UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

[X] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2007.

or

[ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934. For the transition period from _______________________ to ______________________________________

Commission file number 001-11549

BLOUNT INTERNATIONAL, INC.

(Exact name of registrant as specified in its charter)

| | Delaware

(State of

Incorporation) | | 63 0780521

(I.R.S. Employer

Identification No.) | |

|

| | 4909 SE International Way,

Portland, Oregon

(Address of principal executive offices) | |

97222-4679

(Zip Code) | |

|

Registrant's telephone number, including area code: (503) 653-8881

Securities registered pursuant to Section 12(b) of the Act:

| |

Title of each class

Common Stock, $.01 par value | | Name of each exchange

on which registered

New York Stock Exchange | |

|

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. [ ] Yes [X] No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. [ ] Yes [X] No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. [X] Yes [ ] No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the Registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K, or any amendment to this Form 10-K. [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer or a non-accelerated filer (as defined in Rule 12b-2 of the Act).

| Large accelerated filer [ ] | | Accelerated filer [X] | | Non-accelerated filer [ ] | | Smaller reporting company [ ] | |

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). [ ] Yes [X] No

At June 30, 2007, the aggregate market value of the voting and non-voting common stock held by non-affiliates, computed by reference to the last sales price ($13.08) as reported by the New York Stock Exchange, was $495,411,945.

The number of shares outstanding of $0.01 par value common stock as of March 6, 2008 was 47,305,647 shares.

Documents Incorporated By Reference

Portions of the Proxy Statement for the Annual Meeting of stockholders to be held on May 22, 2008, are incorporated by reference in Part III.

BLOUNT INTERNATIONAL, INC. AND SUBSIDIARIES

| Table of Contents | | | | Page | |

| PART I | |

|

| Item 1. | | Business | | | 3 | | |

|

| Item 1A. | | Risk Factors | | | 5 | | |

|

| Item 2. | | Properties | | | 9 | | |

|

| Item 3. | | Legal Proceedings | | | 10 | | |

|

| Item 4. | | Submission of Matters to a Vote of Security Holders | | | 10 | | |

|

| PART II | |

|

| Item 5. | | Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | | | 11 | | |

|

| Item 6. | | Selected Consolidated Financial Data | | | 12 | | |

|

| Item 7. | | Management's Discussion and Analysis of Financial Condition and Results of Operations | | | 13 | | |

|

| Item 7A. | | Quantitative and Qualitative Disclosures about Market Risk | | | 27 | | |

|

| Item 8. | | Financial Statements and Supplementary Data | | | 28 | | |

|

| Item 9. | | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | | | 57 | | |

|

| Item 9A. | | Controls and Procedures | | | 57 | | |

|

| Item 9B. | | Other Information | | | 57 | | |

|

| PART III | |

|

| Item 10. | | Directors and Executive Officers of the Registrant | | | 58 | | |

|

| Item 11. | | Executive Compensation | | | 58 | | |

|

| Item 12. | | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | | | 58 | | |

|

| Item 13. | | Certain Relationships and Related Transactions | | | 58 | | |

|

| Item 14. | | Principal Accounting Fees and Services | | | 58 | | |

|

| PART IV | |

|

| Item 15. | | Exhibits and Financial Statement Schedules | | | 59 | | |

|

| Signatures | | | | | 62 | | |

|

BLOUNT INTERNATIONAL, INC.

2

PART I

ITEM 1. BUSINESS

Blount International, Inc. ("Blount" or the "Company") is an international industrial company with one business segment: Outdoor Products. We also wholly-own and operate a manufacturer of gear-related products. During 2007, we sold our Forestry Division, which constituted the majority of our other business segment at the time. Our products are sold in over 100 countries and approximately 64% of our 2007 sales were made outside the United States of America ("U.S."). Our Company is headquartered in Portland, Oregon. We have manufacturing operations in the U.S., Canada, Brazil and the People's Republic of China ("China"). Additionally, we operate marketing, sales and distribution centers in other parts of the world.

Oregon, Windsor, Power-Match, INTENZ, Jet-Fit, ICS, Redzaw, PRK, SealPro and SpeedHook are registered or pending trademarks of Blount and its subsidiaries. Some forms of Windsor are used under license from affiliates of Snap-On, Inc.

Outdoor Products Segment

Overview. Our Outdoor Products Segment, accounted for 94% of our sales from continuing operations in 2007. This segment manufactures and markets cutting chain, guide bars, sprockets and accessories for chainsaw use, concrete-cutting equipment and accessories and lawnmower blades. This segment also markets branded parts and accessories for the lawn and garden equipment market. The segment's products are sold to original equipment manufacturers ("OEMs") for use on new chainsaws and yard care equipment, and to the retail replacement market through distributors, dealers and mass merchants. Oregon brand chainsaw cutting chain, guide bars and other items are currently sold to most of the chainsaw OEMs, and many of these products are privately branded for our OEM customers. During 2007, approximately 27% of the segment's sales were to OEMs, with the remainde r sold into the replacement market. Approximately 68% of the segment's sales were outside of the U.S. in 2007.

The segment headquarters is in Portland, Oregon. Marketing personnel are located throughout the U.S. and in a number of foreign countries. We manufacture our products in Portland, Oregon; Milan, Tennessee; Kansas City, Missouri; Guelph, Ontario, Canada; Curitiba, Parana, Brazil; and in Fuzhou, Fujian Province, China. A portion of our accessories and spare parts, as well as our concrete-cutting saws, are sourced from vendors in various locations around the world.

Oregon® Products. The Oregon® product line includes a broad range of cutting chain, chainsaw guide bars, cutting chain drive sprockets and maintenance tools used primarily on portable gasoline and electric chainsaws and mechanical timber harvesting equipment. The Oregon product line also includes various cutting attachments and spare parts to service the lawn and garden industry. These lawn and garden equipment parts include lawnmower blades to fit a variety of machines and cutting conditions, as well as replacement parts that meet product specifications of OEMs.

Windsor Products. The Windsor product line includes cutting chain, chainsaw guide bars and cutting chain drive sprockets, as well as products to support mechanical harvesting equipment.

ICS Products. The ICS branded product lines provide specialized concrete-cutting equipment for construction markets. The principal product in the ICS line-up is a proprietary diamond-segmented chain, which is used on gasoline and hydraulic powered saws and equipment. ICS also markets and distributes branded gasoline and hydraulic powered concrete-cutting chainsaws and circular saws to its customers. These saws are manufactured through an agreement with a third party.

Industry Overview. We believe we are the world leader in the production of cutting chain. Oregon and Windsor branded cutting chain and related products are used primarily by professional loggers, farmers, arborists and homeowners. Additionally, the Oregon line of lawnmower-related parts and accessories are used by commercial landscape companies and homeowners. Our ICS products are used by tool rental companies, contractors and concrete-cutting specialists.

Due to the high level of technical expertise and capital investment required to manufacture cutting chain and guide bars, we believe that we are able to produce durable, high-quality cutting chain and guide bars more efficiently than most of our competitors. We also work with our OEM customers to improve the design and specifications of cutting chain and bars used as original equipment on their chainsaws.

Weather and natural disasters influence our sales cycle. For example, severe weather patterns and events, such as hurricanes, tornadoes and storms, generally result in greater chainsaw use and, therefore, stronger sales of saw chain and guide bars. Seasonal rainfall plays a role in demand for our lawnmower blades and yard care-related products. Above-average rainfall drives greater demand for products in this category, while drought conditions tend to reduce demand for these products.

The Outdoor Products Segment's principal raw material, cold-rolled strip steel, is purchased from multiple intermediate steel processors and can be obtained from other sources. Changes in the price of steel can have a significant effect on the manufactured cost of our products and on the gross margin we earn from the sale of these products.

The segment's profitability is also affected by changes in currency exchange rates, changes in economic and political conditions in the various markets in which we

BLOUNT INTERNATIONAL, INC.

3

operate and changes in the regulatory environment in various jurisdictions.

The segment's competitors include Stihl, Carlton, G&B, Tri-Link, Rotary, Stens, and most major outdoor power equipment manufacturers such as Briggs & Stratton, MTD and John Deere. In addition, new and existing competitors are expanding capacity or contracting with suppliers in China and other low cost manufacturing locations. We also supply products or components to some of our competitors.

