nuevos Soles for U.S. Dollars for the indicated months.

| | | | | | | |

| | | (Nominal Nuevos Soles per U.S. Dollar) | |

| 2008 | | | | | | |

| December | | | 3.142 | | | | 3.081 | |

| 2009 | | | | | | | | |

| January | | | 3.187 | | | | 3.131 | |

| February | | | 3.251 | | | | 3.202 | |

| March | | | 3.259 | | | | 3.107 | |

| April | | | 3.145 | | | | 2.981 | |

| May | | | 3.051 | | | | 2.950 | |

| June (through June 25) | | | 3.024 | | | | 2.967 | |

Source: Bloomberg

(1) Highest and lowest of the daily closing exchange rates for each month based on the offered rate.

The average of the bid and offered free market exchange rates published by the SBS for June 25, 2009 was S/.3.024 per US$1.00.

| (B) | Capitalization and Indebtedness |

Not applicable.

| (C) | Reasons for the Offer and Use of Proceeds |

Not applicable.

Our businesses are affected by many external and other factors in the markets in which we operate. Different risk factors can impact our businesses and the ability to effectively operate our businesses and business strategies. You should consider the risk factors carefully and read them in conjunction with all the information in this document.

Our geographic location exposes us to risk related to Peruvian political and economic conditions.

Most of BCP’s, PPS’s and Prima AFP’s operations and customers are located in Peru. In addition, although ASHC is based outside of Peru, most of its customers are located in Peru. Accordingly, our results of operations and financial conditions will be dependent on the level of economic activity in Peru. Changes in economic or other policies of the Peruvian government (which has exercised and continues to exercise a substantial influence over many aspects of the private sector) could affect our results of operations and financial condition. Similarly, other political or economic developments in Peru, including government-induced effects on inflation, devaluation, and economic growth could affect our operations and financial condition.

For several decades, Peru had a history of political instability that has included military coups and a succession of regimes with differing policies and programs. Past governments have frequently intervened in the nation’s economy and social structure. Among other actions, past governments have imposed controls on prices, exchange rates, local and foreign investment, and international trade. Past governments have also restricted the ability of companies to dismiss employees, expropriated private sector assets and prohibited the payment of profits to foreign investors.

In July 1990, Alberto Fujimori was elected President and implemented a broad-based reform of Peru’s political system and economic and social conditions. The reform was aimed at stabilizing the economy, restructuring the national government (by reducing bureaucracy), privatizing state-owned companies, promoting private investment, eradicating corruption and bribery in the judicial system, developing and strengthening free markets, institutionalizing democratic representation, and enacting programs for the strengthening of basic services related to education, health, housing and infrastructure. After taking office for his third term in July 2000, under extreme protest, President Fujimori was forced to call for general elections due to the outbreak of corruption scandals. Fujimori later resigned in favor of a transitory government.

During 1980s and early 1990s the Sendero Luminoso (Shining Path), and the Movimiento Revolucionario Tupac Amaru (MRTA), terrorist organizations were particularly active in Peru. Although the Shining Path and MRTA were almost de-activated in the 1990s, any resumption of activities by these or other terrorist organizations may adversely affect our operations.

In 2001, Alejandro Toledo became President, ending two years of political turmoil. President Toledo retained, for the most part, the economic policies of the previous government. He focused on promoting private investment, eliminating tax exemptions, and reducing underemployment and unemployment. President Toledo also implemented fiscal austerity programs, among other proposals, in order to stimulate the economy. Despite Peru’s moderate economic growth, the Toledo administration faced public unrest spurred by the high rates of unemployment, underemployment, and poverty.

In the elections held in April 2006, no presidential candidate received the required 50% or more of the votes. As a result, a second round election between the top two presidential candidates, Ollanta Humala Tasso from the Partido Unión por el Peru, or the UPP, and Alan García Pérez of the Partido Alianza Popular Revolucionaria, or APRA, was held on June 4, 2006. Although Alan García Pérez was elected, he has no majority in Congress. President García had previously served as President of Peru from 1985 to 1990, a period which was marked by a severe economic crisis. He is following conservative economic policies and has indicated a desire to avoid the mistakes of his past government. The García administration has followed economic policies similar to those of the Toledo administration, which included achieving sustained economic growth, increasing exports of Peruvian goods, reducing unemployment, underemployment, and poverty, reforming the tax system, fostering private investment, and increasing public investment in education, public health and other social programs, while reducing overall public spending.

The Peruvian government’s economic policies during the last decade have provided the fundamentals to support the positive performance of the economy. As a result, the international financial crisis has not impacted Peru as severely as other countries. In addition, the current government has also implemented a US$3 billion anti-crisis program to alleviate the effects of the crisis. However, while the economic policies of recent Peruvian governments have been relatively stable, we cannot assure you that future governments will maintain favorable economic policies.

Foreign exchange fluctuations and exchange controls may adversely affect our financial condition and results of operations.

Even though the functional currency of our financial statements is U.S. Dollars and our dividends are paid in U.S. Dollars, BCP and PPS, for local statutory purposes, prepare their financial statements and pay dividends in Nuevos Soles. The Peruvian government does not currently impose restrictions on a company’s ability to transfer U.S. Dollars from Peru to other countries, to convert Peruvian currency into U.S. Dollars, or to pay dividends abroad. Nevertheless, Peru has had restrictive exchange controls in the past, and there can be no assurance that the Peruvian government will continue to permit such transfers, payments or conversions without any restrictions. See “Item 10. Additional Information—(D) Exchange Controls.” In addition, depreciation of the Nuevo Sol against the U.S. Dollar would decrease the U.S. Dollar value of any dividends BCP and PPS pay us, which would have a negative impact on our ability to pay dividends to shareholders.

