Table of Contents

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 6-K

REPORT OF FOREIGN ISSUER

Pursuant to Rule 13a-16 or 15d-16 of

the Securities Exchange Act of 1934

For the month of May 2013

Eni S.p.A.

(Exact name of Registrant as specified in its charter)

Piazzale Enrico Mattei 1 - 00144 Rome, Italy

(Address of principal executive offices)

(Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F.)

Form 20-F x Form 40-F o

(Indicate by check mark whether the registrant by furnishing the information contained in this Form is also thereby furnishing the information to the Commission pursuant to Rule 12g3-2b under the Securities Exchange Act of 1934.)

Yes o No x

(If “Yes” is marked, indicate below the file number assigned to the registrant in connection with Rule 12g3-2(b): )

Table of Contents

Press Release dated May 10, 2013

Ordinary Shareholders’ Meeting Resolutions

Press Release dated May 28, 2013

Press Release dated May 30, 2013

Table of Contents

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, hereunto duly authorised.

| Eni S.p.A. | ||||

| Name: Antonio Cristodoro | ||||

| Title: | Head of Corporate Secretary's Staff Office | |||

Date: May 31, 2013

Table of Contents

Contents

Table of Contents

Contents

Table of Contents

Contents

Table of Contents

| I Fact Book 2012 | ||||||

| Contents | Eni’s Fact Book is a supplement to Eni’s 2012 Annual Report and is designed to provide supplemental financial and operating information. It contains certain forward-looking statements in particular under the section "Outlook" regarding capital expenditure, development and management of oil and gas resources, dividends, allocation of future cash flow from operations, future operating performance, gearing, targets of production and sale growth, new markets, and the progress and timing of projects. By their nature, forward-looking statements involve risks and uncertainties because they relate to events and depend on circumstances that will or may occur in the future. Actual results may differ from those expressed in such statements, depending on a variety of factors, including the timing of bringing new fields on stream; management’s ability in carrying out industrial plans and in succeeding in commercial transactions; future levels of industry product supply; demand and pricing; operational problems; general economic conditions; political stability and economic growth in relevant areas of the world; changes in laws and governmental regulations; development and use of new technology; changes in public expectations and other changes in business conditions; the actions of competitors and other factors discussed elsewhere in this document. | |||||

| 4 | Eni in 2012 | |||||

| 5 | Eni’s strategy | |||||

| 10 | Eni business model | |||||

| 14 | Exploration & Production | |||||

| 42 | Gas & Power | |||||

| 51 | Refining & Marketing | |||||

| 61 | Chemicals | |||||

| 65 | Engineering & Construction | |||||

| Tables | ||||||

| 71 | Financial Data | |||||

| 85 | Employees | |||||

| 86 | Supplemental oil and gas information | |||||

| 105 | Quarterly information I | |||||

Contents

Eni Fact Book Eni

![]()

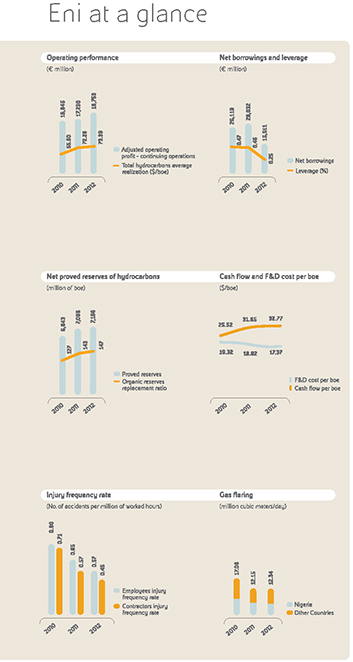

| Eni is an integrated company engaged in the energy chain. Eni’s strong presence in the gas market, our operations in LNG, our skills in the power generation and refinery activities, strengthened by world class skills in engineering and project management, allow us to catch opportunities in the market and to realize integrated projects. In 2012 adjusted net profit was euro 7.13 billion, up by 2.7% from a year ago. It was up by 7.6% when excluding Snam’s results included in the continuing operations1. These results were driven by an excellent performance reported by the Exploration & Production Division on the back of a recovery in Libyan production. Net cash generated by operating activities from continuing operations amounted to euro 12.36 billion and together with the robust proceeds from divestments enabled the Company to finance capital expenditure and other investments of euro 13.33 billion and to pay dividends to Eni’s shareholders and other minorities for euro 4.38 billion, while reducing net borrowings by euro 12.52 billion. Leverage decreased to 0.25 at December 31, 2012 from 0.46 at December 31, 2011. The Board of Directors proposed to the Shareholders’ Meeting the distribution of a dividend of euro 1.08 per share representing a 4% increase from 2011. In 2012, Eni continued its commitment in incident prevention also by means of training programs on safety and emergency prevention. For the seventh consecutive year the injury frequency rate relating to employees and contractors decreased by 12.3% and 21.1% respectively, compared to 2011. In 2012, the Exploration & Production Division reported adjusted net profit amounting to euro 7.43 billion (up 8.2% from 2011) driven by improved operating performance. Oil and natural gas production for the full year was 1,701 kboe/day (up 7% from 2011) sustained by the recovery of activities in Libya, | the start-up/ramp-up of fields, particularly in Russia and Australia, and higher production in Iraq. Net proved reserves at December 31, 2012 was an eight-year record at 7.17 bboe based on a reference Brent price of $111 per barrel. The organic reserves replacement ratio was 147% with a reserves life index of 11.5 years (12.3 years in 2011). All sources reserves replacement ratio was 107%. The Gas & Power Division reported adjusted net profit of euro 473 million, almost doubled from 2011 due to the benefits associated with the renegotiations of the supply contracts and the full recovery of Libyan supplies. Worldwide gas sales, net of Galp sales, maintained their levels supported by a strong presence in the Italian residential market and presence in strategic European markets of France and Germany/Austria in addition to increasing international sales of LNG. In a scenario weighted down by a steep fall in fuel demand in Italy, the Refining & Marketing Division managed to reduce adjusted operating loss by euro 85 million from 2011 (down euro 179 million). This result reflects the better operating performances and improved efficiency and performance of refineries. Results posted by the Marketing activity were impacted by falling demand for fuel, high competitive pressure and increased expenses associated with certain marketing initiatives including a special discount on prices at the pump during the summer week-ends. The average market share in Italy was 31.2%, up 0.7 percentage points from 2011. The Engineering & Construction sector reported adjusted net profit amounting to euro 1,109 million reflecting the robust operating performance recorded mainly in the Drilling businesses, while the Engineering & Construction business reported a decline. The Chemical sector reported a significant increase in adjusted net loss (euro 395 million, down euro 189 million) from 2011, due to a weak trend in demand for commodities reflecting the economic downturn and a fall in unit margins. |

(1) The Snam contribution excluded is the result of Snam transactions with Eni included in the continuing operations according to IFRS 5. Adjusted operating profit and adjusted net profit are not provided by IFRS.

- 4 -

Contents

Eni Fact Book Eni

![]()

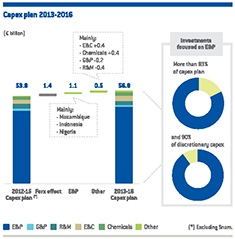

| The energy market has become even more challenging on the back of the uncertainty of the macro-economic scenario, mainly in Europe, recent trends in demand even more hinged on emerging Countries and discoveries of high potential basins for hydrocarbon production. Against this backdrop, Eni’s strategy for the 2013-2016 four-year period confirms the priorities of profitably growing oil and gas production, recovering profitability in the downstream gas sector, improving efficiency in the downstream oil and in the chemical sector. Eni believes that a sustainable business conduct contributes to both the achievement of industrial performance, and the mitigation of political, financial and operational risks. This strengthens Eni’s role as a trustworthy and reliable partner, who is ready to capture new opportunities in the marketplace and able to manage the complexities of the environment. Following the divestment of Snam and other portfolio operations, Eni has strengthened its financial structure reaching a leverage of 0.25. Net cash generated by operating activities and portfolio management will enable Eni to finance the planned relevant capital expenditure to fuel long-term growth (euro 56.8 billion) and to remunerate Eni’s shareholders.

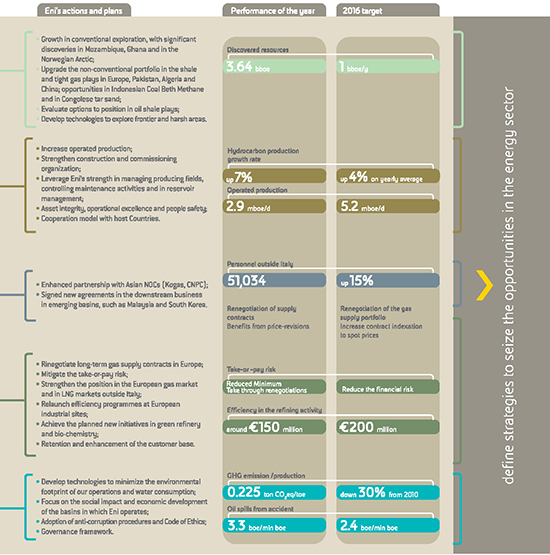

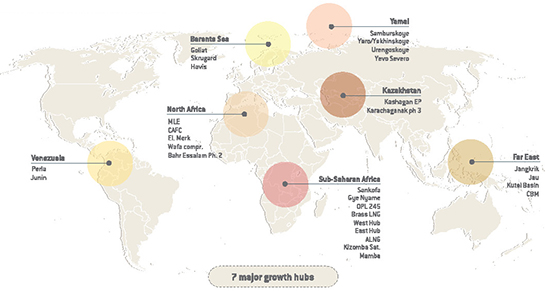

Business strategies and targets In Exploration & Production, Eni confirms its strategy of organic growth focused on exploration and reserve replacement as major drivers for value creation. Growth will be fuelled by new production | additions in Eni’s core areas (North and Sub-Saharan Africa, Venezuela, Barents Sea, Yamal Peninsula, Kazakhstan, Iraq and the Far East) leveraging Eni’s vast knowledge of reservoirs and geological basins, technical and producing synergies, as well as established partnerships with producing Countries. Average production growth is expected at a rate of more than 4% in the 2013-2016 period, supported by the development of core areas (Sub-Saharan Africa, and in particular Mozambique, Venezuela, Barents Sea, Yamal Peninsula in Russia, Kazakhstan, Iraq and Indonesia). Growth will be associated to increased profitability and risk management reducing time to market (more than 90% of the discoveries made in 2008-2012 will reach production within 8 years from their discovery) and retaining large volumes of operated production, in order to directly manage schedules and budget costs of development projects. Technological innovation and the application of proprietary technologies will allow to reach cost efficiency and acquire key competences for supporting increasing production and recovery rates, developing drilling techniques to be applied in complex environments, marginal areas and deep and ultra-deep waters. This growth strategy will be supported by the mitigation of operational, political, Country and environmental risks.