Gear Components

Our wholly-owned subsidiary, Gear Products, Inc. ("Gear Products"), was formerly included in our discontinued Industrial and Power Equipment Segment. Our primary gear-related products are rotation bearings, worm gear reducers, hydraulic pump drives, swing drives and winches. These products are used by heavy equipment OEMs for the forestry, construction and utility industries, and produced 6% of our consolidated 2007 sales. We also sell these products in the replacement parts market in addition to our sales to OEMs. For 2007, approximately 93% of Gear Products' sales were to OEMs and approximately 3% of sales were outside the U.S.

Discontinued Forestry Equipment Division

On November 5, 2007, we sold our Forestry Division, which constituted the majority of our Industrial and Power Equipment segment, to Caterpillar Forest Products Inc., a subsidiary of Caterpillar Inc. ("Caterpillar"), for gross proceeds of $79.1 million. We recognized a pretax gain of $26.0 million net of related transaction expenses on the sale in 2007. This division accounted for 32% of our 2005 consolidated sales, 26% of our 2006 consolidated sales and 21% of our consolidated sales for the first nine months of 2007. The Forestry Division is reported as discontinued operations for all periods presented. This division was headquartered in Zebulon, North Carolina and manufactured and marketed timber harvesting and handling equipment and industrial tractors and loaders. The division had manufacturing facilities in Owatonna, Minnesota; Prentice, Wisconsin; and Söderhamn, Sweden. We retained certain liabilities related to the b usiness, as well as a dormant manufacturing facility located in Menominee, Michigan. In December 2007, we sold the land and building in Menominee, Michigan for net cash proceeds of $0.5 million.

Discontinued Lawnmower Segment

On July 27, 2006, we sold our wholly-owned subsidiary Dixon Industries, Inc. ("Dixon"), which constituted our entire Lawnmower segment, to Husqvarna Professional Outdoor Products Inc. ("Husqvarna Professional Outdoor Products") for gross proceeds of $33.1 million. We recognized a pretax gain of $17.4 million net of related transaction expenses on the sale in 2006. This segment accounted for 7% of our sales in each of 2004, 2005 and the first six months of 2006. The Lawnmower Segment is reported as discontinued operations for all periods presented. Dixon was located in Coffeyville, Kansas, and manufactured zero-turn radius lawnmowers and related attachments. We retained certain liabilities and assets of the business, including land and buildings in Coffeyville, Kansas, following the sale. In September 2007, we sold the land and buildings in Coffeyville, Kansas for net cash proceeds of $1.5 million.

Capacity Utilization

Based on a five-day, three-shift work week, capacity utilization for the year ended December 31, 2007 was as follows:

| | | % of Capacity | |

| Outdoor Products segment | | | 100 | % | |

| Gear components | | | 76 | % | |

Capacity for the Outdoor Products Segment has been expanded with our manufacturing plant in Fuzhou, Fujian Province, China, as well as investments in new machinery and equipment for the manufacturing plants in Portland, Oregon; Kansas City, Missouri; Guelph, Ontario Canada; and Curitiba, Parana, Brazil. To meet the fluctuation in demand for its products, this segment operates on an expanded work week basis from time to time at certain locations.

Backlog

The backlog for our continuing operations was as follows:

| | | December 31, | |

| (Amounts in thousands) | | 2007 | | 2006 | | 2005 | |

| Outdoor Products Segment | | $ | 63,289 | | | $ | 54,785 | | | $ | 82,523 | | |

| Gear components | | | 6,029 | | | | 6,524 | | | | 7,955 | | |

| Total backlog | | $ | 69,318 | | | $ | 61,309 | | | $ | 90,478 | | |

The total backlog as of December 31, 2007 is expected to be completed and shipped within twelve months.

Employees

At December 31, 2007, we employed approximately 3,200 individuals. None of our domestic employees belongs to a union. The number of foreign employees who belong to unions is not significant. We believe our relations with our employees are satisfactory, and we have not experienced any significant labor-related work stoppages in the last three years with the exception of a one week period in June, 2007 at our Curitiba, Parana, Brazil location.

Environmental Matters

The Company's operations are subject to comprehensive U.S. and foreign laws and regulations relating to the protection of the environment, including those governing discharges of pollutants into the air and water, the management

BLOUNT INTERNATIONAL, INC.

4

and disposal of hazardous substances and the cleanup of contaminated sites. Permits and environmental controls are required for certain of those operations, including those required to prevent or reduce air and water pollution, and our permits are subject to modification, renewal and revocation by issuing authorities.

On an ongoing basis, we incur capital and operating costs to comply with environmental laws and regulations. In 2007, we spent approximately $1.3 million for environmental compliance, including approximately $0.2 million in capital expenditures. We expect to spend approximately $1.7 million to $2.5 million per year in capital and operating costs in years 2008 through 2010 for environmental compliance. The actual cost to comply with environmental laws and regulations may be greater than these estimated amounts.

Some of our current and former manufacturing facilities are located on properties with a long history of industrial use, including the use of hazardous substances. For certain of our former facilities, we retained responsibility for past environmental matters under the terms of the agreements by which we sold the properties to third party purchasers. We have identified soil and groundwater contamination from these historical activities at certain of our current and former facilities, which we are currently investigating, monitoring or remediating. Management believes that costs incurred to investigate, monitor and remediate known contamination at these sites will not have a material adverse effect on our business, financial condition, results of operations or cash flow. We cannot be sure, however, that we have identified all existing contamination on our current and former properties or that our operations will not cause contami nation in the future. As a result, we could incur material future costs to clean up contamination.

From time to time we may be identified as a potentially responsible party under the U.S. Comprehensive Environmental Response, Compensation and Liability Act (commonly known as the Superfund law) or similar state statutes with respect to sites at which we may have disposed of wastes. The U.S. Environmental Protection Agency (or an equivalent state agency) can either (a) allow such parties to conduct and pay for a remedial investigation and feasibility study and remedial action or (b) conduct the remedial investigation and action on its own and then seek reimbursement from the parties. Each party can be held liable for all of the costs, but the parties can then bring contribution actions against each other or potentially responsible third parties. As a result, we may be required to expend amounts on such remedial investigations and actions, which amounts cannot be determined at the present time, but which may ultimately prove to be material to the consolidated financial statements.

For additional information regarding certain environmental matters, see Note 11 of Notes to Consolidated Financial Statements.

Financial Information about Industry Segments and Foreign and Domestic Operations

For financial information about industry segments and foreign and domestic operations, see "Management's Discussion and Analysis of Results of Operations and Financial Condition" in Item 7 and Note 14 of Notes to Consolidated Financial Statements.

Seasonality

The Company's operations are somewhat seasonal in nature. Year-to-year and quarter-to-quarter operating results are impacted by economic and business trends within the respective industries in which we compete, as well as seasonal weather patterns. See further discussion within the business descriptions above.

Available Information

Our website address is www.blount.com. You may obtain free electronic copies of our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, all amendments to those reports and other SEC filings by accessing the Investor Relations section of the Company's website under the heading "SEC Filings". These reports are available on our Investor Relations website as soon as reasonably practicable after we electronically file them with the Securities and Exchange Commission ("SEC").

Once filed with the SEC, such documents may be read and/or copied at the SEC's Public Reference Room at 450 Fifth Street, N.W. Washington, D.C. 20549. Information regarding the operation of the Public Reference Room may be obtained by calling the SEC at 1-800-SEC-0330. In addition, the SEC maintains an internet site at www.sec.gov that contains reports, proxy and information statements, and other information regarding issuers, including Blount, who file electronically with the SEC.

ITEM 1A. RISK FACTORS

Substantial Leverage—Due to our substantial leverage, we may have difficulty operating our business and satisfying our debt obligations.

As of December 31, 2007, we have $466.1 million of total liabilities, $297.0 million of total debt and a stockholders' deficit of $54.1 million. While we have reduced our total debt from $494.2 million at the end of 2004, our debt remains significant. This substantial leverage may have important consequences for us, including the following:

< Our ability to obtain additional financing for working capital, capital expenditures or other purposes may be

BLOUNT INTERNATIONAL, INC.

5

impaired, or such financing may not be available on terms favorable to us.

< A significant portion of our cash flow from operations is dedicated to the payment of interest expense, which reduces the funds that would otherwise be available to us for operations and future business opportunities.