Although Peru’s foreign reserves currently compare favorably with those of many other Latin American countries, we cannot assure you that Peru will be able to maintain adequate foreign reserves to meet its foreign currency-denominated obligations. Similarly, we cannot assure you that Peru will not impose exchange controls should its foreign reserves decline. A decline in Peruvian foreign reserves to inadequate levels, among other economic circumstances, could lead to currency devaluation or a volatility of short-term capital inflows. We have taken steps to manage the gap between our foreign currency-denominated assets and liabilities in several ways, including closely matching the volumes and maturities of our Nuevo Sol-denominated loans against our Nuevo Sol-denominated deposits. Nevertheless, a sudden and significant devaluation of the Nuevo Sol could have a material adverse effect on our financial condition and results of operations. See “Item 11. Quantitative and Qualitative Disclosures about Market Risk—Foreign Exchange Risk.”

Also, a significant group of BCP’s borrowers and PPS’s insureds generate Nuevo Sol revenues from their own clients. Devaluation of the Nuevo Sol against the U.S. Dollar could negatively impact BCP’s and PPS’s clients ability to repay loans or make premium payments. Despite any devaluation, and absent any change in foreign exchange regulations, BCP and PPS would be expected to continue to repay U.S. Dollar-denominated deposits and U.S. Dollar-denominated insurance benefits in U.S. Dollars. Therefore, any significant devaluation of the Nuevo Sol against the U.S. Dollar could have a material adverse effect on our results of operations and financial condition.

It may be difficult to serve process on or enforce judgments against us or our principals residing outside of the United States.

A significant majority of our directors and officers live outside the United States (principally in Peru). All or most of our assets and those of our principals are located outside the United States. As a result, it may not be possible for investors to effect service of process within the United States upon us or our principals to bring forth a civil suit under the United States securities laws in United States courts. We have been advised by our Peruvian counsel that liability under the United States federal securities laws may not be enforceable in original actions in Peruvian courts. Also, judgments of United States courts obtained in actions under the United States federal securities laws may not be enforceable. Similarly, Bermudian counsel advised us that courts in Bermuda may not enforce judgments obtained in other jurisdictions, or entertain actions in Bermuda including judgments predicated upon civil liability provisions of the United States federal securities law, against us or our directors or officers under the securities laws of those jurisdictions.

In addition, our bye-laws, contain a broad waiver by shareholders of any claim or right of action, both individually and on our behalf, against any of our officers or directors. This waiver limits the rights of shareholders to assert claims against our officers and directors for any action taken by an officer or director. It also limits the rights of shareholders to assert claims against officers or any directors for the failure of an officer or director to take any action, in the performance of his or her duties, except with respect to any matter involving any willful negligence, willful default, fraud or dishonesty on the part of the officer or director.

Our ability to pay dividends to shareholders and to pay corporate expenses may be adversely affected by the ability of our subsidiaries to pay dividends to us.

As a holding company, our ability to make dividend payments, if any, and to pay corporate expenses will depend upon the receipt of dividends and other distributions from our operating subsidiaries. Our principal subsidiaries are BCP, PPS, ASHC and Grupo Crédito. If our subsidiaries do not have funds available, or are otherwise restricted from paying us dividends, we may be limited in our ability to pay dividends to shareholders. Currently, there are no restrictions on the ability of BCP, ASHC, PPS or Grupo Crédito to pay dividends abroad. In addition, our right to participate in the distribution of assets of any subsidiary, upon any subsidiary’s liquidation or reorganization (and thus the ability of holders of our securities to benefit indirectly from such distribution), is subject to the prior claims of creditors of that subsidiary, except where we are considered a creditor of the subsidiary. Accordingly, our securities will effectively be subordinated to all existing and future liabilities of our subsidiaries, and holders of our securities should look only to our assets for payments.

A deterioration in the quality of our loan portfolio may adversely affect our results of operations.

Given that a significant percentage of our revenues are related to banking activities, a deterioration of loan quality may have an adverse impact on our financial condition and results of operations. On the one hand, loan portfolio risk associated with lending to certain economic sectors or clients in certain market segments can be mitigated through adequate diversification policies. On the other hand, our pursuit of opportunities in which we can charge higher interest rates, thereby increasing revenues, may reduce diversification of the loan portfolio and expose us to greater credit risk. We believe that significant opportunities exist in middle market and consumer lending in Peru. We also believe that we can, on average, charge higher interest rates on such loans as compared with interest charged on loans in our core corporate banking business, made primarily to clients that operate in industrial and commercial economic sectors.

Accordingly, our strategy includes a greater emphasis on middle market and consumer loans, as well as continued growth of our loan portfolio in general. An increase in the portfolio’s exposure to these areas could be accompanied by greater credit risk. The greater credit risk is not only due to the speed and magnitude of the increase, but also to the shift to lending to the middle market and consumer sectors, which have higher risk profiles compared with loans to large corporate customers. Given the changing composition of our loan portfolio, historical loss experience may not be indicative of future loan loss experience.

Because we are subject to banking regulation and supervision in Peru, Bolivia, the Cayman Islands, Panama and the United States, changes to the regulatory framework in any of these countries could adversely affect our business.

We are mainly subject to extensive supervision and regulation through the SBS’s consolidated supervision regulations, which oversee all of our subsidiaries and offices including those located outside Peru. The SBS and the Banco Central de Reserva, or the Central Bank, supervise and regulate BCP’s operations. Peru’s constitution and the SBS’s statutory charter grant the SBS the authority to oversee and control banks and other financial institutions. The SBS and the Central Bank have general administrative responsibilities over BCP, including designation of capitalization and reserve requirements. In past years, the Central Bank has, on numerous occasions, changed the deposit reserve requirements applicable to Peruvian commercial banks as well as the rate of interest paid on deposit reserves and the amount of deposit reserves on which no interest is payable by the Central Bank. Such changes in the supervision and regulation of BCP may adversely affect our results of operations and financial condition. See “Item 4. Information on the Company—(B) Business Overview—(11) Supervision and Regulation—(ii) BCP.”

