|

Fourth Quarter and Year End 2013 Results

Lima, Perú, February 05, 2013 -Credicorp (NYSE:BAP) announced today its unaudited results for the fourth quarter and year- end of 2013. These results are reported on a consolidated basis in accordance with IFRS in nominal US Dollars.

HIGHLIGHTS

·Despite good business evolution and a stable exchange rate this 4Q13, reported results were hurt by extraordinary one-off expenses and came in 15.5% lower than the previous Q’s at US$ 152 million. This, in addition to results reported for the first half of the year, which were marked by the strong currency & market volatility and translation losses, resulted in total net income reported by Credicorp for the year 2013 of US$ 567.1 million, 28.1% lower than the previous year’s.

·However, operational trends and income generation for the 4Q as well as for the year as a whole were significantly better than reported numbers suggest. Net interest income was up 4.7%, but was affected by a newly introduced IFRS valuation for derivatives, that resulted in an adjustment of -US$ 7 million, and led to 3.2% reported growth this 4Q. Non-financial income also showed solid results and was 5.6% higher QoQ reflecting the good business development. Furthermore, even though provisions kept expanding, as a result of the higher PDLs in the SME and Credit Cards portfolios, and increased 5.6% this Q, net interest income after provisions was still up 2% QoQ.

·Operating results for the year, in reported US Dollar terms, show net interest income after provisions for the year also expanded 11%, despite the portfolio quality issues throughout the year. Non-financial income on the other hand, reflects the lower gains in the sale of securities this period given the drop in fixed income valuations experienced in the year, and grew only 4% YoY.

·Growth of average daily balances recorded by currency shows that the Nuevos Soles portfolio expanded by a robust 8.9% QoQ, while the US Dollar portfolio reflected growth of only 0.6% as the shift to local currency borrowings gained momentum. This trend was evident in the Wholesale Banking book, which grew 21.2% QoQ in Nuevos Soles denominated loans, and only 0.2% in US Dollar loans, an evolution that shows a further de-dollarization of the Wholesale Banking portfolio. Consolidated portfolio growth reported in US Dollar terms reached 4.5% for the Q.

·For the year, growth of Nuevos Soles average daily balances was up an impressive 32.7%, with significant growth concentration in the Wholesale Banking book in local currency which grew 64%, whereas the US Dollar average daily balances only expanded 3.1%, resulting in a blended growth rate in constant currencies of about 17% for the year.

·NIMs improved another 10bps this Q and reached 5.2% for the global NIM on total average Interest Earning Assets (IEA) and up 5bps to 8.4% for NIM on loans. For the year, Credicorp added a total of 24bps to its NIM. This was the result of a re-composition of IEA in favor of higher yielding loans, lower funding costs and the corrections in the models of the Retail Banking book which included a more efficient pricing tool that led to overall price increases.

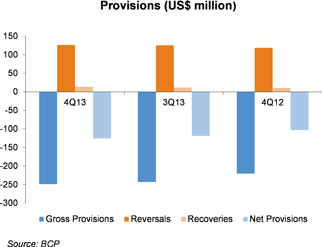

·In line with the expected maturing cycle of the delinquent portfolio, the PDL ratio deteriorated only another 5 bps to reach 2.3% and complete a deterioration of 50 bps for the whole year. However, provisions related to the deterioration of the portfolio were up 5.6% in 4Q, which contributed to a 20% YoY aggregate increase in provisions, but was well compensated by better margins.

·The performance of the insurance business deteriorated this 4Q reporting technical results 3.1% lower as the business volumes dropped due to the loss of a very profitable business in the Life Insurance segment associated with newly introduced auctions for pension fund related insurance, and a one-off adjustment in new regulatory provisions. This 4Q results, plus the increased claims in the previous Qs led to a 1.3% drop in underwriting results for 2013.

·Operating expenses were strongly affected by several one-off costs and adjustments booked in the 4Q, which in turn could not escape the seasonal hike of admin-expenses in the last Q of each year, resulting in a 19% increase QoQ, while personnel expenses were down 7% for the Q, leaving an overall moderate increase. However, one-off costs of more than US$ 28.8 million were recorded due to an IFRS impairment related to IM Trust valuation, some social security liabilities for previous years, tax contingencies in Bolivia, and others. For the year, expenses expansion was lower than originally projected but still reached 14.6%. This increase in expenses was larger than income growth in our reporting currency and resulted in a 1.5% deterioration of Credicorp´s efficiency ratio to 43.7%.

·The recent one-off expenses added to the higher cost of risk we faced this year, the valuation losses in the fixed income portfolio in 2Q due to the increase in interest rates in the US market, and the higher claims in the insurance business, led to the 2% lower operating income for the year. However, the large losses on our LC equity position associated with the almost 10% devaluation of the local currency against the US Dollar in the course of 2013, amounted to US$ 148.5 million for the whole year, and were the main items responsible for the significant drop in reported profitability to 13.5% ROAE for 2013 vs. 20.9% ROAE in 2012.

·Consequently, it is truly noteworthy that after making only the most obvious adjustments and without adjusting for the losses in income due to the exchange rate when converting this to US Dollars, recurring net income for Credicorp would reach roughly US$ 738.3 million in 2013 vs.US$ 733.2 million in 2012. |

I. Credicorp Ltd.

Overview

Despite a stable currency which moved only slightly in 4Q and generated limited translation losses, net earnings reported for 4Q were down 15.5% QoQ and reached only US$ 150.4 million. The aspects responsible for this drop were (i) some one-off expenses related to an impairment in the valuation of IM Trust, Social Security payments on remunerations paid in past years due to a regulatory dispute, provisions for tax contingencies in Bolivia, and others, which in aggregate amounted to US$ 28.8 million, (ii) the cost of approximately US$ 5.4 million due to rule changes that set requirements for additional reserves at Pacifico to cover future administrative expenses (Unallocated loss adjustment expense); (iii) a series of adjustments of costs for the year which were booked in a cumulative way in 4Q, such as a Credit Value Adjustment of derivatives for 2013 of US$ 7 million and an adjustment in fee income following a regulatory accounting change that generated a deduction in income of US$ 4 million for the year booked in the Q; and (iv) the seasonal increase in administrative expenses, all of which affected operating income, which drops also 14.8% for the Q.

Compared to the same period of last year, the drop is more dramatic and reached -24.3%. This result, however, was also highly distorted by the large difference in the exchange rates at which earnings are converted to US Dollars. Consequently, ROAE dropped to 14.6% for 4Q from 18% for 3Q and the 20’s levels for the previous year.

Net interest income (NII) expanded 3.2% for the Q, despite the extraordinary adjustment of derivatives valuation throughout the year mentioned above, which reached in aggregate US$ 7 million and was booked in the 4thQ. Excluding this adjustment, real NII growth for 4Q was 4.7%, in line with average daily loan volumes growth. The good evolution of the business and improved pricing also led to higher NIMs (Net Interest Margin), which expanded a few bps to 5.2% for the global NIM and 8.4% for the NIM on the loan book.

The aforementioned portfolio expansion reached a total of 2.7% in Q-end US Dollar terms. However, using BCP’s average daily balances, which are a more pertinent indicator of performance, the expansion reaches a solid 4.5% QoQ and stems from 5.3% growth in average daily balances in the Wholesale Banking book and 3.2% in the Retail Banking book. Furthermore, it is the Nuevo Soles Wholesale Banking portfolio that grew faster at 21.2%, while the Retail Banking portfolio is still in a contained mode and expanded its LC (Local Currency) balances only 4.8%, leading to a total 8.9% loan expansion in LC. In contrast, the FC (Foreign Currency) portfolios posted completely different performance, with a FC Wholesale Banking book that grew 0.4% and a retail FC portfolio that contracted by -0.9%, leading to a total 0.6% expansion for the whole FC denominated book. This is a reflection of a very clear de-dollarization trend and robust activity in the business world.

The Retail Banking book, on the other hand, reflects our conservative approach to risk management, which has kept a lid on growth and resulted in a very modest QoQ Retail Banking book expansion (especially for typically extremely dynamic 4Qs): 2.5% for Pyme, 2.7% for mortgages, which stems from 6.9% in Nuevos Soles and -3.2% in US Dollar, sound 4% expansion in consumer loans and 3.4% in Credit Cards (CC).

Asset quality showed a moderate 6bps deterioration, which stems from the SME and CC businesses. This is in line with expectations since we have not yet seen the peak in delinquencies for the SME portfolio, and a temporary pick-up in CC delinquencies due to a regulatory change on minimum payments. Consequently, provisions increased 5.6% for the Q.

Despite a reversion of fees of about US$ 4 million due to a regulatory accounting change, non-financial income was up 5.6% in 4Q, with fee income improving 5% in the Q. A slight decrease was posted in gains on FX transactions (in line with the lower volatility of the currency), which were compensated by an improvement in other income and stable gains on the sale of securities.

The insurance business posted 7.7% decrease in premium income this 4Q as the Life Division lost its pension funds insurance business following the introduction of a regulatory auctioning process of this insurance coverage. However, total insurance underwriting results were down only 3.1% following some improvement in commissions (some recoveries for non-use of re-insurance policies) and expenses and despite a one-off US$ 5.4 million adjustment for newly introduced regulatory provisions. However, the medical services business had higher expenses and delivered an underwriting result that was 32% lower.

| 2 |

Operating expenses had mixed results, since personnel expenses dropped an important 7% QoQ, but administrative expenses increased almost 19% QoQ resulting in a more moderate growth of total operating expenses. In this 4Q, operating expenses included a significant amount of non-recurring costs as indicated earlier, in addition to the seasonal increase in expenses which was this year still unavoidable. Those non-recurrent expenses included: (i) an IFRS required impairment of about US$ 14.5 million in the valuation of IMTrust, (ii) some Social Security belated payments of US$ 6.8 million related to compensation awarded in previous years due to a claim and dispute with SUNAT (the Peruvian tax authority), (iii) provisions for US$ 2.1 million of tax contingencies in Bolivia related to expected tax increases; and others than sum up to US$ 28.8 million. The aforementioned resulted in a significant increase of operating expenses, which were to a large extent attenuated by lower personnel expenses as we continued controlling headcount and reduced the provisions for 2013 bonuses.