Eni confirms its commitment to improving the safety of employees and contractors, strengthening the tools for management, training and control, and ensuring asset integrity and process security. Environmental impact targets include the containment of accidental oil spills from 2.9 boe/mmboe to 2.4 boe/mmboe by 2016, an over 30% reduction in GHG emission rates in the E&P segment for each thousand of toe of gross operated production by 2015 as compared to 2010 deploying flaring down policies especially in Africa and energy efficiency programs. Projects for production water reinjection will lead to a rate of reinjection of 65% of total water produced by 2016. |

- 5 -

Contents

Eni Fact Book Eni

| In the Gas & Power Division, Eni intends to recover profitability leveraging on (i) a competitive and flexible cost position thanks to contract renegotiation; (ii) an expansion in gas sales in Italy through its sales force, diversified offer of innovative products and best-in-class services, mainly to the retail segment; (iii) a selective development in activities outside Italy, focusing on more profitable segments and increasing LNG sales in profitable markets outside Europe. In the 2013-2016 period Eni intends to preserve its market share in Italy and abroad taking account of the expected increase in supply and logistics costs implementing efficient marketing initiatives.

Management intends to reach a greater integration of trading and commodity price risk management with the supply activities and the non-retail commercial sales of gas and LNG to fully centralize and optimize Eni’s commodity risk exposure in markets characterized by more and more evolved counterparties. In Refining & Marketing, Eni expects to gradually recover profitability throughout the plan period leveraging on optimization of industrial plants and of logistics operations by means of higher flexibility, process integration and efficiency; selective investments targeting to upgrade conversion capacity and asset integrity; the conversion of the Venice plant into a "bio-refinery" to produce bio-fuels; cost reduction programs.

| In Chemical segment Eni confirms its strategy of progressively reducing the exposure to loss-making commodity chemicals while at the same time developing innovative and niche productions which are expected to yield better returns such as elastomers and the expansion of the specialties segment. Eni intends to grow the green-chemistry business leveraging on the ongoing project of converting its Porto Torres site in a modern plant for the manufacture of eco-compatible chemical products. The recent strategic alliances in Asia, supported by our technological know-how and the enhancement of Eni’s proprietary technology platform confirm a greater internationalization of our business, projecting it towards markets characterized by high-growth demand rates.

In the Engineering & Construction segment, Eni confirms its target of consolidating the global competitive position achieved in the offshore and onshore businesses and its role as high-quality niche player in the deepwater drilling business. Saipem will leverage on the enhancement of the EPC(I)-oriented business model, its world-class technology, engineering and delivering skills, its strong local presence and established relationships with oil Majors and National Oil Companies. |

- 6 -

Contents

Eni Fact Book Eni

Main data

Key financial data (a) | 2003 (*) | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 |

| Net sales from operations | 51,487 | 57,498 | 73,692 | 86,071 | 87,204 | 108,082 | 83,227 | 98,523 | 109,589 | 128,592 | |||||||||||||||||||||

| of which: continuing operations | 106,978 | 81,932 | 96,617 | 107,690 | 127,220 | ||||||||||||||||||||||||||

| Group operating profit | 9,517 | 12,399 | 16,664 | 19,336 | 18,739 | 18,517 | 12,055 | 16,111 | 17,435 | 15,914 | |||||||||||||||||||||

| Special items | (448 | ) | (1,210 | ) | 88 | (620 | ) | 2,034 | 1,295 | 2,290 | 1,567 | 4,795 | |||||||||||||||||||

| Profit (loss) on stock | 631 | 1,942 | 1,059 | 885 | 936 | (345 | ) | (881 | ) | (1,113 | ) | (17 | ) | ||||||||||||||||||

| Group adjusted operating profit | 9,958 | 12,582 | 17,396 | 20,483 | 19,004 | 21,487 | 13,005 | 17,520 | 17,889 | 20,692 | |||||||||||||||||||||

| Adjusted operating profit - continuing operations | 21,322 | 12,722 | 16,845 | 17,230 | 19,753 | ||||||||||||||||||||||||||

| Exploration & Production | 5,973 | 8,202 | 12,649 | 15,521 | 13,770 | 17,166 | 9,489 | 13,898 | 16,075 | 18,518 | |||||||||||||||||||||

| Gas & Power | 3,661 | 3,448 | 3,783 | 4,117 | 4,414 | 1,778 | 2,022 | 1,268 | (247 | ) | 354 | ||||||||||||||||||||

| Refining & Marketing | 584 | 923 | 1,210 | 794 | 292 | 555 | (381 | ) | (181 | ) | (539 | ) | (328 | ) | |||||||||||||||||

| Chemicals | (54 | ) | 263 | 261 | 219 | 116 | (382 | ) | (441 | ) | (96 | ) | (273 | ) | (485 | ) | |||||||||||||||

| Engineering & Construction | 311 | 215 | 314 | 508 | 840 | 1,041 | 1,120 | 1,326 | 1,443 | 1,465 | |||||||||||||||||||||

| Other activities | (236 | ) | (223 | ) | (296 | ) | (299 | ) | (207 | ) | (244 | ) | (258 | ) | (205 | ) | (226 | ) | (224 | ) | |||||||||||

| Corporate and financial companies | (281 | ) | (187 | ) | (384 | ) | (244 | ) | (195 | ) | (282 | ) | (342 | ) | (265 | ) | (266 | ) | (329 | ) | |||||||||||

| Impact of unrealized intragroup profit elimination and consolidation adjustments | (59 | ) | (141 | ) | (133 | ) | (26 | ) | 1,690 | 1,513 | 1,100 | 1,263 | 782 | ||||||||||||||||||

| Adjusted operating profit - discontinued operations | 165 | 283 | 675 | 659 | 939 | ||||||||||||||||||||||||||

| Group net profit | 5,585 | 7,059 | 8,788 | 9,217 | 10,011 | 8,825 | 4,367 | 6,318 | 6,860 | 7,788 | |||||||||||||||||||||

| of which: continuing operations | 8,996 | 4,488 | 6,252 | 6,902 | 4,198 | ||||||||||||||||||||||||||

| of which: discontinued operations | (171 | ) | (121 | ) | 66 | (42 | ) | 3,590 | |||||||||||||||||||||||

| Group adjusted net profit | 5,096 | 6,645 | 9,251 | 10,401 | 9,569 | 10,164 | 5,207 | 6,869 | 6,969 | 7,323 | |||||||||||||||||||||

| of which: continuing operations | 10,315 | 5,321 | 6,770 | 6,938 | 7,128 | ||||||||||||||||||||||||||

| of which: discontinued operations | (151 | ) | (114 | ) | 99 | 31 | 195 | ||||||||||||||||||||||||

| Net cash provided by operating activities | 10,827 | 12,500 | 14,936 | 17,001 | 15,517 | 21,801 | 11,136 | 14,694 | 14,382 | 12,371 | |||||||||||||||||||||

| of which: continuing operations | 21,506 | 10,755 | 14,140 | 13,763 | 12,356 | ||||||||||||||||||||||||||

| of which: discontinued operations | 295 | 381 | 554 | 619 | 15 | ||||||||||||||||||||||||||

| Capital expenditure | 8,802 | 7,499 | 7,414 | 7,833 | 10,593 | 14,562 | 13,695 | 13,870 | 13,438 | 13,517 | |||||||||||||||||||||

| of which: continuing operations | 12,935 | 12,216 | 12,450 | 11,909 | 12,761 | ||||||||||||||||||||||||||

| of which: discontinued operations | 1,627 | 1,479 | 1,420 | 1,529 | 756 | ||||||||||||||||||||||||||

| Shareholders’ equity including non-controlling interest | 28,318 | 35,540 | 39,217 | 41,199 | 42,867 | 48,510 | 50,051 | 55,728 | 60,393 | 62,713 | |||||||||||||||||||||

| Net borrowings | 13,543 | 10,443 | 10,475 | 6,767 | 16,327 | 18,376 | 23,055 | 26,119 | 28,032 | 15,511 | |||||||||||||||||||||

| Leverage | 0.48 | 0.29 | 0.27 | 0.16 | 0.38 | 0.38 | 0.46 | 0.47 | 0.46 | 0.25 | |||||||||||||||||||||

| Net capital employed | 41,861 | 45,983 | 49,692 | 47,966 | 59,194 | 66,886 | 73,106 | 81,847 | 88,425 | 78,224 | |||||||||||||||||||||

| Exploration & Production | 17,340 | 16,770 | 19,109 | 17,783 | 23,826 | 31,362 | 32,455 | 37,646 | 42,024 | 42,445 | |||||||||||||||||||||

| Gas & Power | 15,617 | 19,554 | 20,075 | 19,713 | 21,333 | 9,636 | 11,024 | 12,931 | 12,367 | 11,135 | |||||||||||||||||||||

| Snam | 11,918 | 13,730 | 14,415 | 15,393 | |||||||||||||||||||||||||||

| Refining & Marketing | 5,089 | 5,081 | 5,993 | 5,631 | 7,675 | 7,379 | 8,105 | 8,321 | 9,188 | 8,876 | |||||||||||||||||||||

| Chemicals | 1,821 | 2,076 | 2,018 | 1,953 | 2,228 | 1,915 | 1,774 | 1,978 | 2,252 | 2,569 | |||||||||||||||||||||

| Engineering & Construction | 2,119 | 2,403 | 2,844 | 3,399 | 4,313 | 5,022 | 6,566 | 7,610 | 8,217 | 10,020 | |||||||||||||||||||||

| Corporate financial companies and other activities | (125 | ) | 277 | 2 | (95 | ) | 294 | 24 | (192 | ) | (527 | ) | (393 | ) | 3,682 | ||||||||||||||||

| Impact of unrealized intragroup profit elimination | (178 | ) | (349 | ) | (418 | ) | (475 | ) | (370 | ) | (356 | ) | (527 | ) | (623 | ) | (503 | ) | |||||||||||||

(*) Financial data for 2003 were prepared in accordance to Italian Gaap.

(a) Following the divestment of Regulated Businesses in Italy, results of Snam have been accounted as "discontinued operations". Results for the 2008-2011 period have been restated accordingly.

Key market indicators | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 |

| Average price of Brent dated crude oil (a) | 28.84 | 38.22 | 54.38 | 65.14 | 72.52 | 96.99 | 61.51 | 79.47 | 111.27 | 111.58 | ||||||||||||

| Average EUR/USD exchange rate (b) | 1.131 | 1.244 | 1.244 | 1.256 | 1.371 | 1.471 | 1.393 | 1.327 | 1.392 | 1.285 | ||||||||||||

| Average price in euro of Brent dated crude oil | 25.50 | 30.72 | 43.71 | 51.86 | 52.90 | 65.93 | 44.16 | 59.89 | 79.94 | 86.83 | ||||||||||||

| Average European refining margin (c) | 2.65 | 4.35 | 5.78 | 3.79 | 4.52 | 6.49 | 3.13 | 2.66 | 2.06 | 4.83 | ||||||||||||

| Average European refining margin Brent/Ural (c) | 3.40 | 7.03 | 8.33 | 6.50 | 6.45 | 8.85 | 3.56 | 3.47 | 2.90 | 4.94 | ||||||||||||

| Euribor - three-month euro rate | (%) | 2.3 | 2.1 | 2.2 | 3.1 | 4.3 | 4.6 | 1.2 | 0.8 | 1.4 | 0.6 | |||||||||||

(a) In US dollars per barrel. Source: Platt’s Oilgram.