We are also regulated by the United States Federal Reserve, which shares regulatory responsibility with the State of Florida Department of Banking and Finance - Office of Financial Regulation. Similarly, we are regulated by other governmental entities in other jurisdictions. In the Cayman Islands, we are subject to the supervision and regulation of the Cayman Islands Monetary Authority, or CIMA, while in Bolivia, we are subject to the supervision of the Superintendency of Banks and Financial Entities and regulations established by the Central Bank of Bolivia. In Panama, we are subject to the supervision of the Superintendency of Banks and the regulatory framework set forth in the Decree Law 9 of February 25, 1998. Changes in the supervision and regulation of our subsidiaries in other countries may adversely affect our results of operations and financial condition.

Changes to insurance regulations in Peru may impact the ability of our insurance subsidiary to underwrite and price risk effectively, and may adversely affect our operating performance and financial condition.

Our insurance business is carried out by our subsidiary PPS. The insurance business is subject to regulation by the SBS. Insurance regulation in Peru is an area of constant change. New legislation or regulations may adversely affect PPS’s ability to underwrite and price risks accurately, which in turn would affect underwriting results and business profitability. PPS is unable to predict whether and to what extent new laws and regulations that would affect its business will be adopted in the future. PPS is also unable to predict the timing of any such adoption and what effects any new laws or regulations would have on its operations, profitability, and financial condition.

Our operating performance and financial condition depend on PPS’s ability to underwrite and set premium rates accurately for a full spectrum of risks. PPS must generate sufficient premiums to offset losses, loss adjustment expenses, and underwriting expenses so it may earn a profit. To price premium rates accurately, PPS must:

| | · | collect and analyze a substantial volume of data; |

| | · | develop, test, and apply appropriate rating formulae; |

| | · | closely monitor changes in trends in a timely fashion; and |

| | · | project both severity and frequency with reasonable accuracy. |

If PPS fails to assess accurately the risks that it assumes or does not accurately estimate its retention, it may fail to establish adequate premium rates. Failure to establish adequate premium rates could reduce income and have a materially adverse effect on its operating results or financial condition. Moreover, there is inherent uncertainty in the process of establishing property and casualty loss reserves. Reserves are estimates based on actuarial and statistical projections at a given point in time of what PPS ultimately expects to pay out on claims and the cost of adjusting those claims, based on the facts and circumstances then known. Factors affecting these projections include, among others, changes in medical costs, repair costs, and regulation. Any negative effect on PPS could have a material adverse effect on our results of operations and financial condition.

We are facing increased competition that may impede our growth.

BCP has experienced increased competition, including increased pressure on margins. This is primarily a result of the presence of the following:

| | · | Highly liquid commercial banks in the market; |

| | · | Local and foreign investment banks with substantial capital, technology, and marketing resources; and |

| | · | Local pension funds that lend to BCP’s corporate customers through participation in those customers’ securities issues. |

Larger Peruvian companies have gained access to new sources of capital, through local and international capital markets, and BCP’s existing and new competitors have increasingly made inroads into the higher margin, middle market, and retail banking sectors. Such increased competition, with entrants who may have greater access to capital at lower costs, has affected BCP’s loan growth as well as reduced the average interest rates that BCP can charge its customers.

Competitors may also appropriate greater resources and be more successful in the development of technologically advanced products and services that may compete directly with BCP’s products and services. Such competition would adversely affect the acceptance of BCP’s products and/or lead to adverse changes in spending and saving habits of BCP’s customer base. If competing entities are successful in developing products and services that are more effective or less costly than the products and services developed by BCP, BCP’s products and services may be unable to compete successfully. Even if BCP’s products and services prove to be more effective than those developed by other entities, such other entities may be more successful in marketing their products and services than BCP because of their greater financial resources, higher sales and marketing capacity, and other factors. BCP may not be able to maintain its market share if it is not able to match its competitors’ loan pricing or keep pace with their development of new products and services. Any negative impact on BCP could have a materially adverse effect on our results of operations and financial condition.

Fluctuation and volatility of capital markets and interest rates may decrease our net income.

We may suffer losses related to the investments by BCP, ASCH, PPS, Grupo Crédito and other subsidiaries in fixed income and equity securities, and to their respective positions in currency markets, because of changes in market prices, defaults, fluctuations in market interest rates or exchange rates or other reasons. A downturn in the capital markets may lead us to register net losses due to the decline in the value of these positions. Additionally, a downturn in the capital markets could lead to negative net revenues from trading positions caused by volatility in prices in the financial markets, even in the absence of a general economic downturn.

Fluctuations in market interest rates, or changes in the relative structure between short-term interest rates and long-term interest rates, could cause a decrease in interest rates charged on interest-earning assets, relative to interest rates paid on interest-bearing liabilities. Such an occurrence could adversely affect our financial condition by causing a decrease in net interest income.

| ITEM 4. | INFORMATION ON THE COMPANY |

| (A) | History and Development of the Company |

We are a limited liability company that was incorporated in Bermuda on October 20, 1995 to act as a holding company, coordinate the policy and administration of our subsidiaries, and engage in investing activities. Our principal activity is to coordinate and manage the business plans of our subsidiaries in an effort to implement universal banking services and develop our insurance business, focusing on Peru and Bolivia along with limited investments in other countries of the region. We conduct our financial services business exclusively through our subsidiaries. Our registered address is Clarendon House, 2 Church Street, Bermuda. The management and administrative office (i.e., principal place of business) in Peru of our subsidiary, Banco de Crédito del Perú, is Calle Centenario 156, La Molina, Lima 12, Peru, and the phone number is 51-1-313-2000.