Operating income therefore shows a drop of 14.8%, which led to the 15.5% lower net income reported when adding the Q’s small translation loss.

Consequently, given the absence of any significant distortions related to devaluation of the Nuevo Sol this 4Q, results converted to US Dollars for reporting purposes reflect the good business expansion and income generation of Credicorp, but nonetheless incorporate the impact of the higher cost of risk for the Q (+5.6%), and mainly, the substantial non-recurrent costs, which ultimately were responsible for the drop in ROE to 14.6% for this 4Q13 vs. 18% in 3Q13 and 19.6% in 4Q12.

| Credicorp Ltd. | Quarter | % Change | Year ended | % Change | ||||||||||||||||||||||||||||

| US$ 000 | 4Q13 | 3Q13 | 4Q12 | QoQ | YoY | Dec 13 | Dec 12 | Dec 13 / Dec 12 | ||||||||||||||||||||||||

| Net Interest income | 473,160 | 458,704 | 430,736 | 3.2 | % | 9.8 | % | 1,823,322 | 1,612,126 | 13.1 | % | |||||||||||||||||||||

| Net provisions for loan losses | (125,162 | ) | (118,580 | ) | (102,964 | ) | 5.6 | % | 21.6 | % | (453,562 | ) | (377,841 | ) | 20.0 | % | ||||||||||||||||

| Net interest income after net provisions for loan losses | 347,999 | 340,124 | 327,772 | 2.3 | % | 3.8 | % | 1,369,760 | 1,234,285 | 11.0 | % | |||||||||||||||||||||

| Non financial income | 285,635 | 270,465 | 290,576 | 5.6 | % | -1.7 | % | 1,097,179 | 1,054,788 | 4.0 | % | |||||||||||||||||||||

| Insurance services technical result | 36,879 | 38,055 | 50,894 | -3.1 | % | -27.5 | % | 141,001 | 142,866 | -1.3 | % | |||||||||||||||||||||

| Medical Services Technical Result | 4,656 | 6,927 | 7,538 | -32.8 | % | -38.2 | % | 23,582 | 7,233 | 226.0 | % | |||||||||||||||||||||

| Operating expenses (1) | (452,393 | ) | (393,974 | ) | (438,465 | ) | 14.8 | % | 3.2 | % | (1,666,302 | ) | (1,454,441 | ) | 14.6 | % | ||||||||||||||||

| Operating income (2) | 222,774 | 261,597 | 238,315 | -14.8 | % | -6.5 | % | 965,220 | 984,732 | -2.0 | % | |||||||||||||||||||||

| Core operating income | 251,531 | 261,597 | 238,315 | -14.8 | % | -6.5 | % | 1,055,229 | 984,732 | -2.0 | % | |||||||||||||||||||||

| Non core operating income (expenses) (3) | (28,757 | ) | - | - | - | - | (90,009 | ) | - | - | ||||||||||||||||||||||

| Translation results | (4,792 | ) | (3,312 | ) | 30,475 | 44.7 | % | -115.7 | % | (105,291 | ) | 75,079 | -240.2 | % | ||||||||||||||||||

| Income taxes | (67,595 | ) | (74,757 | ) | (61,585 | ) | -9.6 | % | 9.8 | % | (285,760 | ) | (251,583 | ) | 13.6 | % | ||||||||||||||||

| Net income | 150,387 | 183,528 | 207,204 | -18.1 | % | -27.4 | % | 574,169 | 808,228 | -29.0 | % | |||||||||||||||||||||

| Minority Interest | (1,250 | ) | 4,102 | 7,016 | -130.5 | % | -117.8 | % | 7,091 | 19,449 | -63.5 | % | ||||||||||||||||||||

| Net income attributed to Credicorp | 151,637 | 179,426 | 200,189 | -15.5 | % | -24.3 | % | 567,079 | 788,779 | -28.1 | % | |||||||||||||||||||||

| Net income / share (US$) | 1.90 | 2.25 | 2.51 | -15.5 | % | -24.3 | % | 7.11 | 9.89 | -28.1 | % | |||||||||||||||||||||

| Total loans | 23,003,306 | 22,414,876 | 21,476,520 | 2.6 | % | 7.1 | % | 23,003,306 | 21,476,520 | 7.1 | % | |||||||||||||||||||||

| Deposits and obligations | 24,483,444 | 24,028,000 | 24,050,780 | 1.9 | % | 1.8 | % | 24,483,444 | 24,050,780 | 1.8 | % | |||||||||||||||||||||

| Net shareholders' equity | 4,233,099 | 4,089,916 | 4,167,968 | 3.5 | % | 1.6 | % | 4,233,099 | 4,167,968 | 1.6 | % | |||||||||||||||||||||

| Net interest margin | 5.20 | % | 5.13 | % | 4.96 | % | 5.00 | % | 5.08 | % | ||||||||||||||||||||||

| Efficiency ratio | 45.8 | % | 42.0 | % | 47.9 | % | 43.8 | % | 43.6 | % | ||||||||||||||||||||||

| Return on average shareholders' equity | 14.6 | % | 18.0 | % | 19.6 | % | 13.5 | % | 20.9 | % | ||||||||||||||||||||||

| PDL ratio | 2.24 | % | 2.18 | % | 1.73 | % | 2.24 | % | 1.73 | % | ||||||||||||||||||||||

| PDL over 90 days | 1.53 | % | 1.52 | % | 1.14 | % | 1.53 | % | 1.14 | % | ||||||||||||||||||||||

| NPL ratio (4) | 2.81 | % | 2.76 | % | 2.39 | % | 2.81 | % | 2.39 | % | ||||||||||||||||||||||

| Coverage of PDLs (%) | 157.5 | % | 162.6 | % | 187.7 | % | 157.5 | % | 187.7 | % | ||||||||||||||||||||||

| Coverage of NPLs (%) | 125.1 | % | 128.7 | % | 136.0 | % | 125.1 | % | 136.0 | % | ||||||||||||||||||||||

| Employees | 27,638 | 27,457 | 26,541 | 27,638 | 26,541 | |||||||||||||||||||||||||||

(1) Employees' profit sharing is regisered in Salaries and Employees Benefits since 1Q11 due to local regulator's decision.

(2) Income before translation results and income taxes.

(3) Includes non core operating expenses. 4Q13 figure includes non recurring expenses assocated to SUNAT, provision for contingencies from BCP Bolivia, impairment for valuation of IM Trust, and unallocated loss adjustment expenses. 2013 figure includes aforementioned non recurring expenses and expenses incurred from the sale of BCP Colombia to Credicorp Investments, markdown in value of sovereign bonds and loss in the structural forward valuation.

(4) NPLs: Non-performing loans = Past due loans + Refinanced and restructued loans. NPL Ratio = NPLs / Total loans.

| 3 |

Results 2013 vs. 2012

In 2013, the exchange rate of the Nuevo Sol against the US Dollar experienced volatility at levels we have not seen in the last 20 years. In this context, the Nuevo Sol devaluated 9.6%. Credicorp’s results reflect this volatility, which disguises a significantly better business’s performance.

Based on reported numbers in its functional currency, Credicorp reported net income after minority interest of US$ 567.1 million in 2013, which represents a 29% decline with regard to 2012’s figure (US$ 808.2 million). This led ROAE to drop from 20.9% in 2012 to 13.5% in 2013. In terms of portfolio quality, the Past-Due-Loan (PDL) ratio rose from 1.73% to 2.24%, which was primarily attributable to higher PDL ratios in the SME and Credit Cards as we will discuss later.

Nevertheless, it is important to note that despite aspects of doing business that are beyond our control- such as currency volatility- and which distort final results, operating income only fell 2% with regard to 2012’s, showing the strong income generation capacity given that this figure includes the impact of the devaluation on income denominated in LC but reported in US Dollars.

In fact, operational trends and income generation are significantly better than reported numbers suggest.

The multiple factors that impede a clear view of Credicorp’s performance, which was still robust, and led to an aggregate of losses, extraordinary expenses or charges of US$ 194.4 million, are associated not only with the impact of the devaluation of local currency on our Balance Sheet positions, but also with non-recurring losses due to market issues and non-recurring expenses that complicated transactions this year, and include:

| i) | A translation loss for US$ 105 million that is associated with the portion of equity positioned in LC; |

| ii) | The US$ 43.5 million loss due to the valuation of structural forward contracts, which was also associated with the capital position in LC; |

| iii) | The US$ 11.5 million loss on valuations of investment instruments due to movements in the interest rate relative the US Dollar and BCP’s sovereign bond positions (Peru, Colombia and Brazil); |

| iv) | The cost of approximately US$ 5.4 million due to rule changes that set requirements for additional reserves at Pacifico to cover future administrative expenses (Unallocated loss adjustment expense); |

| v) | Other non-recurring expenses for US$ 28.8 million that are associated with payments to SUNAT and ESSALUD for previous periods; contingent charges in Bolivia; de-recognition of assets associated with system development and installations; and an impairment loss after IM Trust was valuated according to NIIF norms. |

In the first analysis, if we exclude the aforementioned events and the translation gain of 2012, operating income grew 7.1% with respect to 2012’s level (even when 2012’s results included the extraordinary gains generated by sales of securities) and net income also expanded approximately 0.7%. In this scenario, Credicorp’snet recurring income in 2013 was approximatelyUS$ 738.3 million, which compares favorably with 2012’s recurring income (excluding only translation gains after taxes) of US$ 733.2 million.

But it is important to move to the second level of analysis to better appreciate the business’s true performance and eliminate reporting distortions related to moves in the exchange rate. To do this we must look at income and expenses in the currency in which they were generated as indicated in the tables below, which reveal that the evolution was indeed favorable with solid income and good margins.

| 4 |

| % Change LC * | % Change LC | % Change FC | % Total Change | Combined % Total Change | ||||||||||||||||

| BAP | Expressed in PEN 2013 vs. 2012 | Expressed in US$ 2013 vs. 2012 | Expressed in US$ 2013 vs. 2012 | Expressed in US$ 2013 vs. 2012 | Expressed in US$ 2013 vs. 2012 (4) | |||||||||||||||

| Adjusted interest income (1) | 27.8 | % | 16.6 | % | 7.2 | % | 13.7 | % | ||||||||||||

| Adjusted interest expenses (2) | 25.0 | % | 14.1 | % | 11.2 | % | 12.3 | % | ||||||||||||

| Adjusted Net interest income (1)(2)(3) | 28.2 | % | ® | 17.0 | % | + | 2.6 | % | = | 14.2 | % | 24.1 | % | |||||||

| Reported Net interest income | 13.1 | % | ||||||||||||||||||

* Converted at Nuevos Soles at Q-end exchange rate.