(b) Source: ECB.

(c) In US dollars per barrel FOB Mediterranean Brent dated crude oil. Source: Eni calculations based on Platt’s Oilgram data.

- 7 -

Contents

| Eni Fact Book Eni |

Selected operating data | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 |

| Corporate (a) | ||||||||||||||||||||||

| Employees at period end | (number) | 76,529 | 71,572 | 71,773 | 72,850 | 75,125 | 71,714 | 71,461 | 73,768 | 72,574 | 77,838 | |||||||||||

| of which: - women | 11,155 | 10,326 | 10,620 | 10,841 | 10,977 | 11,611 | 11,955 | 12,161 | 12,542 | 12,860 | ||||||||||||

| of which: - outside Italy | 36,678 | 32,691 | 34,036 | 35,818 | 38,634 | 41,971 | 42,633 | 45,967 | 45,516 | 51,034 | ||||||||||||

| Female managers | (%) | 10.9 | 12.5 | 12.4 | 13.5 | 14.1 | 16.3 | 17.3 | 18.0 | 18.5 | 18.9 | |||||||||||

| Employee injury frequency rate | (number of injuries/million of worked hours) | 3.79 | 3.99 | 2.74 | 2.45 | 1.93 | 1.22 | 0.84 | 0.80 | 0.65 | 0.57 | |||||||||||

| Contractor injury frequency rate | 4.12 | 7.84 | 2.59 | 1.54 | 1.45 | 1.09 | 0.97 | 0.71 | 0.57 | 0.45 | ||||||||||||

| Fatality index | (fatal injuries per one hundred million of worked hours) | 5.51 | 5.64 | 3.38 | 2.31 | 2.97 | 2.75 | 1.20 | 4.77 | 1.94 | 1.10 | |||||||||||

| Oil spills | (barrels) | 857 | 7,813 | 6,908 | 6,151 | 6,731 | 4,749 | 6,259 | 4,269 | 7,295 | 3,856 | |||||||||||

| Oil spills due to sabotage and terrorism | n.a. | n.a. | 1,810 | 7,014 | 2,608 | 2,286 | 15,288 | 18,695 | 7,657 | 8,384 | ||||||||||||

| GHG emission | (mmtonnes CO2 eq) | 52.27 | 58.34 | 61.85 | 60.72 | 67.25 | 59.59 | 55.49 | 58.26 | 49.12 | 52.49 | |||||||||||

| R&D expenditures (b) | (euro million) | 238 | 257 | 204 | 222 | 208 | 211 | 233 | 218 | 190 | 211 | |||||||||||

| Exploration & Production | ||||||||||||||||||||||

| Proved reserves of hydrocarbons at period end | (mmboe) | 7,272 | 7,218 | 6,837 | 6,436 | 6,370 | 6,600 | 6,571 | 6,843 | 7,086 | 7,166 | |||||||||||

| Reserve life index | (years) | 12.7 | 12.1 | 10.8 | 10.0 | 10.0 | 10.0 | 10.2 | 10.3 | 12.3 | 11.5 | |||||||||||

| Hydrocarbons production (c) | (kboe/d) | 1,562 | 1,624 | 1,737 | 1,770 | 1,736 | 1,797 | 1,769 | 1,815 | 1,581 | 1,701 | |||||||||||

| Gas & Power | ||||||||||||||||||||||

| Sales of consolidated companies (including own consumption) | (bcm) | 71.39 | 76.49 | 82.62 | 85.76 | 84.83 | 89.32 | 89.60 | 82.00 | 84.37 | 84.67 | |||||||||||

| Sales of Eni’s affiliates (Eni’s share) | 6.94 | 5.84 | 7.08 | 7.65 | 8.74 | 8.91 | 7.95 | 9.41 | 9.53 | 7.92 | ||||||||||||

| Total sales and own consumption (G&P) | 78.33 | 82.33 | 89.70 | 93.41 | 93.57 | 98.23 | 97.55 | 91.41 | 93.90 | 92.59 | ||||||||||||

| E&P gas sales (c) | 4.70 | 4.51 | 4.69 | 5.39 | 6.00 | 6.17 | 5.65 | 2.86 | 2.73 | |||||||||||||

| Worldwide gas sales | 78.33 | 87.03 | 94.21 | 98.10 | 98.96 | 104.23 | 103.72 | 97.06 | 96.76 | 95.32 | ||||||||||||

| Electricity sold | (TWh) | 8.65 | 16.95 | 27.56 | 31.03 | 33.19 | 29.93 | 33.96 | 39.54 | 40.28 | 42.58 | |||||||||||

| Refining & Marketing | ||||||||||||||||||||||

| Throughputs on own account | (mmtonnes) | 35.43 | 37.69 | 38.79 | 38.04 | 37.15 | 35.84 | 34.55 | 34.80 | 31.96 | 30.01 | |||||||||||

| Balanced capacity of wholly-owned refineries at period end | (kbbl/d) | 504 | 504 | 524 | 534 | 544 | 737 | 747 | 757 | 767 | 767 | |||||||||||

| Sales of refined products | (mmtonnes) | 50.43 | 53.54 | 51.63 | 51.13 | 50.15 | 49.16 | 45.59 | 46.80 | 45.02 | 48.33 | |||||||||||

| Retail sales in Europe | (mmtonnes) | 14.01 | 14.40 | 12.42 | 12.48 | 12.65 | 12.03 | 12.02 | 11.73 | 11.37 | 10.87 | |||||||||||

| Service stations at year end | (number) | 10,647 | 9,140 | 6,282 | 6,294 | 6,440 | 5,956 | 5,986 | 6,167 | 6,287 | 6,384 | |||||||||||

| Average throughput per service station | (kliters/y) | 1,771 | 1,970 | 2,479 | 2,470 | 2,486 | 2,502 | 2,477 | 2,353 | 2,206 | 2,064 | |||||||||||

| Chemicals | ||||||||||||||||||||||

| Production | (ktonnes) | 6,907 | 7,118 | 7,282 | 7,072 | 8,795 | 7,372 | 6,521 | 7,220 | 6,245 | 6,090 | |||||||||||

| of which: - Intermediates | 4,014 | 4,236 | 4,450 | 4,275 | 5,688 | 5,110 | 4,350 | 4,860 | 4,101 | 4,112 | ||||||||||||

| of which: - Polymers | 2,893 | 2,882 | 2,832 | 2,797 | 3,107 | 2,262 | 2,171 | 2,360 | 2,144 | 1,978 | ||||||||||||

| Average plant utilization rate | (%) | 71.3 | 75.2 | 78.4 | 76.4 | 80.6 | 68.6 | 65.4 | 72.9 | 65.3 | 66.7 | |||||||||||

| Engineering & Construction | ||||||||||||||||||||||

| Orders acquired | (euro million) | 5,876 | 5,784 | 8,395 | 11,172 | 11,845 | 13,860 | 9,917 | 12,935 | 12,505 | 13,391 | |||||||||||

| Order backlog at year end | 9,405 | 8,521 | 10,122 | 13,191 | 15,390 | 19,105 | 18,370 | 20,505 | 20,417 | 19,739 | ||||||||||||

| (a) Following the divestment of Regulated Businesses in Italy, data for the year 2012 do not include Snam contribution. Results for the 2008-2011 period have been restated accordingly. (b) Net of general and administrative costs. (c) From July 1, 2012, Eni has updated the natural gas conversion factor from 5,550 to 5,490 standard cubic feet of gas per barrel of oil equivalent. The effect of this update on production expressed in boe was 9 kboe/d for the full-year 2012 and on the initial reserves balance as of January 1, 2011, amounted to 40 mmboe. Other per-boe indicators were only marginally affected by the update (e.g. realization prices, costs per boe) and also negligible was the impact on depletion charges. Other oil companies use different conversion rates. |

Share data | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 |

| Net profit (a) (b) | (euro) | 1.48 | 1.87 | 2.34 | 2.49 | 2.73 | 2.43 | 1.21 | 1.74 | 1.89 | 2.15 | |||||||||||

| Net profit - continuing operations (a) (b) (*) | 2.47 | 1.24 | 1.72 | 1.90 | 1.16 | |||||||||||||||||

| Dividend | 0.75 | 0.90 | 1.10 | 1.25 | 1.30 | 1.30 | 1.00 | 1.00 | 1.04 | 1.08 | ||||||||||||

| Dividend pertaining to the year (c) | (euro million) | 2,828 | 3,384 | 4,086 | 4,594 | 4,750 | 4,714 | 3,622 | 3,622 | 3,695 | 3,840 | |||||||||||

| Cash flow | (euro) | 2.87 | 3.31 | 3.97 | 4.59 | 4.23 | 5.99 | 3.07 | 4.06 | 3.97 | 3.41 | |||||||||||

| Dividend yield (d) | (%) | 5.1 | 4.9 | 4.7 | 5.0 | 5.3 | 7.6 | 5.8 | 6.1 | 6.6 | 5.9 | |||||||||||

| Net profit per ADR (e) | (US$) | 3.72 | 4.66 | 5.81 | 6.26 | 7.49 | 7.27 | 3.45 | 4.59 | 5.29 | 2.98 | |||||||||||

| Dividend per ADR (e) | 1.83 | 2.17 | 2.74 | 3.14 | 3.56 | 3.82 | 2.79 | 2.65 | 2.90 | 2.78 | ||||||||||||

| Cash flow per ADR (e) | 7.22 | 8.96 | 9.40 | 11.53 | 11.60 | 17.63 | 8.56 | 10.77 | 11.05 | 8.78 | ||||||||||||

| Dividend yield per ADR (d) | (%) | 5.0 | 5.0 | 4.7 | 5.0 | 5.3 | 7.6 | 5.8 | 6.1 | 6.6 | 5.8 | |||||||||||

| Pay-out | 51 | 48 | 46 | 50 | 47 | 53 | 81 | 57 | 55 | 50 | ||||||||||||

| Number of shares at period end representing share capital | (million shares) | 4,002.9 | 4,004.4 | 4,005.4 | 4,005.4 | 4,005.4 | 4,005.4 | 4,005.4 | 4,005.4 | 4,005.4 | 3,634.2 | |||||||||||

| Average number of share outstanding in the year (f) (fully diluted) | 3,778.4 | 3,771.7 | 3,763.4 | 3,701.3 | 3,669.2 | 3,638.9 | 3,622.4 | 3,622.5 | 3,622.7 | 3,622.8 | ||||||||||||

| TSR | (%) | 4.3 | 28.5 | 35.3 | 14.8 | 3.2 | (29.1 | ) | 13.7 | (2.2 | ) | 5.1 | 22.0 | |||||||||

| (*) Following the divestment of Regulated Businesses in Italy, results of Snam have been accounted for as "discontinued operations", based on IFRS 5. Results for the 2008-2011 period have been restated accordingly. Net profit refers to results of continuing operations as reported in Eni consolidated annual report. (a) Calculated on the average number of Eni shares outstanding during the year. (b) Pertaining to Eni’s shareholders. (c) Amounts due on the payment of the balance of 2012 dividend are estimated. (d) Ratio between dividend of the year and average share price in December. (e) One ADR represents 2 shares. Net profit, dividends and cash flow data were converted using average exchange rates. Dividends data were converted at the Noon Buying Rate of the pay-out date. (f) Calculated by excluding own shares in portfolio. |

