UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 20-F

(Mark One) |

| o | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| | |

| | OR |

| | |

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR (15d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| | For the fiscal year ended March 31, 2007 |

| | |

| | OR |

| | |

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| | |

| | OR |

| | |

| o | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| | Date of event requiring this shell company report For the transition period from __________________ to __________________ |

Commission file number 000-27322

MOUNTAIN PROVINCE DIAMONDS INC.

(Exact name of Registrant as specified in its charter)

Not Applicable

(Translation of Registrant’s name into English)

Ontario

(Jurisdiction of incorporation or organization)

401 Bay Street, Suite 2700, PO Box 152, Toronto, Ontario Canada M5H 2Y4

(Address of principal executive offices)

Securities registered or to be registered pursuant to Section 12(b) of the Act.

| Title of each class | Name of each exchange on which registered |

None | Not Applicable |

Securities registered or to be registered pursuant to Section 12(g) of the Act.

Common shares without par value

(Title of Class)

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act.

None

(Title of Class)

Indicate the number of outstanding shares of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report.

55,670,715

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

Note - Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer o | Accelerated filer o | Non-accelerated filer x |

Indicate by check mark which financial statement item the registrant has elected to follow.

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court.

Not Applicable

TABLES OF CONTENTS

| | |

GLOSSARY OF TECHNICAL TERMS | |

| | |

| Identity of Directors, Senior Management and Advisors. | |

| Offer Statistics and Expected Timetable. | |

| | |

| | |

| Capitalization and indebtedness. | |

| Reasons for the offer and use of proceeds. | |

| | |

| Information on the Company | |

| History and development of the Company. | |

| | |

| Organizational structure. | |

| Property, plants and equipment. | |

| Unresolved Staff Comments | |

| Operating and Financial Review and Prospects. | |

| | |

| Liquidity and capital resources. | |

| Research and development, patents and licenses etc. | |

| | |

| Off-balance sheet arrangements. | |

| Tabular disclosure of contractual obligations. | |

| Directors, Senior Management and Employees. | |

| Directors and Senior Management. | |

| | |

| | |

| | |

| | |

| Major Shareholders and Related Party Transactions. | |

| | |

| Related party transactions. | |

| Interests of experts and counsel. | |

| | |

| Consolidated Statements and Other Financial Information. | |

| | |

| | |

| Offer and Listing Details. | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| Memorandum and articles of association. | |

| | |

| | |

| | |

| Dividends and paying agents. | |

| | |

| | |

| | |

| Quantitative and Qualitative Disclosures About Market Risk. | |

| Description of Securities Other than Equity Securities. | |

| | |

| Defaults, Dividend Arrearages and Delinquencies. | |

| Material Modifications to the Rights of Security Holders and Use of Proceeds. | |

| | |

| | |

| Audit Committee Financial Expert. | |

| | |

| Principal Accountant Fees and Services. | |

| Exemptions from the Listing Standards for Audit Committees. | |

| Purchases of Equity Securities by the Issuer and Affiliated Purchasers. | |

| | |

| | |

| | |

| | |

| | |

| |

GLOSSARY

Affiliate has the meaning given to affiliated bodies corporate under the Ontario Business Corporations Act ;

AK Property means the claims known as the "AK claims" held by the Gahcho Kué Joint Venture;

AK-CJ Properties means, collectively, the AK Property and CJ Property Claims;

AMEC means AMEC E&C Services Ltd.

CJ Property means the claims known as the "CJ claims", which have now lapsed, previously held by MPV;

Arrangement means the arrangement between the Company and Glenmore which was effected as of June 30, 2000;

Arrangement Agreement means the Arrangement Agreement dated as of May 10, 2000, and made between MPV and Glenmore, including the Schedules to that Agreement;

Business Corporations Act [Ontario] means the R.S.O. 1990, CHAPTER B.16, as amended from time to time;

CDNX means the Canadian Venture Exchange Inc, formerly the Vancouver Stock Exchange, and now known as the TSX Venture Exchange;

Camphor means Camphor Ventures Inc.;

Canadian National Instrument 43-101 means the National Instrument 43-101 (Standards of Disclosure for Mineral Projects) adopted by the Canadian Securities Administrators;

Code means the United States Internal Revenue Code of 1986, as amended;

Company,MPV or Registrant means Mountain Province Diamonds Inc.;

De Beers means De Beers Consolidated Mines Ltd.;

De Beers Canada or Monopros means De Beers Canada Exploration Inc., formerly known as Monopros Limited, a wholly-owned subsidiary of De Beers;

Desktop Study means the preliminary technical assessment of the Gahcho Kué resource conducted by De Beers Consolidated Mines Ltd. in 2000 (updated in 2003), which considered an 18 million tonne mineable resource. AMEC provided an Independent Qualified Persons’ review of the Desktop Study. Although the Desktop Study incorporates “inferred mineral resources that are considered too speculative geologically” to be categorized as “mineral reserves”, AMEC’s assessment supports the financial model for the project developed by De Beers. The capital and operating cost estimates are considered to be at scoping level, with an expected range of accuracy of +/- 30 percent.

Exchange Act means the U.S. SecuritiesExchange Act of 1934;

Gahcho Kué Joint Venture Agreement means the joint venture agreement entered into by Mountain Province Diamonds Inc., Camphor Ventures Inc., and De Beers Canada Exploration Inc. on October 24, 2002, but which took effect from January 1, 2002.

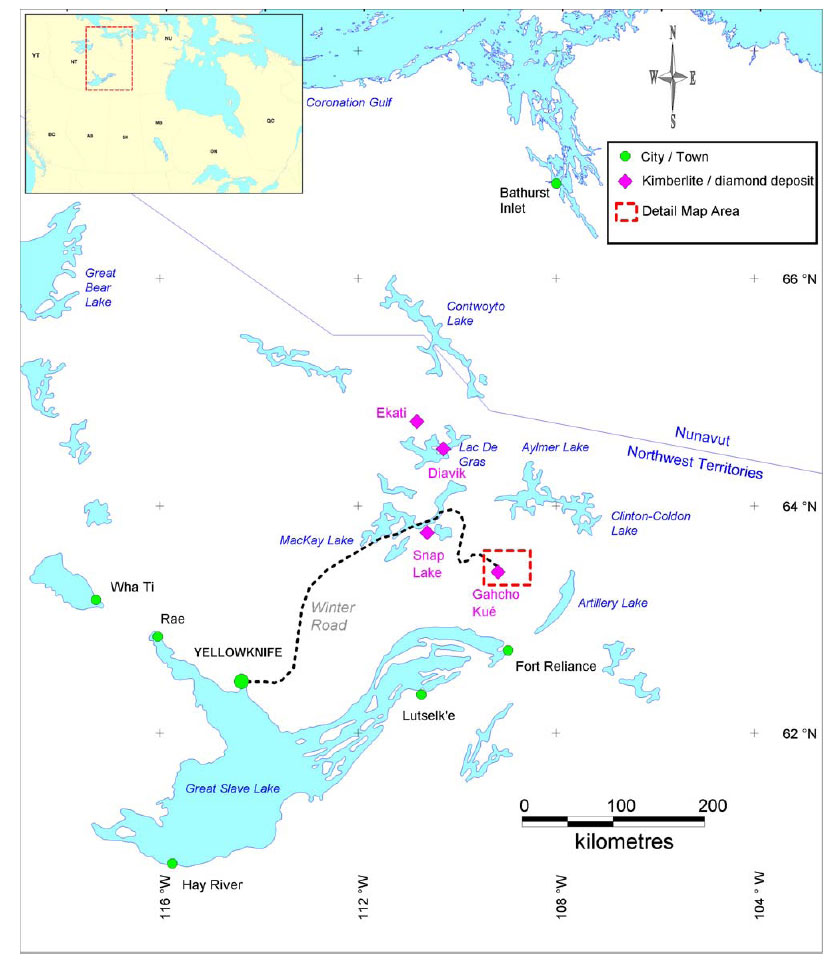

Gahcho Kué Project, located at Kennady Lake, is the aboriginal name for the Kennady Lake Project involving the diamondiferous kimberlite bodies in Kennady Lake located on the AK leased claims;

