QuickLinks -- Click here to rapidly navigate through this document

Exhibit 99.3

World Color Press Inc.

(Formerly Quebecor World Inc.)

MANAGEMENT'S DISCUSSION AND ANALYSIS

THIRD QUARTER ENDED SEPTEMBER 30, 2009

TABLE OF CONTENTS

| | | | | | | | |

Subject | | Page | |

|---|

Introduction and quarterly highlights | | | 3 | |

1. | | Creditor protection and the plan of reorganization | | |

7 | |

2. | | Financial review | | |

13 | |

| | 2.1 | | Industry trends and outlook | | | 13 | |

| | 2.2 | | Third quarter review | | | 15 | |

| | 2.3 | | Year-to-date review | | | 17 | |

| | 2.4 | | Segment results | | | 20 | |

| | 2.5 | | Impairment of assets and restructuring initiatives | | | 21 | |

3. | | Critical accounting estimates, changes in accounting standards and adoption of new accounting policies | | |

23 | |

| | 3.1 | | Critical accounting estimates | | | 23 | |

| | 3.2 | | Changes in accounting standards and adoption of new accounting policies | | | 24 | |

4. | | Liquidity and capital resources | | |

26 | |

| | 4.1 | | DIP financing | | | 26 | |

| | 4.2 | | Exit financing | | | 26 | |

| | 4.3 | | Unsecured notes to be issued | | | 27 | |

| | 4.4 | | Cash flow | | | 28 | |

5. | | Financial position | | |

30 | |

| | 5.1 | | Free cash flow | | | 30 | |

| | 5.2 | | Credit ratings | | | 30 | |

6. | | Off-balance sheet arrangements, derivative financial instruments and other disclosures | | |

30 | |

| | 6.1 | | Risk arising from financial instruments | | | 30 | |

| | 6.2 | | Contractual obligations | | | 31 | |

| | 6.3 | | Share capitalization | | | 32 | |

7. | | Quarterly trends | | |

35 | |

8. | | Controls and procedures | | |

36 | |

| | 8.1 | | Evaluation of disclosure controls and procedures | | | 36 | |

| | 8.2 | | Changes in internal control over financial reporting | | | 37 | |

9. | | Additional information | | |

38 | |

2

Introduction

The following is a discussion of the consolidated financial condition and results of operations of World Color Press Inc. ("we", "us", "our", the "Company", the "Successor" or "Worldcolor"), the successor company of Quebecor World Inc. ("QWI" or the "Predecessor") for the three-month and nine-month periods ended September 30, 2009 and 2008, and it should be read together with the Company's corresponding interim consolidated financial statements as well as the Predecessor's annual report on Form 20-F for the year ended December 31, 2008. All references made to "Notes" in the interim Management's Discussion and Analysis ("MD&A") correspond to the Notes to the interim consolidated financial statements for the period ended September 30, 2009. The interim consolidated financial statements and this interim MD&A have been reviewed and approved by the Company's Audit Committee. This discussion contains forward-looking information that is qualified by reference to, and should be read together with, the discussion regarding forward-looking statements that is part of this interim MD&A. Management determines whether or not information is "material" based on whether it believes a reasonable investor's decision to buy, sell or hold securities in the Company would likely be influenced or changed if the information were omitted or misstated.

Quarterly highlights

Financial

- •

- Combined consolidated operating revenues were $769.9 million, a 23% decrease compared to $993.6 million in the third quarter of 2008; and

- •

- Adjusted EBITDA increased to $103.4 million compared to $94.2 million in the third quarter of 2008, a result of the Company putting in place a number of initiatives designed to help reverse the negative impact of the drop in volume.

Customers

- •

- During the quarter, Worldcolor announced that the following contracts with significant customers were renewed or signed: USA Weekend, Schofield Media Group and Pace Communications;

- •

- Worldcolor won 34 Gold Ink Awards in the annual printing competition sponsored by Publishing Executive, Printing Impressions and Book Business magazines; and

- •

- Worldcolor received the 2008 Exceptional Customer Service Supplier of the Year Award from Walmart.

Other

- •

- On July 21, 2009, QWI emerged from bankruptcy protection, was renamed and began operating as Worldcolor;

- •

- Worldcolor's Common Shares and Series I and II Warrants commenced trading on the Toronto Stock Exchange (TSX) on August 26, 2009;

- •

- On September 17, 2009, Worldcolor introduced its new logo, go to market identity and brand promise which encapsulates Worldcolor`s message to customers: "Worldcolor is the partner of choice for reaching your target audience through print and electronic communications"; and

- •

- The following senior management appointments were made during the quarter:

- •

- Mark Angelson as Chairman and Chief Executive Officer;

- •

- Andrew P. Hines as Interim Chief Financial Officer;

3

- •

- John V. Howard as Executive Vice President, Chief Legal Officer;

- •

- Robert L. Sell as Executive Vice President, Chief Information Officer;

- •

- Ben Schwartz to Executive Vice President, Human Resources;

- •

- Daniel J. Scapin as President of Logistics and Premedia business group in the U.S.;

- •

- Lorien O. Gallo as Senior Vice President, Office of the Chairman; and

- •

- Jo-Ann Longworth to Senior Vice President, Chief Accounting Officer.

Presentation of financial information and combined quarterly financial results

As described in Note 1 to the 2008 annual consolidated financial statements, on January 21, 2008 (the "Filing Date"), QWI obtained an order from the Quebec Superior Court granting creditor protection under theCompanies' Creditors Arrangement Act (the "CCAA") for itself and for 53 U.S. subsidiaries (the "U.S. Subsidiaries" and, collectively with QWI, the "Applicants"). On the same date, the U.S. Subsidiaries filed a petition under Chapter 11 of the U.S. Bankruptcy Code in the Bankruptcy Court for the Southern District of New York. The proceedings under the CCAA and Chapter 11 are hereinafter collectively referred to as the "Insolvency Proceedings".

On June 22, 2009, the creditors of the Applicants approved a plan of compromise and reorganization (the "Plan") under both the CCAA and Chapter 11. On June 30, 2009, the Plan was sanctioned by the Quebec Superior Court, and it was confirmed by the U.S. Bankruptcy Court on July 2, 2009. The Plan was implemented following various transactions that were completed on July 21, 2009 (the "Effective Date"). Accordingly, the Applicants emerged from bankruptcy protection and QWI was renamed and began operating as Worldcolor.

The implementation of the Plan on July 21, 2009 resulted in a substantial realignment of the interests in the Company between its existing creditors and shareholders as of the Filing Date. As a result, the Company adopted fresh start accounting effective July 21, 2009. In light of the proximity of the Effective Date to the end of its accounting period immediately following July 21, 2009, which is July 31, 2009, the Company has elected to adopt fresh start accounting and account for the effects of the Plan, including the cancellation of the old capital stock of QWI and the creation and issuance of Worldcolor's new capital stock, as if such events had occurred on July 31, 2009 (the "Fresh-start Date"). Due to our adoption of fresh start accounting, the accompanying consolidated statement of income (loss) include the results of operations for (i) the one month ended July 31, 2009 of the Predecessor and (ii) the two months ended September 30, 2009 of the Successor. Therefore, for the purpose of the management's discussion and analysis of the results of operations, we combined the period and year-to-date results of operations of the Predecessor and the Successor. The resulting combined results of operations for the three and nine months ended September 30, 2009 are then compared to the corresponding periods in the prior year.

We believe the combined results of operations, specifically revenues, EBITDA and operating income, for the three and nine months ended September 30, 2009 provide management and investors with a more meaningful perspective on Worldcolor's ongoing financial and operational performance and trends than if we did not combine the results of operations of the Predecessor and the Successor in this manner. Similarly, we combined the operations of the Predecessor and the Successor when discussing our sources and uses of cash for the three and nine months ended September 30, 2009. Nevertheless, the application of fresh start accounting results in the financial statements of the Successor not being comparable to the Predecessor in many respects (see "New risks factors" section below).

The consolidated financial statements included in this interim MD&A have been prepared in conformity with Canadian generally accepted accounting principles ("GAAP"). However, the interim

4

consolidated financial statements do not include all disclosures required under Canadian GAAP for annual financial statements and, accordingly, should be read in conjunction with the consolidated financial statements and the notes thereto included in QWI's latest annual consolidated financial statements. The same accounting policies as described in QWI's latest annual consolidated financial statements have been used up to the Fresh-start Date. The accounting policies of the Successor are described in Note 3 of the interim consolidated financial statements.