- 8 - |

Contents

Eni Fact Book Eni

Share information | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 |

| Share price - Milan Stock Exchange | ||||||||||||||||||||||

| High | (euro) | 15.75 | 18.75 | 24.96 | 25.73 | 28.33 | 26.93 | 18.35 | 18.56 | 18.42 | 18.70 | |||||||||||

| Low | 11.88 | 14.72 | 17.93 | 21.82 | 22.76 | 13.80 | 12.30 | 14.61 | 12.17 | 15.25 | ||||||||||||

| Average | 13.64 | 16.94 | 21.60 | 23.83 | 25.10 | 21.43 | 16.59 | 16.39 | 15.95 | 17.18 | ||||||||||||

| End of the period | 14.96 | 18.42 | 23.43 | 25.48 | 25.05 | 16.74 | 17.80 | 16.34 | 16.01 | 18.34 | ||||||||||||

| ADR price (a) - New York Stock Exchange | ||||||||||||||||||||||

| High | (US$) | 94.98 | 126.45 | 151.35 | 67.69 | 78.29 | 84.14 | 54.45 | 53.89 | 53.74 | 49.44 | |||||||||||

| Low | 66.15 | 92.35 | 118.50 | 54.65 | 60.22 | 37.22 | 31.07 | 35.37 | 32.98 | 36.85 | ||||||||||||

| Average | 77.44 | 105.60 | 134.02 | 59.97 | 68.80 | 63.38 | 46.36 | 43.56 | 44.41 | 44.24 | ||||||||||||

| End of the period | 94.98 | 125.84 | 139.46 | 67.28 | 72.43 | 47.82 | 50.61 | 43.74 | 41.27 | 49.14 | ||||||||||||

| Average daily exchanged shares | (million shares) | 22.0 | 20.0 | 28.5 | 26.2 | 30.5 | 28.7 | 27.9 | 20.7 | 22.9 | 15.6 | |||||||||||

| Value | (euro million) | 298.5 | 338.7 | 620.7 | 619.1 | 773.1 | 610.4 | 461.6 | 336.0 | 355.0 | 267.0 | |||||||||||

| Number of shares outstanding at period end (b) | (million shares) | 3,772.3 | 3,770.0 | 3,727.3 | 3,680.4 | 3,656.8 | 3,622.4 | 3,622.4 | 3,622.7 | 3,622.7 | 3,622.8 | |||||||||||

| Market capitalization (c) | ||||||||||||||||||||||

| EUR | (billion) | 56.4 | 69.4 | 87.3 | 93.8 | 91.6 | 60.6 | 64.5 | 59.2 | 58.0 | 66.4 | |||||||||||

| USD | 71.1 | 94.9 | 104.0 | 123.8 | 132.4 | 86.6 | 91.7 | 79.2 | 75.0 | 87.7 | ||||||||||||

(a) Effective January 10, 2006 a 5:2 stock split was made. Previous period’s prices have not been restated.

(b) Excluding treasury shares.

(c) Number of outstanding shares by reference price at period end.

Data on Eni share placement | 1995 | 1996 | 1997 | 1998 | 2001 |

| Offer price | (euro/share) | 5.42 | 7.40 | 9.90 | 11.80 | 13.60 | |||||||

| Number of share placed | (million shares) | 601.9 | 647.5 | 728.4 | 608.1 | 200.1 | |||||||

| of which: through bonus share | 1.9 | 15.0 | 24.4 | 39.6 | |||||||||

| Percentage of share capital (a) | (%) | 15.0 | 16.2 | 18.2 | 15.2 | 5.0 | |||||||

| Proceeds | (euro million) | 3,254 | 4,596 | 6,869 | 6,714 | 2,721 | |||||||

(a) Refers to share capital at December 31, 2012.

- 9 -

Contents

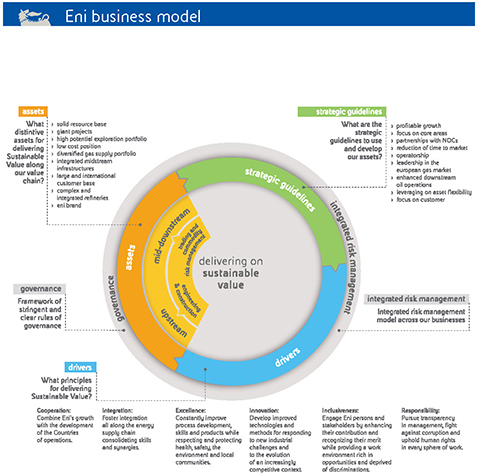

Eni Fact Book Eni business model

| Eni’s excellent market position and competitive advantages derive from the Company’s strategic decision-making which is consistent with the long-term nature of the business, and relies on a sustainable business model fonde on a consolidated and distinctive way of doing business, in a frame work of clear and straightforward rules of corporate governance and respectful of the highest ethical standards and rigorous risk management. Eni’s strategies, decisions in terms of resource allocation and day-by-day operations underpin sustainable value creation to shareholders and, more generally, all of our stakeholders: the host communities where we work through our contribution to socio-economic standards improvement and responsibly using resources; our people to whom we dedicate our best efforts to preserve health and safety of the workplace and to enhance each individual’s contribution and diversity; our suppliers, partners and public administrations with whom we interact by running our | operations in a transparent manner, respecting human rights and tackling with corruption; finally our clients to whom we offer competitive and up with the times commercial choices and high quality services. In 2012 Eni laid the foundations for a new growth phase of its oil and gas production tank to numerous exploration successes, the entry in new Countries and the management of activities in well established Countries of activity. These results are based on the great attention paid to the specific features of the Countries where Eni operates and thus on cooperation for their development. Starting from an assessment of their potential Eni promotes partnerships providing local people new opportunities for growth and development. This is a competitive lever in the Countries where Eni’s experience is more recent but |

- 10 -

Contents

Eni Fact Book Eni business model

| also in more established areas. In each one of them our objective is to create high quality jobs targeted at local resources on an equal opportunity basis. The culture of plurality is a distinctive feature of Eni’s strongly internationally oriented business model. The inclusion of all Eni people with their diversity merges with the protection of health and safety on the workplace, with the professional development and engagement in the company’s objectives. Eni guarantees equal treatment to its entire people defining worldwide remuneration policies and committing itself and its suppliers to the respect of the basic workers’ rights in all the Countries of operation. Responsibility is assumed as commitment to transparency and anticorruption practices while respecting human rights in all areas and promoting the development of Countries and their society. In deploying its activities, Eni activates a flow of resources that can prove crucial for economic growth. Only a strict discipline of integrity and promotion of transparency, in particular as concerns payments to producing Countries can protect from corruption and build the basis for a proper use of these resources aimed at sustainable development. The ultimate aim of sustainable growth is upheld by Eni through a way of operating based on operating excellence that leverages on best practices, quality systems, advanced and high quality technologies to guarantee full respect of communities and their environment. A safe management of plants and the mitigation of risks represent a prerequisite for a proper environmental management and for the reduction of environmental impacts. | The exploration of frontier areas and territories that are considered difficult and environmentally sensitive are the result not only of Eni’s drive to development while applying new technologies but also of a responsible and sustainable corporate strategy. Eni’s presence worldwide in the most sensitive areas was made possible by technological innovation and the application of advanced methodologies that allow work also in harsh contexts guaranteeing the protection of the environments and the conservation of sensitive ecosystems and biodiversity. Lastly, as an integrated energy company, Eni works alongside governments of producing Countries in planning and designing solutions for the development of local energy systems, cooperating with national companies in the development of energy sources and building infrastructure for their use and monetization. One of the main actions performed concerns the fight against energy poverty in particular in Sub-Saharan Africa with the support of the development of local technologies and the reduction of waste where infrastructure already exist. |

Safety | 2008 | 2009 | 2010 | 2011 | 2012 |

| Injury frequency rate | (number of injuries/million of worked hours) | 1.14 | 0.92 | 0.75 | 0.60 | 0.49 | ||||||

| - employees | 1.22 | 0.84 | 0.80 | 0.65 | 0.57 | |||||||

| - contractors | 1.09 | 0.97 | 0.71 | 0.57 | 0.45 | |||||||

| Fatality index | (fatal injuries/one hundred million of worked hours) | 2.75 | 1.20 | 4.77 | 1.94 | 1.10 | ||||||

| - employees | 2.55 | 0.89 | 6.66 | 1.19 | 0.87 | |||||||

| - contractors | 2.85 | 1.40 | 3.55 | 2.38 | 1.23 | |||||||

| Safety expenditure and investments | (euro thousand) | 407,930 | 487,660 | 260,434 | 320,117 | 370,559 | ||||||

| Professional illnesses reported | (number) | 82 | 123 | 184 | 135 | 71 | ||||||

| Health and hygiene expenditure and investments | (euro thousand) | 66,601 | 78,219 | 55,070 | 78,950 | 48,156 | ||||||

Spending for the territory | (euro million) | 2008 | 2009 | 2010 | 2011 | 2012 |

| Total spending for the territory | 85.9 | 97.7 | 107.2 | 100.9 | 90.6 | |||||||

| - of which project investments | 69.4 | 70.4 | 75.4 | 69.3 | 63.1 | |||||||

| - of which short-term investments and donations | 0.5 | 0.9 | 4.4 | 0.9 | 3.4 | |||||||

| - of which association memberships fees | 1.5 | 1.5 | 1.6 | 1.6 | 1.8 | |||||||

| - of which contributions to the Eni Foundation | - | 5.0 | 5.0 | 3.0 | - | |||||||

| - of which sponsorships for the territory | 11.4 | 16.2 | 17.1 | 22.4 | 18.6 | |||||||

| - of which contributions to the Eni Enrico Mattei Foundation | 3.2 | 3.7 | 3.7 | 3.7 | 3.7 | |||||||