(1) Interest income reported - Other income. Other income includes the gain on valuation of derivatives generated by the devaluation of the Nuevo Sol.

(2) Interest expenses reported - Other expenses. Other expenses includes the loss in valuation of derivatives linked to the loss in structural forward contracts for US$ 32.9 million in 2Q13 and US$ 11.7 million in 1Q13.

(3) 84.1% of adjusted Net interest income is generated in local currency.

(4) Calculated by adding up the weighted % change of each currency.

As such, the adjusted NII in LC, which represents 84.1% of total NII, grew 28.2% YoY while the adjusted NII denominated in US dollars reported a very modest 2.6% increase. All of the aforementioned was attributable to the excellent evolution of the loan portfolio, which when measured in BCP’s average daily balances, indicates growth of 32.7% in LC and 3.1% in FC.

In this context Credicorp’s NII, without including the distorting effect of devaluation, reported a risk-weighted increase of approximately 24% YoY, which is significantly higher than the 13.1% growth reported in US Dollars. This coincides with the real weighted growth of approximately 17.3% in the loan portfolio (BCP’s portfolio, Credicorp’s main asset) and is further evidence that margins have improved due to the Bank’s focus on growing income rather than the portfolio, and thanks to a migration of funds to the local currency portfolio and interest rate increases.

Moreover, despite the significant increase in provisions in 2013 (+20%), NII after provisions also grew 11%. This is proof that the Bank’s move to correct prices to reflect and compensate for higher risks was effective.

| % Change LC * | % Change LC | % Change FC | % Total Change | Combined % Total Change | ||||||||||||||||

| BAP | Expressed in PEN 2013 vs. 2012 | Expressed in US$ 2013 vs. 2012 | Expressed in US$ 2013 vs. 2012 | Expressed in US$ 2013 vs. 2012 | Expressed in US$ 2013 vs. 2012 (2) | |||||||||||||||

| Fee income | 24.4 | % | 13.5 | % | 11.5 | % | 13.0 | % | ||||||||||||

| Net gain on foreign exchange transaction | 24.0 | % | 13.1 | % | 1.8 | % | 11.0 | % | ||||||||||||

| Net premiuns earned | 24.9 | % | ® | 13.9 | % | + | 7.1 | % | = | 11.5 | % | |||||||||

| Total non financial income (1) | 24.5 | % | 13.6 | % | 8.5 | % | 12.1 | % | 19.9 | % | ||||||||||

* Converted at Nuevos Soles at Q-end exchange rate.

(1) 71.2% of Total non financial income is generated in local currency.

(2) Calculated by adding up the weighted % change of each currency.

In terms of fee income (banking and pension funds), the gains on foreign exchange transactions and net earned premiums, which represent Credicorp’s core non-interest earning income, reported excellent growth of more than 24% of its component denominated in LC for the three items. The FC component grew 11.5% in terms of fee income, 1.8% in FX gains and 7.1% in net earned premiums with regard to last year’s figures given that business growth in loans, premiums and transactions was principally in LC. This led to total weighted growth for these income components of approximately 20%, which compares favorably with the 12.1% reported in our results expressed in US Dollars.

The stupendous evolution of income allowed it to easily absorb the level of operating expenses and total provisions for loan losses.

As indicated before, total provisions for loan losses grew +20% in 2013. This was due primarily to problems in the SME segment and to a lesser extent to the increase seen in the loss ratio for Credit Cards at year-end. The latter was due to a regulatory change in the way the minimum payment is calculated. In this context, the Bank expects that it will take customers a few months to adjust to the new level of debt service.

| % Change LC * | % Change LC | % Change FC | % Total Change | Combined % Total Change | ||||||||||||||||

| BAP | Expressed in PEN 2013 vs. 2012 | Expressed in US$ 2013 vs. 2012 | Expressed in US$ 2013 vs. 2012 | Expressed in US$ 2013 vs. 2012 | Expressed in US$ 2013 vs. 2012 (3) | |||||||||||||||

| Operating expenses (1) | 19.1 | % | 8.7 | % | 30.7 | % | 14.6 | % | 22.6 | % | ||||||||||

| Adjusted Operating expenses (2) | 18.4 | % | ® | 8.0 | % | + | 25.0 | % | = | 13.6 | % | 20.4 | % | |||||||

* Converted at Nuevos Soles at Q-end exchange rate.

(1) 69.4% of Operating expenses are generated in local curency.

(2) 70.0% of adjusted Operating expenses are generated in local currency. Adjusted Operating expenses excludes expenses associated with SUNAT and ESSALUD for previous periods; contingent charges in Bolivia; de-recognition of assets associated with system development and installations; and an impairment loss after IM Trust was valuated according to NIIF norms.

(3) Calculated by adding up the weighted % change of each currency.

In terms of operating expenses, although the LC component was positively affected by devaluation when the same is expressed in US Dollars, the weighted increase by currency type was 22% as opposed to 14.6% (reported) when we eliminate the positive effect of the devaluation of expenses in LC versus the 14.6% reported. This figure drops to 20.4% when eliminate non-recurring expenses (vs. 13.6% in reported figures).

| 5 |

| Local Currency * | Foreign Curreny | |||||||||||||||

| 2013 vs. 2012 | 2013 vs. 2012 | |||||||||||||||

| BAP | % Change | % Participation | % Change | % Participation | ||||||||||||

| Total Loans | 30.4 | % | 47.2 | % | -1.6 | % | 52.8 | % | ||||||||

* Converted at Nuevos Soles at Q-end exchange rate.

In terms of loans, it is important to note the excellent growth of 30.4% in loan balances denominated in LC, which represented 47.2% of the loan balance at the end of 2013; during the same period, the FC loan balance fell -1.6%. The aforementioned, after excluding the effect of devaluation, represents a +13.5% increase in account balances. This result is much higher than the reported 6.5%.

An analysis of daily average balances is, however, a better indicator of business evolution. In this case, average daily balances are calculated only for BCP, which nonetheless represents 97% of Credicorp’s portfolio. These balances posted an increase of +22.7% in Retail Banking and +39.5% at Edyficar. The portfolio denominated in FC, which only grew 3.1%, reflects a slight increase in Wholesale Banking (+2.1%) and a -10.4% decrease in FC loans at Edyficar while Retail Banking maintained the same level registered last year. The average daily balances, without including devaluation, expanded +17.3% with regard to the level obtained in 2012 and reflect the excellent growth of our business.

This analysis is meant to demonstrate the Credicorp’s business has in fact remained very solid. It has maintained good levels of growth, utilized adequate risk management approaches, and leveraged the large growth potential identified in years past. All of this is hidden behind the distortions created by the nature our banking system, which works in two currencies; the process of change and de-dollarization that we are undergoing; the evolution of the international markets and the regulatory changes that tend to arise in developing economies such as ours.

| 6 |

Credicorp – The Sum of Its Parts

The most noteworthy events for BCP in 4Q13 were:

| i) | The on-going de-dollarization of our economy and our loan portfolio, which greatly benefits our results given that it implies lower funding costs and more profitable assets. |

| ii) | On-going improvements in our margins, guided by the improved pricing tools that were introduced in our scoring models |

| iii) | On-going improvements in retail products and a redistribution of funds denominated in Nuevos Soles to more profitable assets. |

| iv) | Good signs persist that indicate lower costs for risk in the future given that the past due ratio has begun to decelerate in SMEs although we have seen a temporary increase in the exchange rate due to regulatory changes. |

| v) | The advent of some non-recurring extraordinary costs that adversely affect operating results and a related to taxes, insurance reserves, investment valuations and others described later in this report. |

The aforementioned explain BCP’s results this 4Q. At the end of this period, net income totaled US$ 144.3 million and the contribution to Credicorp was US$ 140.8 million. BCP’s operating results were very satisfactory despite a seasonal increase in year-end expenses. Nevertheless, extraordinary non-recurring expenses pushed earnings down and led to a ROE of 19.9%, which fell below expectations.

| Earnings contribution to Credicorp | Quarter | Change % | Year ended | % Change | ||||||||||||||||||||||||||||

| US$ 000 | 4Q13 | 3Q13 | 4Q12 | QoQ | YoY | Dec 13 | Dec 12 | Dec 13 / Dec 12 | ||||||||||||||||||||||||

| Banco de Crédito BCP (1) | 140,818 | 146,677 | 166,701 | -4 | % | -16 | % | 458,325 | 645,750 | -29.0 | % | |||||||||||||||||||||

| BCB (2) | 4,498 | 3,921 | 3,904 | 15 | % | 15 | % | 17,144 | 20,082 | -14.6 | % | |||||||||||||||||||||

| Edyficar | 9,969 | 11,330 | 10,942 | -12 | % | -9 | % | 34,513 | 35,546 | -2.9 | % | |||||||||||||||||||||

| Pacifico Grupo Asegurador | 4,723 | 18,458 | 16,895 | -74 | % | -72 | % | 39,899 | 65,998 | -39.5 | % | |||||||||||||||||||||

| Elimination (3) | (5,985 | ) | - | - | - | - | (5,985 | ) | - | - | ||||||||||||||||||||||

| Atlantic Security Bank | 11,972 | 9,781 | 13,706 | 22 | % | -13 | % | 50,681 | 48,402 | 4.7 | % | |||||||||||||||||||||

| Prima | 12,267 | 12,541 | 8,123 | -2 | % | 51 | % | 50,798 | 38,183 | 33.0 | % | |||||||||||||||||||||

| Credicorp Capital (4) | (11,608 | ) | 886 | 6,396 | -1411 | % | (3 | ) | (2,820 | ) | 6,396 | (1 | ) | |||||||||||||||||||

| Credicorp. Inv (5) | (13,427 | ) | 991 | 3,337 | -1454 | % | (5 | ) | (6,150 | ) | 3,337 | (3 | ) | |||||||||||||||||||

| BCP Capital (6) | 1,819 | (106 | ) | 3,059 | 1821 | % | (0 | ) | 3,330 | 3,059 | 0 | |||||||||||||||||||||

| Credicorp Ltd. (7) | 1,934 | (5,659 | ) | (5,681 | ) | 134 | % | 134 | % | (14,760 | ) | (10,285 | ) | -44 | % | |||||||||||||||||

| Others (8) | (2,485 | ) | (3,259 | ) | (5,951 | ) | 24 | % | 58 | % | (9,060 | ) | (5,666 | ) | -556 | % | ||||||||||||||||

| Net income attributable to Credicorp | 151,636 | 179,425 | 200,189 | -15 | % | -24 | % | 567,078 | 788,779 | -28 | % | |||||||||||||||||||||

(1) Includes Banco de Crédito de Bolivia and Edyficar.