The Company reports on certain non-GAAP measures that are used by management to evaluate performance of business groups. These measures used in this MD&A do not have any standardized meaning under Canadian GAAP. When used, these measures are defined in such terms as to allow the reconciliation to the closest Canadian GAAP measure. Numerical reconciliations are provided in Figure 4. It is unlikely that these measures could be compared to similar measures presented by other companies.

Since the Effective Date, the Company's reporting currency and its functional currency is the U.S. dollar.

Forward-looking statements

To the extent any statements made in this interim MD&A contain information that is not historical, these statements are forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, and are forward-looking information within the meaning of the "safe harbor" provisions of applicable Canadian securities legislation (collectively "forward-looking statements"). These forward-looking statements relate to, among other things, prospects of Worldcolor's industry and its objectives, goals, strategies, beliefs, intentions, plans, estimates, projections and outlook, and can generally be identified by the use of words such as "may," "will," "expect," "intend," "estimate," "anticipate," "plan," "foresee," "believe" or "continue" or the negatives of these terms, variations on them and other similar expressions. In addition, any statements that refer to expectations, projections or other characterizations of future events or circumstances are forward-looking statements. The Company has based these forward-looking statements on its current expectations about future events. Forward-looking statements do not take into account the effect of transactions or other items announced or occurring after the statements are made. For example, they do not include the effect of dispositions, acquisitions, other business transactions, asset write-downs or other charges announced or occurring after the forward-looking statements are made.

Although the Company believes that the expectations reflected in such forward-looking statements are reasonable, it can give no assurance that these expectations will prove to have been correct, and forward-looking statements inherently involve risks and uncertainties, and undue reliance should not be placed on such statements. Certain material factors or assumptions are applied in making forward-looking statements, and actual results may differ materially from those expressed or implied in such forward-looking statements.

Important factors and assumptions as well as the Company's ability to anticipate and manage the risks associated therewith that could cause actual results to differ materially from these expectations are detailed from time to time in the Company's filings with the U.S. Securities and Exchange Commission ("SEC") and the securities regulatory authorities in Canada, available atwww.sec.gov andwww.sedar.com (copies of which are available onwww.worldcolor.com). The Company cautions that any such list of important factors that could affect future results is not exhaustive. Investors and others should carefully consider the factors detailed from time to time in the Company's filings with the SEC and the securities regulatory authorities in Canada and other uncertainties and potential events when relying on its forward-looking statements to make decisions with respect to the Company.

5

Unless mentioned otherwise, the forward-looking statements in this interim MD&A reflect the Company's expectations as of November 12, 2009, being the date at which they have been approved, and are subject to change after this date. The Company expressly disclaims any obligation or intention to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, unless required by applicable securities laws.

New risk factors

This section should be read in conjunction with Item 3-D "Key Information—Risks Factors" of the Predecessor's annual report on Form 20-F for the year ended December 31, 2008.

The Company's actual financial results may vary significantly from the projections filed with the U.S. Bankruptcy Court.

In connection with the Plan process, the Company was required to prepare projected financial information to demonstrate to the U.S. Bankruptcy Court the feasibility of the Plan and the Company's ability to continue operations upon emergence from bankruptcy protection. The Company filed projected financial information with the U.S. Bankruptcy Court most recently on May 18, 2009 as part of the Disclosure Statement approved by the U.S. Bankruptcy Court. The projections reflect numerous assumptions concerning anticipated future performance and prevailing and anticipated market and economic conditions that were and continue to be beyond management's control and that may not materialize either in whole or in part. Projections are inherently subject to uncertainties and to a wide variety of significant business, economic and competitive risks. The Company's actual results will vary from those contemplated by the projections for a variety of reasons, including the fact that given the Company's emergence from bankruptcy protection, the Company has applied The Canadian Institute of Chartered Accountants handbook ("CICA Handbook") Section 1625,Comprehensive Revaluation of Assets and Liabilities ("Section 1625"), regarding fresh start accounting. As indicated in the Disclosure Statement, the projections applied fresh-start accounting provisions. However, these projections were limited by the information available as of the date of the preparation of the projections. Therefore, variations from the projections may be material. The projections have not been incorporated by reference into the interim consolidated financial statements for the nine-month period ended September 30, 2009 nor into this interim MD&A, and neither these projections nor any version of the Disclosure Statement should be considered or relied upon in connection with the purchase of any of the Company's new securities.

Because the Company's consolidated financial statements reflect fresh start accounting adjustments starting in the third quarter of 2009, and because of the effects of the transactions that became effective pursuant to the Plan, financial information in these and future consolidated financial statements will not be comparable to the Company's financial information from prior periods.

On the Company's emergence from creditor protection under Chapter 11 and the CCAA, the Company adopted fresh start accounting in accordance with CICA Handbook Section 1625Comprehensive Revaluation of Assets and Liabilities. Under fresh start accounting, the Company undertook a comprehensive re-evaluation of its assets and liabilities based on the estimated enterprise value of $1.5 billion as established in the Plan. Enterprise value is generally defined to be the Company's estimated fair value at the Fresh-start Date, less cash and cash equivalents. As a result of fresh start accounting, Worldcolor became a new entity for financial reporting purposes. Accordingly, the consolidated financial statements of the Successor on or after August 1, 2009 will not be comparable in many respects to the Company's statement of financial position and statement of operations for periods prior to the adoption of fresh start accounting and prior to accounting for the effects of the Plan.

6

Our estimates of fair value are based on independent appraisals and valuations, some of which are not final. Accordingly, the process of allocating the estimated enterprise value was not fully completed as of the date of issuance of our Consolidated Financial Statements and the amounts assigned to the assets and liabilities may be adjusted as new or improved information on asset and liability appraisals becomes available. This may result in an adjustment to our preliminary allocation of fair value and such adjustments to the recorded fair value of these assets and liabilities at the Fresh-start Date may impact the values ascribed to the Successor's equity. We expect that the allocation of the fair values at the Fresh-start Date will be completed by the time our annual consolidated financial statements are filed in March 2010.

1. Creditor protection and the plan of reorganization

Background and Overview

As described in Note 1 to the 2008 annual consolidated financial statements, on January 21, 2008 QWI obtained an order from the Quebec Superior Court granting creditor protection under theCompanies' Creditors Arrangement Act (the "CCAA") for itself and for 53 U.S. subsidiaries (the "U.S. Subsidiaries" and, collectively with QWI, the "Applicants"). On the same date, the U.S. Subsidiaries filed a petition under Chapter 11 of the U.S. Bankruptcy Code in the Bankruptcy Court for the Southern District of New York. The proceedings under the CCAA and Chapter 11 are hereinafter collectively referred to as the "Insolvency Proceedings". QWI's Latin American subsidiaries were not subject to the Insolvency Proceedings. During the Insolvency Proceedings, the Applicants continued to operate under the protection of the relevant courts.

On June 22, 2009, the creditors of the Applicants approved a plan of compromise and reorganization (the "Plan") under both the CCAA and Chapter 11. On June 30, 2009, the Plan was sanctioned by the Quebec Superior Court, and it was confirmed by the U.S. Bankruptcy Court on July 2, 2009. The Plan was implemented following various transactions that were completed on July 21, 2009 (the "Effective Date"). Accordingly, the Applicants emerged from bankruptcy protection and QWI was renamed and began operating as Worldcolor on the Effective Date.

The implementation of the Plan on July 21, 2009 resulted in a substantial realignment of the interests in the Company between its existing creditors and shareholders as of the Filing Date. As a result, the Company adopted fresh start accounting effective July 21, 2009 in accordance with section 1625 "Comprehensive Revaluation of Assets and Liabilities" of The Canadian Institute of Chartered Accountants Handbook ("CICA Handbook"). Fresh start accounting requires resetting the historical net book value of assets and liabilities to fair value by allocating the entity's reorganization value of $1.5 billion to its assets and liabilities in a manner consistent with section 1581 "Business Combinations" of the CICA Handbook. The excess reorganization value over the fair value of tangible and identifiable intangible assets has been recorded as a charge to capital stock in the consolidated balance sheet. Future income taxes, at the Fresh-start Date, have been determined in conformity with section 3465 "Income Taxes" of the CICA Handbook. For additional information regarding the impact of fresh start accounting, see "Fresh Start Consolidated Balance Sheet" below. In light of the proximity of the Effective Date to the end of its accounting period immediately following July 21, 2009, which is July 31, 2009, the Company has elected to adopt fresh start accounting and account for the effects of the Plan, including the cancellation of the old capital stock of QWI and the creation and issuance of Worldcolor's new capital stock, as if such events had occurred on the Fresh-start Date. The Company evaluated the activity between July 22, 2009 and July 31, 2009 and, based upon the immateriality of such activity, concluded that the use of July 31, 2009 to reflect the fresh start accounting adjustments was appropriate for financial reporting purposes. The use of the July 31, 2009 date is for financial reporting purposes only and does not affect the Effective Date of the Plan.