- 11 -

Contents

Eni Fact Book Eni business model

Employment | 2008 | 2009 | 2010 | 2011 | 2012 |

| Employees as of December 31 | (number) | 71,714 | 71,461 | 73,768 | 72,574 | 77,838 | ||||||

| - men | 60,103 | 59,506 | 61,607 | 60,032 | 64,978 | |||||||

| - women | 11,611 | 11,955 | 12,161 | 12,542 | 12,860 | |||||||

| Employees abroad by type | 41,971 | 42,633 | 45,967 | 45,516 | 51,034 | |||||||

| - locals | 33,233 | 33,483 | 35,835 | 34,801 | 39,668 | |||||||

| - Italian expatriates | 2,769 | 2,771 | 3,123 | 3,208 | 3,867 | |||||||

| - International expatriates (including TCN) | 5,969 | 6,379 | 7,009 | 7,507 | 7,499 | |||||||

| Senior Managers employed | 1,471 | 1,437 | 1,454 | 1,468 | 1,474 | |||||||

| - of which women | 129 | 141 | 147 | 152 | 159 | |||||||

| Managers/Supervisors employed | 12,058 | 12,395 | 12,837 | 12,754 | 13,199 | |||||||

| - of which women | 2,075 | 2,258 | 2,421 | 2,477 | 2,615 | |||||||

| Employees | 33,483 | 33,931 | 34,599 | 36,019 | 38,497 | |||||||

| - of which women | 9,063 | 9,171 | 9,040 | 9,394 | 9,777 | |||||||

| Workers employed | 24,702 | 23,698 | 24,878 | 22,333 | 24,668 | |||||||

| - of which women | 344 | 385 | 553 | 519 | 309 | |||||||

| Local employees abroad by professional category | 33,233 | 33,483 | 35,835 | 34,801 | 39,668 | |||||||

| - of which senior managers | 245 | 224 | 228 | 228 | 223 | |||||||

| - of which managers/supervisors | 2,900 | 3,138 | 3,461 | 3,476 | 3,798 | |||||||

| - of which employees | 14,864 | 15,533 | 16,269 | 17,529 | 19,683 | |||||||

| - of which workers | 15,224 | 14,588 | 15,877 | 13,568 | 15,964 | |||||||

| Training hours | (thousand hours) | 2,888 | 2,930 | 2,949 | 3,127 | 3,132 | ||||||

| Procurement by geographical area 2012 | Africa | Americas | Asia | Italy | Rest of Europe | Oceania | ||||||||

| Number of suppliers used | (number) | 6,920 | 4,541 | 4,436 | 11,092 | 8,573 | 428 | |||||||

| Total procurement | (euro million) | 7,099 | 2,463 | 5,542 | 12,328 | 3,635 | 745 | |||||||

| - in goods | (%) | 11.7 | 29.1 | 11.9 | 20.0 | 17.3 | 18.9 | |||||||

| - in works | 7.3 | 21.1 | 55.5 | 16.3 | 21.8 | 15.4 | ||||||||

| - in services | 49.5 | 44.3 | 28.8 | 56.0 | 48.7 | 56.1 | ||||||||

| - of which unidentifiable | 31.5 | 5.5 | 3.8 | 7.7 | 12.2 | 9.6 | ||||||||

| Local procurement 2012 by Country | |

| % procurement on local market | Countries |

| 0 - 25% | Algeria, Croatia, Iraq, Libya, Luxembourg, Peru, Poland, Portugal, Spain, Venezuela. |

| 25 - 50% | Angola, France, Germany, Ghana, Iran, Kazakhstan, Switzerland. |

| 50 - 75% | Australia, Brazil, Ecuador, Egypt, Gabon, Norway, Pakistan, Republic of Congo, Saudi Arabia, Tunisia, United Kingdom. |

| 75 - 100% | Argentina, Canada, Hungary, India, Indonesia, Italy, Mexico, Netherlands, Nigeria, Romania, Russia, Singapore, United States. |

Relations with suppliers | 2008 | 2009 | 2010 | 2011 | 2012 |

| Procurement by macro-class | (euro million) | 28,375 | 33,084 | 31,187 | 32,586 | 31,811 | ||||||

| Supplier concentration top 20 | (%) | 23 | 24 | 18 | 20 | 15 | ||||||

| Suppliers used | (number) | 27,956 | 33,447 | 32,601 | 31,878 | 32,621 | ||||||

| Qualification cycles carried out during the year | 15,466 | 21,066 | 32,962 | 26,936 | 31,991 | |||||||

| Suppliers subjected to qualification procedures including screening on human rights | 5,772 | 7,798 | 10,096 | 11,471 | 12,471 | |||||||

| % procurement from suppliers subjected to qualification procedures including screening on human rights | (%) | 88 | 87 | 85 | 90 | 88 | ||||||

- 12 -

Contents

Eni Fact Book Eni business model

Relations with customers | 2008 | 2009 | 2010 | 2011 | 2012 |

| R&M Customer satisfaction | ||||||||||||

| Customer satisfaction index | (likert scale) | 8.14 | 7.93 | 7.84 | 7.74 | 7.90 | ||||||

| Clients involved in the survey | (number) | 22,609 | 10,711 | 30,618 | 30,524 | 30,438 | ||||||

| G&P Customer satisfaction | ||||||||||||

| Customer satisfaction index | (%) | 75.3 | 83.7 | 87.4 | 88.6 | 89.8 (b) | ||||||

| Average Panel (G&P) (a) | 84.9 | 87.0 | 87.4 | 90.8 | 90.6 | |||||||

(a) Referred to companies representing more than 50% of the gas market and totaling over 50,000 clients.

(b) 2012 figure is calculated as the average of the CSS detected by the AEEG in the first half of 2012 and the result detected by the Eni satisfaction survey in the second half of 2012.

Technological innovation | 2008 | 2009 | 2010 | 2011 | 2012 |

| R&D expenditure | (euro million) | 338 | 287 | 275 | 246 | 263 | ||||||

| - R&D expenditure net of general and administrative costs | 211 | 233 | 218 | 190 | 211 | |||||||

| Tangible value generated by R&D activities (a) | n.a. | 362 | 540 | 730 | 1,006 | |||||||

| Personnel employed in R&D activities (full time equivalent) | (number) | 1,123 | 1,019 | 1,019 | 925 | 975 | ||||||

| Existing patents | 8,040 | 7,751 | 7,998 | 8,884 | 8,931 | |||||||

(a) Figures refer to E&P, R&M and Versalis activities and had been measured since 2009, when the measurement process started.

Operating efficiency | 2008 | 2009 | 2010 | 2011 | 2012 |

| Direct GHG emissions | (tonnes CO2 eq) | 59,589,334 | 55,494,551 | 58,259,157 | 49,121,224 | 52,493,340 | ||||||

| - of which CO2 from combustion and process | (tonnes) | 36,475,270 | 35,788,121 | 37,948,625 | 35,319,845 | 36,365,220 | ||||||

| - of which CO2 equivalents from flaring | (tonnes CO2 eq) | 16,535,835 | 13,839,353 | 13,834,988 | 9,553,894 | 9,461,518 | ||||||

| - of which CO2 equivalents from CH4 (methane) | 4,187,532 | 3,684,874 | 4,135,523 | 3,214,469 | 4,470,307 | |||||||

| - of which CO2 equivalents from venting | 2,390,697 | 2,182,202 | 2,340,021 | 1,033,017 | 2,196,295 | |||||||

| CO2 eq emissions/100% net operated hydrocarbon production | (tons CO2 eq/toe) | 0.254 | 0.235 | 0.235 | 0.206 | 0.225 | ||||||

| CO2 eq emissions/kWh eq (EniPower) | (kg CO2 eq/kWh eq) | 0.402 | 0.410 | 0.407 | 0.410 | 0.399 | ||||||

| CO2 eq emissions/uEDC (R&M) | (tonnes CO2 eq/kbbl/SD) | 1,297 | 1,240 | 1,284 | 1,229 | 1,141 | ||||||

| NOx (nitrogen oxide) emissions | (tonnes NO2 eq) | 112,328 | 110,910 | 106,040 | 97,114 | 115,571 | ||||||

| SOx (sulphur oxide) emissions | (tonnes SO2 eq) | 47,160 | 45,985 | 50,085 | 37,943 | 30,137 | ||||||

| NMVOC (Non-Methane Volatile Organic Compounds) emissions | (tonnes) | 80,856 | 75,318 | 68,490 | 46,228 | 48,702 | ||||||

| TSP (Total Suspended Particulate) emissions | 4,195 | 3,936 | 3,783 | 3,297 | 3,548 | |||||||

| Energy used/net 100% operated hydrocarbon production | (GJ/toe) | 1.418 | 1.676 | 1.855 | 1.958 | 2.049 | ||||||

| Total water withdrawals | (mmcm) | 3,023.32 | 2,839.97 | 2,786.78 | 2,577.22 | 2,357.56 | ||||||

| Total production and/or process water extracted | (mmcm) | 52.93 | 59.67 | 61.15 | 58.16 | 61.17 (a) | ||||||

| - of which re-injected | 14.88 | 23.32 | 27.11 | 25.18 | 20.82 | |||||||

| Total recycled and/or reused water | (mmcm) | 460.93 | 490.22 | 544.63 | 521.76 | 521.46 | ||||||

| Total number of oil spills (b) | (number) | 382 | 308 | 330 | 418 | 771 | ||||||

| Total volume of oil spills (b) | (barrels) | 7,024 | 21,547 | 22,964 | 14,952 | 12,472 | ||||||

| - of which from sabotage and terrorism | 2,286 | 15,288 | 18,695 | 7,657 | 8,616 | |||||||

| - of which from accidents | 4,749 | 6,259 | 4,269 | 7,295 | 3,856 | |||||||

| Waste from production activities | (tonnes) | 1,186,618 | 1,078,839 | 1,400,488 | 1,309,135 | 1,378,351 | ||||||

| Hazardous waste from production activities | 479,828 | 418,120 | 489,108 | 476,552 | 365,668 | |||||||

| Non-hazardous waste from production activities | 706,790 | 660,719 | 911,380 | 832,582 | 1,012,683 | |||||||

| Waste from reclamation activities to be disposed of or recovered/recycled | (tonnes) | 9,199,934 | 10,163,403 | 11,020,439 | 13,869,509 | 16,294,882 | ||||||

| Environmental expenditure and investments | (euro thousand) | 947,605 | 1,230,503 | 916,201 | 893,421 | 743,183 | ||||||

(a) In 2012 the figure include also the amount of produced water injected into deep wells to disposal purpose, equal to 9.43 mmcm.

(b) In the 2010-2011 period only oil spills of more than one barrel are considered for the E&P sector; in 2012 the figure also includes oil spills of less than one barrel (equal to 453, corresponding to 3,684 barrels).