< A substantial decrease in net operating income and cash flows or an increase in expenses may make it difficult for us to meet our debt service requirements or force us to modify our operations.

< Our substantial leverage may make us more vulnerable to economic downturns and competitive pressures.

The agreements governing our senior credit facilities and the indenture for our 87/8% senior subordinated notes due 2012 contain restrictions that affect our operations, including our and certain of our subsidiaries' ability to incur indebtedness or make acquisitions or capital expenditures. However, these restrictions do not fully prohibit us or our subsidiaries from incurring additional indebtedness or making certain types of acquisitions. In addition, we have available borrowing capacity under the revolving portion of our existing senior credit facilities of $140.9 million as of December 31, 2007. If we or any of our subs idiaries incur additional indebtedness, the risks outlined above could worsen.

Our ability to make payments on our indebtedness and to fund planned capital expenditures and research and product development efforts will depend on our ability to generate cash in the future. Our ability to generate cash, to a certain extent, is subject to general economic, financial, competitive, legislative, regulatory and other factors that are beyond our control.

Our historical financial results have been, and we anticipate that our future financial results will be, subject to fluctuations. Our business may not be able to generate sufficient cash flow from our operations or future borrowings may not be available to us in an amount sufficient to enable us to service our indebtedness or to fund our other liquidity needs. Our inability to pay our debts would require us to pursue one or more alternative strategies, such as selling assets, refinancing or restructuring our indebtedness or selling equity capital. However, alternative strategies may not be feasible at the time or may not prove adequate, which could cause us to default on our obligations and would impair our liquidity. Also, some alternative strategies would require the prior consent of our secured lenders, which we may not be able to obtain. See also "Management's Discussion and Analysis of Financial Condition and Results of Ope rations."

Restrictive Covenants—The terms of our indebtedness contain a number of restrictive covenants, the breach of which could result in acceleration of payment of our senior credit facilities and our 87/8% senior subordinated notes.

The terms of our indebtedness contain a number of restrictive covenants, the breach of which could result in acceleration of our obligations to repay amounts owed under our senior credit facilities and our 87/8% senior subordinated notes. An acceleration of our repayment obligation under our senior credit facilities could result in a payment or distribution of substantially all of our assets to our secured lenders, which would materially impair our ability to operate our business as a going concern. The indenture and our senior credit facilities, among other things, restrict and/or limit our and certain of our subsidiaries' ability to:

< borrow money and issue preferred stock;

< guarantee indebtedness of others;

< pay dividends on our stock;

< purchase our stock or the stock of our "restricted subsidiaries", a defined term;

< make certain types of investments;

< use assets as security in other transactions;

< sell certain assets or merge with or into other companies;

< enter into sale and leaseback transactions;

< enter into certain types of transactions with affiliates;

< enter into new businesses; and

< make certain payments in respect of subordinated indebtedness.

The senior credit facilities also restrict our ability to prepay principal in respect of the 87/8% senior subordinated notes and restrict our ability to engage in any business or operations other than those that are incidental to our ownership of the capital stock of Blount, Inc., our wholly-owned operating subsidiary. In addition, the senior credit facilities require us to maintain certain financial ratios and satisfy certain financial condition tests, which may require that we take actions to reduce debt or to act in a manner contrary to our business objectives. Our ability to meet those financial ratios and tests could be affected by events beyond our control, and there can be no assurance that we will meet those ratios and tests. A breach of any of these covenants could, if uncured, constitute an event of default or a default under the notes or the senior credit facilities. Upon the occurrence of an event of default under the senior credit facilities, the lenders could elect to declare all amounts outstanding under the senior credit facilities, together with any accrued interest and commitment fees, to be immediately due and payable. If we and certain of our subsidiaries were unable to repay those amounts, the lenders under the senior credit facilities could enforce the guarantees from the guarantors and proceed against the

BLOUNT INTERNATIONAL, INC.

6

collateral securing the senior credit facilities. The assets of the applicable guarantors could be insufficient to repay in full that indebtedness and our other indebtedness.

Assets Pledged as Security on Credit Facilities—The majority of our assets and the capital stock of Blount, Inc. are pledged to secure obligations under our senior credit facilities.

The Company and all of its domestic subsidiaries other than Blount, Inc. guarantee Blount, Inc.'s obligations under the senior credit facilities. The obligations under the senior credit facilities are collateralized by a first priority security interest in substantially all of the assets of Blount, Inc. and its domestic subsidiaries, as well as a pledge of all of Blount, Inc.'s capital stock held by Blount International, Inc. and all of the stock of domestic subsidiaries held by Blount, Inc. Blount, Inc. has also pledged 65% of the stock of its non-domestic subsidiaries as additional collateral.

Further, our senior credit facilities provide that payments on the 87/8% notes and the guarantees thereof will be blocked in the event of a default under the senior credit facilities. In addition, upon any distribution to Blount, Inc.'s creditors or the creditors of the guarantors in a bankruptcy, liquidation, receivership, administration for the benefit of creditors or reorganization or similar proceeding relating to the property that constitutes security for the senior credit facilities, the lenders under the senior credit facilities will be entitled to be paid in full in cash before any payment may be made with respect to such notes or the guarantees.

While Blount International, Inc. and all of Blount, Inc.'s existing domestic subsidiaries guarantee the 87/8% senior subordinated notes, none of Blount, Inc.'s existing foreign subsidiaries guarantees these notes. We will not permit any of our non-guarantor restricted subsidiaries to guarantee or pledge any assets to secure the payment of our senior credit facilities, unless that subsidiary is a guarantor of those notes or that subsidiary becomes a guarantor. Any existing or future non-guarantor subsidiary of Blount International, Inc. that we properly designate as an unrestricted subsidiary or a receivables subsidiary will not guarantee those notes.

Competition—Competition may result in decreased sales, operating income and cash flow.

The markets in which we operate are competitive. We believe that design features, product quality, customer service and price are the principal factors considered by our customers. Some of our competitors may have greater financial resources, lower costs, superior technology or more favorable operating conditions than we do. For example, our competitors are expanding capacity or contracting with suppliers located in China and other low cost manufacturing locations as a means to lower costs. Although we have also established a manufacturing facility in China, international competition from emerging economies may nevertheless be formidable and negatively affect our business. We may not be able to compete successfully with our existing or any new competitors, and the competitive pressures we face may result in decreased sales, operating income and cash flows. Competitors could also obtain knowledge of our proprietary manufacturing techniques and processes and reduce our competitive advantage by copying such techniques and processes.

Key Customers—Loss of one or more key customers would substantially decrease our sales.

In 2007, $71.6 million (14%) of our sales were to one customer (Husqvarna AB) and our top five customers accounted for $115.4 million (22%) of our sales. Aside from our top customer, no other customer individually accounted for more than 3% of our sales. While we expect these business relationships to continue, the loss of any of these customers, or a substantial portion of their business, would most likely significantly decrease our sales, operating income and cash flows.

Key Suppliers and Raw Materials Costs—A loss of a few key suppliers or increases in raw materials costs could substantially decrease our sales or increase our costs.

We purchase important materials and parts from a limited number of suppliers that meet certain quality criteria. We generally do not operate under long-term written supply contracts with our suppliers. Although alternative sources of supply are available, the sudden elimination of certain suppliers could result in manufacturing delays, an increase in costs, a reduction in product quality and a possible loss of sales in the near term. In 2007, we purchased approximately $10.0 million of raw material from our largest supplier.

Some of these raw materials, in particular cold-rolled strip steel, are subject to price volatility over periods of time. We have not hedged against the price volatility of any raw materials within our operating segments. It has been our experience that such raw material price increases are difficult to recover from our customers in the short term through increased pricing. For example, we estimate that a 10% change in the price of steel would have affected 2007 income from continuing operations before taxes by an estimated $6.3 million.

Key Employees—The loss of key employees could adversely affect our manufacturing efficiency.

Many of our manufacturing processes require a high level of expertise. For example, we build our own complex dies for use in cutting and shaping steel into components for our products. The design and manufacture of such dies are highly dependent on the expertise of key employees. We have also developed numerous proprietary manufacturing techniques that rely on the expertise of key employees. Our manufacturing efficiency and cost could be adversely affected if we are unable to retain such key employees or continue to train them and their replacements.