7

Plan of Reorganization

Following implementation of the Plan, Worldcolor reorganized its capital structure and issued (or will issue) the following securities in exchange for $3.1 billion of Liabilities Subject to Compromise ("LSTC"):

- •

- New unsecured notes to be issued in the estimated aggregate principal amount of $50 million;

- •

- 12.5 million new convertible Class A preferred shares;

- •

- 73.3 million new common shares; and

- •

- 10.7 million Series I warrants and 10.7 million Series II warrants.

In accordance with the terms of the Plan, the common shares, the preferred shares and the Series I and Series II warrants were issued in escrow as of the Effective Date pending the resolution of claims. Subsequently, a portion of the securities has been released from escrow. These transactions are considered non-cash transactions for cash flow purposes.

In addition, cash payments of $100 million in satisfaction of certain claims were made to holders of the Predecessor's senior secured debt, all of which were paid on the Effective Date. Also, the Company will make payments of approximately $66 million in connection with secured, administrative, priority tax and small convenience unsecured claims, of which $10 million was paid on the Effective Date and $3.3 million was paid prior to September 30, 2009.

The implementation of the Plan also involved the following refinancing transactions:

- •

- Repayment of $586.6 million under the Predecessor's debtor-in-possession ("DIP") financing; and

- •

- Entering into a new exit financing credit facility of $800 million.

Pursuant to the Plan, on the Effective Date, QWI's then existing Multiple Voting Shares, Redeemable First Preferred Shares and Subordinate Voting Shares were effectively cancelled for no consideration in accordance with the Articles of Reorganization that were filed with the Court as one of the steps to implement the Plan.

The Company continues to incur expenses related to the Insolvency Proceedings, primarily professional fees that were classified as reorganization items in the Predecessor's financial results. After emergence, these expenses are classified as Impairment of assets, restructuring and other charges ("IAROC") (Note 7), in the Successor's Consolidated Statement of Income (Loss).

Significant Ongoing Insolvency Proceedings Matters

Claims Procedure

On September 29, 2008, QWI initiated a claims procedure for the identification, resolution and barring of claims against the Applicants as authorized by the courts in the Insolvency Proceedings.

The total amount of such claims filed exceeded the amount recorded in the Predecessor's interim consolidated financial statements as LSTC. Differences in the total dollar value of the claims filed by creditors and the liabilities recorded are being investigated and resolved in connection with the claims resolution process.

As set out in the Canadian and U.S. Claims Procedure Orders, certain claims were excluded from the claims process ("Excluded Claims") and do not have to be proven as part of the Insolvency Proceedings, as they are not LSTC.

8

Claims Assessment

As of October 26, 2009, a total of 10,470 claims ("Total Claims") had been received, of which 1,151 were filed against QWI and 9,319 were filed against the U.S. Subsidiaries. The Total Claims filed, net of subsequent withdrawn claims, amounted to $48.2 billion.

| | | | | |

Claims filed net of withdrawn claims as at October 26, 2009 | | $ | 48,224.5 | |

Less: | | | | |

| | Excluded claims | | | 2,474.8 | |

| | Duplicate claims | | | 42,508.3 | |

| | | | |

Claims files net of withdrawn, excluded and duplicate claims | | | 3,241.4 | |

Claims still under review | | | 460.5 | |

| | | | |

Liabilities subject to compromise (excluding post-filing interest) | | $ | 2,780.9 | |

| | | | |

The Claims Procedure Order required creditors to file a separate proof of claim against each of the Applicants against which they believed they had a claim. For a number of reasons, certain creditors have filed the same claim against two or more of these Applicants. One instance where this duplication occurs is where a creditor takes the position that multiple Applicants are jointly and severally liable for a single Applicant's debt. Another situation that gives rise to duplication is where one or more of the Applicants has or have guaranteed another Applicant's indebtedness. The Total Claims filed included a number of such multiple or duplicate claims and, as a result, the total value of such claims is overstated. The Company believes these multiple or duplicate claims amount to $42.5 billion.

The Total Claims filed less duplicate or multiple claims, Excluded Claims and subsequently withdrawn claims amount to approximately $3.2 billion. Of this amount, QWI recorded $2.8 billion (excluding post-filing interest) as LSTC, on the Predecessor's consolidated balance sheet as of July 31, 2009.

The difference between the recorded LSTC and the amount of Total Claims filed less duplicate or multiple claims, Excluded Claims, and claims subsequently withdrawn amounts to $0.4 billion and continues to be investigated. The Company believes it is unlikely that any of these excess claims, or unaccrued portion thereof, will be allowed by the relevant courts. It is not possible to estimate the quantum of the claims that will ultimately be allowed by the courts. However, we believe there will be no further material impact to the Consolidated Statement of Income (Loss) of the Successor from the settlement of unresolved general unsecured claims against the Canadian and U.S. non-operating debtors because the holders of such claims will receive under the Plan only their pro rata share of the distribution of the newly issued common shares, Class A preferred shares and Series I and Series II warrants. It is however possible that allowed general unsecured claims against the U.S. operating debtors as well as secured priority and administrative claims against the Debtors may be in excess of the amount recorded as of September 30, 2009 given the magnitude of the claims asserted (see Note 16 to our interim consolidated financial statements for a description of the terms and conditions of the unsecured notes to be issued). In light of the substantial number and amount of claims filed, particularly duplicate and multiple claims, the claims resolution process may take considerable time to complete and will continue after the Company's emergence from bankruptcy protection.

Legal issues related to emergence

Pursuant to the Plan, claims for the recovery of amounts paid to the holders of certain senior unsecured notes and/or other creditors prior to the Filing Date as preferential or fraudulent conveyances, whether arising under the Bankruptcy Code or similar state laws, including amounts received by the Applicants on account of such claims prior to the Effective Date (such claims and amounts being collectively referred to as the "Avoidance Actions") were transferred to a trust (the

9

"Litigation Trust") created for the benefit of creditors, as specifically provided for therein. To facilitate the implementation of the Litigation Trust, the Plan requires the Company to fund a secured loan to the Litigation Trust in an amount of up to $5 million in order to pay for the costs and expenses of its administration as well as the prosecution of the Avoidance Actions, and will be funded as these costs and expenses are incurred by the Litigation Trust. The loan will be secured by a pledge in favor of the Company on the Avoidance Actions and all interests thereon and other earnings, income or other assets of the Litigation Trust. There was no funding of this secured loan by the Company as of September 30, 2009.

Fresh-start consolidated balance sheet

As previously noted, the Company adopted "fresh start" accounting at the Fresh-start Date. Under fresh start accounting, the Company undertook a comprehensive re-evaluation of its assets and liabilities based on the estimated enterprise value of $1.5 billion as established in the Plan. Enterprise value is generally defined to be the Company's estimated fair value at the Fresh-start Date, less cash and cash equivalents. As a result of fresh start accounting, Worldcolor became a new entity for financial reporting purposes. Accordingly, the consolidated financial statements of the Successor on or after August 1, 2009 are not comparable to the consolidated financial statements of the Predecessor prior to that date.