Glenmore means Glenmore Highlands Inc., a company incorporated under the Business Corporations Act(Alberta) and which, pursuant to the Arrangement, has amalgamated with the Company's wholly-owned subsidiary, Mountain Glen Mining Inc., to form an amalgamated company, also known as Mountain Glen Mining Inc.;

Glenmore Shares means the common shares of Glenmore, as the same existed before the Arrangement took effect and "Glenmore Share" means any of them;

Glenmore Shareholder means a holder of Glenmore Shares;

Joint Information Circular means the joint information circular of the Company and Glenmore dated May 10, 2000 for the Extraordinary General Meeting and Special Meeting of the Company and Glenmore respectively to approve the Arrangement;

Letter Agreement means the letter agreement dated March 6, 1997 among Mountain Province Mining Inc., Camphor Ventures Inc., Glenmore Highlands Inc., 444965 B.C. Ltd. and Monopros as amended or supplemented by: an agreement dated April 10, 1997 among Mountain Province Mining Inc., Camphor Ventures Inc., Glenmore Highlands Inc., 444965 B.C. Ltd. and Monopros, an assurance given to De Beers by the other parties., dated July, 1997, an agreement given to De Beers by the other parties dated November 1, 1997 and two agreements each dated December 17, 1999 among the parties.

Monopros or De Beers Canada means De Beers Canada Exploration Inc., formerly known as Monopros Limited, a wholly-owned subsidiary of De Beers;

Mountain Glen means Mountain Glen Mining Inc., a wholly-owned subsidiary (now dissolved) of the Company;

MPV, Company or Registrant means Mountain Province Diamonds Inc.;

MPV Shares means the common shares of MPV, and "MPV Share" means any of them;

Nasdaq means the National Association of Securities Dealers Automatic Quotation System;

Old MPV means MPV prior to its amalgamation with 444965 B.C. Ltd.;

OTCBB means the National Association of Securities Dealers over-the-counter bulletin board;

PFIC means Passive Foreign Investment Company under the Code;

Qualified Person as defined by Canadian National Instrument 43-101 (Standards of Disclosure for Mineral Projects), means an individual who

| (a) | is an engineer or geoscientist with a least five years experience in mineral exploration, mine development or operation or mineral project assessment, or any combination of these; |

| (b) | has experience relevant to the subject matter of the mineral project and the technical report; and |

| (c) | is a member in good standing of a professional association (as that term is defined in Canadian National Instrument 43-101); |

Registrant, Company or MPV means Mountain Province Diamonds Inc.;

Sight means an invitation to purchase a certain amount of rough diamonds ten times a year from the De Beers' Diamond Trading Company in London;

Sightholder means a diamantaire who purchases rough diamonds directly from the De Beers' Diamond Trading Company;

TSX means the Toronto Stock Exchange; and

VSE means the Vancouver Stock Exchange, subsequently renamed the Canadian Venture Exchange, and now known as the TSX Venture Exchange.

GLOSSARY OF TECHNICAL TERMS

Adit | A horizontal or nearly horizontal passage driven from the surface for the working of a mine. |

Archean | The earliest eon of geological history or the corresponding system of rocks. |

Area of Interest | A geographic area surrounding a specific mineral property in which more than one party has an interest and within which new acquisitions must be offered to the other party or which become subject automatically to the terms and conditions of the existing agreement between the parties. Typically, the area of interest is expressed in terms of a radius of a finite number of kilometers from each point on the outside boundary of the original mineral property. |

Bulk Sample | Evaluation program of a diamondiferous kimberlite pipe in which a large amount of kimberlite (at least 100 tonnes) is recovered from a pipe. |

Carat | A unit of weight for diamonds, pearls, and other gems. The metric carat, equal to 0.2 gram or 200 milligram, is standard in the principal diamond-producing countries of the world. |

Caustic Fusion | An analytical process for diamonds by which rocks are dissolved at temperatures between 450-600 C. Diamonds remain undissolved by this process and are recovered from the residue that remains. |

Craton | A stable relatively immobile area of the earth's crust that forms the nuclear mass of a continent or the central basin in an ocean. |

Diabase | A fine-grained rock of the composition of gabbro but with an ophitic texture. |

Dyke | A body of igneous rock, tabular in form, formed through the injection of magma. |

Feasibility Study | As defined by Canadian National Instrument 43-101, means a comprehensive study of a deposit in which all geological, engineering, operating, economic and other relevant factors are considered in sufficient detail that it could reasonably serve as the basis for a final decision by a financial institution to finance the development of the deposit for mineral production. |

Gneiss | A banded rock formed during high grade regional metamorphism. It includes a number of different rock types having different origins. It commonly has alternating bands of schistose and granulose material. |

Indicator mineral | Minerals such as garnet, ilmenite, chromite and chrome diopside, which are used in exploration to indicate the presence of kimberlites. |

Jurassic | The period of the Mesozoic era between the Triassic and the Cretaceous or the corresponding system of rocks marked by the presence of dinosaurs and the first appearance of birds. |

Kimberlite | A dark-colored intrusive biotite-peridotite igneous rock that can contain diamonds. It contains the diamonds known to occur in the rock matrix where they originally formed (more than 100 km deep in the earth). |

Macrodiamond | A diamond, two dimensions of which exceed 0.5 millimeters. |

Microdiamond | Generally refers to diamonds smaller than approximately 0.5mm, which are recovered from acid dissolution of kimberlite rock. |

Mineral Reserve | Means the economically mineable part of a Measured Mineral Resource or Indicated Mineral Resource demonstrated by at least a Preliminary Feasibility Study. This study must include adequate information on mining, processing, metallurgical, economic and other relevant factors that demonstrate, at the time of reporting, that economic extraction can be justified. A Mineral Reserve includes diluting materials and allowances for losses that may occur when the material is mined. |

| | THE TERMS "MINERAL RESERVE," "PROVEN MINERAL RESERVE" AND "PROBABLE MINERAL RESERVE" USED IN THIS REPORT ARE CANADIAN MINING TERMS AS DEFINED IN ACCORDANCE WITH NATIONAL INSTRUMENT 43-101 - STANDARDS OF DISCLOSURE FOR MINERAL PROJECTS WHICH INCORPORATES THE DEFINITIONS AND GUIDELINES SET OUT IN THE CANADIAN INSTITUTE OF MINING, METALLURGY AND PETROLEUM (THE "CIM") STANDARDS ON MINERAL RESOURCES AND MINERAL RESERVES DEFINITIONS AND GUIDELINES ADOPTED BY THE CIM COUNCIL ON AUGUST 20, 2000. IN THE UNITED STATES, A MINERAL RESERVE IS DEFINED AS A PART OF A MINERAL DEPOSIT WHICH COULD BE ECONOMICALLY AND LEGALLY EXTRACTED OR PRODUCED AT THE TIME THE MINERAL RESERVE DETERMINATION IS MADE. |

| Under United States standards: |

| "Reserve" means that part of a mineral deposit which can be economically and legally extracted or produced at the time of the reserve determination. |

| "Economically," as used in the definition of reserve, implies that profitable extraction or production has been established or analytically demonstrated to be viable and justifiable under reasonable investment and market assumptions. |

| "Legally," as used in the definition of reserve, does not imply that all permits needed for mining and processing have been obtained or that other legal issues have been completely resolved. However, for a reserve to exist, |

| there should be a reasonable certainty based on applicable laws and regulations that issuance of permits or resolution of legal issues can be accomplished in a timely manner. |

| Mineral Reserves are categorized as follows on the basis of the degree of confidence in the estimate of the quantity and grade of the deposit. |

| "Proven Mineral Reserve" means, in accordance with CIM Standards, the economically viable part of a Measured Mineral Resource demonstrated by at least a Preliminary Feasibility study. This Study must include adequate information on mining, processing, metallurgical, economic, and other relevant factors that demonstrate at the time of reporting, that economic extraction is justified. |

| The definition for "proven mineral reserves" under Canadian standards differs from the standards in the United States, where proven or measured reserves are defined as reserves for which (a) quantity is computed from dimensions revealed in outcrops, trenches, workings or drill holes; grade and/or quality are computed from the results of detailed sampling and (b) the sites for inspection, sampling and measurement are spaced so closely and the geographic character is so well defined that size, shape, depth and mineral content of reserves are well established. |

| "Probable Mineral Reserve" means, in accordance with CIM Standards, the economically mineable part of an Indicated, and in some circumstances a Measured Mineral Resource demonstrated by at least a Preliminary Feasibility Study. This Study must include adequate information on mining, processing, metallurgical, economic and other relevant factors that demonstrate, at the time of reporting, that economic extraction is justified. |

| The definition for "probable mineral reserves" under Canadian standards differs from the standards in the United States, where probable reserves are defined as reserves for which quantity and grade and/or quality are computed from information similar to that of proven reserves (under United States standards), but the sites for inspection, sampling, and measurement are further apart or are otherwise less adequately spaced. The degree of assurance, although lower than that for proven reserves, is high enough to assume continuity between points of observation. |