(2)The figure is lower than the net income of BCB because Credicorp owns 97.7% of BCB (directly and inderectly). 4Q13 figure includes Inversiones Credicorp Bolivia's contribution of US$0.6 millions.

(3) Includes the elimination related to the income obtained by Pacífico from the sale of a stake of Inv. Centenario to Credicorp.

(4) Figures Proforma - Unaudited, according to IFRS. Not yet consolidated but for purposes of this report is the sum of Credicorp Inv. and BCP Capital.

(5) Includes BCP Chile, IMT, Credicorp Inv, CSI, BCP Colombia and Correval.

(6) Includes Credifondo, Credibolsa, Credítitulos.

(7) Includes taxes on BCP's and PPS's dividends, and other expenses at the holding company level. Also includes the elimination related to the adquisition of a stake of Inv. Centenario.

(8) Includes Grupo Crédito excluding Prima (Servicorp and Emisiones BCP Latam), others of Atlantic Security Holding Corporation and others of Credicorp Ltd. Includes in 4Q12 a elimination related to the sale of a property from Prima AFP to Pacífico Grupo Asegurador.

BCP Bolivia, despite regulatory changes in Bolivia, performed positively in 2013 and closed the year with a bottom line result of US$ 16.9 million. Growth in the Bank’s indicators is reflected in the good performance of net interest income (+14.5%), non-financial income (+8.6%) and the coverage ratio (299.7%) as well as a significant increase in loans (+18.3%); all of this was accomplished by keeping the past due ratio under control (1.34%). The positive evolution of these indicators shows that BCP Bolivia is one of the best performers in the Bolivian financial system, where the Bank enjoys a reputation of being one of the most stable and reliable entities on the scene. In this context, BCP Bolivia posted a very respectable and consistent market share of 10.9% in loans and 11.1% in deposits.

Edyficar continued to perform extraordinarily well, which coincides with local economic development in the SME sector in particular. This led to improvements in: (i) the loan level and portfolio profile; this portfolio totaled US$ 938 million at year-end (+23.4%), (ii) net interest income (+38.2%) and (iii) non-financial income (+14.3%). These results generated net earnings of US$ 35.4 million and ROAE of 21.6%. To accompany this growth and be closer to its clients, Edyficar opened new branches to bring the total number of locales to 190 at the end of 2013.

| 7 |

Atlantic Security Bank (ASB) grew its Assets under Management business in 4Q and also increased its contribution to Credicorp, closing the year with US$ 50.7 million (+4.7% higher than the figure reported in 2012) and ROAE of 26.5%. This result was possible thanks to the trust that clients have placed in our equity management services and ASB’s excellent management capacities, which focus on maintaining strict control and follow-up on diversification strategies and the limits set for each type of investment to obtain an optimum balance between the proprietary portfolio, the level of credit quality and investment performance.

Pacifico Insurance Group (PGA) reported net income after minority interest of US$ 4.2 million. This figure, although lower than last quarter’s result, was affected by external factors that have a direct impact on the underwriting result: (i) changes in regulation in the insurance market, whose impact was reflected in the last quarter of the year, (ii) a change in the rules for obligatory insurance in the Life business, which led to the culmination of the contract with Prima AFP, and (iii) higher expenses due to reserve adjustments given that SBS has established new regulatory requirements to cover administrative costs for claims services if the insurer ceases operations. In accumulated terms, the contribution to Credicorp was US$ 39.8 million at the end of 2013.

If we analyze results in each of PGA’s businesses, it is evident that the same trend is in play as described above: i) PPS reported a result of US$ 2.56 million (-67.2% QoQ) due to an increase in the loss ratio for the car line due to an increase in reserves (IBNR and ULAE)); ii) Pacifico Vida reported a total of US$ 7.7 million due primarily to a decline in income following the culmination of the contract with AFP Prima, iii) EPS reported a loss of -US$ 0.2 million (-117.8% QoQ) due to a seasonal increase in the loss ratio (winter) and SCTR (insurance for high risk occupations), which increase the cost of services and (iv) the Medical Subsidiaries reported a negative result of –US$ 3.5 million (+456%), mainly due to an increase in provisions and accounting adjustments stemming from a reorganization of operation following the acquisition of the medical subsidiaries. Regarding this point, it is important to mention that we expect results to improve next Q due to an increase in out-patient and hospital services and the launching of a new medical center.

Prima AFP reported better results than those obtained in 2012. This improvement is evident in the increases posted for fee income (+16.1%) and in the bottom line result with year-end net earnings of US$ 50.7 million (+33.0%) and a ROAE of 31.4%. These advances were possible mainly thanks to growth in the client portfolio during the affiliation period that ran between October 2012 and May 2013 (200,000 new affiliates); natural growth in the income base due to the Peruvian economy’s dynamism (Prima’s client portfolio includes some of the system’s top earners); and the 9.6% (approx.) devaluation of local currency (due to the translation result, which increased +584.3%). The international economic juncture and its effects on the Lima Stock Exchange affected the annual yields of funds under management. Nonetheless, a long-term analysis, which begins with the system’s creation, indicates that the yield was 7.6% in real terms. To address this situation, the Peruvian Central Bank raised the limits placed on the AFPs ability to make foreign investments from 36% to 40%. This change will take place gradually at intervals of 0.5% a month.

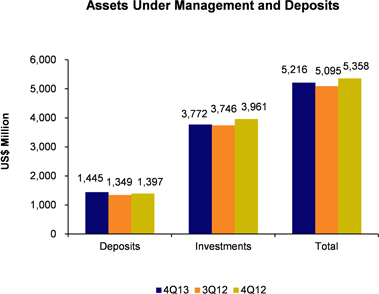

The investment banking business, which is run through Credicorp Capital, continued to effectively position itself as its clients’ best option. Proof of this is that each of Credicorp Capital’s subsidiaries leads the secondary fixed income market (BCP Capital 46.9%, Correval 22.5% and IM Trust 27.7%). The accounting loss incurred by BCP Chile, due to the impairment generated by an accounting adjustment that was made to the valuation of IM Trust, which were below the book value, masked the real business result. If this adjustment had not been made, the bottom line result would have been positive. Lastly, the experience of Credicorp Capital’s staff, as well as the trust that the clients place in its decisions, are reflected in the transactions that were completed and the volume of assets under management, which totaled US$ 7,224 million at year-end.

Credicorp Ltd.’s line mainly includes income tax provisions for dividends for BCP and PPS and other expenses at the holding level. In 4Q13, the results were positive and the contribution to Credicorp totaled US$ 1.9 million. In accumulated terms in 2013, the results were negative (-US$ 14.7 million) and include a write-off for Pacifico Insurance Group’s acquisition of a portion of Inversiones Centenario.

| 8 |

The others account is mainly composed of the results of Grupo Crédito, which manages a number of efforts including Tarjeta Naranja (still in the red and responsible for the majority of the losses reported) and the fiduciary business. In 4Q13, the results improved but still registered losses for -US$ 2.4 million, which include a write off for Prima AFP’s move to sell a property to Pacifico Insurance Group. In annual terms in 2013, the results remained negative (-US$ 9.0 million).

| Regulatory Capital and Capital Adequacy Ratios | Balance as of | % Change | ||||||||||||||||||

| US$ (000) | Dec 13 | Sep 13 | Dec 12 | Dec 13 / Sep 12 | Dec 13 / Dec 12 | |||||||||||||||

| Capital Stock | 496,041 | 496,041 | 505,164 | 0.0 | % | -1.8 | % | |||||||||||||

| Legal and Other capital reserves (1) | 2,903,509 | 2,898,793 | 2,306,561 | 0.2 | % | 25.9 | % | |||||||||||||

| Minority interest (2) | 106,797 | 102,463 | 95,450 | 4.2 | % | 11.9 | % | |||||||||||||

| Loan loss reserves (3) | 323,435 | 310,084 | 297,825 | 4.3 | % | 8.6 | % | |||||||||||||

| Perpetual subordinated debt | 227,500 | 227,500 | 227,500 | 0.0 | % | 0.0 | % | |||||||||||||

| Subordinated Debt | 1,279,765 | 1,282,284 | 1,154,816 | -0.2 | % | 10.8 | % | |||||||||||||

| Investments in equity and subordinated debt of financial and insurance companies | (179,152 | ) | (167,392 | ) | (198,756 | ) | 7.0 | % | -9.9 | % | ||||||||||

| Goodwill | (329,495 | ) | (361,769 | ) | (392,097 | ) | -8.9 | % | -16.0 | % | ||||||||||

| Deduction for subordinated debt limit (50% of Tier I excluding deductions) (4) | - | - | (20,847 | ) | - | - | ||||||||||||||

| Deduction for Tier I Limit (50% of Regulatory capital) (4) | - | - | - | - | - | |||||||||||||||

| Total Regulatory Capital (A) | 4,828,401 | 4,788,004 | 3,975,616 | 0.8 | % | 21.5 | % | |||||||||||||

| Tier I (5) | 2,868,517 | 2,837,758 | 2,168,561 | 1.1 | % | 32.3 | % | |||||||||||||

| Tier II (6) + Tier III (7) | 1,959,884 | 1,950,246 | 1,807,055 | 0.5 | % | 8.5 | % | |||||||||||||

| Financial Consolidated Group (FCG) Regulatory Capital Requirements | 3,808,485 | 3,746,082 | 3,367,681 | 1.7 | % | 13.1 | % | |||||||||||||

| Insurance Consolidated Group (ICG) Capital Requirements | 321,056 | 317,887 | 274,620 | 1.0 | % | 16.9 | % | |||||||||||||

| FCG Capital Requirements related to operations with ICG (8) | (60,494 | ) | (53,879 | ) | (24,179 | ) | 12.3 | % | 150.2 | % | ||||||||||

| ICG Capital Requirements related to operations with FCG (9) | - | - | - | - | - | |||||||||||||||

| Total Regulatory Capital Requirements (B) | 4,069,047 | 4,010,089 | 3,618,122 | 1.5 | % | 12.5 | % | |||||||||||||

| Regulatory Capital Ratio (A) / (B) | 1.19 | 1.19 | 1.10 | -0.6 | % | 8.0 | % | |||||||||||||

| Required Regulatory Capital Ratio (10) | 1.00 | 1.00 | 1.00 | |||||||||||||||||

(1) Legal and Other capital reserves include restricted capital reserves (US$ 2,458 MM) and optional capital reserves ( US$441 MM).