Our estimates of fair value are based on independent appraisals and valuations, some of which are not final. Accordingly, the process of allocating the estimated enterprise value was not fully completed as of the date of issuance of our Consolidated Financial Statements and the amounts assigned to the assets and liabilities may be adjusted as new or improved information on asset and liability appraisals becomes available. This may result in an adjustment to our preliminary allocation of fair value and such adjustments to the recorded fair value of these assets and liabilities at the Fresh-start Date may impact the values ascribed to the Successor's equity. We expect that the allocation of the fair values at the Fresh-start Date will be completed by the time our annual consolidated financial statements are filed in March 2010. To determine the enterprise value of the Successor, management developed a set of financial projections for the Successor using a number of estimates and assumptions. With the assistance of financial advisors, management determined the enterprise value and corresponding equity value of the Successor based on these financial projections using various valuation methods, including (a) selected publicly-traded companies' analysis, (b) selected transactions analysis and (c) a discounted cash flow analysis. Based upon these analyses, management estimated that the going concern enterprise value of the Successor, at the Fresh-start Date, was in a range of $1.25 billion to $1.75 billion. The enterprise value and the corresponding equity value are dependent on achieving the future financial results set forth in management's projections, as well as the realization of certain other assumptions. For the valuation of individual assets and liabilities, management has estimated the fair value using prices for similar assets and liabilities in the market place (market approach) or discounted future cash flows (income approach). The fair value of preferred shares, warrants and embedded derivatives were determined using valuation models for such instruments. All estimates, assumptions, valuations, appraisals and financial projections, including the fresh start adjustments, the enterprise value and equity value, are inherently subject to significant uncertainties outside of management's control. Accordingly, there can be no assurance that the estimates, assumptions, valuations, appraisals and financial projections will be realized and actual results could vary materially.

A fresh-start consolidated balance sheet as at July 31, 2009 is set out below with adjustments summarized in the columns captioned a) Plan of Reorganization, b) Exit Financing and c) Fresh Start Adjustments. These adjustments reflect the effect of the Plan's implementation, including the compromise of various liabilities, the issuance of new securities and various cash payments, as more thoroughly described in the Plan.

10

Fresh-start Consolidated Balance Sheet

(In millions of US dollars)

(Unaudited)

| | | | | | | | | | | | | | | | | |

| | Predecessor

July 31, 2009 | | Plan of

Reorganization | | Exit

Financing | | Fresh Start

Adjustments | | Successor

July 31, 2009 | |

|---|

Assets | | | | | | | | | | | | | | | | |

Current assets: | | | | | | | | | | | | | | | | |

| | Cash and cash equivalents | | $ | 292.5 | | $ | (104.2 | ) | $ | (123.5 | ) | $ | — | | $ | 64.8 | |

| | Accounts receivable | | | 485.2 | | | (23.4 | ) | | — | | | — | | | 461.8 | |

| | Inventories | | | 190.4 | | | — | | | — | | | 5.8 | | | 196.2 | |

| | Income taxes receivable | | | 32.6 | | | (25.7 | ) | | — | | | — | | | 6.9 | |

| | Future income taxes | | | 8.9 | | | 9.5 | | | — | | | (4.4 | ) | | 14.0 | |

| | Prepaid expenses and deposits | | | 60.8 | | | 4.6 | | | — | | | — | | | 65.4 | |

| | | | | | | | | | | | |

Total current assets | | | 1,070.4 | | | (139.2 | ) | | (123.5 | ) | | 1.4 | | | 809.1 | |

Property, plant and equipment | | |

1,121.4 | | |

8.6 | | |

— | | |

(3.1 |

) | |

1,126.9 | |

Intangible assets | | | — | | | — | | | — | | | 389.0 | | | 389.0 | |

Restricted cash | | | 92.7 | | | (32.5 | ) | | — | | | — | | | 60.2 | |

Future income taxes | | | 2.4 | | | 2.7 | | | — | | | 4.1 | | | 9.2 | |

Other assets | | | 348.1 | | | (3.8 | ) | | 0.1 | | | (260.5 | ) | | 83.9 | |

| | | | | | | | | | | | |

Total assets | | $ | 2,635.0 | | $ | (164.2 | ) | $ | (123.4 | ) | $ | 130.9 | | $ | 2,478.3 | |

| | | | | | | | | | | | |

Liabilities and Shareholders' equity (deficit) | | | | | | | | | | | | | | | | |

Current liabilities: | | | | | | | | | | | | | | | | |

| | Bank indebtedness | | $ | 2.1 | | $ | — | | $ | — | | $ | — | | $ | 2.1 | |

| | Trade payables | | | 91.3 | | | (1.9 | ) | | — | | | — | | | 89.4 | |

| | Accrued liabilities | | | 292.3 | | | (7.8 | ) | | — | | | 0.4 | | | 284.9 | |

| | Amounts owing in satisfaction of bankruptcy claims | | | — | | | 55.8 | | | — | | | — | | | 55.8 | |

| | Income and other taxes payable | | | 43.7 | | | (2.3 | ) | | — | | | (28.1 | ) | | 13.3 | |

| | Future income taxes | | | 0.1 | | | — | | | — | | | — | | | 0.1 | |

| | Current portion of long term debt | | | 13.0 | | | — | | | — | | | — | | | 13.0 | |

| | Current portion of liabilities subject to compromise | | | 166.0 | | | (166.0 | ) | | — | | | — | | | — | |

| | | | | | | | | | | | |

Total current liabilities | | | 608.5 | | | (122.2 | ) | | — | | | (27.7 | ) | | 458.6 | |

Liabilities subject to compromise | | |

2,924.0 | | |

(2,924.0 |

) | |

— | | |

— | | |

— | |

DIP financing | | | 586.6 | | | — | | | (586.6 | ) | | — | | | — | |

Long-term debt | | | 57.4 | | | 5.8 | | | — | | | 2.8 | | | 66.0 | |

Exit financing | | | — | | | — | | | 463.2 | | | — | | | 463.2 | |

Unsecured Notes | | | — | | | 50.0 | | | — | | | — | | | 50.0 | |

Other liabilities | | | 183.0 | | | 32.3 | | | — | | | 292.8 | | | 508.1 | |

Future income taxes | | | 46.9 | | | 204.7 | | | — | | | (45.7 | ) | | 205.9 | |

Preferred shares—Predecessor | | | 25.5 | | | — | | | — | | | (25.5 | ) | | — | |

Preferred shares—Successor | | | — | | | 94.1 | | | — | | | — | | | 94.1 | |

Shareholders' equity (deficit): | | | | | | | | | | | | | | | | |

| | Capital stock—Predecessor | | | 1,609.4 | | | — | | | — | | | (1,609.4 | ) | | — | |

| | Capital stock—Successor | | | — | | | 705.8 | | | — | | | (127.3 | ) | | 578.5 | |

| | Contributed surplus | | | 107.2 | | | 53.9 | | | — | | | (107.2 | ) | | 53.9 | |

| | Deficit | | | (3,664.8 | ) | | 1,735.4 | | | — | | | 1,929.4 | | | — | |

| | Accumulated other comprehensive income (loss) | | | 151.3 | | | — | | | — | | | (151.3 | ) | | — | |

| | | | | | | | | | | | |

| | | (1,796.9 | ) | | 2,495.1 | | | — | | | (65.8 | ) | | 632.4 | |

| | | | | | | | | | | | |

Total liabilities and shareholders' equity (deficit) | | $ | 2,635.0 | | $ | (164.2 | ) | $ | (123.4 | ) | $ | 130.9 | | $ | 2,478.3 | |

| | | | | | | | | | | | |

See accompanying assumptions

11

Plan of Reorganization Column

In the Plan of Reorganization column, LSTC of $3.1 billion in the Predecessor was discharged with the issuance of common shares, preferred shares, warrants and unsecured notes by Worldcolor. Certain other claims of holders under the Predecessor's senior secured debt and certain other secured, administrative, priority tax and convenience unsecured claims of approximately $166 million will be paid in cash, of which $110 million was paid on the Effective Date. The remaining balance was recorded as a current liability. In addition, certain income tax liabilities amounting to $25.7 million that were subject to compromise are expected to be settled against income taxes receivable from the current and prior years. Finally, the Plan provides for the repudiation of the non-qualified pension plans, collectively defined as "Rejected Employee Agreements". As of August 10, 2009, almost all of the participants in the Rejected Employee Agreements have agreed to participate in new non-qualified benefit plans and agreements (collectively, the "New Benefits Plan"). As a result, an amount of $32.3 million was recorded to recognize the unfunded liability of the New Benefits Plan, and reflected as other liabilities, in settlement of the liability for Rejected Employee Agreements which was subject to compromise. The employees that did not participate in the new plan filed a claim against the Company prior to emergence, and management's best estimate of the amount to be disbursed was included in the LSTC prior to emergence.