Mineral Resource | Under CIM Standards, Mineral Resource is a concentration or occurrence of natural, solid, inorganic or fossilized organic material in or on the Earth's crust in such form and quantity and of such a grade or quality that it has reasonable prospects for economic extraction. The location, quantity, grade, geological characteristics and continuity of a Mineral Resource are known, estimated or interpreted from specific geological evidence and knowledge. |

| | THE TERMS "MINERAL RESOURCE", "MEASURED MINERAL RESOURCE", "INDICATED MINERAL RESOURCE", "INFERRED MINERAL RESOURCE" USED IN THIS REPORT ARE CANADIAN MINING TERMS AS DEFINED IN ACCORDANCE WITH NATIONAL INSTRUMENT 43-101 - STANDARDS OF DISCLOSURE FOR MINERAL PROJECTS UNDER THE GUIDELINES SET OUT IN THE CIM STANDARDS. THE COMPANY ADVISES U.S. INVESTORS THAT WHILE SUCH TERMS ARE RECOGNIZED AND PERMITTED UNDER CANADIAN REGULATIONS, THE U.S. SECURITIES AND EXCHANGE COMMISSION DOES NOT RECOGNIZE THEM. THESE ARE NOT DEFINED TERMS UNDER THE UNITED STATES STANDARDS AND MAY NOT GENERALLY BE USED IN DOCUMENTS FILED WITH THE UNITED STATES SECURITIES AND EXCHANGE COMMISSION BY U.S. COMPANIES. AS SUCH, INFORMATION CONTAINED IN THIS REPORT CONCERNING DESCRIPTIONS OF MINERALIZATION AND RESOURCES MAY NOT BE COMPARABLE TO INFORMATION MADE PUBLIC BY U.S. COMPANIES SUBJECT TO THE REPORTING AND DISCLOSURE REQUIREMENTS OF THE UNITED STATES SECURITIES AND EXCHANGE COMMISSION. |

| "Inferred Mineral Resource" means, under CIM Standards, that part of a Mineral Resource for which quantity and grade or quality can be estimated on the basis of geological evidence and limited sampling and reasonably assumed, but not verified, geological and grade continuity. The estimate is based on limited information and sampling gathered through appropriate techniques from locations such as outcrops, trenches, pits, workings and drill holes. U.S. INVESTORS ARE CAUTIONED NOT TO ASSUME THAT ANY PART OR ALL OF AN INFERRED RESOURCE EXISTS, OR IS ECONOMICALLY OR LEGALLY MINEABLE. |

| "Indicated Mineral Resource" means, under CIM Standards, that part of a Mineral Resource for which quantity, grade or quality, densities, shape and physical characteristics, can be estimated with a level of confidence sufficient to allow the appropriate application of technical and economic parameters, to support mine planning and evaluation of the economic viability of the deposit. The estimate is based on detailed and reliable exploration and testing information gathered through appropriate techniques from locations such as outcrops, trenches, pits, workings and drill holes that are spaced closely enough for geological and grade continuity to be reasonably assumed. U.S. INVESTORS ARE CAUTIONED NOT TO ASSUME THAT ANY PART OR ALL OF THE MINERAL DEPOSITS IN THIS CATEGORY WILL EVER BE CONVERTED INTO RESERVES. |

| "Measured Mineral Resource" means, under CIM standards that part of a Mineral Resource for which quantity, grade or quality, densities, shape and physical characteristics are so well established that they can be estimated with confidence sufficient to allow the appropriate application of technical and economic parameters, to support production planning and evaluation of the economic viability of the deposit. The estimate is based on detailed and reliable exploration, sampling and testing information gathered through appropriate techniques from locations such as outcrops, trenches, pits, workings and drillholes that are spaced closely enough to confirm both geological and grade continuity. U.S. INVESTORS ARE CAUTIONED NOT TO ASSUME THAT ANY PART OR ALL OF THE MINERAL DEPOSITS IN THIS CATEGORY WILL EVER BE CONVERTED INTO RESERVES. |

Operator | The party in a joint venture which carries out the operations of the joint venture subject at all times to the direction and control of the management committee. |

Ordovician | The period between the Cambrian and the Silurian or the corresponding system of rocks. |

Overburden | A general term for any material covering or obscuring rocks from view. |

Paleozoic | An era of geological history that extends from the beginning of the Cambrian to the close of the Permian and is marked by the culmination of nearly all classes of invertebrates except the insects and in the later epochs by the appearance of terrestrial plants, amphibians, and reptiles. |

Pipe | A kimberlite deposit that is usually, but not necessarily, carrot-shaped. |

Preliminary Feasibility Study | Under the CIM Standards, means a comprehensive study of the viability of a mineral project that has advanced to a stage where the mining method, in the case of underground mining, or the pit configuration, in the case of an open pit, has been established, and which, if an effective method of mineral processing has been determined, includes a financial analysis based on reasonable assumptions of technical, engineering, operating, economic factors and the evaluation of other relevant factors which are sufficient for a Qualified Person acting reasonably, to determine if all or part of the Mineral Resource may be classified as a Mineral Reserve. |

Proterozoic | The eon of geologic time or the corresponding system of rocks that includes the interval between the Archean and Phanerozoic eons, perhaps exceeds in length all of subsequent geological time, and is marked by rocks that contain fossils indicating the first appearance of eukaryotic organisms (as algae). |

Reverse Circulation Drill | A rotary percussion drill in which the drilling mud and cuttings return to the surface through the drill pipe. |

Sill | Tabular intrusion which is sandwiched between layers in the host rock. |

Stringers | The narrow veins or veinlets, often parallel to each other, and often found in a shear zone. |

Tertiary | The Tertiary period or system of rocks. |

Till Sample | A sample of soil taken as part of a regional exploration program and examined for indicator minerals. |

Xenolith | A foreign inclusion in an igneous rock. |

NOTE REGARDING FORWARD LOOKING STATEMENTS

This report contains forward-looking statements within the meaning of the United States Private Securities Litigation Reform Act of 1995 concerning the Company's exploration, operations, planned acquisitions and other matters. These statements relate to analyses and other information that are based on forecasts of future results, estimates of amounts not yet determinable and assumptions of management.

Statements concerning mineral resource estimates may also be deemed to constitute forward-looking statements to the extent that they involve estimates of the mineralization that will be encountered if the property is developed, and based on certain assumptions that the mineral deposit can be economically exploited. Any statements that express or involve discussions with respect to predictions, expectations, beliefs, plans, projections, objectives, assumptions or future events or performance (often, but not always, using words or phrases such as "expects" or "does not expect", "is expected", "anticipates" or "does not anticipate", "plans", "estimates" or "intends", or stating that certain actions, events or results "may", "could", "would", "might" or "will" be taken, occur or be achieved) are not statements of historical fact and may be "forward-looking statements." Forward-looking statements are subject to a variety of risks and uncertainties which could cause actual events or results to differ from those reflected in the forward-looking statements, including, without limitation:

| • | risks and uncertainties relating to the interpretation of drill results, the geology, grade and continuity of mineral deposits; |

| • | results of initial feasibility, pre-feasibility and feasibility studies, and the possibility that future exploration, development or mining results will not be consistent with the Company's expectations; |

| • | mining exploration risks, including risks related to accidents, equipment breakdowns or other unanticipated difficulties with or interruptions in production; |

| • | the potential for delays in exploration activities or the completion of feasibility studies; |

| • | risks related to the inherent uncertainty of exploration and cost estimates and the potential for unexpected costs and expenses; |

| • | risks related to commodity price fluctuations; |

| • | the uncertainty of profitability based upon the Company's history of losses; |

| • | risks related to failure to obtain adequate financing on a timely basis and on acceptable terms; |

| • | risks related to environmental regulation and liability; |

| • | political and regulatory risks associated with mining and exploration; and |

| • | other risks and uncertainties related to the Company's prospects, properties and business strategy. |

Some of the important risks and uncertainties that could affect forward looking statements are described further in this Annual Report under the headings "Risk Factors", "History and Development of Company," "Business Overview," "Property, plants and equipment," and "Operating and Financial Review and Prospects". Should one or more of these risks and uncertainties materialize, or should underlying assumptions prove incorrect, actual results may vary materially from those described in forward-looking statements. Forward looking statements are made based on management's beliefs, estimates and opinions on the date the statements are made and the Company undertakes no obligation to update forward-looking statements if these beliefs, estimates and opinions or other circumstances should change. Investors are cautioned against attributing undue certainty to forward-looking statements.