- 13 -

Contents

Eni Fact Book Exploration & Production

Exploration & Production |

Key performance indicators |

2008 | 2009 | 2010 | 2011 | 2012 | ||||||||

| Employees injury frequency rate | (No. of accidents per million of worked hours) | 0.84 | 0.49 | 0.72 | 0.41 | 0.28 | ||||||

| Contractors injury frequency rate | 0.93 | 0.59 | 0.48 | 0.41 | 0.36 | |||||||

| Fatality index | (No. of fatalities per 100 million of worked hours) | 3.54 | 1.77 | 7.90 | 1.83 | 0.81 | ||||||

| Net sales from operations (a) | (euro million) | 33,042 | 23,801 | 29,497 | 29,121 | 35,881 | ||||||

| Operating profit | 16,239 | 9,120 | 13,866 | 15,887 | 18,451 | |||||||

| Adjusted operating profit | 17,166 | 9,489 | 13,898 | 16,075 | 18,518 | |||||||

| Adjusted net profit | 7,862 | 3,881 | 5,609 | 6,865 | 7,425 | |||||||

| Capital expenditure | 9,281 | 9,486 | 9,690 | 9,435 | 10,307 | |||||||

| Adjusted ROACE | (%) | 29.2 | 12.3 | 16.0 | 17.2 | 17.6 | ||||||

| Profit per boe (b) | ($/boe) | 16.00 | 8.14 | 11.91 | 16.98 | 15.95 | ||||||

| Opex per boe (b) | 5.45 | 5.77 | 6.14 | 7.28 | 7.10 | |||||||

| Cash flow per boe (d) | 32.25 | 23.70 | 25.52 | 31.65 | 32.77 | |||||||

| Finding & Development cost (c) (d) | 28.79 | 28.90 | 19.32 | 18.82 | 17.37 | |||||||

| Average hydrocarbons realizations (d) | 68.13 | 46.90 | 55.60 | 72.26 | 73.39 | |||||||

| Production of hydrocarbons (d) (e) | (kboe/d) | 1,797 | 1,769 | 1,815 | 1,581 | 1,701 | ||||||

| Estimated net proved reserves of hydrocarbons (d) (e) | (mmboe) | 6,600 | 6,571 | 6,843 | 7,086 | 7,166 | ||||||

| Reserves life index (d) | (years) | 10.0 | 10.2 | 10.3 | 12.3 | 11.5 | ||||||

| Organic reserves replacement ratio net of updating the natural gas conversion factor (d) | (%) | 130 | 93 | 127 | 143 | 147 | ||||||

| Employees at year end | (units) | 10,236 | 10,271 | 10,276 | 10,425 | 11,304 | ||||||

| of which: outside Italy | 6,182 | 6,388 | 6,370 | 6,628 | 7,371 | |||||||

| Oil spills | (bbl) | 4,738 | 6,259 | 3,820 | 2,930 | 3,093 | ||||||

| Oil spills from sabotage and terrorism | 2,286 | 15,288 | 18,695 | 7,657 | 8,384 | |||||||

| Produced water re-injected | (%) | 28 | 39 | 44 | 43 | 49 | ||||||

| Direct GHG emissions | (mmtonnes CO2 eq) | 33.21 | 29.73 | 31.20 | 23.59 | 28.46 | ||||||

| of which: from flaring | 16.54 | 13.84 | 13.83 | 9.55 | 9.46 | |||||||

| Community investment | (euro million) | 65 | 67 | 72 | 62 | 59 | ||||||

| (a) Before elimination of intragroup sales. (b) Consolidated subsidiaries. (c) Three-year average. (d) Includes Eni’s share of equity-accounted entities. (e) From July 1, 2012, Eni has updated the natural gas conversion factor from 5,550 to 5,492 standard cubic feet of gas per barrel of oil equivalent. The effect of this update on production expressed in boe was 9 kboe/d for the full-year 2012 and on the initial reserves balance as of January 1, 2012 amounted to 40 mmboe. |

| Performance of the year | ||

| I In 2012 employees and contractors injury frequency rate declined by 31.7% and 12.2% compared to the previous year. - Total greenhouse gas emissions increased by 20.6% due to the recovery of activities in Libya. Greenhouse gas emissions from flaring were in line with 2011 (down 0.9%). - Oil spills increased in the full year (up 5.6% from accidents and up 9.5% from sabotage and terrorism) due to force majeure and security issues in Nigeria. - Achieved the best ever levels in re-injection of the produced water with a level of 49%. In particular, the water re-injection project at the Belayim field (Eni’s interest 100%) in Egypt reported a level equal to 99%. | - In 2012 the E&P Division reported a record performance with an adjusted net profit amounting to euro 7,425 million (up 8.2% from 2011) driven by an ongoing production recovery in Libya. - Eni reported oil and natural gas production for the full year of 1,701 kboe/day (up 7% form 2011)1 sustained by the recovery of activities in Libya, the start-up/ramp-up of fields, particularly in Russia and Australia, and higher production in Iraq. - Estimated net proved reserves at December 31, 2012 was aneight-year record at 7.17 bboe based on a reference Brent price of $111 per barrel. The organic reserves replacement ratio was 147%1 with a reserves life index of 11.5 years (12.3 years in 2011). All sources reserves replacement ratio was 107%1. |

(1) Excluding the impact of updating the natural gas conversion rate.

- 14 -

Contents

Eni Fact Book Exploration & Production

| Exploration activity I Full year 2012 was a record for exploration, adding 3.64 bboe of discovered resources, about six times production of the year, increasing Eni’s reserves to best ever levels with rapid time-to-market and cost effectiveness. Eni’s approach in the selective development initiatives, advanced technologies and knowledge management of core basins will be the key to achieve future targets. | Sustainability and portfolio developments I Signed an agreement with CNPC/Petrochina to sell 28.57% of the share capital of our subsidiary Eni East Africa, which currently owns 70% interest in Area 4 in Mozambique, for an agreed price equal to $4,210 million. The deal is subject to approval by relevant authorities. Once finalized, CNPC indirectly acquires, through its 28.57% equity investment in Eni East Africa, a 20% interest in Area 4, while Eni will retain the 50% interest through the remaining controlling stake in Eni East Africa. |

- 15 -

Contents

Eni Fact Book Exploration & Production

Activity areas

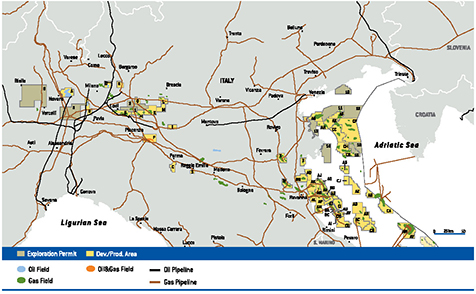

| n Italy Eni has been operating in Italy since 1926. In 2012, Eni’s oil and gas production amounted to 189 kboe/d. Eni’s activities in Italy are deployed in the Adriatic and Ionian Sea, the Central Southern Apennines, mainland and offshore Sicily and the Po Valley, on a total acreage of 22,285 square kilometers (17,556 net to Eni). Eni’s exploration and development activities in Italy are regulated by concession contracts (54 operated onshore and 61 operated offshore). Energy efficiency programs progressed with the application of innovative technologies such as: (i) Organic Rankine Cycle (ORC) technology to increase the efficiency of compression stations with a reduction in CO2 emissions that is expected to be applied to the Fano power station; (ii) the optimization of the LNG refrigeration process, patented by Eni, that increases overall efficiency. Adriatic and Ionian Sea | Development Main development activities concerned: (i) production optimization at the Antonella, Barbara, Basil, Brenda, Naomi & Pandora and Porto Corsini fields; and (ii) upgrading of compression and hydrocarbon treatment facilities at the production platform of the Barbara field. Central-Southern Apennines Sicily |

- 16 -

Contents

Eni Fact Book Exploration & Production

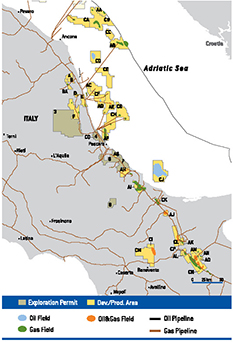

accounted for approximately 10% of Eni’s production in Italy.

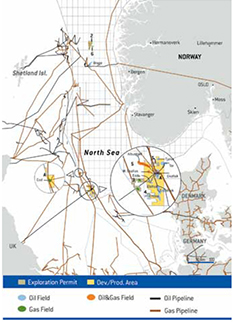

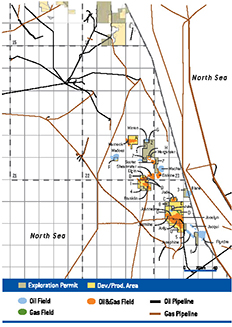

| n Rest of Europe Norway Norwegian Sea Norwegian section of the North Sea |

- 17 -

Contents

Eni Fact Book Exploration & Production

Barents Sea | by a well-advance emergency system for the management of an oil spill, especially in terms of increased resources, organizational innovation, consolidation of the contingency apparatus, as well as equipment development and investment. The Norwegian Authorities acknowledged this project as the reference standard for all future development projects in the Arctic. United Kingdom

|

- 18 -

Contents

Eni Fact Book Exploration & Production

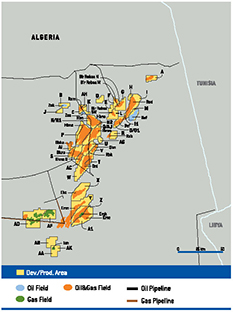

other main fields are Elgin/Franklin, West Franklin (Eni’s interest 21.87%), Liverpool Bay (Eni’s interest 53.9%), J Block Area (Eni’s interest 33%), Flotta Catchment Area (Eni’s interest 20%) and MacCulloch (Eni’s interest 40%), which in 2012 accounted for 91% of Eni’s production in the Country. n North Africa Algeria | Developed and undeveloped acreage of Eni’s interests in Algeria was 3,798 square kilometers (1,232 square kilometers net to Eni). Exploration and production activities in Algeria are regulated by Production Sharing Agreements (PSAs) and concession contracts. Blocks 403a/d and Rom North Blocks 401a/402a Block 403 Block 404

|

- 19 -

Contents

Eni Fact Book Exploration & Production

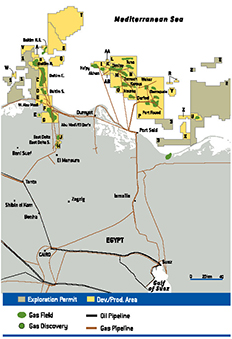

| Block 405b Production In 2013, production started at the MLE field part of the MLE-CAFC integrated project. A natural gas treatment plant started operations with a gross production and export capacity of approximately 320 mmcf/d of gas, 15 kbbl/d of oil and condensates and 12 kbbl/d of LPG. Four export pipelines link it to the national grid system. Development Activities progressed at the CAFC oil project. The project includes the construction of an oil treatment plant and synergies with the MLE production facilities. Production start-up is expected in 2015. The MLE-CAFC integrated project targets a production plateau of approximately 33 kboe/d net to Eni by 2016. Block 208 Egypt

| square kilometers net to Eni). Eni’s main producing liquid fields are located in the Gulf of Suez, primarily the Belayim field (Eni’s interest 100%) and in the Western Desert, mainly the Melehia (Eni’s interest 56%) and the Ras Qattara (Eni’s interest 75%) concessions. Gas production mainly comes from the operated or participated concession of North Port Said (Eni’s interest 100%), El Temsah (Eni’s interest 50%), Baltim (Eni’s interest 50%) and Ras el Barr (Eni’s interest 50%, non operated), located offshore the Nile Delta. In 2012, production from these large concessions accounted for approximately 94% of Eni’s production in Egypt. Exploration and production activities in Egypt are regulated by PSAs. Gulf of Suez Nile Delta Baltim Ras el Barr El Temsah |

