Globix Corporation

September 2005

New York City

Peter Stevenson – CEO • Robert Dennerlein – CFO

AMEX Listed: GEX

1

Forward Looking Information and Pro Forma Statements

“This presentation contains forward-looking information

that is subject to various risks, including risks

described in the most recent Annual Report on Form

10-K of Globix Corporation and other documents filed

by Globix with the SEC.”

2

Overview of Globix

2005 Highlights:

Closed merger with NEON Communication

Listed on American Stock Exchange: GEX

Continued reduction of long-term debt

$12.5M of LT debt converted to equity as of March 05

11% senior notes down to $68 million

Achieving synergies from the merger

Approximately $1.5 million in quarterly cost reductions

Integrated network and facility organizations

Moving Globix 3rd party circuits onto the Neon network

3

Revenue:

$114 (LTM) MM

Employees:

~350

Customers:

~1,500

Major Locations:

New York, NY

Boston MA

London, England

Atlanta, GA

Fairfield, NJ

Reston, VA

Santa Clara, CA

Infrastructure:

POPs:

170+

Current Data Centers:

9

Colocation Facilities:

16

Telecom/Data Center Space:

139,000+ sq. feet

Fiber Miles:

220,000+

Route Miles:

5,000+

What We Do:

Network Services

Hosting and Server Solutions:

- Managed Hosting

- Collocation

- Security

- Applications Management

- IP Connectivity

Media Services

Customers:

Small-Midsize Businesses

Divisions of Fortune 1000

Carriers (e.g. Mobile, PTTs)

Globix is…

…and all the

other Parts too.

A company

with Backbone .

Apps

Media

Security

IP Infrastructure

Data Centers

Network Services

Optical Networking

4

Network Access Point

Access POP’s

Data Center

Managed Hosting including security, applications management,

traditional collocation services, and data back-up

Managed Media Services

Dedicated Internet access

The Globix IP Network Backbone

5

SIX

Seattle

Santa Clara

Los Angeles

Atlanta

Chicago

Ashburn, VA

New York

NYIIX

Washington, DC

Boston

LINX

LONAP

Packet

Exchange

Band-X

London

AMS-IX

SFINX

Paris

Frankfurt

DE-CIX

The Globix Optical Network

Owned & Operated

5,000 Route Miles

Power Company ROW

170+ Buildings On Net

16 Colocation Facilities

Substantial Capacity

Mid-Atlantic Expansion:

South Jersey

North Jersey

Phila Metro

Serves the Nations largest Carriers

Ashburn

VA

McLean/Vienna

MD

Owings Mills

Washington, DC

Baltimore

Rising Sun

DE

Hammonton

Little Egg Harbor

Chester Springs

PA

Hellertown

Philadelphia

NJ

Freehold

New Brunswick

Piscataway

Elizabeth

Newark

New York City

Plainfield

Somerville

Morristown

Rochelle Park/

Hackensack

Suffern

Monroe

New Paltz

Albany

NY

Wappingers Falls

Spackenkill

Poughkeepsie

CT

Greenwich

Stamford

Bridgeport

New Haven

Springfield

New London

Hartford

Brattleboro

VT

MA

Worcester

Waltham/Newton

Keene

Cranston

Warwick

Providence

RI

Brockton

Framingham

Quincy

Boston/Cambridge

Salem

Lawrence

Manchester

Portsmouth

Dover

ME

NH

Portland

Nashua

Burlington

White Plains

Asmonk

Croton-on-Hudson

Elmsford

Greenburgh

Mahopac

Mt. Kisco

Ossining

Peekskill

Putnum Valley

Yorktown Heights

Tarrytown

NEON COLOCATION/CENTRAL

OFFICE

CENTRAL OFFICE

POINT OF PRESENCE

METRO

RING

Northeast and Mid-Atlantic U.S.

