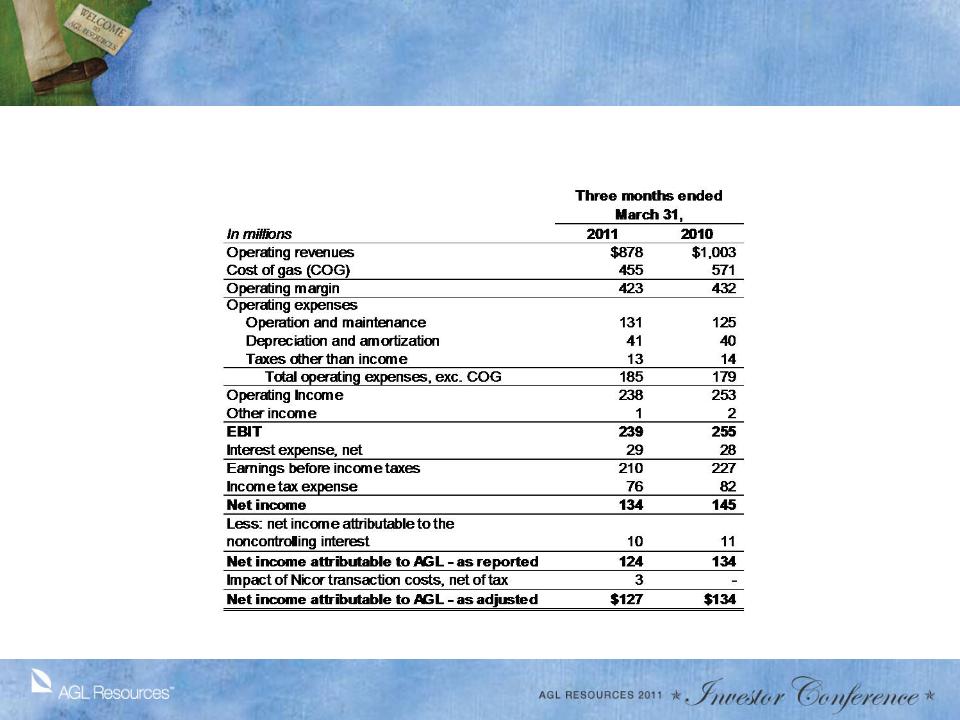

GAAP Reconciliation

Reconciliations of operating margin, EBIT by segment and EPS excluding merger expenses are available in our quarterly reports (Form 10-Q) and

annual reports (Form 10-K) filed with the Securities and Exchange Commission.

Our management evaluates segment financial performance based on EBIT, which includes the effects of corporate expense allocations. EBIT is a non-

GAAP (accounting principles generally accepted in the United States of America) financial measure. Items that are not included in EBIT are financing

costs, including debt and interest expense and income taxes. We evaluate each of these items on a consolidated level and believe EBIT is a useful

measurement of our performance because it provides information that can be used to evaluate the effectiveness of our businesses from an operational

perspective, exclusive of the costs to finance those activities and exclusive of income taxes, neither of which is directly relevant to the efficiency of those

operations.

We also use EBIT internally to measure performance against budget and in reports for management and the Board of Directors. Projections of forward-

looking EBIT are used in our internal budgeting process, and those projections are used in providing forward-looking business segment EBIT projections

to investors. We are unable to reconcile our forward-looking EBIT business segment guidance to GAAP net income, because we do not predict the

future impact of unusual items and mark-to-market gains or losses on energy contracts. The impact of these items could be material to our operating

results reported in accordance with GAAP.

Operating margin is a non-GAAP measure calculated as revenues minus cost of gas, excluding operation and maintenance expense, depreciation and

amortization, taxes other than income taxes, and the gain or loss on the sale of our assets. These items are included in our calculation of operating

income. We believe operating margin is a better indicator than operating revenues of the contribution resulting from customer growth, since cost of gas is

generally passed directly through to customers.

We present our EPS excluding expenses incurred with respect to the proposed merger with Nicor. As we do not routinely engage in transactions of the

magnitude of the proposed Nicor merger, and consequently do not regularly incur transaction related expenses of correlative size, we believe presenting

EPS excluding Nicor merger expenses provides investors with an additional measure of our core operating performance.

EBIT, operating margin and EPS excluding merger expenses should not be considered as alternatives to, or more meaningful indicators of, our

operating performance than operating income or net income, as determined in accordance with GAAP. In addition, our EBIT, operating margin and non-

GAAP EPS may not be comparable to similarly titled measures of another company.

Net income attributable to AGL Resources, as adjusted and Basic and Diluted earnings per share, as adjusted are non-GAAP measures and exclude

transaction costs related to the proposed merger with Nicor. We believe these financial measures are useful to investors because they provide an

alternative method for assessing the Company’s operating results in a manner that is focused on the performance of the Company’s ongoing operations.

The presentation of these financial measures is not meant to be a substitute for financial measures prepared in accordance with GAAP.