- 20 -

Contents

Eni Fact Book Exploration & Production

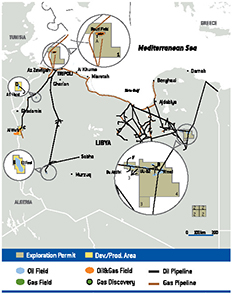

| Natural gas production of this concession is supplied to the Damietta natural gas liquefaction plant owned by Unión Fenosa Gas. Eni, together with other international oil company, have entered into an agreement to supply 310 mmcf/d for 17-year period. Development Infilling and workover activities are being performed in order to maintain the current gas production plateau. Exploration in the Nile Delta Western Desert Libya | Area A Production Located in the Eastern Libyan Desert, it includes six oil fields, started-up in 1984, which are linked to existing facilities at the nearby Bu Attifel field (Area B). In 2012 production from these fields amounted to approximately 11 kbbl/d (approximately 3 kbbl/d net to Eni). Area B Area C Area D

|

- 21 -

Contents

Eni Fact Book Exploration & Production

| oil and condensates. Offshore production is operated through the Sabratha platform located on the Bahr Essalam field where gas and liquids undergo a pre-treatment phase and are delivered via sealine to the Mellitah plant. Most of the natural gas produced is exported to Europe through the GreenStream pipeline. In 2012 volumes delivered through this pipeline were approximately 219 bcf. In addition, approximately 145 bcf were sold on the Libyan market for power generation and approximately 4 bcf to feed the GreenStream compressor station. Area E Tunisia n Sub-Saharan Africa Angola |

In the exploration and development phase, Eni operates Block 15/06 (Eni’s interest 35%). Block 0 |

- 22 -

Contents

Eni Fact Book Exploration & Production

| Block 3 Production Block 3 is divided into three production offshore areas. In 2012, production from this block amounted to approximately 60 kbbl/d (approximately 5 kbbl/d net to Eni). Development Concept Definition studies are underway in the Punja and Caco-Gazela discoveries. Block 14 Block 15 | Block 15/06 Exploration activities yielded positive results with the oil Vandumbu 1 discovery, first commitment well of the second exploration period. The discoveries of Block 15/06 will be developed within two projects: the West Hub project, sanctioned in 2010, and the East Hub. The West Hub project includes the development of the Sangos, N’Goma and Cinguvu discoveries, that will be added in two additional phases of the Mpungi and Vandumbu discoveries, which increases the potential of the hub up to 200 mmbbl. First planned phase (Sangos, N’Goma and Cinguvu) concerned drilling of 14 subsea wells (8 producers and 6 injectors) and linkage to an FPSO unit with a capacity of 100 kbbl/d with start-up expected in the first half of 2014. Two additional phases provides the development of the Mpungi field with the drilling of 7 wells (4 producers and 3 injectors) connected to the FPSO and then the Vandumbu field, under study. Peak production is expected at 84 kbbl/d (25 net to Eni) in 2016. The East Hub project intends to develop the Cabaça North and South-East discoveries with potential resources estimated at more 230 mmbbl. Development activity provides for the drilling of 22 subsea wells and the installation of an FPSO unit with a capacity of 120 kbbl/d. Final investment decision is expected in 2013. Further development phases are planned to start-up nearby discoveries; in particular the significant Lira discoveries. Peak production is expected at approximately 15 kbbl/d net to Eni. The LNG business in Angola Congo |

- 23 -

Contents

Eni Fact Book Exploration & Production

| interest 65%), Kitina (Eni’s interest 35.75%), Awa Paloukou (Eni’s interest 90%), M’Boundi (Eni’s interest 83%), Kouakouala (Eni’s interest 75%), Zingali and Loufika (Eni’s interest 85%) fields, with a production of approximately 77 Kboe/d in the year. Other relevant producing areas are a 35% interest in the Pointe-Noire Grand Fond, PEX and Likouala permits (overall production of 26 kboe/d in 2012). Development Activities on the M’Boundi field moved forward with the application of Eni advanced recovery techniques and a design to monetize associated gas within the activities aimed at zero gas flaring by 2013. Gas is sold under long-term contracts to power plants in the area including the CEC Centrale Electrique du Congo (Eni’s interest 20%) with a 300 MW generation capacity. These facilities will also receive in the future gas from the offshore discoveries of the Marine XII permit. In 2012 M’Boundi contractual supplies were approximately 106 mmcf/d (approximately 17 kboe/d net to Eni). In 2012 the development project for the gas and condensates Litchendjili field in the Block Marine XII has been sanctioned. The project provides for the installation of a production platform, the construction of transport facilities and of an onshore treatment plant. Production will also feed the CEC power station. Other activities in the area concerned the optimization of producing fields of Foukanda and Mwafi by means of Eni’s enhanced recovery that allowed to increase production in both fields. Exploration In the exploration phase, Eni also holds interests in

| the Mer Très Profonde Sud deep offshore block (Eni’s interest 30%), the Noumbi onshore permit (Eni’s interest 37%) and the Marine XII offshore permit. Exploration activities yielded positive results in the offshore block Marine XII with the Nene Marine 1 gas discovery that confirmed the high mineral potential of the area. Ghana Mozambique |

- 24 -

Contents

Eni Fact Book Exploration & Production

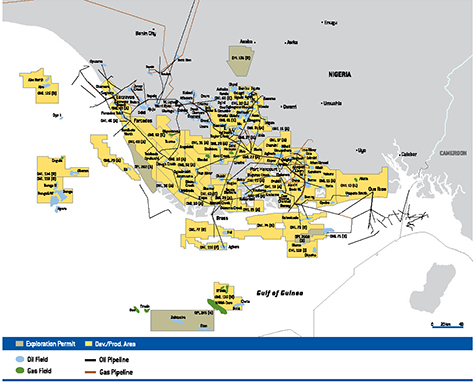

| Authorities. Once finalized, CNPC indirectly acquires, through its 28.57% equity investment in Eni East Africa, a 20% interest in Area 4, while Eni will retain the 50% interest through the remaining controlling stake in Eni East Africa. Feasibility studies are underway to promote some initiatives in the Country such as schooling, health, socio-economic development and the environment. A first program has been launched for the recruitment of 45 recent graduates of the University of Mozambique to spend two years of training in Italy. More recently, in November 2012, a second selection campaign has been launched for a further training initiative to be carried out in 2013. Nigeria | As partners of SPDC JV, the largest joint venture in the Country, Eni also holds a 5% interest in 25 onshore blocks and a 12.86% interest in 5 conventional offshore blocks. In the exploration phase Eni operates offshore Oil Prospecting Leases (OPL) 244 (Eni’s interest 60%), OML 134 (Eni’s interest 85%) and OPL 2009 (Eni’s interest 49%); and onshore OPL 282 (Eni’s interest 90%) and OPL 135 (Eni’s interest 48%). Eni also holds a 12.5% interest in OML 135. Exploration activities yielded positive results in: (i) Block OPL 282 with the Tinpa 1 well containing oil; and (ii) Block OPL 2009 with the Afiando 1 and 2 oil wells. In 2012, Eni completed the divestment of a 5% stake in blocks OMLs 30, 34 and 40 confirming Eni’s strategy of optimizing its producing asset portfolio and selective growth. Starting from March 21, the oil production of the onshore Swamp area mainly in the Bayelsa State in Nigeria has been temporarily shut down due to the increasing bunkering and sabotage acts on the oil trunk lines. Currently, the area produces from 9 fields through 4 flow stations (Ogbainbiri, Tebidaba, Clough Creek, Obama). A detailed survey of the lines affected by the bunkering is in progress in order to identify and repair the damages suffered. As a part of a few Memorandum of Understanding signed with local communities in the Niger Delta, some programs were completed |

- 25 -

Contents

Eni Fact Book Exploration & Production

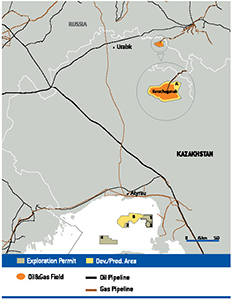

| aimed at improving access to health and education services, initiatives in agriculture and construction of infrastructure for supporting local development. In particular, the following projects were completed: (i) rehabilitation of nine schools for 25 communities; (ii) eight projects allowing access to drinkable water by means of facilities installed in 13 communities; (iii) fifteen projects for electricity supply. Activities are underway to reach other 22 local communities. Exploration and production activities in Nigeria are regulated mainly by PSAs and concession contracts as well as service contracts, in two blocks, where Eni acts as contractor for the state-owned company. Blocks OMLs 60, 61, 62 and 63 Block OML 118 Block OML 119 Block OML 125 | Block OPL 245 This deep offshore block includes the largest undeveloped mineral resources potential in the Country. Eni’s commitment is for a fast track development of the Zabazaba and Etan fields. Drilling activities started up in 2012. The preliminary development scheme provides for the installation of an FPSO unit and the drilling of 8 wells (4 productive and 4 injections). FID is expected in 2014. SPDC Joint Venture (NASE) The LNG business in Nigeria n Kazakhstan Eni has been present in Kazakhstan since 1992 where the Company co-operates the Karachaganak producing field and is a partner of the consortium of the North Caspian Sea PSA to develop the Kashagan field. Kashagan |

- 26 -

Contents

Eni Fact Book Exploration & Production

through an operating model which entails an increased role of the Kazakh partner and defines the international parties’ responsibilities in the execution of the subsequent development phases of the project. The North Caspian Operating Company (NCOC) BV, participated by the seven partners of the consortium has taken over the operatorship of the project. Subsequently development, drilling and production activities have been delegated by NCOC BV to the main partners of the Consortium: Eni has retained the responsibility for the development of Phase 1 of the project (the so-called "Experimental Program") and, when sanctioned, the onshore part of Phase 2. | capacity of 150 kbbl/d; by 2014 a second treatment train and compression facilities for gas reinjection will be completed and put online enabling to increase the production capacity up to 370 kbbl/d. The partners are planning to further increase available production capacity up to 450 kbbl/d by installing additional gas compression capacity for re-injection in the reservoir. The partners submitted the scheme of this additional phase to the relevant Kazakh Authorities and sanction is expected in 2013 to start-up with FEED phase. Eni continues its commitment in the protection of the environment and ecosystems in the Caspian area with the integrated program for the management of biodiversity in the Ural Delta (Ural River Park Project - URPP). The project is almost completed and Eni’s aim is to include it in the Man and Biosphere Program of UNESCO under the patronage of the Kazakh Minister for Environmental Protection. Karachaganak |

- 27 -

Contents

Eni Fact Book Exploration & Production

| n Rest of Asia China Indonesia | Development activities are underway at the Indonesia Deepwater Development project (Eni’s interest 20%), located in the East Kalimantan, to ensure gas supplies to the Bontang plant. The project initially provides for the linkage of the Bangka field to existing facilities, then for the integrated development of four fields through a first Hub serving the Gendalo, Gandang, Maha and a second Hub for Gehem. Iraq Pakistan |