(2) Minority Interest includes USD106.0 MM from minority interest Tier I capital stock and reserves and USD0.8MM from minority interest tier II capital stock and reserves

(3) Up to 1.25% of total risk-weighted assets of Banco de Crédito del Perú, Solución Empresa Administradora Hipotecaria, Financiera Edyficar and Atlantic Security Bank.

(4) Tier II + Tier III can not be more than 50% of total regulatory capital.

(5) Tier II = Capital + Restricted capital Reserves + tier I capital stock and reserves from minority interest Goodwill - (0.5 x Investment in equity and subordinated debt of financial and insurance companies) + Perpetual subordinated debt.

(6) Tier II = Subordinated debt + minority interest tier II capital stock and reserves + Loan loss reserves - (0.5 x Investment in equity and subordinated debt of financial and insurance companies).

(7) Tier III = Subordinated debt covering market risk only.

(8) Includes regulatory capital requirements of the financial consolidated group.

(9) Includes regulatory capital requirements of the insurance consolidated group.

(10) Regulatory Capital / Total Regulatory Capital Requirements (legal minimum = 1.00).

Credicorp has maintained a comfortable capitalization level as a holding, which at the end of December 2013 represents 1.19 times the capital required by Peru’s regulatory entity. This ratio remains stable regarding the figure reported at the end of 3Q13, mainly because: (i) Total Regulatory Capital grew +1.3% QoQ, due to a lower deduction of Goodwill (related mainly to the impairment from BCP Chile) and an increase in Loan loss reserves; and (ii) Regulatory Capital requirements grew +1.5% QoQ, mainly as a result of higher requirement from Financial Consolidated Group, which in turn is related to the expansion of the loan portfolio (credit risk).

Year over year, Credicorp increased its capitalization level from 1.10 times in December 2012 to 1.19 times at the end of 2013 (times the capital required by Peru´s regulatory entity). This is mainly due to a strong increase in Legal and Other capital reserves, and an increase in subordinated debt.

It is also important to note the Tier 1 increased its share of Credicorp’s total regulatory capital, increasing from 59.3% in 3Q13 to 59.6% at the end of 4Q13.

The table shows that the majority of the group’s capital requirement (93.6%) is associated with its financial business, 73.6% of total regulatory capital requirement is concentrated in BCP.

Credicorp’s income generation, coupled with the corporation’s policies on retained earnings, dividend payments, capitalization of earnings and reserve building, has allowed Credicorp to build a comfortable capital reserve to support its business expansion.

In addition, Credicorp holds approximately US$ 600 million in liquid investments that can be used at any time to strengthen its regulatory capital.

| 9 |

II. Banco de Crédito del Perú Consolidated

In 4Q13, BCP reported net income of US$ 144.3 million, which represented a ROAE of 19.9%. Although this result is slightly lower (-4.3%) than last quarter’s, core income evolved favorably. This helped significantly offset the seasonal expenses, the advent of some non-recurring expenses and growth in total provisions for loan losses, as we will explain in more detail later in this report.

The excellent performance of business was reflected primarily in:

| i) | The NII, which grew +3.6% QoQ due to significant expansion in interest on loans, which was in line with growth in average daily balances of loans (+4.5% QoQ); and lower funding costs (-2.9% QoQ) due to an increase in the share that deposits holds within total funding (69.3% en el 3T13 vs. 71.8% en el 4T13). In this context, NIM increased from 5.27% to 5.37%. It is important to consider that NII of 4Q13 included a deduction of US$ 7 million as part of the adequacy to IFRS13 related to derivatives valuation, thus real growth of NII was 5.3% QoQ. |

| ii) | Non-financial income expanded +6.9% QoQ. This was mainly attributable to growth in fee income (+5.1%), which along with a slight gain on sales of securities and other, offset the drop in gains on foreign exchange transactions (-6.3% QoQ). It is noteworthy that in 4Q fee income incorporated a reversal of US$ 4 million after aligning to IFRS (deferred income), which hide fee income’s real growth of 7.5% QoQ. |

The aforementioned attenuated:

| i) | The +5.4% increase in loan provisions, which represented 28.5% of net interest income (vs. 28.4% in 3Q13) and 2.25% of loans (vs. 2.19% in 3Q13). This increase reflects the maturing cycle of the SME PDL portfolio as well as a slight increase in PDL of the Credit Cards segment that was due, in part, to a regulatory change made to the methodology for calculating minimum payments. It will take some time for clients to adjust to the new level of debt service. |

| ii) | The +8.3% increase in operating expenses, which was in turn attributable to the seasonality seen every 4Q, as well as non-recurring expenses, as we will explain later in the report. If we exclude extraordinary expenses, operating expenses only increase +5.3%, which reflects the Bank’s real commitment to achieving improvements in operating efficiency. |

| iii) | The translation loss of 5 million and higher provisions for taxes due to an increase in taxable earnings reported in local accounting. |

In terms of assets, there is once again a shift toward more profitable assets such as loans, which expanded +2.7% QoQ. Average daily balances grew +4.5% QoQ with noteworthy evolution in the Wholesale Banking Portfolio (+5.3% QoQ), which was due to the good performance of Corporate Banking (+5.5% QoQ) and Middle Market Banking (+4.9% QoQ). Retail Banking loans increased +3.2% QoQ, led by the evolution of the Mortgage segment (+2.7% QoQ), followed by Consumer loans (+4% QoQ), SME (+ 2.5% QoQ), Businesses (+4.9% QoQ) and Credit Cards (+ 3.4% QoQ). During the same period, Edyficar maintained solid growth of +9.1% QoQ.

An analysis of NIM on loans reveals a 5bps increase QoQ, going from 8.35% to 8.40% at the end of 4Q13. The aforementioned is clear evidence of the positive impact on margins that adequate pricing in the Retail Banking business, which is now aligned with the risk profile of each segment, and lower funding costs (2% vs. 2.14% in the previous quarter) have had.

In terms of portfolio quality, the PDL ratio increased only 5bps to situate at 2.30% at quarter-end (vs. 2.25% at the end of 3Q13), which indicates that growth in the PDL portfolio has slowed down. Delinquency in the over 90-day PDL portfolio only increased 1bp to situate at 1.53%. This Q’s higher PDL ratio was attributable primarily to the SME and Credit Card segments, which posted ratios of 8.24% and 5.84%, respectively at quarter-end (vs. 8.03% and 5.08% at the end of 3Q13).

| 10 |

| Banco de Credito and Subsidiaries * | Quarter | % Change | Year ended | % Change | ||||||||||||||||||||||||||||

| US$ 000 | 4Q13 | 3Q13 | 4Q12 | QoQ | YoY | Dec 13 | Dec 12 | Dec 13 / Dec 12 | ||||||||||||||||||||||||

| Net financial income | 440,636 | 425,215 | 402,835 | 3.6 | % | 9.4 | % | 1,683,147 | 1,487,726 | 13.1 | % | |||||||||||||||||||||

| Total provisions for loan loasses | (125,395 | ) | (119,019 | ) | (103,083 | ) | 5.4 | % | 21.6 | % | (454,375 | ) | (378,620 | ) | 20.0 | % | ||||||||||||||||

| Net interest income after net provisions for loan losses | 315,241 | 306,196 | 299,752 | 3.0 | % | 2.1 | % | 1,228,772 | 1,109,106 | 10.8 | % | |||||||||||||||||||||

| Non financial income | 226,209 | 211,659 | 232,830 | 6.9 | % | -2.8 | % | 841,582 | 861,266 | -2.3 | % | |||||||||||||||||||||

| Operating expenses (1) | (328,507 | ) | (303,434 | ) | (337,886 | ) | 8.3 | % | -2.8 | % | (1,270,214 | ) | (1,162,506 | ) | 9.3 | % | ||||||||||||||||

| Operating income (2) | 212,943 | 214,421 | 194,696 | -0.7 | % | 9.4 | % | 800,140 | 807,866 | -1.0 | % | |||||||||||||||||||||

| Core operating income | 212,943 | 214,421 | 194,696 | -0.7 | % | 9.4 | % | 800,140 | 807,866 | -1.0 | % | |||||||||||||||||||||

| Non core operating income (expenses) (3) | (8,857 | ) | - | - | 0.0 | % | 0.0 | % | (14,442 | ) | - | 0.0 | % | |||||||||||||||||||

| Translation results | (5,000 | ) | (2,877 | ) | 25,734 | 73.8 | % | -119.4 | % | (87,025 | ) | 63,105 | -237.9 | % | ||||||||||||||||||

| Income taxes | (63,443 | ) | (60,529 | ) | (49,496 | ) | 4.8 | % | 28.2 | % | (248,788 | ) | (208,714 | ) | 19.2 | % | ||||||||||||||||