BLOUNT INTERNATIONAL, INC.

7

Foreign Sales and Operations—We have substantial foreign sales and operations, which could be adversely affected as a result of changes in local economic or political conditions, fluctuations in currency exchange rates, unexpected changes in regulatory environments or potentially adverse tax consequences.

In 2007, approximately 64% of our sales by country of destination occurred outside of the U.S. International sales are subject to inherent risks, including changes in local economic or political conditions, the imposition of currency exchange restrictions, unexpected changes in regulatory environments and potentially adverse tax consequences. Under some circumstances, these factors could result in significant declines in international sales. Some of our sales and expenses are denominated in local currencies that can be affected by fluctuations in currency exchange rates in relation to the U.S. Dollar. Historically, our principal exposures have been related to local currency manufacturing costs and expenses in Canada and Brazil, and local currency sales and expenses in Europe. From time to time, we manage some of our exposure to currency exchange rate fluctuations through derivative products. Any change in the exchange rates of c urrencies of jurisdictions into which we sell products or incur expenses could result in a significant decrease in reported sales and operating income. For example, we estimate that a 10% stronger Canadian Dollar in relation to the U.S. Dollar would have reduced our operating income by $6.0 million in 2007 and a 10% weaker Euro in relation to the U.S. Dollar would have reduced our sales by $4.3 million in 2007.

In addition, we own substantial manufacturing facilities outside the U.S. As of December 31, 2007, 639,730 square feet, or 51% of the total square feet of our owned facilities, were located outside of the U.S. Also, 32% of our leased square footage is located outside the U.S. This foreign-based property, plant and equipment is subject to inherent risks for the reasons cited above. Loss of these facilities or restrictions on our ability to use them would have an adverse effect on our manufacturing capabilities, and would result in reduced sales, operating income and cash flows.

Weather—Sales of many of our products are affected by weather patterns and the occurrence of natural disasters.

Sales of many of our products, such as yard care parts and accessories, including lawnmower blades, are influenced by weather patterns that are clearly outside our control. For example, drought conditions tend to reduce the demand for yard care products. Natural disasters such as hurricanes, typhoons, and ice and wind storms can stimulate demand for our chainsaw-related products. Conversely, a relative lack of severe weather and natural disasters can result in reduced demand for these same products.

General Economic Factors—We are subject to general economic factors that are largely out of our control, any of which could, among other things, result in a decrease in sales and net income and an increase in our interest expense.

Our business is subject to a number of general economic factors, many of which are largely out of our control, that may, among other things, result in a decrease in sales and net income and an increase in our interest expense. These include recessionary economic cycles and downturns in customers' business cycles, as well as downturns in the principal regional economies where our operations are located. Our senior credit facilities permit us to make borrowings at interest rates that are variable. Increases in interest rates could increase our interest expense payable under the senior credit facilities to levels in excess of what we currently expect. We estimate a one hundred basis point higher average level of interest rates on our variable rate debt would have increased our interest expense in 2007 by $1.8 million. Economic conditions may adversely affect our customers' business levels and the amount of products that they need. Furthermore, customers encountering adverse economic conditions may have difficulty in paying for our products and actual bad debts may exceed our allowances. Finally, terrorist activities, anti-terrorist efforts, war or other armed conflicts involving the U.S. or its interests abroad may result in a downturn in the U.S. and global economies and exacerbate the risks to our business described in this paragraph.

Litigation—We may have litigation liabilities that could result in significant costs to us.

Our historical and current business operations, including discontinued operations, have resulted in a number of litigation matters, including litigation involving personal injury or death, as a result of alleged design or manufacturing defects of our products. Some of these product liability suits seek significant or unspecified damages for serious personal injuries for which there are retentions or deductible amounts under our insurance policies. In the future, we may face additional lawsuits, and it is difficult to predict the amount and type of litigation that we may face. Litigation, insurance and other related costs could result in future liabilities that are significant and that could significantly reduce our cash flows and cash balances. See "Business—Legal Proceedings."

Environmental Matters—We face potential exposure to environmental liabilities and costs.

We are subject to various U.S. and foreign environmental laws and regulations relating to the protection of the environment, including those governing discharges of pollutants into the air and water, the management and disposal of hazardous substances and the cleanup of contaminated sites. Violations of, or liabilities incurred under, these laws and regulations could result in an assessment of significant costs to us, including civil or criminal penalties, claims by third parties for personal injury or property damage,

BLOUNT INTERNATIONAL, INC.

8

requirements to investigate and remediate contamination and the imposition of natural resource damages. Furthermore, under certain environmental laws, current and former owners and operators of contaminated property or parties who sent waste to the contaminated site can be held liable for cleanup, regardless of fault or the lawfulness of the disposal activity at the time it was performed. This potential exposure to environmental liabilities and costs can apply to both our current and former operating facilities.

Future events, such as the discovery of additional contamination or other information concerning past releases of hazardous substances at our or others' sites, changes in existing environmental laws or their interpretation and more rigorous enforcement by regulatory authorities may require additional expenditures by us to modify operations, install pollution control equipment, clean contaminated sites or curtail our operations. These expenditures could significantly reduce our net income and cash balances. See "Business—Environmental Matters" and "Business—Legal Proceedings."

Dividends—We may not pay dividends on our common stock in the future.

We have not paid dividends on our common stock since 1999. We intend to retain future earnings for debt service and for funding growth; therefore, we do not expect to pay any dividends in the near term. In addition, our senior credit facilities and the terms of the 87/8% senior subordinated notes limit our ability to pay dividends. See "Item 5, Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities."

Common Stock Sales—Future sales of our common stock in the public market could lower our stock price.

We may sell additional shares of common stock in subsequent public offerings, or our former majority owner, Lehman Brothers Merchant Banking Partners II, L.P. and its affiliates ("Lehman Brothers"), may sell a substantial number of the 8.9 million shares they own in a secondary stock offering or distribute some or all of their shares to investors in one or more of the investment funds they manage. Other stockholders with significant holdings of our common stock may also sell large amounts of shares they own in a secondary or open market stock offering. We may also issue additional shares of common stock to finance future transactions. We cannot predict the size of future issuances of our common stock or the effect, if any, that future issuances and sales of shares of our common stock will have on the market price of our common stock. Sales of substantial amounts of Blount International, Inc.'s common stock (including shares issu ed in connection with an acquisition or shares sold by existing stockholders), or the perception that such sales could occur, may adversely affect the prevailing market price of Blount International, Inc.'s common stock.

Common Stock Price—The price of our common stock may fluctuate significantly, and stockholders could lose all or part of their investment.

Volatility in the market price of our common stock may prevent stockholders from being able to sell their shares at or above the price paid for the shares. The market price of our common stock could fluctuate significantly for various reasons that include:

< our quarterly or annual earnings or those of other companies in our industries;

< the public's reaction to events and results contained in our press releases, our other public announcements and our filings with the SEC;

< changes in earnings estimates or recommendations by research analysts who track our common stock or the stock of other comparable companies;

< changes in general conditions in the U.S. and global economies, financial markets or forestry industry, including those resulting from war, incidents of terrorism or responses to such events;

< sales of common stock by our largest stockholders, directors and executive officers; and

< the other factors described in these "Risk Factors."

In addition, in recent years, the stock market has experienced extreme price and volume fluctuations. This volatility has had a significant impact on the market price of securities issued by many companies, including companies in our industries. The changes in prices frequently appear to occur without regard to the operating performance of these companies. For example, over the two preceding calendar years, our highest closing stock price has exceeded our lowest by 33% in 2007 and by 91% in 2006. The price of our common stock could fluctuate based upon factors that have little or nothing to do with our company, and these fluctuations could materially reduce our stock price.

ITEM 2. PROPERTIES

Our corporate headquarters occupy executive offices at 4909 SE International Way, Portland, Oregon 97222-4679. The other principal properties of the Company and its subsidiaries are as follows:

Cutting chain and accessories manufacturing plants are located in Portland, Oregon; Milan, Tennessee; Guelph, Ontario Canada; Curitiba, Parana, Brazil; and Fuzhou, Fujian Province, China. Sales offices and distribution centers are located in Kansas City, Missouri, Europe, Japan, Australia and Russia. Rotation bearings, worm gear reducers, hydraulic pump drives and swing drives are manufactured in Tulsa, Oklahoma.