6

Outlook for Network Services

Wireless carriers continue to build out their networks

43.1% total carrier growth is expected from wireless providers from 1999 to 2008

Market for carrier fiber services is expected to reach $19.7B in 2008*

…Globix is uniquely positioned and taking advantage of this trend

Wireless carriers represented 56% of FYQ3 sales bookings and

35% of monthly recurring revenue

Enterprise sector continues to demand more bandwidth

Enterprise customers now represent 8% of our network services monthly recurring revenue, up

from 0% in 2001

Network expansion is planned in line with demand

Primarily in the mid-Atlantic region

63 new points of presence (POPs) added in last 7 Quarters

Customers continue to accept multi-year contracts

Terms up to 7 years

42 months average term ytd. 2005

Currently serve 102 network services customers with an ARPU of $43k/mo.**

* Gartner Market Research Report; Forecast: Mobile Data Services, North America, 1999 - 2008

**ARPU (Average Revenue Per Unit) = average contracted monthly recurring revenue

for the period divided by the average number of contracted customers for the period, data is for FY Q3

7

Hosting used to be:

Collocation

Rack Space

Power

Internet Connectivity

…but customer needs are changing

Managed hosting

Security and backup

Management of customer’s applications

Completely outsourced applications (Digital Asset Management and Email)

Monitoring

Hosting for high density servers

Hosting gets a new look

Yr/Yr Revenue Growth

Managed Services: 8%

Q3 2004 - $4.9

Q3 2005 - $5.3

Hosting: 16%

Q3 2004 - $6.1

Q3 2005 - $7.1

8

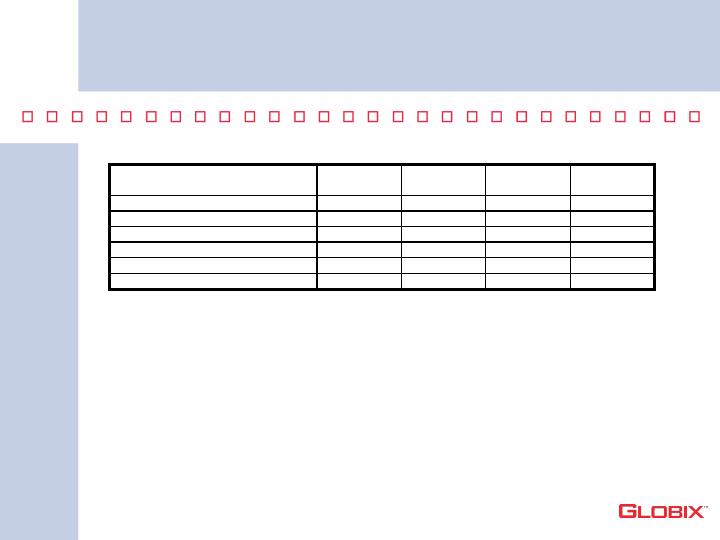

Pro forma Combined Globix & NEON

$0.6**

$16.8

$12.3

$29.1

Q2

3/30/05

$2.2

($0.2)

$1.8

Adjusted

EBITDA*

$16.0

$13.2

$29.2

$16.5

$12.3

$28.8

$16.0

$12.2

$28.2

Globix

NEON

Revenue

Q3

6/30/05

Q1

12/31/04

Q4

9/30/04

Notes:

- Pro forma combines Globix and NEON stand-alone financials

- Adjusted EBITDA: See Appendix

*Includes $2.0 Million of merger related costs recorded in Neon's results.