Projected net future income tax liabilities of approximately $190.7 million were recognized on the discharge of the LSTC. The discharge of the LSTC gives rise to cancellation of debt ("COD") income for income tax purposes and is projected to reduce certain of the Company's tax attributes, such as net operating loss ("NOL") and NOL carry forwards and capital losses carry forwards and the tax basis of the Company's depreciable and non-depreciable assets, which will increase the Company's income tax obligation in the future. Because some of the debtors' outstanding indebtedness will be satisfied under the Plan by way of consideration other than cash, the amount of COD income, and accordingly the amount of tax attributes that may be reduced, will depend in part on the fair market value of such non-cash consideration. The final determination of COD Income for income tax purposes and the related reduction of tax attributes for the U.S. subsidiaries will be based on the final results for 2009. Therefore, the Company may adjust the preliminary allocation of fair value of its future tax assets and liabilities in the fourth quarter of 2009.

Exit Financing Column

The Company obtained exit financing of $800 million including a Term Loan of $450 million, fully drawn, and a Revolving Credit Facility of $350 million, of which $89 million was drawn on the Effective Date. Transaction fees and debt issuance costs of $75.8 million have been reflected as a reduction to the face value of the Term Loan and draws on the Revolving Credit Facility at the Fresh-start Date. Net cash raised from the Term Loan and Revolving Credit Facility, together with cash and cash equivalents of $123.5 million was used to repay the DIP financing of the Predecessor.

Fresh Start Adjustments Column

The fresh start adjustments reflect the estimated fair value of the Company's assets and liabilities as of the Fresh-start Date. The significant fresh start accounting adjustments reflected in the Fresh-start balance sheet, based on current estimates, are summarized as follows:

- (a)

- Working capital:

The historical cost for substantially all of the Company's current assets and liabilities is reflective of their current fair values. Work-in-process inventories were increased by $5.8 million to reflect their market value.

12

- (b)

- Property, plant and equipment:

A fresh start adjustment of $3.1 million was recorded to reduce the historical cost of property, plant and equipment to estimated fair values.

- (c)

- Intangibles and Other assets:

A fresh start adjustment of $389.0 million was recorded for finite-life intangible assets representing the estimated fair value of Worldcolor's customer relationships and contracts. These intangible assets will be amortized on a straight- line basis over their estimated useful lives which range from 4 years to 15 years.

Other fresh start adjustments to estimated fair value include: the reduction of pension assets of $142.5 million, the reduction of contract acquisition costs of $82.3 million, which are effectively included in the aforementioned intangible assets, and other various fair value adjustments totalling $35.7 million.

- (d)

- Other liabilities:

Fresh start adjustments of $293.5 million were recorded to reflect the values of the unfunded pension and other postretirement benefits liabilities at the Fresh-start Date and reflect the Plan assumptions that the existing registered pension plans will remain essentially unchanged. The Company also reclassified $40.7 million of reserves for tax uncertainties, mainly from income and other taxes payable. Other fresh start adjustments amounting to $41.4 million were made to reduce other liabilities to their estimated fair values as of the Fresh-start Date.

- (e)

- Future income taxes:

A fresh start adjustment of $32.3 million, which decreases net future income tax liabilities, has been recorded for the recognition of net future income tax assets related to the aforementioned fresh start adjustments made to property, plant and equipment, intangible assets, other assets and other liabilities, in addition to the reclassification of $13.1 million of reserves for tax uncertainties to other liabilities.

- (f)

- Shareholders' equity (deficit):

Adopting fresh start accounting results in a new reporting entity with no retained earnings or deficit. All Predecessor capital stock has been eliminated and replaced by the new equity structure of the Successor. The fresh start adjustments include the cancellation of Predecessor capital stock, preferred shares, contributed surplus, deficit and accumulated other comprehensive income, as well as a reduction to the Successor Capital Stock as a result of the excess of the reorganization value over the fair value of the identifiable assets and liabilities stemming from fresh start accounting.

2. Financial review

2.1. Industry trends and outlook

Global economic conditions affect our customers' businesses and the markets they serve. The credit crisis and global economic weakness have resulted in constrained advertising spending and, in certain cases, customer financial difficulties in our North American segment. This has put significant downward pressure on both volumes and, to a lesser degree, on price, across nearly all of North America's printing and related services.

13

During 2008 and continuing in 2009, we undertook various initiatives to adapt our cost structure to the rapidly changing economic environment including:

- •

- Divested our non-strategic operations in Europe in June 2008, which allowed us to remain focused on our core business in the Americas and reduced the operational risks associated with the uncertainty of the long-term profitability of the European operations.

- •

- Implemented significant profit improvement initiatives to align our costs with anticipated volume decreases. In June 2008, we integrated and rationalized the number of business divisions in the U.S. from six to three, which allowed us to better serve existing and new customers by having more streamlined and customer-driven operations. Three facilities were closed in 2008, one in April 2009, one in July 2009 and two are scheduled to close at the end of the fourth quarter. Corporate and plant staff levels were reduced by more than 10% in 2008 and were reduced a further 13% on a year-to-date basis in 2009.

- •

- Froze the salaries of all non-unionized North American employees effective January 1, 2009, suspended employer's contributions for non-unionized U.S. employees to the 401(k) plans effective February 1, 2009, and reduced Senior Management salaries by 5%.

- •

- Implemented a significant cost reduction plan in North America, effective April 19, 2009. This plan includes a 10% wage reduction for non-unionized salaried and hourly employees (including sales commissions), a reduction of employees' paid vacation entitlement by one week, suspension of the employer's contribution for non-unionized U.S. employees for the 401(a) plans, standardization in pay for work on holidays to time-and-a-half, and changes to the Company's severance and overtime policies. In connection with the implementation of this cost savings plan, all the collective agreements were re-opened during the second quarter of 2009 and the Company has obtained similar concessions from its union employees. The annual cost savings relating to these initiatives are estimated at approximately $100 million.

The current North American recession is expected to continue to put downward pressure on volumes and prices as retailers and publishers further adjust their budgets for printing services. Competition in the industry remains intense as the industry is still in the process of consolidating and is still suffering from overcapacity. Under these conditions, we are focusing on improving our product and segment mix, adding customer value through initiatives such as our new integrated multi-channel solutions and improving productivity through continuous improvement projects and technology. We are also aggressively aligning our cost structure to mitigate the impact of the economic downturn.

Latin America has been less affected by the global economic weakness than North America, with the exception of its export sales. With current and planned investments in new capacity, this segment's revenues are forecast to increase in line with expected growth from an existing customer base.

14

2.2. Third quarter review

Figure 1

Management assesses the Company's performance based on, among other measures, operating income and Adjusted EBIT. Certain of these measures are not defined by Canadian GAAP. A reconciliation of non-GAAP measures to their respective closest GAAP measures, together with a discussion of their use, is provided in Figure 4. An analysis of the segment results is also presented in Section 2.4.

Operating revenues

Our consolidated operating revenues for the third quarter of 2009 were $769.9 million, a 23% decrease when compared to $993.6 million for the same period in 2008. Excluding the negative impact of currency translation (Figure 2), operating revenues were down 21% compared to the same period in 2008. The decrease in operating revenues resulted primarily from lower volumes mostly due to the North American recession, including reduced advertising spending, and, to a lesser extent, negative price pressures. Management believes that the negative impact on revenues of the Insolvency Proceedings is diminishing in 2009. More details are provided in the "Segment results" section.

Paper sales, excluding the effect of currency translation, decreased by 28% for the third quarter of 2009, compared to the same period in 2008. The decrease in paper sales is mostly explained by lower volumes as well as one large customer now supplying its own paper. The decrease in paper sales has an impact on operating revenues, but it has little impact on operating income because the cost of paper is generally passed on to the customer.

15

Impact of Foreign Currency and Paper Sales

($ millions)

| | | | | | | |

| | Combined | | Combined | |

|---|

| | Three months ended

September 30, 2009 | | Nine months ended

September 30, 2009 | |

|---|

Foreign currency unfavorable impact on revenues | | $ | (14.6 | ) | $ | (81.7 | ) |

Paper sales unfavorable impact on revenues | | | (75.6 | ) | | (199.4 | ) |

Foreign currency favorable (unfavorable) impact on operating income | | | (0.2 | ) | | 3.3 | |

Figure 2 | |

Operating income and adjusted EBIT

In the third quarter of 2009, adjusted EBIT increased to $51.5 million compared to $33.7 million for the same period in 2008 and resulted mainly from lower depreciation and amortization expenses as well as the implementation of a number of initiatives designed to help reverse the negative impact of the drop in volume. Adjusted EBIT margin was 6.7% for the third quarter of 2009, compared to 3.4% for the same period in 2008, which was also helped by lower paper sales, which reduce operating revenues but have little impact on adjusted EBIT. Excluding depreciation and amortization of $45.8 million for the third quarter of 2009 ($54.5 million for the same period in 2008), cost of sales for the third quarter of 2009 decreased by 26% to $606.7 million, compared to $824.3 million for the corresponding period in 2008. Excluding depreciation and amortization, gross profit margin was 21.2% in the third quarter of 2009 compared to 17.0% in 2008.