We are the largest financial services holding company in Peru and are closely identified with our principal subsidiary, BCP, the country’s largest bank and the leading supplier of integrated financial services in Peru. We are engaged principally in commercial banking (including trade finance, corporate finance and leasing services), insurance (including commercial property, transportation and marine hull, automobile, life, health and pension fund underwriting insurance) and investment banking (including brokerage, trust, custody and securitization services, asset management and proprietary trading and investment). As of December 31, 2008, our total assets were US$20.8 billion and our net equity was US$1.8 billion. Our net income attributable to our equity holders in 2007 and 2008 was US$350.7 million and US$357.8 million, respectively. See “Item 3. Key Information—(A) Selected Financial Data” and “Item 5. Operating and Financial Review and Prospects.” The following table gives certain financial information about us by principal business segments as of and for the year ended December 31, 2008 (See Note 26 to the Credicorp Consolidated Financial Statements):

| | | As of and for the Year ended December 31, 2008 | |

| | | | | | | | | | |

| | | (U.S. Dollars in millions) | |

| Commercial Banking | | US$ | 1,797 | | | US$ | 804 | | | US$ | 19,168 | |

| Insurance | | | 469 | | | | 118 | | | | 1,231 | |

| Pension Fund Administration | | | 71 | | | | 0 | | | | 224 | |

| Investment Banking and others | | | 50 | | | | (47 | ) | | | 198 | |

| Credicorp | | US$ | 2,387 | | | US$ | 875 | | | US$ | 20,821 | |

We conduct our commercial banking and investment banking activities primarily through BCP, the largest (in terms of total assets, loans, deposits, net equity and net income) full-service Peruvian commercial bank, and ASHC, a diversified financial services company. We conduct our pension fund business through Prima AFP and our insurance activities through PPS, which is the second largest Peruvian insurance company in terms of premiums, fees and net income. You should note that the term “Peruvian commercial bank,” “Peruvian insurance company” and other similar terms used in this Annual Report do not include the assets, results or operations of any foreign parent company or foreign subsidiary of such Peruvian company.

We were formed in 1995 for the purpose of acquiring, through an exchange offer, the common shares of BCP, ASHC and PPS. Pursuant to this exchange offer, in October 1995 we acquired 90.1% of BCP, 98.2% of ASHC and 75.8% of PPS. We acquired the remaining 1.8% outstanding shares of ASHC in March 1996, pursuant to another exchange offer. See “Item 4. Information on the Company—(C) Organizational Structure.”

In December 1995, we purchased 99.99% of Inversiones Crédito (whose name has changed to Grupo de Crédito), a non-financial entity with assets of US$335.9 million as of December 2008. Grupo de Crédito’s main subsidiary is Prima AFP.

In August 1997, we acquired 39.5% of BCB from BCP for US$9.2 million. In July 1998, we acquired 94.86% of Banco de La Paz, a Bolivian bank with US$52.1 million in assets, which we subsequently merged with BCB in January 1999. During this time, we also increased our beneficial ownership in BCB to 55.79%, which left BCP with ownership of the remaining 44.21%. In November 2001, however, BCP bought back 55.53% of our interest in BCB for US$31.5 million. As of December 31, 2008, BCB operated 63 branches and 181 ATMs located throughout Bolivia. BCB’s results have been consolidated in the BCP financial statements since the date of its acquisition by BCP in November 1993.

In March 2002, we made a tender offer for outstanding BCP shares for S/.1.80 per share, approximately equal to the book value of such shares, disbursing directly and through our subsidiary PPS an amount of approximately US$35.3 million. As a result of the tender offer, our equity stake in BCP increased from 90.6% to 97.0% (including shares held by PPS).

In December 2002, BCP acquired Banco Santander Central Hispano-Perú, or BSCH-Perú, for US$50.0 million. Since that date, BSCH-Perú has been included in BCP’s consolidated financial statements. On December 31, 2002, BSCH-Perú had total assets of US$975.2 million, total loans of US$719.4 million and deposits of US$659.0 million. BSCH-Perú was merged into BCP on February 28, 2003.

In March 2003, BCP added to its 55% stake by acquiring for US$17.0 million the remaining 45% of the equity shares of Solución Financiera de Crédito del Perú S.A. (or Solución) from Banco de Crédito e Inversiones de Chile (or BCI) and other foreign shareholders. As a result, Solución once again became a BCP wholly-owned subsidiary. In March 2004, substantially all of Solución’s assets and liabilities were absorbed into BCP’s Peruvian banking operations. Solución’s net income in 2003 was US$7.6 million, and it had, as of February 28, 2004, a loan portfolio of US$88.4 million, with a 3.0% past-due ratio.

In 2003, BCP converted Banco de Crédito Overseas Limited, or BCOL, its offshore bank in the Bahamas, into a vehicle to conduct investments and sold it to ASHC. ASHC then consolidated BCOL into its operations during 2004. In accordance with our policy regarding holdings of equity interests in non-financial companies, we then caused certain long-term equity interests that were previously held by BCOL to be transferred to BCP and then in turn transferred to Grupo Crédito. In April 2004, PPS sold substantially all of its holdings of our equity shares to ASHC (see “Item 7. Major Shareholders and Related Party Transactions—(A) Major Shareholders”).

In March 2004, PPS acquired 100% of Novasalud Perú S.A. – Entidad Prestadora de Salud, or Novasalud EPS, which is one of three private health insurance providers in Peru, for US$6.5 million. PPS then merged Novasalud EPS with Pacífico S.A. Entidad Prestadora de Salud (or Pacífico Salud), a subsidiary of PPS.

In 1997, we acquired Banco Tequendama, a Colombian banking enterprise. In 2002, we sold Banco Tequendama’s Venezuelan branches. In March 2005, we then sold Banco Tequendama to a Colombian bank. While this sale was publicly announced in October 2004 and became effective on January 1, 2005, it was not completed until March 2005 after all required approvals were obtained from the Colombian authorities. We did not record any significant gain as a result of this transaction.

In January 2005, BCP and Bank of America (the principal shareholder of Fleet Boston N.A.) agreed to engage in a buy-sale transaction of the loan portfolio of the Peruvian branch of Bank Boston N.A. BCP paid approximately US$353.8 million in cash for the loan portfolio, which included commercial loans, mortgage and leasing operations. The transaction was recorded at acquisition cost.