All of these facilities are in good condition, are currently in normal operation and are generally suitable and adequate for the business activity conducted therein. The

BLOUNT INTERNATIONAL, INC.

9

approximate square footage of facilities located at the principal properties by business unit is as follows:

| | | Area in Square Feet | |

| | | Owned | | Leased | |

| Outdoor Products Segment | | | 1,162,251 | | | | 242,536 | | |

| Gear components | | | 98,500 | | | | – | | |

| Corporate | | | 5,000 | | | | – | | |

| Total | | | 1,265,751 | | | | 242,536 | | |

ITEM 3. LEGAL PROCEEDINGS

For information regarding legal proceedings see Note 11 of Notes to Consolidated Financial Statements.

ITEM 4. SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS

No matters were submitted to a vote of our stockholders during the quarter ended December 31, 2007.

BLOUNT INTERNATIONAL, INC.

10

PART II

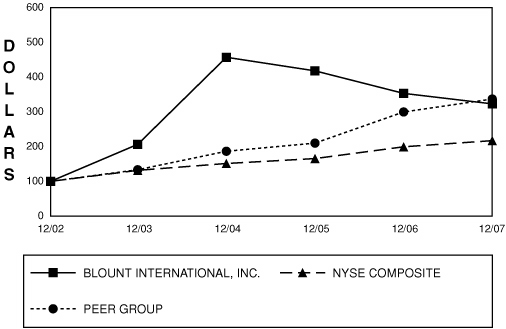

ITEM 5. MARKET FOR REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

The Company's common stock is traded on the New York Stock Exchange (ticker "BLT"). The following table presents the quarterly high and low closing prices for the Company's common stock for the last two years. Cash dividends have not been declared for the Company's common stock since 1999. The Company's senior credit facility and 87/8% senior subordinated note agreements limit our ability to pay dividends. See Item 7, "Management's Discussion and Analysis of Financial Condition and Results of Operations," for further discussion. The Company had approximately 10,000 stockholders of record as of December 31, 2007.

| | | Common Stock | |

| | | High | | Low | |

| Year Ended December 31, 2007: | |

| First quarter | | $ | 13.50 | | | $ | 11.36 | | |

| Second quarter | | | 14.30 | | | | 12.58 | | |

| Third quarter | | | 14.00 | | | | 11.36 | | |

| Fourth quarter | | | 13.19 | | | | 10.76 | | |

| Year Ended December 31, 2006: | |

| First quarter | | $ | 17.10 | | | $ | 15.27 | | |

| Second quarter | | | 16.45 | | | | 11.82 | | |

| Third quarter | | | 12.28 | | | | 8.96 | | |

| Fourth quarter | | | 13.60 | | | | 9.89 | | |

On June 28, 2005, in conjunction with a public offering of our common stock, the Company purchased 382,380 shares of our common stock from a selling stockholder. These shares are held as treasury stock and we have accounted for this treasury stock as constructively retired in the consolidated financial statements.

| Period | | Total Number

of Shares

Purchased | | Average

Price Paid

per Share | | Total Number of

Shares Purchased

as Part of Publicly

Announced Plans

or Programs | | Maximum

Number of Shares

that May Yet Be

Purchased Under

existing Plans or

Programs | |

| June 28, 2005 | | | 382,380 | | | $ | 16.05 | | | | 382,380 | | | | 0 | | |

BLOUNT INTERNATIONAL, INC.

11

ITEM 6. SELECTED CONSOLIDATED FINANCIAL DATA

| | | Year Ended December 31, | |

| (Amounts in thousands except per share data) | | 2007 | | 2006 | | 2005 | | 2004 | | 2003 | |

| Statement of Income Data: | | | | | | | | | | | (1 | ) | | | (2 | ) | | | (3 | ) | |

| Sales | | $ | 515,535 | | | $ | 487,494 | | | $ | 478,829 | | | $ | 445,340 | | | $ | 375,082 | | |

| Operating income | | | 80,700 | | | | 80,460 | | | | 91,628 | | | | 89,265 | | | | 72,853 | | |

| Interest expense, net of interest income | | | 31,706 | | | | 35,404 | | | | 36,707 | | | | 59,019 | | | | 65,406 | | |

| Income (loss) from continuing operations before taxes | | | 48,173 | | | | 46,391 | | | | 53,958 | | | | (13,399 | ) | | | 3,877 | | |

| Income (loss) from continuing operations | | | 32,143 | | | | 32,645 | | | | 88,214 | | | | (11,533 | ) | | | (36,676 | ) | |

| Income from discontinued operations | | | 10,714 | | | | 9,901 | | | | 18,401 | | | | 17,802 | | | | 6,626 | | |

| Net income (loss) | | | 42,857 | | | | 42,546 | | | | 106,615 | | | | 6,269 | | | | (30,050 | ) | |

| Earnings per share: | |

| Basic income (loss) per share: | |

| Continuing operations | | | 0.68 | | | | 0.69 | | | | 1.91 | | | | (0.32 | ) | | | (1.19 | ) | |

| Discontinued operations | | | 0.23 | | | | 0.21 | | | | 0.40 | | | | 0.49 | | | | 0.21 | | |

| Net income (loss) | | | 0.91 | | | | 0.90 | | | | 2.31 | | | | 0.17 | | | | (0.98 | ) | |

| Diluted income (loss) per share: | |

| Continuing operations | | | 0.67 | | | | 0.68 | | | | 1.86 | | | | (0.30 | ) | | | (1.19 | ) | |

| Discontinued operations | | | 0.22 | | | | 0.21 | | | | 0.38 | | | | 0.46 | | | | 0.21 | | |

| Net income (loss) | | | 0.89 | | | | 0.89 | | | | 2.24 | | | | 0.16 | | | | (0.98 | ) | |

| Shares used in earnings per share computations (in thousands): | |

| Basic | | | 47,280 | | | | 47,145 | | | | 46,094 | | | | 36,413 | | | | 30,809 | | |

| Diluted | | | 48,078 | | | | 47,868 | | | | 47,535 | | | | 38,474 | | | | 30,809 | | |

| Balance Sheet Data: | |

| Cash and cash equivalents | | $ | 57,589 | | | $ | 27,636 | | | $ | 12,937 | | | $ | 48,570 | | | $ | 35,194 | | |

| Working capital | | | 128,588 | | | | 117,862 | | | | 112,214 | | | | 97,986 | | | | 86,924 | | |

| Property, plant and equipment, net | | | 89,729 | | | | 99,665 | | | | 101,538 | | | | 97,929 | | | | 91,991 | | |

| Total assets | | | 411,949 | | | | 430,466 | | | | 455,192 | | | | 424,742 | | | | 404,039 | | |

| Long-term debt | | | 295,758 | | | | 349,375 | | | | 405,363 | | | | 491,012 | | | | 603,871 | | |

| Total debt | | | 297,000 | | | | 350,875 | | | | 407,723 | | | | 494,211 | | | | 610,496 | | |

| Stockholders' deficit | | | (54,146 | ) | | | (105,291 | ) | | | (145,187 | ) | | | (256,154 | ) | | | (393,740 | ) | |

The table above gives effect to the sale of the Company's Forestry Division on November 5, 2007 and the sale of the Company's Lawnmower segment on July 27, 2006 and their treatment as discontinued operations for all periods presented.

(1) Income from continuing operations in 2005 includes a $55.5 million tax benefit from the reversal of a valuation allowance against deferred tax assets related to U.S. federal NOL carryforwards.

(2) Loss from continuing operations before taxes in 2004 includes charges totaling $47.0 million related to refinancing transactions.

(3) Loss from continuing operations in 2003 includes a tax provision of $47.2 million to establish a valuation allowance against deferred tax assets related to U.S. federal NOL carryforwards.

BLOUNT INTERNATIONAL, INC.

12

ITEM 7. MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

The following discussion and analysis should be read in conjunction with our consolidated financial statements included elsewhere in this report, as well as the information in Item 6, "Selected Consolidated Financial Data".

Overview

We are an international industrial company that manufactures and markets branded products to OEMs and consumers. Our products are sold in over 100 countries. We believe we are a global leader in the sale of cutting chain, guide bars and accessories for chainsaws.