Selling, general and administrative expenses for the third quarter of 2009 were $65.9 million, a decrease of 19% compared to $81.1 million for the same period in 2008. Excluding depreciation and amortization expense of $3.0 million for the third quarter of 2009 and $2.3 million for the same period in 2008 and excluding the favorable impact of currency translation of $1.4 million, selling, general and administrative expenses decreased by 18%, compared to the same period in 2008. The favorable variance is mainly explained by various workforce reduction initiatives, reduction in salaries and benefits due to the cost reduction plan implemented in April 2009, as well as lower commission and bad debt expenses.

The total depreciation and amortization expense included in cost of sales and selling, general and administrative expense above was $48.8 million for the third quarter of 2009, compared to $56.8 million for the third quarter of 2008. Excluding the favorable impact of currency translation of $0.6 million, depreciation and amortization expenses decreased by 13%, compared to the same period last year. The lower depreciation and amortization resulted mainly from fresh-start adjustments (see the "Fresh Start Adjustments Column" section for more details) which re-set the historical cost of the fixed assets to their fair values. This effectively increased the weighted-average remaining useful lives of the re-valued property, plant and equipment compared to the historical lives. In addition, the lower level of capital investment following finalization of the extensive retooling plan in 2007, the impairment of long-lived assets that was recorded in the fourth quarter of 2008, as well as plant closures that occurred during the last four quarters combined to further reduce depreciation of property, plant and equipment. Offsetting this reduced depreciation expense was an increase in the amortization of customer relationships and contracts amounting to $6.7 million, a result of recording this finite-life intangible asset on the Successor's balance sheet.

Operating income for the quarter ended September 30, 2009 was $39.2 million, compared to $27.0 million for the third quarter ended September 30, 2008, for the reasons explained above for

16

adjusted EBIT, partially offset by higher Impairment of Assets, Restructuring and Other Charges ("IAROC").

As discussed in greater detail in the "Industry trends and outlook" section, the Company put in place in 2009 a number of initiatives, including salaries and benefits reductions as well as the closure of three plants, which are intended to help reverse the negative earnings trend resulting from the drop in volume.

Other items

During the third quarter of 2009, we recorded IAROC of $12.3 million, compared to $6.7 million for the same period in 2008. The charge for the quarter was mainly related to plant closures and workforce reductions in North America. These measures are described below under "Impairment of assets and restructuring initiatives".

Financial income was $9.3 million in the third quarter of 2009, compared to an expense of $72.7 million for the same period in 2008. The decrease is mainly due to gains on foreign exchange ($37.8 million), primarily as a result of favorable movement in the Canadian dollar arising on the translation of net monetary liabilities (principally debt and LSTC) denominated in currencies other than the Canadian dollar, which was the functional currency of the Predecessor. In addition, interest expense decreased as a result of the Company's emergence from bankruptcy protection.

We recorded reorganization items which represent post-filing expenses, gains and losses, and provisions for losses that can be directly associated with the reorganization and restructuring of the Applicants amounting to $14.6 million in the third quarter of 2009 prior to emerging from bankruptcy ($26.4 million in 2008). Following the Company's emergence from the Insolvency Proceedings on July 21, 2009, reorganization expenses are recorded in IAROC.

Income tax expense was $17.6 million in the third quarter of 2009, compared to a recovery of $9.4 million for the same period in 2008. Income tax expense before IAROC was $21.0 million in the third quarter of 2009 compared to an income tax recovery of $7.8 million for the same period last year. In 2009, the effective income tax rate was impacted by the non-deductibility of interest on pre-petition U.S. debt as well as additional valuation allowance mainly related to tax benefits whose realization is not foreseen in Canada and in the U.S. In addition, the 2009 effective income tax rate was favorably affected by foreign tax rate differences.

Net income (loss)

For the third quarter ended September 30, 2009, we reported a net income of $13.3 million compared to a loss from continuing operations of $63.6 million for the same period in 2008. These results incorporated IAROC, net of income taxes, of $8.9 million compared with $5.1 million for the same period in 2008 and reorganization items, net of taxes, of $13.0 million compared to $24.0 million for the same period in 2008.

2.3. Year-to-date review

Operating revenues

On a year-to-date basis, our consolidated operating revenues were $2.22 billion, a 25% decrease when compared to $2.98 billion for the same period in 2008. Excluding the negative impact of currency translation (Figure 2), operating revenues were down 23% compared to the same period in 2008. The decrease in operating revenues resulted primarily from lower volumes mostly due to the North American recession, which resulted in reduced advertising spending, and, to a lesser extent, negative price pressures. We believe that the negative impact on revenues of the Insolvency Proceedings is diminishing in 2009. More details are provided in the "Segment results" section.

17

Paper sales, excluding the effect of currency translation, decreased by 25% on a year-to-date basis, compared to the same period in 2008. The decrease in paper sales is mostly explained by lower volumes as well as one large customer now supplying its own paper. Variance in paper sales has an impact on operating revenues, but it has little impact on operating income because the cost is generally passed on to the customer.

Operating income and adjusted EBIT

On a year-to-date basis, adjusted EBIT decreased to $42.1 million compared to $70.7 million for the same period in 2008. Adjusted EBIT margin was 1.9% for the first nine months of 2009, compared to 2.4% for the same period in 2008. The decrease in adjusted EBIT margin is mostly due to lower volumes and, to a lesser degree, a decrease in scrap paper revenues explained by a significant drop in market prices. However, this was partially offset by cost initiatives, the largest of which was implemented effective April, 19, 2009. Excluding depreciation and amortization of $132.6 million for the first nine months of 2009 ($169.2 million for the same period in 2008), cost of sales for the first nine months of 2009 decreased by 26% to $1.84 billion, compared to $2.48 billion for the corresponding period in 2008. Excluding depreciation and amortization, gross profit margin was 17.1% in the first nine months of 2009 compared to 16.8% in 2008.

Selling, general and administrative expenses were $205.1 million on a year-to-date basis, a decrease of 22% compared to $262.4 million for the same period in 2008. Excluding depreciation and amortization expense of $10.6 million for the first nine months of 2009 and $7.1 million for the same period in 2008 and excluding the favorable impact of currency translation of $9.3 million, selling, general and administrative expenses decreased by 20%, compared to the same period in 2008. The favorable variance is explained mainly by various workforce reduction initiatives, reduction in salaries and benefits due to the significant cost reduction plan implemented in April 2009 as well as lower commission and bad debt expenses.

The total depreciation and amortization included in cost of sales and selling, general and administrative expenses above were $143.2 million for the first nine months of 2009, compared to $176.3 million for the first nine months of 2008. Excluding the favorable impact of currency translation of $4.0 million, depreciation and amortization expense decreased by 17%, compared to the same period last year. Lower depreciation and amortization resulted mainly from the lower level of capital investment following finalization of our extensive retooling plan in 2007, the impairment of long-lived assets that was recorded in the fourth quarter of 2008, as well as plant closures that occurred during the last four quarters. The decrease in depreciation and amortization also resulted from the fresh start adjustments discussed in greater detail in the "Third quarter review" section above, partially offset by the amortization of customer relationships and contracts which were recorded as part of the fresh-start adjustments.

On a year-to-date basis, operating income was $10.9 million, compared to operating income of $16.4 million for the nine months ended September 30, 2008, for the reasons explained above for adjusted EBIT partially offset by lower IAROC.

As discussed in greater details in the "Industry trends and outlook" section, the Company put in place in 2009 a number of initiatives including salaries and benefits reductions as well as the closure of three plants, which are intended to help reverse the negative earnings trend resulting from the drop in volume.

Other items

On a year-to-date basis, we recorded IAROC of $31.2 million, compared to $54.3 million for the same period in 2008. The charge for the first nine months was mainly related to plant closures and

18

workforce reductions in North America. These measures are described below under "Impairment of assets and restructuring initiatives".