In February 2005, we were authorized by Peruvian regulatory authorities to establish Prima AFP, of which Grupo Crédito is the main shareholder. Prima AFP started operations in August 2005.

In August 2006, Prima AFP acquired Unión Vida AFP, which is a pension fund operating in the Peruvian market. Prima AFP’s acquisition of Unión Vida AFP, which was formerly held by Grupo Santander Perú S.A., was a strategic move toward consolidation as part of its efforts to gain a leading position in the pension fund market. This acquisition enabled Prima AFP to position itself as the second ranking company in market share terms (affiliates and assets under management), with the second highest returns and the lowest commission for affiliates (who invest a portion of their salary each month). The merger between Prima AFP and Unión Vida AFP was consummated in December 2006.

In 2006, Prima AFP incurred significant merger expenses relative to its size, reaching the end of the year with losses of US$20.7 million. However, Prima AFP had a net income of US$11.2 million during 2008, with 1,045,410 affiliates and funds under management of US$4,865 million.

In November 2006, we bought PPS’s remaining 1.02% of BCP shares, generating goodwill with respect to the minority interest acquired we acquired (0.25%) of approximately US$7.2 million.

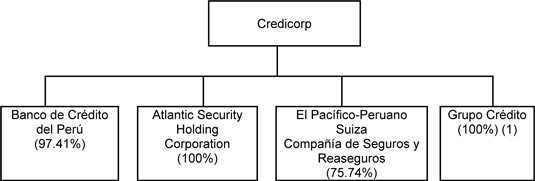

The following tables show our organization and the organization of our principal subsidiaries as of December 31, 2008 and their relative percentage contribution to our total assets, total revenues, net income and net equity at the same date (see “—(C) Organizational Structure”):

| | | As of and for the Year ended December 31, 2008 (1) | |

| | | Total Assets | | | Total Revenue | | | Net Income (Loss) | | | Net Equity | |

| Banco de Crédito del Perú | | | 87.3 | % | | | 75.1 | % | | | 117.9 | % | | | 80.6 | % |

| Atlantic Security Holding Corporation | | | 4.9 | % | | | 1.1 | % | | | -14.1 | % | | | 5.5 | % |

| El Pacífico-Peruano Suiza Compañía de Seguros y Reaseguros (2) | | | 5.9 | % | | | 20.4 | % | | | -5.9 | % | | | 4.3 | % |

| Grupo Crédito (3) | | | 1.5 | % | | | 3.4 | % | | | 5.2 | % | | | 13.9 | % |

| Others (4) | | | 0.4 | % | | | 0.0 | % | | | -3.1 | % | | | -4.3 | % |

| (1) | Percentages determined based on the Credicorp Consolidated Financial Statements. |

| (2) | Includes PPS and Pacífico Vida. |

| (3) | Includes Prima AFP and others. |

| (4) | Includes Credicorp Ltd., CCR Inc., Credicorp Securities Inc. and others. |

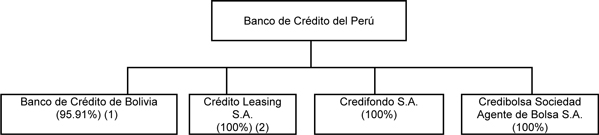

The following tables show the organization of BCP and its principal subsidiaries as of December 31, 2008:

| | | As of and for the Year ended December 31, 2008 (3) | |

| | | Total Assets | | | Total Revenue | | | Net Income (Loss) | | | Net Equity | |

| Banco de Crédito del Perú | | | 93.0 | % | | | 89.9 | % | | | 85.5 | % | | | 84.3 | % |

| Banco de Crédito de Bolivia | | | 5.0 | % | | | 6.6 | % | | | 10.1 | % | | | 8.1 | % |

| Crédito Leasing S.A. | | | 1.3 | % | | | 1.5 | % | | | 0.2 | % | | | 1.7 | % |

| Financiera de Crédito Solución | | | 0.2 | % | | | 0.2 | % | | | 0.0 | % | | | 0.6 | % |

| Credifondo S.A. | | | 0.1 | % | | | 1.2 | % | | | 2.0 | % | | | 1.9 | % |

| Credibolsa Sociedad Agente de Bolsa S.A. | | | 0.1 | % | | | 0.4 | % | | | 0.9 | % | | | 0.9 | % |

| Others (4) | | | 0.3 | % | | | 0.2 | % | | | 1.3 | % | | | 2.5 | % |

| (1) | Credicorp holds an additional 4.08% stake. |

| (2) | It will be absorbed by BCP on July 1, 2009. |

| (3) | Percentages determined based on BCP’s consolidated financial statements as of and for the year ended December 31, 2008. |

| (4) | Includes Creditítulos S.A., Inmobiliaria BCP and others. |

(1) Introduction – Review of 2008

General

Despite the existence of an international financial crisis, in 2008 we recorded net income after minority interests of US$357.8 million, which was 2.0% higher than our net earnings in 2007. We incurred charges of US$181.6 million, which included: (i) US$60.4 million to impair a deteriorated investment portfolio caused by declining stock prices; (ii) US$36.4 million for a provision by ASHC for potential losses and contingencies related to an ASHC-managed fund that had invested with Bernard L. Madoff Investment Securities LLC, or Madoff Securities, on behalf of its clients; (iii) US$67.1 million of expense to hedge SARs Program, and (iv) US$17.7 million from an exchange loss caused by the depreciation of the Nuevo Sol against the U.S. Dollar.