NOTE REGARDING FINANCIAL STATEMENTS AND EXHIBITS

The financial statements and exhibits referred to herein are filed with this report on Form 20-F in the United States. This report is also filed in Canada as an Annual Information Form and the Canadian filing does not include the financial statements and exhibits listed herein. Canadian investors should refer to the annual financial statements of the Company as at March 31, 2007, which are incorporated by reference herewith, as filed with the applicable Canadian Securities regulators on SEDAR (the Canadian Securities Administrators' System for Electronic Document Analysis and Retrieval) under "Audited Annual Financial Statements - English".

METRIC EQUIVALENTS

For ease of reference, the following factors for converting metric measurements into imperial equivalents are provided:

To Convert From Metric | To Imperial | Multiply by |

| Hectares | Acres | 2.471 |

| Metres | Feet (ft.) | 3.281 |

| Kilometres (km.) | Miles | 0.621 |

| Tonnes | Tons (2000 pounds) | 1.102 |

| Grams/tonne | Ounces (troy/ton) | 0.029 |

PART I

Item 1. Identity of Directors, Senior Management and Advisors

Not Applicable

Item 2. Offer Statistics and Expected Timetable

Not Applicable

Item 3. Key Information

| A. | Selected financial data. |

The selected financial data set forth below should be read in conjunction with “Item 5 - Operating and Financial Review and Prospects”, and in conjunction with the consolidated financial statements and related notes of the Company included under “Item 17, Financial Statements." The Company's consolidated financial statements have been prepared in accordance with Canadian generally accepted accounting principles. Material measurement differences between accounting principles generally accepted in Canada and the United States, applicable to the Company, are described in Note 11 to the consolidated financial statements. The Company's financial statements are set forth in Canadian dollars.

The following chart summarizes certain selected financial information for the Company as at and for its fiscal years ended March 31, 2007, 2006, 2005, 2004 and 2003. Except as otherwise indicated, dollar amounts presented are equivalent under Canadian and United States generally accepted accounting principles.

| | | | |

| | | 12 Months Ended March 31, | |

All in CDN$1,000's except Earnings (loss) per Share | | | | | | | | | | | | | | | |

and Number of Common Shares | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | |

| | | (1,961 | ) | | | (2,200 | ) | | | | | | | (1,813 | ) | | | (1,713 | ) |

Under U.S. GAAP: (restated) | | | (1,868 | ) | | | (1,948 | ) | | | | | | | (1,223 | ) | | | (14,513 | ) |

Basic and diluted earnings (loss) per share - | | | | | | | | | | | | | | | | | | | | |

| | | (0.04 | ) | | | (0.04 | ) | | | | | | | (0.04 | ) | | | (0.03 | ) |

Under U.S. GAAP: (restated) | | | (0.03 | ) | | | (0.04 | ) | | | | | | | (0.02 | ) | | | (0.29 | ) |

| | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | |

Under U.S. GAAP (restated) | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | |

Under U.S. GAAP (restated) | | | | | | | | | | | | | | | | | | | | |

Number of Common Shares issued | | | | | | | | | | | | | | | | | | | | |

less shares owned by subsidiary | | | | | | | | | | | | | | | | | | | (16,015,696 | ) |

| | | | | | | | | | | | | | �� | | | | | | | |

*The 16,015,696 shares held by Mountain Glen, were cancelled and returned to treasury on March 30, 2004.

Restated figures include 2006 and prior years’ amounts under U.S. GAAP for the following: Net Earnings (loss) for 2003, 2004 and 2005; Basic and diluted earnings (loss) per share for 2003, 2004, 2005 and 2006; Total Assets under U.S. GAAP for 2003, 2004, 2005, and 2006; and Net Assets under U.S. GAAP for 2003, 2004, 2005, and 2006. These restatements are as a result of an accounting error for U.S. GAAP purposes. Please see the audited consolidated financial statements of the Company for the year ended March 31, 2007 for more information.

No dividends have been declared in any of the years presented above.

Currency and Exchange Rates

All dollar amounts set forth in this report are in Canadian dollars, except where otherwise indicated. The following tables set forth, for the five most recent financial years, (i) the average rate (the "Average Rate") of exchange for the Canadian dollar, expressed in U.S. dollars, calculated by using the average of the exchange rates on the last day for which data is available for each month during such periods; and (ii) the high and low exchange rate during the previous six months, in each case based on the noon buying rate in New York City for cable transfers in Canadian dollars as certified for customs purposes by the Federal Reserve Bank of New York.

The Average Rate is set out for each of the periods indicated in the table below.

The high and low exchange rates for each month during the previous six months are as follows:

On June 28, 2007, the noon buying rate in New York City for cable transfer in Canadian dollars as certified for customer purposes by the Federal Reserve Bank of New York (the "Exchange Rate") was $1 Canadian = US$0.9411.

| B. | Capitalization and indebtedness. |

Not Applicable

| C. | Reasons for the offer and use of proceeds. |

Not Applicable

Risks of Exploration and Development

The Company, and thus the securities of the Company, should be considered a highly speculative investment and investors should carefully consider all of the information disclosed in this Annual Report prior to making an investment in the Company. In addition to the other information presented in this Annual Report, the following risk factors should be given special consideration when evaluating an investment in any of the Company's securities.

| (a) | The Company's limited operating history makes it difficult to evaluate the Company's current business and forecast future results. |

The Company has only a limited operating history on which to base an evaluation of the Company's current business and prospects, each of which should be considered in light of the risks, expenses and problems frequently encountered in the early stages of development of all companies. This limited operating history leads the Company to believe that period-to-period comparisons of its operating results may not be meaningful and that the results for any particular period should not be relied upon as an indication of future performance.

(b) Speculative business

Resource exploration and development is a speculative business, characterized by a number of significant risks including, among other things, unprofitable efforts resulting not only from the failure to discover mineral deposits but from finding mineral deposits which, though present, are insufficient in quantity and quality to return a profit from production. Diamonds acquired or discovered by the Company may be required to be sold to The Diamond Trading Co., a wholly-owned subsidiary of De Beers, as per the Gahcho Kué Joint Venture Agreement (see “Item 4D - Property, plant and equipment - Principal Properties - The AK Property”), at a price which is reflective of the market at that time.

(c) The Company has no significant source of operating cash flow and failure to generate revenues in the future could cause the Company to go out of business.

The Company currently has no significant source of operating cash flow. The Company has limited financial resources. The Company's ability to achieve and maintain profitability and positive cash flow is dependent upon the Company's ability to generate revenues.

(d) Exploration and Development

The Company's properties are primarily in the advanced exploration and permitting stage. Drilling of the 5034 and Hearne kimberlite pipes has been extensive, however, a limited amount of drilling has been conducted at the Tuzo and Telsa kimberlite pipes. There are no estimates of reserves. Estimates of mineral deposits, development plans and production costs, when made, can be affected by such factors as environmental permit regulations and requirements, weather, environmental factors, unforeseen technical difficulties, unusual or unexpected geological formations and work interruptions. In addition, the grade of diamonds ultimately discovered may differ from that indicated by bulk sampling results. Mine plans and processing concepts developed under the scoping and pre-feasibility studies are preliminary in nature. The estimated capital and operating costs developed under scoping and pre-feasibility studies are also preliminary in nature. Historically, pre-feasibility studies have tended to underestimate capital and operating costs.