** Includes approximately $0.8 Million of one time litigation expense.

9

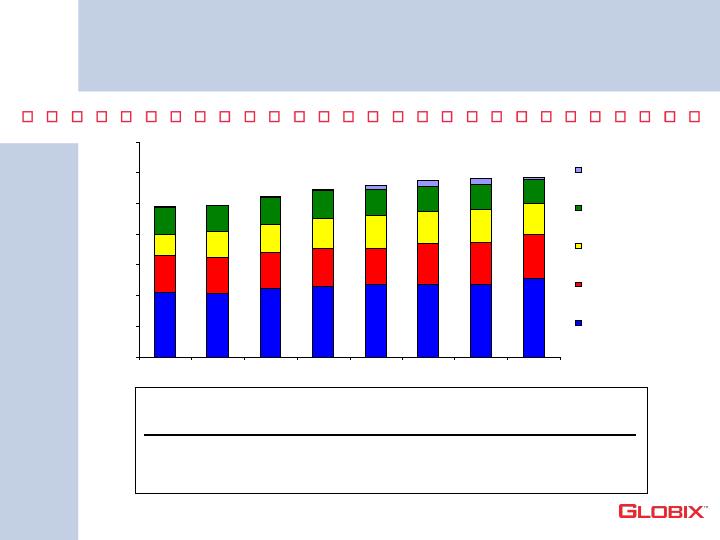

Pro forma Revenue Trends by service

$0

$5

$10

$15

$20

$25

$30

$35

Q4 2003

Q1 2004

Q2 2004

Q3 2004

Q4 2004

Q1 2005

Q2 2005

Q3 2005

Hardware,

Software, DSL

and Other

Network Services

and Internet

Access

Managed

Services

Internet Hosting

and Co-Location

10.6

10.4

11.2

11.6

11.8

11.9

11.9

12.8

6.0

5.9

5.8

6.1

5.9

6.5

6.7

7.1

3.3

4.2

4.6

5.3

5.4

5.5

5.2

4.4

4.2

4.5

4.5

4.3

4.0

4.0

3.8

4.9

Bandwidth

Services

Q403

1,457

$2,700

Q304

1,369

$3,300

Q305

1,318

$3,700

Millions

10

Hosting Group

Customers

ARPU

Moving Forward

Focus sales in product growth areas:

Network services for wireless communications

Managed server services including managed hosting, security,

applications management and professional services

Media services

Continue to eliminate costs through integration

synergies and operational efficiencies

Build brand awareness and position Globix as the

leader in providing seamless, reliable and tailored

network services, managed server solutions and

media services.

11

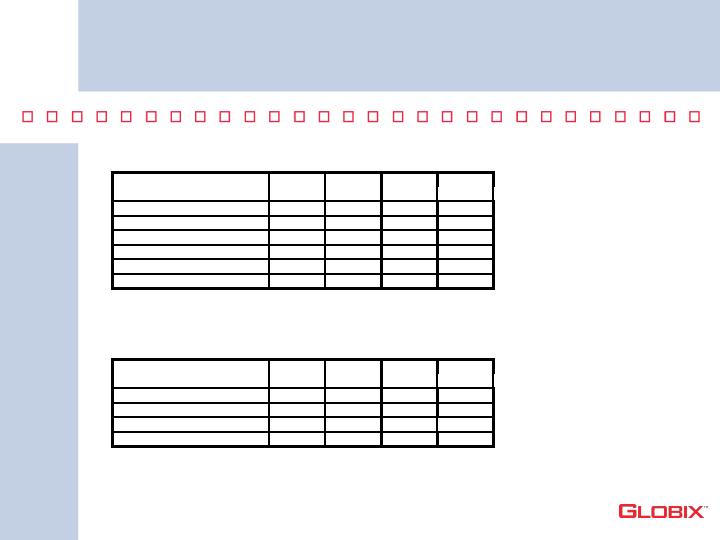

Appendix

* Adjusted EBITDA: We believe Adjusted EBITDA may be useful to investors as a

performance measure and may help them understand our cash resources and

requirements. In addition, we use Adjusted EBITDA in our internal business planning

process, in setting company performance goals and for incentive compensation

purposes. Adjusted EBITDA does not represent cash flow from operations, as defined

under U.S. generally accepted accounting principles, and is not a measure of

operating profitability or net income. Our computation of Adjusted EBITDA may differ

from those used by other companies should not be considered comparable.

Qtr end

9/30/2004

Qtr end

12/31/2004

Qtr end

3/31/2004

Qtr end

6/30/2004

Loss from operations

(4,631)

(28,933)

(6,205)

(4,011)

Loss on impairment of assets

-

22,000

-

-

Depreciation/amortization

6,239

6,480

6,581

5,985

Non cash comp (stock)

23

23

3

7

Rental income

211

212

208

212

Adjusted EBITDA

1,842

(218)

587

2,193

12

Appendix

****Globix Corporation

2004 Adjusted

EBITDA Trend

(Adjusted EBITDA

Reconciliation)

NEON

Communications Inc

2004 EBITDA Trend

(Adjusted EBITDA

Reconciliation)

Qtr end

Qtr end

Qtr end

Qtr end

6/30/2004

9/30/2004

12/31/2004

3/31/2005

Loss from operations

(3,595)

(3,344)

(4,015)

(4,582)

Loss on impairment of assets

0

0

0

0

Depreciation/amortization

3,519

3,465

3,543

3,626

Non cash comp (stock)

(13)

23

23

3

Rental income

224

211

212

208

Adjusted EBITDA

135

355

(237)

(745)

Qtr end

Qtr end

Qtr end

Qtr end

6/30/2004

9/30/2004

12/31/2004

3/31/2005

Loss from operations

(1,391)

(1,287)

(24,918)

(1,623)

Depreciation/amortization

2,629

2,774

2,937

2,955

Loss on impairment of assets

0

0

22,000

0

Adjusted EBITDA

1,238

1,487

19

1,332

13