We have addressed these losses by the following:

| | · | In accordance with our approach toward provisions for market-related value adjustments in our investment portfolio, we made a large provision against our deteriorated investment portfolio that we considered sufficient for the financial year 2008. |

| | · | We implemented tighter and more conservative asset management and investment policies to avoid third party risks, such as those associated with the Madoff Securities. |

| | · | We are introducing a modification of the SAR program to minimize the need for variations in provisions related to the program. We are making this modification because the SAR program has generated income volatility due to an imperfect hedge that has caused fluctuations in provisions, which has been intensified by the recent high volatility of our stock. |

| | · | We gradually reduced our exposure to the volatility of the Nuevo Sol by the end of the first quarter of 2009 by exchanging higher yielding Nuevos Soles-denominated government instruments to investments in U.S. Dollars. |

BCP’s banking business remained strong and profitable in 2008, showing significant resilience to the international financial crisis. Our performance in the asset management business through Prima AFP yielded positive results as the income generation trend continued upwards.

ASHC’s private banking business asset management revenues, however, were negatively impacted by the global financial crisis due to unrealized losses from asset market valuations. Likewise, our results were negatively affected by the insurance business due to high casualties and the restructuring of our insurance business’s risk portfolio which led to an increased emphasis on the mass retail insurance business and a decreased emphasis on lower corporate risk holdings. Despite these negative impacts, however, we experienced growth and generation of revenue.

Our total assets grew to US$20.8 billion as of December 31, 2008, a 17.6% increase from the US$17.7 billion as of December 31, 2007, as a result of strong growth (22.9%) in deposits that supported the expansion of our loan business. Loans grew by 27.8% in 2008 (compared to 39.2% in 2007, 18.2% in 2006) following the progress of the Peruvian economy (which had GDP growth rate of 9.8% in 2008). As part of our provision policy, provision for loan losses net of recoveries increased by 71.5% to US$48.8 million (compared to US$28.4 million in 2007). Our past-due loans ratio of 0.79% at the end of 2008 was consistent with that of 2007 (0.75%) and had a coverage ratio of 270.7% (i.e., reserves for loans as a percentage of past-due loans). Finally, our return on average net equity decreased slightly yet remained at a profitable level of 20.2% in 2008 (compared to 22.7% in 2007).

BCP

In 2008, we received an earnings contribution of US$410.9 million resulting from BCP’s year-end 2008 net profit that totaled US$423.5 million. This earnings contribution was 27.4% larger as compared to last year’s profits (US$322.5 million). Despite the present financial environment, BCP set a new record for earnings in 2008 and continued on its average annual growth trend of 38.2% since 2004. As a result, BCP’s average return on net equity (ROE) improved to 32.8%, which is above the Peruvian financial system’s average (31.1%).

The main drivers behind BCP’s performance were: (i) solid growth in net interest income resulting from significant loan portfolio expansion across all segments and products, (ii) a considerable increase in non-financial income derived from the raise of fees and commissions as well as higher gains on foreign exchange transactions and on sales of securities and (iii) expansion of its network with an appropriate expenditure control.

The significant growth of BCP total assets (22.1%) was a result of the expansion of its loan portfolio by 28.1% (which totaled US$10.2 billion), whose participation in total assets increased from 43.6% in 2007 to 55.9% by the end of 2008. BCP’s total past-due loans reached US$82.1 million (36.1% higher than the US$60.3 million registered in 2007) while refinanced and restructured loans decreased by 37.6%, from US$88.5 million in 2007 to US$55.2 million at the end of 2008. The composition of BCP’s loan portfolio did not change significantly—wholesale banking and retail banking accounted for 62% and 38% of its total portfolio, respectively (similar to the levels registered in 2007 (63% and 37%)).

The average daily balances of BCP’s corporate and middle market banking loans grew significantly, by 40.6% and 30.2%, respectively, from 2007. This growth was driven by expanding domestic demand along with dynamic business at all levels (sector, industry, region and segments). As a result, BCP continued to lead the Peruvian financial system with a market share of 48.1% for the corporate segment and 37.1% for the middle market.

BCP’s retail banking portfolio continued its success and grew 42.9% in 2008, reaching an average daily balance of US$3,390. In terms of growth and yields, BCP’s consumer loans were the best performing product, reaching 72% growth (measured in average daily balances) to a total volume of US$618 million, followed by loans to small companies which grew 54% to US$1,127 million. Credit cards grew 36%, reaching US$384 million, while mortgage credits expanded 27%, totaling US$1,260 million.

In 2008, BCP also restructured all of its other liquid assets. This was reflected by BCP’s share of available funds, such as cash over total assets, which rose from 15.3% to 19.3%. This increase was result of the Central Bank’s policy against inflation through increased reserve requirements during the first nine months of 2008, and a deepening international crisis in the closing quarter during which BCP increased liquidity as a precautionary measure. BCP’s investment portfolio increased 0.4% in 2008 and held positions in conservative, highly liquid and safe instruments, such as BCR certificates of deposit.

On the liabilities side, BCP’s deposits reached US$14,235 million on December 31, 2008 (a 27.3% increase from the previous year). This increase in deposits not only continues to reinforce BCP’s funding structure as deposits account for 84.2% of all funding sources, but also serves to strengthen BCP’s market share (which is 38.5%). Demand deposits experienced the fastest growth at 36.7%, while time and savings deposits grew 25.9% and 24.7%, respectively. Severance Accounts, or CTS, expanded a moderate 16% due to increased market competition and customer sensitivity to interest earned on such deposits. Furthermore, in 2008, BCP, through a special vehicle, CCR Inc. (which was consolidated into Credicorp), issued (i) US$300 million of securitized structured bonds, which were deposited in its Panamanian branch, and (ii) US$410 million of syndicated senior loan facility.

BCP has conservative provisioning and long-term risk management policies, keeping its coverage ratio above the average ratio in the Peruvian banking system. In 2008, however, this ratio decreased from the previous year (351.8% as compared to 271.9%). Total cumulative provisions reached US$223.2 million, which is 6.3% higher from the previous year.