(e) Process Testing

Process testing is limited to small scale testing based on a number of laboratory test programs, trade-off studies and design evaluations conducted in 2002 and 2004. Ore dressing study technical investigations were performed on kimberlite from the 5034 and Hearne pipes. A database of operating information developed during the 1999/2000 bulk sample processing of 2,000 tonnes of kimberlite was used to supplement the ore dressing study data. Limited processing data is available for the Tuzo and Telsa kimberlites. Process plant studies were conducted during the course of 2005. There can be no assurance that diamonds recovered in small scale tests will be duplicated in large scale tests under on-site conditions or in production scale. Difficulties may be experienced in obtaining the expected diamond recoveries when scaling up to a production scale process plant.

(f) Project Funding

De Beers Canada is now paying for all exploration of the AK Property, and can be called on to pay all development costs of the AK Property and, with regard to that property, there is currently no risk to the Company in respect of the further exploration, permitting and development costs. Any separate and additional exploration done by the Company on its other properties may not result in discovery of any diamondiferous kimberlite.

(g) History of Losses or Earnings

The Company has a history of losses and may continue to incur losses for the foreseeable future. During the years ended March 31, 2007, 2006 and 2005, the Company incurred net losses or earnings during each of the following periods:

| • | $1.961 million net loss for the year ended March 31, 2007. |

| • | $2.200 million net loss for the year ended March 31, 2006. |

| • | $1.531 million net earnings for the year ended March 31, 2005 (relating primarily to gain on sale of the Haveri project to Northern Lion Gold Corp.). |

As of March 31, 2007, the Company had an accumulated deficit of $26.1 million. There can be no assurance that the Company will ever be profitable.

None of the Company's properties have advanced to the commercial production stage, and the Company has no history of earnings or cash flow from operations and, as an exploration company, has only a history of losses. The Company has paid no dividends on its shares since incorporation and does not anticipate doing so in the foreseeable future.

(h) Recoverability of capitalized mineral property costs

The recoverability of the amounts capitalized for mineral properties in the Company's consolidated financial statements, prepared in accordance with Canadian generally accepted accounting principles, is dependent upon the ability of the Company to complete exploration and development, the discovery of economically recoverable reserves, and, if warranted, upon future profitable production or proceeds from disposition of some or all of the Company's mineral properties.

(i) Additional Funding Requirements

As of March 31, 2007, the Company had cash and cash equivalents of approximately $0.180 million and working capital of approximately $0.180 million. During the past three fiscal years ended March 31, 2007, the Company has used approximately $2.563 million in cash flows in operating activities including approximately $0.978 million during the fiscal year ended March 31, 2007, $0.727 million during the fiscal year ended March 31, 2006 and $0.858 million during the fiscal year ended March 31, 2005.

The Company's administrative and other expenses are expected to be approximately $1.0 million for the next year. The Company does not have sufficient working capital for administrative purposes for the next year, but intends to raise capital to finance its operations for the next two years or more through either the sale or partial sale of its investment in Northern Lion, and/or through the private placement of shares. The Company also has access to cash and other liquid investments held by Camphor. The Company may be required to raise additional capital through equity and/or debt financings on terms that may be dilutive to its shareholders' interests in the Company and to the value of their common shares. The Company may consider debt financing, joint ventures, production sharing arrangements, disposing of properties or other arrangements to meet its capital requirements in the future. Such arrangements may have a material adverse affect on the Company's business or results of operations.

(j) No Proven Reserves

The properties in which the Company has an interest are all in the advanced exploratory and permitting stage and at this point, there are only indicated and inferred resources in four kimberlite bodies in Kennady Lake. See “Item 4D - Property, plants and equipment - Principal Properties”. The Company has not yet determined whether its mineral properties contain mineral reserves that are economically recoverable. Failure to discover economically recoverable reserves will require the Company to write-off costs capitalized in its financial statements.

(k) Title Matters

While the Company has investigated title to all of its mineral properties and, to the best of its knowledge, title to all of its properties and properties in which it has the right to acquire or earn an interest are in good standing, this should not be construed as a guarantee of title. The properties may be subject to prior unregistered agreements or transfers and title may be affected by undetected defects.

(l) Diamond Prices

The market for rough diamonds is subject to strong influence from the world's largest diamond producing company, De Beers, of South Africa, and from The Diamond Trading Co., (formerly known as the Central Selling Organization), a marketing agency controlled by De Beers. The price of diamonds dropped sharply after September 11, 2001 and has now recovered, but future prices cannot be predicted. Over the past three years, diamond prices have increased on average by approximately 15%. Current trends suggest an over demand for rough diamonds in the near to mid-term.

(m) Compliance with Environmental and Government Regulation

The current and anticipated future operations of the Company, including development activities and commencement of production on its properties, require permits from various federal, territorial and local governmental authorities and such operations are and will be governed by laws and regulations governing prospecting, development, mining, production, exports, taxes, labour standards, occupational health, waste disposal, toxic substances, land use, environmental protection, mine safety and other matters. Companies engaged in the development and operation of mines and related facilities generally experience increased costs, and delays in production and other schedules as a result of the need to comply with applicable laws, regulations and permits. The Company's exploration activities and its potential mining and processing operations in Canada are subject to various Canadian Federal and Territorial laws governing land use, the protection of the environment, prospecting, development, production, exports, taxes, labour standards, occupational health, waste disposal, toxic substances, mine safety and other matters.

Such operations and exploration activities are also subject to substantial regulation under these laws by governmental agencies and may require that the Company obtain permits from various governmental agencies. The Company believes it is in substantial compliance with all material laws and regulations which currently apply to its activities. There can be no assurance, however, that all permits which the Company may require for construction of mining facilities and conduct of mining operations will be obtainable on reasonable terms or that such laws and regulations, or that new legislation or modifications to existing legislation, would not have an adverse effect on any exploration or mining project which the Company might undertake.

Further detail on governmental regulation may be found in Item 4 - Business Review - Government Regulation, below.

Failure to comply with applicable laws, regulations and permit requirements may result in enforcement actions thereunder, including orders issued by regulatory or judicial authorities causing operations to cease or be curtailed, and may include corrective measures requiring capital expenditures, installation of additional equipment or remedial actions. Parties engaged in mining operations may be required to compensate those suffering loss or damage by reason of the mining activities and may have civil or criminal fines or penalties imposed for violation of applicable laws or regulations. The amount of funds required to comply with all environmental regulations and to pay for compensation in the event of a breach of such laws may exceed the Company's ability to pay such amount.

Amendments to current laws, regulations and permits governing operations and activities of mining companies, or more stringent implementation thereof, could have a material adverse impact on the Company and cause increases in capital expenditures or production costs or reduction in levels of production at producing properties or require abandonment or delays in development of new mining properties.

(n) Climate and Transportation

The AK Property is subject to climate and transportation risks because of its remote northern location. Such factors can add to the cost of exploration, development and operation, thereby affecting costs and profitability.

(o) Joint Venture Partner

The Company, and the success of the AK Property, is dependent on the efforts, expertise and capital resources of joint venture partner De Beers Canada and its parent De Beers. De Beers Canada is the project operator and is responsible for exploring, permitting, developing and operating the AK Property. The Company is dependent on De Beers Canada for accurate information about the AK Property and the proper and timely progress of exploration, permitting and development. De Beers Canada and the Company agreed on March 8, 2000 that it was unlikely that the agreed upon rate of return would be achieved from mining the 5034, Hearne and Tuzo pipes using the conventional open pit method. As a result, the Company and De Beers Canada agreed that De Beers would conduct a desktop study examining the costs of both open-pit and underground mining scenarios.