Financial expenses were $85.3 million on a year-to-date basis, compared to $211.3 million for the same period in 2008. The decrease is mainly due to gains on foreign exchange in 2009 ($73.2 million), primarily as a result of favorable movement in the Canadian dollar, and the write-off of deferred financing costs amounting to $58.3 million recorded in the second quarter of 2008.

We recorded reorganization items which represent post-filing expenses, gains and losses, and provisions for losses that can be directly associated with the reorganization and restructuring of the Applicants totaling $67.3 million in the first nine months of 2009 ($68.2 million in 2008).

Income tax expense was $26.3 million on a year-to-date basis, compared to $22.2 million for the same period in 2008. Income tax expense before IAROC was $35.8 million in the first nine months of 2009 compared to $28.7 million for the same period last year. In 2009, the effective income tax rate was impacted by the non-deductibility of interest on pre-petition U.S. debt as well as additional valuation allowance mainly related to tax benefits whose realization is not foreseen in Canada and in the U.S. In addition, the 2009 effective income tax rate was unfavorably affected by foreign tax rate differences.

Net loss

On a year-to-date basis, we reported a net loss of $172.1 million compared to a net loss from continuing operations of $289.9 million for the same period in 2008. These results incorporated IAROC, net of income taxes, of $21.8 million compared with $47.8 million for the same period in 2008 and reorganization items, net of taxes, of $62.1 million compared to $62.3 million for the same period in 2008.

19

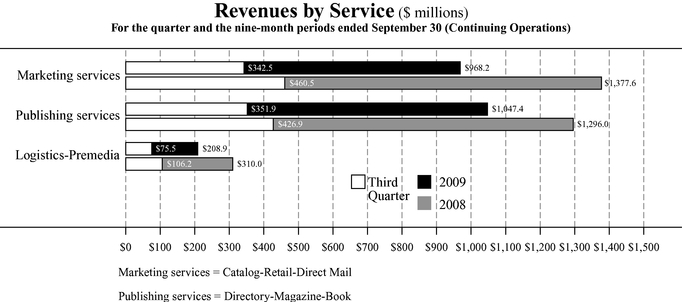

2.4. Segment results

The following is a review of activities by segment which, except as otherwise indicated, focuses only on continuing operations. The reporting structure includes two segments: North America and Latin America.

Segment Results of Continuing Operations ($ millions)

Selected Performance Indicators

| | | | | | | | | | | | | | | | | | | | | | | | | |

| | North America | | Latin America | | Inter-Segment

and Others | | Total | |

|---|

| | Combined

2009 | | Predecessor

2008 | | Combined

2009 | | Predecessor

2008 | | Combined

2009 | | Predecessor

2008 | | Combined

2009 | | Predecessor

2008 | |

|---|

Three months ended September 30 | | | | | | | | | | | | | | | | | | | | | | | | | |

Operating revenues | | $ | 709.7 | | $ | 921.1 | | $ | 60.2 | | $ | 72.5 | | $ | — | | $ | — | | $ | 769.9 | | $ | 993.6 | |

Adjusted EBITDA | | | 100.3 | | | 89.3 | | | 5.0 | | | 6.3 | | | (1.9 | ) | | (1.4 | ) | | 103.4 | | | 94.2 | |

Adjusted EBIT | | | 51.9 | | | 32.3 | | | 1.5 | | | 2.9 | | | (1.9 | ) | | (1.5 | ) | | 51.5 | | | 33.7 | |

IAROC | | | 11.0 | | | 6.1 | | | 0.1 | | | 0.2 | | | 1.2 | | | 0.4 | | | 12.3 | | | 6.7 | |

Operating income (loss) | | | 40.9 | | | 26.2 | | | 1.4 | | | 2.7 | | | (3.1 | ) | | (1.9 | ) | | 39.2 | | | 27.0 | |

Adjusted EBITDA margin | | |

14.1 |

% | |

9.7 |

% | |

8.3 |

% | |

8.7 |

% | |

— | | |

— | | |

13.4 |

% | |

9.5 |

% |

Adjusted EBIT margin | | | 7.3 | % | | 3.5 | % | | 2.5 | % | | 4.0 | % | | — | | | — | | | 6.7 | % | | 3.4 | % |

Operating margin | | | 5.8 | % | | 2.8 | % | | 2.3 | % | | 3.8 | % | | — | | | — | | | 5.1 | % | | 2.7 | % |

Capital expenditures(1) | |

$ |

32.0 | |

$ |

13.8 | |

$ |

2.4 | |

$ |

2.4 | |

$ |

— | |

$ |

1.8 | |

$ |

34.4 | |

$ |

18.0 | |

Change in non-cash balances related to operations, cash flow (outflow)(1) | | | (65.0 | ) | | (21.7 | ) | | (3.9 | ) | | (6.2 | ) | | (13.6 | ) | | 64.5 | | | (82.5 | ) | | 36.6 | |

| | | | | | | | | | | | | | | | | | |

Nine months ended September 30 | | | | | | | | | | | | | | | | | | | | | | | | | |

Operating revenues | | $ | 2,053.0 | | $ | 2,765.8 | | $ | 171.5 | | $ | 217.8 | | $ | — | | $ | — | | $ | 2,224.5 | | $ | 2,983.6 | |

Adjusted EBITDA | | | 188.3 | | | 250.0 | | | 15.7 | | | 17.9 | | | (7.0 | ) | | (6.8 | ) | | 197.0 | | | 261.1 | |

Adjusted EBIT | | | 43.0 | | | 70.0 | | | 6.5 | | | 7.6 | | | (7.4 | ) | | (6.9 | ) | | 42.1 | | | 70.7 | |

IAROC | | | 29.3 | | | 52.7 | | | 0.4 | | | 1.2 | | | 1.5 | | | 0.4 | | | 31.2 | | | 54.3 | |

Operating income (loss) | | | 13.7 | | | 17.3 | | | 6.1 | | | 6.4 | | | (8.9 | ) | | (7.3 | ) | | 10.9 | | | 16.4 | |

Adjusted EBITDA margin | | |

9.2 |

% | |

9.0 |

% | |

9.2 |

% | |

8.2 |

% | |

— | | |

— | | |

8.9 |

% | |

8.8 |

% |

Adjusted EBIT margin | | | 2.1 | % | | 2.5 | % | | 3.8 | % | | 3.5 | % | | — | | | — | | | 1.9 | % | | 2.4 | % |

Operating margin | | | 0.7 | % | | 0.6 | % | | 3.6 | % | | 2.9 | % | | — | | | — | | | 0.5 | % | | 0.6 | % |

Capital expenditures(1) | |

$ |

67.7 | |

$ |

66.7 | |

$ |

6.9 | |

$ |

4.6 | |

$ |

— | |

$ |

8.1 | |

$ |

74.6 | |

$ |

79.4 | |

Change in non-cash balances related to operations, cash flow (outflow)(1) | | | 134.8 | | | 32.6 | | | (2.9 | ) | | (8.8 | ) | | 7.1 | | | 90.0 | | | 139.0 | | | 113.8 | |

| | | | | | | | | | | | | | | | | | |

Figure 3 | |

IAROC: Impairment of assets, restructuring and other charges

Adjusted: Defined as before IAROC

- (1)

- Including both continuing and discontinued operations

20

North America

North American operating revenues for the third quarter of 2009 were $709.7 million, down 23% from $921.1 million in 2008. Excluding the effect of currency translation, operating revenues decreased by 22% in the third quarter of 2009, compared to the same period in 2008. Operating revenues in the North American segment continued to be principally impacted by volume declines and, to a lesser extent, negative price pressures. Volume in North America decreased during the third quarter of 2009 as a result of the North American recession and the resultant negative impact on the markets we serve.

Adjusted EBITDA in North America increased in the third quarter of 2009 compared to the same period in 2008. The adjusted EBITDA margin increased in the third quarter of 2009 to 14.1% compared to 9.7% for the same period in 2008. The increase of adjusted EBITDA margin is mainly due to lower paper sales, which reduce operating revenues but have little impact on adjusted EBITDA. Adjusted EBITDA in North America also continues to be impacted by challenging market conditions. The impact of the decrease in volume, as discussed above, was offset by restructuring initiatives, the reduction in salaries and benefits (more details are provided in the "Industry trends and outlook" section) and efficiencies realized through productivity gains.