In 2008, BCP focused its strategy on strengthening its customer service, which is related to its goal of providing improved customer access to the financial system and thereby increasing its penetration into the market. In following its network expansion plan, BCP opened 57 additional branches (58.3% more than 2007) by the end of 2008, further strengthening its market position. BCP also opened 142 new ATMs in 2008 (for a total of 890 ATMs), while its Agente BCP grew significantly by adding 630 agents (for a total of 1,851 agents as of December 2008). As a result of its strategy, BCP’s average number of transactions in 2008 increased 22.1% from 2007 and its transactional business was therefore able to originate higher income for fees and commissions.

As a result of strong growth in its branch network, BCP’s operating expenses increased 12%. This increase is largely attributed to higher personnel expenses as more employees were hired (15,971 at the end of 2008 as compared to 12,667 in 2007), and to increased general and administrative expenses due mainly to marketing campaigns and IT growth. Nevertheless, an increase of 29.9% in operating income offset the higher operating expenses and BCP’s efficiency ratio thereby reached 50.3% (which was lower than its 2007 ratio of 51.3%).

Overall, BCP’s results exceeded forecasts and contributed to our achievements and increased profitability.

BCP Bolivia

In 2008, Banco de Crédito de Bolivia, or BCP Bolivia, obtained a net profit of US$44.5 million, which was 64.5% higher than its 2007 results of US$27 million. BCP Bolivia’s 2008 results were due in part to the strong performance of high return business segments, such as consolidated markets (businesses larger than the small business segment but that do not qualify for the wholesale segment) which grew 77.2%, and the small business segment which expanded its loan portfolio by 42.7%. The performance in these segments resulted in increased diversification growth in BCP Bolivia’s retail banking portfolio.

BCP Bolivia remained as one of the top banks in Bolivia in 2008, posting better results in the following categories as compared to the averages in the Bolivian banking system: 39.9% return on equity, 2.0% past-due loan ratio and 230.6% coverage ratio (as compared to 20.7%, 4.8% and 144.3%, respectively).

BCP Bolivia’s loan portfolio expanded by 2.8% from year-end 2007 totaling US$472.6 million at year-end 2008. This expansion was mainly due to a 17.8% growth in retail banking, which compensated for its 9.6% contraction in wholesale banking.

Although BCP Bolivia increased its positive contribution to our results in 2008, the country of Bolivia still experiences a volatile political environment and shows evidence of significant stagnation in investment activity.

ASHC

Of all our subsidiaries, ASHC experienced the worst effects of the global financial crisis. In 2008, ASHC recorded a US$22.4 million loss, which gave us a negative contribution of US$50.4 million after our dividend revenues were canceled as part of our consolidation of financial statements. This negative performance by ASHC was caused mainly by (i) a large impairment charge required for ASHC’s portfolio of investment securities due to a decline in the capital markets and (ii) by a provision for potential losses and contingencies related to the alleged Madoff fraud.

As a result of these non-recurring and extraordinary events, ASHC’s total assets contracted by 10%, resulting in total assets of US$1,454.2 million at year-end 2008 (as compared to US$1,615.7 million at year-end 2007). Also, third party assets under management decreased 26.8% from US$2,241.8 million at year-end 2007 to US$1,639.3 million at year-end 2008, and deposits dropped 8.1% to US$1,283.6 million as of December 31, 2008. Nevertheless, ASHC’s loan portfolio expanded 54.8% during 2008 with a 0.0% NPL ratio.

In 2009, although ASHC will not modify its low-risk proprietary investment strategy, we expect an increase in ASHC’s financial margin as a direct consequence of widening credit spreads. We expect ASHC’s asset management business to take advantage of the fact that, in spite of the market conditions of 2008, it still achieved adequate returns for its customers. ASHC aims to improve its 2008 results in order to continue to give us a positive contribution.

PPS

In 2008, PPS, which encompasses Pacífico Seguros, Pacífico Vida and Pacífico Salud EPS, reported a net loss of US$15.0 million (compared to a US$12.5 million net earnings in 2007). Although PPS’s net earned premiums grew 32% from 2007, its claims rose by 43.3% which caused its earnings of US$15.5 million in 2007 to turn to losses of US$7.7 million in 2008. Additionally, PPS recorded US$11.3 million as an impairment and US$3.4 million as a translation loss (which was attributable to the devaluation of the Nuevo Sol against the U.S. Dollar). As a result, the contribution we received from PPS dropped considerably, from earnings of US$9.4 million in 2007 to a loss of US$15.9 million in 2008. Nevertheless, PPS maintains its position as one of the primary insurance groups in Peru with a combined market share of 34.4% for the general insurance, health insurance and life insurance segments.

PPS completed its restructuring plan that started in 2006 and achieved a reduction in retained premiums in its high risk property and casualty segment from 51.9% in 2007 to 35% in 2008. Additionally, PPS’s premiums from the retail business increased as a percentage of total premiums, rising from 38% in 2006 to 47% in 2008.

In 2009, PPS will continue to focus on its retail business by developing products to introduce customers to the advantages of insurance. There is enormous potential growth in Peru’s insurance industry given the industry’s weak market penetration. Efficiency and risk management will continue to be main indicators in measuring PPS’s performance. Efficiently utilizing the BCP network is an essential component of PPS’s growth strategy for 2009 since capitalizing on synergies between the insurance business and the distribution channels of the banking business may lead PPS to greater penetration in the insurance industry.

Prima AFP

Peruvian pension funds experienced a difficult year in 2008. The international financial crisis caused a combined negative yield of 20.4% for the three types of funds managed by AFPs. Nevertheless, Prima AFP was able to continue to strengthen its position by adjusting its processes and organization to provide high-quality services and timely and transparent information to its clients. As a result, the contribution we received from Prima AFP in 2008 reached US$11.2 million, as compared to US$3.0 million in 2007.

Prima AFP assets under management decreased 24.1% from US$6.4 billion at year-end 2007 to US$4.9 billion as of December 31, 2008. By year-end 2008, Prima AFP’s share of total funds under management reached 30.6%, slightly lower than 31.4% at year-end 2007, ranking Prima AFP as the second largest fund management company in the sector.