The results of the desktop study were presented on August 4, 2000 to the board of directors of the Company. The study showed that the modeled rate of return for the mining of the three main diamond pipes was below the agreed upon rate of return needed to proceed to the next phase, but sufficiently close to only require an increase in diamond revenues of approximately 15% to achieve the agreed upon rate. A management committee was constituted and it was decided that the best options to advance the project were an additional bulk sample and additional exploration. The bulk sample was completed in May 2001 and the exploration in June 2001. The final results were reported on December 18, 2001 and were encouraging enough for De Beers to commit to another bulk sample in the winter of 2002. The results of the 2002 bulk sample program of the Hearne and 5034 pipes were reported in April 2003 and the results of the updated desk top study two weeks later. Even though the study showed that estimated capital costs had increased only slightly and that the estimated operating costs had dropped significantly, the effect of lower diamond values (especially for the Hearne pipe) and a lower US dollar against the Canadian dollar since the 2000 desktop study, had resulted in an internal rate of return (IRR), which was well below the agreed hurdle rate. Combined with the then current geo-political environment and uncertainties, De Beers decided to postpone a pre-feasibility decision until the following year when the desktop study would be updated again. In the meantime, De Beers would continue with exploration in the Kelvin-Faraday area with an objective of adding to the existing resource.

However, at the end of July 2003, De Beers notified the Company that they had started work on a detailed cost estimate of a pre-feasibility study of the Gahcho Kué Project. They based their decision on the improving geo-political and economic conditions which supported confidence in longer-term diamond price projections. In November 2003, the Joint Venture approved a budget of approximately $25 million for a pre-feasibility study, which started in January 2004. The first phase of the study was completed in June 2004.

The pre-feasibility study was completed in mid-2005. The projected profitability levels were sufficiently encouraging to support the Joint Venture’s decision to proceed to the next phase of permitting and advanced exploration to improve the resource confidence and input data for mine design to support a definitive feasibility study. On July 11, 2005, De Beers reported an increase in the modeled value of the diamonds for the Gahcho Kué project with the modeled values increasing by approximately 6, 7 and 8 percent for the Tuzo, Hearne and 5034 pipes respectively.

The table below summarizes the 2005 Gahcho Kué Resource Statement.

Cautionary Note to U.S. Investors concerning estimates of Indicated and Inferred Resources. This section uses the terms "indicated" and "inferred resources." We advise U.S. investors that while those terms are recognized and required by Canadian regulations, the U.S. Securities and Exchange Commission does not recognize them. "Inferred resources" have a great amount of uncertainty as to their existence, and great uncertainty as to their economic and legal feasibility. It cannot be assumed that all or any part of an Inferred Mineral Resource will ever be upgraded to a higher category. Under Canadian rules, estimates of Inferred Mineral Resources may not form the basis of feasibility or pre-feasibility studies, except in rare cases.

U.S. investors are cautioned not to assume that any part or all of mineral deposits in these categories will ever be converted into reserves.

U.S. investors are cautioned not to assume that part or all of an inferred resource exists, or is economically or legally minable.

2005 GAHCHO KUÉ RESOURCE STATEMENT

Pipe Resource | Category | Tonnes | Carats | Grade (cpht)(1) |

| 5034 | Indicated Inferred | 8,715,000 4,921,000 | 13,943,000 8,366,000 | 160 170 |

| Hearne | Indicated Inferred | 5,678,000 1,546,000 | 9,676,000 2,373,000 | 170 153 |

| Tuzo | Inferred | 10,550,000 | 12,152,000 | 115 |

| Summary | Indicated Inferred | 14,392,000 17,017,000 | 23,619,000 22,890,000 | 164 135 |

(1) Resource cutoff is 1.5 mm

On July 25, 2005, the Joint Venture announced the Joint Venture Management Committee had approved a budget of $38.5 million for the environmental assessment and permitting process and for an advanced exploration program. On November 29, 2005, it was announced that the Joint Venture had submitted an application with the Mackenzie Valley Land and Water Board for permits required to construct and operate a diamond mine at Gahcho Kué. The permit applications were submitted to the Mackenzie Valley Environmental Impact Review Board for an Environmental Assessment (EA). The Review Board ordered the Gahcho Kué application to an Environmental Impact Review (EIR) in June 2006. Out of concern that the Review Board may have exceeded its authority in referring the Gahcho Kué application to EIR prior to conclusive completion of the EA, De Beers took the Review Board’s decision to judicial review in the Supreme Court on the Northwest Territories. On April 2, 2007 the Supreme Court ruled that the Review Board had acted within its authority and upheld the decision to refer the application to EIR.

On January 12, 2006, the Joint Venture announced details of the advanced exploration program which commenced in February 2006 and was projected to be completed by May 2006. Inadequacies on the part of the casing drill contractor resulted in the failure of the 2006 bulk sampling programs at Tuzo and the 5034 North Lobe. The 2006 core drilling program was successful and laid the groundwork for an extended core drilling program at Tuzo during the summer of 2006. The 2006 core drilling program confirmed the presence of flaring of the Tuzo kimberlite to depth. The program also confirmed the presence of kimberlite between the 5034 South Lobe and the Wallace Anomaly and also between the 5034 South Lobe and the 5034 West Lobe.

On December 19, 2006, the Joint Venture announced the details of a $30 million 2007 work program designed to conduct extensive core drilling over the Tuzo kimberlite pipe; complete a review of the 2005 pre-feasibility study; and advance the permitting for the Gahcho Kue project.

(p) Operating Hazards and Risks

Diamond exploration involves many risks which even a combination of experience, knowledge and careful evaluation may not be able to overcome. Operations in which the Company has a direct or indirect interest will be subject to all the hazards and risks normally incidental to exploration, development and production of resources, any of which could result in work stoppages, damage to property and possible environmental damage. The Company maintains insurance policies relating to directors and officers liability, but can give no guarantees that such insurance will be sufficient to protect the Company from losses.

(q) Numerous factors beyond the control of the Company affect the marketability of any diamonds discovered.

Factors beyond the control of the Company may affect the marketability of any diamonds produced. Significant price movements over short periods of time may be affected by numerous factors beyond the control of the Company, including international economic and political trends, expectations of inflation, currency exchange fluctuations (specifically, the U.S. dollar relative to the Canadian dollar and other currencies), interest rates and global or regional consumption patterns. The effect of these factors on the prices of diamonds and therefore the economic viability of any of the Company's projects cannot accurately be predicted.

(r) The Company's expectations reflected in forward looking statements may prove to be incorrect.

This Form 20-F includes "forward looking statements" A shareholder or prospective shareholder should bear this in mind when assessing the Company's business. All statements, other than statements of historical facts, included in this annual report, including, without limitation, the statements under and located elsewhere herein regarding industry prospects and the Company's financial position are forward-looking statements. Although the Company believes that the expectations reflected in such forward looking statements are reasonable, such expectations may prove to be incorrect.

(s) Competition

The resource industry is intensely competitive in all of its phases, and the Company competes with many companies possessing greater financial resources and technical facilities. Competition could adversely affect the Company's ability to acquire suitable producing properties or prospects for exploration in the future. The Company may be required under the Gahcho Kué Joint Venture Agreement (see “Item 4B - Information on the Company - Business Overview”) to sell its rough diamonds at a price that is reflective of the market price, to The Diamond Trading Co., a wholly-owned subsidiary of De Beers, which controls approximately 50% of the diamond market. There may therefore be no competition for diamonds produced from the Company's properties. The Company only competes in the acquisition of new properties.

(t) Financing Risks

The Company's current operations do not generate any cash flow. If the Company seeks additional equity financing, the issuance of additional shares will dilute the interests of the Company's current shareholders. The amount of the dilution would depend on the number of new shares issued and the price at which they are issued. The Company has successfully raised funds in recent years through share, option and warrant issuances. As at June 22, 2007, the Company had approximately $0.3 million in cash, including cash that it can access through its subsidiary, Camphor, and the Company intends to raise capital to finance its operations for the next two years or more through either the sale or partial sale of its investment in Northern Lion, and/or through the private placement of shares.