- 28 -

Contents

Eni Fact Book Exploration & Production

| Russia Eni has been present in Russia since 2007 following the acquisition of assets in the Yukos liquidation procedure. In 2012, Eni’s production averaged 11 kboe/d, mainly of gas. Activities are located in the onshore western Siberia, over a developed and undeveloped acreage of 4,996 square kilometers (1,469 square kilometers net to Eni). The assets in joint venture with Enel (Eni 60%; Enel 40%) are managed by the subholding OOO SeverEnergia (Eni’s interest 29.4%) and own 4 exploration/development blocks located in the Yamal Nenets Region, with significant predominantly gas resources estimated in 1.6 bboe. Production In 2012, production started-up at the Samburgskoye field located in the Yamal-Nenets area, in Siberia, by means of the first and the second train with an expected production level of 95 kboe/d (28 kboe/d net to Eni). Development activities progressed with completion expected in 2015 and production peak of 146 kboe/d (43 kboe/d net to Eni) in 2016. The gas production is sold to Gazprom under the agreement signed in September 2011 while the condensate production is sold to Novatek under the relevant agreement signed in 2012. Eni retains the right to lift its share of natural gas and sell it to any third parties in the domestic market. Development Planned activities progressed at the sanctioned Urengoiskoye field. Start-up is expected in 2014. In June 2012, Eni and the Authority of the Yamal-Nenets Autonomous District signed a Memorandum of Understanding which outlines a plan for implementing joint socio-economic and cultural projects in the area. The agreement includes training initiatives in the Oil&Gas sector, cultural programs and financial support. Exploration In April 2012, Eni and Rosneft signed an agreement related to a strategic cooperation whereby the two companies will set up joint ventures (Eni 33.33%) for the exploration and development of the Fedynsky and Tsentralno-Barentsevsky licenses, located offshore Russia in the Barents Sea, and Zapadno-Cernomorsky, located offshore Russia in the Black Sea. Finalization is expected in 2013.

| Turkmenistan Eni started its activities in Turkmenistan with the purchase of the British company Burren Energy plc in 2008. Activities are focused in the Western part of the Country over a developed area of 200 square kilometers net to Eni, splitted into four development areas. In 2012, Eni’s production averaged 11 kboe/d. Exploration and production activities in Turkmenistan are regulated by PSAs. Production Eni is operator of the Nebit Dag producing block (with a 100% interest). Production derives mainly from the Burun oil field. Oil production is shipped to the Turkmenbashi refinery plant. Eni receives, by means of a swap with the Turkmen Authorities, an equivalent amount of oil at the Okarem terminal, close to the South coast of the Caspian Sea. Eni’s entitlement is sold FOB. Associated natural gas is used for own consumption and gas lift system. The remaining amount is delivered to Turkmenneft, via national grid. n America Ecuador Trinidad & Tobago United States |

- 29 -

Contents

Eni Fact Book Exploration & Production

| Gulf of Mexico Eni holds interests in 281 exploration and production blocks in the conventional and deep-offshore in the Gulf of Mexico, of which 172 are operated by Eni. Production The main fields operated by Eni are Allegheny, Appaloosa and Morpeth (Eni’s interest 100%), Longhorn-Leo, Devils Towers and Triton (Eni’s interest 75%) as well as Pegasus (Eni’s interest 58%). Eni also holds interests in the Medusa (Eni’s interest 25%), Europa (Eni’s interest 32%) and Thunderhawk (Eni’s interest 25%) fields. Development Development activities mainly concerned: (i) drilling activities at the Allegheny, Appaloosa and Devils Towers operated fields; (ii) production optimization of the Front Runner (Eni’s interest 37.5%), Europa, Popeye (Eni’s interest 50%) and Thunderhawk fields; (iii) the start-up of drilling programs at the Hadrian South (Eni’s interest 30%) and St. Malo (Eni’s interest 1.25%) fields. Exploration Exploration outlining activity of the Heidelberg oil discovery (Eni’s interest 12.5%) in the Gulf of Mexico yielded positive results and increased recoverable resources up to approximately 200 mmbbl. Studies are underway for a fast track development. In March 2013, Eni was awarded five offshore blocks, located in Mississippi Canyon and Desoto Canyon. | Texas Production Development activity progressed at the Alliance area (Eni’s interest 27.5%), in the Fort Worth basin in Texas. This area, including gas shale reserves, was acquired following a strategic partnership between Eni and Quicksilver. In particular, 12 new wells entered in production and contributed to a total production of approximately 10 kboe/d net to Eni in the year. Alaska Venezuela |

- 30 -

Contents

Eni Fact Book Exploration & Production

| Belt, over a developed and undeveloped acreage of 2,805 square kilometers (1,066 square kilometers net to Eni). Exploration and production of oil fields are regulated by the terms of the so-called Empresa Mixta. Under the new legal framework, only a company incorporated under the law of Venezuela is entitled to conduct petroleum operations. A stake of at least 60% in the capital of such company is held by an affiliate of the Venezuela state oil company, PDVSA, preferably Corporación Venezuelana de Petróleo (CVP). Production In March 2013, production started up at the giant Junin 5 field (Eni’s interest 40%) with 35 bbbl of certified heavy oil in place, located in the Orinoco oil belt. Early production of the first phase is expected at plateau of 75 kbbl/d in 2015, targeting a long-term production plateau of 240 kbbl/d to be reached by 2018. The project provides also for the construction of a refinery with a capacity of approximately 350 kbbl/d. The drilling activity started during the year. Eni agreed to finance part of PDVSA’s development costs for the early production phase and engineering activity of refinery plant up to $1.74 billion. Eni signed a loan agreement in the fourth quarter 2012. In 2012, the start-up of the Central Production Facility (CPF) at the Corocoro field (Eni’s interest 26%) allowed to achieve a production peak of approximately 42 kbbl/d (approximately 11 kbbl/d net to Eni). Development Venezuelan relevant Authority sanctioned the development plan of the Perla gas discovery, located in the Cardón IV block (Eni’s interest 50%), in the Gulf of Venezuela. PDVSA exercised its 35% back-in right in 2012 and the completion of the stake transfer is expected in 2013. Eni retains the 32.5% joint controlled interest in the company. The early production phase includes the utilization of the already successfully drilled discovery/appraisal wells and the installation of production platforms linked by pipelines to the onshore treatment plant. Target production of approximately 300 mmcf/d is expected in 2015. The development program will continue with the drilling of additional wells and the upgrading of treatment facilities to reach a production plateau of approximately 1,200 mmcf/d. In 2012 the FIDs of the further phases were sanctioned. Exploration Exploration activity mainly concerned the Gulfo de Paria Centrale offshore oil exploration block (Eni’s interest 19.5%), where the Punta Sur oil discovery is located and the Punta Pescador and Gulfo de Paria Ovest (Eni’s interest 40%), the latter coinciding with the Corocoro oil field area. | n Australia and Oceania Australia Block JPDA 06-105 Block WA-33-L Block JPDA 03-13 |

- 31 -

Contents

Eni Fact Book Exploration & Production

| Estimated net proved hydrocarbons reserves by geographic area (a) | (mmboe) |

| (at December 31) | Italy (b) | Rest of Europe | North Africa | Sub-Saharan Africa | Kazakhstan (c) | Rest of Asia (d) | America | Australia and Oceania | Total | |||||||||

| 2008 | ||||||||||||||||||

| Estimated net proved hydrocarbons reserves | 681 | 525 | 1,939 | 1,154 | 1,336 | 579 | 254 | 132 | 6,600 | |||||||||

| Consolidated subsidiaries | 681 | 525 | 1,922 | 1,146 | 1,336 | 265 | 235 | 132 | 6,242 | |||||||||

| Equity-accounted entities | 17 | 8 | 314 | 19 | 358 | |||||||||||||

| Developed | 465 | 417 | 1,242 | 831 | 647 | 212 | 140 | 62 | 4,016 | |||||||||

| Consolidated subsidiaries | 465 | 417 | 1,229 | 827 | 647 | 168 | 133 | 62 | 3,948 | |||||||||

| Equity-accounted entities | 13 | 4 | 44 | 7 | 68 | |||||||||||||

| Undeveloped | 216 | 108 | 697 | 323 | 689 | 367 | 114 | 70 | 2,584 | |||||||||

| Consolidated subsidiaries | 216 | 108 | 693 | 319 | 689 | 97 | 102 | 70 | 2,294 | |||||||||

| Equity-accounted entities | 4 | 4 | 270 | 12 | 290 | |||||||||||||

| 2009 | ||||||||||||||||||

| Estimated net proved hydrocarbons reserves | 703 | 590 | 1,937 | 1,163 | 1,221 | 545 | 279 | 133 | 6,571 | |||||||||

| Consolidated subsidiaries | 703 | 590 | 1,922 | 1,141 | 1,221 | 236 | 263 | 133 | 6,209 | |||||||||

| Equity-accounted entities | 15 | 22 | 309 | 16 | 362 | |||||||||||||

| Developed | 490 | 432 | 1,278 | 804 | 614 | 183 | 181 | 122 | 4,104 | |||||||||

| Consolidated subsidiaries | 490 | 432 | 1,266 | 799 | 614 | 139 | 168 | 122 | 4,030 | |||||||||

| Equity-accounted entities | 12 | 5 | 44 | 13 | 74 | |||||||||||||

| Undeveloped | 213 | 158 | 659 | 359 | 607 | 362 | 98 | 11 | 2,467 | |||||||||

| Consolidated subsidiaries | 213 | 158 | 656 | 342 | 607 | 97 | 95 | 11 | 2,179 | |||||||||

| Equity-accounted entities | 3 | 17 | 265 | 3 | 288 | |||||||||||||

| 2010 | ||||||||||||||||||

| Estimated net proved hydrocarbons reserves | 724 | 601 | 2,119 | 1,161 | 1,126 | 612 | 373 | 127 | 6,843 | |||||||||

| Consolidated subsidiaries | 724 | 601 | 2,096 | 1,133 | 1,126 | 295 | 230 | 127 | 6,332 | |||||||||

| Equity-accounted entities | 23 | 28 | 317 | 143 | 511 | |||||||||||||

| Developed | 554 | 405 | 1,237 | 817 | 543 | 182 | 167 | 117 | 4,022 | |||||||||

| Consolidated subsidiaries | 554 | 405 | 1,215 | 812 | 543 | 139 | 141 | 117 | 3,926 | |||||||||

| Equity-accounted entities | 22 | 5 | 43 | 26 | 96 | |||||||||||||

| Undeveloped | 170 | 196 | 882 | 344 | 583 | 430 | 206 | 10 | 2,821 | |||||||||

| Consolidated subsidiaries | 170 | 196 | 881 | 321 | 583 | 156 | 89 | 10 | 2,406 | |||||||||

| Equity-accounted entities | 1 | 23 | 274 | 117 | 415 | |||||||||||||

| 2011 | ||||||||||||||||||

| Estimated net proved hydrocarbons reserves | 707 | 630 | 2,052 | 1,104 | 950 | 886 | 624 | 133 | 7,086 | |||||||||

| Consolidated subsidiaries | 707 | 630 | 2,031 | 1,021 | 950 | 230 | 238 | 133 | 5,940 | |||||||||

| Equity-accounted entities | 21 | 83 | 656 | 386 | 1,146 | |||||||||||||

| Developed | 540 | 374 | 1,194 | 746 | 482 | 134 | 188 | 112 | 3,770 | |||||||||

| Consolidated subsidiaries | 540 | 374 | 1,175 | 742 | 482 | 129 | 162 | 112 | 3,716 | |||||||||

| Equity-accounted entities | 19 | 4 | 5 | 26 | 54 | |||||||||||||

| Undeveloped | 167 | 256 | 858 | 358 | 468 | 752 | 436 | 21 | 3,316 | |||||||||

| Consolidated subsidiaries | 167 | 256 | 856 | 279 | 468 | 101 | 76 | 21 | 2,224 | |||||||||

| Equity-accounted entities | 2 | 79 | 651 | 360 | 1,092 | |||||||||||||