Year-over-year, the North American workforce was reduced by 3,243 employees, down 17%, of which 284 positions were eliminated in the third quarter of 2009, mainly due to various restructuring initiatives, including the closure of the Covington, TN facility which was completed in July 2009, the closure of the Memphis, TN facility in the second quarter of 2009 and the closure of the Islington facility in Ontario, which was completed in the fourth quarter of 2008. We also reduced our workforce in most of our other facilities, including our corporate offices, in order to better align our costs with current market conditions.

Latin America

Latin America operates mainly in the Book, Directory, Magazine, Catalog and Retail markets. Latin America's operating revenues for the third quarter of 2009 were $60.2 million, down 17% from $72.5 million for the same period in 2008 primarily due to the unfavorable impact of foreign currency coupled with lower paper prices. Excluding the impact of foreign currency, operating revenues for the third quarter of 2009 were down 6% compared to 2008. Volume in Latin America decreased as a result of the economic slowdown and a decrease in exports to North America, which also resulted in price erosion during the third quarter of 2009. Adjusted EBITDA for the third quarter of 2009 was down 21% compared to the same period in 2008. In addition to volume declines, the unfavorable impact of foreign currency also negatively impacted adjusted EBITDA in the third quarter compared to last year. Overall, recent and upcoming investments in new capacity are expected to improve the product mix of the region and accommodate growth projected from the existing customer base.

2.5. Impairment of assets and restructuring initiatives

Impairment of assets

During the first quarter of 2008, impairment tests were triggered in North America as a result of the retooling plan and the relocation of existing presses and we recorded impairment charges of $16.7 million mainly on machinery and equipment.

Restructuring initiatives

We have undertaken various restructuring initiatives in order to ensure that our facilities are operating at optimal pressroom efficiencies and generating higher returns. Restructuring costs relate largely to plant closures and workforce reductions that occurred in current and prior years. A description of these initiatives is provided in Note 7 to our interim consolidated financial statements for the period ended September 30, 2009.

21

The 2009 restructuring initiatives affected a total of 1,705 employees, of which 1,418 positions were eliminated as of September 30, 2009 and a further 287 are expected to be eliminated. However, we estimate that 161 new jobs will be created in other facilities with respect to the 2009 initiatives. During the first three quarters of 2009, the execution of prior years' initiatives resulted in the elimination of 410 positions with 22 positions still to be eliminated.

As at September 30, 2009, the balance of the restructuring reserve was $10.2 million. The total cash disbursement related to this reserve is expected to be $8.0 million for the remainder of 2009. Finally, the Company expects to record a charge of $11.6 million in upcoming quarters for restructuring initiatives that have already been announced as at September 30, 2009.

Reconciliation of non-GAAP measures

($ millions)

| | | | | | | | | | | | | | |

| | Combined | | Predecessor | | Combined | | Predecessor | |

|---|

| | Three months ended

September 30, | | Nine months ended

September 30, | |

|---|

| | 2009 | | 2008 | | 2009 | | 2008 | |

|---|

Operating income from continuing operations—adjusted | | | | | | | | | | | | | |

| | Operating income | | $ | 39.2 | | $ | 27.0 | | $ | 10.9 | | $ | 16.4 | |

| | Impairment of assets, restructuring and other charges ("IAROC") | | | 12.3 | | | 6.7 | | | 31.2 | | | 54.3 | |

| | | | | | | | | | |

| | Adjusted EBIT(1) | | $ | 51.5 | | $ | 33.7 | | $ | 42.1 | | $ | 70.7 | |

| | | | | | | | | | |

| | Operating income | | $ | 39.2 | | $ | 27.0 | | $ | 10.9 | | $ | 16.4 | |

| | Depreciation of property, plant and equipment(2) | | | 42.1 | | | 56.8 | | | 136.5 | | | 198.3 | |

| | Amortization of other assets(2) | | | 3.1 | | | 3.7 | | | 11.7 | | | 14.2 | |

| | Amortization of customer relationships(2) | | | 6.7 | | | — | | | 6.7 | | | — | |

| | Less depreciation and amortization from discontinued operations | | | — | | | — | | | — | | | (22.1 | ) |

| | | | | | | | | | |

| | Operating income before depreciation and amortization ("EBITDA") | | $ | 91.1 | | $ | 87.5 | | $ | 165.8 | | $ | 206.8 | |

| | IAROC | | | 12.3 | | | 6.7 | | | 31.2 | | | 54.3 | |

| | | | | | | | | | |

| | Adjusted EBITDA(1) | | $ | 103.4 | | $ | 94.2 | | $ | 197.0 | | $ | 261.1 | |

| | | | | | | | | | |

| | Figure 4 | |

- (1)

- Adjusted EBIT and Adjusted EBITDA are the measures the Company has historically used to assess segment profitability. Adjusted EBITDA excludes the following items: IAROC, financial expenses, dividends on preferred shares classified as liability, dividends, depreciation, amortization, reorganization expenses and income taxes, that are not under the control of the business segments and that are not considered in the measurement of their profitability. These items are typically managed by Worldcolor's corporate head office which focuses on strategy development and oversees governance, policy, compliance, human resources, legal, tax and other financial matters. These measures do not have any standardized meanings provided by GAAP and are therefore unlikely to be comparable to similar measures presented by other companies.

- (2)

- As reported in the Consolidated Statement of Cash Flows.

22

Reconciliation of non-GAAP measures

($ millions)

| | | | | | | | | | | | | | |

| | Combined | | Predecessor | | Combined | | Predecessor | |

|---|

| | Three months ended

September 30, | | Nine months ended

September 30, | |

|---|

| | 2009 | | 2008 | | 2009 | | 2008 | |

|---|

Free cash flow(1) | | | | | | | | | | | | | |

| | Cash provided by (used in) operating activities | | $ | (24.9 | ) | $ | 19.7 | | $ | 116.8 | | $ | 99.4 | |

| | Additions to property, plant and equipment | | | (34.4 | ) | | (18.0 | ) | | (74.6 | ) | | (79.4 | ) |

| | Net proceeds from disposal of assets | | | 1.6 | | | 3.0 | | | 3.2 | | | 25.3 | |

| | Net proceeds from business disposals | | | — | | | (0.6 | ) | | — | | | 43.4 | |

| | | | | | | | | | |

| | Free cash flow | | $ | (57.7 | ) | $ | 4.1 | | $ | 45.4 | | $ | 88.7 | |

| | | | | | | | | | |

Figure 4 | |

- (1)

- We present free cash flow as additional information as we believe it is a useful indicator of our ability to operate without reliance on additional borrowing or usage of existing cash. Free cash flow is a measure of the net cash generated which is available for debt repayment and investment in strategic opportunities. Free cash flow is not a calculation based on or derived from Canadian or U.S. GAAP and should not be considered as an alternative to the Consolidated Statement of Cash Flows and is unlikely to be comparable to similar measures presented by other companies.

3. Critical accounting estimates, changes in accounting standards and adoption of new accounting policies

3.1. Critical accounting estimates

The preparation of financial statements in accordance with Canadian GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities, the reported amounts of operating revenues and expenses, and disclosure with respect to contingent assets and liabilities. Critical accounting estimates are generally defined as those requiring assumptions made about matters that are highly uncertain at the time the estimate is made, and when the use of different reasonable estimates or changes to the accounting estimates would have a material impact on a company's financial condition or results of operations. A complete discussion of the critical accounting estimates made by the Company is included in QWI's latest annual report on Form 20-F.

In addition, the adoption of fresh start accounting resulted in the revaluation of all of our assets and liabilities at the Fresh-start Date. Estimates of fair value are not final. Accordingly, the process of allocating the estimated enterprise value was not fully completed as of the date of issuance of our Consolidated Financial Statements and the amounts assigned to the assets and liabilities may be adjusted as new or improved information on asset and liability appraisals becomes available. This may result in an adjustment to our preliminary allocation of fair value and such adjustments to the recorded fair value of these assets and liabilities at the Fresh-start Date may impact the values ascribed to the Successor equity. Changes to estimates made at the Fresh-start Date based on the information that should have been reasonably available at the Fresh-start Date will be accounted in the Statement of Income (Loss) in the period in which the change is made. We expect that the allocation of the fair values at the Fresh-start Date will be completed by the time our annual consolidated financial statements are filed in March 2010. To determine the enterprise value of the Successor, management developed a set of financial projections for the Successor using a number of estimates and assumptions. With the assistance of financial advisors, management determined the enterprise value and corresponding equity value of the Successor based on these financial projections using various valuation

23