(u) Dilution from Outstanding Securities

As at June 28, 2007, there were 608,850 options at exercise prices ranging from $0.56 to $4.50 (expiring at various dates), and no warrants outstanding. Of these, 198,850 options were issued in exchange for stock options of Camphor Ventures tendered to complete the acquisition of Camphor. The stock options, if fully exercised, would increase the number of shares outstanding by 608,850. Such options, if fully exercised, would constitute approximately 1% (out of 60,332,381 shares (59,723,531 issued and outstanding, plus total options) respectively) of the Company's resulting share capital as at June 28, 2007. It is unlikely that options would be exercised unless the market price of the Company's common shares exceeds the exercise price at the date of exercise. The exercise of such options and the subsequent resale of such Common shares in the public market could adversely affect the prevailing market price and the Company's ability to raise equity capital in the future at a time and price which it deems appropriate. The Company may also enter into commitments in the future which would require the issuance of additional common shares and the Company may grant new share purchase warrants and stock options. Any share issuances from the Company's treasury will result in immediate dilution to existing shareholders.

(v) Conflicts of Interest

At the present time, except to the extent that Patrick Evans and Jennifer Dawson have Consulting Agreements with the Company (see “Item 6C - Board Practices”), none of the officers and directors are in a position of conflict of interest. However, certain officers and directors of the Company are associated with other natural resource companies that acquire interests in mineral properties. Such associations may give rise to conflicts of interest from time to time.

The directors of the Company are required by law to act honestly and in good faith with a view to the best interest of the Company and to disclose any interest which they may have in any project or opportunity of the Company. If a conflict of interest arises at a meeting of the board of directors, any director in a conflict is required to disclose his interest and abstain from voting on such matter. In determining whether or not the Company will participate in any project or opportunity, the director will primarily consider the degree of risk to which the Company may be exposed and its financial position at that time.

(w) Dependence on Key Management Employees

The nature of the Company's business, its ability to continue its exploration and development activities and to thereby develop a competitive edge in its marketplace depends, in large part, on its ability to attract and maintain qualified key management personnel. Competition for such personnel is intense, and there can be no assurance that the Company will be able to attract and retain such personnel. The Company's development to date has depended, and in the future will continue to depend, on the efforts of Patrick Evans. See “Item 7B -Related party transactions”, “Item 6C - Board Practices”, and “Item 10C- Material Contracts”. Loss of the key person could have a material adverse effect on the Company. The Company does not maintain key-man life insurance on Patrick Evans.

(x) Fluctuations in Company Stock Prices

Prices for the Company's shares on the TSX and on the Amex, have been extremely volatile. The price for the Company's common shares on the TSX ranged from $3.05 (low) and $5.05 (high) during the fiscal year ended March 31, 2007, and from $2.15 (low) to $4.96 (high) during the fiscal year ended March 31, 2006. The price on the Amex ranged from $2.70 US (low) and $4.40 US (high) during the fiscal year ended March 31, 2007, and from $1.70 US (low) to $4.26 US (high) during the fiscal year ended March 31, 2006. Any investment in the Company's securities is therefore subject to considerable fluctuations in value.

(w) Currency Rate Fluctuations

Feasibility and other studies conducted to evaluate the Company's properties are denominated in U.S. dollars, and the Company conducts a significant portion of its operations and incurs a significant portion of its administrative and operating costs in Canadian dollars. The exchange rate for converting U.S. dollars into Canadian dollars has fluctuated in recent years. Accordingly, the Company is subject to fluctuations in the rates of currency exchange between the U.S. dollar and the Canadian dollar, and these fluctuations in the rates of currency exchange may materially affect the Company's financial position, results of operations and timing of the development of its properties.

(y) The Mineral resources industry is intensely competitive and the Company competes with many companies that have greater financial means and technical facilities.

The mineral resources industry is intensely competitive and the Company competes with many companies that have greater financial means and technical facilities. Significant competition exists for the limited number of mineral acquisition opportunities available. As a result of this competition, the Company's ability to acquire additional attractive mining properties, should it decide to do so in the future, on terms it considers acceptable, may be adversely affected.

(z) De Beers Support

The exploration of the AK Property has been primarily funded by De Beers, and De Beers Canada has made an equity investment in the Company. However, there is no assurance that the level of support provided by De Beers will continue in the future.

General

As the Company is a Canadian company, it may be difficult for U.S. shareholders of the Company to effect service of process on the Company or to realize on judgments obtained against the Company in the United States. Some of its directors and officers are residents of Canada and a significant part of its assets are, or will be, located outside of the United States. As a result, it may be difficult for shareholders resident in the United States to effect service of process within the United States upon the Company, directors, officers or experts who are not residents of the United States, or to realize in the United States judgments of courts of the United States predicated upon civil liability of any of the Company, directors or officers under the United States federal securities laws. If a judgment is obtained in the U.S. courts based on civil liability provisions of the U.S. federal securities laws against the Company or its directors or officers it will be difficult to enforce the judgment in the Canadian courts against the Company and any of the Company's non-U.S. resident executive officers or directors. Accordingly, United States shareholders may be forced to bring actions against the Company and its respective directors and officers under Canadian law and in Canadian courts in order to enforce any claims that they may have against the Company or its directors and officers. Subject to necessary registration, as an extra provincial company, under applicable provincial corporate statutes in the case of a corporate shareholder, Canadian courts do not restrict the ability of non-resident persons to sue in their courts. Nevertheless it may be difficult for United States shareholders to bring an original action in the Canadian courts to enforce liabilities based on the U.S. federal securities laws against the Company and any of the Company's Canadian executive officers or directors.

Item 4. Information on the Company

| A. | History and development of the company. |

The Corporate Organization

Mountain Province Diamonds Inc., formerly Mountain Province Mining Inc., was formed on November 1, 1997 by the amalgamation (the "MPV Amalgamation") of Mountain Province Mining Inc. ("Old MPV") and 444965 B.C. Ltd. ("444965") pursuant to an amalgamation agreement (the "MPV Amalgamation Agreement") dated as of August 21, 1997.

Under the terms of the MPV Amalgamation Agreement, as at November 1, 1997, each Old MPV share was exchanged for one MPV Share and each 444965 share was exchanged for approximately 0.80 of one MPV Share. The conversion ratios reflect the respective interests of Old MPV and 444965 in the AK-CJ Properties prior to the date of the MPV Amalgamation.

Old MPV was incorporated under the laws of British Columbia on December 2, 1986 under the British Columbia Company Act (the "Old Act") and was engaged in the exploration of precious and base mineral resource properties until the date of the MPV Amalgamation. Prior to the date of the MPV Amalgamation, Old MPV held an undivided 50% interest in the AK-CJ Properties and an interest in each of the other properties which are currently held by MPV, as described below.

444965, a wholly-owned subsidiary of Glenmore Highlands Inc., (Glenmore being a former controlling shareholder of the Company as defined under the Securities Act, British Columbia) prior to the MPV Amalgamation, was incorporated under the laws of British Columbia on August 20, 1993. Prior to the MPV Amalgamation, 444965's only material asset consisted of a 40% undivided interest in the AK-CJ Properties.

As of March 31, 2000, the Company had one wholly-owned subsidiary, Mountain Province Mining Corp. (USA), which has since been voluntarily dissolved.

On April 4, 2000, the Company incorporated a wholly-owned subsidiary, Mountain Glen Mining Inc. in Alberta. Pursuant to an arrangement agreement (the "Arrangement Agreement") with Glenmore dated May 10, 2000, Glenmore was amalgamated with Mountain Glen effective as of June 30, 2000 to form a wholly-owned subsidiary (also known as "Mountain Glen Mining Inc.") of the Company. All Glenmore Shares were exchanged for common shares in the Company on the basis of 0.5734401 MPV Shares to one Glenmore Share, and Glenmore Shares were concurrently cancelled. All of the assets of Glenmore became assets of Mountain Glen, including 16,015,696 MPV Shares previously held by Glenmore.

Glenmore had two wholly-owned subsidiaries, Baltic Minerals BV, incorporated in the Netherlands, and Baltic Minerals Finland OY, incorporated in Finland. Pursuant to the Arrangement Agreement, these companies became wholly-owned subsidiaries of the Company.

The Company changed its name from Mountain Province Mining Inc. to Mountain Province Diamonds Inc. effective October 16, 2000. It commenced trading under its new name on the TSX on October 25, 2000.