We have one operating and reporting segment, Outdoor Products, which accounted for 94% of our revenue in 2007. This segment manufactures and markets forestry-related cutting chain, guide bars, sprockets and accessories for chainsaw use, concrete-cutting equipment and accessories, and outdoor equipment parts that include lawnmower blades and other replacement parts and accessories. The segment's products are sold to OEMs for use on new chainsaws and landscaping equipment and to the retail replacement market through distributors, dealers and mass merchants. During 2007, approximately 27% of the segment's sales were to OEMs, with the remainder sold into the replacement market. Approximately 68% of the segment's sales were outside of the U.S. in 2007, up from 65% in 2006 and 64% in 2005. The Outdoor Products segment's performance can be impacted by trends in the forestry industry, weather patterns and natural disasters, including wi nd and ice storms, foreign currency fluctuations and general economic conditions. The segment faces price pressure from competitors on a worldwide basis. The maintenance of competitive selling prices is dependent on the segment's ability to efficiently manufacture its products and successfully market newly developed products, such as our replacement chain and bars and concrete-cutting saws. This segment operates three manufacturing plants in the U.S., one in Canada, one in Brazil and one in China, all of which are focused on continuous cost improvement. The Chinese facility was constructed in 2004, and manufacturing at this facility commenced in 2005. Production capacity for the Chinese facility was increased throughout 2005, 2006 and 2007, with further expansion expected in 2008. Timely capital investment into this segment's manufacturing plants for added capacity and cost reductions, as well as effectively sourcing critical raw materials at favorable prices, is required for us to remain competitive.

We also own and operate a gear components business specializing in the manufacture of mobile equipment rotation bearings, worm gear reducers, hydraulic pump drives and swing drives. Sales in this business accounted for 6% of our total sales in 2007. In 2007, 93% of these sales were made to OEMs, and 97% of sales were to customers in the U.S. This business's customers supply equipment primarily to the utility, construction and forestry markets. The performance of this unit is closely aligned with general economic trends and more specifically with business conditions for these three industries in North America.

We maintain a centralized administrative staff at our headquarters in Portland, Oregon. This centralized administrative staff provides the accounting, finance and information technology functions, administers various health and welfare plans and supervises the Company's capital structure and regulatory, compliance and legal matters.

In November 2007, we sold our Forestry Division to Caterpillar. The Forestry Division constituted the majority of the operations comprising our former Industrial and Power Equipment Segment. The Forestry Division manufactured timber harvesting equipment and industrial tractors and loaders and is reported as discontinued operations for all periods presented.

In July 2006, we sold our Lawnmower segment business, consisting of our Dixon subsidiary, to Husqvarna Professional Outdoor Products. The Lawnmower segment manufactured zero-turning radius riding lawnmowers and is reported as discontinued operations for all periods presented.

Our capital structure has experienced significant changes over the past three years. We began 2005 with $494.2 million in total debt and Lehman Brothers owning 33.4% of our common stock. In 2005, as a result of secondary public offerings of our stock, Lehman Brothers reduced its holdings to its current level of approximately 19% of our outstanding common stock. In 2005, 2006 and 2007, we made significant reductions in outstanding debt by utilizing cash generated from operations and the proceeds from the sale of our discontinued businesses. Debt outstanding at the end of 2007 was $297.0 million, representing a reduction of $197.2 million over the three-year period.

BLOUNT INTERNATIONAL, INC.

13

Operating Results

Year ended December 31, 2007 compared to year ended December 31, 2006

The table below provides a summary of results and the primary contributing factors to the year over year change.

| (Amounts in millions) | | 2007 | | 2006 | | Change | | Contributing Factor | |

| Sales | | $ | 515.5 | | | $ | 487.5 | | | $ | 28.0 | | | | | | |

| | | | | | | | | | | | | | | $10.0 | | Sales volume | |

| | | | | | | | | | | | | | | 10.0 | | Price and mix | |

| | | | | | | | | | | | | | | 8.0 | | Foreign currency translation | |

| Gross profit | | | 175.0 | | | | 173.7 | | | | 1.3 | | | | | | |

| Gross margin | | | 33.9 | % | | | 35.6 | % | | | | | | 6.3 | | Sales volume | |

| | | | | | | | | | | | | | | 10.0 | | Selling price and mix | |

| | | | | | | | | | | | | | | (13.2) | | Product cost and mix | |

| | | | | | | | | | | | | | | (1.1) | | Warehouse consolidation expenses | |

| | | | | | | | | | | | | | | (0.7) | | Foreign currency translation | |

Selling, general and administrative

Expenses ("SG&A") | | | 94.3 | | | | 89.5 | | | | 4.8 | | | | | | |

| | | | | | | | | | | | | | | 2.0 | | Cash compensation expense | |

| | | | | | | | | | | | | | | 0.7 | | Stock compensation expense | |

| | | | | | | | | | | | | | | 0.8 | | Professional services | |

| | | | | | | | | | | | | | | (1.2) | | Retirement benefits expense | |

| | | | | | | | | | | | | | | 2.6 | | Foreign currency translation | |

| | | | | | | | | | | | | | | (0.1) | | Other, net | |

| Operating income | | | 80.7 | | | | 80.5 | | | | 0.2 | | | | | | |

| Operating margin | | | 15.7 | % | | | 16.5 | % | | | | | | 1.3 | | Increase in gross profit | |

| | | | | | | | | | | | | | | (4.8) | | Increase in SG&A | |

| | | | | | | | | | | | | | | 3.7 | | 2006 retirement plan redesign | |

| Income from continuing operations | | | 32.1 | | | | 32.6 | | | | (0.5 | ) | | | | | |

| | | | | | | | | | | | | | | 0.2 | | Increase in operating income | |

| | | | | | | | | | | | | | | 3.7 | | Decrease in net interest expense | |

| | | | | | | | | | | | | | | (2.1) | | Change in other income/expense | |

| | | | | | | | | | | | | | | (2.3) | | Increase in income tax provision | |

| Income from discontinued operations | | | 10.7 | | | | 9.9 | | | | 0.8 | | | | | | |

| | | | | | | | | | | | | | | 8.6 | | Increase in gain on sale of net assets | |

| | | | | | | | | | | | | | | (2.9) | | Decrease in operating results | |

| | | | | | | | | | | | | | | (4.9) | | Increase in income tax provision | |

| Net income | | $ | 42.9 | | | $ | 42.5 | | | $ | 0.4 | | | | | | |

Sales in 2007 increased $28.0 million (6%) from 2006, due to higher sales volume, price and mix improvements, and the favorable effect of translation of foreign currency denominated sales transactions, given the weaker U.S. Dollar in comparison to 2006, particularly in relation to the Euro. The Outdoor Products segment experienced a $31.7 million (7%) increase in sales during 2007 compared to 2006, while sales of our gear-related products decreased $3.7 million (11%) from 2006 to 2007. International sales increased $34.6 million (12%), but domestic sales declined $6.3 million (3%). Included in the international increase is the $8.0 million favorable impact from movement in foreign currency exchange rates compared to 2006. The decline in U.S. sales is attributed to weaker market conditions in the lawn care, forestry and construction industries. By product line, sales of saw chain, bars, sprockets and accessories increased 6% and sales of outdoor equipment parts were up 15%. Sales of concrete-cutting products increased 3% from 2006 to 2007, lead by strength in Europe.

Consolidated order backlog for continuing operations at December 31, 2007 was $69.3 million compared to $61.3 million at December 31, 2006. The year-over-year increase primarily occurred in the Outdoor Products segment.

Gross profit increased $1.3 million (1%) from 2006 to 2007. Gross margin in 2007 was 33.9% of sales compared to 35.6% in 2006. Higher sales volume and improved price and product mix were largely offset by increases in product costs, including higher freight and distribution costs, and $1.1 million incurred to consolidate our North American distribution centers. The increases in product costs include the effects of higher energy costs for utilities, annual wage increases to our manufacturing employees, $1.0 million in higher steel costs and the effects of inflation on other cost elements.

BLOUNT INTERNATIONAL, INC.

14

Fluctuations in currency exchange rates decreased our gross profit in 2007 compared to 2006 by $0.7 million on a consolidated basis. The translation of stronger foreign currencies into a weaker U.S. Dollar resulted in higher manufacturing costs in Brazil and Canada, where local currencies strengthened compared to the U.S. Dollar, which were only partially offset by higher sales in Europe.