| Net income | 144,287 | 150,826 | 170,958 | -4.3 | % | -15.6 | % | 463,532 | 661,358 | -29.9 | % | |||||||||||||||||||||

| Net income / share (US$) | 0.047 | 0.049 | 0.055 | -4.3 | % | -15.6 | % | 0.149 | 0.213 | -29.9 | % | |||||||||||||||||||||

| Total loans | 22,308,659 | 21,715,317 | 20,754,941 | 2.7 | % | 7.5 | % | 22,308,659 | 20,754,941 | 7.5 | % | |||||||||||||||||||||

| Deposits and obligations | 23,174,089 | 22,784,081 | 22,835,451 | 1.7 | % | 1.5 | % | 23,174,089 | 22,835,451 | 1.5 | % | |||||||||||||||||||||

| Net shareholders' equity | 2,972,064 | 2,843,292 | 2,775,351 | 4.5 | % | 7.1 | % | 2,972,064 | 2,775,351 | 7.1 | % | |||||||||||||||||||||

| Net financial margin | 5.37 | % | 5.27 | % | 5.22 | % | 5.14 | % | 5.21 | % | ||||||||||||||||||||||

| Efficiency ratio | 46.9 | % | 46.1 | % | 52.3 | % | 47.7 | % | 49.2 | % | ||||||||||||||||||||||

| Return on average equity | 19.9 | % | 21.9 | % | 25.2 | % | 16.1 | % | 25.9 | % | ||||||||||||||||||||||

| PDL ratio | 2.30 | % | 2.25 | % | 1.78 | % | 2.30 | % | 1.78 | % | ||||||||||||||||||||||

| NPL ratio (4) | 2.90 | % | 2.84 | % | 2.47 | % | 2.90 | % | 2.47 | % | ||||||||||||||||||||||

| Coverage of PDLs | 157.6 | % | 162.7 | % | 188.6 | % | 157.6 | % | 188.6 | % | ||||||||||||||||||||||

| Coverage of NPLs | 125.2 | % | 128.7 | % | 136.4 | % | 125.2 | % | 136.4 | % | ||||||||||||||||||||||

| BIS ratio | 14.46 | % | 14.12 | % | 14.72 | % | 14.5 | % | 14.7 | % | ||||||||||||||||||||||

| Branches | 401 | 387 | 365 | 401 | 365 | |||||||||||||||||||||||||||

| Agentes BCP | 5,820 | 5,385 | 5,713 | 5,820 | 5,713 | |||||||||||||||||||||||||||

| ATMs | 2,091 | 2,039 | 1,844 | 2,091 | 1,844 | |||||||||||||||||||||||||||

| Employees (5) | 22,657 | 22,403 | 21,798 | 22,657 | 21,798 | |||||||||||||||||||||||||||

* See notes in BCP and Subsidiaries income statement and balance sheet.

(1) Employees' profit sharing is registered in Salaries and Employees Benefits since 1Q11 due to local regulator's decision.

(2) Income before translation results and income taxes.

(3) Includes non core operating expenses. 4Q13 figure includes non recurring expenses assocated to SUNAT and provision for contingencies from BCP Bolivia. 2013 figure includes aforementioned non recurring expenses and expenses incurred from the sale of BCP Colombia to Credicorp Investments.

(4) NPLs: Non-performing lons = Past due loans + Refinanced and restructured loans. NPL Ratio = NPLs / Total loans.

(5) Excludes employees from BCP Colombia and BCP Chile.

Liabilities at the end of 4Q13 increased +2.5% QoQ. This was primarily attributable to growth in total deposits (+1.7% QoQ) and expansion in due to Banks and Correspondents (+12.9% QoQ). The new funding structure lowered the cost of funding, which went from 2.14% to 2%.

| Core income | Quarter | Change % | Year ended | % Change | ||||||||||||||||||||||||||||

| US$ 000 | 4Q13 | 3Q13 | 4Q12 | QoQ | YoY | Dec 13 | Dec 12 | Dec 13 / Dec 12 | ||||||||||||||||||||||||

| Net interest income | 440,636 | 425,215 | 402,835 | 3.6 | % | 9.4 | % | 1,683,147 | 1,487,726 | 13.1 | % | |||||||||||||||||||||

| Fee income | 170,992 | 162,715 | 172,495 | 5.1 | % | -0.9 | % | 648,774 | 620,058 | 4.6 | % | |||||||||||||||||||||

| Net gain on foreign exchange transactions | 44,490 | 47,487 | 47,996 | -6.3 | % | -7.3 | % | 190,763 | 174,049 | 9.6 | % | |||||||||||||||||||||

| Core income | 656,118 | 635,417 | 623,326 | 3.3 | % | 5.3 | % | 2,522,684 | 2,281,833 | 10.6 | % | |||||||||||||||||||||

* See note in BCP and Subsidiaries income statement.

Finally, core income increased +3.3% QoQ due to the excellent evolution of NII and fee income.

| 11 |

Results 2013 vs. 2012

As in the analysis of Credicorp’s results for 2013, an analysis of BCP reflects the effects of the strong volatility of the Nuevo Sol with regard to the US Dollar. This masks the fact that the Bank’s performance was truly excellent. The analysis we will present in the paragraphs that follow will eliminate distortions and isolate the non-recurring elements to fully appreciate the real performance of our banking business.

This Q in IFRS, BCP reported net income after minority interest of US$ 463.5 million in 2013, which is 29.9% lower than the figure obtained in 2012 (US$ 661.4 million). The aforementioned led ROAE to drop from 26.4% in 2012 to 16.6% in 2013. Additionally, despite the net result obtained, the efficiency ratio fell from 49.2% to 47.7% in 2013 due to the Bank’s efforts to control expenses since the beginning of the second half of the year. In terms of portfolio quality, the PDL ratio increased from 1.78% to 2.30%. This was due primarily to an increase in the PDL ratios of the SME and Credit Card segments of 1.78% a 2.30% respectively, which will be discussed in further detail later on in the report.

Nevertheless, it is important to note that despite the impact that factors outside of our control had on business performance, operating income only fell 1% with regard to 2012’s figure. This figure indicates a satisfactory evolution if we consider that it incorporates the effect of the devaluation of income denominated in LC.

The external factors that hide business’s real performance represented a total of US$ 172 million, stemming from losses due to market issues and non-recurring expenses such as:

| i) | The translation loss of US$ 87 million associated with the capital position in LC; |

| ii) | The loss of US$ 43.5 million due to the valuation of forward contracts, which were also associated with the capital position in LC; |

| iii) | The loss of US$ 27 million that was generated by a shift in interest rates on the US Dollar and the position of BCP’s sovereign bonds (Peru, Colombia and Brasil); and |

| iv) | Other non-recurring expenses for US$ 14.5 million stemming from payments to SUNAT for previous periods, contingencies in Bolivia and a loss of the sale of BCP Colombia to Correval. |

In this first analysis, if we exclude the aforementioned elements, operating income grew 9.6% with regard to 2012’s level (despite that 2012’s results included gains on sales of securities for US$ 43.3 million). In this context and after we deduct part of the translation gains posted in 2012, net income remains almost flat (-0.2% YoY).

In the second level of analysis, the business’s real performance is even more evident given that it considers income and expenses in the currency in which they were originated, as is evident in the tables below. From this perspective, the Bank’s evolution has been healthy and indicates that both income and margins are solid.

| % Change LC | % Change LC * | % Change FC | % Total Change | Combined % Total Change | ||||||||||||||||

| BCP | Expressed in PEN 2013 vs. 2012 | Expressed in US$ 2013 vs. 2012 | Expressed in US$ 2013 vs. 2012 | Expressed in US$ 2013 vs. 2012 | Expressed in US$ 2013 vs. 2012 (4) | |||||||||||||||

| Adjusted interest income (1) | 10.6 | % | 0.9 | % | 30.6 | % | 14.4 | % | ||||||||||||

| Adjusted interest expenses (2) | 19.4 | % | 8.9 | % | 10.3 | % | 10.6 | % | ||||||||||||

| Adjusted Net interest income (1)(2)(3) | 8.6 | % | ® | -0.9 | % | + | 52.7 | % | = | 15.9 | % | 20.1 | % | |||||||

| Reported Net interest income | 13.1 | % | ||||||||||||||||||

* Converted at USDollars at Q-end exchange rate.

(1) Interest income reported - Other income. Other income includes the gain on valuation of derivatives generated by the devaluation of the Nuevo Sol.

(2) Interest expenses reported - Other expenses. Other expenses includes the loss in valuation of derivatives linked to the loss in structural forward contracts for US$ 32.9 million in 2Q13 and US$ 11.7 million in 1Q13.

(3) 74.0% of adjusted Net interest income is generated in local currency.

(4) Calculated by adding up the weighted % change of each currency.

The adjusted NII in LC, which represents 74% of the total, grew 8.6% with regard to 2012’s while the adjusted NII in FC reported a significant increase of 52.7%. All of this was the result of the excellent evolution of the loan portfolio, which when measured in average daily balances, reflects growth of 32.7% in LC and 3.1% in FC.

| 12 |

As such NII, if we isolate the distortion generated by devaluation, reported an increase of approximately 20.1% in comparison with 2012’s figure following real portfolio growth of approximately 17.3%.

| % Change LC | % Change LC * | % Change FC | % Total Change | Combined % Total Change | ||||||||||||||||

| BCP | Expressed in PEN 2013 vs. 2012 | Expressed in US$ 2013 vs. 2012 | Expressed in US$ 2013 vs. 2012 | Expressed in US$ 2013 vs. 2012 | Expressed in US$ 2013 vs. 2012 (3) | |||||||||||||||

| Fee income | 13.3 | % | 3.3 | % | -8.1 | % | 4.6 | % | ||||||||||||

| Net gain on foreign exchange transaction | 16.6 | % | ® | 6.3 | % | + | -9.8 | % | = | 9.6 | % | |||||||||

| Adjusted non financial income (1)(2) | 14.1 | % | 4.1 | % | -8.3 | % | 5.7 | % | 8.6 | % | ||||||||||

* Converted at USDollars at Q-end exchange rate.

(1) Excludes Net gain on sales of securities and other income.

(2) 75.1% of Total non financial income is generated in local currency.