Prima AFP’s revenues in 2008 reached US$70.7 million, an increase of 23.1% from 2007, as a result of a stable and improved portfolio of contributing members that was supported by a growing Peruvian labor market. These revenues, however, were partially offset by the increase of 15.8% in operating expenses.

In 2009, Prima AFP plans to maximize its contribution to us by focusing on strengthening its affiliate base, preserving its existing client portfolio through providing pension and investment counseling, and controlling operating expenses.

The following table sets forth the contribution to the consolidated net income attributable to our equity holders by each of our principal subsidiaries:

| | | 2006 | | | 2007 | | 2008 | | | Variation 2008/2007 | |

| | | (U.S. Dollars in millions, except percentages) | |

| BCP (1) | | | 238.9 | | | | 322.5 | | | | 410.9 | | | | 27 | % |

| ASCH | | | 15.4 | | | | 20.5 | | | | (50.4 | ) | | | -345 | % |

| PPS | | | 14.5 | | | | 9.4 | | | | (15.9 | ) | | | -269 | % |

| Grupo Crédito (2) | | | (38.8 | ) | | | (1.7 | ) | | | 13.2 | | | | 876 | % |

| Total | | | 230.0 | | | | 350.7 | | | | 357.8 | | | | 2 | % |

| (1) | Includes Banco de Crédito de Bolivia, which contributed US$42.9 million in 2008, US$27.0 million in 2007, and US$14.1 million in 2006. |

| (2) | Includes Prima AFP (which recorded a net income of US$11.2 million in 2008, US$3.0 million in 2007 and losses of US$20.7 million in 2006), Credicorp Securities, Credicorp Ltd. (which mainly includes expenses and the tax withheld in connection with the estimation of the dividends to be distributed to us by our Peruvian subsidiaries (BCP and PPS)) and others. |

(2) Strategy

Credicorp was established to create a financial group that would benefit from the synergies among the group’s companies and would become a leader within each business market in which the companies operate. In moving steadily toward achieving these strategic goals, we have become a leading financial group. However, we do not operate in a static environment and 2008 has demonstrated how quickly and dramatically the world can change.

Our greatest challenge is to adapt to these changes without losing focus of our goals. The financial crisis that peaked in 2008 and its effect on economies throughout the world will continue in 2009. Although its effect on us was not significant compared to other companies, the crisis has led us to more closely scrutinize each of the strategic decisions that shape our business.

In reviewing our strategic decisions, we re-formulated our basic strategy to focus on identifying synergies that will increase our efficiencies. This strategy involves greater integration to improve the management of our companies by more extensively sharing our talents, intelligence and experience.

In 2009, through greater interaction in the decision-making process, we will seek to capitalize our synergies by aligning the individual interests of each of our companies with our overall objectives. Additionally, we will take into account the capacities available throughout the entire organization when making decisions about achieving the objectives of an individual company. Furthermore, we have incorporated sustainability into our objectives as the financial crisis has once again demonstrated the need to build a business that can be sustained over time.

The strength of our businesses has been built on the foundation of an organization with a long tradition, deep-rooted culture of customer service, and true commitment to developing our country’s economy and markets. Consequently, we believe we must:

| | · | Focus on our core traditional banking business, on the development of our insurance business and on responsible asset management; |

| | · | Place our customers’ interests first by preserving and investing our assets conservatively and by providing innovative products that meet our customers’ needs; and |

| | · | Contribute to developing Peru’s financial system by increasing bank penetration, increasing product accessibility, and introducing insurance to additional customers while keeping it affordable. |

We are convinced that our 2008 results confirm that we are moving toward accomplishing our objectives. For this reason, many of our strategic steps for 2009 are focused not only on business segments experiencing the largest growth but also improving our own decision-making processes and designing strategies to better consolidate information, capabilities and strengths shared between our companies.

The following is a description of the specific strategies employed by our various businesses:

Banking Business

| | · | Banco de Crédito del Perú – BCP |

| | · | Banco de Crédito – BCP Bolivia |

| | · | Atlantic Security Bank – ASB |

The main objective of our banking business strategy is to accomplish sustainable and highly profitable growth. We can accomplish this objective by greater bank penetration, responding to our customer’s needs, increasing efficiency, and global and comprehensive risk management, which require focusing on:

| | · | Designing innovative products that meet our customers’ needs; |

| | · | Improving risk management and more quickly assessing risk while we incorporate the four types of risk—credit, market, operational and reputational risk; |

| | · | Reviewing and streamlining our operative processes; and |

| | · | Improving our distribution model to offer greater value added through our different distribution channels and automated transactional services. |

Through these initiatives, we expect to accomplish higher efficiencies and grow actively but profitably. This strategy, while applied to all three entities, may vary slightly with each entity. For BCP Bolivia, our strategy also includes reconciling its interests with those of the Bolivian nation as well as adapting the above initiatives to a less dynamic market. With respect to ASB, as a consequence of global financial crisis, we must reestablish its customers’ trust in the investment markets and in our own asset management capabilities.

Insurance Business

Our strategy in the insurance business includes being more selective in our risk retention in the general corporate insurance market, given the mismatch between insured levels and our ability to underwrite and/or absorb such risk. Although fully implementing this strategy will require time, we have already started to see its positive effects.

Given the enormous potential in the retail insurance business due to the industry’s low penetration into the general public, we also focused on PPS’s retail business by developing products that will introduce customers to the advantages of insurance.

The strategies described above for the banking business that focus on growth, efficiency and risk management apply as well to PPS and its life and health insurance business. In addition, the strategy of capitalizing synergies is of great importance in the insurance business as a result of the insurance business’s considerable potential to benefit from the distribution channels of the banking business in selling insurance products, which may also lead to greater market penetration. Consequently, the efficient use of the BCP network through greater integration and alignment of objectives between the two companies is an essential component of PPS’s growth strategy and will receive special attention in 2009.

Asset Management Business

| | · | Atlantic Security Holding Corporation – ASHC |