SG&A was $94.3 million in 2007 compared to $89.5 million in 2006, representing a year-over-year increase of $4.8 million (5%). As a percent of sales, SG&A remained at 18.3% in both 2007 and 2006. Cash-based compensation increased by $2.0 million year-over-year, reflecting annual merit increases for our employees and higher variable compensation expenses. Stock-based compensation expense increased $0.7 million in 2007 as we continued to expense stock compensation granted in 2006 over the three year vesting periods, as well as recognizing expense on 2007 grants. We expect stock compensation expense to increase again in 2008. Future levels of stock-based compensation expense will depend on many factors, including the quantity, type and vesting schedule of future grants, the price of our stock, the volatility of our stock and risk-free interest rates. Professional services expense increased $0.8 million, primarily due to hig her legal costs. Employee benefits expenses decreased $1.2 million primarily due to the redesign of the Company's U.S. retirement plans effective January 1, 2007. International operating expenses increased $2.6 million from the prior year due to the weaker U.S. Dollar and its effect on the translation of foreign expenses.

We maintain defined benefit pension plans for substantially all employees and retirees in the U.S., Canada and Belgium. In addition, we maintain post-retirement medical and other benefit plans covering most of our employees and retirees in the U.S. The costs of these benefit plans are included in cost of goods sold and SG&A. The accounting effects and funding requirements for these plans are subject to actuarial estimates, actual plan experience and the assumptions we make regarding future trends and expectations. See further discussion below of these key assumptions and estimates under "Critical Accounting Policies and Estimates". Total expense recognized for these pension and other post-retirement plans was $5.8 million and $14.3 million for the years ended December 31, 2007 and 2006, respectively. These amounts, which include amounts charged to both continuing and discontinued operations, also include pension curtailment charges of $0.2 million in 2007 related to our discontinued Forestry Division, and $3.6 million in 2006 to reflect the freezing of our U.S. defined benefit pension plan effective December 31, 2006. At December 31, 2007, we have $41.2 million of accumulated other comprehensive losses, related to our domestic and foreign pension and other post-employment benefit plans, that will be amortized to expense over future years, including $1.9 million to be expensed in 2008.

Operating income increased slightly by $0.2 million from 2006 to 2007, resulting in an operating margin for 2007 of 15.7% of sales compared to 16.5% for 2006. The increase was due to higher gross profit and the non-recurrence of a $3.7 million charge to continuing operations in 2006 for the redesign of our U.S. retirement plans, partially offset by higher SG&A expenses in 2007.

Interest expense of $33.1 million in 2007 compared to $35.8 million in 2006.The decrease was largely due to lower average outstanding debt balances. Interest income increased by $1.0 million from 2006 to 2007, reflecting higher average balances of cash and cash equivalents.

Other expense of $0.8 million in 2007 compared to other income of $1.3 million in 2006. The net expense in 2007 reflects losses on the sale of idle real estate, as well as the write-off of deferred financing costs from the prepayment of principal on our term loans. The income in 2006 is largely due to proceeds from insurance settlements.

The following table summarizes our income tax provision for continuing operations in 2007 and 2006:

| | | Year Ended December 31, | |

| (Amounts in thousands) | | 2007 | | 2006 | |

Income from continuing

operations before income taxes | | $ | 48,173 | | | $ | 46,391 | | |

| Provision for income taxes | | | 16,030 | | | | 13,746 | | |

| Income from continuing operations | | $ | 32,143 | | | $ | 32,645 | | |

| Effective tax rate | | | 33.3 | % | | | 29.6 | % | |

The increase in the effective tax rate from 2006 to 2007 is largely due to the discontinuation of a special deduction for U.S. export sales, partially offset by the phase-in of a new deduction for domestic production activities.

Our U.S. federal Net Operating Loss ("NOL") carryforward was fully utilized during 2007. We estimate our state NOL carryforwards are $30.3 million as of December 31, 2007. These carryforwards expire at various dates from 2008 through 2024. Additionally, we have a foreign tax credit carryforward of approximately $1.7 million that expires in 2010. We also have state tax credit carryforwards of approximately $0.2 million that expire at various dates from 2008 through 2021. Our federal research credits and alternative minimum tax credits are fully utilized as of December 31, 2007. The state NOL and other carryforwards are available to reduce cash taxes on future domestic taxable income, although a portion of the state NOL carryforwards are reduced by a valuation allowance reflecting the expectation that the carryforward period will expire before they can all be fully utilized.

Income from continuing operations in 2007 was $32.1 million, or $0.67 per diluted share, compared to $32.6 million, or $0.68 per diluted share, in 2006.

Income from discontinued operations in 2007 was $10.7 million, or $0.22 per diluted share, compared to $9.9 million, or $0.21 per diluted share in 2006. The 2007 results

BLOUNT INTERNATIONAL, INC.

15

consisted solely of our discontinued Forestry Division through the disposition date of November 5, 2007. Results for 2006 include both the full year of activity of our Forestry Division and activity of our discontinued Lawnmower segment through July 26, 2006. The Lawnmower segment, consisting of our former wholly-owned subsidiary, Dixon, was sold on July 27, 2006.

Discontinued operations are summarized as follows:

| | | Year Ended December 31, | |

| (Amounts in millions) | | 2007 | | 2006 | |

| Sales | | $ | 111.9 | | | $ | 196.8 | | |

| Operating income (loss) | | | (0.2 | ) | | | 2.7 | | |

| Gain on disposition of net assets | | | 26.0 | | | | 17.4 | | |

Income before taxes from

discontinued operations | | | 25.8 | | | | 20.1 | | |

| Income tax provision | | | 15.1 | | | | 10.2 | | |

| Income from discontinued operations | | $ | 10.7 | | | $ | 9.9 | | |

Sales by the Forestry Division were $111.9 million in 2007 and $167.3 million in 2006. The Forestry Division incurred a net loss of $0.2 million in 2007 and contributed $8.5 million to operating income in 2006. The decline in year-over-year sales and earnings was primarily due to a deepening of the cyclical downturn in the North American forest products equipment market in 2007, as well as charges of $4.5 million incurred in 2007 for employee severance, employee benefits, transition and closure costs. Included in operating income from the Forestry Division in 2006 is a charge of $1.2 million for costs to shut down one of the Forestry Division's three manufacturing plants. The 2007 results reflect the $26.0 million pretax gain on the disposal of the Forestry Division's net assets. The net cash proceeds received in 2007 from the sale of the Forestry Division were approximately $68.3 million and were used to reduce outstanding debt . We expect to incur cash expenditures of approximately $15.0 million in 2008 for the payment of income taxes on the gain, as well as other liabilities associated with the discontinued business.

Sales by the Lawnmower segment for the partial 2006 year were $29.5 million. The Lawnmower segment recognized a loss from operations in 2006 of $5.3 million. The 2006 loss from operations was primarily due to expenses necessary to finalize the closure of the facility, including the termination of the majority of the Lawnmower segment employees, and to facilitate the transfer of assets sold to the buyer. These results included compensation, severance and benefits costs, a charge to write down assets we retained (primarily the land and building) and other expenses. The 2006 results reflect the $17.4 million pretax gain on the disposal of the segment's net assets. The net cash proceeds from the sale of the Lawnmower segment were approximately $32.4 million and were used to reduce outstanding debt.

Segment Results. The following table reflects segment sales and operating income for 2007 and 2006:

| | | Year Ended December 31, | |

| (Amounts in thousands) | | 2007 | | 2006 | | 2007 as

% of 2006 | |

| Sales: | |

| Outdoor Products | | $ | 486,739 | | | $ | 455,009 | | | | 107 | % | |

| Corporate and other | | | 28,796 | | | | 32,485 | | | | 89 | % | |

| Total sales | | $ | 515,535 | | | $ | 487,494 | | | | 106 | % | |

| Operating income | |

| Outdoor Products | | $ | 95,932 | | | $ | 97,805 | | | | 98 | % | |

| Corporate and other | | | (15,232 | ) | | | (13,598 | ) | | | 112 | % | |

| Retirement plan redesign | | | – | | | | (3,747 | ) | | | – | | |

| Operating income | | $ | 80,700 | | | $ | 80,460 | | | | 100 | % | |

Outdoor Products Segment. Sales for the Outdoor Products segment increased $31.7 million (7%) in 2007 compared to 2006. Of this increase, $15.7 million was due to additional sales volume, primarily from an increase in sales of wood-cutting saw chain and outdoor equipment parts and, to a lesser extent, concrete-cutting saw chain. Improved price and product mix also contributed $7.9 million to the year-over-year sales increase. Fluctuations in foreign currency exchange rates added another $8.0 million to segment sales in 2007 compared to 2006. International sales grew nearly 12% year over year, while domestic sales decreased about 2%. Sales to OEMs increased by 4% ,while replacement sales increased 5%. Sales of concrete-cutting products increased $0.8 million (3%). Order backlog increased by $8.5 million to $63.3 million at December 31, 2007.