(3) Calculated by adding up the weighted % change of each currency.

Fee income and gains on foreign exchange transactions, which compose BCP’s core income along with NII, posted excellent growth of 13.3% and 16.6%, respectively, in the component denominated in LC. The component denominated in FC for both items fell -8.1% and -9.8% in 2013, respectively, given that business growth in loans and transactions was seen primarily in LC.

The stupendous evolution of BCP’s income allowed it to easily absorb operating expenses and total provisions for loan losses.

Total provisions for loan losses increased +20%, which was primarily due to problems that have been identified in the SME segment and, to a lesser degree, due to the increase seen at year-end in the PDL ratio of the Credit Card segment. The latter was due to a regulatory change in the way the minimum payment is calculated. We expect that clients will need a few months more to adjust to the new level of debt service.

In terms of operating expenses, although the LC component was positively affected by devaluation when expressed in US Dollars, growth, if we consider the currency of origin, was significantly lower (+7%) than that reported in previous years due to the Bank’s efforts in the second half of the year to control spending and achieve more operating efficiency. Growth in expenses denominated in FC (+24.9%) incorporates the effect of non-recurring expense. As such, operating expenses grew 12.3% if we consider the impact of devaluation but the rate falls to 11% if we exclude non-recurring expenses.

| % Change LC | % Change LC * | % Change FC | % Total Change | Combined % Total Change | ||||||||||||||||

| BCP | Expressed in PEN 2013 vs. 2012 | Expressed in US$ 2013 vs. 2012 | Expressed in US$ 2013 vs. 2012 | Expressed in US$ 2013 vs. 2012 | Expressed in US$ 2013 vs. 2012 (2) | |||||||||||||||

| Operating expenses (1) | 7.0 | % | ® | -2.4 | % | + | 24.9 | % | = | 9.3 | % | 12.3 | % | |||||||

* Converted at US Dollars at Q-end exchange rate.

(1) 70.3% of Operating expenses are generated in local curency.

(2) Calculated by adding up the weighted % change of each currency.

In terms of assets, it is important to note the excellent growth of 30.9% in the year-end balance of loans denominated in LC, which represented 49% of the total balance at the end of 2013 while the year-end balance of loans originated in FC fell -1.9%. The aforementioned represents expansion of +14.2% in year-end loan balances after excluding the effect of devaluation.

The evolution is even more favorable when we analyze the evolution of average daily balances, which increased +32.7% in LC and +3.1% in FC. This expansion was attributable to growth in Wholesale Banking’s LC portfolio (+64.9%), which was accompanied by solid growth of +22.7% in Retail Banking and +39.5% at Edyficar. The portfolio denominated in FC, which only grew 3.1%, reflected a slight increase in Wholesale Banking (+2.1%) and a decline of -10.4% in Edyficar’s FC loans while Retail Banking posted levels similar to those seen last year. If we exclude the effect of devaluation, average daily balances expanded 17.3% with regard to the level obtained in 2012.

| Local Currency | Foreign Curreny | |||||||||||||||

| 2013 vs. 2012 | 2013 vs. 2012 | |||||||||||||||

| BCP | Change % | % Participation | Change% | % Participation | ||||||||||||

| Total Loans | 30.9 | % | 49.0 | % | -1.9 | % | 51.0 | % | ||||||||

| Total Assets | 5.7 | % | 45.0 | % | -0.1 | % | 55.0 | % | ||||||||

| Total Deposits | 1.4 | % | 49.5 | % | 12.1 | % | 50.5 | % | ||||||||

| Total Liabilities | 5.6 | % | 43.0 | % | 5.7 | % | 57.0 | % | ||||||||

| 13 |

Finally, the balance of LC deposits increased very slightly (+1.4%) while the balance of deposits denominated in FC grew +12.1%. This is more than likely related to the evolution of the Nuevo Sol against the US Dollar in 2013.

II.1 Interest-earning assets

Interest-earning assets increased +2.2% QoQ and +2.4% YoY. This growth represented a recomposition of the portfolio to favor more profitable assets. This coincided with loan expansion (+2.7% QoQ and +7.5% YoY) and the increase in trading securities (+303.4% QoQ and +511.6% YoY).

| Interest earning assets | Quarter | % Change | ||||||||||||||||||

| US$ 000 | 4Q13 | 3Q13 | 4Q12 | QoQ | YoY | |||||||||||||||

| BCRP and other banks | 6,365,825 | 6,519,429 | 6,821,579 | -2.4 | % | -6.7 | % | |||||||||||||

| Interbank funds | 67,786 | 101,562 | 17,441 | -33.3 | % | 288.7 | % | |||||||||||||

| Trading securities | 436,202 | 108,130 | 71,323 | 303.4 | % | 511.6 | % | |||||||||||||

| Securities available for sale | 3,975,058 | 3,998,181 | 4,702,394 | -0.6 | % | -15.5 | % | |||||||||||||

| Total loans | 22,308,659 | 21,715,317 | 20,754,941 | 2.7 | % | 7.5 | % | |||||||||||||

| Total interest earning assets | 33,153,530 | 32,442,619 | 32,367,678 | 2.2 | % | 2.4 | % | |||||||||||||

Interest-earning assets expanded +2.2% QoQ, mainly due to +2.7% QoQ growth in current loans and +303.4% QoQ in trading securities. The increase in loans was associated primarily with expansion in the Wholesale Banking portfolio, which when measured in average daily balances reflects growth of +5.3% QoQ. By the same measure, Retail Banking and Edyficar reported an increase of +3.2% and +9.1%, respectively. The increase in trading securities was associated with a higher level of BCRP certificates of deposits. All the aforementioned was attenuated by the decline in the BCRP account and other banks (-2.4% QoQ) as a result of a decline in reserve requirements in local currency, which allowed the Bank to free up funds to direct them to more profitable assets.

The +2.4% YoY increase in interest-earning assets was also attributable to growth in current loans (+7.5% YoY) and trading securities (+511.6% YoY). Loans, when measured in average daily balances, increased +11.9% YoY. This growth was also led by the Wholesale Banking portfolio (+11.9% YoY), followed by Retail Banking (+9.3% YoY) and Edyficar (+28.1% YoY).

Loan Portfolio

At the end of 2013, the year-end balance of total loans at BCP was situated at US$ 22,309 million, which represents growth of +2.7% QoQ and +7.5% YoY. The figure below shows the evolution of quarter-end balances and average daily balances for every month of the last year. During the months of 4Q13, an upward trend is evident in average daily balances, particularly in the month of October.

| 14 |

An analysis of average daily balances indicates:

Average Daily Balances

| TOTAL LOANS (1) | ||||||||||||||||||||

| (US$ million) | ||||||||||||||||||||

| 4Q13 | 3Q13 | 4Q12 | QoQ | YoY | ||||||||||||||||

| Wholesale Banking | 10,419.2 | 9,897.0 | 9,313.6 | 5.3 | % | 11.9 | % | |||||||||||||

| - Corporate | 6,681.8 | 6,335.9 | 5,783.9 | 5.5 | % | 15.5 | % | |||||||||||||

| - Middle Market | 3,737.4 | 3,561.1 | 3,529.7 | 4.9 | % | 5.9 | % | |||||||||||||

| Retail Banking | 9,930.1 | 9,623.9 | 9,088.7 | 3.2 | % | 9.3 | % | |||||||||||||

| - SME | 2,543.1 | 2,480.0 | 2,362.1 | 2.5 | % | 7.7 | % | |||||||||||||

| - Business | 948.8 | 904.7 | 860.5 | 4.9 | % | 10.3 | % | |||||||||||||

| - Mortgages | 3,493.2 | 3,401.7 | 3,119.2 | 2.7 | % | 12.0 | % | |||||||||||||

| - Consumer | 1,926.6 | 1,852.7 | 1,739.6 | 4.0 | % | 10.8 | % | |||||||||||||

| - Credit Cards | 1,018.3 | 984.7 | 1,007.3 | 3.4 | % | 1.1 | % | |||||||||||||

| Edyficar | 898.0 | 822.9 | 700.8 | 9.1 | % | 28.1 | % | |||||||||||||

| Others (2) | 1,168.6 | 1,107.0 | 988.0 | 5.6 | % | 18.3 | % | |||||||||||||

| Consolidated total loans | 22,415.8 | 21,450.8 | 20,091.0 | 4.5 | % | 11.6 | % | |||||||||||||

(1)Average daily balance.

(2) Includes Work Out Unit, other banking and BCP Bolivia.

Source: BCP

The analysis of average daily balances indicates that expansion this Q was the result of excellent dynamism of the Wholesale Banking portfolio (+5.3% QoQ), which was attributable to +5.5% QoQ growth in Corporate Banking and +4.9% QoQ in Middle Market Banking. It is important to note that Wholesale Banking portfolio in LC grew considerably (+21.2% QoQ and +64.9% YoY) while the portfolio denominated in FC reported moderate growth (+0.4% QoQ and +2.1% YoY), which reflects a preference for LC loans that is primarily associated with the volatility present in previous periods and better credit conditions in LC in a scenario marked by the reduction of the reference rate and reserve requirements.