Pursuant to an Assignment and Assumption Agreement dated March 25, 2004 between the Company and Mountain Glen, Mountain Glen distributed its property and assets in specie to the Company with the object of winding up the affairs of Mountain Glen. The property transferred included Mountain Glen's shares in Baltic Minerals BV and the 16,015,696 MPV Shares. On March 30, 2004, the 16,015,696 MPV Shares were cancelled and returned to treasury.

Mountain Glen was voluntarily dissolved on August 4, 2004.

Pursuant to the repeal of the British Columbia Company Act and its replacement by the British Columbia Business Corporations Act (the "New Act"), the Company transitioned to the New Act and adopted new Articles of Incorporation. On September 20, 2005, the Company’s shareholders approved a special resolution for the continuance of the Company into Ontario, and the Company amended its articles and continued incorporation under the Ontario Business Corporation Act, transferring from the Company Act (British Columbia).

The Company is domiciled in Canada.

The names of the Company's subsidiaries, their dates of incorporation and the jurisdictions in which they were incorporated as at the date of filing of this Annual Report, are as follows:

| | Juridiction of Incorporation |

| | |

Baltic Minerals Finland OY | | |

| May 9, 1986 (as Sierra Madre Resources Inc.) | |

The subsidiaries of the Company, represented diagrammatically, are as follows:

The Company's registered, records and executive office is at 401 Bay Street, Suite 2700, PO Box 152, Toronto, Ontario, Canada M5H 2Y4. The Company’s administrative and executive office is at 401 Bay Street, Suite 2700, PO Box 152, Toronto, Ontario, Canada M5H 2Y4, the telephone number is (416) 361-3562, and the fax number is (416) 603-8565.

The Company's initial public offering on the Vancouver Stock Exchange ("VSE") was pursuant to a prospectus dated July 28, 1988 and was only offered to investors in British Columbia. The Company listed its shares on the Toronto Stock Exchange ("TSX") (Trading Symbol "MPV") on January 22, 1999 and on the Nasdaq Smallcap Market (Trading Symbol "MPVIF") on May 1, 1996. Its shares were delisted from the Vancouver Stock Exchange (now known as the TSX Venture Exchange and prior to that, as the Canadian Venture Exchange ("CDNX")) on January 31, 2000 and from the Nasdaq Smallcap Market on September 29, 2000. Presently, the Company's shares trade on the TSX under the symbol "MPV" and also on the Amex under the symbol MDM. Prior to April 4, 2005, the Company's shares traded on the OTCBB under the symbol "MPVI". The Company is also registered extra-provincially in the Northwest Territories, and is a reporting issuer in British Columbia, Ontario and Alberta. The Company files reports in the United States pursuant to Section 13 of the Securities Exchange Act.

Principal Capital Expenditures and Divestitures

There are no principal capital expenditures and divestitures currently in progress.

Takeover offers

There were no public takeover offers by third parties in respect of the Company's shares or by the Company in respect of other companies' shares during the last and current financial year, except as discussed under “Acquisitions and Dispositions” relating to Camphor Ventures.

Acquisitions and Dispositions

On October 10, 2002, the Company granted an option for the acquisition by Vision Gate Ventures Limited (now known as Northern Lion Gold Corp.) of a 70% interest in its Haveri Gold Property, which was not considered to be a property that was material to the Company. On October 4, 2004, the Company agreed to exchange the Company's 30% interest in the Haveri Gold Property for 4,000,000 common shares of Northern Lion Gold Corp. The shares were subject to a two-year hold period and there are volume restrictions on re-sale thereafter.

On July 5, 2006, the Company announced that it had entered into an agreement with certain Camphor Ventures Inc. (“Camphor”) shareholders to acquire approximately 33.5 percent of the issued and outstanding shares of Camphor through a private agreement exempt share exchange on the basis of 0.3975 Mountain Province shares for each Camphor share. The acquisition was completed on July 24, 2006.

On January 19, 2007 the Company announced that Camphor had accepted an offer letter from the Company in terms of which the Company offered, subject to certain conditions, to acquire all of the outstanding securities of Camphor Ventures on the basis of 0.41 Mountain Province common shares, options or warrants (as the case may be) per Camphor common share, option, or warrant. Offering documents and the Camphor Directors’ Circular were mailed to Camphor shareholders on February 23, 2007, and the offer remained open until March 30, 2007, following which Mountain Province took up the Camphor shares tendered into the offer increasing the Company’s interest in Camphor to over 90 percent. The offer was subsequently extended until April 16, 2007, following which the Company’s interest in Camphor increased to 96% percent on a fully diluted basis. On April 19, 2007, the Company issued a Notice of Compulsory Acquisition to acquire the balance of the outstanding shares of Camphor. The Notice expired June 19, 2007 and the Company took up the balance of the Camphor shares. Camphor Ventures has been de-listed and is now a wholly owned subsidiary of Mountain Province.

1.1 Introduction

The Company is a natural resource property exploration and development company. The Company has interests in several natural resource properties, the most significant and principal property being a 49% interest (including the 4.9% interest of Camphor) in the AK Property located in the Northwest Territories. See "Item 4D - Property, plants and equipment".

The Company, as yet, does not have any commercially viable resource properties. Permitting, bulk sampling and drilling continues on the AK Property.

1.2 Historical Corporate Development

In August 1992, the Company acquired a 100% interest in the AK-CJ Properties that encompassed approximately 520,000 acres. Pursuant to an agreement dated November 18, 1993 (as amended), the Company optioned 40% of its interest in the AK-CJ Claims to 444965, a subsidiary of Glenmore.

Pursuant to an agreement dated August 16, 1994 (as amended), the Company also optioned 10% of its interest in the AK-CJ Claims to Camphor. Following the merger of the Company with 444965, the Company held a 90% interest in the AK-CJ Claims, and Camphor, the remaining 10%. Exploration work in the form of soil sampling, aerial geophysical surveys and geochemical and geophysical analysis were undertaken on these properties during the period from 1992 to 1995.

During fiscal 1995, the Company focused the majority of its attention on the AK Property. In February 1995, a diamondiferous kimberlite was discovered (the "5034" kimberlite pipe) and a program of delineation drilling was undertaken. Activity during this period on the Company's other properties was minimal because of the focus on the AK Property.

During 1996, the Company completed a 104-tonne mini-bulk sample from the 5034 kimberlite pipe. The results indicated an average grade of 2.48 carats per tonne. During 1997, the Company concluded a joint venture agreement (the "Letter Agreement") with Monopros, a wholly-owned subsidiary of De Beers, and now known as De Beers Canada Exploration Inc., Camphor Ventures Inc., and other parties, and further amended it (as the Gahcho Kué Joint Venture Agreement) in 2002, to develop the AK-CJ Properties. The Letter Agreement granted De Beers the sole and exclusive right and option to acquire a 51% ownership interest in the Property in consideration of incurring certain expenditures.

During the 1997 exploration season, De Beers Canada discovered three new kimberlite pipes on the AK property: Tesla, Tuzo and Hearne. All are diamondiferous.

During the spring of 1998, De Beers Canada conducted mini-bulk sampling on the three new pipes as well as the 5034 kimberlite pipe, the original pipe discovery on the AK Property. The results were positive enough for De Beers to commit to a major bulk sample in 1999.

During 1999, De Beers Canada completed a major bulk sample of the four major pipes. For the 5034 kimberlite pipe, a total of 1044 carats were recovered from 609 tonnes of kimberlite. For the Hearne pipe, a total of 856 carats were recovered from 469 tonnes of kimberlite. For the Tuzo pipe, a total of 533 carats were recovered from 523 tonnes of kimberlite. For the Tesla pipe, 64 carats were recovered from 184 tonnes of kimberlite. The Tesla pipe was too low grade to be considered as part of a mine plan.

On March 8, 2000, the Company agreed to extend the feasibility study decision date and De Beers Canada agreed to carry all exploration, development and other project costs.

On August 4, 2000, De Beers Canada presented the desktop study to the Company. Upon presentation, De Beers Canada was deemed to earn a 51% interest in the AK-CJ Properties. Consequently, the Company was left with a 44.1% interest and Camphor. with a 4.9% interest in the AK-CJ Properties. The main conclusion of the desktop study was that only a 15 percent increase in diamond revenues was needed for De Beers Canada to proceed to the feasibility stage.