Segment contribution to operating income decreased $1.9 million (2%) in 2007 compared to 2006. The favorable effects of increased sales volume ($7.9 million) and improved price and mix ($7.9 million) were offset by higher product cost and mix ($12.4 million), higher SG&A expenses ($2.0 million) and the net unfavorable effect of fluctuations in foreign currency translation rates ($3.3 million). The higher product cost and mix, excluding the foreign currency exchange effect, includes inflationary pressures of higher wages and other conversion costs, higher freight and shipping costs, $1.1 million incurred to

BLOUNT INTERNATIONAL, INC.

16

consolidate the North American distribution center and $0.5 million in higher steel costs. The operating margin of 19.7% in 2007 compares to 21.5% in 2006.

Corporate and Other. The corporate and other category includes the activity of our gear components business, as well as the costs of certain centralized management and administrative functions. Sales of gear-related products decreased 11% from 2006 to 2007, with lower volume of $5.7 million partially offset by improved price and mix of $2.0 million. Weak market conditions in the construction and forestry equipment markets in the U.S. were partially offset by increased business in the utility equipment market. The contribution to operating income from our gear components business decreased $1.7 million (45%) year over year due to lower sales revenue. Corporate expense was flat year over year, with higher stock compensation costs ($0.7 million) and merit wage increases off-set by reduced legal and compliance costs.

Year ended December 31, 2006 compared to year ended December 31, 2005

The table below provides a summary of results and the primary contributing factors to the year over year change.

| (Amounts in millions) | | 2006 | | 2005 | | Change | | Contributing Factor | |

| Sales | | $ | 487.5 | | | $ | 478.8 | | | $ | 8.7 | | | | | | |

| | | | | | | | | | | | | | | $7.2 | | Sales volume | |

| | | | | | | | | | | | | | | 0.9 | | Price and mix | |

| | | | | | | | | | | | | | | 0.6 | | Foreign currency translation | |

| Gross profit | | | 173.7 | | | | 181.1 | | | | (7.4 | ) | | | | | |

| Gross margin | | | 35.6 | % | | | 37.8 | % | | | | | | 3.3 | | Sales volume | |

| | | | | | | | | | | | | | | 0.9 | | Selling price and mix | |

| | | | | | | | | | | | | | | (7.4) | | Product cost and mix | |

| | | | | | | | | | | | | | | (4.2) | | Foreign currency translation | |

| SG&A | | | 89.5 | | | | 89.5 | | | | 0.0 | | | | | | |

| | | | | | | | | | | | | | | 2.5 | | Stock compensation expense | |

| | | | | | | | | | | | | | | (2.1) | | Cash compensation expense | |

| | | | | | | | | | | | | | | (1.6) | | Legal and compliance costs | |

| | | | | | | | | | | | | | | 0.5 | | Depreciation and advertising | |

| | | | | | | | | | | | | | | 0.5 | | Foreign currency translation | |

| | | | | | | | | | | | | | | 0.2 | | Other, net | |

| Operating income | | | 80.5 | | | | 91.6 | | | | (11.1 | ) | | | | | |

| Operating margin | | | 16.5 | % | | | 19.1 | % | | | | | | (7.4) | | Decrease in gross profit | |

| | | | | | | | | | | | | | | (3.7) | | Retirement plan redesign | |

| Income from continuing operations | | | 32.6 | | | | 88.2 | | | | (55.6 | ) | | | | | |

| | | | | | | | | | | | | | | (11.1) | | Decrease in operating income | |

| | | | | | | | | | | | | | | 1.3 | | Decrease in net interest expense | |

| | | | | | | | | | | | | | | 2.3 | | Change in other income/expense | |

| | | | | | | | | | | | | | | (48.0) | | Change in income tax provision | |

| | | | | | | | | | | | | | | (0.1) | | Other, net | |

| Income from discontinued operations | | | 9.9 | | | | 18.4 | | | | (8.5 | ) | | | | | |

| | | | | | | | | | | | | | | 17.4 | | Gain on sale of net assets | |

| | | | | | | | | | | | | | | (26.7) | | Decrease in operating results | |

| | | | | | | | | | | | | | | 0.8 | | Decrease in income tax expense | |

| Net income | | $ | 42.5 | | | $ | 106.6 | | | $ | (64.1 | ) | | | | | |

Sales in 2006 increased $8.7 million (2%) from 2005, primarily due to higher sales volume. The Outdoor Products segment experienced a $2.7 million (1%) increase in sales during 2006 compared to 2005. Sales of our gear-related products increased $6.0 million (23%) from 2005 to 2006. International sales increased $6.9 million (2%) and domestic sales increased $2.2 million (1%). Included in the international sales increase is a $0.6 million favorable impact from movement in foreign currency exchange rates compared to 2005, primarily from the stronger Canadian Dollar. The relatively flat U.S. sales growth is attributed to weaker market conditions in the lawn care and forestry industries, offset by stronger sales of our gear-related products. Sales of concrete-cutting products increased 10% from 2005 to 2006, lead by new product introductions and improved market penetration.

Consolidated order backlog for continuing operations at December 31, 2006 was $61.3 million compared to $90.5 million at December 31, 2005. The year-over-year decline is primarily due to improved production capacity and related responsiveness to customer orders in our Outdoor Products segment, which lead to shorter lead times on

BLOUNT INTERNATIONAL, INC.

17

product delivery. We believe that prior to 2006, customers were ordering more than their short term needs to ensure product delivery.

Gross profit decreased $7.4 million (4%) from 2005 to 2006. Gross margin in 2006 was 35.6% of sales compared to 37.8% in 2005. Average selling prices increased slightly in 2006, primarily from shifts in product mix and price increases on selected products. The decrease related to product cost and mix includes the effect of higher energy costs for utilities, annual wage increases to our manufacturing employees and inflation on other cost elements. These product cost increases were partially offset by a decrease in steel costs estimated at $1.0 million compared to the previous year. Fluctuations in currency exchange rates decreased our gross profit in 2006 compared to 2005 by $4.2 million. The largest effects were in our plants in Canada and Brazil, which were impacted by higher manufacturing costs resulting from translation to the weaker U.S. Dollar estimated at $4.8 million. These higher translated costs were partially offset by a modest increase in sales, estimated at $0.6 million, due to currency exchange rates.

SG&A was $89.5 million in 2006 and in 2005. As a percent of sales, SG&A decreased slightly to 18.4% in 2006 compared to 18.7% in 2005. Stock-based compensation expense increased $2.5 million in 2006 following the adoption of a new accounting standard. Cash-based compensation decreased by $2.1 million year over year, reflecting lower incentive compensation cost and selected adjustments to work force levels partially offset by annual merit increases. Compliance-related and legal professional services decreased $1.6 million year-over-year. Depreciation and advertising expenses increased $0.5 million, primarily due to additional investments in infrastructure and administrative systems. International operating expenses increased $0.5 million from the prior year due to the weaker U.S. Dollar and its effect on the translation of foreign expenses.

Total expense recognized for our pension and other post-retirement plans was $14.3 million and $12.8 million for the years ended December 31, 2006 and 2005, respectively. These amounts, which include amounts charged to both continuing and discontinued operations, also include a pension curtailment charge of $3.6 million in 2006 to reflect the freezing of our U.S. defined benefit pension plan effective December 31, 2006 and the related write-off of unamortized prior service cost for plan participants. We also recognized an additional charge of $0.5 million for related fees and costs associated with the changes to our retirement plans.