The Retail Banking portfolio experienced growth of +3.2% QoQ, which was associated with:

| i) | +2.5% QoQ expansion in the SME portfolio, which was based on developing business only with clients with very good risk ratings until the tools for risk analysis are duly calibrated. |

| ii) | Growth in the Mortgage segment (+2.7% QoQ), which continues to undergo a noteworthy process of de-dollarization. The LC portfolio expanded +6.9% QoQ, while the FC portfolio dropped -3.2%. It is important to note thatMiVivienda loans went from representing 14.8% of total mortgage loans at the end of 3Q13 to accounting for 15.5% of this portfolio at the end of 4Q13. TheMiVivienda fund seeks to provide access to housing for lower income families. |

| iii) | The Consumer and Credit Card segments expanded +4% QoQ and +3.4% QoQ respectively. De-dollarization is on-going in both segments given that consumer loans and credit card debt in LC grew at a faster rate (+4.3% QoQ and +3.3% QoQ respectively) than consumer loans in FC (+2.2% QoQ and +2.6% QoQ). It is important to note that both the consumer and credit card portfolios posted lower growth this Q than has been reported in the 4Qs of recent years due to the adjustments made in 2012 and part of 2013. |

In the YoY evolution, loans grew +11.6%. This was in line with Wholesale Banking’s performance (+11.9% YoY), which posted noteworthy evolution in its LC-denominated portfolio (+64.9% YoY). In Retail Banking (+9.3% YoY), solid growth was evident in all segments and was particularly strong in Mortgage, Consumer and SME loans, which posted good growth in LC following portfolio de-dollarization. Edyficar maintained an excellent growth rate of +28.1% YoY. It is important to note that devaluation hides real portfolio growth, which in annual terms was 17.3%. This expansion was due to +32.7% growth in the LC portfolio and +3.1% in the portfolio denominated in FC.

| 15 |

| Average Daily Balances | ||||||||||||||||||||||||||||||||||||||||

| DOMESTIC CURRENCY LOANS (1) | FOREIGN CURRENCY LOANS (1) | |||||||||||||||||||||||||||||||||||||||

| (Nuevos Soles million) | (US$ million) | |||||||||||||||||||||||||||||||||||||||

| 4Q13 | 3Q13 | 4Q12 | QoQ | YoY | 4Q13 | 3Q13 | 4Q12 | QoQ | YoY | |||||||||||||||||||||||||||||||

| Wholesale Banking | 7,730.1 | 6,379.1 | 4,687.0 | 21.2 | % | 64.9 | % | 7,647.1 | 7,613.4 | 7,492.4 | 0.4 | % | 2.1 | % | ||||||||||||||||||||||||||

| - Corporate | 5,131.7 | 4,214.7 | 2,781.2 | 21.8 | % | 84.5 | % | 4,841.5 | 4,827.1 | 4,703.4 | 0.3 | % | 2.9 | % | ||||||||||||||||||||||||||

| - Middle Market | 2,598.4 | 2,164.4 | 1,905.9 | 20.1 | % | 36.3 | % | 2,805.7 | 2,786.3 | 2,789.0 | 0.7 | % | 0.6 | % | ||||||||||||||||||||||||||

| Retail Banking | 19,607.6 | 18,715.5 | 15,985.9 | 4.8 | % | 22.7 | % | 2,897.5 | 2,924.4 | 2,895.8 | -0.9 | % | 0.1 | % | ||||||||||||||||||||||||||

| - SME | 6,319.4 | 6,131.6 | 5,352.1 | 3.1 | % | 18.1 | % | 274.1 | 285.1 | 285.4 | -3.8 | % | -4.0 | % | ||||||||||||||||||||||||||

| - Business | 716.7 | 640.7 | 554.5 | 11.9 | % | 29.2 | % | 693.7 | 675.4 | 661.3 | 2.7 | % | 4.9 | % | ||||||||||||||||||||||||||

| - Mortgages | 5,819.5 | 5,445.3 | 4,196.3 | 6.9 | % | 38.7 | % | 1,406.3 | 1,452.4 | 1,488.3 | -3.2 | % | -5.5 | % | ||||||||||||||||||||||||||

| - Consumer | 4,243.3 | 4,069.7 | 3,566.5 | 4.3 | % | 19.0 | % | 404.8 | 395.9 | 353.6 | 2.2 | % | 14.5 | % | ||||||||||||||||||||||||||

| - Credit Cards | 2,508.8 | 2,428.2 | 2,316.4 | 3.3 | % | 8.3 | % | 118.5 | 115.5 | 107.2 | 2.6 | % | 10.6 | % | ||||||||||||||||||||||||||

| Edyficar | 2,476.9 | 2,270.4 | 1,775.3 | 9.1 | % | 39.5 | % | 9.7 | 10.2 | 10.8 | -4.4 | % | -10.4 | % | ||||||||||||||||||||||||||

| Others (2) | 148.9 | 149.9 | 127.7 | -0.7 | % | 16.6 | % | 1,116.0 | 1,053.4 | 918.7 | 5.9 | % | 21.5 | % | ||||||||||||||||||||||||||

| Consolidated total loans | 29,963.5 | 27,514.9 | 22,575.9 | 8.9 | % | 32.7 | % | 11,670.3 | 11,601.3 | 11,317.7 | 0.6 | % | 3.1 | % | ||||||||||||||||||||||||||

(1) Average daily balance.

(2) Includes Work Out Unit, other banking and BCP Bolivia.

Source: BCP

Loan Market Share

At the end of November, BCP consolidated continued to lead the loan market with a 31% share, which situates it over 10 percentage points ahead of its closest competitor.

Retail Banking posted a stable market share maintaining its leadership in all segments. On the other hand, Middle-market experienced an increase going from 33.7% on September 2013 to 34.3% on December 2013, while Corporate Banking fell from 45.7% on September to 43% on December 2013.

Dollarization

The LC-denominated portfolio’s share of total loans increased QoQ and YoY, going from 44.1% in 4Q12 and 46.9% in 3Q13 to 49.0% in 4Q13. This was primarily attributable to solid QoQ and YoY expansion in Wholesale Banking loans in LC.

| 16 |

II. 2 Liabilities

At the end of 4Q13, total liabilities increased +2.5% QoQ due to growth in deposits (+1.7% QoQ), which is the Bank’s main source of funding, and expansion in due to banks and correspondents (+12.9% QoQ). The funding cost was situated at 2%, which falls below the 2.14% reported in 3Q13 due to a decrease in the expenses associated with deposits.

| Liabilities* | Quarter | % Change | ||||||||||||||||||

| US$ 000 | 4Q13 | 3Q13 | 4Q12 | QoQ | YoY | |||||||||||||||

| Non-interest bearing deposits | 6,167,110 | 5,801,751 | 6,205,849 | 6.3 | % | -0.6 | % | |||||||||||||

| Demand deposits | 1,273,472 | 1,351,176 | 1,376,971 | -5.8 | % | -7.5 | % | |||||||||||||

| Saving deposits | 6,355,705 | 6,070,575 | 6,084,550 | 4.7 | % | 4.5 | % | |||||||||||||

| Time deposits | 6,915,603 | 7,357,460 | 6,872,223 | -6.0 | % | 0.6 | % | |||||||||||||

| Severance indemnity deposits (CTS) | 2,390,742 | 2,130,214 | 2,232,492 | 12.2 | % | 7.1 | % | |||||||||||||

| Interest payable | 71,457 | 72,905 | 63,366 | -2.0 | % | 12.8 | % | |||||||||||||

| Total deposits | 23,174,089 | 22,784,081 | 22,835,451 | 1.7 | % | 1.5 | % | |||||||||||||

| Due to banks and correspondents | 4,327,719 | 3,832,745 | 4,379,853 | 12.9 | % | -1.2 | % | |||||||||||||

| Bonds and subordinated debt | 4,137,652 | 4,147,354 | 3,684,908 | -0.2 | % | 12.3 | % | |||||||||||||

| Other liabilities | 619,956 | 723,650 | 2,043,750 | -14.3 | % | -69.7 | % | |||||||||||||

| Total liabilities | 32,259,416 | 31,487,830 | 32,943,962 | 2.5 | % | -2.1 | % | |||||||||||||

| * See note in BCP and Subsidiaries income statement. | ||||||||||||||||||||

Deposits

Total deposits expanded +1.7% QoQ, due primarily to +5.4% growth QoQ in core deposits (Demand, Savings and CTS). The increase in demand and savings deposits came from Retail Banking clients and was primarily LC-denominated. This went hand-in-hand with the campaigns held to stimulate growth in this segment. CTS deposits grew +12.2% QoQ due to seasonal factors that are present in the fourth quarter every year given that CTS payments are made in November. In this scenario core deposits’ share of total deposits increased from 67.4% to 69.8%, which helped push funding costs down.

Time deposits, which are not considered core deposits, posted a decrease of -6.0% QoQ. This was due primarily to maturities and withdrawals in LC in the Middle Market portfolio.

In annual terms, deposits grew +1.5%, which was mainly due to the +4.5% increase posted in savings deposits and +7.1% growth in CTS deposits. This expansion was attributable to the year-end campaigns conducted in these segments. Nevertheless, if we analyze these deposits by currency type, it is evident that deposits denominated in US Dollars grew at a faster rate than their counterparts in Nuevos Soles, which may be due to the devaluation that affected the local currency during the year.

At the end of 4Q13, the loan/deposit ratio was situated at 96.3% (vs. 95.3% in 3Q13) due to more growth in loans than in deposits. An analysis by currency shows that this indicator reached 95.3% in LC (vs. 85.1% in 3Q13) and 97.2% in FC (vs. 106.6% in 2Q13).

| 17 |

Other funding sources

The increase in other sources of funding (+4.4% QoQ) was mainly attributable to expansion in the level relative to banks and correspondents (+12.9% QoQ) that was due to a REPO negotiated with BCRP in the month of December for approximately US$350 million and the fact that the Bank increased its financing obligations with Standard Chartered Bank and Citi Bank.

The aforementioned was attenuated by the drop in Other Liabilities (-14.3% QoQ). This was due to a QoQ decrease in transactions pending liquidation, which are in turn attributable to the purchase of sovereign papers and CDs.

In annual terms, bonds and subordinated debt increased (+12.3% YoY). This was due to a US$350 million issuance of BCP’s international corporate bonds; a move to reopen BCP subordinated bond 2027 for US$ 170 million; and the exchange of BCP bonds 2016 that were issued in 2011 for BCP bonds 2023, which were recently issued in a transaction that generated an additional US$366.3 million. These operations allowed the Bank to efficiently match currencies while taking advantage of historically low rates in the international capital market. In this context, bonds and subordinated debt’s share of total funding increased 11.2% at the end of 2012 to situate at 12.8% at the end of 2013. It is important to note that the -69.7% decline YoY in Other Liabilities is related to Credicorp Capital’s purchase of Correval in June 2013.

Funding Cost

The Bank’s funding cost was situated at 2.00%1 in 4Q13, which represents a 14bp decline with regard to 3Q13’s figure (2.14%). This result was due primarily to a decrease in interest expenses on deposits relative to higher level of core deposits and lower figure of time deposits, the former linked to lower cost.

Market Share of Deposits